Description

Technology industry

findings & implications

6th Annual Digital IQ

Technology Institute

August 2014

. Executive summary

The role of digital in the Technology

industry might seem like a no-brainer.

It’s the engine behind the Technology

industry’s tectonic shift from

predominately product-based business

models to those that are built on or

incorporate services and experiences.

But as our 6th Annual Digital IQ survey

revealed, the relationship is actually

more complicated. How Technology

companies understand the value of

technology and weave it throughout the

fabric of their own businesses—what

we call Digital IQ—is uneven. Yes, the

industry leads all others, with 40% of

companies having a very strong Digital

IQ, compared with an average of just

20%. Yet that still leaves the majority

(60%) of Technology companies

trailing behind.

Like so many of their own customers,

Technology companies are investing

in digital to meet changing customer

demands.

They’re transforming the way they engage with customers and how they provide products and services. Technology companies are also exploring new business and revenue models, even pursuing opportunities at the intersection of industries—for example Retail and Technology, or RetailTech. 1 6th Annual Digital IQ: Technology industry findings & implications Digital is often short-hand for these market-facing efforts, while in the rest of the organization digital technology has yet to fully make its mark. That’s not all that different from other industries, but here it’s arguably a bigger challenge because Technology companies should be standard bearers for digital transformation.

One Computer and Networking executive we spoke with summed up why Digital IQ matters so much to the industry: “We are a Technology company. It is our lifeblood.” In this report, we examine the Technology industry findings from our Digital IQ survey in five critical areas: strategy, customer engagement, analytics, innovation, and IT delivery. . The five Digital IQ behaviors Our 6th Annual Digital IQ study of nearly 1,500 business and IT executives across 11 industries identified the five corporate behaviors that enable companies to maximize their use of digital technology and position them for better performance. The businesses in our study that leveraged these five interlocking behaviors were 2.2 times more likely to be top-performers in revenue growth, profitability, and innovation.1 Behavior 1: CEO actively champions digital Today’s CEOs shouldn’t delegate digital or view it as a separate strategy. A digital CEO sets and steers the company’s digital vision and tackles the inevitable challenges that come with new ways of doing business. This means developing a digital strategy that considers everything the business does—its growth and cost goals, products and services, partnerships, marketing and customer engagement, talent acquisition and retention, operations, and more. Behavior 2: Strong CIO-CMO relationship The CIO-CMO relationship is important because a great many digital technology initiatives are driven by marketing needs. Organizations must develop a digital operating model to remove any room for interpretation when it comes to responsibilities for market-facing digital technology like consumer apps, websites, or customer analytics. Behavior 3: Outside-in approach to digital innovation Global CEOs ranked product and service innovation as their top strategy for growth, over increasing market share, entering new geographic markets, M&A, or joint ventures and strategic alliances.

Yet most businesses don’t cast a wide enough net in their pursuit. Organizations must develop an outside-in learning pipeline to seek out and share new ideas and applications for emerging technology from sources outside the company, such as universities, labs, complementary businesses, and vendors. Behavior 4: Significant New IT Platform investments A company’s IT capabilities and infrastructure face crushing pressure from every direction to meet the daunting demands of the digital age. To address these demands, we believe an integration approach is required— what we call the New IT Platform.

This entails designing an IT strategy and enterprise architecture that considers the increased demands of new and emerging digital channels, your mobile workforce and partners, thirdparty data, new analytics requirements, and cloud-based business and technology services Behavior 5: View Digital as an enterprise capability Companies must begin broadening how they think about their digitallysavvy resources, realizing that it is becoming essential to have a digital capability that is woven throughout the business rather than only centralized in a single function and hidden in the shadows throughout the business. To do this effectively requires developing a single view of the digital skills required to meet business goals. It also requires creating a common talent framework to manage and develop those in digital roles. 1.

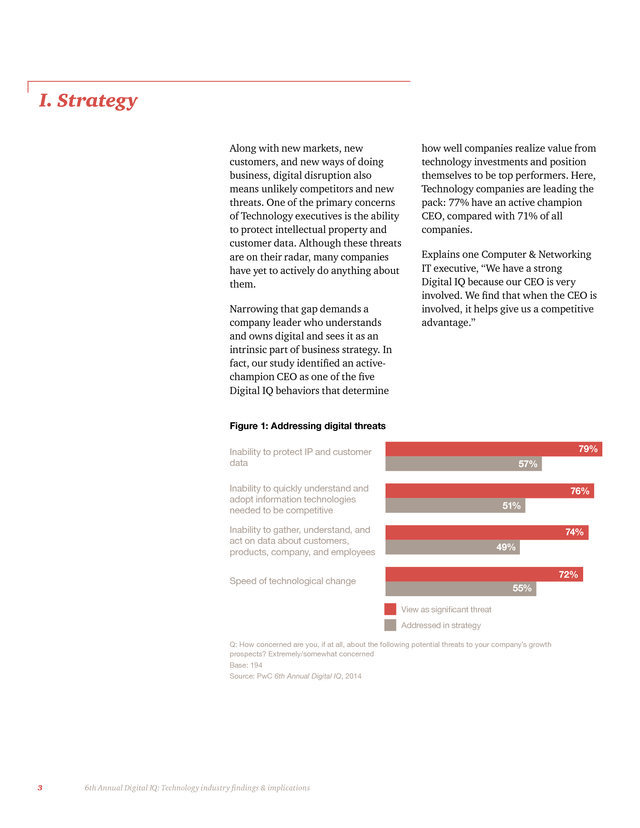

PwC, 6th Annual Digital IQ survey, 2014. PwC 2 . I. Strategy Along with new markets, new customers, and new ways of doing business, digital disruption also means unlikely competitors and new threats. One of the primary concerns of Technology executives is the ability to protect intellectual property and customer data. Although these threats are on their radar, many companies have yet to actively do anything about them. Narrowing that gap demands a company leader who understands and owns digital and sees it as an intrinsic part of business strategy.

In fact, our study identified an activechampion CEO as one of the five Digital IQ behaviors that determine how well companies realize value from technology investments and position themselves to be top performers. Here, Technology companies are leading the pack: 77% have an active champion CEO, compared with 71% of all companies. Explains one Computer & Networking IT executive, “We have a strong Digital IQ because our CEO is very involved. We find that when the CEO is involved, it helps give us a competitive advantage.” Figure 1: Addressing digital threats Inability to protect IP and customer data Inability to quickly understand and adopt information technologies needed to be competitive 51% Inability to gather, understand, and act on data about customers, products, company, and employees 49% Speed of technological change 55% View as significant threat Addressed in strategy Q: How concerned are you, if at all, about the following potential threats to your company’s growth prospects? Extremely/somewhat concerned Base: 194 Source: PwC 6th Annual Digital IQ, 2014 3 6th Annual Digital IQ: Technology industry findings & implications 79% 57% 76% 74% 72% .

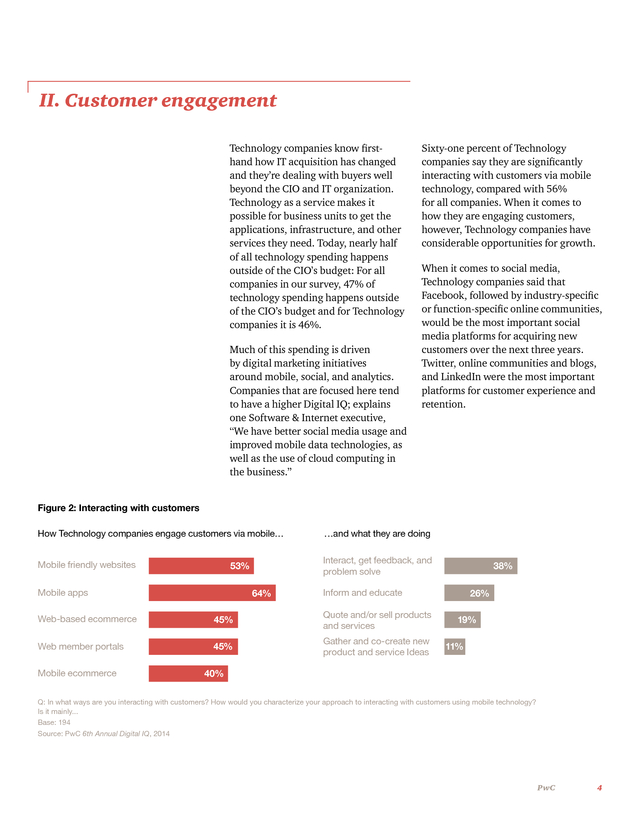

II. Customer engagement Technology companies know firsthand how IT acquisition has changed and they’re dealing with buyers well beyond the CIO and IT organization. Technology as a service makes it possible for business units to get the applications, infrastructure, and other services they need. Today, nearly half of all technology spending happens outside of the CIO’s budget: For all companies in our survey, 47% of technology spending happens outside of the CIO’s budget and for Technology companies it is 46%. Much of this spending is driven by digital marketing initiatives around mobile, social, and analytics. Companies that are focused here tend to have a higher Digital IQ; explains one Software & Internet executive, “We have better social media usage and improved mobile data technologies, as well as the use of cloud computing in the business.” Sixty-one percent of Technology companies say they are significantly interacting with customers via mobile technology, compared with 56% for all companies. When it comes to how they are engaging customers, however, Technology companies have considerable opportunities for growth. When it comes to social media, Technology companies said that Facebook, followed by industry-specific or function-specific online communities, would be the most important social media platforms for acquiring new customers over the next three years. Twitter, online communities and blogs, and LinkedIn were the most important platforms for customer experience and retention. Figure 2: Interacting with customers How Technology companies engage customers via mobile… …and what they are doing Mobile friendly websites Interact, get feedback, and problem solve 53% Mobile apps 64% Inform and educate Web-based ecommerce 45% Quote and/or sell products and services Web member portals 45% Gather and co-create new product and service Ideas Mobile ecommerce 38% 26% 19% 11% 40% Q: In what ways are you interacting with customers? How would you characterize your approach to interacting with customers using mobile technology? Is it mainly... Base: 194 Source: PwC 6th Annual Digital IQ, 2014 PwC 4 .

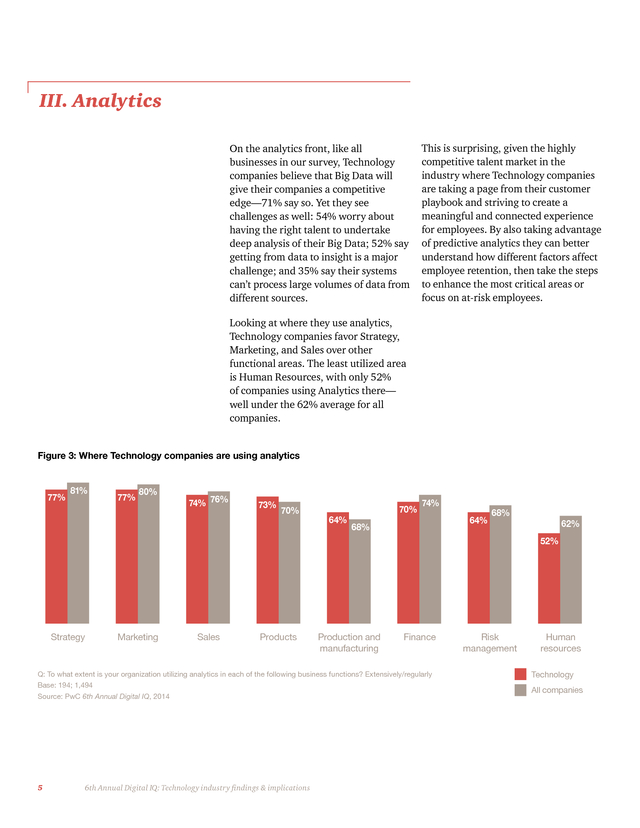

III. Analytics On the analytics front, like all businesses in our survey, Technology companies believe that Big Data will give their companies a competitive edge—71% say so. Yet they see challenges as well: 54% worry about having the right talent to undertake deep analysis of their Big Data; 52% say getting from data to insight is a major challenge; and 35% say their systems can’t process large volumes of data from different sources. This is surprising, given the highly competitive talent market in the industry where Technology companies are taking a page from their customer playbook and striving to create a meaningful and connected experience for employees. By also taking advantage of predictive analytics they can better understand how different factors affect employee retention, then take the steps to enhance the most critical areas or focus on at-risk employees. Looking at where they use analytics, Technology companies favor Strategy, Marketing, and Sales over other functional areas.

The least utilized area is Human Resources, with only 52% of companies using Analytics there— well under the 62% average for all companies. Figure 3: Where Technology companies are using analytics 77% 81% Strategy 77% 80% Marketing 74% 76% Sales 73% 70% Products 64% 70% 74% 68% Production and manufacturing Source: PwC 6th Annual Digital IQ, 2014 5 6th Annual Digital IQ: Technology industry findings & implications 68% 62% 52% Finance Q: To what extent is your organization utilizing analytics in each of the following business functions? Extensively/regularly Base: 194; 1,494 64% Risk management Human resources Technology All companies . IV. Innovation For Technology companies, of course, innovation is critical. If they don’t relentlessly pursue new customers, markets, and business models, an upstart or unexpected competitor from a different industry might come in and disrupt their business. Emphasizes one Computers & Networking executive we spoke with, “Our market domain is innovation.” This year’s study identified an outsidein approach to innovation as being another one of the Digital IQ behaviors critical to success.

What do we mean by outside-in? Casting a wide net and looking beyond the company’s four walls for ways to apply emerging technology to enhance products or services or create new ones. While Technology companies are more likely to look outside the organization to gather ideas for applying emerging technologies—41% use outside methods like customer or vendor input or industry analysts, compared with 33% of all companies—there’s still plenty of room for improvement. Looking outside means you will gather more new ideas for your pipeline. It is important to quickly and systematically filter them so that you end up with a short list of those that are promising and you will act upon. Part of this well-defined process is measurement— another factor in top performance. Technology companies are consistently higher in measuring innovation on all counts.

For example, 51% measure innovation success by explicit business value added, 25% by the number of patents filed, and 33% by ideas commercialized by explicit business value added. Another area that’s ripe for improvement is in the CIO’s role in innovation. As with the full sample, only about 30% of Technology companies have the CIO focus on external aspects of innovation, such as acquiring new customers or improving products. In our core survey, the top-five emerging technologies that companies identified as being of most strategic importance to their business in 3 to 5 years were: mobile customer technology, private cloud, data mining and analysis, externally-focused social media, and cybersecurity. Additionally, Technology companies are focused on public cloud apps and infrastructure, as many are moving to technology-as-aservice or other cloud-enabled business models. While their level of investment in these strategic technologies is increasing, not all companies are as forwardlooking.

Complains one Software & Internet executive, “Executive staff still put a premium on short-term profit over investment in newer technology. Mid-level management and front-line employees have a higher Digital IQ and understand the value of investment.” PwC 6 . Technology companies are focused on public cloud apps and infrastructure as many are moving to cloud-enabled business models. Figure 4: Top strategic technologies Technology companies All companies Private cloud 37% 29% Cybersecurity 33% 30% Public cloud applications 29% 18% Mobile for customers 28% 31% Public cloud infrastructure 25% 14% Data mining and analysis 25% 29% Digital delivery 21% 25% Data visualization 20% 19% Mobile for employees 18% 18% Open source applications 16% 16% Simulation, scenario modeling 16% 12% Social media for external 15% 29% Open source infrastructure 13% 10% Robotics 11% 15% 3D printing 11% 7% Virtual meeting and collaboration 10% 15% Sensors 10% 14% Social media for internal 9% 13% Battery and Power 8% 9% NoSQL databases 8% 7% Wearable computing 7% 5% Gamification 5% 4% Q: Overall, which of these technologies will be of the highest strategic importance to your organization over the next 3-5 years? Base: 194; 1,494 Source: PwC 6th Annual Digital IQ, 2014 7 6th Annual Digital IQ: Technology industry findings & implications . V. IT Delivery Our study revealed that how Technology companies think about IT is also ripe for change. Adopting a new approach, what we call the New IT Platform (NITP), was one of the five Digital IQ behaviors that better positioned companies for top performance. Moving to a NITP requires rethinking everything about IT so that it functions as a services orchestrator and business consultant who empowers those in the organization through appropriate governance. To make that work, you need strong relationships among the CIO and the rest of the C-suite and have ongoing “digital conversations.” Especially crucial is a strong CMO-CIO relationship.

Technology CIOs are lagging behind here, with just 46% having a strong relationship between the two executives, compared with 51% of companies overall. This must be addressed as our study found that the majority of top-performing companies, 70%, had a strong CIOCMO relationship. Figure 5: Why IT initiatives fail for Technology companies Other 6% Old technologies 9% Ineffective third-party partners 14% Lack of properly skilled teams 20% Inflexible or slow project lifecycle processes 28% Don’t know 1% Ineffective project management and governance 22% When it comes to the successful delivery of strategic IT initiatives, Technology companies also ranked below the average: 48% delivering on time (versus 53% overall), 36% deliver at or below budget (compared with 38% overall), and 39% with 100% of scope (versus 45%). Technology companies say the biggest barrier is inflexible or slow project lifecycle processes. Explained one business executive at a Software & Internet company, “We are a company based on making the Internet faster and use technology to sell services to our customers.

I would rate our Digital IQ as very strong except that we don’t leverage enough technology in a consistent and structured manner to support our daily operations.” For Technology companies—and all companies—we see the adoption of Agile processes as an important way to improve delivery and integration. Technology companies are more likely to use agile processes on a majority of projects (37% versus 29% for all companies) and more are planning to increase their use of agile (44% versus 33% overall). Technology companies also tend to have a higher level of skills in what we call the digital keystone skills. They especially stand out on crucial skills for operating in an environment with service providers and rapid innovation: technology prototyping (69% versus 60% for all companies), strategic partner management (65% versus 57% for all companies), and user experience design (61% versus 55% for all companies). Q: What in your view is the single largest barrier to executing your strategic IT initiatives successfully? Base: 194 Source: PwC 6th Annual Digital IQ, 2014 PwC 8 . Conclusion: Implications for Technology executives As Technology companies navigate the New Digital Ecosystem Reality, Digital IQ has never been more important. “Business units have embraced and integrated with digital business ecosystems, where not only technologies are important but new inter-organizational business architectures. This approach enables us to respond to the velocity and turbulence of changes in our business environment, taking advantage of today’s low-cost and widespread digital technologies,” explains one Computer & Networking executive in our study. How can Technology companies up their Digital IQ? We see three important steps: 1. Assess your Digital IQ. It starts with knowing where you stand, relative to your peers as well as your customers. Digital IQ encompasses a range of dimensions that we’ve codified into five fundamental behaviors that position a company to get more from its digital investment and achieve better performance.

To see how your company measures up, explore our findings by industry or region here: http://pwc.to/DIQData About this report 9 2. Advance your Digital IQ by developing the five behaviors. For recommendations that all companies can take today around each of the five behaviors, see our full Digital IQ report here: http://pwc.to/DIQ 3. Help your customers understand and enhance their own Digital IQs. As the Technology industry shifts from selling distinct products to one that provides solutions to its customers, we see Digital IQ as an important part of this valueadd.

As you engage with customers to identify and deliver the right products, services, and experiences, use the Digital IQ framework to help them get more out of their technology investments. Our 6th Annual Digital IQ Survey, which examines the attitudes and practices of IT and business leaders around the globe, surveyed 194 Technology industry leaders about these themes. For more insights and to explore the data, visit www.pwc.com/us/digitaliq 6th Annual Digital IQ: Technology industry findings & implications . www.pwc.com PwC can help For a deeper discussion on the five Digital IQ behaviors, and implications to the Technology industry, please contact one of our leaders: Tom Archer US Technology Industry Leader 408 817 3836 thomas.archer@us.pwc.com Kayvan Shahabi US Technology Advisory Leader 408 817 5724 kayvan.shahabi@us.pwc.com Chris Curran Principal and Chief Technologist 214 754 5055 christopher.b.curran@us.pwc.com Let’s talk Please reach out to any of our Technology leaders to discuss this or other challenges. We’re here to help: Tom Archer US Technology Industry Leader 408 817 3836 thomas.archer@us.pwc.com Cory Starr US Technology Assurance Leader 408 817 1215 cory.j.starr@us.pwc.com Kayvan Shahabi US Technology Advisory Leader 408 817 5724 kayvan.shahabi@us.pwc.com Diane Baylor US Technology Tax Leader 408 817 5005 diane.baylor@us.pwc.com About PwC’s Technology Institute The Technology Institute is PwC’s global research network that studies the business of technology and the technology of business with the purpose of creating thought leadership that offers both fact-based analysis and experience-based perspectives. Technology Institute insights and viewpoints originate from active collaboration between our professionals across the globe and their first-hand experiences working in and with the Technology industry. For more information please contact Tom Archer, US Technology Industry Leader. © 2014 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

PwC refers to the US member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

DH-15-0002 This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. PwC US helps organizations and individuals create the value they’re looking for. We’re a member of the PwC network of firms in 158 countries with more than 180,000 people. We’re committed to delivering quality in assurance, tax and advisory services.

Tell us what matters to you and find out more by visiting us at www.pwc.com/us. .

They’re transforming the way they engage with customers and how they provide products and services. Technology companies are also exploring new business and revenue models, even pursuing opportunities at the intersection of industries—for example Retail and Technology, or RetailTech. 1 6th Annual Digital IQ: Technology industry findings & implications Digital is often short-hand for these market-facing efforts, while in the rest of the organization digital technology has yet to fully make its mark. That’s not all that different from other industries, but here it’s arguably a bigger challenge because Technology companies should be standard bearers for digital transformation.

One Computer and Networking executive we spoke with summed up why Digital IQ matters so much to the industry: “We are a Technology company. It is our lifeblood.” In this report, we examine the Technology industry findings from our Digital IQ survey in five critical areas: strategy, customer engagement, analytics, innovation, and IT delivery. . The five Digital IQ behaviors Our 6th Annual Digital IQ study of nearly 1,500 business and IT executives across 11 industries identified the five corporate behaviors that enable companies to maximize their use of digital technology and position them for better performance. The businesses in our study that leveraged these five interlocking behaviors were 2.2 times more likely to be top-performers in revenue growth, profitability, and innovation.1 Behavior 1: CEO actively champions digital Today’s CEOs shouldn’t delegate digital or view it as a separate strategy. A digital CEO sets and steers the company’s digital vision and tackles the inevitable challenges that come with new ways of doing business. This means developing a digital strategy that considers everything the business does—its growth and cost goals, products and services, partnerships, marketing and customer engagement, talent acquisition and retention, operations, and more. Behavior 2: Strong CIO-CMO relationship The CIO-CMO relationship is important because a great many digital technology initiatives are driven by marketing needs. Organizations must develop a digital operating model to remove any room for interpretation when it comes to responsibilities for market-facing digital technology like consumer apps, websites, or customer analytics. Behavior 3: Outside-in approach to digital innovation Global CEOs ranked product and service innovation as their top strategy for growth, over increasing market share, entering new geographic markets, M&A, or joint ventures and strategic alliances.

Yet most businesses don’t cast a wide enough net in their pursuit. Organizations must develop an outside-in learning pipeline to seek out and share new ideas and applications for emerging technology from sources outside the company, such as universities, labs, complementary businesses, and vendors. Behavior 4: Significant New IT Platform investments A company’s IT capabilities and infrastructure face crushing pressure from every direction to meet the daunting demands of the digital age. To address these demands, we believe an integration approach is required— what we call the New IT Platform.

This entails designing an IT strategy and enterprise architecture that considers the increased demands of new and emerging digital channels, your mobile workforce and partners, thirdparty data, new analytics requirements, and cloud-based business and technology services Behavior 5: View Digital as an enterprise capability Companies must begin broadening how they think about their digitallysavvy resources, realizing that it is becoming essential to have a digital capability that is woven throughout the business rather than only centralized in a single function and hidden in the shadows throughout the business. To do this effectively requires developing a single view of the digital skills required to meet business goals. It also requires creating a common talent framework to manage and develop those in digital roles. 1.

PwC, 6th Annual Digital IQ survey, 2014. PwC 2 . I. Strategy Along with new markets, new customers, and new ways of doing business, digital disruption also means unlikely competitors and new threats. One of the primary concerns of Technology executives is the ability to protect intellectual property and customer data. Although these threats are on their radar, many companies have yet to actively do anything about them. Narrowing that gap demands a company leader who understands and owns digital and sees it as an intrinsic part of business strategy.

In fact, our study identified an activechampion CEO as one of the five Digital IQ behaviors that determine how well companies realize value from technology investments and position themselves to be top performers. Here, Technology companies are leading the pack: 77% have an active champion CEO, compared with 71% of all companies. Explains one Computer & Networking IT executive, “We have a strong Digital IQ because our CEO is very involved. We find that when the CEO is involved, it helps give us a competitive advantage.” Figure 1: Addressing digital threats Inability to protect IP and customer data Inability to quickly understand and adopt information technologies needed to be competitive 51% Inability to gather, understand, and act on data about customers, products, company, and employees 49% Speed of technological change 55% View as significant threat Addressed in strategy Q: How concerned are you, if at all, about the following potential threats to your company’s growth prospects? Extremely/somewhat concerned Base: 194 Source: PwC 6th Annual Digital IQ, 2014 3 6th Annual Digital IQ: Technology industry findings & implications 79% 57% 76% 74% 72% .

II. Customer engagement Technology companies know firsthand how IT acquisition has changed and they’re dealing with buyers well beyond the CIO and IT organization. Technology as a service makes it possible for business units to get the applications, infrastructure, and other services they need. Today, nearly half of all technology spending happens outside of the CIO’s budget: For all companies in our survey, 47% of technology spending happens outside of the CIO’s budget and for Technology companies it is 46%. Much of this spending is driven by digital marketing initiatives around mobile, social, and analytics. Companies that are focused here tend to have a higher Digital IQ; explains one Software & Internet executive, “We have better social media usage and improved mobile data technologies, as well as the use of cloud computing in the business.” Sixty-one percent of Technology companies say they are significantly interacting with customers via mobile technology, compared with 56% for all companies. When it comes to how they are engaging customers, however, Technology companies have considerable opportunities for growth. When it comes to social media, Technology companies said that Facebook, followed by industry-specific or function-specific online communities, would be the most important social media platforms for acquiring new customers over the next three years. Twitter, online communities and blogs, and LinkedIn were the most important platforms for customer experience and retention. Figure 2: Interacting with customers How Technology companies engage customers via mobile… …and what they are doing Mobile friendly websites Interact, get feedback, and problem solve 53% Mobile apps 64% Inform and educate Web-based ecommerce 45% Quote and/or sell products and services Web member portals 45% Gather and co-create new product and service Ideas Mobile ecommerce 38% 26% 19% 11% 40% Q: In what ways are you interacting with customers? How would you characterize your approach to interacting with customers using mobile technology? Is it mainly... Base: 194 Source: PwC 6th Annual Digital IQ, 2014 PwC 4 .

III. Analytics On the analytics front, like all businesses in our survey, Technology companies believe that Big Data will give their companies a competitive edge—71% say so. Yet they see challenges as well: 54% worry about having the right talent to undertake deep analysis of their Big Data; 52% say getting from data to insight is a major challenge; and 35% say their systems can’t process large volumes of data from different sources. This is surprising, given the highly competitive talent market in the industry where Technology companies are taking a page from their customer playbook and striving to create a meaningful and connected experience for employees. By also taking advantage of predictive analytics they can better understand how different factors affect employee retention, then take the steps to enhance the most critical areas or focus on at-risk employees. Looking at where they use analytics, Technology companies favor Strategy, Marketing, and Sales over other functional areas.

The least utilized area is Human Resources, with only 52% of companies using Analytics there— well under the 62% average for all companies. Figure 3: Where Technology companies are using analytics 77% 81% Strategy 77% 80% Marketing 74% 76% Sales 73% 70% Products 64% 70% 74% 68% Production and manufacturing Source: PwC 6th Annual Digital IQ, 2014 5 6th Annual Digital IQ: Technology industry findings & implications 68% 62% 52% Finance Q: To what extent is your organization utilizing analytics in each of the following business functions? Extensively/regularly Base: 194; 1,494 64% Risk management Human resources Technology All companies . IV. Innovation For Technology companies, of course, innovation is critical. If they don’t relentlessly pursue new customers, markets, and business models, an upstart or unexpected competitor from a different industry might come in and disrupt their business. Emphasizes one Computers & Networking executive we spoke with, “Our market domain is innovation.” This year’s study identified an outsidein approach to innovation as being another one of the Digital IQ behaviors critical to success.

What do we mean by outside-in? Casting a wide net and looking beyond the company’s four walls for ways to apply emerging technology to enhance products or services or create new ones. While Technology companies are more likely to look outside the organization to gather ideas for applying emerging technologies—41% use outside methods like customer or vendor input or industry analysts, compared with 33% of all companies—there’s still plenty of room for improvement. Looking outside means you will gather more new ideas for your pipeline. It is important to quickly and systematically filter them so that you end up with a short list of those that are promising and you will act upon. Part of this well-defined process is measurement— another factor in top performance. Technology companies are consistently higher in measuring innovation on all counts.

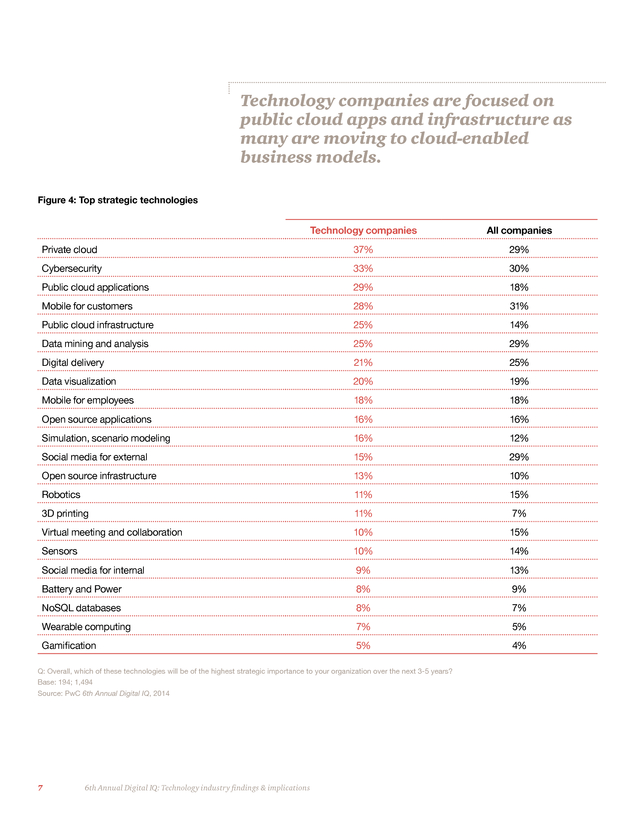

For example, 51% measure innovation success by explicit business value added, 25% by the number of patents filed, and 33% by ideas commercialized by explicit business value added. Another area that’s ripe for improvement is in the CIO’s role in innovation. As with the full sample, only about 30% of Technology companies have the CIO focus on external aspects of innovation, such as acquiring new customers or improving products. In our core survey, the top-five emerging technologies that companies identified as being of most strategic importance to their business in 3 to 5 years were: mobile customer technology, private cloud, data mining and analysis, externally-focused social media, and cybersecurity. Additionally, Technology companies are focused on public cloud apps and infrastructure, as many are moving to technology-as-aservice or other cloud-enabled business models. While their level of investment in these strategic technologies is increasing, not all companies are as forwardlooking.

Complains one Software & Internet executive, “Executive staff still put a premium on short-term profit over investment in newer technology. Mid-level management and front-line employees have a higher Digital IQ and understand the value of investment.” PwC 6 . Technology companies are focused on public cloud apps and infrastructure as many are moving to cloud-enabled business models. Figure 4: Top strategic technologies Technology companies All companies Private cloud 37% 29% Cybersecurity 33% 30% Public cloud applications 29% 18% Mobile for customers 28% 31% Public cloud infrastructure 25% 14% Data mining and analysis 25% 29% Digital delivery 21% 25% Data visualization 20% 19% Mobile for employees 18% 18% Open source applications 16% 16% Simulation, scenario modeling 16% 12% Social media for external 15% 29% Open source infrastructure 13% 10% Robotics 11% 15% 3D printing 11% 7% Virtual meeting and collaboration 10% 15% Sensors 10% 14% Social media for internal 9% 13% Battery and Power 8% 9% NoSQL databases 8% 7% Wearable computing 7% 5% Gamification 5% 4% Q: Overall, which of these technologies will be of the highest strategic importance to your organization over the next 3-5 years? Base: 194; 1,494 Source: PwC 6th Annual Digital IQ, 2014 7 6th Annual Digital IQ: Technology industry findings & implications . V. IT Delivery Our study revealed that how Technology companies think about IT is also ripe for change. Adopting a new approach, what we call the New IT Platform (NITP), was one of the five Digital IQ behaviors that better positioned companies for top performance. Moving to a NITP requires rethinking everything about IT so that it functions as a services orchestrator and business consultant who empowers those in the organization through appropriate governance. To make that work, you need strong relationships among the CIO and the rest of the C-suite and have ongoing “digital conversations.” Especially crucial is a strong CMO-CIO relationship.

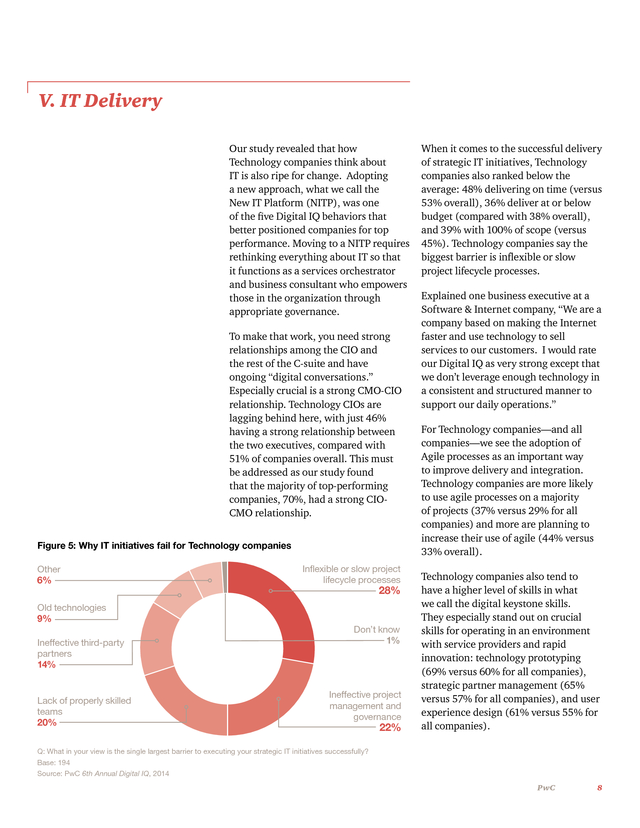

Technology CIOs are lagging behind here, with just 46% having a strong relationship between the two executives, compared with 51% of companies overall. This must be addressed as our study found that the majority of top-performing companies, 70%, had a strong CIOCMO relationship. Figure 5: Why IT initiatives fail for Technology companies Other 6% Old technologies 9% Ineffective third-party partners 14% Lack of properly skilled teams 20% Inflexible or slow project lifecycle processes 28% Don’t know 1% Ineffective project management and governance 22% When it comes to the successful delivery of strategic IT initiatives, Technology companies also ranked below the average: 48% delivering on time (versus 53% overall), 36% deliver at or below budget (compared with 38% overall), and 39% with 100% of scope (versus 45%). Technology companies say the biggest barrier is inflexible or slow project lifecycle processes. Explained one business executive at a Software & Internet company, “We are a company based on making the Internet faster and use technology to sell services to our customers.

I would rate our Digital IQ as very strong except that we don’t leverage enough technology in a consistent and structured manner to support our daily operations.” For Technology companies—and all companies—we see the adoption of Agile processes as an important way to improve delivery and integration. Technology companies are more likely to use agile processes on a majority of projects (37% versus 29% for all companies) and more are planning to increase their use of agile (44% versus 33% overall). Technology companies also tend to have a higher level of skills in what we call the digital keystone skills. They especially stand out on crucial skills for operating in an environment with service providers and rapid innovation: technology prototyping (69% versus 60% for all companies), strategic partner management (65% versus 57% for all companies), and user experience design (61% versus 55% for all companies). Q: What in your view is the single largest barrier to executing your strategic IT initiatives successfully? Base: 194 Source: PwC 6th Annual Digital IQ, 2014 PwC 8 . Conclusion: Implications for Technology executives As Technology companies navigate the New Digital Ecosystem Reality, Digital IQ has never been more important. “Business units have embraced and integrated with digital business ecosystems, where not only technologies are important but new inter-organizational business architectures. This approach enables us to respond to the velocity and turbulence of changes in our business environment, taking advantage of today’s low-cost and widespread digital technologies,” explains one Computer & Networking executive in our study. How can Technology companies up their Digital IQ? We see three important steps: 1. Assess your Digital IQ. It starts with knowing where you stand, relative to your peers as well as your customers. Digital IQ encompasses a range of dimensions that we’ve codified into five fundamental behaviors that position a company to get more from its digital investment and achieve better performance.

To see how your company measures up, explore our findings by industry or region here: http://pwc.to/DIQData About this report 9 2. Advance your Digital IQ by developing the five behaviors. For recommendations that all companies can take today around each of the five behaviors, see our full Digital IQ report here: http://pwc.to/DIQ 3. Help your customers understand and enhance their own Digital IQs. As the Technology industry shifts from selling distinct products to one that provides solutions to its customers, we see Digital IQ as an important part of this valueadd.

As you engage with customers to identify and deliver the right products, services, and experiences, use the Digital IQ framework to help them get more out of their technology investments. Our 6th Annual Digital IQ Survey, which examines the attitudes and practices of IT and business leaders around the globe, surveyed 194 Technology industry leaders about these themes. For more insights and to explore the data, visit www.pwc.com/us/digitaliq 6th Annual Digital IQ: Technology industry findings & implications . www.pwc.com PwC can help For a deeper discussion on the five Digital IQ behaviors, and implications to the Technology industry, please contact one of our leaders: Tom Archer US Technology Industry Leader 408 817 3836 thomas.archer@us.pwc.com Kayvan Shahabi US Technology Advisory Leader 408 817 5724 kayvan.shahabi@us.pwc.com Chris Curran Principal and Chief Technologist 214 754 5055 christopher.b.curran@us.pwc.com Let’s talk Please reach out to any of our Technology leaders to discuss this or other challenges. We’re here to help: Tom Archer US Technology Industry Leader 408 817 3836 thomas.archer@us.pwc.com Cory Starr US Technology Assurance Leader 408 817 1215 cory.j.starr@us.pwc.com Kayvan Shahabi US Technology Advisory Leader 408 817 5724 kayvan.shahabi@us.pwc.com Diane Baylor US Technology Tax Leader 408 817 5005 diane.baylor@us.pwc.com About PwC’s Technology Institute The Technology Institute is PwC’s global research network that studies the business of technology and the technology of business with the purpose of creating thought leadership that offers both fact-based analysis and experience-based perspectives. Technology Institute insights and viewpoints originate from active collaboration between our professionals across the globe and their first-hand experiences working in and with the Technology industry. For more information please contact Tom Archer, US Technology Industry Leader. © 2014 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

PwC refers to the US member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

DH-15-0002 This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. PwC US helps organizations and individuals create the value they’re looking for. We’re a member of the PwC network of firms in 158 countries with more than 180,000 people. We’re committed to delivering quality in assurance, tax and advisory services.

Tell us what matters to you and find out more by visiting us at www.pwc.com/us. .