A brave new world for international leveraged debt - The reshaping of the wider economy – February 11, 2016

White & Case

Description

A brave new world

Cover title, initial

for international

cap only, goes here

leveraged debt

Cover: Stand first. Omnihill oribusapis erum ad

mo dolore de expere pro od quidign ihilicit

The reshaping of the wider economy has led

moditatur? Cabore nissint ibustiis ma natur, nias

to increasinglyquo omnis a and competitive

anis et latium converging quunturibus aut

leveraged finance markets

auditis

A brave new world for international leveraged debt

I

. Innovation and

collaboration are driving

leveraged debt markets

European high yield and leveraged loan markets have a

distinctly different feel from 12 months ago. Volumes and

values notably dropped over 2015, leaving issuers and

lenders wondering what to expect in 2016 and beyond.

O

ur report last year, Coming of age, revealed that the European and international markets

were converging in a number of significant ways—across products, markets and investors;

across a broader choice of financial instruments; and across legal platforms. We asked

the question: how would this trend, and the related development of the European and international

financial markets, be impacted by a strong, neutral or a declining market?

As volumes have retracted from the boom in issuance in 2014, 2015 provides part of the answer, and

the start of 2016 sees a more cautious market due to macroeconomic uncertainty, increased interest

rates in the United States, market volatility and compliance reform. These factors have led to some

interesting developments across platforms:

Rob Mathews

Partner, White & Case

Â…Â…in leveraged finance, the emergence of the European Term Loan B as a complementary (or

competitive) product to high yield bonds has further narrowed the space between bank and

bond deals, as well as US banks and European banks;

Â…Â…in private equity, while sponsors continue to push for looser deal terms, the markets may

be pausing for breath, with some deal terms tightened in the face of a more discerning and

assertive investor base;

Â…Â…in emerging markets, where natural resource price volatility and concerns about capital

structures drove a market retraction in 2015, the high yield and Eurobond markets continue to

converge (particularly in Africa, as the market matures from sovereign and bank issuances to

corporate credits);

Â…Â…in restructurings, the tension among US Chapter 11, the UK scheme of arrangement and

other voluntary restructuring strategies has become more apparent as the new generation of

international bank/bond structures continues to come under pressure; and

Â…Â…credit funds and other one-off investors continue to look for unique opportunities and yield—

in some cases, taking advantage of the more reticent public markets to get deals done.

Common across each of the platforms are the key themes for 2016—innovation and

collaboration—with all market participants working with their advisers to create structures that are

suitable for both investors and issuers.

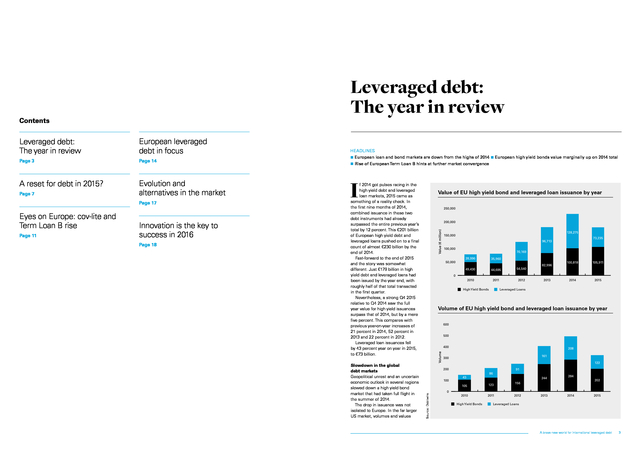

The boom times are not over for European high yield and leveraged loans in the long term, but the pace, flavour and overall feel will be different from the US-style model. It is going to be an interesting ride. II White & Case Lee Cullinane Partner, White & Case . Leveraged debt: The year in review Leveraged debt: The year in review European leveraged debt in focus Page 3 Page 14 A reset for debt in 2015? Evolution and alternatives in the market Page 7 Page 17 Eyes on Europe: cov-lite and Term Loan B rise Page 11 Innovation is the key to success in 2016 Page 18 HEADLINES n European loan and bond markets are down from the highs of 2014 n European high yield bonds value marginally up on 2014 total n Rise of European Term Loan B hints at further market convergence I f 2014 got pulses racing in the high yield debt and leveraged loan markets, 2015 came as something of a reality check. In the first nine months of 2014, combined issuance in these two debt instruments had already surpassed the entire previous year’s total by 12 percent. This €201 billion of European high yield debt and leveraged loans pushed on to a final count of almost €230 billion by the end of 2014. Fast-forward to the end of 2015 and the story was somewhat different. Just €179 billion in high yield debt and leveraged loans had been issued by the year end, with roughly half of that total transacted in the first quarter. Nevertheless, a strong Q4 2015 relative to Q4 2014 saw the full year value for high yield issuances surpass that of 2014, but by a mere five percent.

This compares with previous year-on-year increases of 21 percent in 2014, 52 percent in 2013 and 22 percent in 2012. Leveraged loan issuances fell by 43 percent year on year in 2015, to €73 billion. Slowdown in the global debt markets Geopolitical unrest and an uncertain economic outlook in several regions slowed down a high yield bond market that had taken full flight in the summer of 2014. The drop in issuance was not isolated to Europe. In the far larger US market, volumes and values Value of EU high yield bond and leveraged loan issuance by year 250,000 200,000 128,275 150,000 73,235 96,713 100,000 70,169 28,996 35,960 49,430 44,695 54,540 2010 50,000 2011 2012 82,996 100,818 105,911 2014 2015 0 High Yield Bonds 2013 Leveraged Loans Volume of EU high yield bond and leveraged loan issuance by year 600 500 400 208 161 300 122 200 100 91 43 86 244 105 Source: Debtwire Contents 123 2010 2011 2012 284 202 156 0 High Yield Bonds 2013 2014 2015 Leveraged Loans A brave new world for international leveraged debt 3 . Value of US high yield bond and leveraged loans issuances by year 1,000,000 Value (US$ million) 800,000 600,000 579,587 272,949 400,000 152,969 387,978 260,342 219,097 200,000 301,054 238,006 272,706 191,097 248,172 223,335 2014 2015 0 2010 2011 High Yield Bonds 2012 2013 Leveraged Loans were down in 2015, with the second quarter responsible for the year’s peak. A slump in the third quarter saw the lowest issuance of US high yield bonds in the last four years in terms of value, with barely US$223 billion being transacted in 2015 compared with US$301 billion at the market’s peak in 2012. It is a similar story for leveraged loans— 2015 saw the US have its worst year of capital-raising in leveraged loans since 2011. However, there was still demand for funding using high yield-style covenants and the markets shifted, in part, towards cov-lite Term Loan B (TLB) from instruments such as senior secured TLB. The former grew substantially over the last year— particularly in Europe. Vast differences in economic policy have impacted debt issuance on either side of the Atlantic, but there are reasons closer to home for both of them to explain why numbers have not kept up the pace in the past 18 months.

Not all of them are causes for alarm—and many will be important factors in 2016. Volume of US high yield bond and leveraged loans issuances by year 1,800 1,600 1,400 1,200 Volume 1,032 1,000 583 791 800 600 303 417 459 400 200 583 491 561 383 484 350 Source: Debtwire 0 2010 High Yield Bonds 4 White & Case 2011 2012 Leveraged Loans 2013 2014 2015 There was still demand for funding using high yield-style covenants and the markets shifted, in part, towards US Term Loan B, which grew substantially over the last year— particularly in Europe. CASE STUDY The rise of TLB Cabot Financial Cov-lite Term Loan B (TLB), in terms of covenant protection, has many similarities to high yield, though the former has typically softer call protections than those on the latter. This debt instrument caught on in Europe in 2014 and took hold in 2015. “Cov-lite” came into fashion from across the Atlantic and the issuing community has taken note. As the rest of the bond market slowed, TLBs came into their own, with a threefold uptick in European issuance year on year. However, despite investors’ search for yield, as volatility increases investors will limit how much risk they are willing to take.

The US$5.6 billion cross-border loan for tech company Veritas was pulled in November, for example, as prospective investors stayed cool on the deal due to a variety of reasons. This marked the second withdrawal of underwritten loan financing in a week, coming just after OM Group’s withdrawal of a US$575 million financing round. “It’s not unheard of for a bond on a best efforts basis to be withdrawn but the loan underwritten ones less so, one buy-sider told ” Debtwire at the time.

“Market volatility is the driver behind it. ” This indicates how quickly the market can change and how there can be new lines drawn in the sand for the sector as global economics shift. While the numbers show that looser terms became very successful in 2015, issuers and their advisers have been learning, innovating and talking with investors directly to refine and understand market focus points, helping deals get to market and doing their best to ensure no one loses out if and when financial difficulty strikes. As international M&A heats up and complex corporate structures become the new normal, White & Case has helped create a template for sophisticated, multi-subsidiary financings. The team advised Cabot Group in November 2015 on a transaction that amended a £200 million English law revolving credit facility agreement (including an accordion and amendments to accommodate Cabot Group’s growth in certain other jurisdictions) and issued €310 million in New York law senior secured floating rate notes. The proceeds were partially used to prepay a £90 million acquisition bridge facility which was entered into in June 2015. Additional sterling-denominated debt was also issued, taking the total existing indebtedness in the form of notes—other than the newly issued €310 million floating rate notes—to £690 million. The deal was certainly innovative as the revolving credit facility agreement and the senior secured floating rate notes, along with the additional debt issued, are regulated by two intercreditor agreements yet secured by the same security package (with different rankings). Additionally, the security package includes, amongst other security documents governed by Luxembourg law or Irish law, two separate English law debentures, each subject to a different intercreditor agreement. Following a major acquisition by one of its subsidiaries of the Marlin Financial Group in February 2014, Cabot did not terminate the existing Marlin intercreditor agreement regulating the debt of the acquired Marlin Financial Group due to the existence of £150 million senior secured fixed rate notes issued by a Marlin company.

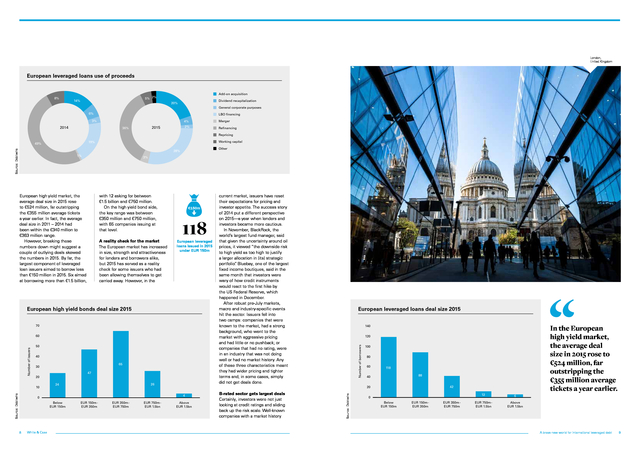

Instead, Cabot amended it to align with its own conditions, meaning the consolidated group’s financial indebtedness has since been regulated by two intercreditor agreements. This extremely sophisticated deal forged an innovative legal solution for acquiring companies with complex existing debt arrangements. A brave new world for international leveraged debt 5 . A reset for debt in 2015? HEADLINES n Mean European leveraged loan deal size in 2015 was €600 million, compared with €617 million a year earlier n High yield bond issuances and leveraged loan allocations for refinancing have fallen substantially n Europe matures but 2015 is “reality check” for issuers A t the beginning of 2015, it was believed that the high yield bond and leveraged loan markets would continue at the levels seen in 2014. Issuance had peaked and terms were loosening. Indeed, the first quarter started well; however, as the midpoint of the year arrived, it was becoming clear that 2015 was not going to match the previous 12 months for issuance in the US and Europe. In 2014, some 60 percent of high yield bonds and 49 percent of leveraged loans had been issued in Europe for refinancing purposes. In 2015, that figure dropped to 46 percent and 36 percent, respectively. € 46% proceeds of 2015 European high yield bonds used for refinancing, compared with 60% in 2014 Many private equity sponsors looking to exit were seeing better valuations through an IPO than through a secondary sale or debt issuance. European equity markets have been very strong as a result, and this has cannibalised some of the demand for high yield.

The traditional tension between a leveraged refinancing, an IPO and an M&A exit shifted in 2015, as the IPO market proved stronger than in recent years. However, private equity did boost the market with funding for leveraged buyouts in 2015, particularly on the loans side. While the percentage of high yield bond proceeds used to finance these deals grew from five percent to nine percent, leveraged loan issuance for leveraged acquisitions over the two years grew from 33 percent for add-ons and leveraged buyouts in 2014 to 48 percent for the same in 2015. Loan sizes remain resilient Further evidence of this growing depth and strength can be seen in the size of deals that were transacted successfully in 2015. Despite the relative drop off in issuance, the ticket size offered by those coming to market has been resilient. The mean European leveraged loan deal size in 2015 was €600 million compared with €617 million a year earlier.

In the European high yield bonds use of proceeds 3% Add-on acquisition 2% General corporate purposes 20% 29% LBO ï¬nancing Reï¬nancing Spin-off Source: Debtwire 2014 60% 12% 46% 2015 5% Other 14% 9% A brave new world for international leveraged debt 7 . London, United Kingdom European leveraged loans use of proceeds 8% Add-on acquisition 5% 2% 14% Dividend recapitalization 20% General corporate purposes 6% LBO ï¬nancing 3% 2014 4% Merger 2% 2015 36% Reï¬nancing Repricing Working capital 19% Other 28% 1% 3% A reality check for the market The European market has increased in size, strength and attractiveness for lenders and borrowers alike, but 2015 has served as a reality check for some issuers who had been allowing themselves to get carried away. However, in the €150m 118 European leveraged loans issued in 2015 under EUR 150m European high yield bonds deal size 2015 70 Number of issuers 60 50 40 30 47 20 10 Source: Debtwire 65 26 24 Below EUR 150m 8 White & Case EUR 150m EUR 350m EUR 350m EUR 750m EUR 750m EUR 1.5bn European leveraged loans deal size 2015 Above EUR 1.5bn B-rated sector gets largest deals Certainly, investors were not just looking at credit ratings and sliding back up the risk scale. Well-known companies with a market history In the European high yield market, the average deal size in 2015 rose to €524 million, far outstripping the €355 million average tickets a year earlier. 140 120 100 80 60 118 88 40 42 20 4 0 current market, issuers have reset their expectations for pricing and investor appetite. The success story of 2014 put a different perspective on 2015—a year when lenders and investors became more cautious. In November, BlackRock, the world’s largest fund manager, said that given the uncertainty around oil prices, it viewed “the downside risk to high yield as too high to justify a larger allocation in [its] strategic portfolio” Bluebay, one of the largest . fixed income boutiques, said in the same month that investors were wary of how credit instruments would react to the first hike by the US Federal Reserve, which happened in December. After robust pre-July markets, macro and industry-specific events hit the sector.

Issuers fell into two camps: companies that were known to the market, had a strong background, who went to the market with aggressive pricing and had little or no pushback; or companies that had no rating, were in an industry that was not doing well or had no market history. Any of these three characteristics meant they had wider pricing and tighter terms and, in some cases, simply did not get deals done. Number of borrowers with 12 asking for between €1.5 billion and €750 million. On the high yield bond side, the key range was between €350 million and €750 million, with 65 companies issuing at that level. European high yield market, the average deal size in 2015 rose to €524 million, far outstripping the €355 million average tickets a year earlier. In fact, the average deal size in 2011 – 2014 had been within the €340 million to €363 million range. However, breaking these numbers down might suggest a couple of outlying deals skewed the numbers in 2015.

By far, the largest component of leveraged loan issuers aimed to borrow less than €150 million in 2015. Six aimed at borrowing more than €1.5 billion, Source: Debtwire Source: Debtwire 49% 12 0 Below EUR 150m EUR 150m EUR 350m EUR 350m EUR 750m 6 EUR 750m EUR 1.5bn Above EUR 1.5bn A brave new world for international leveraged debt 9 . European bond issuance by S&P rating, 2015 # Issues Amount (EUR m) Weighted Average YTM Weighted Average Net Leverage BB+ 23 16,063 4.74% 4.05x BB 15 9,379 3.46% 23 17,396 5.31% 3.92x B+ 30 8,899 6.04% 4.24x B 32 25,598 6.02% 4.63x B- 15 5,377 7.26% 4.86x CCC+ 8 2,542 7.50% 4.85x CCC 2 490 11.66% 6.97x Total 148 85,745 6.50% 4.67x were doing well. With bonds worth €25.6 billion, collective capital raised by 32 B-rated issuers surpassed the next largest group by almost €8.2 billion in 2015. Some 23 BBissuers raised €17 billion, while .4 23 BB+ issuers raised €16.1 billion, according to Standard & Poor’s. In fact, there were more deals in the B and B+ sector than in the BB- to BB+ sector put together in 2015. At an average €789.9 million, issuers awarded a B by Standard & Poor’s managed to get the largest deals away—many of which were oversubscribed, according to Reuters data. Investors willing to venture this far down the risk scale were rewarded with relatively impressive returns.

In 2015, the weighted average yield to maturity on B and B+ rated issuers were 6.02 percent and 6.04 percent, respectively. 10 Eyes on Europe: Cov-lite and Term Loan B rise 3.84x BB- Source: Debtwire Rating White & Case CASE STUDY GTECH/IGT Plc Innovation was key to the largest Italian bond issued on international capital markets to date, with White & Case acting as the issuer’s international counsel for New York, English and Italian law. The firm represented gaming business GTECH on its issuance of senior secured notes denominated in three tranches of US$3.2 billion and two tranches of €1.55 billion in February 2015. The deal, which helped finance the acquisition of IGT Group by the issuer, used a cross-border pari passu bond/bank transaction and supported a complex capital structure. The team employed —and enhanced—the latest technologies in European bond/bank structures. An innovative temporary note structure allowed for the issuance of notes pre-completion—which would not have been permitted by the existing capital structure—thus allowing timely access to the market and improved commercial terms. The deal also was the first in Europe to see existing Eurobond note holders obtain a pre-agreement to enter an intercreditor agreement at completion, as the issuance of new secured notes tripped their negative pledge. The deal was one of the few secured “covenant lite” high yield transactions completed in Europe, and it proved to be a marketleading precedent for companies temporarily crossing into the sub-investment grade space. HEADLINES n US issuers look to Europe n Cov-lite loans growing in popularity on the continent n US Term Loan B structure has been adopted across the other side of the Atlantic n Investors concerned over erosion of covenant protection T he growth of European markets was noticed by US issuers, who have looked across the Atlantic to borrow as pricing widened in the US and appetite increased in Europe. In the second quarter of 2015, US issuers were the second-largest group raising euro-denominated debt, according to Source Ratings. At certain points in 2015, the difference in margin meant it was cheaper to raise funds in Europe than in the US.

Companies that were well known to investors or had a good credit rating were able to take advantage. Even with FX costs, in some cases this still proved to be cheaper than raising dollars in the US itself. Europe—at least for the moment —offers better macroeconomic conditions for both issuers and lenders than the US. On the east of the Atlantic, the European Central Bank has launched further quantitative easing to flood markets with liquidity; to the west, the financial sector had been anxiously waiting for a rate rise for several months and finally got one in December. Liquidity favours Europe for now, and this looks set to endure as the European Central Bank said it will extend its quantitative easing program until at least March 2017 , while its interest rate remains at record lows. The right credits are getting deals done at the right pricing in Europe, with limited or no flex.

This will 23% European first lien cov-lite loans in 2015, compared with 15% in 2014 41% US first lien loans that were cov-lite in 2015, compared with 48% in 2014 likely continue in early 2016 due to these underlying fundamentals, whereas the US may struggle. In current market conditions in the US, as the Veritas deal has shown, even after flex some deals are not getting sold. Covenant-lite rises in Europe This flex has become necessary— in some cases—due to the phenomenon that has swept through European debt markets to great triumph since last year. The phrase “covenant-lite” which has , long been common parlance in the US market, was increasingly used by European issuers in 2014. In the last 12 months, it has seen even more frequent usage and acceptance.

However, the majority of European leveraged loans still retain a quarterly tested leverage ratio for the benefit of both the revolving and term loan lenders. One of the few leveraged loan instruments that saw an increase in issuance in Europe last year was the “covenant-lite Term Loan B” . However, that increase was huge. In 2014, some €6.3 billion was transacted through ten deals. The next year, more than €19.5 billion had been issued through 48 deals. Greater flexibility has been afforded to issuers in 2015, as participants engage in dialogue to address business needs for borrowers and investment risk for lenders. This has meant companies have been able to transact using terms that are more suited to their circumstances and needs within acceptable parameters for lenders. Borrowers should now be asking themselves several questions when deciding what covenant package will be negotiated into documentation. These include finding out whether there’s a maintenance covenant on the debt, whether they have amortisation, whether they have baskets that grow with EBITDA or assets, and whether they have an excess cash-flow sweep. This is vital, as all these points have moved towards the borrower over recent years.

It is now very common for a loan in Europe to be non-amortising, with no maintenance covenant and with flexible baskets. Both parties need to start on the same page to ensure expectations are met. Investors cautious over cov-lite As this part of the market moves to benefit issuers, investors need to be cautious as there are fundamental differences between the US and European jurisdictions—and they should be aware of them before buying into the cov-lite phenomenon. Cov-lite works in the US because of the liquidity and depth of the market. One of the reasons investors in the US typically do not require a financial covenant is because the investment model suggests that they should be able to trade out should the need arise. That is generally not the case in Europe—at least not yet. The market is growing, however, it is still A brave new world for international leveraged debt 11 .

reasonably nascent, and investors cannot adopt the same assumption that they will be able to exit if they decide that a credit’s performance and forecast numbers are not to their liking anymore. While a move back to non-cov-lite may not be on the cards, investors are being very selective and more focused on the same issues they look at in a bond, such as wider industry benchmarks and leverage levels. As the secondary market develops, it will mean more flexible terms are agreed to as a result of the ability to move easily between primary and secondary lenders. But the new kid on the block, which is becoming increasingly established, is the non-bank lender. 26,634 Senior Secured TLB 42,600 19,569 Covenant-lite TLB 6,331 7,202 Senior Secured Term Loan 10,729 Senior Secured Revolver 4,083 Covenant-lite Term Loan 3,945 19,387 13,479 7,062 1,687 Senior Unsecured Term Loan 6,200 1,669 Super Senior Revolver 1,147 1,079 Covenant-lite Revolver 798 1,078 Senior Secured TLC 1,370 1,076 Second Lien 3,100 Senior Unsecured Revolver White & Case 0% 45 10 38 10% 20% European cov-lite 30% 40% 50% US cov-lite 7 Senior Secured TLA 27 Senior Unsecured 5 Term Loan 9 10 Super Senior Revolver 19 9 Covenant-lite Revolver 11 3 Senior Secured TLC 7 10 Second Lien 19 3 2 11 Senior Secured Capex / Acquisition Facility 25 Covenant-lite 5 Second Lien 1,344 9 2 475 75 6,294 2014 41 99 Covenant-lite Term Loan 10,000 20,000 30,000 40,000 50,000 While a move back to non-cov-lite may not be on the cards yet, investors are being very selective and more focused on the same issues they look at in a bond, such as wider industry benchmarks and leverage levels. First lien 1 11 Other Source: Debtwire Source: Debtwire 4,083 23 2015 23 Senior Unsecured Revolver 1,087 2015 48 21 Senior Secured Revolver 556 0 2014 10 Senior Secured Term Loan 1,184 Other 12 Covenant-lite TLB 775 First lien 24 106 15 643 Covenant-lite Second Lien 2013 48 668 Senior Secured Capex / Acquisition Facility First lien loans (percentage) 64 Senior Secured TLB Rise of non-bank lending Where non-banks are providing the funding, typically, the debt is not being distributed and the original provider generally remains as the lender. They will, therefore, agree bespoke packages for the business because they don’t need to sell the debt on, thereby adjusting the balance between achieving a solution for credit purposes and documenting a transaction that looks like all the others. The market is also growing at pace. Non-bank lenders are raising funds very regularly, and they are getting bigger; there is a great deal of appetite for investing money in non-bank finance structures. 1,699 Senior Secured TLA European leveraged loan instrument by volume Source: Xtract European leveraged loan instrument by value 25 0 2015 20 40 60 80 100 120 2014 A brave new world for international leveraged debt 13 .

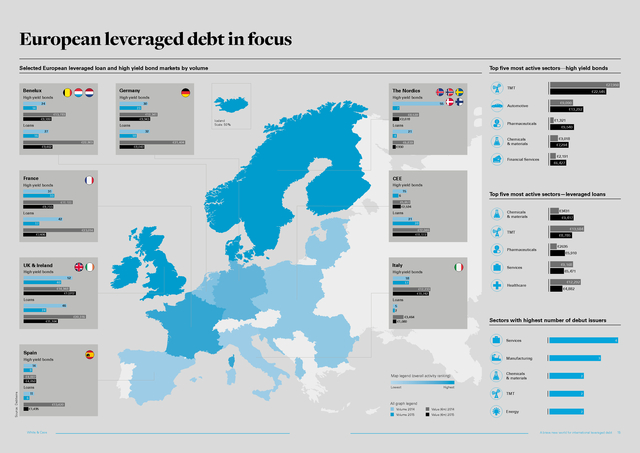

European leveraged debt in focus Selected European leveraged loan and high yield bond markets by volume Benelux Germany High yield bonds Top five most active sectors—high yield bonds High yield bonds 24 55 23 €13,793 7 €12,341 €9,943 €9,180 Loans Iceland Scale: 50% Loans 27 Pharmaceuticals Loans €9,462 4 €21,404 €8,040 €9,090 €13,292 €1,321 €9,540 21 18 €22,903 Automotive €8,539 €2,078 32 16 €22,545 High yield bonds 30 14 €27,950 TMT The Nordics Chemicals & materials €6,839 €930 Financial Services France €2,191 €6,427 CEE High yield bonds €3,018 €7,294 High yield bonds 15 31 33 Top five most active sectors—leveraged loans 6 €5,651 €2,594 €16,100 €9,733 Chemicals & materials Loans Loans 21 42 €3431 €9,417 28 17 €12,046 €11,172 €23,014 €7,406 TMT Pharmaceuticals UK & Ireland Italy High yield bonds High yield bonds 52 Services 18 17 40 €14,948 €17,012 Loans Healthcare €12,233 €11,742 €13,584 €8,785 €2635 €5,910 €9,168 €5,471 €12,292 €4,882 Loans 46 5 2 24 €20,316 €11,104 €3,464 €1,080 Sectors with highest number of debut issuers Services 4 Spain Manufacturing High yield bonds 3 14 9 Loans Lowest 2 2 Energy 2 Highest 11 Source: Debtwire Chemicals & materials TMT Map legend (overall activity ranking) €4,007 €4,050 6 €13,420 €1,495 All graph legend 14 White & Case Volume 2014 Value (€m) 2014 Volume 2015 Value (€m) 2015 A brave new world for international leveraged debt 15 . Evolution and alternatives in the market While fears of another downturn loom, the European financial markets have innovated, evolved and grown. F ollowing the collapse of Lehman Brothers and the period that followed, the markets have more understanding of the credit risk spectrum. This includes jurisdictional risk, available restructuring options and the complexity involved in any enforcement process. Further, restructuring is not the unknown prospect it was pre-crisis, as a generation of issuers, bankers and lawyers have all been through years of turmoil—and come out the other side much wiser. There is a larger pool of professionals who understand what it means to consider solutions for a debtor or issuer facing a liquidity or covenant crisis, including what entering into a restructuring process means and the key issues that are likely to arise. The certainty around relevant restructuring processes—including the English scheme of arrangement— has improved as the body of precedent has grown. High yield As the market considers the chance of another downturn, there is an expectation of a wave of high yield bond restructurings. debt has also been issued in record volumes in recent years.

Now, as the market considers the chance of another downturn, there is an expectation of a wave of high yield bond restructurings, and thought of the solutions that may follow. Non-traditional finance steps in However, many companies are not even getting as far as needing restructuring advice, due to another shift within the industry. There were fewer high yield bond restructurings in 2015 than some commentators had forecasted, due in the main to the available liquidity in the market. Further, non-traditional finance providers, being largely credit funds, have stepped in to offer a different option to issuers where traditional lending institutions have been unable to provide additional funding or refinancing options. It has become increasingly common for issuers to seek non-traditional financing solutions in the event of financial difficulty, allowing them to amend terms or to action softer restructuring options. Borrowers often do not care what form their finance takes. What is important is how much money can be borrowed, what interest rates are going to be like, what terms are going to be attached, and when a covenant might be breached that puts the borrower in default. These financings, which avoid a full scale restructuring, form part of a larger move towards a more flexible debt market on both sides of the Atlantic.

The low yield environment and strong liquidity have also gone some way to encourage lenders, such as fund managers and large institutional investors, to be a little more lenient—as long as the terms are right—as a default is arguably in no one’s interest. However, alternative capital still has a much higher yield expectation—and protection—than traditional high yield debt. Changing the law on high yield In 2014, German car park firm APCOA blazed a trail for a new restructuring solution when it became the first company to request lender consent to amend the governing law of its bank debt, in order to create sufficient connection to the UK to use a scheme of arrangement. Since this decision, several companies with high yield debt and no immediately apparent connection to the UK, including DTEK (a Ukrainian power company), have requested holders agree to change the governing law of their high yield bonds from New York to English law, so that the company can use the flexibility of an English scheme of arrangement. This is partly due to high yield bonds tending to be widely held and any amendment to key economic terms typically requires 90 percent consent.

This step may also be a more palatable option for companies who do not believe that a local law process can achieve a solution they are seeking. The English scheme of arrangement therefore forms a more user-friendly option for companies negotiating a solution to the capital structure. A brave new world for international leveraged debt 17 . Paris, France Innovation is the key to success in 2016 18 White & Case A s global debt markets push into 2016, diverging economic conditions on either side of the Atlantic—as well as geopolitical issues such as global stock market volatility and plummeting oil prices—mean issuers, lenders and their advisers are entering unknown territory. Two certainties remain, however: companies require financing, and investors still continue to hunt for yield. As a result, the European high yield and leveraged loan markets have been steadily growing in size and sophistication since the financial crisis, and are now established and accessible tools for borrowers and lenders alike. And after a slump in 2015, leveraged debt looks set to advance at a sustainable pace rather than the notable surge witnessed in 2014. Innovation is likely to continue into 2016, with issuers working with their advisers to structure new ways of raising capital that work for them, including continuing to import technology from the US markets. Bespoke deals are on the rise, and increasing levels of capital are being put to work by investors who prefer to stand by companies and work out strategies to get them through tough times rather than to head for default, insolvency or a complex and lengthy restructuring process. Additionally, secondary markets are developing in Europe, enhancing liquidity and strengthening the region’s position on the world’s stage. However, issuers are not going to have it all their own way. Lenders have begun to push back on terms that have become ever-more loose in recent years as volumes and values have risen. This will continue to be relevant in 2016. Given these considerations, perhaps a sophisticated and keen understanding of the differences between debt products and legal jurisdictional rules and their implications will define 2016. There is some way to go until Europe’s debt markets challenge the US, but if issuers and borrowers can work together, they will have already started out strongly on the right path. Innovation is likely to continue into 2016, with issuers working with their advisers to structure new ways of raising capital that work for them, including continuing to import technology from the US markets. A brave new world for international leveraged debt 19 . Contributors David Becker Partner E dbecker@whitecase.com Paul Clews Partner E pclews@whitecase.com Jill Concannon Partner E jconcannon@whitecase.com Lee Cullinane Partner E lcullinane@whitecase.com Jeremy Duffy Partner E jduffy@whitecase.com 20 White & Case Gareth Eagles Partner E geagles@whitecase.com Rob Mathews Partner E rmathews@whitecase.com Laura Prater Partner E lprater@whitecase.com Justin Wagstaff Partner E jwagstaff@whitecase.com James Greene Associate E jgreene@whitecase.com . Lee Cullinane Partner T +44 20 7532 1409 E lcullinane@whitecase.com In this publication, White & Case Rob Mathews means Partner the international legal practice comprising T +44 20 7532 1429 White & Case LLP a New , E rmathews@whitecase.comYork State registered limited liability partnership, White & Case LLP , a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities. whitecase.com This publication is © 2016 White & Case LLPprepared for the general information of our clients and other interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice. ATTORNEY ADVERTISING. Prior results do not guarantee a similar outcome. .

The boom times are not over for European high yield and leveraged loans in the long term, but the pace, flavour and overall feel will be different from the US-style model. It is going to be an interesting ride. II White & Case Lee Cullinane Partner, White & Case . Leveraged debt: The year in review Leveraged debt: The year in review European leveraged debt in focus Page 3 Page 14 A reset for debt in 2015? Evolution and alternatives in the market Page 7 Page 17 Eyes on Europe: cov-lite and Term Loan B rise Page 11 Innovation is the key to success in 2016 Page 18 HEADLINES n European loan and bond markets are down from the highs of 2014 n European high yield bonds value marginally up on 2014 total n Rise of European Term Loan B hints at further market convergence I f 2014 got pulses racing in the high yield debt and leveraged loan markets, 2015 came as something of a reality check. In the first nine months of 2014, combined issuance in these two debt instruments had already surpassed the entire previous year’s total by 12 percent. This €201 billion of European high yield debt and leveraged loans pushed on to a final count of almost €230 billion by the end of 2014. Fast-forward to the end of 2015 and the story was somewhat different. Just €179 billion in high yield debt and leveraged loans had been issued by the year end, with roughly half of that total transacted in the first quarter. Nevertheless, a strong Q4 2015 relative to Q4 2014 saw the full year value for high yield issuances surpass that of 2014, but by a mere five percent.

This compares with previous year-on-year increases of 21 percent in 2014, 52 percent in 2013 and 22 percent in 2012. Leveraged loan issuances fell by 43 percent year on year in 2015, to €73 billion. Slowdown in the global debt markets Geopolitical unrest and an uncertain economic outlook in several regions slowed down a high yield bond market that had taken full flight in the summer of 2014. The drop in issuance was not isolated to Europe. In the far larger US market, volumes and values Value of EU high yield bond and leveraged loan issuance by year 250,000 200,000 128,275 150,000 73,235 96,713 100,000 70,169 28,996 35,960 49,430 44,695 54,540 2010 50,000 2011 2012 82,996 100,818 105,911 2014 2015 0 High Yield Bonds 2013 Leveraged Loans Volume of EU high yield bond and leveraged loan issuance by year 600 500 400 208 161 300 122 200 100 91 43 86 244 105 Source: Debtwire Contents 123 2010 2011 2012 284 202 156 0 High Yield Bonds 2013 2014 2015 Leveraged Loans A brave new world for international leveraged debt 3 . Value of US high yield bond and leveraged loans issuances by year 1,000,000 Value (US$ million) 800,000 600,000 579,587 272,949 400,000 152,969 387,978 260,342 219,097 200,000 301,054 238,006 272,706 191,097 248,172 223,335 2014 2015 0 2010 2011 High Yield Bonds 2012 2013 Leveraged Loans were down in 2015, with the second quarter responsible for the year’s peak. A slump in the third quarter saw the lowest issuance of US high yield bonds in the last four years in terms of value, with barely US$223 billion being transacted in 2015 compared with US$301 billion at the market’s peak in 2012. It is a similar story for leveraged loans— 2015 saw the US have its worst year of capital-raising in leveraged loans since 2011. However, there was still demand for funding using high yield-style covenants and the markets shifted, in part, towards cov-lite Term Loan B (TLB) from instruments such as senior secured TLB. The former grew substantially over the last year— particularly in Europe. Vast differences in economic policy have impacted debt issuance on either side of the Atlantic, but there are reasons closer to home for both of them to explain why numbers have not kept up the pace in the past 18 months.

Not all of them are causes for alarm—and many will be important factors in 2016. Volume of US high yield bond and leveraged loans issuances by year 1,800 1,600 1,400 1,200 Volume 1,032 1,000 583 791 800 600 303 417 459 400 200 583 491 561 383 484 350 Source: Debtwire 0 2010 High Yield Bonds 4 White & Case 2011 2012 Leveraged Loans 2013 2014 2015 There was still demand for funding using high yield-style covenants and the markets shifted, in part, towards US Term Loan B, which grew substantially over the last year— particularly in Europe. CASE STUDY The rise of TLB Cabot Financial Cov-lite Term Loan B (TLB), in terms of covenant protection, has many similarities to high yield, though the former has typically softer call protections than those on the latter. This debt instrument caught on in Europe in 2014 and took hold in 2015. “Cov-lite” came into fashion from across the Atlantic and the issuing community has taken note. As the rest of the bond market slowed, TLBs came into their own, with a threefold uptick in European issuance year on year. However, despite investors’ search for yield, as volatility increases investors will limit how much risk they are willing to take.

The US$5.6 billion cross-border loan for tech company Veritas was pulled in November, for example, as prospective investors stayed cool on the deal due to a variety of reasons. This marked the second withdrawal of underwritten loan financing in a week, coming just after OM Group’s withdrawal of a US$575 million financing round. “It’s not unheard of for a bond on a best efforts basis to be withdrawn but the loan underwritten ones less so, one buy-sider told ” Debtwire at the time.

“Market volatility is the driver behind it. ” This indicates how quickly the market can change and how there can be new lines drawn in the sand for the sector as global economics shift. While the numbers show that looser terms became very successful in 2015, issuers and their advisers have been learning, innovating and talking with investors directly to refine and understand market focus points, helping deals get to market and doing their best to ensure no one loses out if and when financial difficulty strikes. As international M&A heats up and complex corporate structures become the new normal, White & Case has helped create a template for sophisticated, multi-subsidiary financings. The team advised Cabot Group in November 2015 on a transaction that amended a £200 million English law revolving credit facility agreement (including an accordion and amendments to accommodate Cabot Group’s growth in certain other jurisdictions) and issued €310 million in New York law senior secured floating rate notes. The proceeds were partially used to prepay a £90 million acquisition bridge facility which was entered into in June 2015. Additional sterling-denominated debt was also issued, taking the total existing indebtedness in the form of notes—other than the newly issued €310 million floating rate notes—to £690 million. The deal was certainly innovative as the revolving credit facility agreement and the senior secured floating rate notes, along with the additional debt issued, are regulated by two intercreditor agreements yet secured by the same security package (with different rankings). Additionally, the security package includes, amongst other security documents governed by Luxembourg law or Irish law, two separate English law debentures, each subject to a different intercreditor agreement. Following a major acquisition by one of its subsidiaries of the Marlin Financial Group in February 2014, Cabot did not terminate the existing Marlin intercreditor agreement regulating the debt of the acquired Marlin Financial Group due to the existence of £150 million senior secured fixed rate notes issued by a Marlin company.

Instead, Cabot amended it to align with its own conditions, meaning the consolidated group’s financial indebtedness has since been regulated by two intercreditor agreements. This extremely sophisticated deal forged an innovative legal solution for acquiring companies with complex existing debt arrangements. A brave new world for international leveraged debt 5 . A reset for debt in 2015? HEADLINES n Mean European leveraged loan deal size in 2015 was €600 million, compared with €617 million a year earlier n High yield bond issuances and leveraged loan allocations for refinancing have fallen substantially n Europe matures but 2015 is “reality check” for issuers A t the beginning of 2015, it was believed that the high yield bond and leveraged loan markets would continue at the levels seen in 2014. Issuance had peaked and terms were loosening. Indeed, the first quarter started well; however, as the midpoint of the year arrived, it was becoming clear that 2015 was not going to match the previous 12 months for issuance in the US and Europe. In 2014, some 60 percent of high yield bonds and 49 percent of leveraged loans had been issued in Europe for refinancing purposes. In 2015, that figure dropped to 46 percent and 36 percent, respectively. € 46% proceeds of 2015 European high yield bonds used for refinancing, compared with 60% in 2014 Many private equity sponsors looking to exit were seeing better valuations through an IPO than through a secondary sale or debt issuance. European equity markets have been very strong as a result, and this has cannibalised some of the demand for high yield.

The traditional tension between a leveraged refinancing, an IPO and an M&A exit shifted in 2015, as the IPO market proved stronger than in recent years. However, private equity did boost the market with funding for leveraged buyouts in 2015, particularly on the loans side. While the percentage of high yield bond proceeds used to finance these deals grew from five percent to nine percent, leveraged loan issuance for leveraged acquisitions over the two years grew from 33 percent for add-ons and leveraged buyouts in 2014 to 48 percent for the same in 2015. Loan sizes remain resilient Further evidence of this growing depth and strength can be seen in the size of deals that were transacted successfully in 2015. Despite the relative drop off in issuance, the ticket size offered by those coming to market has been resilient. The mean European leveraged loan deal size in 2015 was €600 million compared with €617 million a year earlier.

In the European high yield bonds use of proceeds 3% Add-on acquisition 2% General corporate purposes 20% 29% LBO ï¬nancing Reï¬nancing Spin-off Source: Debtwire 2014 60% 12% 46% 2015 5% Other 14% 9% A brave new world for international leveraged debt 7 . London, United Kingdom European leveraged loans use of proceeds 8% Add-on acquisition 5% 2% 14% Dividend recapitalization 20% General corporate purposes 6% LBO ï¬nancing 3% 2014 4% Merger 2% 2015 36% Reï¬nancing Repricing Working capital 19% Other 28% 1% 3% A reality check for the market The European market has increased in size, strength and attractiveness for lenders and borrowers alike, but 2015 has served as a reality check for some issuers who had been allowing themselves to get carried away. However, in the €150m 118 European leveraged loans issued in 2015 under EUR 150m European high yield bonds deal size 2015 70 Number of issuers 60 50 40 30 47 20 10 Source: Debtwire 65 26 24 Below EUR 150m 8 White & Case EUR 150m EUR 350m EUR 350m EUR 750m EUR 750m EUR 1.5bn European leveraged loans deal size 2015 Above EUR 1.5bn B-rated sector gets largest deals Certainly, investors were not just looking at credit ratings and sliding back up the risk scale. Well-known companies with a market history In the European high yield market, the average deal size in 2015 rose to €524 million, far outstripping the €355 million average tickets a year earlier. 140 120 100 80 60 118 88 40 42 20 4 0 current market, issuers have reset their expectations for pricing and investor appetite. The success story of 2014 put a different perspective on 2015—a year when lenders and investors became more cautious. In November, BlackRock, the world’s largest fund manager, said that given the uncertainty around oil prices, it viewed “the downside risk to high yield as too high to justify a larger allocation in [its] strategic portfolio” Bluebay, one of the largest . fixed income boutiques, said in the same month that investors were wary of how credit instruments would react to the first hike by the US Federal Reserve, which happened in December. After robust pre-July markets, macro and industry-specific events hit the sector.

Issuers fell into two camps: companies that were known to the market, had a strong background, who went to the market with aggressive pricing and had little or no pushback; or companies that had no rating, were in an industry that was not doing well or had no market history. Any of these three characteristics meant they had wider pricing and tighter terms and, in some cases, simply did not get deals done. Number of borrowers with 12 asking for between €1.5 billion and €750 million. On the high yield bond side, the key range was between €350 million and €750 million, with 65 companies issuing at that level. European high yield market, the average deal size in 2015 rose to €524 million, far outstripping the €355 million average tickets a year earlier. In fact, the average deal size in 2011 – 2014 had been within the €340 million to €363 million range. However, breaking these numbers down might suggest a couple of outlying deals skewed the numbers in 2015.

By far, the largest component of leveraged loan issuers aimed to borrow less than €150 million in 2015. Six aimed at borrowing more than €1.5 billion, Source: Debtwire Source: Debtwire 49% 12 0 Below EUR 150m EUR 150m EUR 350m EUR 350m EUR 750m 6 EUR 750m EUR 1.5bn Above EUR 1.5bn A brave new world for international leveraged debt 9 . European bond issuance by S&P rating, 2015 # Issues Amount (EUR m) Weighted Average YTM Weighted Average Net Leverage BB+ 23 16,063 4.74% 4.05x BB 15 9,379 3.46% 23 17,396 5.31% 3.92x B+ 30 8,899 6.04% 4.24x B 32 25,598 6.02% 4.63x B- 15 5,377 7.26% 4.86x CCC+ 8 2,542 7.50% 4.85x CCC 2 490 11.66% 6.97x Total 148 85,745 6.50% 4.67x were doing well. With bonds worth €25.6 billion, collective capital raised by 32 B-rated issuers surpassed the next largest group by almost €8.2 billion in 2015. Some 23 BBissuers raised €17 billion, while .4 23 BB+ issuers raised €16.1 billion, according to Standard & Poor’s. In fact, there were more deals in the B and B+ sector than in the BB- to BB+ sector put together in 2015. At an average €789.9 million, issuers awarded a B by Standard & Poor’s managed to get the largest deals away—many of which were oversubscribed, according to Reuters data. Investors willing to venture this far down the risk scale were rewarded with relatively impressive returns.

In 2015, the weighted average yield to maturity on B and B+ rated issuers were 6.02 percent and 6.04 percent, respectively. 10 Eyes on Europe: Cov-lite and Term Loan B rise 3.84x BB- Source: Debtwire Rating White & Case CASE STUDY GTECH/IGT Plc Innovation was key to the largest Italian bond issued on international capital markets to date, with White & Case acting as the issuer’s international counsel for New York, English and Italian law. The firm represented gaming business GTECH on its issuance of senior secured notes denominated in three tranches of US$3.2 billion and two tranches of €1.55 billion in February 2015. The deal, which helped finance the acquisition of IGT Group by the issuer, used a cross-border pari passu bond/bank transaction and supported a complex capital structure. The team employed —and enhanced—the latest technologies in European bond/bank structures. An innovative temporary note structure allowed for the issuance of notes pre-completion—which would not have been permitted by the existing capital structure—thus allowing timely access to the market and improved commercial terms. The deal also was the first in Europe to see existing Eurobond note holders obtain a pre-agreement to enter an intercreditor agreement at completion, as the issuance of new secured notes tripped their negative pledge. The deal was one of the few secured “covenant lite” high yield transactions completed in Europe, and it proved to be a marketleading precedent for companies temporarily crossing into the sub-investment grade space. HEADLINES n US issuers look to Europe n Cov-lite loans growing in popularity on the continent n US Term Loan B structure has been adopted across the other side of the Atlantic n Investors concerned over erosion of covenant protection T he growth of European markets was noticed by US issuers, who have looked across the Atlantic to borrow as pricing widened in the US and appetite increased in Europe. In the second quarter of 2015, US issuers were the second-largest group raising euro-denominated debt, according to Source Ratings. At certain points in 2015, the difference in margin meant it was cheaper to raise funds in Europe than in the US.

Companies that were well known to investors or had a good credit rating were able to take advantage. Even with FX costs, in some cases this still proved to be cheaper than raising dollars in the US itself. Europe—at least for the moment —offers better macroeconomic conditions for both issuers and lenders than the US. On the east of the Atlantic, the European Central Bank has launched further quantitative easing to flood markets with liquidity; to the west, the financial sector had been anxiously waiting for a rate rise for several months and finally got one in December. Liquidity favours Europe for now, and this looks set to endure as the European Central Bank said it will extend its quantitative easing program until at least March 2017 , while its interest rate remains at record lows. The right credits are getting deals done at the right pricing in Europe, with limited or no flex.

This will 23% European first lien cov-lite loans in 2015, compared with 15% in 2014 41% US first lien loans that were cov-lite in 2015, compared with 48% in 2014 likely continue in early 2016 due to these underlying fundamentals, whereas the US may struggle. In current market conditions in the US, as the Veritas deal has shown, even after flex some deals are not getting sold. Covenant-lite rises in Europe This flex has become necessary— in some cases—due to the phenomenon that has swept through European debt markets to great triumph since last year. The phrase “covenant-lite” which has , long been common parlance in the US market, was increasingly used by European issuers in 2014. In the last 12 months, it has seen even more frequent usage and acceptance.

However, the majority of European leveraged loans still retain a quarterly tested leverage ratio for the benefit of both the revolving and term loan lenders. One of the few leveraged loan instruments that saw an increase in issuance in Europe last year was the “covenant-lite Term Loan B” . However, that increase was huge. In 2014, some €6.3 billion was transacted through ten deals. The next year, more than €19.5 billion had been issued through 48 deals. Greater flexibility has been afforded to issuers in 2015, as participants engage in dialogue to address business needs for borrowers and investment risk for lenders. This has meant companies have been able to transact using terms that are more suited to their circumstances and needs within acceptable parameters for lenders. Borrowers should now be asking themselves several questions when deciding what covenant package will be negotiated into documentation. These include finding out whether there’s a maintenance covenant on the debt, whether they have amortisation, whether they have baskets that grow with EBITDA or assets, and whether they have an excess cash-flow sweep. This is vital, as all these points have moved towards the borrower over recent years.

It is now very common for a loan in Europe to be non-amortising, with no maintenance covenant and with flexible baskets. Both parties need to start on the same page to ensure expectations are met. Investors cautious over cov-lite As this part of the market moves to benefit issuers, investors need to be cautious as there are fundamental differences between the US and European jurisdictions—and they should be aware of them before buying into the cov-lite phenomenon. Cov-lite works in the US because of the liquidity and depth of the market. One of the reasons investors in the US typically do not require a financial covenant is because the investment model suggests that they should be able to trade out should the need arise. That is generally not the case in Europe—at least not yet. The market is growing, however, it is still A brave new world for international leveraged debt 11 .

reasonably nascent, and investors cannot adopt the same assumption that they will be able to exit if they decide that a credit’s performance and forecast numbers are not to their liking anymore. While a move back to non-cov-lite may not be on the cards, investors are being very selective and more focused on the same issues they look at in a bond, such as wider industry benchmarks and leverage levels. As the secondary market develops, it will mean more flexible terms are agreed to as a result of the ability to move easily between primary and secondary lenders. But the new kid on the block, which is becoming increasingly established, is the non-bank lender. 26,634 Senior Secured TLB 42,600 19,569 Covenant-lite TLB 6,331 7,202 Senior Secured Term Loan 10,729 Senior Secured Revolver 4,083 Covenant-lite Term Loan 3,945 19,387 13,479 7,062 1,687 Senior Unsecured Term Loan 6,200 1,669 Super Senior Revolver 1,147 1,079 Covenant-lite Revolver 798 1,078 Senior Secured TLC 1,370 1,076 Second Lien 3,100 Senior Unsecured Revolver White & Case 0% 45 10 38 10% 20% European cov-lite 30% 40% 50% US cov-lite 7 Senior Secured TLA 27 Senior Unsecured 5 Term Loan 9 10 Super Senior Revolver 19 9 Covenant-lite Revolver 11 3 Senior Secured TLC 7 10 Second Lien 19 3 2 11 Senior Secured Capex / Acquisition Facility 25 Covenant-lite 5 Second Lien 1,344 9 2 475 75 6,294 2014 41 99 Covenant-lite Term Loan 10,000 20,000 30,000 40,000 50,000 While a move back to non-cov-lite may not be on the cards yet, investors are being very selective and more focused on the same issues they look at in a bond, such as wider industry benchmarks and leverage levels. First lien 1 11 Other Source: Debtwire Source: Debtwire 4,083 23 2015 23 Senior Unsecured Revolver 1,087 2015 48 21 Senior Secured Revolver 556 0 2014 10 Senior Secured Term Loan 1,184 Other 12 Covenant-lite TLB 775 First lien 24 106 15 643 Covenant-lite Second Lien 2013 48 668 Senior Secured Capex / Acquisition Facility First lien loans (percentage) 64 Senior Secured TLB Rise of non-bank lending Where non-banks are providing the funding, typically, the debt is not being distributed and the original provider generally remains as the lender. They will, therefore, agree bespoke packages for the business because they don’t need to sell the debt on, thereby adjusting the balance between achieving a solution for credit purposes and documenting a transaction that looks like all the others. The market is also growing at pace. Non-bank lenders are raising funds very regularly, and they are getting bigger; there is a great deal of appetite for investing money in non-bank finance structures. 1,699 Senior Secured TLA European leveraged loan instrument by volume Source: Xtract European leveraged loan instrument by value 25 0 2015 20 40 60 80 100 120 2014 A brave new world for international leveraged debt 13 .

European leveraged debt in focus Selected European leveraged loan and high yield bond markets by volume Benelux Germany High yield bonds Top five most active sectors—high yield bonds High yield bonds 24 55 23 €13,793 7 €12,341 €9,943 €9,180 Loans Iceland Scale: 50% Loans 27 Pharmaceuticals Loans €9,462 4 €21,404 €8,040 €9,090 €13,292 €1,321 €9,540 21 18 €22,903 Automotive €8,539 €2,078 32 16 €22,545 High yield bonds 30 14 €27,950 TMT The Nordics Chemicals & materials €6,839 €930 Financial Services France €2,191 €6,427 CEE High yield bonds €3,018 €7,294 High yield bonds 15 31 33 Top five most active sectors—leveraged loans 6 €5,651 €2,594 €16,100 €9,733 Chemicals & materials Loans Loans 21 42 €3431 €9,417 28 17 €12,046 €11,172 €23,014 €7,406 TMT Pharmaceuticals UK & Ireland Italy High yield bonds High yield bonds 52 Services 18 17 40 €14,948 €17,012 Loans Healthcare €12,233 €11,742 €13,584 €8,785 €2635 €5,910 €9,168 €5,471 €12,292 €4,882 Loans 46 5 2 24 €20,316 €11,104 €3,464 €1,080 Sectors with highest number of debut issuers Services 4 Spain Manufacturing High yield bonds 3 14 9 Loans Lowest 2 2 Energy 2 Highest 11 Source: Debtwire Chemicals & materials TMT Map legend (overall activity ranking) €4,007 €4,050 6 €13,420 €1,495 All graph legend 14 White & Case Volume 2014 Value (€m) 2014 Volume 2015 Value (€m) 2015 A brave new world for international leveraged debt 15 . Evolution and alternatives in the market While fears of another downturn loom, the European financial markets have innovated, evolved and grown. F ollowing the collapse of Lehman Brothers and the period that followed, the markets have more understanding of the credit risk spectrum. This includes jurisdictional risk, available restructuring options and the complexity involved in any enforcement process. Further, restructuring is not the unknown prospect it was pre-crisis, as a generation of issuers, bankers and lawyers have all been through years of turmoil—and come out the other side much wiser. There is a larger pool of professionals who understand what it means to consider solutions for a debtor or issuer facing a liquidity or covenant crisis, including what entering into a restructuring process means and the key issues that are likely to arise. The certainty around relevant restructuring processes—including the English scheme of arrangement— has improved as the body of precedent has grown. High yield As the market considers the chance of another downturn, there is an expectation of a wave of high yield bond restructurings. debt has also been issued in record volumes in recent years.

Now, as the market considers the chance of another downturn, there is an expectation of a wave of high yield bond restructurings, and thought of the solutions that may follow. Non-traditional finance steps in However, many companies are not even getting as far as needing restructuring advice, due to another shift within the industry. There were fewer high yield bond restructurings in 2015 than some commentators had forecasted, due in the main to the available liquidity in the market. Further, non-traditional finance providers, being largely credit funds, have stepped in to offer a different option to issuers where traditional lending institutions have been unable to provide additional funding or refinancing options. It has become increasingly common for issuers to seek non-traditional financing solutions in the event of financial difficulty, allowing them to amend terms or to action softer restructuring options. Borrowers often do not care what form their finance takes. What is important is how much money can be borrowed, what interest rates are going to be like, what terms are going to be attached, and when a covenant might be breached that puts the borrower in default. These financings, which avoid a full scale restructuring, form part of a larger move towards a more flexible debt market on both sides of the Atlantic.

The low yield environment and strong liquidity have also gone some way to encourage lenders, such as fund managers and large institutional investors, to be a little more lenient—as long as the terms are right—as a default is arguably in no one’s interest. However, alternative capital still has a much higher yield expectation—and protection—than traditional high yield debt. Changing the law on high yield In 2014, German car park firm APCOA blazed a trail for a new restructuring solution when it became the first company to request lender consent to amend the governing law of its bank debt, in order to create sufficient connection to the UK to use a scheme of arrangement. Since this decision, several companies with high yield debt and no immediately apparent connection to the UK, including DTEK (a Ukrainian power company), have requested holders agree to change the governing law of their high yield bonds from New York to English law, so that the company can use the flexibility of an English scheme of arrangement. This is partly due to high yield bonds tending to be widely held and any amendment to key economic terms typically requires 90 percent consent.

This step may also be a more palatable option for companies who do not believe that a local law process can achieve a solution they are seeking. The English scheme of arrangement therefore forms a more user-friendly option for companies negotiating a solution to the capital structure. A brave new world for international leveraged debt 17 . Paris, France Innovation is the key to success in 2016 18 White & Case A s global debt markets push into 2016, diverging economic conditions on either side of the Atlantic—as well as geopolitical issues such as global stock market volatility and plummeting oil prices—mean issuers, lenders and their advisers are entering unknown territory. Two certainties remain, however: companies require financing, and investors still continue to hunt for yield. As a result, the European high yield and leveraged loan markets have been steadily growing in size and sophistication since the financial crisis, and are now established and accessible tools for borrowers and lenders alike. And after a slump in 2015, leveraged debt looks set to advance at a sustainable pace rather than the notable surge witnessed in 2014. Innovation is likely to continue into 2016, with issuers working with their advisers to structure new ways of raising capital that work for them, including continuing to import technology from the US markets. Bespoke deals are on the rise, and increasing levels of capital are being put to work by investors who prefer to stand by companies and work out strategies to get them through tough times rather than to head for default, insolvency or a complex and lengthy restructuring process. Additionally, secondary markets are developing in Europe, enhancing liquidity and strengthening the region’s position on the world’s stage. However, issuers are not going to have it all their own way. Lenders have begun to push back on terms that have become ever-more loose in recent years as volumes and values have risen. This will continue to be relevant in 2016. Given these considerations, perhaps a sophisticated and keen understanding of the differences between debt products and legal jurisdictional rules and their implications will define 2016. There is some way to go until Europe’s debt markets challenge the US, but if issuers and borrowers can work together, they will have already started out strongly on the right path. Innovation is likely to continue into 2016, with issuers working with their advisers to structure new ways of raising capital that work for them, including continuing to import technology from the US markets. A brave new world for international leveraged debt 19 . Contributors David Becker Partner E dbecker@whitecase.com Paul Clews Partner E pclews@whitecase.com Jill Concannon Partner E jconcannon@whitecase.com Lee Cullinane Partner E lcullinane@whitecase.com Jeremy Duffy Partner E jduffy@whitecase.com 20 White & Case Gareth Eagles Partner E geagles@whitecase.com Rob Mathews Partner E rmathews@whitecase.com Laura Prater Partner E lprater@whitecase.com Justin Wagstaff Partner E jwagstaff@whitecase.com James Greene Associate E jgreene@whitecase.com . Lee Cullinane Partner T +44 20 7532 1409 E lcullinane@whitecase.com In this publication, White & Case Rob Mathews means Partner the international legal practice comprising T +44 20 7532 1429 White & Case LLP a New , E rmathews@whitecase.comYork State registered limited liability partnership, White & Case LLP , a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities. whitecase.com This publication is © 2016 White & Case LLPprepared for the general information of our clients and other interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice. ATTORNEY ADVERTISING. Prior results do not guarantee a similar outcome. .