Description

{reflections}

2016 the road ahead

Insights to build a bridge

from the realities of 2015 to

the expectations for 2016

and establish a framework

for portfolio positioning.

.

. reflections

Top Six Investment Themes for 2016

1

2

3

Diversification is key – selecting the

right mix of assets for a portfolio is

more important than the individual

investments themselves. Critical

steps for any successful investment

strategy are establishing and adhering

to a broadly diversified strategic asset

allocation framework that appropriately

reflects one’s desired return, risk

tolerance, and investment time horizon.

Higher rates may be inevitable, but

it can be a positive development

for both stocks and bonds. Both the

Fed and the markets are projecting

a gradual pace for rate hikes in the

coming years. A slower, gradual

tightening cycle has historically been

supportive of equities.

Meanwhile, higher yields translate into higher interest income on bonds, which will boost returns over time and can help buffer against lower bond prices. Despite a low-yield environment, fixed income continues to play a critical role in a well-diversified portfolio. Investors can take solace in the fact that the primary benefits of their fixed-income portfolio – protection and diversification – remain intact. Bonds remain an effective diversifier to stocks and other risk assets, providing a source of volatility reduction and stability to an investment portfolio. Moreover, municipal bonds look attractive for many investors – not only those in the highest tax brackets. 4 5 6 The backdrop for equities is positive, particularly relative to cash or high-quality bonds. While we anticipate that volatility may be more prevalent in the next few years when compared to the last few, recent economic data out of the U.S. remain supportive of equities while market valuations based on forward earnings appear reasonable. The case for international equities remains strong for investors with a long-term time horizon.

The combination of attractive valuations, a supportive global economic backdrop, and the ongoing and aggressive monetary stimulus efforts from central banks around the globe paint a compelling picture for international equities and a longerterm investment opportunity for patient investors. Keep emotions at bay by maintaining a long-term focus and sticking to a plan. History has taught us that there will always be more questions than answers about the future. Instead of speculating about the unknown, investors with a wellconceived plan, discipline, and the patience to navigate through both calm and rough waters should be able to achieve their goals. 1 .

2 2016 the road ahead Focusing on Tomorrow A STRATEGIC MINDSET Return “A rising tide lifts all boats” has been a common idiom associated with the capital markets in recent years. Since the lows of the Great Recession in 2009, the economy and the capital markets have been on a fairly steady Bull And Bear Markets upward trajectory. The combination of an exceptionally accommodative 550% Fed, moderate economic growth, and muted inflation has been a broadly 450% positive formula for stocks and other 350% risk assets. In fact, the current rally 250% has been remarkable for a number of reasons: (1) its length – now the third 150% longest bull-market rally in stocks 50% since 1929, (2) its magnitude – as of -50% the time of this writing, the S&P 500 1 6 1 1 1 1 1 1 6 6 6 6 6 6 94 195 195 196 196 197 197 198 198 199 199 200 200 201 1 Index has gained over 200% since its March 2009 bottom, and (3) its Bear Market Bull Market Recession Periods subdued volatility – registering very A bear market is deï¬ned as a peak-to-trough decline in the S&P 500 Index (price only) of 20% or more.

The bull run data reflect the market expansion few corrections along that path. from the bear market low to the subsequent market peak. Source: PMFA, Morningstar, Inc., National Bureau of Economic Research (NBER) . reflections The question, of course, is what is the likely path from here? We believe that even the best prognosticators cannot accurately predict the future. While the 17% per year pace that equities have returned in the last six calendar years is not likely to be repeated over the next 10 years, equities are still likely to deliver respectable gains that should exceed the returns provided by cash and high-quality bonds, particularly given the low interestrate environment that persists today. Today, overall economic and market fundamentals continue to be supportive of equities. Ultimately, the primary driver of long-term stock market returns is earnings growth, which tends to correlate highly with nominal economic growth (real GDP growth plus inflation). This helps to explain why the majority of bear markets are caused, at least in part, by a recession.

While there has been some increasing angst of late about the slowing global economy, most expect that the U.S. economy will continue to grow over the next few years and that an imminent recession in the U.S. is unlikely.

In fact, recent economic data out of the U.S. have painted a positive backdrop for equities. GDP growth has been fairly steady, inflation remains under control, the labor market continues to strengthen, and consumer confidence remains elevated. While we anticipate that volatility may be more prevalent in the next few years when compared to the last few, we believe that the multi-year outlook for domestic equities remains positive. Looking beyond our borders, we also believe that the case for international equities remains strong for investors with a long-term time horizon. During the past year, we modestly increased allocations to international equities, as valuations looked attractive relative to domestic equities.

Aggressive monetary stimulus across Europe and Asia should also be broadly supportive of the economy and, in turn, equities in those regions. On the opposite end of the risk spectrum, the fixed income market continues to pose challenges amid today’s lowyield environment. Although investors received some clarity before the year-end regarding domestic monetary policy, a degree of uncertainty still persists about the timing and magnitude of future rate hikes. Coming out of the December Federal Open Market Committee meeting, policymakers increased the fed funds rate by 0.25%, marking the start of the central bank’s first tightening cycle in a decade. In the long run, higher interest rates would be a positive for bond investors. Higher yields translate into greater interest income over time, which can help buffer the effect of falling prices.

Despite the low interest rate environment, bonds still play a critical role in a well-diversified portfolio for many investors who desire a degree of capital preservation, income generation, and portfolio stability that stocks alone cannot provide. 3 . 4 2016 the road ahead Moving beyond traditional conditions to identify stocks and bonds, meaningful opportunities alternative investments also where the risk/return serve an important role in trade-off presents a portfolios. Alternatives that compelling opportunity. may have low correlations We believe that a Gaining a to stocks and bonds successful investment complete can improve portfolio strategy requires a understanding diversification and thus framework that aligns reduce portfolio volatility with one’s stated of the unique over time. Certainly, tolerance for risk and attributes of alternative investments return expectations. Our any alternative can take on many different primary focus is to ensure attributes and may enhance that client portfolios are investment is risk-adjusted returns positioned in a diversified critical prior to over a full market cycle; manner that appropriately implementation. however, they may not be reflects their desired appropriate for all investors. return, risk tolerance, and Gaining a complete investment time horizon. understanding of the unique attributes of We take a long-term view surrounding any alternative investment is critical prior portfolio positioning and will be diligent to implementation. in making adjustments at the margin when appropriate. We are constantly evaluating capital market valuations and economic .

reflections Fixed Income STILL THE SAFETY NET Fixed income investors began the year by circling dates on the calendar in anticipation of the much-awaited Federal Reserve hike of the fed funds rate. After all, the economy was growing at a moderate pace and the jobs picture was improving steadily. Despite the fact that inflation was still below its 2% target, the Fed seemed prepared to pull the trigger. The combination of slower growth in China, uncertainty in energy markets, and a decline in confidence in the global economy prompted the Fed to delay plans for beginning the process of monetary policy normalization. However, that changed in December as policymakers moved forward with a widely expected rate increase before year end.

While the December liftoff eliminated one source of uncertainty heading into 2016, questions remain around the magnitude and timing of future hikes. In its statement, the Fed indicated that it expects that conditions will require only “gradual increases” in the fed funds rate. Nonetheless, its updated 5 .

6 2016 the road ahead projections for 2016 continue to signal four quarter-point hikes, which is in line with previous projections. Contrary to the Fed’s projections, fed funds futures indicate that investors expect a more prolonged process toward normalization of the fed funds rate than the path projected by the Fed. Put simply, the markets do not The Fed Has Lowered Expectations, But The Market Remains Skeptical 7.0 Fed Funds Rate (%) 6.0 5.0 4.0 3.0 2.0 1.0 0.0 9 199 03 01 20 20 Fed Funds Rate 07 05 20 20 09 20 Fed Median Expectations (Dec. 2015) 11 20 13 20 15 17 20 20 Market Expectations (Dec. 1, 2015) Source: PMFA, CME Group, Federal Reserve Short-term Rates React More Sharply to Changes in Fed Policy 10.0 Yield (%) 8.0 6.0 4.0 2.0 0.0 0 199 5 199 00 20 05 20 Effective Fed Funds Rate Source: PMFA, Federal Reserve 10 20 2 Year 15 20 10 Year think that the Fed will be able to raise rates as quickly as the Fed projects. This creates an unwanted scenario for Fed policymakers: their goal of increased transparency has been hindered by their ongoing decisions to push back rate hikes, which has in turn harmed their credibility with at least some increasingly skeptical investors. Nonetheless, the markets will continue to closely watch the Fed for any hints about its next moves. Beyond the evolution of Fed policy, among the more significant developments of the past year was the increased value proposition presented by municipal bonds.

While Treasury rates fell, municipal yields were comparatively firm. Historically, municipal bonds have been an attractive alternative for investors in the highest tax brackets. Today, taxexempt bonds look relatively attractive even for lower bracket taxpayers who cannot otherwise shield the income generated by their bond portfolio in a tax-deferred account. As we look ahead, bond investors can take solace in the fact that the primary benefits of their fixed-income portfolio remain intact.

Bonds are still an effective diversifier to stocks and other risk assets, providing a source of risk reduction and relative stability. Although fluctuations in interest rates can be a source of volatility within fixed income portfolios, higher rates would . reflections ultimately be a positive development, lifting returns for long-term investors. We strive to make portfolio adjustments and identify active bond managers who can add value over the long term. As we entered 2015, our thesis for fixed income was to reduce, but not eliminate, the risk of rising rates, maintain a yield advantage over the benchmark by owning non-U.S. Treasury securities, and have a portion of the portfolio that is opportunistic to take advantage of periods of expected volatility. The key tenets of that thesis remain largely unchanged today. Bottom line: While the Fed has finally embarked on its path toward normalization of monetary policy, the move was expected and may not result in a material increase in rates at the long end of the yield curve.

Recognizing that, we have made some manager changes during the course of the last year to slightly increase the duration (interest rate sensitivity) of our portfolios, though ...higher rates not significantly so. We would ultimately continue to take a longterm view and will adjust be a positive portfolios on the margin to development, support our objectives for lifting returns fixed income portfolios – the ultimate goal of which for long-term is to deliver protection and investors. diversification, particularly in periods when riskier assets suffer losses. 7 . 8 2016 the road ahead Equities VOLATILITY RESURFACES Equity markets took investors for a wild ride in 2015, as volatility returned around mid-year and equities sold off across the globe. Several years have passed since an equity pullback of any real magnitude, but pullbacks and even corrections of 10% or more are actually quite common. While they may cause anxiety, market corrections are part of a normal market cycle, and more often than not do not signal the end of a bull market. Broad equity market forward valuations appear fairly valued, particularly given the low-interest rate environment. Of course, some sectors and companies are better positioned than others at any given point in time, and conditions today are no exception.

The sharp decline in commodity prices, for example, has weighed heavily on the recent profitability of the energy and material sectors. Nonetheless, as we look toward 2016 and beyond, periods of volatility should likely be viewed as potential buying opportunities. Broadly speaking, U.S. corporations still enjoy a strong financial footing.

Profit margins are strong, corporate cash positions are near a 25-year high, and debt-to-equity ratios are near 25-year lows. With higher short-term interest rates now at the doorstep, investors may be questioning what Fed tightening will mean for equities and their portfolio returns. In previous cycles, rate hikes have typically . 9 reflections Balance Sheet Expansion caused some short-term provide some reassurance pain, but stocks have that the economy is strong almost always been higher enough to grow without within a year after the start needing the same degree of of the tightening cycle. In support. Again, that would While they the current environment, be a positive for stocks. may cause it’s possible that a rate Looking beyond the U.S., anxiety, market increase is so widely monetary policy around expected that even the corrections are the globe remains highly short-term market reaction part of a normal accommodative, as Japan’s may not be meaningful. quantitative easing (QE) market cycle, In fact, stocks rallied in program is in full effect and and more often response to the recent the push for structural reform release of the minutes than not don’t continues. The European from the October Fed signal the end of Central Bank (ECB) also meeting, which hinted appears to be having some a bull market. strongly that the central success with its QE program bank was leaning toward to combat slow growth and a December rate increase. potential deflation in the Eurozone.

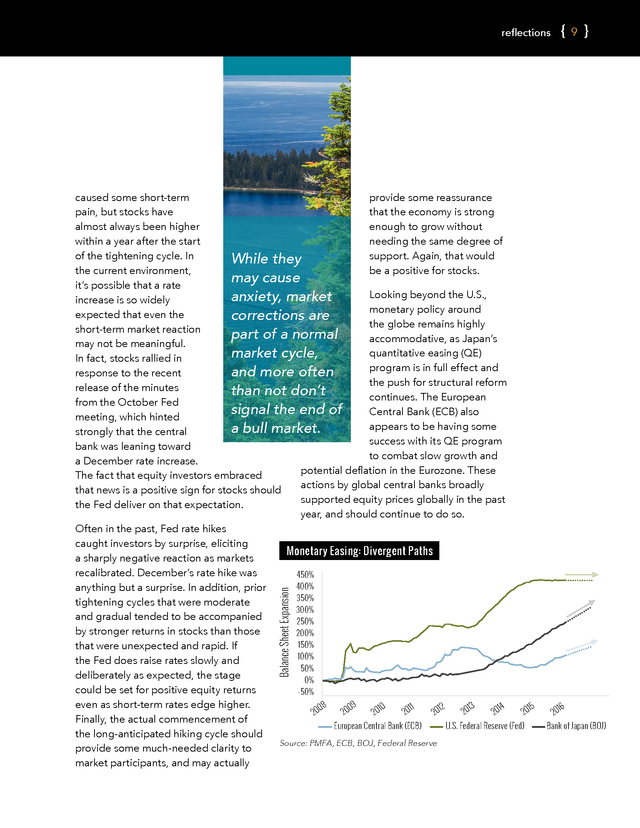

These The fact that equity investors embraced actions by global central banks broadly that news is a positive sign for stocks should supported equity prices globally in the past the Fed deliver on that expectation. year, and should continue to do so. Often in the past, Fed rate hikes caught investors by surprise, eliciting Monetary Easing: Divergent Paths a sharply negative reaction as markets recalibrated. December’s rate hike was 450% 400% anything but a surprise. In addition, prior 350% tightening cycles that were moderate 300% and gradual tended to be accompanied 250% by stronger returns in stocks than those 200% 150% that were unexpected and rapid.

If 100% the Fed does raise rates slowly and 50% deliberately as expected, the stage 0% could be set for positive equity returns -50% even as short-term rates edge higher. 13 09 11 15 14 08 10 12 20 20 20 20 20 20 20 20 Finally, the actual commencement of European Central Bank (ECB) U.S. Federal Reserve (Fed) the long-anticipated hiking cycle should Source: PMFA, ECB, BOJ, Federal Reserve provide some much-needed clarity to market participants, and may actually 16 20 Bank of Japan (BOJ) . 10 2016 the road ahead U.S. EQUITIES: A POSITIVE BACKDROP slightly above their long-term averages, which isn’t unreasonable given the low interest rate environment. The volatility in the U.S. stock market tested investor mettle at times this year. A strong October rally lifted returns back into positive territory through the end of November, but as we write this, there is no way to know whether 2015 will ultimately be another positive year for U.S. equity markets.

As the bull market ages into its seventh year, investors naturally question how long it will last. As already noted, market valuations based on forward earnings are not overstretched. In fact, market volatility during 2015 brought valuations back into a more fairly valued zone and reduced some of the froth that had built up in some of the more speculative areas of the market.

Although some parts of the market still look pricier than others (with small caps being a notable example), valuations today are U.S. Large Caps Remain Inexpensive Relative to Small Caps 1.4 S&P 500 Expensive vs. S&P 600 Relative P/E Ratio 1.2 1.0 0.8 0.6 0.4 S&P 600 Expensive vs.

S&P 500 0.2 19 95 19 96 19 97 98 19 Relative P/E Ratio 9 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 199 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 Average Relative P/E Ratio Source: PMFA, Standard & Poor’s –1 SD +1 SD –2 SD +2 SD The economy continued to expand at a moderate pace in 2015, but it proved to be a challenging year for corporate earnings, as a confluence of factors caused earnings growth to stall. Extreme weakness in the energy and materials sectors were detractors, as both struggled in the midst of a sharp, dramatic drop in commodity prices that began in mid-2014. The recent strength of the U.S.

dollar also presented a strong headwind for U.S. multinationals that derive much of their revenue and earnings abroad. Despite these challenges, many companies continued to post record earnings, and analysts are optimistic, calling for a rebound in earnings growth in the coming year. Domestically, we continue to favor large caps over their small and mid-cap counterparts given their attractive relative valuations.

History also suggests that large caps tend to outperform in the latter stages of a bull market, as small caps are more susceptible to broad sell-offs and “risk-off” periods. While small cap earnings growth has historically been relatively higher, smaller companies are also likely to be negatively impacted by rising wages, input costs, and interest rates to a greater degree than larger companies. Large caps are a bit more defensive in nature as well and should hold up better in the face of slower growth, rising interest rates, or higher inflation. . reflections INTERNATIONAL EQUITIES: AN ATTRACTIVE OPPORTUNITY SET compounded losses for U.S.-based investors. While risks certainly remain, we believe a dedicated allocation to emerging As we shift toward a more markets is still prudent global focus, we believe the within the context of a backdrop for international diversified long-term equities remains compelling. portfolio. Valuations have Relative to U.S. equities, become more attractive, international equities We believe the providing greater upside continue to trade at more potential for EM equities backdrop for attractive valuations.

Within moving forward. Perhaps international Japan and Europe, earnings more importantly from a equities remains and profit margins still have long-term perspective, meaningful room to rebound most emerging economies compelling. further toward their peaks continue to grow at a prior to the global financial rate higher than much crisis. These regions also stand to benefit of the developed world, and most longfrom a QE-induced devaluation of their term capital market forecasts call for EM currencies and lower oil prices, which equities to outperform nearly every other may help stimulate export activity and asset class over a 5- to 10-year timeframe. consumer spending.

In Japan, despite Bottom line: We believe the long-term limited economic growth, long-needed outlook for stocks is attractive, particularly corporate reforms appear to be having relative to cash and high-quality bonds. a positive effect, and signs of wage We also remain vigilant in evaluating growth have begun to emerge. In Europe, cyclical risks and opportunities. For most economic activity has shown recent long-term investors with a sufficient signs of reacceleration, as consumer tolerance for risk and a need to grow their confidence, domestic demand, and credit capital, an allocation to equities should growth have all been improving. continue to be a foundational element Within international equity allocations, of their portfolios to build wealth and we continue to hold a neutral weighting increase purchasing power over time. between developed and emerging markets (EM).

EM equities struggled significantly throughout 2015, as the global flight to quality contributed to significant currency depreciation that 11 . 12 2016 the road ahead Alternatives EXPANDING BEYOND THE TRADITIONAL Cyclicality is a part of nature, as evidenced in something as simple as waves, which represent the transfer of energy through Alternatives Have Outperformed Traditional Stocks Or Bonds Two-thirds Of The Time water. As this energy transfer occurs, a wave rises to a crest at its strongest point, and then collapses to a trough as the energy transfer fades. This science behind waves has a connection to investing, whereby the performance of various investment strategies tends to exhibit periods of strength, but then fades as the environment becomes less conducive. 40% 30% Return 20% 10% 0% -10% -20% -30% -40% -50% 8 199 9 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 199 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 S&P 500 Index Barclays U.S. Aggregate Index HFRX Global Hedge Fund Index Source: PMFA As an example, over the past few years, shorting stocks has been a drag on the performance for some hedge fund strategies.

The strong recovery in the broad market has helped most stocks to perform positively during this bull market run, including those of companies with poor fundamentals. This is analogous to the “rising tide” environment, in which all boats are lifted as we discussed at the . reflections opening of this piece. The challenge for broad, alternatives can enhance portfolio active managers (including long/short returns, reduce portfolio risk, or both over specialists) is that differentiating between the course of a market cycle. relative winners and losers As with any investment, has been difficult, because there are pros and cons both are riding the same to alternatives that are wave. Over the past few essential for the investor quarters, however, stocks As with any to understand. Whether have begun to show bouts investment, there it be the risks, costs, of increased dispersion, tax consequences, or with greater disparity in are pros and cons liquidity limitations, many returns between winners to alternatives alternatives are extremely and losers.

This has created that are essential complex, and may not be greater opportunities for suitable for all investors. active managers broadly, for the investor and long/short managers in Bottom line: We believe to understand. particular. that alternative investments The case for owning alternatives in a portfolio is to provide exposure to investment structures or strategies that may react differently than traditional stocks and bonds during different points in the market cycle. They may have return drivers or tap into an opportunity set that stocks and bonds do not. In other cases, their returns may be largely based on manager skill.

Those characteristics can provide a portfolio with an expanded tool set to navigate choppy waters over the long run. While the range of strategies is very should be part of a wellstructured portfolio, but the characteristics of each investment must be considered on its own merits. “Alternatives” are not an “asset class” like large cap stocks.

Rather, each alternative investment and manager must be evaluated individually in relation to how it will help a portfolio. We believe there are many opportunities within the alternative investment space, but their use and suitability will vary depending on each investor’s circumstances, needs, and goals. 13 . 14 2016 the road ahead Conclusion BRIDGING THE GAP In the preceding pages, we have set the stage for our forward-looking expectations. Economic fundamentals in the U.S. are positive, despite the slowdown in global growth in the latter half of the year. Meanwhile, most major central banks remain highly accommodative, injecting unprecedented liquidity in an effort to stimulate growth and reflate their respective economies.

Corporate fundamentals are generally attractive, while broad market valuations are reasonable, particularly in the current low-rate environment. While bond yields (particularly short-term yields) remain near historical lows and are now at the point of turning higher, we expect that the path to a more normalized rate environment is likely to be a gradual one. Moreover, while rates rising can be a catalyst for volatility, bond investors would benefit from higher yields in the long run.

We also believe that equity returns could still be positive even against a backdrop of Fed tightening and an extended period of rising rates. There have always been unknowns that must be faced by investors; that is the nature of risk. When conditions appear tranquil, risk is still there, and investors should temper their optimism. When uncertainty creates anxiety, opportunity is still present, and investors who recognize that opportunity will typically be compensated over time for investing because of these risks. .

reflections As we bring this year’s edition of the assessment. There are plenty of reasons Road Ahead to a close, we’re reminded to be optimistic. Perhaps a “bridge of the 1970 song Bridge over uneven water” would over Troubled Water by be a more appropriate American music legends description today, but it Simon & Garfunkel. The seems unlikely that title song was the recipient of would have had that same multiple Grammy awards, artistic appeal.

We will and it can serve as a fitting make due for the purpose analogy for investors. The of our analogy. Just as water is day-to-day flow of news always in a state What tomorrow will bring can, at times, influence for the economy or capital of flux, so is the the near-term direction markets remains to be seen. of the capital markets. dynamic world The sources of uncertainty It can be tempting in which we live. that exist today are unlikely to make investment to dissipate in the near changes in anticipation term. Just as water is always of or in response to in a state of flux, so is the such news.

However, we dynamic world in which believe that investors we live. There will always who have established a be more questions than disciplined investment answers about the future. policy, consistent with Instead of speculating their tolerance for risk, about the unknown, can rise above the rough we believe it is critical waters and maintain focus that investors develop a on the path to achieving well-conceived plan and their long-term goals maintain the discipline and and objectives. A wellpatience needed to stick to formulated plan acts as that plan.

Doing so will not that bridge. allow you to avoid the rough Admittedly, the waters, but it will allow you comparison of current to maintain your bearings conditions with troubled and keep your eyes on the water might seem too horizon on the metaphorical negative given the road ahead. overall outlook today. We would agree with that 15 . 16 2016 the road ahead Contributing authors Jim Baird, CPA, CFP®, CIMA® Chief Investment Officer Eric Dahlberg Senior Equity Analyst Erin Goss, CFA, CAIASM, CIMA®, CFS® Senior Alternative Investment Analyst Jeremy Kedzior Analyst Tricia Newcomb, CIMA® Senior Strategy Analyst Paul Olmsted Senior Fixed Income Analyst Max Wellinger Analyst Visit us at: wealth.plantemoran.com Investment Management Consultants Association (IMCA®) is the owner of the certification marks “CIMA®,” and “Certified Investment Management Analyst ®.” Use of CIMA® or Certified Investment Management Analyst ® signifies that the user has successfully completed IMCA’s initial and ongoing credentialing requirements for investment management consultants. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The CAIA Association® may grant the right to use the CAIASM Marks to those individuals who have been granted the status of either “Full Member” or “Retired Member” by the CAIA Association®.

The Institute of Business and Finance owns the certification marks CFS® and Certified Fund Specialist ®, which it awards to individuals who successfully complete its initial and ongoing certification requirements. Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain. Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness.

Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation. Investment recommendations provided herein are subject to change at any time.

Those recommendations provided herein are provided for informational purposes only and are not provided as a recommendation to buy or sell any one security or allocate to any asset class. Past and current recommendations that are profitable are not indicative of future results, which may in fact result in a loss. Please contact PMFA if you are interested in receiving a list of all past specific investment recommendations for the preceding 12 months. .

reflections 17 . .

Meanwhile, higher yields translate into higher interest income on bonds, which will boost returns over time and can help buffer against lower bond prices. Despite a low-yield environment, fixed income continues to play a critical role in a well-diversified portfolio. Investors can take solace in the fact that the primary benefits of their fixed-income portfolio – protection and diversification – remain intact. Bonds remain an effective diversifier to stocks and other risk assets, providing a source of volatility reduction and stability to an investment portfolio. Moreover, municipal bonds look attractive for many investors – not only those in the highest tax brackets. 4 5 6 The backdrop for equities is positive, particularly relative to cash or high-quality bonds. While we anticipate that volatility may be more prevalent in the next few years when compared to the last few, recent economic data out of the U.S. remain supportive of equities while market valuations based on forward earnings appear reasonable. The case for international equities remains strong for investors with a long-term time horizon.

The combination of attractive valuations, a supportive global economic backdrop, and the ongoing and aggressive monetary stimulus efforts from central banks around the globe paint a compelling picture for international equities and a longerterm investment opportunity for patient investors. Keep emotions at bay by maintaining a long-term focus and sticking to a plan. History has taught us that there will always be more questions than answers about the future. Instead of speculating about the unknown, investors with a wellconceived plan, discipline, and the patience to navigate through both calm and rough waters should be able to achieve their goals. 1 .

2 2016 the road ahead Focusing on Tomorrow A STRATEGIC MINDSET Return “A rising tide lifts all boats” has been a common idiom associated with the capital markets in recent years. Since the lows of the Great Recession in 2009, the economy and the capital markets have been on a fairly steady Bull And Bear Markets upward trajectory. The combination of an exceptionally accommodative 550% Fed, moderate economic growth, and muted inflation has been a broadly 450% positive formula for stocks and other 350% risk assets. In fact, the current rally 250% has been remarkable for a number of reasons: (1) its length – now the third 150% longest bull-market rally in stocks 50% since 1929, (2) its magnitude – as of -50% the time of this writing, the S&P 500 1 6 1 1 1 1 1 1 6 6 6 6 6 6 94 195 195 196 196 197 197 198 198 199 199 200 200 201 1 Index has gained over 200% since its March 2009 bottom, and (3) its Bear Market Bull Market Recession Periods subdued volatility – registering very A bear market is deï¬ned as a peak-to-trough decline in the S&P 500 Index (price only) of 20% or more.

The bull run data reflect the market expansion few corrections along that path. from the bear market low to the subsequent market peak. Source: PMFA, Morningstar, Inc., National Bureau of Economic Research (NBER) . reflections The question, of course, is what is the likely path from here? We believe that even the best prognosticators cannot accurately predict the future. While the 17% per year pace that equities have returned in the last six calendar years is not likely to be repeated over the next 10 years, equities are still likely to deliver respectable gains that should exceed the returns provided by cash and high-quality bonds, particularly given the low interestrate environment that persists today. Today, overall economic and market fundamentals continue to be supportive of equities. Ultimately, the primary driver of long-term stock market returns is earnings growth, which tends to correlate highly with nominal economic growth (real GDP growth plus inflation). This helps to explain why the majority of bear markets are caused, at least in part, by a recession.

While there has been some increasing angst of late about the slowing global economy, most expect that the U.S. economy will continue to grow over the next few years and that an imminent recession in the U.S. is unlikely.

In fact, recent economic data out of the U.S. have painted a positive backdrop for equities. GDP growth has been fairly steady, inflation remains under control, the labor market continues to strengthen, and consumer confidence remains elevated. While we anticipate that volatility may be more prevalent in the next few years when compared to the last few, we believe that the multi-year outlook for domestic equities remains positive. Looking beyond our borders, we also believe that the case for international equities remains strong for investors with a long-term time horizon. During the past year, we modestly increased allocations to international equities, as valuations looked attractive relative to domestic equities.

Aggressive monetary stimulus across Europe and Asia should also be broadly supportive of the economy and, in turn, equities in those regions. On the opposite end of the risk spectrum, the fixed income market continues to pose challenges amid today’s lowyield environment. Although investors received some clarity before the year-end regarding domestic monetary policy, a degree of uncertainty still persists about the timing and magnitude of future rate hikes. Coming out of the December Federal Open Market Committee meeting, policymakers increased the fed funds rate by 0.25%, marking the start of the central bank’s first tightening cycle in a decade. In the long run, higher interest rates would be a positive for bond investors. Higher yields translate into greater interest income over time, which can help buffer the effect of falling prices.

Despite the low interest rate environment, bonds still play a critical role in a well-diversified portfolio for many investors who desire a degree of capital preservation, income generation, and portfolio stability that stocks alone cannot provide. 3 . 4 2016 the road ahead Moving beyond traditional conditions to identify stocks and bonds, meaningful opportunities alternative investments also where the risk/return serve an important role in trade-off presents a portfolios. Alternatives that compelling opportunity. may have low correlations We believe that a Gaining a to stocks and bonds successful investment complete can improve portfolio strategy requires a understanding diversification and thus framework that aligns reduce portfolio volatility with one’s stated of the unique over time. Certainly, tolerance for risk and attributes of alternative investments return expectations. Our any alternative can take on many different primary focus is to ensure attributes and may enhance that client portfolios are investment is risk-adjusted returns positioned in a diversified critical prior to over a full market cycle; manner that appropriately implementation. however, they may not be reflects their desired appropriate for all investors. return, risk tolerance, and Gaining a complete investment time horizon. understanding of the unique attributes of We take a long-term view surrounding any alternative investment is critical prior portfolio positioning and will be diligent to implementation. in making adjustments at the margin when appropriate. We are constantly evaluating capital market valuations and economic .

reflections Fixed Income STILL THE SAFETY NET Fixed income investors began the year by circling dates on the calendar in anticipation of the much-awaited Federal Reserve hike of the fed funds rate. After all, the economy was growing at a moderate pace and the jobs picture was improving steadily. Despite the fact that inflation was still below its 2% target, the Fed seemed prepared to pull the trigger. The combination of slower growth in China, uncertainty in energy markets, and a decline in confidence in the global economy prompted the Fed to delay plans for beginning the process of monetary policy normalization. However, that changed in December as policymakers moved forward with a widely expected rate increase before year end.

While the December liftoff eliminated one source of uncertainty heading into 2016, questions remain around the magnitude and timing of future hikes. In its statement, the Fed indicated that it expects that conditions will require only “gradual increases” in the fed funds rate. Nonetheless, its updated 5 .

6 2016 the road ahead projections for 2016 continue to signal four quarter-point hikes, which is in line with previous projections. Contrary to the Fed’s projections, fed funds futures indicate that investors expect a more prolonged process toward normalization of the fed funds rate than the path projected by the Fed. Put simply, the markets do not The Fed Has Lowered Expectations, But The Market Remains Skeptical 7.0 Fed Funds Rate (%) 6.0 5.0 4.0 3.0 2.0 1.0 0.0 9 199 03 01 20 20 Fed Funds Rate 07 05 20 20 09 20 Fed Median Expectations (Dec. 2015) 11 20 13 20 15 17 20 20 Market Expectations (Dec. 1, 2015) Source: PMFA, CME Group, Federal Reserve Short-term Rates React More Sharply to Changes in Fed Policy 10.0 Yield (%) 8.0 6.0 4.0 2.0 0.0 0 199 5 199 00 20 05 20 Effective Fed Funds Rate Source: PMFA, Federal Reserve 10 20 2 Year 15 20 10 Year think that the Fed will be able to raise rates as quickly as the Fed projects. This creates an unwanted scenario for Fed policymakers: their goal of increased transparency has been hindered by their ongoing decisions to push back rate hikes, which has in turn harmed their credibility with at least some increasingly skeptical investors. Nonetheless, the markets will continue to closely watch the Fed for any hints about its next moves. Beyond the evolution of Fed policy, among the more significant developments of the past year was the increased value proposition presented by municipal bonds.

While Treasury rates fell, municipal yields were comparatively firm. Historically, municipal bonds have been an attractive alternative for investors in the highest tax brackets. Today, taxexempt bonds look relatively attractive even for lower bracket taxpayers who cannot otherwise shield the income generated by their bond portfolio in a tax-deferred account. As we look ahead, bond investors can take solace in the fact that the primary benefits of their fixed-income portfolio remain intact.

Bonds are still an effective diversifier to stocks and other risk assets, providing a source of risk reduction and relative stability. Although fluctuations in interest rates can be a source of volatility within fixed income portfolios, higher rates would . reflections ultimately be a positive development, lifting returns for long-term investors. We strive to make portfolio adjustments and identify active bond managers who can add value over the long term. As we entered 2015, our thesis for fixed income was to reduce, but not eliminate, the risk of rising rates, maintain a yield advantage over the benchmark by owning non-U.S. Treasury securities, and have a portion of the portfolio that is opportunistic to take advantage of periods of expected volatility. The key tenets of that thesis remain largely unchanged today. Bottom line: While the Fed has finally embarked on its path toward normalization of monetary policy, the move was expected and may not result in a material increase in rates at the long end of the yield curve.

Recognizing that, we have made some manager changes during the course of the last year to slightly increase the duration (interest rate sensitivity) of our portfolios, though ...higher rates not significantly so. We would ultimately continue to take a longterm view and will adjust be a positive portfolios on the margin to development, support our objectives for lifting returns fixed income portfolios – the ultimate goal of which for long-term is to deliver protection and investors. diversification, particularly in periods when riskier assets suffer losses. 7 . 8 2016 the road ahead Equities VOLATILITY RESURFACES Equity markets took investors for a wild ride in 2015, as volatility returned around mid-year and equities sold off across the globe. Several years have passed since an equity pullback of any real magnitude, but pullbacks and even corrections of 10% or more are actually quite common. While they may cause anxiety, market corrections are part of a normal market cycle, and more often than not do not signal the end of a bull market. Broad equity market forward valuations appear fairly valued, particularly given the low-interest rate environment. Of course, some sectors and companies are better positioned than others at any given point in time, and conditions today are no exception.

The sharp decline in commodity prices, for example, has weighed heavily on the recent profitability of the energy and material sectors. Nonetheless, as we look toward 2016 and beyond, periods of volatility should likely be viewed as potential buying opportunities. Broadly speaking, U.S. corporations still enjoy a strong financial footing.

Profit margins are strong, corporate cash positions are near a 25-year high, and debt-to-equity ratios are near 25-year lows. With higher short-term interest rates now at the doorstep, investors may be questioning what Fed tightening will mean for equities and their portfolio returns. In previous cycles, rate hikes have typically . 9 reflections Balance Sheet Expansion caused some short-term provide some reassurance pain, but stocks have that the economy is strong almost always been higher enough to grow without within a year after the start needing the same degree of of the tightening cycle. In support. Again, that would While they the current environment, be a positive for stocks. may cause it’s possible that a rate Looking beyond the U.S., anxiety, market increase is so widely monetary policy around expected that even the corrections are the globe remains highly short-term market reaction part of a normal accommodative, as Japan’s may not be meaningful. quantitative easing (QE) market cycle, In fact, stocks rallied in program is in full effect and and more often response to the recent the push for structural reform release of the minutes than not don’t continues. The European from the October Fed signal the end of Central Bank (ECB) also meeting, which hinted appears to be having some a bull market. strongly that the central success with its QE program bank was leaning toward to combat slow growth and a December rate increase. potential deflation in the Eurozone.

These The fact that equity investors embraced actions by global central banks broadly that news is a positive sign for stocks should supported equity prices globally in the past the Fed deliver on that expectation. year, and should continue to do so. Often in the past, Fed rate hikes caught investors by surprise, eliciting Monetary Easing: Divergent Paths a sharply negative reaction as markets recalibrated. December’s rate hike was 450% 400% anything but a surprise. In addition, prior 350% tightening cycles that were moderate 300% and gradual tended to be accompanied 250% by stronger returns in stocks than those 200% 150% that were unexpected and rapid.

If 100% the Fed does raise rates slowly and 50% deliberately as expected, the stage 0% could be set for positive equity returns -50% even as short-term rates edge higher. 13 09 11 15 14 08 10 12 20 20 20 20 20 20 20 20 Finally, the actual commencement of European Central Bank (ECB) U.S. Federal Reserve (Fed) the long-anticipated hiking cycle should Source: PMFA, ECB, BOJ, Federal Reserve provide some much-needed clarity to market participants, and may actually 16 20 Bank of Japan (BOJ) . 10 2016 the road ahead U.S. EQUITIES: A POSITIVE BACKDROP slightly above their long-term averages, which isn’t unreasonable given the low interest rate environment. The volatility in the U.S. stock market tested investor mettle at times this year. A strong October rally lifted returns back into positive territory through the end of November, but as we write this, there is no way to know whether 2015 will ultimately be another positive year for U.S. equity markets.

As the bull market ages into its seventh year, investors naturally question how long it will last. As already noted, market valuations based on forward earnings are not overstretched. In fact, market volatility during 2015 brought valuations back into a more fairly valued zone and reduced some of the froth that had built up in some of the more speculative areas of the market.

Although some parts of the market still look pricier than others (with small caps being a notable example), valuations today are U.S. Large Caps Remain Inexpensive Relative to Small Caps 1.4 S&P 500 Expensive vs. S&P 600 Relative P/E Ratio 1.2 1.0 0.8 0.6 0.4 S&P 600 Expensive vs.

S&P 500 0.2 19 95 19 96 19 97 98 19 Relative P/E Ratio 9 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 199 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 Average Relative P/E Ratio Source: PMFA, Standard & Poor’s –1 SD +1 SD –2 SD +2 SD The economy continued to expand at a moderate pace in 2015, but it proved to be a challenging year for corporate earnings, as a confluence of factors caused earnings growth to stall. Extreme weakness in the energy and materials sectors were detractors, as both struggled in the midst of a sharp, dramatic drop in commodity prices that began in mid-2014. The recent strength of the U.S.

dollar also presented a strong headwind for U.S. multinationals that derive much of their revenue and earnings abroad. Despite these challenges, many companies continued to post record earnings, and analysts are optimistic, calling for a rebound in earnings growth in the coming year. Domestically, we continue to favor large caps over their small and mid-cap counterparts given their attractive relative valuations.

History also suggests that large caps tend to outperform in the latter stages of a bull market, as small caps are more susceptible to broad sell-offs and “risk-off” periods. While small cap earnings growth has historically been relatively higher, smaller companies are also likely to be negatively impacted by rising wages, input costs, and interest rates to a greater degree than larger companies. Large caps are a bit more defensive in nature as well and should hold up better in the face of slower growth, rising interest rates, or higher inflation. . reflections INTERNATIONAL EQUITIES: AN ATTRACTIVE OPPORTUNITY SET compounded losses for U.S.-based investors. While risks certainly remain, we believe a dedicated allocation to emerging As we shift toward a more markets is still prudent global focus, we believe the within the context of a backdrop for international diversified long-term equities remains compelling. portfolio. Valuations have Relative to U.S. equities, become more attractive, international equities We believe the providing greater upside continue to trade at more potential for EM equities backdrop for attractive valuations.

Within moving forward. Perhaps international Japan and Europe, earnings more importantly from a equities remains and profit margins still have long-term perspective, meaningful room to rebound most emerging economies compelling. further toward their peaks continue to grow at a prior to the global financial rate higher than much crisis. These regions also stand to benefit of the developed world, and most longfrom a QE-induced devaluation of their term capital market forecasts call for EM currencies and lower oil prices, which equities to outperform nearly every other may help stimulate export activity and asset class over a 5- to 10-year timeframe. consumer spending.

In Japan, despite Bottom line: We believe the long-term limited economic growth, long-needed outlook for stocks is attractive, particularly corporate reforms appear to be having relative to cash and high-quality bonds. a positive effect, and signs of wage We also remain vigilant in evaluating growth have begun to emerge. In Europe, cyclical risks and opportunities. For most economic activity has shown recent long-term investors with a sufficient signs of reacceleration, as consumer tolerance for risk and a need to grow their confidence, domestic demand, and credit capital, an allocation to equities should growth have all been improving. continue to be a foundational element Within international equity allocations, of their portfolios to build wealth and we continue to hold a neutral weighting increase purchasing power over time. between developed and emerging markets (EM).

EM equities struggled significantly throughout 2015, as the global flight to quality contributed to significant currency depreciation that 11 . 12 2016 the road ahead Alternatives EXPANDING BEYOND THE TRADITIONAL Cyclicality is a part of nature, as evidenced in something as simple as waves, which represent the transfer of energy through Alternatives Have Outperformed Traditional Stocks Or Bonds Two-thirds Of The Time water. As this energy transfer occurs, a wave rises to a crest at its strongest point, and then collapses to a trough as the energy transfer fades. This science behind waves has a connection to investing, whereby the performance of various investment strategies tends to exhibit periods of strength, but then fades as the environment becomes less conducive. 40% 30% Return 20% 10% 0% -10% -20% -30% -40% -50% 8 199 9 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 199 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 S&P 500 Index Barclays U.S. Aggregate Index HFRX Global Hedge Fund Index Source: PMFA As an example, over the past few years, shorting stocks has been a drag on the performance for some hedge fund strategies.

The strong recovery in the broad market has helped most stocks to perform positively during this bull market run, including those of companies with poor fundamentals. This is analogous to the “rising tide” environment, in which all boats are lifted as we discussed at the . reflections opening of this piece. The challenge for broad, alternatives can enhance portfolio active managers (including long/short returns, reduce portfolio risk, or both over specialists) is that differentiating between the course of a market cycle. relative winners and losers As with any investment, has been difficult, because there are pros and cons both are riding the same to alternatives that are wave. Over the past few essential for the investor quarters, however, stocks As with any to understand. Whether have begun to show bouts investment, there it be the risks, costs, of increased dispersion, tax consequences, or with greater disparity in are pros and cons liquidity limitations, many returns between winners to alternatives alternatives are extremely and losers.

This has created that are essential complex, and may not be greater opportunities for suitable for all investors. active managers broadly, for the investor and long/short managers in Bottom line: We believe to understand. particular. that alternative investments The case for owning alternatives in a portfolio is to provide exposure to investment structures or strategies that may react differently than traditional stocks and bonds during different points in the market cycle. They may have return drivers or tap into an opportunity set that stocks and bonds do not. In other cases, their returns may be largely based on manager skill.

Those characteristics can provide a portfolio with an expanded tool set to navigate choppy waters over the long run. While the range of strategies is very should be part of a wellstructured portfolio, but the characteristics of each investment must be considered on its own merits. “Alternatives” are not an “asset class” like large cap stocks.

Rather, each alternative investment and manager must be evaluated individually in relation to how it will help a portfolio. We believe there are many opportunities within the alternative investment space, but their use and suitability will vary depending on each investor’s circumstances, needs, and goals. 13 . 14 2016 the road ahead Conclusion BRIDGING THE GAP In the preceding pages, we have set the stage for our forward-looking expectations. Economic fundamentals in the U.S. are positive, despite the slowdown in global growth in the latter half of the year. Meanwhile, most major central banks remain highly accommodative, injecting unprecedented liquidity in an effort to stimulate growth and reflate their respective economies.

Corporate fundamentals are generally attractive, while broad market valuations are reasonable, particularly in the current low-rate environment. While bond yields (particularly short-term yields) remain near historical lows and are now at the point of turning higher, we expect that the path to a more normalized rate environment is likely to be a gradual one. Moreover, while rates rising can be a catalyst for volatility, bond investors would benefit from higher yields in the long run.

We also believe that equity returns could still be positive even against a backdrop of Fed tightening and an extended period of rising rates. There have always been unknowns that must be faced by investors; that is the nature of risk. When conditions appear tranquil, risk is still there, and investors should temper their optimism. When uncertainty creates anxiety, opportunity is still present, and investors who recognize that opportunity will typically be compensated over time for investing because of these risks. .

reflections As we bring this year’s edition of the assessment. There are plenty of reasons Road Ahead to a close, we’re reminded to be optimistic. Perhaps a “bridge of the 1970 song Bridge over uneven water” would over Troubled Water by be a more appropriate American music legends description today, but it Simon & Garfunkel. The seems unlikely that title song was the recipient of would have had that same multiple Grammy awards, artistic appeal.

We will and it can serve as a fitting make due for the purpose analogy for investors. The of our analogy. Just as water is day-to-day flow of news always in a state What tomorrow will bring can, at times, influence for the economy or capital of flux, so is the the near-term direction markets remains to be seen. of the capital markets. dynamic world The sources of uncertainty It can be tempting in which we live. that exist today are unlikely to make investment to dissipate in the near changes in anticipation term. Just as water is always of or in response to in a state of flux, so is the such news.

However, we dynamic world in which believe that investors we live. There will always who have established a be more questions than disciplined investment answers about the future. policy, consistent with Instead of speculating their tolerance for risk, about the unknown, can rise above the rough we believe it is critical waters and maintain focus that investors develop a on the path to achieving well-conceived plan and their long-term goals maintain the discipline and and objectives. A wellpatience needed to stick to formulated plan acts as that plan.

Doing so will not that bridge. allow you to avoid the rough Admittedly, the waters, but it will allow you comparison of current to maintain your bearings conditions with troubled and keep your eyes on the water might seem too horizon on the metaphorical negative given the road ahead. overall outlook today. We would agree with that 15 . 16 2016 the road ahead Contributing authors Jim Baird, CPA, CFP®, CIMA® Chief Investment Officer Eric Dahlberg Senior Equity Analyst Erin Goss, CFA, CAIASM, CIMA®, CFS® Senior Alternative Investment Analyst Jeremy Kedzior Analyst Tricia Newcomb, CIMA® Senior Strategy Analyst Paul Olmsted Senior Fixed Income Analyst Max Wellinger Analyst Visit us at: wealth.plantemoran.com Investment Management Consultants Association (IMCA®) is the owner of the certification marks “CIMA®,” and “Certified Investment Management Analyst ®.” Use of CIMA® or Certified Investment Management Analyst ® signifies that the user has successfully completed IMCA’s initial and ongoing credentialing requirements for investment management consultants. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The CAIA Association® may grant the right to use the CAIASM Marks to those individuals who have been granted the status of either “Full Member” or “Retired Member” by the CAIA Association®.

The Institute of Business and Finance owns the certification marks CFS® and Certified Fund Specialist ®, which it awards to individuals who successfully complete its initial and ongoing certification requirements. Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain. Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness.

Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation. Investment recommendations provided herein are subject to change at any time.

Those recommendations provided herein are provided for informational purposes only and are not provided as a recommendation to buy or sell any one security or allocate to any asset class. Past and current recommendations that are profitable are not indicative of future results, which may in fact result in a loss. Please contact PMFA if you are interested in receiving a list of all past specific investment recommendations for the preceding 12 months. .

reflections 17 . .