Description

Electricity Derivatives and Bank Guarantees

Geir Høidal Bjønnes and Jo Saakvitne

BI Norwegian Business School

1

. TABLE OF CONTENTS

1

Executive Summary ......................................................................................................................... 3

2

Introduction ..................................................................................................................................... 4

3

The market for energy derivatives .................................................................................................. 5

3.1

The Nordic energy market .......................................................................................................

7 4 Regulation of central clearing in energy derivatives markets ......................................................... 8 5 Central clearing in the nordic market.............................................................................................. 9 5.1 5.2 The use of bank guarantees and introduction of the DS futures ..........................................

12 5.3 Risk profile of bank guarantees ............................................................................................. 15 5.4 Systemic risk and central counterparties .............................................................................. 19 5.5 6 Overview of central clearing in the Nordic Market .................................................................

9 Systemic risk and bank guarantees ....................................................................................... 22 Likely impact of regulatory changes .............................................................................................. 23 6.1 Increased costs of hedging for industrial firms .....................................................................

23 6.2 Reduced hedging activity ...................................................................................................... 25 6.3 Non-financials move to indirect clearing members .............................................................. 25 6.4 Increased use of bilateral and physical contracts .................................................................

28 6.5 Impact on systemic risk ......................................................................................................... 28 7 Conclusions.................................................................................................................................... 31 8 Literature and references ..............................................................................................................

32 2 . 1 EXECUTIVE SUMMARY This report analyzes the use and risk of bank guarantees in the clearing of energy derivatives. In particular, we examine the systemic risk component of bank guarantees in central clearing, and the likely effects of an effective ban on the current use of bank guarantees. Our main conclusions are that  It is likely that the use of exchange-traded energy derivatives will decrease significantly if the current use of bank guarantees are disallowed.  We expect an increase in bilateral trading and physical hedging of energy prices. Systemic risk may increase, since o Bilateral markets are not subject to the same regulatory oversight as exchange-traded markets. o Bilateral trades are not necessarily cleared. o Transparency is much lower in bilateral markets.  Central counterparties face risk when accepting bank guarantees as margin collateral, as they do when accepting any other financial asset. However, we do not find that the bank guarantees used in energy markets today constitute a significant systemic risk factor. The main message from this report is that disallowing the current use of bank guarantees in energy markets, however well intended, may cause adverse consequences.

In addition, the benefits from imposing the regulation is likely to be small, if any. 3 . 2 INTRODUCTION This report is written on behalf of the Working Party on Bank Guarantees in European Energy Markets1, by associate professor Geir Høidal Bjønnes2 and Jo Saakvitne3. The aim and mandate of the report is to analyze whether the current use of bank guarantees, as they are used in energy markets today, poses any unacceptable systemic risk; and how any potential risk can be mitigated. Further, the report aims to examine likely scenarios if bank guarantees are not allowed as eligible collateral for nonfinancial participants in the power and gas market. The authors take full responsibility for any errors or omissions in the work. In this report, we put a special emphasis on the Nordic energy market. The Nordic energy market has been a success story, and influences other European markets, while at the same time it is particularly affected by the pending regulatory changes. Sections 3-4 in this report provide key background information, while sections 5-6 contain the bulk of the analysis.

In section 3, we describe energy markets, with a special emphasis on features separating them from other financial markets. We highlight why well-functioning energy derivatives markets yield valuable benefits to society. In section 4, we describe the key regulatory issues facing the market participants.

In section 5, we discuss risk from central clearing and bank guarantees. Section 6 discusses the likely impact of regulatory changes, while section 7 concludes. 1 The members of the Working Party are Nasdaq Commodities, Finnish Energy Industries, Confederation of Finnish Industries (EK), Energy Norway, Swedenenergy, Oberoende Elhandlare, The Nordic Association of Electricity Traders (NAET), Nord Pool Spot, and Dansk Energi. Beyond the Working Party, the project steering group also included the Finnish Ministry of Employment, the Finnish Ministry of Finance, the Iberian energy derivatives exchange (OMIP), the Iberian energy clearing house (OMIClear), and the Warsaw Commodity Clearing House (IRGIT). 2 3 BI Norwegian Business School BI Norwegian Business School and Fixed Point Consulting 4 .

3 THE MARKET FOR ENERGY DERIVATIVES In this section, we discuss key features of energy markets, with a special emphasis on what separates energy markets from other financial and commodities markets. We argue that well-functioning markets for energy derivatives ultimately lead to lower electricity prices and higher investments in the sector. Electricity production is capital-intensive and financial risk management is important for investments The business of producing, delivering and retailing electricity is complex. It requires capital-intensive investments and long-term financing, which gives financial risk management a crucial role in the determination of electricity prices and viability of investment projects. Electricity markets have several unique features, which are lacking in other financial and commodity markets. Firstly, electricity cannot be stored, and hence suppliers and consumers lack inventories. Therefore, the dynamics of derivative prices may behave differently than for instance oil price derivatives, where the underlying asset can be stored. Secondly, electricity markets have historically been geographically distinct.

Even today, moving power between regions may be economically or even physically unviable due to energy lost to resistance in the grid. In Europe, lack of cross-border transmission capacity is a hindrance to energy market integration (Nowak, 2010). This has led to fragmented and specialized derivative markets, and substantial price differences across regions. Figure 1: Large price differences in electricity prices in EU. Electricity markets are geographically distinct Source: Eurostat. Prices for 2500-5000 kWh, excluding taxes. 5 .

Figure 2: The five wide area electricity grids in Europe Electricity prices feature extreme variations, making hedging important for electricity suppliers and consumers Well-functioning financial derivatives markets lower the costs of hedging… … which in turn lowers electricity prices and increase investments Electricity prices also feature large variations. Part of this variation is due to strong seasonality in supply and demand over days, weeks and months. In addition, there is also the possibility of unexpected dramatic price changes over the very short term, caused by supply disturbances. These price changes manifest themselves in sudden upward jumps shortly followed by a rapid reversion to normal levels. These extreme spikes are a major concern for risk management of utilities, and imply an important role for financial derivatives (Geman, 2002, Carmona and Coulon, 2014).

The large variations in spot prices do not carry directly over to derivative prices. Due to the well-known Samuelson effect (Samuelson, 1965), the effects of spot market volatility on futures prices will decrease with time to delivery on the futures contract. The large spot price variations and non-storability of electricity have always prompted electricity suppliers to hedge their price risk by selling power with future delivery. Historically, energy markets have been in line with the classical Keynes-Hicks theory of “normal backwardation”, meaning that power producers have sold future power at a discount to spot prices in order to incentivize external capital to take on the producers’ risk of falling prices.

(Keynes 1930, Hicks 1939). A gradual reversal of this discount has taken place as standardized exchange-traded financial derivatives have allowed a broader investor base to participate in the risk sharing (Carmona and Coulon 2014, Bouchouev 2012). In general, reduced forward premiums caused by improved risk sharing are characteristics of efficient and well-functioning markets. When electricity producers can hedge their commercial risk, the uncertainty about returns to investments in the electrical power utilities sector decreases. This in turn decreases capital costs of 6 .

electricity investment projects, and ultimately leads to lower prices of electricity and increased investments. 3.1 THE NORDIC ENERGY MARKET This report has a special emphasis on the Nordic energy market The energy derivatives market of other parts of northern Europe is gradually moving towards the same structure as the Nordic market The Nordic market is exchange-traded and cleared by central counterparty (CCP) Multilateral and cleared markets have clear benefits in terms of risk and efficiency We will now examine the Nordic energy market in detail. This market has been a success story, and influences other European markets. At the same time, the market is particularly affected by the pending regulatory changes. Furthermore, the energy derivatives markets of other parts of northern Europe are gradually moving towards the same structure as the Nordic market.

Nasdaq Commodities lists, in addition to the Nordic market and Baltic electricity price area differential products, derivatives on electricity in the Netherlands, Germany and UK,. The Nordic market is of particular interest for three reasons. Firstly, the Nordic electricity power market is often held to be one of the most efficient, transparent and liquid electricity power markets in the world (Mork (2001), Bergman (2002, 2003), Amundsen and Bergman (2006)). Secondly, the Nordic market will be significantly affected by the regulatory changes at hand.

Thirdly, there is a trend in other European markets toward a structure similar to the one in the Nordic market. The Nordic electricity power market was deregulated in the mid 1990’s. The aim of the reform was to separate the production and sale of electricity from the transmission of electricity (the network operation). The reform led to active trading of spot electricity and derivatives by a large number of participants at the Nordic exchanges for electricity spot (currently Nord Pool Spot) and financial derivatives (currently Nasdaq Commodities).

Currently, members from around 20 countries are trading at the derivatives market at Nasdaq Commodities. Worldwide, only 40 per cent of outstanding commodities derivative contracts are exchange traded (BIS 2013, WFE 2013). Energy derivatives (not including oil) make up around 35 per cent of commodities contracts traded worldwide. It is therefore of particular interest that the Nordic energy market is to a large degree exchange traded, with trading centered on the Oslo-based Nasdaq Commodities exchange4.

Exchange traded markets are multilateral, meaning that multiple buying and selling interests may interact and contract in accordance with non-discretionary rules. This market 4 NASDAQ OMX Oslo ASA 7 . structure provides a wide range of benefits over an OTC structure, and it has been a major regulatory effort since the financial crisis to promote multilateral trading venues for financial derivatives. Multilateral markets provide transparency of prices and standardization of terms, and subsequently efficient price discovery, increased liquidity and decreased trading costs. 4 REGULATION OF CENTRAL CLEARING IN ENERGY DERIVATIVES MARKETS A major policy objective has been to move derivatives market to multilateral and cleared venues In September 2009, the G20 leaders meeting in Pittsburgh agreed that: “All standardized OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest.” In Europe, the European Market Infrastructure Regulation (EMIR) dictates the details of central clearing. Article 46 of EMIR allows nonfinancial clearing members to post bank guarantees as collateral for a) Derivatives relating to electricity or natural gas produced, traded or delivered in the Union b) Derivatives relating to the transportation of electricity or natural gas in the Union Pending regulatory changes will affect energy markets The European Securities and Markets Authority (ESMA) specifies the conditions for accepting bank guarantees in their technical standards. These standards specify, among other requirements, that commercial bank guarantees must be “fully backed by collateral”, a requirement that market participants claim, in practice, negates the use of commercial bank guarantees (European Association of CCP Clearing Houses, 2014). An exemption period was granted for commodity markets in 2013. This period will expire in March 2016. There is an ongoing initiative to make the exemption permanent, by policymakers, regulators and the energy industry.

During the legislative procedure in 2012, the four Nordic financial supervisory authorities (FSAs) requested in a letter to ESMA that the requirements prohibiting use of non-fully backed commercial bank guarantees be removed. In 2015, seven governments in the Nordic and Baltic region (Sweden, Denmark, Finland, Norway, Estonia, Latvia and Lithuania) urged the European Commission to reconsider the ban on non-fully backed commercial bank guarantees as collateral. 8 . The Working Party on Bank Guarantees in European Energy Markets, The Union of the Electricity Industry (Eurelectric), EACH (European Association of CCP), European Federation of Energy Traders (EFET) and Eurogas have also sent letters to the European Commission in which they urge the European Commission to reconsider the ban on non-fully backed commercial bank guarantees as collateral. 5 CENTRAL MARKET CLEARING IN THE NORDIC In this section, we discuss the details of central clearing with a special emphasis on the Nordic market. Furthermore, we analyze bank guarantees in central clearing. In the final subsection, we examine the important role of central counterparties in tackling systemic risk. 5.1 OVERVIEW OF CENTRAL CLEARING IN THE NORDIC MARKET A central counterparty (CCP) is an entity that interposes itself between counterparties to contracts traded in a financial or physical market, becoming the buyer to every seller and the seller to every buyer, thereby guaranteeing the performance of all contracts. Central counterparties provide significant risk-reducing benefits due to improved oversight of market participants and the coordinated management of open positions following the default of a market participant (Milne 2012, Wendt 2015). Following the financial crisis in 2008, a major regulatory effort has been focused on imposing mandatory central counterparty clearing in derivative markets. The participants in the energy market is primarily the suppliers and demanders of electricity The participants in the market for financial derivatives on Nordic power are primarily the suppliers and demanders of electricity (i.e. the producers and wholesale consumers).

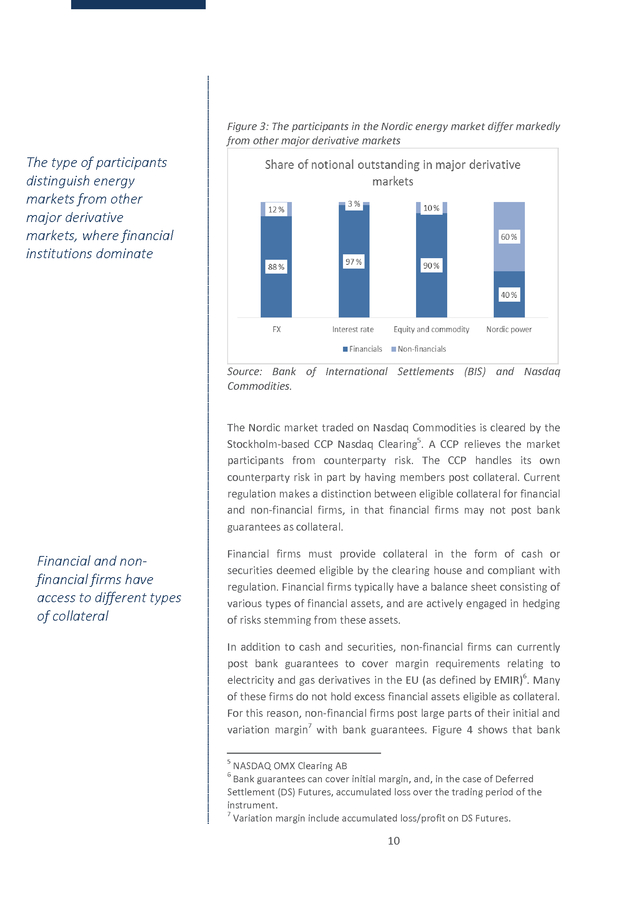

In this aspect the energy markets differ from financial markets in general, as participants in other financial markets to a large extent are banks, dealers and other financial institutions. This can be confirmed by a mere glance at figure 3. The figure show the relative share of financial versus nonfinancial firms, for major OTC derivatives markets and for the Nordic power market. 9 .

Figure 3: The participants in the Nordic energy market differ markedly from other major derivative markets The type of participants distinguish energy markets from other major derivative markets, where financial institutions dominate Source: Bank of International Settlements (BIS) and Nasdaq Commodities. The Nordic market traded on Nasdaq Commodities is cleared by the Stockholm-based CCP Nasdaq Clearing5. A CCP relieves the market participants from counterparty risk. The CCP handles its own counterparty risk in part by having members post collateral. Current regulation makes a distinction between eligible collateral for financial and non-financial firms, in that financial firms may not post bank guarantees as collateral. Financial and nonfinancial firms have access to different types of collateral Financial firms must provide collateral in the form of cash or securities deemed eligible by the clearing house and compliant with regulation.

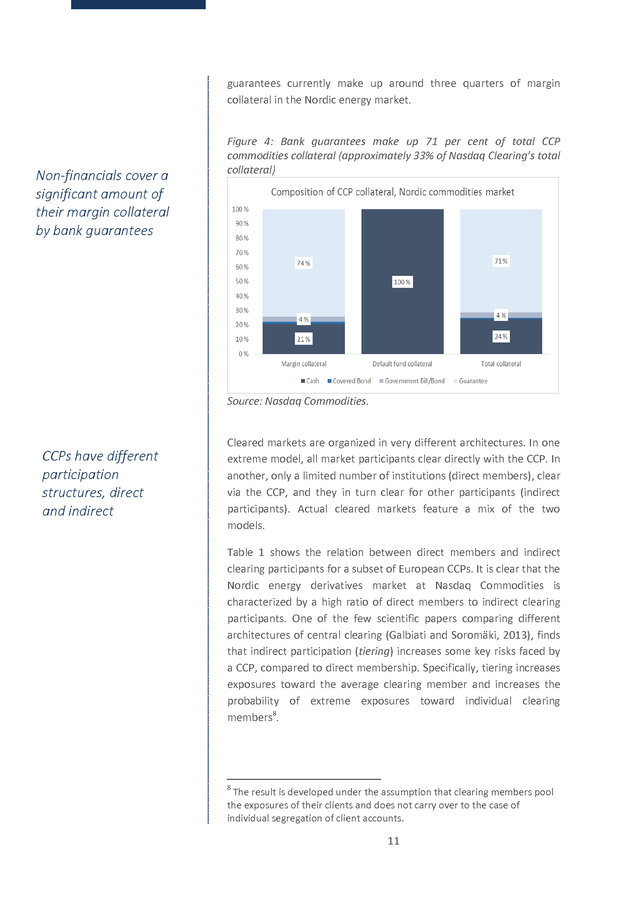

Financial firms typically have a balance sheet consisting of various types of financial assets, and are actively engaged in hedging of risks stemming from these assets. In addition to cash and securities, non-financial firms can currently post bank guarantees to cover margin requirements relating to electricity and gas derivatives in the EU (as defined by EMIR)6. Many of these firms do not hold excess financial assets eligible as collateral. For this reason, non-financial firms post large parts of their initial and variation margin7 with bank guarantees. Figure 4 shows that bank 5 NASDAQ OMX Clearing AB Bank guarantees can cover initial margin, and, in the case of Deferred Settlement (DS) Futures, accumulated loss over the trading period of the instrument. 7 Variation margin include accumulated loss/profit on DS Futures. 6 10 .

guarantees currently make up around three quarters of margin collateral in the Nordic energy market. Non-financials cover a significant amount of their margin collateral by bank guarantees Figure 4: Bank guarantees make up 71 per cent of total CCP commodities collateral (approximately 33% of Nasdaq Clearing’s total collateral) Source: Nasdaq Commodities. CCPs have different participation structures, direct and indirect Cleared markets are organized in very different architectures. In one extreme model, all market participants clear directly with the CCP. In another, only a limited number of institutions (direct members), clear via the CCP, and they in turn clear for other participants (indirect participants). Actual cleared markets feature a mix of the two models. Table 1 shows the relation between direct members and indirect clearing participants for a subset of European CCPs.

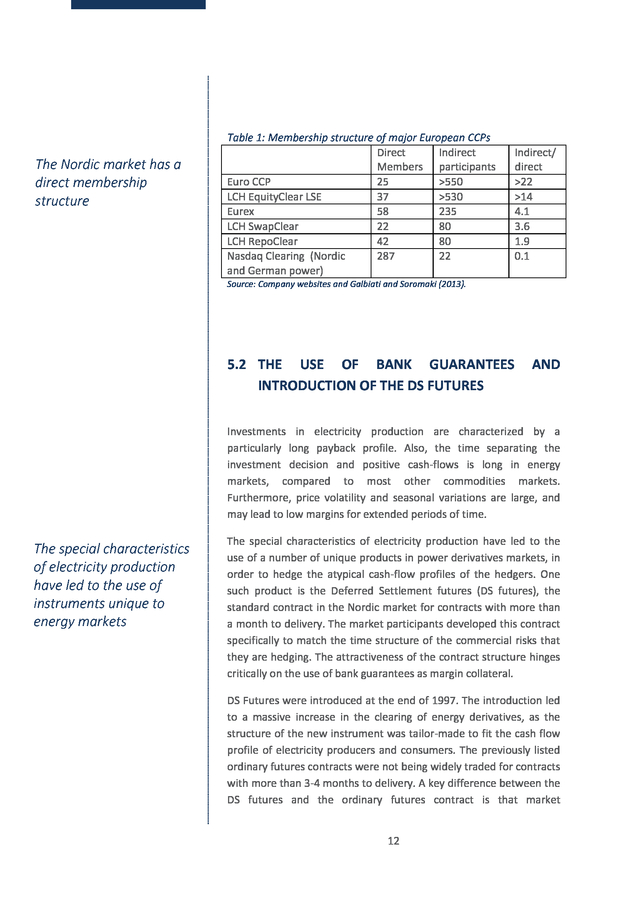

It is clear that the Nordic energy derivatives market at Nasdaq Commodities is characterized by a high ratio of direct members to indirect clearing participants. One of the few scientific papers comparing different architectures of central clearing (Galbiati and Soromäki, 2013), finds that indirect participation (tiering) increases some key risks faced by a CCP, compared to direct membership. Specifically, tiering increases exposures toward the average clearing member and increases the probability of extreme exposures toward individual clearing members8. 8 The result is developed under the assumption that clearing members pool the exposures of their clients and does not carry over to the case of individual segregation of client accounts. 11 .

The Nordic market has a direct membership structure Table 1: Membership structure of major European CCPs Direct Indirect Members participants Euro CCP 25 >550 LCH EquityClear LSE 37 >530 Eurex 58 235 LCH SwapClear 22 80 LCH RepoClear 42 80 Nasdaq Clearing (Nordic 287 22 and German power) Indirect/ direct >22 >14 4.1 3.6 1.9 0.1 Source: Company websites and Galbiati and Soromaki (2013). 5.2 THE USE OF BANK GUARANTEES INTRODUCTION OF THE DS FUTURES AND Investments in electricity production are characterized by a particularly long payback profile. Also, the time separating the investment decision and positive cash-flows is long in energy markets, compared to most other commodities markets. Furthermore, price volatility and seasonal variations are large, and may lead to low margins for extended periods of time. The special characteristics of electricity production have led to the use of instruments unique to energy markets The special characteristics of electricity production have led to the use of a number of unique products in power derivatives markets, in order to hedge the atypical cash-flow profiles of the hedgers. One such product is the Deferred Settlement futures (DS futures), the standard contract in the Nordic market for contracts with more than a month to delivery. The market participants developed this contract specifically to match the time structure of the commercial risks that they are hedging.

The attractiveness of the contract structure hinges critically on the use of bank guarantees as margin collateral. DS Futures were introduced at the end of 1997. The introduction led to a massive increase in the clearing of energy derivatives, as the structure of the new instrument was tailor-made to fit the cash flow profile of electricity producers and consumers. The previously listed ordinary futures contracts were not being widely traded for contracts with more than 3-4 months to delivery.

A key difference between the DS futures and the ordinary futures contract is that market 12 . participants can post bank guarantees as variation margin for their DS futures in the trade period. A key feature of these instruments is the possibility to post bank guarantees as collateral The DS futures contract specifies two time frames; the trade period and the delivery period. The trade-period can last for as long as ten years. In the trade period the contract is marked-to-market, but no cash-flows occur. Bank guarantees can be posted as collateral for the resulting exposure towards the CCP.

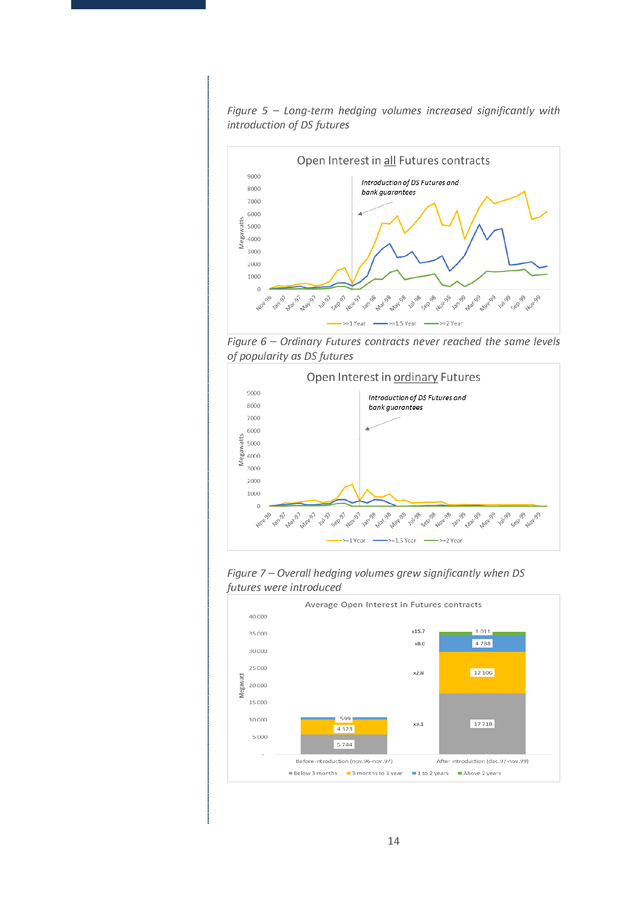

In the delivery period, there is a daily exchange of the net of spot price and the agreed futures price, as for a regular futures contract. This contract structure implies that the parties avoid the cash settlement and funding costs associated with margin requirements and daily settlements in the trade period. Figure 5 shows megawatts open interest for ordinary futures contracts and DS futures with more than one year to maturity around the introduction of DS futures (November 1996 – December 1999).9 One can clearly see that open interest grew significantly during this period. Exchange-traded hedging volumes increased significantly when these tailored instruments were introduced Figure 6 shows the developments in open interest for ordinary futures contracts. These are contracts of the same type that is standard in other commodities markets, for which the variation margin cannot be collateralized by bank guarantees.

The figure shows that this contract type never gained any particular traction in the market, and eventually died out. The growth in open interest was particularly pronounced for contracts with more than one year to delivery, but also overall hedging volumes grew, as shown in figure 7. We think the evidence provided in figures 5 to 7 suggests that DS futures have characteristics that the market participants want. In particular, market participants report that it is the possibility to collateralize the contract using bank guarantees in the trade period that makes the contract attractive. In section 6, we show that the monetary costs of replacing bank guarantees with cash collateral are significant. The introduction of DS futures led to significantly more trading on the exchange.

We will also argue that an effective ban on bank guarantees is likely to revert the development shown in figures 5 and 7. 9 This is monthly data that is collected on day 15 every month. If the exchange is closed on day 15, we collect data on day 16, and then day 14 if the exchange is not open on day 16. 13 . Figure 5 – Long-term hedging volumes increased significantly with introduction of DS futures Figure 6 – Ordinary Futures contracts never reached the same levels of popularity as DS futures Figure 7 – Overall hedging volumes grew significantly when DS futures were introduced 14 . 5.3 RISK PROFILE OF BANK GUARANTEES The bank guarantees used in commodity derivative markets today are on-demand, continuing, unconditional and irrevocable. Box 1 summarizes some key features of this instrument. Box 1: On-demand bank guarantees Bank guarantees eligible as collateral in European energy derivatives markets are on-demand, unconditional, irrevocable and continuing. i. On-demand - The guarantor must pay upon demand, without making any objection or invoking any defence. ii. Unconditional and irrevocable - An unconditional guarantee is a pledge by the guarantor to make payments, as stated in the guarantee, without any conditions. An irrevocable guarantee cannot be cancelled or modified in any way without explicit consent by the affected parties involved. iii. Continuing - A continuing guarantee is a guarantee where the guarantor assumes liability for any past, present and future obligations owed by a debtor to a lender or creditor. Even where the amount owing has been completely paid, the guarantor can still be liable under that line of credit if there is a subsequent indebtedness. In this report, when we refer to bank guarantees, we mean nonfully backed commercial bank guarantees, unless otherwise explicitly stated. The main risk dimensions of CCP collateral are credit, market and concentration risk The risk profile of an instrument posted as collateral can be evaluated along several dimensions.

The most important ones in this context are credit risk, market risk and concentration risk. Credit risk is the risk that a debtor fails to meet its financial obligations. The credit risk the CCP takes on when accepting collateral for a position consists of two parts – the event that the 15 . debtor defaults (direct credit risk) and the event that the entity issuing the collateral defaults (indirect credit risk). 10 Credit risk of a bank guarantee stems from the event that both the debtor and the issuing bank simultaneously default Figure 8 sketches a stylized overview of the credit risk to the CCP with bank guarantees as bank guarantees as collateral, and with asset collateral. In the case of bank guarantees, if the debtor does not meet its obligation upon settlement or defaults in the trade period of the instrument, the CCP directs its claim to the bank issuing the guarantee. The bank has to pay the debt owed by the original debtor in accordance with the terms laid out in box 1.

Thus, the relevant credit risk from a bank guarantee stems from the event that both the debtor and the issuing bank simultaneously default, at a time when the market value of the position is negative. Figure 8: Stylized overview of bank guarantees and other assets as collateral 10 If the issuer of collateral defaults, the original debtor (to whom the CCP has the credit risk towards) is liable to provide new collateral or otherwise fulfill its financial obligation towards the CCP. 16 . Panel A (Bank guarantees): The hedgers secure their trades with a bank guarantee. If a hedger with debt to the CCP defaults, the CCP directs the claim to the bank issuing the guarantee. If the bank and the hedger default simultaneously, the CCP may incur a loss. Panel B (Asset collateral): The hedgers secure their trades with assets11. If a hedger with debt defaults, the CCP claims the asset and sells it. CCPs mitigates credit risk with requirements on the guarantors’ and members’ credit worthiness A CCP will mitigate credit risk by only accepting guarantees from banks with low credit risk.

In the case of Nasdaq Clearing, only guarantees from banks with low credit risk and an investment grade credit rating are eligible as collateral. In case a bank issuing a bank guarantee no longer fulfills the requirements stipulated by the CCP, the bank guarantee has to be replaced within a timeframe specified in the rules. The CCP will continuously monitor the credit risk associated with both clearing members and issuing banks to ensure that the risk of simultaneous default is minimized.

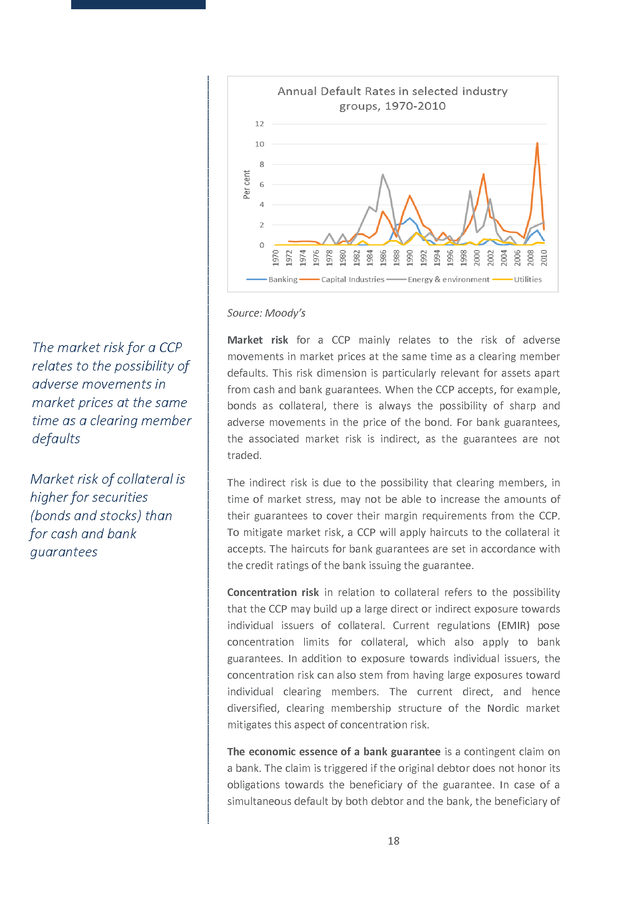

Obviously, a similar risk is present with other forms of collateral. If the issuer of the collateral and the debtor posting the collateral defaults simultaneously, the CCP can potentially incur a loss. Figure 9 illustrates the direct credit risk by showing annual default rates in selected industry groups. The “utilities” sector includes traditional electricity producers and grid operators.

One can estimate the risk of a simultaneous default by examining the probabilistic dependence between default rates for utilities and the banking sector. The figure clearly shows that utilities have a very low probability of default. The correlation coefficient of the default rates of the two sectors, a standard measure of dependency, is around 0.4 in the series shown in figure 9. Figure 9: Annual default rates in selected industries 11 This asset may be cash, which the CCP will invest in highly liquid financial instruments as specified by EMIR.

The asset might also be a highly liquid financial instrument as specified in the CCP’s eligible collateral list. 17 . Source: Moody’s The market risk for a CCP relates to the possibility of adverse movements in market prices at the same time as a clearing member defaults Market risk of collateral is higher for securities (bonds and stocks) than for cash and bank guarantees Market risk for a CCP mainly relates to the risk of adverse movements in market prices at the same time as a clearing member defaults. This risk dimension is particularly relevant for assets apart from cash and bank guarantees. When the CCP accepts, for example, bonds as collateral, there is always the possibility of sharp and adverse movements in the price of the bond. For bank guarantees, the associated market risk is indirect, as the guarantees are not traded. The indirect risk is due to the possibility that clearing members, in time of market stress, may not be able to increase the amounts of their guarantees to cover their margin requirements from the CCP. To mitigate market risk, a CCP will apply haircuts to the collateral it accepts.

The haircuts for bank guarantees are set in accordance with the credit ratings of the bank issuing the guarantee. Concentration risk in relation to collateral refers to the possibility that the CCP may build up a large direct or indirect exposure towards individual issuers of collateral. Current regulations (EMIR) pose concentration limits for collateral, which also apply to bank guarantees. In addition to exposure towards individual issuers, the concentration risk can also stem from having large exposures toward individual clearing members.

The current direct, and hence diversified, clearing membership structure of the Nordic market mitigates this aspect of concentration risk. The economic essence of a bank guarantee is a contingent claim on a bank. The claim is triggered if the original debtor does not honor its obligations towards the beneficiary of the guarantee. In case of a simultaneous default by both debtor and the bank, the beneficiary of 18 .

the bank guarantee will have a claim on the assets of the defaulting bank, alongside other creditors and depositors. 5.4 SYSTEMIC RISK AND CENTRAL COUNTERPARTIES By systemic risk we mean the risk that an event will trigger a loss of confidence in a substantial portion of the financial system that is serious enough to have adverse effects on the real economy.12 Systemic risk factors exhibit propagation mechanisms to the wider financial system Systemic risk factors have three identifying characteristics useful for operational analysis (Taylor, 2009). Firstly, there must be a risk of a large triggering shock. This may, for instance, be a severe natural disaster, or it may be the sudden default of a major firm in a sector. Secondly, there must be a channel or a mechanism for the shock to propagate to other parts of the financial system. Thirdly, this financial distribution must affect the real economy. A major policy initiative in the years since 2007-2008 has been to identify and handle systemic risk factors.

An important part of this initiative has been to push OTC derivatives markets onto multilateral trading venues such as exchanges, and to introduce mandatory clearing through central counterparties in these markets. CCPs generally improves safety and transparency in financial markets … … but also introduce new systemic risk factors CCPs are considered systemically important institutions, and are subject to regulatory oversight A well-functioning CCP can greatly improve safety, efficiency and transparency in a market. Market participants are no longer exposed to each other, but to the CCP. If a clearing member defaults, the CCP may facilitate the transfer of customer positions and collateral of that failing clearing member to solvent, surviving clearing members, and coordinate the orderly replacement of defaulted trades through auctions and hedging of exposures.

The CCP can be characterized as a firewall, hindering the propagation of an external shock through a system (Wendt, 2015). However, since the CCP serves as a hub in the market architecture, the possibility that the CCP itself may fail constitutes a systemic risk factor. A potential CCP default may have a severe impact on clearing members, the affected market, and other linked CCPs. For this reason, CCPs are considered systemically important institutions, and are subject to regulatory oversight. The negative externality to the rest of society, should a CCP experience financial distress, may rationalize imposing tighter risk management practices through regulation, than those the CCP itself would prefer to implement.

However, it is important to keep in mind that it is not only the CCP capital structure or margin procedures per 12 This is the G-10 definition of systemic risk. 19 . se which reduce systemic risk, but also the transparency and potential for orderly resolutions these institutions provide. If the compliance burden on firms for trading on centrally cleared markets gets too high, there may be a return to bilateral, physical hedging contracts, in which case the potential benefits of central clearing disappear. A second possible systemic risk stemming from CCPs is the potential for liquidity squeezes imposed by margin calls. If a severe economic shock affects a market, we will expect to see sharp price movements, thereby increasing the volatility of the traded assets. The increase in volatility leads to higher margin requirements from the CCP, which in turn may lead to a scramble for highly liquid assets by the market participants.

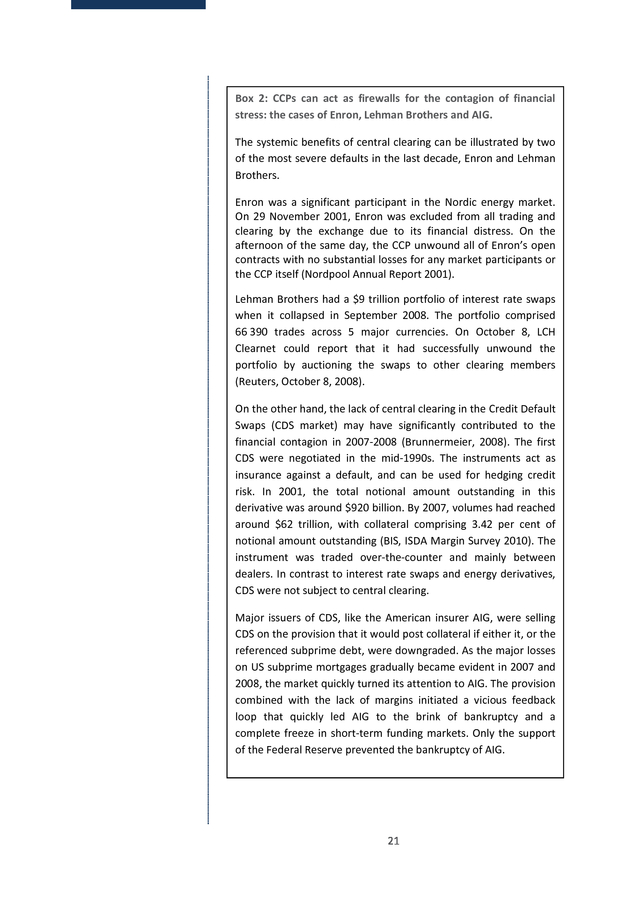

Since highly liquid, secure assets are in high demand during times of market stress, this scramble may, in a worst-case scenario, ultimately lead to a negative feedback loop, with short term funding markets drying up, liquidity squeezes leading to fire-sales of assets, and subsequent higher volatility (Brunnermeier and Pedersen, 2009). This second mechanism of systemic risk from a CCP may be mitigated by allowing for some heterogeneity in the type of assets that are eligible as collateral. One could argue that banks are less susceptible to these feedback loops than, for example non-financial firms, since banks have access to central bank liquidity facilities and may thereby transform less liquid assets into base money. 20 . Box 2: CCPs can act as firewalls for the contagion of financial stress: the cases of Enron, Lehman Brothers and AIG. The systemic benefits of central clearing can be illustrated by two of the most severe defaults in the last decade, Enron and Lehman Brothers. Enron was a significant participant in the Nordic energy market. On 29 November 2001, Enron was excluded from all trading and clearing by the exchange due to its financial distress. On the afternoon of the same day, the CCP unwound all of Enron’s open contracts with no substantial losses for any market participants or the CCP itself (Nordpool Annual Report 2001). Lehman Brothers had a $9 trillion portfolio of interest rate swaps when it collapsed in September 2008. The portfolio comprised 66 390 trades across 5 major currencies. On October 8, LCH Clearnet could report that it had successfully unwound the portfolio by auctioning the swaps to other clearing members (Reuters, October 8, 2008). On the other hand, the lack of central clearing in the Credit Default Swaps (CDS market) may have significantly contributed to the financial contagion in 2007-2008 (Brunnermeier, 2008).

The first CDS were negotiated in the mid-1990s. The instruments act as insurance against a default, and can be used for hedging credit risk. In 2001, the total notional amount outstanding in this derivative was around $920 billion.

By 2007, volumes had reached around $62 trillion, with collateral comprising 3.42 per cent of notional amount outstanding (BIS, ISDA Margin Survey 2010). The instrument was traded over-the-counter and mainly between dealers. In contrast to interest rate swaps and energy derivatives, CDS were not subject to central clearing. Major issuers of CDS, like the American insurer AIG, were selling CDS on the provision that it would post collateral if either it, or the referenced subprime debt, were downgraded.

As the major losses on US subprime mortgages gradually became evident in 2007 and 2008, the market quickly turned its attention to AIG. The provision combined with the lack of margins initiated a vicious feedback loop that quickly led AIG to the brink of bankruptcy and a complete freeze in short-term funding markets. Only the support of the Federal Reserve prevented the bankruptcy of AIG. 21 .

5.5 SYSTEMIC RISK AND BANK GUARANTEES Are there any particular systemic risks stemming from the use of bank guarantees as collateral to the CCP? Bank guarantees have a higher risk of loss than some other forms of collateral If the likelihood of the CCP incurring a major loss is higher when it accepts bank guarantees rather than other forms of eligible collateral, one could argue that the use of bank guarantees increases systemic risk. It is not clear that the probability of simultaneous default is higher when the collateral posted are bank guarantees rather than some other eligible collateral classes. However, if one for some reason believes that CCPs insufficiently address the default risk inherent to bank guarantees (or any other form of collateral) through the standard risk management tools outlined above, regulators should ask for adjustments in the risk management practices of these CCPs. But one can also argue that bank guarantees actually reduce systemic risk On the other hand, one can also argue that systemic risk is lower in a clearing structure with bank guarantees. One reason for this is that counterparty concentration is lower in direct membership structures such as the Nordic energy market.

Without bank guarantees, the market may change into an indirect membership structure, and the CCPs direct counterparty exposure towards banks will increase. Higher counterparty concentration for the CCP leads to higher default risk for the CCP, and thereby higher systemic risk. The use of bank guarantees may also decrease the risk of a liquidity squeeze in the financial system. If the universe of eligible collateral is larger, the probability of a liquidity squeeze is lower, and the system as a whole is more resilient to shocks. The most important thing for handling systemic risk is making sure that markets are exchangetraded and centrally cleared Finally, the use of bank guarantees may be necessary in order to keep the power market as an exchange-cleared market. The alternative is a move to bilateral trading in the OTC market, or direct physical hedging by electricity suppliers and major industrial firms.

The exchange-traded market structure guarantees transparency and central clearing, which is of fundamental importance for a robust system. Indeed, the current overall market structure of exchangetraded power markets is exactly what the regulation of derivative markets seeks to accomplish. 22 . 6 LIKELY IMPACT OF REGULATORY CHANGES We argue that effectively prohibiting bank guarantees in energy markets will likely lead to changes in firm behavior and market structure. These changes induce welfare costs. We argue that if the use of bank guarantees in energy markets is effectively prohibited, hedging costs for non-financial market participants are likely to increase. One should fully expect these firms to adapt their behavior in response to the increased costs. Likely responses are a reduction in the hedging activity of these firms, a move to an indirect clearing structure, and a substitution by firms of the current cleared contracts for non-cleared instruments or physical delivery contracts. There are welfare costs associated with each of these responses.

In addition, we find the impact of the regulatory changes on systemic risk to be at best negligible, and at worst detrimental. 6.1 INCREASED COSTS OF HEDGING FOR INDUSTRIAL FIRMS Electricity suppliers report that their hedging cost will increase significantly with the pending regulations Electricity suppliers report that their hedging cost will increase significantly if they have to post other types of collateral instead of the current bank guarantees. In this section, we will illustrate this cost increase with a general example. It should be kept in mind that these cost calculations are based on a partial approach, meaning that they do not reflect changes to the market structure which are likely to come as a response to regulatory changes. The most likely structural changes to the market, and their effects on market functioning, are explored in the next sections of this chapter.

It should also be kept in mind that the costs calculated here do not reflect the true economic cost to society. The economic cost will come from efficiency losses incurred by changes in the market structure and behavior of market participants. As such, the effects calculated here comprise the incentives of market participants to change their behavior in response to the pending regulations. Non-financial market participants, for instance electricity suppliers or producers, can currently choose to post bank guarantees as collateral instead of securities or cash.

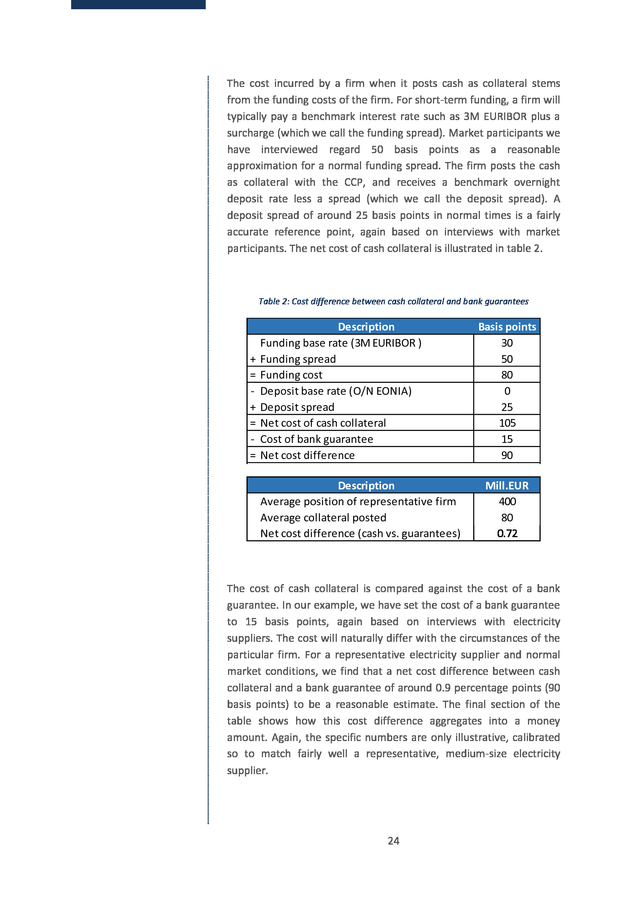

In this example, we calculate the difference in cost between posting cash collateral and bank guarantees. The example is stark, but also relevant since many nonfinancial firms will realistically not hold portfolios of liquid securities that can be used instead of posting cash as collateral The specific numbers in our example are made-up and for illustration purposes only, but the structure of the calculation, and the approximate size of the net cost difference, is realistic. 23 . The cost incurred by a firm when it posts cash as collateral stems from the funding costs of the firm. For short-term funding, a firm will typically pay a benchmark interest rate such as 3M EURIBOR plus a surcharge (which we call the funding spread). Market participants we have interviewed regard 50 basis points as a reasonable approximation for a normal funding spread. The firm posts the cash as collateral with the CCP, and receives a benchmark overnight deposit rate less a spread (which we call the deposit spread).

A deposit spread of around 25 basis points in normal times is a fairly accurate reference point, again based on interviews with market participants. The net cost of cash collateral is illustrated in table 2. Table 2: Cost difference between cash collateral and bank guarantees + = + = = Description Funding base rate (3M EURIBOR ) Funding spread Funding cost Deposit base rate (O/N EONIA) Deposit spread Net cost of cash collateral Cost of bank guarantee Net cost difference Description Average position of representative firm Average collateral posted Net cost difference (cash vs. guarantees) Basis points 30 50 80 0 25 105 15 90 Mill.EUR 400 80 0.72 The cost of cash collateral is compared against the cost of a bank guarantee.

In our example, we have set the cost of a bank guarantee to 15 basis points, again based on interviews with electricity suppliers. The cost will naturally differ with the circumstances of the particular firm. For a representative electricity supplier and normal market conditions, we find that a net cost difference between cash collateral and a bank guarantee of around 0.9 percentage points (90 basis points) to be a reasonable estimate.

The final section of the table shows how this cost difference aggregates into a money amount. Again, the specific numbers are only illustrative, calibrated so to match fairly well a representative, medium-size electricity supplier. 24 . 6.2 REDUCED HEDGING ACTIVITY Increased hedging costs will likely lead to reduced hedging activity Reduced commercial hedging activity can translate into a loss of market liquidity In the previous section, we showed how the costs of non-financial firms are likely to increase if they can no longer post bank guarantees as collateral. The next sections will elaborate on likely responses to this cost increase. The perhaps most obvious response of a firm would be to scale back on hedging activity. Per standard economic reasoning, firms will hedge their commercial risk until the marginal gain from hedging equates the marginal costs.

When marginal costs of hedging increase, one would expect to see, as a first-order effect, a decrease in hedging activity. When the possibility of using future contracts collateralized by bank guarantees was introduced in the Nordic market in 1997, hedging volumes on the power exchange grew dramatically (see section 3). A ban on bank guarantees may revert this development. Reduced commercial hedging activity would imply lower trade volumes in energy derivatives, which could translate into a loss of market liquidity.

As liquidity generally begets liquidity, this secondorder effect might, in the worst-case scenario, end up having a severe negative impact on the functioning of the market. Reduced hedging activity would entail a real economic cost to society, as increased capital costs of energy suppliers would ultimately show up in higher electricity prices and reduced investments in the sector. Essentially, we would see a partial reversal of the beneficial effects of energy derivatives markets highlighted earlier in this report. 6.3 NON-FINANCIALS MOVE TO INDIRECT CLEARING MEMBERS Increased hedging costs may also lead to an indirect market structure It is possible that hedging activity would fall in response to an effective ban on bank guarantees in clearing. Another possible scenario is a change in the market structure to mitigate the cost increases of prohibiting bank guarantees.

One such change in the structure might be a move by non-financial firms to become indirect clearing participants. The market may, with this change, take on the characteristics of a dealer-based market, which in in turn may adversely affect informational asymmetries, resulting in reduced liquidity and increased spreads (Ripatti, 2004). 25 . Indirect clearing participants would clear their derivatives transactions through a clearing member, usually a bank or another large financial institution. The clearing bank would post collateral on behalf of the indirect participant. The move from direct membership to indirect participation may have unwanted consequences This indirect structure is a typical feature in many derivatives markets. However, the move from direct membership to indirect participation may have unwanted consequences. The clearing banks will have access to information about the structure and size of customer positions, which may give rise to informational asymmetry and adverse selection.

This informational asymmetry may reduce the popularity of the exchange-traded contracts, leading to reduced liquidity and a move to bilateral trading. One can see an example of this mechanism in foreign exchange markets. There, major banks involved in clearing and dealing have a significant informational advantage over other participants because they can monitor FX flows (Bjønnes et al, 2015 and Bjønnes and Rime, 2005). This advantage makes it difficult for smaller participants to compete, which again results in less competition. Seemingly small changes in market structure can lead to major changes in market functioning Given that the market for energy derivatives is quite new relative to other commodities markets, and that the competition from the bilateral market is strong, small changes to the market microstructure can be sufficient to cause a significant impact on market functioning.

For an example of this, see box 3, (“How misstep over trading fractions wounded ICAP's EBS”). 26 . Box 3: How a misstep over trading fractions wounded ICAP's EBS (Reuters, September 20, 2012) “- Who knew a single decimal point could cause so much trouble? Worried about diminishing market share and increasing competition, EBS, at one point the world's top foreign exchange dealing system, took a gamble and decided to let clients trade out to a fifth decimal point - that's one-thousandth of a cent. The move backfired. It accelerated a decline in the firm's market share in the nearly $5 trillion forex market and contributed to a management shake-up that caused three top executives to leave earlier this year.” The example above shows that even small changes to market structure can have a large impact. The only change by ICAP was to change the minimum tick size from 0.0001 to 0.00001. This small change led to a significant drop in EBS market share.

Compared to the new regulation discussed in this paper, the change made by ICAP is small. 27 . 6.4 INCREASED USE OF BILATERAL AND PHYSICAL CONTRACTS We have seen that the pending regulation would entail increased costs to non-financial firms, which in turn would likely affect the behavior of these firms, and consequently the market structure of the energy derivatives market. This section will describe what we view to be a highly likely change in the market structure, an increased use of bilateral hedging contracts based on physical deliveries. Non-financial firms have the option to bypass the financial market, using non-cleared and physical contracts Liquidity and market efficiency is likely to suffer Electricity suppliers and wholesale buyers hedge their risk with financial derivatives because they will buy or sell electricity in the future. The future spot price of electricity is uncertain, and firms can eliminate this uncertainty by entering into offsetting derivative contracts. However, these market participants often also have the option to enter into bilateral contracts on physical delivery of electricity at a specified future date.

As such, non-financial firms have the option to “bypass” the financial market and regulations specific to the financial marketplace. An increased use of bilateral and physical hedging instruments is likely to have a detrimental effect on market efficiency. Firstly, liquidity in the multilateral marketplace suffers as trade volumes decrease. Again, as liquidity begets liquidity, reduced trading from non-financial firms may induce a spiral that ends up having a significant negative effect on transaction costs and price discovery. Secondly, as discussed in the previous section, bilateral markets are more prone to informational asymmetry and related efficiency losses. A third detrimental effect of increased bilateral trading is the impact on systemic risk.

This will be the topic of the concluding section of this chapter. 6.5 IMPACT ON SYSTEMIC RISK We have argued that prohibiting the use of bank guarantees will incur increased costs to non-financial participants in the energy derivatives market. Likely responses to this cost increase from nonfinancial firms include reducing hedging activity, becoming indirect clearing participants instead of direct clearing members, or increasing the use of bilateral and physical contracts. In this section, we discuss the impact these changes are likely to have on systemic risk.

We will 28 . argue that while the regulation in isolation is likely to give somewhat reduced credit risk to the CCP, there will likely also be changes to the market structure that create more systemic risk. The isolated effect of regulatory changes is somewhat lower credit risk of CCP collateral The isolated effect of the regulation is that non-financial firms have to post cash or other high-quality assets as collateral instead of bank guarantees. In the case of the Nordic energy market, we have seen that bank guarantees currently make up approximately 70% of margin collateral. The isolated effect on the CCP of receiving cash or high-quality financial instruments instead of a guarantee, could mean lower risk of the simultaneous default of a clearing member and a collateral issuer. This argument is valid if one assumes that a bank issuing a guarantee has a higher probability of default than other collateral issuers.

This might be true for classes of some eligible collateral, but not necessarily for all. As for market risk, the risk associated with bank guarantees is lower than for marketable assets, since these might experience severe price movements. On the other hand, there might be circumstances in which it will take some time for a CCP to recover a debt secured by a bank guarantee, while a liquid financial instrument or cash is immediately marketable. If the market adapts to new regulations by changing into an indirect membership structure, the CCP will likely have higher direct counterparty exposure towards banks. This could possibly lead to higher default risk of the CCP, and thereby increase systemic risk. There is little reason to believe that prohibiting bank guarantees will have any significant impact on the overall risk of the CCP However, central counterparties manage their credit and market risk using tools such as haircuts and concentration limits, as well as credit surveillance of clearing members, guarantors and issuers.

These tools will counteract the risk effect of replacing one type of collateral with another, less risky type. For instance, if firms replace bank guarantees with covered bonds, other haircuts and concentration limits will apply. To the extent that CCPs already internalizes and adequately manage credit and market risk, there is little reason to believe that prohibiting bank guarantees will have any significant impact on the overall risk of the CCP. The above discussion indicates the important difference between traditional risk factors such as market or credit risk, and the concept of systemic risk.

A cornerstone in the regulatory effort to tackle systemic risk is the introduction of mandatory clearing of derivatives through central counterparties. As we discussed in chapter 5, CCPs offer oversight and the potential for ordered resolutions of defaults. At the same time, it is clear that CCPs have the potential to become systemic risk factors themselves, as propagation mechanisms for 29 . shocks. Regulation of CCPs should thus aim to maximize the systemic benefits of central clearing, while minimizing the potential drawbacks. The systemic impact of bank guarantees should be understood with this in mind. The impact on systemic risk from effectively prohibiting the use of bank guarantees will, in isolation, be small In isolation, effectively prohibiting the use of bank guarantees will have little impact on systemic risk. Non-financial firms will replace posted bank guarantees with financial instruments or cash.

CCPs will offset the somewhat lower credit risk by haircuts and other risk management tools. Non-financial firms will experience higher costs from hedging with cleared derivatives, which in turn are likely to increase the use of bilateral and physical hedging contracts. However, the induced changes in market structure may have a detrimental effect on systemic risk Bilateral trading of non-cleared derivatives will have a severe and detrimental effect on the systemic risk stemming from the energy market. The massive stress contagion coming from the CDS market in 2007 to 2008 provides ample illustration of the perils of opaque and non-cleared derivatives markets.

On the other hand, Nasdaq’s orderly resolution of Enron’s Nordic energy derivatives in 2002 and LCH’s unwinding of Lehman’s interest rate swap portfolio in 2008 (confer box 2) illustrates the benefit of cleared markets. 30 . 7 CONCLUSIONS Summing up, we find that the direct effect on systemic risk by effectively prohibiting bank guarantees is small. However, the regulation may change the market structure in an adverse manner. The effect on systemic risk is uncertain. Keeping bank guarantees in their current form will leave the CCP vulnerable to the simultaneous default of a clearing member and a bank guarantee issuer. However, this risk is not unique for bank guarantees, but is also present when participants post other financial instruments as collateral.

The handling and procedures to mitigate credit risk of different collateral types do not differ and there is no apparent reason why a CCP should not be able to handle the risk of bank guarantees as it is handling the risk of other types of collateral. Systemic risk may, on the other hand, increase as the market structure adapts to new regulations. If the market changes into an indirect membership structure, the CCPs concentration risk would increase due to larger direct counterparty exposure towards banks, possibly leading to higher default risk for the CCP, and thereby increased systemic risk. Moreover, systemic risk will increase if the energy market moves to a bilateral non-cleared market with little or no regulatory oversight.

Central counterparties face risk when accepting bank guarantees as margin collateral, as they do when accepting any other financial asset. However, we do not find that the bank guarantees used in energy markets today constitute a significant systemic risk factor. 31 . 8 LITERATURE AND REFERENCES Amundsen, Eirik S., and Lars Bergman. "Why has the Nordic electricity market worked so well?" Utilities Policy 14.3 (2006): 148157. Bank of International Settlements Seminannual OTC derivatives statistics. Bergman, Lars. "European electricity market integration: the Nordic experiences." Research Symposium European Electricity Markets. 2003. Bergman, Lars. "The Nordic electricity market-continued success or emerging problems? " Swedish economic policy review 9.2 (2002): 5188. Bjønnes, Geir H., Osler, Carol and Dagfinn Rime.

“Sources of Information Advantage in the Foreign Exchange Market”, Working Paper, 2015. Bjønnes, Geir H. and Dagfinn Rime. “Dealer Behavior and Trading Systems in Foreign Exchange Markets", Journal of Financial Economics, feb., 2005. Bouchouev, Ilia.

"Inconvenience yield, or the theory of normal contango." Quantitative Finance 12.12 (2012): 1773-1777. Brunnermeier, Markus K., and Lasse Heje Pedersen. "Market liquidity and funding liquidity." Review of Financial studies 22.6 (2009): 22012238. Brunnermeier, Markus K. Deciphering the liquidity and credit crunch 2007-08.

No. w14612. National Bureau of Economic Research, 2008. Carmona, René, and Michael Coulon.

"A survey of commodity markets and structural models for electricity prices." Quantitative Energy Finance. Springer New York, 2014. 41-83. EACH paper - Bank guarantees as collateral for non-financial participants.

European Association of CCP Clearing Houses. October 2014. Galbiati, Marco, and Kimmo Soramaki. "Central counterparties and the topology of clearing networks." Bank of England Working paper. no.

480. 2013. Geman, Helyette. "Towards a European market of electricity: spot and derivatives trading." Universität Paris IX Dauphine, Paris (2002). 32 .

Hicks J. Value and Capital. Oxford University Press. 1939 Keynes J.

A Treatise on Money, Vol II. Macmillan, London. 1930 Ripatti, Kirsi.

"Central counterparty clearing: constructing a framework for evaluation of risks and benefits." Available at SSRN 787606 (2004). Samuelson, Paul A. "Proof that properly anticipated prices fluctuate randomly." Industrial management review 6.2: pages 41-49. 1965. Milne, Alistair.

"OTC central counterparty clearing: Myths and reality." Journal of Risk Management in Financial Institutions 5.3 , pages 335-346, 2012 Moody’s Investor Service. “Corporate Default and Recovery Rates, 1920-2010”. February 28, 2011. Mork, Erling.

"Emergence of financial markets for electricity: a European perspective." Energy policy 29.1 (2001): 7-15. Nordic FSAs. “The Nordic FSAs request use of bank guarantees as collateral for non-financial clearing members in line with current commodity market practice”. Letter from the Nordic Financial Supervisory Authorities to European Securities and Markets Authorithy.

21 September 2012. Nowak, Bartlomiej. "Energy Market of the European Union: Common or Segmented?" The Electricity Journal 23.10 (2010): 27-37. Taylor, Charles. “Managing Systemic Risk”.

PEW Briefing paper no. 11, 2009. Wendt, Froukelien. "Central Counterparties: Addressing their Too Important to Fail Nature." IMF Working Paper (2015). World Federation of Exchanges (WFE) / IOMA Derivatives Market Survey 2013. 33 .

7 4 Regulation of central clearing in energy derivatives markets ......................................................... 8 5 Central clearing in the nordic market.............................................................................................. 9 5.1 5.2 The use of bank guarantees and introduction of the DS futures ..........................................

12 5.3 Risk profile of bank guarantees ............................................................................................. 15 5.4 Systemic risk and central counterparties .............................................................................. 19 5.5 6 Overview of central clearing in the Nordic Market .................................................................

9 Systemic risk and bank guarantees ....................................................................................... 22 Likely impact of regulatory changes .............................................................................................. 23 6.1 Increased costs of hedging for industrial firms .....................................................................

23 6.2 Reduced hedging activity ...................................................................................................... 25 6.3 Non-financials move to indirect clearing members .............................................................. 25 6.4 Increased use of bilateral and physical contracts .................................................................

28 6.5 Impact on systemic risk ......................................................................................................... 28 7 Conclusions.................................................................................................................................... 31 8 Literature and references ..............................................................................................................

32 2 . 1 EXECUTIVE SUMMARY This report analyzes the use and risk of bank guarantees in the clearing of energy derivatives. In particular, we examine the systemic risk component of bank guarantees in central clearing, and the likely effects of an effective ban on the current use of bank guarantees. Our main conclusions are that  It is likely that the use of exchange-traded energy derivatives will decrease significantly if the current use of bank guarantees are disallowed.  We expect an increase in bilateral trading and physical hedging of energy prices. Systemic risk may increase, since o Bilateral markets are not subject to the same regulatory oversight as exchange-traded markets. o Bilateral trades are not necessarily cleared. o Transparency is much lower in bilateral markets.  Central counterparties face risk when accepting bank guarantees as margin collateral, as they do when accepting any other financial asset. However, we do not find that the bank guarantees used in energy markets today constitute a significant systemic risk factor. The main message from this report is that disallowing the current use of bank guarantees in energy markets, however well intended, may cause adverse consequences.

In addition, the benefits from imposing the regulation is likely to be small, if any. 3 . 2 INTRODUCTION This report is written on behalf of the Working Party on Bank Guarantees in European Energy Markets1, by associate professor Geir Høidal Bjønnes2 and Jo Saakvitne3. The aim and mandate of the report is to analyze whether the current use of bank guarantees, as they are used in energy markets today, poses any unacceptable systemic risk; and how any potential risk can be mitigated. Further, the report aims to examine likely scenarios if bank guarantees are not allowed as eligible collateral for nonfinancial participants in the power and gas market. The authors take full responsibility for any errors or omissions in the work. In this report, we put a special emphasis on the Nordic energy market. The Nordic energy market has been a success story, and influences other European markets, while at the same time it is particularly affected by the pending regulatory changes. Sections 3-4 in this report provide key background information, while sections 5-6 contain the bulk of the analysis.

In section 3, we describe energy markets, with a special emphasis on features separating them from other financial markets. We highlight why well-functioning energy derivatives markets yield valuable benefits to society. In section 4, we describe the key regulatory issues facing the market participants.

In section 5, we discuss risk from central clearing and bank guarantees. Section 6 discusses the likely impact of regulatory changes, while section 7 concludes. 1 The members of the Working Party are Nasdaq Commodities, Finnish Energy Industries, Confederation of Finnish Industries (EK), Energy Norway, Swedenenergy, Oberoende Elhandlare, The Nordic Association of Electricity Traders (NAET), Nord Pool Spot, and Dansk Energi. Beyond the Working Party, the project steering group also included the Finnish Ministry of Employment, the Finnish Ministry of Finance, the Iberian energy derivatives exchange (OMIP), the Iberian energy clearing house (OMIClear), and the Warsaw Commodity Clearing House (IRGIT). 2 3 BI Norwegian Business School BI Norwegian Business School and Fixed Point Consulting 4 .

3 THE MARKET FOR ENERGY DERIVATIVES In this section, we discuss key features of energy markets, with a special emphasis on what separates energy markets from other financial and commodities markets. We argue that well-functioning markets for energy derivatives ultimately lead to lower electricity prices and higher investments in the sector. Electricity production is capital-intensive and financial risk management is important for investments The business of producing, delivering and retailing electricity is complex. It requires capital-intensive investments and long-term financing, which gives financial risk management a crucial role in the determination of electricity prices and viability of investment projects. Electricity markets have several unique features, which are lacking in other financial and commodity markets. Firstly, electricity cannot be stored, and hence suppliers and consumers lack inventories. Therefore, the dynamics of derivative prices may behave differently than for instance oil price derivatives, where the underlying asset can be stored. Secondly, electricity markets have historically been geographically distinct.

Even today, moving power between regions may be economically or even physically unviable due to energy lost to resistance in the grid. In Europe, lack of cross-border transmission capacity is a hindrance to energy market integration (Nowak, 2010). This has led to fragmented and specialized derivative markets, and substantial price differences across regions. Figure 1: Large price differences in electricity prices in EU. Electricity markets are geographically distinct Source: Eurostat. Prices for 2500-5000 kWh, excluding taxes. 5 .

Figure 2: The five wide area electricity grids in Europe Electricity prices feature extreme variations, making hedging important for electricity suppliers and consumers Well-functioning financial derivatives markets lower the costs of hedging… … which in turn lowers electricity prices and increase investments Electricity prices also feature large variations. Part of this variation is due to strong seasonality in supply and demand over days, weeks and months. In addition, there is also the possibility of unexpected dramatic price changes over the very short term, caused by supply disturbances. These price changes manifest themselves in sudden upward jumps shortly followed by a rapid reversion to normal levels. These extreme spikes are a major concern for risk management of utilities, and imply an important role for financial derivatives (Geman, 2002, Carmona and Coulon, 2014).

The large variations in spot prices do not carry directly over to derivative prices. Due to the well-known Samuelson effect (Samuelson, 1965), the effects of spot market volatility on futures prices will decrease with time to delivery on the futures contract. The large spot price variations and non-storability of electricity have always prompted electricity suppliers to hedge their price risk by selling power with future delivery. Historically, energy markets have been in line with the classical Keynes-Hicks theory of “normal backwardation”, meaning that power producers have sold future power at a discount to spot prices in order to incentivize external capital to take on the producers’ risk of falling prices.

(Keynes 1930, Hicks 1939). A gradual reversal of this discount has taken place as standardized exchange-traded financial derivatives have allowed a broader investor base to participate in the risk sharing (Carmona and Coulon 2014, Bouchouev 2012). In general, reduced forward premiums caused by improved risk sharing are characteristics of efficient and well-functioning markets. When electricity producers can hedge their commercial risk, the uncertainty about returns to investments in the electrical power utilities sector decreases. This in turn decreases capital costs of 6 .

electricity investment projects, and ultimately leads to lower prices of electricity and increased investments. 3.1 THE NORDIC ENERGY MARKET This report has a special emphasis on the Nordic energy market The energy derivatives market of other parts of northern Europe is gradually moving towards the same structure as the Nordic market The Nordic market is exchange-traded and cleared by central counterparty (CCP) Multilateral and cleared markets have clear benefits in terms of risk and efficiency We will now examine the Nordic energy market in detail. This market has been a success story, and influences other European markets. At the same time, the market is particularly affected by the pending regulatory changes. Furthermore, the energy derivatives markets of other parts of northern Europe are gradually moving towards the same structure as the Nordic market.

Nasdaq Commodities lists, in addition to the Nordic market and Baltic electricity price area differential products, derivatives on electricity in the Netherlands, Germany and UK,. The Nordic market is of particular interest for three reasons. Firstly, the Nordic electricity power market is often held to be one of the most efficient, transparent and liquid electricity power markets in the world (Mork (2001), Bergman (2002, 2003), Amundsen and Bergman (2006)). Secondly, the Nordic market will be significantly affected by the regulatory changes at hand.

Thirdly, there is a trend in other European markets toward a structure similar to the one in the Nordic market. The Nordic electricity power market was deregulated in the mid 1990’s. The aim of the reform was to separate the production and sale of electricity from the transmission of electricity (the network operation). The reform led to active trading of spot electricity and derivatives by a large number of participants at the Nordic exchanges for electricity spot (currently Nord Pool Spot) and financial derivatives (currently Nasdaq Commodities).

Currently, members from around 20 countries are trading at the derivatives market at Nasdaq Commodities. Worldwide, only 40 per cent of outstanding commodities derivative contracts are exchange traded (BIS 2013, WFE 2013). Energy derivatives (not including oil) make up around 35 per cent of commodities contracts traded worldwide. It is therefore of particular interest that the Nordic energy market is to a large degree exchange traded, with trading centered on the Oslo-based Nasdaq Commodities exchange4.

Exchange traded markets are multilateral, meaning that multiple buying and selling interests may interact and contract in accordance with non-discretionary rules. This market 4 NASDAQ OMX Oslo ASA 7 . structure provides a wide range of benefits over an OTC structure, and it has been a major regulatory effort since the financial crisis to promote multilateral trading venues for financial derivatives. Multilateral markets provide transparency of prices and standardization of terms, and subsequently efficient price discovery, increased liquidity and decreased trading costs. 4 REGULATION OF CENTRAL CLEARING IN ENERGY DERIVATIVES MARKETS A major policy objective has been to move derivatives market to multilateral and cleared venues In September 2009, the G20 leaders meeting in Pittsburgh agreed that: “All standardized OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest.” In Europe, the European Market Infrastructure Regulation (EMIR) dictates the details of central clearing. Article 46 of EMIR allows nonfinancial clearing members to post bank guarantees as collateral for a) Derivatives relating to electricity or natural gas produced, traded or delivered in the Union b) Derivatives relating to the transportation of electricity or natural gas in the Union Pending regulatory changes will affect energy markets The European Securities and Markets Authority (ESMA) specifies the conditions for accepting bank guarantees in their technical standards. These standards specify, among other requirements, that commercial bank guarantees must be “fully backed by collateral”, a requirement that market participants claim, in practice, negates the use of commercial bank guarantees (European Association of CCP Clearing Houses, 2014). An exemption period was granted for commodity markets in 2013. This period will expire in March 2016. There is an ongoing initiative to make the exemption permanent, by policymakers, regulators and the energy industry.

During the legislative procedure in 2012, the four Nordic financial supervisory authorities (FSAs) requested in a letter to ESMA that the requirements prohibiting use of non-fully backed commercial bank guarantees be removed. In 2015, seven governments in the Nordic and Baltic region (Sweden, Denmark, Finland, Norway, Estonia, Latvia and Lithuania) urged the European Commission to reconsider the ban on non-fully backed commercial bank guarantees as collateral. 8 . The Working Party on Bank Guarantees in European Energy Markets, The Union of the Electricity Industry (Eurelectric), EACH (European Association of CCP), European Federation of Energy Traders (EFET) and Eurogas have also sent letters to the European Commission in which they urge the European Commission to reconsider the ban on non-fully backed commercial bank guarantees as collateral. 5 CENTRAL MARKET CLEARING IN THE NORDIC In this section, we discuss the details of central clearing with a special emphasis on the Nordic market. Furthermore, we analyze bank guarantees in central clearing. In the final subsection, we examine the important role of central counterparties in tackling systemic risk. 5.1 OVERVIEW OF CENTRAL CLEARING IN THE NORDIC MARKET A central counterparty (CCP) is an entity that interposes itself between counterparties to contracts traded in a financial or physical market, becoming the buyer to every seller and the seller to every buyer, thereby guaranteeing the performance of all contracts. Central counterparties provide significant risk-reducing benefits due to improved oversight of market participants and the coordinated management of open positions following the default of a market participant (Milne 2012, Wendt 2015). Following the financial crisis in 2008, a major regulatory effort has been focused on imposing mandatory central counterparty clearing in derivative markets. The participants in the energy market is primarily the suppliers and demanders of electricity The participants in the market for financial derivatives on Nordic power are primarily the suppliers and demanders of electricity (i.e. the producers and wholesale consumers).

In this aspect the energy markets differ from financial markets in general, as participants in other financial markets to a large extent are banks, dealers and other financial institutions. This can be confirmed by a mere glance at figure 3. The figure show the relative share of financial versus nonfinancial firms, for major OTC derivatives markets and for the Nordic power market. 9 .