Description

TRS

NEWS

DECEMBER 2015

TEACHER RETIREMENT SYSTEM OF TEXAS

Health care options discussed at town hall meeting

The TRS Board of Trustees hosted a Health Care Town Hall meeting in Austin in October. The interactive meeting was part of a board

meeting focusing solely on the health care environment affecting health plans across the country. The meeting featured presentations

from national health care experts, and the related discussion focused specifically on TRS-Care and TRS-ActiveCare.

More than 100 people attended the meeting at TRS, which included question-and-answer sessions with the panelists and TRS trustees.

Those viewing the meeting through the TRS website submitted their questions electronically via Facebook and Twitter. Questions that

were not addressed during the meeting will be categorized and answered by common topic on the TRS website.

“TRS health care programs face a number of challenging issues including funding, sustainability and affordability.

The Town Hall meeting provided both an update for our members as well as a forum to listen to ideas regarding possible solutions,” said TRS Executive Director Brian Guthrie. “It was an outstanding day of information. We are looking forward to working with our members and stakeholders to prepare for the next legislative session on some of the issues and challenges discussed.” Panel discussions during the day featured national health care experts speaking on topics such as the health care market and the context in which TRS plans operate.

Strategies for cost containment in health care as well as the history, structure and financial status of TRSCare and TRS-ActiveCare were also discussed. Board meeting webcasts are available on the TRS website. To view the October town hall meeting, visit the TRS website which is located at www.trs.texas.gov. Click on the “General Information” tab, select “Board of Trustees” on the left side of your screen, select TRS Board Meeting Webcasts, and choose the October 22 board meeting to access the webcast. TRS website to feature new TRS Benefits Handbook in December TRS will publish an updated version of the TRS Benefits Handbook in December, including changes in the law enacted by the 84th Texas Legislature and amendments to plan rules adopted by the TRS Board of Trustees.

While handbooks are mailed only upon request, members and retirees can view and print a copy of the handbook by visiting the TRS website which is located at www.trs.texas.gov. You can also receive a notice when the new handbook is available by signing up for email subscriptions on the MyTRS section of the website. This year’s handbook provides information about a new rule amendment that may impact future retirees. Beginning with the 2015-16 school year, annual compensation for the school year in which you retire will be the highest total of compensation received during a 12-consecutive-month period that occurs during a 14-consecutivemonth period and meets eight specific requirements, including the requirement that the period begins no earlier than the first month of your qualified contract period.

(To view these provisions, see the section titled “Determining Annual Compensation.”) This rule change is not retroactive for retirements or deaths prior to the 2015-16 school year. . MEMBERS FROM MEMO TO Executive Director Brian K. Guthrie As you read this final TRS News issue of 2015, we hope you are able to take time off to enjoy the holidays, look back upon the past year and have an even better one in the year to come. We at TRS are also looking back upon 2015 -- and laying the groundwork for initiatives to better serve you in the coming year. During the past year, TRS named three new chief officers – Chief Information Officer Chris Cutler, Chief Benefit Officer Barbie Pearson and Chief Health Care Officer Katrina Daniel. We also made other organizational changes to better position us to focus on our key challenges moving forward: health care fund solvency, pension trust fund sustainability, long-term investment returns, and replacing legacy technology systems. Thanks to the hard work and dedication of our employees, TRS was also named a “Top Workplace” by the Austin American-Statesman for the fourth year in a row. For the 12-month period ending Aug.

31, 2015, the TRS portfolio had a return of -0.3 percent during a challenging year for all investors. However, our 2015 return surpassed the fund’s benchmark by 0.5 percent. For the past 10 years, our time-weighted compound annual return has been 6.2 percent.

On a three-year annualized basis, your fund has returned 8.3 percent, which is 1 percent above its benchmark. Annual rates of return for the five- and 10-year periods ending Aug. 31, 2015 were 9.6 percent and 6.2 percent, respectively. As of Aug.

31, 2015, the system had a funded ratio of 80.2 percent with an Unfunded Actuarial Accrued Liability of $33 billion. The system is now deferring net investment losses of $4.9 billion. The time necessary to amortize the unfunded liability R.

DAVID KELLY, Chair, Plano has also increased NANETTE SISSNEY, Vice Chair, Whitesboro from 29.8 years TODD BARTH, Houston to 33.3 years. Our KAREN CHARLESTON, Houston actuary estimates that JOE COLONNETTA, Dallas our unfunded liability DAVID CORPUS, Humble Board of Trustees CHRISTOPHER MOSS, Lufkin ANITA PALMER, Jacksboro DOLORES RAMIREZ, San Benito BRIAN K. GUTHRIE, Executive Director 2 and the funding period will both continue to increase over the next few years before beginning to once again decline. This newsletter includes articles on several important topics, including a town hall meeting conducted this fall to discuss the affordability of TRS-Care and sustainability of TRS-ActiveCare.

These same challenges will be studied by a joint interim committee created by the 84th Texas Legislature, and TRS will support the committee’s work to address these issues. Other topics include accessing 1099-R forms electronically, employment after retirement, federal income tax withholding preferences, TRS service and compensation deadlines, and our latest videos on 2015 TRS-related legislation and financial education. This past fall, Texas school children in K-5th grades participated in a TRS art contest where they submitted artwork depicting their teachers as superheroes. More than 3,500 art entries were received! The first place winner was Natalie Martinez of Clark Elementary, Laredo.

Stephanie Garces of San Antonio’s Roosevelt Elementary came in second, and Joi Speck of Live Oak Learning Center, Rockport, placed third. Liliana Hale of Ramirez Elementary, Lubbock, also received an honorable mention. I am amazed at how good these drawings are, and I think you will be too.

Please take a moment to view the winning art work and all the other great entries at www.trs.texas.gov. We invite you to stay current about your retirement system by visiting our website, TRS News is published by Teacher Retirement System of Texas reading our newsletters and following us on 1000 Red River Street Facebook and Twitter. In the meantime, all of Austin, Texas 78701-2698 us at TRS wish you and your families the (512) 542-6400 or 1-800-223-8778 happiest of holidays and all the best in 2016. www.trs.texas.gov The Teacher Retirement System of Texas does not discriminate on the basis of race, color, national origin, sex, religion, age or disability in employment or the provision of services. A copy of the complete TRS plan is available at the above address during regular business hours. .

New website videos feature updates on health care programs, 2015 legislation, financial education Three new videos are now available on the TRS website, which offer members, retirees and others updated news on TRS operations. The videos, produced by TRS’ Communications Department, are part of the series called “TRS Today.” One video features an interview with Chief Health Care Officer Katrina Daniel titled “Status of TRS-ActiveCare and TRS-Care” where Daniel talks about issues affecting both health benefits programs. In a second video titled “2015 TRS-Related Legislation,” Executive Director Brian Guthrie walks us through legislation impacting TRS that was passed during the 84th legislative session, including information regarding TRS-Care funding. In a third video, Guthrie explains financial education options available to members.

He also shares how TRS is launching a financial awareness program to help members identify the important questions to consider before retirement. The videos provide information on various topics, including estimating your TRS annuity, Social Security considerations related to TRS benefits, the impact of compounding interest, the TRS 403(b) certification program, and more. The videos on health care programs, 2015 legislation and financial education are approximately six-to-10 minutes long and are available through TRS.TV on the TRS website (www.trs.texas.gov). From the TRS home page, select the “Watch TRS Today Videos” link near the bottom of the column on the right side of your screen. Access next year’s 1099-R forms quickly and easily online In late January 2016, TRS will send 1099-R forms to those who have received one or more payments from TRS during calendar year 2015. The 1099-R is an Internal Revenue Service form that the recipient uses to report any distributions paid by TRS during the prior calendar year. or by fax.

The duplicate copies must be mailed. However, retirees and payment beneficiaries who have a MyTRS password can view and print a copy of their 1099-R forms, even before forms are mailed in January. As a reminder, recent legislation changed the annuity payment date to the last day of the month beginning with the September payment. This payment date change will result in annuitants receiving 13 annuity payments during calendar year 2015 and may affect the amount of federal income tax that you owe for this calendar year. If you subscribe now on MyTRS, you can have TRS send you an email message to notify you as soon as your 1099-R form is posted online. If you haven’t registered yet for MyTRS, doing so is easy. Simply go to the TRS website at www.trs.texas.gov and click on the MyTRS link under “Quicklinks” on the right-hand side of the home page.

Follow the instructions from there. From the time this form is distributed in January until April 15, TRS receives numerous requests for duplicate copies. Due to confidentiality requirements, TRS cannot provide the information over the phone Note: Individuals who receive payments from the TRS excess benefit arrangement will receive a W-2 form from TRS for the amounts paid out of the excess benefit fund during the 2015 calendar year. Are you a retiree considering employment after retirement? If you are retired or planning to retire and you are considering employment with a TRS-covered employer after you retire, take some time to review the Employment After Retirement brochure on the TRS website. TRS laws and rules that pertain to working for a TRS-covered employer are different based on the date you retired and whether or not you are retired under Service Retirement or Disability Retirement. If you work more than allowed, you will lose your annuity for each month that you exceed the limits.

If you go back to work – any kind of work, even working as a substitute – for a TRS-covered employer in the calendar month following your retirement (or in the two months following retirement if you worked into June but retired in May), you can actually REVOKE your retirement. You can also revoke your retirement by contracting too soon to return to work. If you revoke your retirement, you forfeit any benefits paid to you because you were not eligible for any benefits.

You are required to pay back all of your annuities, any PLSO or DROP payments, and health benefit payments made by TRS- Cont. on page 8 3 . Notice to retirees and beneficiaries about tax withholding preferences At the start of each calendar year TRS provides notice to retirees and beneficiaries who are receiving monthly payments to remind them that they can change their federal income tax withholding preferences. You are not required to change your withholding preference if you are satisfied with the amount currently being withheld. This article provides instruction on how to check your current withholding preference and how to change it only if you wish to do so. If you are satisfied with your current amount, you DO NOT need to take any action at all. If you wish to see your current withholding preference (such as married with one allowance) and your monthly withholding amount, you may do so through MyTRS on the TRS website. If you would like to estimate a new withholding amount, TRS has two withholding calculators: there is one inside MyTRS after you log in, which automatically imports the current annuity and withholding preferences from your TRS account. You can modify your marital status, the number of exemptions, and other deductions to estimate changes in your withholding.

There is also a generic income tax withholding estimate calculator on the TRS website that does not require you to log in to MyTRS, to estimate taxes. It does not import any data; you input all the data. If you wish to change your withholding preference, you may do so through MyTRS. Log into MyTRS and select Modify Withholding Preference.

You may also change your withholding preference by printing a copy of form TRS 228A from the TRS website. Go to the section for Retirees and Beneficiaries, then select Forms from the left-hand menu. Select the TRS 228A from the list, prepare, print and sign. For your convenience, a link to the current tax tables is provided within the form on the website. If you prefer, you may call TRS at 1-800-223-8778 to request a copy of the form TRS 228A through our automated telephone system.

Completed forms should be mailed to TRS at 1000 Red River St., Austin, TX 78701. Any new preference for the amount of withholding applies to future payments only; TRS cannot apply a new preference to any payment already made. TRS will withhold federal income tax on monthly annuity payments to retirees and beneficiaries unless you elect not to have withholding apply. You have the right to elect not to have withholding apply to your monthly payments from TRS. Your preference will remain in effect until you revoke it.

You may revoke a preference of no withholding at any time by following the instructions in this article. If you elect not to have with- holding apply to your TRS payments, or if you do not have enough federal income tax withheld from your TRS payments, you may be responsible for payment of estimated tax. You may incur penalties under the federal estimated tax rules if your withholding and estimated tax payments are not sufficient. Please note that if you are not a U.S. citizen or resident alien of the U.S., you may not elect not to have withholding apply to your TRS payments.

TRS is required to withhold 30 percent for federal income tax unless you qualify for benefits under a U.S. tax treaty. If so, you must notify TRS of your eligibility for reduced withholding or exemption from withholding and provide TRS with the required documentation. If you have questions regarding your tax withholding status, TRS suggests you contact a tax professional. TRS to conduct member satisfaction survey in spring 2016 Once every two years, TRS conducts a member satisfaction survey to learn how we can better serve our members and retirees.

While TRS is prohibited by law from advocating for legislative changes to member benefits, we strive to continuously improve how we deliver legislatively approved benefits to you. That means that we want your interactions with us to be timely, accurate and as convenient as possible whether you contact us by phone, visit our website, apply for benefits by mail, meet in person with a benefits counselor, receive information by mail or electronically, or attend a benefit presentation. Our 2016 member satisfaction survey will be conducted between late February and April. If you are asked to participate, please do so because your input is valuable in helping us better serve you. 4 .

TRS annual statements mailed to active members TRS mailed annual statements to active TRS members in October. These statements contain information pertaining to the recently completed 2014-15 school year as well as information regarding the total accumulated contributions in your member account and the amount of service credit recognized by TRS. Review your statement carefully. MISSING ONE MONTH OF SALARY. A TRS rule change adopted in December 2014 may affect the amount of compensation you see reflected on your annual statement for 2014-15. The rule change requires reporting entities to report compensation to TRS in the month in which it is paid instead of the month in which it was earned.

This change took effect Sept. 1, 2015 and was needed to standardize how compensation is reported to TRS by all employers. If your employer previously reported compensation to TRS in the month it was earned, the shift to reporting compensation to TRS in the month it is paid could cause you to have one month in the 2014-15 school year in which no compensation was reported to TRS. If your employer made this change, you may notice on your annual statement that your compensation for the 2014-15 school year does not include 12 months of compensation.

In such a situation, it is most likely the compensation for August 2015 that is not included in your salary for the 2014-15 school year. Rather, the compensation for August 2015 was reported in September 2015 and will be reflected in the annual statement for the 2015-16 school year. If the 2014-15 school year is short one month of compensation due to the change in employer reporting requirement AND the 2014-15 school year would be one of your highest years of compensation TRS uses to calculate your benefit or benefit estimate, TRS will attribute an additional month of compensation to you in the 2014-15 school year for benefit calculation purposes. The amount of compensation that TRS will attribute for the 2014-15 school year will not be reflected on your annual statement.

The amount of compensation that TRS will attribute for the missing month of salary is the amount of compensation that would have been reported for the missing month if the requirement to report compensation in the month it is paid was not in place and your employer reported the compensation earned in the missing month. If you are not retiring or the 2014-15 school year would not be in the salaries used to calculate your TRS benefit, TRS will not attribute an additional month of compensation to the 2014-15 school year. If you are missing compensation from the 2014-15 school year for any other reason, TRS will not attribute additional salary to the 2014-15 school year. If you have unreported service or compensation that is not due to the change in reporting requirements discussed previously, see below to learn how you may be able to receive credit for the unreported service and/or compensation without paying more than the member contributions due on the unreported amounts. MAY 31, 2016 DEADLINE FOR CORRECTING MISSING SERVICE CREDIT AND/OR COMPENSATION IN THE 2014-15 SCHOOL YEAR AT NO ADDITIONAL COST TO YOU.

If you rendered service and/or received compensation from a TRS-covered employer in the 2014-15 school year that is not reflected on your statement and the missing service credit and/or compensation is not due to the change in reporting requirements as described previously, please notify TRS immediately. If you are still working for the same employer and are due additional compensation from that employer, the error can be corrected in the current school year if you pay the member contributions that are due on the unreported service and/or compensation. You must notify TRS by May 31, 2016 of the error in order for the correction to be made by your employer in the current school year. An error cannot be corrected in this manner if you are no longer employed by the same employer or there is no additional compensation due to you from that employer in the current year.

If the error is not corrected in the current school year, you can still purchase the unreported service and/or compensation if it is verified to TRS by the end of the fifth school year after the school year in which the service was rendered or the compensation was paid. However, the cost to purchase the service credit and/or compensation credit increases significantly to the actuarial cost of the increased benefits associated with the unreported service and/ or compensation paid if the error is not corrected by the end of the school year following the school year in which the error was made. NOTE: ERRORS IN SERVICE CREDIT OR COMPENSATION FOR SCHOOL YEARS PRIOR TO AUG. 31, 2011 MUST BE VERIFIED BY AUG.

31, 2016, OR THE SERVICE CREDIT AND/OR COMPENSATION CREDIT CANNOT BE PURCHASED. RETIREMENT ESTIMATE MISSING OR DOES NOT INCLUDE CORRECT COMPENSATION. If you met age and service requirements for retirement, your annual statement included an unaudited estimate of your retirement benefits. However, if you received an estimate prepared by TRS within the previous 12 months, you may not have received an estimate on your statement.

If your statement does not include an estimate of your retirement benefits, you may find it helpful to visit the TRS website and use the Retirement Estimate Calculator in creating your own retirement estimate. The calculator is featured in the MyTRS portion of the website. You can register for MyTRS via the TRS website at www.trs.texas.gov.

Click on the MyTRS link under “Quicklinks” on the right-hand side of the home page and follow the instructions for registering. Cont. on page 8 5 . Important deadlines for verification of unreported service and unreported compensation and service reported by your employer but not credited on your annual statement Changes to TRS laws that took effect on Sept. 1, 2011, established a new five-year time limit for you to notify TRS and provide verification to TRS of service reported to TRS but not credited on your annual statement, and to provide verification to TRS of any unreported service, unreported compensation, and substitute service that you may wish to purchase for service credit. All unreported service rendered prior to Sept. 1, 2011, unreported compensation paid prior to Sept.

1, 2011, and any service not credited on your annual statement for the fiscal year that ended Aug. 31, 2011, must be verified no later than Aug. 31, 2016.

Unreported service, unreported compensation, substitute service, and service that was reported by your employer but not credited on your annual statement that is not verified within the required timeframe will not be eligible for purchase or credit and cannot be used to determine eligibility for, or the amount of, any of your benefits. year, you may be able to correct the error without paying more than the member contributions that would have been due but you must notify TRS by May 31, 2016. If you are still employed with the same employer and you have additional compensation that is due to you, your employer may request a waiver of the reporting deadline and submit the corrected reports reflecting your missing service and/or compensation. Your member contributions must be paid with pre-tax dollars in the same manner that they are paid each payday.

That is why it is important that you are still due compensation by the same employer. If you can’t correct the error in this manner or you miss the deadline for correcting an error that occurred in the prior year, you may still verify the unreported service and/or compensation by the end of the fifth school year following the school year in which the error occurred and purchase the additional service and/or compensation at a significantly higher, actuarial cost. PRIOR SCHOOL YEAR ERROR. If the unreported service was rendered or the unreported compensation was paid in the 2014-15 school Cont.

on page 7 2015 Annual Financial Report now on TRS website In November, TRS published its 2015 Comprehensive Annual Financial Report. The report may be found on the What’s New page and Publications page of the TRS website at www.trs.texas.gov. In early 2016, TRS will also publish a supplement to the report that will provide additional information regarding important developments involving the TRS retirement plan during the past year. You will be able to view the supplement on our website in early 2016 or, if you prefer, TRS can notify you by email when it has been posted 6 to our website.

If you prefer to receive an email notification, you must register for the MyTRS Email Subscription list named “Other Publications.” To enroll in MyTRS Email Subscriptions, log in to MyTRS. If you are already registered to use MyTRS, simply log in, select MyTRS Email Subscriptions and follow the instructions. If you are not yet a MyTRS registered user, simply register and then select MyTRS Email Subscriptions when you are in MyTRS. Information on MyTRS is on the right-hand side of the TRS website’s home page. As part of your registration for MyTRS, you provide TRS your email address.

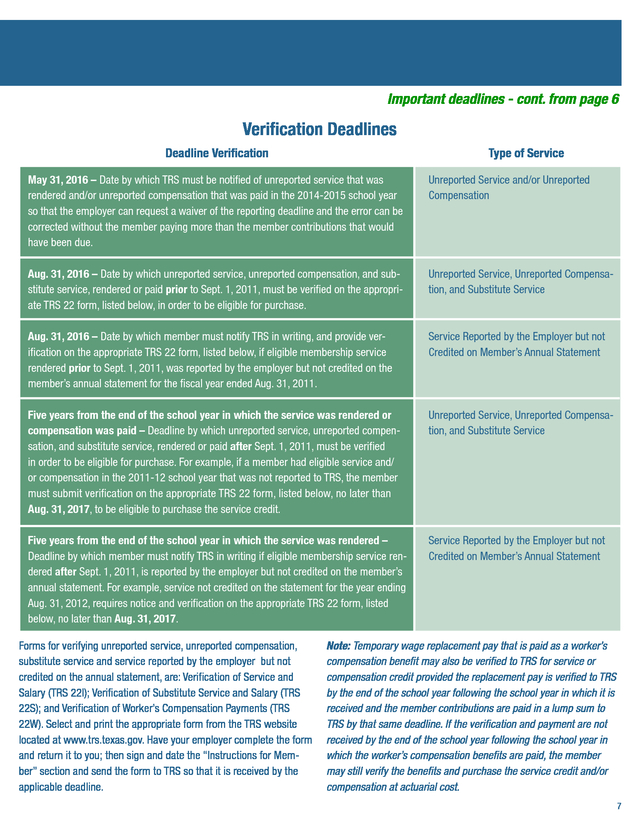

When you enroll in MyTRS Email Subscriptions, TRS uses the email address you provided to send you communications about your TRS benefits and related news. Once you have enrolled in MyTRS Email Subscriptions, you should receive an email message from TRS within a short time asking you to “activate” the email address by clicking a link within the message and following the directions that appear on the screen to complete your enrollment in the subscription service. . Important deadlines - cont. from page 6 Verification Deadlines Deadline Verification Type of Service May 31, 2016 – Date by which TRS must be notified of unreported service that was rendered and/or unreported compensation that was paid in the 2014-2015 school year so that the employer can request a waiver of the reporting deadline and the error can be corrected without the member paying more than the member contributions that would have been due. Unreported Service and/or Unreported Compensation Aug. 31, 2016 – Date by which unreported service, unreported compensation, and substitute service, rendered or paid prior to Sept. 1, 2011, must be verified on the appropriate TRS 22 form, listed below, in order to be eligible for purchase. Unreported Service, Unreported Compensation, and Substitute Service Aug.

31, 2016 – Date by which member must notify TRS in writing, and provide verification on the appropriate TRS 22 form, listed below, if eligible membership service rendered prior to Sept. 1, 2011, was reported by the employer but not credited on the member’s annual statement for the fiscal year ended Aug. 31, 2011. Service Reported by the Employer but not Credited on Member’s Annual Statement Five years from the end of the school year in which the service was rendered or compensation was paid – Deadline by which unreported service, unreported compensation, and substitute service, rendered or paid after Sept.

1, 2011, must be verified in order to be eligible for purchase. For example, if a member had eligible service and/ or compensation in the 2011-12 school year that was not reported to TRS, the member must submit verification on the appropriate TRS 22 form, listed below, no later than Aug. 31, 2017, to be eligible to purchase the service credit. Unreported Service, Unreported Compensation, and Substitute Service Five years from the end of the school year in which the service was rendered – Deadline by which member must notify TRS in writing if eligible membership service rendered after Sept.

1, 2011, is reported by the employer but not credited on the member’s annual statement. For example, service not credited on the statement for the year ending Aug. 31, 2012, requires notice and verification on the appropriate TRS 22 form, listed below, no later than Aug.

31, 2017. Service Reported by the Employer but not Credited on Member’s Annual Statement Forms for verifying unreported service, unreported compensation, substitute service and service reported by the employer but not credited on the annual statement, are: Verification of Service and Salary (TRS 22I); Verification of Substitute Service and Salary (TRS 22S); and Verification of Worker’s Compensation Payments (TRS 22W). Select and print the appropriate form from the TRS website located at www.trs.texas.gov. Have your employer complete the form and return it to you; then sign and date the “Instructions for Member” section and send the form to TRS so that it is received by the applicable deadline. Note: Temporary wage replacement pay that is paid as a worker’s compensation benefit may also be verified to TRS for service or compensation credit provided the replacement pay is verified to TRS by the end of the school year following the school year in which it is received and the member contributions are paid in a lump sum to TRS by that same deadline.

If the verification and payment are not received by the end of the school year following the school year in which the worker’s compensation benefits are paid, the member may still verify the benefits and purchase the service credit and/or compensation at actuarial cost. 7 . TRS TEACHER RETIREMENT SYSTEM OF TEXAS PRSRT STD U.S. POSTAGE PAID Austin, Texas PERMIT # 2603 1000 Red River Street Austin, Texas 78701-2698 CHANGE SERVICE REQUESTED TRS annual statements - cont. from page 5 If your annual statement included an estimate but your employer’s report to TRS for September had not been received at the time the estimate was prepared, your compensation for the 2014-15 school year may not have been used in the estimate or, if it was used, it may have only included 11 months of salary due to the change in reporting requirements addressed previously. If this occurred, future retirement estimates will include the additional month of salary attributed to the 2014-15 school year, or you may contact TRS for a current estimate. criteria, which took effect Sept.

1, 2014. However, the changes only affect members who did not have at least five years of service credit on Aug. 31, 2014, those persons who become members of TRS on or after Sept.

1, 2014, or members who had five years of service credit, terminate TRS membership by withdrawal of accumulated contributions on or after Sept. 1, 2014, and then later resume membership. For answers to frequently asked questions on annual statements, please visit www.trs.texas.gov. NO ANNUAL STATEMENT. If you became a new member of TRS or recently returned to TRS-covered employment after the end of the 2014-15 school year, you will not receive an annual statement until the fall of 2016.

When you receive your annual statement, please review it carefully and promptly notify TRS if your records are inconsistent with the reported compensation or number of years of service credit shown on your statement Employment after retirement - cont. from page 3 More information about service credit and/or compensation verification deadlines is included in the article titled “Important deadlines for verification of unreported service and service reported but not credited on your annual statement” on pages six and seven of this TRS News issue. Avoid jeopardizing your retirement benefit or forfeiting annuity payments and any health benefits paid on your behalf by TRS-Care. Know the facts – there are different limitations on full-time employment, substitute work and half-time employment. It is important that you review your annual statements carefully. In 2013, the Texas Legislature made changes to retirement eligibility 8 Care on your behalf or on behalf of your dependents.

If you can’t pay back the amount owed, TRS must permanently reduce your monthly benefit by an actuarially reduction to cover the benefits you were not eligible to receive. All of these situations and more are covered in the brochure. If you have questions about your individual situation after you read the Employment After Retirement brochure, please call TRS at 1-800-223-8778 and speak to a benefit counselor. .

The Town Hall meeting provided both an update for our members as well as a forum to listen to ideas regarding possible solutions,” said TRS Executive Director Brian Guthrie. “It was an outstanding day of information. We are looking forward to working with our members and stakeholders to prepare for the next legislative session on some of the issues and challenges discussed.” Panel discussions during the day featured national health care experts speaking on topics such as the health care market and the context in which TRS plans operate.

Strategies for cost containment in health care as well as the history, structure and financial status of TRSCare and TRS-ActiveCare were also discussed. Board meeting webcasts are available on the TRS website. To view the October town hall meeting, visit the TRS website which is located at www.trs.texas.gov. Click on the “General Information” tab, select “Board of Trustees” on the left side of your screen, select TRS Board Meeting Webcasts, and choose the October 22 board meeting to access the webcast. TRS website to feature new TRS Benefits Handbook in December TRS will publish an updated version of the TRS Benefits Handbook in December, including changes in the law enacted by the 84th Texas Legislature and amendments to plan rules adopted by the TRS Board of Trustees.

While handbooks are mailed only upon request, members and retirees can view and print a copy of the handbook by visiting the TRS website which is located at www.trs.texas.gov. You can also receive a notice when the new handbook is available by signing up for email subscriptions on the MyTRS section of the website. This year’s handbook provides information about a new rule amendment that may impact future retirees. Beginning with the 2015-16 school year, annual compensation for the school year in which you retire will be the highest total of compensation received during a 12-consecutive-month period that occurs during a 14-consecutivemonth period and meets eight specific requirements, including the requirement that the period begins no earlier than the first month of your qualified contract period.

(To view these provisions, see the section titled “Determining Annual Compensation.”) This rule change is not retroactive for retirements or deaths prior to the 2015-16 school year. . MEMBERS FROM MEMO TO Executive Director Brian K. Guthrie As you read this final TRS News issue of 2015, we hope you are able to take time off to enjoy the holidays, look back upon the past year and have an even better one in the year to come. We at TRS are also looking back upon 2015 -- and laying the groundwork for initiatives to better serve you in the coming year. During the past year, TRS named three new chief officers – Chief Information Officer Chris Cutler, Chief Benefit Officer Barbie Pearson and Chief Health Care Officer Katrina Daniel. We also made other organizational changes to better position us to focus on our key challenges moving forward: health care fund solvency, pension trust fund sustainability, long-term investment returns, and replacing legacy technology systems. Thanks to the hard work and dedication of our employees, TRS was also named a “Top Workplace” by the Austin American-Statesman for the fourth year in a row. For the 12-month period ending Aug.

31, 2015, the TRS portfolio had a return of -0.3 percent during a challenging year for all investors. However, our 2015 return surpassed the fund’s benchmark by 0.5 percent. For the past 10 years, our time-weighted compound annual return has been 6.2 percent.

On a three-year annualized basis, your fund has returned 8.3 percent, which is 1 percent above its benchmark. Annual rates of return for the five- and 10-year periods ending Aug. 31, 2015 were 9.6 percent and 6.2 percent, respectively. As of Aug.

31, 2015, the system had a funded ratio of 80.2 percent with an Unfunded Actuarial Accrued Liability of $33 billion. The system is now deferring net investment losses of $4.9 billion. The time necessary to amortize the unfunded liability R.

DAVID KELLY, Chair, Plano has also increased NANETTE SISSNEY, Vice Chair, Whitesboro from 29.8 years TODD BARTH, Houston to 33.3 years. Our KAREN CHARLESTON, Houston actuary estimates that JOE COLONNETTA, Dallas our unfunded liability DAVID CORPUS, Humble Board of Trustees CHRISTOPHER MOSS, Lufkin ANITA PALMER, Jacksboro DOLORES RAMIREZ, San Benito BRIAN K. GUTHRIE, Executive Director 2 and the funding period will both continue to increase over the next few years before beginning to once again decline. This newsletter includes articles on several important topics, including a town hall meeting conducted this fall to discuss the affordability of TRS-Care and sustainability of TRS-ActiveCare.

These same challenges will be studied by a joint interim committee created by the 84th Texas Legislature, and TRS will support the committee’s work to address these issues. Other topics include accessing 1099-R forms electronically, employment after retirement, federal income tax withholding preferences, TRS service and compensation deadlines, and our latest videos on 2015 TRS-related legislation and financial education. This past fall, Texas school children in K-5th grades participated in a TRS art contest where they submitted artwork depicting their teachers as superheroes. More than 3,500 art entries were received! The first place winner was Natalie Martinez of Clark Elementary, Laredo.

Stephanie Garces of San Antonio’s Roosevelt Elementary came in second, and Joi Speck of Live Oak Learning Center, Rockport, placed third. Liliana Hale of Ramirez Elementary, Lubbock, also received an honorable mention. I am amazed at how good these drawings are, and I think you will be too.

Please take a moment to view the winning art work and all the other great entries at www.trs.texas.gov. We invite you to stay current about your retirement system by visiting our website, TRS News is published by Teacher Retirement System of Texas reading our newsletters and following us on 1000 Red River Street Facebook and Twitter. In the meantime, all of Austin, Texas 78701-2698 us at TRS wish you and your families the (512) 542-6400 or 1-800-223-8778 happiest of holidays and all the best in 2016. www.trs.texas.gov The Teacher Retirement System of Texas does not discriminate on the basis of race, color, national origin, sex, religion, age or disability in employment or the provision of services. A copy of the complete TRS plan is available at the above address during regular business hours. .

New website videos feature updates on health care programs, 2015 legislation, financial education Three new videos are now available on the TRS website, which offer members, retirees and others updated news on TRS operations. The videos, produced by TRS’ Communications Department, are part of the series called “TRS Today.” One video features an interview with Chief Health Care Officer Katrina Daniel titled “Status of TRS-ActiveCare and TRS-Care” where Daniel talks about issues affecting both health benefits programs. In a second video titled “2015 TRS-Related Legislation,” Executive Director Brian Guthrie walks us through legislation impacting TRS that was passed during the 84th legislative session, including information regarding TRS-Care funding. In a third video, Guthrie explains financial education options available to members.

He also shares how TRS is launching a financial awareness program to help members identify the important questions to consider before retirement. The videos provide information on various topics, including estimating your TRS annuity, Social Security considerations related to TRS benefits, the impact of compounding interest, the TRS 403(b) certification program, and more. The videos on health care programs, 2015 legislation and financial education are approximately six-to-10 minutes long and are available through TRS.TV on the TRS website (www.trs.texas.gov). From the TRS home page, select the “Watch TRS Today Videos” link near the bottom of the column on the right side of your screen. Access next year’s 1099-R forms quickly and easily online In late January 2016, TRS will send 1099-R forms to those who have received one or more payments from TRS during calendar year 2015. The 1099-R is an Internal Revenue Service form that the recipient uses to report any distributions paid by TRS during the prior calendar year. or by fax.

The duplicate copies must be mailed. However, retirees and payment beneficiaries who have a MyTRS password can view and print a copy of their 1099-R forms, even before forms are mailed in January. As a reminder, recent legislation changed the annuity payment date to the last day of the month beginning with the September payment. This payment date change will result in annuitants receiving 13 annuity payments during calendar year 2015 and may affect the amount of federal income tax that you owe for this calendar year. If you subscribe now on MyTRS, you can have TRS send you an email message to notify you as soon as your 1099-R form is posted online. If you haven’t registered yet for MyTRS, doing so is easy. Simply go to the TRS website at www.trs.texas.gov and click on the MyTRS link under “Quicklinks” on the right-hand side of the home page.

Follow the instructions from there. From the time this form is distributed in January until April 15, TRS receives numerous requests for duplicate copies. Due to confidentiality requirements, TRS cannot provide the information over the phone Note: Individuals who receive payments from the TRS excess benefit arrangement will receive a W-2 form from TRS for the amounts paid out of the excess benefit fund during the 2015 calendar year. Are you a retiree considering employment after retirement? If you are retired or planning to retire and you are considering employment with a TRS-covered employer after you retire, take some time to review the Employment After Retirement brochure on the TRS website. TRS laws and rules that pertain to working for a TRS-covered employer are different based on the date you retired and whether or not you are retired under Service Retirement or Disability Retirement. If you work more than allowed, you will lose your annuity for each month that you exceed the limits.

If you go back to work – any kind of work, even working as a substitute – for a TRS-covered employer in the calendar month following your retirement (or in the two months following retirement if you worked into June but retired in May), you can actually REVOKE your retirement. You can also revoke your retirement by contracting too soon to return to work. If you revoke your retirement, you forfeit any benefits paid to you because you were not eligible for any benefits.

You are required to pay back all of your annuities, any PLSO or DROP payments, and health benefit payments made by TRS- Cont. on page 8 3 . Notice to retirees and beneficiaries about tax withholding preferences At the start of each calendar year TRS provides notice to retirees and beneficiaries who are receiving monthly payments to remind them that they can change their federal income tax withholding preferences. You are not required to change your withholding preference if you are satisfied with the amount currently being withheld. This article provides instruction on how to check your current withholding preference and how to change it only if you wish to do so. If you are satisfied with your current amount, you DO NOT need to take any action at all. If you wish to see your current withholding preference (such as married with one allowance) and your monthly withholding amount, you may do so through MyTRS on the TRS website. If you would like to estimate a new withholding amount, TRS has two withholding calculators: there is one inside MyTRS after you log in, which automatically imports the current annuity and withholding preferences from your TRS account. You can modify your marital status, the number of exemptions, and other deductions to estimate changes in your withholding.

There is also a generic income tax withholding estimate calculator on the TRS website that does not require you to log in to MyTRS, to estimate taxes. It does not import any data; you input all the data. If you wish to change your withholding preference, you may do so through MyTRS. Log into MyTRS and select Modify Withholding Preference.

You may also change your withholding preference by printing a copy of form TRS 228A from the TRS website. Go to the section for Retirees and Beneficiaries, then select Forms from the left-hand menu. Select the TRS 228A from the list, prepare, print and sign. For your convenience, a link to the current tax tables is provided within the form on the website. If you prefer, you may call TRS at 1-800-223-8778 to request a copy of the form TRS 228A through our automated telephone system.

Completed forms should be mailed to TRS at 1000 Red River St., Austin, TX 78701. Any new preference for the amount of withholding applies to future payments only; TRS cannot apply a new preference to any payment already made. TRS will withhold federal income tax on monthly annuity payments to retirees and beneficiaries unless you elect not to have withholding apply. You have the right to elect not to have withholding apply to your monthly payments from TRS. Your preference will remain in effect until you revoke it.

You may revoke a preference of no withholding at any time by following the instructions in this article. If you elect not to have with- holding apply to your TRS payments, or if you do not have enough federal income tax withheld from your TRS payments, you may be responsible for payment of estimated tax. You may incur penalties under the federal estimated tax rules if your withholding and estimated tax payments are not sufficient. Please note that if you are not a U.S. citizen or resident alien of the U.S., you may not elect not to have withholding apply to your TRS payments.

TRS is required to withhold 30 percent for federal income tax unless you qualify for benefits under a U.S. tax treaty. If so, you must notify TRS of your eligibility for reduced withholding or exemption from withholding and provide TRS with the required documentation. If you have questions regarding your tax withholding status, TRS suggests you contact a tax professional. TRS to conduct member satisfaction survey in spring 2016 Once every two years, TRS conducts a member satisfaction survey to learn how we can better serve our members and retirees.

While TRS is prohibited by law from advocating for legislative changes to member benefits, we strive to continuously improve how we deliver legislatively approved benefits to you. That means that we want your interactions with us to be timely, accurate and as convenient as possible whether you contact us by phone, visit our website, apply for benefits by mail, meet in person with a benefits counselor, receive information by mail or electronically, or attend a benefit presentation. Our 2016 member satisfaction survey will be conducted between late February and April. If you are asked to participate, please do so because your input is valuable in helping us better serve you. 4 .

TRS annual statements mailed to active members TRS mailed annual statements to active TRS members in October. These statements contain information pertaining to the recently completed 2014-15 school year as well as information regarding the total accumulated contributions in your member account and the amount of service credit recognized by TRS. Review your statement carefully. MISSING ONE MONTH OF SALARY. A TRS rule change adopted in December 2014 may affect the amount of compensation you see reflected on your annual statement for 2014-15. The rule change requires reporting entities to report compensation to TRS in the month in which it is paid instead of the month in which it was earned.

This change took effect Sept. 1, 2015 and was needed to standardize how compensation is reported to TRS by all employers. If your employer previously reported compensation to TRS in the month it was earned, the shift to reporting compensation to TRS in the month it is paid could cause you to have one month in the 2014-15 school year in which no compensation was reported to TRS. If your employer made this change, you may notice on your annual statement that your compensation for the 2014-15 school year does not include 12 months of compensation.

In such a situation, it is most likely the compensation for August 2015 that is not included in your salary for the 2014-15 school year. Rather, the compensation for August 2015 was reported in September 2015 and will be reflected in the annual statement for the 2015-16 school year. If the 2014-15 school year is short one month of compensation due to the change in employer reporting requirement AND the 2014-15 school year would be one of your highest years of compensation TRS uses to calculate your benefit or benefit estimate, TRS will attribute an additional month of compensation to you in the 2014-15 school year for benefit calculation purposes. The amount of compensation that TRS will attribute for the 2014-15 school year will not be reflected on your annual statement.

The amount of compensation that TRS will attribute for the missing month of salary is the amount of compensation that would have been reported for the missing month if the requirement to report compensation in the month it is paid was not in place and your employer reported the compensation earned in the missing month. If you are not retiring or the 2014-15 school year would not be in the salaries used to calculate your TRS benefit, TRS will not attribute an additional month of compensation to the 2014-15 school year. If you are missing compensation from the 2014-15 school year for any other reason, TRS will not attribute additional salary to the 2014-15 school year. If you have unreported service or compensation that is not due to the change in reporting requirements discussed previously, see below to learn how you may be able to receive credit for the unreported service and/or compensation without paying more than the member contributions due on the unreported amounts. MAY 31, 2016 DEADLINE FOR CORRECTING MISSING SERVICE CREDIT AND/OR COMPENSATION IN THE 2014-15 SCHOOL YEAR AT NO ADDITIONAL COST TO YOU.

If you rendered service and/or received compensation from a TRS-covered employer in the 2014-15 school year that is not reflected on your statement and the missing service credit and/or compensation is not due to the change in reporting requirements as described previously, please notify TRS immediately. If you are still working for the same employer and are due additional compensation from that employer, the error can be corrected in the current school year if you pay the member contributions that are due on the unreported service and/or compensation. You must notify TRS by May 31, 2016 of the error in order for the correction to be made by your employer in the current school year. An error cannot be corrected in this manner if you are no longer employed by the same employer or there is no additional compensation due to you from that employer in the current year.

If the error is not corrected in the current school year, you can still purchase the unreported service and/or compensation if it is verified to TRS by the end of the fifth school year after the school year in which the service was rendered or the compensation was paid. However, the cost to purchase the service credit and/or compensation credit increases significantly to the actuarial cost of the increased benefits associated with the unreported service and/ or compensation paid if the error is not corrected by the end of the school year following the school year in which the error was made. NOTE: ERRORS IN SERVICE CREDIT OR COMPENSATION FOR SCHOOL YEARS PRIOR TO AUG. 31, 2011 MUST BE VERIFIED BY AUG.

31, 2016, OR THE SERVICE CREDIT AND/OR COMPENSATION CREDIT CANNOT BE PURCHASED. RETIREMENT ESTIMATE MISSING OR DOES NOT INCLUDE CORRECT COMPENSATION. If you met age and service requirements for retirement, your annual statement included an unaudited estimate of your retirement benefits. However, if you received an estimate prepared by TRS within the previous 12 months, you may not have received an estimate on your statement.

If your statement does not include an estimate of your retirement benefits, you may find it helpful to visit the TRS website and use the Retirement Estimate Calculator in creating your own retirement estimate. The calculator is featured in the MyTRS portion of the website. You can register for MyTRS via the TRS website at www.trs.texas.gov.

Click on the MyTRS link under “Quicklinks” on the right-hand side of the home page and follow the instructions for registering. Cont. on page 8 5 . Important deadlines for verification of unreported service and unreported compensation and service reported by your employer but not credited on your annual statement Changes to TRS laws that took effect on Sept. 1, 2011, established a new five-year time limit for you to notify TRS and provide verification to TRS of service reported to TRS but not credited on your annual statement, and to provide verification to TRS of any unreported service, unreported compensation, and substitute service that you may wish to purchase for service credit. All unreported service rendered prior to Sept. 1, 2011, unreported compensation paid prior to Sept.

1, 2011, and any service not credited on your annual statement for the fiscal year that ended Aug. 31, 2011, must be verified no later than Aug. 31, 2016.

Unreported service, unreported compensation, substitute service, and service that was reported by your employer but not credited on your annual statement that is not verified within the required timeframe will not be eligible for purchase or credit and cannot be used to determine eligibility for, or the amount of, any of your benefits. year, you may be able to correct the error without paying more than the member contributions that would have been due but you must notify TRS by May 31, 2016. If you are still employed with the same employer and you have additional compensation that is due to you, your employer may request a waiver of the reporting deadline and submit the corrected reports reflecting your missing service and/or compensation. Your member contributions must be paid with pre-tax dollars in the same manner that they are paid each payday.

That is why it is important that you are still due compensation by the same employer. If you can’t correct the error in this manner or you miss the deadline for correcting an error that occurred in the prior year, you may still verify the unreported service and/or compensation by the end of the fifth school year following the school year in which the error occurred and purchase the additional service and/or compensation at a significantly higher, actuarial cost. PRIOR SCHOOL YEAR ERROR. If the unreported service was rendered or the unreported compensation was paid in the 2014-15 school Cont.

on page 7 2015 Annual Financial Report now on TRS website In November, TRS published its 2015 Comprehensive Annual Financial Report. The report may be found on the What’s New page and Publications page of the TRS website at www.trs.texas.gov. In early 2016, TRS will also publish a supplement to the report that will provide additional information regarding important developments involving the TRS retirement plan during the past year. You will be able to view the supplement on our website in early 2016 or, if you prefer, TRS can notify you by email when it has been posted 6 to our website.

If you prefer to receive an email notification, you must register for the MyTRS Email Subscription list named “Other Publications.” To enroll in MyTRS Email Subscriptions, log in to MyTRS. If you are already registered to use MyTRS, simply log in, select MyTRS Email Subscriptions and follow the instructions. If you are not yet a MyTRS registered user, simply register and then select MyTRS Email Subscriptions when you are in MyTRS. Information on MyTRS is on the right-hand side of the TRS website’s home page. As part of your registration for MyTRS, you provide TRS your email address.

When you enroll in MyTRS Email Subscriptions, TRS uses the email address you provided to send you communications about your TRS benefits and related news. Once you have enrolled in MyTRS Email Subscriptions, you should receive an email message from TRS within a short time asking you to “activate” the email address by clicking a link within the message and following the directions that appear on the screen to complete your enrollment in the subscription service. . Important deadlines - cont. from page 6 Verification Deadlines Deadline Verification Type of Service May 31, 2016 – Date by which TRS must be notified of unreported service that was rendered and/or unreported compensation that was paid in the 2014-2015 school year so that the employer can request a waiver of the reporting deadline and the error can be corrected without the member paying more than the member contributions that would have been due. Unreported Service and/or Unreported Compensation Aug. 31, 2016 – Date by which unreported service, unreported compensation, and substitute service, rendered or paid prior to Sept. 1, 2011, must be verified on the appropriate TRS 22 form, listed below, in order to be eligible for purchase. Unreported Service, Unreported Compensation, and Substitute Service Aug.

31, 2016 – Date by which member must notify TRS in writing, and provide verification on the appropriate TRS 22 form, listed below, if eligible membership service rendered prior to Sept. 1, 2011, was reported by the employer but not credited on the member’s annual statement for the fiscal year ended Aug. 31, 2011. Service Reported by the Employer but not Credited on Member’s Annual Statement Five years from the end of the school year in which the service was rendered or compensation was paid – Deadline by which unreported service, unreported compensation, and substitute service, rendered or paid after Sept.

1, 2011, must be verified in order to be eligible for purchase. For example, if a member had eligible service and/ or compensation in the 2011-12 school year that was not reported to TRS, the member must submit verification on the appropriate TRS 22 form, listed below, no later than Aug. 31, 2017, to be eligible to purchase the service credit. Unreported Service, Unreported Compensation, and Substitute Service Five years from the end of the school year in which the service was rendered – Deadline by which member must notify TRS in writing if eligible membership service rendered after Sept.

1, 2011, is reported by the employer but not credited on the member’s annual statement. For example, service not credited on the statement for the year ending Aug. 31, 2012, requires notice and verification on the appropriate TRS 22 form, listed below, no later than Aug.

31, 2017. Service Reported by the Employer but not Credited on Member’s Annual Statement Forms for verifying unreported service, unreported compensation, substitute service and service reported by the employer but not credited on the annual statement, are: Verification of Service and Salary (TRS 22I); Verification of Substitute Service and Salary (TRS 22S); and Verification of Worker’s Compensation Payments (TRS 22W). Select and print the appropriate form from the TRS website located at www.trs.texas.gov. Have your employer complete the form and return it to you; then sign and date the “Instructions for Member” section and send the form to TRS so that it is received by the applicable deadline. Note: Temporary wage replacement pay that is paid as a worker’s compensation benefit may also be verified to TRS for service or compensation credit provided the replacement pay is verified to TRS by the end of the school year following the school year in which it is received and the member contributions are paid in a lump sum to TRS by that same deadline.

If the verification and payment are not received by the end of the school year following the school year in which the worker’s compensation benefits are paid, the member may still verify the benefits and purchase the service credit and/or compensation at actuarial cost. 7 . TRS TEACHER RETIREMENT SYSTEM OF TEXAS PRSRT STD U.S. POSTAGE PAID Austin, Texas PERMIT # 2603 1000 Red River Street Austin, Texas 78701-2698 CHANGE SERVICE REQUESTED TRS annual statements - cont. from page 5 If your annual statement included an estimate but your employer’s report to TRS for September had not been received at the time the estimate was prepared, your compensation for the 2014-15 school year may not have been used in the estimate or, if it was used, it may have only included 11 months of salary due to the change in reporting requirements addressed previously. If this occurred, future retirement estimates will include the additional month of salary attributed to the 2014-15 school year, or you may contact TRS for a current estimate. criteria, which took effect Sept.

1, 2014. However, the changes only affect members who did not have at least five years of service credit on Aug. 31, 2014, those persons who become members of TRS on or after Sept.

1, 2014, or members who had five years of service credit, terminate TRS membership by withdrawal of accumulated contributions on or after Sept. 1, 2014, and then later resume membership. For answers to frequently asked questions on annual statements, please visit www.trs.texas.gov. NO ANNUAL STATEMENT. If you became a new member of TRS or recently returned to TRS-covered employment after the end of the 2014-15 school year, you will not receive an annual statement until the fall of 2016.

When you receive your annual statement, please review it carefully and promptly notify TRS if your records are inconsistent with the reported compensation or number of years of service credit shown on your statement Employment after retirement - cont. from page 3 More information about service credit and/or compensation verification deadlines is included in the article titled “Important deadlines for verification of unreported service and service reported but not credited on your annual statement” on pages six and seven of this TRS News issue. Avoid jeopardizing your retirement benefit or forfeiting annuity payments and any health benefits paid on your behalf by TRS-Care. Know the facts – there are different limitations on full-time employment, substitute work and half-time employment. It is important that you review your annual statements carefully. In 2013, the Texas Legislature made changes to retirement eligibility 8 Care on your behalf or on behalf of your dependents.

If you can’t pay back the amount owed, TRS must permanently reduce your monthly benefit by an actuarially reduction to cover the benefits you were not eligible to receive. All of these situations and more are covered in the brochure. If you have questions about your individual situation after you read the Employment After Retirement brochure, please call TRS at 1-800-223-8778 and speak to a benefit counselor. .