Description

How We Rate Insurers

Criteria Officers:

Emmanuel Dubois-Pelerin, Global Criteria Officer, Financial Services, Paris (33) 1-4420-6673;

emmanuel.dubois-pelerin@standardandpoors.com

Michelle Brennan, EMEA Financial Services Criteria Officer, London (44) 20-7176-7205;

michelle.brennan@standardandpoors.com

Primary Credit Analysts:

Rodney A Clark, FSA, New York (1) 212-438-7245; rodney.clark@standardandpoors.com

Rob C Jones, London (44) 20-7176-7041; rob.jones@standardandpoors.com

Michael J Vine, Melbourne (61) 3-9631-2102; michael.vine@standardandpoors.com

Angelica G Bala, Mexico City (52) 55-5081-4405; angelica.bala@standardandpoors.com

Mark Button, London (44) 20-7176-7045; mark.button@standardandpoors.com

Table Of Contents

Business Risk Profile

Financial Risk Profile

Other Assessments Or "Modifiers"

Support Framework

The ICR and FSR

Related Criteria

Related Research

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

APRIL 3, 2014 1

1289949 | 300000294

. How We Rate Insurers

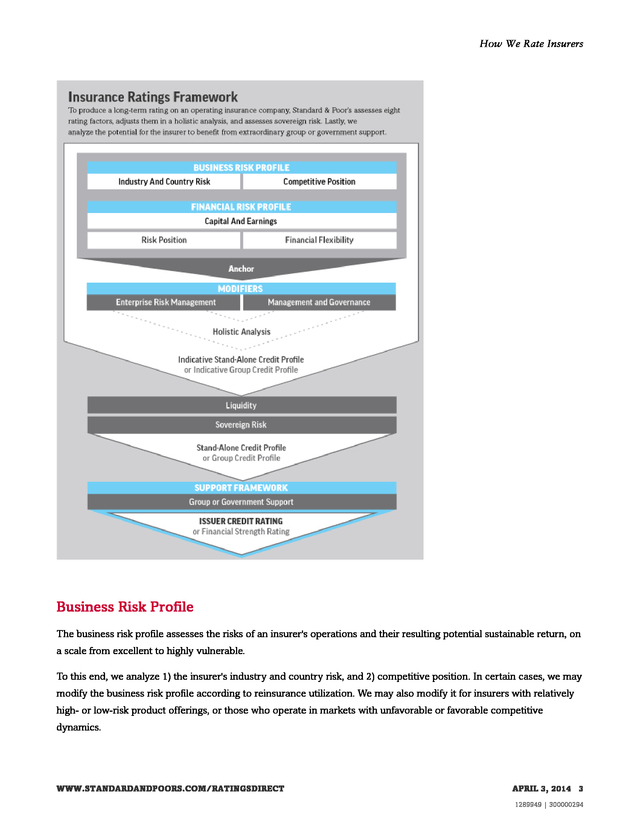

Here, Standard & Poor's Ratings Services provides a step-by-step summary of how we use our insurance criteria to

produce an issuer credit rating or a financial strength rating (ICR or FSR). (See chart 1 below.)

First, using reported data and our own metrics, we evaluate an insurer's business risk profile and financial risk profile.

For the business risk profile, we undertake a detailed analysis of industry and country risk, and competitive position.

For the financial risk profile, we examine capital and earnings, risk position, and financial flexibility.

Jointly, these two profiles provide the "anchor" to our rating. We then add our assessments of the insurer's enterprise

risk management, and management and governance, as well as what we call a "holistic analysis" of its performance.

This results in an "indicative stand-alone credit profile" for a company or "indicative group credit profile" for an

insurance group.

Next we look at the company's liquidity, and then whether it can be rated above the relevant sovereign or sovereigns.

At this point, we assign a stand-alone credit profile (SACP) or group credit profile (GCP). This gives our view about the

intrinsic creditworthiness of the company or group.

If we believe the insurer faces a present risk of default, the SACP or GCP is set according to separate criteria (see Related Criteria section). Finally, we assess the likelihood of group or government support for the company, and assign an ICR or FSR. The criteria apply to all our global insurance ratings in the life, health, property/casualty (also called non-life), and reinsurance sectors. The criteria do not apply to ratings on bond insurers, insurance brokers, and mortgage and title insurers. For More Information This article provides a summary of each key stage of our insurance criteria methodology.

For a comprehensive understanding of our approach, please refer to the articles and resources in the Related Criteria and Related Research sections at the end of this article. Our methodology is forward-looking. The metrics we use are projections for the current and upcoming two years. These projections take into account the insurer's past five years of performance, unless otherwise stated. In addition, they take into consideration developments since the company's most recent release of information, its strategy, our expectations about its operating environment, and our expectation of negative or positive developments such as planned dividends or repayments of existing debt. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 2 1289949 | 300000294 .

How We Rate Insurers Business Risk Profile The business risk profile assesses the risks of an insurer's operations and their resulting potential sustainable return, on a scale from excellent to highly vulnerable. To this end, we analyze 1) the insurer's industry and country risk, and 2) competitive position. In certain cases, we may modify the business risk profile according to reinsurance utilization. We may also modify it for insurers with relatively high- or low-risk product offerings, or those who operate in markets with unfavorable or favorable competitive dynamics. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 3 1289949 | 300000294 . How We Rate Insurers 1. Industry and country risk We use nine subfactors to analyze the risks typically faced by insurers operating in specific industries and countries, and this is generally determined at a country or regional level, e.g. the Canadian P/C sector, the Australian health sector, and the Japanese life sector. We also analyze industry and country risk on a global basis for four specific sectors: P/C reinsurance, life reinsurance, trade credit insurance, and marine protection and indemnity sectors. The five industry risk subfactors are: return on equity, product risk, barriers to entry, market growth prospects, and institutional framework.

The four country risk subfactors are: economic risk, political risk, financial system risk, and payment culture and the rule of law. 2. Competitive position We assess an insurer's competitive position using six subfactors: operating performance, differentiation of brand or reputation, market position, the level of distribution channels, geographic diversification, and other types of diversification such as additional business lines or product types. Financial Risk Profile The financial risk profile assesses decisions management has made about capital and earnings, risk position, and financial flexibility. The assessment may be limited by our view of "total asset quality." 1.

Capital and earnings Capital and earnings measures an insurer's ability to absorb losses by assessing capital adequacy. This compares currently available capital resources with a company's ability and willingness to build capital through net retained earnings. 2. Risk position We assess risk position by analyzing five subfactors: exposure to employee benefits, foreign exchange risk exposure, investment leverage, investment portfolio diversification, and additional sources of capital and earnings volatility. 3.

Financial flexibility We use three subfactors to assess financial flexibility: access to sources of external capital and liquidity, financial leverage, and fixed-charge coverage. Other Assessments Or "Modifiers" The criteria use additional assessments that may modify the ratings: 1) enterprise risk management (ERM) and management and governance, 2) holistic analysis, 3) liquidity, and 4) rating above the sovereign. 1. ERM and management and governance ERM and management and governance combine into a single assessment ranging from very strong to weak. ERM examines whether risk management practices are executed in a way that is systematic, consistent, and strategic, to minimize the impact of risk on a company's capital and earnings. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 4 1289949 | 300000294 . How We Rate Insurers Management and governance addresses how management's strategic competence, operational effectiveness, and financial management and governance practices shape the insurer's competitiveness in the marketplace. 2. Holistic analysis Our holistic analysis recognizes sustained, predictable operating and financial underperformance or outperformance compared to peers. The peers of an insurance company generally comprise those in the same country and sector. 3. Liquidity The liquidity analysis centers on an insurer's ability to cover its liquidity needs, including under moderately stressful market and economic conditions.

The analysis is absolute, rather than relative to peers. 4. Rating above the sovereign The criteria may result in a domestic, unsupported insurer having an SACP or GCP--and potentially a rating--above the sovereign rating in the jurisdiction where the company has most of its business (see Related Criteria). In these cases, the criteria typically subject the SACP or GCP to a capital and liquidity test which, if failed, caps the insurer at the sovereign rating level. In rating an insurer above the sovereign, Standard & Poor's believes that the company's willingness and ability to service debt is superior to the sovereign's and that, ultimately, if the sovereign defaults, there is a measurable probability that the insurance company would not default. Support Framework To set the ICR, we combine our views about the SACP or GCP with our opinion about the possibility of extraordinary support coming from the wider group or related government.

We use our separate support framework criteria to determine how many notches of uplift (or, in some cases, negative adjustment) we apply, if any, for support. Only this step, or the application of our holistic analysis, may lead to an 'AAA' rating on an insurer. The ICR and FSR The FSR, if any, equals the ICR. That's unless policyholder obligations, and not other financial obligations, are supported by a more creditworthy counterparty.

A holding company rating is assigned by notching down from the group's GCP, typically by a maximum of three notches, unless we determine a present risk of default (see "Group Rating Methodology"). Related Criteria • • • • • Ratings Above The Sovereign--Corporate And Government Ratings: Methodology And Assumptions, Nov. 19, 2013 Group Rating Methodology, Nov. 19, 2013 Insurers: Rating Methodology, May 7, 2013 Enterprise Risk Management, May 7, 2013 Methodology For Linking Short-Term And Long-Term Ratings For Corporate, Insurance, And Sovereign Issuers, May 7, 2013 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 5 1289949 | 300000294 .

How We Rate Insurers • • • • • Management And Governance Credit Factors For Corporate Entities And Insurers, Nov. 13, 2012 Criteria For Assigning 'CCC+', 'CCC', 'CCC-', And 'CC' Ratings, Oct. 1, 2012 Stand-Alone Credit Profiles: One Component Of A Rating, Oct. 1, 2010 Credit Stability Criteria, May 3, 2010 Understanding Standard & Poor's Rating Definitions, June 3, 2009 Related Research • • • • Credit FAQ: Standard & Poor's Criteria Process, Dec.

31, 2013 What May Cause Insurance Companies To Fail--And How This Influences Our Criteria, June 13, 2013 2012 Annual Global Corporate Default Study And Rating Transitions, March 18, 2013 The Time Dimension Of Standard & Poor's Credit Ratings, Sept. 22, 2010 More reports and videos about the insurance criteria are available at: www.standardandpoors.com/insurancecriteria and on RatingsDirect. Under Standard & Poor's policies, only a Rating Committee can determine a Credit Rating Action (including a Credit Rating change, affirmation or withdrawal, Rating Outlook change, or CreditWatch action). This commentary and its subject matter have not been the subject of Rating Committee action and should not be interpreted as a change to, or affirmation of, a Credit Rating or Rating Outlook. Additional Contact: Insurance Ratings Europe; InsuranceInteractive_Europe@standardandpoors.com WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 6 1289949 | 300000294 .

Copyright © 2015 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content.

S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION.

In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format.

The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion.

S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors.

S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 7 1289949 | 300000294 .

If we believe the insurer faces a present risk of default, the SACP or GCP is set according to separate criteria (see Related Criteria section). Finally, we assess the likelihood of group or government support for the company, and assign an ICR or FSR. The criteria apply to all our global insurance ratings in the life, health, property/casualty (also called non-life), and reinsurance sectors. The criteria do not apply to ratings on bond insurers, insurance brokers, and mortgage and title insurers. For More Information This article provides a summary of each key stage of our insurance criteria methodology.

For a comprehensive understanding of our approach, please refer to the articles and resources in the Related Criteria and Related Research sections at the end of this article. Our methodology is forward-looking. The metrics we use are projections for the current and upcoming two years. These projections take into account the insurer's past five years of performance, unless otherwise stated. In addition, they take into consideration developments since the company's most recent release of information, its strategy, our expectations about its operating environment, and our expectation of negative or positive developments such as planned dividends or repayments of existing debt. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 2 1289949 | 300000294 .

How We Rate Insurers Business Risk Profile The business risk profile assesses the risks of an insurer's operations and their resulting potential sustainable return, on a scale from excellent to highly vulnerable. To this end, we analyze 1) the insurer's industry and country risk, and 2) competitive position. In certain cases, we may modify the business risk profile according to reinsurance utilization. We may also modify it for insurers with relatively high- or low-risk product offerings, or those who operate in markets with unfavorable or favorable competitive dynamics. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 3 1289949 | 300000294 . How We Rate Insurers 1. Industry and country risk We use nine subfactors to analyze the risks typically faced by insurers operating in specific industries and countries, and this is generally determined at a country or regional level, e.g. the Canadian P/C sector, the Australian health sector, and the Japanese life sector. We also analyze industry and country risk on a global basis for four specific sectors: P/C reinsurance, life reinsurance, trade credit insurance, and marine protection and indemnity sectors. The five industry risk subfactors are: return on equity, product risk, barriers to entry, market growth prospects, and institutional framework.

The four country risk subfactors are: economic risk, political risk, financial system risk, and payment culture and the rule of law. 2. Competitive position We assess an insurer's competitive position using six subfactors: operating performance, differentiation of brand or reputation, market position, the level of distribution channels, geographic diversification, and other types of diversification such as additional business lines or product types. Financial Risk Profile The financial risk profile assesses decisions management has made about capital and earnings, risk position, and financial flexibility. The assessment may be limited by our view of "total asset quality." 1.

Capital and earnings Capital and earnings measures an insurer's ability to absorb losses by assessing capital adequacy. This compares currently available capital resources with a company's ability and willingness to build capital through net retained earnings. 2. Risk position We assess risk position by analyzing five subfactors: exposure to employee benefits, foreign exchange risk exposure, investment leverage, investment portfolio diversification, and additional sources of capital and earnings volatility. 3.

Financial flexibility We use three subfactors to assess financial flexibility: access to sources of external capital and liquidity, financial leverage, and fixed-charge coverage. Other Assessments Or "Modifiers" The criteria use additional assessments that may modify the ratings: 1) enterprise risk management (ERM) and management and governance, 2) holistic analysis, 3) liquidity, and 4) rating above the sovereign. 1. ERM and management and governance ERM and management and governance combine into a single assessment ranging from very strong to weak. ERM examines whether risk management practices are executed in a way that is systematic, consistent, and strategic, to minimize the impact of risk on a company's capital and earnings. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 4 1289949 | 300000294 . How We Rate Insurers Management and governance addresses how management's strategic competence, operational effectiveness, and financial management and governance practices shape the insurer's competitiveness in the marketplace. 2. Holistic analysis Our holistic analysis recognizes sustained, predictable operating and financial underperformance or outperformance compared to peers. The peers of an insurance company generally comprise those in the same country and sector. 3. Liquidity The liquidity analysis centers on an insurer's ability to cover its liquidity needs, including under moderately stressful market and economic conditions.

The analysis is absolute, rather than relative to peers. 4. Rating above the sovereign The criteria may result in a domestic, unsupported insurer having an SACP or GCP--and potentially a rating--above the sovereign rating in the jurisdiction where the company has most of its business (see Related Criteria). In these cases, the criteria typically subject the SACP or GCP to a capital and liquidity test which, if failed, caps the insurer at the sovereign rating level. In rating an insurer above the sovereign, Standard & Poor's believes that the company's willingness and ability to service debt is superior to the sovereign's and that, ultimately, if the sovereign defaults, there is a measurable probability that the insurance company would not default. Support Framework To set the ICR, we combine our views about the SACP or GCP with our opinion about the possibility of extraordinary support coming from the wider group or related government.

We use our separate support framework criteria to determine how many notches of uplift (or, in some cases, negative adjustment) we apply, if any, for support. Only this step, or the application of our holistic analysis, may lead to an 'AAA' rating on an insurer. The ICR and FSR The FSR, if any, equals the ICR. That's unless policyholder obligations, and not other financial obligations, are supported by a more creditworthy counterparty.

A holding company rating is assigned by notching down from the group's GCP, typically by a maximum of three notches, unless we determine a present risk of default (see "Group Rating Methodology"). Related Criteria • • • • • Ratings Above The Sovereign--Corporate And Government Ratings: Methodology And Assumptions, Nov. 19, 2013 Group Rating Methodology, Nov. 19, 2013 Insurers: Rating Methodology, May 7, 2013 Enterprise Risk Management, May 7, 2013 Methodology For Linking Short-Term And Long-Term Ratings For Corporate, Insurance, And Sovereign Issuers, May 7, 2013 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 5 1289949 | 300000294 .

How We Rate Insurers • • • • • Management And Governance Credit Factors For Corporate Entities And Insurers, Nov. 13, 2012 Criteria For Assigning 'CCC+', 'CCC', 'CCC-', And 'CC' Ratings, Oct. 1, 2012 Stand-Alone Credit Profiles: One Component Of A Rating, Oct. 1, 2010 Credit Stability Criteria, May 3, 2010 Understanding Standard & Poor's Rating Definitions, June 3, 2009 Related Research • • • • Credit FAQ: Standard & Poor's Criteria Process, Dec.

31, 2013 What May Cause Insurance Companies To Fail--And How This Influences Our Criteria, June 13, 2013 2012 Annual Global Corporate Default Study And Rating Transitions, March 18, 2013 The Time Dimension Of Standard & Poor's Credit Ratings, Sept. 22, 2010 More reports and videos about the insurance criteria are available at: www.standardandpoors.com/insurancecriteria and on RatingsDirect. Under Standard & Poor's policies, only a Rating Committee can determine a Credit Rating Action (including a Credit Rating change, affirmation or withdrawal, Rating Outlook change, or CreditWatch action). This commentary and its subject matter have not been the subject of Rating Committee action and should not be interpreted as a change to, or affirmation of, a Credit Rating or Rating Outlook. Additional Contact: Insurance Ratings Europe; InsuranceInteractive_Europe@standardandpoors.com WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 6 1289949 | 300000294 .

Copyright © 2015 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content.

S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION.

In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format.

The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion.

S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors.

S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 3, 2014 7 1289949 | 300000294 .