Filling the UK pensions gap - following the introduction of a tapered annual allowance – May 11, 2016

White & Case

Description

Filling the UK

pensions gap

Tweaks to UK pensions policy may send top earners

and their employers looking for alternatives

. Tapered annual allowance saps

tax-relieved savings

The base annual allowance is still

£40,000 per tax year. An individual can

also carry forward any unused annual

allowance from up to three previous

tax years. Contributions exceeding the

allowance are taxed as income.

From 6 April 2016, changes came

into effect that apply to individuals

£10,000

The new annual

allowance per tax

year for individuals

with adjusted

income over

£210,000

Source:

2015 Summer Budget

What is adjusted income

and threshold income?

Pension flexibilities go hand in hand

with the tapered annual allowance

Adjusted income is all taxable

income for a tax year including

employer and executive pension

contributions.

A person with adjusted income exceeding £210,000

and threshold income exceeding £110,000 will have a

tapered annual allowance of only £10,000.

Threshold income is all taxable

income for a tax year excluding

employer and executive pension

contributions.

If such individuals also flexibly access their pension

benefits, they will only have a £10,000 money

purchase annual allowance, and no alternative

allowance if they max out the money purchase annual

allowance (although any unused annual allowance from

the previous three tax years can be carried forward).

Proposals [by previous governments for

the pensions regime of “simplicity, security

and choice”] have been replaced by a reality

of complication, chaos and chance

Chris Holmes, Lord Holmes of Richmond MBE

1

White & Case

More changes may be on the way

In the build-up to the March 2016

budget, the Chancellor was said to be

strongly considering three options for

sweeping reform.

Under the flat-rate option, higher‑rate

and additional-rate taxpayers would

be taxed twice: once on their

contributions going into a pension plan,

and again when they withdraw those

funds as taxable income.

According to a Treasury source,

these proposals were dropped in

the end because 2016 was “not the

right time” to make major changes

to pension tax relief. However,

although no changes were made in

the 2016 budget, Lord Holmes says,

in the future “more radical changes

are likely”

.

Employers have options, and risks

These cumulative changes have

not only further complicated the

pensions landscape, but also eroded

the long-term appeal of saving into a

1.5

150

100

1.25

Annual allowance (£ 000s)

200

50

20

16

/1

7

20

15

/1

6

20

14

/1

5

20

13

/1

4

20

12

/1

3

20

11

/1

2

/1

0

20

10

/1

1

09

20

08

20

07

/0

9

0

/0

8

1

/0

7

Interaction with “flexible access”

Since the reforms in the 2014

budget, individuals aged 55 or

older or those who meet ill-health

criteria have had the option of

“flexible access” to their defined

contribution pension benefits.

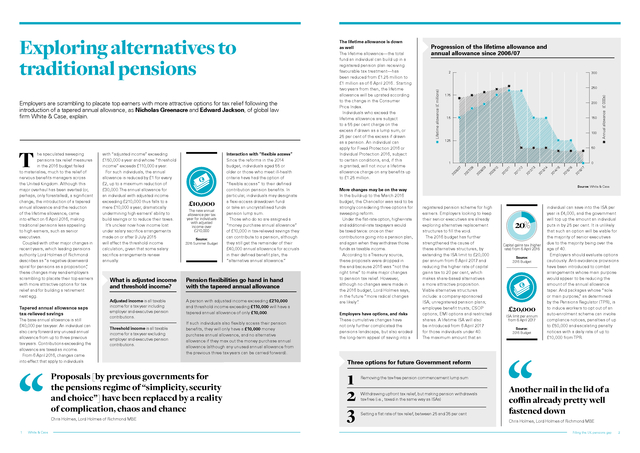

In particular, individuals may designate a flexi‑access drawdown fund or take an uncrystallised funds pension lump sum. Those who do so are assigned a “money purchase annual allowance” of £10,000 in tax-relieved savings they can contribute to a pension, although they still get the remainder of their £40,000 annual allowance for accruals in their defined benefit plan, the “alternative annual allowance. ” 250 1.75 20 with “adjusted income” exceeding £150,000 a year and whose “threshold income” exceeds £110,000 a year. For such individuals, the annual allowance is reduced by £1 for every £2, up to a maximum reduction of £30,000.The annual allowance for an individual with adjusted income exceeding £210,000 thus falls to a mere £10,000 a year, dramatically undermining high earners’ ability to build savings or to reduce their taxes. It’s unclear now how income lost under salary sacrifice arrangements made on or after 9 July 2015 will affect the threshold income calculation, given that some salary sacrifice arrangements renew annually. 300 06 T he speculated sweeping pensions tax relief measures in the 2016 budget failed to materialise, much to the relief of nervous benefits managers across the United Kingdom. Although this major overhaul has been averted (or, perhaps, only forestalled), a significant change, the introduction of a tapered annual allowance and the reduction of the lifetime allowance, came into effect on 6 April 2016, making traditional pensions less appealing to high earners, such as senior executives. Coupled with other major changes in recent years, which leading pensions authority Lord Holmes of Richmond describes as “a negative downward spiral for pensions as a proposition” , these changes may send employers scrambling to placate their top earners with more attractive options for tax relief and for building a retirement nest egg. 2 20 Employers are scrambling to placate top earners with more attractive options for tax relief following the introduction of a tapered annual allowance, as Nicholas Greenacre and Edward Jackson, of global law firm   White & Case, explain. Progression of the lifetime allowance and annual allowance since 2006/07 Lifetime allowance (£ millions) Exploring alternatives to traditional pensions The lifetime allowance is down as well The lifetime allowance—the total fund an individual can build up in a registered pension plan receiving favourable tax treatment—has been reduced from £1.25 million to £1 million as of 6 April 2016.. Starting two years from then, the lifetime allowance will be uprated according to the change in the Consumer Price Index. Individuals who exceed the lifetime allowance are subject to a 55 per cent charge on the excess if drawn as a lump sum, or 25 per cent of the excess if drawn as a pension.

An individual can apply for Fixed Protection 2016 or Individual Protection 2016, subject to certain conditions, and, if this is granted, will not incur a lifetime allowance charge on any benefits up to £1.25 million. Source: White & Case registered pension scheme for high earners. Employers looking to keep their senior executives are already exploring alternative replacement structures to fill the void. The 2016 budget has further strengthened the cause of these alternative structures, by extending the ISA limit to £20,000 per annum from 6 April 2017 and reducing the higher rate of capital gains tax to 20 per cent, which makes share‑based alternatives a more attractive proposition. Viable alternative structures include: a company‑sponsored ISA; unregistered pension plans; employee benefit trusts; CSOP options; EMI options and restricted shares. A lifetime ISA will also be introduced from 6 April 2017 for those individuals under 40. The maximum amount that an 20% Capital gains tax (higher rate) from 6 April 2016 Source: 2016 Budget £20,000 ISA limit per annum from 6 April 2017 Source: 2016 Budget individual can save into the ISA per year is £4,000, and the government will top up the amount an individual puts in by 25 per cent.

It is unlikely that such an option will be viable for the majority of senior executives due to the majority being over the age of 40. Employers should evaluate options cautiously. Anti-avoidance provisions have been introduced to combat arrangements whose main purpose would appear to be reducing the amount of the annual allowance taper. And packages whose “sole or main purpose, as determined ” by the Pensions Regulator (TPR), is to induce workers to opt out of an auto-enrolment scheme can invoke compliance notices, penalties of up to £50,000 and escalating penalty notices with a daily rate of up to £10,000 from TPR. Three options for future Government reform 1 2 3 Removing the tax-free pension commencement lump sum Withdrawing upfront tax relief, but making pension withdrawals tax‑free (i.e., taxed in the same way as ISAs) Setting a flat rate of tax relief, between 25 and 35 per cent Another nail in the lid of a coffin already pretty well fastened down Chris Holmes, Lord Holmes of Richmond MBE Filling the UK pensions gap 2 .

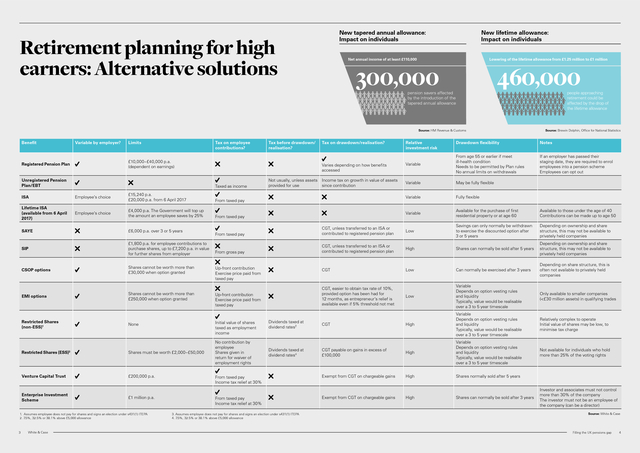

New tapered annual allowance: Impact on individuals Retirement planning for high earners: Alternative solutions New lifetime allowance: Impact on individuals Net annual income of at least £110,000 Lowering of the lifetime allowance from £1.25 million to £1 million 300,000 pension savers affected by the introduction of the tapered annual allowance 460,000 Source: HM Revenue & Customs Benefit Variable by employer? Limits Tax on employee contributions? Unregistered Pension Plan/EBT Notes Variable From age 55 or earlier if meet ill‑health condition Needs to be permitted by Plan rules No annual limits on withdrawals If an employer has passed their staging date, they are required to enrol employees into a pension scheme Employees can opt out Variable May be fully flexible Variable Fully flexible Variable Available for the purchase of first residential property or at age 60 Available to those under the age of 40 Contributions can be made up to age 50 From taxed pay CGT, unless transferred to an ISA or contributed to registered pension plan Low Savings can only normally be withdrawn to exercise the discounted option after 3 or 5 years Depending on ownership and share structure, this may not be available to privately held companies From gross pay CGT, unless transferred to an ISA or contributed to registered pension plan High Shares can normally be sold after 5 years Depending on ownership and share structure, this may not be available to privately held companies CGT Low Can normally be exercised after 3 years Depending on share structure, this is often not available to privately held companies Low Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Only available to smaller companies (<£30 million assets) in qualifying trades High Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Relatively complex to operate Initial value of shares may be low, to minimise tax charge CGT payable on gains in excess of £100,000 High Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Not available for individuals who hold more than 25% of the voting rights Exempt from CGT on chargeable gains High Shares normally sold after 5 years ISA Employee’s choice £15,240 p.a. £20,000 p.a. from 6 April 2017 Employee’s choice £4,000 p.a. The Government will top up the amount an employee saves by 25% Not usually, unless assets Income tax on growth in value of assets provided for use since contribution From taxed pay Lifetime ISA (available from 6 April 2017) Relative investment risk Varies depending on how benefits accessed Taxed as income Tax on drawdown/realisation? From taxed pay SAYE £6,000 p.a. over 3 or 5 years SIP £1,800 p.a.

for employee contributions to purchase shares, up to £7,200 p.a. in value for further shares from employer CSOP options Shares cannot be worth more than £30,000 when option granted EMI options Restricted Shares (non-ESS)1 Shares cannot be worth more than £250,000 when option granted Restricted Shares (ESS)3 Shares must be worth £2,000–£50,000 Venture Capital Trust £200,000 p.a. Enterprise Investment Scheme £1 million p.a. 1. Assumes employee does not pay for shares and signs an election under s431(1) ITEPA 2.

7 .5%, 32.5% or 38.1% above £5,000 allowance White & Case Up-front contribution Exercise price paid from taxed pay CGT, easier to obtain tax rate of 10%, provided option has been had for 12 months, as entrepreneur’s relief is available even if 5% threshold not met Up-front contribution Exercise price paid from taxed pay Initial value of shares taxed as employment income None Source: Brewin Dolphin, Office for National Statistics Drawdown flexibility £10,000–£40,000 p.a. (dependent on earnings) Registered Pension Plan 3 Tax before drawdown/ realisation? people approaching retirement could be affected by the drop of the lifetime allowance No contribution by employee Shares given in return for waiver of employment rights Dividends taxed at dividend rates2 Dividends taxed at dividend rates4 From taxed pay Income tax relief at 30% From taxed pay Income tax relief at 30% 3. Assumes employee does not pay for shares and signs an election under s431(1) ITEPA 4. 7 .5%, 32.5% or 38.1% above £5,000 allowance CGT Exempt from CGT on chargeable gains High Shares can normally be sold after 3 years Investor and associates must not control more than 30% of the company The investor must not be an employee of the company (can be a director) Source: White & Case Filling the UK pensions gap 4 .

Nicholas Greenacre Partner T +44 20 7532 2141 E ngreenacre@whitecase.com Edward Jackson Associate T +44 20 7532 2995 E ejackson@whitecase.com whitecase.com © 2016 White & Case LLP Cover photography: Canary Wharf, London. Image by IR Stone. © Shutterstock. .

In particular, individuals may designate a flexi‑access drawdown fund or take an uncrystallised funds pension lump sum. Those who do so are assigned a “money purchase annual allowance” of £10,000 in tax-relieved savings they can contribute to a pension, although they still get the remainder of their £40,000 annual allowance for accruals in their defined benefit plan, the “alternative annual allowance. ” 250 1.75 20 with “adjusted income” exceeding £150,000 a year and whose “threshold income” exceeds £110,000 a year. For such individuals, the annual allowance is reduced by £1 for every £2, up to a maximum reduction of £30,000.The annual allowance for an individual with adjusted income exceeding £210,000 thus falls to a mere £10,000 a year, dramatically undermining high earners’ ability to build savings or to reduce their taxes. It’s unclear now how income lost under salary sacrifice arrangements made on or after 9 July 2015 will affect the threshold income calculation, given that some salary sacrifice arrangements renew annually. 300 06 T he speculated sweeping pensions tax relief measures in the 2016 budget failed to materialise, much to the relief of nervous benefits managers across the United Kingdom. Although this major overhaul has been averted (or, perhaps, only forestalled), a significant change, the introduction of a tapered annual allowance and the reduction of the lifetime allowance, came into effect on 6 April 2016, making traditional pensions less appealing to high earners, such as senior executives. Coupled with other major changes in recent years, which leading pensions authority Lord Holmes of Richmond describes as “a negative downward spiral for pensions as a proposition” , these changes may send employers scrambling to placate their top earners with more attractive options for tax relief and for building a retirement nest egg. 2 20 Employers are scrambling to placate top earners with more attractive options for tax relief following the introduction of a tapered annual allowance, as Nicholas Greenacre and Edward Jackson, of global law firm   White & Case, explain. Progression of the lifetime allowance and annual allowance since 2006/07 Lifetime allowance (£ millions) Exploring alternatives to traditional pensions The lifetime allowance is down as well The lifetime allowance—the total fund an individual can build up in a registered pension plan receiving favourable tax treatment—has been reduced from £1.25 million to £1 million as of 6 April 2016.. Starting two years from then, the lifetime allowance will be uprated according to the change in the Consumer Price Index. Individuals who exceed the lifetime allowance are subject to a 55 per cent charge on the excess if drawn as a lump sum, or 25 per cent of the excess if drawn as a pension.

An individual can apply for Fixed Protection 2016 or Individual Protection 2016, subject to certain conditions, and, if this is granted, will not incur a lifetime allowance charge on any benefits up to £1.25 million. Source: White & Case registered pension scheme for high earners. Employers looking to keep their senior executives are already exploring alternative replacement structures to fill the void. The 2016 budget has further strengthened the cause of these alternative structures, by extending the ISA limit to £20,000 per annum from 6 April 2017 and reducing the higher rate of capital gains tax to 20 per cent, which makes share‑based alternatives a more attractive proposition. Viable alternative structures include: a company‑sponsored ISA; unregistered pension plans; employee benefit trusts; CSOP options; EMI options and restricted shares. A lifetime ISA will also be introduced from 6 April 2017 for those individuals under 40. The maximum amount that an 20% Capital gains tax (higher rate) from 6 April 2016 Source: 2016 Budget £20,000 ISA limit per annum from 6 April 2017 Source: 2016 Budget individual can save into the ISA per year is £4,000, and the government will top up the amount an individual puts in by 25 per cent.

It is unlikely that such an option will be viable for the majority of senior executives due to the majority being over the age of 40. Employers should evaluate options cautiously. Anti-avoidance provisions have been introduced to combat arrangements whose main purpose would appear to be reducing the amount of the annual allowance taper. And packages whose “sole or main purpose, as determined ” by the Pensions Regulator (TPR), is to induce workers to opt out of an auto-enrolment scheme can invoke compliance notices, penalties of up to £50,000 and escalating penalty notices with a daily rate of up to £10,000 from TPR. Three options for future Government reform 1 2 3 Removing the tax-free pension commencement lump sum Withdrawing upfront tax relief, but making pension withdrawals tax‑free (i.e., taxed in the same way as ISAs) Setting a flat rate of tax relief, between 25 and 35 per cent Another nail in the lid of a coffin already pretty well fastened down Chris Holmes, Lord Holmes of Richmond MBE Filling the UK pensions gap 2 .

New tapered annual allowance: Impact on individuals Retirement planning for high earners: Alternative solutions New lifetime allowance: Impact on individuals Net annual income of at least £110,000 Lowering of the lifetime allowance from £1.25 million to £1 million 300,000 pension savers affected by the introduction of the tapered annual allowance 460,000 Source: HM Revenue & Customs Benefit Variable by employer? Limits Tax on employee contributions? Unregistered Pension Plan/EBT Notes Variable From age 55 or earlier if meet ill‑health condition Needs to be permitted by Plan rules No annual limits on withdrawals If an employer has passed their staging date, they are required to enrol employees into a pension scheme Employees can opt out Variable May be fully flexible Variable Fully flexible Variable Available for the purchase of first residential property or at age 60 Available to those under the age of 40 Contributions can be made up to age 50 From taxed pay CGT, unless transferred to an ISA or contributed to registered pension plan Low Savings can only normally be withdrawn to exercise the discounted option after 3 or 5 years Depending on ownership and share structure, this may not be available to privately held companies From gross pay CGT, unless transferred to an ISA or contributed to registered pension plan High Shares can normally be sold after 5 years Depending on ownership and share structure, this may not be available to privately held companies CGT Low Can normally be exercised after 3 years Depending on share structure, this is often not available to privately held companies Low Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Only available to smaller companies (<£30 million assets) in qualifying trades High Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Relatively complex to operate Initial value of shares may be low, to minimise tax charge CGT payable on gains in excess of £100,000 High Variable Depends on option vesting rules and liquidity Typically, value would be realisable over a 3 to 5 year timescale Not available for individuals who hold more than 25% of the voting rights Exempt from CGT on chargeable gains High Shares normally sold after 5 years ISA Employee’s choice £15,240 p.a. £20,000 p.a. from 6 April 2017 Employee’s choice £4,000 p.a. The Government will top up the amount an employee saves by 25% Not usually, unless assets Income tax on growth in value of assets provided for use since contribution From taxed pay Lifetime ISA (available from 6 April 2017) Relative investment risk Varies depending on how benefits accessed Taxed as income Tax on drawdown/realisation? From taxed pay SAYE £6,000 p.a. over 3 or 5 years SIP £1,800 p.a.

for employee contributions to purchase shares, up to £7,200 p.a. in value for further shares from employer CSOP options Shares cannot be worth more than £30,000 when option granted EMI options Restricted Shares (non-ESS)1 Shares cannot be worth more than £250,000 when option granted Restricted Shares (ESS)3 Shares must be worth £2,000–£50,000 Venture Capital Trust £200,000 p.a. Enterprise Investment Scheme £1 million p.a. 1. Assumes employee does not pay for shares and signs an election under s431(1) ITEPA 2.

7 .5%, 32.5% or 38.1% above £5,000 allowance White & Case Up-front contribution Exercise price paid from taxed pay CGT, easier to obtain tax rate of 10%, provided option has been had for 12 months, as entrepreneur’s relief is available even if 5% threshold not met Up-front contribution Exercise price paid from taxed pay Initial value of shares taxed as employment income None Source: Brewin Dolphin, Office for National Statistics Drawdown flexibility £10,000–£40,000 p.a. (dependent on earnings) Registered Pension Plan 3 Tax before drawdown/ realisation? people approaching retirement could be affected by the drop of the lifetime allowance No contribution by employee Shares given in return for waiver of employment rights Dividends taxed at dividend rates2 Dividends taxed at dividend rates4 From taxed pay Income tax relief at 30% From taxed pay Income tax relief at 30% 3. Assumes employee does not pay for shares and signs an election under s431(1) ITEPA 4. 7 .5%, 32.5% or 38.1% above £5,000 allowance CGT Exempt from CGT on chargeable gains High Shares can normally be sold after 3 years Investor and associates must not control more than 30% of the company The investor must not be an employee of the company (can be a director) Source: White & Case Filling the UK pensions gap 4 .

Nicholas Greenacre Partner T +44 20 7532 2141 E ngreenacre@whitecase.com Edward Jackson Associate T +44 20 7532 2995 E ejackson@whitecase.com whitecase.com © 2016 White & Case LLP Cover photography: Canary Wharf, London. Image by IR Stone. © Shutterstock. .