Description

Our Perspective

PENSION CRISIS - AUGUST 2016

Ronald Schwartz, CFA

Managing Director,

Senior Portfolio Manager,

Tax-Exempt

Ron is a Senior Portfolio

Manager focused on the TaxExempt Strategies. He has

worked in the investment

management industry since

1982. Ron received a B.A. in

Business Administration from

Adelphi University and is a CFA

Charterholder and a member of

the CFA Society of Orlando.

U.S.

public pension investment returns for fiscal year 2016, which ended on June 30th, are currently being released, and the largest funds have posted returns well below target. Negative headlines surrounding state and cities’ underfunded pension plans now appear almost daily and it’s no coincidence that the states with the worst pension funding ratios now have the widest credit spreads (IL, CT, PA, NJ, and KY). Unfunded pension liabilities of state and local issuers have increased significantly over the past decade and have become a key credit driver for the municipal bond asset class.

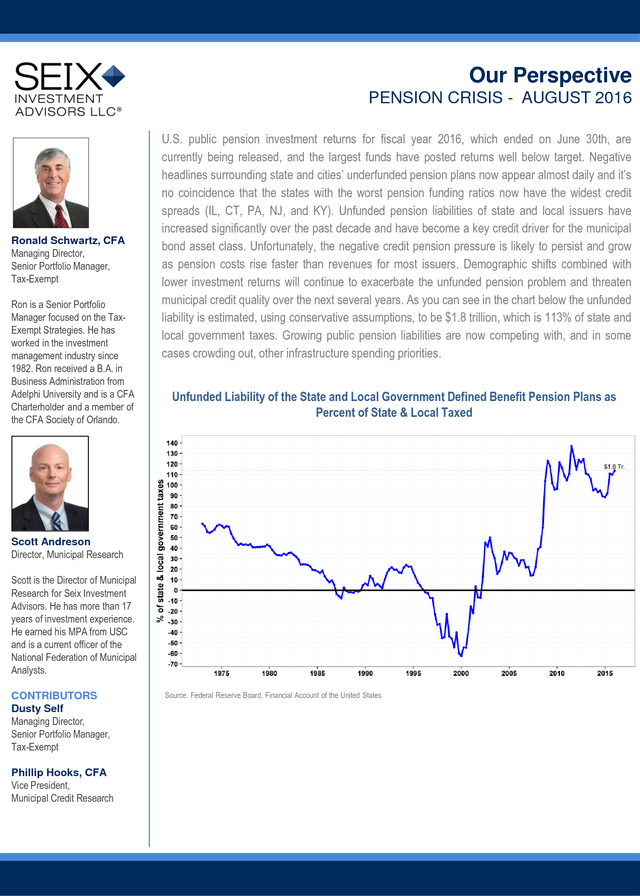

Unfortunately, the negative credit pension pressure is likely to persist and grow as pension costs rise faster than revenues for most issuers. Demographic shifts combined with lower investment returns will continue to exacerbate the unfunded pension problem and threaten municipal credit quality over the next several years. As you can see in the chart below the unfunded liability is estimated, using conservative assumptions, to be $1.8 trillion, which is 113% of state and local government taxes.

Growing public pension liabilities are now competing with, and in some cases crowding out, other infrastructure spending priorities. Unfunded Liability of the State and Local Government Defined Benefit Pension Plans as Percent of State & Local Taxed Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 17 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research Source: Federal Reserve Board, Financial Account of the United States . Our Perspective PENSION CRISIS - AUGUST 2016 As recently as 2001, public pension funds on average were fully funded, but have dropped nearly 30% since then to 73.6% (see chart below). This is despite many states enacting pension reform over the past few years and increasing contributions. Pension asset growth has not kept pace with unfunded liabilities as a result of weak investment returns and the graying demographics of public workers. Even pension systems that are comparatively well-funded are at greater risk of market value loss as they pursue high risk-return investment strategies in the current low rate environment. Public Pension Plans’ Funded Ratios Have Dropped Nearly 30% Since 2001 Source: PublicPlansData.org Public pension systems have posted their worst investment results since the financial crisis, recording a median increase of 0.36% for 2015, falling far short of their 7%-8% targeted annual returns that they need to pay retirement benefits, according to the Wilshire Trust Universe Comparison Service.

As you can see in the chart below, the three largest pension systems (CalPERS, CalSTRS, NYCRF) just posted their 2016 investment results last month, which were their worst performance in seven years, and are far short of their assumed returns. Investment earnings are key as they account for half of all pension revenues and must meet the assumed rate, or pension contributions must increase for liabilities to not grow. With unfunded pension liabilities at historic highs, and investment returns well below targeted returns, public pension risks are clearly growing. California and New York Public Pension Investment Returns in Fiscal 2016 Actual public pension investment returns fell far short of assumed returns. Note: Fiscal year ends 30 June for CalPERS and CalSTRS and 31 March for NYCRF Source: Pension system websites .

Our Perspective PENSION CRISIS - AUGUST 2016 Negative headlines surrounding unfunded pension liabilities are only going to increase as a result of weak investment returns for fiscal year 2016 and implementation of GASB 67/68 accounting standards (see our January 2015 report). Credit differentiation surrounding pension funding in the municipal asset class continues to intensify and security selection has never been more important, particularly in the current narrow credit spread environment. Municipal issuers that have had the political fortitude and good management skills to enact pension reform will clearly benefit from an improving credit profile while those that have kicked the pension can down-the-road will continue to significantly underperform. We have been using conservative pension methodology in our credit analysis over the past few years and have positioned our portfolios with credits and sectors that do not have pension problems. The assertions in this perspective are Seix Investment Advisors’ opinion. BofA Merrill Lynch Municipal Master Index tracks the performance of the investment-grade U.S.

tax-exempt bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule, and an investment grade rating (based on average of Moody’s, S&P, and Fitch). Investment Risks: All investments involve risk. Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss.

Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa. A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax.

There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative. All information contained herein is believed to be correct, but accuracy cannot be guaranteed.

This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice. Seix Investment Advisors does not provide legal, estate planning or tax advice.

Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2016 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .

public pension investment returns for fiscal year 2016, which ended on June 30th, are currently being released, and the largest funds have posted returns well below target. Negative headlines surrounding state and cities’ underfunded pension plans now appear almost daily and it’s no coincidence that the states with the worst pension funding ratios now have the widest credit spreads (IL, CT, PA, NJ, and KY). Unfunded pension liabilities of state and local issuers have increased significantly over the past decade and have become a key credit driver for the municipal bond asset class.

Unfortunately, the negative credit pension pressure is likely to persist and grow as pension costs rise faster than revenues for most issuers. Demographic shifts combined with lower investment returns will continue to exacerbate the unfunded pension problem and threaten municipal credit quality over the next several years. As you can see in the chart below the unfunded liability is estimated, using conservative assumptions, to be $1.8 trillion, which is 113% of state and local government taxes.

Growing public pension liabilities are now competing with, and in some cases crowding out, other infrastructure spending priorities. Unfunded Liability of the State and Local Government Defined Benefit Pension Plans as Percent of State & Local Taxed Scott Andreson Director, Municipal Research Scott is the Director of Municipal Research for Seix Investment Advisors. He has more than 17 years of investment experience. He earned his MPA from USC and is a current officer of the National Federation of Municipal Analysts. CONTRIBUTORS Dusty Self Managing Director, Senior Portfolio Manager, Tax-Exempt Phillip Hooks, CFA Vice President, Municipal Credit Research Source: Federal Reserve Board, Financial Account of the United States . Our Perspective PENSION CRISIS - AUGUST 2016 As recently as 2001, public pension funds on average were fully funded, but have dropped nearly 30% since then to 73.6% (see chart below). This is despite many states enacting pension reform over the past few years and increasing contributions. Pension asset growth has not kept pace with unfunded liabilities as a result of weak investment returns and the graying demographics of public workers. Even pension systems that are comparatively well-funded are at greater risk of market value loss as they pursue high risk-return investment strategies in the current low rate environment. Public Pension Plans’ Funded Ratios Have Dropped Nearly 30% Since 2001 Source: PublicPlansData.org Public pension systems have posted their worst investment results since the financial crisis, recording a median increase of 0.36% for 2015, falling far short of their 7%-8% targeted annual returns that they need to pay retirement benefits, according to the Wilshire Trust Universe Comparison Service.

As you can see in the chart below, the three largest pension systems (CalPERS, CalSTRS, NYCRF) just posted their 2016 investment results last month, which were their worst performance in seven years, and are far short of their assumed returns. Investment earnings are key as they account for half of all pension revenues and must meet the assumed rate, or pension contributions must increase for liabilities to not grow. With unfunded pension liabilities at historic highs, and investment returns well below targeted returns, public pension risks are clearly growing. California and New York Public Pension Investment Returns in Fiscal 2016 Actual public pension investment returns fell far short of assumed returns. Note: Fiscal year ends 30 June for CalPERS and CalSTRS and 31 March for NYCRF Source: Pension system websites .

Our Perspective PENSION CRISIS - AUGUST 2016 Negative headlines surrounding unfunded pension liabilities are only going to increase as a result of weak investment returns for fiscal year 2016 and implementation of GASB 67/68 accounting standards (see our January 2015 report). Credit differentiation surrounding pension funding in the municipal asset class continues to intensify and security selection has never been more important, particularly in the current narrow credit spread environment. Municipal issuers that have had the political fortitude and good management skills to enact pension reform will clearly benefit from an improving credit profile while those that have kicked the pension can down-the-road will continue to significantly underperform. We have been using conservative pension methodology in our credit analysis over the past few years and have positioned our portfolios with credits and sectors that do not have pension problems. The assertions in this perspective are Seix Investment Advisors’ opinion. BofA Merrill Lynch Municipal Master Index tracks the performance of the investment-grade U.S.

tax-exempt bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule, and an investment grade rating (based on average of Moody’s, S&P, and Fitch). Investment Risks: All investments involve risk. Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss.

Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally, a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa. A portfolio’s income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax.

There is no guarantee a specific investment strategy will be successful. This information and general market-related projections are based on information available at the time, are subject to change without notice, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not intended to be authoritative. All information contained herein is believed to be correct, but accuracy cannot be guaranteed.

This information may coincide or conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice. Seix Investment Advisors does not provide legal, estate planning or tax advice.

Investors are advised to consult with their investment processional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results. ©2016 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital Management LLC network of investment firms. .