Description

Filed Electronically at Regulations.gov

July 21, 2015

Office of Regulations and Interpretations

Employee Benefits Security Administration

Attn: Conflict of Interest Rule

Room N-5655

U.S. Department of Labor

200 Constitution Avenue N.W.

Washington, DC 20210

Re:

Office of Exemption Determinations

Employee Benefits Security Administration

Attn: D-11712

Suite 400

U.S. Department of Labor

200 Constitution Avenue N.W.

Washington, DC 20210

Definition of the Term “Fiduciary”; Conflict of Interest Rule – Retirement

Investment Advice (RIN 1210-AB32)

Proposed Best Interest Contract Exemption (ZRIN 1210-ZA25)

Dear Sir or Madam:

The SPARK Institute, Inc.1 appreciates the opportunity to comment on the Department of

Labor’s (“Department”) proposed rule concerning the definition of the term “fiduciary” (the

“Proposal”)2 and the corresponding proposals for new and amended prohibited transaction

exemptions.3 The SPARK Institute supports the Department’s goal of ensuring that persons in a

position of trust and confidence are subject to fiduciary standards when providing investment

advice with respect to employee benefit plans (“plans”) and individual retirement accounts

(“IRAs”). However, we remain concerned, as we were in 2010 with respect to the Department’s

previous proposal to amend the definition of “fiduciary,”4 that the Proposal will have significant

unintended consequences both for persons subject to the regulation and for millions of

Americans saving for retirement.

As explained in more detail below, we are very concerned that the Proposal is likely to create the

following problems (among others) for plan and IRA service providers.

Each of these problems 1 The SPARK Institute represents the interests of a broad-based cross section of retirement plan service providers and investment managers, including banks, mutual fund companies, insurance companies, third-party administrators, trade clearing firms, and benefits consultants. Collectively, our members serve approximately 70 million employersponsored plan participants. 2 80 Fed. Reg.

21,928 (Apr. 20, 2015). 3 See, e.g., 80 Fed. Reg.

21,960 (Apr. 20, 2015); 80 Fed. Reg.

22,010 (Apr. 20, 2015). 4 75 Fed. Reg.

65,263 (Oct. 22, 2010). . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 2 of 32 will ultimately have negative consequences for retirement savers’5 ability to obtain the education and information they need to more effectively and efficiently save for retirement: • The Proposal would make it difficult for service providers to: (1) provide meaningful assistance for small businesses, (2) provide general investment guidance to individuals, and (3) provide rollover and distribution information and guidance to individuals; • The Proposal would force service providers to scale back on several very important and meaningful parts of investment education that have positively engaged retirement savers; and • The Proposal affects, but does not seem to take into account, service providers’ standard industry practices and does not fully reflect how the market operates. Consequently, the Proposal will make it very difficult for plan recordkeepers and other service providers to respond to requests for proposals (“RFPs”) and other information requests from plan sponsors or IRA owners who seek a service provider or investment adviser. The SPARK Institute’s members, which include leading recordkeepers, third-party administrators, investment fund managers, and other service providers, have a critical interest in the Proposal because the Proposal’s conversion of certain functions and information that have historically been non-fiduciary in nature into the provision of “investment advice” subject to fiduciary standards will have a substantial effect on our members’ ability to continue providing many forms of their valuable services to plans and IRAs. Most of the useful services that the SPARK Institute’s members provide to plan fiduciaries and plan participants are not intended to be fiduciary in nature. The SPARK Institute’s members must keep these services non-fiduciary because of prohibited transaction, co-fiduciary, and other concerns, including how to truly satisfy ERISA’s exclusive benefit requirements6 in the context of sales conversations.

Therefore, most of our comments are aimed at helping the Department craft a line between fiduciary and nonfiduciary actions that is clear and that does not prevent the furnishing of valuable information and guidance to plan sponsors and participants. As we said in 2010, and continue to believe, a service provider and a plan sponsor should be permitted to agree upon and define, in writing, the service provider’s role, whether a fiduciary relationship is intended or expected, and, if it is, the scope of that fiduciary relationship. While there may be different considerations in the context of participants and IRA owners, it is fundamental that non-fiduciary service providers should be able to make their services available to plan sponsors without triggering fiduciary status. An inability to continue these services will leave plan sponsors without these services, or will require them to obtain the services at a much higher cost. Throughout this letter we have provided concrete examples of common situations where it will be harder for service providers to provide meaningful assistance. 5 Throughout this letter, we refer generally to plan participants and beneficiaries and IRA owners as “retirement savers.” 6 ERISA § 403(c)(1); see also ERISA § 404(a)(1) (duty of loyalty). . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 3 of 32 I. Executive Summary The following is a summary of the SPARK Institute’s various concerns, requests, and recommendations as further described below in this letter. Definition of “Fiduciary” – Investment Advice (Part II of this letter) • The inclusion of a recommendation that is “specifically directed to” an advice recipient could be interpreted too broadly, calling into question very standard forms of communications from service providers such as a subset of participants receiving general information about a specific issue or call center interactions in which a call center employee provides general information to only one person. Accordingly, we recommend that “specifically directed to” be removed from proposed section 2510.3-21(a)(2)(ii). • The Department should exclude from the term “recommendation” information that is intended to provide general guidance and that a reasonable person would believe is not intended to provide individualized investment advice. Many service providers play a crucial role in educating and motivating participants who are increasingly responsible for their own retirement savings in participant-directed defined contribution plans, and service providers’ continued ability to provide suggestions (e.g., to diversify an account) to retirement savers without becoming fiduciaries is critical. • The Department should clarify that the phrase “agreement, arrangement or understanding” requires a meeting of the minds. A service provider should not be designated a fiduciary simply because a participant decides that there was an “understanding” that fiduciary investment advice is or was being provided, despite the service provider not acting in any way that would make it reasonable to conclude that such an “understanding” exists (or existed). • Because the Proposal appears to turn ordinary “hire me” conversations with plan sponsors into investment advice, such as where a service provider responds to an RFP from a prospective customer, we urge the Department to amend the Proposal so that a “recommendation” from a service provider that the service provider be engaged to provide investment advice, investment management, or valuation services (which is really a sales conversation) is not considered fiduciary investment advice. • The Department should not adopt FINRA’s standards for defining what constitutes a “recommendation” because those standards sweep in too much activity that should be considered non-fiduciary and were developed specifically with broker/dealers (rather than plan service providers and other parties) in mind. • The Department should clarify the definition of “recommendation” so that it is not fiduciary investment advice to recommend another person to provide advice or investment management services, unless the person making the recommendation was specifically engaged to make such a recommendation for a fee. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 4 of 32 • The Department should clarify that investment advice does not include pricing valuations and informational reporting activities such as the valuation of an annuity for an individual considering a Roth conversion who uses the valuation to determine whether to proceed with the conversion. • We ask that the Department confirm longstanding guidance that a fiduciary may limit the scope and time frame of the fiduciary’s duties and obligations. Carve-Outs (Part III of this letter) • The Department’s significant scaling back of what qualifies as “investment education” under the investment education carve-out is too severe and would result in many forms of very helpful information and tools no longer being made available to retirement savers. The Department should not amend Interpretive Bulletin 96-1 to no longer permit the mention of specific investments in asset allocation models because the ability to do so in the context of investment education has been critical in helping retirement savers “connect the dots” between the generic concept of asset allocation and understanding which of the available investment options fit in each asset allocation category. In addition, we urge the Department to provide that factual conversations between a service provider and a retirement saver regarding the pros and cons of various distribution options, and/or the existence of certain available products, not be considered investment advice. • Unless the seller’s carve-out is extended to small plans, small plan sponsors will not receive the guidance they need concerning products and services available to them, which will discourage small employers with fewer than 100 employees (which represent nearly 40 million workers) from offering or maintaining a retirement plan for their employees. Even small plan fiduciaries are able to determine whether they are being sold a product or service as opposed to receiving impartial investment advice, especially when provided with a specific written disclosure. ERISA itself makes no distinction between the duties and requirements of small and large plan fiduciaries. If the Department is unwilling to broadly expand the seller’s carve-out to small plans, we then urge the Department to consider requiring an additional disclosure for use specifically with small plans, making the carve-out available in service provider transactions for which the new 408(b)(2) disclosures will be required. • The platform provider carve-out should be expanded to apply to IRAs because the carveout only provides relief for marketing a platform of investments.

The assembly of a platform not targeted to anyone in particular should not be considered investment advice, including with respect to individual IRA owners, simply because the platform includes some investments and excludes others. • The selection and monitoring carve-out should not be limited to selection and monitoring assistance provided only in connection with a platform. In addition, the carve-out should be available if the service provider identifies investment alternatives based on objective criteria disclosed to the advice recipient (rather than “specified” by the advice recipient). . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 5 of 32 Prohibited Transaction Exemptions (Part IV of this letter) • The Best Interest Contract Exemption (“BICE”) will not permit service providers to continue performing many important functions for plans and retirement savers if service providers are considered fiduciaries due to BICE’s numerous requirements. Due to our members’ concerns with BICE, we believe that many retirement service providers will not attempt to use BICE at all. Accordingly, to better accommodate the important functions of service providers, we ask the Department to focus on the requests and suggestions we have made elsewhere in this letter for changes to the scope of what constitutes investment advice, the definition of “recommendation,” and the scope and availability of the carve-outs. • We are concerned that the BICE is neither workable, nor does it appear to be designed to be workable, for service provider call center conversations with participants. Thus, the SPARK Institute’s members are unlikely to rely on the BICE to communicate with participants verbally or in writing. Timing of Effective and Applicability Dates (Part V of this letter) • II. We urge the Department to allow 36 months from the date a final rule is published for such rule to be both effective and “applicable.” This suggestion is well in line with the time frame provided by the United Kingdom when it implemented a similarly sweeping rule. Definition of “Fiduciary” – Investment Advice (Proposed Rule 29 C.F.R.

§ 2510.321(a)) Under the Proposal, 29 C.F.R. § 2510.3-21 would be revised to redefine the definition of a fiduciary of an employee benefit plan under the Employee Retirement Income Security Act of 1974 (“ERISA”) due to the provision of investment advice to a plan or to the plan’s participants or beneficiaries. The Proposal would also apply the revised definition of a fiduciary of a plan, including IRAs, to section 4975 of the Internal Revenue Code (“Code”).

In accordance with the Department’s intentions for the Proposal, the revised definition would result in a wider array of persons being treated as fiduciaries under ERISA and the Code than under the current rules, which have been in effect since 1975. In general, the Proposal provides that a person renders investment advice by providing recommendations to a plan, plan fiduciary, participant or beneficiary, or IRA owner or fiduciary, and either (1) the person acknowledges the fiduciary nature of the advice or (2) the person acts pursuant to an agreement, arrangement, or understanding with the advice recipient that the advice is individualized to, or specifically directed to, the recipient for consideration in making investment or management decisions regarding plan assets. Under the Proposal, the covered recommendations include those regarding securities or other property, distributions, rollovers, the management of securities or other property, statements regarding the value of securities or other property in connection with a specific transaction, and the engagement of a person who . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 6 of 32 will receive a fee for providing advice for any of the foregoing. The Department proposes to define the term recommendation as “a communication that, based on its content, context, and presentation, would reasonably be viewed as a suggestion that the advice recipient engage in or refrain from taking a particular course of action.” Where such a recommendation for investment advice is provided for a fee or other compensation, direct or indirect, the person would be a fiduciary.7 A. The inclusion in the definition of investment advice of any recommendation that is “specifically directed to” the recipient will likely result in the cessation of many helpful forms of communication to retirement savers. A person who renders one of the Proposal’s specified categories of advice or recommendations “pursuant to a written or verbal agreement, arrangement, or understanding that the advice is individualized to, or that such advice is specifically directed to, the advice recipient” for consideration in making certain investment decisions with respect to a plan or IRA would be a fiduciary under the Proposal (emphasis added). We understand that the phrase “specifically directed to” was intended to address concerns with the 2010 proposal that newspaper advertisements and brochures might be covered. We are concerned, however, that the phrase “specifically directed to” is too broad. When used in conjunction with the Proposal’s definition of “recommendation,” many forms of written communications and call center interactions that are currently viewed as investment education or other information not constituting advice could become investment advice under the Proposal. The Proposal does not clarify what “specifically directed to” means, which potentially calls into question every interaction our members have with participants or beneficiaries that is not replicated to every other person in the plan. EXAMPLE As part of a diversification campaign, a service provider sends a communication to all participants whose account holds a single fund that is not a target date fund using each participant’s own mailing or email address.

The letter (or email) has the participant’s name at the top. The letter reminds the individual of the importance of diversification. 7 The Department proposes to define “fee or other compensation, direct or indirect” to mean “any fee or compensation for the advice received by the person (or by an affiliate) from any source and any fee or compensation incident to the transaction in which the investment advice has been rendered or will be rendered.” Proposed rule, 29 C.F.R. § 2510.3-21(f)(6) (80 Fed.

Reg. 21,960). Some SPARK members expressed concern that it is not clear how broadly this definition sweeps, particularly where a service provider receiving some compensation for non-fiduciary services makes a recommendation (or has an employee make a recommendation) that triggers the Department’s test, but is not being compensated directly or indirectly for that “advice” – that is, there is no incremental fee or other compensation for the “advice.” Most SPARK members are reading the definition to be very broad, which results in a number of concerns expressed in our comment letter.

We recommend the Department clarify the application of this definition. . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 7 of 32 The letter also provides a list of all the target date fund (“TDF”) options available under the participant’s plan, and explains that a TDF is designed to provide diversification and age-appropriate allocations within a single fund so that it may be appropriate for someone looking for a simple way to diversify their account with a “one fund” investment approach. This communication appears “specifically directed to” the participant. EXAMPLE A plan fiduciary is concerned that some participants are heavily invested in employer stock and directs the service provider to send letters to participants with more than 20% of their account in employer stock. The letter explains the benefits of diversification similar to the statement required by ERISA. The letter is intended to be viewed as a “suggestion” the participant take a course of action (to diversify), and would be viewed as “specifically directed to” the participant. EXAMPLE A participant calls the service provider’s call center to discuss loan options.

The call center employee uses a script with generic information about the potential implications of taking a loan, including lost retirement savings and tax consequences upon default. The call center employee does not advise the participant on what is right for that participant’s circumstances, but because the participant is the only person on the phone listening to the call center employee, the conversation appears “specifically directed to” the participant. As written, the Proposal would lead many service providers to stop providing to retirement savers forms of communication that have been carefully developed over the years to provide helpful and timely information, encourage general diversification and increased retirement savings, and provide basic investment education. We understand that the Department has concerns with the practice described as the advertisement of one-on-one advice that an adviser disclaims in fine print as not being fiduciary advice. However, we urge the Department to protect routine letters addressed to a particular person and the many other forms of communication that are targeted to a particular issue (rather than to a particular person). Finally, a product provider should be able to explain the attributes of its products without becoming a fiduciary. EXAMPLE A participant owns an annuity or other investment that includes a guaranteed minimum withdrawal benefit (GMWB).

The participant attempts to make an “excess” withdrawal, which would reduce the value of the GMWB. The insurance company or other provider should be able to explain the consequences of making the withdrawal to the participant, . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 8 of 32 regardless of whether first asked by the participant, without engaging in the provision of fiduciary investment advice, even if its explanation of the consequences would lead a participant to (appropriately) seriously reconsider the decision. Accordingly, we recommend that the Department remove the phrase “or that such advice is specifically directed to” from proposed section 2510.3-21(a)(2)(ii).8 B. The Department should amend the Proposal to exclude recommendations that a reasonable person would not believe are intended to be individually tailored to the recipient. A fundamental concern that SPARK Institute members have with the Proposal is that the Proposal calls into question a variety of communications that service providers might have with participants that would not reasonably be viewed as an undertaking to provide investment advice. Participants generally receive two kinds of information from plan sponsors and service providers. The first category is generic plan-related information, much of which is required by law. This includes the Summary Plan Description and the annual fee and investment disclosure. These documents are important, but they are not enough to motivate participants to save in the plan, diversify their accounts, and preserve plan savings for retirement. All other communications (some of which squarely fit into the example of “education” under current law, and others that are similar to education) are actually intended to provide guidance.

Because of the responsibility placed on participants under participant-directed defined contribution plans, participants must be educated and motivated, and thus many service provider communications are “suggestions” that a participant either take an action (e.g., diversify) or not take an action (e.g., keep savings preserved in a plan or IRA). EXAMPLE A representative of a plan sponsor’s 401(k) service provider hosts an educational workshop over the lunch hour at the employer’s work site to help employees understand their 401(k) plan and make informed choices. An employee attending the workshop raises his hand and says “I’m trying to decide if I should use the default investment or manage my account myself.” The representative responds, “I can’t tell you what to do or provide investment advice, but here are a few things that we tell employees to keep in mind. First, the default investment is intended as an all-in investment because it is diversified, so if you use it, consider putting all of your account in the default.

Second, if you manage your account on your own, be careful not to put too many of your eggs in one basket and think about the advantages of diversification in long-term investing. For example, investing all of your account in the plan’s international equity fund has considerable risk given the lack of diversification.” This is an incredibly helpful conversation that goes on every day, and the employee should not reasonably view the information and guidance provided as an undertaking to provide fiduciary investment 8 If the Department elects to retain the “specifically directed to” language, the Department needs to provide more focused guidance distinguishing routine communications like those described in Part II.A. of this letter. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 9 of 32 advice. Further, if this conversation is deemed fiduciary in nature, the plan sponsor will not permit educational workshops such as this to occur. We do not think the Department intends to cover communications that a reasonable person would not understand to be impartial or trusted investment advice. Thus, we recommend that the Department build into section 2510.3-21(a)(2)(ii) a requirement that the advice be provided under circumstances that a “reasonable person would understand to be individualized advice that may be relied upon in making investment or investment management decisions.”9 C. The Department should clarify that the phrase “agreement, arrangement or understanding” requires a meeting of the minds. The Department has expressed concern that the current regulation’s requirement for a “mutual” agreement, arrangement, or understanding can allow a person who acts in all ways like a fiduciary to escape fiduciary status through a boilerplate disclosure. The Department deleted the word “mutual” from the definition, but retained the phrase “agreement, arrangement or understanding.” We believe that this remaining phrase continues to require a bilateral element – after all, an “agreement” or “arrangement” requires two parties to agree, and the term “understanding” appears in this context to mean an “understanding” between the advice provider and the advice recipient to provide advice that will be individualized and that will be relied upon in making investment decisions.

To illustrate, we believe that unsolicited communications should never be considered advice because they would not be provided to the recipient pursuant to an agreement, arrangement, or understanding. If a participant can simply decide that he or she has an “understanding” that fiduciary investment advice will be or, after the fact, was provided – despite the service provider not acting in any way to make the existence of an “understanding” reasonable – then a service provider can never be confident that its actions have not triggered fiduciary status. Thus, we ask you to confirm that there must be objective evidence that a meeting of the minds demonstrates an agreement, arrangement, or understanding between the advice provider and the advice recipient. We appreciate that this should not be judged solely on a single disclosure but on all of the surrounding communications. It should not be enough for a participant to merely believe that fiduciary investment advice is being provided, if that belief is not reasonable under the circumstances. D. The Department should amend or clarify the Proposal so that “hire me” conversations are not a fiduciary act. Proposed rule 29 C.F.R.

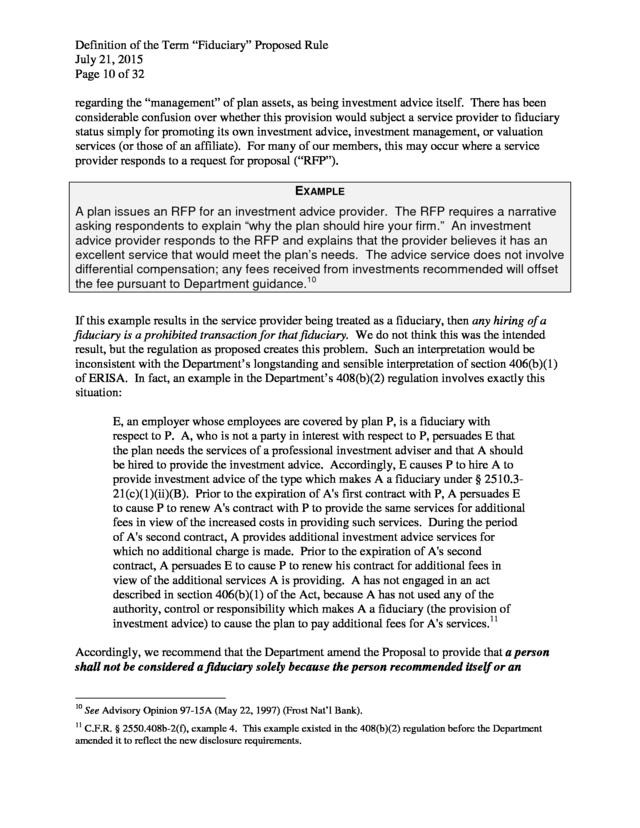

§ 2510.3-21(a)(1)(iv) would result in a recommendation of a person who would receive compensation for providing investment advice, or a recommendation 9 This standard used to determine what a “reasonable person would understand” could be coupled with factors that should be considered or are relevant, such as the degree to which advice is individualized, any disclosures provided, and the nature of the relationship, with no one factor being determinative. . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 10 of 32 regarding the “management” of plan assets, as being investment advice itself. There has been considerable confusion over whether this provision would subject a service provider to fiduciary status simply for promoting its own investment advice, investment management, or valuation services (or those of an affiliate). For many of our members, this may occur where a service provider responds to a request for proposal (“RFP”). EXAMPLE A plan issues an RFP for an investment advice provider. The RFP requires a narrative asking respondents to explain “why the plan should hire your firm.” An investment advice provider responds to the RFP and explains that the provider believes it has an excellent service that would meet the plan’s needs.

The advice service does not involve differential compensation; any fees received from investments recommended will offset the fee pursuant to Department guidance.10 If this example results in the service provider being treated as a fiduciary, then any hiring of a fiduciary is a prohibited transaction for that fiduciary. We do not think this was the intended result, but the regulation as proposed creates this problem. Such an interpretation would be inconsistent with the Department’s longstanding and sensible interpretation of section 406(b)(1) of ERISA.

In fact, an example in the Department’s 408(b)(2) regulation involves exactly this situation: E, an employer whose employees are covered by plan P, is a fiduciary with respect to P. A, who is not a party in interest with respect to P, persuades E that the plan needs the services of a professional investment adviser and that A should be hired to provide the investment advice. Accordingly, E causes P to hire A to provide investment advice of the type which makes A a fiduciary under § 2510.321(c)(1)(ii)(B).

Prior to the expiration of A's first contract with P, A persuades E to cause P to renew A's contract with P to provide the same services for additional fees in view of the increased costs in providing such services. During the period of A's second contract, A provides additional investment advice services for which no additional charge is made. Prior to the expiration of A's second contract, A persuades E to cause P to renew his contract for additional fees in view of the additional services A is providing.

A has not engaged in an act described in section 406(b)(1) of the Act, because A has not used any of the authority, control or responsibility which makes A a fiduciary (the provision of investment advice) to cause the plan to pay additional fees for A's services.11 Accordingly, we recommend that the Department amend the Proposal to provide that a person shall not be considered a fiduciary solely because the person recommended itself or an 10 11 See Advisory Opinion 97-15A (May 22, 1997) (Frost Nat’l Bank). C.F.R. § 2550.408b-2(f), example 4. This example existed in the 408(b)(2) regulation before the Department amended it to reflect the new disclosure requirements. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 11 of 32 affiliate to provide the services described in section 3(21) of ERISA or section (a)(1) of the [proposed] regulation. If the Department does not make this change, it is possible that there is no construct under which a “hire me” discussion could occur with a small plan sponsor. That is, the seller’s carve-out may be available for offering services to large plans (although the seller’s carve-out does not explicitly refer to the provision of “services”). If the seller’s carve-out were expanded beyond large plans (which we recommend and as further discussed below), this issue may be resolved. If the Department decides to make “hire me” discussions subject to fiduciary status – which we believe is inappropriate and contrary to ERISA and DOL regulations – then the Department needs to address the prohibited transaction concerns. A completely new exemption would need to be proposed and comments sought.

The BICE is not designed for this situation, as it is designed for advice recommendations to individuals generating differential compensation. E. The Department should not adopt FINRA’s standards for defining what constitutes a “recommendation” because that is too low a bar and is not appropriate for ERISA’s fiduciary line. Noting that most communications must constitute a “recommendation” to fall within the scope of fiduciary advice,12 the Department commented in the Proposal that it believes FINRA guidance regarding the evaluation of whether a particular communication could be viewed as a recommendation would provide useful standards and guideposts for distinguishing investment education from investment advice under ERISA.13 In this regard, the Department requested comments on whether it should adopt some or all of the standards developed by FINRA in defining communications that rise to the level of a recommendation for purposes of distinguishing between investment education and investment advice. For example, FINRA Policy Statement 01-23 provides guidelines to assist brokers in evaluating whether a communication could be viewed as a recommendation, which would in turn trigger additional requirements to help ensure the suitability of the recommendation for FINRA purposes. We do not think that it is appropriate to adopt a broad definition of “recommendation” based on FINRA rules. FINRA is a separate regulatory body that has developed guidance designed specifically with broker/dealers and its own penalty system in mind.

FINRA’s definition of recommendation – although appropriate for FINRA’s purposes in regulating those who sell securities – is too low a bar for purposes of the Proposal, making too many communications fiduciary in nature. Merely defining a recommendation as a “suggestion” that the advice recipient take (or not take) a certain action could be read very expansively; rather, a definition of recommendation that involves the “advocacy” of a specific act, would be a more appropriate – and workable – definition for purposes of the Proposal. 12 See proposed rule, 29 C.F.R. § 2510.3-21(a)(1)(i), (ii), (iv) (80 Fed.

Reg. 21,957). 13 See 80 Fed. Reg.

21,938. . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 12 of 32 Many of the concerns we lay out in this letter are created, in part, because the definition of “recommendation” is not well suited to the kinds of communications typical in a 401(k) plan. To illustrate: When the Department finalized its 404a-5 regulations requiring a fee and investment disclosure, it became apparent that even though the disclosure is required to be furnished by the plan administrator, any FINRA-regulated entity could be subject to FINRA rules if it assisted in the preparation of the disclosure. Accordingly, even a disclosure required by the Department and not intended to be a recommendation could be subject to FINRA’s rules. The salient point is that FINRA’s rules deliberately set a low bar for what constitutes a “recommendation.” We disagree that the Department should adopt such a low bar.

Instead, the Department should develop guidance that is narrower than the FINRA guidance regarding what constitutes a “recommendation.” The adoption of FINRA’s standards would result in a wide variety of persons not involved in the selling of securities (e.g., recordkeepers and other third-party administrators) becoming subject to standards that were not developed with them in mind. This would be very troublesome in the context of the Proposal, where the consequences for committing a prohibited transaction are draconian. In addition, we are concerned that whenever FINRA makes future changes to its guidance regarding what constitutes a “recommendation,” it will do so only with broker/dealers in mind (as would be expected), and that FINRA would not consider the impact of any changes on service providers and other entities that are subject to its guidance only due to the Department’s adoption of FINRA guidance for purposes of the fiduciary rule. To our knowledge, this sort of tying one regulatory line to the guidance from another regulator with a completely different purpose is unprecedented.

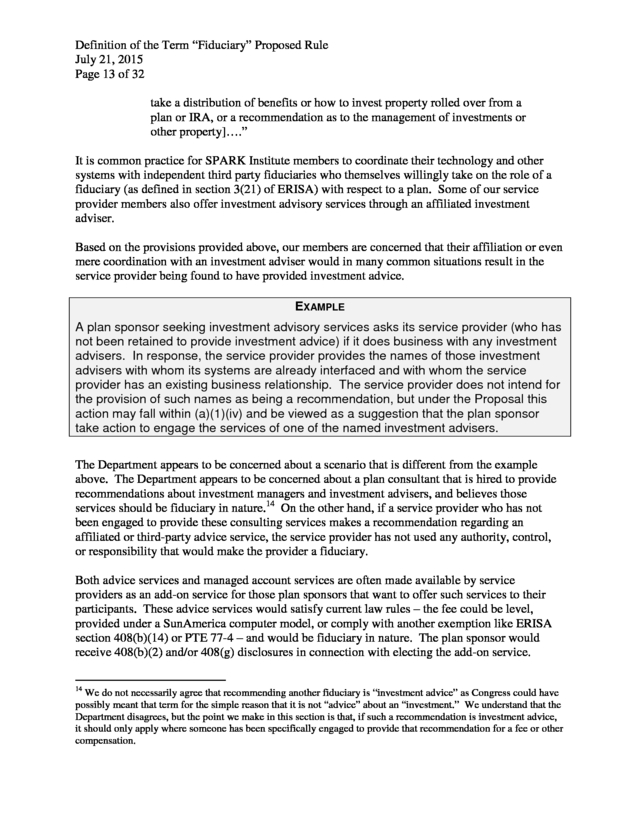

It would not be FINRA’s job to monitor or understand the impact of any changes to its guidance on parties other than those whom it regulates for its own purposes. Allowing an external entity to alter the definition of “recommendation” would be very problematic, especially because a service provider or other non-broker/dealer entity would not be able to seek a fix from FINRA. F. The Department should clarify that it is not fiduciary investment advice to recommend another person to provide advice or investment management services, unless the person was specifically engaged to make such a recommendation for a fee or other compensation. As described above, the provision of investment or investment management recommendations would result in the provider of the recommendation being treated as a fiduciary in certain cases. One of the categories of investment advice under the Proposal, which is provided for in proposed rule 29 C.F.R. § 2510.3-21(a)(1)(iv), is, “in exchange for a fee or other compensation, whether direct or indirect”: “[a] recommendation of a person who is also going to receive a fee or other compensation for providing any of the types of advice described in paragraphs (i) through (iii) [such as a recommendation to acquire, hold, dispose of, or exchange securities or other property, a recommendation to . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 13 of 32 take a distribution of benefits or how to invest property rolled over from a plan or IRA, or a recommendation as to the management of investments or other property]….” It is common practice for SPARK Institute members to coordinate their technology and other systems with independent third party fiduciaries who themselves willingly take on the role of a fiduciary (as defined in section 3(21) of ERISA) with respect to a plan. Some of our service provider members also offer investment advisory services through an affiliated investment adviser. Based on the provisions provided above, our members are concerned that their affiliation or even mere coordination with an investment adviser would in many common situations result in the service provider being found to have provided investment advice. EXAMPLE A plan sponsor seeking investment advisory services asks its service provider (who has not been retained to provide investment advice) if it does business with any investment advisers. In response, the service provider provides the names of those investment advisers with whom its systems are already interfaced and with whom the service provider has an existing business relationship. The service provider does not intend for the provision of such names as being a recommendation, but under the Proposal this action may fall within (a)(1)(iv) and be viewed as a suggestion that the plan sponsor take action to engage the services of one of the named investment advisers. The Department appears to be concerned about a scenario that is different from the example above.

The Department appears to be concerned about a plan consultant that is hired to provide recommendations about investment managers and investment advisers, and believes those services should be fiduciary in nature.14 On the other hand, if a service provider who has not been engaged to provide these consulting services makes a recommendation regarding an affiliated or third-party advice service, the service provider has not used any authority, control, or responsibility that would make the provider a fiduciary. Both advice services and managed account services are often made available by service providers as an add-on service for those plan sponsors that want to offer such services to their participants. These advice services would satisfy current law rules – the fee could be level, provided under a SunAmerica computer model, or comply with another exemption like ERISA section 408(b)(14) or PTE 77-4 – and would be fiduciary in nature. The plan sponsor would receive 408(b)(2) and/or 408(g) disclosures in connection with electing the add-on service. 14 We do not necessarily agree that recommending another fiduciary is “investment advice” as Congress could have possibly meant that term for the simple reason that it is not “advice” about an “investment.” We understand that the Department disagrees, but the point we make in this section is that, if such a recommendation is investment advice, it should only apply where someone has been specifically engaged to provide that recommendation for a fee or other compensation. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 14 of 32 Making these services available to plan sponsors, in coordination with other non-advisory services, enables plan sponsors to streamline the services needed to implement and manage their plans. The Proposal in its current form is problematic because if a service provider cannot market these add-on services without becoming a fiduciary, the services may not be offered. Accordingly, we recommend that the Department clarify that it is not fiduciary investment advice to recommend another person to provide advice or investment management services, unless the person was specifically engaged to make such a recommendation for a separate fee. Service providers should be able to communicate their offerings and capabilities to the market, including statements as to the third party(ies) and/or affiliate(s) with which the service provider has the ability to interface, without such a factual communication being a “recommendation.”15 If the final rule provides that such actions are investment advice under the Proposal, plan sponsors and retirement savers risk losing access to financial advisers and managed account services. We emphasize once again that any investment advisers or managed account providers that are engaged by a plan already accept fiduciary status for the fiduciary activities inherent in their services – meaning the plan and its participants are fully protected. G. The Department should clarify that investment advice does not include pricing valuations and informational reporting activities. Under the Proposal, investment advice could include “[a]n appraisal, fairness opinion, or similar statement whether verbal or written concerning the value of securities or other property if provided in connection with a specific transaction or transactions involving the acquisition, disposition, or exchange, or such securities or other property by the plan or IRA.”16 We understand that the Department’s primary concern behind this provision is a plan’s purchase or sale of nontraditional assets like real estate where the plan fiduciary receives, for example, an appraisal of the asset’s value. We support a definition of investment advice where such an appraisal of real estate or other nontraditional assets would be fiduciary in nature. We are concerned, however, that the term “transaction” will be interpreted broadly and that the Proposal would sweep in routine valuations that service providers perform for plans and retirement savers. EXAMPLE An individual who owns a traditional IRA annuity is considering whether to convert the IRA to a Roth IRA.

The owner asks the insurance company for the value of his annuity because he would like to estimate the tax consequences of a conversion. The amount 15 The requested change is needed because without it the implication will be that a service provider has to offer more than one option in order to be able to offer any of these “add-on” services. 16 Proposed rule, 29 C.F.R. § 2510.3-21(a)(1)(iii) (80 Fed.

Reg. 21,957). . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 15 of 32 of taxable income is based on the fair market value of the annuity on the date of conversion.17 The insurance company’s provision of the annuity valuation would be investment advice under the Proposal because a Roth conversion is a “transaction.” EXAMPLE A 401(k) service provider’s platform offers a mix of registered mutual funds, collective trusts, and separate accounts. Separate accounts, when offered, are investments similar to the mutual funds and collective trusts offered to 401(k) plans, but are designed for a plan large enough to justify separate account pricing; otherwise a separate account operates like a collective trust with just one plan investor. As is now standard in the market, the service provider offers asset reallocation on each business day. Accordingly, the service provider’s trust company affiliate “strikes” a daily net asset value (NAV) for collective trusts and separate accounts, using procedures similar to those used for registered mutual funds.

This NAV is reported daily by the service provider to plan fiduciaries and participants, and plan transactions are based on the NAV reported. While any asset values reported to the collective trust are covered by the carve-out, identical reporting to the separate account appears to be fiduciary in nature, increasing the cost of the separate account. In addition, the reporting of the NAV itself could be viewed as fiduciary investment advice. EXAMPLE A plan’s assets are invested in insurance company separate accounts.

The insurance company provides the plan’s fiduciaries with monthly asset valuations. The asset valuation reports are intended for informational purposes and are used by plan fiduciaries for benchmarking purposes. If the plan fiduciaries engage in a transaction that is connected to the asset valuation reports, then the insurance company would be treated as a fiduciary due to its provision of the informational reports. We request that the Department clarify that investment advice does not include pricing valuations and informational reporting activities such as those in the examples above.

We appreciate that the Department provided a carve-out in the Proposal to except certain valuations from being treated as investment advice, but the carve-out is too narrow to cover the valuations described above. As an alternative, the Department could broaden the financial reports and valuation carve-out to exempt these types of transactions from being treated as fiduciary in nature. Finally, while we appreciate and support the carve-out in section (b)(5)(ii) of the proposed regulation for appraisals, fairness opinions, or statement of values provided to an investment fund with multiple unaffiliated plan investors, we believe this carve-out should not be limited to 17 26 C.F.R. § 1.408A-4, Q&A-14. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 16 of 32 funds that hold the assets of more than one unaffiliated plan. Otherwise, there is an artificial incentive to pool plans together when the economics otherwise justify a separate account. These are significant and important issues. If the Department cannot address them fully, the Department should defer all valuation issues – not just ESOPs – to a separate rulemaking. H. Clarification is requested on the role and scope of what it means to be a “fiduciary” under the Proposal. As described above, the Proposal would expand the definition of the term “fiduciary” such that more persons would become subject to ERISA’s fiduciary standards than under the current regulations. At the same time, fiduciaries relying on BICE would be prohibited under BICE from disclaiming or otherwise limiting the investment advice fiduciary’s liability. Under current law, a fiduciary is generally only subject to fiduciary standards to the extent the fiduciary has authority and only during the time period while the fiduciary exercises its fiduciary obligation.

However, between the Proposal’s expansion of who is considered a fiduciary and BICE’s limitation on a fiduciary’s ability to limit its liability, we are unsure whether longstanding understandings of the scope of fiduciary status continue to apply. We therefore request that the Department confirm that its long-standing interpretations regarding the scope of fiduciary duties and fiduciaries’ ability to allocate those duties continue to apply under the Proposal. We recommend the following clarifications:18 • If a person becomes a fiduciary because of a recommendation, fiduciary status relates only with respect to the recommendation triggering fiduciary status, and not for any other past, present, or future communications that do not meet the test for fiduciary status. • Fiduciary status does not automatically require a duty to monitor the advice provided, unless the fiduciary investment adviser is so engaged and agrees to ongoing monitoring. • Fiduciary status due to the provision of investment advice only applies to the individual(s) meeting the definition of fiduciary and does not create fiduciary status for an individual’s employer unless that employer affirmatively accepts fiduciary status. For example, inadvertent fiduciary status arising from a call center employee who crosses the line from education to advice does not result in the call center employee’s employer being treated as an investment advice fiduciary. 18 In a related matter, we appreciate the Department’s comments in the preamble that the Proposal clarifies that attorneys, accountants, and actuaries would not be treated as fiduciaries merely because they provide certain professional assistance to a plan in connection with a particular investment transaction, and we agree that this is the correct result.

However, the Proposal’s proposed amendments to 29 C.F.R. § 2510.3-21 do not appear to make this clarification. We recommend that the Department incorporate the intended clarification on this matter in the final rule. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 17 of 32 • The BICE’s prohibition on disclaimers and liability limits does not prohibit a fiduciary from limiting the scope of the advice that will be given. For example, a fiduciary relying on BICE could limit its advice to one particular investment, one asset class, or to a single recommendation. • If a person provides investment advice, but the recipient does not act reasonably promptly on that advice, both fiduciary status and the requirements of the BICE end. • The Department should clarify that, due to the inadvertent fiduciaries that will be created by the Proposal, the Proposal will not require every fiduciary associated with the plan to continually monitor all others to avoid co-fiduciary liability under ERISA section 405. (The Department also needs to ensure that its economic analysis takes into account the costs of co-fiduciary liability, including the cost of insurance, because of the vast number of new fiduciaries that will be created.) The Department has addressed these questions to some extent in section (c) of the Proposal, but section (c) appears to relate only to particular assets and not the scope and timing of fiduciary obligations. We think all of these clarifications are simply expressions of ERISA’s rule that a fiduciary’s duties apply only “to the extent” of the fiduciary’s discretion or authority.

The Department should clarify these duties. III. Carve-Outs – Investment Advice (Proposed Rule 29 C.F.R. § 2510.3-21(b)) Under the Proposal, 29 C.F.R. § 2510.3-21(b) provides several carve-outs under which the rendering of advice or other communications in conformance with one of the carve-outs will not cause the person who renders the advice to be treated as an investment advice fiduciary.19 The general categories of carve-outs offered under the Proposal consist of (1) counterparties to the plan (i.e., a “seller’s carve-out”), (2) employees of the plan sponsor, (3) platform providers, (4) selection and monitoring assistance, (5) financial reports and valuations, and (6) investment education.

Our comments and suggestions regarding the carve-outs are set forth below. A. The proposed investment education carve-out’s narrowing of what constitutes investment education will cause service providers to cease providing several forms of helpful support and information to plan sponsors, participants, and IRA owners. EXAMPLE One SPARK Institute member, a major provider of defined contribution services, estimates it processes over 2.1 million calls per year regarding asset allocation issues, loans, distributions, enrollments, or rollovers. The member estimates that the Proposal would affect approximately 30% of these calls, meaning less information would be provided during nearly 1/3 of the calls the member handles. Another SPARK Institute 19 If a person represents or acknowledges that he or she is acting as an ERISA fiduciary with respect to the investment advice provided, then the carve-outs do not apply. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 18 of 32 member, also a major provider of defined contribution services, estimates that it processes over 2.3 million such calls and that the Proposal would potentially affect approximately 55% of these calls. 1. References to specific investments Under the Proposal’s investment education carve-out, the ability to mention a specific investment available under a plan or IRA would be severely curtailed. The proposed carve-out provides that the following information and materials would not constitute investment education and could therefore subject the provider of the information to fiduciary treatment: (1) plan information that references the appropriateness of an individual investment alternative; (2) general financial, investment, and retirement information that addresses specific investment products available; and (3) asset allocation models that include or even identify any specific investment product or specific alternative available under the plan or IRA. This is a significant narrowing of the Department’s Interpretive Bulletin 96-1 (“IB 96-1”),20 which is one of the Department’s most successful pieces of guidance. The SPARK Institute’s members are very concerned about their inability under the Proposal to continue many beneficial forms of communication to plan sponsors and retirement savers without crossing the line into providing investment advice. This concern is especially acute in the context of participants in self-directed plans and the service provider’s ability to provide information critical to participants’ ability to make decisions with respect to their investments. IB 96-1 currently permits the use of asset allocation models that reference specific investments available under the plan or IRA as long as the model is accompanied by the specified disclosure statement.

The Department expressed concern in the Proposal that the ability to refer to specific investments in an asset allocation model can be used to “steer recipients to particular investments” without adequate protections against abuse. The Department provided no evidence, however, that IB 96-1 is being used inappropriately today. As discussed below, IB 961 is working particularly well within asset allocation models and other education provided to participants where the plan fiduciary has already selected the menu of investments from which participants may choose.

The mere mention of a fund that has been selected by the plan fiduciary should not be a fiduciary act. Within the parameters of IB 96-1 as it exists today, service providers are able to provide very helpful information to retirement savers in the form of asset allocation models, educational documents, and interactive online tools that include references to the specific investment options available under the plan or IRA. This factual information serves a critical role in helping such individuals connect the dots between general investing principles and understanding which specific investments may be used to put that information into play for their particular situations. Without this information readily available, all but the most sophisticated retirement savers will be challenged in knowing how to select from what may be dozens or hundreds of investment options made available to them. As described below, in many instances, other materials such as 20 29 C.F.R.

§ 2509.96-1. . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 19 of 32 a comparative chart or other fund materials will identify each available investment option by asset class. It would be extremely burdensome for retirement savers to have to refer to those materials versus simply being provided with a list of some or all of the available funds by asset allocation in a tool. Unfortunately, difficulties such as this are one of the primary reasons why many individuals are not engaged and may not even participate in a plan for which they are eligible. The Proposal will make it very difficult for employers or their service providers to provide any meaningful investment tools to perform the same function of helping individuals connect the dots that asset allocation model tools may perform today. EXAMPLE A plan offers an interactive web tool that allows a participant to enter general information about her age and risk tolerance and then generates an asset allocation model based on generally accepted investment theories.

The tool follows the requirements of IB 96-1. Where an asset class is represented among the plan’s investments, the tool references one or more of the investments within that particular asset class. The tool is designed to make it very easy for the participant to move from education to implement the education provided.

If this is now considered a fiduciary act, that information will likely no longer be provided. Even if a service provider is careful not to recommend particular investments, the Department’s rules require that there be no recommendations “standing alone or in combination with other materials.” This makes it difficult to provide effective information to participants at the time it may be most needed without triggering fiduciary status. EXAMPLE The enrollment packet for a 401(k) plan provides basic asset allocation models to help educate a participant about the value of proper asset allocation. The materials include three pie charts that might be appropriate for a “conservative,” “moderate,” or “aggressive” investor, referencing particular asset classes. As required by Department rules, the same enrollment packet includes the fee and investment disclosure,21 which identifies each investment by its asset class.

The educational materials “in conjunction with” the required fee and investment disclosure appear to make a recommendation as to a specific investment. Separating the items to avoid fiduciary entanglements may result in higher printing and mailing costs that would likely be passed along to plan participants. We believe that IB 96-1, with the helpful additions in the Proposal regarding distribution education, should be retained in its entirety. IB 96-1 in its current form is working well and appropriately balances the need to reference specific investment option information to retirement savers without such information automatically being found to be investment advice.

This is particularly true for service providers providing asset allocation models and other education to 21 29 C.F.R. § 2550.404a-5. . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 20 of 32 participants where the plan fiduciary has already selected the menu of investments from which the participants may choose. Further, many asset allocation tools currently in use allow the plan fiduciary to select the investment used within the standard model(s) in place for its participants. In these situations there is no evidence that service providers are abusing IB 96-1 as a subterfuge for selling a particular investment. The service provider is simply educating participants on, or applying the plan fiduciary-selected investments to, each category and making it easier for participants to implement the education. IB 96-1 provides plan fiduciaries valuable protections that should be retained and should continue to allow them to direct the use of these asset allocation tools by their hired service providers, without assuming additional fiduciary liability for themselves as a provider of investment advice or assigning fiduciary status to the provider of the tools. The Proposal’s restrictions on the ability for service providers to mention a specific investment option without such communication crossing the line into investment advice seem to create a conflict with the requirements that regulatory notices discussing specific investments be provided in certain situations.

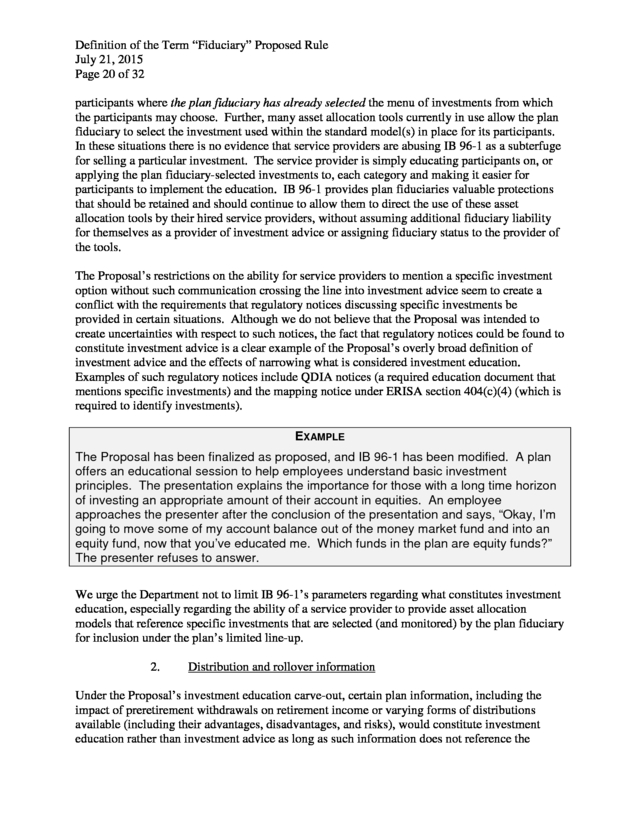

Although we do not believe that the Proposal was intended to create uncertainties with respect to such notices, the fact that regulatory notices could be found to constitute investment advice is a clear example of the Proposal’s overly broad definition of investment advice and the effects of narrowing what is considered investment education. Examples of such regulatory notices include QDIA notices (a required education document that mentions specific investments) and the mapping notice under ERISA section 404(c)(4) (which is required to identify investments). EXAMPLE The Proposal has been finalized as proposed, and IB 96-1 has been modified. A plan offers an educational session to help employees understand basic investment principles. The presentation explains the importance for those with a long time horizon of investing an appropriate amount of their account in equities.

An employee approaches the presenter after the conclusion of the presentation and says, “Okay, I’m going to move some of my account balance out of the money market fund and into an equity fund, now that you’ve educated me. Which funds in the plan are equity funds?” The presenter refuses to answer. We urge the Department not to limit IB 96-1’s parameters regarding what constitutes investment education, especially regarding the ability of a service provider to provide asset allocation models that reference specific investments that are selected (and monitored) by the plan fiduciary for inclusion under the plan’s limited line-up. 2. Distribution and rollover information Under the Proposal’s investment education carve-out, certain plan information, including the impact of preretirement withdrawals on retirement income or varying forms of distributions available (including their advantages, disadvantages, and risks), would constitute investment education rather than investment advice as long as such information does not reference the . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 21 of 32 “appropriateness” of any individual benefit distribution option for the plan, IRA, or retirement saver. Our members are very concerned about their ability to determine the difference between providing information on the advantages, disadvantages, and risks of the distribution options available to a person (including rollover options), which would fit within the carve-out, and information on the appropriateness of such distribution options, which would disqualify the information from fitting within the carve-out. Consideration of the advantages and disadvantages of a particular course of action leads to a determination of the appropriateness of such action, making it difficult to understand why the carve-out would be available to information regarding the former but not the latter. Even if our members could find comfort in understanding what the difference is, they would be further challenged by having to train hundreds or thousands of call center employees on where the line is and hope that a front-line employee does not inadvertently cross the line into providing investment advice. Without a clear line that can be easily communicated and implemented with respect to all service provider employees that interact with retirement savers, our members will have little choice but to cease providing helpful information to retirement savers regarding distributions and rollovers. This response by service providers will ultimately harm participants and IRA owners who will no longer receive this very beneficial information and, as a result, may withdraw money or choose a distribution form that will harm their retirement outcome simply because they were unaware of its implications and/or of other options that were available to them. EXAMPLE A participant who is terminating employment calls the plan’s call center to discuss her options.

The plan includes the right to elect an annuity distribution. The participant says “I really want to have guaranteed income for my life, so what would be good for me?” The call center representative has been trained to only discuss the “pros” and “cons” of the annuity distribution, but the list of “pros” has five items (including the availability of guaranteed income) and the “cons” has only two items. The representative also explains to the participant how the specific annuity works, and the features of any riders attached to the annuity that provide unique benefits.

The participant ends the call with the impression that the conversation is a suggestion to elect the annuity. This call center interaction presents a problem because it is unclear whether the “pros” and “cons” would be considered advantages and disadvantages of electing an annuity distribution, or a discussion concerning the “appropriateness” of doing so. The availability of the investment education carve-out depends on which side of the line this conversation falls. EXAMPLE A participant who is terminating employment calls the plan’s call center to discuss her options.

The call center employee has been trained to help a participant understand the . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 22 of 32 downsides of taking a distribution and not rolling it over, including the significant tax penalty and loss of future retirement income. The call center employee has also been trained not to appear to favor leaving the money in the plan versus conducting an IRA rollover. Similar to the example above, it is unclear whether the call center employee is covered by the investment education carve-out because the Proposal does not explain the difference between “disadvantages” and “appropriateness” in this situation. Retirement savers’ decisions regarding whether to take a distribution from a plan or IRA and the form of distribution to take are some of the most critical decisions that such individuals can make. While the current Proposal allows a discussion of the “advantages, disadvantages, and risk” of various forms of distribution, the Proposal also prohibits information or materials that address “distribution options available” to participants and prohibits any information regarding the “appropriateness” of any distribution option (including any discussion of the appropriateness of not taking a distribution).22 This suggests that an educational program or a call center representative can discuss the pros and cons of theoretical distribution options but not the pros and cons of the actual distribution options available in the plan.

For many participants without access to this information elsewhere, especially those with lower incomes who could not afford, or would choose not to spend money, to procure this general information via advisory fees, the ability to receive necessary information regarding distribution options from their plan’s service provider is especially beneficial. We also feel strongly that is it unreasonable to believe that terminated employees will simply leave their money in a former employer’s plan, absent solid information regarding their options. There are often many reasons that terminated employees want to fully disconnect from a former employer, and we believe the more likely result of the Proposal will be increased leakage from retirement plans and IRAs. The ability to provide accurate and helpful information on distribution options is critical.

The term “investment advice” refers to counseling a participant regarding the investment of his or her plan account (e.g., recommending a specific asset allocation among funds available in the plan). Discussion of specific plan distribution options, designated investment alternative information required under Regulation § 2550.404a-5, and general information and materials regarding specific alternatives or services available outside the plan is not investment advice. Rather, a discussion of such features and options available to a participant serves to educate a participant about his or her rights under his or her particular plan and federal law. For example, Texas has recently experienced significant destruction due to flooding. As a result, President Obama declared much of Texas a national disaster zone.

This declaration is significant for retirement plan purposes because it allows participants to make expedited loan and hardship distribution requests. If a plan provider representative speaks with a participant to discuss whether he or she can take a hardship distribution under the terms of the plan, that discussion is not, and should not be, “investment advice” under any reasonable reading of ERISA section 22 In fact, many notices actually required by the Code could be said to reflect the “appropriateness” of particular distribution options. This includes the notice that describes the consequences of a failure to defer a distribution under Code section 411(a)(11) and the relative value notices required by the regulations under Code section 417. See Proposed Regulations, 73 Fed.

Reg. 59,575 (Oct. 9, 2008); 26 C.F.R.

§ 1.417(a)(3)-1(c). . Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 23 of 32 3(21)(A)(ii). Rather, the discussion is informing the participant on how he or she can access money desperately needed to address a significant hardship event. Further, rendering a service provider unable to present this level of information to participants will effectively drive employees to their employers for answers, increasing the overall burden on plan sponsors of offering plans. Accordingly, we urge the Department to provide that factual conversations concerning distribution options (including rollovers) would not be considered investment advice, including conversations regarding the pros and cons of a specific product or option.23 B. The seller’s carve-out should be extended to plans of all sizes. Under the Proposal, a carve-out would be available for a counterparty that transacts with a plan fiduciary of a large plan (i.e., the “seller’s carve-out”). However, this carve-out is not available to small plans, IRA owners, and plan participants and beneficiaries, due to the carve-out’s requirement that the counterparty either obtain a written disclosure from the plan fiduciary that the plan has at least 100 participants, or that the counterparty reasonably believes that the plan fiduciary has responsibility for managing at least $100 million in plan assets. The Department explains in the Proposal that the overall purpose of the seller’s carve-out is to avoid imposing ERISA fiduciary obligations on sales pitches where plans do not expect a relationship of undivided loyalty or trust.

In certain situations, the buyer is said to understand that it is buying an investment product rather than advice, and the seller’s invitation to buy a product is not understood to be a recommendation. In a change from the Department’s previous proposal to redefine the term “fiduciary” in 2010, the Department in its new proposal decided that the seller’s carve-out should not cover recommendations to retail investors. The Department states that “[m]ost retail investors and many small plan sponsors are not financial experts, are unaware of the magnitude and impact of conflicts of interest, and are unable effectively to assess the quality of the advice they receive.”24 The Department requested comments on whether the plan size limitation of 100 plan participants or the $100 million plan asset requirement are appropriate conditions.

In response, we strongly urge the Department – at a minimum – to extend the seller’s carve-out to all plan fiduciaries, regardless of plan size.25 The consequences of not doing so will mean that small plans do not receive the guidance they need concerning products and services available to them. This result would very likely discourage small employers with fewer than 100 employees – who employed 23 For example, we recommend that the Department remove the words “or any individual benefit distribution option” from the first sentence of proposed rule 29 C.F.R. § 2510.3-21(b)(6)(i). 24 25 80 Fed.

Reg. 21,942. In addition, if the Department retains the 100 participant threshold, we request that the Department confirm that the participant count used to determine whether a plan has more than 100 participants is determined via the aggregation of all plans sponsored by the employer and its affiliates. An employer with three plans of 90 participants each is functionally similar to an employer with one plan containing 270 participants. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 24 of 32 nearly 40 million people, or more than 30% of all employees, in 201226 – from offering or maintaining a plan for their employees. Multiple SPARK Institute members who are major providers of defined contribution services reported that more than 80% of the plans to which they provide services have fewer than 100 participants. Unless the Department addresses this critical problem by expanding the seller’s carve-out (and making the other changes we recommend), many plan fiduciaries will simply lose access to any assistance. Although we understand the Department’s comments that small plan fiduciaries may not have the extensive investment expertise that large plan fiduciaries have, in the context of the seller’s carve-out, the only question is whether the fiduciary is knowledgeable enough to know the difference between someone who is selling a product to the plan and someone who is undertaking to provide impartial investment advice. Extensive investment expertise is not required to make this determination.

Owners of small businesses routinely deal in the marketplace and routinely deal with vendors of all kinds. A business owner can make independent judgments of this nature and does so all the time.27 If the service provider cannot provide any guidance to the plan sponsor, that means every plan must hire and pay an independent adviser at additional cost. According to one SPARK Institute member, only about 1/3 of plans under 100 participants have an independent adviser.28 ERISA already requires all plan fiduciaries to be knowledgeable and sophisticated enough to act prudently when dealing with vendors.

ERISA does not distinguish between fiduciaries of small and large plans – all fiduciaries are held to the same fiduciary standards. The seller’s carve-out would already require several conditions that we believe would provide adequate protection for small plans. For example, under (b)(1)(i)(B), the counterparty would be required to inform the plan fiduciary of the existence and nature of the person’s financial interests in the transaction. Also, as proposed, the counterparty must know or reasonably believe that the independent plan fiduciary has sufficient expertise to evaluate the transaction and determine whether the transaction is prudent and in the best interest of plan participants.

If the counterparty has reason to believe that the plan fiduciary does not have such sufficient expertise, then the seller’s carve-out would not be available to that plan, regardless of the size of the plan. If the Department is not comfortable that these protections are enough with respect to transactions involving small plans, then we suggest that the Department consider introducing a requirement for a standard, easy-to-read disclaimer that would be provided to small plan 26 ANTHONY CARUSO, U.S. CENSUS BUREAU, STATISTICS OF U.S. BUSINESSES EMPLOYMENT AND PAYROLL SUMMARY: 2012 at 1 (released Feb.

2015). 27 The Department cites various studies purporting to show that individual investors may have difficulty distinguishing different kinds of financial professionals. Even if these studies are analogous to the ERISA fiduciary question in the IRA context, the Department neither cites data, nor provides any substantive proof or analysis, that suggests small business owners are incapable of distinguishing a sales pitch from fiduciary investment advice. 28 Other members report that a majority of plans, but certainly not all, have an intermediary. This is more common with insurance and investment managers that generally sell through intermediaries. .

Definition of the Term “Fiduciary” Proposed Rule July 21, 2015 Page 25 of 32 fiduciaries within the seller’s carve-out. By offering guidelines for the wording, font size, placement, and the manner and timing of its delivery, we believe that the Department could address its current concerns over loopholes in which boilerplate disclaimers can be used to escape fiduciary status. Another reason to support an expansion of the proposed seller’s carve-out is the relatively new 408(b)(2) disclosure requirement for service providers. With the 408(b)(2) disclosure rules now in place, plan sponsors receive very detailed information including the financial interests of their service provider. Much of this information is repetitive to what would be required under the seller’s carve-out.

Many of the concerns the Department heard over the seller’s carve-out in the 2010 proposal have been addressed through the information now required to be included in the 408(b)(2) disclosures. In this regard, we suggest that one alternative the Department might consider is making the seller’s carve-out available to small plans in each instance where the resulting transaction between a counterparty and the small plan would result (or has already resulted) in the provision of 408(b)(2) disclosures on the subject(s) of the transaction. We have two final comments on the seller’s carve-out. First, our members expressed concern about needing to “know[ ] or reasonably believe[ ]” that a fiduciary has a certain level of expertise – a standard that invites frivolous litigation.