Description

{forging ahead}

2015 the road ahead

Assessing the key milestones

of 2014 and taking stock

of the path before us are

critical steps as we prepare

to forge ahead into what

2015 has in store.

.

. forging ahead

Executive summary.

•

Despite a slow start to the year, U.S. economic

growth rebounded and advanced at a

moderate pace in the quarters that followed.

Steady economic growth supported the

Fed’s decision to end its latest round

of quantitative easing (QE) in October;

however, the timing of the first interest rate

hike will be heavily dependent on the Fed’s

interpretation of ongoing economic data

and remains a wild card for capital markets.

•

Throughout the latter part of 2014,

developed regions across the globe were

once again challenged by signs of slow

economic growth and disinflationary

pressures. International equities remained

volatile and the strengthening U.S. dollar

detracted from returns for U.S.-based

investors.

Ongoing stimulus efforts in those regions should help support economic growth, eventually boosting earnings growth and equity prices for patient, long-term investors. • After long-term interest rates moved lower — contrary to expectations heading into 2014 — room for additional downside in yields is even more limited today. All eyes remain on the Fed, as the timing, magnitude, and pace of interest rate hikes remain a question mark. Many bond managers maintain a somewhat defensive positioning against rising rates within their portfolios, as higher rates seem to be the path of least resistance. • Stocks followed a bumpier path in 2014, following an extended period of exceptionally low volatility, but appear positioned to end the year on a positive note. Given the backdrop of current valuations, expectations for modest economic growth, tepid inflation, and high profit margins, we anticipate equity returns to be below historical averages over a multiyear timeframe.

Fundamentals and valuations are likely to become an even greater focal point for investors, particularly as the Fed eventually shifts toward a more hawkish stance. • Following a multiyear bull market in equities, interest rates near historical lows, and modest inflation expectations, we remain convinced that the case for broadening the opportunity set beyond traditional stocks and bonds is still strong. Alternative investments should continue to play a role within diversified portfolios for long-term investors. • As in previous years, our outlook for the coming years is founded on economic and market conditions, asset class valuations, and other macro themes that may provide either support or a headwind for the capital markets. What cannot be easily integrated into those views are the unknown developments — positive or negative — that will inevitably occur over time, altering the expected path of the markets.

As such, long-term investors are well advised to remain patient and disciplined, maintain a diversified investment approach consistent with their risk tolerance, and maintain a long-term view. Constructing a wellconceived portfolio and remaining committed to one’s investment plan should allow investors to stay the course, as they travel along the road ahead. 1 . 2 2015 the road ahead 2014 revisited. For equity investors, the first half of 2014 began where 2013 left off. Markets climbed higher on earnings growth, rising confidence, and generally positive economic data, all of which helped fuel modest multiple expansion in stocks and pushed broad equity market indexes to all-time highs. After the S&P 500 Index closed above the 2,000 mark several times during September, equity markets experienced what some considered a long-awaited but short-lived retrenchment. Volatility spiked in October and erased much of the yearto-date gains achieved to that point. This uptick in volatility was more pronounced for riskier assets, such as small caps and emerging-market equities, but wasn’t limited to stocks alone.

Long-term Treasury yields moved meaningfully over a matter of days, and commodities were also hit. Nonetheless, stocks quickly recaptured those losses in subsequent trading days, and many indexes not only recovered, but ended the month even higher. In what came as a surprise to most, longterm interest rates edged lower over the course of much of the year, despite moderate economic growth in the U.S. and the unwinding of the Fed’s QE program, which came to a close in October. After starting the year at 3.0%, the 10-year Treasury yield marched steadily lower, breaching the 2% threshold briefly during intra-day trading in mid-October, before moving back to the 2.2% – 2.4% range. The move in yields supported fixed-income returns, but flew in the face of consensus .

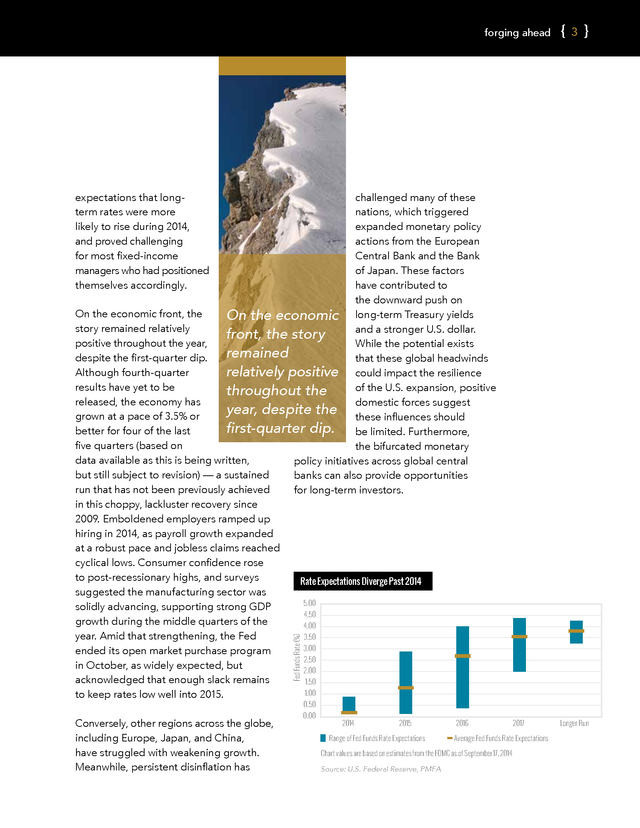

forging ahead 3 challenged many of these nations, which triggered expanded monetary policy actions from the European Central Bank and the Bank of Japan. These factors have contributed to the downward push on On the economic front, the On the economic long-term Treasury yields story remained relatively and a stronger U.S. dollar. front, the story positive throughout the year, While the potential exists remained despite the first-quarter dip. that these global headwinds Although fourth-quarter relatively positive could impact the resilience results have yet to be of the U.S. expansion, positive throughout the released, the economy has domestic forces suggest year, despite the these influences should grown at a pace of 3.5% or first-quarter dip.

be limited. Furthermore, better for four of the last five quarters (based on the bifurcated monetary data available as this is being written, policy initiatives across global central but still subject to revision) — a sustained banks can also provide opportunities run that has not been previously achieved for long-term investors. in this choppy, lackluster recovery since 2009. Emboldened employers ramped up hiring in 2014, as payroll growth expanded at a robust pace and jobless claims reached cyclical lows.

Consumer confidence rose to post-recessionary highs, and surveys Rate Expectations Diverge Past 2014 suggested the manufacturing sector was 5.00 solidly advancing, supporting strong GDP 4.50 growth during the middle quarters of the 4.00 year. Amid that strengthening, the Fed 3.50 3.00 ended its open market purchase program 2.50 in October, as widely expected, but 2.00 acknowledged that enough slack remains 1.50 1.00 to keep rates low well into 2015. Fed Funds Rate (%) expectations that longterm rates were more likely to rise during 2014, and proved challenging for most fixed-income managers who had positioned themselves accordingly. 0.50 Conversely, other regions across the globe, including Europe, Japan, and China, have struggled with weakening growth. Meanwhile, persistent disinflation has 0.00 2014 2015 Range of Fed Funds Rate Expectations 2016 Average Fed Funds Rate Expectations Chart values are based on estimates from the FOMC as of September 17, 2014 Source: U.S. Federal Reserve, PMFA 2017 Longer Run .

4 2015 the road ahead Navigating the road ahead in 2015. The theme for this year’s piece is “Forging Ahead,” a fitting tagline for where the economy and capital markets currently stand at this stage in the cycle — somewhere between the expectations set by the runaway optimism of a term such as full steam ahead, but substantially more promising than the so-called muddle-through economy popularized in the wake of the great recession. Certainly, from an economic standpoint, data over the last year indicates the economy is forging ahead. Whether or not the recent strength is sufficient to allow the economy to reach “escape velocity” — expanding without the influence of accommodative monetary policy — remains a question. Current Fed policy is also aligned with the “forge ahead” mentality, as the Federal Open Market Committee remains focused on gradually easing its way toward policy normalization, while still providing sufficient support to an economy that is recapturing demand lost during the great recession. The progress made to date has allowed the Fed to cease its outright bond purchases, as noted above. This exceptionally accommodative policy has been winding down since early 2014, with the Fed ending the current round of quantitative easing in October. Despite these changes, shortterm rates remain exceptionally low, and the Fed is generally expected to stay accommodative on that front until at least midway through 2015.

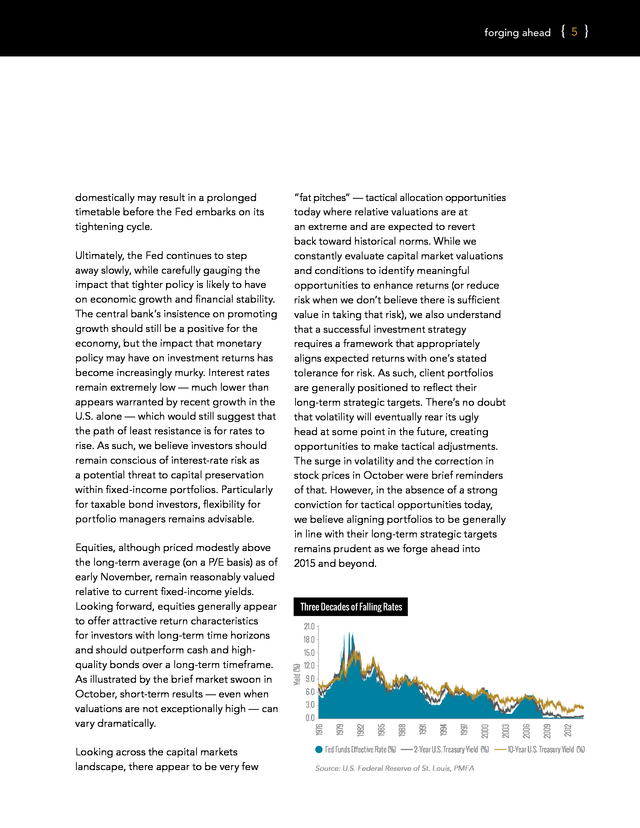

However, recent comments from various Fed governors have suggested that persistently slow growth internationally or financial instability . forging ahead Looking across the capital markets landscape, there appear to be very few Three Decades of Falling Rates THREE 21.0 18.0 15.0 12.0 9.0 6.0 3.0 Fed Funds Effective Rate (%) 2-Year U.S. Treasury Yield (%) Source: U.S. Federal Reserve of St. Louis, PMFA 2012 2009 2006 2003 2000 1997 1994 1991 1988 1985 1982 0.0 1979 Equities, although priced modestly above the long-term average (on a P/E basis) as of early November, remain reasonably valued relative to current fixed-income yields. Looking forward, equities generally appear to offer attractive return characteristics for investors with long-term time horizons and should outperform cash and highquality bonds over a long-term timeframe. As illustrated by the brief market swoon in October, short-term results — even when valuations are not exceptionally high — can vary dramatically. 1976 Ultimately, the Fed continues to step away slowly, while carefully gauging the impact that tighter policy is likely to have on economic growth and financial stability. The central bank’s insistence on promoting growth should still be a positive for the economy, but the impact that monetary policy may have on investment returns has become increasingly murky.

Interest rates remain extremely low — much lower than appears warranted by recent growth in the U.S. alone — which would still suggest that the path of least resistance is for rates to rise. As such, we believe investors should remain conscious of interest-rate risk as a potential threat to capital preservation within fixed-income portfolios.

Particularly for taxable bond investors, flexibility for portfolio managers remains advisable. “fat pitches” — tactical allocation opportunities today where relative valuations are at an extreme and are expected to revert back toward historical norms. While we constantly evaluate capital market valuations and conditions to identify meaningful opportunities to enhance returns (or reduce risk when we don’t believe there is sufficient value in taking that risk), we also understand that a successful investment strategy requires a framework that appropriately aligns expected returns with one’s stated tolerance for risk. As such, client portfolios are generally positioned to reflect their long-term strategic targets.

There’s no doubt that volatility will eventually rear its ugly head at some point in the future, creating opportunities to make tactical adjustments. The surge in volatility and the correction in stock prices in October were brief reminders of that. However, in the absence of a strong conviction for tactical opportunities today, we believe aligning portfolios to be generally in line with their long-term strategic targets remains prudent as we forge ahead into 2015 and beyond. Yield (%) domestically may result in a prolonged timetable before the Fed embarks on its tightening cycle. 5 10-Year U.S. Treasury Yield (%) .

6 2015 the road ahead Will 2015 be a turning point in the interest rate cycle? FIXED INCOME For fixed-income investors, the much anticipated increase in bond yields did not come to pass in 2014. In fact, longer-term yields steadily fell throughout the year; the benchmark 10-year U.S. Treasury began the year at 3%. Speculation around the timing of a Fed decision to increase the Fed funds rate caused markets to behave reactively to the Fed’s messaging, picking apart not only policy statements from the central bank, but any comments from its members that might provide additional color on current thinking within policymaking circles. Despite the prospects for stronger domestic economic growth, yields continued to fall throughout the year. As rate moves have historically often presaged turning points in the actual economy, declining Treasury yields caused some investors and market observers to question whether the expansion remained on track.

Investor focus eventually turned toward a variety of headwinds to higher interest rates, including a low inflation outlook, a global economic slowdown and, given their comparatively low yields, surprisingly strong demand for fixedincome investments. These issues are likely to remain on the table into 2015 and may help keep rates lower than what would be expected during a more typical expansion — one free from extraordinary measures such as quantitative easing and policy rates pushing against the zero bound. . forging ahead 7 OUTLOOK & STRATEGY 3.0 2.0 1.0 Fed Funds Effective Rate (%) Implied by Fed Dots Source: U.S. Federal Reserve, PMFA 2017 2016 2015 2014 2013 2012 2011 2010 2009 0.0 2008 From an interest rate perspective, while we anticipate rates to trend higher over a secular (or long-term) horizon, the timing and magnitude of a sustained upward move in rates remain uncertain. While it is impossible to accurately predict the direction of interest rates in the short term, it is possible that rates could remain low and Percent (%) in a somewhat narrow range. The near-term direction for rates will likely hinge on any As we forge ahead into 2015, action by the Fed to increase the dispersion of potential its policy rate or stand pat, outcomes has seemingly as well as the global appetite become wider. Our long-term for yield or, conversely, for conviction about higher Treasuries as a safe haven. rates remains a primary The chart below shows the We can be theme within fixed-income potential direction of rates portfolios, but diversification certain that and paints a clear picture of continues to be an important fixed-income how the market’s implied path factor. markets are of short-term rates differs We anticipate that from that of the Federal priced for uncertainty around the Reserve.

In addition, during greater volatility the past two Fed hiking cycles bond market will persist. in 2015. The strong conviction of in 1994 and 2004, increases most market prognosticators in short-term rates have been was off target in 2014, and the outlook has accompanied by higher long-term rates. become increasingly murky. When will the This provides support for implementing Fed raise rates? Can the economy reach bond portfolios with core bond strategies “escape velocity”? Will global growth with alpha-generating potential and concerns persist? Will Treasuries remain a modest allocation to more flexible an attractive safe haven investment for mandates that afford managers greater foreign investors despite their low yields? ability to meaningfully adjust their portfolio Can inflation stay low even as the economy structure and duration positioning. gathers momentum and the expansion matures? While the answers to these Fed Funds Rate Projection questions will eventually be answered, we can be certain that fixed-income markets 4.0 are priced for greater volatility in 2015. Market expectations as of Oct. 28, 2014 .

8 2015 the road ahead The return of equity volatility. EQUITIES Volatility returned to equity markets in 2014 after nearly three years of a virtually uninterrupted bull market. It seemed a natural next step as this bull market matured, valuations may have become a bit extended, and various indexes continually Market Volatility Re-emerges 30 2,000 S&P 500 Index 20 1,850 1,800 15 1,750 10 1,700 5 1,650 1,600 Oct 2013 S&P 500 Index Jan 2014 Apr 2014 Jul 2014 VIX CBOE S&P Market Volatility Index Source: U.S. Federal Reserve of St. Louis Oct 2014 0 CBOE VIX Index 25 1,950 1,900 set new highs.

Biotech, social media, and cloud computing stocks sold off sharply from mid-March through April, weighing on the broad market as well, but equity investors subsequently shrugged off those losses and pushed markets higher. Later in the year, summertime complacency was met with a renewed bout of instability in stocks during September and October, as oil — and commodity prices broadly — declined in the face of diminished global growth expectations. Throughout the year, though, underlying economic fundamentals in the U.S. remained largely supportive for equities, with solid GDP growth underpinned by robust job creation and rising consumer confidence. Outside of the U.S., it was a .

forging ahead different and varied picture. European equities were dragged down by slowing growth, especially in the second half of the year, as the ECB contemplated a large scale quantitative easing program. In Japan, quantitative easing was expanded and helped support Japanese equities while weighing on the yen, making Japanese exports cheaper for much of the world. Emerging-market stocks rebounded early in the year — after relative underperformance during the prior two years — yet concerns over potentially slowing global growth and an increasing sense that long-term growth expectations for the Chinese economy should be curtailed weighed on second-half returns. Whereas 2013 equity performance was driven mainly by an expansion in P/E ratios, returns in 2014 were much more balanced with earnings growth carrying its weight. Valuations rose, though not to euphoric levels, while earnings grew at a mid-to-high single-digit pace, and revenues expanded moderately. Profit margins remained at historically high levels, begging the question of when they may revert back toward their long-term average.

We look for further clarity around that issue, along with other considerations surrounding geopolitical events and global economic growth, in the coming year. OUTLOOK & STRATEGY With the end of asset purchases by the Fed that provided a strong tailwind for equities in recent years, investors naturally question what the end of QE will mean for stocks. It is notable, though, that the Fed’s zero interest rate policy remains in place and should be supportive of equities and other risk assets for some time to come. Environments characterized by both low inflation and interest rates have historically tended to justify equity valuations above their long-term average. While rising interest rates have often presented a short-term obstacle to stock returns, the stronger growth that often accompanies the rising rate cycle is generally supportive of corporate earnings as well, and equities have generally moved even higher after that initial phase. The past year saw fundamentals and valuations become a greater factor in driving equity market performance once again.

Many companies that missed on already reduced earnings or revenue expectations saw their stock prices punished by investors. As markets forge ahead, we anticipate that equity returns may be influenced to an even greater degree by fundamentals, valuations, and growth prospects. Correlations across stocks were mixed in 2014, yet remain near long-term averages. They generally fell through the summer as volatility was low and complacency seeped into equity markets. Yet, they increased sharply during the sell-off in September and October.

Higher correlations tend to create a more challenging environment for active managers to add value through stock selection. Dispersion, meanwhile, has remained low across developed global equities. As an alternative to 9 .

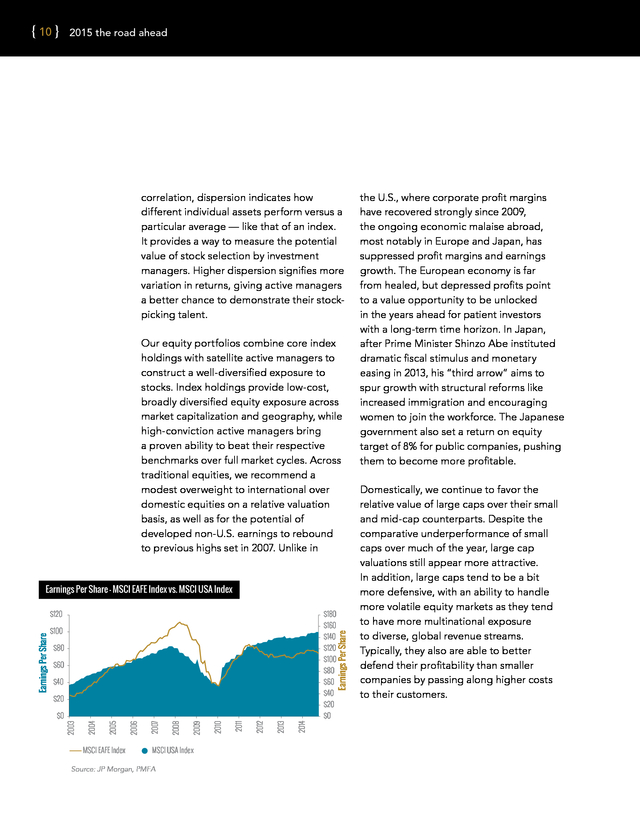

10 2015 the road ahead correlation, dispersion indicates how different individual assets perform versus a particular average — like that of an index. It provides a way to measure the potential value of stock selection by investment managers. Higher dispersion signifies more variation in returns, giving active managers a better chance to demonstrate their stockpicking talent. Our equity portfolios combine core index holdings with satellite active managers to construct a well-diversified exposure to stocks. Index holdings provide low-cost, broadly diversified equity exposure across market capitalization and geography, while high-conviction active managers bring a proven ability to beat their respective benchmarks over full market cycles. Across traditional equities, we recommend a modest overweight to international over domestic equities on a relative valuation basis, as well as for the potential of developed non-U.S.

earnings to rebound to previous highs set in 2007. Unlike in Earnings Per Share – MSCI EAFE Index vs. MSCI USA Index $180 $140 $80 Earnings Per Share $160 $100 $120 $100 $60 $80 $40 $60 $40 $20 $20 $0 MSCI EAFE Index MSCI USA Index Source: JP Morgan, PMFA 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 $0 2003 Earnings Per Share $120 the U.S., where corporate profit margins have recovered strongly since 2009, the ongoing economic malaise abroad, most notably in Europe and Japan, has suppressed profit margins and earnings growth.

The European economy is far from healed, but depressed profits point to a value opportunity to be unlocked in the years ahead for patient investors with a long-term time horizon. In Japan, after Prime Minister Shinzo Abe instituted dramatic fiscal stimulus and monetary easing in 2013, his “third arrow” aims to spur growth with structural reforms like increased immigration and encouraging women to join the workforce. The Japanese government also set a return on equity target of 8% for public companies, pushing them to become more profitable. Domestically, we continue to favor the relative value of large caps over their small and mid-cap counterparts.

Despite the comparative underperformance of small caps over much of the year, large cap valuations still appear more attractive. In addition, large caps tend to be a bit more defensive, with an ability to handle more volatile equity markets as they tend to have more multinational exposure to diverse, global revenue streams. Typically, they also are able to better defend their profitability than smaller companies by passing along higher costs to their customers. . forging ahead Diversification beyond stocks and bonds. ALTERNATIVES Over the past few years, traditional investments — particularly domestic stocks — have delivered absolute returns that have exceeded investor expectations and historical average returns. At the same time, other parts of the capital markets have trailed the robust returns of stocks. Among those are cash, high-quality bonds, and some alternative investments. As is often the case when stocks perform exceptionally well, some investors have questioned the long-term benefits of investing in alternatives, just as others may question the benefit of investing in bonds with yields at exceptionally low levels. We continue to believe in the principles of modern portfolio theory that convey simply that the inclusion of alternative investments should help to smooth the ride to a targeted return goal over the long term. Today, given the strong equity market rally in recent years and persistently low interest rates and low market expectations for inflation, we feel strongly that investors should not abandon their alternative investments. Fundamentally, they still exhibit the risk, return, and correlation benefits that make them effective diversifiers to a core portfolio of traditional stocks and bonds. In an optimized portfolio, alternative investments may be alternatives to not only equities, but to core fixed income as well. As such, the measuring stick for evaluating 11 .

12 2015 the road ahead considerations. With their expanded alternatives shouldn’t be whether or not flexibility and ability to profit on both long they outperformed equities alone, just as and short positions in their portfolios, the value of investing in bonds shouldn’t hedged equity strategies be determined solely still offer compelling risk/ on whether or not they return characteristics outperformed stocks in a and remain an attractive given period. The value diversifier to a portfolio provided by holding bonds of core bonds and stocks. or alternative investments Moreover, a wide range isn’t based on performance Alternatives of other alternative alone; if it was, a portfolio investments may merit of stocks alone would (just like bonds) consideration for investors almost always “win” over can play a role who seek to further not only many relatively diversify their portfolios short periods, but the long in a diversified and have the ability to term as well. Investors are portfolio. accept the often-higher typically targeting a stated investment minimums, rate of return within risk liquidity restrictions, and constraints determined by tax requirements. their individual tolerance for risk as summarized in their investment policy.

Within that context, alternatives (just like bonds) can play a role in a diversified portfolio to position the portfolio to achieve the investor’s long-term return goal while reducing portfolio risk. Today, we still see value in hedging strategies, including liquid long/ short funds and traditional multistrategy hedge funds, for investors who meet the minimum investment requirements and are comfortable with the liquidity and tax reporting . forging ahead Change may be on the horizon, but will it matter? TAXES The coming year holds the potential to bring significant changes to tax policy. The conclusion of the mid-term elections opens a window of opportunity for legislative action. Although 2014 was a year of little change in the law, it was one of significant adjustment for taxpayers as the full impact of tax increases and the new net investment income tax that were effective for returns filed in 2014 were realized. Tax efficiency in investments and business entity selection are more important now and will continue to be so in 2015.

Income shifting to lower-income family members, timing of gain and loss recognition, and increasing levels of participation in family business activities can all have positive impacts on net, after-tax income. Wealth transfer taxes are less significant for the majority of families as the gift and estate tax exclusion rises to $5.43M in 2015 (a combined $10.86M for married couples). The rise in the exclusion amount has shifted planning for most couples to include efforts to take maximum advantage of the step-up in basis for assets included in the estate of a first spouse to die, providing significant income tax benefits to the surviving spouse and family. Families with taxable estates (above the exclusion amounts) also benefit from the higher exclusion as it expands opportunities for lifetime wealth transfers that cannot only minimize estate taxes for the current and next generation, but for generations to come. 13 . 14 2015 the road ahead Moving forward in 2015 will initially as the potential for tax reform is realized. focus planning efforts on fully What hasn’t changed is that those who implementing changes to business, take a wait and see approach run the risk of investment, income tax, paying more tax than those and estate tax planning who plan ahead. Even with strategies that were the uncertainty around how made emergent by recent tax policy may change in changes in the tax laws. the coming years, we urge Regretfully, no As the year unfolds, new clients to forge ahead in a one can predict opportunities may arise deliberate, informed manner. the future. If we could, investing would be a much easier proposition. . forging ahead Preparing for the road ahead. CONCLUSION While the preceding pages have provided support for our outlook on the path that lies ahead, we’d be the first to acknowledge that predictions about the future, regardless of how interesting they may be, are still nothing more than educated guesses. We are reminded of the old tongue-in-cheek rule about forecasting. While it’s fine to opine about either a specific outcome or a specific timeframe for some outcome, one should never be specific on both. It’s somewhat ironic that this is particularly true over shorter periods for investing, as market movements are exceptionally unpredictable.

Of course, no one can predict the future. If we could, investing would be a much easier proposition, to say the least. However, we continue to believe it’s a healthy intellectual exercise to contemplate potential outcomes and consider how those outcomes should influence portfolio strategy decisions. Moreover, time may be the best friend of patient investors, as fundamentals tend to be much more meaningful to the long-term market and portfolio performance than to short-term results. While “forging ahead” can have various connotations, a more technical definition for the word “forge” is the process of forming or shaping metal by heating and applying compressive forces.

By its very nature, this practice produces two powerful outcomes. 15 . 16 2015 the road ahead markets, while longer-term trends can be influenced by exogenous factors and “Forging ahead” play out in unexpected ways. Regardless of these suggests uncontrollable factors, we • Second, it allows one to that one stay believe one of the most manipulate its form into focused on critical determinants of a desired output with success is the underlying those long-term long-lasting results. process behind the objectives and creation of one’s This process is commonly move forward investment portfolio. used in the creation in a disciplined, Utilizing a disciplined, of components for time-tested approach to transportation equipment, deliberate portfolio construction like planes, trains, and manner toward (much like the process automobiles — where the those goals. of forging) can deliver a strength and precision of portfolio that is strong, the individual components enduring, and appropriately are critical for an enduring molded to each individual’s tolerance for lifespan of the end product. Unfortunately, risk and long-term goals and objectives. today’s investment landscape cannot be so easily manipulated to achieve a What specifically the coming year may hold desired outcome. for investors remains to be seen. There are many questions left unanswered, as is A less literal interpretation of the term is always the case in a dynamic world.

There often associated with moving forward, or is no formula that can be used to divine making strong, steady progress toward the future for the economy or the capital a goal. In this sense, we believe that it is markets. The key is to approach it with very apropos to the topic at hand.

Most investors have a number of goals, with most a well-conceived plan and maintain the discipline and patience needed to stick to being long term in nature. In that context, that plan through turmoil, euphoria, and “forging ahead” suggests that one stay anything in between. focused on those long-term objectives and move forward in a disciplined, deliberate Armed with those, we believe that investors manner toward those goals. are well positioned to reach their goals and achieve success as they travel along the The daily inflow of news can, at times, road ahead. materially influence the mood of investors and the near-term direction of the capital • First, it strengthens the metal significantly by sealing cracks, minimizing impurities, and improving its overall integrity. . Contributing authors Jim Baird, CPA, CFP®, CIMA® Chief Investment Officer Eric Dahlberg Senior Equity Analyst Erin Goss, CFA, CAIASM, CIMA®, CFS® Senior Alternative Investment Analyst James Minutolo, JD Senior Tax Manager Tricia Newcomb, CIMA® Senior Strategy Analyst Paul Olmsted Senior Fixed Income Analyst Ed Rumler, CFA® Alternative Investments Analyst Contact us at: wealth.plantemoran.com Investment Management Consultants Association (IMCA®) is the owner of the certification marks “CIMA®,” and “Certified Investment Management Analyst ®.” Use of CIMA® or Certified Investment Management Analyst ® signifies that the user has successfully completed IMCA’s initial and ongoing credentialing requirements for investment management consultants. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The CAIA Association® may grant the right to use the CAIASM Marks to those individuals who have been granted the status of either “Full Member” or “Retired Member” by the CAIA Association®.

The Institute of Business and Finance owns the certification marks CFS® and Certified Fund Specialist ®, which it awards to individuals who successfully complete its initial and ongoing certification requirements. Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain. Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness.

Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation. Investment recommendations provided herein are subject to change at any time.

Those recommendations provided herein are provided for informational purposes only and are not provided as a recommendation to buy or sell any one security or allocate to any asset class. Past and current recommendations that are profitable are not indicative of future results, which may in fact result in a loss. Please contact PMFA if you are interested in receiving a list of all past specific investment recommendations for the preceding 12 months. .

wealth.plantemoran.com .

Ongoing stimulus efforts in those regions should help support economic growth, eventually boosting earnings growth and equity prices for patient, long-term investors. • After long-term interest rates moved lower — contrary to expectations heading into 2014 — room for additional downside in yields is even more limited today. All eyes remain on the Fed, as the timing, magnitude, and pace of interest rate hikes remain a question mark. Many bond managers maintain a somewhat defensive positioning against rising rates within their portfolios, as higher rates seem to be the path of least resistance. • Stocks followed a bumpier path in 2014, following an extended period of exceptionally low volatility, but appear positioned to end the year on a positive note. Given the backdrop of current valuations, expectations for modest economic growth, tepid inflation, and high profit margins, we anticipate equity returns to be below historical averages over a multiyear timeframe.

Fundamentals and valuations are likely to become an even greater focal point for investors, particularly as the Fed eventually shifts toward a more hawkish stance. • Following a multiyear bull market in equities, interest rates near historical lows, and modest inflation expectations, we remain convinced that the case for broadening the opportunity set beyond traditional stocks and bonds is still strong. Alternative investments should continue to play a role within diversified portfolios for long-term investors. • As in previous years, our outlook for the coming years is founded on economic and market conditions, asset class valuations, and other macro themes that may provide either support or a headwind for the capital markets. What cannot be easily integrated into those views are the unknown developments — positive or negative — that will inevitably occur over time, altering the expected path of the markets.

As such, long-term investors are well advised to remain patient and disciplined, maintain a diversified investment approach consistent with their risk tolerance, and maintain a long-term view. Constructing a wellconceived portfolio and remaining committed to one’s investment plan should allow investors to stay the course, as they travel along the road ahead. 1 . 2 2015 the road ahead 2014 revisited. For equity investors, the first half of 2014 began where 2013 left off. Markets climbed higher on earnings growth, rising confidence, and generally positive economic data, all of which helped fuel modest multiple expansion in stocks and pushed broad equity market indexes to all-time highs. After the S&P 500 Index closed above the 2,000 mark several times during September, equity markets experienced what some considered a long-awaited but short-lived retrenchment. Volatility spiked in October and erased much of the yearto-date gains achieved to that point. This uptick in volatility was more pronounced for riskier assets, such as small caps and emerging-market equities, but wasn’t limited to stocks alone.

Long-term Treasury yields moved meaningfully over a matter of days, and commodities were also hit. Nonetheless, stocks quickly recaptured those losses in subsequent trading days, and many indexes not only recovered, but ended the month even higher. In what came as a surprise to most, longterm interest rates edged lower over the course of much of the year, despite moderate economic growth in the U.S. and the unwinding of the Fed’s QE program, which came to a close in October. After starting the year at 3.0%, the 10-year Treasury yield marched steadily lower, breaching the 2% threshold briefly during intra-day trading in mid-October, before moving back to the 2.2% – 2.4% range. The move in yields supported fixed-income returns, but flew in the face of consensus .

forging ahead 3 challenged many of these nations, which triggered expanded monetary policy actions from the European Central Bank and the Bank of Japan. These factors have contributed to the downward push on On the economic front, the On the economic long-term Treasury yields story remained relatively and a stronger U.S. dollar. front, the story positive throughout the year, While the potential exists remained despite the first-quarter dip. that these global headwinds Although fourth-quarter relatively positive could impact the resilience results have yet to be of the U.S. expansion, positive throughout the released, the economy has domestic forces suggest year, despite the these influences should grown at a pace of 3.5% or first-quarter dip.

be limited. Furthermore, better for four of the last five quarters (based on the bifurcated monetary data available as this is being written, policy initiatives across global central but still subject to revision) — a sustained banks can also provide opportunities run that has not been previously achieved for long-term investors. in this choppy, lackluster recovery since 2009. Emboldened employers ramped up hiring in 2014, as payroll growth expanded at a robust pace and jobless claims reached cyclical lows.

Consumer confidence rose to post-recessionary highs, and surveys Rate Expectations Diverge Past 2014 suggested the manufacturing sector was 5.00 solidly advancing, supporting strong GDP 4.50 growth during the middle quarters of the 4.00 year. Amid that strengthening, the Fed 3.50 3.00 ended its open market purchase program 2.50 in October, as widely expected, but 2.00 acknowledged that enough slack remains 1.50 1.00 to keep rates low well into 2015. Fed Funds Rate (%) expectations that longterm rates were more likely to rise during 2014, and proved challenging for most fixed-income managers who had positioned themselves accordingly. 0.50 Conversely, other regions across the globe, including Europe, Japan, and China, have struggled with weakening growth. Meanwhile, persistent disinflation has 0.00 2014 2015 Range of Fed Funds Rate Expectations 2016 Average Fed Funds Rate Expectations Chart values are based on estimates from the FOMC as of September 17, 2014 Source: U.S. Federal Reserve, PMFA 2017 Longer Run .

4 2015 the road ahead Navigating the road ahead in 2015. The theme for this year’s piece is “Forging Ahead,” a fitting tagline for where the economy and capital markets currently stand at this stage in the cycle — somewhere between the expectations set by the runaway optimism of a term such as full steam ahead, but substantially more promising than the so-called muddle-through economy popularized in the wake of the great recession. Certainly, from an economic standpoint, data over the last year indicates the economy is forging ahead. Whether or not the recent strength is sufficient to allow the economy to reach “escape velocity” — expanding without the influence of accommodative monetary policy — remains a question. Current Fed policy is also aligned with the “forge ahead” mentality, as the Federal Open Market Committee remains focused on gradually easing its way toward policy normalization, while still providing sufficient support to an economy that is recapturing demand lost during the great recession. The progress made to date has allowed the Fed to cease its outright bond purchases, as noted above. This exceptionally accommodative policy has been winding down since early 2014, with the Fed ending the current round of quantitative easing in October. Despite these changes, shortterm rates remain exceptionally low, and the Fed is generally expected to stay accommodative on that front until at least midway through 2015.

However, recent comments from various Fed governors have suggested that persistently slow growth internationally or financial instability . forging ahead Looking across the capital markets landscape, there appear to be very few Three Decades of Falling Rates THREE 21.0 18.0 15.0 12.0 9.0 6.0 3.0 Fed Funds Effective Rate (%) 2-Year U.S. Treasury Yield (%) Source: U.S. Federal Reserve of St. Louis, PMFA 2012 2009 2006 2003 2000 1997 1994 1991 1988 1985 1982 0.0 1979 Equities, although priced modestly above the long-term average (on a P/E basis) as of early November, remain reasonably valued relative to current fixed-income yields. Looking forward, equities generally appear to offer attractive return characteristics for investors with long-term time horizons and should outperform cash and highquality bonds over a long-term timeframe. As illustrated by the brief market swoon in October, short-term results — even when valuations are not exceptionally high — can vary dramatically. 1976 Ultimately, the Fed continues to step away slowly, while carefully gauging the impact that tighter policy is likely to have on economic growth and financial stability. The central bank’s insistence on promoting growth should still be a positive for the economy, but the impact that monetary policy may have on investment returns has become increasingly murky.

Interest rates remain extremely low — much lower than appears warranted by recent growth in the U.S. alone — which would still suggest that the path of least resistance is for rates to rise. As such, we believe investors should remain conscious of interest-rate risk as a potential threat to capital preservation within fixed-income portfolios.

Particularly for taxable bond investors, flexibility for portfolio managers remains advisable. “fat pitches” — tactical allocation opportunities today where relative valuations are at an extreme and are expected to revert back toward historical norms. While we constantly evaluate capital market valuations and conditions to identify meaningful opportunities to enhance returns (or reduce risk when we don’t believe there is sufficient value in taking that risk), we also understand that a successful investment strategy requires a framework that appropriately aligns expected returns with one’s stated tolerance for risk. As such, client portfolios are generally positioned to reflect their long-term strategic targets.

There’s no doubt that volatility will eventually rear its ugly head at some point in the future, creating opportunities to make tactical adjustments. The surge in volatility and the correction in stock prices in October were brief reminders of that. However, in the absence of a strong conviction for tactical opportunities today, we believe aligning portfolios to be generally in line with their long-term strategic targets remains prudent as we forge ahead into 2015 and beyond. Yield (%) domestically may result in a prolonged timetable before the Fed embarks on its tightening cycle. 5 10-Year U.S. Treasury Yield (%) .

6 2015 the road ahead Will 2015 be a turning point in the interest rate cycle? FIXED INCOME For fixed-income investors, the much anticipated increase in bond yields did not come to pass in 2014. In fact, longer-term yields steadily fell throughout the year; the benchmark 10-year U.S. Treasury began the year at 3%. Speculation around the timing of a Fed decision to increase the Fed funds rate caused markets to behave reactively to the Fed’s messaging, picking apart not only policy statements from the central bank, but any comments from its members that might provide additional color on current thinking within policymaking circles. Despite the prospects for stronger domestic economic growth, yields continued to fall throughout the year. As rate moves have historically often presaged turning points in the actual economy, declining Treasury yields caused some investors and market observers to question whether the expansion remained on track.

Investor focus eventually turned toward a variety of headwinds to higher interest rates, including a low inflation outlook, a global economic slowdown and, given their comparatively low yields, surprisingly strong demand for fixedincome investments. These issues are likely to remain on the table into 2015 and may help keep rates lower than what would be expected during a more typical expansion — one free from extraordinary measures such as quantitative easing and policy rates pushing against the zero bound. . forging ahead 7 OUTLOOK & STRATEGY 3.0 2.0 1.0 Fed Funds Effective Rate (%) Implied by Fed Dots Source: U.S. Federal Reserve, PMFA 2017 2016 2015 2014 2013 2012 2011 2010 2009 0.0 2008 From an interest rate perspective, while we anticipate rates to trend higher over a secular (or long-term) horizon, the timing and magnitude of a sustained upward move in rates remain uncertain. While it is impossible to accurately predict the direction of interest rates in the short term, it is possible that rates could remain low and Percent (%) in a somewhat narrow range. The near-term direction for rates will likely hinge on any As we forge ahead into 2015, action by the Fed to increase the dispersion of potential its policy rate or stand pat, outcomes has seemingly as well as the global appetite become wider. Our long-term for yield or, conversely, for conviction about higher Treasuries as a safe haven. rates remains a primary The chart below shows the We can be theme within fixed-income potential direction of rates portfolios, but diversification certain that and paints a clear picture of continues to be an important fixed-income how the market’s implied path factor. markets are of short-term rates differs We anticipate that from that of the Federal priced for uncertainty around the Reserve.

In addition, during greater volatility the past two Fed hiking cycles bond market will persist. in 2015. The strong conviction of in 1994 and 2004, increases most market prognosticators in short-term rates have been was off target in 2014, and the outlook has accompanied by higher long-term rates. become increasingly murky. When will the This provides support for implementing Fed raise rates? Can the economy reach bond portfolios with core bond strategies “escape velocity”? Will global growth with alpha-generating potential and concerns persist? Will Treasuries remain a modest allocation to more flexible an attractive safe haven investment for mandates that afford managers greater foreign investors despite their low yields? ability to meaningfully adjust their portfolio Can inflation stay low even as the economy structure and duration positioning. gathers momentum and the expansion matures? While the answers to these Fed Funds Rate Projection questions will eventually be answered, we can be certain that fixed-income markets 4.0 are priced for greater volatility in 2015. Market expectations as of Oct. 28, 2014 .

8 2015 the road ahead The return of equity volatility. EQUITIES Volatility returned to equity markets in 2014 after nearly three years of a virtually uninterrupted bull market. It seemed a natural next step as this bull market matured, valuations may have become a bit extended, and various indexes continually Market Volatility Re-emerges 30 2,000 S&P 500 Index 20 1,850 1,800 15 1,750 10 1,700 5 1,650 1,600 Oct 2013 S&P 500 Index Jan 2014 Apr 2014 Jul 2014 VIX CBOE S&P Market Volatility Index Source: U.S. Federal Reserve of St. Louis Oct 2014 0 CBOE VIX Index 25 1,950 1,900 set new highs.

Biotech, social media, and cloud computing stocks sold off sharply from mid-March through April, weighing on the broad market as well, but equity investors subsequently shrugged off those losses and pushed markets higher. Later in the year, summertime complacency was met with a renewed bout of instability in stocks during September and October, as oil — and commodity prices broadly — declined in the face of diminished global growth expectations. Throughout the year, though, underlying economic fundamentals in the U.S. remained largely supportive for equities, with solid GDP growth underpinned by robust job creation and rising consumer confidence. Outside of the U.S., it was a .

forging ahead different and varied picture. European equities were dragged down by slowing growth, especially in the second half of the year, as the ECB contemplated a large scale quantitative easing program. In Japan, quantitative easing was expanded and helped support Japanese equities while weighing on the yen, making Japanese exports cheaper for much of the world. Emerging-market stocks rebounded early in the year — after relative underperformance during the prior two years — yet concerns over potentially slowing global growth and an increasing sense that long-term growth expectations for the Chinese economy should be curtailed weighed on second-half returns. Whereas 2013 equity performance was driven mainly by an expansion in P/E ratios, returns in 2014 were much more balanced with earnings growth carrying its weight. Valuations rose, though not to euphoric levels, while earnings grew at a mid-to-high single-digit pace, and revenues expanded moderately. Profit margins remained at historically high levels, begging the question of when they may revert back toward their long-term average.

We look for further clarity around that issue, along with other considerations surrounding geopolitical events and global economic growth, in the coming year. OUTLOOK & STRATEGY With the end of asset purchases by the Fed that provided a strong tailwind for equities in recent years, investors naturally question what the end of QE will mean for stocks. It is notable, though, that the Fed’s zero interest rate policy remains in place and should be supportive of equities and other risk assets for some time to come. Environments characterized by both low inflation and interest rates have historically tended to justify equity valuations above their long-term average. While rising interest rates have often presented a short-term obstacle to stock returns, the stronger growth that often accompanies the rising rate cycle is generally supportive of corporate earnings as well, and equities have generally moved even higher after that initial phase. The past year saw fundamentals and valuations become a greater factor in driving equity market performance once again.

Many companies that missed on already reduced earnings or revenue expectations saw their stock prices punished by investors. As markets forge ahead, we anticipate that equity returns may be influenced to an even greater degree by fundamentals, valuations, and growth prospects. Correlations across stocks were mixed in 2014, yet remain near long-term averages. They generally fell through the summer as volatility was low and complacency seeped into equity markets. Yet, they increased sharply during the sell-off in September and October.

Higher correlations tend to create a more challenging environment for active managers to add value through stock selection. Dispersion, meanwhile, has remained low across developed global equities. As an alternative to 9 .

10 2015 the road ahead correlation, dispersion indicates how different individual assets perform versus a particular average — like that of an index. It provides a way to measure the potential value of stock selection by investment managers. Higher dispersion signifies more variation in returns, giving active managers a better chance to demonstrate their stockpicking talent. Our equity portfolios combine core index holdings with satellite active managers to construct a well-diversified exposure to stocks. Index holdings provide low-cost, broadly diversified equity exposure across market capitalization and geography, while high-conviction active managers bring a proven ability to beat their respective benchmarks over full market cycles. Across traditional equities, we recommend a modest overweight to international over domestic equities on a relative valuation basis, as well as for the potential of developed non-U.S.

earnings to rebound to previous highs set in 2007. Unlike in Earnings Per Share – MSCI EAFE Index vs. MSCI USA Index $180 $140 $80 Earnings Per Share $160 $100 $120 $100 $60 $80 $40 $60 $40 $20 $20 $0 MSCI EAFE Index MSCI USA Index Source: JP Morgan, PMFA 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 $0 2003 Earnings Per Share $120 the U.S., where corporate profit margins have recovered strongly since 2009, the ongoing economic malaise abroad, most notably in Europe and Japan, has suppressed profit margins and earnings growth.

The European economy is far from healed, but depressed profits point to a value opportunity to be unlocked in the years ahead for patient investors with a long-term time horizon. In Japan, after Prime Minister Shinzo Abe instituted dramatic fiscal stimulus and monetary easing in 2013, his “third arrow” aims to spur growth with structural reforms like increased immigration and encouraging women to join the workforce. The Japanese government also set a return on equity target of 8% for public companies, pushing them to become more profitable. Domestically, we continue to favor the relative value of large caps over their small and mid-cap counterparts.

Despite the comparative underperformance of small caps over much of the year, large cap valuations still appear more attractive. In addition, large caps tend to be a bit more defensive, with an ability to handle more volatile equity markets as they tend to have more multinational exposure to diverse, global revenue streams. Typically, they also are able to better defend their profitability than smaller companies by passing along higher costs to their customers. . forging ahead Diversification beyond stocks and bonds. ALTERNATIVES Over the past few years, traditional investments — particularly domestic stocks — have delivered absolute returns that have exceeded investor expectations and historical average returns. At the same time, other parts of the capital markets have trailed the robust returns of stocks. Among those are cash, high-quality bonds, and some alternative investments. As is often the case when stocks perform exceptionally well, some investors have questioned the long-term benefits of investing in alternatives, just as others may question the benefit of investing in bonds with yields at exceptionally low levels. We continue to believe in the principles of modern portfolio theory that convey simply that the inclusion of alternative investments should help to smooth the ride to a targeted return goal over the long term. Today, given the strong equity market rally in recent years and persistently low interest rates and low market expectations for inflation, we feel strongly that investors should not abandon their alternative investments. Fundamentally, they still exhibit the risk, return, and correlation benefits that make them effective diversifiers to a core portfolio of traditional stocks and bonds. In an optimized portfolio, alternative investments may be alternatives to not only equities, but to core fixed income as well. As such, the measuring stick for evaluating 11 .

12 2015 the road ahead considerations. With their expanded alternatives shouldn’t be whether or not flexibility and ability to profit on both long they outperformed equities alone, just as and short positions in their portfolios, the value of investing in bonds shouldn’t hedged equity strategies be determined solely still offer compelling risk/ on whether or not they return characteristics outperformed stocks in a and remain an attractive given period. The value diversifier to a portfolio provided by holding bonds of core bonds and stocks. or alternative investments Moreover, a wide range isn’t based on performance Alternatives of other alternative alone; if it was, a portfolio investments may merit of stocks alone would (just like bonds) consideration for investors almost always “win” over can play a role who seek to further not only many relatively diversify their portfolios short periods, but the long in a diversified and have the ability to term as well. Investors are portfolio. accept the often-higher typically targeting a stated investment minimums, rate of return within risk liquidity restrictions, and constraints determined by tax requirements. their individual tolerance for risk as summarized in their investment policy.

Within that context, alternatives (just like bonds) can play a role in a diversified portfolio to position the portfolio to achieve the investor’s long-term return goal while reducing portfolio risk. Today, we still see value in hedging strategies, including liquid long/ short funds and traditional multistrategy hedge funds, for investors who meet the minimum investment requirements and are comfortable with the liquidity and tax reporting . forging ahead Change may be on the horizon, but will it matter? TAXES The coming year holds the potential to bring significant changes to tax policy. The conclusion of the mid-term elections opens a window of opportunity for legislative action. Although 2014 was a year of little change in the law, it was one of significant adjustment for taxpayers as the full impact of tax increases and the new net investment income tax that were effective for returns filed in 2014 were realized. Tax efficiency in investments and business entity selection are more important now and will continue to be so in 2015.

Income shifting to lower-income family members, timing of gain and loss recognition, and increasing levels of participation in family business activities can all have positive impacts on net, after-tax income. Wealth transfer taxes are less significant for the majority of families as the gift and estate tax exclusion rises to $5.43M in 2015 (a combined $10.86M for married couples). The rise in the exclusion amount has shifted planning for most couples to include efforts to take maximum advantage of the step-up in basis for assets included in the estate of a first spouse to die, providing significant income tax benefits to the surviving spouse and family. Families with taxable estates (above the exclusion amounts) also benefit from the higher exclusion as it expands opportunities for lifetime wealth transfers that cannot only minimize estate taxes for the current and next generation, but for generations to come. 13 . 14 2015 the road ahead Moving forward in 2015 will initially as the potential for tax reform is realized. focus planning efforts on fully What hasn’t changed is that those who implementing changes to business, take a wait and see approach run the risk of investment, income tax, paying more tax than those and estate tax planning who plan ahead. Even with strategies that were the uncertainty around how made emergent by recent tax policy may change in changes in the tax laws. the coming years, we urge Regretfully, no As the year unfolds, new clients to forge ahead in a one can predict opportunities may arise deliberate, informed manner. the future. If we could, investing would be a much easier proposition. . forging ahead Preparing for the road ahead. CONCLUSION While the preceding pages have provided support for our outlook on the path that lies ahead, we’d be the first to acknowledge that predictions about the future, regardless of how interesting they may be, are still nothing more than educated guesses. We are reminded of the old tongue-in-cheek rule about forecasting. While it’s fine to opine about either a specific outcome or a specific timeframe for some outcome, one should never be specific on both. It’s somewhat ironic that this is particularly true over shorter periods for investing, as market movements are exceptionally unpredictable.

Of course, no one can predict the future. If we could, investing would be a much easier proposition, to say the least. However, we continue to believe it’s a healthy intellectual exercise to contemplate potential outcomes and consider how those outcomes should influence portfolio strategy decisions. Moreover, time may be the best friend of patient investors, as fundamentals tend to be much more meaningful to the long-term market and portfolio performance than to short-term results. While “forging ahead” can have various connotations, a more technical definition for the word “forge” is the process of forming or shaping metal by heating and applying compressive forces.

By its very nature, this practice produces two powerful outcomes. 15 . 16 2015 the road ahead markets, while longer-term trends can be influenced by exogenous factors and “Forging ahead” play out in unexpected ways. Regardless of these suggests uncontrollable factors, we • Second, it allows one to that one stay believe one of the most manipulate its form into focused on critical determinants of a desired output with success is the underlying those long-term long-lasting results. process behind the objectives and creation of one’s This process is commonly move forward investment portfolio. used in the creation in a disciplined, Utilizing a disciplined, of components for time-tested approach to transportation equipment, deliberate portfolio construction like planes, trains, and manner toward (much like the process automobiles — where the those goals. of forging) can deliver a strength and precision of portfolio that is strong, the individual components enduring, and appropriately are critical for an enduring molded to each individual’s tolerance for lifespan of the end product. Unfortunately, risk and long-term goals and objectives. today’s investment landscape cannot be so easily manipulated to achieve a What specifically the coming year may hold desired outcome. for investors remains to be seen. There are many questions left unanswered, as is A less literal interpretation of the term is always the case in a dynamic world.

There often associated with moving forward, or is no formula that can be used to divine making strong, steady progress toward the future for the economy or the capital a goal. In this sense, we believe that it is markets. The key is to approach it with very apropos to the topic at hand.

Most investors have a number of goals, with most a well-conceived plan and maintain the discipline and patience needed to stick to being long term in nature. In that context, that plan through turmoil, euphoria, and “forging ahead” suggests that one stay anything in between. focused on those long-term objectives and move forward in a disciplined, deliberate Armed with those, we believe that investors manner toward those goals. are well positioned to reach their goals and achieve success as they travel along the The daily inflow of news can, at times, road ahead. materially influence the mood of investors and the near-term direction of the capital • First, it strengthens the metal significantly by sealing cracks, minimizing impurities, and improving its overall integrity. . Contributing authors Jim Baird, CPA, CFP®, CIMA® Chief Investment Officer Eric Dahlberg Senior Equity Analyst Erin Goss, CFA, CAIASM, CIMA®, CFS® Senior Alternative Investment Analyst James Minutolo, JD Senior Tax Manager Tricia Newcomb, CIMA® Senior Strategy Analyst Paul Olmsted Senior Fixed Income Analyst Ed Rumler, CFA® Alternative Investments Analyst Contact us at: wealth.plantemoran.com Investment Management Consultants Association (IMCA®) is the owner of the certification marks “CIMA®,” and “Certified Investment Management Analyst ®.” Use of CIMA® or Certified Investment Management Analyst ® signifies that the user has successfully completed IMCA’s initial and ongoing credentialing requirements for investment management consultants. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The CAIA Association® may grant the right to use the CAIASM Marks to those individuals who have been granted the status of either “Full Member” or “Retired Member” by the CAIA Association®.

The Institute of Business and Finance owns the certification marks CFS® and Certified Fund Specialist ®, which it awards to individuals who successfully complete its initial and ongoing certification requirements. Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain. Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness.

Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation. Investment recommendations provided herein are subject to change at any time.

Those recommendations provided herein are provided for informational purposes only and are not provided as a recommendation to buy or sell any one security or allocate to any asset class. Past and current recommendations that are profitable are not indicative of future results, which may in fact result in a loss. Please contact PMFA if you are interested in receiving a list of all past specific investment recommendations for the preceding 12 months. .

wealth.plantemoran.com .