Description

Advisory Solutions Monthly Update

March 2017

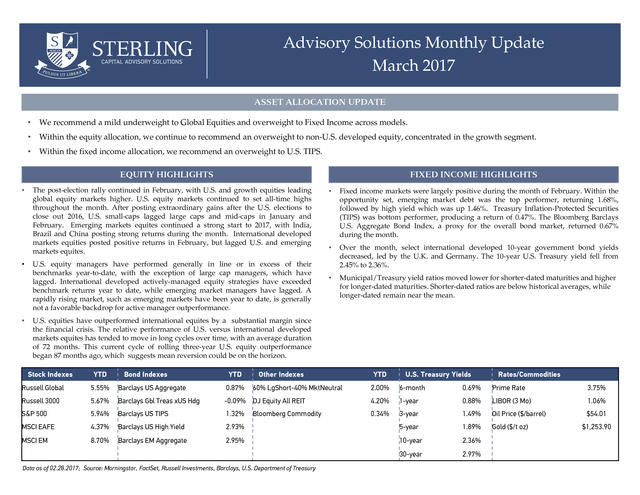

ASSET ALLOCATION UPDATE

•

We recommend a mild underweight to Global Equities and overweight to Fixed Income across models.

•

Within the equity allocation, we continue to recommend an overweight to non-U.S. developed equity, concentrated in the growth segment.

•

Within the fixed income allocation, we recommend an overweight to U.S. TIPS.

EQUITY HIGHLIGHTS

•

•

•

FIXED INCOME HIGHLIGHTS

The post-election rally continued in February, with U.S. and growth equities leading

global equity markets higher.

U.S. equity markets continued to set all-time highs throughout the month. After posting extraordinary gains after the U.S.

elections to close out 2016, U.S. small-caps lagged large caps and mid-caps in January and February. Emerging markets equites continued a strong start to 2017, with India, Brazil and China posting strong returns during the month.

International developed markets equities posted positive returns in February, but lagged U.S. and emerging markets equites. U.S. equity managers have performed generally in line or in excess of their benchmarks year-to-date, with the exception of large cap managers, which have lagged.

International developed actively-managed equity strategies have exceeded benchmark returns year to date, while emerging market managers have lagged. A rapidly rising market, such as emerging markets have been year to date, is generally not a favorable backdrop for active manager outperformance. • Fixed income markets were largely positive during the month of February. Within the opportunity set, emerging market debt was the top performer, returning 1.68%, followed by high yield which was up 1.46%.

Treasury Inflation-Protected Securities (TIPS) was bottom performer, producing a return of 0.47%. The Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the overall bond market, returned 0.67% during the month. • Over the month, select international developed 10-year government bond yields decreased, led by the U.K.

and Germany. The 10-year U.S. Treasury yield fell from 2.45% to 2.36%. • Municipal/Treasury yield ratios moved lower for shorter-dated maturities and higher for longer-dated maturities.

Shorter-dated ratios are below historical averages, while longer-dated remain near the mean. U.S. equities have outperformed international equites by a substantial margin since the financial crisis. The relative performance of U.S.

versus international developed markets equites has tended to move in long cycles over time, with an average duration of 72 months. This current cycle of rolling three-year U.S. equity outperformance began 87 months ago, which suggests mean reversion could be on the horizon. Stock Indexes YTD Bond Indexes YTD Russell Global 5.55% Barclays US Aggregate 0.87% Russell 3000 5.67% Barclays Gbl Treas xUS Hdg S&P 500 5.94% MSCI EAFE MSCI EM Other Indexes 60% LgShort-40% MktNeutral YTD U.S.

Treasury Yields Rates/Commodities 2.00% 6-month 0.69% Prime Rate 3.75% -0.09% DJ Equity All REIT 4.20% 1-year 0.88% LIBOR (3 Mo) 1.06% Barclays US TIPS 1.32% 0.34% 3-year 1.49% Oil Price ($/barrel) $54.01 4.37% Barclays US High Yield 2.93% 5-year 1.89% Gold ($/t oz) 8.70% Barclays EM Aggregate 2.95% 10-year 2.36% 30-year 2.97% Bloomberg Commodity Data as of 02.28.2017; Source: Morningstar, FactSet, Russell Investments, Barclays, U.S. Department of Treasury $1,253.90 . YOY Real GDP Growth ($U.S.) 20.00 15.00 10.00 5.00 0.00 -5.00 -10.00 -15.00 -20.00 U.S. Eurozone U.S. Industrial Production (LHS) Japan As of 12.31.2016. Source: FactSet 7.00 5.00 3.00 1.00 -1.00 -3.00 -5.00 -7.00 U.S. Labor Productivity (RHS) Industrial Production as of 01.31.2017; U.S.

Labor Productivity as of 12.31.2016; Source: FactSet Core Consumer Price Index (YoY Growth) U.S. - Unemployment Rate 4.00 12.00 3.00 10.00 2.00 Percent (%) 1.00 0.00 -1.00 8.00 6.00 4.00 2.00 Feb-97 Sep-97 Apr-98 Nov-98 Jun-99 Jan-00 Aug-00 Mar-01 Oct-01 May-02 Dec-02 Jul-03 Feb-04 Sep-04 Apr-05 Nov-05 Jun-06 Jan-07 Aug-07 Mar-08 Oct-08 May-09 Dec-09 Jul-10 Feb-11 Sep-11 Apr-12 Nov-12 Jun-13 Jan-14 Aug-14 Mar-15 Oct-15 May-16 Dec-16 -2.00 U.S. Eurozone Japan U.S. data as of 01.31.2017; Eurozone data as of 02.28.2017.

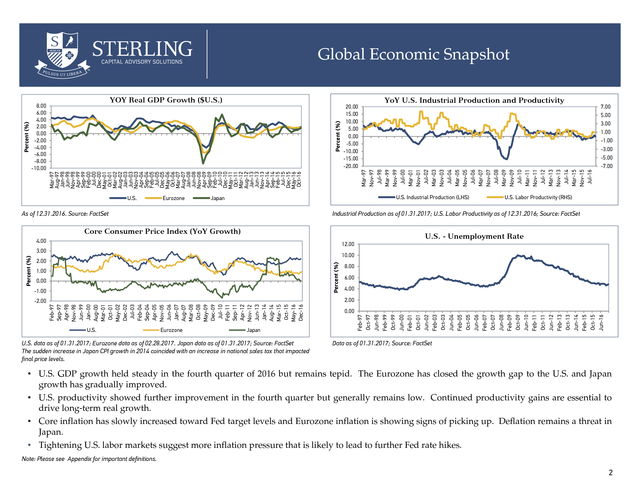

Japan data as of 01.31.2017; Source: FactSet The sudden increase in Japan CPI growth in 2014 coincided with an increase in national sales tax that impacted final price levels. 0.00 Feb-97 Oct-97 Jun-98 Feb-99 Oct-99 Jun-00 Feb-01 Oct-01 Jun-02 Feb-03 Oct-03 Jun-04 Feb-05 Oct-05 Jun-06 Feb-07 Oct-07 Jun-08 Feb-09 Oct-09 Jun-10 Feb-11 Oct-11 Jun-12 Feb-13 Oct-13 Jun-14 Feb-15 Oct-15 Jun-16 Percent (%) YoY U.S. Industrial Production and Productivity Mar-97 Nov-97 Jul-98 Mar-99 Nov-99 Jul-00 Mar-01 Nov-01 Jul-02 Mar-03 Nov-03 Jul-04 Mar-05 Nov-05 Jul-06 Mar-07 Nov-07 Jul-08 Mar-09 Nov-09 Jul-10 Mar-11 Nov-11 Jul-12 Mar-13 Nov-13 Jul-14 Mar-15 Nov-15 Jul-16 Percent (%) 8.00 6.00 4.00 2.00 0.00 -2.00 -4.00 -6.00 -8.00 -10.00 Mar-97 Aug-97 Jan-98 Jun-98 Nov-98 Apr-99 Sep-99 Feb-00 Jul-00 Dec-00 May-01 Oct-01 Mar-02 Aug-02 Jan-03 Jun-03 Nov-03 Apr-04 Sep-04 Feb-05 Jul-05 Dec-05 May-06 Oct-06 Mar-07 Aug-07 Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10 Dec-10 May-11 Oct-11 Mar-12 Aug-12 Jan-13 Jun-13 Nov-13 Apr-14 Sep-14 Feb-15 Jul-15 Dec-15 May-16 Oct-16 Percent (%) Global Economic Snapshot Data as of 01.31.2017; Source: FactSet • U.S. GDP growth held steady in the fourth quarter of 2016 but remains tepid.

The Eurozone has closed the growth gap to the U.S. and Japan growth has gradually improved. • U.S. productivity showed further improvement in the fourth quarter but generally remains low.

Continued productivity gains are essential to drive long-term real growth. • Core inflation has slowly increased toward Fed target levels and Eurozone inflation is showing signs of picking up. Deflation remains a threat in Japan. • Tightening U.S. labor markets suggest more inflation pressure that is likely to lead to further Fed rate hikes. Note: Please see Appendix for important definitions. 2 .

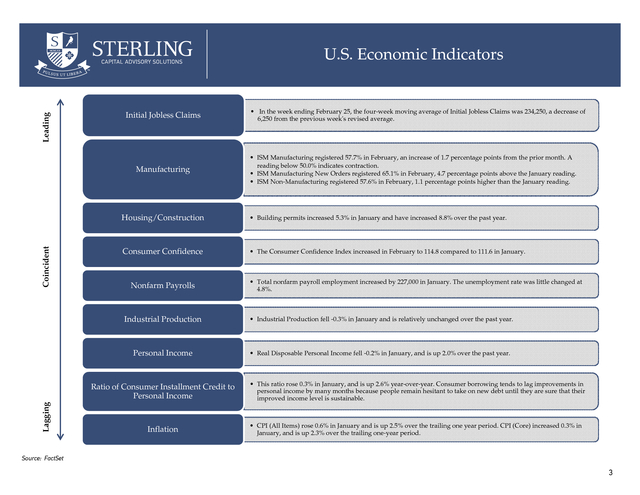

Leading U.S. Economic Indicators Initial Jobless Claims Manufacturing • In the week ending February 25, the four-week moving average of Initial Jobless Claims was 234,250, a decrease of 6,250 from the previous week's revised average. • ISM Manufacturing registered 57.7% in February, an increase of 1.7 percentage points from the prior month. A reading below 50.0% indicates contraction. • ISM Manufacturing New Orders registered 65.1% in February, 4.7 percentage points above the January reading. • ISM Non-Manufacturing registered 57.6% in February, 1.1 percentage points higher than the January reading. Coincident Housing/Construction • Building permits increased 5.3% in January and have increased 8.8% over the past year. Consumer Confidence • The Consumer Confidence Index increased in February to 114.8 compared to 111.6 in January. Nonfarm Payrolls • Total nonfarm payroll employment increased by 227,000 in January. The unemployment rate was little changed at 4.8%. Industrial Production • Industrial Production fell -0.3% in January and is relatively unchanged over the past year. Personal Income • Real Disposable Personal Income fell -0.2% in January, and is up 2.0% over the past year. Lagging Ratio of Consumer Installment Credit to Personal Income • This ratio rose 0.3% in January, and is up 2.6% year-over-year.

Consumer borrowing tends to lag improvements in personal income by many months because people remain hesitant to take on new debt until they are sure that their improved income level is sustainable. Inflation • CPI (All Items) rose 0.6% in January and is up 2.5% over the trailing one year period. CPI (Core) increased 0.3% in January, and is up 2.3% over the trailing one-year period. Source: FactSet 3 . Currency Nominal Trade-Weighted U.S. Dollar Major Currencies Euro per U.S. Dollar Feb-17 Jul-16 Dec-15 May-15 Oct-14 Mar-14 Aug-13 Jan-13 Jun-12 Nov-11 Apr-11 Sep-10 Feb-10 Jul-09 Dec-08 May-08 Oct-07 Mar-07 Feb-17 Jul-16 0.60 Dec-15 60.60 May-15 0.65 Oct-14 65.60 Mar-14 0.70 Aug-13 70.60 Jan-13 0.75 Jun-12 75.60 Nov-11 0.80 Apr-11 80.60 Sep-10 0.85 Feb-10 85.60 Jul-09 0.90 Dec-08 90.60 May-08 0.95 Oct-07 95.60 Mar-07 100.60 1.00 • The Trade-Weighted U.S. Dollar Index (Major Currencies) rose 1.2% in February and the index is down 1.5% year-to-date.

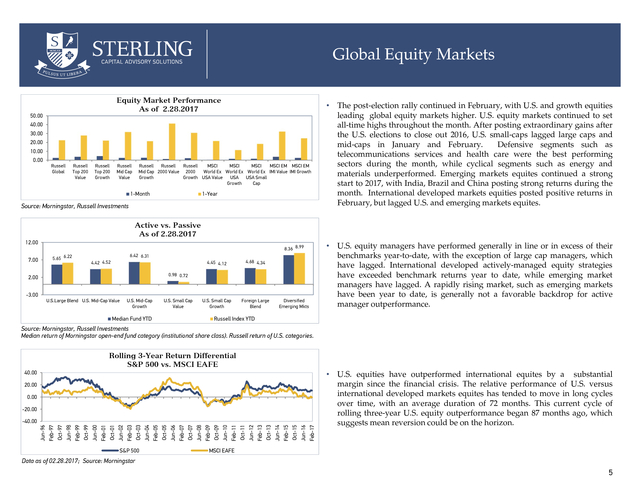

The dollar appreciated 1.7% versus the euro in February. Data as of 02.28.2017; Source: FactSet 4 . Global Equity Markets Equity Market Performance As of 2.28.2017 50.00 40.00 30.00 20.00 10.00 0.00 Russell Global Russell Top 200 Value Russell Top 200 Growth Russell Mid Cap Value Russell Russell Russell MSCI MSCI MSCI MSCI EM MSCI EM Mid Cap 2000 Value 2000 World Ex World Ex World Ex IMI Value IMI Growth Growth Growth USA Value USA USA Small Growth Cap 1-Month 1-Year Source: Morningstar, Russell Investments • The post-election rally continued in February, with U.S. and growth equities leading global equity markets higher. U.S. equity markets continued to set all-time highs throughout the month.

After posting extraordinary gains after the U.S. elections to close out 2016, U.S. small-caps lagged large caps and mid-caps in January and February. Defensive segments such as telecommunications services and health care were the best performing sectors during the month, while cyclical segments such as energy and materials underperformed.

Emerging markets equites continued a strong start to 2017, with India, Brazil and China posting strong returns during the month. International developed markets equities posted positive returns in February, but lagged U.S. and emerging markets equites. Active vs.

Passive As of 2.28.2017 12.00 • U.S. equity managers have performed generally in line or in excess of their benchmarks year-to-date, with the exception of large cap managers, which have lagged. International developed actively-managed equity strategies have exceeded benchmark returns year to date, while emerging market managers have lagged.

A rapidly rising market, such as emerging markets have been year to date, is generally not a favorable backdrop for active manager outperformance. 8.36 8.99 6.42 6.31 5.65 6.22 7.00 4.45 4.12 4.68 4.34 U.S. Small Cap Growth 4.42 4.52 Foreign Large Blend 0.98 0.72 2.00 -3.00 U.S.Large Blend U.S. Mid-Cap Value U.S.

Mid-Cap Growth U.S. Small Cap Value Median Fund YTD Diversified Emerging Mkts Russell Index YTD Source: Morningstar, Russell Investments Median return of Morningstar open-end fund category (institutional share class). Russell return of U.S.

categories. Rolling 3-Year Return Differential S&P 500 vs. MSCI EAFE 40.00 20.00 0.00 -20.00 Feb-17 Oct-15 Jun-16 Feb-15 Oct-13 Jun-14 Feb-13 Oct-11 Jun-12 Feb-11 Oct-09 Jun-10 Feb-09 Oct-07 Jun-08 Feb-07 Oct-05 Jun-06 Feb-05 Oct-03 S&P 500 Jun-04 Feb-03 Oct-01 Jun-02 Feb-01 Oct-99 Jun-00 Feb-99 Oct-97 Jun-98 Jun-96 Feb-97 -40.00 • U.S. equities have outperformed international equites by a substantial margin since the financial crisis.

The relative performance of U.S. versus international developed markets equites has tended to move in long cycles over time, with an average duration of 72 months. This current cycle of rolling three-year U.S.

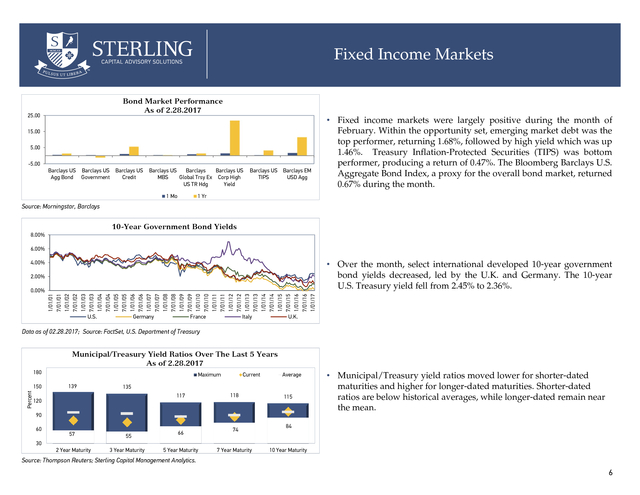

equity outperformance began 87 months ago, which suggests mean reversion could be on the horizon. MSCI EAFE Data as of 02.28.2017; Source: Morningstar 5 . Fixed Income Markets Bond Market Performance As of 2.28.2017 25.00 15.00 5.00 -5.00 Barclays US Barclays US Barclays US Agg Bond Government Credit Barclays US Barclays Barclays US MBS Global Trsy Ex Corp High US TR Hdg Yield 1 Mo Barclays US Barclays EM TIPS USD Agg • Fixed income markets were largely positive during the month of February. Within the opportunity set, emerging market debt was the top performer, returning 1.68%, followed by high yield which was up 1.46%. Treasury Inflation-Protected Securities (TIPS) was bottom performer, producing a return of 0.47%. The Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the overall bond market, returned 0.67% during the month. 1 Yr Source: Morningstar, Barclays 10-Year Government Bond Yields 8.00% 6.00% • Over the month, select international developed 10-year government bond yields decreased, led by the U.K.

and Germany. The 10-year U.S. Treasury yield fell from 2.45% to 2.36%. 4.00% 2.00% 1/01/01 7/01/01 1/01/02 7/01/02 1/01/03 7/01/03 1/01/04 7/01/04 1/01/05 7/01/05 1/01/06 7/01/06 1/01/07 7/01/07 1/01/08 7/01/08 1/01/09 7/01/09 1/01/10 7/01/10 1/01/11 7/01/11 1/01/12 7/01/12 1/01/13 7/01/13 1/01/14 7/01/14 1/01/15 7/01/15 1/01/16 7/01/16 1/01/17 0.00% U.S. Germany France Italy U.K. Data as of 02.28.2017; Source: FactSet, U.S.

Department of Treasury Municipal/Treasury Yield Ratios Over The Last 5 Years As of 2.28.2017 180 Percent 150 Maximum 139 Current Average 135 117 120 118 115 90 60 57 55 2 Year Maturity 3 Year Maturity 66 74 • Municipal/Treasury yield ratios moved lower for shorter-dated maturities and higher for longer-dated maturities. Shorter-dated ratios are below historical averages, while longer-dated remain near the mean. 84 30 5 Year Maturity 7 Year Maturity 10 Year Maturity Source: Thompson Reuters; Sterling Capital Management Analytics. 6 . Fixed Income Spreads and TIPS Breakeven 10-Year TIPS Breakeven 3.50 2000 Feb-17 Dec-16 Aug-15 May-16 May-16 Feb-14 Nov-14 Aug-12 May-13 Feb-11 Nov-11 Aug-09 Breakeven May-10 Feb-08 Nov-08 Aug-06 May-07 Feb-05 Nov-05 Aug-03 May-04 Feb-02 U.S. Corporate High Yield (RHS) Average Data as of 02.28.2017; Source: Federal Reserve Board of Governors Data as of 02.28.2017; Source: FactSet EM Debt OAS Yield Spread of Barclays U.S. Treasury Index to Global Ex-U.S. Treasury Index 1400 1200 3.00 1000 Percent (%) Blended Treasury Spread Data as of 02.28.2017; Source: Barclays -1.00 Average Yield Spread Oct-15 Mar-15 Jan-14 Aug-14 Jun-13 Apr-12 Nov-12 Feb-11 Sep-11 Jul-10 Dec-09 Oct-08 May-09 Mar-08 Jan-07 Aug-07 Jun-06 Nov-05 Apr-05 Feb-04 Sep-04 -2.00 Jul-03 May-96 Dec-96 Jul-97 Feb-98 Sep-98 Apr-99 Nov-99 Jun-00 Jan-01 Aug-01 Mar-02 Oct-02 May-03 Dec-03 Jul-04 Feb-05 Sep-05 Apr-06 Nov-06 Jun-07 Jan-08 Aug-08 Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13 Nov-13 Jun-14 Jan-15 Aug-15 Mar-16 Oct-16 0 0.00 Dec-02 200 Oct-01 400 1.00 May-02 600 2.00 Mar-01 800 Aug-00 Basis Points Nov-02 Feb-99 Feb-15 0.00 Nov-15 Aug-16 May-14 Feb-12 Nov-12 Aug-13 Aug-10 May-11 Feb-09 Nov-09 Aug-07 May-08 Feb-06 Nov-06 Aug-04 May-05 Nov-03 Aug-01 May-02 Feb-03 Feb-00 Nov-00 Aug-98 May-99 Feb-97 Nov-97 1.00 0.50 0 U.S.

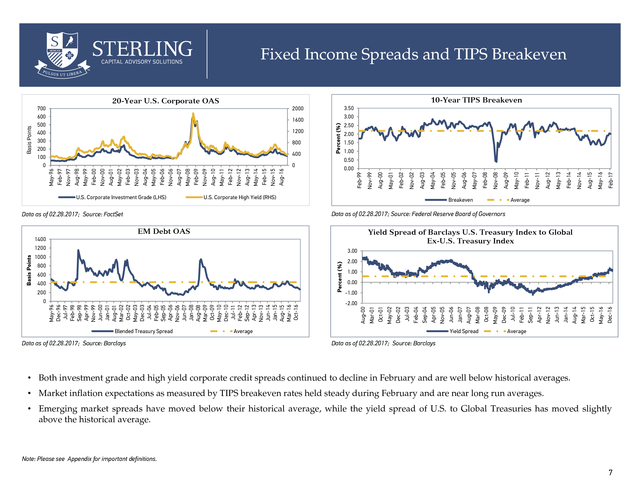

Corporate Investment Grade (LHS) 1.50 Aug-00 400 2.00 May-01 800 2.50 Nov-99 1200 3.00 Percent (%) 1600 May-96 Basis Points 20-Year U.S. Corporate OAS 700 600 500 400 300 200 100 0 Average Data as of 02.28.2017; Source: Barclays • Both investment grade and high yield corporate credit spreads continued to decline in February and are well below historical averages. • Market inflation expectations as measured by TIPS breakeven rates held steady during February and are near long run averages. • Emerging market spreads have moved below their historical average, while the yield spread of U.S. to Global Treasuries has moved slightly above the historical average. Note: Please see Appendix for important definitions. 7 .

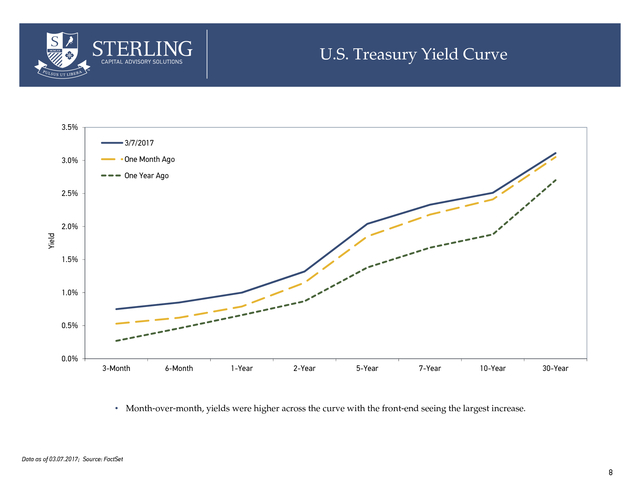

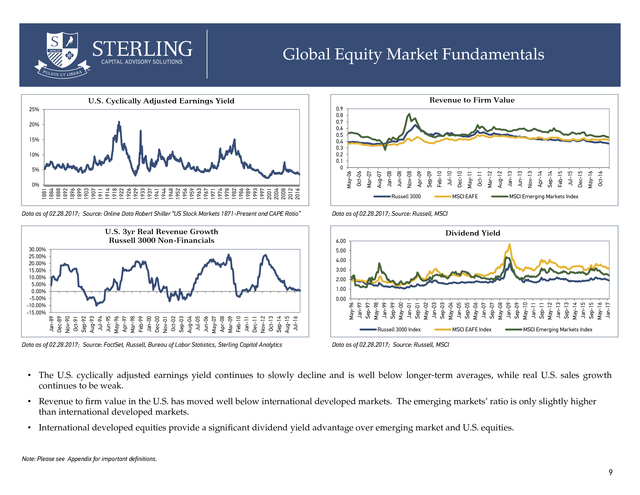

U.S. Treasury Yield Curve 3.5% 3/7/2017 One Month Ago 3.0% One Year Ago 2.5% Yield 2.0% 1.5% 1.0% 0.5% 0.0% 3-Month 6-Month 1-Year 2-Year 5-Year 7-Year 10-Year 30-Year • Month-over-month, yields were higher across the curve with the front-end seeing the largest increase. Data as of 03.07.2017; Source: FactSet 8 . Global Equity Market Fundamentals Revenue to Firm Value U.S. Cyclically Adjusted Earnings Yield 1881 1884 1888 1892 1896 1899 1903 1907 1911 1914 1918 1922 1926 1929 1933 1937 1941 1944 1948 1952 1956 1959 1963 1967 1971 1974 1978 1982 1986 1989 1993 1997 2001 2004 2008 2012 2016 Data as of 02.28.2017; Source: Online Data Robert Shiller “US Stock Markets 1871-Present and CAPE Ratio” U.S. 3yr Real Revenue Growth Russell 3000 Non-Financials 30.00% 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% -5.00% -10.00% -15.00% MSCI EAFE Oct-16 Dec-15 May-16 Jul-15 Feb-15 Apr-14 Sep-14 Nov-13 Jan-13 Jun-13 Mar-12 Aug-12 Oct-11 May-11 Jul-10 Russell 3000 Dec-10 Feb-10 Apr-09 Sep-09 Nov-08 0% Jan-08 May-06 5% Jun-08 10% Aug-07 15% Oct-06 20% Mar-07 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0 25% MSCI Emerging Markets Index Data as of 02.28.2017; Source: Russell, MSCI Dividend Yield 6.00 5.00 4.00 3.00 2.00 1.00 Data as of 02.28.2017; Source: FactSet, Russell, Bureau of Labor Statistics, Sterling Capital Analytics May-96 Jan-97 Sep-97 May-98 Jan-99 Sep-99 May-00 Jan-01 Sep-01 May-02 Jan-03 Sep-03 May-04 Jan-05 Sep-05 May-06 Jan-07 Sep-07 May-08 Jan-09 Sep-09 May-10 Jan-11 Sep-11 May-12 Jan-13 Sep-13 May-14 Jan-15 Sep-15 May-16 Jan-17 Jan-89 Dec-89 Nov-90 Oct-91 Sep-92 Aug-93 Jul-94 Jun-95 May-96 Apr-97 Mar-98 Feb-99 Jan-00 Dec-00 Nov-01 Oct-02 Sep-03 Aug-04 Jul-05 Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14 Aug-15 Jul-16 0.00 Russell 3000 Index MSCI EAFE Index MSCI Emerging Markets Index Data as of 02.28.2017; Source: Russell, MSCI • The U.S. cyclically adjusted earnings yield continues to slowly decline and is well below longer-term averages, while real U.S.

sales growth continues to be weak. • Revenue to firm value in the U.S. has moved well below international developed markets. The emerging markets’ ratio is only slightly higher than international developed markets. • International developed equities provide a significant dividend yield advantage over emerging market and U.S.

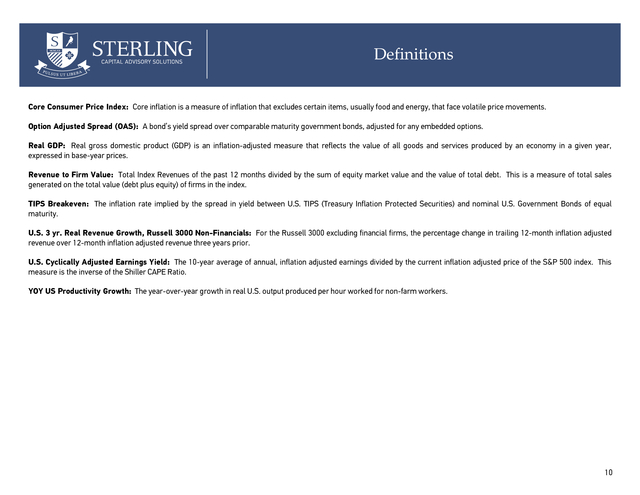

equities. Note: Please see Appendix for important definitions. 9 . Appendix . Definitions Core Consumer Price Index: Core inflation is a measure of inflation that excludes certain items, usually food and energy, that face volatile price movements. Option Adjusted Spread (OAS): A bond’s yield spread over comparable maturity government bonds, adjusted for any embedded options. Real GDP: Real gross domestic product (GDP) is an inflation-adjusted measure that reflects the value of all goods and services produced by an economy in a given year, expressed in base-year prices. Revenue to Firm Value: Total Index Revenues of the past 12 months divided by the sum of equity market value and the value of total debt. This is a measure of total sales generated on the total value (debt plus equity) of firms in the index. TIPS Breakeven: The inflation rate implied by the spread in yield between U.S. TIPS (Treasury Inflation Protected Securities) and nominal U.S. Government Bonds of equal maturity. U.S.

3 yr. Real Revenue Growth, Russell 3000 Non-Financials: For the Russell 3000 excluding financial firms, the percentage change in trailing 12-month inflation adjusted revenue over 12-month inflation adjusted revenue three years prior. U.S. Cyclically Adjusted Earnings Yield: The 10-year average of annual, inflation adjusted earnings divided by the current inflation adjusted price of the S&P 500 index.

This measure is the inverse of the Shiller CAPE Ratio. YOY US Productivity Growth: The year-over-year growth in real U.S. output produced per hour worked for non-farm workers. 10 . Disclosures The opinions expressed herein are those of Sterling Capital Management and the Sterling Advisory Solutions Team, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice. They are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice.

Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other federal government agency, and are subject to investment risk, including possible loss of principal invested. The securities/instruments discussed in this material may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives. Asset allocation and diversification do not assure a profit or protect against loss in declining financial markets. The indexes are unmanaged and are shown for illustrative purposes only. Indexes do not represent the performance of any specific investment.

An investor cannot invest directly in an index. The indexes selected by Sterling Capital Management to measure performance are representative of broad asset classes. Sterling Capital Management retains the right to change representative indexes at any time. 11 .

U.S. equity markets continued to set all-time highs throughout the month. After posting extraordinary gains after the U.S.

elections to close out 2016, U.S. small-caps lagged large caps and mid-caps in January and February. Emerging markets equites continued a strong start to 2017, with India, Brazil and China posting strong returns during the month.

International developed markets equities posted positive returns in February, but lagged U.S. and emerging markets equites. U.S. equity managers have performed generally in line or in excess of their benchmarks year-to-date, with the exception of large cap managers, which have lagged.

International developed actively-managed equity strategies have exceeded benchmark returns year to date, while emerging market managers have lagged. A rapidly rising market, such as emerging markets have been year to date, is generally not a favorable backdrop for active manager outperformance. • Fixed income markets were largely positive during the month of February. Within the opportunity set, emerging market debt was the top performer, returning 1.68%, followed by high yield which was up 1.46%.

Treasury Inflation-Protected Securities (TIPS) was bottom performer, producing a return of 0.47%. The Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the overall bond market, returned 0.67% during the month. • Over the month, select international developed 10-year government bond yields decreased, led by the U.K.

and Germany. The 10-year U.S. Treasury yield fell from 2.45% to 2.36%. • Municipal/Treasury yield ratios moved lower for shorter-dated maturities and higher for longer-dated maturities.

Shorter-dated ratios are below historical averages, while longer-dated remain near the mean. U.S. equities have outperformed international equites by a substantial margin since the financial crisis. The relative performance of U.S.

versus international developed markets equites has tended to move in long cycles over time, with an average duration of 72 months. This current cycle of rolling three-year U.S. equity outperformance began 87 months ago, which suggests mean reversion could be on the horizon. Stock Indexes YTD Bond Indexes YTD Russell Global 5.55% Barclays US Aggregate 0.87% Russell 3000 5.67% Barclays Gbl Treas xUS Hdg S&P 500 5.94% MSCI EAFE MSCI EM Other Indexes 60% LgShort-40% MktNeutral YTD U.S.

Treasury Yields Rates/Commodities 2.00% 6-month 0.69% Prime Rate 3.75% -0.09% DJ Equity All REIT 4.20% 1-year 0.88% LIBOR (3 Mo) 1.06% Barclays US TIPS 1.32% 0.34% 3-year 1.49% Oil Price ($/barrel) $54.01 4.37% Barclays US High Yield 2.93% 5-year 1.89% Gold ($/t oz) 8.70% Barclays EM Aggregate 2.95% 10-year 2.36% 30-year 2.97% Bloomberg Commodity Data as of 02.28.2017; Source: Morningstar, FactSet, Russell Investments, Barclays, U.S. Department of Treasury $1,253.90 . YOY Real GDP Growth ($U.S.) 20.00 15.00 10.00 5.00 0.00 -5.00 -10.00 -15.00 -20.00 U.S. Eurozone U.S. Industrial Production (LHS) Japan As of 12.31.2016. Source: FactSet 7.00 5.00 3.00 1.00 -1.00 -3.00 -5.00 -7.00 U.S. Labor Productivity (RHS) Industrial Production as of 01.31.2017; U.S.

Labor Productivity as of 12.31.2016; Source: FactSet Core Consumer Price Index (YoY Growth) U.S. - Unemployment Rate 4.00 12.00 3.00 10.00 2.00 Percent (%) 1.00 0.00 -1.00 8.00 6.00 4.00 2.00 Feb-97 Sep-97 Apr-98 Nov-98 Jun-99 Jan-00 Aug-00 Mar-01 Oct-01 May-02 Dec-02 Jul-03 Feb-04 Sep-04 Apr-05 Nov-05 Jun-06 Jan-07 Aug-07 Mar-08 Oct-08 May-09 Dec-09 Jul-10 Feb-11 Sep-11 Apr-12 Nov-12 Jun-13 Jan-14 Aug-14 Mar-15 Oct-15 May-16 Dec-16 -2.00 U.S. Eurozone Japan U.S. data as of 01.31.2017; Eurozone data as of 02.28.2017.

Japan data as of 01.31.2017; Source: FactSet The sudden increase in Japan CPI growth in 2014 coincided with an increase in national sales tax that impacted final price levels. 0.00 Feb-97 Oct-97 Jun-98 Feb-99 Oct-99 Jun-00 Feb-01 Oct-01 Jun-02 Feb-03 Oct-03 Jun-04 Feb-05 Oct-05 Jun-06 Feb-07 Oct-07 Jun-08 Feb-09 Oct-09 Jun-10 Feb-11 Oct-11 Jun-12 Feb-13 Oct-13 Jun-14 Feb-15 Oct-15 Jun-16 Percent (%) YoY U.S. Industrial Production and Productivity Mar-97 Nov-97 Jul-98 Mar-99 Nov-99 Jul-00 Mar-01 Nov-01 Jul-02 Mar-03 Nov-03 Jul-04 Mar-05 Nov-05 Jul-06 Mar-07 Nov-07 Jul-08 Mar-09 Nov-09 Jul-10 Mar-11 Nov-11 Jul-12 Mar-13 Nov-13 Jul-14 Mar-15 Nov-15 Jul-16 Percent (%) 8.00 6.00 4.00 2.00 0.00 -2.00 -4.00 -6.00 -8.00 -10.00 Mar-97 Aug-97 Jan-98 Jun-98 Nov-98 Apr-99 Sep-99 Feb-00 Jul-00 Dec-00 May-01 Oct-01 Mar-02 Aug-02 Jan-03 Jun-03 Nov-03 Apr-04 Sep-04 Feb-05 Jul-05 Dec-05 May-06 Oct-06 Mar-07 Aug-07 Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10 Dec-10 May-11 Oct-11 Mar-12 Aug-12 Jan-13 Jun-13 Nov-13 Apr-14 Sep-14 Feb-15 Jul-15 Dec-15 May-16 Oct-16 Percent (%) Global Economic Snapshot Data as of 01.31.2017; Source: FactSet • U.S. GDP growth held steady in the fourth quarter of 2016 but remains tepid.

The Eurozone has closed the growth gap to the U.S. and Japan growth has gradually improved. • U.S. productivity showed further improvement in the fourth quarter but generally remains low.

Continued productivity gains are essential to drive long-term real growth. • Core inflation has slowly increased toward Fed target levels and Eurozone inflation is showing signs of picking up. Deflation remains a threat in Japan. • Tightening U.S. labor markets suggest more inflation pressure that is likely to lead to further Fed rate hikes. Note: Please see Appendix for important definitions. 2 .

Leading U.S. Economic Indicators Initial Jobless Claims Manufacturing • In the week ending February 25, the four-week moving average of Initial Jobless Claims was 234,250, a decrease of 6,250 from the previous week's revised average. • ISM Manufacturing registered 57.7% in February, an increase of 1.7 percentage points from the prior month. A reading below 50.0% indicates contraction. • ISM Manufacturing New Orders registered 65.1% in February, 4.7 percentage points above the January reading. • ISM Non-Manufacturing registered 57.6% in February, 1.1 percentage points higher than the January reading. Coincident Housing/Construction • Building permits increased 5.3% in January and have increased 8.8% over the past year. Consumer Confidence • The Consumer Confidence Index increased in February to 114.8 compared to 111.6 in January. Nonfarm Payrolls • Total nonfarm payroll employment increased by 227,000 in January. The unemployment rate was little changed at 4.8%. Industrial Production • Industrial Production fell -0.3% in January and is relatively unchanged over the past year. Personal Income • Real Disposable Personal Income fell -0.2% in January, and is up 2.0% over the past year. Lagging Ratio of Consumer Installment Credit to Personal Income • This ratio rose 0.3% in January, and is up 2.6% year-over-year.

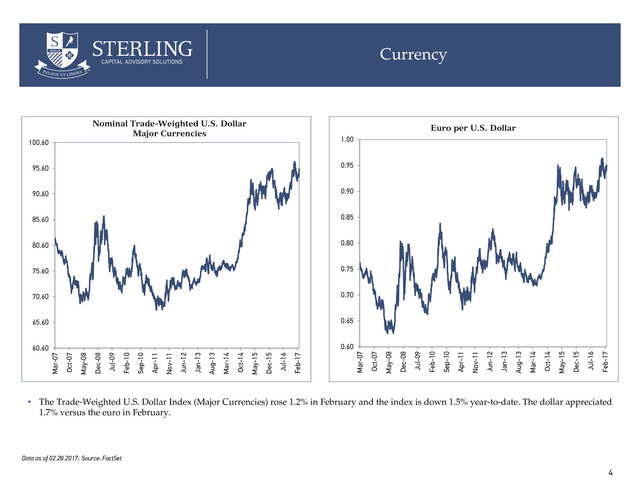

Consumer borrowing tends to lag improvements in personal income by many months because people remain hesitant to take on new debt until they are sure that their improved income level is sustainable. Inflation • CPI (All Items) rose 0.6% in January and is up 2.5% over the trailing one year period. CPI (Core) increased 0.3% in January, and is up 2.3% over the trailing one-year period. Source: FactSet 3 . Currency Nominal Trade-Weighted U.S. Dollar Major Currencies Euro per U.S. Dollar Feb-17 Jul-16 Dec-15 May-15 Oct-14 Mar-14 Aug-13 Jan-13 Jun-12 Nov-11 Apr-11 Sep-10 Feb-10 Jul-09 Dec-08 May-08 Oct-07 Mar-07 Feb-17 Jul-16 0.60 Dec-15 60.60 May-15 0.65 Oct-14 65.60 Mar-14 0.70 Aug-13 70.60 Jan-13 0.75 Jun-12 75.60 Nov-11 0.80 Apr-11 80.60 Sep-10 0.85 Feb-10 85.60 Jul-09 0.90 Dec-08 90.60 May-08 0.95 Oct-07 95.60 Mar-07 100.60 1.00 • The Trade-Weighted U.S. Dollar Index (Major Currencies) rose 1.2% in February and the index is down 1.5% year-to-date.

The dollar appreciated 1.7% versus the euro in February. Data as of 02.28.2017; Source: FactSet 4 . Global Equity Markets Equity Market Performance As of 2.28.2017 50.00 40.00 30.00 20.00 10.00 0.00 Russell Global Russell Top 200 Value Russell Top 200 Growth Russell Mid Cap Value Russell Russell Russell MSCI MSCI MSCI MSCI EM MSCI EM Mid Cap 2000 Value 2000 World Ex World Ex World Ex IMI Value IMI Growth Growth Growth USA Value USA USA Small Growth Cap 1-Month 1-Year Source: Morningstar, Russell Investments • The post-election rally continued in February, with U.S. and growth equities leading global equity markets higher. U.S. equity markets continued to set all-time highs throughout the month.

After posting extraordinary gains after the U.S. elections to close out 2016, U.S. small-caps lagged large caps and mid-caps in January and February. Defensive segments such as telecommunications services and health care were the best performing sectors during the month, while cyclical segments such as energy and materials underperformed.

Emerging markets equites continued a strong start to 2017, with India, Brazil and China posting strong returns during the month. International developed markets equities posted positive returns in February, but lagged U.S. and emerging markets equites. Active vs.

Passive As of 2.28.2017 12.00 • U.S. equity managers have performed generally in line or in excess of their benchmarks year-to-date, with the exception of large cap managers, which have lagged. International developed actively-managed equity strategies have exceeded benchmark returns year to date, while emerging market managers have lagged.

A rapidly rising market, such as emerging markets have been year to date, is generally not a favorable backdrop for active manager outperformance. 8.36 8.99 6.42 6.31 5.65 6.22 7.00 4.45 4.12 4.68 4.34 U.S. Small Cap Growth 4.42 4.52 Foreign Large Blend 0.98 0.72 2.00 -3.00 U.S.Large Blend U.S. Mid-Cap Value U.S.

Mid-Cap Growth U.S. Small Cap Value Median Fund YTD Diversified Emerging Mkts Russell Index YTD Source: Morningstar, Russell Investments Median return of Morningstar open-end fund category (institutional share class). Russell return of U.S.

categories. Rolling 3-Year Return Differential S&P 500 vs. MSCI EAFE 40.00 20.00 0.00 -20.00 Feb-17 Oct-15 Jun-16 Feb-15 Oct-13 Jun-14 Feb-13 Oct-11 Jun-12 Feb-11 Oct-09 Jun-10 Feb-09 Oct-07 Jun-08 Feb-07 Oct-05 Jun-06 Feb-05 Oct-03 S&P 500 Jun-04 Feb-03 Oct-01 Jun-02 Feb-01 Oct-99 Jun-00 Feb-99 Oct-97 Jun-98 Jun-96 Feb-97 -40.00 • U.S. equities have outperformed international equites by a substantial margin since the financial crisis.

The relative performance of U.S. versus international developed markets equites has tended to move in long cycles over time, with an average duration of 72 months. This current cycle of rolling three-year U.S.

equity outperformance began 87 months ago, which suggests mean reversion could be on the horizon. MSCI EAFE Data as of 02.28.2017; Source: Morningstar 5 . Fixed Income Markets Bond Market Performance As of 2.28.2017 25.00 15.00 5.00 -5.00 Barclays US Barclays US Barclays US Agg Bond Government Credit Barclays US Barclays Barclays US MBS Global Trsy Ex Corp High US TR Hdg Yield 1 Mo Barclays US Barclays EM TIPS USD Agg • Fixed income markets were largely positive during the month of February. Within the opportunity set, emerging market debt was the top performer, returning 1.68%, followed by high yield which was up 1.46%. Treasury Inflation-Protected Securities (TIPS) was bottom performer, producing a return of 0.47%. The Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the overall bond market, returned 0.67% during the month. 1 Yr Source: Morningstar, Barclays 10-Year Government Bond Yields 8.00% 6.00% • Over the month, select international developed 10-year government bond yields decreased, led by the U.K.

and Germany. The 10-year U.S. Treasury yield fell from 2.45% to 2.36%. 4.00% 2.00% 1/01/01 7/01/01 1/01/02 7/01/02 1/01/03 7/01/03 1/01/04 7/01/04 1/01/05 7/01/05 1/01/06 7/01/06 1/01/07 7/01/07 1/01/08 7/01/08 1/01/09 7/01/09 1/01/10 7/01/10 1/01/11 7/01/11 1/01/12 7/01/12 1/01/13 7/01/13 1/01/14 7/01/14 1/01/15 7/01/15 1/01/16 7/01/16 1/01/17 0.00% U.S. Germany France Italy U.K. Data as of 02.28.2017; Source: FactSet, U.S.

Department of Treasury Municipal/Treasury Yield Ratios Over The Last 5 Years As of 2.28.2017 180 Percent 150 Maximum 139 Current Average 135 117 120 118 115 90 60 57 55 2 Year Maturity 3 Year Maturity 66 74 • Municipal/Treasury yield ratios moved lower for shorter-dated maturities and higher for longer-dated maturities. Shorter-dated ratios are below historical averages, while longer-dated remain near the mean. 84 30 5 Year Maturity 7 Year Maturity 10 Year Maturity Source: Thompson Reuters; Sterling Capital Management Analytics. 6 . Fixed Income Spreads and TIPS Breakeven 10-Year TIPS Breakeven 3.50 2000 Feb-17 Dec-16 Aug-15 May-16 May-16 Feb-14 Nov-14 Aug-12 May-13 Feb-11 Nov-11 Aug-09 Breakeven May-10 Feb-08 Nov-08 Aug-06 May-07 Feb-05 Nov-05 Aug-03 May-04 Feb-02 U.S. Corporate High Yield (RHS) Average Data as of 02.28.2017; Source: Federal Reserve Board of Governors Data as of 02.28.2017; Source: FactSet EM Debt OAS Yield Spread of Barclays U.S. Treasury Index to Global Ex-U.S. Treasury Index 1400 1200 3.00 1000 Percent (%) Blended Treasury Spread Data as of 02.28.2017; Source: Barclays -1.00 Average Yield Spread Oct-15 Mar-15 Jan-14 Aug-14 Jun-13 Apr-12 Nov-12 Feb-11 Sep-11 Jul-10 Dec-09 Oct-08 May-09 Mar-08 Jan-07 Aug-07 Jun-06 Nov-05 Apr-05 Feb-04 Sep-04 -2.00 Jul-03 May-96 Dec-96 Jul-97 Feb-98 Sep-98 Apr-99 Nov-99 Jun-00 Jan-01 Aug-01 Mar-02 Oct-02 May-03 Dec-03 Jul-04 Feb-05 Sep-05 Apr-06 Nov-06 Jun-07 Jan-08 Aug-08 Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13 Nov-13 Jun-14 Jan-15 Aug-15 Mar-16 Oct-16 0 0.00 Dec-02 200 Oct-01 400 1.00 May-02 600 2.00 Mar-01 800 Aug-00 Basis Points Nov-02 Feb-99 Feb-15 0.00 Nov-15 Aug-16 May-14 Feb-12 Nov-12 Aug-13 Aug-10 May-11 Feb-09 Nov-09 Aug-07 May-08 Feb-06 Nov-06 Aug-04 May-05 Nov-03 Aug-01 May-02 Feb-03 Feb-00 Nov-00 Aug-98 May-99 Feb-97 Nov-97 1.00 0.50 0 U.S.

Corporate Investment Grade (LHS) 1.50 Aug-00 400 2.00 May-01 800 2.50 Nov-99 1200 3.00 Percent (%) 1600 May-96 Basis Points 20-Year U.S. Corporate OAS 700 600 500 400 300 200 100 0 Average Data as of 02.28.2017; Source: Barclays • Both investment grade and high yield corporate credit spreads continued to decline in February and are well below historical averages. • Market inflation expectations as measured by TIPS breakeven rates held steady during February and are near long run averages. • Emerging market spreads have moved below their historical average, while the yield spread of U.S. to Global Treasuries has moved slightly above the historical average. Note: Please see Appendix for important definitions. 7 .

U.S. Treasury Yield Curve 3.5% 3/7/2017 One Month Ago 3.0% One Year Ago 2.5% Yield 2.0% 1.5% 1.0% 0.5% 0.0% 3-Month 6-Month 1-Year 2-Year 5-Year 7-Year 10-Year 30-Year • Month-over-month, yields were higher across the curve with the front-end seeing the largest increase. Data as of 03.07.2017; Source: FactSet 8 . Global Equity Market Fundamentals Revenue to Firm Value U.S. Cyclically Adjusted Earnings Yield 1881 1884 1888 1892 1896 1899 1903 1907 1911 1914 1918 1922 1926 1929 1933 1937 1941 1944 1948 1952 1956 1959 1963 1967 1971 1974 1978 1982 1986 1989 1993 1997 2001 2004 2008 2012 2016 Data as of 02.28.2017; Source: Online Data Robert Shiller “US Stock Markets 1871-Present and CAPE Ratio” U.S. 3yr Real Revenue Growth Russell 3000 Non-Financials 30.00% 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% -5.00% -10.00% -15.00% MSCI EAFE Oct-16 Dec-15 May-16 Jul-15 Feb-15 Apr-14 Sep-14 Nov-13 Jan-13 Jun-13 Mar-12 Aug-12 Oct-11 May-11 Jul-10 Russell 3000 Dec-10 Feb-10 Apr-09 Sep-09 Nov-08 0% Jan-08 May-06 5% Jun-08 10% Aug-07 15% Oct-06 20% Mar-07 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0 25% MSCI Emerging Markets Index Data as of 02.28.2017; Source: Russell, MSCI Dividend Yield 6.00 5.00 4.00 3.00 2.00 1.00 Data as of 02.28.2017; Source: FactSet, Russell, Bureau of Labor Statistics, Sterling Capital Analytics May-96 Jan-97 Sep-97 May-98 Jan-99 Sep-99 May-00 Jan-01 Sep-01 May-02 Jan-03 Sep-03 May-04 Jan-05 Sep-05 May-06 Jan-07 Sep-07 May-08 Jan-09 Sep-09 May-10 Jan-11 Sep-11 May-12 Jan-13 Sep-13 May-14 Jan-15 Sep-15 May-16 Jan-17 Jan-89 Dec-89 Nov-90 Oct-91 Sep-92 Aug-93 Jul-94 Jun-95 May-96 Apr-97 Mar-98 Feb-99 Jan-00 Dec-00 Nov-01 Oct-02 Sep-03 Aug-04 Jul-05 Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14 Aug-15 Jul-16 0.00 Russell 3000 Index MSCI EAFE Index MSCI Emerging Markets Index Data as of 02.28.2017; Source: Russell, MSCI • The U.S. cyclically adjusted earnings yield continues to slowly decline and is well below longer-term averages, while real U.S.

sales growth continues to be weak. • Revenue to firm value in the U.S. has moved well below international developed markets. The emerging markets’ ratio is only slightly higher than international developed markets. • International developed equities provide a significant dividend yield advantage over emerging market and U.S.

equities. Note: Please see Appendix for important definitions. 9 . Appendix . Definitions Core Consumer Price Index: Core inflation is a measure of inflation that excludes certain items, usually food and energy, that face volatile price movements. Option Adjusted Spread (OAS): A bond’s yield spread over comparable maturity government bonds, adjusted for any embedded options. Real GDP: Real gross domestic product (GDP) is an inflation-adjusted measure that reflects the value of all goods and services produced by an economy in a given year, expressed in base-year prices. Revenue to Firm Value: Total Index Revenues of the past 12 months divided by the sum of equity market value and the value of total debt. This is a measure of total sales generated on the total value (debt plus equity) of firms in the index. TIPS Breakeven: The inflation rate implied by the spread in yield between U.S. TIPS (Treasury Inflation Protected Securities) and nominal U.S. Government Bonds of equal maturity. U.S.

3 yr. Real Revenue Growth, Russell 3000 Non-Financials: For the Russell 3000 excluding financial firms, the percentage change in trailing 12-month inflation adjusted revenue over 12-month inflation adjusted revenue three years prior. U.S. Cyclically Adjusted Earnings Yield: The 10-year average of annual, inflation adjusted earnings divided by the current inflation adjusted price of the S&P 500 index.

This measure is the inverse of the Shiller CAPE Ratio. YOY US Productivity Growth: The year-over-year growth in real U.S. output produced per hour worked for non-farm workers. 10 . Disclosures The opinions expressed herein are those of Sterling Capital Management and the Sterling Advisory Solutions Team, and not those of BB&T Corporation or its executives. The stated opinions are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice. They are not intended as an offer or solicitation with respect to the purchase or sale of any security. This information and these opinions are subject to change without notice.

Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result from the reliance by any person upon such information or opinions. Investment advisory services are available through Sterling Capital Management LLC, a separate subsidiary of BB&T Corporation. Sterling Capital Management LLC manages customized investment portfolios, provides asset allocation analysis and offers other investment-related services to affluent individuals and businesses.

Securities and other investments held in investment management or investment advisory accounts at Sterling Capital Management LLC are not deposits or other obligations of BB&T Corporation, Branch Banking and Trust Company or any affiliate, are not guaranteed by Branch Banking and Trust Company or any other bank, are not insured by the FDIC or any other federal government agency, and are subject to investment risk, including possible loss of principal invested. The securities/instruments discussed in this material may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives. Asset allocation and diversification do not assure a profit or protect against loss in declining financial markets. The indexes are unmanaged and are shown for illustrative purposes only. Indexes do not represent the performance of any specific investment.

An investor cannot invest directly in an index. The indexes selected by Sterling Capital Management to measure performance are representative of broad asset classes. Sterling Capital Management retains the right to change representative indexes at any time. 11 .