A Summary of Compensation-Related Updates to the Proxy Voting Guidelines of ISS and Glass Lewis – December 7, 2015

Shearman & Sterling

Description

CLIENT PUBLICATION

COMPENSATION, GOVERNANCE & ERISA | DECEMBER 7, 2015

A Summary of Compensation-Related Updates to the Proxy

Voting Guidelines of ISS and Glass Lewis

Institutional Shareholder Services Inc. (“ISS”) recently finalized its Proxy Voting Guidelines (the

“ISS Guidelines”) that apply to all shareholder meetings held after February 1, 2016.1 A number

of the updates relate to executive compensation matters, including changes to ISS’s US Equity

Plan Scorecard (the “EPSC”).2

In addition, Glass, Lewis & Co., LLC (“Glass Lewis”) has posted its 2016 Guidelines (the “Glass

Lewis Guidelines”),3 which clarify Glass Lewis’s compensation policies. This publication

summarizes the compensation-related updates to both the ISS Guidelines and the Glass Lewis

Guidelines.

ISS Updates

Shareholder Proposals: Equity Retention Periods

ISS currently has two policies relating to shareholder proposals on executive equity retention.



The first covers those proposals that do not include a specific retention ratio. These proposals require retention

of all or a significant portion of the shares acquired pursuant to compensation plans for two years following

termination of employment, or for a substantial period following the lapse of all other vesting requirements for

the award (the “lock-up period”), with a ratable release of a portion of the shares annually during the lock-up

period.



The second covers those proposals that require retention of 75% of net shares acquired pursuant to

compensation plans.

These proposals require retention during employment, and for two years following the termination of employment, and for the company to report to shareholders regarding the policy. Under existing policies, ISS considers each proposal on a case-by-case basis, taking into account: (1) any holding period, retention ratio or ownership requirements already in place at the company, and whether these polices are rigorous and meaningful; (2) actual officer ownership, and how it compares to the company’s policy or the proponent’s suggested policy; and (3) problematic pay practices, current and past, which may promote a short-term 1 The ISS Guidelines are available at: http://www.issgovernance.com/policy-gateway/2016-policy-information/. 2 The EPSC is available at: http://www.issgovernance.com/file/policy/faq-on-iss-us-equity-plan-scorecard-methodology.pdf. 3 The Glass Lewis Guidelines are available at: http://www.glasslewis.com/assets/uploads/2015/11/GUIDELINES_United_States_20161.pdf. . focus. In addition, ISS considers any post-termination holding requirements, and any other policies aimed at mitigating risk-taking by senior executives, when evaluating proposals that did not contain a retention ratio. For 2016, ISS has amended its policies to address equity retention proposals more generally. ISS will evaluate all equity retention proposals for senior executive officers on a case-by-case basis, with the following factors taken into account:  The percentage of net shares required to be retained;  The required retention period;  Whether the company has equity retention, holding period or stock ownership requirements in place and the robustness of those requirements;  Whether the company has any other policies aimed at mitigating risk taking by executives;  The executives’ actual stock ownership levels and the degree to which they meet or exceed the proponents’ suggested holding period/retention ratio or the company’s existing requirements; and  Problematic pay practices, current and past, which may demonstrate a short-term versus long-term focus. Updates to the Equity Plan Scorecard In 2015, ISS implemented a new model for evaluating equity incentive plan proposals, the EPSC, which ISS believes allows for a more nuanced consideration of equity incentive programs.4 Rather than applying a series of “pass/fail” tests, the EPSC considers a range of positive and negative factors, each of which it groups into one of three “pillars”: Plan Cost, Plan Features and Grant Practices. Each factor is provided a maximum number of points, with the total number of points that can be earned equaling 100, and a score of 53 or above earning a company a positive recommendation on its equity incentive plan proposal.

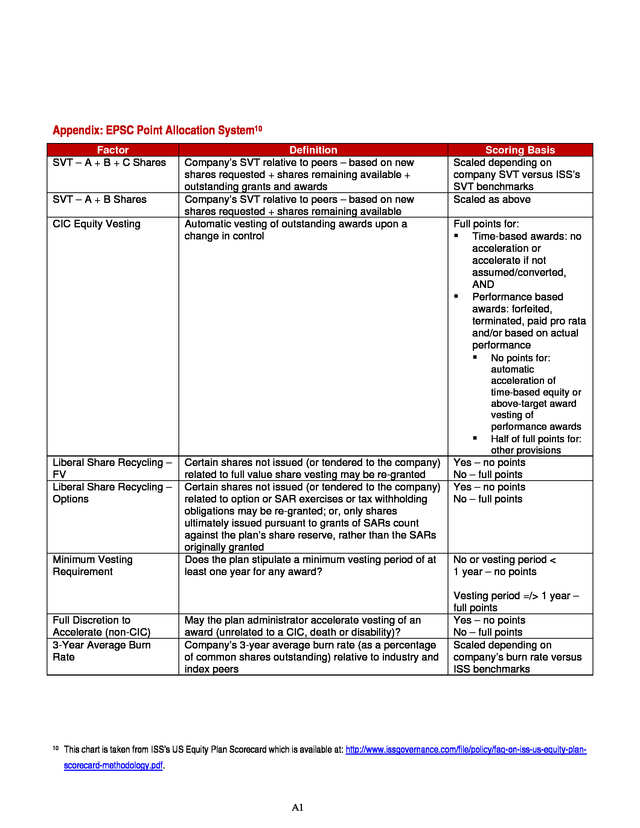

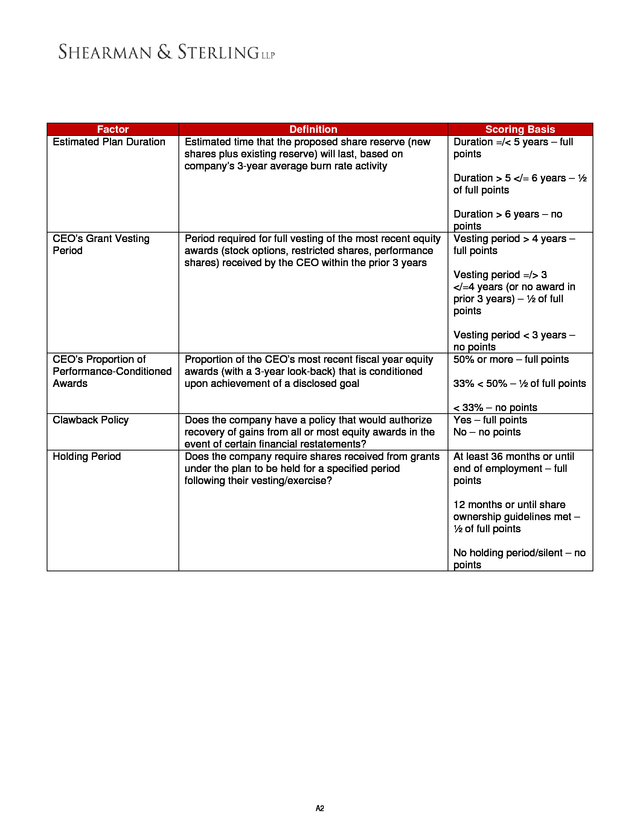

(A chart listing each factor, the pillar in which it is grouped, and ISS’s method for allocating points with respect to each factor, is included as an Appendix at the end of this memo.) Although ISS keeps confidential the number of points available for each individual factor, it does disclose the maximum number of points that can be earned for each pillar. These maximum pillar scores vary depending on the type of company whose plan is being evaluated. In 2015, there were four different models, one for each of: (1) S&P 500 companies, (2) Russell 3000 companies, (3) Non-Russell 3000 companies and (4) Post-IPO/Bankruptcy companies. 4 The EPSC evaluates proposals to approve or amend: (i) stock option plans; (ii) restricted stock plans; (iii) omnibus stock plans; and (iv) stock settled stock appreciation rights plans.

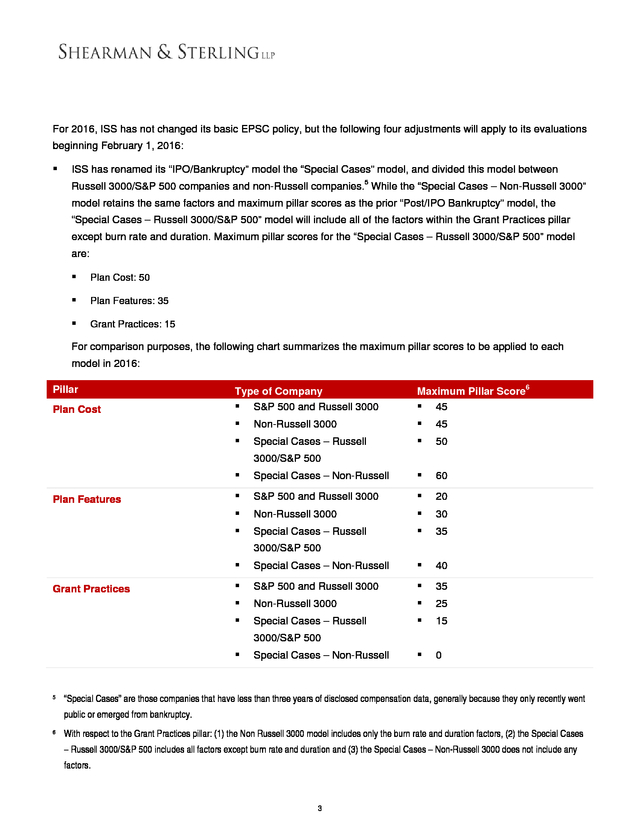

For more information on the EPSC, please see our client memo, “ISS Publishes FAQs on Equity Plan Scorecard,” available at: http://www.shearman.com/~/media/Files/NewsInsights/Publications/2015/01/ISS-Publishes-FAQs-on-Equity-PlanScorecard-EC-and-CG-011215.pdf. 2 . For 2016, ISS has not changed its basic EPSC policy, but the following four adjustments will apply to its evaluations beginning February 1, 2016:  ISS has renamed its “IPO/Bankruptcy” model the “Special Cases” model, and divided this model between Russell 3000/S&P 500 companies and non-Russell companies.5 While the “Special Cases – Non-Russell 3000” model retains the same factors and maximum pillar scores as the prior “Post/IPO Bankruptcy” model, the “Special Cases – Russell 3000/S&P 500” model will include all of the factors within the Grant Practices pillar except burn rate and duration. Maximum pillar scores for the “Special Cases – Russell 3000/S&P 500” model are:  Plan Cost: 50  Plan Features: 35  Grant Practices: 15 For comparison purposes, the following chart summarizes the maximum pillar scores to be applied to each model in 2016: Maximum Pillar Score6  45 Non-Russell 3000  45  Plan Cost Type of Company  S&P 500 and Russell 3000  Pillar Special Cases – Russell  50 3000/S&P 500   60  S&P 500 and Russell 3000  20  Non-Russell 3000  30  Plan Features Special Cases – Non-Russell Special Cases – Russell  35 3000/S&P 500   40  S&P 500 and Russell 3000  35  Non-Russell 3000  25  Grant Practices Special Cases – Non-Russell Special Cases – Russell  15  0 3000/S&P 500  5 Special Cases – Non-Russell “Special Cases” are those companies that have less than three years of disclosed compensation data, generally because they only recently went public or emerged from bankruptcy. 6 With respect to the Grant Practices pillar: (1) the Non Russell 3000 model includes only the burn rate and duration factors, (2) the Special Cases – Russell 3000/S&P 500 includes all factors except burn rate and duration and (3) the Special Cases – Non-Russell 3000 does not include any factors. 3 .  The “Automatic Single-Trigger Vesting” factor, which is grouped under the Plan Features pillar, is renamed “CIC Vesting” with the following scoring levels7:  Full points: Time-based awards only accelerate if they are not assumed or converted, and performancebased awards are forfeited, terminated or vested based on actual performance and/or on a pro-rata basis for time elapsed in the ongoing performance period(s).  No points: Automatic accelerated vesting of time-based awards or payout of performance-based awards above target level.   Half points: Any other vesting terms related to a change in control. With respect to the “Post-Vesting/Exercise Holding Period” factor, which is grouped under the Grant Practice pillar, full points are awarded for holding periods of at least 36 months (rather than 12 months), or until employment termination. A holding period of between 12 and 36 months, or until share ownership guidelines are met, will earn a company half points.8  Finally, ISS has adjusted certain of its confidential factor scores. Say-on-Pay Proposals: Insufficient Executive Compensation Disclosure by Externally Managed Issuers ISS maintains a list of problematic pay practices that it uses to evaluate say-on-pay proposals.9 These practices generally reflect pay elements that are not directly based on performance. ISS evaluates these practices on a case-by-case basis, considering the context of the company’s overall pay program and demonstrated pay for performance philosophy. Beginning in 2016, ISS will include “Insufficient Executive Compensation Disclosure by Externally Managed Issuers” as a problematic pay practice that will generally result in an adverse recommendation on say-on-pay. Externally managed issuers (“EMIs”) are issuers who retain an outside management company to provide services that would otherwise be provided by employees of the issuer.

Executives of an EMI are typically employees of, and compensated by, the external manager. The external manager is then reimbursed by the EMI through a management fee. ISS stated that it identified approximately 60 EMIs (which are typically REITs), and that these 7 The previous policy awarded no points if the plan provided for automatic vesting of outstanding awards upon a change in control and full points if it did not. 8 In order to receive full points, ISS’s new policy requires companies to implement retention requirements that are longer than market standard. According to Shearman & Sterling LLP’s 2015 Annual Survey of the 100 Largest US Public Companies, 67 of the largest US Companies maintain stock retention requirements.

Of these companies, 49 require retention until share ownership guidelines are satisfied and 11 require retention for one-year post exercise or settlement. 9 The complete list of problematic pay practices for 2015 is contained in ISS’s “2015 US Compensation Policies, Frequently Asked Questions,” available at http://www.issgovernance.com/file/policy/2015-us-comp-faqs.pdf. We expect an updated version of this document, effective for shareholder meetings occurring after February 1, 2016, to be made available later in December. 4 . EMIs often do not disclose any details about their executives’ compensation arrangements. In most cases, disclosure is limited to the management fee paid by the EMI to the manager. Notwithstanding these arrangements, EMIs that are public companies must still hold periodic, advisory say-on-pay votes. Previously, ISS raised concerns about a lack of transparency when EMIs subject to a say-on-pay vote did not provide disclosure sufficient to enable investors to cast an informed advisory vote. A major point of concern for ISS was the potential for conflicts of interests.

Without adequate information, shareholders would not be able to judge whether executives were being incentivized to act in the best interests of the external manager, rather than in the best interests of the issuer’s shareholders. Notwithstanding these concerns, ISS does not currently classify “Insufficient Executive Compensation Disclosure by Externally Managed Issuers” as a problematic pay practice that would result in an adverse recommendation on say-on-pay. In August, however, 71% of investors who responded to ISS’s annual policy survey answered that ISS should advise voting against a say-on-pay proposal at an EMI that provides minimal disclosure. Going forward, ISS will generally recommend voting against the say-on-pay proposal of an EMI when insufficient compensation disclosure precludes a reasonable assessment of pay programs and practices applicable to the EMI’s executives. Glass Lewis Updates Unlike the updates to the ISS Guidelines, the updates to the Glass Lewis Guidelines serve to clarify, rather than alter, the policies currently in effect.

This year, Glass Lewis provided further information on its policy towards transitional and one-off awards, factors it considers when issuing recommendations on say-on-pay votes. In addition, Glass Lewis clarified the manner in which it analyzes equity-based compensation plans when those plans are put to shareholders for approval. Finally, Glass Lewis provided additional guidance with respect to the disclosure of long-term incentive awards.  Transitional and One-Off Awards: With respect to executive transitions, Glass Lewis stated that additional information should be provided discussing the terms of any sign-on arrangements or make-whole payments, as well as the process by which the amounts were reached.

In addition, the company should provide a meaningful explanation of any benefits agreed upon outside of the company’s typical arrangements. Glass Lewis will consider the executive’s regular target compensation levels, or sums paid to other executives (including the recipient’s predecessor), in evaluating the appropriateness of these arrangements.  Equity-Based Compensation Plan Proposals (“EBCPPs”): In previous years, Glass Lewis described its analysis of EBCPPs as “primarily quantitative,” and did not provide a narrative discussion of the qualitative factors it considered. The 2016 update, however, includes a summary of the qualitative factors Glass Lewis uses to analyze equity compensation plans, which include plan administration, the method and terms of exercise, repricing history, express or implied rights to reprice, the presence of evergreen provisions and the use of, and difficulty of, performance metrics.

Glass Lewis expects that any changes to the terms of the plan be explained to shareholders, and states that a company’s size and operating environment may be relevant in assessing its concerns, or the benefits of any changes. 5 .  Long-Term Incentive Awards. The Glass Lewis Guidelines now states that companies should disclose the actual performance and vesting levels for previous grants that are earned during the fiscal year. Conclusion As was the case in 2015, neither ISS nor Glass Lewis has adopted major changes to their voting guidelines. Although companies should be aware of and consider the policy recommendations of each advisor, these recommendations should not overrule the judgment of the companies’ directors on compensation policy. 6 . Appendix: EPSC Point Allocation System10 Factor SVT – A + B + C Shares SVT – A + B Shares CIC Equity Vesting Definition Company’s SVT relative to peers – based on new shares requested + shares remaining available + outstanding grants and awards Company’s SVT relative to peers – based on new shares requested + shares remaining available Automatic vesting of outstanding awards upon a change in control Scoring Basis Scaled depending on company SVT versus ISS’s SVT benchmarks Scaled as above Full points for: Time-based awards: no acceleration or accelerate if not assumed/converted, AND  Performance based awards: forfeited, terminated, paid pro rata and/or based on actual performance    Liberal Share Recycling – FV Liberal Share Recycling – Options Minimum Vesting Requirement Full Discretion to Accelerate (non-CIC) 3-Year Average Burn Rate 10 Certain shares not issued (or tendered to the company) related to full value share vesting may be re-granted Certain shares not issued (or tendered to the company) related to option or SAR exercises or tax withholding obligations may be re-granted; or, only shares ultimately issued pursuant to grants of SARs count against the plan’s share reserve, rather than the SARs originally granted Does the plan stipulate a minimum vesting period of at least one year for any award? May the plan administrator accelerate vesting of an award (unrelated to a CIC, death or disability)? Company’s 3-year average burn rate (as a percentage of common shares outstanding) relative to industry and index peers No points for: automatic acceleration of time-based equity or above-target award vesting of performance awards Half of full points for: other provisions Yes – no points No – full points Yes – no points No – full points No or vesting period < 1 year – no points Vesting period =/> 1 year – full points Yes – no points No – full points Scaled depending on company’s burn rate versus ISS benchmarks This chart is taken from ISS’s US Equity Plan Scorecard which is available at: http://www.issgovernance.com/file/policy/faq-on-iss-us-equity-planscorecard-methodology.pdf. A1 . Factor Estimated Plan Duration Definition Estimated time that the proposed share reserve (new shares plus existing reserve) will last, based on company’s 3-year average burn rate activity Scoring Basis Duration =/< 5 years – full points Duration > 5 </= 6 years – ½ of full points CEO’s Grant Vesting Period Period required for full vesting of the most recent equity awards (stock options, restricted shares, performance shares) received by the CEO within the prior 3 years Duration > 6 years – no points Vesting period > 4 years – full points Vesting period =/> 3 </=4 years (or no award in prior 3 years) – ½ of full points CEO’s Proportion of Performance-Conditioned Awards Proportion of the CEO’s most recent fiscal year equity awards (with a 3-year look-back) that is conditioned upon achievement of a disclosed goal Clawback Policy Does the company have a policy that would authorize recovery of gains from all or most equity awards in the event of certain financial restatements? Does the company require shares received from grants under the plan to be held for a specified period following their vesting/exercise? Holding Period Vesting period < 3 years – no points 50% or more – full points 33% < 50% – ½ of full points < 33% – no points Yes – full points No – no points At least 36 months or until end of employment – full points 12 months or until share ownership guidelines met – ½ of full points No holding period/silent – no points A2 . CONTACTS John J. Cannon III New York + 1.212.848.8159 jcannon@shearman.com Kenneth J. Laverriere New York + 1.212.848.8172 klaverriere@shearman.com Doreen E. Lilienfeld New York + 1.212.848.7171 dlilienfeld@shearman.com Linda E.

Rappaport New York + 1.212.848.7004 lrappaport@shearman.com George T. Spera, Jr. New York + 1.212.848.7636 gspera@shearman.com ABU DHABI | BEIJING | BRUSSELS | DUBAI | FRANKFURT | HONG KONG | LONDON | MENLO PARK | MILAN | NEW YORK PARIS | ROME | SAN FRANCISCO | SÃO PAULO | SAUDI ARABIA* | SHANGHAI | SINGAPORE | TOKYO | TORONTO | WASHINGTON, DC This memorandum is intended only as a general discussion of these issues. It should not be regarded as legal advice.

We would be pleased to provide additional details or advice about specific situations if desired. 599 LEXINGTON AVENUE | NEW YORK | NY | 10022-6069 Copyright © 2015 Shearman & Sterling LLP. Shearman & Sterling LLP is a limited liability partnership organized under the laws of the State of Delaware, with an affiliated limited liability partnership organized for the practice of law in the United Kingdom and Italy and an affiliated partnership organized for the practice of law in Hong Kong. *Abdulaziz Alassaf & Partners in association with Shearman & Sterling LLP A3 . . . . . . . . . . . . . . . . . . . . . . . .

These proposals require retention during employment, and for two years following the termination of employment, and for the company to report to shareholders regarding the policy. Under existing policies, ISS considers each proposal on a case-by-case basis, taking into account: (1) any holding period, retention ratio or ownership requirements already in place at the company, and whether these polices are rigorous and meaningful; (2) actual officer ownership, and how it compares to the company’s policy or the proponent’s suggested policy; and (3) problematic pay practices, current and past, which may promote a short-term 1 The ISS Guidelines are available at: http://www.issgovernance.com/policy-gateway/2016-policy-information/. 2 The EPSC is available at: http://www.issgovernance.com/file/policy/faq-on-iss-us-equity-plan-scorecard-methodology.pdf. 3 The Glass Lewis Guidelines are available at: http://www.glasslewis.com/assets/uploads/2015/11/GUIDELINES_United_States_20161.pdf. . focus. In addition, ISS considers any post-termination holding requirements, and any other policies aimed at mitigating risk-taking by senior executives, when evaluating proposals that did not contain a retention ratio. For 2016, ISS has amended its policies to address equity retention proposals more generally. ISS will evaluate all equity retention proposals for senior executive officers on a case-by-case basis, with the following factors taken into account:  The percentage of net shares required to be retained;  The required retention period;  Whether the company has equity retention, holding period or stock ownership requirements in place and the robustness of those requirements;  Whether the company has any other policies aimed at mitigating risk taking by executives;  The executives’ actual stock ownership levels and the degree to which they meet or exceed the proponents’ suggested holding period/retention ratio or the company’s existing requirements; and  Problematic pay practices, current and past, which may demonstrate a short-term versus long-term focus. Updates to the Equity Plan Scorecard In 2015, ISS implemented a new model for evaluating equity incentive plan proposals, the EPSC, which ISS believes allows for a more nuanced consideration of equity incentive programs.4 Rather than applying a series of “pass/fail” tests, the EPSC considers a range of positive and negative factors, each of which it groups into one of three “pillars”: Plan Cost, Plan Features and Grant Practices. Each factor is provided a maximum number of points, with the total number of points that can be earned equaling 100, and a score of 53 or above earning a company a positive recommendation on its equity incentive plan proposal.

(A chart listing each factor, the pillar in which it is grouped, and ISS’s method for allocating points with respect to each factor, is included as an Appendix at the end of this memo.) Although ISS keeps confidential the number of points available for each individual factor, it does disclose the maximum number of points that can be earned for each pillar. These maximum pillar scores vary depending on the type of company whose plan is being evaluated. In 2015, there were four different models, one for each of: (1) S&P 500 companies, (2) Russell 3000 companies, (3) Non-Russell 3000 companies and (4) Post-IPO/Bankruptcy companies. 4 The EPSC evaluates proposals to approve or amend: (i) stock option plans; (ii) restricted stock plans; (iii) omnibus stock plans; and (iv) stock settled stock appreciation rights plans.

For more information on the EPSC, please see our client memo, “ISS Publishes FAQs on Equity Plan Scorecard,” available at: http://www.shearman.com/~/media/Files/NewsInsights/Publications/2015/01/ISS-Publishes-FAQs-on-Equity-PlanScorecard-EC-and-CG-011215.pdf. 2 . For 2016, ISS has not changed its basic EPSC policy, but the following four adjustments will apply to its evaluations beginning February 1, 2016:  ISS has renamed its “IPO/Bankruptcy” model the “Special Cases” model, and divided this model between Russell 3000/S&P 500 companies and non-Russell companies.5 While the “Special Cases – Non-Russell 3000” model retains the same factors and maximum pillar scores as the prior “Post/IPO Bankruptcy” model, the “Special Cases – Russell 3000/S&P 500” model will include all of the factors within the Grant Practices pillar except burn rate and duration. Maximum pillar scores for the “Special Cases – Russell 3000/S&P 500” model are:  Plan Cost: 50  Plan Features: 35  Grant Practices: 15 For comparison purposes, the following chart summarizes the maximum pillar scores to be applied to each model in 2016: Maximum Pillar Score6  45 Non-Russell 3000  45  Plan Cost Type of Company  S&P 500 and Russell 3000  Pillar Special Cases – Russell  50 3000/S&P 500   60  S&P 500 and Russell 3000  20  Non-Russell 3000  30  Plan Features Special Cases – Non-Russell Special Cases – Russell  35 3000/S&P 500   40  S&P 500 and Russell 3000  35  Non-Russell 3000  25  Grant Practices Special Cases – Non-Russell Special Cases – Russell  15  0 3000/S&P 500  5 Special Cases – Non-Russell “Special Cases” are those companies that have less than three years of disclosed compensation data, generally because they only recently went public or emerged from bankruptcy. 6 With respect to the Grant Practices pillar: (1) the Non Russell 3000 model includes only the burn rate and duration factors, (2) the Special Cases – Russell 3000/S&P 500 includes all factors except burn rate and duration and (3) the Special Cases – Non-Russell 3000 does not include any factors. 3 .  The “Automatic Single-Trigger Vesting” factor, which is grouped under the Plan Features pillar, is renamed “CIC Vesting” with the following scoring levels7:  Full points: Time-based awards only accelerate if they are not assumed or converted, and performancebased awards are forfeited, terminated or vested based on actual performance and/or on a pro-rata basis for time elapsed in the ongoing performance period(s).  No points: Automatic accelerated vesting of time-based awards or payout of performance-based awards above target level.   Half points: Any other vesting terms related to a change in control. With respect to the “Post-Vesting/Exercise Holding Period” factor, which is grouped under the Grant Practice pillar, full points are awarded for holding periods of at least 36 months (rather than 12 months), or until employment termination. A holding period of between 12 and 36 months, or until share ownership guidelines are met, will earn a company half points.8  Finally, ISS has adjusted certain of its confidential factor scores. Say-on-Pay Proposals: Insufficient Executive Compensation Disclosure by Externally Managed Issuers ISS maintains a list of problematic pay practices that it uses to evaluate say-on-pay proposals.9 These practices generally reflect pay elements that are not directly based on performance. ISS evaluates these practices on a case-by-case basis, considering the context of the company’s overall pay program and demonstrated pay for performance philosophy. Beginning in 2016, ISS will include “Insufficient Executive Compensation Disclosure by Externally Managed Issuers” as a problematic pay practice that will generally result in an adverse recommendation on say-on-pay. Externally managed issuers (“EMIs”) are issuers who retain an outside management company to provide services that would otherwise be provided by employees of the issuer.

Executives of an EMI are typically employees of, and compensated by, the external manager. The external manager is then reimbursed by the EMI through a management fee. ISS stated that it identified approximately 60 EMIs (which are typically REITs), and that these 7 The previous policy awarded no points if the plan provided for automatic vesting of outstanding awards upon a change in control and full points if it did not. 8 In order to receive full points, ISS’s new policy requires companies to implement retention requirements that are longer than market standard. According to Shearman & Sterling LLP’s 2015 Annual Survey of the 100 Largest US Public Companies, 67 of the largest US Companies maintain stock retention requirements.

Of these companies, 49 require retention until share ownership guidelines are satisfied and 11 require retention for one-year post exercise or settlement. 9 The complete list of problematic pay practices for 2015 is contained in ISS’s “2015 US Compensation Policies, Frequently Asked Questions,” available at http://www.issgovernance.com/file/policy/2015-us-comp-faqs.pdf. We expect an updated version of this document, effective for shareholder meetings occurring after February 1, 2016, to be made available later in December. 4 . EMIs often do not disclose any details about their executives’ compensation arrangements. In most cases, disclosure is limited to the management fee paid by the EMI to the manager. Notwithstanding these arrangements, EMIs that are public companies must still hold periodic, advisory say-on-pay votes. Previously, ISS raised concerns about a lack of transparency when EMIs subject to a say-on-pay vote did not provide disclosure sufficient to enable investors to cast an informed advisory vote. A major point of concern for ISS was the potential for conflicts of interests.

Without adequate information, shareholders would not be able to judge whether executives were being incentivized to act in the best interests of the external manager, rather than in the best interests of the issuer’s shareholders. Notwithstanding these concerns, ISS does not currently classify “Insufficient Executive Compensation Disclosure by Externally Managed Issuers” as a problematic pay practice that would result in an adverse recommendation on say-on-pay. In August, however, 71% of investors who responded to ISS’s annual policy survey answered that ISS should advise voting against a say-on-pay proposal at an EMI that provides minimal disclosure. Going forward, ISS will generally recommend voting against the say-on-pay proposal of an EMI when insufficient compensation disclosure precludes a reasonable assessment of pay programs and practices applicable to the EMI’s executives. Glass Lewis Updates Unlike the updates to the ISS Guidelines, the updates to the Glass Lewis Guidelines serve to clarify, rather than alter, the policies currently in effect.

This year, Glass Lewis provided further information on its policy towards transitional and one-off awards, factors it considers when issuing recommendations on say-on-pay votes. In addition, Glass Lewis clarified the manner in which it analyzes equity-based compensation plans when those plans are put to shareholders for approval. Finally, Glass Lewis provided additional guidance with respect to the disclosure of long-term incentive awards.  Transitional and One-Off Awards: With respect to executive transitions, Glass Lewis stated that additional information should be provided discussing the terms of any sign-on arrangements or make-whole payments, as well as the process by which the amounts were reached.

In addition, the company should provide a meaningful explanation of any benefits agreed upon outside of the company’s typical arrangements. Glass Lewis will consider the executive’s regular target compensation levels, or sums paid to other executives (including the recipient’s predecessor), in evaluating the appropriateness of these arrangements.  Equity-Based Compensation Plan Proposals (“EBCPPs”): In previous years, Glass Lewis described its analysis of EBCPPs as “primarily quantitative,” and did not provide a narrative discussion of the qualitative factors it considered. The 2016 update, however, includes a summary of the qualitative factors Glass Lewis uses to analyze equity compensation plans, which include plan administration, the method and terms of exercise, repricing history, express or implied rights to reprice, the presence of evergreen provisions and the use of, and difficulty of, performance metrics.

Glass Lewis expects that any changes to the terms of the plan be explained to shareholders, and states that a company’s size and operating environment may be relevant in assessing its concerns, or the benefits of any changes. 5 .  Long-Term Incentive Awards. The Glass Lewis Guidelines now states that companies should disclose the actual performance and vesting levels for previous grants that are earned during the fiscal year. Conclusion As was the case in 2015, neither ISS nor Glass Lewis has adopted major changes to their voting guidelines. Although companies should be aware of and consider the policy recommendations of each advisor, these recommendations should not overrule the judgment of the companies’ directors on compensation policy. 6 . Appendix: EPSC Point Allocation System10 Factor SVT – A + B + C Shares SVT – A + B Shares CIC Equity Vesting Definition Company’s SVT relative to peers – based on new shares requested + shares remaining available + outstanding grants and awards Company’s SVT relative to peers – based on new shares requested + shares remaining available Automatic vesting of outstanding awards upon a change in control Scoring Basis Scaled depending on company SVT versus ISS’s SVT benchmarks Scaled as above Full points for: Time-based awards: no acceleration or accelerate if not assumed/converted, AND  Performance based awards: forfeited, terminated, paid pro rata and/or based on actual performance    Liberal Share Recycling – FV Liberal Share Recycling – Options Minimum Vesting Requirement Full Discretion to Accelerate (non-CIC) 3-Year Average Burn Rate 10 Certain shares not issued (or tendered to the company) related to full value share vesting may be re-granted Certain shares not issued (or tendered to the company) related to option or SAR exercises or tax withholding obligations may be re-granted; or, only shares ultimately issued pursuant to grants of SARs count against the plan’s share reserve, rather than the SARs originally granted Does the plan stipulate a minimum vesting period of at least one year for any award? May the plan administrator accelerate vesting of an award (unrelated to a CIC, death or disability)? Company’s 3-year average burn rate (as a percentage of common shares outstanding) relative to industry and index peers No points for: automatic acceleration of time-based equity or above-target award vesting of performance awards Half of full points for: other provisions Yes – no points No – full points Yes – no points No – full points No or vesting period < 1 year – no points Vesting period =/> 1 year – full points Yes – no points No – full points Scaled depending on company’s burn rate versus ISS benchmarks This chart is taken from ISS’s US Equity Plan Scorecard which is available at: http://www.issgovernance.com/file/policy/faq-on-iss-us-equity-planscorecard-methodology.pdf. A1 . Factor Estimated Plan Duration Definition Estimated time that the proposed share reserve (new shares plus existing reserve) will last, based on company’s 3-year average burn rate activity Scoring Basis Duration =/< 5 years – full points Duration > 5 </= 6 years – ½ of full points CEO’s Grant Vesting Period Period required for full vesting of the most recent equity awards (stock options, restricted shares, performance shares) received by the CEO within the prior 3 years Duration > 6 years – no points Vesting period > 4 years – full points Vesting period =/> 3 </=4 years (or no award in prior 3 years) – ½ of full points CEO’s Proportion of Performance-Conditioned Awards Proportion of the CEO’s most recent fiscal year equity awards (with a 3-year look-back) that is conditioned upon achievement of a disclosed goal Clawback Policy Does the company have a policy that would authorize recovery of gains from all or most equity awards in the event of certain financial restatements? Does the company require shares received from grants under the plan to be held for a specified period following their vesting/exercise? Holding Period Vesting period < 3 years – no points 50% or more – full points 33% < 50% – ½ of full points < 33% – no points Yes – full points No – no points At least 36 months or until end of employment – full points 12 months or until share ownership guidelines met – ½ of full points No holding period/silent – no points A2 . CONTACTS John J. Cannon III New York + 1.212.848.8159 jcannon@shearman.com Kenneth J. Laverriere New York + 1.212.848.8172 klaverriere@shearman.com Doreen E. Lilienfeld New York + 1.212.848.7171 dlilienfeld@shearman.com Linda E.

Rappaport New York + 1.212.848.7004 lrappaport@shearman.com George T. Spera, Jr. New York + 1.212.848.7636 gspera@shearman.com ABU DHABI | BEIJING | BRUSSELS | DUBAI | FRANKFURT | HONG KONG | LONDON | MENLO PARK | MILAN | NEW YORK PARIS | ROME | SAN FRANCISCO | SÃO PAULO | SAUDI ARABIA* | SHANGHAI | SINGAPORE | TOKYO | TORONTO | WASHINGTON, DC This memorandum is intended only as a general discussion of these issues. It should not be regarded as legal advice.

We would be pleased to provide additional details or advice about specific situations if desired. 599 LEXINGTON AVENUE | NEW YORK | NY | 10022-6069 Copyright © 2015 Shearman & Sterling LLP. Shearman & Sterling LLP is a limited liability partnership organized under the laws of the State of Delaware, with an affiliated limited liability partnership organized for the practice of law in the United Kingdom and Italy and an affiliated partnership organized for the practice of law in Hong Kong. *Abdulaziz Alassaf & Partners in association with Shearman & Sterling LLP A3 . . . . . . . . . . . . . . . . . . . . . . . .