It may not feel urgent, but it is: A timeline for implementing the new revenue recognition standard - January 11, 2016

Plante Moran Financial Advisors

Description

Recognizing

IT MAY NOT FEEL URGENT, BUT IT IS:

A timeline for implementing the new revenue recognition standard

. 2

RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD

. Recognizing

revenue

It may not feel urgent,

but it is:

A TIMELINE FOR IMPLEMENTING THE NEW

REVENUE RECOGNITION STANDARD

Look, we’re accountants. We understand “last minute.” We know our

clients count on us to make sense out of last year’s tax receipts or journal

entries in short order, often in the face of tight deadlines. And we take

pride in meeting and often exceeding your high expectations when it

comes to delivering quality work in a timely manner.

So we hope you’ll consider the source when we tell you that there’s an

accounting deadline approaching and we’re becoming concerned that

affected entities have not done enough to begin preparations for this

significant change. The new standard that governs the recognition of

revenue from contracts with customers is currently scheduled to become

effective for public company financial statements in 2018 and all other

entities in 2019.

It’s easy to dismiss this deadline as “years away,” but the work needed to prepare for this change is quite possibly unlike any accounting project your organization has undertaken before. 1 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . Readiness in the marketplace We’ve discussed readiness for this change with our clients. We also watch reports in the financial press for surveys from other sources. Since the new standard was issued, the number of organizations stating that they have not yet begun work on implementation is alarmingly high. The fact is, the amount of time and effort necessary to successfully implement the new standard will vary widely based on the individual circumstances of each affected entity. While some are hopeful that the number and complexity of questions yet to be answered may cause the FASB to once again delay the effective date, no organization should be counting on such a delay as part of the timeline for its implementation strategy.

This is not like a tax deadline, where you can count on being granted an automatic extension. The timeline and, more importantly, what should be happening now In a [previous article], we published a suggested timeline for organizations that need to implement the new revenue recognition standard. For 2015, the goals were fairly modest. Management needed to assemble the team that will lead the implementation process for the organization.

So if you haven’t paid attention yet, you should be able to catch up without too much difficulty. It’s important for the implementation team to include members from management, accounting and finance, information technology (IT), human resources, and the sales and operations side of the business. The sales and operations members are critical to making sure that the rest of the team understands how contracts function where the rubber meets the road. Does the business really have a few standard contracts, or does each contract start with a standard template that is modified based on specific negotiations with each client? The accounting and finance members need to understand how each type of contract will be treated under the new standard and identify issues that might lead to possible changes in processes, controls, information systems, or even future contracts.

The IT specialists will be instrumental in making the necessary changes to processes, systems, and controls. Management representatives need to understand what the team is doing, report back to leadership on progress, and raise relevant questions for resolution. For some 2 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

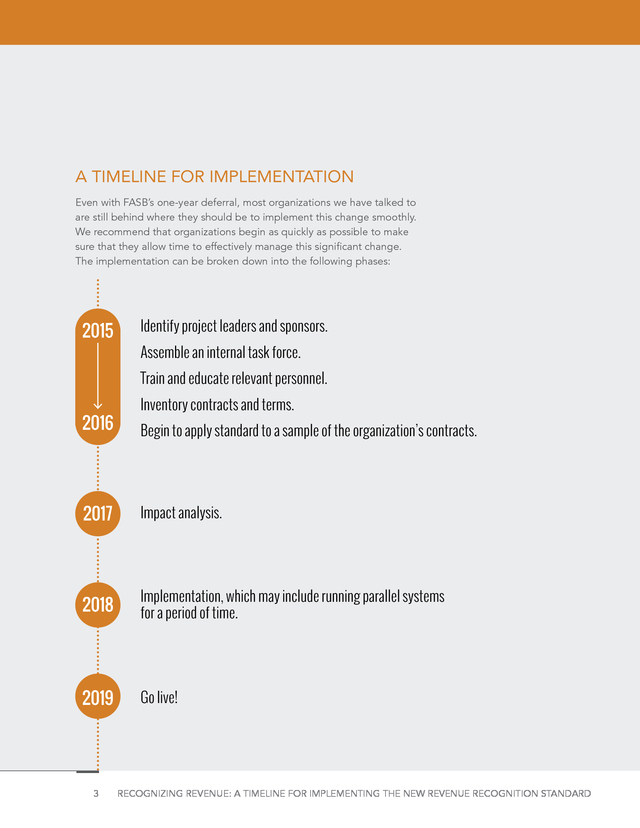

A TIMELINE FOR IMPLEMENTATION Even with FASB’s one-year deferral, most organizations we have talked to are still behind where they should be to implement this change smoothly. We recommend that organizations begin as quickly as possible to make sure that they allow time to effectively manage this significant change. The implementation can be broken down into the following phases: 2015 Identify project leaders and sponsors. Assemble an internal task force. Train and educate relevant personnel. 2016 Inventory contracts and terms. Begin to apply standard to a sample of the organization’s contracts. 2017 Impact analysis. 2018 Implementation, which may include running parallel systems for a period of time. 2019 Go live! 3 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . 5 STEPS FOR EVERY CONTRACT We recommend that you review each individual customer contract on its own merits to determine how to appropriately recognize revenue under the new standard. The analysis is a five-step process: 4 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . organizations, the implementation team may also need to include representatives from human resources, tax, and legal to the extent the changes affect compensation arrangements, tax filings, or other contracts. 2016, however, is a pivotal year for implementation. Team leaders and their groups need to learn about the new rules and begin training relevant personnel. There is already a fair amount of guidance on this topic and more is expected throughout the year ahead. As entities begin to understand the new guidance, more and more of them ask new questions of the standard-setters that lead to additional guidance and interpretations on the new rules.

The team needs to stay current on this information in order to lead the organization through the process. Plante Moran has created a [step-by-step] guide to support your implementation team as it leads this change. It’s a valuable resource for moving your organization through the process and for identifying where your contracts might raise issues that should be discussed with us. Keep in mind that it’s new ground for most entities and it’s not unusual to come across questions specific to your unique circumstances that won’t be covered in previous guidance. Inventory your contracts With your team up and running, a critical early step in the process is to create an inventory of all contracts between your organization and your customers.

The inventory needs to include specific details, such as payment terms and obligations. As noted above, this is a key point in the process to rely on people with experience in the specific contracts your organization has with each customer. We have already seen several instances where management and the accounting department think the firm operates on one standard form contract with every customer, but those who negotiate the deals with customers explain that almost every contract includes modifications unique to each relationship.

In terms of timeline, we’re still talking about work that needs to be done before the end of 2016. In fact, this work needs to be done early enough in the year to allow for some initial tests of how the new guidance affects the recognition of revenue from these agreements. While every step in the process is important, the success of the implementation depends on the foundation created with the contract inventory. Even 5 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

if you perform the rest of the steps correctly, there is the potential that the revenue recognized will be incorrect if not all contracts are analyzed. Apply the standard to a sample of contracts Once you have completed the contract inventory, you need to select a sample of representative agreements to begin understanding how each contract fits within the new rules. Perform the 5-step analysis described in the FASB guidance for each of these contracts. Identify each specific performance obligation and the total transaction price. Allocate the transaction price to each specific performance obligation, then determine the revenue that should be recognized for that obligation as it is satisfied. Look for the similarities and differences between recognition processes under the old guidance and the new guidance.

As you study the effect of the new rules on this group of contracts, consider how your business processes might need to change in order to gather contract data that you may not have needed before now. If your revenue contracts are based off of a handful of basic agreements that undergo slight modifications for each customer, look for standard provisions that can be modified to help you manage revenue recognition more effectively. Impact analysis 2017 is the year for figuring out how things will look when the new standard goes live, and for modifying contracts and accounting processes if necessary to make sure that your financial statements continue to present an accurate picture of your operations. This process involves looking back at the work done in 2016 and projecting the effect of each contract’s revenue recognition forward onto the income statement.

In some cases, the contracts you enter today will be the ones you are evaluating in 2016 and 2017. If it turns out that your organization’s contracts contain provisions that have a negative impact on revenue recognition, 2017 and 2018 will be the time to redraft your customer agreements and make sure that your organization is fully prepared for implementation in 2018 (if you are a public entity) or 2019. 6 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . Implementation If you’ve done the groundwork in 2016 and 2017, you should be ready for a smooth implementation of the new standard. Depending on the transition guidance you use, you may actually run parallel systems in the year prior to implementation. After 2018, the training wheels come off and the standard should be fully implemented. Your results may vary The timeline that we describe in this article could vary widely from entity to entity. This chart shows some of the factors that will affect the complexity of the implementation for different companies. WHEN IS THE RIGHT TIME TO START? More Time Needed to Implement Less Time Needed to Implement Number and Diversity of Contracts and/or Revenue Streams More and diverse contracts and/or revenue streams Fewer and less diverse contracts and/or revenue streams Complexity of Contracts More complex customer contracts Less complex customer contracts Availability of Data Data not currently available, or will require significant effort to compile Data currently available, or will not require significant effort to compile Processes and Systems Significant changes to processes and systems needed to implement No significant changes to processes and systems necessary Resource Availability Outside resources needed to implement Internal resources will have capacity to handle implementation 7 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

Unfortunately, the only way to know for certain how long it will take your organization to implement the new standard is to implement the new standard. If the organization needs to provide its financial statements to outside parties, it’s critical to stay ahead of the timeline as much as possible. With so much complexity involved in the analysis and so many questions still to be answered, organizations need to remember the advice of Yogi Berra, who warned that, “It gets late early out here.” If you have any questions about the new standard or if you need assistance with the implementation process, please contact your Plante Moran engagement team or a member of our revenue recognition implementation team. 8 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . 9 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . PLANTE MORAN 27400 Northwestern Highway Southfield, MI 48034 Are you on track for implementation? Assess your progress by taking our quick survey: revrecsurvey.plantemoran.com Check back for more article resources: • 2016: The Impact on Taxes .

It’s easy to dismiss this deadline as “years away,” but the work needed to prepare for this change is quite possibly unlike any accounting project your organization has undertaken before. 1 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . Readiness in the marketplace We’ve discussed readiness for this change with our clients. We also watch reports in the financial press for surveys from other sources. Since the new standard was issued, the number of organizations stating that they have not yet begun work on implementation is alarmingly high. The fact is, the amount of time and effort necessary to successfully implement the new standard will vary widely based on the individual circumstances of each affected entity. While some are hopeful that the number and complexity of questions yet to be answered may cause the FASB to once again delay the effective date, no organization should be counting on such a delay as part of the timeline for its implementation strategy.

This is not like a tax deadline, where you can count on being granted an automatic extension. The timeline and, more importantly, what should be happening now In a [previous article], we published a suggested timeline for organizations that need to implement the new revenue recognition standard. For 2015, the goals were fairly modest. Management needed to assemble the team that will lead the implementation process for the organization.

So if you haven’t paid attention yet, you should be able to catch up without too much difficulty. It’s important for the implementation team to include members from management, accounting and finance, information technology (IT), human resources, and the sales and operations side of the business. The sales and operations members are critical to making sure that the rest of the team understands how contracts function where the rubber meets the road. Does the business really have a few standard contracts, or does each contract start with a standard template that is modified based on specific negotiations with each client? The accounting and finance members need to understand how each type of contract will be treated under the new standard and identify issues that might lead to possible changes in processes, controls, information systems, or even future contracts.

The IT specialists will be instrumental in making the necessary changes to processes, systems, and controls. Management representatives need to understand what the team is doing, report back to leadership on progress, and raise relevant questions for resolution. For some 2 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

A TIMELINE FOR IMPLEMENTATION Even with FASB’s one-year deferral, most organizations we have talked to are still behind where they should be to implement this change smoothly. We recommend that organizations begin as quickly as possible to make sure that they allow time to effectively manage this significant change. The implementation can be broken down into the following phases: 2015 Identify project leaders and sponsors. Assemble an internal task force. Train and educate relevant personnel. 2016 Inventory contracts and terms. Begin to apply standard to a sample of the organization’s contracts. 2017 Impact analysis. 2018 Implementation, which may include running parallel systems for a period of time. 2019 Go live! 3 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . 5 STEPS FOR EVERY CONTRACT We recommend that you review each individual customer contract on its own merits to determine how to appropriately recognize revenue under the new standard. The analysis is a five-step process: 4 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . organizations, the implementation team may also need to include representatives from human resources, tax, and legal to the extent the changes affect compensation arrangements, tax filings, or other contracts. 2016, however, is a pivotal year for implementation. Team leaders and their groups need to learn about the new rules and begin training relevant personnel. There is already a fair amount of guidance on this topic and more is expected throughout the year ahead. As entities begin to understand the new guidance, more and more of them ask new questions of the standard-setters that lead to additional guidance and interpretations on the new rules.

The team needs to stay current on this information in order to lead the organization through the process. Plante Moran has created a [step-by-step] guide to support your implementation team as it leads this change. It’s a valuable resource for moving your organization through the process and for identifying where your contracts might raise issues that should be discussed with us. Keep in mind that it’s new ground for most entities and it’s not unusual to come across questions specific to your unique circumstances that won’t be covered in previous guidance. Inventory your contracts With your team up and running, a critical early step in the process is to create an inventory of all contracts between your organization and your customers.

The inventory needs to include specific details, such as payment terms and obligations. As noted above, this is a key point in the process to rely on people with experience in the specific contracts your organization has with each customer. We have already seen several instances where management and the accounting department think the firm operates on one standard form contract with every customer, but those who negotiate the deals with customers explain that almost every contract includes modifications unique to each relationship.

In terms of timeline, we’re still talking about work that needs to be done before the end of 2016. In fact, this work needs to be done early enough in the year to allow for some initial tests of how the new guidance affects the recognition of revenue from these agreements. While every step in the process is important, the success of the implementation depends on the foundation created with the contract inventory. Even 5 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

if you perform the rest of the steps correctly, there is the potential that the revenue recognized will be incorrect if not all contracts are analyzed. Apply the standard to a sample of contracts Once you have completed the contract inventory, you need to select a sample of representative agreements to begin understanding how each contract fits within the new rules. Perform the 5-step analysis described in the FASB guidance for each of these contracts. Identify each specific performance obligation and the total transaction price. Allocate the transaction price to each specific performance obligation, then determine the revenue that should be recognized for that obligation as it is satisfied. Look for the similarities and differences between recognition processes under the old guidance and the new guidance.

As you study the effect of the new rules on this group of contracts, consider how your business processes might need to change in order to gather contract data that you may not have needed before now. If your revenue contracts are based off of a handful of basic agreements that undergo slight modifications for each customer, look for standard provisions that can be modified to help you manage revenue recognition more effectively. Impact analysis 2017 is the year for figuring out how things will look when the new standard goes live, and for modifying contracts and accounting processes if necessary to make sure that your financial statements continue to present an accurate picture of your operations. This process involves looking back at the work done in 2016 and projecting the effect of each contract’s revenue recognition forward onto the income statement.

In some cases, the contracts you enter today will be the ones you are evaluating in 2016 and 2017. If it turns out that your organization’s contracts contain provisions that have a negative impact on revenue recognition, 2017 and 2018 will be the time to redraft your customer agreements and make sure that your organization is fully prepared for implementation in 2018 (if you are a public entity) or 2019. 6 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . Implementation If you’ve done the groundwork in 2016 and 2017, you should be ready for a smooth implementation of the new standard. Depending on the transition guidance you use, you may actually run parallel systems in the year prior to implementation. After 2018, the training wheels come off and the standard should be fully implemented. Your results may vary The timeline that we describe in this article could vary widely from entity to entity. This chart shows some of the factors that will affect the complexity of the implementation for different companies. WHEN IS THE RIGHT TIME TO START? More Time Needed to Implement Less Time Needed to Implement Number and Diversity of Contracts and/or Revenue Streams More and diverse contracts and/or revenue streams Fewer and less diverse contracts and/or revenue streams Complexity of Contracts More complex customer contracts Less complex customer contracts Availability of Data Data not currently available, or will require significant effort to compile Data currently available, or will not require significant effort to compile Processes and Systems Significant changes to processes and systems needed to implement No significant changes to processes and systems necessary Resource Availability Outside resources needed to implement Internal resources will have capacity to handle implementation 7 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD .

Unfortunately, the only way to know for certain how long it will take your organization to implement the new standard is to implement the new standard. If the organization needs to provide its financial statements to outside parties, it’s critical to stay ahead of the timeline as much as possible. With so much complexity involved in the analysis and so many questions still to be answered, organizations need to remember the advice of Yogi Berra, who warned that, “It gets late early out here.” If you have any questions about the new standard or if you need assistance with the implementation process, please contact your Plante Moran engagement team or a member of our revenue recognition implementation team. 8 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . 9 RECOGNIZING REVENUE: A TIMELINE FOR IMPLEMENTING THE NEW REVENUE RECOGNITION STANDARD . PLANTE MORAN 27400 Northwestern Highway Southfield, MI 48034 Are you on track for implementation? Assess your progress by taking our quick survey: revrecsurvey.plantemoran.com Check back for more article resources: • 2016: The Impact on Taxes .