Municipal Market Update: Tax Reform And Munis - January 25, 2017

Seix Investment Advisors

Description

Our Perspective

TAX REFORM AND MUNIS – JANUARY 2017

Ronald Schwartz, CFA

Managing Director,

Senior Portfolio Manager,

Tax-Exempt

Ron is a Senior Portfolio

Manager focused on the TaxExempt Strategies. He has

worked in the investment

management industry since

1982. Ron received a B.A. in

Business Administration from

Adelphi University and is a CFA

Charterholder and a member of

the CFA Society of Orlando.

The Trump election is clearly a potential paradigm shift for the U.S.

economy and asset markets, and until there is greater clarity surrounding budget and policy priorities in the coming weeks and months, market volatility will likely remain high. Per our election report, we believe the election impact on the municipal market will surround three key policies: tax reform, repeal of the Affordable Care Act (ACA), and an increase in domestic infrastructure spending. This month we are going to focus on tax reform and the possible implications for tax exempt bonds. Tax reform could impact municipal bonds directly by eliminating or capping the tax exemption or indirectly by lowering of the personal and corporate marginal tax rates, thereby possibly changing investor demand.

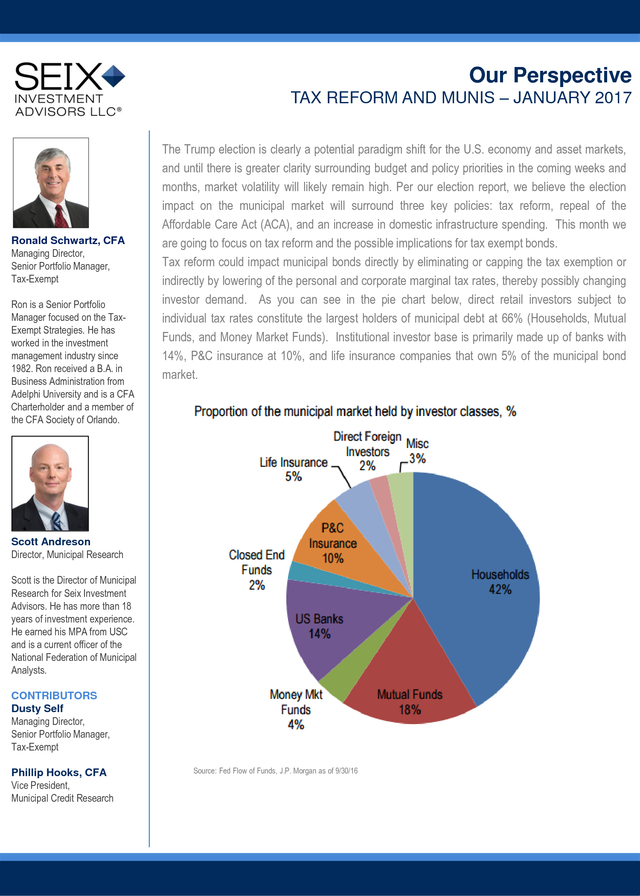

As you can see in the pie chart below, direct retail investors subject to individual tax rates constitute the largest holders of municipal debt at 66% (Households, Mutual Funds, and Money Market Funds). Institutional investor base is primarily made up of banks with 14%, P&C insurance at 10%, and life insurance companies that own 5% of the municipal bond market. Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 18 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research Source: Fed Flow of Funds, J.P.

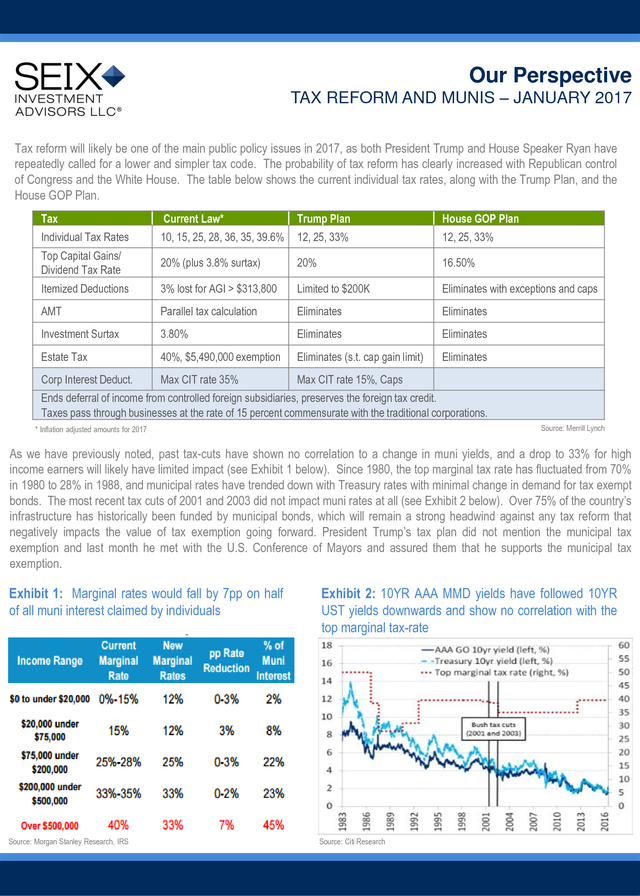

Morgan as of 9/30/16 . Our Perspective TAX REFORM AND MUNIS – JANUARY 2017 Tax reform will likely be one of the main public policy issues in 2017, as both President Trump and House Speaker Ryan have repeatedly called for a lower and simpler tax code. The probability of tax reform has clearly increased with Republican control of Congress and the White House. The table below shows the current individual tax rates, along with the Trump Plan, and the House GOP Plan. Tax Current Law* Trump Plan House GOP Plan Individual Tax Rates 10, 15, 25, 28, 36, 35, 39.6% 12, 25, 33% 12, 25, 33% Top Capital Gains/ Dividend Tax Rate 20% (plus 3.8% surtax) 20% 16.50% Itemized Deductions 3% lost for AGI > $313,800 Limited to $200K Eliminates with exceptions and caps AMT Parallel tax calculation Eliminates Eliminates Investment Surtax 3.80% Eliminates Eliminates Estate Tax 40%, $5,490,000 exemption Eliminates (s.t. cap gain limit) Eliminates Corp Interest Deduct. Max CIT rate 35% Max CIT rate 15%, Caps Ends deferral of income from controlled foreign subsidiaries, preserves the foreign tax credit. Taxes pass through businesses at the rate of 15 percent commensurate with the traditional corporations. Source: Merrill Lynch * Inflation adjusted amounts for 2017 As we have previously noted, past tax-cuts have shown no correlation to a change in muni yields, and a drop to 33% for high income earners will likely have limited impact (see Exhibit 1 below).

Since 1980, the top marginal tax rate has fluctuated from 70% in 1980 to 28% in 1988, and municipal rates have trended down with Treasury rates with minimal change in demand for tax exempt bonds. The most recent tax cuts of 2001 and 2003 did not impact muni rates at all (see Exhibit 2 below). Over 75% of the country’s infrastructure has historically been funded by municipal bonds, which will remain a strong headwind against any tax reform that negatively impacts the value of tax exemption going forward.

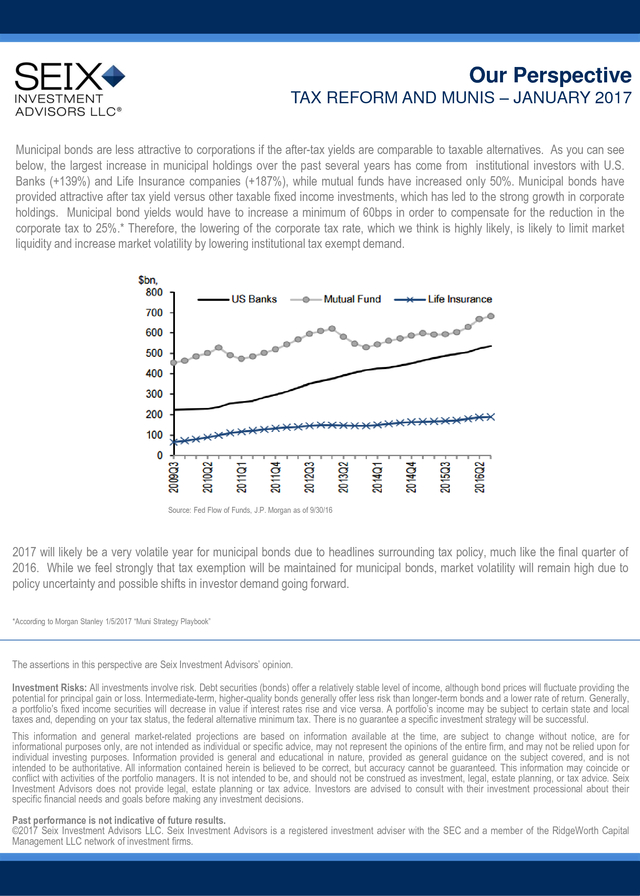

President Trump’s tax plan did not mention the municipal tax exemption and last month he met with the U.S. Conference of Mayors and assured them that he supports the municipal tax exemption. Exhibit 1: Marginal rates would fall by 7pp on half of all muni interest claimed by individuals Exhibit 2: 10YR AAA MMD yields have followed 10YR UST yields downwards and show no correlation with the top marginal tax-rate Source: Morgan Stanley Research, IRS Source: Citi Research . Our Perspective TAX REFORM AND MUNIS – JANUARY 2017 Municipal bonds are less attractive to corporations if the after-tax yields are comparable to taxable alternatives. As you can see below, the largest increase in municipal holdings over the past several years has come from institutional investors with U.S. Banks (+139%) and Life Insurance companies (+187%), while mutual funds have increased only 50%. Municipal bonds have provided attractive after tax yield versus other taxable fixed income investments, which has led to the strong growth in corporate holdings. Municipal bond yields would have to increase a minimum of 60bps in order to compensate for the reduction in the corporate tax to 25%.* Therefore, the lowering of the corporate tax rate, which we think is highly likely, is likely to limit market liquidity and increase market volatility by lowering institutional tax exempt demand. Source: Fed Flow of Funds, J.P.

Morgan as of 9/30/16 2017 will likely be a very volatile year for municipal bonds due to headlines surrounding tax policy, much like the final quarter of 2016. While we feel strongly that tax exemption will be maintained for municipal bonds, market volatility will remain high due to policy uncertainty and possible shifts in investor demand going forward. *According to Morgan Stanley 1/5/2017 “Muni Strategy Playbook” The assertions in this perspective are Seix Investment Advisors’ opinion. Investment Risks: All investments involve risk. Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss.

Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa. A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax.

There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative. All information contained herein is believed to be correct, but accuracy cannot be guaranteed.

This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice. Seix Investment Advisors does not provide legal, estate planning or tax advice.

Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2017 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .

economy and asset markets, and until there is greater clarity surrounding budget and policy priorities in the coming weeks and months, market volatility will likely remain high. Per our election report, we believe the election impact on the municipal market will surround three key policies: tax reform, repeal of the Affordable Care Act (ACA), and an increase in domestic infrastructure spending. This month we are going to focus on tax reform and the possible implications for tax exempt bonds. Tax reform could impact municipal bonds directly by eliminating or capping the tax exemption or indirectly by lowering of the personal and corporate marginal tax rates, thereby possibly changing investor demand.

As you can see in the pie chart below, direct retail investors subject to individual tax rates constitute the largest holders of municipal debt at 66% (Households, Mutual Funds, and Money Market Funds). Institutional investor base is primarily made up of banks with 14%, P&C insurance at 10%, and life insurance companies that own 5% of the municipal bond market. Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 18 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research Source: Fed Flow of Funds, J.P.

Morgan as of 9/30/16 . Our Perspective TAX REFORM AND MUNIS – JANUARY 2017 Tax reform will likely be one of the main public policy issues in 2017, as both President Trump and House Speaker Ryan have repeatedly called for a lower and simpler tax code. The probability of tax reform has clearly increased with Republican control of Congress and the White House. The table below shows the current individual tax rates, along with the Trump Plan, and the House GOP Plan. Tax Current Law* Trump Plan House GOP Plan Individual Tax Rates 10, 15, 25, 28, 36, 35, 39.6% 12, 25, 33% 12, 25, 33% Top Capital Gains/ Dividend Tax Rate 20% (plus 3.8% surtax) 20% 16.50% Itemized Deductions 3% lost for AGI > $313,800 Limited to $200K Eliminates with exceptions and caps AMT Parallel tax calculation Eliminates Eliminates Investment Surtax 3.80% Eliminates Eliminates Estate Tax 40%, $5,490,000 exemption Eliminates (s.t. cap gain limit) Eliminates Corp Interest Deduct. Max CIT rate 35% Max CIT rate 15%, Caps Ends deferral of income from controlled foreign subsidiaries, preserves the foreign tax credit. Taxes pass through businesses at the rate of 15 percent commensurate with the traditional corporations. Source: Merrill Lynch * Inflation adjusted amounts for 2017 As we have previously noted, past tax-cuts have shown no correlation to a change in muni yields, and a drop to 33% for high income earners will likely have limited impact (see Exhibit 1 below).

Since 1980, the top marginal tax rate has fluctuated from 70% in 1980 to 28% in 1988, and municipal rates have trended down with Treasury rates with minimal change in demand for tax exempt bonds. The most recent tax cuts of 2001 and 2003 did not impact muni rates at all (see Exhibit 2 below). Over 75% of the country’s infrastructure has historically been funded by municipal bonds, which will remain a strong headwind against any tax reform that negatively impacts the value of tax exemption going forward.

President Trump’s tax plan did not mention the municipal tax exemption and last month he met with the U.S. Conference of Mayors and assured them that he supports the municipal tax exemption. Exhibit 1: Marginal rates would fall by 7pp on half of all muni interest claimed by individuals Exhibit 2: 10YR AAA MMD yields have followed 10YR UST yields downwards and show no correlation with the top marginal tax-rate Source: Morgan Stanley Research, IRS Source: Citi Research . Our Perspective TAX REFORM AND MUNIS – JANUARY 2017 Municipal bonds are less attractive to corporations if the after-tax yields are comparable to taxable alternatives. As you can see below, the largest increase in municipal holdings over the past several years has come from institutional investors with U.S. Banks (+139%) and Life Insurance companies (+187%), while mutual funds have increased only 50%. Municipal bonds have provided attractive after tax yield versus other taxable fixed income investments, which has led to the strong growth in corporate holdings. Municipal bond yields would have to increase a minimum of 60bps in order to compensate for the reduction in the corporate tax to 25%.* Therefore, the lowering of the corporate tax rate, which we think is highly likely, is likely to limit market liquidity and increase market volatility by lowering institutional tax exempt demand. Source: Fed Flow of Funds, J.P.

Morgan as of 9/30/16 2017 will likely be a very volatile year for municipal bonds due to headlines surrounding tax policy, much like the final quarter of 2016. While we feel strongly that tax exemption will be maintained for municipal bonds, market volatility will remain high due to policy uncertainty and possible shifts in investor demand going forward. *According to Morgan Stanley 1/5/2017 “Muni Strategy Playbook” The assertions in this perspective are Seix Investment Advisors’ opinion. Investment Risks: All investments involve risk. Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss.

Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa. A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax.

There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative. All information contained herein is believed to be correct, but accuracy cannot be guaranteed.

This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice. Seix Investment Advisors does not provide legal, estate planning or tax advice.

Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2017 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .