Description

1825 NW Corporate Blvd., Suite 300 • Boca Raton, FL 33431 • Tel: 561-241-2425 • www.polencapital.com

October 18, 2016

Polen Global Growth Portfolio

3rd Quarter 2016 Commentary

Summary:

ï‚· In the 3rd quarter of 2016, the Polen Global Growth Portfolio (the “Portfolio”) returned 6.48% before fees,

compared to 5.30% for the MSCI Allâ€Country World Index, a difference of 1.18%.

ï‚· The portfolio’s annualized return since inception on January 1st, 2015 is 8.58% before fees compared to

2.31% for MSCI ACWI, a difference of 6.27%.

ï‚· We believe investment performance since inception has been driven by consistent, doubleâ€digit earnings

growth and we expect this to continue in 2016 and going forward.

ï‚· Approximately 14% growth in earnings per share is expected for the Portfolio in 2016, compared to 1%

growth in earnings per share for the Global stock market index.

Investment Performance Commentary:

In the 3rd quarter of 2016, the Polen Global Growth Portfolio returned 6.48% before fees compared to 5.30% for

the MSCI Allâ€Country World Index, a difference of 1.18%. Most portfolio holdings, sectors and regions contributed

positively to investment performance last quarter, with the strongest absolute performance coming from several

holdings in the technology sector and the Asiaâ€Pacific region. Weaker investment performance came from the

very few investments the Portfolio holds in the materials and industrials sectors.

Yearâ€toâ€date investment performance was 4.93% at the end of the quarter, clearly in positive territory, but some

way behind MSCI ACWI at 6.60%, a difference of 1.67%. The Portfolio is managed for absolute returns, rather than

relative return, and I expect business performance – specifically compound earnings growth – to be the main

driver of investment performance over the years. Realistically, periods of some relative underperformance

compared to stock markets are likely, if not inevitable, along the way. That said, it is still useful to think through

the reasons for any lag in relative performance, mainly as a check on the quality of the businesses the Portfolio

holds.

The macroeconomic environment mentioned in past commentaries – especially the 1st quarter 2016 commentary

– has persisted, with relatively slow and uneven growth but with some increasing signs of price disâ€inflation

appearing through the year and signs of price deflation here and there. Developed economies continue to underâ€

achieve their potential growth rates mainly, it seems, due to selfâ€inflicted and structural challenges, and both the

United States and the Euro area are currently seeing growth in gross domestic product of less than 2%. Consumer

prices are increasing slightly according to government statistics but barely and, in any case, not enough to dissuade

central banks from a continuing and very aggressive policy stance, typically including quantitative easing and

targeting historically low short†and longâ€term interest rates. For example, it is not easy to identify any developed

economy with 10â€year government bonds yielding more than 2% and bond yields nearer 0% are increasingly

normal. A common thread from our last research trip to visit consumer and healthcare businesses based in Europe

was management comments indicating a slower growth environment in emerging markets compared to the last

few years. Among the largest emerging market economies, China is experiencing at least a mild slowdown in

Please reference the supplemental information to the composite performance which accompanies this commentary.

. growth according to official data. Brazil and Russia are in recession. Of the four BRICs, only India continues to

perform relatively well.

This is not a promising backdrop for growth in corporate earnings, yet global stock markets have performed

reasonably well so far this year. Extremely low interest rates help to explain this disconnect. On one hand,

traditionally defensive sectors of the stock market including consumer staples, telecommunications and utilities

are performing relatively well. For some investors, stocks in these sectors have been acceptable substitutes for

bonds because of their relatively recurring revenues and dividend yields near or above yields available on

government bonds. Low interest rates are also fueling “risk on” stock market sentiment, helping to explain even

stronger performance in proâ€cyclical sectors including energy, industrials and materials. These three sectors

comprise just over 20% of the global stock market index and, with doubleâ€digit gains in each sector, have

contributed close to 3.5% or almost half of the stock market’s performance this year.

As an investment team, we quite often find the quality of earnings we are looking for among consumer staples

companies but not always the rate of sustainable growth we are looking for. Both quality and growth rate of

earnings are lacking across almost all energy, industrial and materials companies from our point of view. In these

sectors, the outlook for earnings may or may not improve in the shortâ€term but the Portfolio remains effectively

underweight with holdings limited to companies in sectors with more persistent and sustainable earnings.

Overview of the Portfolio:

The Portfolio remains concentrated with investments in 30 businesses. Sixteen holdings are based in the United

States and 14 in the rest of the world. Revenues provide a clearer picture of economic exposure and, on this basis,

the Portfolio has close to 50% exposure to the United States and 50% to the rest of the world. The Portfolio also

has a strong bias to larger cap and globally competitive businesses which remain the backbone of the holdings and

more than 75% of assets. These companies tend to have the advantages to compete successfully in many different

countries. This approach is intended to lessen the impact of macroeconomic risks on the Portfolio, especially

country and currencyâ€specific risk. There are currently no holdings listed on stock exchanges in emerging markets,

although emerging market economies are 15% †20% of total revenues.

Earlier in the year, the Portfolio was on track to generate earnings growth in the range of 12% †14% in U.S. dollars

in 2016. Coming into the home stretch, that range seems a little conservative. Relative strength of currencies

including the U.S. dollar and Swiss Franc has been a slight headwind to earnings growth but more than offset by

resilient, underlying earnings performance. Earnings growth of 14% †15% is now more realistic this year. This

range is consistent with the outlook for the next five years. As mentioned in the 1st Quarter commentary,

consensus estimates of earnings growth for the broader global stock market always looked a bit generous. As the

year has gone on, those estimates have come down, and consensus expectations are now 0% †1% earnings growth

in 2016.

Performance Attribution:

Contributors to performance included ARM Holdings plc, Tencent Holdings Ltd. and Alibaba Group Holdings Ltd.

ARM is discussed in some more detail below.

Tencent was included in the Portfolio at inception and is now a top five holding. The company has successfully

bundled and integrated a range of online services used by almost 700 million smartphone subscribers in China.

Tencent provides services that seem to have become indispensable to users including messaging, social

networking, voice calls, browsing, gaming ecommerce and payments, among many others. The WeChat app might

be used to book a hospital appointment, or pay a parking ticket or by parents to stay in touch with small children.

Please reference the supplemental information to the composite performance which accompanies this commentary.

. Infants too young to carry a mobile phone may have a cuddly toy that is also a connected device to chat with mum

and dad. The app might be better described as a kind of operating system that helps users navigate the day. It has

become such a part of people lives that it now accounts for about 33% of the time Chinese mobile phone users

spend online. About half of all users have linked their bank accounts to the WeChat app, which is routinely used

for a variety of online and offline payments. If all of this sounds hard to imagine, it is because nothing outside

China has come close to the usefulness WeChat provides. To most WeChat users, Western apps would look like a

step backward in time. You might say that to understand the future of the mobile internet, the West should look

to China, except even the strongest internet enterprises in the United States will struggle to achieve the

integration of offerings WeChat has. It is still relatively early in seeing how much revenue Tencent can generate

from its current base of users, but the strong engagement Tencent enjoys from a very large population and a

scalable business model indicates a highly sustainable stream of earnings to come. Tencent’s share price has

appreciated approximately inâ€line with earnings growth, which is expected to be around 30% in U.S. dollars this

year. While some growth has been coming from further expansion in the number of WeChat users, recent

earnings reports have shown that most earnings growth has been driven by increasing revenue per user across

smartphone games, advertising and social networking. At the time of writing, Tencent’s market capitalization of

approximately $250 billion makes it the most valuable public company based outside the United States.

Alibaba was also a contributor to investment performance. In previous commentaries I have outlined our

conviction in Alibaba as a sustainable growth business. I said that the company provides and operates the

technology that connects buyers and sellers, enabling most of the eâ€commerce in the world’s second largest

economy, which is woefully underâ€served by traditional, bricks and mortar retailers. As with Tencent, there is no

precise comparison we can make with a familiar online business in the West. Alibaba is not technically an online

retailer, like Amazon, for example, because it owns little or no inventory. If it were a retailer though, it would be

the world’s largest, slightly ahead of Walâ€Mart with more than $500 billion of sales across its two retail

marketplaces. Recent earnings reports have indicated continued growth in the number of shoppers. The number

is approaching 500 million, or approximately 60% of China’s internet population. Customers seem to be very

comfortable with the range of product offerings, the convenience, the overnight delivery Alibaba’s logistics

partners are frequently able to provide, and the secure payment method provided through Alipay, which was

critical to the company’s early success and ability to scale. Shoppers are, on average, ordering more than once a

week. To put this in context, Alibaba and its partners are handling in the region of 25 billion individual orders per

year, or 70 million orders every day. The sheer magnitude of orders helps to explain why Amazon has struggled to

bring its model to the Chinese market. A growing number of Alibaba customers are spending about $19 on an

average order and about 50 cents per order comes to Alibaba in the form of advertising and other revenues. This

take rate has been edging up recently as Alibaba deepens its engagement with shoppers. With very little capital

investment needed, the balance sheet is asset light and debt free. This also means that much of the revenue tends

to convert to free cash flow and Alibaba seems likely to generate 20 – 25 cents per order (40% †50% of revenue) in

free cash flow again this year. It has been remarkable to see wild swings in stock market sentiment around such a

consistent business, but as with other holdings in the Portfolio, we anticipate earnings performance will resolve

any doubts over time. A reasonable expectation would be 25% growth in earnings and cash flow in 2016.

The main detractor from performance last quarter was the relatively small holding in Novo Nordisk A/S. Novo is

the leading diabetes care business in the world with a track record of innovation and consistent, profitable growth.

Diabetes is both a pandemic that affects about 400 million people and a chronic disease that can lead to increased

risk of heart attack, stroke, kidney failure and blindness, among other complications. The diabetes patient

population continues to grow as a result of dietary trends, rising incidence of obesity and the rate of urbanization

in emerging markets, yet relatively few patients receive the care they need. The primary treatment for diabetes is

a range of insulin analogs that do not cure diabetes but effectively and safely control the disease, reducing the risk

of complications and even more serious illness (and of course the costly additional burden for health care

systems). Still, only about 50 million people, or less than 15% of the patient population, use insulin, which suggests

Please reference the supplemental information to the composite performance which accompanies this commentary.

. a long runway of growth for the company. Novo’s market share of insulin is about 40% but its shares are higher, in

the 50% †60% range, in nextâ€generation diabetes products. This market positon reflects the company’s

commitment to science and innovation over the decades, as well as a $2 billion annual investment in research and

development that fuels a healthy product pipeline. The margin of safety around the business is partly the

recurring, usually at least daily, use of insulin to control diabetes and partly the company’s commitment to science,

but also its financial strength. Over the last 5 years the business has generated $20 billion in free cash flow after

its investment in research and sales (almost all of which has been returned to shareholders). Other competitive

advantages include lowâ€cost production and a global sales footprint. In summary, Novo has many of the attributes

of a steady and sustainable growth business. In 2016, earnings per share will probably grow in the low doubleâ€

digits, roughly inâ€line with our expectation for the next several years. However, the company’s share price

suffered a correction during the 3rd Quarter. The stock has become a poster child of sorts for the opaque,

convoluted and perhaps dysfunctional way insulin prices are being set in the United States. For some patients, the

cost of insulin is soaring but rising prices seem to be benefiting pharmacy benefit managers who control

distribution, rather than manufacturers like Novo Nordisk. There is no doubt that market power has shifted in a

way that benefits intermediaries in the United States, an important market for Novo and around 50% of the

group’s sales. Following a recent research visit to the company’s headquarters in Copenhagen, and given a

potentially more attractive level at which to add to the holding, we are reâ€evaluating the investment case.

Changes to the Portfolio:

The investment in ARM Holdings plc was sold during the quarter. ARM is one of the world’s leading technology

enterprises based outside the United States and is a great example of our ability to find the highestâ€quality

business regardless of their domicile. The company’s engineers design processor chips used in mobile phones and

a range of other connected devices. Over the years, it has specialized in processors designed to extract more

computing power and performance from limited battery life. Through continuous improvements in design an ARM

smartphone, for example, provides more computing power than the supercomputers of the early 1990s even

though battery life, unfortunately, has barely changed. As rival Intel has struggled to make any inroads in smart

devices, ARM’s designs have become industry standard and are now used in more than 90% of all mobile phones.

Putting this another way, almost 5 billion people – most of world’s population, in fact – rely on an ARMâ€powered

mobile phone every day and throughout the day. ARM is probably the most pervasive technology company almost

no one has heard of. But besides mobile phones, ARM’s designs are used in a range of other consumer electronics

products. This year, the company will earn an average royalty of a few cents (5.5 cents, to be precise) on more

than 16 billion devices that will be shipped to customers. Looking ahead to the next 5â€10 years, ARM is in a strong

positon to maintain its leadership in mobile computing and extend its technology into less mature markets

including networking equipment, server computers, and connected devices that will become the internet of things.

We have been looking forward to doubleâ€digit unit growth, mostly recurring royalty revenues at very high margins

and strong generation of free cash flow over time, although with some cyclicality along the way. However, we

have parted company with ARM sooner than expected, following an offer made for the company by SoftBank

Group Corp. in July. SoftBank’s cash offer of GBP 17 per share represented a premium of 71% to the yearâ€toâ€date

average price. It also implied a multiple of 50 times adjusted earnings per share for 2016, based on our estimates.

This compares to the price to the earnings multiple of 25 that we have been using to estimate an expected return

for the investment. In effect, the offer compressed the returns we expected from compounding over the next four

to five years into 2016. Further, the offer was recommended by ARM’s board of directors. Given the adequate

premium and the very low probability of any higher offer in my view the position was sold from the Portfolio.

An investment in Align Technology Inc. was added to the Portfolio during the quarter. Align is a midâ€sized medical

devices company that manufactures small, clear, customized plastic braces used by orthodontists and dentists to

straighten teeth. It is also a global market leader that is leading and driving the development of a product category

as clear plastic braces become a better alternative to traditional metal wire orthodontics for many patients. This

Please reference the supplemental information to the composite performance which accompanies this commentary.

. category seems particularly attractive because straight (and white) teeth have become increasingly important or

even needsâ€based to both adults and teenagers. Demand is still discretionary, but braces are increasingly seen as a

kind of investment in personal and professional success, as well as selfâ€image. Most sales come from the Invisalign

brand which is well established and often requested by name. Although Invisalign dominates the space with more

than 90% share of clear braces and more than 4 million cases to date, the company is still in the early stages of

realizing its growth opportunity, with no more than 10% share of its addressable market. We believe the

competitive moat around the business is very strong for a company of this size. Aside from the brand that

resonates with consumers, Align has forged strong relationships with the approximately 50,000 orthodontist and

dental practices it serves. Wouldâ€be competitors have been slow to enter the space but, even if they can work

around the patents protecting designs unique to Invisalign designs, they may struggle to match Align’s material

science, the science that allows a lightweight and removable piece of plastic to safely and effectively move bones

in the jaw. The knowâ€how required to manufacture customized braces at scale and the digital asset – the

accumulation of knowledge and experience over more than 15 years used to design molds before braces are

printed †are additional, formidable competitive barriers. The investment has been added to the Portfolio with a

view to adding to the holding over time.

Outlook:

The Portfolio continues to hold relatively few highâ€quality growth businesses with each holding being selected for

its ability to sustain earnings growth. Portfolio turnover has remained low this year and less than 10% annualized

since inception. The Portfolio will continue to hold many of the same businesses it has since inception, although

turnover is likely to pick up a little from here to a more normal range of 10% †20% as I review a small number of

investment candidates to further reduce cash. Looking into the remainder of 2016 and beyond, I anticipate doubleâ€

digit compound earnings growth will be the main driver of investment returns.

Thank you for your investment in the Polen Global Growth Portfolio.

Sincerely,

Julian Pick, CFA

The commentary is not intended as a guarantee of profitable outcomes. Any forwardâ€looking statements are based on certain

expectations and assumptions that are susceptible to changes in circumstances.

Please reference the supplemental information to the composite performance which accompanies this commentary.

. Historical Performance

Polen Global Growth Performance †September 30, 2016

Polen (Gross)

Polen (Net)

MSCI ACWI

3Q16

6.48%

6.26%

5.30%

YTD

4.93%

4.25%

6.60%

1 Year

13.61%

12.65%

11.96%

Since Inception (1/1/15)

8.58%

7.66%

2.31%

*Returns are trailing through 09/30/16. Annualized returns are presented for periods greater than 1 year.

Please reference the supplemental information to the composite performance which accompanies this commentary.

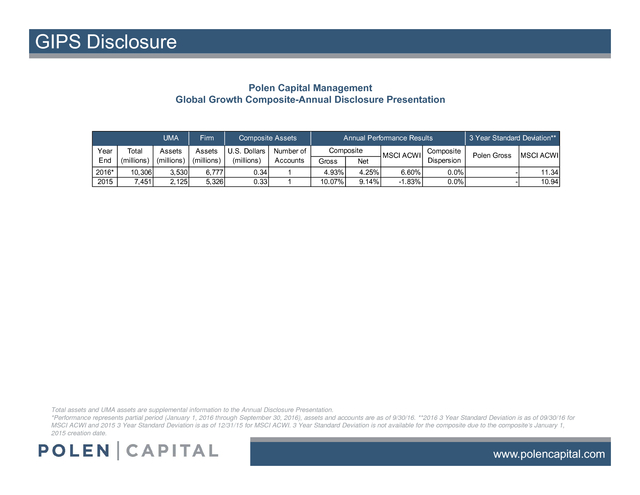

. GIPS Disclosure

Polen Capital Management

Global Growth Composite-Annual Disclosure Presentation

UMA

Year

End

2016*

2015

Total

(millions)

10,306

7,451

Assets

(millions)

3,530

2,125

Firm

Composite Assets

Assets U.S. Dollars

(millions)

(millions)

6,777

5,326

0.34

0.33

Number of

Accounts

1

1

Annual Performance Results

Composite

Gross

Net

4.93%

10.07%

4.25%

9.14%

MSCI ACWI

6.60%

-1.83%

3 Year Standard Deviation**

Composite

Dispersion

0.0%

0.0%

Polen Gross

MSCI ACWI

-

11.34

10.94

Total assets and UMA assets are supplemental information to the Annual Disclosure Presentation.

*Performance represents partial period (January 1, 2016 through September 30, 2016), assets and accounts are as of 9/30/16. **2016 3 Year Standard Deviation is as of 09/30/16 for

MSCI ACWI and 2015 3 Year Standard Deviation is as of 12/31/15 for MSCI ACWI. 3 Year Standard Deviation is not available for the composite due to the composite’s January 1,

2015 creation date.

www.polencapital.com

.

GIPS Disclosure The Global Growth Composite created on January 1, 2015 contains fully discretionary global growth accounts that are not managed within a wrap fee structure and for comparison purposes is measured against MSCI ACWI. Prior to October 18, 2016, the benchmark for the Global Growth Composite was the MSCI ACWI variant with gross dividends. As of October 18, 2016, the benchmark was changed to the MSCI ACWI variant with net dividends, to more accurately reflect the Global Growth Composite’s strategy. Polen Capital invests exclusively in a portfolio of high quality liquid companies. Polen Capital Management claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards.

Polen Capital Management has been independently verified by Ashland Partners & Company LLP for the periods April 1, 1992 through December 31, 2015. The verification is available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation. Polen Capital Management is an independent registered investment adviser.

The firm maintains a complete list and description of composites, which is available upon request. In July 2007, the firm was reorganized from an S-corporation into an LLC and changed names from Polen Capital Management, Inc. to Polen Capital Management, LLC. Results are based on fully discretionary accounts under management, including those accounts no longer with the firm.

Past performance is not indicative of future results. The U.S. Dollar is the currency used to express performance. Returns are presented gross and net of management fees and include the reinvestment of all income.

Net of fee performance was calculated using actual management fees. The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. The management fee schedule is as follows: Institutional: Per annum fees for managing accounts are 85 basis points (0.85%) on the first $50 Million and 65 basis points (0.65%) on all assets above $50 Million of assets under management.

HNW: Per annum fees for managing accounts are 150 basis points (1.5%) of the first $500,000 of assets under management and 100 basis points (1.0%) of amounts above $500,000 of assets under management. Actual investment advisory fees incurred by clients may vary. Past performance does not guarantee future results and future accuracy and profitable results cannot be guaranteed. Performance figures are presented gross and net of management fees and have been calculated after the deduction of all transaction costs and commissions.

Polen Capital is a SEC registered investment advisor and its investment advisory fees are described in its Form ADV Part 2A. The advisory fees will reduce client’s returns. The chart below depicts the effect of a 1% management fee on the growth of one dollar over a 10 year period at 10% (9% after fees) and 20% (19% after fees) assumed rates of return. The MSCI ACWI Index is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world.

The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets. The information provided in this document should not be construed as a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain the composite or that the securities sold will not be repurchased. The securities discussed do not represent the composite’s entire portfolio.

Actual holdings will vary depending on the size of the account, cash flows, and restrictions. It should not be assumed that any of the securities transactions or holdings discussed will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. A complete list of our past specific recommendations for the last year is available upon request. Return 1 Year 2 Years 3 Years 4 Years 5 Years 6 Years 7 Years 8 Years 9 Years 10 Years 10% 1.1 1.21 1.33 1.46 1.61 1.71 1.95 2.14 2.36 2.59 9% 1.09 1.19 1.3 1.41 1.54 1.68 1.83 1.99 2.17 2.39 20% 1.2 1.44 1.73 2.07 2.49 2.99 3.58 4.3 5.16 6.19 19% 1.19 1.42 1.69 2.01 2.39 2.84 3.38 4.02 4.79 5.69 www.polencapital.com .

GIPS Disclosure The Global Growth Composite created on January 1, 2015 contains fully discretionary global growth accounts that are not managed within a wrap fee structure and for comparison purposes is measured against MSCI ACWI. Prior to October 18, 2016, the benchmark for the Global Growth Composite was the MSCI ACWI variant with gross dividends. As of October 18, 2016, the benchmark was changed to the MSCI ACWI variant with net dividends, to more accurately reflect the Global Growth Composite’s strategy. Polen Capital invests exclusively in a portfolio of high quality liquid companies. Polen Capital Management claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards.

Polen Capital Management has been independently verified by Ashland Partners & Company LLP for the periods April 1, 1992 through December 31, 2015. The verification is available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation. Polen Capital Management is an independent registered investment adviser.

The firm maintains a complete list and description of composites, which is available upon request. In July 2007, the firm was reorganized from an S-corporation into an LLC and changed names from Polen Capital Management, Inc. to Polen Capital Management, LLC. Results are based on fully discretionary accounts under management, including those accounts no longer with the firm.

Past performance is not indicative of future results. The U.S. Dollar is the currency used to express performance. Returns are presented gross and net of management fees and include the reinvestment of all income.

Net of fee performance was calculated using actual management fees. The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. The management fee schedule is as follows: Institutional: Per annum fees for managing accounts are 85 basis points (0.85%) on the first $50 Million and 65 basis points (0.65%) on all assets above $50 Million of assets under management.

HNW: Per annum fees for managing accounts are 150 basis points (1.5%) of the first $500,000 of assets under management and 100 basis points (1.0%) of amounts above $500,000 of assets under management. Actual investment advisory fees incurred by clients may vary. Past performance does not guarantee future results and future accuracy and profitable results cannot be guaranteed. Performance figures are presented gross and net of management fees and have been calculated after the deduction of all transaction costs and commissions.

Polen Capital is a SEC registered investment advisor and its investment advisory fees are described in its Form ADV Part 2A. The advisory fees will reduce client’s returns. The chart below depicts the effect of a 1% management fee on the growth of one dollar over a 10 year period at 10% (9% after fees) and 20% (19% after fees) assumed rates of return. The MSCI ACWI Index is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world.

The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets. The information provided in this document should not be construed as a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain the composite or that the securities sold will not be repurchased. The securities discussed do not represent the composite’s entire portfolio.

Actual holdings will vary depending on the size of the account, cash flows, and restrictions. It should not be assumed that any of the securities transactions or holdings discussed will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. A complete list of our past specific recommendations for the last year is available upon request. Return 1 Year 2 Years 3 Years 4 Years 5 Years 6 Years 7 Years 8 Years 9 Years 10 Years 10% 1.1 1.21 1.33 1.46 1.61 1.71 1.95 2.14 2.36 2.59 9% 1.09 1.19 1.3 1.41 1.54 1.68 1.83 1.99 2.17 2.39 20% 1.2 1.44 1.73 2.07 2.49 2.99 3.58 4.3 5.16 6.19 19% 1.19 1.42 1.69 2.01 2.39 2.84 3.38 4.02 4.79 5.69 www.polencapital.com .