Beyond Bitcoin: Blockchain The Essential Building Block in Designing the Future – May 11, 2016 - ( White Paper )

Reed Smith

Description

IP, Information & Innovation

White Paper

Beyond Bitcoin: Blockchain

The Essential Building Block in Designing the Future

. Contents

The Mysterious Origins of Bitcoin

1

Bitcoin 101 – A Primer

2

The Blockchain

2

A Bitcoin Transaction

3

Summary

3

Blockchain 101

4

How It Works

4

Advantages of Blockchain

5

Disadvantages of Blockchain

5

Summary

6

U.S. Regulatory Landscape

7

State Regulation

7

Federal Regulation

9

Enforcement

11

Conclusion

11

International Regulatory Landscape

12

Europe

12

Asia

14

The Americas

14

Africa

14

Insuring Bitcoin and Bitcoin Business

15

Does Bitcoin Raise Unique Insurance and Underwriting Issues?

15

Potential Insurance Coverage Under Traditional Policies

16

Bitcoin-Specific Insurance

17

The Bottom Line

18

Applications in Capital Markets

19

Greater Efficiencies

19

More Security and Transparency

19

“Smart Contracts”

20

Potential Risks

20

Conclusion

20

. Bitcoin, Privacy, and Reidentification

21

Intellectual Property

23

Bitcoin’s Open Source License

23

Other Blockchain Application Licenses

23

The Rise of Blockchain Patents

23

Social Impact

25

Lowered Transaction Fees Mean More Money for Causes

25

Greater Transparency

25

Access to Financial Services

25

Financial Empowerment

25

Improving Governance and Minimizing Corruption

26

Summary

26

Closing Note

27

Glossary of Terms

28

Key Contacts

32

Endnotes

33

.

. The Mysterious Origins of Bitcoin

Introduction

Though the following chapters are mostly devoted to

informing and enlightening the reader about the

potential of cryptocurrency and the underlying

blockchain technology, the origins of these

developments are somewhat shrouded in mystery.

Halloween 2008 may have been a particularly frightening

one, as the world economy was facing its most

dangerous crisis since the Great Depression. Yet, it also

happened to be the day that Bitcoin, the most widely

used cryptocurrency to date, was introduced in a rather

simple and unassuming email to several hundred

members of an obscure mailing list comprising

cryptography experts and enthusiasts.

The sender, known only as Satoshi Nakamoto, wrote:

“I've been working on a new electronic cash system that's

fully peer-to-peer, with no trusted third party,” followed

by directions to the link

http://www.bitcoin.org/bitcoin.pdf, a nine-page white

paper about a peer-to-peer trustless system of digital

“currency” that purports to solve the problem of doublespending.

After first becoming operational in January 2009, Bitcoin

and its related progeny have exploded in just a short

number of years. Exactly seven years after the initial

enigmatic email was sent, the October 31, 2015, cover of

The Economist featured an article on the blockchain (the

technology underlying Bitcoin), dubbing it “the trust

machine.” Blockchain technology, which is described

below, provides a cryptographically secured ledger that

can be examined by all authorized parties, but cannot be

changed.

Though Nakamoto initially collaborated with developers

on what has been called a revolutionizing innovation, his

participation ended in mid-2010, and in April 2011, he

completely disappeared with the final words, “I’ve moved

onto other things.”

Though we may never uncover the originator of Bitcoin,

we are left with a rapidly developing open source

technology that continues to find increasing mainstream

acceptance and simply cannot be ignored.

In fact, we have seen every sign that blockchain

technology will be widely adopted in various industries.

For example, the Hyperledger Project provides open

source blockchain software that can be adapted to

various applications. Intel has joined IBM, Digital Asset

Holdings, and others in providing code and support for

this project.

Also, Digital Asset Holdings has collaborated with the Depository Trust and Clearing Corporation (DTCC) to test and build a blockchain-type distributed ledger to track and settle financial assets. The R3 consortium is a group of FinTech companies and large banks that are developing a distributed ledger customized for financial institutions. The blockchain has also garnered the attention of government agencies and regulators, of course. For example, the U.S.

Office of Comptroller of Currency (OCC) has released a white paper posing an approach to handling how banking institutions should experiment with new technologies such as the blockchain. As discussed below, regulators in other countries and the European Union are also paying attention. The application of the blockchain is anticipated to extend far beyond financial services to include various applications of authentication and data storage. Potential applications of the blockchain include real property records, digital content ownership verification, and business process management. Bitcoin 101 – A Primer Reed Smith LLP 01 .

Bitcoin 101 – A Primer Cryptocurrencies1 have gained significant attention since the introduction of Bitcoin in 2009. They offer a new medium of exchange created by and for the Internet that could potentially democratize the very idea of money itself. The following is a short primer on bitcoin’s underlying technology2 and a breakdown of a sample bitcoin transaction. Armed with this understanding, we can more clearly see the potential impact, issues, and opportunities presented by Bitcoin, similar cryptocurrencies, and the underlying blockchain technology. Bitcoin became the first decentralized cryptocurrency, from which hundreds more cryptocurrencies have been derived.

Essential to its operation are two underlying technologies: public key cryptography and peer-to-peer networking. • Public key cryptography is the use of digital signatures to secure information. These signatures consist of a public key, which is known by everyone, and a private key, known only by its owner. • Peer-to-peer networking is a way to organize the flow of information among equal participants on a network, rather than relying on a central authority. Bitcoin secures transactions between currency users with digital signatures and then requires verification over a peer-to-peer network. Thus, when spending bitcoins3, you sign the transaction with your private key to prove you own the bitcoin you want to spend.

Then, your public key and the details of the transaction are published to a public ledger so that everyone knows that your bitcoin has changed hands. This public ledger is constantly being verified by the members of Bitcoin’s peer-to-peer network to ensure that each bitcoin is spent only once and is held by its verifiable owner. As such, Bitcoin replaces trust with mathematical proof and accountability among currency users themselves, thereby doing away with a central authority to monitor the currency, or trusted third parties to clear transactions. Unlike a digital file on your computer, a bitcoin cannot be copied and pasted infinitely.

It can only be transferred, and transferred only once, by signing the transaction with your private digital key and recording the transaction on a shared public ledger. Not only did Bitcoin solve the so-called “double spending” problem, where currency risked being spent more than once without the involvement of a middleman, but just as importantly, Bitcoin, owing to this middleman 02 Reed Smith LLP Bitcoin 101 – A Primer elimination, cut down the time required to verify and finalize transactions from what can take several days in a traditional system, to a matter of minutes – thereby enabling significant efficiencies and the growth of tremendous opportunities. The Blockchain Bitcoin relies on its peer-to-peer network to do two things: maintain the authoritative ledger of transactions and issue new currency. To understand how this works, we must briefly explain the bookkeeping algorithm behind Bitcoin, known as the blockchain4. The blockchain is a decentralized ledger that records information about transactions occurring in real time in “blocks” that are linked together through a secure mathematical function, thereby forming a chain of records (hence the name blockchain). To add a new block of records to the blockchain, someone must discover the mathematical key (called a “nonce”) that will fit the next block of records into the chain.

This is done by making millions upon millions of guesses (done by computers), the process of which is called “mining” and is done by participants on the Bitcoin network. Once discovered, the nonce must also be double-checked by other users in order to be verified. Mining secures the ledger, because once a block of records is added to the blockchain, the transactions recorded are considered final. In order to tamper with those records, a fraudster would have to re-discover the proof that allowed the records to be added in the first place.

This is very unlikely for two key reasons. First, the Bitcoin network is built to adjust the difficulty (up or down) of finding the key, based on the amount of computing power on the network, to ensure that just the right amount of work is necessitated for mining so that it is neither too hard (thereby requiring too much time), nor too easy. Second, the Bitcoin network is designed to follow only the longest chain of blocks.

This means that in order to go back and tamper with the ledger, you would have to find the key for the block you want to change and any others that were found after it in order to replace the longest chain. The computational difficulty of that task is so high that most bitcoin transactions are considered verified after six blocks are added to the network (which takes one hour on average). So why do miners dedicate computing power to finding mathematical keys to verify bitcoin transactions? The answer lies in how new bitcoins are issued. Rather than relying on a central bank or other authority, the Bitcoin network itself creates new bitcoins as a reward for .

miners who successfully find the next key. The miner who successfully creates a block of records receives a set reward of new bitcoins, plus any transaction fees attached to the transactions that the block records. This incentive has led to the creation of large bitcoin mining pools and other organizations dedicating raw computing power to claim new bitcoins, while at the same time securing Bitcoin’s ledger. A Bitcoin Transaction It would be illustrative to follow one bitcoin transaction from beginning to end to see how all the pieces fit together5. Say Alice, who owns three bitcoins, wants to send Bill two bitcoins.

She would go to her digital “wallet,” which is a program or online service that stores the keys that Alice needs to access her bitcoins. Alice puts in the address for Bill’s digital wallet, which is a 27-34 character code. She knows that the Bitcoin network tends to prioritize recording transactions that include a fee, so she offers 0.05 bitcoins to the miner who records her transaction. Alice’s digital wallet creates a data packet containing Bill’s wallet address, the number of bitcoins to be sent, the 0.05 transaction fee, and Alice’s digital signature.

This data packet is propagated through the Bitcoin network. It will flow in Bitcoin’s peer-to-peer network, from one computer to another, until each member knows of the pending transaction (this will usually take less than a minute). Within about 10 minutes, a miner finds the right nonce to record the next block of transactions. This miner prefers transactions with fees attached, so Alice and Bill’s transaction is at the top of the queue to record.

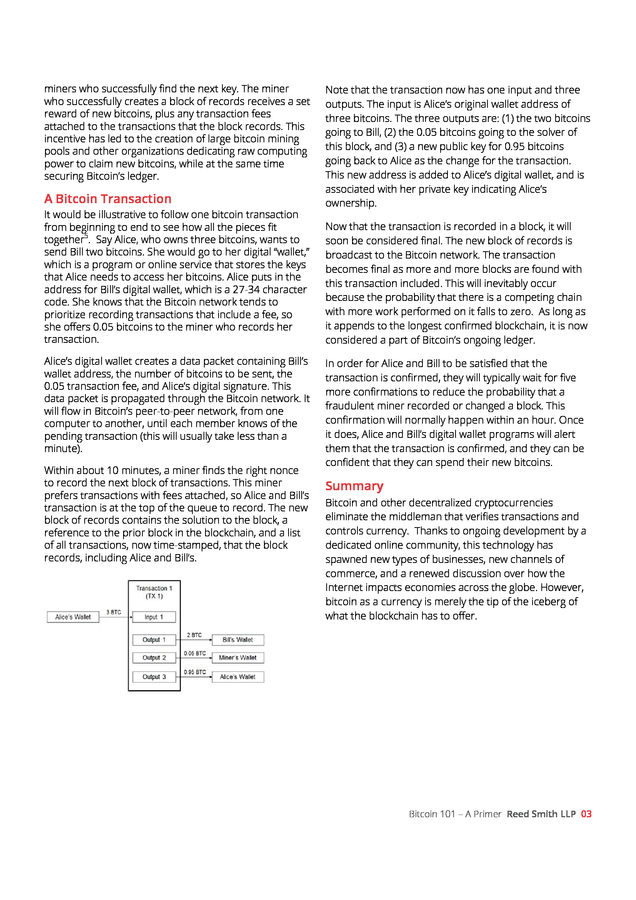

The new block of records contains the solution to the block, a reference to the prior block in the blockchain, and a list of all transactions, now time-stamped, that the block records, including Alice and Bill’s. Note that the transaction now has one input and three outputs. The input is Alice’s original wallet address of three bitcoins. The three outputs are: (1) the two bitcoins going to Bill, (2) the 0.05 bitcoins going to the solver of this block, and (3) a new public key for 0.95 bitcoins going back to Alice as the change for the transaction. This new address is added to Alice’s digital wallet, and is associated with her private key indicating Alice’s ownership. Now that the transaction is recorded in a block, it will soon be considered final.

The new block of records is broadcast to the Bitcoin network. The transaction becomes final as more and more blocks are found with this transaction included. This will inevitably occur because the probability that there is a competing chain with more work performed on it falls to zero.

As long as it appends to the longest confirmed blockchain, it is now considered a part of Bitcoin’s ongoing ledger. In order for Alice and Bill to be satisfied that the transaction is confirmed, they will typically wait for five more confirmations to reduce the probability that a fraudulent miner recorded or changed a block. This confirmation will normally happen within an hour. Once it does, Alice and Bill’s digital wallet programs will alert them that the transaction is confirmed, and they can be confident that they can spend their new bitcoins. Summary Bitcoin and other decentralized cryptocurrencies eliminate the middleman that verifies transactions and controls currency.

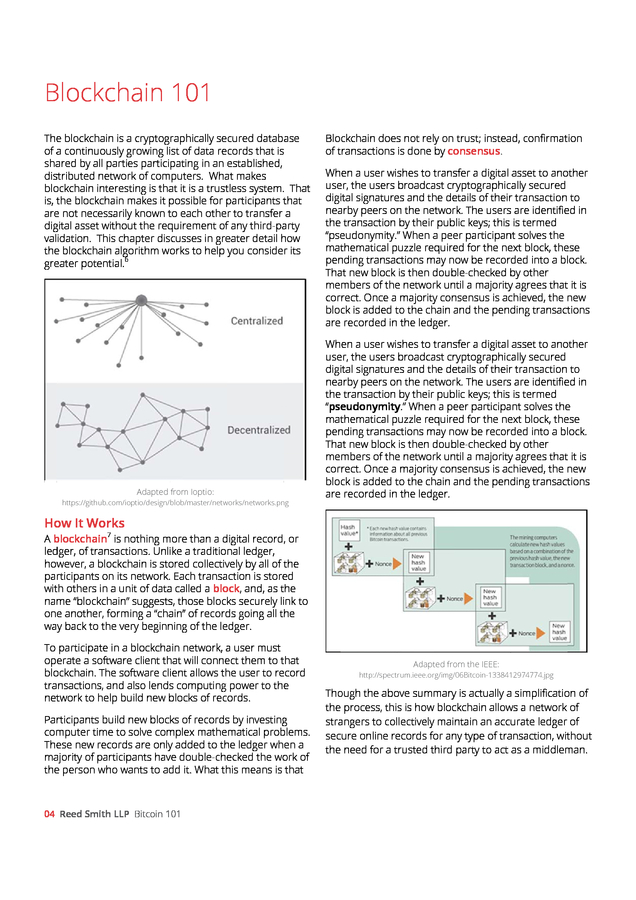

Thanks to ongoing development by a dedicated online community, this technology has spawned new types of businesses, new channels of commerce, and a renewed discussion over how the Internet impacts economies across the globe. However, bitcoin as a currency is merely the tip of the iceberg of what the blockchain has to offer. Bitcoin 101 – A Primer Reed Smith LLP 03 . B Blockc chain 101 The blockchain is a cryptographically secured database e of a continuous growing list of data records that is sly s sha ared by all pa arties participating in an established, dis stributed netw work of computers. Wha makes at blo ockchain inte eresting is tha it is a trust at tless system. That is, t blockcha makes it p the ain possible for p participants t that are not necessa e arily known t each other to transfer a to dig gital asset wit thout the req quirement of any third-pa f arty validation. This chapter discusses in gre s eater detail h how the blockchain algorithm wo e orks to help you consider its gre eater potenti 6 ial. Adapted from Ioptio: https://github.co om/ioptio/design/blob/master/netw works/networks.pn ng Blockchain does not rely on trust; instea confirmation s ad, of t transactions is done by co onsensus. When a user wis shes to trans a digital asset to ano sfer other use the users broadcast cr er, ryptographically secured digi signature and the de ital es etails of their transaction to r nea arby peers on the networ The users are identifie in n rk. s ed the transaction by their pub keys; this is termed blic “pse eudonymity.” When a pee participan solves the ” er nt mat thematical puzzle require for the ne block, the ed ext ese pen nding transac ctions may now be recorded into a bl lock. Tha new block is then doub at ble-checked b other by members of the network un a majority agrees that it is e ntil y t nsensus is ac chieved, the n new correct.

Once a majority con to and ding transact tions block is added t the chain a the pend are recorded in the ledger. sfer other shes to trans a digital asset to ano When a user wis er, ryptographically secured use the users broadcast cr digi signature and the de ital es etails of their transaction to r nea arby peers on the networ The users are identifie in n rk. s ed the transaction by their pub keys; this is termed blic y.” eer e “pseudonymity When a pe participant solves the thematical puzzle require for the ne block, the ed ext ese mat pen nding transac ctions may now be recorded into a bl lock. Tha new block is then doub at ble-checked b other by members of the network un a majority agrees that it is e ntil y t correct. Once a majority con nsensus is ac chieved, the n new to and ding transact tions block is added t the chain a the pend are recorded in the ledger. Ho It Work ow ks Ab blockchain7 is nothing m more than a d digital record, or led dger, of trans sactions. Unli a traditional ledger, ike how wever, a bloc ckchain is sto ored collectiv by all of t vely the participants on its network.

Each transa action is store ed wit others in a unit of data called a blo th a ock, and, as the name “blockcha suggests those blocks securely li to ain” s, ink one another, fo orming a “cha of record going all the ain” ds e ning of the le edger. way back to the very beginn ain To participate in a blockcha network, a user must operate a softw ware client th will conne them to t hat ect that blo ockchain. The software cli e ient allows th user to re he ecord transactions, an also lends computing power to the nd s net twork to help build new b p blocks of records. Participants build new blocks of records by investing s g com mputer time to solve com mplex mathematical prob blems. The new reco ese ords are only added to th ledger when a y he ma ajority of part ticipants hav double-che ve ecked the wo of ork the person who wants to ad it. What th means is that e o dd his 04 Reed Smith LLP Bitcoin 101 Adapted fro the IEEE: om http://spectrum.ieee.org/img/ /06Bitcoin-133841 12974774.jpg ough the abo summary is actually a simplificatio of ove y on Tho the process, this is how bloc ckchain allow a network of ws angers to collectively maintain an accurate ledger of stra sec cure online re ecords for an type of tra ny ansaction, wit thout the need for a trusted third party to act as a middlem man. .

As time goes on, more and more blocks of records are added to the blockchain, each one securely referencing the next. This is important because if someone wanted to go back and change a transaction on the ledger – to cook the digital books – she would not only have to resolve the mathematical puzzle allowing her to create a fraudulent block, but she would also have to re-solve every subsequent block in the blockchain. Even worse for the fraudster, she would have to convince a majority of network participants to accept these fake blocks before the next legitimate participant added the next real block. The sheer volume of work and speed required make it extremely difficult to alter transactions on a blockchain. This means that after a certain number of new blocks are added, the parties to a transaction can be well-assured that the transaction is considered final – not only by them, but also by the entire community of participants on the network. It is precisely this assurance that allows blockchain participants to trust the ledger itself, even though they do not necessarily trust (or know) their fellow participants on the network. Advantages of Blockchain Distributed ledgers like Blockchain solve important problems in Internet commerce.

Chief among them is the problem of double spending, where two transactions draw upon the same underlying asset. By requiring every transaction to be at least partly public, distributed ledgers dramatically increase counterparty trust. Moreover, because Blockchain requires proof of work and consensus to record new transactions, it is very difficult for fraudsters to tamper with digital records to steal or re-spend assets. Blockchain also helps achieve certainty in the concept of digital ownership itself. A consummate problem with digital information is that it is freely transferable and may be copied.

This means that possession cannot be equated with ownership. Merely having a copy of a file does not include the right to exclude – a touchstone right built into the concept of property. Distributed ledgers like blockchain make proving the ownership of a digital asset more like performing a real property title search.

Like the grantor-grantee index in land records, the blockchain records every transaction involving a particular digital asset. The advantage of blockchain over other forms of exclusive digital ownership, like encryption at rest,8 is that there is always a record that reflects not only the current possession of the asset, but also the history of rightful ownership going all the way back to the digital asset’s creation. Disadvantages of Blockchain Like all technical solutions, the blockchain algorithm reflects certain tradeoffs. Because of latency and scalability issues, many current blockchain applications put severe limits on the size of each new block of records.

This limits the frequency with which a blockchain network can process transactions. For example, the Bitcoin network can only process seven payments per second, while major credit card providers can handle more than 1,400. Designers of applications that leverage blockchain should carefully consider factors such as block size, the proof of work required to verify blocks, and the expected number of participants on a blockchain, to ensure the ledger operates efficiently and effectively. Blockchain relies heavily on public key cryptography to identify users and permit access to assets tracked through the ledger.

For this reason, key security is of increased concern. If a user’s private key is lost or stolen, the user has lost access to his or her assets on the blockchain forever. For example, as many as 4 percent of bitcoins have been rendered permanently ownerless because users have misplaced their digital keys.

Future applications of blockchain, especially in private or semiprivate contexts, should consider employing multi-factor authentication or digital certificates to safeguard the cryptographic keys used to identify rightful owners and permit access. While smaller blockchain networks may offer more technical security options, they are not necessarily safer. Organizations that host private or semi-private blockchains should especially consider the possibility of so-called “51% attacks,” where the majority of the network’s mining hashrate is concentrated in a single entity, thereby allowing that single entity to manipulate the public ledger at will. In addition, the pseudonymous nature of blockchain transactions can make fraud detection and collusion between users more difficult to detect. Carefully consider the sensitivity of information stored in a distributed ledger, the type and number of network participants, and the incentives for fair play on the network. Bitcoin 101 Reed Smith LLP 05 .

Summary The blockchain algorithm is an important contribution to the foundational technologies we use to store and secure information. It addresses particular problems with counterparty trust and digital asset ownership. While not a panacea, the blockchain algorithm presents exciting opportunities in how we store and share information securely online. Many commentators posit that the invention of the blockchain will be remembered in the same vein as the invention of the World Wide Web 06 Reed Smith LLP Bitcoin 101 or email.9 As a foundational technology, the blockchain could one day be a major part of how we store and transmit electronic information itself.10 The opportunity is wide open for innovators to apply blockchain across the digital landscape. Armed with an understanding of how the blockchain works, you can be a part of that conversation. .

U.S. Regulatory Landscape In the United States, it is currently legal to transmit, mine, and develop cryptocurrencies, such as Bitcoin. It is also generally legal to use cryptocurrencies to purchase goods and services, or for investment purposes. However, with their dramatic increase in prevalence and overall use, cryptocurrencies have become the target of regulations issued by both the federal and state governments. The increase in regulatory oversight has been particularly significant during the past year. One state, New York, has already issued regulations explicitly subjecting those engaging in virtual currencybased business activities to licensing, supervision, and other compliance requirements.

In addition, various federal agencies have provided guidance that certain virtual currency-related activities may be subject to already-existing regulations, such as those governing money transmission. Furthermore, several agencies have initiated enforcement actions against businesses and individuals related to cryptocurrency activities. The focus of these regulations tends to be on virtual currencies themselves and their transmission, as opposed to the pure development of cryptocurrency technology and software. For example, the New York BitLicense regulations explicitly provide that those who only develop virtual currency software and technology are not subject to licensure. These recently promulgated regulatory regimes, along with the guidance provided by other agencies clarifying the application of already existing regulations to virtual currency-related activities, have major implications to companies engaged in virtual currency activities from a licensing, supervision, compliance, and cost perspective. Undoubtedly, with the sustained growth of cryptocurrency, governments will continue to adapt, and one can expect additional regulations from governmental authorities within the coming years. State Regulation New York: The BitLicense Regime Led by former Superintendent of Financial Services Ben Lawsky, New York state has been at the forefront of virtual currency regulation since 2014. In July 2014, through its Department of Financial Services (“NYDFS”), New York became the first state to propose a comprehensive regulatory regime governing virtual currency business activities.11 And on June 3, 2015, following comments from numerous interested parties, New York became the first state to implement a comprehensive virtual currency regulatory regime – popularly known as “BitLicense.”12 As of September 2015, NYDFS has already received 25 initial BitLicense applications.13 Recently, NYDFS issued the first license under the BitLicense regime to Circle Internet Financial, a Bitcoin wallet and creator of the app Circle Pay.14 However, the BitLicense regulations have been divisive, and some have criticized the burdens that it places on virtual currency-related businesses.

As a result, some companies have attempted to block users from New York in an attempt to avoid falling under the BitLicense regulations.15 Under the BitLicense regime, companies engaged in “virtual currency business activities” Under the BitLicense regime, companies engaged in “virtual currency business activities” are required to undergo a thorough application process, obtain a license, abide by numerous compliance requirements similar to banks and other financial institutions, and be subject to examinations by NYDFS. Who Must Obtain a License? Under BitLicense, a “virtual currency” is a digital unit that is a digital medium of exchange or form of stored value, with specific exceptions for prepaid cards, customer rewards programs, in-game currency and reward points.16 Companies that conduct “virtual currency business activities,” as defined in the BitLicense regulations, and that operate in New York, or engage in business with New York customers, are subject to the BitLicense regime.17 Under BitLicense, the following five activities constitute “virtual currency business activities”: • Receiving virtual currency for transmission or transmitting virtual currency through a third party • Maintaining custody of virtual currency or holding virtual currency on behalf of others • Buying or selling virtual currency as a customer business • Performing virtual currency exchange or conversion services (whether converting virtual currency to fiat currency or vice versa; or converting one type of virtual currency for another type of virtual currency) U.S. Regulatory Landscape Reed Smith LLP 07 . • Controlling, administering, or issuing virtual currency18 BitLicense exempts several activities from licensure. For example, cryptocurrency mining on its own would not subject a party to the BitLicense regime.19 Similarly, consumers or merchants only using virtual currency to buy or sell goods or services would not be required to obtain a license.20 And finally, parties who engage purely in software development and dissemination do not fall under BitLicense.21 However, there are many unanswered questions as to the particular circumstances in which various exceptions would apply. For example, BitLicense exempts from licensure the transmission of “nominal amounts” of virtual currency for “non-financial purposes.”22 Some have surmised that this would allow for transmission of nominal amounts of cryptocurrency for purposes of, for example, identity verification. However, it is less clear whether this exception would apply to the use of a nominal amount of cryptocurrency to create a “digital contract.” Likewise, there are several gray areas as to whether certain businesses are engaged in one of the five “virtual currency business activities,” or mere software development. Application and Licensing Process The BitLicense application and licensing process is extensive, and is similar to the licensing required for other types of financial institutions chartered in New York. Applicants must pay a $5,000 application fee, and submit to NYDFS extensive biographical, historical, financial, and business information about the applicant, its principal officers, and its principal stockholders.23 Under BitLicense, NYDFS must approve or deny applications within 90 days of deeming the application complete.24 However, in practice, the regulators can also ask for more documentation, and likely often will as is the case with other financial regulatory licensing.

Further, the superintendent may also extend the 90-day window in certain cases.25 Therefore, as with the licensing process for other financial institutions, the BitLicense application will likely be time- and cost-intensive. NYDFS may also issue conditional licenses under BitLicense for those applicants that do not comply with all BitLicense requirements upon licensing.26 This conditional license is valid for two years. However, the conditional license may be issued subject to reasonable conditions imposed by NYDFS, and the licensee may be subject to heightened scrutiny, review, and examination. Licensees must also obtain NYDFS written approval to offer any materially new product, service, or activity, or to make a material change to an existing product, service, or activity.27 Finally, NYDFS has the authority to suspend or revoke both full and conditional licenses on several 08 Reed Smith LLP U.S. Regulatory Landscape grounds, including on any ground that the superintendent may refuse an initial license, for violation of any provision of BitLicense, good cause, or for failure to pay a judgment.28 AML, KYC, Compliance Issues, and Examinations Perhaps the most significant BitLicense provisions are the numerous ongoing compliance provisions that the NYDFS requires of licensees.

Many such compliance regulations are similar to those required of New Yorkchartered banks and other types of financial institutions. Licensees under BitLicense must maintain a comprehensive anti-money laundering (AML) policy.29 This policy is subject to both an initial risk assessment and ongoing annual risk assessments.30 Licensees must adopt internal controls and policies to ensure AML compliance, including appointing a dedicated compliance officer and subjecting the policy to review and approval by the licensee’s board of directors.31 The policy must be subject to annual independent testing, and the audit report must be submitted to NYDFS.32 The AML provisions also include numerous additional know-your-customer (“KYC”) requirements similar to those in existence for other financial institutions, or for money transmitters under FinCEN regulations.33 Licensees must identify and verify customers’ identities, check customers against the list of Specifically Designated Nationals maintained by the Office of Foreign Assets Control (“OFAC”), and maintain customer records.34 Licensees are also required to submit to NYDFS suspicious activity reports (“SARs”) and currency transaction reports for transactions in cryptocurrency of more than $10,000.35 Additional compliance regulations promulgated by the BitLicense regime include those addressing a licensee’s: • Capital requirements36 • Custody and protection of assets37 • Books and records38 • Consumer protection disclosures39 • Consumer complaint policies40 • Advertising41 • Anti-fraud policies42 • Cybersecurity programs43 • Business continuity and disaster recovery plans44 Under BitLicense, licensees are subject to at least one examination by NYDFS every two years.45 Licensees . must also submit numerous financial statements and reports to NYDFS on a quarterly and annual basis.46 Conference of State Bank Supervisors On September 15, 2015, the Conference of State Bank Supervisors issued a model licensing regime as a guide to states in regulating virtual currency. The Conference recommends that companies involved in the exchange and transmission of virtual currencies and “services that facilitate the third-party exchange, storage and/or transmission of virtual currency (e.g. wallets, vaults, kiosks, merchant-acquirers, and payment processors),” be supervised and licensed by state banking regulators.47 “Virtual currency” is defined here as a digital representation of value used as a medium of exchange, unit of account, or store of value, but which does not hold legal tender status. Virtual currency would not include the software or protocols governing transfer.48 Other State Proposals Following New York’s lead, other states have made various proposals to implement virtual currency regulations within the past year. Perhaps most prominently, in June 2015, the California House of Representatives passed AB-1326.49 The bill, introduced in February 2015, would provide for a similar, but not quite as extensive, licensing regime to New York’s BitLicense.50 Like BitLicense, AB-1326 would provide that virtual currency businesses could not operate unless licensed by the California Department of Business Oversight.

The proposal also calls for capital requirements and an extensive application process. However, the California proposal would be more relaxed than BitLicense in certain areas: for example, it would not require submission of state-level SARs and would contain less stringent AML requirements. As of September 2015, AB-1326 stalled in the California Senate and is no longer listed as an active bill; however, it could be revived on a future date.51 At least three states have issued guidance as to how state law, particularly concerning money transmission, applies to virtual currency transactions. Washington state has concluded that virtual currency is included in the definition of “money transmission” in its Uniform Money Services Act.52 However, both Kansas and Texas have concluded that virtual currency does not constitute money under its money transmission laws, and therefore, the two states’ respective money transmission laws generally do not apply to virtual currency transactions; the one exception may be where the acts may apply is transactions in which virtual currency is exchanged for sovereign fiat currency through a third-party exchange site.53 New Jersey, Connecticut, Pennsylvania, North Carolina, Utah, and New Hampshire have also made various virtual currency regulation proposals; however, none has been adopted as of this writing.54 Federal Regulation Unlike New York state, federal agencies have not yet issued specific sets of regulations specifically addressing virtual currency.

However, in recent years, agencies have clarified that certain laws and regulations already in existence may apply equally to activities and transactions involving virtual currency as to those involving traditional fiat currency. Two of the agencies whose regulations may most impact virtual currency businesses include the Commodity Futures Trading Commission (“CFTC”) and Financial Crimes Enforcement Network (“FinCEN”). Commodity Futures Trading Commission (“CFTC”) On September 17, 2015, the CFTC confirmed that it would treat bitcoin and other virtual currencies as “commodities” for regulatory purposes under the Commodity Exchange Act (“CEA”) and other CFTC regulations.55 Under the CEA and its regulations, the CFTC may assert jurisdiction over the trading of futures, options, and swaps on “commodities.”56 The term “commodity” is defined broadly to include “goods and articles…and all services, rights and interests…”57 The CFTC’s determination came in the form of a settlement order against Coinflip, Inc., which is discussed in more detail below. The decision to treat virtual currencies as “commodities” under the CEA and CFTC regulations confirms prior informal guidance provided by CFTC Chairman Timothy Massad and other CFTC officials, who had commented in testimony and speeches that the CFTC would be able to assert jurisdiction over virtual currencies.58 The order also appears to confirm that the CFTC would only treat virtual currency as a “commodity,” and that it would not treat virtual currency as “currency”; and therefore virtual currencies would not be subject to certain regulations governing foreign exchange derivatives.59 The treatment of virtual currency as a “commodity” carries significant implications for businesses that engage in the trading of virtual currency-based derivatives.

Such firms that come under the CFTC’s jurisdiction may have to register with the CFTC, and could be subject to regulation by the CFTC and/or the National Futures Association. This supervision will undoubtedly subject the firms to numerous regulatory obligations. As a result of the CFTC’s September 2015 settlement with Coinflip, almost any business whose business activities involve virtual currency-based derivatives will need to assess whether it is required to register with the CFTC and may be subject to CFTC regulation.

Two such businesses might include firms running trading platforms U.S. Regulatory Landscape Reed Smith LLP 09 . involving virtual currency-based derivatives, or firms providing advisory services concerning virtual currencybased derivatives. Financial Crimes Enforcement Network (“FinCEN”) Like the CFTC, FinCEN has not issued any regulations directly addressing virtual currency. However, businesses engaged in virtual currency activities may come under the purview of FinCEN’s regulations concerning money services businesses (“MSBs”). Under FinCEN regulations, MSBs include “money transmitters.”60 In 2011, FinCEN opened the door to regulation of virtual currency businesses as money transmitters – and therefore MSBs – when it revised the definition of “money transmission services” to include “the acceptance of currency, funds, or other value that substitutes for currency from one person and the transmission of currency, funds, or other value that substitutes for currency to another location or person by any means.”61 Therefore, any party that engages in the transmission of virtual currency must abide by FinCEN’s MSB regulations, just as if the business transmitted traditional currency. The implications for being deemed a money transmitter and MSB are significant. MSBs must comply with numerous AML requirements, including implementation, adoption, and maintenance of an AML program; independent review of such AML program; filing of SARs and currency transaction reports; and maintenance of records.62 Further, MSBs must register with FinCEN.

It is a federal crime to knowingly conduct an MSB while failing to register with FinCEN (or state licensing money transmission licensing agencies).63 Starting in 2013, FinCEN has issued guidance clarifying what types of virtual currency activities could trigger treatment as an MSB by FinCEN. In March 2013, FinCEN provided three types of parties that may engage in virtual currency activities: • Users (those who use virtual currency to purchase goods or services) • Exchangers (those providing for the exchange of virtual currency for real currency, funds or other virtual currency) • Administrators (those issuing virtual currency, or with the authority to redeem virtual currency)64 FinCEN concluded that, broadly speaking, users of virtual currency would not be considered MSBs, but that exchangers and administrators would fall under the MSB regulations.65 Since then, FinCEN has provided additional guidance as to what types of activities may trigger regulation. FinCEN has issued various guidance providing that it would not 10 Reed Smith LLP U.S.

Regulatory Landscape view the following activities as subjecting a party to MSB regulations: • Mining virtual currency66 • Use of virtual currency to purchase goods and services67 • Conversion of virtual currency to fiat currency for one’s own use68 • Investing in virtual currency for one’s own account69 • Renting out of computer systems and software that mine virtual currency to third parties (where any virtual currency mined by the third party using the software would remain the property of that third party)70 Many of the above were deemed not to constitute the activities of an MSB because they were performed for one’s own account; however, as soon as such activities were performed by or on behalf of a third party, the analysis could change. On the other hand, FinCEN has confirmed that the following activities would constitute engaging in business as an MSB: • Maintaining a trading system to match offers to buy and sell virtual currency for fiat currency71 • Maintaining a set of book accounts where customers may deposit virtual currency72 • Developing and maintaining a system to provide virtual currency payments to merchants in the United States and Latin America wishing to receive payment for goods/services sold in a currency other than that of legal tender73 • Conducting Internet-based brokerage services between buyers and sellers of precious metals, in which buyers pay sellers directly by check, wire, or bitcoin; and the entity uses the bitcoin blockchain to transfer previous metal ownership by issuing a digital certificate. The customer could then later exchange its holdings using the bitcoin blockchain ledger.74 Other Federal Agencies Numerous other federal agencies have also issued guidance on virtual currency or issued consumer advisories, although not as significant as the CFTC’s or FinCEN’s interpretations. For example, the Securities and Exchange Commission (“SEC”) has issued guidance stating that, even if it does not consider virtual currencies to be “securities,” it may still invoke its enforcement authority to prosecute virtual currency-based Ponzi schemes and other fraud – which it has already done.75 .

The Internal Revenue Service has concluded that cryptocurrency should be considered “property” under the Internal Revenue Code, and thus transfers involving virtual currencies would be taxable events.76 Other agencies issuing guidance and consumer advisories include the Consumer Financial Protection Bureau, Board of Directors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the Office of the Comptroller of the Currency, the Federal Trade Commission, and FINRA. Enforcement Over the past several years, various federal agencies have stepped up their enforcement of virtual currencyrelated activities. Although no federal agencies have yet issued virtual currency-specific regulatory regimes, such as New York’s BitLicense, the agencies have prosecuted numerous individuals applying existing laws to virtual currency-based activities. In some cases, these enforcement actions have been precedent-creating, such as the settlement agreement between Coinflip and the CFTC, in which the CFTC confirmed its interpretation that virtual currencies constituted “commodities” under the CEA. Some examples of key enforcement actions include the following: CFTC On September 17, 2015, the CFTC settled an enforcement action against Coinflip, Inc. and its chief executive officer.

Coinflip operated an online facility called Derivabit that matched buyers and sellers of bitcoin option contracts. The CFTC found that Coinflip was operating a facility for trading commodity options in violation of the CEA and CFTC regulations, including by operating the facility without having registered with the CFTC. Although the Order did not carry any monetary penalties, this enforcement action was especially significant because, through the Order, the CFTC established that it considered virtual currencies to be “commodities” under the CEA, and thus could exercise jurisdiction over various virtual currency-related derivatives.77 FinCEN On May 15, 2015, FinCEN issued a $700,000 civil monetary penalty against Ripple Labs, Inc.

for willful violations of the Bank Secrecy Act regulations. Specifically, FinCEN accused Ripple of acting as a money services business by selling virtual currency. However, Ripple did not register with FinCEN, failed to implement appropriate AML programs, and failed to report suspicious activities, among other violations.78 SEC In September 2014, the United States District Court for the Eastern District of Texas entered a final judgment against Bitcoin Savings & Trust and Trenton Shavers following an SEC enforcement action. The SEC alleged, and the court found, that Bitcoin Savings & Trust and Shavers conducted a Ponzi scheme soliciting investments in bitcoin-related investment opportunities.79 In December 2014, the SEC sanctioned Ethan Burnside for operating two digital currency exchanges without registering them as either broker-dealers or stock exchanges.80 In June 2014, Erik Vorhees was sanctioned by the SEC for violating sections 5(a) and 5(c) of the Securities Act of 1933 for publicly offering unregistered securities in two Bitcoin-related ventures, SatoshiDICE and FeedzeBirds.81 FBI/DOJ Following an investigation by numerous agencies, Ross Ulbricht was sentenced to life in prison in May 2015 in connection with his role in Silk Road.

Mr. Ulbricht founded Silk Road, an online black marketplace used to facilitate criminal activity; the site was later shut down by government task forces. Mr.

Ulbricht was found guilty in February 2015 of conspiracy to distribute controlled substances, computer hacking, and money laundering.82 Blake Benthall, who operated Silk Road 2.0, a follow-on site to Silk Road, was arrested in November 2014 on similar charges.83 Charlie Shrem, a former vice chairman of the Bitcoin Foundation, and Robert Faiella, were arrested for unlawfully converting dollars into bitcoin for users of Silk Road. Each pleaded guilty in September 2014, and were sentenced to two years and four years in prison, respectively. Shrem and Faiella were charged with operating an unlicensed Money Transmitting Business (failure to register with FinCEN), money laundering, and willful failure to file SARs with FinCEN.84 Conclusion The explosion of cryptocurrencies over the past several years has not escaped the attention of regulators in the United States.

For at least the past two years, agencies have applied already existing laws and regulations to adapt to the virtual currency landscape, notably FinCEN and the CFTC. In addition, New York’s BitLicense regime became the first comprehensive regulatory regime aimed squarely at regulating virtual currency. The continued growth and prevalence of cryptocurrency will undoubtedly continue to solicit attention from regulators and additional regulations and enforcement actions at the federal and state level. U.S.

Regulatory Landscape Reed Smith LLP 11 . International Regulatory Landscape Internationally, the regulation of cryptocurrency varies substantially by jurisdiction. Some countries have minimal regulations on the subject. Several countries have proceeded with cryptocurrency regulation in ways similar to the United States—that is, they are currently studying the potential regulation of virtual currencies, and are working to adapt and/or update their alreadyexisting anti-money laundering (“AML”) and money transmission laws and regulations to cover virtual currencies. These countries include, among others, Canada, France, Italy, Singapore, and Japan. Within Europe, the European Court of Justice just ruled that bitcoin should be treated as a currency.

This ruling will undoubtedly have a major impact on virtual currency regulation in the international sphere, and stands in contrast to the U.S. CFTC’s decision that virtual currencies should be treated as commodities. This and future rulings, along with a 2014 Opinion issued by the European Banking Authority urging an EU-wide virtual currency regulatory regime, could have the effect of unifying European regulation on the subject, which had varied more substantially from country to country. However, other countries have imposed much more stringent regulations, and in some cases have banned or criminalized the use of virtual currencies.

These more stringent laws may make it effectively impossible to deal in virtual currency in various countries. For example, Russia has recently proposed legislation to make the use of virtual currency a criminal misdemeanor. Virtual currency has been banned outright in Ecuador and Bolivia (although the Ecuadorian government has created its own state-backed digital currency).

In Bangladesh, virtual currency is not considered legal tender, and its use may lead to jail time. Iceland has indicated that virtual currency is not protected currency, and its purchase may violate the country’s Foreign Exchange Act. And the Chinese government has instructed its commercial banks to halt all dealings with virtual currency exchanges, and has prohibited these banks from clearing virtual currency transactions – particularly notable since more than 80 percent of bitcoin transactions take place in Chinese yuan. As noted above, international regulation of virtual currency is fast-evolving and varies substantially across jurisdictions.

This chapter is just a sampling of notable regulations in certain countries, and is not meant to serve as a thorough analysis of all virtual currency regulations across the globe. 12 Reed Smith LLP International Regulatory Landscape Europe October 2015 European Court of Justice Ruling In one of the first major virtual currency court cases impacting the European Union as a whole, on October 22, 2015, the European Court of Justice (“ECJ”) held that bitcoin should be treated as a currency and means of payment for tax purposes.85 This holding stands in contrast to regulation in the United States, in which the U.S. Commodity Futures Trading Commission (“CFTC”) has recently determined that virtual currencies should not be treated as currencies, but instead as commodities.86 The ECJ’s ruling has major implications for all players in the cryptocurrency space, especially from a tax standpoint. Under the EU’s Directive concerning value added taxes (“VAT”), member states may not use their value added taxes to tax “transactions, including negotiation, concerning currency, bank notes and coins used as legal tender.”87 Because the ECJ held that virtual currencies constitute currency and a means of payment for purposes of the EU’s VAT Directive, the EU member states may not use their VAT to tax cryptocurrency transactions.

Therefore, bitcoin and virtual currency exchanges that convert traditional currency to virtual currency are exempt from VAT, and consumers making a bitcoin exchange would not face a VAT charge as a result of the transfer. A holding by the ECJ that virtual currencies should be treated more like commodities (in line with the CFTC) would have made transfers of fiat currency to virtual currency potentially taxable under various EU members’ VATs, similar to the general tax treatment of other commodities. The ECJ’s ruling was also significant because it resolved a conflict among the member states’ taxing authorities on how exactly to treat virtual currency from a tax perspective—whether as a currency or a commodity. For example, while the UK tax authority had taken the position—like the ECJ—that virtual currency should be treated as a currency, the tax authorities from Sweden and Germany argued that virtual currency should be treated as a commodity, and thus subject to the VAT.88 The ECJ’s ruling should provide a boost to bitcoin and other cryptocurrency trading in Europe, adding certainty that exchanges involving cryptocurrencies may be made free of VAT. The ruling had an immediate impact on bitcoin, as its price rose 3 percent immediately following news of the ruling.89 It may also pave the way for additional harmonizing of virtual currency regulations across the EU member states. .

It should be noted that this ruling applies primarily to the application of the VAT to the exchange of fiat currency for virtual currency, or vice versa, or the exchange of virtual currency for another type of virtual currency. Sales of goods and services subject to VAT but paid for with virtual currency would likely still be subject to VAT. And any capital gains on virtual currency appreciation could still potentially be taxed by member states in conjunction with their income tax laws. European Banking Authority Opinion In July 2014, the European Banking Authority (“EBA”) issued an opinion regarding virtual currency, providing recommendations to the EU Council, European Commission, and European Parliament regarding an EUwide regulatory regime of virtual currencies.90 The opinion also provides recommendations to national banking authorities regarding intermediate regulatory steps that can be taken to address the risks of virtual currency before a full European regulatory regime is implemented. Overall, the EBA’s Opinion concluded that, although virtual currencies have the potential to create certain benefits –particularly in the areas of reduced transaction costs and increased transaction speeds – these benefits would have less impact in the EU, because of EU directives aimed squarely at those same goals. 91 The Opinion also found that the numerous risks of virtual currency (more than 70 were identified in the Opinion) would likely outweigh the potential benefits.92 In order to address the numerous risks of virtual currency, the EBA’s Opinion advocated that “a substantial body of regulation” be implemented.93 Such a comprehensive regulatory regime would need to include, at a minimum, measures addressing governance requirements of market participants, segregation of client accounts, capital requirements, and the creation of “scheme governing authorities.”94 In order to mitigate the risks of virtual currencies prior to the implementation of such a regulatory regime, the EBA recommended that national banking authorities should immediately “discourage credit institutions, payment institutions and e-money institutions from buying, holding or selling virtual currencies.95 Finally, the EBA urged EU legislators to declare market participants in virtual currencies as “obligated entities” under the EU’s Anti Money Laundering Directive, and therefore subject to AML and counter-terrorist financing requirements.96 Regulatory Status of Cryptocurrencies in Individual European Countries Although the ECJ’s recent ruling has provided clarity on the tax status of virtual currency in EU member states, the regulations of virtual currency across Europe still vary substantially. Generally speaking, the mining, exchanging, and buying and/or selling of goods or services with cryptocurrency is generally legal and permitted across Europe. However, much like the United States, many European countries are currently seeking to apply existing laws to virtual currency, virtual currency transactions, and players in the virtual currency space. For example, Germany, France, Italy, and the Czech Republic, among others, have explored adapting existing laws concerning money transmission, AML, taxation, and registration/licensure of financial institutions to apply to virtual currency.97 Of course, any prior differences on tax treatment of virtual currency vis-à-vis the VAT may now be eliminated following the ECJ ruling. Notable European nations that many view as having less stringent virtual currency regulation include the United Kingdom and Switzerland.

Many believe the United Kingdom has a relatively more favorable view of blockchain and digital ledger technology. Numerous technology incubators focusing on blockchain technology and cryptocurrencies, such as those backed by Barclays and others, are headquartered in the United Kingdom. Further, in September 2014, the Bank of England released papers praising the potential benefits of blockchain technology and its potentially wide impact on the financial system as a whole. The Bank of England’s papers note that distributed ledger technology is “the key innovation of digital currencies,” and is “a genuine technological innovation which demonstrates that digital records can be held securely without any central authority.” The Bank of England has also concluded that virtual currencies as a whole “do not currently pose a material risk to monetary or financial stability in the United Kingdom.”98 In June 2014, the Swiss government affirmatively decided not to propose any new statutory provisions regarding virtual currency for the immediate future.

Although a report by the Swiss Federal Council urged caution when conducting cryptocurrency transactions, the report concluded that no new legislation was necessary, in part, because “the economic importance of virtual currencies like Bitcoin as a means of payment is fairly insignificant at the moment and the Federal Council believes that this will not change in the foreseeable future.”99 On the other end of the spectrum, Russia and Iceland have each passed laws that are particularly hostile to virtual currency. Legislation has been introduced in Russia that would prohibit the distribution, creation and use of “money substitutes,” which includes virtual currencies; violators of the law would face criminal penalties.100 Various sources have suggested that the legislation will be enacted by the end of 2015.101 Even though the legislation has not passed, as early as International Regulatory Landscape Reed Smith LLP 13 . February 2014, Russian authorities warned that the ruble was the sole currency of Russia, and using virtual currency as a money substitute was illegal.102 The Central Bank of Iceland has also declared that neither bitcoin nor Auroracoin is a recognized currency or legal tender under Icelandic law, and that the purchase of virtual currency is restricted under Iceland’s Foreign Exchange Act.103 Asia Generally speaking, Asian countries have more stringent regulations governing virtual currency compared with the rest of the world. For example, the use of Bitcoin and other virtual currencies is completely barred in Bangladesh, and officials from the Bangladesh Bank have stated that anyone caught using virtual currencies may be sentenced to up to 12 years in jail under the country’s strict AML laws.104 In China, while the use of Bitcoin and virtual currencies by individuals technically remains legal, its use is difficult if not impossible. This is because the People’s Bank of China has warned financial institutions, payment institutions, and third-party payment providers that they may not accept, use, or sell virtual currencies; may not generally be involved in virtual currency transactions; and may not work with virtual currencyrelated businesses.105 The regulatory status of virtual currency in Thailand is far from clear: in 2013, the Bank of Thailand informed a virtual currency-based business that virtual currency activities were illegal in Thailand; however, one year later, the same bank reportedly concluded that Thai law does not regulate virtual currency, but that exchanges still could not operate if they could not prevent virtual currencies from being exchanged with currencies other than the Thai Baht.106 On the other end of the spectrum, Japan stated in June 2014 that, despite the fall of Japanese-based bitcoin exchange Mt. Gox, the country would not move to regulate virtual currencies in the immediate future.107 Finally, several other Asian countries, such as India and Singapore, are pursuing a more cautious approach similar to Europe and the United States, where they are seeking to adapt already existing laws to cover virtual currencies.108 The Americas Outside of the United States, two countries in the Americas hold “first” status in digital currency regulation: Canada became the first country in the world to enact a national law specifically regulating virtual currencies, while Ecuador became the first country to issue its own state-backed digital currency. In June 2014, Canada amended its Proceeds of Crime (Money Laundering) and Terrorist Financing Act to include provisions specifically governing virtual 14 Reed Smith LLP International Regulatory Landscape currencies from an AML perspective.109 Pursuant to the amended statute, dealers in virtual currencies would be subjected to the same regulations as money services businesses.110 The implications of this classification are that those dealing in virtual currencies would be required to register with the Financial Transactions and Reports Analysis Centre of Canada (“FINTRAC,” similar to FinCEN in the United States), and abide by various regulatory obligations surrounding recordkeeping, suspicious transaction reporting, and verification procedures, among others.111 Under the revised statutes, banks are also prohibited from opening or maintaining banking relationships with unregistered businesses that are now classified as money services businesses on account of dealing in virtual currency.112 Second, in 2015, Ecuador became the first nation to issue its own, state-sponsored digital currency—the dinero electrónico—that is officially legal tender in the country alongside the U.S.

dollar.113 However, although the Ecuadorian government’s own digital currency is legal tender, Ecuador has explicitly banned Bitcoin, Ripple, and other types of virtual currency.114 Bolivia has a similar ban on virtual currency, but has not issued its own digital currency as a substitute.115 Perhaps because of these bans issued by its South American neighbors, authorities in Argentina and Brazil have issued warnings about the risks of using virtual currencies not recognized as legal; however, these countries have not banned virtual currency themselves.116 Africa There is limited data on the regulation of virtual currency throughout Africa.117 In South Africa, a joint statement issued by the National Treasury, the South African Reserve Bank, the Financial Services Board, the South African Revenue Service and the Financial Intelligence Centre confirmed that “[c]urrently in South Africa there are no specific laws or regulations that address the use of virtual currencies.”118 Therefore, the use of the virtual currency in the country is generally permissible. However, the same authorities warned against the risks of virtual currency, and also clarified that because of this unregulated status, “no legal protection or recourse is afforded to users of virtual currencies,” and “virtual currencies cannot be classified as legal tender as any merchant may refuse them as a payment instrument.”119 . Insuring Bitcoin and Bitcoin Business Companies that service the Bitcoin industry and its holders face risks unique to the bitcoin120 market, as well as to the financial services market generally. Thus, key questions for potential policyholders include how, if at all, insuring bitcoin is different from insuring other currencies? What insurance products currently exist that may cover bitcoin holders, servicers, and third-party vendors, and is the industry developing new types of coverage specific to bitcoin? And, to date, how has the insurance industry responded to claims made under those insurance policies? This chapter examines these questions and identifies practical concerns and tips for policyholders. Does Bitcoin Raise Unique Insurance and Underwriting Issues? Bitcoin is both an asset akin to currency and a protocol for digitally recording transactions. Viewed from this (simplified) perspective, insuring bitcoin holders, storage providers, exchanges, or related companies should be no different in terms of risk than any other business that safeguards or transfers an anonymous commodity, like cash, or that must protect its trade secrets or sensitive digital information. A variety of “traditional” insurance coverages exist, for example, to insure financial institutions and technology companies and their management, including network security and privacy liability (cyberliability) insurance, financial institution bonds and commercial crime insurance, directors’ and officers’ liability (D&O) insurance, and professional liability (E&O) insurance.

At least one court even has characterized bitcoin as equivalent to traditional assets like “money” or “securities,”121 suggesting that traditional insurance ought to respond to risks faced by the Bitcoin industry, just as insurance responds to similar risks in more established financial and technology industry sectors. But novel issues abound, as Bitcoin (and its derivatives) feature several unique characteristics. Unlike most “traditional” currencies, bitcoin requires no financial institutions to issue new currency and no banks to store it, and transactions may be anonymous and are nonreversible. Also, because Bitcoin is decentralized, and its software is open-source, there is limited control over the currency or technology beyond a core group of developers and dedicated individuals.

Thus, Bitcoin raises potentially unique issues with regulation, information security, price volatility, and reputation. Regulation As discussed in Chapters 3 and 4, governments have taken divergent approaches to regulating Bitcoin, with some outright banning cryptocurrencies altogether.122 The possibility remains that governments will impose substantial regulatory burdens or penalties on companies operating within the industry, including the risk of fines, application of anti-money laundering laws, and rigorous oversight by government agencies that range in focus from consumer protection to commodities regulation. Information Security The cryptocurrency industry is seeking consensus on how best to secure Bitcoin and other cryptocurrencies, and the companies that service cryptocurrency holders, including storage companies, trading platforms, and exchanges. Ownership of cryptocurrency is synonymous with knowing a private “key” associated with an address on the public chain of title (the “blockchain”). To conduct transactions, owners may use the services of a company acting as an intermediary to secure their private keys and run the software needed to spend bitcoin.

These companies take varied approaches to securing private keys in their possession. Some put private keys in “cold storage,” meaning keys are saved in computers not connected to the public Internet. Other companies utilize (among other methods) “multi-sig” technology that requires knowledge of multiple keys before a transfer of bitcoin is possible, with the company holding one key, the owner another, and a third retained offline as a backup.

Thus, neither the industry serving bitcoin users nor the users of the currency have yet identified preferred standards of asset protection. Price Volatility Bitcoin has risen and fallen in price dramatically since its introduction. Price volatility raises issues with respect to the financial strength of insured companies, the severity of the risks they face, and how to predict or quantify losses. Reputation Concerns Bitcoin’s infancy has been plagued by an association with criminal activity. Media reports often discuss Bitcoin in connection with cybercrime, including schemes to defraud, phishing attacks, and theft.

Bitcoin has also reportedly been used by criminals as an anonymous means of payment for drugs, extortion schemes, and other illegal activities. Insuring Bitcoin and Bitcoin Business Reed Smith LLP 15 . Given these issues and concerns, what can companies operating within the bitcoin economy expect? In short, a rigorous insurance underwriting process, and potentially a rigorous claims process when losses ultimately occur. Insurers may assess a company’s current practices and protocols concerning data, network and privacy security, physical protections for data held in cold storage, and breach or loss response. In the event of a loss, insurance policies may require rapid identification of the breach or loss, collection and preservation of information, mitigation of any damages or losses, and prompt notification to the insurance carrier. Due to the sensitivity of the information a policyholder may be required to share with insurers, both during the underwriting process and in the event of a loss, companies should insist on signing strong confidentiality agreements with insurers and brokers. Coverage counsel can help policyholders navigate these and other related issues both during placement of coverage and after a loss occurs. Potential Insurance Coverage Under Traditional Policies Although Bitcoin raises a number of novel issues, insurance companies may seek (and have sought) to insure the risks arising from this technology with wellestablished forms of coverage.

Some insurers also have begun developing hybrid forms of insurance coverage to address both the more traditional risks associated with the industry and the unique aspects of bitcoin and bitcoin technology. Cyberliability Cyberliability insurance is designed to address first-party losses and third-party liability as a result of data security breaches and the disclosure of or failure to protect private information. It commonly insures against (or helps defray) the cost of misappropriated data, investigating a breach, responding to regulators, defending against lawsuits, notifying affected persons, restoring or recreating any lost data, and paying damages and settlements, among other expenses. Cyberliability policies often are negotiable and may be tailored to a particular company or industry. Ideally, a cyberliability policy intended to cover Bitcoin or Bitcoin-related operations should be drafted broadly enough to cover issues unique to the currency and technology. The policy thus might insure against liability related to the company’s storage or exchange of bitcoin, corruption or breach of its associated technology, or losses due to a compromised vendor.

The definition of a liability event should be broad enough to include disclosure of or damage to the types of confidential information unique to Bitcoin, including users’ private keys. Security concerns or vulnerabilities particular to 16 Reed Smith LLP Insuring Bitcoin and Bitcoin Business bitcoin and bitcoin technology also should be addressed where possible, including the generation of flawed keys, transaction malleability attacks, 51 percent attacks intended to manipulate the blockchain, sybil attacks, and distributed denial of service attacks.123 Financial Institution Bonds and Commercial Crime Policies These policies insure against first-party losses caused by certain types of criminal, fraudulent or dishonest activity, including employee dishonesty, fraud, forgery, and extortion. Many bonds and commercial crime policies contain coverage for computer crimes and frauds that directly result from the use of a computer and result in the transfer of money, property, or securities from within the company to parties outside of the company. Businesses that use, keep, or perform services related to bitcoin should ensure that “bitcoin” is included in the definition of “money,” “currency,” “property” or any related terms or definitions that identify covered types of loss.124 Bitcoin transactions may be conducted “peer-topeer,” meaning the buyer and seller do not need to use a central exchange.

Companies should examine their potential exposure to losses arising from peer-to-peer transactions, because at least one insurer has publicly stated that peer-to-peer transactions are not covered under its commercial crime policy form.125 Social engineering and “phishing” attacks also are a threat to a Bitcoin business. A bad actor could seek to convince an employee that they are conducting a genuine transaction or sharing private information with a trustworthy recipient, when the employee is in fact an unwitting intermediary in a scheme to defraud. Social engineering attacks can implicate the “direct” causation and intent standards in many bonds and commercial crime policies.

Traditional financial institution bonds cover only losses “directly caused” by a covered activity. The “direct loss” standard is not uniformly interpreted by the courts and is a frequent source of insurance disputes. Some courts hold that the “direct loss” standard is equivalent to proximate causation under traditional tort law, but others hold that “direct loss” means that there can be no intervening cause between an action intended to cause harm and the harm itself. If the latter interpretation applies, it may be difficult to obtain insurance proceeds for losses caused by a social engineering or phishing attack on a bitcoin company. A recent lawsuit filed by bitcoin payment processor Bitpay, Inc.

against its commercial crime insurer illustrates this issue. 126 After a phishing attack compromised the email account of a Bitpay executive, the hacker used information collected from the executive’s email to induce the company to transfer funds to an ostensible customer wallet that was, in fact, . controlled by the hacker. Bitpay’s commercial crime insurer denied coverage, asserting that because the Bitpay executive acted as an unwilling intermediary in the scheme, the loss was not “directly caused” by the activity of the hacker. (Bitpay’s lawsuit remains pending as of this writing.) In addition, many policies require “manifest intent” by an employee before a loss caused by employee dishonesty is insured, a phrase sometimes interpreted by courts to mean that an employee must not only intend to personally gain from his or her dishonesty, but also to intend to harm the company. Thus, an insurer may assert a defense to coverage if a defalcating employee’s intent was directed at the bitcoin holder, not the company. D&O Insurance D&O insurance is designed to protect a company’s directors and officers, and often to a more limited extent, the company, against third-party liability.

D&O policies commonly insure individual directors and officers when they cannot be indemnified by their companies (“Side A” coverage), the company when it pays indemnification to its directors and officers (“Side B” coverage), and the company in connection with lawsuits alleging violations of the securities laws (“Side C” coverage). Monetary damages may be covered, but property damage generally is not. D&O insurance often can be negotiated. Although a variety of D&O policy provisions should be tailored to Bitcoin-related risks, three are of particular note.

First, any Bitcoin-related company should ensure its policy will cover securities lawsuits triggered by a loss of bitcoin or damage to the company’s bitcoin operations. Second, given the prevalence of criminal activity related to the currency and technology, as well as the uncertain regulatory environment, the insurance policy should clearly insure the costs of cooperating with government investigations, inquiries, and any administrative proceedings related to Bitcoin. Finally, companies should pay attention to any exclusion for loss arising from professional services provided by the company. E&O Insurance E&O insurance is designed to protect individuals and companies from liability for mistakes, omissions, and other errors made in the performance of a professional service. E&O polices can be tailored to specific risks and are frequently negotiable.

Every company that provides services related to bitcoin in return for a fee – whether they host or maintain customer “wallets,” operate exchanges, facilitate transactions, or provide any of the myriad services relevant to the industry – can potentially benefit from having E&O insurance. A lawsuit accusing a company of an error, even if frivolous or baseless, could result in substantial legal expenses and reputational damage. Would a traditional E&O policy cover a financial institution utilizing new bitcoin technology, such as a financial institution implementing blockchain technology, to record and maintain the ledger of private stock transactions? Although many E&O policies broadly define what constitutes a covered “professional services,” E&O policies are not entirely uniform among different insurers and different industries and may be tailored to specific risks, and thus the definition of “professional services” may or may not automatically include such services. For instance, many E&O policies issued to financial institutions define “professional services” simply as those services provided by the insureds to a customer or client for a fee or other form of compensation or services.