Description

Investment Review and Outlook

June 30, 2016

Review and Outlook

“Courage is what it takes to stand up and speak; courage is also what it takes to sit down and listen”

― Winston Churchill, British Prime Minister, 1940-1945 and 1951-1955.

The British are now living both sides of their beloved Prime Minister’s definition of courage. In a shocking

passage of the “Brexit” referendum in the closing days of June the citizens of the United Kingdom stood up and

said to the world they want to leave the European Union and take control of their social and economic future.

Following their vote to exit the 23 nation confederation which includes over 500 million people, the U.K. is now

forced to show courage in dealing with the world’s economic and political reaction.

Economists, media, and policymakers spent the second quarter distracted by rising presidential campaign rhetoric,

engaged in debates over Janet Yellen’s next move as chair of the Federal Reserve, and focused on deconstructing

meaningless economic data. On a more serious note the world confronted escalating terrorist activity that fueled

rising security fears – further fracturing an already divided Washington.

Although all of these developments added volatility to the financial markets, the real economic and geopolitical

surprise was lurking in the U.K.

voting booth. At the start of the second quarter Brexit attracted little global attention, and was rarely the source of economic discussion. The 52% to 48% majority decision by the second largest economy in the E.U.

to exit this economic alliance caught the world by surprise. The vote quickly set into motion fears of a global economic dislocation, resulting in a selling frenzy, and driving world markets sharply lower as investors scrambled for answers. As with most reactions driven by fear and uncertainty the initial shock subsided as more rational thinking and long term perspective took hold in the final days of the quarter with markets recovering what they initially lost. Despite the turmoil and angst, the second quarter rewarded investors with positive returns across most asset classes. The broad-based S&P 500 gained 2.5% with small and mid-cap stocks rising over 3%.

A bounce in oil prices from historic lows pushed energy stocks higher as defensive sectors such as utilities, health care, and telecommunications all outperformed. Stocks were held back by lagging returns in the economically sensitive technology, industrials, and consumer discretionary sectors. International equities posted mixed results as emerging markets offered marginally positive gains. However, developed markets within EAFE dropped 1.5%, with many European markets failing to make a substantial recovery following Brexit. Fixed income markets delivered positive returns as investors crowded into safe haven investments such as high grade corporate bonds, agencies, and Treasury securities.

The yield curve remained positioned similarly to where it began the quarter as yields fell across the maturity spectrum. The 10-year Treasury closed near record lows at 1.50% - down from 1.85% in late March, and 2.40% a year ago. Corporate spreads tightened to 185 basis points, .

Page 2 down from 200 in early April. For the quarter all major taxable and tax-exempt fixed income indices delivered solid results with the Barclays 1-10 Municipal Index rising 1.44%, and the Barclays Aggregate jumping 2.21%. Commodity markets broke with their long term trend, and gained ground on financial assets in the quarter. The Commodity Research Board (CRB) Index of 24 commodities rose 14%. However, this rise was not consistent across all commodities.

Oil prices surged over 25% on positive inventory data and a rise in the value of the U.S. dollar. Gold benefited from its safe haven status during uncertain times and rose 7%. In addition, many agricultural commodity prices, such as grains and dairy also rose during the period.

Despite increases in these closely watched commodities, industrial products such as metals and chemicals all experienced sharp declines. The mixed commodity markets were a reflection of global economic forces driven by slow growth and investor anxiety. Mid-year offers a good opportunity for investors to pause and assess where the markets stand. Despite the clutter of economic news, political wrangling, and tumultuous global events, the financial markets delivered solid returns for investors in the first half of 2016.

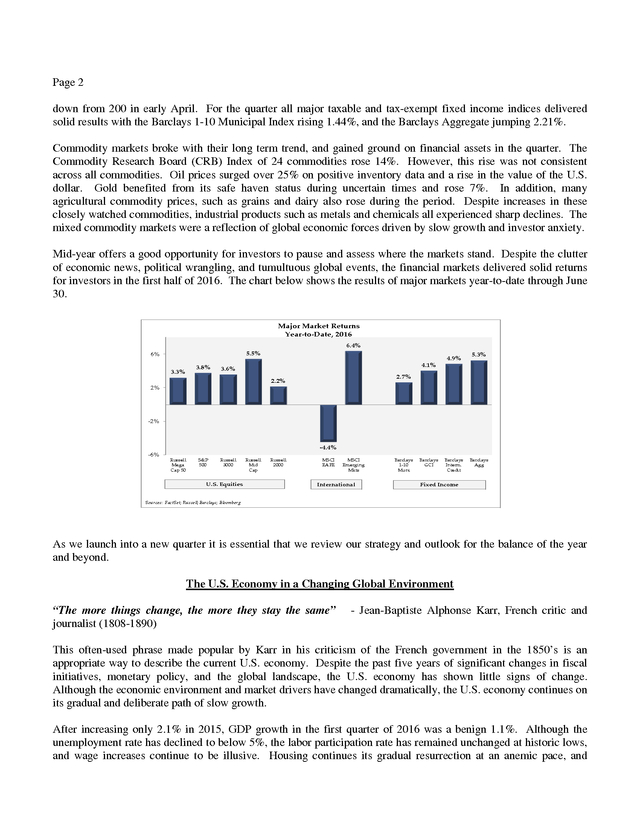

The chart below shows the results of major markets year-to-date through June 30. Major Market Returns Year-to-Date, 2016 6.4% 5.5% 6% 3.8% 3.3% 4.9% 5.3% 4.1% 3.6% 2.7% 2.2% 2% -2% -4.4% -6% Russell Mega Cap 50 S&P 500 Russell 3000 U.S. Equities Russell Mid Cap Russell 2000 MSCI EAFE MSCI Emerging Mkts International Barclays 1-10 Muni Barclays GCI Barclays Interm. Credit Barclays Agg Fixed Income Sources: FactSet; Russell; Barclays; Bloomberg As we launch into a new quarter it is essential that we review our strategy and outlook for the balance of the year and beyond. The U.S. Economy in a Changing Global Environment “The more things change, the more they stay the same” journalist (1808-1890) - Jean-Baptiste Alphonse Karr, French critic and This often-used phrase made popular by Karr in his criticism of the French government in the 1850’s is an appropriate way to describe the current U.S.

economy. Despite the past five years of significant changes in fiscal initiatives, monetary policy, and the global landscape, the U.S. economy has shown little signs of change. Although the economic environment and market drivers have changed dramatically, the U.S.

economy continues on its gradual and deliberate path of slow growth. After increasing only 2.1% in 2015, GDP growth in the first quarter of 2016 was a benign 1.1%. Although the unemployment rate has declined to below 5%, the labor participation rate has remained unchanged at historic lows, and wage increases continue to be illusive. Housing continues its gradual resurrection at an anemic pace, and .

Page 3 inflation has held constant below 4% for years. Since 2010 quarterly GDP growth has seldom dipped below zero and never exceeded 2.5%. The U.S. economy has not posted an annualized growth rate of greater than 3% since 2005 – the longest stretch of economic malaise since the Bureau of Labor Statistics started tracking GDP in 1930. Despite the sluggish economy, the U.S.

is performing better than most global economies. Many of the emerging markets have become victims of industrial commodity deflation and slowing demand. China’s transition from an industrial-based to a consumer-led economy is taking longer than expected.

Although growth is likely to be more than twice that of the developed world, China’s growth rates have been steadily ratcheted lower over the past two years. Brexit is forcing Europe to embark on a new economic path that will take several years to effectively define and adjust. Trade agreements, immigration reforms, tax law revisions, and changes in political leadership will need to be negotiated and re-established at a pace that balances speed, confidence, and financial stability. Although the U.K.

is less than 4% of global GDP, the European Union’s current membership comprises over 20% of global GDP – making it the world’s second largest economy. Our view is that slow, but steady, U.S. economic growth is a positive. Stability is a significant asset during times of economic and political upheaval.

Our economy is expected to continue to be the envy of global investors, and our markets should be the beneficiaries. We continue to see full year GDP growth hovering around 2.5% as the second half gets an incremental lift from consumer spending, housing, and an uptick in delayed capital spending. As global changes unfold over the next several quarters, we anticipate that the U.S. economy will continue to provide the same gradual pace of growth.

Therefore, Karr’s description of French politics in the 19th century is good news for today’s investors. “The more things change, the more they stay the same”. The Financial Sector: A Key Sector Under Scrutiny “I’ve been in the glare of the spotlight, I prefer to play my role behind the scenes” – Andrew Lloyd Webber, English Composer and Theater Director Over the past decade no segment of our economy has been in the spotlight more than the financial industry. Capital is the life blood of a growing and dynamic economy.

There is limited creative innovation, productivity improvement, or incentive to advance an economy without the access and ability to quickly and effectively transfer capital. Financial institutions were once praised for their ability to create and provide capital to businesses, consumers, and governments to allow them to produce, deliver, and consume goods and services. As a result, this essential segment of our global economy was rewarded in the marketplace by investors who viewed financial institutions as a relatively secure and reliable source of price appreciation and dividend flow. This has dramatically changed since the global economic crisis began in 2007-2008.

As a result, the industry has come under significant scrutiny, oversight, and regulation. Laws have been revised and implemented to restrict particular activities. These include regulations that affect capital requirements, mergers and acquisitions, compensation practices, and certain types of lending.

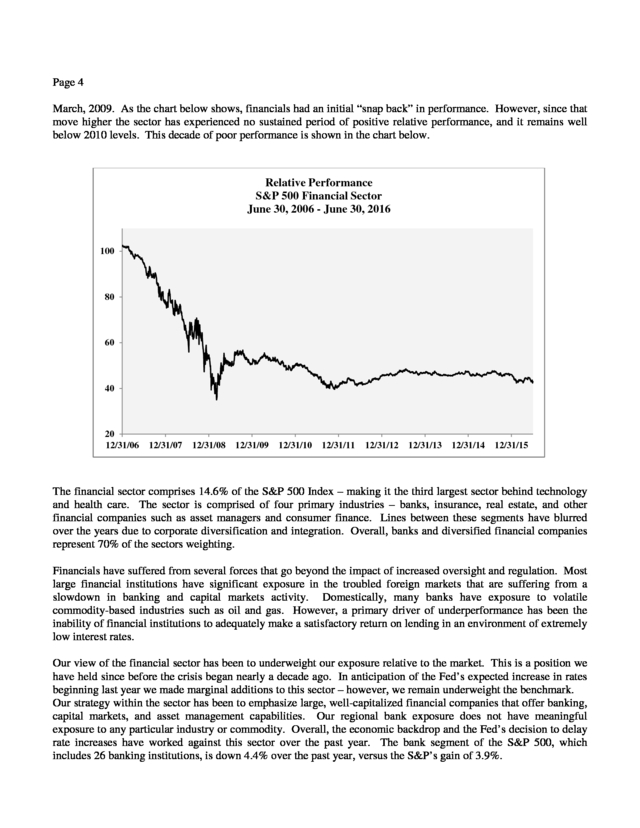

Overall, this has significantly impacted the sector’s performance since the start of the market’s recovery in . Page 4 March, 2009. As the chart below shows, financials had an initial “snap back” in performance. However, since that move higher the sector has experienced no sustained period of positive relative performance, and it remains well below 2010 levels. This decade of poor performance is shown in the chart below. Relative Performance S&P 500 Financial Sector June 30, 2006 - June 30, 2016 100 80 60 40 20 12/31/06 12/31/07 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15 The financial sector comprises 14.6% of the S&P 500 Index – making it the third largest sector behind technology and health care.

The sector is comprised of four primary industries – banks, insurance, real estate, and other financial companies such as asset managers and consumer finance. Lines between these segments have blurred over the years due to corporate diversification and integration. Overall, banks and diversified financial companies represent 70% of the sectors weighting. Financials have suffered from several forces that go beyond the impact of increased oversight and regulation.

Most large financial institutions have significant exposure in the troubled foreign markets that are suffering from a slowdown in banking and capital markets activity. Domestically, many banks have exposure to volatile commodity-based industries such as oil and gas. However, a primary driver of underperformance has been the inability of financial institutions to adequately make a satisfactory return on lending in an environment of extremely low interest rates. Our view of the financial sector has been to underweight our exposure relative to the market.

This is a position we have held since before the crisis began nearly a decade ago. In anticipation of the Fed’s expected increase in rates beginning last year we made marginal additions to this sector – however, we remain underweight the benchmark. Our strategy within the sector has been to emphasize large, well-capitalized financial companies that offer banking, capital markets, and asset management capabilities. Our regional bank exposure does not have meaningful exposure to any particular industry or commodity.

Overall, the economic backdrop and the Fed’s decision to delay rate increases have worked against this sector over the past year. The bank segment of the S&P 500, which includes 26 banking institutions, is down 4.4% over the past year, versus the S&P’s gain of 3.9%. . Page 5 Within the financial sector we are emphasizing broad-based, multi-line insurers over traditional banks. Insurance company balance sheets benefit more directly from improving financial markets – particularly high quality fixed income markets. Although insurers are highly regulated, the growing reality continues to be that banks will be the focus of new and more onerous statutes and oversight. Overall, we view financials with skepticism due to the factors we believe will continue to overhang the sector. We feel portfolios are appropriately positioned for the current environment.

However, we will consider a shift in exposures when the outlook appears more favorable – which is expected to come after the global economic turmoil subsides and the Fed gets back on course. But, for now, the spotlight burns too brightly for us to get overly optimistic on this important sector of our economy. Investment Strategy “Consistency is better than rare moments of greatness separated by periods of failure.” – Tom Seaver, Major League Baseball Pitcher and member of the Baseball Hall of Fame Global developments that occurred in the final weeks of June have serious implications for world economies and financial markets. However, we don’t believe these events rise to a level that alters our core belief in the benefits of diversification and focus on the long term.

In fact, the surprise Brexit vote and current global economic uncertainty only makes us more committed to these investment principles. Our goal is to remain consistent with our approach to implement strategies that position us to avoid periods of failure in achieving investment objectives. As with the majority of observers, we believed that the people of Britain would choose to remain in the E.U. However, in the current environment of unpredictable political and economic events we are not surprised by the outcome. Uncertainties over the full impact of Brexit on the U.K.

and the implications for key economic drivers such as emerging markets, currencies, inflation, interest rates, and trade will persist beyond the balance of 2016. The growing political attraction to protectionist economic policies appears to be underway – and the Brexit vote confirmed this pendulum shift. After a process of analysis and debate, markets will adjust to changes in macroeconomic forces such as the cost of capital, labor supply, and consumer demand. However, a dislocation in global trade policies that alters incentives, regulation, and other costs will result in a much more protracted period of uncertainty and market volatility.

Should some of what is being discussed by potential policymakers come to pass, there will be winners and losers. We will be watching these developments closely over the next several quarters and move to take advantage of any opportunities that are presented. As we navigate into the second half of the year we remain committed to our belief that U.S. equities offer attractive opportunities for investors who are guided by the principles of diversification and long term focus.

We are in an environment of steady economic growth, positive earnings, and low inflation. Our continued focus is on balance sheets, cash flow, durable earnings growth, dividend hikes, share repurchases, and M&A activity. This simple philosophy keeps us grounded during turbulent and uncertain times.

In addition, earnings potential and market valuations have improved. Second quarter earnings releases are poised to meet or potentially exceed expectations. The ratio of earnings pre-releases that are negative versus positive is at its lowest level since 3Q’2011. Further, valuations have improved as the dividend yield of the S&P 500 currently exceeds the 30-year Treasury bond for the first time in history.

Over 300 stocks in the S&P 500 yield more than the 10-year Treasury – marking another valuation indicator that has turned positive. Outside of the U.S., we maintain our long term exposure to international markets; although we are underweight relative to U.S. equities. We expect global markets to suffer sharp volatility as financial, currency, and commodity markets adjust to new levels following recent events.

Although the U.K. will gain more direct control over its . Page 6 social and economic destiny, the near term impact of this vote is expected to result in a slowdown in growth, rise in unemployment, currency devaluation, and short term political void. Similar reactions will ripple through other international markets in both developed and emerging markets. Although unsettling in the near term, non-U.S. markets continue to represent over 50% of global capitalization, provide positive growth opportunities, and offer improving valuations. Our fixed income strategy has not been materially impacted by recent events. We have positioned our portfolios defensively with intermediate and long-term portfolios managed short versus their benchmarks.

Gradual improvement in the economy favors overweighting corporate securities relative to Treasury and agency bonds. Municipal bonds have performed well making them modestly expensive relative to taxable securities. We have shifted our view on the Fed’s next move in interest rates. Our expectation was that the Fed would move to raise short term rates at mid-year.

Although the Fed’s posture remains biased towards higher rates, global volatility and the impending presidential election should keep the Fed on the sidelines until year end. We believe active asset allocation allows investors to take advantage of opportunities as they arise. When we see these situations developing we will take appropriate actions in a thoughtful and deliberate way. Although making near term market predictions is a futile exercise, we are confident of one market forecast for the second half of 2016 – that is, we assure you the market will be filled with unplanned surprises and scary volatility. However, maintaining a thoughtful and consistent approach to the markets will allow us weather the storms that are ahead. The opinions contained in the preceding commentary reflect those of Sterling Capital Management LLC, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice.

They also are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice. Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon any such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other government agency, and are subject to investment risk, including possible loss of principal invested. .

voting booth. At the start of the second quarter Brexit attracted little global attention, and was rarely the source of economic discussion. The 52% to 48% majority decision by the second largest economy in the E.U.

to exit this economic alliance caught the world by surprise. The vote quickly set into motion fears of a global economic dislocation, resulting in a selling frenzy, and driving world markets sharply lower as investors scrambled for answers. As with most reactions driven by fear and uncertainty the initial shock subsided as more rational thinking and long term perspective took hold in the final days of the quarter with markets recovering what they initially lost. Despite the turmoil and angst, the second quarter rewarded investors with positive returns across most asset classes. The broad-based S&P 500 gained 2.5% with small and mid-cap stocks rising over 3%.

A bounce in oil prices from historic lows pushed energy stocks higher as defensive sectors such as utilities, health care, and telecommunications all outperformed. Stocks were held back by lagging returns in the economically sensitive technology, industrials, and consumer discretionary sectors. International equities posted mixed results as emerging markets offered marginally positive gains. However, developed markets within EAFE dropped 1.5%, with many European markets failing to make a substantial recovery following Brexit. Fixed income markets delivered positive returns as investors crowded into safe haven investments such as high grade corporate bonds, agencies, and Treasury securities.

The yield curve remained positioned similarly to where it began the quarter as yields fell across the maturity spectrum. The 10-year Treasury closed near record lows at 1.50% - down from 1.85% in late March, and 2.40% a year ago. Corporate spreads tightened to 185 basis points, .

Page 2 down from 200 in early April. For the quarter all major taxable and tax-exempt fixed income indices delivered solid results with the Barclays 1-10 Municipal Index rising 1.44%, and the Barclays Aggregate jumping 2.21%. Commodity markets broke with their long term trend, and gained ground on financial assets in the quarter. The Commodity Research Board (CRB) Index of 24 commodities rose 14%. However, this rise was not consistent across all commodities.

Oil prices surged over 25% on positive inventory data and a rise in the value of the U.S. dollar. Gold benefited from its safe haven status during uncertain times and rose 7%. In addition, many agricultural commodity prices, such as grains and dairy also rose during the period.

Despite increases in these closely watched commodities, industrial products such as metals and chemicals all experienced sharp declines. The mixed commodity markets were a reflection of global economic forces driven by slow growth and investor anxiety. Mid-year offers a good opportunity for investors to pause and assess where the markets stand. Despite the clutter of economic news, political wrangling, and tumultuous global events, the financial markets delivered solid returns for investors in the first half of 2016.

The chart below shows the results of major markets year-to-date through June 30. Major Market Returns Year-to-Date, 2016 6.4% 5.5% 6% 3.8% 3.3% 4.9% 5.3% 4.1% 3.6% 2.7% 2.2% 2% -2% -4.4% -6% Russell Mega Cap 50 S&P 500 Russell 3000 U.S. Equities Russell Mid Cap Russell 2000 MSCI EAFE MSCI Emerging Mkts International Barclays 1-10 Muni Barclays GCI Barclays Interm. Credit Barclays Agg Fixed Income Sources: FactSet; Russell; Barclays; Bloomberg As we launch into a new quarter it is essential that we review our strategy and outlook for the balance of the year and beyond. The U.S. Economy in a Changing Global Environment “The more things change, the more they stay the same” journalist (1808-1890) - Jean-Baptiste Alphonse Karr, French critic and This often-used phrase made popular by Karr in his criticism of the French government in the 1850’s is an appropriate way to describe the current U.S.

economy. Despite the past five years of significant changes in fiscal initiatives, monetary policy, and the global landscape, the U.S. economy has shown little signs of change. Although the economic environment and market drivers have changed dramatically, the U.S.

economy continues on its gradual and deliberate path of slow growth. After increasing only 2.1% in 2015, GDP growth in the first quarter of 2016 was a benign 1.1%. Although the unemployment rate has declined to below 5%, the labor participation rate has remained unchanged at historic lows, and wage increases continue to be illusive. Housing continues its gradual resurrection at an anemic pace, and .

Page 3 inflation has held constant below 4% for years. Since 2010 quarterly GDP growth has seldom dipped below zero and never exceeded 2.5%. The U.S. economy has not posted an annualized growth rate of greater than 3% since 2005 – the longest stretch of economic malaise since the Bureau of Labor Statistics started tracking GDP in 1930. Despite the sluggish economy, the U.S.

is performing better than most global economies. Many of the emerging markets have become victims of industrial commodity deflation and slowing demand. China’s transition from an industrial-based to a consumer-led economy is taking longer than expected.

Although growth is likely to be more than twice that of the developed world, China’s growth rates have been steadily ratcheted lower over the past two years. Brexit is forcing Europe to embark on a new economic path that will take several years to effectively define and adjust. Trade agreements, immigration reforms, tax law revisions, and changes in political leadership will need to be negotiated and re-established at a pace that balances speed, confidence, and financial stability. Although the U.K.

is less than 4% of global GDP, the European Union’s current membership comprises over 20% of global GDP – making it the world’s second largest economy. Our view is that slow, but steady, U.S. economic growth is a positive. Stability is a significant asset during times of economic and political upheaval.

Our economy is expected to continue to be the envy of global investors, and our markets should be the beneficiaries. We continue to see full year GDP growth hovering around 2.5% as the second half gets an incremental lift from consumer spending, housing, and an uptick in delayed capital spending. As global changes unfold over the next several quarters, we anticipate that the U.S. economy will continue to provide the same gradual pace of growth.

Therefore, Karr’s description of French politics in the 19th century is good news for today’s investors. “The more things change, the more they stay the same”. The Financial Sector: A Key Sector Under Scrutiny “I’ve been in the glare of the spotlight, I prefer to play my role behind the scenes” – Andrew Lloyd Webber, English Composer and Theater Director Over the past decade no segment of our economy has been in the spotlight more than the financial industry. Capital is the life blood of a growing and dynamic economy.

There is limited creative innovation, productivity improvement, or incentive to advance an economy without the access and ability to quickly and effectively transfer capital. Financial institutions were once praised for their ability to create and provide capital to businesses, consumers, and governments to allow them to produce, deliver, and consume goods and services. As a result, this essential segment of our global economy was rewarded in the marketplace by investors who viewed financial institutions as a relatively secure and reliable source of price appreciation and dividend flow. This has dramatically changed since the global economic crisis began in 2007-2008.

As a result, the industry has come under significant scrutiny, oversight, and regulation. Laws have been revised and implemented to restrict particular activities. These include regulations that affect capital requirements, mergers and acquisitions, compensation practices, and certain types of lending.

Overall, this has significantly impacted the sector’s performance since the start of the market’s recovery in . Page 4 March, 2009. As the chart below shows, financials had an initial “snap back” in performance. However, since that move higher the sector has experienced no sustained period of positive relative performance, and it remains well below 2010 levels. This decade of poor performance is shown in the chart below. Relative Performance S&P 500 Financial Sector June 30, 2006 - June 30, 2016 100 80 60 40 20 12/31/06 12/31/07 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15 The financial sector comprises 14.6% of the S&P 500 Index – making it the third largest sector behind technology and health care.

The sector is comprised of four primary industries – banks, insurance, real estate, and other financial companies such as asset managers and consumer finance. Lines between these segments have blurred over the years due to corporate diversification and integration. Overall, banks and diversified financial companies represent 70% of the sectors weighting. Financials have suffered from several forces that go beyond the impact of increased oversight and regulation.

Most large financial institutions have significant exposure in the troubled foreign markets that are suffering from a slowdown in banking and capital markets activity. Domestically, many banks have exposure to volatile commodity-based industries such as oil and gas. However, a primary driver of underperformance has been the inability of financial institutions to adequately make a satisfactory return on lending in an environment of extremely low interest rates. Our view of the financial sector has been to underweight our exposure relative to the market.

This is a position we have held since before the crisis began nearly a decade ago. In anticipation of the Fed’s expected increase in rates beginning last year we made marginal additions to this sector – however, we remain underweight the benchmark. Our strategy within the sector has been to emphasize large, well-capitalized financial companies that offer banking, capital markets, and asset management capabilities. Our regional bank exposure does not have meaningful exposure to any particular industry or commodity.

Overall, the economic backdrop and the Fed’s decision to delay rate increases have worked against this sector over the past year. The bank segment of the S&P 500, which includes 26 banking institutions, is down 4.4% over the past year, versus the S&P’s gain of 3.9%. . Page 5 Within the financial sector we are emphasizing broad-based, multi-line insurers over traditional banks. Insurance company balance sheets benefit more directly from improving financial markets – particularly high quality fixed income markets. Although insurers are highly regulated, the growing reality continues to be that banks will be the focus of new and more onerous statutes and oversight. Overall, we view financials with skepticism due to the factors we believe will continue to overhang the sector. We feel portfolios are appropriately positioned for the current environment.

However, we will consider a shift in exposures when the outlook appears more favorable – which is expected to come after the global economic turmoil subsides and the Fed gets back on course. But, for now, the spotlight burns too brightly for us to get overly optimistic on this important sector of our economy. Investment Strategy “Consistency is better than rare moments of greatness separated by periods of failure.” – Tom Seaver, Major League Baseball Pitcher and member of the Baseball Hall of Fame Global developments that occurred in the final weeks of June have serious implications for world economies and financial markets. However, we don’t believe these events rise to a level that alters our core belief in the benefits of diversification and focus on the long term.

In fact, the surprise Brexit vote and current global economic uncertainty only makes us more committed to these investment principles. Our goal is to remain consistent with our approach to implement strategies that position us to avoid periods of failure in achieving investment objectives. As with the majority of observers, we believed that the people of Britain would choose to remain in the E.U. However, in the current environment of unpredictable political and economic events we are not surprised by the outcome. Uncertainties over the full impact of Brexit on the U.K.

and the implications for key economic drivers such as emerging markets, currencies, inflation, interest rates, and trade will persist beyond the balance of 2016. The growing political attraction to protectionist economic policies appears to be underway – and the Brexit vote confirmed this pendulum shift. After a process of analysis and debate, markets will adjust to changes in macroeconomic forces such as the cost of capital, labor supply, and consumer demand. However, a dislocation in global trade policies that alters incentives, regulation, and other costs will result in a much more protracted period of uncertainty and market volatility.

Should some of what is being discussed by potential policymakers come to pass, there will be winners and losers. We will be watching these developments closely over the next several quarters and move to take advantage of any opportunities that are presented. As we navigate into the second half of the year we remain committed to our belief that U.S. equities offer attractive opportunities for investors who are guided by the principles of diversification and long term focus.

We are in an environment of steady economic growth, positive earnings, and low inflation. Our continued focus is on balance sheets, cash flow, durable earnings growth, dividend hikes, share repurchases, and M&A activity. This simple philosophy keeps us grounded during turbulent and uncertain times.

In addition, earnings potential and market valuations have improved. Second quarter earnings releases are poised to meet or potentially exceed expectations. The ratio of earnings pre-releases that are negative versus positive is at its lowest level since 3Q’2011. Further, valuations have improved as the dividend yield of the S&P 500 currently exceeds the 30-year Treasury bond for the first time in history.

Over 300 stocks in the S&P 500 yield more than the 10-year Treasury – marking another valuation indicator that has turned positive. Outside of the U.S., we maintain our long term exposure to international markets; although we are underweight relative to U.S. equities. We expect global markets to suffer sharp volatility as financial, currency, and commodity markets adjust to new levels following recent events.

Although the U.K. will gain more direct control over its . Page 6 social and economic destiny, the near term impact of this vote is expected to result in a slowdown in growth, rise in unemployment, currency devaluation, and short term political void. Similar reactions will ripple through other international markets in both developed and emerging markets. Although unsettling in the near term, non-U.S. markets continue to represent over 50% of global capitalization, provide positive growth opportunities, and offer improving valuations. Our fixed income strategy has not been materially impacted by recent events. We have positioned our portfolios defensively with intermediate and long-term portfolios managed short versus their benchmarks.

Gradual improvement in the economy favors overweighting corporate securities relative to Treasury and agency bonds. Municipal bonds have performed well making them modestly expensive relative to taxable securities. We have shifted our view on the Fed’s next move in interest rates. Our expectation was that the Fed would move to raise short term rates at mid-year.

Although the Fed’s posture remains biased towards higher rates, global volatility and the impending presidential election should keep the Fed on the sidelines until year end. We believe active asset allocation allows investors to take advantage of opportunities as they arise. When we see these situations developing we will take appropriate actions in a thoughtful and deliberate way. Although making near term market predictions is a futile exercise, we are confident of one market forecast for the second half of 2016 – that is, we assure you the market will be filled with unplanned surprises and scary volatility. However, maintaining a thoughtful and consistent approach to the markets will allow us weather the storms that are ahead. The opinions contained in the preceding commentary reflect those of Sterling Capital Management LLC, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice.

They also are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice. Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon any such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other government agency, and are subject to investment risk, including possible loss of principal invested. .