Description

Investment Review and Outlook

December 31, 2016

Review and Outlook

“The pendulum of the mind alternates between sense and nonsense, not between right and wrong.” - Carl Jung,

Swiss Psychiatrist (1875-1961).

History will remember 2016 as the year the pendulum of political, social, and economic forces abruptly reversed

and began to swing toward a new world order. This abrupt reversal played out on the global stage with challenges

to the status quo occurring across Europe, the Middle East, Asia, and the U.S. Dr. Jung’s description of the

pendulum of the mind can easily be used to describe what began in 2016, and will impact politics and the markets

for many years to come.

The question of whether our new path is “sense or non-sense” is yet unknown. We entered the year with the world operating within a political and economic framework that had been established over many years. Although it was far from perfect, issues of leadership and global protocols had been loosely defined and policymakers, investors, and the political elite had learned to operate within that environment. In 2016, the tranquility of the status quo was shattered. Economic alliances, immigration policies, and entire governments came under siege.

The power of the ballot box and the economic and social ramifications of globalization shook the foundation of the world’s political and economic model. Despite this upheaval most global economies and financial markets managed to deliver solid results for the full year. Recent economic data indicates the U.S. expansion gained strength in 2016 as first half GDP grew 1.2%, while second half growth is expected to be 2.6%.

Although still below trend, GDP growth should finish above 2% for the first time since 2013. Home prices rose to levels last seen during the height of the housing boom in 2006. In addition, consumer confidence closed the year at its highest level since 2001 and fourth quarter year-over-year corporate profit growth is expected to turn positive for the first time in five quarters. Bond yields moved higher on the prospect of accelerating economic growth and an accompanying rise in inflation. The yield on the benchmark ten-year Treasury ended the year at 2.44%, up marginally from its 2.31% start – however, at mid-year the yield had dropped to a historic low of 1.36%.

In December, the Federal Reserve bumped up the fed funds target rate and signaled more increases are in store for 2017. Global equity markets were mixed. After a sharp selloff in the first six weeks of the year U.S. equity markets rallied with the S&P 500 closing the year up 11.95%.

International markets trailed the U.S. with significant dispersion. Developed markets in Europe and the Far East rose a meager 1.0% while the MSCI Emerging Markets Index that includes China, India, and Brazil jumped 11.2%. .

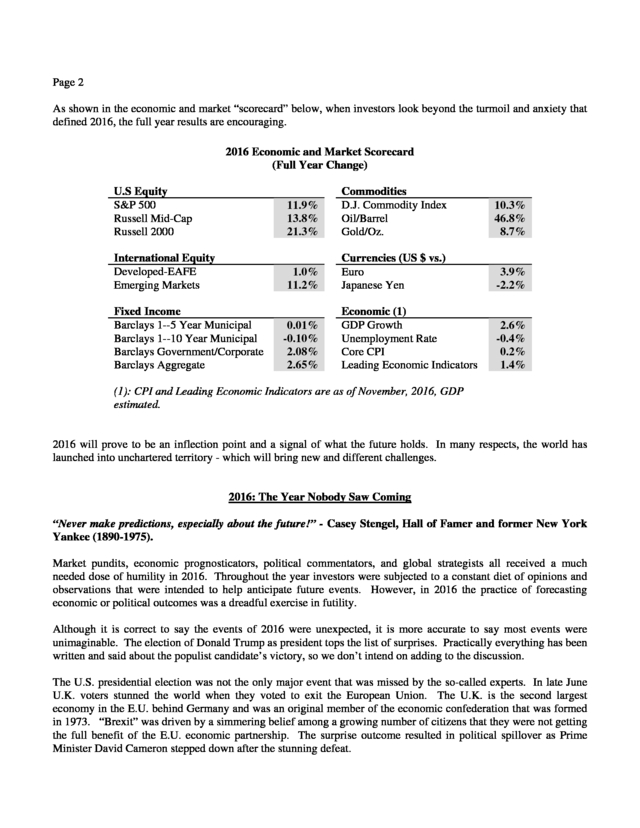

Page 2 As shown in the economic and market “scorecard” below, when investors look beyond the turmoil and anxiety that defined 2016, the full year results are encouraging. 2016 Economic and Market Scorecard (Full Year Change) U.S Equity S&P 500 Russell Mid-Cap Russell 2000 11.9% 13.8% 21.3% Commodities D.J. Commodity Index Oil/Barrel Gold/Oz. 10.3% 46.8% 8.7% International Equity Developed-EAFE Emerging Markets 1.0% 11.2% Currencies (US $ vs.) Euro Japanese Yen 3.9% -2.2% Economic (1) GDP Growth Unemployment Rate Core CPI Leading Economic Indicators 2.6% -0.4% 0.2% 1.4% Fixed Income Barclays 1--5 Year Municipal Barclays 1--10 Year Municipal Barclays Government/Corporate Barclays Aggregate 0.01% -0.10% 2.08% 2.65% (1): CPI and Leading Economic Indicators are as of November, 2016, GDP estimated. 2016 will prove to be an inflection point and a signal of what the future holds. In many respects, the world has launched into unchartered territory - which will bring new and different challenges. 2016: The Year Nobody Saw Coming “Never make predictions, especially about the future!” - Casey Stengel, Hall of Famer and former New York Yankee (1890-1975). Market pundits, economic prognosticators, political commentators, and global strategists all received a much needed dose of humility in 2016. Throughout the year investors were subjected to a constant diet of opinions and observations that were intended to help anticipate future events.

However, in 2016 the practice of forecasting economic or political outcomes was a dreadful exercise in futility. Although it is correct to say the events of 2016 were unexpected, it is more accurate to say most events were unimaginable. The election of Donald Trump as president tops the list of surprises. Practically everything has been written and said about the populist candidate’s victory, so we don’t intend on adding to the discussion. The U.S.

presidential election was not the only major event that was missed by the so-called experts. In late June U.K. voters stunned the world when they voted to exit the European Union.

The U.K. is the second largest economy in the E.U. behind Germany and was an original member of the economic confederation that was formed in 1973.

“Brexit” was driven by a simmering belief among a growing number of citizens that they were not getting the full benefit of the E.U. economic partnership. The surprise outcome resulted in political spillover as Prime Minister David Cameron stepped down after the stunning defeat. .

Page 3 On the economic and financial fronts there was plenty of forecasting stumbles. Investors came into 2016 with two overwhelmingly strong convictions – that oil prices would continue to fall, and the Fed would systematically hike interest rates throughout the year. These expectations for two of the most important drivers of economic activity proved to be completely wrong! In the fourth quarter of 2015 oil prices were spiraling lower. Crude had declined 18% in the final quarter - on its way to a 35% fall for the full year.

Investors, economists, and analysts were all lined up behind the view that 2016 would bring further declines in this economic commodity. The debate was not about if oil prices would continue to fall; instead the discussion was about how far prices would decline. In addition, economists completely missed on the outlook for interest rates.

In early 2016 the strongly held belief was that the Federal Reserve would hike interest rates at least three or four times in the new year. Rate increases throughout the new year were practically guaranteed by economists. In both cases the “greatest minds” missed the mark completely. In the end, the Fed made only one marginal rate adjustment in the final weeks of 2016 when the fed funds target rate was increased by 0.25%.

In the energy markets, oil prices surged with crude prices rising nearly 45%. Beyond the Brexit and U.S. presidential surprises, and the interest rate and oil price miscues, there were several other false expectations touted by market experts. The U.S.

equity market selloff of nearly 15% in the first six weeks of the year caught everyone by surprise. In mid-February, many strategists were waving the white flag of surrender and sounding the alarm that equites were heading into a new bear market. This outcry of pessimism was quickly followed by a market reversal as the S&P 500 surged over 10% in the second and third quarters – hitting record highs. As the presidential election approached in November the thought of a Trump victory was considered impossible by practically every political analyst and media commentator.

In addition, market pundits were telling investors that if the unimaginable happens and Trump emerges victorious we should brace for a market collapse. After election results were confirmed and a brief overnight selloff, U.S. markets rallied through year end with the S&P rising 5.3% and the Russell 2000 jumping 13.5%. With practically every political, economic, and market prediction missing its mark we must agree with Casey Stengel’s views on making predictions. 2017: A Year of Transition “Cheers for a new year, and another chance to get it right!”- Comedian Dan Aykroyd 2016 taught everyone a harsh lesson on the risks of engaging in economic and political forecasting.

However, our view is that taking a position and setting a direction based on our economic outlook is essential to successfully managing client assets. To insure that we avoid unnecessary risks it is important that we consider several factors when developing our outlook. First, we adhere closely to our core investment philosophy which emphasizes diversification across asset classes and maintains a focus on the long term. In addition, we view asset allocation as a dynamic process that allows flexibility in managing assets across multiple strategies.

This includes the ability to shift strategies among capitalization, sectors, credits, and other segments to take advantages of opportunities. This also allows for blending of active and passive strategies where appropriate. . Page 4 These principals will prove especially valuable in the new year. Our expectation is that 2017 will become a year of transition, and many of the trends that began in 2016 will move towards implementation. We expect a shift from an environment of stagnation and deflation fears to one of better growth, higher inflation and rising interest rates. The changing landscape will create significant volatility. The redesign of our economic and political framework will require transition across multiple segments of the economy.

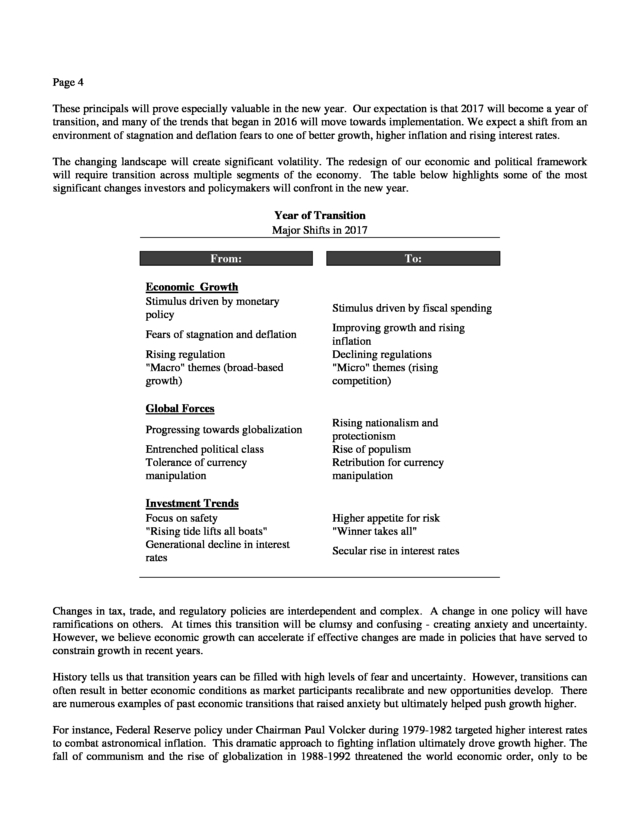

The table below highlights some of the most significant changes investors and policymakers will confront in the new year. Year of Transition Major Shifts in 2017 From: To: Economic Growth Stimulus driven by monetary policy Stimulus driven by fiscal spending Improving growth and rising inflation Declining regulations "Micro" themes (rising competition) Fears of stagnation and deflation Rising regulation "Macro" themes (broad-based growth) Global Forces Rising nationalism and protectionism Rise of populism Retribution for currency manipulation Progressing towards globalization Entrenched political class Tolerance of currency manipulation Investment Trends Focus on safety "Rising tide lifts all boats" Generational decline in interest rates Higher appetite for risk "Winner takes all" Secular rise in interest rates Changes in tax, trade, and regulatory policies are interdependent and complex. A change in one policy will have ramifications on others. At times this transition will be clumsy and confusing - creating anxiety and uncertainty. However, we believe economic growth can accelerate if effective changes are made in policies that have served to constrain growth in recent years. History tells us that transition years can be filled with high levels of fear and uncertainty.

However, transitions can often result in better economic conditions as market participants recalibrate and new opportunities develop. There are numerous examples of past economic transitions that raised anxiety but ultimately helped push growth higher. For instance, Federal Reserve policy under Chairman Paul Volcker during 1979-1982 targeted higher interest rates to combat astronomical inflation. This dramatic approach to fighting inflation ultimately drove growth higher.

The fall of communism and the rise of globalization in 1988-1992 threatened the world economic order, only to be . Page 5 followed by higher levels of innovation and capital creation. More recently, the financial crisis of 2007-2010 and accompanying monetary stimulus resulted in significant market shifts and helped reverse an economic spiral. These periods of transition were filled with uncertainty; however, these transitions ultimately helped drive asset values higher. In the new environment, investors will need to adjust long held beliefs and recalibrate expectations. The thirty year disinflationary, falling interest rate environment is coming to an end. Investors should expect rising volatility and modest returns across all asset classes.

An economic playbook that includes lower taxes, reduced regulations, and tighter labor markets is ideal for capital creation and rising asset values. However, the journey from where we stood in 2016 to the new environment will be filled with uncertainties regarding the pace and magnitude of change. Investment Strategy in a Transition Year “Bull markets are born in pessimism, grow in skepticism, mature in optimism and die in euphoria” - Sir John Templeton, Investor and Philanthropist (1912 – 2008) The biggest risk for investors in 2017 is that expectations for economic improvement get too far ahead of real fundamental results. The “Trump rally” is a welcome boost that will have a positive impact on consumer sentiment, employment, and capital spending.

However, the recent rally in stock prices is being driven by the expectation that tax reform, reduced regulations, and other business-friendly campaign promises will be fulfilled quickly. This optimism is likely to last well into the new year. However, implementation and execution of new policies will need to occur to support the rising valuation levels. The market will find itself in a precarious situation in late-2017 if interest rates and valuations are higher than current levels and there is no sign of meaningful revenue and earnings growth to support the market.

Although we believe this risk exists, we think there is ample opportunity for the markets to avoid this outcome. However, investor skepticism is expected to cause seismic volatility. Skepticism is an uncomfortable state of mind for investors. However, Mr.

Templeton’s advice gives us comfort that as long term investors we should stay committed to the market, and focus our attention on discovering opportunities. Throughout the new year we will be developing new ideas and strategies to take advantage of the changing environment. As we enter this transition year, here is a brief review of our current thoughts on various asset classes. U.S.

Equities We expect the investment environment will be driven less by broad macro issues and more by security-specific fundamentals. A shift from “a rising tide lifts all boats” to an environment of “winners and losers” is expected to develop as new policies and reforms reward companies that can adjust quickly and execute effectively. This new corporate environment raises questions about active versus passive management.

We are believers that a blend of active and passive approaches in certain asset classes can help smooth returns over time. In the new environment, the rein of passive outperformance versus active management is expected to be challenged. In addition, we expect the recent rally in small caps to result in breaking their five year drought of relative underperformance versus large caps. Valuations have improved and their concentration in the U.S.

economy should benefit small company earnings. In addition, the expectation of reduced regulations should also help the cost structure of small businesses. . Page 6 Our long held focus on balance sheet strength is expected to reward investors as we enter a period of rising corporate borrowing costs. Similarly, expected proposals to reduce taxes on movement of cash back into the U.S. from abroad should help multinational companies more profitably deploy capital into dividend increases, share repurchases, M&A activity and capital spending. International Markets Non-U.S. markets have significantly underperformed domestic markets. Despite short bursts of relative strength, international equities have trailed U.S.

stocks by a wide margin. For the five year period ending December 31, the S&P 500 has posted an annual return of 14.7% versus 6.5% for EAFE and a paltry 1.3% for emerging markets. Non-U.S. markets have been plagued by declining growth, recurring debt problems, national security issues, and political unrest. The developed economies of Europe and Japan are expected to grow by less than 2% in 2017.

Lots of economic “slack” exists in these economies as a result of rolling recessions over the past decade. Uncertainties continue to grow over the economic implications of the U.K.’s exit from the E.U. In addition, the political landscape is expected to remain shaky as the global populist movement influences key elections that will take place in Germany and France in the first half of the year.

Emerging markets will face their own set of challenges as economic growth settles around 5%-7% for China, Brazil, and India. Emerging markets should benefit from commodity price stability and the continued rise in consumer and infrastructure spending. However, uncertainty over trade policy will overhang this important market segment throughout the year. Despite this seemingly bleak outlook for the international economies we continue to maintain exposure to these important markets.

Over 50% of global market capitalization is outside of the U.S. In the current environment we continue to be underweighted international equities in diversified portfolios pending better clarity of economic growth, trade policy, and political outcomes. Within our international allocation, our bias is towards developed economies versus emerging markets due our higher level of comfort during this time of uncertainty. Although growth rates will be low, it is expected that Europe and Asia will avoid recession - marking the first year since before the 2008 global financial crisis that all major developed economies avoided economic contraction. Although economic activity will be far from robust, growth should be sufficient to keep the wheels of economic expansion turning.

This positive growth, along with attractive valuations relative to the U.S. should reap benefits for patient investors. Besides, Mr.

Templeton would likely support this strategy as there is an abundance of “pessimism” among international investors. Fixed Income We believe interest rates bottomed last July following the Brexit vote when the ten-year Treasury yield hit 1.36%. Our view is that interest rates are headed higher over the next year accompanied by 3-4 rate hikes by the Fed. This should come as no surprise to investors; however, it will make for a challenging bond market. In anticipation of positive economic growth and rising rates we are overweighting corporate securities relative to Treasury and agency bonds in taxable portfolios. Our portfolios are also positioned short of benchmark duration in order to reduce negative price pressure and allow for reinvestment as rates rise.

Like all fixed income indices municipal bonds posted negative returns in the fourth quarter – however, municipals suffered declines greater than taxable bonds. This was primarily due to concerns relating to future tax policies. Overall, we believe bonds will face a challenging year in 2017.

However, the upward move in interest rates will eventually provide more attractive cash flow to meet income needs. We anxiously await what this year of transition offers. Although we expect a higher level of volatility and anxiety than we’ve seen since the financial crisis, we are confident that opportunities will be presented, and that our philosophy of focusing on the long term will deliver results that best meet your investment objectives. . Page 7 The opinions contained in the preceding commentary reflect those of Sterling Capital Management LLC, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice. They also are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice.

Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon any such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other government agency, and are subject to investment risk, including possible loss of principal invested. .

The question of whether our new path is “sense or non-sense” is yet unknown. We entered the year with the world operating within a political and economic framework that had been established over many years. Although it was far from perfect, issues of leadership and global protocols had been loosely defined and policymakers, investors, and the political elite had learned to operate within that environment. In 2016, the tranquility of the status quo was shattered. Economic alliances, immigration policies, and entire governments came under siege.

The power of the ballot box and the economic and social ramifications of globalization shook the foundation of the world’s political and economic model. Despite this upheaval most global economies and financial markets managed to deliver solid results for the full year. Recent economic data indicates the U.S. expansion gained strength in 2016 as first half GDP grew 1.2%, while second half growth is expected to be 2.6%.

Although still below trend, GDP growth should finish above 2% for the first time since 2013. Home prices rose to levels last seen during the height of the housing boom in 2006. In addition, consumer confidence closed the year at its highest level since 2001 and fourth quarter year-over-year corporate profit growth is expected to turn positive for the first time in five quarters. Bond yields moved higher on the prospect of accelerating economic growth and an accompanying rise in inflation. The yield on the benchmark ten-year Treasury ended the year at 2.44%, up marginally from its 2.31% start – however, at mid-year the yield had dropped to a historic low of 1.36%.

In December, the Federal Reserve bumped up the fed funds target rate and signaled more increases are in store for 2017. Global equity markets were mixed. After a sharp selloff in the first six weeks of the year U.S. equity markets rallied with the S&P 500 closing the year up 11.95%.

International markets trailed the U.S. with significant dispersion. Developed markets in Europe and the Far East rose a meager 1.0% while the MSCI Emerging Markets Index that includes China, India, and Brazil jumped 11.2%. .

Page 2 As shown in the economic and market “scorecard” below, when investors look beyond the turmoil and anxiety that defined 2016, the full year results are encouraging. 2016 Economic and Market Scorecard (Full Year Change) U.S Equity S&P 500 Russell Mid-Cap Russell 2000 11.9% 13.8% 21.3% Commodities D.J. Commodity Index Oil/Barrel Gold/Oz. 10.3% 46.8% 8.7% International Equity Developed-EAFE Emerging Markets 1.0% 11.2% Currencies (US $ vs.) Euro Japanese Yen 3.9% -2.2% Economic (1) GDP Growth Unemployment Rate Core CPI Leading Economic Indicators 2.6% -0.4% 0.2% 1.4% Fixed Income Barclays 1--5 Year Municipal Barclays 1--10 Year Municipal Barclays Government/Corporate Barclays Aggregate 0.01% -0.10% 2.08% 2.65% (1): CPI and Leading Economic Indicators are as of November, 2016, GDP estimated. 2016 will prove to be an inflection point and a signal of what the future holds. In many respects, the world has launched into unchartered territory - which will bring new and different challenges. 2016: The Year Nobody Saw Coming “Never make predictions, especially about the future!” - Casey Stengel, Hall of Famer and former New York Yankee (1890-1975). Market pundits, economic prognosticators, political commentators, and global strategists all received a much needed dose of humility in 2016. Throughout the year investors were subjected to a constant diet of opinions and observations that were intended to help anticipate future events.

However, in 2016 the practice of forecasting economic or political outcomes was a dreadful exercise in futility. Although it is correct to say the events of 2016 were unexpected, it is more accurate to say most events were unimaginable. The election of Donald Trump as president tops the list of surprises. Practically everything has been written and said about the populist candidate’s victory, so we don’t intend on adding to the discussion. The U.S.

presidential election was not the only major event that was missed by the so-called experts. In late June U.K. voters stunned the world when they voted to exit the European Union.

The U.K. is the second largest economy in the E.U. behind Germany and was an original member of the economic confederation that was formed in 1973.

“Brexit” was driven by a simmering belief among a growing number of citizens that they were not getting the full benefit of the E.U. economic partnership. The surprise outcome resulted in political spillover as Prime Minister David Cameron stepped down after the stunning defeat. .

Page 3 On the economic and financial fronts there was plenty of forecasting stumbles. Investors came into 2016 with two overwhelmingly strong convictions – that oil prices would continue to fall, and the Fed would systematically hike interest rates throughout the year. These expectations for two of the most important drivers of economic activity proved to be completely wrong! In the fourth quarter of 2015 oil prices were spiraling lower. Crude had declined 18% in the final quarter - on its way to a 35% fall for the full year.

Investors, economists, and analysts were all lined up behind the view that 2016 would bring further declines in this economic commodity. The debate was not about if oil prices would continue to fall; instead the discussion was about how far prices would decline. In addition, economists completely missed on the outlook for interest rates.

In early 2016 the strongly held belief was that the Federal Reserve would hike interest rates at least three or four times in the new year. Rate increases throughout the new year were practically guaranteed by economists. In both cases the “greatest minds” missed the mark completely. In the end, the Fed made only one marginal rate adjustment in the final weeks of 2016 when the fed funds target rate was increased by 0.25%.

In the energy markets, oil prices surged with crude prices rising nearly 45%. Beyond the Brexit and U.S. presidential surprises, and the interest rate and oil price miscues, there were several other false expectations touted by market experts. The U.S.

equity market selloff of nearly 15% in the first six weeks of the year caught everyone by surprise. In mid-February, many strategists were waving the white flag of surrender and sounding the alarm that equites were heading into a new bear market. This outcry of pessimism was quickly followed by a market reversal as the S&P 500 surged over 10% in the second and third quarters – hitting record highs. As the presidential election approached in November the thought of a Trump victory was considered impossible by practically every political analyst and media commentator.

In addition, market pundits were telling investors that if the unimaginable happens and Trump emerges victorious we should brace for a market collapse. After election results were confirmed and a brief overnight selloff, U.S. markets rallied through year end with the S&P rising 5.3% and the Russell 2000 jumping 13.5%. With practically every political, economic, and market prediction missing its mark we must agree with Casey Stengel’s views on making predictions. 2017: A Year of Transition “Cheers for a new year, and another chance to get it right!”- Comedian Dan Aykroyd 2016 taught everyone a harsh lesson on the risks of engaging in economic and political forecasting.

However, our view is that taking a position and setting a direction based on our economic outlook is essential to successfully managing client assets. To insure that we avoid unnecessary risks it is important that we consider several factors when developing our outlook. First, we adhere closely to our core investment philosophy which emphasizes diversification across asset classes and maintains a focus on the long term. In addition, we view asset allocation as a dynamic process that allows flexibility in managing assets across multiple strategies.

This includes the ability to shift strategies among capitalization, sectors, credits, and other segments to take advantages of opportunities. This also allows for blending of active and passive strategies where appropriate. . Page 4 These principals will prove especially valuable in the new year. Our expectation is that 2017 will become a year of transition, and many of the trends that began in 2016 will move towards implementation. We expect a shift from an environment of stagnation and deflation fears to one of better growth, higher inflation and rising interest rates. The changing landscape will create significant volatility. The redesign of our economic and political framework will require transition across multiple segments of the economy.

The table below highlights some of the most significant changes investors and policymakers will confront in the new year. Year of Transition Major Shifts in 2017 From: To: Economic Growth Stimulus driven by monetary policy Stimulus driven by fiscal spending Improving growth and rising inflation Declining regulations "Micro" themes (rising competition) Fears of stagnation and deflation Rising regulation "Macro" themes (broad-based growth) Global Forces Rising nationalism and protectionism Rise of populism Retribution for currency manipulation Progressing towards globalization Entrenched political class Tolerance of currency manipulation Investment Trends Focus on safety "Rising tide lifts all boats" Generational decline in interest rates Higher appetite for risk "Winner takes all" Secular rise in interest rates Changes in tax, trade, and regulatory policies are interdependent and complex. A change in one policy will have ramifications on others. At times this transition will be clumsy and confusing - creating anxiety and uncertainty. However, we believe economic growth can accelerate if effective changes are made in policies that have served to constrain growth in recent years. History tells us that transition years can be filled with high levels of fear and uncertainty.

However, transitions can often result in better economic conditions as market participants recalibrate and new opportunities develop. There are numerous examples of past economic transitions that raised anxiety but ultimately helped push growth higher. For instance, Federal Reserve policy under Chairman Paul Volcker during 1979-1982 targeted higher interest rates to combat astronomical inflation. This dramatic approach to fighting inflation ultimately drove growth higher.

The fall of communism and the rise of globalization in 1988-1992 threatened the world economic order, only to be . Page 5 followed by higher levels of innovation and capital creation. More recently, the financial crisis of 2007-2010 and accompanying monetary stimulus resulted in significant market shifts and helped reverse an economic spiral. These periods of transition were filled with uncertainty; however, these transitions ultimately helped drive asset values higher. In the new environment, investors will need to adjust long held beliefs and recalibrate expectations. The thirty year disinflationary, falling interest rate environment is coming to an end. Investors should expect rising volatility and modest returns across all asset classes.

An economic playbook that includes lower taxes, reduced regulations, and tighter labor markets is ideal for capital creation and rising asset values. However, the journey from where we stood in 2016 to the new environment will be filled with uncertainties regarding the pace and magnitude of change. Investment Strategy in a Transition Year “Bull markets are born in pessimism, grow in skepticism, mature in optimism and die in euphoria” - Sir John Templeton, Investor and Philanthropist (1912 – 2008) The biggest risk for investors in 2017 is that expectations for economic improvement get too far ahead of real fundamental results. The “Trump rally” is a welcome boost that will have a positive impact on consumer sentiment, employment, and capital spending.

However, the recent rally in stock prices is being driven by the expectation that tax reform, reduced regulations, and other business-friendly campaign promises will be fulfilled quickly. This optimism is likely to last well into the new year. However, implementation and execution of new policies will need to occur to support the rising valuation levels. The market will find itself in a precarious situation in late-2017 if interest rates and valuations are higher than current levels and there is no sign of meaningful revenue and earnings growth to support the market.

Although we believe this risk exists, we think there is ample opportunity for the markets to avoid this outcome. However, investor skepticism is expected to cause seismic volatility. Skepticism is an uncomfortable state of mind for investors. However, Mr.

Templeton’s advice gives us comfort that as long term investors we should stay committed to the market, and focus our attention on discovering opportunities. Throughout the new year we will be developing new ideas and strategies to take advantage of the changing environment. As we enter this transition year, here is a brief review of our current thoughts on various asset classes. U.S.

Equities We expect the investment environment will be driven less by broad macro issues and more by security-specific fundamentals. A shift from “a rising tide lifts all boats” to an environment of “winners and losers” is expected to develop as new policies and reforms reward companies that can adjust quickly and execute effectively. This new corporate environment raises questions about active versus passive management.

We are believers that a blend of active and passive approaches in certain asset classes can help smooth returns over time. In the new environment, the rein of passive outperformance versus active management is expected to be challenged. In addition, we expect the recent rally in small caps to result in breaking their five year drought of relative underperformance versus large caps. Valuations have improved and their concentration in the U.S.

economy should benefit small company earnings. In addition, the expectation of reduced regulations should also help the cost structure of small businesses. . Page 6 Our long held focus on balance sheet strength is expected to reward investors as we enter a period of rising corporate borrowing costs. Similarly, expected proposals to reduce taxes on movement of cash back into the U.S. from abroad should help multinational companies more profitably deploy capital into dividend increases, share repurchases, M&A activity and capital spending. International Markets Non-U.S. markets have significantly underperformed domestic markets. Despite short bursts of relative strength, international equities have trailed U.S.

stocks by a wide margin. For the five year period ending December 31, the S&P 500 has posted an annual return of 14.7% versus 6.5% for EAFE and a paltry 1.3% for emerging markets. Non-U.S. markets have been plagued by declining growth, recurring debt problems, national security issues, and political unrest. The developed economies of Europe and Japan are expected to grow by less than 2% in 2017.

Lots of economic “slack” exists in these economies as a result of rolling recessions over the past decade. Uncertainties continue to grow over the economic implications of the U.K.’s exit from the E.U. In addition, the political landscape is expected to remain shaky as the global populist movement influences key elections that will take place in Germany and France in the first half of the year.

Emerging markets will face their own set of challenges as economic growth settles around 5%-7% for China, Brazil, and India. Emerging markets should benefit from commodity price stability and the continued rise in consumer and infrastructure spending. However, uncertainty over trade policy will overhang this important market segment throughout the year. Despite this seemingly bleak outlook for the international economies we continue to maintain exposure to these important markets.

Over 50% of global market capitalization is outside of the U.S. In the current environment we continue to be underweighted international equities in diversified portfolios pending better clarity of economic growth, trade policy, and political outcomes. Within our international allocation, our bias is towards developed economies versus emerging markets due our higher level of comfort during this time of uncertainty. Although growth rates will be low, it is expected that Europe and Asia will avoid recession - marking the first year since before the 2008 global financial crisis that all major developed economies avoided economic contraction. Although economic activity will be far from robust, growth should be sufficient to keep the wheels of economic expansion turning.

This positive growth, along with attractive valuations relative to the U.S. should reap benefits for patient investors. Besides, Mr.

Templeton would likely support this strategy as there is an abundance of “pessimism” among international investors. Fixed Income We believe interest rates bottomed last July following the Brexit vote when the ten-year Treasury yield hit 1.36%. Our view is that interest rates are headed higher over the next year accompanied by 3-4 rate hikes by the Fed. This should come as no surprise to investors; however, it will make for a challenging bond market. In anticipation of positive economic growth and rising rates we are overweighting corporate securities relative to Treasury and agency bonds in taxable portfolios. Our portfolios are also positioned short of benchmark duration in order to reduce negative price pressure and allow for reinvestment as rates rise.

Like all fixed income indices municipal bonds posted negative returns in the fourth quarter – however, municipals suffered declines greater than taxable bonds. This was primarily due to concerns relating to future tax policies. Overall, we believe bonds will face a challenging year in 2017.

However, the upward move in interest rates will eventually provide more attractive cash flow to meet income needs. We anxiously await what this year of transition offers. Although we expect a higher level of volatility and anxiety than we’ve seen since the financial crisis, we are confident that opportunities will be presented, and that our philosophy of focusing on the long term will deliver results that best meet your investment objectives. . Page 7 The opinions contained in the preceding commentary reflect those of Sterling Capital Management LLC, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice. They also are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice.

Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon any such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other government agency, and are subject to investment risk, including possible loss of principal invested. .