Description

DEAL LAWYERS

Vol. 10, No. 2

March-April 2016

Spin-Offs: Frequently Asked Questions

By Eric Krautheimer, John Savva and Davis Wang, Partners of Sullivan & Cromwell LLP

Like many cycles in the M&A world, spin-offs come and go. At the moment, spin-offs (and to some

extent split-offs) appear to continue to be something that many companies are considering.

Over 100 spin-offs and similar transactions were announced in 2014 and 2015. For example, eBay spun-off PayPal, Hewlett-Packard spun-off its PC and printer business, Yahoo! initially announced its intention to spin-off its majority stake in Alibaba and subsequently announced that it was suspending work on the spin-off, Symantec announced its intention to spin-off Veritas Software (but instead eventually agreed to sell the business, something that happens from time to time) and Madison Square Garden completed a spin-off in which it separated its cable networks from the rest of its operations. Spin-offs allow companies to get out of certain business while often giving their shareholders value on a “tax-free” basis. Below are some FAQs with respect to spin-offs covering some of the basic and preliminary questions that companies considering spin-offs may have. What is a spin-off? A spin-off is a distribution (dividend) by a company (“parent”) of the shares of a subsidiary (“spin-co”) to the shareholders of parent, pro rata in accordance with their common stock ownership.

Parent may decide to spin-off all or a portion of the shares that it holds, and the spin-off could be preceded by an IPO of spin-co (raising some proceeds for parent and creating a trading market for spin-co) followed by the distribution of the remaining shares of spin-co to the shareholders of parent. Tax considerations are extremely important and are likely to guide the manner in which the spin-off is executed. What is a split-off? A split-off involves a distribution to shareholders of a subsidiary, but is implemented by way of an exchange offer whereby parent offers shares in spin-co in exchange for the shares of parent. In this case parent is using spin-co shares as consideration for the repurchase of parent’s stock. A split-off is generally preceded by an IPO of spin-co to establish a market price for spin-co stock and to determine an appropriate exchange ratio.

Often an inducement is provided for making the exchange TABLE OF CONTENTS – Spin-Offs: Frequently Asked Questions . . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . 1 – More Reminders That “Boilerplate” Matters .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

6 – Short-Term Investment Strategies Can Create Board Conflicts of Interest . . .

. . .

. . .

. . .

. . .

8 – Delaware’s Latest M&A Export to Other States: Streamlined Tender Offers & Section 251(h) . . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

11 – A Russian Proverb Explains Investor Approaches to Risk Management . . .

. . .

. . .

. . .

. . .

. 12 © 2016 Executive Press, Inc. DealLawyers.com • P.O. Box 1549 • Austin, TX 78767 • (925) 685-5111 • Fax (925) 930-9284 • info@DealLawyers.com ISSN 1944-7590 .

(i.e., the shares of parent are acquired at a premium to their market price). Generally, if there is a failure to receive a full subscription to the offer, the remaining shares of spin-co are distributed pro rata to parent shareholders. In these FAQs, we refer generally to spin-offs, although most of the considerations discussed also apply to split-offs. What are some of the factors contributing to the frequency of spin-offs in recent years? Spin-offs are pursued for a variety of reasons. Spin-offs often create significant incremental market value, including by enhancing management focus on, and increased investor awareness of, spin-co.

Spin-offs can eliminate conflicts of interest between spin-co and parent and provide spin-co with strategic autonomy and its own acquisition currency. A recent study by The Boston Consulting Group1 concluded that spin-offs generate cumulative abnormal returns that have exceeded those generated by selling spin-co in an IPO or to a strategic or financial buyer. Pressure from activist investors has also increased the prevalence of spin-off activity and the frequency with which Boards of Directors are called upon to review spin-offs as well as other restructuring activities. Is a spin-off taxable? A spin-off or split-off is generally completed in a manner that is non-taxable to the companies and to the shareholders receiving the spin-co shares. The tax rules relating to spin-offs and split-offs are complicated, and tax attorneys should be consulted prior to commencing any work on a spin-off process. Will a private letter ruling be obtained from the IRS in connection with a spin-off? Historically, taxpayers have frequently sought private letter rulings from the IRS addressing spin-offs that are intended to qualify as tax-free; taxpayers then obtain an opinion from counsel on spin-off requirements that are not addressed by the ruling. In 2013, the IRS modified its ruling practice to limit the ability to obtain the previously-sought rulings in many cases.

This development has increased the relative number of spinoffs that are completed relying solely on opinions of counsel. However, as a practical matter, taxpayers do still tend to favor seeking a ruling where possible, if for no other reason than the “halo” effect from having obtained a ruling. In September 2015, the IRS indicated that it will suspend issuing rulings in three types of situations: (1) spinoffs involving a conversion into a REIT or RIC (common in so-called “opco propco structures”), (2) spinoffs where the assets constituting the required “active trade or business” account for less than 5% of the value of the gross assets of each of parent and spinco, and (3) spinoffs involving substantial investment assets that are “skewed” between parent and spinco and where the assets constituting the “active trade or business” are less than 10% of the fair market value of the investment assets. The IRS indicated that it is studying these issues and could issue future guidance that is potentially adverse with respect to the “no rule” fact patterns. How can spin-offs provide financing for the parent company? A variety of structures have been used in conjunction with spin-offs to provide financing for parent.

For example, spin-co may incur indebtedness prior to the spin-off and distribute the proceeds to parent. Alternatively, prior to the spin-off, spin-co may conduct an IPO and distribute the proceeds to parent, or parent may sell a portion of its ownership to the public directly in a secondary offering. A spin-off may also be coupled with a private equity investment (for less than 50% of spin-co), with parent realizing the economic benefit of such proceeds. In addition, parent may use spin-co debt or equity to retire parent debt, although the ability to do so for recently-issued debt for parent has been limited by IRS’s ruling policy. The structure used is often driven by tax considerations, including those relating to preserving the tax-free nature of the spin-off and those Creating Superior Value Through Spin-Offs, February 08, 2016 by Jeff Kotzen, Felix Stellmaszek, Jeff Gell, Daniel Friedman, and Karthik Valluru. 1 Deal Lawyers March-April 2016 2 .

relating to the potential that subsidiary distributions to parent in excess of the parent’s basis in spin‑co’s stock is taxable. If significant debt is incurred, fraudulent conveyance concerns will be increased. In addition, tax considerations may favor reversing the direction of the spin-off to achieve the optimal monetization strategy, and the use of that structure could raise additional debt covenant, consent and other concerns. What are the considerations involved in conducting an IPO of a subsidiary prior to a spin-off? An IPO of spin-co prior to a spin-off allows an investor base to form for spin-co prior to the distribution or exchange of spin-co shares to parent stockholders and also establishes a value for spin-co shares that can be used to calculate an appropriate exchange ratio for a split-off. In addition, an IPO can raise proceeds to finance spin-co, parent or both. In order to preserve the ability to complete the spin-off on a tax free basis, parent must continue to own 80% or more of the voting power of spin-co’s voting stock after the IPO, and such IPOs have, therefore, generally been limited to 20% of spin-co’s stock. Also, recent ruling guidelines restricting the use of high-vote/low-vote stock have limited the ability to issue shares in an IPO representing more than 20% of the economic interest in spin-co.

Following the IPO of spin-co and prior to the spin-off, parent will be a controlling shareholder of spin-co and have fiduciary duties to spin-co’s public shareholders. As a result, the contractual arrangements between parent and spin-co relating to the spin-off should be in place at the time of the spin-off. What are the securities law implications of a spin-off? Generally, spin-offs can be completed without registration of spin-co’s stock under the Securities Act (the SEC’s Staff Legal Bulletin No. 4 describes the conditions to ensure Securities Act registration is not required).

However, an Exchange Act registration statement on Form 10, which will need to be declared effective by the SEC, is generally necessary to complete a spin-off. The Form 10 will contain an information statement that is distributed to shareholders of parent. If the spin-off is preceded by an IPO, then a Securities Act registration statement on Form S-1 will be necessary for the issuance of the spin-co stock in the IPO, but a full Form 10 filing is not required. A split-off requires a Securities Act registration statement as well as tender offer documents. The registration statement on Form 10 contains disclosure requirements that are similar to the disclosure requirements applicable to a registration statement under the Securities Act in an IPO.

The Form 10 will be subject to review and comment by the SEC Staff, as would any Securities Act registration statement. What are some of the complexities involved in separating the business to be spun-off from the parent? In effecting a spin-off, the business and assets to be spun-off must be separated and placed in a separate legal entity. Even if that business has been historically operated in a separate subsidiary, additional assets frequently need to be transferred into or out of the subsidiary prior to the spin-off. These asset transfers frequently require third-party consents or governmental approvals and may raise complex structuring issues. The appropriate capital structure of spin-co will need to be determined, and cash, debt and other liabilities may need to be allocated between parent and spin-co.

Also, complicated operational arrangements may need to be put together to ensure that the business continues to function. What consideration should be given to the solvency of the parent and spin-co in connection with a spin-off? In connection with a spin-off, it is important to consider the solvency of both the parent and spin-co after giving effect to inter-company transfers, the incurrence of indebtedness and the consummation of the spin-off. Some of the inter-company transactions (including dividends of spin-co to parent and by parent of spin-co stock to parent’s stockholders) may not be for reasonably equivalent value and may be 3 Deal Lawyers March-April 2016 . susceptible to challenge as constructive fraudulent transfers if the transferor is not solvent after giving effect to the transfer. Spin-offs that impair creditors’ ability to enforce their debts may be challenged as involving actual fraud. Separate but inter-dependent steps of a transaction may be collapsed for purposes of these analyses. Depending on the circumstances, it may be appropriate and helpful to obtain one or more third-party solvency opinions. In addition, spin-offs involve one or more transactions that are dividends under state corporation laws, including the distribution of spin-co shares to parent stockholders and, potentially, the distribution by spin-co of assets to its parent. Under Delaware law, for example, such dividends may be paid only out of surplus or the net profits of the company for the fiscal year in which the dividend is paid and/or for the preceding fiscal year. Directors of a corporation who act negligently in connection with the approval of an unlawful dividend may be held personally liable. However, directors are entitled to rely in good faith on the opinions of experts as to the availability of surplus or other funds from which a dividend may be paid and, accordingly, it is frequently prudent for a Board of Directors to obtain a valuation report or opinion from a financial expert to support a conclusion that a lawful source exists for those dividends.

Although a split-off involves an exchange of spin-co stock for shares of parent rather than a dividend, state corporation laws generally require that such repurchases not impair the capital of parent, which has a similar effect as the restriction on dividends. How do I execute a spin-off? The securities laws documents discussed above will need to be filed and disseminated. In the case of a spin-off (but not a split-off ), a dividend will need to be declared by the board of the parent. The stock of spin-co will need to be listed for trading.

Agreements will need to be put into place to document the actions required and, if necessary, to allocate assets and liabilities and establish necessary contractual relationships between spin-co and parent. In certain cases (discussed below), approval by parent shareholders may be required. Third-party consents and regulatory approvals may need to be obtained. What documentation do I need to complete a spin-off/split-off? There are a number of categories of documentation required.

In addition to the securities law documentation discussed above and the documentation needed in connection with spin-co becoming public through the spin-off (or a prior IPO), there are a number of documents required to establish the relevant arrangements between spin-co and parent, including the following: – Separation Agreement (allocating assets and liabilities between spin-co and parent) – Employee Matters Agreement (dividing up employee liabilities and potentially requiring certain commitments) – Tax Matters Agreement (allocating historic tax liabilities and containing the arrangements that would apply in the event that the spin-off fails to maintain “tax free” treatment) – Litigation Matters Agreement (allocating responsibility for litigation) – Transition Services Agreement (providing for post-spin-off services until the companies can fully separate) – Intellectual Property Matters Agreement (usually containing cross-licenses for intellectual property, potentially on only a transition basis) – Other necessary commercial arrangements Do my shareholders need to approve a spin-off? Under Delaware law, the generally accepted view is that a spin-off is not a “sale, lease or exchange” of property or assets of the parent that may implicate the requirement to obtain shareholder approval. In contrast, it is likely that a split-off would be viewed as involving an “exchange” under Delaware Deal Lawyers March-April 2016 4 . law and would, therefore, require shareholder approval if spin-co constitutes all or substantially all of parent’s assets. In other jurisdictions, the relevant corporations statutes and case law may require shareholder approval of a spin-off or a split-off if spin-co constitutes all or substantially all of the assets of parent. Do I need to be worried about breaching any contracts to complete the spin-off? A spin-off may have a variety of contractual implications. Contracts assigned to spin-co may require the counterparty’s consent to the assignment. To the extent that parent and spin-co both require rights under a contract, new contracts with third parties providing for the separation of contractual rights may be required. Contracts that are assigned to spin-co, as well as those to which spin-co is already a party, need to be reviewed to determine whether they contain change-of-control provisions that may be implicated. Parent’s credit facilities, indentures, leases, severance agreements, IP licenses and other agreements must be reviewed to determine whether they contain restrictions or other provisions (such as financial covenants or restrictions on material asset sales, dividends or related party transactions) that are implicated by the spin-off, the restructuring activities conducted in contemplation of the spin-off or the relationships between parent and spin-co following the spin-off. What are the implications of announcing a plan to spin-off spin-co on the ability to negotiate with a third party that may be interested in acquiring parent or spin-co after the spin-off? In order to preserve the tax-free nature of the spin-off, it is generally critical that discussions regarding an acquisition of parent or spin-co do not occur until after the spin-off is completed to ensure that the acquisition is not considered part of the same “plan” as the spin-off.

If discussions have already occurred before the spin-off, it is generally necessary that discussions do not resume for six months or one year after the spin-off. In contrast, a potential acquirer that had not engaged in such discussions with parent or spin-co for at least 2 years prior to the spin-off could generally begin discussions immediately following the spin-off, but should proceed with caution. These limitations do not generally apply to a so-called “Reverse Morris Trust” or RMT transaction if the consideration for the acquisition is solely acquirer stock that represents more than 50% of the acquirer’s outstanding common stock (i.e., if the acquirer is smaller than the company, whether parent or spinco, that it is acquiring). In that limited situation, the acquisition could be completed as part of the same plan as the spin-off without affecting the tax-free nature of the spin-off.

Acquirers are generally likely to be advised regarding these restrictions and (absent use of the RMT structures) are likely to defer approaching parent or spin-co to discuss an acquisition until after completion of the spin-off. In addition, the tax sharing agreement between parent and spin-co will typically allocate responsibility for spin-off taxes to the party that breached such “plan” requirements, thus imposing the appropriate incentives for the parties to comply. It is typical (but not universal) in such arrangements that parent consent (or an IRS ruling or an unqualified opinion of counsel) is required before spin-co can be acquired within the 2-year period after the spin-off. 5 Deal Lawyers March-April 2016 . More Reminders That “Boilerplate” Matters By Christopher E. Austin, Robert P. Davis, Mitchell A. Lowenthal and Aaron J.

Meyers of Cleary Gottlieb Steen & Hamilton LLP Acquisition agreements in private M&A transactions frequently contain language that purports to limit the purchaser’s recourse against the seller for extra-contractual misrepresentations, even if fraudulent, in order to allocate among the parties the risk of potential post-closing losses. Such limitations on liability are generally enforceable under Delaware law when they have been specifically negotiated between sophisticated parties, and are commonly implemented through a combination of a so-called “entire agreement” integration clause, an “exclusive representation” provision and, in the case of an acquisition agreement providing expressly for indemnification rights, an “exclusive remedy” provision. Three recent opinions by Delaware’s lower courts have addressed the enforceability of specific implementations of disclaimers of extra-contractual liability.

Together, these decisions underscore the importance of carefully drafting these often-overlooked provisions. TrueBlue In TrueBlue, Inc. et al. v.

Leeds Equity Partners IV, LP, memo. op. (Del.

Super. Sept. 25, 2015), the purchaser acquired the shares of a company that had a liability (an obligation to make an “earn-out” payment to the former owners of a previously acquired company) that became payable after completion of the acquisition. The purchaser alleged, among other things, that in the course of negotiating the acquisition agreement the seller had made a fraudulent promise, separate from the acquisition agreement, to the effect that the seller would satisfy the earn-out obligation when it became payable. One of the requirements of a prima facie fraud claim is reasonable reliance on a false statement (in this case, the seller’s alleged promise to satisfy the earn-out obligation), and the Delaware Superior Court’s decision turned on whether the purchaser’s reliance could have been reasonable.

In addition to an integration clause, the acquisition agreement contained a somewhat unusual “exclusive representation” provision in which the purchaser affirmatively acknowledged that the representations and warranties in the acquisition agreement superseded any other statement made to the purchaser. Applying the relatively plaintiff-friendly standard used in considering motions to dismiss, the court refused to dismiss the purchaser’s fraud claim, noting that the “exclusive representation” provision did not “clearly state that the parties disclaim reliance upon extra-contractual statements.” Prior Delaware cases, including Abry Partners V, L.P. v. F&W Acquisition LLC, et al.

(Del. Ch. 2006), had held a specific acknowledgement of non-reliance to be necessary in order to avoid fraud claims based on extra-contractual statements. The court also noted that the acquisition agreement contained an exception to its “exclusive remedy” provision (i.e., the provision stating that the seller’s indemnity would be the purchaser’s sole post-closing recourse), and that exception permitted non-indemnity-based claims for “actual fraud”.

The court referred to this language as indicating that fraud claims were expressly contemplated by the parties, and may have survived even if the agreement included broader non-reliance language in its “exclusive representation” provision. Prairie Capital Prairie Capital III, LP v. Double E Holding Corp. (Del.

Ch. Nov. 25, 2015) arose out of the sale of a portfolio company by one private equity firm to another.

The purchasers asserted following closing that the sellers had, among other things, committed fraud grounded in alleged misrepresentations not contained in the acquisition agreement and in the failure to disclose the facts underlying such misrepresentations to the purchasers. The acquisition agreement contained an integration clause as well as an “exclusive representation” provision in which the purchasers stated affirmatively that they had relied on their own independent investigation and on the representations expressly set forth in the agreement. The provision also included a disclaimer of all extra-contractual representations, but did not expressly state that the purchasers had not relied on any extra-contractual representations. Deal Lawyers March-April 2016 6 . The purchasers argued that their fraud claim should survive the sellers’ motion to dismiss due to the absence in the acquisition agreement of an explicit disclaimer of “reliance” on extra-contractual representations. The purchasers’ position appeared to be somewhat consistent with the recent trajectory of Delaware case law, including True Blue, which had begun to suggest that specific phrasing was required for such a disclaimer to be effective. But the Delaware Court of Chancery was not persuaded by the purchasers’ assertions in Prairie Capital, dismissing their claim and holding that no “magic words” were required for such disclaimers to be effective so long as they “add up to a clear anti-reliance clause.” The court also rejected the purchasers’ argument that a fraud exception contained in the acquisition agreement’s “exclusive remedy” provision could form a basis for the purchasers’ extra-contractual fraudulent misrepresentation claim, concluding that the fraud exception did not address which representations the purchasers could rely on and, accordingly, did not override the “exclusive representation” provision’s limitations on the universe of information on which a fraud claim could be based. FdG Logistics The Chancery Court most recently addressed disclaimers of extra-contractual liabilities in FdG Logistics LLC v. A&R Logistics Holdings, Inc., et al.

(Del. Ch. Feb.

23, 2016), which arose out of the purchase of a trucking company by a private equity firm through a merger. The purchaser alleged that the target company “engaged in an extensive series of illegal and improper activities that were concealed from it during pre-merger due diligence” and asserted, among other things, that the selling securityholders had committed common law fraud based on alleged misrepresentations in extra-contractual materials, including a confidential information memorandum and a management presentation. The acquisition agreement included a customary integration clause and an “exclusive representation” provision, located at the end of the list of representations and warranties by the target company, pursuant to which the target company affirmatively disclaimed all extra-contractual representations. Reviewing Abry Partners and its progeny, the Chancery Court explained that an effective disclaimer must amount to a contractual promise by the purchaser that it has not relied upon extra-contractual statements by the seller. Applying this reading, the court concluded that such a disclaimer must be expressed as an affirmative statement by the aggrieved party in order to be effective.

Since the “exclusive representation” provision at issue was worded as a declaration by the target company, rather than an acknowledgment and agreement by the purchaser, and since the integration clause “does not contain an unambiguous statement by [the purchaser] disclaiming reliance on extra-contractual statements”, the court denied the motion to dismiss the purchaser’s extra-contractual fraud claim. Conclusion Most purchase agreements in private M&A transactions contain some formulation of the provisions mentioned above and, in Delaware, a seller should be able to insulate itself from claims of fraud based on statements outside of the acquisition agreement so long as these provisions are properly drafted. Although the Chancery Court’s decision in Prairie Capital may provide some flexibility to those drafting disclaimers of extra-contractual liability, the inconsistency in recent Delaware lower court decisions, absent further clarification from the Delaware Supreme Court, cautions practitioners to continue to draft these provisions as unambiguously as possible. In particular, we continue to recommend that an acquisition agreement contain a standard integration clause along with an acknowledgment by the purchaser expressly disclaiming the existence of, and any reliance by the purchaser on, any representations from the seller other than those expressly set forth in the agreement (including in particular any representations as to the “accuracy or completeness” of the information made available to the purchaser). In addition, any “fraud” exception to the “exclusive remedy” provision should be carefully tailored to permit only fraud claims based on the representations and warranties included in the acquisition agreement and not claims based on extra-contractual statements. 7 Deal Lawyers March-April 2016 .

Short-Term Investment Strategies Can Create Board Conflicts of Interest By Steven Haas, Partner, Hunton & Williams LLP* Last year was reportedly a record-setting year for stockholder activism in the United States. Activist campaigns were at an all-time high.1 Some of these campaigns resulted in proxy contests in which the activist hedge fund was successful. Many more, however, resulted in a settlement in which the company agreed to name one or more of the hedge fund’s nominees to the board of directors. While these nominees may be “independent” of management and satisfy applicable stock exchange listing standards, they may be deemed “interested” under state corporate laws when acting as directors in specific circumstances. This issue arose last Fall in PLX Technology,2 where the Delaware Court of Chancery upheld a claim that a director who voted to approve a merger had a conflict of interest.

The alleged conflict centered on the director’s affiliation with an activist hedge fund focused on short-term gains. In refusing to dismiss the complaint, Vice Chancellor J. Travis Laster placed significant weight on the incumbent board’s “fight letters” during a proxy contest, which argued that the hedge fund was pursuing a quick sale of the company to advance its own interests at the expense of other stockholders. The court’s finding that pursuing short-term investment strategies—which are frequently associated with activist hedge funds—can give rise to a conflict of interest represents a significant development in the ongoing debate surrounding activist investing.

Activist investors often seek board representation in parallel with their aggressive advocacy of short-term gains. When these two elements converge, the court’s ruling counsels incumbent boards and activist designees to carefully consider the takeaway lessons described below, especially in the context of a board’s consideration of any significant transaction after the activist’s representatives join the board. Background The decision in PLX arose from a post-closing challenge to the $300 million sale of PLX Technology (“PLX” or the “Company”). Prior to the transaction, PLX had lost a proxy contest led by Potomac Capital, an activist hedge fund that advocated a sale of the company.

In public letters to its stockholders during the proxy contest, PLX accused Potomac of being a “self-interested activist investor that is focused on short-term gains at the expense” of other stockholders. It also claimed that Potomac’s “primary goal is to force a quick sale of the Company in order to realize a short-term gain on its investment.” The proxy contest resulted in the election of three of Potomac’s nominees, including one of its principals. Approximately six months after the proxy contest, PLX entered into a merger agreement with a third party. PLX stockholders challenged the merger claiming, among other things, that the board of directors did not obtain the best price reasonably available. The plaintiffs also alleged that certain directors, including Potomac’s principal who represented the hedge fund on PLX’s board, had a conflict of interest. The Court of Court’s Ruling In a bench ruling, the court held that the stockholder-plaintiffs had stated a claim for breach of fiduciary duty against most of PLX’s directors.

Of particular significance, the court held that Potomac’s principal was a “dual fiduciary” by virtue of his status as both a PLX director and a principal of the hedge fund. The court acknowledged that large stockholders typically do not have a conflict of interest when they are treated equally in a sale of the company because their interest, like that of the rest of the stockholders, *The views expressed in this article are solely those of the author and not his firm or its clients. John Laide, SharkRepellent.net, Record-Setting Year for Activism (Dec. 15, 2015), at https://www.sharkrepellent.net/request?an=dt.getPage&st=undefined&pg=/pub/rs_20151215.html&rnd=774545. 1 2 In re PLX Technology Inc. Stockholders Litigation, C.A.

No. 9880-VCL, trans. ruling (Del.

Ch. Sept. 3, 2015). Deal Lawyers March-April 2016 8 .

should be to maximize the value of their shares.3 The court explained, however, that this presumption of aligned interests can be rebutted by specific facts. In PLX, the court relied in large part on the incumbent directors’ public fight letters in the proxy contest to conclude that Potomac’s principal might have a conflict of interest. Both Delaware law and federal securities laws require accuracy in a company’s public statements to stockholders. The court therefore took the board’s prior statements at face value. In particular, the incumbent directors had repeatedly stated that Potomac was willing to sell PLX at an inopportune time to advance its own interests at the expense of long-term stockholder value.

The court explained that, as specifically alleged in the complaint, “the board believed and represented that Potomac was a short-term investor that had a disparate investment horizon, was trying to get a short-term sale event from which it would benefit primarily because of its low basis, and that it had interests that were different from those of the stockholders as a whole” (emphasis added).4 The court analogized the hedge fund principal’s situation to a “golden leash” arrangement because he allegedly “was getting paid for a near-term event,” which gave him an incentive that differed from those of the other directors. The court also held that the plaintiffs stated a claim against the incumbent outside directors. The court said the complaint adequately alleged that they “did not engage in the sale process entirely because it was in the best interests of the stockholders but rather did so … because of Potomac and [its principal’s] badgering.” The court cautioned that the ruling against the incumbent outside directors was a “very close” call. The most important allegation to the court was that, when previously confronted by a proxy contest from a different hedge fund, PLX’s board had the same response: it initially resisted a sale of the Company and then shifted to support one.

The court granted the motion to dismiss with respect to the two independent directors who were nominated by Potomac. The court said they did not have divided loyalties and there were no allegations that they were badgered into the sale process. Takeaways PLX is a fact-dependent case that arose out of unusual circumstances and was issued on a plaintiff-friendly pleading standard. Other allegations not discussed above also factored into the court’s decision, including claims that management’s internal projections were manipulated to justify the sale process and that the board of directors did not appropriately address conflicts of interest of its financial advisor.

Still, there are several important takeaways from this ruling with respect to activist hedge funds. Activist Hedge Fund Strategies May Create Conflicts of Interest PLX addressed a pressing corporate governance at the forefront of almost every fight between a company and an activist hedge fund—namely, whether the activist is pursuing short-term gains at the expense of long-term stockholder value. Activist hedge funds frequently push companies to implement strategies intended to generate near-term returns, such as a leveraged recapitalization or a sale of the company. The PLX court held that an activist’s short-term investment strategy can, under certain circumstances, create a conflict of interest for a director.5 Although hedge funds (as stockholders) may not owe fiduciary duties, See, e.g., Iroquois Master Fund, Ltd.

v. Answers Corp., 105 A.3d 989, n.1 (Del. 2014) (ORDER) (“When a large stockholder supports a sales process and receives the same per share consideration as every other stockholder, that is ordinarily evidence of fairness, not of the opposite, especially because the support of a large stockholder for the sale helps assure buyers that it can get the support needed to close the deal.”); In re Synthes, Inc.

S’holder Litig., 50 A.3d 1022 (Del. Ch. 2012) (concluding that a controlling stockholder did not have a conflict of interest where all shares received the same consideration); In re CompuCom Sys.

Stockholders Litig., 2005 Del. Ch. LEXIS 145 (Sept. 29, 2005) (same); In re Schawk, Inc.

S’holders Litig., Consol. C.A. No.

9510-VCL, trans. ruling (Del. Ch.

Sept. 15, 2015) (granting a motion to dismiss where the founding family received the same consideration paid to minority stockholders); but see McMullin v. Beran, 765 A.2d 910 (Del.

2000) (denying a motion to dismiss where directors allegedly breached their duty of loyalty by approving a transaction negotiated by a controlling stockholder to satisfy its liquidity needs); N.J. Carpenters Pension Fund v. infoGROUP, Inc., 2011 Del.

Ch. LEXIS 147 (Sept. 30, 2011) (denying a motion to dismiss where directors allegedly breached their duty of loyalty by acquiescing to a sale alleged to benefit a large stockholder in need of liquidity); Tooley v.

AXA Fin., Inc., 2005 Del. Ch. LEXIS 67 (May 13, 2005) (refusing, “albeit barely,” to dismiss a claim where the plaintiff alleged that the board delayed the closing of a third party’s tender offer to accommodate the controlling stockholder’s administrative needs). 3 In its discussion, the court also referenced this law review article: William W.

Bratton & Michael L. Wachter, The Case Against Shareholder Empowerment, 158 U. PENN.

L. REV. 653 (2010). 4 See also In re Answers Corp.

S’holders Litig., Consol. C.A. No.

6170-VCN, mem. op. (Del.

Ch. Apr. 11, 2012) (refusing to dismiss complaint where certain directors allegedly had a conflict of interest in seeking liquidity for an affiliated investment fund); but see In re Answers Corp.

S’holders Litig., Consol. C.A. No.

6170-VCN, mem. op. (Del.

Ch. Feb. 3, 2014) (granting summary judgment in favor of directors). 5 9 Deal Lawyers March-April 2016 .

their board representatives, like all directors, owe fiduciary duties to the company and its stockholders. As a result, PLX is an important warning to hedge fund principals and other constituent directors sitting on boards of directors, particularly where the challenged board action is subject to enhanced judicial scrutiny such as in a change-of-control transaction.6 It’s Still Difficult for Plaintiffs to Claim that a Desire to Sell is a Disabling Conflict of Interest It bears noting that in several cases, including Synthes and Mortons, the Court of Chancery set a very high bar for stockholder-plaintiffs who claim that a sale process was improperly influenced by a large stockholder that received the same per share consideration as all other stockholders.7 Generally, plaintiffs must sufficiently allege an urgent need for liquidity (i.e., a “fire sale”) in which a large stockholder needs to sell immediately, even if at a suboptimal price. PLX does not change this law, but it does show how plaintiffs might rebut that presumption in certain circumstances. At the same time, the specific arguments made by the PLX stockholders typically would not apply to private equity firms, founding families, and other large investors that have held their shares much longer than Potomac did. Whether plaintiffs can successfully use these arguments at other companies responding to activist hedge funds remains to be seen. Lessons for Directors in Dealing with Activist Hedge Funds PLX holds several lessons for incumbent directors dealing with stockholder activists.

First, PLX shows how statements made in the heat of a proxy fight might haunt an incumbent board later. It should go without saying that just because the board opposed Potomac’s nominees and argued against Potomac’s proposals does not mean the ultimate sale of the company was a breach of fiduciary duty.8 PLX shows, however, how plaintiffs might use a board’s communications to stockholders against the directors in litigation, both to challenge a later decision and to argue that one or more directors have a conflict of interest. Moreover, this case is a reminder that directors must not let their passion in a proxy contest affect the accuracy of the company’s disclosures. Second, following a proxy contest, the directors must be cognizant that an activist’s board representatives might have a conflict of interest that needs to be addressed. In some situations, forming a special committee of independent directors might be advisable to consider the activist’s proposal.

In other situations, the activist’s representatives might need to recuse themselves from certain board deliberations. Third, directors need to remain diligent when dealing with an activist’s representatives in the boardroom. Experience indicates that many activist representatives have strong personalities and, once in the boardroom, will forcefully advocate the hedge fund’s views. In PLX, the incumbent directors were allegedly badgered into a sale of the company. Such a theory for holding outside directors liable would appear to be very difficult to prove, and the court expressed skepticism in allowing the claim to proceed.

Nevertheless, similar allegations were upheld in the 2011 decision in infoGROUP based on very unusual allegations.9 Finally, directors should be prepared to defend their decision to change course. In situations like PLX, directors should be prepared to articulate why they chartered a new corporate strategy or otherwise took a course of action that materially deviated from prior statements. Relying on outside advisors and documenting board decisions through proper meeting minutes will help build a demonstrable record to support such decisions. See also Allen C.

Goolsby & Steven M. Haas, Constituent Directors: Court Allows Company to Impose Confidentiality Restrictions on Stockholder’s Right to Designate a Director (July 8, 2015). 6 See, e.g., In re Morton’s Rest. Grp., Inc., 74 A.3d 656, 667 (Del.

Ch. 2013) (“Thus, there are only ‘narrow circumstances’ where a controlling stockholder’s desire to sell in a transaction according equal treatment to all stockholders would create a disabling conflict of interest. Those unusual circumstances ‘involve a crisis, a fire sale’ in which the pressure on the controller to sell quickly is so high that the controller imposes pressure on the corporation to artificially truncate the market check and forgo the additional value that could be brought about by making ‘logical buyers aware’ that the company is for sale and giving them a reasonable time and fair opportunity to consider whether to make an offer.”). 7 Indeed, the court stated that “you should change your mind when you get new information ….

Somebody who isn’t fanatically wed to a particular point of view should have the humility to think, ‘You know what? I may not have all the answers. I should listen to this person, and I might change my mind.’” PLX trans. ruling, at 48. 8 See N.J.

Carpenters Pension Fund v. infoGROUP, Inc., 2011 Del. Ch.

LEXIS 147 (Sept. 30, 2011) (“[I]t is reasonable to infer that [the interested director] dominated the Board Defendants through a pattern of threats aimed at intimidating them, thus rendering them non-independent for purposes of voting on the Merger.”). 9 Deal Lawyers March-April 2016 10 . Delaware’s Latest M&A Export to Other States: Streamlined Tender Offers & Section 251(h) By Paul Scrivano and Noah Kornblith of O’Melveny & Myers LLP* Delaware has been the leading jurisdiction for corporate law (particularly in relation to M&A) in the United States for decades, and it is not uncommon for legislatures and courts in other states to look to Delaware for guidance on various M&A legal issues. Delaware has also been an innovator in corporate law, including as recently as 2013 when it adopted Section 251(h) to the Delaware General Corporation Law (DGCL). Section 251(h) of the DGCL streamlined two-step acquisitions (comprised of a first-step tender or exchange offer, followed by a second-step merger) by dispensing with, in the second-step merger, the need to hold a stockholder meeting or utilize a short-form merger (if available, including via a top-up option) to squeeze out target stockholders who did not tender into the first-step tender or exchange offer. In effect, Section 251(h) removed the risk that the second-step transaction could not close immediately following the closing of the first-step tender or exchange offer. Section 251(h) has been widely used in M&A transactions since its adoption, and has significantly facilitated structuring and execution of acquisitions via tender or exchange offers. One question that many deal lawyers have had was whether any other states would follow the lead of Delaware and also adopt a statute similar to Section 251(h).

There are signs that other states are now beginning to follow suit, beginning with Maryland, Texas, and Virginia. Maryland, Texas & Virginia In 2014, Maryland enacted Section 3-106.1 of the Maryland General Corporation Law (MGCL). Section 3-106.1 of the MGCL is closely modelled on Section 251(h) of the DGCL, and even permits the offeror to be an entity other than a corporation, thereby providing increased structuring flexibility. Section 3-106.1 also specifically applies to a Maryland real estate investment trust (REIT).

Similar to the existing MGCL short-form merger provision, Section 3-106.1 contains a requirement to deliver notice of the transaction to target shareholders 30 days before the second-step merger, which notice requirement could presumably be satisfied by mailing the notice at or prior to commencing the tender offer. In 2015, Texas enacted Section 21.459(c) of the Texas Corporation Law (TCL) sub-sections of the Texas Business Organizations Code. Section 21.459(c) of the TCL also bears a strong resemblance to Section 251(h) of the DGCL. Similar to Section 3-106.1 of the MGCL, Section 21.459(c) does not require that the offeror be a corporation, and instead permits almost any entity form—including a joint venture, bank, or insurance company—to utilize Section 21.459(c). Also in 2015, Virginia enacted Section 13.1-718.G of the Virginia Stock Corporation Act (VSCA).

Notably, Section 13.1-718.G of the VSCA permits a corporation or limited liability company offeror to consummate the second-step squeeze-out transaction by way of a statutory share exchange or a merger. A second-step share exchange may be of particular use to foreign acquirers in cross-border deals (with Spain being one such jurisdiction), who—due to foreign-law corporate and tax issues—may not be able use a merger to issue acquirer shares in the transaction. While the adoption by three other states of a Section 251(h)-type provision does not in and of itself constitute a trend, it is a welcome development for deal lawyers and deal participants, dispensing with both the need for a second-step short-form merger and top-up options and the risk of a time delay between the tender offer closing and the merger closing in a two-step transaction. While Maryland, Texas, and Virginia provide some hope to deal lawyers that other jurisdictions may yet follow suit, it remains to be seen whether Section 251(h) will be more broadly adopted in other states in the next several years. *Paul Scrivano, an O’Melveny partner licensed to practice law in California and New York, and Noah Kornblith, an O’Melveny associate licensed to practice law in California, contributed to the content of this newsletter.

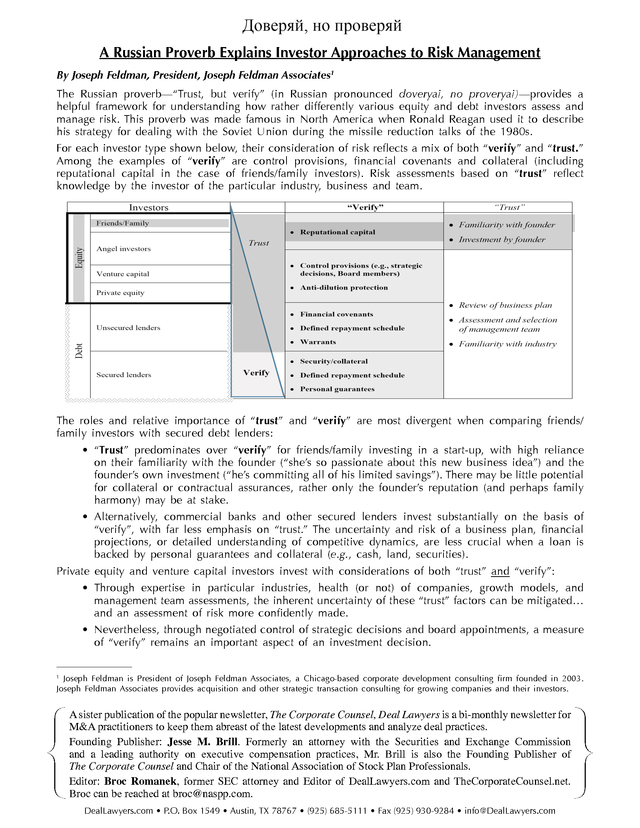

Please direct all inquiries regarding New York’s Rules of Professional Conduct to O’Melveny & Myers LLP, Times Square Tower, 7 Times Square, New York, NY, 10036, Phone:+1-212-326-2000. © 2016 O’Melveny & Myers LLP. All Rights Reserved. 11 Deal Lawyers March-April 2016 . A Russian Proverb Explains Investor Approaches to Risk Management By Joseph Feldman, President, Joseph Feldman Associates1 The Russian proverb—“Trust, but verify” (in Russian pronounced doveryai, no proveryai)—provides a helpful framework for understanding how rather differently various equity and debt investors assess and manage risk. This proverb was made famous in North America when Ronald Reagan used it to describe his strategy for dealing with the Soviet Union during the missile reduction talks of the 1980s. For each investor type shown below, their consideration of risk reflects a mix of both “verify” and “trust.” Among the examples of “verify” are control provisions, financial covenants and collateral (including reputational capital in the case of friends/family investors). Risk assessments based on “trust” reflect knowledge by the investor of the particular industry, business and team. The roles and relative importance of “trust” and “verify” are most divergent when comparing friends/ family investors with secured debt lenders: • “Trust” predominates over “verify” for friends/family investing in a start-up, with high reliance on their familiarity with the founder (“she’s so passionate about this new business idea”) and the founder’s own investment (“he’s committing all of his limited savings”). There may be little potential for collateral or contractual assurances, rather only the founder’s reputation (and perhaps family harmony) may be at stake. • Alternatively, commercial banks and other secured lenders invest substantially on the basis of “verify”, with far less emphasis on “trust.” The uncertainty and risk of a business plan, financial projections, or detailed understanding of competitive dynamics, are less crucial when a loan is backed by personal guarantees and collateral (e.g., cash, land, securities). Private equity and venture capital investors invest with considerations of both “trust” and “verify”: • Through expertise in particular industries, health (or not) of companies, growth models, and management team assessments, the inherent uncertainty of these “trust” factors can be mitigated… and an assessment of risk more confidently made. • Nevertheless, through negotiated control of strategic decisions and board appointments, a measure of “verify” remains an important aspect of an investment decision. Joseph Feldman is President of Joseph Feldman Associates, a Chicago-based corporate development consulting firm founded in 2003. Joseph Feldman Associates provides acquisition and other strategic transaction consulting for growing companies and their investors. 1 A sister publication of the popular newsletter, The Corporate Counsel, Deal Lawyers is a bi-monthly newsletter for M&A practitioners to keep them abreast of the latest developments and analyze deal practices. Founding Publisher: Jesse M.

Brill. Formerly an attorney with the Securities and Exchange Commission and a leading authority on executive compensation practices, Mr. Brill is also the Founding Publisher of The Corporate Counsel and Chair of the National Association of Stock Plan Professionals. Editor: Broc Romanek, former SEC attorney and Editor of DealLawyers.com and TheCorporateCounsel.net. Broc can be reached at broc@naspp.com. DealLawyers.com • P.O.

Box 1549 • Austin, TX 78767 • (925) 685-5111 • Fax (925) 930-9284 • info@DealLawyers.com .

Over 100 spin-offs and similar transactions were announced in 2014 and 2015. For example, eBay spun-off PayPal, Hewlett-Packard spun-off its PC and printer business, Yahoo! initially announced its intention to spin-off its majority stake in Alibaba and subsequently announced that it was suspending work on the spin-off, Symantec announced its intention to spin-off Veritas Software (but instead eventually agreed to sell the business, something that happens from time to time) and Madison Square Garden completed a spin-off in which it separated its cable networks from the rest of its operations. Spin-offs allow companies to get out of certain business while often giving their shareholders value on a “tax-free” basis. Below are some FAQs with respect to spin-offs covering some of the basic and preliminary questions that companies considering spin-offs may have. What is a spin-off? A spin-off is a distribution (dividend) by a company (“parent”) of the shares of a subsidiary (“spin-co”) to the shareholders of parent, pro rata in accordance with their common stock ownership.

Parent may decide to spin-off all or a portion of the shares that it holds, and the spin-off could be preceded by an IPO of spin-co (raising some proceeds for parent and creating a trading market for spin-co) followed by the distribution of the remaining shares of spin-co to the shareholders of parent. Tax considerations are extremely important and are likely to guide the manner in which the spin-off is executed. What is a split-off? A split-off involves a distribution to shareholders of a subsidiary, but is implemented by way of an exchange offer whereby parent offers shares in spin-co in exchange for the shares of parent. In this case parent is using spin-co shares as consideration for the repurchase of parent’s stock. A split-off is generally preceded by an IPO of spin-co to establish a market price for spin-co stock and to determine an appropriate exchange ratio.

Often an inducement is provided for making the exchange TABLE OF CONTENTS – Spin-Offs: Frequently Asked Questions . . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . 1 – More Reminders That “Boilerplate” Matters .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

6 – Short-Term Investment Strategies Can Create Board Conflicts of Interest . . .

. . .

. . .

. . .

. . .

8 – Delaware’s Latest M&A Export to Other States: Streamlined Tender Offers & Section 251(h) . . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

11 – A Russian Proverb Explains Investor Approaches to Risk Management . . .

. . .

. . .

. . .

. . .

. 12 © 2016 Executive Press, Inc. DealLawyers.com • P.O. Box 1549 • Austin, TX 78767 • (925) 685-5111 • Fax (925) 930-9284 • info@DealLawyers.com ISSN 1944-7590 .

(i.e., the shares of parent are acquired at a premium to their market price). Generally, if there is a failure to receive a full subscription to the offer, the remaining shares of spin-co are distributed pro rata to parent shareholders. In these FAQs, we refer generally to spin-offs, although most of the considerations discussed also apply to split-offs. What are some of the factors contributing to the frequency of spin-offs in recent years? Spin-offs are pursued for a variety of reasons. Spin-offs often create significant incremental market value, including by enhancing management focus on, and increased investor awareness of, spin-co.

Spin-offs can eliminate conflicts of interest between spin-co and parent and provide spin-co with strategic autonomy and its own acquisition currency. A recent study by The Boston Consulting Group1 concluded that spin-offs generate cumulative abnormal returns that have exceeded those generated by selling spin-co in an IPO or to a strategic or financial buyer. Pressure from activist investors has also increased the prevalence of spin-off activity and the frequency with which Boards of Directors are called upon to review spin-offs as well as other restructuring activities. Is a spin-off taxable? A spin-off or split-off is generally completed in a manner that is non-taxable to the companies and to the shareholders receiving the spin-co shares. The tax rules relating to spin-offs and split-offs are complicated, and tax attorneys should be consulted prior to commencing any work on a spin-off process. Will a private letter ruling be obtained from the IRS in connection with a spin-off? Historically, taxpayers have frequently sought private letter rulings from the IRS addressing spin-offs that are intended to qualify as tax-free; taxpayers then obtain an opinion from counsel on spin-off requirements that are not addressed by the ruling. In 2013, the IRS modified its ruling practice to limit the ability to obtain the previously-sought rulings in many cases.

This development has increased the relative number of spinoffs that are completed relying solely on opinions of counsel. However, as a practical matter, taxpayers do still tend to favor seeking a ruling where possible, if for no other reason than the “halo” effect from having obtained a ruling. In September 2015, the IRS indicated that it will suspend issuing rulings in three types of situations: (1) spinoffs involving a conversion into a REIT or RIC (common in so-called “opco propco structures”), (2) spinoffs where the assets constituting the required “active trade or business” account for less than 5% of the value of the gross assets of each of parent and spinco, and (3) spinoffs involving substantial investment assets that are “skewed” between parent and spinco and where the assets constituting the “active trade or business” are less than 10% of the fair market value of the investment assets. The IRS indicated that it is studying these issues and could issue future guidance that is potentially adverse with respect to the “no rule” fact patterns. How can spin-offs provide financing for the parent company? A variety of structures have been used in conjunction with spin-offs to provide financing for parent.

For example, spin-co may incur indebtedness prior to the spin-off and distribute the proceeds to parent. Alternatively, prior to the spin-off, spin-co may conduct an IPO and distribute the proceeds to parent, or parent may sell a portion of its ownership to the public directly in a secondary offering. A spin-off may also be coupled with a private equity investment (for less than 50% of spin-co), with parent realizing the economic benefit of such proceeds. In addition, parent may use spin-co debt or equity to retire parent debt, although the ability to do so for recently-issued debt for parent has been limited by IRS’s ruling policy. The structure used is often driven by tax considerations, including those relating to preserving the tax-free nature of the spin-off and those Creating Superior Value Through Spin-Offs, February 08, 2016 by Jeff Kotzen, Felix Stellmaszek, Jeff Gell, Daniel Friedman, and Karthik Valluru. 1 Deal Lawyers March-April 2016 2 .

relating to the potential that subsidiary distributions to parent in excess of the parent’s basis in spin‑co’s stock is taxable. If significant debt is incurred, fraudulent conveyance concerns will be increased. In addition, tax considerations may favor reversing the direction of the spin-off to achieve the optimal monetization strategy, and the use of that structure could raise additional debt covenant, consent and other concerns. What are the considerations involved in conducting an IPO of a subsidiary prior to a spin-off? An IPO of spin-co prior to a spin-off allows an investor base to form for spin-co prior to the distribution or exchange of spin-co shares to parent stockholders and also establishes a value for spin-co shares that can be used to calculate an appropriate exchange ratio for a split-off. In addition, an IPO can raise proceeds to finance spin-co, parent or both. In order to preserve the ability to complete the spin-off on a tax free basis, parent must continue to own 80% or more of the voting power of spin-co’s voting stock after the IPO, and such IPOs have, therefore, generally been limited to 20% of spin-co’s stock. Also, recent ruling guidelines restricting the use of high-vote/low-vote stock have limited the ability to issue shares in an IPO representing more than 20% of the economic interest in spin-co.

Following the IPO of spin-co and prior to the spin-off, parent will be a controlling shareholder of spin-co and have fiduciary duties to spin-co’s public shareholders. As a result, the contractual arrangements between parent and spin-co relating to the spin-off should be in place at the time of the spin-off. What are the securities law implications of a spin-off? Generally, spin-offs can be completed without registration of spin-co’s stock under the Securities Act (the SEC’s Staff Legal Bulletin No. 4 describes the conditions to ensure Securities Act registration is not required).

However, an Exchange Act registration statement on Form 10, which will need to be declared effective by the SEC, is generally necessary to complete a spin-off. The Form 10 will contain an information statement that is distributed to shareholders of parent. If the spin-off is preceded by an IPO, then a Securities Act registration statement on Form S-1 will be necessary for the issuance of the spin-co stock in the IPO, but a full Form 10 filing is not required. A split-off requires a Securities Act registration statement as well as tender offer documents. The registration statement on Form 10 contains disclosure requirements that are similar to the disclosure requirements applicable to a registration statement under the Securities Act in an IPO.

The Form 10 will be subject to review and comment by the SEC Staff, as would any Securities Act registration statement. What are some of the complexities involved in separating the business to be spun-off from the parent? In effecting a spin-off, the business and assets to be spun-off must be separated and placed in a separate legal entity. Even if that business has been historically operated in a separate subsidiary, additional assets frequently need to be transferred into or out of the subsidiary prior to the spin-off. These asset transfers frequently require third-party consents or governmental approvals and may raise complex structuring issues. The appropriate capital structure of spin-co will need to be determined, and cash, debt and other liabilities may need to be allocated between parent and spin-co.

Also, complicated operational arrangements may need to be put together to ensure that the business continues to function. What consideration should be given to the solvency of the parent and spin-co in connection with a spin-off? In connection with a spin-off, it is important to consider the solvency of both the parent and spin-co after giving effect to inter-company transfers, the incurrence of indebtedness and the consummation of the spin-off. Some of the inter-company transactions (including dividends of spin-co to parent and by parent of spin-co stock to parent’s stockholders) may not be for reasonably equivalent value and may be 3 Deal Lawyers March-April 2016 . susceptible to challenge as constructive fraudulent transfers if the transferor is not solvent after giving effect to the transfer. Spin-offs that impair creditors’ ability to enforce their debts may be challenged as involving actual fraud. Separate but inter-dependent steps of a transaction may be collapsed for purposes of these analyses. Depending on the circumstances, it may be appropriate and helpful to obtain one or more third-party solvency opinions. In addition, spin-offs involve one or more transactions that are dividends under state corporation laws, including the distribution of spin-co shares to parent stockholders and, potentially, the distribution by spin-co of assets to its parent. Under Delaware law, for example, such dividends may be paid only out of surplus or the net profits of the company for the fiscal year in which the dividend is paid and/or for the preceding fiscal year. Directors of a corporation who act negligently in connection with the approval of an unlawful dividend may be held personally liable. However, directors are entitled to rely in good faith on the opinions of experts as to the availability of surplus or other funds from which a dividend may be paid and, accordingly, it is frequently prudent for a Board of Directors to obtain a valuation report or opinion from a financial expert to support a conclusion that a lawful source exists for those dividends.

Although a split-off involves an exchange of spin-co stock for shares of parent rather than a dividend, state corporation laws generally require that such repurchases not impair the capital of parent, which has a similar effect as the restriction on dividends. How do I execute a spin-off? The securities laws documents discussed above will need to be filed and disseminated. In the case of a spin-off (but not a split-off ), a dividend will need to be declared by the board of the parent. The stock of spin-co will need to be listed for trading.

Agreements will need to be put into place to document the actions required and, if necessary, to allocate assets and liabilities and establish necessary contractual relationships between spin-co and parent. In certain cases (discussed below), approval by parent shareholders may be required. Third-party consents and regulatory approvals may need to be obtained. What documentation do I need to complete a spin-off/split-off? There are a number of categories of documentation required.

In addition to the securities law documentation discussed above and the documentation needed in connection with spin-co becoming public through the spin-off (or a prior IPO), there are a number of documents required to establish the relevant arrangements between spin-co and parent, including the following: – Separation Agreement (allocating assets and liabilities between spin-co and parent) – Employee Matters Agreement (dividing up employee liabilities and potentially requiring certain commitments) – Tax Matters Agreement (allocating historic tax liabilities and containing the arrangements that would apply in the event that the spin-off fails to maintain “tax free” treatment) – Litigation Matters Agreement (allocating responsibility for litigation) – Transition Services Agreement (providing for post-spin-off services until the companies can fully separate) – Intellectual Property Matters Agreement (usually containing cross-licenses for intellectual property, potentially on only a transition basis) – Other necessary commercial arrangements Do my shareholders need to approve a spin-off? Under Delaware law, the generally accepted view is that a spin-off is not a “sale, lease or exchange” of property or assets of the parent that may implicate the requirement to obtain shareholder approval. In contrast, it is likely that a split-off would be viewed as involving an “exchange” under Delaware Deal Lawyers March-April 2016 4 . law and would, therefore, require shareholder approval if spin-co constitutes all or substantially all of parent’s assets. In other jurisdictions, the relevant corporations statutes and case law may require shareholder approval of a spin-off or a split-off if spin-co constitutes all or substantially all of the assets of parent. Do I need to be worried about breaching any contracts to complete the spin-off? A spin-off may have a variety of contractual implications. Contracts assigned to spin-co may require the counterparty’s consent to the assignment. To the extent that parent and spin-co both require rights under a contract, new contracts with third parties providing for the separation of contractual rights may be required. Contracts that are assigned to spin-co, as well as those to which spin-co is already a party, need to be reviewed to determine whether they contain change-of-control provisions that may be implicated. Parent’s credit facilities, indentures, leases, severance agreements, IP licenses and other agreements must be reviewed to determine whether they contain restrictions or other provisions (such as financial covenants or restrictions on material asset sales, dividends or related party transactions) that are implicated by the spin-off, the restructuring activities conducted in contemplation of the spin-off or the relationships between parent and spin-co following the spin-off. What are the implications of announcing a plan to spin-off spin-co on the ability to negotiate with a third party that may be interested in acquiring parent or spin-co after the spin-off? In order to preserve the tax-free nature of the spin-off, it is generally critical that discussions regarding an acquisition of parent or spin-co do not occur until after the spin-off is completed to ensure that the acquisition is not considered part of the same “plan” as the spin-off.

If discussions have already occurred before the spin-off, it is generally necessary that discussions do not resume for six months or one year after the spin-off. In contrast, a potential acquirer that had not engaged in such discussions with parent or spin-co for at least 2 years prior to the spin-off could generally begin discussions immediately following the spin-off, but should proceed with caution. These limitations do not generally apply to a so-called “Reverse Morris Trust” or RMT transaction if the consideration for the acquisition is solely acquirer stock that represents more than 50% of the acquirer’s outstanding common stock (i.e., if the acquirer is smaller than the company, whether parent or spinco, that it is acquiring). In that limited situation, the acquisition could be completed as part of the same plan as the spin-off without affecting the tax-free nature of the spin-off.

Acquirers are generally likely to be advised regarding these restrictions and (absent use of the RMT structures) are likely to defer approaching parent or spin-co to discuss an acquisition until after completion of the spin-off. In addition, the tax sharing agreement between parent and spin-co will typically allocate responsibility for spin-off taxes to the party that breached such “plan” requirements, thus imposing the appropriate incentives for the parties to comply. It is typical (but not universal) in such arrangements that parent consent (or an IRS ruling or an unqualified opinion of counsel) is required before spin-co can be acquired within the 2-year period after the spin-off. 5 Deal Lawyers March-April 2016 . More Reminders That “Boilerplate” Matters By Christopher E. Austin, Robert P. Davis, Mitchell A. Lowenthal and Aaron J.

Meyers of Cleary Gottlieb Steen & Hamilton LLP Acquisition agreements in private M&A transactions frequently contain language that purports to limit the purchaser’s recourse against the seller for extra-contractual misrepresentations, even if fraudulent, in order to allocate among the parties the risk of potential post-closing losses. Such limitations on liability are generally enforceable under Delaware law when they have been specifically negotiated between sophisticated parties, and are commonly implemented through a combination of a so-called “entire agreement” integration clause, an “exclusive representation” provision and, in the case of an acquisition agreement providing expressly for indemnification rights, an “exclusive remedy” provision. Three recent opinions by Delaware’s lower courts have addressed the enforceability of specific implementations of disclaimers of extra-contractual liability.

Together, these decisions underscore the importance of carefully drafting these often-overlooked provisions. TrueBlue In TrueBlue, Inc. et al. v.

Leeds Equity Partners IV, LP, memo. op. (Del.

Super. Sept. 25, 2015), the purchaser acquired the shares of a company that had a liability (an obligation to make an “earn-out” payment to the former owners of a previously acquired company) that became payable after completion of the acquisition. The purchaser alleged, among other things, that in the course of negotiating the acquisition agreement the seller had made a fraudulent promise, separate from the acquisition agreement, to the effect that the seller would satisfy the earn-out obligation when it became payable. One of the requirements of a prima facie fraud claim is reasonable reliance on a false statement (in this case, the seller’s alleged promise to satisfy the earn-out obligation), and the Delaware Superior Court’s decision turned on whether the purchaser’s reliance could have been reasonable.

In addition to an integration clause, the acquisition agreement contained a somewhat unusual “exclusive representation” provision in which the purchaser affirmatively acknowledged that the representations and warranties in the acquisition agreement superseded any other statement made to the purchaser. Applying the relatively plaintiff-friendly standard used in considering motions to dismiss, the court refused to dismiss the purchaser’s fraud claim, noting that the “exclusive representation” provision did not “clearly state that the parties disclaim reliance upon extra-contractual statements.” Prior Delaware cases, including Abry Partners V, L.P. v. F&W Acquisition LLC, et al.

(Del. Ch. 2006), had held a specific acknowledgement of non-reliance to be necessary in order to avoid fraud claims based on extra-contractual statements. The court also noted that the acquisition agreement contained an exception to its “exclusive remedy” provision (i.e., the provision stating that the seller’s indemnity would be the purchaser’s sole post-closing recourse), and that exception permitted non-indemnity-based claims for “actual fraud”.

The court referred to this language as indicating that fraud claims were expressly contemplated by the parties, and may have survived even if the agreement included broader non-reliance language in its “exclusive representation” provision. Prairie Capital Prairie Capital III, LP v. Double E Holding Corp. (Del.

Ch. Nov. 25, 2015) arose out of the sale of a portfolio company by one private equity firm to another.

The purchasers asserted following closing that the sellers had, among other things, committed fraud grounded in alleged misrepresentations not contained in the acquisition agreement and in the failure to disclose the facts underlying such misrepresentations to the purchasers. The acquisition agreement contained an integration clause as well as an “exclusive representation” provision in which the purchasers stated affirmatively that they had relied on their own independent investigation and on the representations expressly set forth in the agreement. The provision also included a disclaimer of all extra-contractual representations, but did not expressly state that the purchasers had not relied on any extra-contractual representations. Deal Lawyers March-April 2016 6 . The purchasers argued that their fraud claim should survive the sellers’ motion to dismiss due to the absence in the acquisition agreement of an explicit disclaimer of “reliance” on extra-contractual representations. The purchasers’ position appeared to be somewhat consistent with the recent trajectory of Delaware case law, including True Blue, which had begun to suggest that specific phrasing was required for such a disclaimer to be effective. But the Delaware Court of Chancery was not persuaded by the purchasers’ assertions in Prairie Capital, dismissing their claim and holding that no “magic words” were required for such disclaimers to be effective so long as they “add up to a clear anti-reliance clause.” The court also rejected the purchasers’ argument that a fraud exception contained in the acquisition agreement’s “exclusive remedy” provision could form a basis for the purchasers’ extra-contractual fraudulent misrepresentation claim, concluding that the fraud exception did not address which representations the purchasers could rely on and, accordingly, did not override the “exclusive representation” provision’s limitations on the universe of information on which a fraud claim could be based. FdG Logistics The Chancery Court most recently addressed disclaimers of extra-contractual liabilities in FdG Logistics LLC v. A&R Logistics Holdings, Inc., et al.

(Del. Ch. Feb.

23, 2016), which arose out of the purchase of a trucking company by a private equity firm through a merger. The purchaser alleged that the target company “engaged in an extensive series of illegal and improper activities that were concealed from it during pre-merger due diligence” and asserted, among other things, that the selling securityholders had committed common law fraud based on alleged misrepresentations in extra-contractual materials, including a confidential information memorandum and a management presentation. The acquisition agreement included a customary integration clause and an “exclusive representation” provision, located at the end of the list of representations and warranties by the target company, pursuant to which the target company affirmatively disclaimed all extra-contractual representations. Reviewing Abry Partners and its progeny, the Chancery Court explained that an effective disclaimer must amount to a contractual promise by the purchaser that it has not relied upon extra-contractual statements by the seller. Applying this reading, the court concluded that such a disclaimer must be expressed as an affirmative statement by the aggrieved party in order to be effective.

Since the “exclusive representation” provision at issue was worded as a declaration by the target company, rather than an acknowledgment and agreement by the purchaser, and since the integration clause “does not contain an unambiguous statement by [the purchaser] disclaiming reliance on extra-contractual statements”, the court denied the motion to dismiss the purchaser’s extra-contractual fraud claim. Conclusion Most purchase agreements in private M&A transactions contain some formulation of the provisions mentioned above and, in Delaware, a seller should be able to insulate itself from claims of fraud based on statements outside of the acquisition agreement so long as these provisions are properly drafted. Although the Chancery Court’s decision in Prairie Capital may provide some flexibility to those drafting disclaimers of extra-contractual liability, the inconsistency in recent Delaware lower court decisions, absent further clarification from the Delaware Supreme Court, cautions practitioners to continue to draft these provisions as unambiguously as possible. In particular, we continue to recommend that an acquisition agreement contain a standard integration clause along with an acknowledgment by the purchaser expressly disclaiming the existence of, and any reliance by the purchaser on, any representations from the seller other than those expressly set forth in the agreement (including in particular any representations as to the “accuracy or completeness” of the information made available to the purchaser). In addition, any “fraud” exception to the “exclusive remedy” provision should be carefully tailored to permit only fraud claims based on the representations and warranties included in the acquisition agreement and not claims based on extra-contractual statements. 7 Deal Lawyers March-April 2016 .