Description

POLEN CAPITAL THOUGHT LEADERSHIP

June 2015

A L L E RG A N : A H

Q

C

POLENCAPITAL.COM

Executive Summary

The recent $70.5 billion acquisi on of Allergan by the Irish pharmaceu cal company, Actavis plc,

turned the ï¬nal page on Polen Capital’s sixâ€year investment in Allergan— this was a proï¬table

period that yielded a robust return of approximately sixâ€fold for Polen clients.

The Allergan investment decision was the natural outcome of successfully execu ng our investment

discipline. When we began researching Allergan in 2005, it met all of the quan ta ve hurdles that

we ini ally look for: sustained high returns on capital, aboveâ€average earnings per share and free

cash flow growth, strong and improving margins, reasonable debt levels, and a very capable manageâ€

ment team.

But while those are all the earmarks of a great business, our investment team s ll needed to dedicate

the me to more carefully evaluate whether it truly was a great business. We pa ently built our

knowledge of the company over several years and waited for a compelling risk/reward scenario to

present itself. The global ï¬nancial crisis in late 2008 provided that compelling opportunity. Allergan

shares declined as sales of its discre onary aesthe c products slowed pushing the company’s P/E

mul ple below 15x. Given our longâ€term view on the business’s growth poten al, we believed this

was an ideal entry point.

We built a posi on in Allergan, and as the business delivered solid fundamental performance during

the next several years—consistent with its history and its favorable ongoing market posi on—the

shares rose as well. While we consider underlying earnings per share and free cash flow growth to

be the primary drivers of longâ€term share price performance, Allergan’s stock also beneï¬ted as the

P/E mul ple expanded from depressed levels. While it was never central to our investment thesis,

we always recognized that Allergan’s strong growth and leadership posi on in its specialty markets

also made the company an a rac ve acquisi on target for larger healthcare companies seeking to

maintain a rac ve growth proï¬les. We never invest in a business on the hope of a takeâ€out, but

being an everâ€a rac ve acquisi on candidate can provide a measure of downside protec on

(par cularly at a more depressed valua on).

In this paper, we examine some of the unique factors that drove our decision to invest ini ally, and

to maintain our posi on even during a par cularly difficult me for the pharmaceu cal ï¬rm. We will

also lay out some of the a ributes that made Allergan an a rac ve acquisi on target, and we

explore some of its hidden strengths that enabled the company to successfully defend itself during

the acquisi on process, push the buying price of the company to unexpected levels, and extract full

and fair value for its shareholders.

Stephen Atkins, CFA

Research Analyst

KEY THEMES

BUSINESS TRANSFORMATION

Allergan shi ed its business

mix away from medical

devices to faster growing

specialty pharmaceu cal

treatments.

REASONABLE VALUATION

We ini ated our posi on in

Allergan for less than 15

mes current EPS for a busiâ€

ness that was growing 20%

annually.

PATIENT APPROACH

We maintained our posi on

through some temporary

setbacks because of our

convic on in the company

and its management team.

COMPOUNDING MACHINE

Over the six years in which

we were investors, Allergan

compounded EPS at 21% per

year with an average annual

rate of return of 32%.

. A LLERGAN

A

Investment Case Study

s 2014 wound to a close, Polen Capital

celebrated the 26th anniversary of the ï¬rm’s

founding. This milestone was borne out of the

hard work and determina on of our employees,

past and present, as well as the loyalty of our clients.

Though not nearly as signiï¬cant as surviving—and, indeed,

prospering—for a quarter of a century in the investment

industry, we achieved another milestone in 2014: the pubâ€

lica on of our ï¬rst white paper.

We view the crea on of white papers and other “thought

pieces” as part of the natural evolu on of our business.

Along with our quarterly commentaries, these serve as a

conduit to communicate with our clients and provide

greater clarity on our investment ï¬rm and the industry in

which we operate.

No sooner had we put the ï¬nishing touches on our ï¬rst

white paper than the discussion of our next white paper

topic had begun. Several ideas were bandied about, many

of which may become future thought pieces, but in the

midst of all the debate, it was our own por olio that

provided inspira on. In the ï¬rst quarter of 2015 we

divested our remaining posi on in Allergan Inc., which

brought to an end a very rewarding sixâ€year rela onship

with the company. Over that me, Allergan’s stock

increased roughly sixâ€fold and provided our clients with a

32% annualized total return.

PART I — THE WAITING GAME

T

he ï¬rst research note on Allergan, courtesy of

our coâ€por olio manager Damon Ficklin, dates

back to August 2005. Typically our ini al reâ€

search notes on a company contain just that,

our ini al thoughts on the business a er reading their

annual reports, earnings releases and other relevant

informa on.

For some background, Allergan is a healthcare company

that was once a subsidiary of SmithKline Beecham

before being spun out in 1989. Since then it had been

transforming itself from a medical deviceâ€focused

company into a specialty pharmaceu cals business

focused on ophthalmic and aesthe c products. The

company is perhaps best known for its injectable

neurotoxin, Botox, which was approved for a number

of medical condi ons and was becoming hugely popular

as a cosme c treatment for wrinkles.

The best companies usually stand out immediately and

Allergan was no excep on. Damon noted at the me

that the company “Looks like a solid business with

some interes ng possibili es.” What caught Damon’s

eye was Allergan’s business mix, which by 2005 was

fully dedicated to innova ve specialty pharmaceu cal

products with more promising growth poten al than

the medical device businesses that had preceded them.

To be clear, this isn’t about us taking a victory lap over a

successful investment. Rather, it struck us that the He was also impressed with Allergan’s commitment to

R&D, nearly 20% of sales at that point, as well as with

Allergan story involves many of the investment merits that

their highâ€powered Board of Directors which included

we covet most at Polen: an easy to understand company, a

Herbert Boyer, the founder of Genentech, and a numâ€

clear path to strong earnings growth over many years, a

ber of other experienced execu ves from the pharmaâ€

capable management team, high returns on capital and a

ceu cal, medical devices, health insurance and consumâ€

dominant market posi on with high barriers to entry.

er products industries.

Ul mately it was these a ributes, along with a pa ent outâ€

Finally, Botox stood out as a par cularly remarkable

look, that led to the investment being such a success for

therapy in that it was a biological medicine which was

our clients. It occurred to us that a case study of our

difficult to manufacture and had already lost patent

Allergan holding might be a great way for investors to

protec on several years prior. It also had a variety of

be er understand our investment approach. Thus, what

therapeu c uses, an established cosme c brand and

follows is a detailed account of Allergan’s “lifecycle” in our

dominant market share. S ll, this was just a ï¬rst pass.

por olio, star ng from our ini al research on the company

Much more work would need to be done in order to

and concluding with its eventual acquisi on by Actavis plc.

determine whether Allergan was worthy of one of the

We hope that you ï¬nd the discussion instruc ve and enâ€

twenty or so spots in our por olio.

lightening.

2

. A er his ini al note, Damon con nued to follow Allergan

closely and updated his thoughts with addi onal notes

every three months. He examined the company’s 2005

acquisi on of Inamed, a manufacturer of breast implants

and dermal ï¬llers, for which Allergan paid $3bn and

trumped a compe ng offer from rival Medicis. The deal

wasn’t cheap, with Allergan paying over 30x adjusted

earnings, but it was becoming clear that Allergan’s CEO

since 1998, David Pyo , had a vision for where he wanted

to take the company. Allergan’s product set focused

increasingly on localized treatments (eye drops, injectable

medicines, skin creams) rather than systemic ones

(tradi onal oral medica ons). Localized treatments are

o en more effec ve with less side effects than their

systemic counterparts.

Furthermore, Inamed’s focus on breast and facial aesâ€

the cs would be a nice complement to the company’s

Botox franchise. The aesthe cs business had a rac ve

economics due to the fact it was more of a consumer

franchise than a true pharmaceu cal one. Therefore

typical obstacles for drug companies, such as insurance

reimbursement and patent expira ons, weren’t as big an

issue. Addi onally, Pyo made a point of becoming verâ€

cally integrated so that Allergan controlled the developâ€

ment, manufacturing and distribu on of its products. As

a result, a defendable moat was forming around the enâ€

re business that would increasingly enable Allergan to

gain scale rela ve to many of its smaller peers. Pyo ’s

goal was for Allergan to be the number one or two playâ€

er in its major markets (something that would subseâ€

quently be achieved).

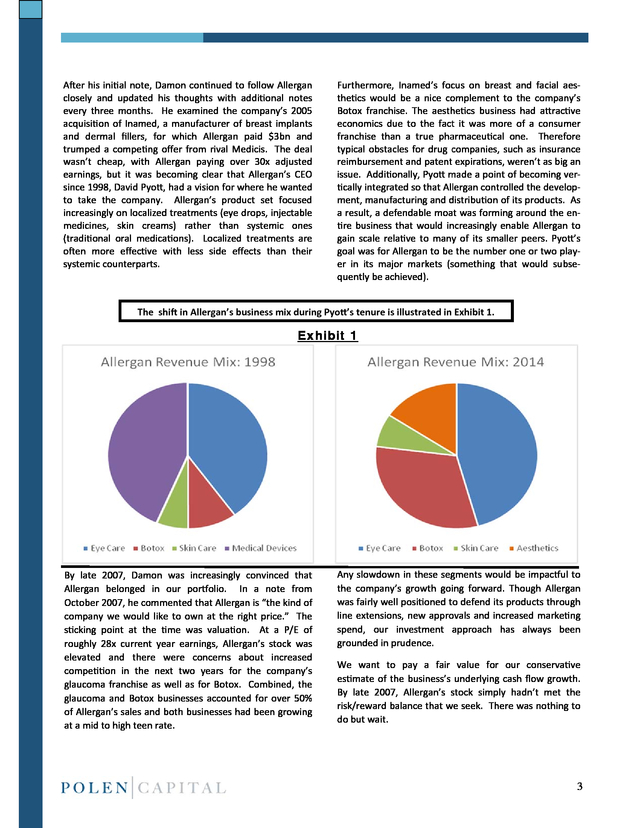

The shi in Allergan’s business mix during Pyo ’s tenure is illustrated in Exhibit 1.

Exhibit 1

By late 2007, Damon was increasingly convinced that

Allergan belonged in our por olio. In a note from

October 2007, he commented that Allergan is “the kind of

company we would like to own at the right price.” The

s cking point at the me was valua on. At a P/E of

roughly 28x current year earnings, Allergan’s stock was

elevated and there were concerns about increased

compe on in the next two years for the company’s

glaucoma franchise as well as for Botox. Combined, the

glaucoma and Botox businesses accounted for over 50%

of Allergan’s sales and both businesses had been growing

at a mid to high teen rate.

Any slowdown in these segments would be impac ul to

the company’s growth going forward. Though Allergan

was fairly well posi oned to defend its products through

line extensions, new approvals and increased marke ng

spend, our investment approach has always been

grounded in prudence.

We want to pay a fair value for our conserva ve

es mate of the business’s underlying cash flow growth.

By late 2007, Allergan’s stock simply hadn’t met the

risk/reward balance that we seek. There was nothing to

do but wait.

3

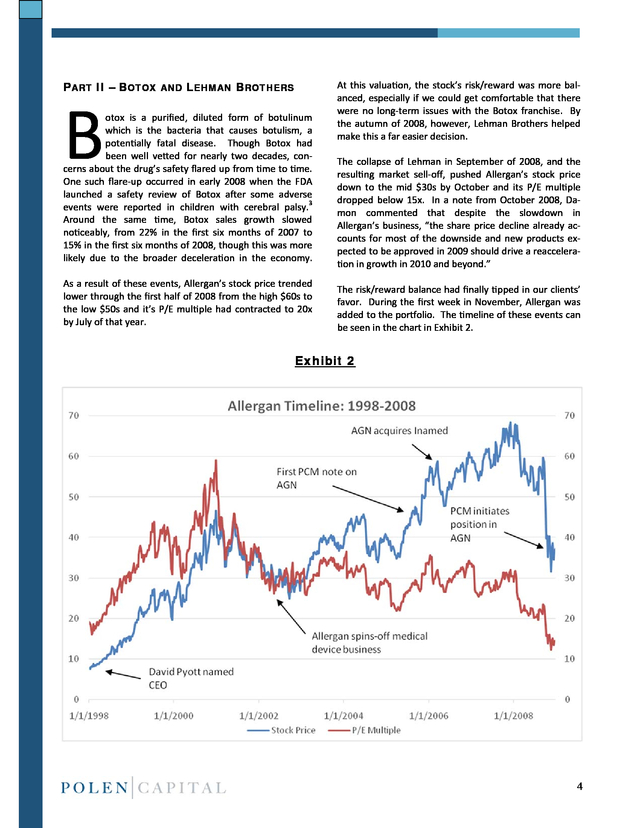

. PART II – BOTOX AND LEHMAN BROTHERS

B

otox is a puriï¬ed, diluted form of botulinum

which is the bacteria that causes botulism, a

poten ally fatal disease. Though Botox had

been well ve ed for nearly two decades, conâ€

cerns about the drug’s safety flared up from me to me.

One such flareâ€up occurred in early 2008 when the FDA

launched a safety review of Botox a er some adverse

events were reported in children with cerebral palsy.3

Around the same me, Botox sales growth slowed

no ceably, from 22% in the ï¬rst six months of 2007 to

15% in the ï¬rst six months of 2008, though this was more

likely due to the broader decelera on in the economy.

As a result of these events, Allergan’s stock price trended

lower through the ï¬rst half of 2008 from the high $60s to

the low $50s and it’s P/E mul ple had contracted to 20x

by July of that year.

At this valua on, the stock’s risk/reward was more balâ€

anced, especially if we could get comfortable that there

were no longâ€term issues with the Botox franchise. By

the autumn of 2008, however, Lehman Brothers helped

make this a far easier decision.

The collapse of Lehman in September of 2008, and the

resul ng market sellâ€off, pushed Allergan’s stock price

down to the mid $30s by October and its P/E mul ple

dropped below 15x. In a note from October 2008, Daâ€

mon commented that despite the slowdown in

Allergan’s business, “the share price decline already acâ€

counts for most of the downside and new products exâ€

pected to be approved in 2009 should drive a reacceleraâ€

on in growth in 2010 and beyond.”

The risk/reward balance had ï¬nally pped in our clients’

favor. During the ï¬rst week in November, Allergan was

added to the por olio. The meline of these events can

be seen in the chart in Exhibit 2.

Exhibit 2

4

. PART III – LET THE COMPOUNDING BEGIN

A

The global market for Wet AMD drugs was nearly $4bn

at the me with the vast majority of sales split among

only three drugs which meant that DARPin, to the extent

it was truly differen ated, could be a meaningful

revenue contributor to Allergan if it proved to be

successful.4 Finally, the company was running trials to

inves gate whether its product La sse, which was

approved as a treatment to thicken eyelashes, might also

be u lized as a treatment for hair regrowth that would

be superior to the widely used Minoxidil. Allergan’s

future looked as bright as ever.

er our ini al purchase of Allergan in Novemâ€

ber of 2008, we gradually built our posi on in

the stock during the next several months; by

midâ€2009 it was a 6% weight in our por olio.

As Damon had predicted the slowdown in Allergan’s

aesthe c businesses, namely Botox, proved to be

temporary and star ng in late 2009, the company’s

business began to reâ€accelerate. In the ï¬rst quarter of

2009 Allergan’s sales declined by 6.5%, but by the fourth

quarter of 2009 total sales growth had reâ€accelerated to

16%. Importantly, on an annual basis Allergan grew both

sales and earnings during the recession.

PART IV – DOUBLE WHAMMY

This has been a hallmark of the types of businesses we

or longâ€term investors, the convic on they have

seek to invest in at Polen Capital: those with the ability to

in an investment thesis is inevitably put to the

grow even during tough economic periods. Allergan’s

test at some point during their holding period.

strong growth con nued during the next three years and

Polen’s moment with Allergan occurred in 2013

from 2009â€2012 the company had annual compounded

when the company was hit with two bits of bad news in

earnings growth of 14%. Addi onally, the stock’s P/E

short succession.

mul ple began to expand again as business fundamentals

improved, which propelled Allergan’s stock from $40 per

The year had started out great for Allergan investors and

share at the end of 2008 to $91 per share by yearâ€end

in the ï¬rst four months of 2013 the stock had risen 24%.

2012, an annualized gain of nearly 23%.

But that ebullience quickly subsided when the company

reported its ï¬rst quarter earnings and surprised

Botox grew during this period to become a $1.8bn

investors by announcing that their promising DARPin

franchise by yearâ€end 2012. Even at this size it was s ll

therapy as well as La sse for hair regrowth would both

growing at a low doubleâ€digit rate and this was despite

be delayed as the company needed to run more trials.

new compe on that had entered the market in the past

In both cases it appeared that the clinical results were

two years. The eye care division also con nued its steady

not as encouraging as ini ally hoped and more data

growth, despite increased compe on. The standout in

would be needed to prove the efficacy of the therapies.

the company’s eye care franchise was Restasis, the only

Though it was notable that the trials for both therapies

FDAâ€approved prescrip on treatment for dryâ€eye. By year

were only delayed and not terminated—a far more

â€end 2012, Restasis was growing at a midâ€teens rate and

nega ve outcome—investors were s ll dissa sï¬ed.

generated nearly $800mm in sales, 14% of the company’s

total revenues at that point.

Allergan’s stock fell 13% the day the news was anâ€

nounced. Despite this setback, and somewhat lost in the

Allergan’s management team also con nued to devote

noise around the disappoin ng trial results, Allergan’s

substan al company cash flow to new product

core business was s ll performing very well with ï¬rst

development. Botox had received approval for treatment

quarter sales up 9% and adjusted EPS up 16%. With such

of chronic daily headaches and was likely to be approved

strong ongoing fundamental business performance, we

for treatment of overâ€ac ve bladder in the coming

were comfortable looking beyond a couple of temporary

months. The company had also licensed a drug called

pipeline setbacks.

DARPin, which is a therapy for Wet Ageâ€Related Macular

Degenera on (Wet AMD) that was in Phase II trials. Wet

Allergan was broadsided again less than two months

AMD is a chronic eye disease that can cause permanent

later when the FDA proposed dra guidance that would

vision loss and is typically treated with painful injec ons

lower the bar for bringing a generic form of Restasis to

to the back of the eye. Newer treatments such as DARPin

market. For some context, Restasis (a prescrip on

featured a longer treatmentâ€dura on proï¬le, which

treatment for dry eye that comprised nearly 15% of

meant pa ents could poten ally go extended intervals

Allergan’s sales) was a hardâ€toâ€manufacture emulsion

(every three months) between injec ons.

product.

F

5

. The company’s patent on the drug was due to expire in

2014 but, because of the difficul es in manufacturing and

tes ng a compe ve emulsion, no generic company had

even bothered to challenge the patent. This niche

prescrip on market essen ally belonged to Allergan.

The FDA’s new dra guidance, however, would poten ally

make it much easier to develop a compe ve product by

not requiring a generic company to run the large pa ent

trials previously deemed necessary to gain approval.

Essen ally, the dra guidance proposed that by simply

proving their emulsion was close enough in characteris cs

(“bioequivalence” in industry parlance), a generic drug

manufacturer could poten ally get approval. Typically

the FDA only grants these types of approvals for oral pills

that are easier to manufacture. For a more complex

product like Restasis this appeared to be an unusual deâ€

cision. Not surprisingly, Allergan’s stock was hit hard

once again; it fell 12% the day the FDA released their

dra guidance and was down 30% from its April high.

Once a Wall Street darling, sellâ€side analysts

began abandoning the Allergan ship and a slew of downâ€

grades followed. It was only natural that we asked

ourselves if we should consider doing the same.

A meline of the events from 2009â€2013 are shown in the chart in Exhibit 3.

Exhibit 3

Despite much consterna on, there was one ques on that

was paramount: Even with these recent issues, was

Allergan s ll a great business for the longâ€term? Our

answer was undoubtedly yes. The company’s midâ€stage

pipeline had taken a couple of hits with delays for DARPin

and La sse, but this seemed fully accounted for now in

the stock price. Even the poten al for generic

compe on with Restasis appeared to be discounted in

the current valua on. By midâ€year 2013 Allergan shares

traded for about 18x earnings, the lowest P/E mul ple

since 2009. Growth in the core franchise was s ll very

healthy, the compe ve advantages around the business

remained very strong and management had several levers

it could pull.

Measures such as cost reduc ons or share repurchases

could be implemented to enhance earnings growth.

Furthermore, it was en rely possible that the current

issues that had affected the company might resolve

favorably. Both DARPin and La sse had been delayed

but not terminated and the company planned to

vigorously challenge the FDA’s dra guidance on Restasis

generics.

Since the bad news had already been priced into the

stock, there was op onality if any of these issues worked

out posi vely. With Allergan’s stock a 5.5% weight in our

por olio, we decided to maintain our posi on.

6

. PART V – A ‘VALEANT’ FIGHT

F

rom June 2013 un l November of that year,

Allergan’s stock treaded water. By late in the

fourth quarter, however, the stock began to reâ€

cover nicely and for the year actually appreciated

21%. The company’s fundamentals con nued to shine

through, and for the full year 2013 total sales grew 11.5%

and adjusted EPS grew 18%. Addi onally, late in the year

the company began to take aggressive ac on to defend its

Restasis franchise by ï¬ling new patents on the product

that would have poten ally delayed any generic compe â€

on for several addi onal years.

As the calendar flipped into 2014 it appeared that the

issues that had plagued Allergan the year before may have

simply been speed bumps. But then in midâ€April of that

year something odd began to happen. Allergan’s stock

price started rapidly apprecia ng on heavy volume. From

April 10 to April 21 the stock price rallied from $116 to

$142. We speculated as to what could be driving the

share price higher in such brisk fashion, and by the end of

the day on April 21 we had our answer.

Valeant Pharmaceu cals, in collabora on with the hedge

fund Pershing Square, made an unsolicited offer to acâ€

quire Allergan for nearly $48bn, or roughly $160/share.

The offer was a mix of cash (roughly $15bn) and Valeant

stock. Addi onally, Pershing Square, run by wellâ€known

hedge fund manager Bill Ackman, had accumulated a

nearly 10% stake in Allergan in the days leading up to the

offer announcement. Allergan’s stock moved sharply highâ€

er and by April 25 was $168.

This unusual partnership, with Ackman’s fund acquiring a

massive stake in Allergan immediately prior to a deal

being made public, quite frankly didn’t pass the smell test

to us. But it became clear in the days following the

announcement that both Pershing Square and Valeant

had taken great pains to ensure compliance with SEC regâ€

ula ons.

There were two issues that immediately leapt out to us

shortly a er the Valeant/Pershing proposal was anâ€

nounced. First, the offer was far short of our es mate

of fair value for Allergan’s business. Second, it was very

unlikely that we would be interested in holding Valeant

stock should a deal between the companies actually be

consummated. Valeant Pharmaceu cals was a Canadaâ€

based business that had grown rapidly over the last few

years with an aggressive M&A strategy that took

advantage of the company’s low corporate tax rate.

This low rate, only 8% in Canada, allowed Valeant to

acquire businesses in higher tax jurisdic ons such as

the U.S. and make them highly accre ve almost

immediately. Valeant pursued what we liked to term

an “op miza on strategy.”

The company was led by a no nonâ€sense CEO, Mike

Pearson, who felt that the pharmaceu cal industry wastâ€

ed far too much money in trying to develop drugs, many

of which would never even reach commercializa on. His

approach was to acquire companies with

products that had steady, predictable growth and li le

patent risk or insurance reimbursement issues and then

“op mize” the assets by stripping out excess costs

associated with R&D and marke ng.

To this end, Allergan was an ideal target for him with its

mix of durable products in aesthe cs, skin care and eye

care. Valeant had already acquired Allergan’s rival

Medicis in 2012 as well as contact lens manufacturer

Bausch & Lomb in 2013. As a result of this aggressive

buying spree, Valeant’s balance sheet had in excess of

$17bn in longâ€term debt by the end of 2013 compared to

only a li le over $5bn in equity.

With our strict focus on companies with strong balance

sheets, Valeant’s aggressive M&A strategy and high debt

levels made it a poor ï¬t for our por olio.5 Because the

majority of Valeant’s offer for Allergan was comprised of

stock rather than cash it was clear from the outset that

Valeant’s management would be keen on promo ng the

value their deal created for both companies’ shareholdâ€

ers. As investor conï¬dence in the deal increased, so too

would Valeant’s stock price which in turn would push up

the overall value of their offer.

So it was not a surprise to us, as a large Allergan

shareholder, when in early May we were contacted by

Valeant’s management team. They wanted to meet to

discuss the offer and were willing to come down to our

office in Florida. At that mee ng Mike Pearson, as well

as Valeant’s CFO Howard Schiller, laid out their case for

the deal and why our focus shouldn’t just be on the offer

at hand but on the longâ€term poten al of the combined

businesses. We discussed with them our concerns

around Valeant’s business model and balance sheet and

expressed that we were not likely to own the combined

company in our por olio.

As such, we were not interested in the poten al for

postâ€deal synergies, but were seeking full and certain

value for our Allergan shares. Furthermore, we were

content to con nue to own standâ€alone Allergan and let

the business compound earnings and value over me.

7

.

To the extent Valeant was feeling us out to see if we

would support the deal, they likely le disappointed.

A er our mee ng with Valeant, we scheduled a mee ng

with Allergan’s management team at their company

headquarters in Irvine, CA. At that mee ng, our CIO Dan

Davidowitz was forthright about where we stood. “We

view Allergan as a great business,” he told CEO David Pyâ€

o , “so if someone wants our shares they’ll need to pay a

premium to get them.”

Pyo , a so â€spoken Brit with Sco sh parents, happily

agreed telling us that, despite his long tenure at Allergan,

this was not an emo onal decision. His priority was to

maximize value for Allergan shareholders by providing the

investment community with perspec ve on the compaâ€

ny’s future growth poten al. Doing so would effec vely

raise the bar for an acquirer, Valeant or otherwise, as Alâ€

lergan shareholders would see the true value of the busiâ€

ness and demand a fair price for it. But this process would

take me and require some pa ence. We le the mee ng

feeling conï¬dent that management’s priori es appeared

to be completely aligned with ours and our clients. The

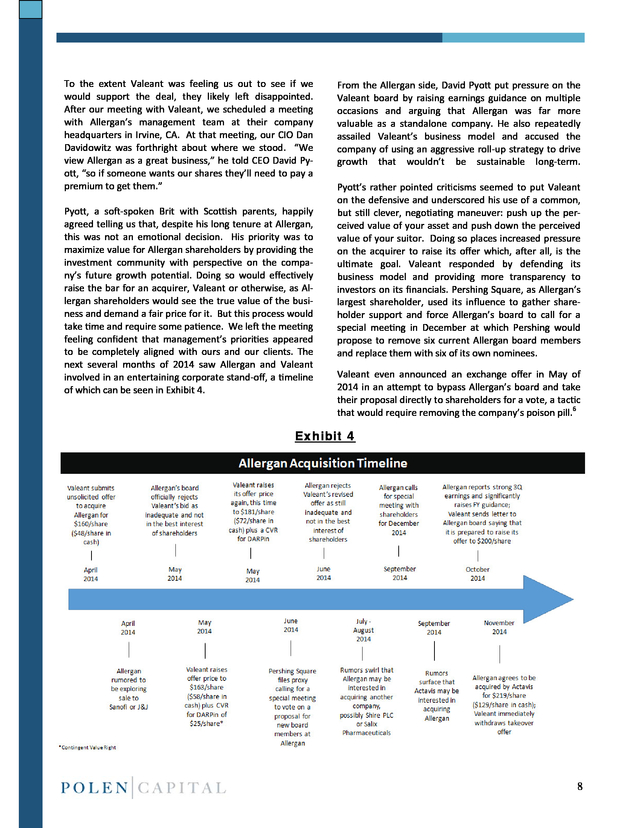

next several months of 2014 saw Allergan and Valeant

involved in an entertaining corporate standâ€off, a meline

of which can be seen in Exhibit 4.

From the Allergan side, David Pyo put pressure on the

Valeant board by raising earnings guidance on mul ple

occasions and arguing that Allergan was far more

valuable as a standalone company. He also repeatedly

assailed Valeant’s business model and accused the

company of using an aggressive rollâ€up strategy to drive

growth that wouldn’t be sustainable longâ€term.

Pyo ’s rather pointed cri cisms seemed to put Valeant

on the defensive and underscored his use of a common,

but s ll clever, nego a ng maneuver: push up the perâ€

ceived value of your asset and push down the perceived

value of your suitor. Doing so places increased pressure

on the acquirer to raise its offer which, a er all, is the

ul mate goal. Valeant responded by defending its

business model and providing more transparency to

investors on its ï¬nancials. Pershing Square, as Allergan’s

largest shareholder, used its influence to gather shareâ€

holder support and force Allergan’s board to call for a

special mee ng in December at which Pershing would

propose to remove six current Allergan board members

and replace them with six of its own nominees.

Valeant even announced an exchange offer in May of

2014 in an a empt to bypass Allergan’s board and take

their proposal directly to shareholders for a vote, a tac c

that would require removing the company’s poison pill.6

Exhibit 4

8

. All of this was great theater but one issue we needed to

contend with was what to do with our posi on in

Allergan, which by June 2014 was nearly a 9% weight in

our por olio. Clients repeatedly inquired if we were preâ€

paring to trim our weight in the stock. They asked if we

were concerned what would happen if the deal fell

through and Valeant walked away. Wouldn’t Allergan’s

stock plummet back to where it was before the offer was

announced in April? While these concerns were certainly

legi mate, Dan and Damon were steadfast in their belief

that the risk/reward was s ll very much skewed in our

clients’ favor. Their argument was that Allergan’s

increased guidance helped put a floor under the stock as

the company’s earnings power was now more evident.

W

Furthermore, based on Allergan’s 2015 EPS guidance of

roughly $8.50 and assuming a historically average mul â€

ple for the stock of 23x, the implied fair value for the

company was nearly $200/share. Thus, Valeant’s various

bids appeared to offer li le in the way of a true premium

to our reasonable assessment of intrinsic value for the

business. In Dan and Damon’s es ma on, a higher offer

was likely. Indeed, when Actavis announced in

November that Allergan had agreed to an offer valued at

$219/share there was a feeling of bi ersweet sa sfacâ€

on. The premium we sought for our clients was ï¬nally

achieved though at the cost of losing one of the best

businesses that we had ever owned.

POST-MORTEM

e maintained our signiï¬cant weigh ng in

Allergan un l December of 2014. By this

me the stock was at $211 per share and

a 10% weight in our por olio. At this price

it was a 6.5% discount to the announced offer price and

with the risk/reward now more balanced, and a higher

offer much less likely, the prudent course of ac on was to

begin trimming our holding. Actavis, similar to Valeant,

was a fast growing pharmaceu cal company that had

been on an aggressive acquisi on spree. Tradi onally it

had focused on generic medicines but was now beginning

to branch out to the branded space as well. Prior to

acquiring Allergan, the company had purchased drug

maker Forest Labs for $23bn in early 2014. Also similar to

Valeant, this acquisi on binge had caused the company’s

debt to balloon to levels that we felt were not

appropriate for our por olio. Thus by February of 2015,

with no inten on of holding Actavis stock and the

remaining premium to the closing of the deal in March at

only 3%, we sold our remaining stake in Allergan at $226/

share.

All told, since our ini al purchase in 2008 Allergan stock

delivered to our clients an annualized total return of

32%. Over that same me period the business grew its

adjusted EPS at about 21% per annum. It’s this last

sta s c that is perhaps the most per nent one.

Ul mately, the majority of Allergan’s return during our

holding period was propelled by the company’s

underlying earnings growth with the remainder driven by

P/E mul ple expansion. We expect that this would hold

true for all of our investments. That is, for the majority

(if not all) of the total investment return to be driven by

earnings growth with mul ple expansion and dividend

yield being more modest contributors. Our longâ€term

approach remains the same: iden fy wellâ€run businesses

with sustainable compe ve advantages, high returns on

capital, above average earnings and free cash flow

growth, rockâ€solid balance sheets and strong secular

tailwinds. We believe focusing on just a handful of these

most excep onal companies leads to the best

investment outcomes for our clients.

Endnotes

1. Allergan’s ophthalmic franchise consisted of prescription treatments

for glaucoma and dry eye as well as OTC eye care products such as

Refresh.

2. By 2006, Botox was approved for a wide range of neuromuscular

disorders such as blepharospasm (eyelid spams), strabismus (crosseyed) and hyperhidrosis (excessive underarm sweating). About half of

Botox’s sales were therapeutic with the other half being cosmetic.

3.

Botox was not approved for cerebral palsy but was sometimes used off-label to help control spasms. 4. Those three drugs were Lucentis and Avastin (Roche) and Eylea (Regeneron) 5. Though not a good fit for us, Valeant has proven to be a highly successful investment and we hold the company’s largest shareholder, Ruane, Cunniff & Goldfarb, in high esteem.

As of 12/31/2014 VRX’s 10-year annualized total return was nearly 30% compared to 8% for the S&P 500. Source: Factset. 6. Immediately after the Valeant offer was announced, Allergan’s board adopted a poison pill that effectively blocked any shareholder from acquiring more than a 10% stake in the company.

The only practical way of removing this poison pill was to vote in new board members who would be supportive of such action. In order to change board members, one would need votes from a majority of the shareholder base. Hence, garnering at least 50% of shareholders’ support was a critical goal for Valeant and Pershing Square. 9 .

About the Author Stephen Atkins, CFA, Research Analyst, joined Polen Capital in 2012 a er a 12â€year tenure as a por olio manager at Northern Trust investments—including eight years as a mutual fund coâ€por olio manager. Mr. Atkins also spent two years at Carl Domino Associates, LP. He received his B.S. in Business Administra on from Georgetown University and a General Course degree from the London School of Economics. Mr. Atkins is a CFA Charterholder and a member of the CFA Ins tute and CFA Society of South Florida. About Polen Capital Polen Capital is an independentlyâ€owned Growth equity bou que that is managed and run by an experienced and though ul group of ï¬nancial professionals who are focused on our disciplined Investment Strategy. At Polen Capital, we believe that consistent earnings growth is the primary driver of intrinsic value and long â€term stock apprecia on. Our efforts focus on iden fying and inves ng in a concentrated por olio of high quality companies that we believe are capable of delivering sustainable, aboveâ€average earnings growth. By thinking and inves ng like a business owner and taking a longâ€term investment approach, we believe we can preserve capital and provide stability in vola le markets. Our Strategy is accessible through our Mutual Fund, Separately Managed Accounts (SMAs) and Undertakings for the Collec ve Investment of Transferable Securi es (UCITS). Ins tu onal Rela ons + 1â€800â€358â€1887 Ins tu onalrela ons@polencapital.com 1825 NW Corporate Blvd. Suite 300, Boca Raton, FL 33431 www.polencapital.com The information provided in this report should not be construed as a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in the composite at the time you receive this report or that the securities sold have not been repurchased. The securities discussed do not represent the composite’s entire portfolio. Actual holdings will vary depending on the size of the account, cash flows and restrictions. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

For a complete list of Polen’s past specific recommendations holdings report and current holdings as of the current quarter end, please contact Polen Capital at info@polencapital.com 10 .

Botox was not approved for cerebral palsy but was sometimes used off-label to help control spasms. 4. Those three drugs were Lucentis and Avastin (Roche) and Eylea (Regeneron) 5. Though not a good fit for us, Valeant has proven to be a highly successful investment and we hold the company’s largest shareholder, Ruane, Cunniff & Goldfarb, in high esteem.

As of 12/31/2014 VRX’s 10-year annualized total return was nearly 30% compared to 8% for the S&P 500. Source: Factset. 6. Immediately after the Valeant offer was announced, Allergan’s board adopted a poison pill that effectively blocked any shareholder from acquiring more than a 10% stake in the company.

The only practical way of removing this poison pill was to vote in new board members who would be supportive of such action. In order to change board members, one would need votes from a majority of the shareholder base. Hence, garnering at least 50% of shareholders’ support was a critical goal for Valeant and Pershing Square. 9 .

About the Author Stephen Atkins, CFA, Research Analyst, joined Polen Capital in 2012 a er a 12â€year tenure as a por olio manager at Northern Trust investments—including eight years as a mutual fund coâ€por olio manager. Mr. Atkins also spent two years at Carl Domino Associates, LP. He received his B.S. in Business Administra on from Georgetown University and a General Course degree from the London School of Economics. Mr. Atkins is a CFA Charterholder and a member of the CFA Ins tute and CFA Society of South Florida. About Polen Capital Polen Capital is an independentlyâ€owned Growth equity bou que that is managed and run by an experienced and though ul group of ï¬nancial professionals who are focused on our disciplined Investment Strategy. At Polen Capital, we believe that consistent earnings growth is the primary driver of intrinsic value and long â€term stock apprecia on. Our efforts focus on iden fying and inves ng in a concentrated por olio of high quality companies that we believe are capable of delivering sustainable, aboveâ€average earnings growth. By thinking and inves ng like a business owner and taking a longâ€term investment approach, we believe we can preserve capital and provide stability in vola le markets. Our Strategy is accessible through our Mutual Fund, Separately Managed Accounts (SMAs) and Undertakings for the Collec ve Investment of Transferable Securi es (UCITS). Ins tu onal Rela ons + 1â€800â€358â€1887 Ins tu onalrela ons@polencapital.com 1825 NW Corporate Blvd. Suite 300, Boca Raton, FL 33431 www.polencapital.com The information provided in this report should not be construed as a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in the composite at the time you receive this report or that the securities sold have not been repurchased. The securities discussed do not represent the composite’s entire portfolio. Actual holdings will vary depending on the size of the account, cash flows and restrictions. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

For a complete list of Polen’s past specific recommendations holdings report and current holdings as of the current quarter end, please contact Polen Capital at info@polencapital.com 10 .