Description

Vol 3/Issue 1 – WINTER 2014

Global

outlook 2014

asset class:

volatility

china’s

bold move

screens

on esG

. Welcome

to the NeW edItIoN

of stoXX Pulse

meet stoXX

at a conFerence

»

» Mar. 26, shanghai, China

Ruben Feldman, manager, Market

Development, STOXX, speaks on

“Managing Risk through Indexation”

on Mar. 26.

Alain Picard, head of product

management, Business & Market

Development, SIX AG, speaks about

SMI indices, the specialties of the

Swiss ETF market and the advantage

of listing ETFs in Switzerland.

Mar. 25-26, London, UK

UK EDHEC RIsK Days,

EURopE RUbEN FELDMaN

CHINa INDExINg & ETF CoNFERENCE

.

As STOXX expands into China, we bring you an interview with Julian Tsung-Sheng Liu, president and chief executive officer of Yuanta Securities Investment Trust Co., an asset manager based in Taiwan. Liu offers his views on the Shanghai Free Trade Zone, which opened in September, 2013, and represents the boldest move yet by China to open up its currency and its economy to foreign investors. HaRTMUT gRaF Ceo, stoXX limited dear readers, I hope all of you had a good holiday season, and I wish you a successful 2014. Speaking of success, I would like to talk about the STOXX Pulse newsletter. We published our first issue in the fall of 2012, with about a thousand subscribers. Our aim was to offer news and views on indexing and investing themes to clients. This issue, the sixth, goes out to more than 8,000 subscribers, highlighting the growth of this publication. In this issue, we bring you an outlook for 2014 from Andreas Utermann, the global chief investment officer at Allianz Global Investors. We are delighted that he has taken the time to offer his perspective to our readers. Volatility has been established as an asset class for more a decade, and investors are increasingly recognizing the importance of this asset class. For this issue, we talked to a few clients who use VSTOXX products to get their views on volatility in general and “volatility tools” that are available to investors. STOXX introduced the iSTOXX Global ESG Select 100 Index in December, 2013. The index offers investors exposure to sustainable companies with the lowest volatility and the highest dividends. We also talked to an equity derivatives structurer at J.P. Morgan to get his perspective on applying screens to a sustainability index and what that means for investors. I hope you enjoy this issue.

For comments and/or suggestions, please contact the editor Rajiv Sekhri at rajiv.sekhri@stoxx.com Regards, Hartmut Graf CEO, STOXX Limited . ‘ TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 ‘TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 4 aNDREas UTERMaNN Allianz Global Investors . sToxx Pulse – WINteR 2014 Even though we are seeing what is arguably one of the loosest monetary conditions in history, many countries and regions have yet to reach pre-crisis output levels. There is also low, and in many cases, falling inflation rates along with high unemployment. Many policy makers, such as the European Central bank (ECb), don’t see inflation as the biggest risk, but rather deflation, as seen in the ECb’s recent rate cut. STOXX Pulse asked Andreas Utermann, the Global CIO of Allianz Global Investors, to write a commentary for this issue on a global investment outlook for 2014. ALLIAnZ GLOBAL InvESTOrS CIO SAYS ‘STOCkS ArE ThE AnSWEr’ ThIS YEAr Father Time may have delivered a new year, but don’t expect central banks to cut any monetary umbilical cords anytime soon. We are still in a post-financial crisis environment.

Loose monetary policy by central banks, led by the Fed, will likely continue for much longer than most anticipate. In our view, loose monetary policy will remain the key driver of the global financial markets in 2014. As we were saying in 2013, to not take risk is the biggest risk an investor can take. For us, the continuation of financial repression dynamics that we have experienced over the last few years is a call for investors to gain more exposure to risk assets, equities in particular. We believe investors should use market weakness or corrections as buying opportunities. In our opinion, stocks offer investors the most attractive long-term returns in 2014.

In many respects, stocks are the answer for delivering needed capital returns. Equities, unlike government bonds, are less likely to be impacted by unsustainable levels of sovereign debt and will benefit more from a recovery of the global economy. For the first time since the onset of the global financial crisis, we see a moderate global cyclical recovery. The global economy is indeed recovering, but the economic recovery has come about largely because of quantitative easing (QE) by the Fed and other central banks. Before central banks begin to tighten earnestly, they will first need to see several quarters of at- or above-trend growth and lower levels of unemployment coupled with rising inflation expectations and evidence that global debt levels are shrinking in real terms.

We are optimistic about global growth in 2014 though we don’t see the conditions for a change in global central bank policy to happen until at least 2015. Let us now take a look at regional markets. us The major question is, should investors fear rising interest rates in the US this year? Our answer is that we do not see a rise in interest rates in the short term. For one, we believe the Fed — and this applies to central banks globally — will willingly stay behind the curve in terms of the timing and the magnitude of 5 . ‘ TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 brics (brazil, russia, india and china) and emerGinG markets europe Crossing the Atlantic over to Europe, we finally find growth after years of crisis. Europe had staggered from one debt crisis to the next but saw relative stability in 2013. We believe this trend will continue and will help to support European markets in 2014. interest rate hikes. Inflation expectations remain subdued in the US and very well could remain so throughout 2014. Two, the Fed would rather err on the side of inflation than risk deflating asset prices by applying the monetary brakes too soon. Investors should be aware that the Fed will likely be very cautious in applying tighter monetary policy. We expect the Fed to carefully gauge market sentiment before implementing any policies and those policies should surprise asset markets to the upside. Risk assets will once again drive returns in the US in 2014 as the low-interest rate environment continues. 6 Ireland has just returned to the capital markets, exiting the existing external support mechanisms, and Portugal is also planning to return to the capital markets this year.

Both countries continue to implement fiscal and structural reforms, and Greece and Spain as well, but it will be a long, difficult road to recovery. It is here we find the biggest risk in the Eurozone. because structural reforms are often painful and unpopular, there is the threat of a political backlash that could have significant consequences for the Eurozone. That said, Greece, the weakest country economically, is now seen returning to 0.6% growth this year and growing 2.9% in 2015, according to the winter 2013 forecast by the European Commission.

Even though larger economies, such as France and Italy, are struggling to implement reforms to shrink their debt burdens, we believe the Eurozone is on the path to recovery and there are positive impulses in the overall Eurozone economy backing our optimism. After a prolonged period of weaker economic growth in the BRICs and emerging markets, there are signs that a turnaround is underway, with China and Poland especially well positioned to benefit from the recovery we’re seeing in developed markets. China is transitioning under its new leadership in a positive direction, moving from “Made in China” to “Made for China.” We believe carefully selected emerging market stocks offer investors the prospect of attractive returns. Though some of these stocks are no longer cheap, an investor may want to consider buying shares of companies in developed markets that are well-positioned to benefit from growth in emerging markets. Another area to consider is exposure to emerging market currencies and debt. Here you will find opportunities to invest in countries with positive demographic trends and without the debt burden of many countries with developed markets. Japan The recovery in Japan is simply unsustainable.

The Japanese central bank’s expansive monetary policy, termed “Abenomics,” has only limited prospects for long-term success. Japan’s central bank is trying to fight deflation and sluggish growth by weakening the yen. This has helped in the short term to raise equity markets, but what needs to be addressed in Japan goes much deeper and involves breaking down cemented structures before we would feel comfortable in saying that the country is on its way to sustainable long-term growth. Investors may see their shares of Japanese companies rise as the yen weakens, but they better keep on their toes, because as soon as the expansionary policy is reduced, we see the yen rising again and Japanese government bond yields once again sinking. We feel current share prices in Japan are optimistically high.« .

STOXX pulsE – WINTER 2014 7 . vOLATILITY AS An ASSET CLASS AS An ASSET CLASS 8 . sToxx Pulse – WINteR 2014 of mid-term futures when the volatility forward curve is in contango. VSTOXX AnD DYnAMIC vSTOXX Volatility has become an important tool for investors to diversify traditional equity portfolios and for taking outright views on the direction of equity markets. STOXX offers several indices to help investors benefit from volatility as an asset class. The EUrO STOXX 50 volatility Index (vSTOXX), for example, measures the implied variance across all options of a given time to expiry. The vSTOXX family includes many indices, including the VSTOXX Short-Term Futures Index, which measures return from a rolling long position in first and second month EUrEX vSTOXX futures contracts. The EUrO STOXX 50 Volatility Mid-Term Futures Index replicates a constant five-month forward, one-month implied volatility. STOXX Pulse talked to three experts to get their views on volatility as an asset class and volatility products available in the market. Abhinandan Deb is head of European equity derivatives research at bank of America Merrill Lynch Global Research. Prior to joining BofA Merrill Lynch in 2010, he was a senior equity derivatives research analyst at Barclays Capital. he holds a master’s degree in Advanced Computing from Imperial College London and bachelors’ degrees in computing and in physics from Oxford University and St Stephen’s College, University of Delhi. The Dynamic VSTOXX Index is a combination of two indices, the VSTOXX Short-Term Futures and Mid-Term Futures Indices.

The rationale behind dynamic allocation is to exploit in a timely manner the superior performance of short-term futures when the volatility forward curve is in backwardation and John-Mark Piampiano is a portfolio manager at Pine River Capital Management since 2010. Before joining Pine River, Piampiano was a principal at Engineered Portfolio Partners. From 2002 to 2009, he worked as senior portfolio manager hbk Investments in Dallas, where he was responsible for the global volatility business including portfolio trading, risk management and staffing. he has also worked as an equities derivative trader at KBC Financial Products in new York and as a trader at hess Energy Trading Co.

Piampiano received a bachelor of science degree in economics and biology from the Massachusetts Institute of Technology in 1999. JoHN-MaRK pIaMpIaNo Pine River Capital Management abHINaNDaN DEb Bank of America Merrill lynch 9 . AS An ASSET CLASS our investors eXpect us to search the Globe For ineXpensive hedGes and relative value trades in the volatility space. John-mark piampiano VSTOXX AnD DYnAMIC vSTOXX Volatility has become an important tool for investors to diversify traditional equity portfolios and for taking outright views on the direction of equity markets. STOXX offers several indices to help investors benefit from volatility as an asset class. The EUrO STOXX 50 volatility Index (vSTOXX), for example, measures the implied variance across all options of a given time to expiry. The vSTOXX family includes many indices, including the VSTOXX Short-Term Futures Index, which measures return from a rolling long position in first and second month EUrEX vSTOXX futures contracts. The EUrO STOXX 50 Volatility Mid-Term Futures Index replicates a constant five-month forward, one-month implied volatility. The Dynamic VSTOXX Index is a combination of two indices, the VSTOXX Short-Term Futures and Mid-Term Futures Indices.

The rationale behind dynamic allocation is to exploit in a timely manner the superior performance of short-term futures when the volatility forward curve is in backwardation and of mid-term futures when the volatility forward curve is in contango. STOXX Pulse talked to three experts to get their views on volatility as an asset class and volatility products available in the market. Abhinandan Deb is head of European equity derivatives research at bank of America Merrill Lynch Global Research. Prior to joining BofA Merrill Lynch in 2010, he was a senior equity derivatives research analyst at Barclays Capital. he holds a master’s degree in Advanced Computing from Imperial College London and bachelors’ degrees in computing and in physics from Oxford University and St Stephen’s College, University of Delhi. John-Mark Piampiano is a portfolio manager at Pine River Capital Management since 2010. Before joining Pine River, Piampiano was a principal at Engineered Portfolio Partners. From 2002 to 2009, he worked as senior portfolio manager hbk Investments in Dallas, where he was responsible for the global volatility business including portfolio trading, risk management and staffing. he has also worked as an equities derivative trader at KBC Financial Products in new York and as a trader at hess Energy Trading Co.

Piampiano received a bachelor of science degree in economics and biology from the Massachusetts Institute of Technology in 1999. What sort oF interest are you seeinG amonG your customers in products that help FiGht volatility? deb: The volatility regime is changing. While fewer investors are as keyed up on fighting tail risk as they were during the height of the European sovereign crisis, we’re seeing rapidly growing interest and trading activity in volatility products from a wide variety of clients in diverse geographies. Selling volatility has been a winner in 2013 and this hasn’t been lost on most investors. Consequently, volatility put strategies have been in strong demand.

Relative value volatility has also picked up and our hedge fund clients were active in forward variance spreads; with volatilities generally low to sell outright and costly to buy and hold outright, relative value becomes a natural play. piampiano: Our investors expect us to search the globe for inexpensive hedges and relative value trades in the volatility space. Index products provide a “benchmark” in each geographic region since they represent the most liquid suite of products and provide a basis for comparison for the price of other option products in that region. 10 . STOXX pulsE – WINTER 2014 Cyprus, Turkey and Israel. He is also responsible for the sales activities of Eurex vSTOXX Derivatives. before joining Eurex, Markus worked as a senior equity derivatives and fixed income derivatives trader at Citibank in Germany and Switzerland for almost a decade. MaRKUs-aLExaNDER FLEsCH eurex Zurich AG complex is the reduced liquidity relative to options on EUrO STOXX 50 or other major European equity indices. in your opinion, What kind oF product or products are the best tools to fight volatility in the market? Which vstoXX indeX or indices do you use and What are the pros and cons of this product? deb: I tend to follow the VSTOXX futures curve. While it is still far less liquid than the VIX, there are a few reasons why investor interest in trading VSTOXX has grown: » Relative value opportunities arise due to the difference in steepness of the two futures curves; the VSTOXX curve is less impacted by ETP flows than VIX is. » European risk is better hedged with VSTOXX than VIX. » Diversification: like any asset, there is scope for regional diversification and investors will look more seriously at vSTOXX once volumes/liquidity grow sufficiently for trading costs to reduce. piampiano: We trade VSTOXX futures and options in both a hedging and relative value context.

VSTOXX derivatives give us exposure to market implied volatility without any direct exposure to the underlying cash index (EUrO STOXX 50), in contrast to EUrO STOXX 50 put or call options, which lose their convexity profile if we move away from our strike price. This makes the VSTOXX derivatives unique among listed European volatility products in that they provide us with this “strikeless” exposure. Our primary concern with the vSTOXX deb: Generally, volatility products are well suited to hedge risk-off events, given outsized moves in volatility versus large moves in risk assets. The key always is how to manage long volatility exposure, and we have worked to deliver our clients volatility option based hedges that also have superior carry profiles, indeed with the potential to carry positively.

Few if any other asset classes can offer such payoffs. piampiano: There is no product which provides the best hedge 100% of the time. Each product has advantages and disadvantages both with respect to the nature of the convexity profile and with the price relative to other hedges. Our investors expect us to make a careful analysis of the relative merits of all the potential hedges in the market to ensure the hedge we offer represents the cheapest possible convexity profile at any given time to protect each of our portfolios. can you tell us Why the vstoXX and dynamic vstoXX indices are popular amonG investors? Flesch: VSTOXX is becoming increasingly popular amongst institutional investors, even though 2013 was a year in which overall volatility levels were suppressed. A growing number of clients have discovered volatility as an asset class and value "pure" volatility trading in comparison to trading a "proxy" of volatility with straddles on the underlying index market, which is subject to transaction costs from dynamic delta management. With the VSTOXX itself and a wide range of dynamic vSTOXX Indices, Europe is catching up with US market development.

In the US, volatility products have been more mainstream for many years and are also actively used by retail investors. With our listed European volatility derivatives, clients can gain exposure more efficiently than in the past, when Markus-Alexander Flesch has been an executive director at Eurex Zurich AG since 2003 and is responsible for the derivative business for sell-side and buy-side clients in Switzerland, Italy, 11 . ChInA’S “FInAnCIAL STYLE bIG ChINA’s “fINANCIAl style BIG BANG” 12 . sToxx Pulse – WINteR 2014 What does the chinese Government need to do, especially With reGard to foreign exchange and customs reGulations, to ensure that this liberalization proGram enables interested investors and the country to beneFit? I see this move as China’s commitment to economic and financial change. This is a kind of Chinese style financial big bang, similar to what happened in 1986 in the UK and in 1993 in Japan. JULIaN TsUNg-sHENg LIU yuanta securities Investment trust Co ThE ShAnGhAI FrEE TrADE ZOnE China launched the Shanghai Free Trade Zone on Sep. 29, 2013, a move hailed by many analysts and media as the boldest step yet by the country to liberalize rules that govern finance, currency, investment, trade and interest rates. The plan of the SFTZ is to open up to foreign competition in the zone and use it as a testing laboratory for reforms, including a convertible yuan and liberalized interest rates. More than 1,400 companies had registered in the SFTZ within two months of its launch, the Financial Times reported in november. Reuters reported in December that Charles Schwab had traveled to Shanghai to discuss opening an office in the free trade zone. "The next step is to open an office in the new free trade zone in Shanghai," Schwab was quoted as saying by reuters.

"The rules and regulations are not completely clear." Some analysts say that the SFTZ does not sound appealing to foreign investors because the political will behind the project seems lacking. In addition, more clarity regarding customs and foreign exchange regulations in the free zone need to be clarified. STOXX Pulse spoke with Julian TsungSheng Liu, president and chief executive of Yuanta Securities Investment Trust Co., an asset manager headquartered in Taipei, to get his views on what this move means for China. Liu visited the SFTZ in 2013.

Yuanta Securities is a subsidiary of Yuanta Financial holding, and also has representative offices in Shenzhen and Shanghai. Yuanta SITC has 10 billion US dollars of assets under management. In terms of the forex control, we will see a lot of relaxation of currency control from the Central Bank of China. The first move would be trying to cap the weight for renminbi internationalization.

We see that a lot of offshore centers started by Hong Kong and Taiwan and Singapore and London are coming into play. We see that renminbi is heavily controled by China as it tries to stabilize its currency movement, its international trade and its economic performance. But I think now China believes the timing is good to remove all trading bans for the currency. In this new zone, China plans a mechanism for two-way movement – in and out – for renminbi internationalization and liberalization. At the same time, we are seeing a lot of new measures toward interest rates, lending rates and deposit rates.

Wealthmanagement wise, we see that banks like Citibank from the US and DbS from Singapore want to have a presence and exposure in the SFTZ. Meanwhile, in terms of customs control, I think there will be special treatment for the SFTZ. For example, automakers will enjoy many tax reductions. 13 . ChInA’S “FInAnCIAL STYLE bIG For right now in Shenzhen, the Chinese government allows a 49% ownership for a joint venture in the mutual fund and securities industry. There are more than 80 mutual fund companies currently domiciled in China. In the future, the intention of the government is to allow more than 50% foreign ownership, but, do remember, the government also does not want to jeopardize local industry. As of right now, it is not clear whether you can own 100% of your company in the SFTZ. But things will become clearer over time. do you think the sFtz poses a threat to hong kong? I was at the SFTZ in mid-november, and it is a very small area, just 11 kilometers.

I think it is very symbolic. I think the banking, manufacturing and logistics industries will benefit from such openness. hoW lonG do you think it Will take beFore the sFtz becomes Fully Functional and solves its teethinG problems? That is easier said than done. This is just the launch. There will be trial and error as China tests the waters.

I think stage one will take one or two years. Our anticipation for now is that it will take three to four years to establish all the necessary infrastructure and also take another two or three years after that to finalize. So in terms of the time horizon, I think the SFTZ will become the engine for mainland China by 2020 in terms of liberalization and deregulation. That said, I think in five years from now, we will begin to see a lot of the measures taking effect. 14 I think there will be more synergy than competition between Hong Kong and Shanghai.

Or, more likely, co-competition, which is a mix of cooperation and competition. There are no major political barriers between Hong Kong and mainland China, compared to the barriers that exist between mainland China and Taiwan. I think Hong Kong and Shanghai can play different roles, because I think the target of the mainland China government is to set up Shanghai to become the international financial center, while Hong Kong is the financial center of Asia. Also, in terms of the structure of the economy, Hong Kong is a city economy, while mainland China is a continental economy.

Hong Kong was also occupied by a service industry, while mainland China has a lot of trading, import and export industry. However, Hong Kong does have a more mature economy, a better platform for accounting, laws, etc., so I think Hong Kong can be leveraged by Shanghai. does yuanta have any plans to move into this Free trade zone? We have a mutual fund joint venture with China resources Group in Shenzhen. Shenzhen is a special economic zone too. In the SFTZ we will get another tax break of 10% but we are well established in Shenzhen and right now we have no plans to open an office in Shanghai. Just a last question about hoW Well versed you think asian investors are With diFFerent products in the etp space? Asian investors have a good knowledge base about ETPs, ETFs and also different strategies, such as low volatility. For example, Taiwanese pension funds are keen to invest in global low volatility products. In East Asia such as Japan and korea, I think investors are fast movers and have greater acceptance for innovative and new financial products, while I think that in Hong Kong and Singapore investors have a good variety of ETD products available. And many big steps in the investment sector are being taken by governments in Asia. Singapore, Malaysia and Thailand just entered an agreement to sign the Collective Investment Scheme (CIS), which is a three-country mutual fund passport.

It is very, very similar to UCITs in Europe. So funds that are domiciled in Singapore can be easily redistributed to Thailand or Malaysia. This is bound to change the mutual fund landscape of Southeast Asia.

In the same way, the Greater China market also needs to be consolidated. Meanwhile, mainland China has encouraged financial innovation in recent years. In 2013, China had a fixed income ETF, it had a gold ETF and cross-border ETF. So China remains a big market with endless possibilities.« .

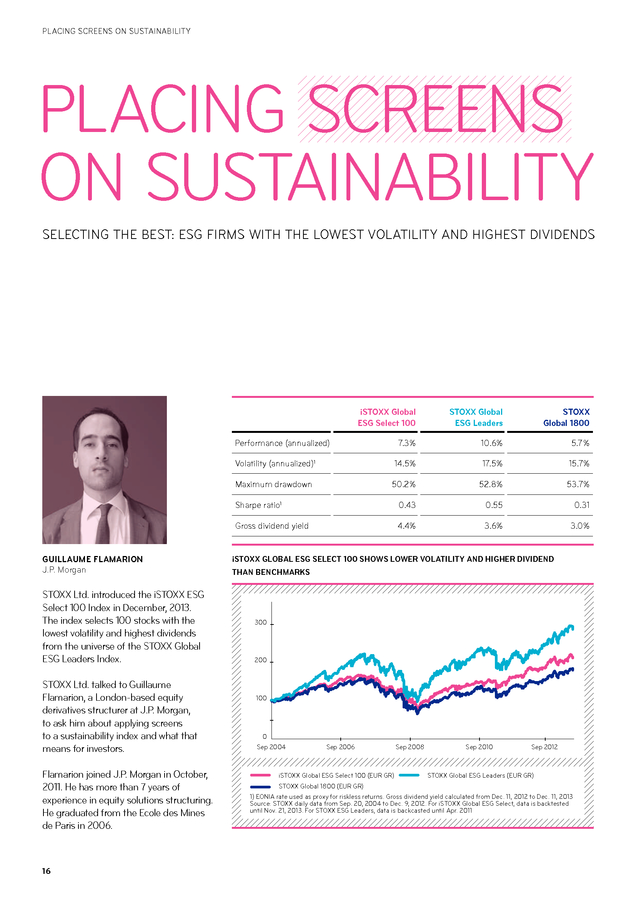

sToxx pulsE WINTER STOXX Pulse – WINteR 2014 15 . PLACInG SCrEEnS On SUSTAInAbILITY PLACInG SCrEEnS On SUSTAInAbILITY SELECTInG ThE bEST: ESG FIrMS WITh ThE LOWEST vOLATILITY AnD hIGhEST DIvIDEnDS isToxx global Esg select 100 sToxx global Esg Leaders sToxx global 1800 7.3% 10.6% 5.7% volatility (annualized)1 14.5% 17.5% 15.7% Maximum drawdown 50.2% 52.8% 53.7% Sharpe ratio1 0.43 0.55 0.31 Gross dividend yield 4.4% 3.6% 3.0% Performance (annualized) gUILLaUME FLaMaRIoN J.P. Morgan STOXX Ltd. introduced the iSTOXX ESG Select 100 Index in December, 2013. The index selects 100 stocks with the lowest volatility and highest dividends from the universe of the STOXX Global ESG Leaders Index. STOXX Ltd. talked to Guillaume Flamarion, a London-based equity derivatives structurer at J.P.

Morgan, to ask him about applying screens to a sustainability index and what that means for investors. Flamarion joined J.P. Morgan in October, 2011. He has more than 7 years of experience in equity solutions structuring. he graduated from the Ecole des Mines de Paris in 2006. 16 isToxx gLobaL Esg sELECT 100 sHoWs LoWER voLaTILITy aND HIgHER DIvIDEND THaN bENCHMaRKs 300 200 100 0 Sep 2004 Sep 2006 iSTOXX Global ESG Select 100 (EUr Gr) Sep 2008 Sep 2010 Sep 2012 STOXX Global ESG Leaders (EUr Gr) STOXX Global 1800 (EUr Gr) 1) EOnIA rate used as proxy for riskless returns.

Gross dividend yield calculated from Dec. 11, 2012 to Dec. 11, 2013 Source: STOXX daily data from Sep.

20, 2004 to Dec. 9, 2012. For iSTOXX Global ESG Select, data is backtested until nov.

21, 2013. For STOXX ESG Leaders, data is backcasted until Apr. 2011 .

STOXX pulsE – WINTER 2014 don’t esG and sustainable indices already have companies that pay relatively hiGh dividends and Whose shares display relatively loWer volatility? or is that Just an assumption, and hence the need to apply these screens to an esG indeX? What is the beneFit oF applyinG screens For loW volatility and hiGh dividends on a sustainability indeX? I would like to emphasize that first of all, an ESG index tracks the returns of a basket of sustainable stocks. Companies that implement strict controls on Environmental, Social and Governance (ESG) standards are usually better positioned to deliver consistent performance in the long term. This ESG filter is mainly a qualitative factor which can be combined with more quantitative gauges, like low volatility and high dividends. Investing in low volatility stocks has been very popular among investors recently. Usually, high volatility stocks are relatively overpriced as mutual fund managers, who might have limitations on the use of leverage, are tilting towards high volatility stocks to generate performance. Moreover, stocks with low historical volatility, exhibit historically superior risk-adjusted returns (Sharpe ratio). Companies that pay high dividends are generally seen as stable, generating consistent earnings and returns in the long term. A high dividend yield can indicate undervaluation of the stock , because the stock s dividend is high relative to its price. Moreover, in a low interest rate environment, high dividend stocks can provide consistent income to investors. Stocks from the ESG universe are generally stable companies which could be seen as already displaying lower volatility and paying relatively high dividends. The ESG filters are mainly non-financial qualitative criteria which can be balanced efficiently with two financial quantitative gauges – low volatility and high dividends. Theoretically, orthogonal (independent) factors would form a complete and diversified set of investments.

In practice, it is difficult to associate completely independent factors. The three levels of selection within the index achieve their objective of complementing each other efficiently: qualitative and quantitative, quality and stability, potential growth and regular income. however, investors must not forget that while this selection process exhibits efficiencies in theory, there is no guarantee that the iSTOXX Global ESG Select 100 Index will necessarily outperform its benchmark. this esg filter is mainly a qualitative Factor Which can be combined with more quantitative GauGes, like loW volatility and hiGh dividends. Guillaume Flamarion launches have gathered considerable assets, and today most index providers have flagship low volatility and select dividend indices.

However the combination of both is still rare. As explained, low volatility and select dividends are two complementary factors within an index like the iSTOXX Global ESG Select 100 Index. This concept could be extended to STOXX indices other than ESG, for example on benchmark indices (EUrO STOXX 50, STOXX Europe 50, STOXX Europe 600), thematic indices (STOXX Strong Quality index family), or sector indices. It is important to remember that there is no guarantee that quantitative factors will always enhance performance.« In a nutshell, the iSTOXX Global ESG Select 100 Index intends to combine these three complementary factors: quality (ESG filter), low risk (low historical volatility) and value (high dividend). can the perFormance oF broad or other types oF indices be enhanced by applying screens to these indices? hoW? The demand for low volatility and high dividend strategies has grown significantly over the past few years due to strong risk-adjusted performance and increased investors’ appetite for smarter equity exposure.

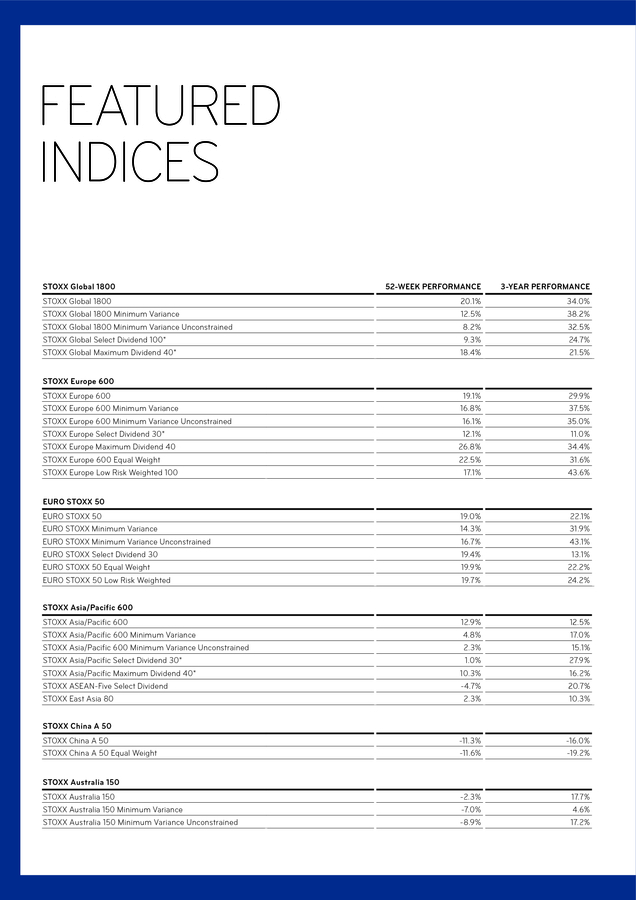

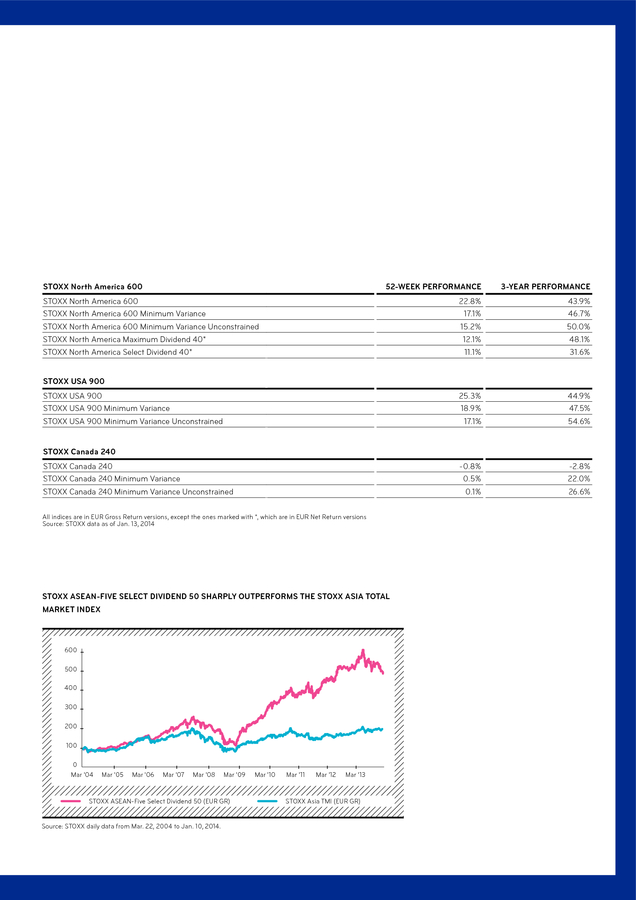

In fact, recent ETF 17 . FEATUrED InDICES feAtuRed INdICes sToxx global 1800 52-WEEK pERFoRMaNCE 3-yEaR pERFoRMaNCE STOXX Global 1800 STOXX Global 1800 Minimum Variance STOXX Global 1800 Minimum Variance Unconstrained STOXX Global Select Dividend 100* 20.1% 12.5% 8.2% 9.3% 34.0% 38.2% 32.5% 24.7% STOXX Global Maximum Dividend 40* 18.4% 21.5% STOXX Europe 600 STOXX Europe 600 Minimum variance STOXX Europe 600 Minimum variance Unconstrained STOXX Europe Select Dividend 30* STOXX Europe Maximum Dividend 40 19.1% 16.8% 16.1% 12.1% 26.8% 29.9% 37.5% 35.0% 11.0% 34.4% STOXX Europe 600 Equal Weight STOXX Europe Low risk Weighted 100 22.5% 17.1% 31.6% 43.6% 19.0% 14.3% 16.7% 19.4% 19.9% 19.7% 22.1% 31.9% 43.1% 13.1% 22.2% 24.2% 12.9% 4.8% 2.3% 1.0% 10.3% -4.7% 2.3% 12.5% 17.0% 15.1% 27.9% 16.2% 20.7% 10.3% -11.3% -11.6% -16.0% -19.2% -2.3% -7.0% -8.9% 17.7% 4.6% 17.2% sToxx Europe 600 EURo sToxx 50 EUrO STOXX 50 EUrO STOXX Minimum variance EUrO STOXX Minimum variance Unconstrained EUrO STOXX Select Dividend 30 EUrO STOXX 50 Equal Weight EUrO STOXX 50 Low risk Weighted sToxx asia/pacific 600 STOXX Asia/Pacific 600 STOXX Asia/Pacific 600 Minimum Variance STOXX Asia/Pacific 600 Minimum Variance Unconstrained STOXX Asia/Pacific Select Dividend 30* STOXX Asia/Pacific Maximum Dividend 40* STOXX ASEAn-Five Select Dividend STOXX East Asia 80 sToxx China a 50 STOXX China A 50 STOXX China A 50 Equal Weight sToxx australia 150 STOXX Australia 150 STOXX Australia 150 Minimum Variance STOXX Australia 150 Minimum Variance Unconstrained 18 . STOXX pulsE – WINTER 2014 sToxx North america 600 52-WEEK pERFoRMaNCE 3-yEaR pERFoRMaNCE 22.8% 17.1% 15.2% 12.1% 11.1% 43.9% 46.7% 50.0% 48.1% 31.6% 25.3% 18.9% 17.1% 44.9% 47.5% 54.6% -0.8% 0.5% 0.1% -2.8% 22.0% 26.6% STOXX north America 600 STOXX north America 600 Minimum Variance STOXX north America 600 Minimum Variance Unconstrained STOXX north America Maximum Dividend 40* STOXX north America Select Dividend 40* sToxx Usa 900 STOXX USA 900 STOXX USA 900 Minimum Variance STOXX USA 900 Minimum Variance Unconstrained sToxx Canada 240 STOXX Canada 240 STOXX Canada 240 Minimum Variance STOXX Canada 240 Minimum Variance Unconstrained All indices are in EUr Gross return versions, except the ones marked with *, which are in EUr net return versions Source: STOXX data as of Jan. 13, 2014 sToxx asEaN-FIvE sELECT DIvIDEND 50 sHaRpLy oUTpERFoRMs THE sToxx asIa ToTaL MaRKET INDEx 600 500 400 300 200 100 0 Mar '04 Mar '05 Mar '06 Mar '07 Mar '08 Mar '09 STOXX ASEAn-Five Select Dividend 50 (EUr Gr) Mar '10 Mar '11 Mar '12 Mar '13 STOXX Asia TMI (EUr Gr) Source: STOXX daily data from Mar. 22, 2004 to Jan. 10, 2014. 19 .

CoNTaCTs Vol 3/Issue 1 – WINTER 2014 Printed in January 2014 Selnaustrasse 30 CH-8021 Zurich P +41 (0)58 399 5300 stoxx@stoxx.com www.stoxx.com Frankfurt: +49 (0)69 211 13243 Hong Kong: +852 6307 9316 London: +44 (0)20 7862 7680 Madrid: +34 (0)91 369 1229 new York: +1 212 669 6426 Singapore: +65 9189 7970 Stockholm: +46 (0)8 4600 6090 sToxx is part of Deutsche börse and sIx This newsletter contains opinions and statements from various information providers. STOXX Limited does not represent or endorse any of these views or opinions and does not vouch for their accuracy or reliability. The views expressed by the information providers in this newsletter are their own views and do not reflect the views and opinions of STOXX Limited. STOXX® indices are protected through various intellectual property rights. ‘STOXX’, ‘EUrO STOXX 50’ and ‘iSTOXX’ are registered trademarks.

The use of the STOXX® indices for financial products or for other purposes requires a license from STOXX. STOXX does not make any warranties or representations, expressed or implied with respect to the timeliness, sequence, accuracy, completeness, currentness, merchantability, quality or fitness for any particular purpose of its index data. STOXX is not providing investment advice through the publication of the STOXX® indices or in connection therewith.

In particular, the inclusion of a company in an index, its weighting, or the exclusion of a company from an index, does not in any way reflect an opinion of STOXX on the merits of that company. Financial instruments based on the STOXX® indices are in no way sponsored, endorsed, sold or promoted by STOXX. © STOXX Limited. All rights reserved. .

As STOXX expands into China, we bring you an interview with Julian Tsung-Sheng Liu, president and chief executive officer of Yuanta Securities Investment Trust Co., an asset manager based in Taiwan. Liu offers his views on the Shanghai Free Trade Zone, which opened in September, 2013, and represents the boldest move yet by China to open up its currency and its economy to foreign investors. HaRTMUT gRaF Ceo, stoXX limited dear readers, I hope all of you had a good holiday season, and I wish you a successful 2014. Speaking of success, I would like to talk about the STOXX Pulse newsletter. We published our first issue in the fall of 2012, with about a thousand subscribers. Our aim was to offer news and views on indexing and investing themes to clients. This issue, the sixth, goes out to more than 8,000 subscribers, highlighting the growth of this publication. In this issue, we bring you an outlook for 2014 from Andreas Utermann, the global chief investment officer at Allianz Global Investors. We are delighted that he has taken the time to offer his perspective to our readers. Volatility has been established as an asset class for more a decade, and investors are increasingly recognizing the importance of this asset class. For this issue, we talked to a few clients who use VSTOXX products to get their views on volatility in general and “volatility tools” that are available to investors. STOXX introduced the iSTOXX Global ESG Select 100 Index in December, 2013. The index offers investors exposure to sustainable companies with the lowest volatility and the highest dividends. We also talked to an equity derivatives structurer at J.P. Morgan to get his perspective on applying screens to a sustainability index and what that means for investors. I hope you enjoy this issue.

For comments and/or suggestions, please contact the editor Rajiv Sekhri at rajiv.sekhri@stoxx.com Regards, Hartmut Graf CEO, STOXX Limited . ‘ TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 ‘TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 4 aNDREas UTERMaNN Allianz Global Investors . sToxx Pulse – WINteR 2014 Even though we are seeing what is arguably one of the loosest monetary conditions in history, many countries and regions have yet to reach pre-crisis output levels. There is also low, and in many cases, falling inflation rates along with high unemployment. Many policy makers, such as the European Central bank (ECb), don’t see inflation as the biggest risk, but rather deflation, as seen in the ECb’s recent rate cut. STOXX Pulse asked Andreas Utermann, the Global CIO of Allianz Global Investors, to write a commentary for this issue on a global investment outlook for 2014. ALLIAnZ GLOBAL InvESTOrS CIO SAYS ‘STOCkS ArE ThE AnSWEr’ ThIS YEAr Father Time may have delivered a new year, but don’t expect central banks to cut any monetary umbilical cords anytime soon. We are still in a post-financial crisis environment.

Loose monetary policy by central banks, led by the Fed, will likely continue for much longer than most anticipate. In our view, loose monetary policy will remain the key driver of the global financial markets in 2014. As we were saying in 2013, to not take risk is the biggest risk an investor can take. For us, the continuation of financial repression dynamics that we have experienced over the last few years is a call for investors to gain more exposure to risk assets, equities in particular. We believe investors should use market weakness or corrections as buying opportunities. In our opinion, stocks offer investors the most attractive long-term returns in 2014.

In many respects, stocks are the answer for delivering needed capital returns. Equities, unlike government bonds, are less likely to be impacted by unsustainable levels of sovereign debt and will benefit more from a recovery of the global economy. For the first time since the onset of the global financial crisis, we see a moderate global cyclical recovery. The global economy is indeed recovering, but the economic recovery has come about largely because of quantitative easing (QE) by the Fed and other central banks. Before central banks begin to tighten earnestly, they will first need to see several quarters of at- or above-trend growth and lower levels of unemployment coupled with rising inflation expectations and evidence that global debt levels are shrinking in real terms.

We are optimistic about global growth in 2014 though we don’t see the conditions for a change in global central bank policy to happen until at least 2015. Let us now take a look at regional markets. us The major question is, should investors fear rising interest rates in the US this year? Our answer is that we do not see a rise in interest rates in the short term. For one, we believe the Fed — and this applies to central banks globally — will willingly stay behind the curve in terms of the timing and the magnitude of 5 . ‘ TO nOT TAkE rISk IS ThE bIGGEST rISk An InvESTOr CAn TAkE’ In 2014 brics (brazil, russia, india and china) and emerGinG markets europe Crossing the Atlantic over to Europe, we finally find growth after years of crisis. Europe had staggered from one debt crisis to the next but saw relative stability in 2013. We believe this trend will continue and will help to support European markets in 2014. interest rate hikes. Inflation expectations remain subdued in the US and very well could remain so throughout 2014. Two, the Fed would rather err on the side of inflation than risk deflating asset prices by applying the monetary brakes too soon. Investors should be aware that the Fed will likely be very cautious in applying tighter monetary policy. We expect the Fed to carefully gauge market sentiment before implementing any policies and those policies should surprise asset markets to the upside. Risk assets will once again drive returns in the US in 2014 as the low-interest rate environment continues. 6 Ireland has just returned to the capital markets, exiting the existing external support mechanisms, and Portugal is also planning to return to the capital markets this year.

Both countries continue to implement fiscal and structural reforms, and Greece and Spain as well, but it will be a long, difficult road to recovery. It is here we find the biggest risk in the Eurozone. because structural reforms are often painful and unpopular, there is the threat of a political backlash that could have significant consequences for the Eurozone. That said, Greece, the weakest country economically, is now seen returning to 0.6% growth this year and growing 2.9% in 2015, according to the winter 2013 forecast by the European Commission.

Even though larger economies, such as France and Italy, are struggling to implement reforms to shrink their debt burdens, we believe the Eurozone is on the path to recovery and there are positive impulses in the overall Eurozone economy backing our optimism. After a prolonged period of weaker economic growth in the BRICs and emerging markets, there are signs that a turnaround is underway, with China and Poland especially well positioned to benefit from the recovery we’re seeing in developed markets. China is transitioning under its new leadership in a positive direction, moving from “Made in China” to “Made for China.” We believe carefully selected emerging market stocks offer investors the prospect of attractive returns. Though some of these stocks are no longer cheap, an investor may want to consider buying shares of companies in developed markets that are well-positioned to benefit from growth in emerging markets. Another area to consider is exposure to emerging market currencies and debt. Here you will find opportunities to invest in countries with positive demographic trends and without the debt burden of many countries with developed markets. Japan The recovery in Japan is simply unsustainable.

The Japanese central bank’s expansive monetary policy, termed “Abenomics,” has only limited prospects for long-term success. Japan’s central bank is trying to fight deflation and sluggish growth by weakening the yen. This has helped in the short term to raise equity markets, but what needs to be addressed in Japan goes much deeper and involves breaking down cemented structures before we would feel comfortable in saying that the country is on its way to sustainable long-term growth. Investors may see their shares of Japanese companies rise as the yen weakens, but they better keep on their toes, because as soon as the expansionary policy is reduced, we see the yen rising again and Japanese government bond yields once again sinking. We feel current share prices in Japan are optimistically high.« .

STOXX pulsE – WINTER 2014 7 . vOLATILITY AS An ASSET CLASS AS An ASSET CLASS 8 . sToxx Pulse – WINteR 2014 of mid-term futures when the volatility forward curve is in contango. VSTOXX AnD DYnAMIC vSTOXX Volatility has become an important tool for investors to diversify traditional equity portfolios and for taking outright views on the direction of equity markets. STOXX offers several indices to help investors benefit from volatility as an asset class. The EUrO STOXX 50 volatility Index (vSTOXX), for example, measures the implied variance across all options of a given time to expiry. The vSTOXX family includes many indices, including the VSTOXX Short-Term Futures Index, which measures return from a rolling long position in first and second month EUrEX vSTOXX futures contracts. The EUrO STOXX 50 Volatility Mid-Term Futures Index replicates a constant five-month forward, one-month implied volatility. STOXX Pulse talked to three experts to get their views on volatility as an asset class and volatility products available in the market. Abhinandan Deb is head of European equity derivatives research at bank of America Merrill Lynch Global Research. Prior to joining BofA Merrill Lynch in 2010, he was a senior equity derivatives research analyst at Barclays Capital. he holds a master’s degree in Advanced Computing from Imperial College London and bachelors’ degrees in computing and in physics from Oxford University and St Stephen’s College, University of Delhi. The Dynamic VSTOXX Index is a combination of two indices, the VSTOXX Short-Term Futures and Mid-Term Futures Indices.

The rationale behind dynamic allocation is to exploit in a timely manner the superior performance of short-term futures when the volatility forward curve is in backwardation and John-Mark Piampiano is a portfolio manager at Pine River Capital Management since 2010. Before joining Pine River, Piampiano was a principal at Engineered Portfolio Partners. From 2002 to 2009, he worked as senior portfolio manager hbk Investments in Dallas, where he was responsible for the global volatility business including portfolio trading, risk management and staffing. he has also worked as an equities derivative trader at KBC Financial Products in new York and as a trader at hess Energy Trading Co.

Piampiano received a bachelor of science degree in economics and biology from the Massachusetts Institute of Technology in 1999. JoHN-MaRK pIaMpIaNo Pine River Capital Management abHINaNDaN DEb Bank of America Merrill lynch 9 . AS An ASSET CLASS our investors eXpect us to search the Globe For ineXpensive hedGes and relative value trades in the volatility space. John-mark piampiano VSTOXX AnD DYnAMIC vSTOXX Volatility has become an important tool for investors to diversify traditional equity portfolios and for taking outright views on the direction of equity markets. STOXX offers several indices to help investors benefit from volatility as an asset class. The EUrO STOXX 50 volatility Index (vSTOXX), for example, measures the implied variance across all options of a given time to expiry. The vSTOXX family includes many indices, including the VSTOXX Short-Term Futures Index, which measures return from a rolling long position in first and second month EUrEX vSTOXX futures contracts. The EUrO STOXX 50 Volatility Mid-Term Futures Index replicates a constant five-month forward, one-month implied volatility. The Dynamic VSTOXX Index is a combination of two indices, the VSTOXX Short-Term Futures and Mid-Term Futures Indices.

The rationale behind dynamic allocation is to exploit in a timely manner the superior performance of short-term futures when the volatility forward curve is in backwardation and of mid-term futures when the volatility forward curve is in contango. STOXX Pulse talked to three experts to get their views on volatility as an asset class and volatility products available in the market. Abhinandan Deb is head of European equity derivatives research at bank of America Merrill Lynch Global Research. Prior to joining BofA Merrill Lynch in 2010, he was a senior equity derivatives research analyst at Barclays Capital. he holds a master’s degree in Advanced Computing from Imperial College London and bachelors’ degrees in computing and in physics from Oxford University and St Stephen’s College, University of Delhi. John-Mark Piampiano is a portfolio manager at Pine River Capital Management since 2010. Before joining Pine River, Piampiano was a principal at Engineered Portfolio Partners. From 2002 to 2009, he worked as senior portfolio manager hbk Investments in Dallas, where he was responsible for the global volatility business including portfolio trading, risk management and staffing. he has also worked as an equities derivative trader at KBC Financial Products in new York and as a trader at hess Energy Trading Co.

Piampiano received a bachelor of science degree in economics and biology from the Massachusetts Institute of Technology in 1999. What sort oF interest are you seeinG amonG your customers in products that help FiGht volatility? deb: The volatility regime is changing. While fewer investors are as keyed up on fighting tail risk as they were during the height of the European sovereign crisis, we’re seeing rapidly growing interest and trading activity in volatility products from a wide variety of clients in diverse geographies. Selling volatility has been a winner in 2013 and this hasn’t been lost on most investors. Consequently, volatility put strategies have been in strong demand.

Relative value volatility has also picked up and our hedge fund clients were active in forward variance spreads; with volatilities generally low to sell outright and costly to buy and hold outright, relative value becomes a natural play. piampiano: Our investors expect us to search the globe for inexpensive hedges and relative value trades in the volatility space. Index products provide a “benchmark” in each geographic region since they represent the most liquid suite of products and provide a basis for comparison for the price of other option products in that region. 10 . STOXX pulsE – WINTER 2014 Cyprus, Turkey and Israel. He is also responsible for the sales activities of Eurex vSTOXX Derivatives. before joining Eurex, Markus worked as a senior equity derivatives and fixed income derivatives trader at Citibank in Germany and Switzerland for almost a decade. MaRKUs-aLExaNDER FLEsCH eurex Zurich AG complex is the reduced liquidity relative to options on EUrO STOXX 50 or other major European equity indices. in your opinion, What kind oF product or products are the best tools to fight volatility in the market? Which vstoXX indeX or indices do you use and What are the pros and cons of this product? deb: I tend to follow the VSTOXX futures curve. While it is still far less liquid than the VIX, there are a few reasons why investor interest in trading VSTOXX has grown: » Relative value opportunities arise due to the difference in steepness of the two futures curves; the VSTOXX curve is less impacted by ETP flows than VIX is. » European risk is better hedged with VSTOXX than VIX. » Diversification: like any asset, there is scope for regional diversification and investors will look more seriously at vSTOXX once volumes/liquidity grow sufficiently for trading costs to reduce. piampiano: We trade VSTOXX futures and options in both a hedging and relative value context.

VSTOXX derivatives give us exposure to market implied volatility without any direct exposure to the underlying cash index (EUrO STOXX 50), in contrast to EUrO STOXX 50 put or call options, which lose their convexity profile if we move away from our strike price. This makes the VSTOXX derivatives unique among listed European volatility products in that they provide us with this “strikeless” exposure. Our primary concern with the vSTOXX deb: Generally, volatility products are well suited to hedge risk-off events, given outsized moves in volatility versus large moves in risk assets. The key always is how to manage long volatility exposure, and we have worked to deliver our clients volatility option based hedges that also have superior carry profiles, indeed with the potential to carry positively.

Few if any other asset classes can offer such payoffs. piampiano: There is no product which provides the best hedge 100% of the time. Each product has advantages and disadvantages both with respect to the nature of the convexity profile and with the price relative to other hedges. Our investors expect us to make a careful analysis of the relative merits of all the potential hedges in the market to ensure the hedge we offer represents the cheapest possible convexity profile at any given time to protect each of our portfolios. can you tell us Why the vstoXX and dynamic vstoXX indices are popular amonG investors? Flesch: VSTOXX is becoming increasingly popular amongst institutional investors, even though 2013 was a year in which overall volatility levels were suppressed. A growing number of clients have discovered volatility as an asset class and value "pure" volatility trading in comparison to trading a "proxy" of volatility with straddles on the underlying index market, which is subject to transaction costs from dynamic delta management. With the VSTOXX itself and a wide range of dynamic vSTOXX Indices, Europe is catching up with US market development.

In the US, volatility products have been more mainstream for many years and are also actively used by retail investors. With our listed European volatility derivatives, clients can gain exposure more efficiently than in the past, when Markus-Alexander Flesch has been an executive director at Eurex Zurich AG since 2003 and is responsible for the derivative business for sell-side and buy-side clients in Switzerland, Italy, 11 . ChInA’S “FInAnCIAL STYLE bIG ChINA’s “fINANCIAl style BIG BANG” 12 . sToxx Pulse – WINteR 2014 What does the chinese Government need to do, especially With reGard to foreign exchange and customs reGulations, to ensure that this liberalization proGram enables interested investors and the country to beneFit? I see this move as China’s commitment to economic and financial change. This is a kind of Chinese style financial big bang, similar to what happened in 1986 in the UK and in 1993 in Japan. JULIaN TsUNg-sHENg LIU yuanta securities Investment trust Co ThE ShAnGhAI FrEE TrADE ZOnE China launched the Shanghai Free Trade Zone on Sep. 29, 2013, a move hailed by many analysts and media as the boldest step yet by the country to liberalize rules that govern finance, currency, investment, trade and interest rates. The plan of the SFTZ is to open up to foreign competition in the zone and use it as a testing laboratory for reforms, including a convertible yuan and liberalized interest rates. More than 1,400 companies had registered in the SFTZ within two months of its launch, the Financial Times reported in november. Reuters reported in December that Charles Schwab had traveled to Shanghai to discuss opening an office in the free trade zone. "The next step is to open an office in the new free trade zone in Shanghai," Schwab was quoted as saying by reuters.

"The rules and regulations are not completely clear." Some analysts say that the SFTZ does not sound appealing to foreign investors because the political will behind the project seems lacking. In addition, more clarity regarding customs and foreign exchange regulations in the free zone need to be clarified. STOXX Pulse spoke with Julian TsungSheng Liu, president and chief executive of Yuanta Securities Investment Trust Co., an asset manager headquartered in Taipei, to get his views on what this move means for China. Liu visited the SFTZ in 2013.

Yuanta Securities is a subsidiary of Yuanta Financial holding, and also has representative offices in Shenzhen and Shanghai. Yuanta SITC has 10 billion US dollars of assets under management. In terms of the forex control, we will see a lot of relaxation of currency control from the Central Bank of China. The first move would be trying to cap the weight for renminbi internationalization.

We see that a lot of offshore centers started by Hong Kong and Taiwan and Singapore and London are coming into play. We see that renminbi is heavily controled by China as it tries to stabilize its currency movement, its international trade and its economic performance. But I think now China believes the timing is good to remove all trading bans for the currency. In this new zone, China plans a mechanism for two-way movement – in and out – for renminbi internationalization and liberalization. At the same time, we are seeing a lot of new measures toward interest rates, lending rates and deposit rates.

Wealthmanagement wise, we see that banks like Citibank from the US and DbS from Singapore want to have a presence and exposure in the SFTZ. Meanwhile, in terms of customs control, I think there will be special treatment for the SFTZ. For example, automakers will enjoy many tax reductions. 13 . ChInA’S “FInAnCIAL STYLE bIG For right now in Shenzhen, the Chinese government allows a 49% ownership for a joint venture in the mutual fund and securities industry. There are more than 80 mutual fund companies currently domiciled in China. In the future, the intention of the government is to allow more than 50% foreign ownership, but, do remember, the government also does not want to jeopardize local industry. As of right now, it is not clear whether you can own 100% of your company in the SFTZ. But things will become clearer over time. do you think the sFtz poses a threat to hong kong? I was at the SFTZ in mid-november, and it is a very small area, just 11 kilometers.

I think it is very symbolic. I think the banking, manufacturing and logistics industries will benefit from such openness. hoW lonG do you think it Will take beFore the sFtz becomes Fully Functional and solves its teethinG problems? That is easier said than done. This is just the launch. There will be trial and error as China tests the waters.

I think stage one will take one or two years. Our anticipation for now is that it will take three to four years to establish all the necessary infrastructure and also take another two or three years after that to finalize. So in terms of the time horizon, I think the SFTZ will become the engine for mainland China by 2020 in terms of liberalization and deregulation. That said, I think in five years from now, we will begin to see a lot of the measures taking effect. 14 I think there will be more synergy than competition between Hong Kong and Shanghai.

Or, more likely, co-competition, which is a mix of cooperation and competition. There are no major political barriers between Hong Kong and mainland China, compared to the barriers that exist between mainland China and Taiwan. I think Hong Kong and Shanghai can play different roles, because I think the target of the mainland China government is to set up Shanghai to become the international financial center, while Hong Kong is the financial center of Asia. Also, in terms of the structure of the economy, Hong Kong is a city economy, while mainland China is a continental economy.

Hong Kong was also occupied by a service industry, while mainland China has a lot of trading, import and export industry. However, Hong Kong does have a more mature economy, a better platform for accounting, laws, etc., so I think Hong Kong can be leveraged by Shanghai. does yuanta have any plans to move into this Free trade zone? We have a mutual fund joint venture with China resources Group in Shenzhen. Shenzhen is a special economic zone too. In the SFTZ we will get another tax break of 10% but we are well established in Shenzhen and right now we have no plans to open an office in Shanghai. Just a last question about hoW Well versed you think asian investors are With diFFerent products in the etp space? Asian investors have a good knowledge base about ETPs, ETFs and also different strategies, such as low volatility. For example, Taiwanese pension funds are keen to invest in global low volatility products. In East Asia such as Japan and korea, I think investors are fast movers and have greater acceptance for innovative and new financial products, while I think that in Hong Kong and Singapore investors have a good variety of ETD products available. And many big steps in the investment sector are being taken by governments in Asia. Singapore, Malaysia and Thailand just entered an agreement to sign the Collective Investment Scheme (CIS), which is a three-country mutual fund passport.

It is very, very similar to UCITs in Europe. So funds that are domiciled in Singapore can be easily redistributed to Thailand or Malaysia. This is bound to change the mutual fund landscape of Southeast Asia.

In the same way, the Greater China market also needs to be consolidated. Meanwhile, mainland China has encouraged financial innovation in recent years. In 2013, China had a fixed income ETF, it had a gold ETF and cross-border ETF. So China remains a big market with endless possibilities.« .

sToxx pulsE WINTER STOXX Pulse – WINteR 2014 15 . PLACInG SCrEEnS On SUSTAInAbILITY PLACInG SCrEEnS On SUSTAInAbILITY SELECTInG ThE bEST: ESG FIrMS WITh ThE LOWEST vOLATILITY AnD hIGhEST DIvIDEnDS isToxx global Esg select 100 sToxx global Esg Leaders sToxx global 1800 7.3% 10.6% 5.7% volatility (annualized)1 14.5% 17.5% 15.7% Maximum drawdown 50.2% 52.8% 53.7% Sharpe ratio1 0.43 0.55 0.31 Gross dividend yield 4.4% 3.6% 3.0% Performance (annualized) gUILLaUME FLaMaRIoN J.P. Morgan STOXX Ltd. introduced the iSTOXX ESG Select 100 Index in December, 2013. The index selects 100 stocks with the lowest volatility and highest dividends from the universe of the STOXX Global ESG Leaders Index. STOXX Ltd. talked to Guillaume Flamarion, a London-based equity derivatives structurer at J.P.

Morgan, to ask him about applying screens to a sustainability index and what that means for investors. Flamarion joined J.P. Morgan in October, 2011. He has more than 7 years of experience in equity solutions structuring. he graduated from the Ecole des Mines de Paris in 2006. 16 isToxx gLobaL Esg sELECT 100 sHoWs LoWER voLaTILITy aND HIgHER DIvIDEND THaN bENCHMaRKs 300 200 100 0 Sep 2004 Sep 2006 iSTOXX Global ESG Select 100 (EUr Gr) Sep 2008 Sep 2010 Sep 2012 STOXX Global ESG Leaders (EUr Gr) STOXX Global 1800 (EUr Gr) 1) EOnIA rate used as proxy for riskless returns.

Gross dividend yield calculated from Dec. 11, 2012 to Dec. 11, 2013 Source: STOXX daily data from Sep.

20, 2004 to Dec. 9, 2012. For iSTOXX Global ESG Select, data is backtested until nov.

21, 2013. For STOXX ESG Leaders, data is backcasted until Apr. 2011 .

STOXX pulsE – WINTER 2014 don’t esG and sustainable indices already have companies that pay relatively hiGh dividends and Whose shares display relatively loWer volatility? or is that Just an assumption, and hence the need to apply these screens to an esG indeX? What is the beneFit oF applyinG screens For loW volatility and hiGh dividends on a sustainability indeX? I would like to emphasize that first of all, an ESG index tracks the returns of a basket of sustainable stocks. Companies that implement strict controls on Environmental, Social and Governance (ESG) standards are usually better positioned to deliver consistent performance in the long term. This ESG filter is mainly a qualitative factor which can be combined with more quantitative gauges, like low volatility and high dividends. Investing in low volatility stocks has been very popular among investors recently. Usually, high volatility stocks are relatively overpriced as mutual fund managers, who might have limitations on the use of leverage, are tilting towards high volatility stocks to generate performance. Moreover, stocks with low historical volatility, exhibit historically superior risk-adjusted returns (Sharpe ratio). Companies that pay high dividends are generally seen as stable, generating consistent earnings and returns in the long term. A high dividend yield can indicate undervaluation of the stock , because the stock s dividend is high relative to its price. Moreover, in a low interest rate environment, high dividend stocks can provide consistent income to investors. Stocks from the ESG universe are generally stable companies which could be seen as already displaying lower volatility and paying relatively high dividends. The ESG filters are mainly non-financial qualitative criteria which can be balanced efficiently with two financial quantitative gauges – low volatility and high dividends. Theoretically, orthogonal (independent) factors would form a complete and diversified set of investments.

In practice, it is difficult to associate completely independent factors. The three levels of selection within the index achieve their objective of complementing each other efficiently: qualitative and quantitative, quality and stability, potential growth and regular income. however, investors must not forget that while this selection process exhibits efficiencies in theory, there is no guarantee that the iSTOXX Global ESG Select 100 Index will necessarily outperform its benchmark. this esg filter is mainly a qualitative Factor Which can be combined with more quantitative GauGes, like loW volatility and hiGh dividends. Guillaume Flamarion launches have gathered considerable assets, and today most index providers have flagship low volatility and select dividend indices.

However the combination of both is still rare. As explained, low volatility and select dividends are two complementary factors within an index like the iSTOXX Global ESG Select 100 Index. This concept could be extended to STOXX indices other than ESG, for example on benchmark indices (EUrO STOXX 50, STOXX Europe 50, STOXX Europe 600), thematic indices (STOXX Strong Quality index family), or sector indices. It is important to remember that there is no guarantee that quantitative factors will always enhance performance.« In a nutshell, the iSTOXX Global ESG Select 100 Index intends to combine these three complementary factors: quality (ESG filter), low risk (low historical volatility) and value (high dividend). can the perFormance oF broad or other types oF indices be enhanced by applying screens to these indices? hoW? The demand for low volatility and high dividend strategies has grown significantly over the past few years due to strong risk-adjusted performance and increased investors’ appetite for smarter equity exposure.

In fact, recent ETF 17 . FEATUrED InDICES feAtuRed INdICes sToxx global 1800 52-WEEK pERFoRMaNCE 3-yEaR pERFoRMaNCE STOXX Global 1800 STOXX Global 1800 Minimum Variance STOXX Global 1800 Minimum Variance Unconstrained STOXX Global Select Dividend 100* 20.1% 12.5% 8.2% 9.3% 34.0% 38.2% 32.5% 24.7% STOXX Global Maximum Dividend 40* 18.4% 21.5% STOXX Europe 600 STOXX Europe 600 Minimum variance STOXX Europe 600 Minimum variance Unconstrained STOXX Europe Select Dividend 30* STOXX Europe Maximum Dividend 40 19.1% 16.8% 16.1% 12.1% 26.8% 29.9% 37.5% 35.0% 11.0% 34.4% STOXX Europe 600 Equal Weight STOXX Europe Low risk Weighted 100 22.5% 17.1% 31.6% 43.6% 19.0% 14.3% 16.7% 19.4% 19.9% 19.7% 22.1% 31.9% 43.1% 13.1% 22.2% 24.2% 12.9% 4.8% 2.3% 1.0% 10.3% -4.7% 2.3% 12.5% 17.0% 15.1% 27.9% 16.2% 20.7% 10.3% -11.3% -11.6% -16.0% -19.2% -2.3% -7.0% -8.9% 17.7% 4.6% 17.2% sToxx Europe 600 EURo sToxx 50 EUrO STOXX 50 EUrO STOXX Minimum variance EUrO STOXX Minimum variance Unconstrained EUrO STOXX Select Dividend 30 EUrO STOXX 50 Equal Weight EUrO STOXX 50 Low risk Weighted sToxx asia/pacific 600 STOXX Asia/Pacific 600 STOXX Asia/Pacific 600 Minimum Variance STOXX Asia/Pacific 600 Minimum Variance Unconstrained STOXX Asia/Pacific Select Dividend 30* STOXX Asia/Pacific Maximum Dividend 40* STOXX ASEAn-Five Select Dividend STOXX East Asia 80 sToxx China a 50 STOXX China A 50 STOXX China A 50 Equal Weight sToxx australia 150 STOXX Australia 150 STOXX Australia 150 Minimum Variance STOXX Australia 150 Minimum Variance Unconstrained 18 . STOXX pulsE – WINTER 2014 sToxx North america 600 52-WEEK pERFoRMaNCE 3-yEaR pERFoRMaNCE 22.8% 17.1% 15.2% 12.1% 11.1% 43.9% 46.7% 50.0% 48.1% 31.6% 25.3% 18.9% 17.1% 44.9% 47.5% 54.6% -0.8% 0.5% 0.1% -2.8% 22.0% 26.6% STOXX north America 600 STOXX north America 600 Minimum Variance STOXX north America 600 Minimum Variance Unconstrained STOXX north America Maximum Dividend 40* STOXX north America Select Dividend 40* sToxx Usa 900 STOXX USA 900 STOXX USA 900 Minimum Variance STOXX USA 900 Minimum Variance Unconstrained sToxx Canada 240 STOXX Canada 240 STOXX Canada 240 Minimum Variance STOXX Canada 240 Minimum Variance Unconstrained All indices are in EUr Gross return versions, except the ones marked with *, which are in EUr net return versions Source: STOXX data as of Jan. 13, 2014 sToxx asEaN-FIvE sELECT DIvIDEND 50 sHaRpLy oUTpERFoRMs THE sToxx asIa ToTaL MaRKET INDEx 600 500 400 300 200 100 0 Mar '04 Mar '05 Mar '06 Mar '07 Mar '08 Mar '09 STOXX ASEAn-Five Select Dividend 50 (EUr Gr) Mar '10 Mar '11 Mar '12 Mar '13 STOXX Asia TMI (EUr Gr) Source: STOXX daily data from Mar. 22, 2004 to Jan. 10, 2014. 19 .

CoNTaCTs Vol 3/Issue 1 – WINTER 2014 Printed in January 2014 Selnaustrasse 30 CH-8021 Zurich P +41 (0)58 399 5300 stoxx@stoxx.com www.stoxx.com Frankfurt: +49 (0)69 211 13243 Hong Kong: +852 6307 9316 London: +44 (0)20 7862 7680 Madrid: +34 (0)91 369 1229 new York: +1 212 669 6426 Singapore: +65 9189 7970 Stockholm: +46 (0)8 4600 6090 sToxx is part of Deutsche börse and sIx This newsletter contains opinions and statements from various information providers. STOXX Limited does not represent or endorse any of these views or opinions and does not vouch for their accuracy or reliability. The views expressed by the information providers in this newsletter are their own views and do not reflect the views and opinions of STOXX Limited. STOXX® indices are protected through various intellectual property rights. ‘STOXX’, ‘EUrO STOXX 50’ and ‘iSTOXX’ are registered trademarks.

The use of the STOXX® indices for financial products or for other purposes requires a license from STOXX. STOXX does not make any warranties or representations, expressed or implied with respect to the timeliness, sequence, accuracy, completeness, currentness, merchantability, quality or fitness for any particular purpose of its index data. STOXX is not providing investment advice through the publication of the STOXX® indices or in connection therewith.

In particular, the inclusion of a company in an index, its weighting, or the exclusion of a company from an index, does not in any way reflect an opinion of STOXX on the merits of that company. Financial instruments based on the STOXX® indices are in no way sponsored, endorsed, sold or promoted by STOXX. © STOXX Limited. All rights reserved. .