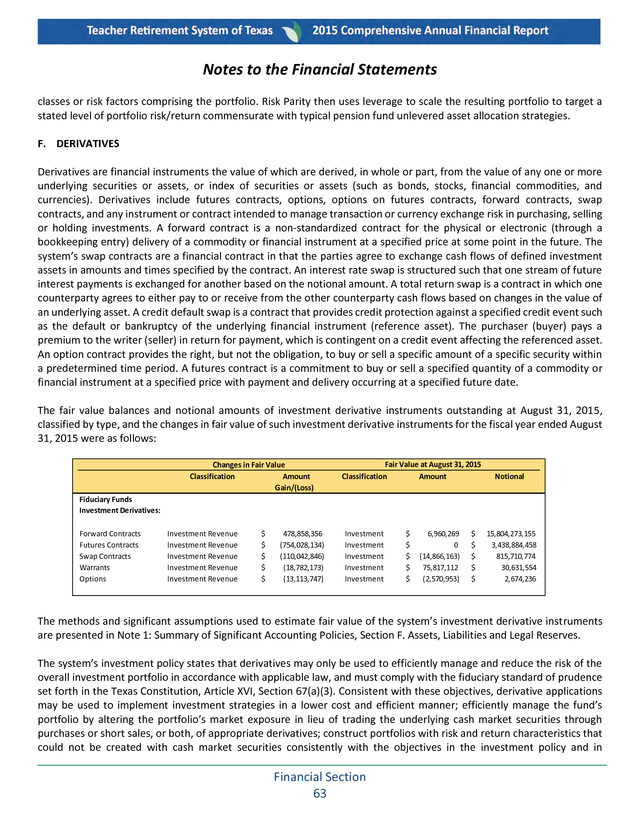

Description

2015

Teacher Retirement System of Texas

Comprehensive

Annual

Financial

Report

A Component Unit of the State of Texas

Fiscal Year Ended August 31, 2015

NN

WI

1st

E

PLAC

ER

TRS o

rher

Supe her

Teac

Art

st

onte

C

. TRS Mission Statement

The mission of the Teacher Retirement System of Texas is:

Improving the retirement security of Texas educators

by prudently investing and managing trust assets

and delivering benefits that make a positive difference

in members’ lives.

R

WINNE

2nd

PLACE

TRS

Superh

ero

Teache

r

Art

Contes

t

This year’s Comprehensive Annual Financial Report (CAFR) features some amazing artwork submitted by K-5 students from across Texas. More

than 3,500 students participated in TRS’ “My Superhero Teacher Art Contest.” Top entries were then placed on our Facebook page for voting. The

art reflects how the students view their teachers as superheroes, and we’re proud to share the contest winners’ artwork with you in this

publication.

First place was awarded to a 3rd grader from Clark Elementary in Laredo, whose artwork appears on our cover. Second place went to a 4th grader from Roosevelt Elementary in San Antonio, whose artwork is on the inside cover, and 3rd place went to a 3rd grader from Live Oak Learning

Center in Rockport, whose artwork is on the document’s title page.

A 4th grader from Ramirez Elementary in Lubbock, received an Honorable Mention. That artwork is on the back of the CAFR. Top ten artwork from Facebook is featured throughout the CAFR; however, we feel that every participant is a winner. We plan to recognize them and their teachers in other publications and on our website. .

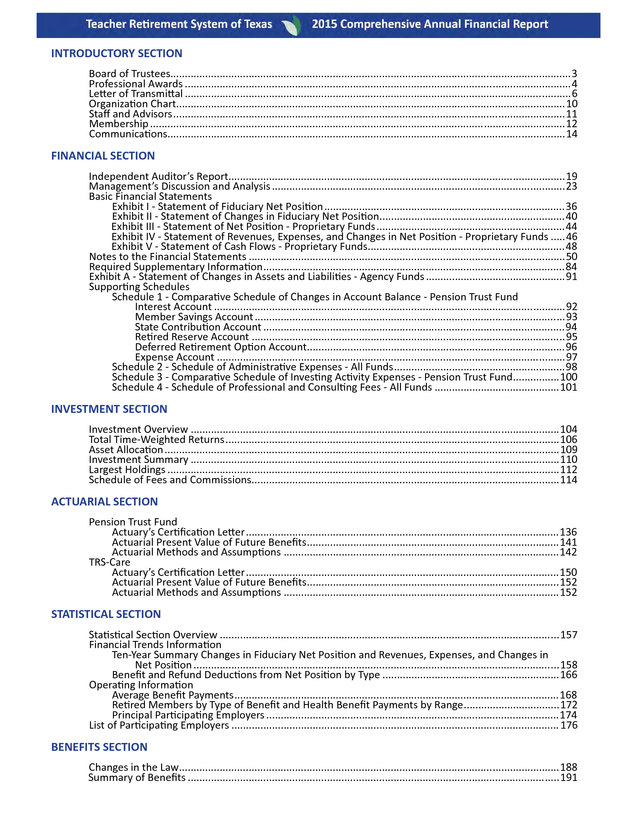

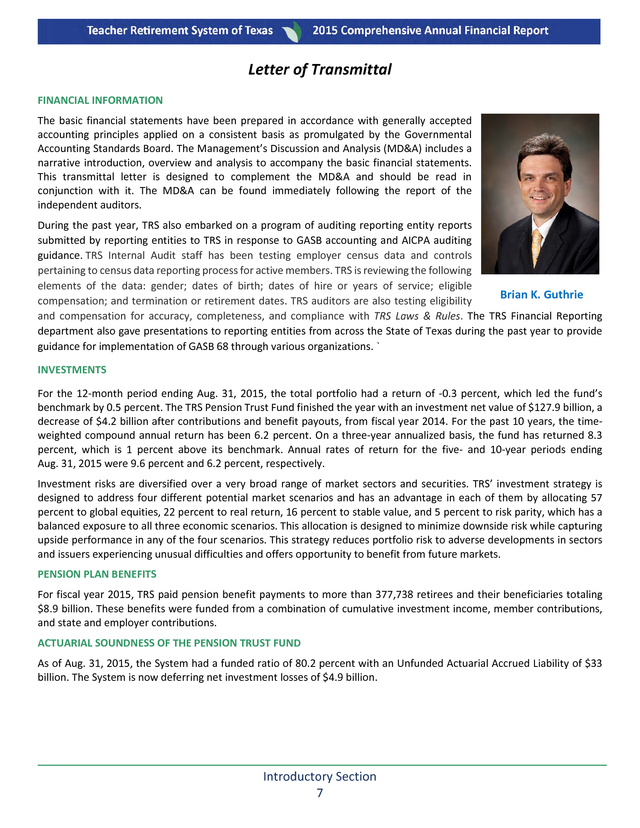

Teacher Retirement System of Texas COMPREHENSIVE ANNUAL FINANCIAL REPORT A Component Unit of the State of Texas Fiscal Year Ended August 31, 2015 Prepared by Teacher Retirement System of Texas 1000 Red River Street Austin, Texas 78701-2698 (512) 542-6400 1-800-223-8778 R WINNE 3rd PLACE TRS Superh ero Teache r Art Contes t Brian K. Guthrie, Executive Director www.trs.texas.gov . INTRODUCTORY SECTION Board of Trustees..........................................................................................................................................3 Professional Awards .....................................................................................................................................4 Le er of Transmi al .....................................................................................................................................6 Organiza on Chart......................................................................................................................................10 Staff and Advisors .......................................................................................................................................11 Membership ...............................................................................................................................................12 Communica ons.........................................................................................................................................14 FINANCIAL SECTION Independent Auditor’s Report....................................................................................................................19 Management’s Discussion and Analysis .....................................................................................................23 Basic Financial Statements Exhibit I - Statement of Fiduciary Net Posi on ...................................................................................36 Exhibit II - Statement of Changes in Fiduciary Net Posi on................................................................40 Exhibit III - Statement of Net Posi on - Proprietary Funds .................................................................44 Exhibit IV - Statement of Revenues, Expenses, and Changes in Net Posi on - Proprietary Funds .....46 Exhibit V - Statement of Cash Flows - Proprietary Funds....................................................................48 Notes to the Financial Statements .............................................................................................................50 Required Supplementary Informa on ........................................................................................................84 Exhibit A - Statement of Changes in Assets and Liabili es - Agency Funds ................................................91 Suppor ng Schedules Schedule 1 - Compara ve Schedule of Changes in Account Balance - Pension Trust Fund Interest Account .........................................................................................................................92 Member Savings Account ...........................................................................................................93 State Contribu on Account ........................................................................................................94 Re red Reserve Account ............................................................................................................95 Deferred Re rement Op on Account.........................................................................................96 Expense Account ........................................................................................................................97 Schedule 2 - Schedule of Administra ve Expenses - All Funds ...........................................................98 Schedule 3 - Compara ve Schedule of Inves ng Ac vity Expenses - Pension Trust Fund................100 Schedule 4 - Schedule of Professional and Consul ng Fees - All Funds ...........................................101 INVESTMENT SECTION Investment Overview ...............................................................................................................................104 Total Time-Weighted Returns ...................................................................................................................106 Asset Alloca on ........................................................................................................................................109 Investment Summary ...............................................................................................................................110 Largest Holdings .......................................................................................................................................112 Schedule of Fees and Commissions..........................................................................................................114 ACTUARIAL SECTION Pension Trust Fund Actuary’s Cer ï¬ca on Le er ............................................................................................................136 Actuarial Present Value of Future Beneï¬ts.......................................................................................141 Actuarial Methods and Assump ons ...............................................................................................142 TRS-Care Actuary’s Cer ï¬ca on Le er ............................................................................................................150 Actuarial Present Value of Future Beneï¬ts.......................................................................................152 Actuarial Methods and Assump ons ...............................................................................................152 STATISTICAL SECTION Sta s cal Sec on Overview .....................................................................................................................157 Financial Trends Informa on Ten-Year Summary Changes in Fiduciary Net Posi on and Revenues, Expenses, and Changes in Net Posi on ..............................................................................................................................158 Beneï¬t and Refund Deduc ons from Net Posi on by Type .............................................................166 Opera ng Informa on Average Beneï¬t Payments ................................................................................................................168 Re red Members by Type of Beneï¬t and Health Beneï¬t Payments by Range .................................172 Principal Par cipa ng Employers .....................................................................................................174 List of Par cipa ng Employers ................................................................................................................. 176 BENEFITS SECTION Changes in the Law...................................................................................................................................188 Summary of Beneï¬ts ................................................................................................................................191 . INTRODUCTORY SECTION . This page is intentionally left blank. Introductory Section 2 . Board of Trustees R. David Kelly, Chair Nanette Sissney Vice Chair Managing Partner Straight Line Realty Partners, Plano Direct appointment of the governor Term expires 2017 School Counselor Whitesboro ISD, Whitesboro Active public education position Term expires 2015 Todd Barth Karen Charleston President Bowers Properties Inc., Houston Direct appointment of the governor Term expires 2015 Space Management Assistant Prairie View A&M University, Houston Higher education position Term expires 2017 Joe Colonnetta David Corpus Private Investor Dallas Direct appointment of the governor Term expires 2019 Senior Vice President CommunityBank of Texas, Humble Position nominated by the State Board of Education Term expires 2019 Christopher Moss Vice President The Advanced Financial Group, Lufkin Position nominated by the State Board of Education Term expires 2015 Anita Palmer Former Texas Public School Teacher, Administrator and University Adjunct Professor Jacksboro Retiree position Term expires 2017 Dolores Ramirez Teacher San Benito CISD, San Benito Active public education position Term expires 2019 For information on the board election process, please refer to Note 1 in the Financial Section. Introductory Section 3 . Professional Awards Government Finance Officers Association Certificate of Achievement for Excellence in Financial Reporting Presented to Teacher Retirement System of Texas For its Comprehensive Annual Financial Report for the Fiscal Year Ended August 31, 2014 Executive Director/CEO Introductory Section 4 . Professional Awards PC PC Public Pension Coordinating Council Recognition Award for Administration 2014 Presented to Teacher Retirement System of Texas In recognition of meeting professional standards for plan administration as set forth in the Public Pension Standards. Presented by the Public Pension Coordinating Council, a confederation of National Association of State Retirement Administrators (NASRA) National Conference on Public Employee Retirement Systems (NCPERS) National Council on Teacher Retirement (NCTR) Alan H. Winkle Program Administrator Introductory Section 5 . Letter of Transmittal November 18, 2015 The Honorable Greg Abbott The Honorable Dan Patrick The Honorable Joe Straus The Board of Trustees and Members   of the Teacher Retirement System Dear Governor Abbott, Lieutenant Governor Patrick, Speaker Straus, TRS Board of Trustees, and Members of the Teacher Retirement System: On behalf of the board of trustees, I am pleased to present the Comprehensive Annual Financial Report (CAFR) of the Teacher Retirement System of Texas (TRS or System) for the fiscal year ended August 31, 2015, the System’s 78th year of operation. During the past fiscal year, the System experienced modest growth as membership grew to approximately 1,459,243 participants. The pension trust fund saw slightly negative returns in the past year, consistent with a downturn in world markets. The fund ended the 2015 fiscal year with a net position of $128.5 billion compared to $132.8 billion at the close of the 2014 fiscal year.

However, contribution increases and benefit changes that were approved by the 83rd Texas Legislature, are continuing to enable TRS to provide secure benefits for current and future retirees. MANAGEMENT RESPONSIBILITY This report consists of management’s representations concerning TRS finances. Management assumes full responsibility for the completeness and reliability of all information presented in this report. To provide a reasonable basis for making these representations, management has established a comprehensive internal control framework that is designed both to protect the assets from loss, theft, or misuse and to compile sufficient, reliable information for the preparation of TRS financial statements in conformity with generally accepted accounting principles.

The cost of controls should not exceed the benefits to be derived as the objective of the internal control framework is to provide reasonable rather than absolute assurance that the financial statements will be free from material misstatement. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects. CERTIFICATE OF ACHIEVEMENT FOR EXCELLENCE IN FINANCIAL REPORTING The Government Finance Officers Association of the United States and Canada (GFOA) awarded TRS the Certificate of Achievement for Excellence in Financial Reporting for its Comprehensive Annual Financial Report for the previous fiscal year. To be awarded the certificate, a report must meet or exceed program standards and must satisfy both generally accepted accounting principles and applicable legal requirements.

TRS has received a Certificate of Achievement for the last 25 years. We believe that the current report continues to meet program requirements, and it is being submitted to the GFOA for consideration again this year. Introductory Section 6 . Letter of Transmittal FINANCIAL INFORMATION The basic financial statements have been prepared in accordance with generally accepted accounting principles applied on a consistent basis as promulgated by the Governmental Accounting Standards Board. The Management’s Discussion and Analysis (MD&A) includes a narrative introduction, overview and analysis to accompany the basic financial statements. This transmittal letter is designed to complement the MD&A and should be read in conjunction with it. The MD&A can be found immediately following the report of the independent auditors. During the past year, TRS also embarked on a program of auditing reporting entity reports submitted by reporting entities to TRS in response to GASB accounting and AICPA auditing guidance. TRS Internal Audit staff has been testing employer census data and controls pertaining to census data reporting process for active members.

TRS is reviewing the following elements of the data: gender; dates of birth; dates of hire or years of service; eligible Brian K. Guthrie compensation; and termination or retirement dates. TRS auditors are also testing eligibility and compensation for accuracy, completeness, and compliance with TRS Laws & Rules.

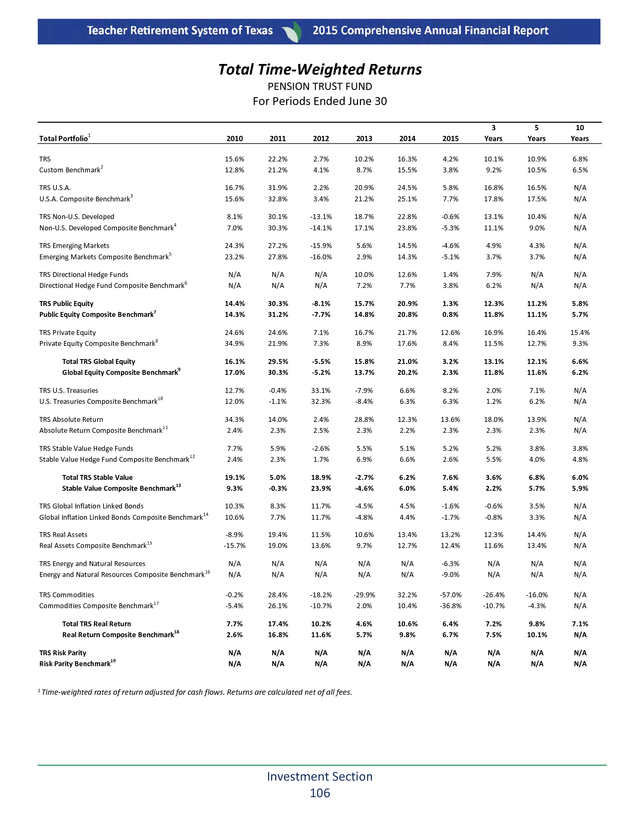

The TRS Financial Reporting department also gave presentations to reporting entities from across the State of Texas during the past year to provide guidance for implementation of GASB 68 through various organizations. ` INVESTMENTS For the 12-month period ending Aug. 31, 2015, the total portfolio had a return of -0.3 percent, which led the fund’s benchmark by 0.5 percent.

The TRS Pension Trust Fund finished the year with an investment net value of $127.9 billion, a decrease of $4.2 billion after contributions and benefit payouts, from fiscal year 2014. For the past 10 years, the timeweighted compound annual return has been 6.2 percent. On a three-year annualized basis, the fund has returned 8.3 percent, which is 1 percent above its benchmark.

Annual rates of return for the five- and 10-year periods ending Aug. 31, 2015 were 9.6 percent and 6.2 percent, respectively. Investment risks are diversified over a very broad range of market sectors and securities. TRS’ investment strategy is designed to address four different potential market scenarios and has an advantage in each of them by allocating 57 percent to global equities, 22 percent to real return, 16 percent to stable value, and 5 percent to risk parity, which has a balanced exposure to all three economic scenarios.

This allocation is designed to minimize downside risk while capturing upside performance in any of the four scenarios. This strategy reduces portfolio risk to adverse developments in sectors and issuers experiencing unusual difficulties and offers opportunity to benefit from future markets. PENSION PLAN BENEFITS For fiscal year 2015, TRS paid pension benefit payments to more than 377,738 retirees and their beneficiaries totaling $8.9 billion. These benefits were funded from a combination of cumulative investment income, member contributions, and state and employer contributions. ACTUARIAL SOUNDNESS OF THE PENSION TRUST FUND As of Aug.

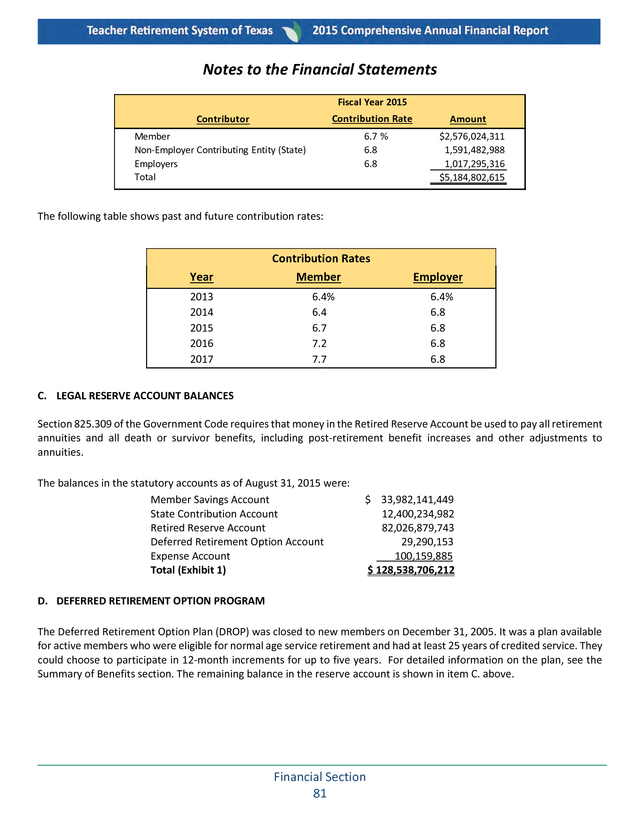

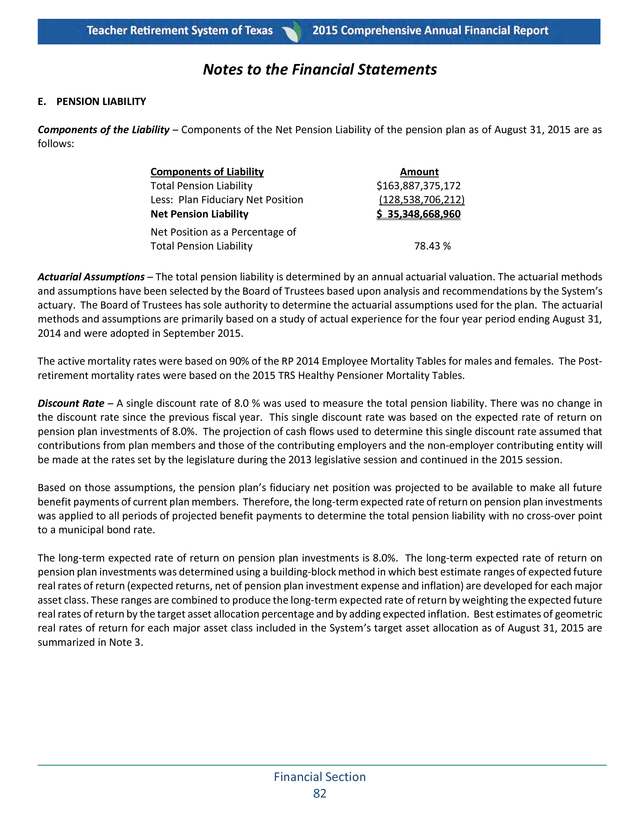

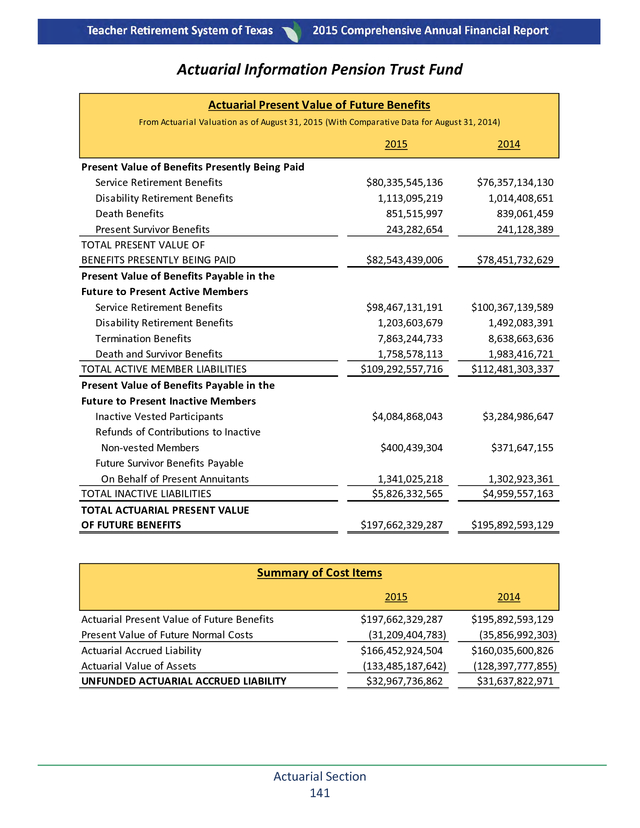

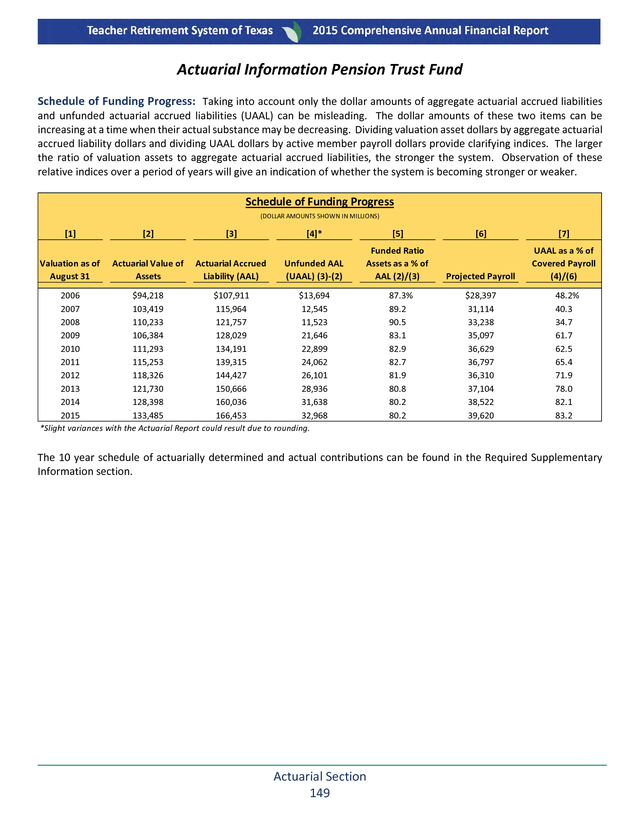

31, 2015, the System had a funded ratio of 80.2 percent with an Unfunded Actuarial Accrued Liability of $33 billion. The System is now deferring net investment losses of $4.9 billion. Introductory Section 7 . Letter of Transmittal The period of time necessary to amortize the unfunded liability has increased from 29.8 years to 33.3 years. Given that current contributions cannot amortize the unfunded liability in less than 31 years, the System does not meet the definition for actuarial soundness. The increase in the period of time necessary to amortize the unfunded liability was anticipated and is partially due to the phasing in of contribution rate increases adopted by the 83rd Texas Legislature. In 2013, the Legislature adopted Senate Bill 1458 that provided a stair-step increase in the member contribution rate from 6.4 percent in FY 2014 to 7.7 percent in FY 2017.

The member contribution rate for FY 2015 was 6.7 percent. While the increased contribution rates are an actuarial gain to the System, the phased-in approach has partially contributed to the funding period and unfunded liability growth. The state contribution rate for FY 2015 was 6.8 percent, and in FY 2015 school districts that do not participate in Social Security began paying a 1.5 percent contribution rate to the System. Also impacting the growth of the unfunded liability are lower than expected investment returns for FY 2015 and the adoption of a new mortality assumption based on the increased life expectancy of System members.

Adoption of the new mortality assumption was part of a larger study of System experience for the last five years. Texas Government Code Section 825.206 requires TRS to conduct an actuarial experience study at least once every five years to examine the mortality, service, and compensation experience of the members and beneficiaries of the retirement system. The TRS Board is then required to review and adopt the System’s actuarial assumptions in light of the relevant experience.

In September 2015, TRS concluded the experience study for the four-year period ending Aug. 31, 2014 and adopted a new assumption set. In addition to updating the mortality assumption, the board kept the assumed investment return rate at 8 percent and lowered the assumptions for inflation, real wage growth, and payroll growth.

The new assumption set more accurately portrays the actuarial condition of the System given that it incorporates System experience for FY 2011 to FY 2014. It is estimated that the unfunded liability and the funding period will both continue to increase over the next few years before beginning to once again decline. However, the funding period is anticipated to remain a finite number until the unfunded liability is amortized and the pension fund is fully funded. Several important legislative changes were enacted by the 84th Texas Legislature during the past year. Some of the bills that most directly impacted TRS members included House Bill 2, a supplemental funding bill, which provided biennial funding for TRS-Care in the amount of roughly $768 million.

House Bill 2168 stipulated that monthly annuity payments be paid on the last working day of the month for which the payment accrues. House Bill 2974 contained a variety of selected omnibus provisions covering several important areas. It also created a joint interim committee to study TRS-Care and TRSActiveCare.

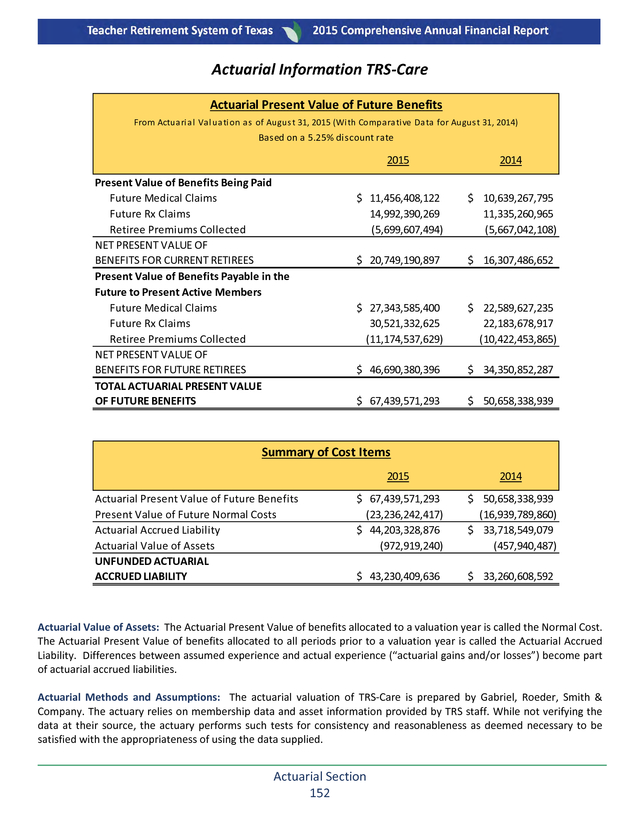

TRS-related legislation is covered in more detail in the “Changes in the Law” section of this report. RETIREE HEALTH BENEFITS PROGRAM TRS administers TRS-Care, a health benefits program for retirees that was established in 1985. TRS-Care is the source of health benefits coverage, which almost all retired public school employees rely upon. Funding is provided by premium payments from retiree participants and contributions from the state, school districts and active employees.

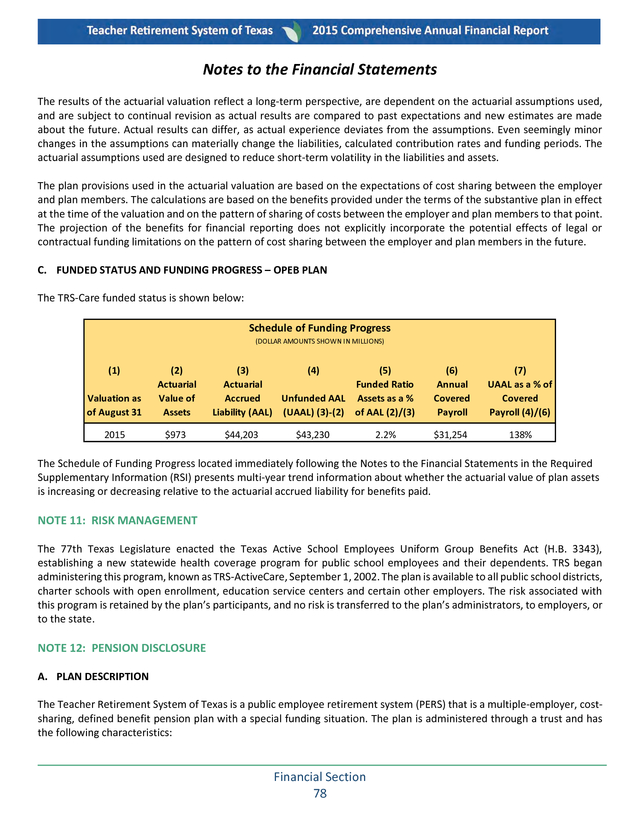

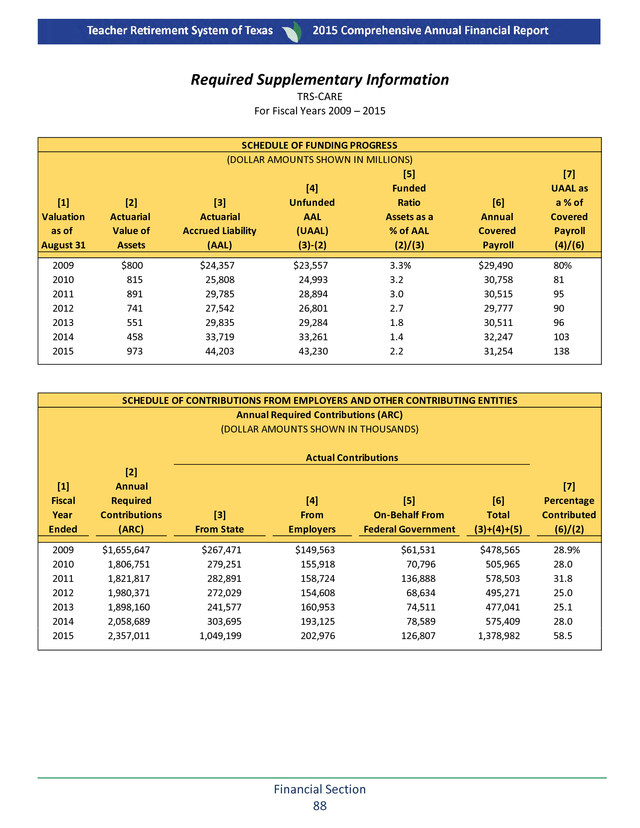

TRS-Care also receives additional revenue from the Medicare Part D prescription drug program. An actuarial valuation for TRS-Care was conducted as of Aug. 31, 2015. The valuation results indicate that TRS-Care has an Unfunded Actuarial Accrued Liability of $44.2 billion.

The plan was 2.2 percent funded as of the end of the Fiscal Year 2015. More detailed information about the valuation results is included in the Notes to the Financial Statements and the Required Supplementary Information. The current funding formula of 1 percent of public school payroll from the State, .55 percent from the district and .65 percent from the member is insufficient to sustain the, TRS-Care Program. The state legislature infused $768 million into the program as a measure intended to ensure solvency of the TRS-Care fund through the FY 16-17 Biennium.

The 84th Legislature also created a joint interim committee to study TRS-Care and also TRS-ActiveCare. TRS will be supporting the work of the committee to address the ongoing solvency and affordability of the TRS-Care and TRS-ActiveCare programs. Introductory Section 8 . Letter of Transmittal ACTIVE MEMBER HEALTH BENEFITS PROGRAM TRS-ActiveCare, initiated in 2002, is a self-funded health benefits program that offers options ranging from catastrophic coverage with reduced premiums to a comprehensive plan at higher premiums. TRS-ActiveCare covers members currently employed by public education employers that participate in the plan. TRS establishes premiums to pay for the cost of the program. The TRS Board of Trustees approved an additional increase in premiums for fiscal year 2014 and froze TRSActiveCare 3 for new enrollment.

As noted above, TRS also updated an earlier study submitted to the 83rd Legislature of options for improving the sustainability of TRS-Care and expanded the study to also include options to improve the affordability of TRS-ActiveCare. ORGANIZATIONAL CHANGE During the past year, TRS named three new chief officers. Chris Cutler became TRS’ new chief information officer, Barbie Pearson was named chief benefit officer, and Katrina Daniel joined TRS as the agency’s new chief health care officer. Over the past year, we have also made a handful of other organizational changes to focus on our key challenges moving forward: health care fund solvency, pension trust fund sustainability, long-term investment returns, and replacing legacy technology systems.

These changes are reflected in the updated organizational chart on the following page. During the past year, TRS increased its focus on the agency’s core values: Customer Satisfaction; Collaboration and Teamwork; Accountability; Respect; Ethics; Excellence; and Employee Fulfillment. These values continue to be incorporated throughout TRS’ work environment, including in performance evaluations, employee recognition programs and communications. They also continuously focus our efforts on how to best serve our members. Thanks to the hard work and dedication of its employees, TRS was named a “Top Workplace” by the Austin AmericanStatesman for the fourth year in a row. ACKNOWLEDGMENTS We wish to express our appreciation for the support of the Governor’s, Lieutenant Governor’s, and Speaker’s Offices, as well as members of the legislature, in maintaining a strong retirement system, which provides valuable benefits for public education employees and retirees. We are grateful for the dedicated service of all of our trustees.

Trustee willingness to accept the substantial responsibilities of directing system administration is a great service to the state and to the members served by TRS. TRS trustees and staff are keenly focused on prudent pension trust fund portfolio management and efficient, serviceoriented delivery of valuable retirement and related benefits for public education employees and retirees. We are pleased to report on operational results for the year and to acknowledge the substantial support of state leadership, trustees, members, interested associations, and TRS staff. Respectfully submitted, Brian K. Guthrie Executive Director Introductory Section 9 .

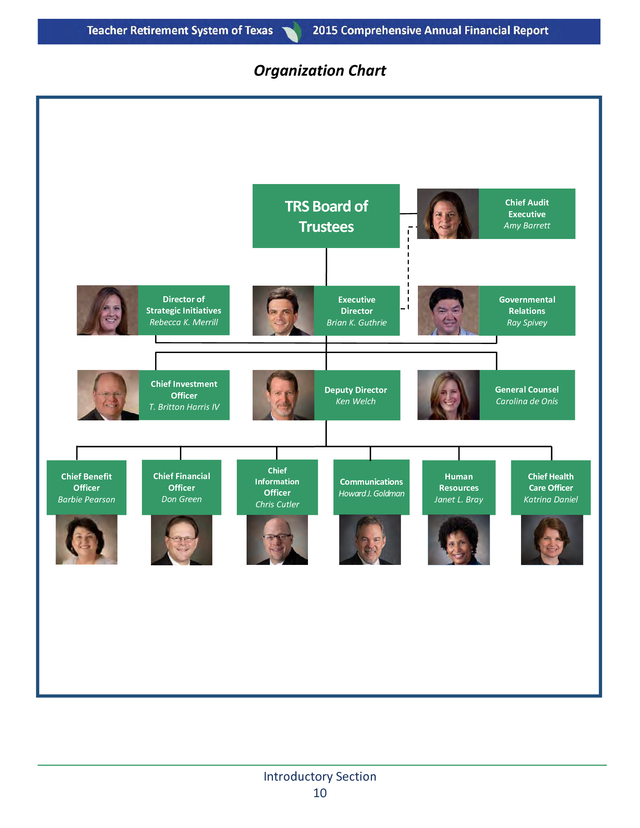

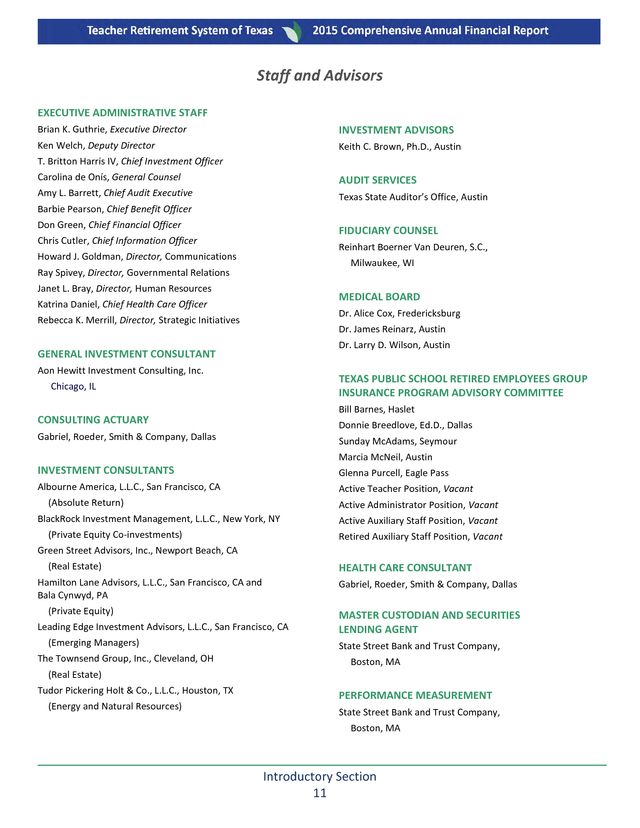

Organization Chart Chief Audit Executive Amy Barrett TRS Board of Trustees Director of Strategic Initiatives Rebecca K. Merrill Governmental Relations Ray Spivey Chief Investment Officer T. Britton Harris IV Chief Benefit Officer Barbie Pearson Executive Director Brian K. Guthrie Deputy Director Ken Welch General Counsel Carolina de Onís Chief Financial Officer Don Green Chief Information Officer Chris Cutler Communications Howard J. Goldman Introductory Section 10 Human Resources Janet L. Bray Chief Health Care Officer Katrina Daniel . Staff and Advisors EXECUTIVE ADMINISTRATIVE STAFF Brian K. Guthrie, Executive Director INVESTMENT ADVISORS Ken Welch, Deputy Director Keith C. Brown, Ph.D., Austin T. Britton Harris IV, Chief Investment Officer Carolina de Onís, General Counsel AUDIT SERVICES Amy L.

Barrett, Chief Audit Executive Texas State Auditor’s Office, Austin Barbie Pearson, Chief Benefit Officer Don Green, Chief Financial Officer FIDUCIARY COUNSEL Chris Cutler, Chief Information Officer Reinhart Boerner Van Deuren, S.C., Howard J. Goldman, Director, Communications Milwaukee, WI Ray Spivey, Director, Governmental Relations Janet L. Bray, Director, Human Resources MEDICAL BOARD Katrina Daniel, Chief Health Care Officer Dr.

Alice Cox, Fredericksburg Rebecca K. Merrill, Director, Strategic Initiatives Dr. James Reinarz, Austin Dr.

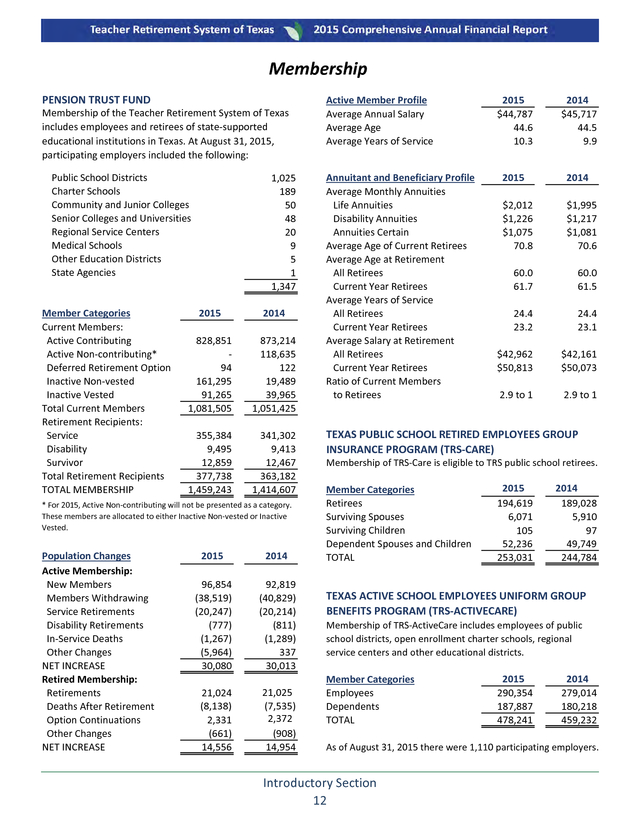

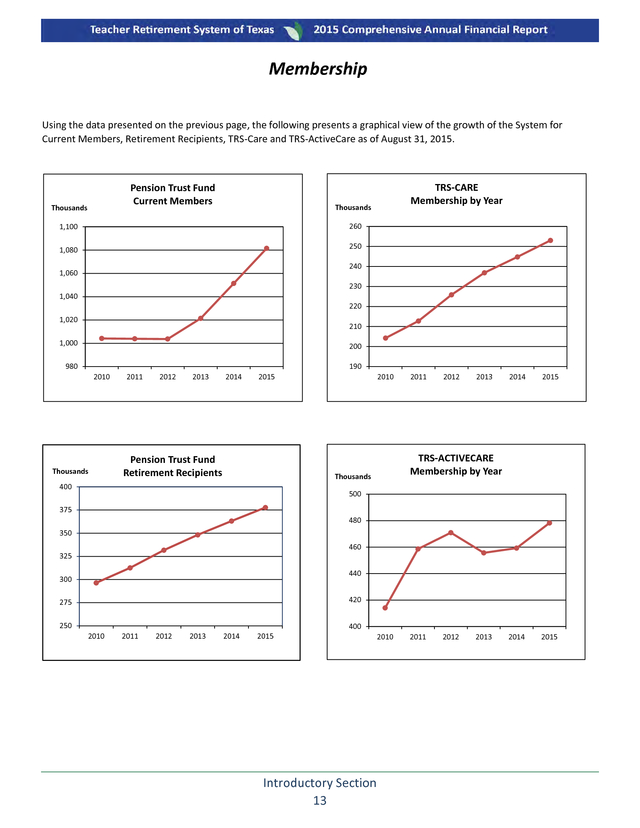

Larry D. Wilson, Austin GENERAL INVESTMENT CONSULTANT Aon Hewitt Investment Consulting, Inc. TEXAS PUBLIC SCHOOL RETIRED EMPLOYEES GROUP INSURANCE PROGRAM ADVISORY COMMITTEE Chicago, IL Bill Barnes, Haslet CONSULTING ACTUARY Donnie Breedlove, Ed.D., Dallas Gabriel, Roeder, Smith & Company, Dallas Sunday McAdams, Seymour Marcia McNeil, Austin INVESTMENT CONSULTANTS Glenna Purcell, Eagle Pass Albourne America, L.L.C., San Francisco, CA Active Teacher Position, Vacant (Absolute Return) Active Administrator Position, Vacant BlackRock Investment Management, L.L.C., New York, NY (Private Equity Co-investments) Active Auxiliary Staff Position, Vacant Retired Auxiliary Staff Position, Vacant Green Street Advisors, Inc., Newport Beach, CA (Real Estate) HEALTH CARE CONSULTANT Hamilton Lane Advisors, L.L.C., San Francisco, CA and Bala Cynwyd, PA Gabriel, Roeder, Smith & Company, Dallas (Private Equity) Leading Edge Investment Advisors, L.L.C., San Francisco, CA (Emerging Managers) The Townsend Group, Inc., Cleveland, OH (Real Estate) Tudor Pickering Holt & Co., L.L.C., Houston, TX (Energy and Natural Resources) MASTER CUSTODIAN AND SECURITIES LENDING AGENT State Street Bank and Trust Company, Boston, MA PERFORMANCE MEASUREMENT State Street Bank and Trust Company, Boston, MA Introductory Section 11 . Membership PENSION TRUST FUND Membership of the Teacher Retirement System of Texas includes employees and retirees of state-supported educational institutions in Texas. At August 31, 2015, participating employers included the following: Public School Districts Charter Schools Community and Junior Colleges Senior Colleges and Universities Regional Service Centers Medical Schools Other Education Districts State Agencies Member Categories Current Members: Active Contributing Active Non-contributing* Deferred Retirement Option Inactive Non-vested Inactive Vested Total Current Members Retirement Recipients: Service Disability Survivor Total Retirement Recipients TOTAL MEMBERSHIP 1,025 189 50 48 20 9 5 1 1,347 2015 2014 828,851 94 161,295 91,265 1,081,505 873,214 118,635 122 19,489 39,965 1,051,425 355,384 9,495 12,859 377,738 1,459,243 341,302 9,413 12,467 363,182 1,414,607 * For 2015, Active Non-contributing will not be presented as a category. These members are allocated to either Inactive Non-vested or Inactive Vested. Population Changes Active Membership: New Members Members Withdrawing Service Retirements Disability Retirements In-Service Deaths Other Changes NET INCREASE Retired Membership: Retirements Deaths After Retirement Option Continuations Other Changes NET INCREASE 2015 2014 96,854 (38,519) (20,247) (777) (1,267) (5,964) 30,080 92,819 (40,829) (20,214) (811) (1,289) 337 30,013 21,024 (8,138) 2,331 (661) 14,556 21,025 (7,535) 2,372 (908) 14,954 Active Member Profile Average Annual Salary Average Age Average Years of Service Annuitant and Beneficiary Profile Average Monthly Annuities Life Annuities Disability Annuities Annuities Certain Average Age of Current Retirees Average Age at Retirement All Retirees Current Year Retirees Average Years of Service All Retirees Current Year Retirees Average Salary at Retirement All Retirees Current Year Retirees Ratio of Current Members to Retirees 2015 $44,787 44.6 10.3 2014 $45,717 44.5 9.9 2015 2014 $2,012 $1,226 $1,075 70.8 $1,995 $1,217 $1,081 70.6 60.0 61.7 60.0 61.5 24.4 23.2 24.4 23.1 $42,962 $50,813 $42,161 $50,073 2.9 to 1 2.9 to 1 TEXAS PUBLIC SCHOOL RETIRED EMPLOYEES GROUP INSURANCE PROGRAM (TRS-CARE) Membership of TRS-Care is eligible to TRS public school retirees. Member Categories Retirees Surviving Spouses Surviving Children Dependent Spouses and Children TOTAL 2015 194,619 6,071 105 52,236 253,031 2014 189,028 5,910 97 49,749 244,784 TEXAS ACTIVE SCHOOL EMPLOYEES UNIFORM GROUP BENEFITS PROGRAM (TRS-ACTIVECARE) Membership of TRS-ActiveCare includes employees of public school districts, open enrollment charter schools, regional service centers and other educational districts. Member Categories Employees Dependents TOTAL 2015 290,354 187,887 478,241 2014 279,014 180,218 459,232 As of August 31, 2015 there were 1,110 participating employers. Introductory Section 12 . Membership Using the data presented on the previous page, the following presents a graphical view of the growth of the System for Current Members, Retirement Recipients, TRS-Care and TRS-ActiveCare as of August 31, 2015. Pension Trust Fund Current Members Thousands TRS-CARE Membership by Year Thousands 1,100 260 1,080 250 240 1,060 230 1,040 220 1,020 210 1,000 200 190 980 2010 Thousands 2011 2012 2013 2014 2010 2015 Pension Trust Fund Retirement Recipients 2012 2013 2014 2015 2014 2015 TRS-ACTIVECARE Membership by Year Thousands 400 2011 500 375 480 350 460 325 440 300 420 275 250 2010 2011 2012 2013 2014 2015 400 Introductory Section 13 2010 2011 2012 2013 . Communications During fiscal year 2015, TRS communicated with members, retirees, participating employers, and the general public over the telephone as well as through group presentations, one-on-one meetings, print publications, webcasts, videos, social media, the agency’s website, and email. TRS staff also spoke at conferences across the state to update members and retirees on their pension and health care benefits as well as TRS investment performance. Major communications from the past year are summarized below: PRINT PUBLICATIONS During fiscal year 2015, TRS published three TRS News issues to provide members and retirees with important information relating to their benefits. The summer 2015 issue described TRS-related legislative changes enacted into law. Employers received TRS-related information through nine Update newsletters.

Annual statements were distributed in October 2014 to all active members of the system. TRS also published a number of publications for members and retirees, including brochures and other materials related to TRS pension and health care benefits. THE INTERNET Over the past year, the TRS website received a total of 3,328,859 visits, representing a 9.7 percent increase from 3,033,862 visits in the previous fiscal year. In addition, 1,732,348 unique visitors used the site during fiscal year 2015 — a 9.6 percent increase from 1,580,841 visitors in fiscal year 2014. MyTRS was promoted during the year through email, newsletter articles, social media, and the agency website. As of Aug. 31, 2015, 490,739 members and retirees had registered to participate in MyTRS, nearly 70,000 more than in the previous year. In 2015, significant online improvements were being developed through the TRS Enterprise Application Modernization (TEAM), a multi-year initiative to update business processes and core technologies used by TRS.

While TEAM will ultimately bring enhanced customer service, members experienced temporary, minimal reductions in MyTRS functionality during the year as work on TEAM progressed. As a result, it was temporarily not possible to access the following information online in 2015: • members’ beneficiary information • service purchase forms (once they have been created for a bill) and • replacement retirement packets (still available by contacting TRS directly) During the past year, TRS also developed a detailed approach to guide a redesign of the TRS website. A contract to develop and implement a redesigned website was awarded to a contractor in the fall of 2015. SOCIAL MEDIA In 2014-15, TRS broadened its engagement through social media with a growing number of members, retirees, and others. In fiscal year 2015, TRS recorded more than 7,860 Facebook likes, 2,200 followers on LinkedIn and 1,800 followers on Twitter.

In addition, TRS videos were viewed 81,334 times on YouTube. During the year, TRS expanded its use of LinkedIn to attract and recruit new employees through a new Career Page managed by Human Resources. At fiscal year-end, TRS heavily promoted a student art contest (kindergarten through fifth grade) to select art work for use in this publication. Submission of art work was slated for September, and voting on Facebook for best art among finalists was scheduled for October. Introductory Section 14 .

Communications WEBCASTING OF BOARD MEETINGS As part of its commitment to open and transparent communication, TRS continued to webcast board meetings during the past year. All board meetings are streamed live so members and others can watch the proceedings as they take place from anywhere in Texas or around the world. Each meeting is also recorded for on-demand playback. All TRS board meetings are archived on the TRS website where individual agenda items can be easily accessed through an online catalog.

In late fiscal year 2015, TRS announced plans to conduct an October webcast town hall meeting to discuss the sustainability and affordability of TRS-Care and TRS-ActiveCare. ASSOCIATION MEETINGS Early in the fiscal year, TRS continued its outreach to members and retirees through a series of Texas Retired Teacher Association meetings. TRS officials spoke to retirees at more than 20 conventions around the state and provided updates on TRS developments. These meetings provide an opportunity for TRS representatives to meet with members and retirees face-to-face and answer any questions they may have.

Legislators or their representatives from the area also frequently attend the meetings. GROUP PRESENTATIONS AND INDIVIDUAL RETIREMENT COUNSELING SESSIONS Over the past year, TRS made a number of group presentations to professional associations, employee and retiree groups and at regional education service centers. Presentations focused on retirement options, health care benefits for active and retired members, long-term care insurance, employment after retirement, and other TRS benefits. A total of 11,405 people attended 173 group presentations, and 20,800 people attended five conventions where TRS was represented.

In addition, 9,300 people visited individually with a TRS counselor – 8,883 in Austin and 417 in field office visit locations. Fiscal year 2015 was the ninth year that one-on-one retirement counseling sessions were offered in limited field locations throughout Texas (450 available appointments in 10 cities). TELECOMMUNICATIONS In fiscal year 2015, the agency’s Benefit Counseling department handled a total of 486,572 calls. In addition, 181,117 calls were completed during the past year within the agency’s automated telephone system. TRS and its contractors also provided telephone assistance to a large number of members seeking health care-related information. TRS-ActiveCare staff and contractors responded to 460,407 calls, and TRS-Care staff and contractors responded to 589,547 calls. COORDINATION WITH REPORTING ENTITIES The TRS Reporting and Query System (TRAQS), the agency’s internet-based reporting system for employers, had 1,362 reporting entities submit monthly reports to TRS by year end.

During the year, eight professional association and software user group presentations were attended by 420 people. One conference exhibit booth was attended by more than 2,000 school business staff, and one webinar was recorded and posted to the TRS website. In addition, a webinar in partnership with TASBO (Texas Association of School Business Officials) was recorded.

One participating employer traveled to TRS for onsite training, and one face-to-face conference training session was conducted with a reporting official. Twenty-six TRS-ActiveCare training seminars were conducted around the state for more than 1,200 benefit administrators of TRS-ActiveCare participating employers. Additionally, 10 webinars were conducted with 185 registered participants. For 2015, YouTube tutorials were also offered with 3,245 total views, as well as, on-demand voiceover webinars were offered to plan participants. There were 2,643 people who viewed the English version and 261 people who viewed the Spanish version.

These seminars/webinars provided information regarding enrollment, changes and ongoing administrative issues for TRS-ActiveCare. Introductory Section 15 . This page is intentionally left blank. Introductory Section 16 . FINANCIAL SECTION . This page is intentionally left blank. Financial Section 18 . Financial Section 19 . Financial Section 20 . Financial Section 21 . Financial Section 22 . Management’s Discussion and Analysis The following is Management’s Discussion and Analysis (MD&A) of the Teacher Retirement System’s (TRS or system) financial performance for the fiscal year ended August 31, 2015. The information presented here should be considered in conjunction with other areas of the Financial Section as well as information presented in the Executive Director’s Letter of Transmittal in the Introductory Section of the TRS Comprehensive Annual Financial Report. FINANCIAL HIGHLIGHTS The net position of the TRS Pension Trust Fund was $128.5 billion as of August 31, 2015, a decrease of 3.2%, in fiscal year 2015. ï‚· As of August 31, 2015, the date of the most recent actuarial valuation, the TRS Pension Trust Fund’s ratio of actuarial assets, as a percentage of actuarial liabilities, was 80.2%, which is the same as the level at August 31, 2014. The unfunded actuarial accrued liability was $33 billion, which is more than the $31.6 billion reported at August 31, 2014. ï‚· The annual rate of return on investments for the pension fund for the year ended August 31, 2015 was (0.27%). The rate of return for fiscal year 2014 was 16.9%. ï‚· The net position of TRS-Care was $972.9 million as of August 31, 2015, an increase of $515 million from fiscal year end 2014. ï‚· As of August 31, 2015, the date of the most recent actuarial valuation, TRS-Care trust fund’s unfunded actuarial accrued liability was $43.2 billion, which is more than the $33.3 billion reported at August 31, 2014. ï‚· TRS-ActiveCare had a net position of $87.8 million as of August 31, 2015, an increase of $65.0 million or 285% in fiscal year 2015. OVERVIEW OF THE FINANCIAL STATEMENTS This discussion and analysis is intended to serve as an introduction to the TRS financial presentation, which consists of the following components: ï‚· Fund financial statements ï‚· Notes to the financial statements ï‚· Required supplementary information ï‚· Other supplementary schedules Collectively, this information presents the net position available for pension and other post-employment benefits, health care benefits, and other purposes as of August 31, 2015, and summarizes any changes in net position for the year then ended. The information available in each of these sections is summarized as follows: Fund Financial Statements Individual fund financial statements are presented for all fiduciary and proprietary funds as of August 31, 2015 and for the year then ended.

Comparative data in total as of August 31, 2014, and for the year then ended has also been presented with the exception of agency funds. These financial statements reflect the resources available to pay benefits to retirees Financial Section 23 . Management’s Discussion and Analysis and other beneficiaries, to pay health care benefits for covered participants, and to administer the 403(b) Administrative Program. Fiduciary funds presented include the Pension Trust Fund, TRS-Care and Agency Funds. Fiduciary funds are used to account for resources held for the benefit of parties outside of TRS. Proprietary funds account for business-type activities and include the TRS-ActiveCare and the non-major 403(b) Administrative Program enterprise funds. Notes to the Financial Statements The financial statement notes provide additional information that is essential to a full understanding of the data provided in the fund financial statements.

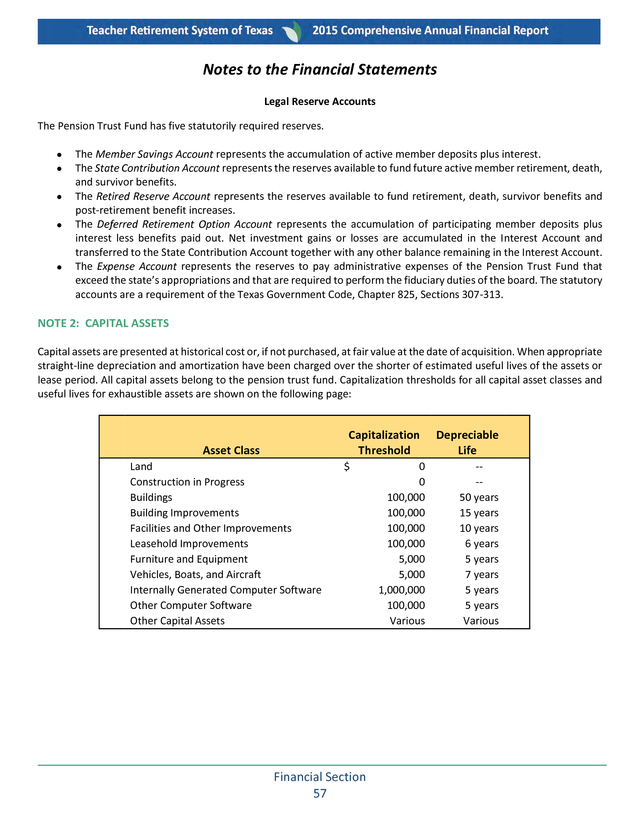

Information available in the notes to the financial statements is described below: ï‚· Note 1 provides a summary of significant accounting policies, including the basis of accounting, budgets and appropriations, explanations of major asset and liability classes, and legal reserve account information. Also included is a general description of TRS as well as a description of each of the funds administered by TRS. ï‚· Note 2 provides information on capital assets. ï‚· Note 3 describes deposits and investments, including investing authority, investment risk categorizations, and additional information about cash, derivatives, securities lending, alternative investments and contingent commitments. ï‚· Note 4 provides information on employee compensable leave. ï‚· Note 5 provides information on the operating lease. ï‚· Note 6 provides information on fringe benefits paid by the state and federal government on behalf of employees and participants of the health care plans. ï‚· Note 7 describes deferred compensation plans available to TRS employees. ï‚· Note 8 provides information on contingent liabilities such as TRS employees’ accumulated sick leave, lump sum death benefits, incentive compensation, retiree benefits and any pending litigation. ï‚· Note 9 addresses TRS’ continuance subject to review under the Texas Sunset Act. ï‚· Note 10 describes other post-employment health care benefits provided to TRS’ employees and retired public school employees, contributions to the plan and its funded status. ï‚· Note 11 addresses risk management issues related to the health benefits program for active school district employees. ï‚· Note 12 provides pension disclosure information including detailed data on the plan description, contributions, legal reserve balances and the net pension liability. ï‚· Note 13 provides information on subsequent events. Required Supplementary Information Required supplementary information for the pension plan consists of schedules related to the net pension liability, contributions from employers and the non-employer contributing entity, and the annual money weighted rate of return on pension plan investments. RSI for the other employee benefit plan administered by TRS includes schedules related to the funding progress and the contributions from the participating employers.

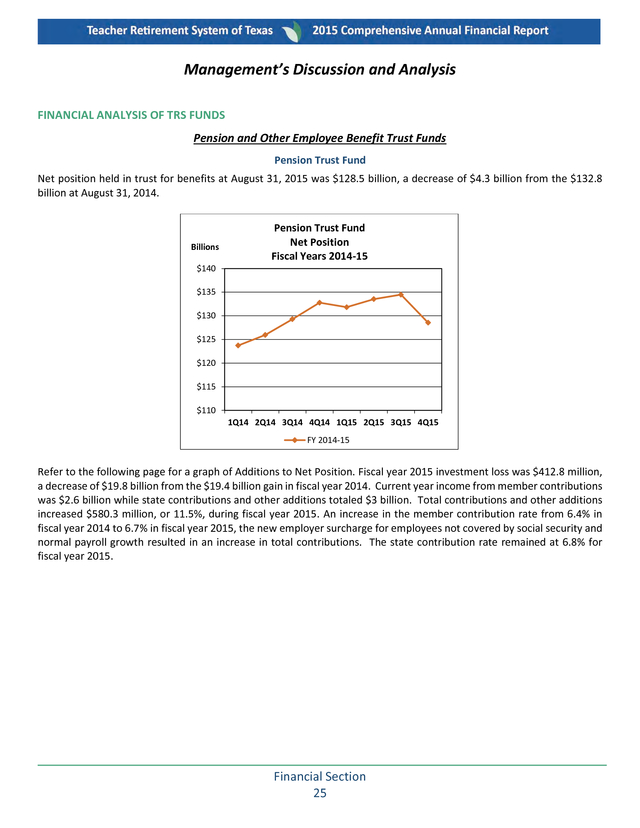

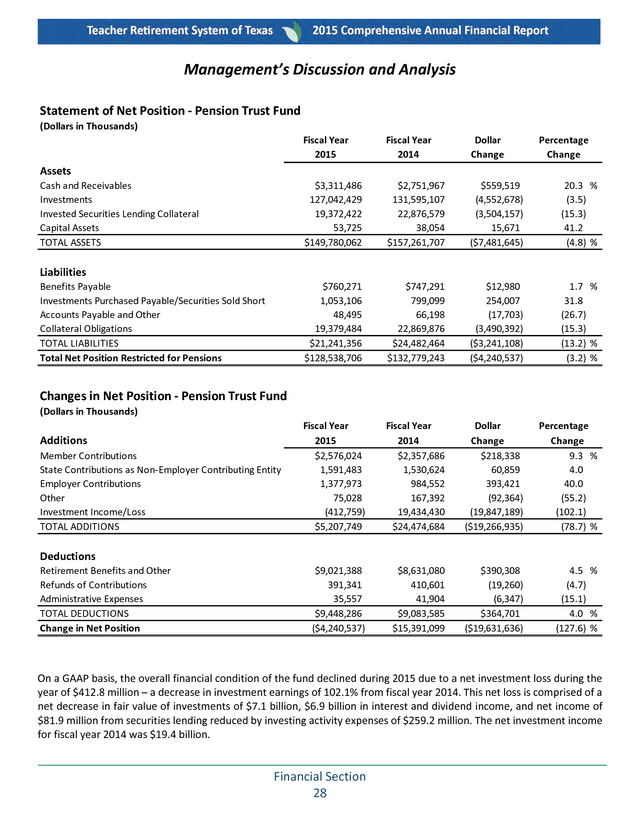

Also included in this component is Management’s Discussion and Analysis. Other Supplementary Schedules Other schedules include information on agency funds, changes in statutory reserve account balances, schedule of administrative expenses, investing activity expenses, and payments to consultants. Financial Section 24 . Management’s Discussion and Analysis FINANCIAL ANALYSIS OF TRS FUNDS Pension and Other Employee Benefit Trust Funds Pension Trust Fund Net position held in trust for benefits at August 31, 2015 was $128.5 billion, a decrease of $4.3 billion from the $132.8 billion at August 31, 2014. Billions Pension Trust Fund Net Position Fiscal Years 2014-15 $140 $135 $130 $125 $120 $115 $110 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 FY 2014-15 Refer to the following page for a graph of Additions to Net Position. Fiscal year 2015 investment loss was $412.8 million, a decrease of $19.8 billion from the $19.4 billion gain in fiscal year 2014. Current year income from member contributions was $2.6 billion while state contributions and other additions totaled $3 billion. Total contributions and other additions increased $580.3 million, or 11.5%, during fiscal year 2015.

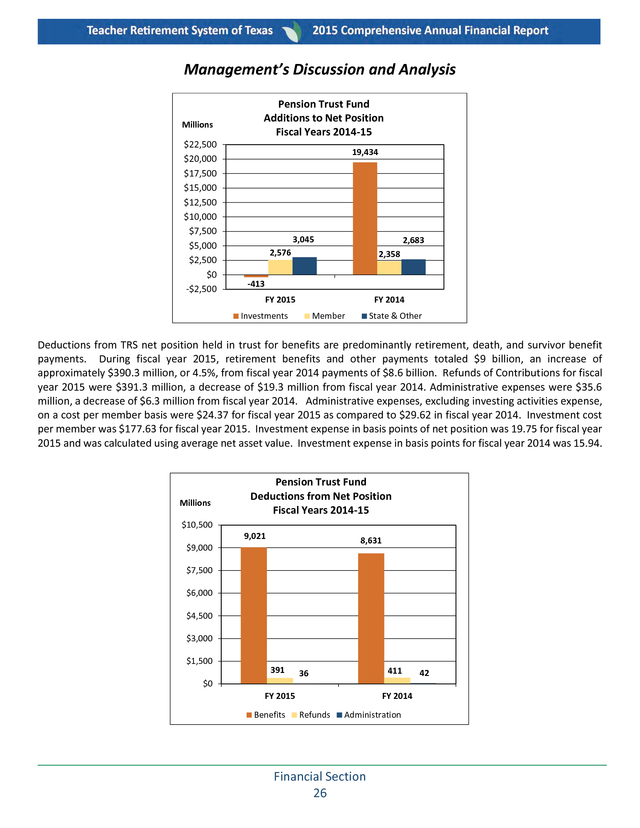

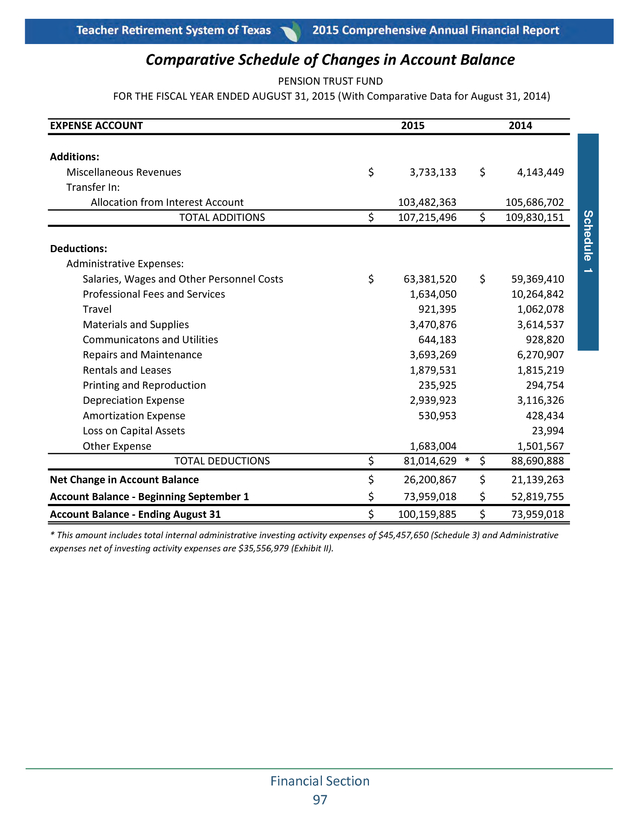

An increase in the member contribution rate from 6.4% in fiscal year 2014 to 6.7% in fiscal year 2015, the new employer surcharge for employees not covered by social security and normal payroll growth resulted in an increase in total contributions. The state contribution rate remained at 6.8% for fiscal year 2015. Financial Section 25 . Management’s Discussion and Analysis Millions $22,500 $20,000 $17,500 $15,000 $12,500 $10,000 $7,500 $5,000 $2,500 $0 -$2,500 Pension Trust Fund Additions to Net Position Fiscal Years 2014-15 19,434 3,045 2,683 2,576 2,358 FY 2015 FY 2014 -413 Investments Member State & Other Deductions from TRS net position held in trust for benefits are predominantly retirement, death, and survivor benefit payments. During fiscal year 2015, retirement benefits and other payments totaled $9 billion, an increase of approximately $390.3 million, or 4.5%, from fiscal year 2014 payments of $8.6 billion. Refunds of Contributions for fiscal year 2015 were $391.3 million, a decrease of $19.3 million from fiscal year 2014. Administrative expenses were $35.6 million, a decrease of $6.3 million from fiscal year 2014.

Administrative expenses, excluding investing activities expense, on a cost per member basis were $24.37 for fiscal year 2015 as compared to $29.62 in fiscal year 2014. Investment cost per member was $177.63 for fiscal year 2015. Investment expense in basis points of net position was 19.75 for fiscal year 2015 and was calculated using average net asset value.

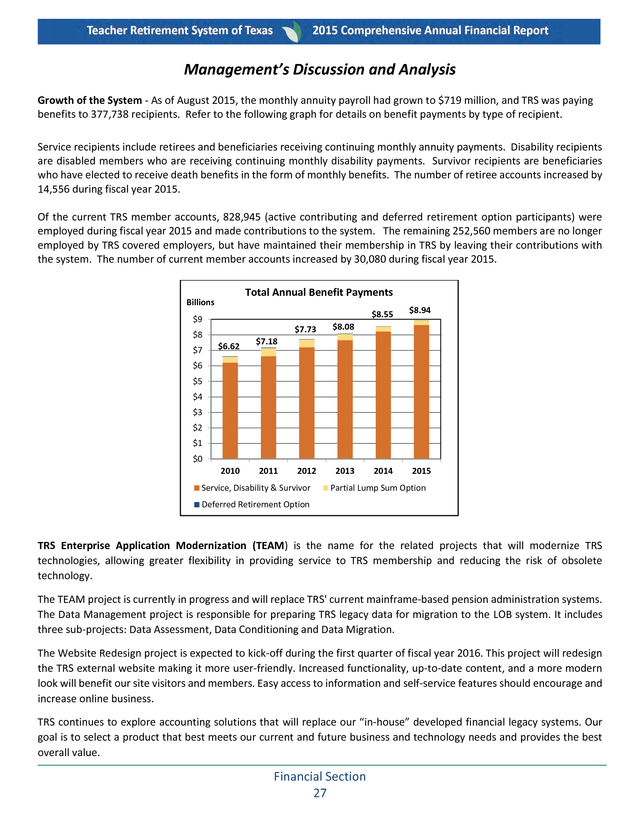

Investment expense in basis points for fiscal year 2014 was 15.94. Millions Pension Trust Fund Deductions from Net Position Fiscal Years 2014-15 $10,500 9,021 8,631 $9,000 $7,500 $6,000 $4,500 $3,000 $1,500 391 411 36 $0 FY 2015 Benefits FY 2014 Refunds Administration Financial Section 26 42 . Management’s Discussion and Analysis Growth of the System - As of August 2015, the monthly annuity payroll had grown to $719 million, and TRS was paying benefits to 377,738 recipients. Refer to the following graph for details on benefit payments by type of recipient. Service recipients include retirees and beneficiaries receiving continuing monthly annuity payments. Disability recipients are disabled members who are receiving continuing monthly disability payments. Survivor recipients are beneficiaries who have elected to receive death benefits in the form of monthly benefits.

The number of retiree accounts increased by 14,556 during fiscal year 2015. Of the current TRS member accounts, 828,945 (active contributing and deferred retirement option participants) were employed during fiscal year 2015 and made contributions to the system. The remaining 252,560 members are no longer employed by TRS covered employers, but have maintained their membership in TRS by leaving their contributions with the system. The number of current member accounts increased by 30,080 during fiscal year 2015. Total Annual Benefit Payments Billions $8.55 $9 $7.73 $8 $7 $6.62 2013 2014 2015 $8.08 2012 $8.94 $7.18 $6 $5 $4 $3 $2 $1 $0 2010 2011 Service, Disability & Survivor Partial Lump Sum Option Deferred Retirement Option TRS Enterprise Application Modernization (TEAM) is the name for the related projects that will modernize TRS technologies, allowing greater flexibility in providing service to TRS membership and reducing the risk of obsolete technology. The TEAM project is currently in progress and will replace TRS' current mainframe-based pension administration systems. The Data Management project is responsible for preparing TRS legacy data for migration to the LOB system.

It includes three sub-projects: Data Assessment, Data Conditioning and Data Migration. The Website Redesign project is expected to kick-off during the first quarter of fiscal year 2016. This project will redesign the TRS external website making it more user-friendly. Increased functionality, up-to-date content, and a more modern look will benefit our site visitors and members.

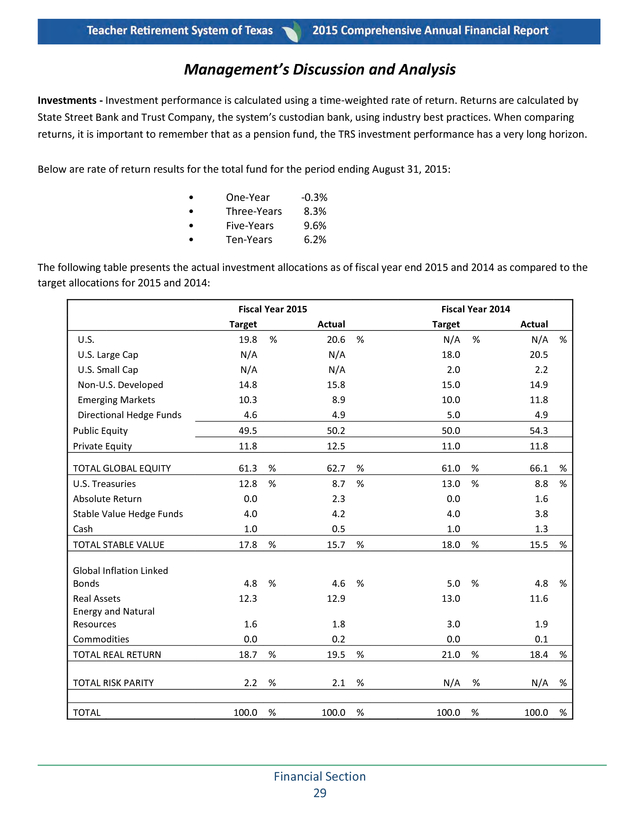

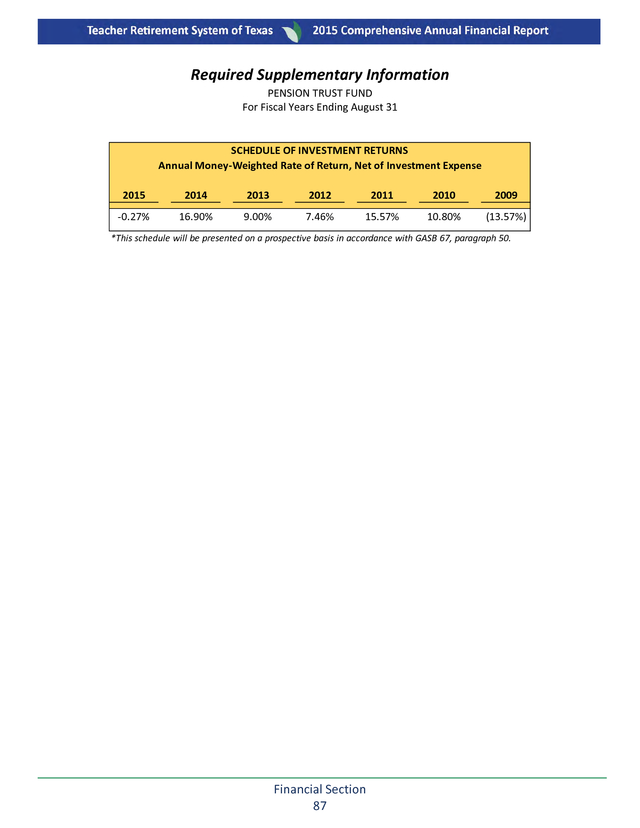

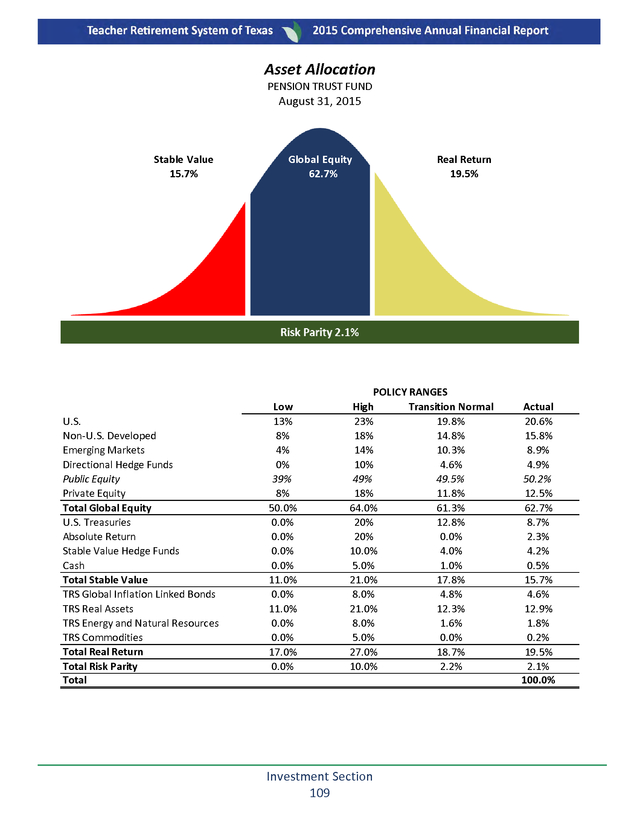

Easy access to information and self-service features should encourage and increase online business. TRS continues to explore accounting solutions that will replace our “in-house” developed financial legacy systems. Our goal is to select a product that best meets our current and future business and technology needs and provides the best overall value. Financial Section 27 . Management’s Discussion and Analysis Statement of Net Position - Pension Trust Fund (Dollars in Thousands) Fiscal Year 2015 Fiscal Year 2014 Dollar Change Percentage Change $3,311,486 127,042,429 19,372,422 53,725 $149,780,062 $2,751,967 131,595,107 22,876,579 38,054 $157,261,707 $559,519 (4,552,678) (3,504,157) 15,671 ($7,481,645) 20.3 % (3.5) (15.3) 41.2 (4.8) % $760,271 1,053,106 48,495 19,379,484 $21,241,356 $128,538,706 $747,291 799,099 66,198 22,869,876 $24,482,464 $132,779,243 $12,980 254,007 (17,703) (3,490,392) ($3,241,108) ($4,240,537) 1.7 % 31.8 (26.7) (15.3) (13.2) % (3.2) % Fiscal Year 2015 $2,576,024 1,591,483 1,377,973 75,028 (412,759) $5,207,749 Fiscal Year 2014 $2,357,686 1,530,624 984,552 167,392 19,434,430 $24,474,684 Dollar Change $218,338 60,859 393,421 (92,364) (19,847,189) ($19,266,935) Percentage Change 9.3 % 4.0 40.0 (55.2) (102.1) (78.7) % $9,021,388 391,341 35,557 $9,448,286 ($4,240,537) $8,631,080 410,601 41,904 $9,083,585 $15,391,099 $390,308 (19,260) (6,347) $364,701 ($19,631,636) 4.5 % (4.7) (15.1) 4.0 % (127.6) % Assets Cash and Receivables Investments Invested Securities Lending Collateral Capital Assets TOTAL ASSETS Liabilities Benefits Payable Investments Purchased Payable/Securities Sold Short Accounts Payable and Other Collateral Obligations TOTAL LIABILITIES Total Net Position Restricted for Pensions Changes in Net Position - Pension Trust Fund (Dollars in Thousands) Additions Member Contributions State Contributions as Non-Employer Contributing Entity Employer Contributions Other Investment Income/Loss TOTAL ADDITIONS Deductions Retirement Benefits and Other Refunds of Contributions Administrative Expenses TOTAL DEDUCTIONS Change in Net Position On a GAAP basis, the overall financial condition of the fund declined during 2015 due to a net investment loss during the year of $412.8 million – a decrease in investment earnings of 102.1% from fiscal year 2014. This net loss is comprised of a net decrease in fair value of investments of $7.1 billion, $6.9 billion in interest and dividend income, and net income of $81.9 million from securities lending reduced by investing activity expenses of $259.2 million. The net investment income for fiscal year 2014 was $19.4 billion. Financial Section 28 . Management’s Discussion and Analysis Investments - Investment performance is calculated using a time-weighted rate of return. Returns are calculated by State Street Bank and Trust Company, the system’s custodian bank, using industry best practices. When comparing returns, it is important to remember that as a pension fund, the TRS investment performance has a very long horizon. Below are rate of return results for the total fund for the period ending August 31, 2015: • • • • One-Year Three-Years Five-Years Ten-Years -0.3% 8.3% 9.6% 6.2% The following table presents the actual investment allocations as of fiscal year end 2015 and 2014 as compared to the target allocations for 2015 and 2014: U.S. U.S. Large Cap U.S.

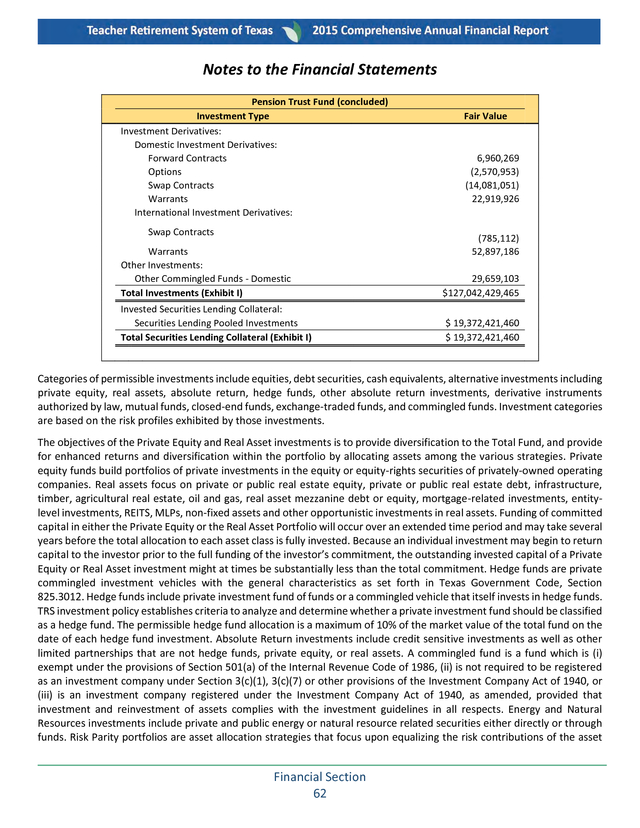

Small Cap Non-U.S. Developed Emerging Markets Directional Hedge Funds Fiscal Year 2015 Target Actual 19.8 % 20.6 N/A N/A N/A N/A 14.8 15.8 10.3 8.9 4.6 4.9 Public Equity Private Equity 49.5 11.8 TOTAL GLOBAL EQUITY U.S. Treasuries Absolute Return Stable Value Hedge Funds Cash TOTAL STABLE VALUE 61.3 12.8 0.0 4.0 1.0 17.8 % % 4.8 12.3 % Global Inflation Linked Bonds Real Assets Energy and Natural Resources Commodities TOTAL REAL RETURN TOTAL RISK PARITY TOTAL 1.6 0.0 18.7 % 50.2 12.5 % 50.0 11.0 62.7 8.7 2.3 4.2 0.5 15.7 % % 4.6 12.9 % % 1.8 0.2 19.5 2.2 % 100.0 % Fiscal Year 2014 Target Actual N/A % N/A 18.0 20.5 2.0 2.2 15.0 14.9 10.0 11.8 5.0 4.9 % % % 5.0 13.0 % % 2.1 % 100.0 % Financial Section 29 54.3 11.8 61.0 13.0 0.0 4.0 1.0 18.0 3.0 0.0 21.0 % % 66.1 8.8 1.6 3.8 1.3 15.5 % % 4.8 11.6 % % % 1.9 0.1 18.4 % N/A % N/A % 100.0 % 100.0 % .

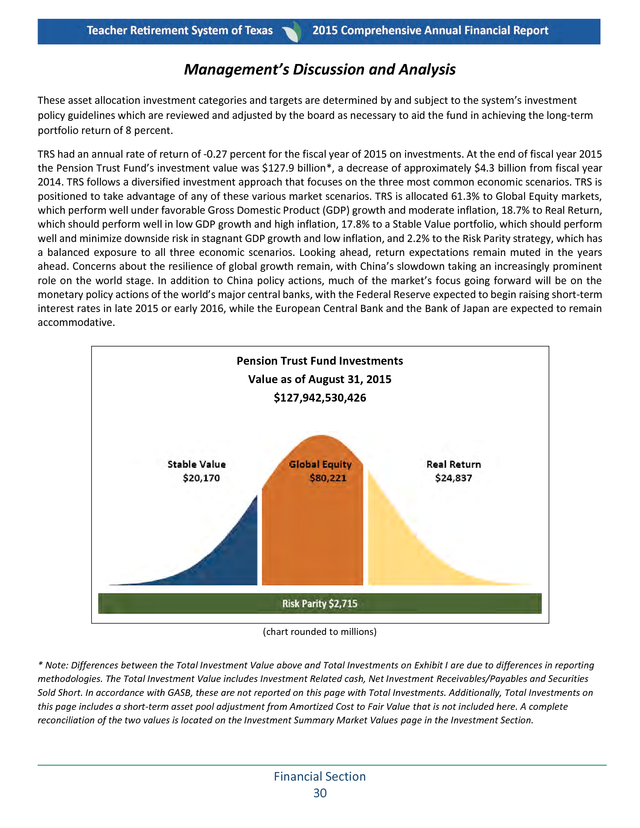

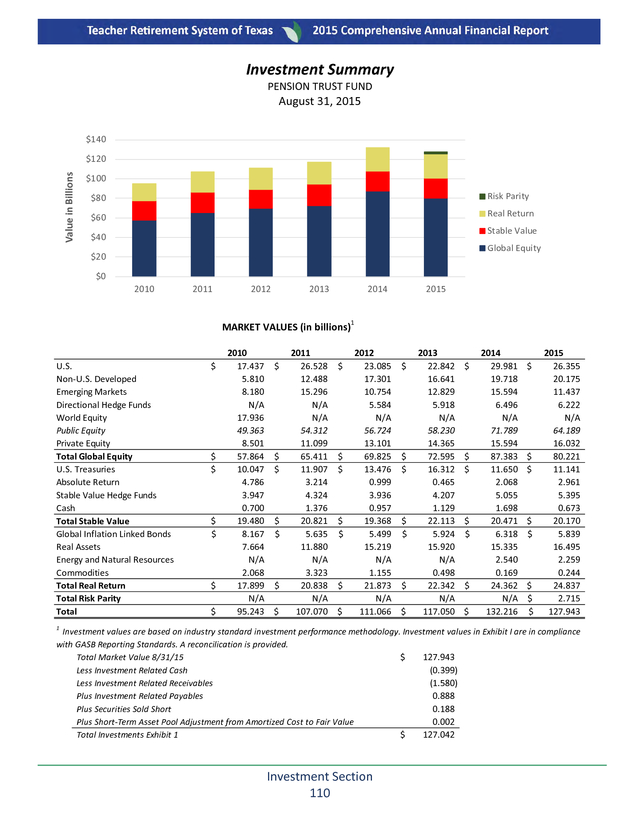

Management’s Discussion and Analysis These asset allocation investment categories and targets are determined by and subject to the system’s investment policy guidelines which are reviewed and adjusted by the board as necessary to aid the fund in achieving the long-term portfolio return of 8 percent. TRS had an annual rate of return of -0.27 percent for the fiscal year of 2015 on investments. At the end of fiscal year 2015 the Pension Trust Fund’s investment value was $127.9 billion*, a decrease of approximately $4.3 billion from fiscal year 2014. TRS follows a diversified investment approach that focuses on the three most common economic scenarios. TRS is positioned to take advantage of any of these various market scenarios.

TRS is allocated 61.3% to Global Equity markets, which perform well under favorable Gross Domestic Product (GDP) growth and moderate inflation, 18.7% to Real Return, which should perform well in low GDP growth and high inflation, 17.8% to a Stable Value portfolio, which should perform well and minimize downside risk in stagnant GDP growth and low inflation, and 2.2% to the Risk Parity strategy, which has a balanced exposure to all three economic scenarios. Looking ahead, return expectations remain muted in the years ahead. Concerns about the resilience of global growth remain, with China’s slowdown taking an increasingly prominent role on the world stage.

In addition to China policy actions, much of the market’s focus going forward will be on the monetary policy actions of the world’s major central banks, with the Federal Reserve expected to begin raising short-term interest rates in late 2015 or early 2016, while the European Central Bank and the Bank of Japan are expected to remain accommodative. Pension Trust Fund Investments Value as of August 31, 2015 $127,942,530,426 (chart rounded to millions) * Note: Differences between the Total Investment Value above and Total Investments on Exhibit I are due to differences in reporting methodologies. The Total Investment Value includes Investment Related cash, Net Investment Receivables/Payables and Securities Sold Short. In accordance with GASB, these are not reported on this page with Total Investments.

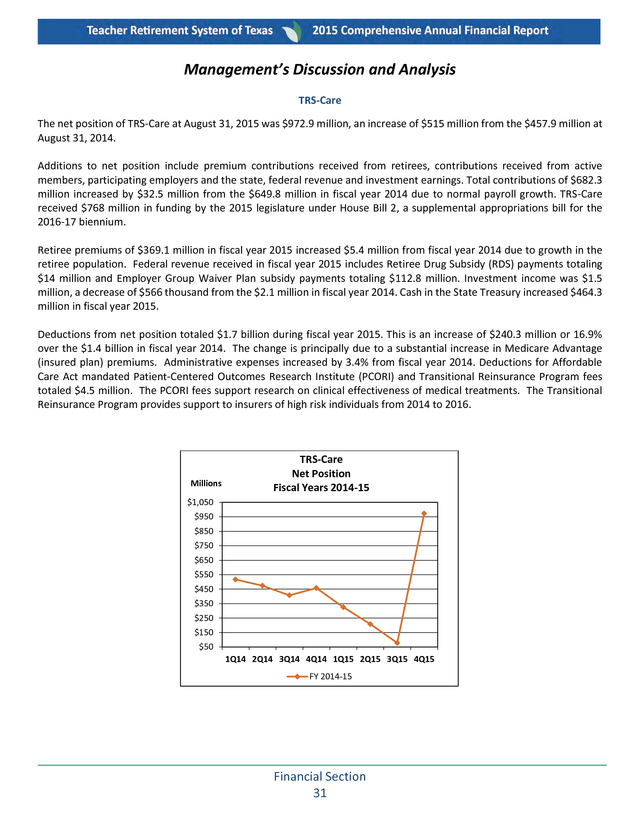

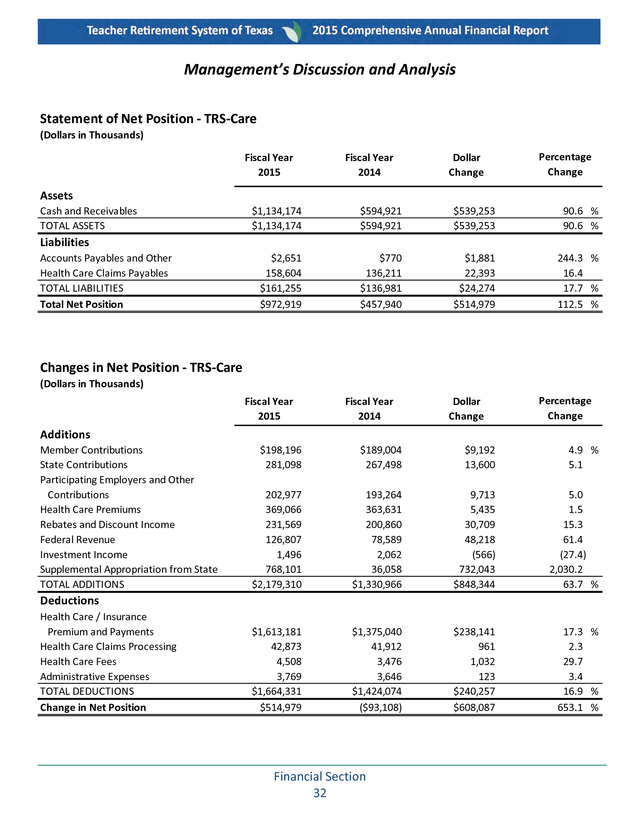

Additionally, Total Investments on this page includes a short-term asset pool adjustment from Amortized Cost to Fair Value that is not included here. A complete reconciliation of the two values is located on the Investment Summary Market Values page in the Investment Section. Financial Section 30 . Management’s Discussion and Analysis TRS-Care The net position of TRS-Care at August 31, 2015 was $972.9 million, an increase of $515 million from the $457.9 million at August 31, 2014. Additions to net position include premium contributions received from retirees, contributions received from active members, participating employers and the state, federal revenue and investment earnings. Total contributions of $682.3 million increased by $32.5 million from the $649.8 million in fiscal year 2014 due to normal payroll growth. TRS-Care received $768 million in funding by the 2015 legislature under House Bill 2, a supplemental appropriations bill for the 2016-17 biennium. Retiree premiums of $369.1 million in fiscal year 2015 increased $5.4 million from fiscal year 2014 due to growth in the retiree population. Federal revenue received in fiscal year 2015 includes Retiree Drug Subsidy (RDS) payments totaling $14 million and Employer Group Waiver Plan subsidy payments totaling $112.8 million.

Investment income was $1.5 million, a decrease of $566 thousand from the $2.1 million in fiscal year 2014. Cash in the State Treasury increased $464.3 million in fiscal year 2015. Deductions from net position totaled $1.7 billion during fiscal year 2015. This is an increase of $240.3 million or 16.9% over the $1.4 billion in fiscal year 2014.

The change is principally due to a substantial increase in Medicare Advantage (insured plan) premiums. Administrative expenses increased by 3.4% from fiscal year 2014. Deductions for Affordable Care Act mandated Patient-Centered Outcomes Research Institute (PCORI) and Transitional Reinsurance Program fees totaled $4.5 million.

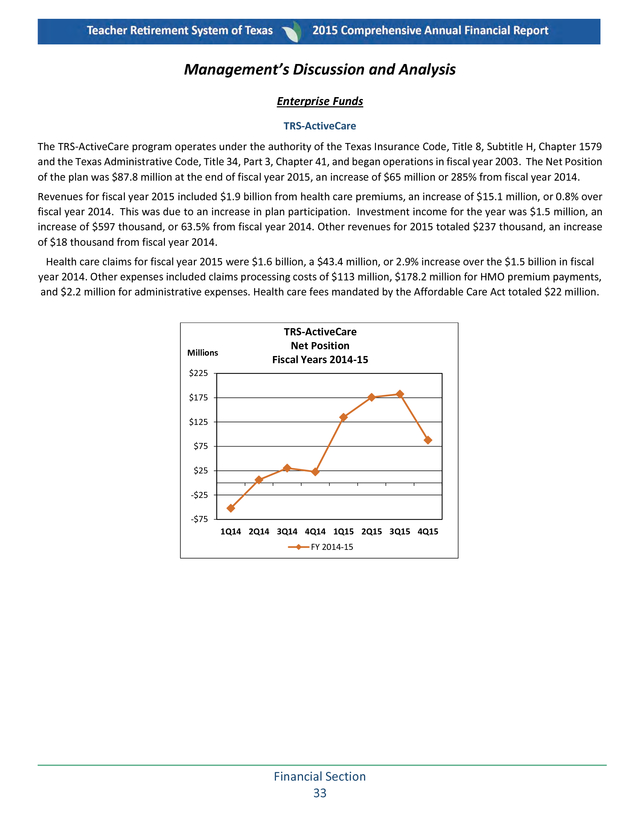

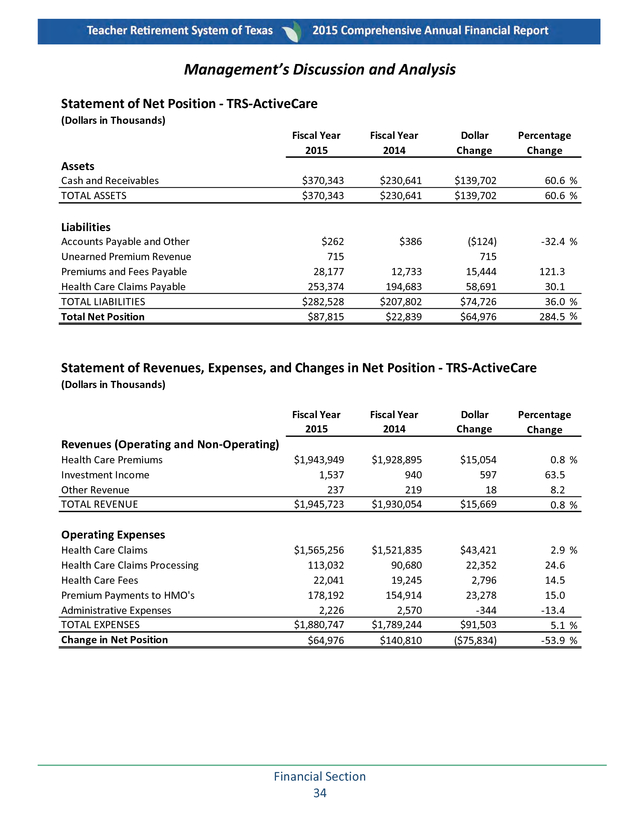

The PCORI fees support research on clinical effectiveness of medical treatments. The Transitional Reinsurance Program provides support to insurers of high risk individuals from 2014 to 2016. Millions TRS-Care Net Position Fiscal Years 2014-15 $1,050 $950 $850 $750 $650 $550 $450 $350 $250 $150 $50 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 FY 2014-15 Financial Section 31 . Management’s Discussion and Analysis Statement of Net Position - TRS-Care (Dollars in Thousands) Fiscal Year 2015 Fiscal Year 2014 Dollar Change Percentage Change Assets Cash and Receivables TOTAL ASSETS $1,134,174 $1,134,174 $594,921 $594,921 $539,253 $539,253 90.6 % 90.6 % $2,651 158,604 $161,255 $972,919 $770 136,211 $136,981 $457,940 $1,881 22,393 $24,274 $514,979 244.3 % 16.4 17.7 % 112.5 % Liabilities Accounts Payables and Other Health Care Claims Payables TOTAL LIABILITIES Total Net Position Changes in Net Position - TRS-Care (Dollars in Thousands) Fiscal Year 2015 Fiscal Year 2014 Dollar Change Percentage Change Additions Member Contributions State Contributions Participating Employers and Other Contributions Health Care Premiums Rebates and Discount Income Federal Revenue Investment Income Supplemental Appropriation from State TOTAL ADDITIONS $198,196 281,098 $189,004 267,498 $9,192 13,600 4.9 % 5.1 202,977 369,066 231,569 126,807 1,496 768,101 $2,179,310 193,264 363,631 200,860 78,589 2,062 36,058 $1,330,966 9,713 5,435 30,709 48,218 (566) 732,043 $848,344 5.0 1.5 15.3 61.4 (27.4) 2,030.2 63.7 % $1,613,181 42,873 4,508 3,769 $1,664,331 $514,979 $1,375,040 41,912 3,476 3,646 $1,424,074 ($93,108) $238,141 961 1,032 123 $240,257 $608,087 17.3 % 2.3 29.7 3.4 16.9 % 653.1 % Deductions Health Care / Insurance Premium and Payments Health Care Claims Processing Health Care Fees Administrative Expenses TOTAL DEDUCTIONS Change in Net Position Financial Section 32 . Management’s Discussion and Analysis Enterprise Funds TRS-ActiveCare The TRS-ActiveCare program operates under the authority of the Texas Insurance Code, Title 8, Subtitle H, Chapter 1579 and the Texas Administrative Code, Title 34, Part 3, Chapter 41, and began operations in fiscal year 2003. The Net Position of the plan was $87.8 million at the end of fiscal year 2015, an increase of $65 million or 285% from fiscal year 2014. Revenues for fiscal year 2015 included $1.9 billion from health care premiums, an increase of $15.1 million, or 0.8% over fiscal year 2014. This was due to an increase in plan participation. Investment income for the year was $1.5 million, an increase of $597 thousand, or 63.5% from fiscal year 2014.

Other revenues for 2015 totaled $237 thousand, an increase of $18 thousand from fiscal year 2014. Health care claims for fiscal year 2015 were $1.6 billion, a $43.4 million, or 2.9% increase over the $1.5 billion in fiscal year 2014. Other expenses included claims processing costs of $113 million, $178.2 million for HMO premium payments, and $2.2 million for administrative expenses. Health care fees mandated by the Affordable Care Act totaled $22 million. Millions TRS-ActiveCare Net Position Fiscal Years 2014-15 $225 $175 $125 $75 $25 -$25 -$75 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 FY 2014-15 Financial Section 33 .