Sustainable Investing as Performance Investing - May 2016

Thornburg Investment Management

Description

Sustainable Investing as Performance Investing

Rolf Kelly, cfa | Portfolio Manager

January 2016 (updated May 2016)

How does a best-in-class, publicly traded company that incorporates

high standards for its environmental impact, social values, and corporate governance generate meaningful returns for its shareholders?

By doing just that.

Executive Summary

• The reputation of Environmental, Social, and Governance (ESG) investing of inherent underperformance is slowly changing, as empirical evidence demonstrates that this approach can

provide outperformance over time.

• Sustainable investing is increasingly gaining more of the spotlight in this space, much the

result of nascent but widening attention from Millennials.

• Individuals and institutions alike embrace sustainable investing for its focus on financial results

as well as “positive screens” that seek both social, environmental, and governance impact.

• Data show that companies that exhibit meaningful and measurable sustainable investing

attributes tend to outperform over the long term.

thornburg.com | 877.215.1330

. 2 | Sustainable Investing as Performance Investing

Responsible investing has evolved in

the past decade to encompass strategies ranging from socially responsible

investing (SRI) to proactively executed impact investing. ESG (environmental, social, and governance) is

one such strategy of a more modern

vintage. One criticism that ESG and

other responsible investing strategies

face is the perception of underperformance. Empirical results show ESG

investing not only lives up to the performance of conventional fund benchmarks, but that it has the potential to

outperform them.

Early Negative Impressions

Slowly Reversing

The impression of assumed underperformance around responsible investing

came from the early days of socially

responsible investing, especially within

“green” focused strategies.

SRI investment strategies typically used only negative screening to exclude companies or industries that didn’t align with sometimes myopic personal values or ethical guidelines. In the process, such strategies frequently sacrificed ESG investing not only lives up to the performance of conventional fund benchmarks, but it has the potential to outperform them. diversification and fiduciary duty to SRI-imposed strictures. The result was imbalanced portfolios that were heavy in small and early-stage technology companies.

Therefore, they may have been socially responsible, but they were also non-diversified, higher-risk portfolios. Moreover, they eventually underperformed the indexes to the detriment of investors, who felt good about their strategies but were left with little to show for their efforts. This left a negative impression not only of SRI but of any investing strategies that incorporate non-financial factors. Attitudes are changing, however, as more attention—and data—heighten appreciation for the dynamic nature of the ESG space.

For example, a growing body of research suggests that performance of more developed, well-conceived strategies often perform in line with, or even outperform, conventional indexes. One study combined the results of 60 empirical reports that compared the performance of SRI funds against their non-SRI peers. The result showed significant alignment in the performance of SRI funds with that of their peer group (see Figure 1).1 This is surprising, given that SRI strategies may summarily side-step potentially rewarding companies, even whole sectors, using negative screens.

What is encouraging, however, is the fact that this is a quantum leap from where they were 20 years ago. As the space evolves—and differentiating approaches emerge— opportunities will abound for significant outperformance. To this point, a Figure 1 | Academic Evidence on SRI Looks Mostly Aligned, but Far Better than 20 Years Ago Studies on the Performance of SRI Funds Versus Non-SRI Funds Number of Papers Reaching Each Conclusion, 1990 through Early-May 2014 Today, traditional (“negative screening”) SRI fund returns align with conventional funds.

The few that outperform typically apply “positive” screens to stock selection. Source: “ESG and Stock Selection,” Rochester H. Cahan, cfa. Empirical Research Partners (2015). Past performance does not guarantee future results. .

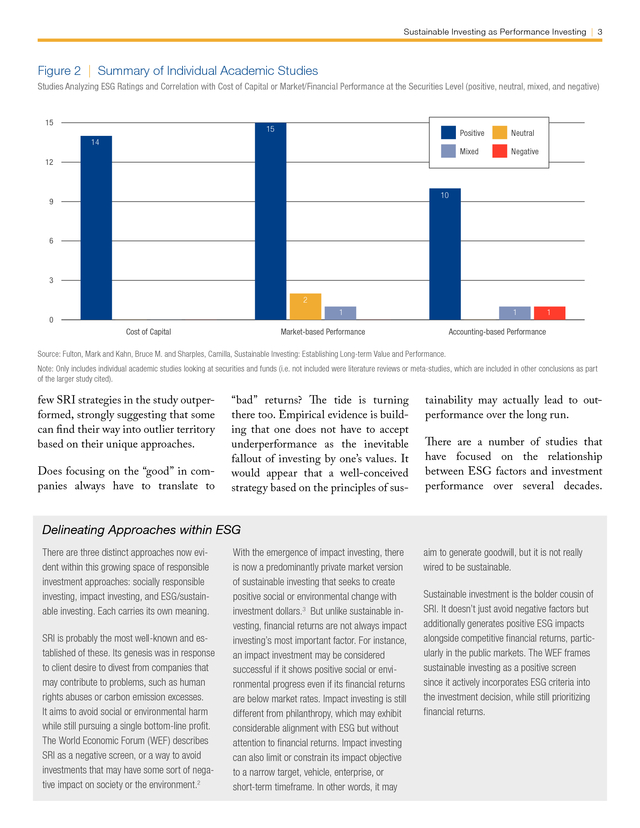

Sustainable Investing as Performance Investing | 3 Figure 2 | Summary of Individual Academic Studies Studies Analyzing ESG Ratings and Correlation with Cost of Capital or Market/Financial Performance at the Securities Level (positive, neutral, mixed, and negative) 15 15 Positive Neutral Mixed 14 Negative 12 10 9 6 3 2 1 0 Cost of Capital 1 Market-based Performance 1 Accounting-based Performance Source: Fulton, Mark and Kahn, Bruce M. and Sharples, Camilla, Sustainable Investing: Establishing Long-term Value and Performance. Note: Only includes individual academic studies looking at securities and funds (i.e. not included were literature reviews or meta-studies, which are included in other conclusions as part of the larger study cited). few SRI strategies in the study outperformed, strongly suggesting that some can find their way into outlier territory based on their unique approaches. Does focusing on the “good” in companies always have to translate to “bad” returns? The tide is turning there too. Empirical evidence is building that one does not have to accept underperformance as the inevitable fallout of investing by one’s values.

It would appear that a well-conceived strategy based on the principles of sus- tainability may actually lead to outperformance over the long run. There are a number of studies that have focused on the relationship between ESG factors and investment performance over several decades. Delineating Approaches within ESG There are three distinct approaches now evident within this growing space of responsible investment approaches: socially responsible investing, impact investing, and ESG/sustainable investing. Each carries its own meaning. SRI is probably the most well-known and established of these. Its genesis was in response to client desire to divest from companies that may contribute to problems, such as human rights abuses or carbon emission excesses. It aims to avoid social or environmental harm while still pursuing a single bottom-line profit. The World Economic Forum (WEF) describes SRI as a negative screen, or a way to avoid investments that may have some sort of negative impact on society or the environment.2 With the emergence of impact investing, there is now a predominantly private market version of sustainable investing that seeks to create positive social or environmental change with investment dollars.3 But unlike sustainable investing, financial returns are not always impact investing’s most important factor.

For instance, an impact investment may be considered successful if it shows positive social or environmental progress even if its financial returns are below market rates. Impact investing is still different from philanthropy, which may exhibit considerable alignment with ESG but without attention to financial returns. Impact investing can also limit or constrain its impact objective to a narrow target, vehicle, enterprise, or short-term timeframe.

In other words, it may aim to generate goodwill, but it is not really wired to be sustainable. Sustainable investment is the bolder cousin of SRI. It doesn’t just avoid negative factors but additionally generates positive ESG impacts alongside competitive financial returns, particularly in the public markets. The WEF frames sustainable investing as a positive screen since it actively incorporates ESG criteria into the investment decision, while still prioritizing financial returns. .

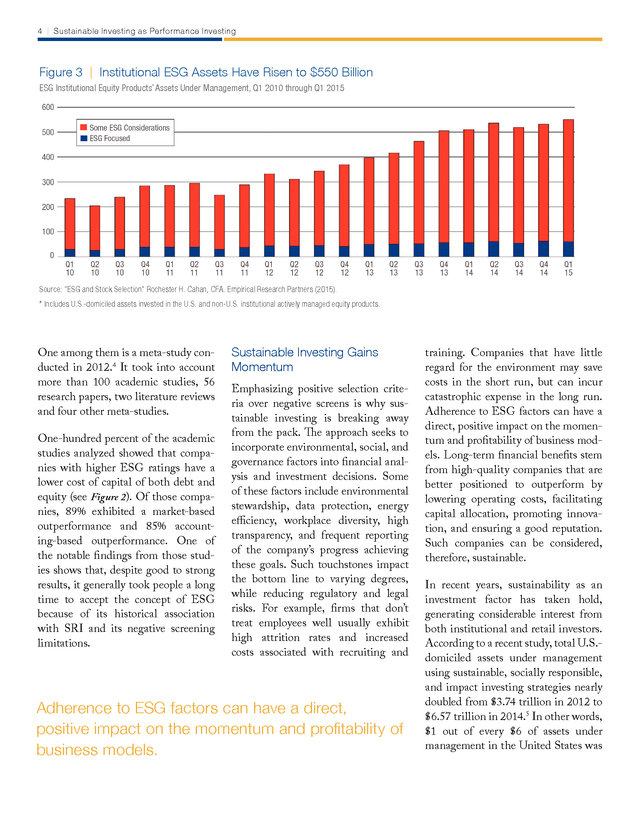

4 | Sustainable Investing as Performance Investing Figure 3 | Institutional ESG Assets Have Risen to $550 Billion ESG Institutional Equity Products* Assets Under Management, Q1 2010 through Q1 2015 Source: “ESG and Stock Selection” Rochester H. Cahan, CFA. Empirical Research Partners (2015). * Includes U.S.-domiciled assets invested in the U.S. and non-U.S.

institutional actively managed equity products. One among them is a meta-study conducted in 2012.4 It took into account more than 100 academic studies, 56 research papers, two literature reviews and four other meta-studies. One-hundred percent of the academic studies analyzed showed that companies with higher ESG ratings have a lower cost of capital of both debt and equity (see Figure 2). Of those companies, 89% exhibited a market-based outperformance and 85% accounting-based outperformance. One of the notable findings from those studies shows that, despite good to strong results, it generally took people a long time to accept the concept of ESG because of its historical association with SRI and its negative screening limitations. Sustainable Investing Gains Momentum Emphasizing positive selection criteria over negative screens is why sustainable investing is breaking away from the pack.

The approach seeks to incorporate environmental, social, and governance factors into financial analysis and investment decisions. Some of these factors include environmental stewardship, data protection, energy efficiency, workplace diversity, high transparency, and frequent reporting of the company’s progress achieving these goals. Such touchstones impact the bottom line to varying degrees, while reducing regulatory and legal risks.

For example, firms that don’t treat employees well usually exhibit high attrition rates and increased costs associated with recruiting and Adherence to ESG factors can have a direct, positive impact on the momentum and profitability of business models. training. Companies that have little regard for the environment may save costs in the short run, but can incur catastrophic expense in the long run. Adherence to ESG factors can have a direct, positive impact on the momentum and profitability of business models. Long-term financial benefits stem from high-quality companies that are better positioned to outperform by lowering operating costs, facilitating capital allocation, promoting innovation, and ensuring a good reputation. Such companies can be considered, therefore, sustainable. In recent years, sustainability as an investment factor has taken hold, generating considerable interest from both institutional and retail investors. According to a recent study, total U.S.domiciled assets under management using sustainable, socially responsible, and impact investing strategies nearly doubled from $3.74 trillion in 2012 to $6.57 trillion in 2014.5 In other words, $1 out of every $6 of assets under management in the United States was .

Sustainable Investing as Performance Investing | 5 invested in some form of responsible investment strategy. This is a good sign that implies the misconception of underperformance associated with socially responsible investing is nearing an end. It is no longer a fringe movement. Further evidence in the “Global Sustainable Investment Review 2014” found that the responsible investing market (broadly defined to include socially responsible, ESG/sustainable, and impact investing) has continued to grow in both absolute and relative terms, rising from $13.3 trillion at the outset of 2012 to $21.4 trillion at the start of 2014.6 The market has also grown from 21.5% to 30.2% of the professionally managed assets in the regions covered. Over this two-year period, the fastest-growing region of demand has been within the United States, followed by Canada and Europe, where adoption already is very high. Hand in glove with the growing sustainable investing market is the approach’s increasing credibility as a mainstream investment theme.

For example, the Rockefeller Brothers Fund’s decision to align its endowment’s environmental and investing goals represents an iconic institutional level move that opened a lot of eyes, and could help advance the cause of “fossil-free investing.” By example, it has helped to boost divestment and investor interest in limiting or removing the worst carbon-emitting industries from portfolios. As an industry, we may be able to learn much from pension funds, sovereign wealth vehicles, endowments, and other institutions that have been experimenting with ways to incorporate ESG factors into their investment processes while ... sustainability as an investment factor has taken hold, generating considerable interest from both institutional and retail investors. balancing long-term risks against short-term share price movements (See Figure 3). On the individual level, too, sustainable investing is in demand because it offers clients a way to align pocketbooks with ethics.

According to Morningstar, about 84% of Millennials (those born between 1980 and 2002) express specific desire for sustainable investing. As they enter their 40s and hit their financial planning stride, it can only spell ever-higher demand for investing that combines meaningful impact alongside returns. Whether at the institutional or the individual level, sustainable investing is increasingly tantamount to proactively promoting environmental stewardship, encouraging good corporate practices, or supporting workplace diversity among individual holdings. Sustainable Investing: Meaningful & Measurable Sustainable investing strategies pay attention to a few specific areas as they incorporate ESG attributes into their selection process: is the company a good corporate citizen (i.e., does it show a commitment to things like workplace diversity, environmentally friendly practices, and investing in the local economy)? Does it live up to the disclosure and governance guidelines set forth by shareholders? In many regards, value investors, who are perhaps the most well-equipped and experienced to embrace sustainable investing principles, have been asking these questions all along. After all, value disciplines and sustainable investing are all about patience, intensive research, and finding individual high-quality companies with longterm growth potential. In sustainable investing, the ideal business models would have to demonstrate measurable value to both the company and its stakeholders (customers, employees, government, and communities).

Stakeholders can have a direct effect on a company’s profits and progress, so how they are affected is a key component in the evaluation of a company’s ESG impact. Many different outcomes may be measured to evaluate a company’s progress with ESG: environmental performance, number of women in leadership roles, history of regulatory and legal actions against the company, capital allocation, etc. The Opportunity Ahead Responsible investing has traveled a long way from the initial stages of simply applying negative screens. The use of ESG factors to enhance a portfolio with positive selection criteria is here to stay. Despite growing interest and awareness, alignment with positive impact factors should not be viewed as .

6 | Sustainable Investing as Performance Investing a panacea, but rather as one investment approach among many. And, like any discipline, it should be considered on a strategy-by-strategy basis. Finally, the sustainable investing approach is not about passing moral judgment on companies, but rather reaching for a better way to analyze and project long-term performance of their business models. Companies that incorporate ESG into their operations tend to be well positioned to outperform, as they can work more productively with their stakeholders, lower their operating costs over the long run, and facilitate better capital allocation, greater innovation, and enhanced reputations. With these goals, sustainable business models and practices are poised to generate profits over the long-term and, ultimately, higher share prices.

n ... the sustainable investing approach is not about passing moral judgment on companies, but rather reaching for a better way to analyze and project long-term performance of their business models. 1. “ESG and Stock Selection” Rochester H. Cahan, cfa. Empirical Research Partners (2015), http://www.empirical-research.com/esg-and-stock-selection/ 2. “From the Margins to the Mainstream: Assessment of the Impact Investment Sector and Opportunities to Engage Mainstream Investors,” World Economic Forum Investors Industries and Deloitte Touche Tohmatsu (2013), http://www3.weforum.org/docs/WEF_II_FromMarginsMainstream_Report_2013.pdf com/abstract=2222740 orhttp://dx.doi.org/10.2139/ ssrn.2222740 5. Investment Company Institute. 6. “Global Sustainable Investment Review 2014,” Global Sustainable Investment Alliance (2015): 3, accessed on September 6, 2015, http://www.gsi-alliance.org/ wp-content/uploads/2015/02/GSIA_Review_download.pdf 3. “Introducing the Impact Investing Benchmark,” Cambridge Associates and the Global Impact Investing Network (2015), accessed on September 5, 2015, http://www.thegiin.org/assets/documents/pub/Introducing_the_Impact_Investing_Benchmark.pdf 4. Fulton, Mark and Kahn, Bruce M.

and Sharples, Camilla, “Sustainable Investing: Establishing Long-term Value and Performance” (June 12, 2012). http://ssrn. Sustainable Investing at Thornburg As a successful value investor, Thornburg seamlessly embraced sustainable investing to create an ESG-tilted mandate for retail and institutional clients. After all, sustainable investing—much like value strategies—requires a long-term, patient, and research-intensive mindset to succeed.

In searching the investment universe to support our ESG mandate, we typically focus on components that affect an investment’s sustainability attributes, like climate change, social conflicts, availability of natural resources, etc. As we see it, sustainable investing practices span all industries, but some attributes are industry specific. For example, carbon emissions are not necessarily a material issue for an IT firm, but they are for a utility company. In some business models, we look for positive “sustainable investing momentum,” which means the company may not be perfect on ESG currently, but it is demonstrably taking ESG issues seriously by actively improving on them. Alternatively, the ESG classification of a company would be low if the company has a poor sustainability rating relative to its industry peers or is dismissive of sustainable investing values.

Companies not performing up to our ESG standards are typically called upon, so that we can directly engage with company management to find answers. Thornburg has been managing separate accounts under sustainable investing standards for more than 10 years. Portfolio Manager Rolf Kelly, cfa, has been the primary steward on these accounts since 2010. “At first, I had my doubts, given wide misconception about sustainable investing’s effectiveness. We’re trained early on that if you limit the investible universe, it makes it harder to find relative value and outperform,” Kelly says.

“But this isn’t always true. In fact, narrowing your focus through ESG enables you to select from a smaller universe of better-run, more sustainable companies. Done the right way, we found that this approach to sustainable investing can indeed outperform.” .

. Important Information The views expressed by the portfolio manager reflect his professional opinions and should not be considered buy or sell recommendations. These views are subject to change. Investments carry risks, including possible loss of principal. Additional risks may be associated with investments outside the United States, especially in emerging markets, including currency fluctuations, illiquidity, volatility, and political and economic risks. Investments in small- and mid-capitalization companies may increase the risk of greater price fluctuations. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses. Past performance does not guarantee future results. Before investing, carefully consider the Fund’s investment goals, risks, charges, and expenses.

For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit thornburg.com. Read them carefully before investing. 5/23/16 Thornburg Securities Corporation, Distributor | 2300 North Ridgetop Road | Santa Fe, New Mexico 87506 | 877.215.1330 TH3442 .

SRI investment strategies typically used only negative screening to exclude companies or industries that didn’t align with sometimes myopic personal values or ethical guidelines. In the process, such strategies frequently sacrificed ESG investing not only lives up to the performance of conventional fund benchmarks, but it has the potential to outperform them. diversification and fiduciary duty to SRI-imposed strictures. The result was imbalanced portfolios that were heavy in small and early-stage technology companies.

Therefore, they may have been socially responsible, but they were also non-diversified, higher-risk portfolios. Moreover, they eventually underperformed the indexes to the detriment of investors, who felt good about their strategies but were left with little to show for their efforts. This left a negative impression not only of SRI but of any investing strategies that incorporate non-financial factors. Attitudes are changing, however, as more attention—and data—heighten appreciation for the dynamic nature of the ESG space.

For example, a growing body of research suggests that performance of more developed, well-conceived strategies often perform in line with, or even outperform, conventional indexes. One study combined the results of 60 empirical reports that compared the performance of SRI funds against their non-SRI peers. The result showed significant alignment in the performance of SRI funds with that of their peer group (see Figure 1).1 This is surprising, given that SRI strategies may summarily side-step potentially rewarding companies, even whole sectors, using negative screens.

What is encouraging, however, is the fact that this is a quantum leap from where they were 20 years ago. As the space evolves—and differentiating approaches emerge— opportunities will abound for significant outperformance. To this point, a Figure 1 | Academic Evidence on SRI Looks Mostly Aligned, but Far Better than 20 Years Ago Studies on the Performance of SRI Funds Versus Non-SRI Funds Number of Papers Reaching Each Conclusion, 1990 through Early-May 2014 Today, traditional (“negative screening”) SRI fund returns align with conventional funds.

The few that outperform typically apply “positive” screens to stock selection. Source: “ESG and Stock Selection,” Rochester H. Cahan, cfa. Empirical Research Partners (2015). Past performance does not guarantee future results. .

Sustainable Investing as Performance Investing | 3 Figure 2 | Summary of Individual Academic Studies Studies Analyzing ESG Ratings and Correlation with Cost of Capital or Market/Financial Performance at the Securities Level (positive, neutral, mixed, and negative) 15 15 Positive Neutral Mixed 14 Negative 12 10 9 6 3 2 1 0 Cost of Capital 1 Market-based Performance 1 Accounting-based Performance Source: Fulton, Mark and Kahn, Bruce M. and Sharples, Camilla, Sustainable Investing: Establishing Long-term Value and Performance. Note: Only includes individual academic studies looking at securities and funds (i.e. not included were literature reviews or meta-studies, which are included in other conclusions as part of the larger study cited). few SRI strategies in the study outperformed, strongly suggesting that some can find their way into outlier territory based on their unique approaches. Does focusing on the “good” in companies always have to translate to “bad” returns? The tide is turning there too. Empirical evidence is building that one does not have to accept underperformance as the inevitable fallout of investing by one’s values.

It would appear that a well-conceived strategy based on the principles of sus- tainability may actually lead to outperformance over the long run. There are a number of studies that have focused on the relationship between ESG factors and investment performance over several decades. Delineating Approaches within ESG There are three distinct approaches now evident within this growing space of responsible investment approaches: socially responsible investing, impact investing, and ESG/sustainable investing. Each carries its own meaning. SRI is probably the most well-known and established of these. Its genesis was in response to client desire to divest from companies that may contribute to problems, such as human rights abuses or carbon emission excesses. It aims to avoid social or environmental harm while still pursuing a single bottom-line profit. The World Economic Forum (WEF) describes SRI as a negative screen, or a way to avoid investments that may have some sort of negative impact on society or the environment.2 With the emergence of impact investing, there is now a predominantly private market version of sustainable investing that seeks to create positive social or environmental change with investment dollars.3 But unlike sustainable investing, financial returns are not always impact investing’s most important factor.

For instance, an impact investment may be considered successful if it shows positive social or environmental progress even if its financial returns are below market rates. Impact investing is still different from philanthropy, which may exhibit considerable alignment with ESG but without attention to financial returns. Impact investing can also limit or constrain its impact objective to a narrow target, vehicle, enterprise, or short-term timeframe.

In other words, it may aim to generate goodwill, but it is not really wired to be sustainable. Sustainable investment is the bolder cousin of SRI. It doesn’t just avoid negative factors but additionally generates positive ESG impacts alongside competitive financial returns, particularly in the public markets. The WEF frames sustainable investing as a positive screen since it actively incorporates ESG criteria into the investment decision, while still prioritizing financial returns. .

4 | Sustainable Investing as Performance Investing Figure 3 | Institutional ESG Assets Have Risen to $550 Billion ESG Institutional Equity Products* Assets Under Management, Q1 2010 through Q1 2015 Source: “ESG and Stock Selection” Rochester H. Cahan, CFA. Empirical Research Partners (2015). * Includes U.S.-domiciled assets invested in the U.S. and non-U.S.

institutional actively managed equity products. One among them is a meta-study conducted in 2012.4 It took into account more than 100 academic studies, 56 research papers, two literature reviews and four other meta-studies. One-hundred percent of the academic studies analyzed showed that companies with higher ESG ratings have a lower cost of capital of both debt and equity (see Figure 2). Of those companies, 89% exhibited a market-based outperformance and 85% accounting-based outperformance. One of the notable findings from those studies shows that, despite good to strong results, it generally took people a long time to accept the concept of ESG because of its historical association with SRI and its negative screening limitations. Sustainable Investing Gains Momentum Emphasizing positive selection criteria over negative screens is why sustainable investing is breaking away from the pack.

The approach seeks to incorporate environmental, social, and governance factors into financial analysis and investment decisions. Some of these factors include environmental stewardship, data protection, energy efficiency, workplace diversity, high transparency, and frequent reporting of the company’s progress achieving these goals. Such touchstones impact the bottom line to varying degrees, while reducing regulatory and legal risks.

For example, firms that don’t treat employees well usually exhibit high attrition rates and increased costs associated with recruiting and Adherence to ESG factors can have a direct, positive impact on the momentum and profitability of business models. training. Companies that have little regard for the environment may save costs in the short run, but can incur catastrophic expense in the long run. Adherence to ESG factors can have a direct, positive impact on the momentum and profitability of business models. Long-term financial benefits stem from high-quality companies that are better positioned to outperform by lowering operating costs, facilitating capital allocation, promoting innovation, and ensuring a good reputation. Such companies can be considered, therefore, sustainable. In recent years, sustainability as an investment factor has taken hold, generating considerable interest from both institutional and retail investors. According to a recent study, total U.S.domiciled assets under management using sustainable, socially responsible, and impact investing strategies nearly doubled from $3.74 trillion in 2012 to $6.57 trillion in 2014.5 In other words, $1 out of every $6 of assets under management in the United States was .

Sustainable Investing as Performance Investing | 5 invested in some form of responsible investment strategy. This is a good sign that implies the misconception of underperformance associated with socially responsible investing is nearing an end. It is no longer a fringe movement. Further evidence in the “Global Sustainable Investment Review 2014” found that the responsible investing market (broadly defined to include socially responsible, ESG/sustainable, and impact investing) has continued to grow in both absolute and relative terms, rising from $13.3 trillion at the outset of 2012 to $21.4 trillion at the start of 2014.6 The market has also grown from 21.5% to 30.2% of the professionally managed assets in the regions covered. Over this two-year period, the fastest-growing region of demand has been within the United States, followed by Canada and Europe, where adoption already is very high. Hand in glove with the growing sustainable investing market is the approach’s increasing credibility as a mainstream investment theme.

For example, the Rockefeller Brothers Fund’s decision to align its endowment’s environmental and investing goals represents an iconic institutional level move that opened a lot of eyes, and could help advance the cause of “fossil-free investing.” By example, it has helped to boost divestment and investor interest in limiting or removing the worst carbon-emitting industries from portfolios. As an industry, we may be able to learn much from pension funds, sovereign wealth vehicles, endowments, and other institutions that have been experimenting with ways to incorporate ESG factors into their investment processes while ... sustainability as an investment factor has taken hold, generating considerable interest from both institutional and retail investors. balancing long-term risks against short-term share price movements (See Figure 3). On the individual level, too, sustainable investing is in demand because it offers clients a way to align pocketbooks with ethics.

According to Morningstar, about 84% of Millennials (those born between 1980 and 2002) express specific desire for sustainable investing. As they enter their 40s and hit their financial planning stride, it can only spell ever-higher demand for investing that combines meaningful impact alongside returns. Whether at the institutional or the individual level, sustainable investing is increasingly tantamount to proactively promoting environmental stewardship, encouraging good corporate practices, or supporting workplace diversity among individual holdings. Sustainable Investing: Meaningful & Measurable Sustainable investing strategies pay attention to a few specific areas as they incorporate ESG attributes into their selection process: is the company a good corporate citizen (i.e., does it show a commitment to things like workplace diversity, environmentally friendly practices, and investing in the local economy)? Does it live up to the disclosure and governance guidelines set forth by shareholders? In many regards, value investors, who are perhaps the most well-equipped and experienced to embrace sustainable investing principles, have been asking these questions all along. After all, value disciplines and sustainable investing are all about patience, intensive research, and finding individual high-quality companies with longterm growth potential. In sustainable investing, the ideal business models would have to demonstrate measurable value to both the company and its stakeholders (customers, employees, government, and communities).

Stakeholders can have a direct effect on a company’s profits and progress, so how they are affected is a key component in the evaluation of a company’s ESG impact. Many different outcomes may be measured to evaluate a company’s progress with ESG: environmental performance, number of women in leadership roles, history of regulatory and legal actions against the company, capital allocation, etc. The Opportunity Ahead Responsible investing has traveled a long way from the initial stages of simply applying negative screens. The use of ESG factors to enhance a portfolio with positive selection criteria is here to stay. Despite growing interest and awareness, alignment with positive impact factors should not be viewed as .

6 | Sustainable Investing as Performance Investing a panacea, but rather as one investment approach among many. And, like any discipline, it should be considered on a strategy-by-strategy basis. Finally, the sustainable investing approach is not about passing moral judgment on companies, but rather reaching for a better way to analyze and project long-term performance of their business models. Companies that incorporate ESG into their operations tend to be well positioned to outperform, as they can work more productively with their stakeholders, lower their operating costs over the long run, and facilitate better capital allocation, greater innovation, and enhanced reputations. With these goals, sustainable business models and practices are poised to generate profits over the long-term and, ultimately, higher share prices.

n ... the sustainable investing approach is not about passing moral judgment on companies, but rather reaching for a better way to analyze and project long-term performance of their business models. 1. “ESG and Stock Selection” Rochester H. Cahan, cfa. Empirical Research Partners (2015), http://www.empirical-research.com/esg-and-stock-selection/ 2. “From the Margins to the Mainstream: Assessment of the Impact Investment Sector and Opportunities to Engage Mainstream Investors,” World Economic Forum Investors Industries and Deloitte Touche Tohmatsu (2013), http://www3.weforum.org/docs/WEF_II_FromMarginsMainstream_Report_2013.pdf com/abstract=2222740 orhttp://dx.doi.org/10.2139/ ssrn.2222740 5. Investment Company Institute. 6. “Global Sustainable Investment Review 2014,” Global Sustainable Investment Alliance (2015): 3, accessed on September 6, 2015, http://www.gsi-alliance.org/ wp-content/uploads/2015/02/GSIA_Review_download.pdf 3. “Introducing the Impact Investing Benchmark,” Cambridge Associates and the Global Impact Investing Network (2015), accessed on September 5, 2015, http://www.thegiin.org/assets/documents/pub/Introducing_the_Impact_Investing_Benchmark.pdf 4. Fulton, Mark and Kahn, Bruce M.

and Sharples, Camilla, “Sustainable Investing: Establishing Long-term Value and Performance” (June 12, 2012). http://ssrn. Sustainable Investing at Thornburg As a successful value investor, Thornburg seamlessly embraced sustainable investing to create an ESG-tilted mandate for retail and institutional clients. After all, sustainable investing—much like value strategies—requires a long-term, patient, and research-intensive mindset to succeed.

In searching the investment universe to support our ESG mandate, we typically focus on components that affect an investment’s sustainability attributes, like climate change, social conflicts, availability of natural resources, etc. As we see it, sustainable investing practices span all industries, but some attributes are industry specific. For example, carbon emissions are not necessarily a material issue for an IT firm, but they are for a utility company. In some business models, we look for positive “sustainable investing momentum,” which means the company may not be perfect on ESG currently, but it is demonstrably taking ESG issues seriously by actively improving on them. Alternatively, the ESG classification of a company would be low if the company has a poor sustainability rating relative to its industry peers or is dismissive of sustainable investing values.

Companies not performing up to our ESG standards are typically called upon, so that we can directly engage with company management to find answers. Thornburg has been managing separate accounts under sustainable investing standards for more than 10 years. Portfolio Manager Rolf Kelly, cfa, has been the primary steward on these accounts since 2010. “At first, I had my doubts, given wide misconception about sustainable investing’s effectiveness. We’re trained early on that if you limit the investible universe, it makes it harder to find relative value and outperform,” Kelly says.

“But this isn’t always true. In fact, narrowing your focus through ESG enables you to select from a smaller universe of better-run, more sustainable companies. Done the right way, we found that this approach to sustainable investing can indeed outperform.” .

. Important Information The views expressed by the portfolio manager reflect his professional opinions and should not be considered buy or sell recommendations. These views are subject to change. Investments carry risks, including possible loss of principal. Additional risks may be associated with investments outside the United States, especially in emerging markets, including currency fluctuations, illiquidity, volatility, and political and economic risks. Investments in small- and mid-capitalization companies may increase the risk of greater price fluctuations. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses. Past performance does not guarantee future results. Before investing, carefully consider the Fund’s investment goals, risks, charges, and expenses.

For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit thornburg.com. Read them carefully before investing. 5/23/16 Thornburg Securities Corporation, Distributor | 2300 North Ridgetop Road | Santa Fe, New Mexico 87506 | 877.215.1330 TH3442 .