The Real Economy - Here is why recession fears are overblown March 2016 Volume 15

RSM US (formerly McGladrey)

Description

THE REAL

ECONOMY

MARCH 2016 I VOLUME 15

FEAR A SLOWDOWN?

HERE’S WHY RECESSION FEARS ARE OVERBLOWN

NEAR-TERM RECESSION FEARS ARE

OVERBLOWN, BUT HERE ARE THE SEEDS

OF THE NEXT ECONOMIC DOWNTURN

DIMINISHING OPPORTUNITIES AMID

EXCESS CAPITAL TO DRIVE REAL ESTATE

DEAL FLOW IN 2016

REAL ESTATE OUTLOOK Q&A

. THOUGHT LEADERS

Our thought leaders are professionals with years of experience in their

fields who strive to help you and your business succeed. Thought leaders

who have contributed content to this issue include:

Joe Brusuelas is the chief economist for RSM US LLP. Brusuelas has 20 years of experience analyzing

U.S. monetary policy, labor markets, fiscal policy, economic indicators and the condition of the U.S.

consumer.

As co-founder of the award-winning Bloomberg Economics Brief, Brusuelas was named one of the 26 economists to follow by the Huffington Post. He is a graduate of the University of Southern California and San Diego State University. Rick Edelheit is the national real estate leader for RSM US LLP. He oversees all activities across a broad array of services, including assurance, tax, transactional due diligence, lease consulting, financial reporting outsourcing, cost segregation and other consulting services. Tom Green is the assurance lead of the national real estate practice at RSM US LLP.

He is the regional leader of the Great Lakes real estate practice and the practice lead for real estate private equity and opportunity funds. Green is the lead partner for several of the firm’s largest real estate clients. He specializes in audits of large multi-investment real estate portfolio companies and the consolidation and fair value reporting issues related to those concerns. 2 | MARCH 2016 .

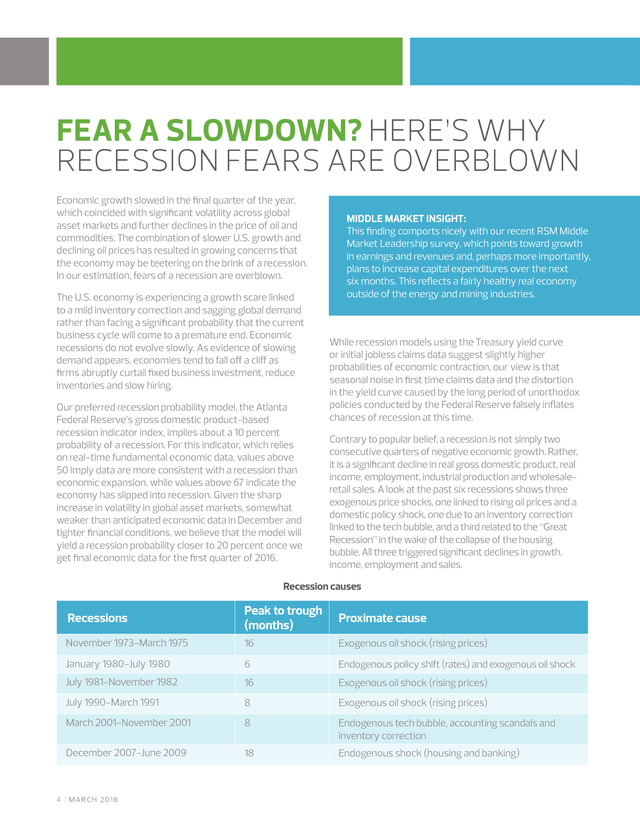

TABLE OF CONTENTS Fear a slowdown? Here’s why recession fears are overblown 4 Near-term recession fears are overblown, but here are the seeds of the next economic downturn 6 Diminishing opportunities amid excess capital to drive real estate deal flow in 2016 8 2016 Real estate outlook Q & A RSM Industry coverage 10 11 This publication represents the views of the author(s), and does not necessarily represent the views of RSM. This publication does not constitute professional advice. RSM | TH E RE A L ECO N O MY | 3 . FEAR A SLOWDOWN? HERE’S WHY RECESSION FEARS ARE OVERBLOWN Economic growth slowed in the final quarter of the year, which coincided with significant volatility across global asset markets and further declines in the price of oil and commodities. The combination of slower U.S. growth and declining oil prices has resulted in growing concerns that the economy may be teetering on the brink of a recession. In our estimation, fears of a recession are overblown. The U.S. economy is experiencing a growth scare linked to a mild inventory correction and sagging global demand rather than facing a significant probability that the current business cycle will come to a premature end.

Economic recessions do not evolve slowly. As evidence of slowing demand appears, economies tend to fall off a cliff as firms abruptly curtail fixed business investment, reduce inventories and slow hiring. Our preferred recession probability model, the Atlanta Federal Reserve’s gross domestic product-based recession indicator index, implies about a 10 percent probability of a recession. For this indicator, which relies on real-time fundamental economic data, values above 50 imply data are more consistent with a recession than economic expansion, while values above 67 indicate the economy has slipped into recession.

Given the sharp increase in volatility in global asset markets, somewhat weaker than anticipated economic data in December and tighter financial conditions, we believe that the model will yield a recession probability closer to 20 percent once we get final economic data for the first quarter of 2016. MIDDLE MARKET INSIGHT: This finding comports nicely with our recent RSM Middle Market Leadership survey, which points toward growth in earnings and revenues and, perhaps more importantly, plans to increase capital expenditures over the next six months. This reflects a fairly healthy real economy outside of the energy and mining industries. While recession models using the Treasury yield curve or initial jobless claims data suggest slightly higher probabilities of economic contraction, our view is that seasonal noise in first time claims data and the distortion in the yield curve caused by the long period of unorthodox policies conducted by the Federal Reserve falsely inflates chances of recession at this time. Contrary to popular belief, a recession is not simply two consecutive quarters of negative economic growth. Rather, it is a significant decline in real gross domestic product, real income, employment, industrial production and wholesaleretail sales.

A look at the past six recessions shows three exogenous price shocks, one linked to rising oil prices and a domestic policy shock, one due to an inventory correction linked to the tech bubble, and a third related to the “Great Recession” in the wake of the collapse of the housing bubble. All three triggered significant declines in growth, income, employment and sales. Recession causes Recessions Peak to trough (months) Proximate cause November 1973-March 1975 16 Exogenous oil shock (rising prices) January 1980-July 1980 6 Endogenous policy shift (rates) and exogenous oil shock July 1981-November 1982 16 Exogenous oil shock (rising prices) July 1990-March 1991 8 Exogenous oil shock (rising prices) March 2001-November 2001 8 Endogenous tech bubble, accounting scandals and inventory correction December 2007-June 2009 18 Endogenous shock (housing and banking) 4 | MARCH 2016 . Recession probability model 110.0 Recessions Recession probability index 100.0 Percentage probability 90.0 80.0 70.0 60.0 50.0 40.0 30.0 20.0 10.0 0.0 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Source: RSM US, Federal Reserve So where are we now? The current business cycle is on pace to be one of the longest expansions in the post-World War II era. While growth remains slow by historical standards, the risk of a recession based on the proximate causes of the past six recessions remains low. The following is a quick synopsis that underscores our estimation that the current expansion will continue through 2016 and into 2017. Policy: The primary policy risk remains firmly rooted in the path of interest rates. While the central bank increased the federal funds rate by 25 basis points in December, recent testimony by Fed Chair Janet Yellen, and the January Federal Reserve Open Market Committee minutes make it clear that rates may move higher at a very slow pace. At this time, the market is pricing in one 25 basis point rate hike this year, which is below our forecast of 50 basis points.

Due to the policy polarization in Washington, there is little risk of a fiscal shock that could cause a recession this year. Inventory correction: Historically, the two most likely indicators of recession are inventory overhangs in the auto and housing industries. Through the end of the year, the major auto producers had about 61 days of inventory in showrooms (65 days is considered equilibrium), which implied a pickup in production early this year. The housing sector is actually experiencing an inventory shortfall as the building community is having problems finding enough workers to build new homes and there simply aren’t enough existing homes on the market to meet demand. Exogenous shocks: Sharp increases in oil prices caused recessions in 1973, 1981 and 1990.

Currently, the United States is experiencing a positive supply shock thanks to an increase in the extraction of oil linked to the domestic use of hydraulic fracking. Meanwhile, falling gasoline prices have resulted in an increase in real income for U.S. households. Sustained low oil and natural gas prices should result in cheaper costs of production for domesticallybased industries. Asset bubbles: The greatest risk of recession is clearly linked to the recent sell off in U.S.

equity markets. The Standard and Poor’s 500 index is down 9.73 percent from its cyclical peak of 2,130.82 in May of last year. The rotation in portfolio exposure away from China, energy, commodities and financials may be quite noisy but isn’t enough on its own to cause an economic contraction. Meanwhile, the linkages between asset markets and the real economy is quite limited. Fundamentals: Declining unemployment, rising wages, a noticeable increase in inflation-adjusted income and solid wholesale-retail sales all suggest that there is more than enough economic activity to offset the contraction in the manufacturing sector.

Moreover, the January industrial production report indicated a modest rebound in factory orders, and production excluding motor vehicles are consistent with our forecast for a mild recovery in the manufacturing sector this year. While it is still early in the quarterly data cycle, GDP is tracking near 2.7 percent in the first quarter of the year, which suggests a strong rebound after last quarter’s slowdown and is consistent with our preferred recession probability model which implies a low risk for recession. RSM | TH E RE A L ECO N O MY | 5 . NEAR-TERM RECESSION FEARS ARE OVERBLOWN, BUT HERE ARE THE SEEDS OF THE NEXT ECONOMIC DOWNTURN During the first two months of 2016, risk appetite in financial markets turned decisively negative and investors began pricing in a much slower economy than what has actually occurred. The key question that needs to be addressed now is, what are the major causes behind the shift in sentiment and do those factors carry enough elements of a negative self-fulfilling prophecy to turn what has been a modest correction in asset prices into an end to the business cycle? value of the yuan, we anticipate that they will choose growth via lower rates and a cheaper currency, which runs the risk of causing an increase in capital outflows and of the $3.1 trillion in currency reserves the country says it possesses. If the fiscal authority loses control and the yuan depreciates at a more rapid pace than the 3.5 percent implied by the nondeliverable forward market, this runs the risk of a major disruption in competitiveness and global trade. Several major concerns among global investors and firm managers have emerged that together may contain the seeds of the next economic downturn. China debt burden becoming worrisome Moreover, with corporate debt standing at 160 percent of GDP, and household debt as a percentage of GDP at 36 percent, there is legitimate concern about where a rebound in growth will originate. Thus, with the People’s Bank of China (PBOC) facing a choice between stabilizing growth or the 6 | MARCH 2016 160 140 Percentage (annual) 220 120 210 100 200 80 190 60 180 Percentage (annual) Capital outflows were close to $1 trillion in 2015, which caused fiscal and monetary authorities to use $1 trillion to prop up equity markets and support the currency. Given that total debt-to-GDP in China rose above 260 percent as of the end of 2014, and likely soared above 300 percent last year, there are questions regarding what steps the fiscal authority could take to support growth without intensifying the debt and deleveraging cycle that has begun. 180 230 China: The economic slowdown in China has been much sharper than contained by official statistics.

Electricity demand on a year-ago basis turned negative in 2015 and implies a growth rate closer to 3 percent, much less than the 7 percent policymaker target. 240 40 China total debt as percentage of GDP (lhs) 170 20 China corporate debt as percentage of GDP (rhs) 160 2006 2007 2008 2009 2010 2011 2012 2013 2014 0 2015 Source: RSM US, Bloomberg European banking: Growing concerns about the ability of euro-area banks’ ability to cover contingent convertible bonds, which would require another round of recapitalization to avoid investor losses, have caused credit default swaps on select European banks to noticeably widen to levels last seen in 2012, at the height of the European sovereign debt crisis. Widening credit default swaps (CDS) spreads are related to falling commodity prices and deflation risk in Europe. . Global oil markets: Oil prices have yet to find a price floor, which is feeding into fears of a global recession based on a combination of oversupply and falling demand, especially from China and emerging markets. Meanwhile, OPEC countries haven’t been able to reach an agreement to curtail or freeze production. Credit default swaps on European banks widening 400 S&P/ISDA CDS select OTR-weighted average index spread DB five-year credit default swaps 350 300 Index 250 200 150 100 50 0 2012 2013 2014 2015 2016 Source: RSM US, Bloomberg In our 2016 year-ahead growth forecast, we noted there was a risk that the price of oil may fall to about $20 per barrel, just above the inflation-adjusted low of $17.26 reached in 1998 ($11.91 in non-inflation-adjusted terms). Given the 70 percent decline in oil prices since June 2014, countries such as Venezuela, Nigeria and Russia have fallen into economic depression and may choose to default on global debt obligations. During a time of regional geopolitical tensions, global investors and firm managers with exposure to the region are rightfully concerned that conditions could deteriorate and spillover into global financial markets. Central banking: Investor confidence in global central banks appears to be waning. There is a growing impression that central banks have reached the outer limits of conventional and nonconventional policies to support growth.

Moreover, with the Federal Reserve unlikely to push rates up the 400 basis points that is typically needed to provide monetary accommodation during economic downturns, there is a fear that the Fed will need to resort to a negative interest rate policy during the next recession, which will negatively affect financial institutions. Fiscal policy: With interest rates near zero, and real interest rates in the developed economies negative, a rational economic choice would be to turn to fiscal policy to support growth during an economic slowdown. Monetary policy is constrained by the zero bound, so policymakers would get more bang for the buck, so to speak, through fiscal policy. That, however, has not been the choice of decisionmakers in the major economies.

In Europe, the choice has been austerity, which triggered a bout of deflation that the continental economy has yet to recover from. In the United States, political polarization and stark ideological differences have, until very recently, resulted limited fiscal support for the economy. We have made the case that, with borrowing costs near zero in the United States, conditions are ripe for a $1 trillion infrastructure project that could be financed out over 30 or even 50 years.

The greater concern going forward is that if fiscal policy is off the table, what policy flexibility do decision-makers have if the business cycle ends during the next two to three years? MIDDLE MARKET INSIGHT: Direct concerns about a possible increase in tariffs on imported goods, a reduction in foreign labor and punitive taxation on businesses to fund a rapid expansion of government-supported entitlements has shocked many middle market firms. In our estimation, unless the electoral equation changes soon, there is a risk that fixed business investment, which as a percentage of GDP has only recovered to Clinton-era levels, could slow noticeably and is a potential harbinger of the next economic downturn. U.S. political risk: During the past four decades, the federal government has been more or less friendly to business and global commerce.

However, in this election year, the leading candidates in both political parties are promising to overturn the commercial consensus that has prevailed since the early 1980s. For the first time in recent memory, firms are looking at how they may need to price U.S. political risk into the cost of business operations. RSM | TH E RE A L ECO N O MY | 7 . DIMINISHING OPPORTUNITIES AMID EXCESS CAPITAL TO DRIVE REAL ESTATE DEAL FLOW IN 2016 With interest rates relatively low and periods of high volatility in equity markets, real estate will likely continue to draw investor interest that is sure to spark more dealmaking in 2016. Transaction activity in commercial real estate will be dominated by multifamily housing that is expected to draw greater investor interest and stir up more development. “You go around the country and you see more cranes going up. Multifamily is still a good place to be,” says Richard Edleheit, national real estate leader for RSM US LLP. “People are changing the way they are living. More and more people are living in the city,” says Tom Green, partner and assurance lead at RSM’s national real estate practice. According to Green, this shift in living patterns has not gone by unnoticed by private equity investors and pensions.

Pensions are increasingly putting their money to work directly into the asset class; some, for example, will partner up with a designated real estate company that tailors a specific investment platform for them. Mortgage rates, 5-year ARM 4.00 Much of this activity is tied to changes in attitudes about homeownership and affordability. Some recent government data show that as homeownership rates in the single-family arena have slid down to levels not seen since the mid-1990s, vacancy rates for multifamily properties are also down to 20-year lows. Some of that shift may be tied to affordability issues that keep some consumers from buying a single-family home, but much of it likely is a change in the tastes of the U.S. population. 8 | MARCH 2016 5-year ARM rate 3.80 3.60 3.40 Mortgage rate (percentage) Multifamily starts will likely see an increase in activity in 2016 from 2015 and 2014, according to projections made by the Mortgage Bankers Association.

Earlier this year, the industry group said it expects commercial and multifamily mortgage banker originations to set a new record and surpass the $508 billion mark of 2007. “You will continue to see development in the larger gateway markets of the United States and you will see it in secondary cities such as Austin, Portland, Nashville, Charlotte and similar cities,” says Edelheit. “We are going to see plenty of real estate activity in the marketplace.” 3.20 3.00 2.80 2.60 2.40 2.20 2.00 1/14/2011 1/14/2012 1/14/2013 1/14/2014 1/14/2015 Source: Mortgage Bankers Association In addition to demographics, the development in commercial real estate such as multifamily housing is being driven by private equity funds eager to put money to work. A November survey of private equity real estate fund managers—the results of which were published in February 2016—found that “finding attractive investment opportunities” is the single biggest challenge faced by a majority of the survey’s respondents.

Investors—90 . Refi and purchase indexes Demographics have not just reshaped how investors view multifamily housing. They have forced institutional investors to focus on facilities designed to cater to the needs of an ageing population. MBA refi index MBA purchase index 6,000 300 200 4,000 150 3,000 MBA purchase index MBA refinance index 250 5,000 100 2,000 1,000 1/10 50 0 10/10 7/11 4/12 1/13 10/13 7/14 4/15 Source: Mortgage Bankers Association percent of them said their investment in the asset class met or exceeded their expectations - are conducting more due diligence and they are expanding their investment teams. Of those fund managers surveyed, 67 percent say it is more difficult to find attractive investment opportunities than one year ago. That collision of diminishing opportunities and excess capital may also serve as a reminder to market participants of the importance of keeping up with stringent due diligence, say Green and Edelheit. Other segments of commercial real estate that likely will continue to see more activity in 2016 are retail and continuing care properties. When it comes to brick-and-mortar locations, retailers are shifting how they use and present their physical space to customers. For example, auto dealers are rearranging floor plans of sales outlets – borrowing design elements from mobile phone retail outlets that involve fewer desks and use more open space.

Then, there is what may be the biggest development for retail investors: the possibility that Amazon may open some physical store locations. “Things are ever evolving,” says Green. “The demographics alone have made this an attractive space for investors and developers,” says Green. “We are seeing a lot of conversions of former use properties into senior housing. We are starting to see more funds just focused on these health care opportunities.

It is really something that is attractive to all corners of America because of the demographics.” Despite changing preferences, the single-family world of real estate is also expected to be active this year, according to Green and Edelheit. 5.50 Mortgage rates, 30 year & 15 year contract Fixed rate 30-year contract rate Fixed rate 15-year contract rate 5.00 Mortgage Rates (%) 350 7,000 4.50 4.00 3.50 3.00 2.50 2.00 1/10 7/10 1/11 7/11 1/12 7/12 1/13 7/13 1/14 7/14 1/15 7/15 1/16 Source: Mortgage Bankers Association Mortgage lenders are expected to have their hands full in 2016 when it comes to applications to buy home loans and the business of refinancing existing mortgages. In February, refinancing alone accounted for over 60 percent of all single-family home loans processed by lenders–a high not seen since February 2014. Whether this type of business dominates lender activity for the rest of the year is unclear. Much of that activity will be shaped by the direction of U.S. Treasury rates.

“With low rates, continuous refinancing is wonderful for the mortgage bankers,” says Green. RSM | TH E RE A L ECO N O MY | 9 . Q&A 2016 REAL ESTATE OUTLOOK RICK EDELHEIT AND TOM GREEN Q: What should we expect for the real estate markets in 2016? Rick: Notwithstanding some hiccups in the global marketplace, we are going to see some of the same trends we saw in 2015. We are going to see plenty of real estate activity in the marketplace, both acquisitions and dispositions. Cap rates will continue to stay a bit low, which is what we have seen in the last handful of years. We might see some international funds coming into the United States. Q: With all of the heightened investor interest, is the real estate market too hot and how is that impacting loan standards? Rick: As we see more and more transactions, the biggest concern is underwriting.

Sometimes with more deals getting done, there is actually less due diligence. If we start seeing bigger deals, and we are not being called upon to provide underlying financial due diligence services, we know that things are going on in the marketplace that start to look a little bit cavalier. If we are representing the lender, at times, what we will see is that they have a bogey set in which they are mandated to have due diligence.

If that bogey starts to climb higher from a $100 million loan to a $150 million loan, then we know by definition that the underwriting process can be negatively impacted. Q: Is any property type more active in real estate? Rick: Residential property values are continuing to climb, and as they climb, to a certain extent, it makes it more difficult for homeowners to buy homes. So, multifamily is still a good place to be and it will continue to be a good place to be for quite a while. You will continue to see development, in particular, in the larger MSAs in the United States. You are seeing more and more people coming back into the cities.

We are going to see it in secondary markets as well. We will see more development in multifamily. You go around the country and you see more cranes going up. When it comes to energy prices, the reduced price of oil is going to enhance net operating income and returns to investors. Q: What is your view on recent data that shows homeownership rates falling to lows not seen since the mid-1990s? Tom: People are changing the way they live and on top of that you have millennials. More and more people are moving into cities, and you are seeing more development of multifamily properties. Q: How do private equity funds fit into your outlook? Tom: Over the next year or two, we are going to continue to see a lot of activity in commercial real estate and that has to do with the available capital that private equity companies are sitting on and the entry of foreign investors into the U.S.

market. That’s 10 | MARCH 2016 really keeping prices somewhat inflated and capital rates low. That will continue for a while. Rick: There are private equity companies that are focused on the single-family home rental strategy. The amount of single-family homes that have been accumulated by this handful of companies has been very substantial.

They have spent a lot of money developing the infrastructure to support that investment. Tom: Property values are climbing, generally speaking, across the country. In Chicago, we are starting to see a nice increase in the values of homes. I think that—maybe except for an area like Houston which may be hit by the impact of oil—most of the United States has seen an appreciation in value. Q: What is your outlook for retail, industrial and retirement community properties? Rick: In 2015, retail had a very good year, probably better than was expected.

As long as your retailers continue to change with the times to reinvent themselves, brick-and-mortar will continue to be here. Tom: Industrial properties have been strong. It has certainly been an active market. The demographics alone have made continuing care properties an attractive space for investors and developers. We are seeing a lot of conversions of former use properties into senior housing, whether it is assisted living or independent living. If you take the entire spectrum, these continuing-care retirement communities are pretty attractive.

We are starting to see more funds solely focused on these health care opportunities. There is a lot of ground-up development, and it is something that is attractive to all corners of America because of the demographics. Rick: You have a lot of baby boomers that have been very successful over the last four years and what you are finding is that baby boomer needs are different than what they used to be. Some of the answer, and opportunity, has been through the development of high-end facilities. Q: When it comes to changes in accounting treatments, are there any issues we should consider when it comes to leasing? Tom: There are some proposed changes related to lease accounting that have not been finalized yet.

It will probably have a bigger impact on tenants and it has to do more with them having to onboard the lease liability onto their balance sheet. Previously, they recognized it as an income statement item in terms of reflecting the current-year lease activity. The thought is that this is going to have a big impact because it will dramatically affect the way the balance sheet looks.

And, it will have an impact on certain financial metrics and ratios that are key to allowing them to do business, especially on the borrowing side. . RSM INDUSTRY COVERAGE SPECIALTY FINANCE Deterring and detecting internal and external fraud for specialty lenders RSM recently conducted research among specialty finance firms on both internal and external fraud and found that roughly half of all surveyed firms had experienced fraud. While fraud losses tended to be relatively low, they are almost never recovered. Half of the companies that experienced one form of fraud also experienced the other, which seems to indicate a relatively lax internal control environment at those companies and underscores the importance of effective controls. Partner Ronnie Lee outlined the issues and then ways to detect and deter fraud in this article. Details of the study can be found here. LAW FIRMS Law firm look-back and outlook Barry Rosenthal, leader for the national business and professional services practice, reviewed trends shaping, and shaking up, the law firms.

In a Q&A, Rosenthal found that firms are expanding their global knowledge and presence to tap into a global economy, who are doing business worldwide. Law firms are also looking to control costs through the use of artificial intelligence (AI) to handle routine work such as document scanning. Another cost trend: firms are rethinking their office space to reduce the cost of rent, which is the second largest firm cost, after compensation.

On the practice side, litigation and bankruptcy work is down, while M&A work is rising, which is good news for firms with private equity and real estate clients. Growth in technology and life sciences is also spurring an increase in intellectual property work. For the complete Q&A, look here. activities or expenditures may not be prohibited, depending on the facts and circumstances.

So, certain voter education activities—including presenting public forums and publishing voter education guides—conducted in a nonpartisan manner do not constitute prohibited political campaign activity. This white paper by partner James Sweeney looks at the do’s and don’ts of elections, with six situations where section 501(c)(4), (5) or (6) organizations have entered into political activities. TECHNOLOGY AND MANAGEMENT CONSULTING Leveraging the third platform: New technology enhances business insights The latest step in the technology environment is called the third platform. It consists of resources that add dimensions and information capabilities to help you make better business decisions and increase revenue.

These resources include: •• Mobility •• Cloud computing •• Social media •• The Internet of Things •• Big data The third platform’s rise reflects increased computer processing power, enhanced mobile technologies and evolving demographics. To leverage the opportunities, organizations must evaluate the technology budget and existing priorities, and make changes to properly integrate the new technology. RSM principals, Jim Klimkowski and Bill Kracunas, provide more details on the sources of value and ideas for implementation in the complete article, available here. NONPROFIT PRIVATE EQUITY Election year do’s and don’ts for nonprofits In a seller’s market, accelerating the deal close is critical—and risky The start of the 2016 general election is a good time for taxexempt organizations to review their compliance with political regulations. Under the Internal Revenue Code, all section 501(c)(3) organizations are absolutely prohibited from directly or indirectly participating in, or intervening in, any political campaign on behalf of (or in opposition to) any candidate for elective public office.

Contributions to political campaign funds and public statements of position (verbal or written) made on behalf of the organization in favor of or in opposition to any candidate for public office clearly violate the prohibition against political campaign activity. Violating this prohibition may result in denial or revocation of tax-exempt status and the imposition of certain excise taxes. However, certain Private equity firms sometimes race to close deals within 30 days of letters of intent (LOIs).

Competition is intense—and sellers know it. But closing a deal too quickly—before truly understanding the business, its people and systems—can hold back growth potential, lead to unexpected costs and destroy value in the long term. Striking the right balance between speed and thoroughness is especially challenging, and may require investing in additional resources to close the deal on time and according to plan.

RSM principal, Christina Churchill, and director, Dennis Cail, examine the risks and responses to fast closes using examples of a family-owned business, a new industry and a carve-out, in this piece from RSM’s Insight newsletter. RSM | TH E RE A L ECO N O MY | 11 . For more information on RSM, please visit www.rsmus.com. For media inquiries, please contact Terri Andrews, National Public Relations Director, +1 980 233 4710 or Terri.Andrews@rsmus.com. www.rsmus.com This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. RSM US LLP, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services.

This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed. RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other.

Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International. RSM® and the RSM logo are registered trademarks of RSM International Association. The power of being understood® is a registered trademark of RSM US LLP. © 2016 RSM US LLP.

All Rights Reserved. TRE-NT-ALL-ALL-0315 .

As co-founder of the award-winning Bloomberg Economics Brief, Brusuelas was named one of the 26 economists to follow by the Huffington Post. He is a graduate of the University of Southern California and San Diego State University. Rick Edelheit is the national real estate leader for RSM US LLP. He oversees all activities across a broad array of services, including assurance, tax, transactional due diligence, lease consulting, financial reporting outsourcing, cost segregation and other consulting services. Tom Green is the assurance lead of the national real estate practice at RSM US LLP.

He is the regional leader of the Great Lakes real estate practice and the practice lead for real estate private equity and opportunity funds. Green is the lead partner for several of the firm’s largest real estate clients. He specializes in audits of large multi-investment real estate portfolio companies and the consolidation and fair value reporting issues related to those concerns. 2 | MARCH 2016 .

TABLE OF CONTENTS Fear a slowdown? Here’s why recession fears are overblown 4 Near-term recession fears are overblown, but here are the seeds of the next economic downturn 6 Diminishing opportunities amid excess capital to drive real estate deal flow in 2016 8 2016 Real estate outlook Q & A RSM Industry coverage 10 11 This publication represents the views of the author(s), and does not necessarily represent the views of RSM. This publication does not constitute professional advice. RSM | TH E RE A L ECO N O MY | 3 . FEAR A SLOWDOWN? HERE’S WHY RECESSION FEARS ARE OVERBLOWN Economic growth slowed in the final quarter of the year, which coincided with significant volatility across global asset markets and further declines in the price of oil and commodities. The combination of slower U.S. growth and declining oil prices has resulted in growing concerns that the economy may be teetering on the brink of a recession. In our estimation, fears of a recession are overblown. The U.S. economy is experiencing a growth scare linked to a mild inventory correction and sagging global demand rather than facing a significant probability that the current business cycle will come to a premature end.

Economic recessions do not evolve slowly. As evidence of slowing demand appears, economies tend to fall off a cliff as firms abruptly curtail fixed business investment, reduce inventories and slow hiring. Our preferred recession probability model, the Atlanta Federal Reserve’s gross domestic product-based recession indicator index, implies about a 10 percent probability of a recession. For this indicator, which relies on real-time fundamental economic data, values above 50 imply data are more consistent with a recession than economic expansion, while values above 67 indicate the economy has slipped into recession.

Given the sharp increase in volatility in global asset markets, somewhat weaker than anticipated economic data in December and tighter financial conditions, we believe that the model will yield a recession probability closer to 20 percent once we get final economic data for the first quarter of 2016. MIDDLE MARKET INSIGHT: This finding comports nicely with our recent RSM Middle Market Leadership survey, which points toward growth in earnings and revenues and, perhaps more importantly, plans to increase capital expenditures over the next six months. This reflects a fairly healthy real economy outside of the energy and mining industries. While recession models using the Treasury yield curve or initial jobless claims data suggest slightly higher probabilities of economic contraction, our view is that seasonal noise in first time claims data and the distortion in the yield curve caused by the long period of unorthodox policies conducted by the Federal Reserve falsely inflates chances of recession at this time. Contrary to popular belief, a recession is not simply two consecutive quarters of negative economic growth. Rather, it is a significant decline in real gross domestic product, real income, employment, industrial production and wholesaleretail sales.

A look at the past six recessions shows three exogenous price shocks, one linked to rising oil prices and a domestic policy shock, one due to an inventory correction linked to the tech bubble, and a third related to the “Great Recession” in the wake of the collapse of the housing bubble. All three triggered significant declines in growth, income, employment and sales. Recession causes Recessions Peak to trough (months) Proximate cause November 1973-March 1975 16 Exogenous oil shock (rising prices) January 1980-July 1980 6 Endogenous policy shift (rates) and exogenous oil shock July 1981-November 1982 16 Exogenous oil shock (rising prices) July 1990-March 1991 8 Exogenous oil shock (rising prices) March 2001-November 2001 8 Endogenous tech bubble, accounting scandals and inventory correction December 2007-June 2009 18 Endogenous shock (housing and banking) 4 | MARCH 2016 . Recession probability model 110.0 Recessions Recession probability index 100.0 Percentage probability 90.0 80.0 70.0 60.0 50.0 40.0 30.0 20.0 10.0 0.0 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Source: RSM US, Federal Reserve So where are we now? The current business cycle is on pace to be one of the longest expansions in the post-World War II era. While growth remains slow by historical standards, the risk of a recession based on the proximate causes of the past six recessions remains low. The following is a quick synopsis that underscores our estimation that the current expansion will continue through 2016 and into 2017. Policy: The primary policy risk remains firmly rooted in the path of interest rates. While the central bank increased the federal funds rate by 25 basis points in December, recent testimony by Fed Chair Janet Yellen, and the January Federal Reserve Open Market Committee minutes make it clear that rates may move higher at a very slow pace. At this time, the market is pricing in one 25 basis point rate hike this year, which is below our forecast of 50 basis points.

Due to the policy polarization in Washington, there is little risk of a fiscal shock that could cause a recession this year. Inventory correction: Historically, the two most likely indicators of recession are inventory overhangs in the auto and housing industries. Through the end of the year, the major auto producers had about 61 days of inventory in showrooms (65 days is considered equilibrium), which implied a pickup in production early this year. The housing sector is actually experiencing an inventory shortfall as the building community is having problems finding enough workers to build new homes and there simply aren’t enough existing homes on the market to meet demand. Exogenous shocks: Sharp increases in oil prices caused recessions in 1973, 1981 and 1990.

Currently, the United States is experiencing a positive supply shock thanks to an increase in the extraction of oil linked to the domestic use of hydraulic fracking. Meanwhile, falling gasoline prices have resulted in an increase in real income for U.S. households. Sustained low oil and natural gas prices should result in cheaper costs of production for domesticallybased industries. Asset bubbles: The greatest risk of recession is clearly linked to the recent sell off in U.S.

equity markets. The Standard and Poor’s 500 index is down 9.73 percent from its cyclical peak of 2,130.82 in May of last year. The rotation in portfolio exposure away from China, energy, commodities and financials may be quite noisy but isn’t enough on its own to cause an economic contraction. Meanwhile, the linkages between asset markets and the real economy is quite limited. Fundamentals: Declining unemployment, rising wages, a noticeable increase in inflation-adjusted income and solid wholesale-retail sales all suggest that there is more than enough economic activity to offset the contraction in the manufacturing sector.

Moreover, the January industrial production report indicated a modest rebound in factory orders, and production excluding motor vehicles are consistent with our forecast for a mild recovery in the manufacturing sector this year. While it is still early in the quarterly data cycle, GDP is tracking near 2.7 percent in the first quarter of the year, which suggests a strong rebound after last quarter’s slowdown and is consistent with our preferred recession probability model which implies a low risk for recession. RSM | TH E RE A L ECO N O MY | 5 . NEAR-TERM RECESSION FEARS ARE OVERBLOWN, BUT HERE ARE THE SEEDS OF THE NEXT ECONOMIC DOWNTURN During the first two months of 2016, risk appetite in financial markets turned decisively negative and investors began pricing in a much slower economy than what has actually occurred. The key question that needs to be addressed now is, what are the major causes behind the shift in sentiment and do those factors carry enough elements of a negative self-fulfilling prophecy to turn what has been a modest correction in asset prices into an end to the business cycle? value of the yuan, we anticipate that they will choose growth via lower rates and a cheaper currency, which runs the risk of causing an increase in capital outflows and of the $3.1 trillion in currency reserves the country says it possesses. If the fiscal authority loses control and the yuan depreciates at a more rapid pace than the 3.5 percent implied by the nondeliverable forward market, this runs the risk of a major disruption in competitiveness and global trade. Several major concerns among global investors and firm managers have emerged that together may contain the seeds of the next economic downturn. China debt burden becoming worrisome Moreover, with corporate debt standing at 160 percent of GDP, and household debt as a percentage of GDP at 36 percent, there is legitimate concern about where a rebound in growth will originate. Thus, with the People’s Bank of China (PBOC) facing a choice between stabilizing growth or the 6 | MARCH 2016 160 140 Percentage (annual) 220 120 210 100 200 80 190 60 180 Percentage (annual) Capital outflows were close to $1 trillion in 2015, which caused fiscal and monetary authorities to use $1 trillion to prop up equity markets and support the currency. Given that total debt-to-GDP in China rose above 260 percent as of the end of 2014, and likely soared above 300 percent last year, there are questions regarding what steps the fiscal authority could take to support growth without intensifying the debt and deleveraging cycle that has begun. 180 230 China: The economic slowdown in China has been much sharper than contained by official statistics.

Electricity demand on a year-ago basis turned negative in 2015 and implies a growth rate closer to 3 percent, much less than the 7 percent policymaker target. 240 40 China total debt as percentage of GDP (lhs) 170 20 China corporate debt as percentage of GDP (rhs) 160 2006 2007 2008 2009 2010 2011 2012 2013 2014 0 2015 Source: RSM US, Bloomberg European banking: Growing concerns about the ability of euro-area banks’ ability to cover contingent convertible bonds, which would require another round of recapitalization to avoid investor losses, have caused credit default swaps on select European banks to noticeably widen to levels last seen in 2012, at the height of the European sovereign debt crisis. Widening credit default swaps (CDS) spreads are related to falling commodity prices and deflation risk in Europe. . Global oil markets: Oil prices have yet to find a price floor, which is feeding into fears of a global recession based on a combination of oversupply and falling demand, especially from China and emerging markets. Meanwhile, OPEC countries haven’t been able to reach an agreement to curtail or freeze production. Credit default swaps on European banks widening 400 S&P/ISDA CDS select OTR-weighted average index spread DB five-year credit default swaps 350 300 Index 250 200 150 100 50 0 2012 2013 2014 2015 2016 Source: RSM US, Bloomberg In our 2016 year-ahead growth forecast, we noted there was a risk that the price of oil may fall to about $20 per barrel, just above the inflation-adjusted low of $17.26 reached in 1998 ($11.91 in non-inflation-adjusted terms). Given the 70 percent decline in oil prices since June 2014, countries such as Venezuela, Nigeria and Russia have fallen into economic depression and may choose to default on global debt obligations. During a time of regional geopolitical tensions, global investors and firm managers with exposure to the region are rightfully concerned that conditions could deteriorate and spillover into global financial markets. Central banking: Investor confidence in global central banks appears to be waning. There is a growing impression that central banks have reached the outer limits of conventional and nonconventional policies to support growth.

Moreover, with the Federal Reserve unlikely to push rates up the 400 basis points that is typically needed to provide monetary accommodation during economic downturns, there is a fear that the Fed will need to resort to a negative interest rate policy during the next recession, which will negatively affect financial institutions. Fiscal policy: With interest rates near zero, and real interest rates in the developed economies negative, a rational economic choice would be to turn to fiscal policy to support growth during an economic slowdown. Monetary policy is constrained by the zero bound, so policymakers would get more bang for the buck, so to speak, through fiscal policy. That, however, has not been the choice of decisionmakers in the major economies.

In Europe, the choice has been austerity, which triggered a bout of deflation that the continental economy has yet to recover from. In the United States, political polarization and stark ideological differences have, until very recently, resulted limited fiscal support for the economy. We have made the case that, with borrowing costs near zero in the United States, conditions are ripe for a $1 trillion infrastructure project that could be financed out over 30 or even 50 years.

The greater concern going forward is that if fiscal policy is off the table, what policy flexibility do decision-makers have if the business cycle ends during the next two to three years? MIDDLE MARKET INSIGHT: Direct concerns about a possible increase in tariffs on imported goods, a reduction in foreign labor and punitive taxation on businesses to fund a rapid expansion of government-supported entitlements has shocked many middle market firms. In our estimation, unless the electoral equation changes soon, there is a risk that fixed business investment, which as a percentage of GDP has only recovered to Clinton-era levels, could slow noticeably and is a potential harbinger of the next economic downturn. U.S. political risk: During the past four decades, the federal government has been more or less friendly to business and global commerce.

However, in this election year, the leading candidates in both political parties are promising to overturn the commercial consensus that has prevailed since the early 1980s. For the first time in recent memory, firms are looking at how they may need to price U.S. political risk into the cost of business operations. RSM | TH E RE A L ECO N O MY | 7 . DIMINISHING OPPORTUNITIES AMID EXCESS CAPITAL TO DRIVE REAL ESTATE DEAL FLOW IN 2016 With interest rates relatively low and periods of high volatility in equity markets, real estate will likely continue to draw investor interest that is sure to spark more dealmaking in 2016. Transaction activity in commercial real estate will be dominated by multifamily housing that is expected to draw greater investor interest and stir up more development. “You go around the country and you see more cranes going up. Multifamily is still a good place to be,” says Richard Edleheit, national real estate leader for RSM US LLP. “People are changing the way they are living. More and more people are living in the city,” says Tom Green, partner and assurance lead at RSM’s national real estate practice. According to Green, this shift in living patterns has not gone by unnoticed by private equity investors and pensions.

Pensions are increasingly putting their money to work directly into the asset class; some, for example, will partner up with a designated real estate company that tailors a specific investment platform for them. Mortgage rates, 5-year ARM 4.00 Much of this activity is tied to changes in attitudes about homeownership and affordability. Some recent government data show that as homeownership rates in the single-family arena have slid down to levels not seen since the mid-1990s, vacancy rates for multifamily properties are also down to 20-year lows. Some of that shift may be tied to affordability issues that keep some consumers from buying a single-family home, but much of it likely is a change in the tastes of the U.S. population. 8 | MARCH 2016 5-year ARM rate 3.80 3.60 3.40 Mortgage rate (percentage) Multifamily starts will likely see an increase in activity in 2016 from 2015 and 2014, according to projections made by the Mortgage Bankers Association.

Earlier this year, the industry group said it expects commercial and multifamily mortgage banker originations to set a new record and surpass the $508 billion mark of 2007. “You will continue to see development in the larger gateway markets of the United States and you will see it in secondary cities such as Austin, Portland, Nashville, Charlotte and similar cities,” says Edelheit. “We are going to see plenty of real estate activity in the marketplace.” 3.20 3.00 2.80 2.60 2.40 2.20 2.00 1/14/2011 1/14/2012 1/14/2013 1/14/2014 1/14/2015 Source: Mortgage Bankers Association In addition to demographics, the development in commercial real estate such as multifamily housing is being driven by private equity funds eager to put money to work. A November survey of private equity real estate fund managers—the results of which were published in February 2016—found that “finding attractive investment opportunities” is the single biggest challenge faced by a majority of the survey’s respondents.

Investors—90 . Refi and purchase indexes Demographics have not just reshaped how investors view multifamily housing. They have forced institutional investors to focus on facilities designed to cater to the needs of an ageing population. MBA refi index MBA purchase index 6,000 300 200 4,000 150 3,000 MBA purchase index MBA refinance index 250 5,000 100 2,000 1,000 1/10 50 0 10/10 7/11 4/12 1/13 10/13 7/14 4/15 Source: Mortgage Bankers Association percent of them said their investment in the asset class met or exceeded their expectations - are conducting more due diligence and they are expanding their investment teams. Of those fund managers surveyed, 67 percent say it is more difficult to find attractive investment opportunities than one year ago. That collision of diminishing opportunities and excess capital may also serve as a reminder to market participants of the importance of keeping up with stringent due diligence, say Green and Edelheit. Other segments of commercial real estate that likely will continue to see more activity in 2016 are retail and continuing care properties. When it comes to brick-and-mortar locations, retailers are shifting how they use and present their physical space to customers. For example, auto dealers are rearranging floor plans of sales outlets – borrowing design elements from mobile phone retail outlets that involve fewer desks and use more open space.

Then, there is what may be the biggest development for retail investors: the possibility that Amazon may open some physical store locations. “Things are ever evolving,” says Green. “The demographics alone have made this an attractive space for investors and developers,” says Green. “We are seeing a lot of conversions of former use properties into senior housing. We are starting to see more funds just focused on these health care opportunities.

It is really something that is attractive to all corners of America because of the demographics.” Despite changing preferences, the single-family world of real estate is also expected to be active this year, according to Green and Edelheit. 5.50 Mortgage rates, 30 year & 15 year contract Fixed rate 30-year contract rate Fixed rate 15-year contract rate 5.00 Mortgage Rates (%) 350 7,000 4.50 4.00 3.50 3.00 2.50 2.00 1/10 7/10 1/11 7/11 1/12 7/12 1/13 7/13 1/14 7/14 1/15 7/15 1/16 Source: Mortgage Bankers Association Mortgage lenders are expected to have their hands full in 2016 when it comes to applications to buy home loans and the business of refinancing existing mortgages. In February, refinancing alone accounted for over 60 percent of all single-family home loans processed by lenders–a high not seen since February 2014. Whether this type of business dominates lender activity for the rest of the year is unclear. Much of that activity will be shaped by the direction of U.S. Treasury rates.

“With low rates, continuous refinancing is wonderful for the mortgage bankers,” says Green. RSM | TH E RE A L ECO N O MY | 9 . Q&A 2016 REAL ESTATE OUTLOOK RICK EDELHEIT AND TOM GREEN Q: What should we expect for the real estate markets in 2016? Rick: Notwithstanding some hiccups in the global marketplace, we are going to see some of the same trends we saw in 2015. We are going to see plenty of real estate activity in the marketplace, both acquisitions and dispositions. Cap rates will continue to stay a bit low, which is what we have seen in the last handful of years. We might see some international funds coming into the United States. Q: With all of the heightened investor interest, is the real estate market too hot and how is that impacting loan standards? Rick: As we see more and more transactions, the biggest concern is underwriting.

Sometimes with more deals getting done, there is actually less due diligence. If we start seeing bigger deals, and we are not being called upon to provide underlying financial due diligence services, we know that things are going on in the marketplace that start to look a little bit cavalier. If we are representing the lender, at times, what we will see is that they have a bogey set in which they are mandated to have due diligence.

If that bogey starts to climb higher from a $100 million loan to a $150 million loan, then we know by definition that the underwriting process can be negatively impacted. Q: Is any property type more active in real estate? Rick: Residential property values are continuing to climb, and as they climb, to a certain extent, it makes it more difficult for homeowners to buy homes. So, multifamily is still a good place to be and it will continue to be a good place to be for quite a while. You will continue to see development, in particular, in the larger MSAs in the United States. You are seeing more and more people coming back into the cities.

We are going to see it in secondary markets as well. We will see more development in multifamily. You go around the country and you see more cranes going up. When it comes to energy prices, the reduced price of oil is going to enhance net operating income and returns to investors. Q: What is your view on recent data that shows homeownership rates falling to lows not seen since the mid-1990s? Tom: People are changing the way they live and on top of that you have millennials. More and more people are moving into cities, and you are seeing more development of multifamily properties. Q: How do private equity funds fit into your outlook? Tom: Over the next year or two, we are going to continue to see a lot of activity in commercial real estate and that has to do with the available capital that private equity companies are sitting on and the entry of foreign investors into the U.S.

market. That’s 10 | MARCH 2016 really keeping prices somewhat inflated and capital rates low. That will continue for a while. Rick: There are private equity companies that are focused on the single-family home rental strategy. The amount of single-family homes that have been accumulated by this handful of companies has been very substantial.

They have spent a lot of money developing the infrastructure to support that investment. Tom: Property values are climbing, generally speaking, across the country. In Chicago, we are starting to see a nice increase in the values of homes. I think that—maybe except for an area like Houston which may be hit by the impact of oil—most of the United States has seen an appreciation in value. Q: What is your outlook for retail, industrial and retirement community properties? Rick: In 2015, retail had a very good year, probably better than was expected.

As long as your retailers continue to change with the times to reinvent themselves, brick-and-mortar will continue to be here. Tom: Industrial properties have been strong. It has certainly been an active market. The demographics alone have made continuing care properties an attractive space for investors and developers. We are seeing a lot of conversions of former use properties into senior housing, whether it is assisted living or independent living. If you take the entire spectrum, these continuing-care retirement communities are pretty attractive.

We are starting to see more funds solely focused on these health care opportunities. There is a lot of ground-up development, and it is something that is attractive to all corners of America because of the demographics. Rick: You have a lot of baby boomers that have been very successful over the last four years and what you are finding is that baby boomer needs are different than what they used to be. Some of the answer, and opportunity, has been through the development of high-end facilities. Q: When it comes to changes in accounting treatments, are there any issues we should consider when it comes to leasing? Tom: There are some proposed changes related to lease accounting that have not been finalized yet.

It will probably have a bigger impact on tenants and it has to do more with them having to onboard the lease liability onto their balance sheet. Previously, they recognized it as an income statement item in terms of reflecting the current-year lease activity. The thought is that this is going to have a big impact because it will dramatically affect the way the balance sheet looks.

And, it will have an impact on certain financial metrics and ratios that are key to allowing them to do business, especially on the borrowing side. . RSM INDUSTRY COVERAGE SPECIALTY FINANCE Deterring and detecting internal and external fraud for specialty lenders RSM recently conducted research among specialty finance firms on both internal and external fraud and found that roughly half of all surveyed firms had experienced fraud. While fraud losses tended to be relatively low, they are almost never recovered. Half of the companies that experienced one form of fraud also experienced the other, which seems to indicate a relatively lax internal control environment at those companies and underscores the importance of effective controls. Partner Ronnie Lee outlined the issues and then ways to detect and deter fraud in this article. Details of the study can be found here. LAW FIRMS Law firm look-back and outlook Barry Rosenthal, leader for the national business and professional services practice, reviewed trends shaping, and shaking up, the law firms.

In a Q&A, Rosenthal found that firms are expanding their global knowledge and presence to tap into a global economy, who are doing business worldwide. Law firms are also looking to control costs through the use of artificial intelligence (AI) to handle routine work such as document scanning. Another cost trend: firms are rethinking their office space to reduce the cost of rent, which is the second largest firm cost, after compensation.

On the practice side, litigation and bankruptcy work is down, while M&A work is rising, which is good news for firms with private equity and real estate clients. Growth in technology and life sciences is also spurring an increase in intellectual property work. For the complete Q&A, look here. activities or expenditures may not be prohibited, depending on the facts and circumstances.

So, certain voter education activities—including presenting public forums and publishing voter education guides—conducted in a nonpartisan manner do not constitute prohibited political campaign activity. This white paper by partner James Sweeney looks at the do’s and don’ts of elections, with six situations where section 501(c)(4), (5) or (6) organizations have entered into political activities. TECHNOLOGY AND MANAGEMENT CONSULTING Leveraging the third platform: New technology enhances business insights The latest step in the technology environment is called the third platform. It consists of resources that add dimensions and information capabilities to help you make better business decisions and increase revenue.

These resources include: •• Mobility •• Cloud computing •• Social media •• The Internet of Things •• Big data The third platform’s rise reflects increased computer processing power, enhanced mobile technologies and evolving demographics. To leverage the opportunities, organizations must evaluate the technology budget and existing priorities, and make changes to properly integrate the new technology. RSM principals, Jim Klimkowski and Bill Kracunas, provide more details on the sources of value and ideas for implementation in the complete article, available here. NONPROFIT PRIVATE EQUITY Election year do’s and don’ts for nonprofits In a seller’s market, accelerating the deal close is critical—and risky The start of the 2016 general election is a good time for taxexempt organizations to review their compliance with political regulations. Under the Internal Revenue Code, all section 501(c)(3) organizations are absolutely prohibited from directly or indirectly participating in, or intervening in, any political campaign on behalf of (or in opposition to) any candidate for elective public office.

Contributions to political campaign funds and public statements of position (verbal or written) made on behalf of the organization in favor of or in opposition to any candidate for public office clearly violate the prohibition against political campaign activity. Violating this prohibition may result in denial or revocation of tax-exempt status and the imposition of certain excise taxes. However, certain Private equity firms sometimes race to close deals within 30 days of letters of intent (LOIs).

Competition is intense—and sellers know it. But closing a deal too quickly—before truly understanding the business, its people and systems—can hold back growth potential, lead to unexpected costs and destroy value in the long term. Striking the right balance between speed and thoroughness is especially challenging, and may require investing in additional resources to close the deal on time and according to plan.

RSM principal, Christina Churchill, and director, Dennis Cail, examine the risks and responses to fast closes using examples of a family-owned business, a new industry and a carve-out, in this piece from RSM’s Insight newsletter. RSM | TH E RE A L ECO N O MY | 11 . For more information on RSM, please visit www.rsmus.com. For media inquiries, please contact Terri Andrews, National Public Relations Director, +1 980 233 4710 or Terri.Andrews@rsmus.com. www.rsmus.com This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. RSM US LLP, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services.

This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed. RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other.

Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International. RSM® and the RSM logo are registered trademarks of RSM International Association. The power of being understood® is a registered trademark of RSM US LLP. © 2016 RSM US LLP.

All Rights Reserved. TRE-NT-ALL-ALL-0315 .