Description

Our Perspective

BREXIT AND MUNIS - JUNE 2016

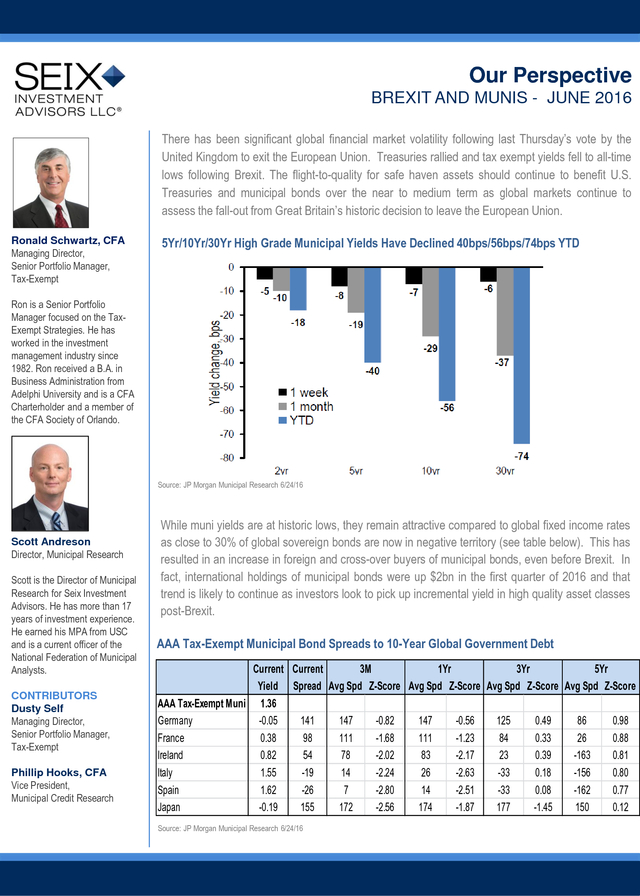

There has been significant global financial market volatility following last Thursday’s vote by the

United Kingdom to exit the European Union. Treasuries rallied and tax exempt yields fell to all-time

lows following Brexit. The flight-to-quality for safe haven assets should continue to benefit U.S.

Treasuries and municipal bonds over the near to medium term as global markets continue to

assess the fall-out from Great Britain’s historic decision to leave the European Union.

Ronald Schwartz, CFA

Managing Director,

Senior Portfolio Manager,

Tax-Exempt

5Yr/10Yr/30Yr High Grade Municipal Yields Have Declined 40bps/56bps/74bps YTD

Ron is a Senior Portfolio

Manager focused on the TaxExempt Strategies. He has

worked in the investment

management industry since

1982.

Ron received a B.A. in Business Administration from Adelphi University and is a CFA Charterholder and a member of the CFA Society of Orlando. Source: JP Morgan Municipal Research 6/24/16 Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 17 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research While muni yields are at historic lows, they remain attractive compared to global fixed income rates as close to 30% of global sovereign bonds are now in negative territory (see table below).

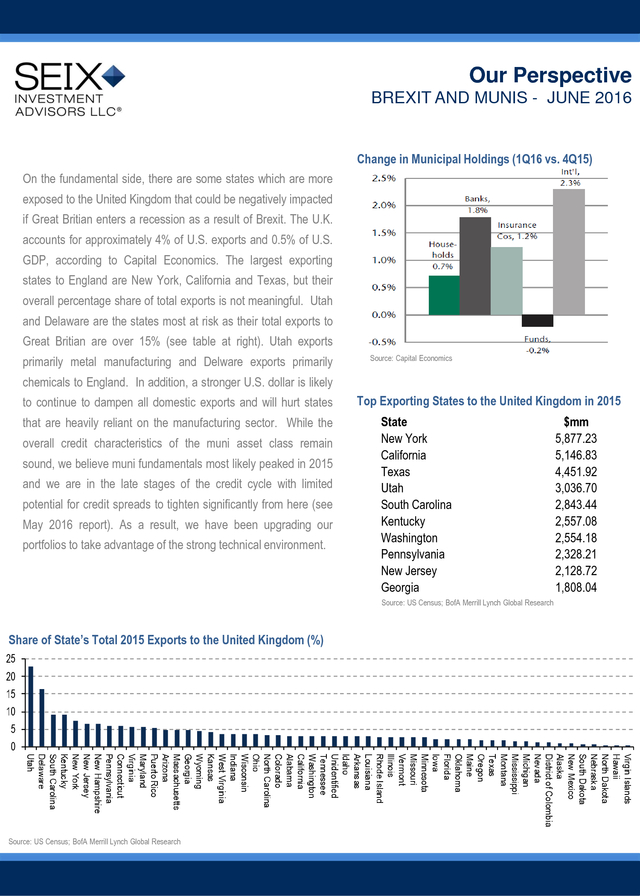

This has resulted in an increase in foreign and cross-over buyers of municipal bonds, even before Brexit. In fact, international holdings of municipal bonds were up $2bn in the first quarter of 2016 and that trend is likely to continue as investors look to pick up incremental yield in high quality asset classes post-Brexit. AAA Tax-Exempt Municipal Bond Spreads to 10-Year Global Government Debt Current Current 3M 1Yr 3Yr 5Yr Yield Spread Avg Spd Z-Score Avg Spd Z-Score Avg Spd Z-Score Avg Spd Z-Score AAA Tax-Exempt Muni 1.36 Germany -0.05 141 147 -0.82 147 -0.56 125 0.49 86 0.98 France 0.38 98 111 -1.68 111 -1.23 84 0.33 26 0.88 Ireland 0.82 54 78 -2.02 83 -2.17 23 0.39 -163 0.81 Italy 1.55 -19 14 -2.24 26 -2.63 -33 0.18 -156 0.80 Spain 1.62 -26 7 -2.80 14 -2.51 -33 0.08 -162 0.77 Japan -0.19 155 172 -2.56 174 -1.87 177 -1.45 150 0.12 Source: JP Morgan Municipal Research 6/24/16 . Our Perspective BREXIT AND MUNIS - JUNE 2016 Change in Municipal Holdings (1Q16 vs. 4Q15) On the fundamental side, there are some states which are more exposed to the United Kingdom that could be negatively impacted if Great Britian enters a recession as a result of Brexit. The U.K. accounts for approximately 4% of U.S. exports and 0.5% of U.S. GDP, according to Capital Economics.

The largest exporting states to England are New York, California and Texas, but their overall percentage share of total exports is not meaningful. Utah and Delaware are the states most at risk as their total exports to Great Britian are over 15% (see table at right). Utah exports primarily metal manufacturing and Delware exports primarily Source: Capital Economics chemicals to England.

In addition, a stronger U.S. dollar is likely to continue to dampen all domestic exports and will hurt states that are heavily reliant on the manufacturing sector. While the overall credit characteristics of the muni asset class remain sound, we believe muni fundamentals most likely peaked in 2015 and we are in the late stages of the credit cycle with limited potential for credit spreads to tighten significantly from here (see May 2016 report).

As a result, we have been upgrading our portfolios to take advantage of the strong technical environment. Top Exporting States to the United Kingdom in 2015 State New York California Texas Utah South Carolina Kentucky Washington Pennsylvania New Jersey Georgia Source: US Census; BofA Merrill Lynch Global Research Share of State’s Total 2015 Exports to the United Kingdom (%) Source: US Census; BofA Merrill Lynch Global Research $mm 5,877.23 5,146.83 4,451.92 3,036.70 2,843.44 2,557.08 2,554.18 2,328.21 2,128.72 1,808.04 . Our Perspective BREXIT AND MUNIS - JUNE 2016 Post-Brexit anxiety, coupled with a growing risk of recession for many sovereign economies, will likely keep long term rates lower for longer. Financial market volatility is likely to remain throughout the year given the current macroeconomic backdrop and increasing political uncertainty as we approach the presidential election. Investors are likely to keep seeking safe havens from global financial market volatility and evolving monetary policy. Tax exempt bonds fit the safe haven bill as they are highly rated with an extremely low default rate (see February 2016 report).

As a result, we remain constructive on the municipal sector because of its tax exempt income, strong technical factors, and compelling yields compared to other global fixed income rates for the second half of 2016. The assertions in this perspective are Seix Investment Advisors’ opinion. BofA Merrill Lynch Municipal Master Index tracks the performance of the investment-grade U.S. tax-exempt bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule, and an investment grade rating (based on average of Moody’s, S&P, and Fitch). Investment Risks: All investments involve risk.

Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa.

A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax. There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative.

All information contained herein is believed to be correct, but accuracy cannot be guaranteed. This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice.

Seix Investment Advisors does not provide legal, estate planning or tax advice. Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2016 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .

Ron received a B.A. in Business Administration from Adelphi University and is a CFA Charterholder and a member of the CFA Society of Orlando. Source: JP Morgan Municipal Research 6/24/16 Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 17 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research While muni yields are at historic lows, they remain attractive compared to global fixed income rates as close to 30% of global sovereign bonds are now in negative territory (see table below).

This has resulted in an increase in foreign and cross-over buyers of municipal bonds, even before Brexit. In fact, international holdings of municipal bonds were up $2bn in the first quarter of 2016 and that trend is likely to continue as investors look to pick up incremental yield in high quality asset classes post-Brexit. AAA Tax-Exempt Municipal Bond Spreads to 10-Year Global Government Debt Current Current 3M 1Yr 3Yr 5Yr Yield Spread Avg Spd Z-Score Avg Spd Z-Score Avg Spd Z-Score Avg Spd Z-Score AAA Tax-Exempt Muni 1.36 Germany -0.05 141 147 -0.82 147 -0.56 125 0.49 86 0.98 France 0.38 98 111 -1.68 111 -1.23 84 0.33 26 0.88 Ireland 0.82 54 78 -2.02 83 -2.17 23 0.39 -163 0.81 Italy 1.55 -19 14 -2.24 26 -2.63 -33 0.18 -156 0.80 Spain 1.62 -26 7 -2.80 14 -2.51 -33 0.08 -162 0.77 Japan -0.19 155 172 -2.56 174 -1.87 177 -1.45 150 0.12 Source: JP Morgan Municipal Research 6/24/16 . Our Perspective BREXIT AND MUNIS - JUNE 2016 Change in Municipal Holdings (1Q16 vs. 4Q15) On the fundamental side, there are some states which are more exposed to the United Kingdom that could be negatively impacted if Great Britian enters a recession as a result of Brexit. The U.K. accounts for approximately 4% of U.S. exports and 0.5% of U.S. GDP, according to Capital Economics.

The largest exporting states to England are New York, California and Texas, but their overall percentage share of total exports is not meaningful. Utah and Delaware are the states most at risk as their total exports to Great Britian are over 15% (see table at right). Utah exports primarily metal manufacturing and Delware exports primarily Source: Capital Economics chemicals to England.

In addition, a stronger U.S. dollar is likely to continue to dampen all domestic exports and will hurt states that are heavily reliant on the manufacturing sector. While the overall credit characteristics of the muni asset class remain sound, we believe muni fundamentals most likely peaked in 2015 and we are in the late stages of the credit cycle with limited potential for credit spreads to tighten significantly from here (see May 2016 report).

As a result, we have been upgrading our portfolios to take advantage of the strong technical environment. Top Exporting States to the United Kingdom in 2015 State New York California Texas Utah South Carolina Kentucky Washington Pennsylvania New Jersey Georgia Source: US Census; BofA Merrill Lynch Global Research Share of State’s Total 2015 Exports to the United Kingdom (%) Source: US Census; BofA Merrill Lynch Global Research $mm 5,877.23 5,146.83 4,451.92 3,036.70 2,843.44 2,557.08 2,554.18 2,328.21 2,128.72 1,808.04 . Our Perspective BREXIT AND MUNIS - JUNE 2016 Post-Brexit anxiety, coupled with a growing risk of recession for many sovereign economies, will likely keep long term rates lower for longer. Financial market volatility is likely to remain throughout the year given the current macroeconomic backdrop and increasing political uncertainty as we approach the presidential election. Investors are likely to keep seeking safe havens from global financial market volatility and evolving monetary policy. Tax exempt bonds fit the safe haven bill as they are highly rated with an extremely low default rate (see February 2016 report).

As a result, we remain constructive on the municipal sector because of its tax exempt income, strong technical factors, and compelling yields compared to other global fixed income rates for the second half of 2016. The assertions in this perspective are Seix Investment Advisors’ opinion. BofA Merrill Lynch Municipal Master Index tracks the performance of the investment-grade U.S. tax-exempt bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule, and an investment grade rating (based on average of Moody’s, S&P, and Fitch). Investment Risks: All investments involve risk.

Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa.

A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax. There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative.

All information contained herein is believed to be correct, but accuracy cannot be guaranteed. This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice.

Seix Investment Advisors does not provide legal, estate planning or tax advice. Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2016 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .