FY 2016 Federal Tax proposed budget or 2016 FY budget proposals or Obama tax plan - February 4, 2015

Plante Moran Financial Advisors

Description

February 4, 2015

taxalerts.plantemoran.com

Fiscal Year (FY) 2016 Budget Proposals

Administration’s FY 2016 Budget: Compromise/Tax Reform Next Steps

President Obama released his $3.99 trillion fiscal year (FY 2016) federal budget proposals on February 2, 2015,

calling for expansion of tax incentives for families, consolidation of education tax breaks, creation of new retirement

savings opportunities, and tax increases for higher-income taxpayers. The President’s proposals did not leave out

businesses. As in past years, the President signaled his support for a reduction in the corporate tax rate but only if

businesses agree to base broadening measures. The President also proposed a new tax regime on foreign

earnings, a permanent research tax credit, repeal of the last-in, first-out (LIFO) method of accounting, permanently

enhanced Code Sec.

179 expensing, and much more. The IRS, which has had its budget cut in recent years, would receive nearly $2 billion more in funding for FY 2016. IMPACT. President Obama’s FY 2016 Budget immediately made headlines as containing some room for deal making and compromise.

Both the White House and the Republican-controlled Congress have admitted over the last few months that the only way legislation will get approved and signed is through compromise. While the Administration’s Budget remains aimed at gaining populist support by calling for middle-class relief and higher-income taxpayers paying their fair share, it also looks to compromise with Republicans through using tax revenues for infrastructure and defense spending, as well as provisions that work toward corporate tax reform, a permanent research credit, and other business-friendly measures. Tax Reform. Both the President and Congressional Republicans have been fairly tight-lipped about specifics of tax reform but both sides have indicated a willingness to engage in serious discussions this year. President Obama and other administration officials alluded to behind the scenes talks with Congressional Republicans about tax reform.

In May, the Senate Finance Committee is expected to announce the results of a study of tax reform and the results could reflect a bipartisan path to tax reform. Many Capitol Hill observers predict that initial momentum for tax reform will come from the Senate. Senate Majority Leader Mitch McConnell, R-Ky., and Vice President Joe Biden have successfully brokered tax deals in the past. COMMENT.

Just like 2014, this year is again shaping up to be a battle over the tax extenders. The Tax Increase Prevention Act of 2014 only extended the extenders through 2014, leaving their fate to the 114th Congress. The extenders could be bargaining chips in negotiations over comprehensive tax reform. .

INDIVIDUAL REFORMS President Obama’s FY 2016 reforms for individuals are a mix of old and new proposals. Some provisions are grounds for compromise. Capital Gains Tax Rates The President proposed increasing the top long-term capital gains and qualified dividends tax rate from 20 percent to 24.2 percent for tax years beginning after December 31, 2015. IMPACT. Including the 3.8-percent tax on net investment income (NII), this proposal would increase the top effective long-term capital gains and qualified dividends tax rate to 28 percent. In perhaps a way out for some Republicans to support this increase, the White House stressed that 28 percent had been the capital gains rate under the Reagan Administration. Child and Dependent Care Credit The maximum child and dependent care credit for families with children under age five would increase to $3,000 per child.

The full, regular credit for the care of children under age 13 would be available to qualified taxpayers with incomes of up to $120,000. IMPACT. Child and dependent care credits that enable parents and other care-givers to work would effectively triple for many and also become available to a wider income band. The reduced portion of the credit would completely phase out only when income exceeded $178,000.

In return, however, the President proposed ending flexible spending accounts for dependent care. Second Earner Credit President Obama proposed a new “second earner” tax credit of up to $500 for qualified couples where both spouses work. IMPACT. Aimed principally at the middle income families, the full credit would start to be phased out at adjusted gross income (AGI) over $120,000, with complete phaseout reached at the $210,000 AGI level. Higher Income Taxpayers President Obama proposed to limit the value of itemized deductions and other tax preferences to 28 percent for certain higher income taxpayers. The President also renewed his “Buffett Rule” proposal of taxing higher-income taxpayers with large deductions and other tax preferences at a minimum 30-percent tax rate. IMPACT.

The President also used a “paying their fair share” theme to propose raising the top capital gain rate to 28 percent and recognizing taxable gain on the transfer of appreciated assets via gifts or inheritance (discussed below). EIC/Child Tax Credit Temporary enhancements to the earned income credit (EIC) and child tax credit, scheduled to expire after 2017, would be made permanent. Education Under the President’s plan, the American Opportunity Tax Credit (AOTC) would be made permanent and would be consolidated with other education incentives. IMPACT. The maximum refundable AOTC would be increased, and the AOTC would be available for five years as well as extended to part-time students. COMMENT. The President’s budget would repeal or let expire the Lifetime Learning Credit, the higher education tuition deduction, the student loan interest deduction (for new borrowers), and Coverdell Education Savings Accounts (for new contributions).

The President, however, backed down on his recent 2 . attempt to return to the pre-2001 taxation of 529 plans (i.e. no exclusion for withdrawals for educational purposes). Estate and Gift Planning The President’s budget would generally treat bequests and gifts of appreciated property above certain threshold amounts as realization events that would trigger tax liability for capital gains. Only then would an heir receive a “stepped-up basis.” Generally, a $100,000-exemption per person would exist, along with exceptions for surviving spouses, small businesses, charities, and residences, among others. IMPACT. The White House characterized this existing “stepped-up basis regime” as one of the largest existing loopholes left to be plugged. The President also renewed his proposal to reinstate the 2009 estate and gift tax rates and exclusions.

That benchmark calls for a top rate of 45 percent and an exclusion of $3.5 million for estates and $1 million for lifetime gifts. COMMENT. In contrast, some Republicans have called for complete elimination of the estate and gift tax. BUSINESS REFORMS Most business tax proposals are reiterated from past-year budget proposals. Many continue to have the support of Republican members of Congress and are seen as the area in which negotiations and compromise might be most easily jump-started. Corporate Tax Rate The President’s budget would reduce the corporate tax rate to 28 percent, with a 25 percent effective rate for domestic manufacturing.

The rate reduction would be offset, in part, by eliminating fossil fuel tax breaks and other unspecified business tax incentives to “broaden the tax base.” IMPACT. Previous statements by the White House and Congressional GOP leaders have indicated some common ground on reducing the corporate tax rate but show disagreement over how to pay for any reduction. Although President Obama’s proposal is not brand new, renewed interest in the corporate tax area as a starting point for “tax reform” is becoming more evident. Code Sec.

179 Expensing The President called for a $500,000 dollar limit and $2 million investment limit for 2015. For 2016, the dollar limit would be $1 million and the investment limit would be $2 million. These amounts would be indexed for inflation after 2016. COMMENT.

Congress extended the enhanced levels for 2014 only. Current levels without any “extenders legislation” are set at a $25,000 dollar limit, with a $200,000 investment level. With support for higher expensing on both sides of the aisle as a way for small businesses to avoid otherwise complex depreciation rules as well as cash-flow issues, consensus is that the existing 2015 levels will be increased as well. COMMENT.

President Obama did not propose to extend bonus depreciation, which expired after 2014 (after 2015 for certain longer-lived and transportation property). Small Business Stock The President renewed his proposal to permanently extend the 100-percent exclusion from tax by a non-corporate taxpayer for capital gains realized on the sale of qualified small business stock held for more than five-years. IMPACT. The proposal would apply to qualified stock issued after September 27, 2010 and held for more than five years. The amount of gain eligible for exclusion would be limited to the greater of $10 million or 10 times the taxpayer’s basis in the stock. 3 .

COMMENT. The proposal would create a new option that would extend the period for acquiring replacement stock to six months for stock held more than three years. Permanent Research Tax Credit The Tax Increase Prevention Act of 2014 extended the research tax credit through 2014. President Obama proposed to simplify the research credit and make it permanent. COMMENT. The research tax credit was identified as one key incentive to be made permanent in the failed House-Senate negotiations on the extenders legislations in November 2104.

As in past negotiations, the cost of a permanent credit emerged as one of the greatest stumbling blocks. Including a permanent provision in a tax package with a broader scope likely remains its best path to success. LIFO The President called for repeal of the last-in, first-out (LIFO) method of accounting. COMMENT. In 2014, the then chair of the House Ways and Means Committee, Dave Camp, R-Mich., included LIFO repeal in his comprehensive tax reform package. Expanded Code Sec.

45R Credit President Obama’s Budget calls for the expansion of the credit for small employers to provide health insurance to apply to up to 50 (rather than 25) full-time equivalent employees, with a phase out between 20-and-50 employees (rather than between 10 and 25). Financial Fees On Highly-Leveraged Banks President Obama’s FY 2016 Budget proposes the imposition of a tax on large banks and other financial institutions for highly leveraged activities. Large financial firms would pay a 7-basis point fee on their liabilities. IMPACT. This financial fee is designed to reduce the incentive for large financial institutions to leverage, therefore reducing the chances of default and any resulting costs to the federal government.

At a revenue gain of $111 billion, it is also expected to fund a portion of the middle-income tax relief within the President’s Budget. More Business Reforms Other business reforms include: ï‚· Permanent Work Opportunity Tax Credit ï‚· Permanent Production Tax Credit ï‚· Permanent Indian Employment Credit ï‚· New business credit for costs incurred with insourcing a U.S. business ï‚· Tax carried interest profits as ordinary income ï‚· Expanded use of the cash method of accounting for certain small businesses ï‚· Increased deduction for start-up expenses ï‚· Permanent New Markets Tax Credit ï‚· America Fast Forward Bonds and Qualified Public Infrastructure Bonds 4 . ï‚· Carbon Dioxide Investment and Sequestration Tax Credit ï‚· Reformed/Expanded Low-Income Housing Tax Credit (LIHTC) RETIREMENT REFORMS In the retirement area, President Obama called for increasing access to savings vehicles. Part-Time Employees The President’s budget would make employees who have worked for an employer at least 500 hours per year for at least three years eligible to participate in the employer’s existing retirement plan. COMMENT. Under the proposal, employers would not be required to offer matching contributions. Other retirement reforms include, among others: ï‚· Automatic enrollment in IRAs for workers without employer-sponsored retirement plans ï‚· Expanded tax breaks to assist employers setting up retirement savings plans. INTERNATIONAL REFORMS The President’s FY 2016 budget includes a number of international reforms. Among them is an attempt to build a hybrid territorial/worldwide system of international taxation. New for the FY 2016 budget is a mandatory two-part tax that would allow foreign profits to be repatriated into the U.S.: a one-time 14-percent tax and a 19-percent minimum tax going forward. One-Time Tax On Foreign Earnings President Obama called for a one-time 14-percent tax on earnings accumulated in controlled foreign corporations (CFCs) that have not previously been subject to U.S.

tax. Accumulated income could then be repatriated to the U.S. without further tax. IMPACT. Revenues from the one-time tax would be used for transportation and infrastructure spending, thus making these otherwise non-starter proposals possible trade offs for some members of Congress. COMMENT.

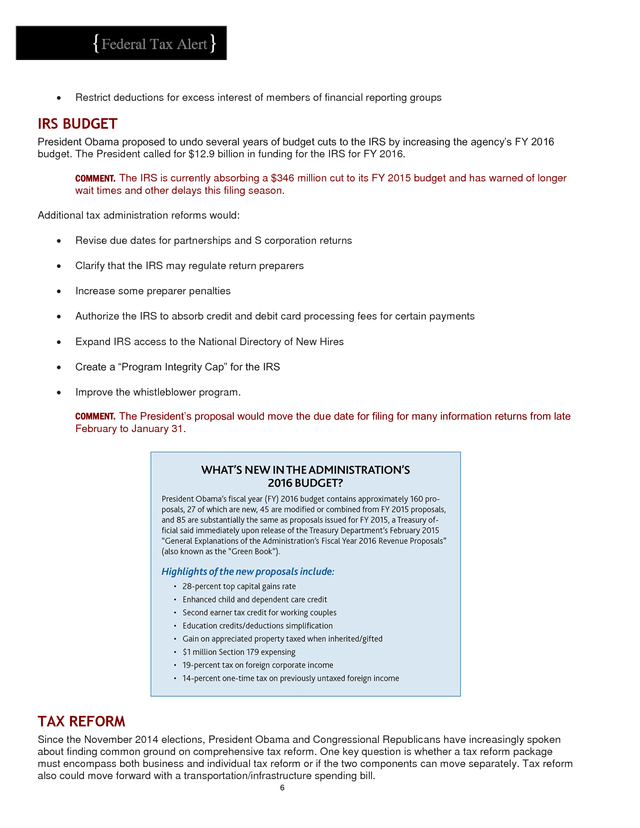

The one-time tax would apply to earnings accumulated for tax years beginning before January 1, 2016, and would be payable ratably over five years. Minimum Tax The President also proposed to impose a minimum tax on foreign income of U.S. multinationals at a rate of 19 percent reduced (but not below zero) by 85 percent of the effective foreign tax rate imposed on that income. More International Reforms Other international reforms would: ï‚· Remove tax deductions for outsourcing ï‚· Curb corporate inversions ï‚· Limit the shifting of income through intangible property transfers ï‚· Make revisions to Subpart F ï‚· Restrict the use of hybrid arrangements that create stateless income 5 . ï‚· Restrict deductions for excess interest of members of financial reporting groups IRS BUDGET President Obama proposed to undo several years of budget cuts to the IRS by increasing the agency’s FY 2016 budget. The President called for $12.9 billion in funding for the IRS for FY 2016. COMMENT. The IRS is currently absorbing a $346 million cut to its FY 2015 budget and has warned of longer wait times and other delays this filing season. Additional tax administration reforms would: ï‚· Revise due dates for partnerships and S corporation returns ï‚· Clarify that the IRS may regulate return preparers ï‚· Increase some preparer penalties ï‚· Authorize the IRS to absorb credit and debit card processing fees for certain payments ï‚· Expand IRS access to the National Directory of New Hires ï‚· Create a “Program Integrity Cap” for the IRS ï‚· Improve the whistleblower program. COMMENT. The President’s proposal would move the due date for filing for many information returns from late February to January 31. TAX REFORM Since the November 2014 elections, President Obama and Congressional Republicans have increasingly spoken about finding common ground on comprehensive tax reform.

One key question is whether a tax reform package must encompass both business and individual tax reform or if the two components can move separately. Tax reform also could move forward with a transportation/infrastructure spending bill. 6 . IMPACT. Both President Obama and Congressional Republicans have called for revenue neutral tax reform. Their definitions of revenue neutral often differ based on projections of economic growth and the impact of tax reform on the economy. House Republicans have approved the use of dynamic scoring for major bills and Senate Republicans may go along. The White House counters that dynamic scoring distorts the economic impact of tax cuts. COMMENT.

Comprehensive individual tax reform is likely not to be sorted out until after the 2016 Presidential Elections, although it likely will grow in visibility as candidates take sides and smaller tax bills are introduced this year. Business tax reform, on the other hand, remains more likely to take shape in 2015, especially on the corporate and international sides. President Obama’s Proposals President Obama has said that while he would prefer business tax reform be linked to individual tax reform, he is not adverse to starting with business tax reform first. The President has also not abandoned his 2012 Framework for Business Tax Reform.

That framework would reduce the corporate tax rate in exchange for the elimination of unspecified business tax breaks. The Framework also called for a minimum tax on foreign earnings. For individuals, President Obama wants to make permanent temporary enhancements to the earned income credit (EIC), consolidate and enhance education tax breaks, and boost the child and dependent care credit (discussed above). IMPACT.

President Obama has not, so far, discussed revisiting the individual income tax rates (although he has called for changes in the capital gains and dividends tax rates, discussed above). Many Congressional Republicans would like to see a roll back of the top 39.6 percent rate put in place in 2013. COMMENT. Some big-ticket proposals enjoy bipartisan support until lawmakers are reminded of the cost in lost revenues.

These include elimination of the alternative minimum tax (AMT), a permanent research tax credit, a permanent state and local sales tax deduction, and others. Congressional Republicans At this time, there is not a common Congressional GOP position on tax reform. The House Ways and Means Committee and the Senate Finance Committee (SFC) are expected to begin hearings on tax reform this spring. COMMENT. SFC Chair Orrin Hatch, R-Utah, has predicted that the committee can assemble a tax reform package by year-end 2015.

Hatch has not, however, predicted what would be in that package. Ways and Means Chair Paul Ryan, R-Wisc., has, so far, not made any predictions about the timing of a tax reform bill in his committee. COMMENT. Some Republicans in Congress have looked to the Tax Reform Bill of 2014, introduced by now retired Ways and Means Chair Dave Camp, R-Mich, as a blueprint for tax reform in 2015.

The 2014 bill would have eliminated a host of popular tax credits and deductions for both individuals and businesses in exchange for lower tax rates. Any attempt to eliminate popular tax breaks, such as the home mortgage interest deduction, bonus depreciation, and more, ultimately hit roadblocks from supporters. Congressional Democrats In January, a group of House Democrats unveiled a tax proposal. The proposal includes a Paycheck Bonus Tax Credit of $1,000 per worker per year, or $2,000 for a two-earner couple (subject to income thresholds), a Saver’s Bonus, and tax incentives for businesses that invest in apprenticeship or other training programs.

Costs would be offset by reducing tax incentives for higher-income earners and a new financial trading fee. AFFORDABLE CARE ACT With Republicans in control of both the House and Senate, opponents of the Affordable Care Act have been emboldened to move for repeal of the law. President Obama has said he will veto any legislation that rolls back the Affordable Care Act. Legislation, however, is not the only potential game-changer to the Affordable Care Act.

In June, the U.S. Supreme Court is expected to rule in a case dealing with the Code Sec. 36B premium assistance tax credit that could have major ramifications on the Affordable Care Act. 7 .

Employer Mandate The Affordable Care Act imposes new play or pay requirements on individuals who fail to carry minimum essential health coverage, unless exempt; and applicable large employers that do not offer health coverage or offer coverage that is deemed unaffordable. Several bills have been introduced in Congress to eliminate or scale back the employer mandate. Employer Mandate. In January, the House approved the Save American Workers Bill of 2015 (HR 30), which would generally revise the definition of full-time employment for the employer shared responsibility provisions from 30 hours per week to 40 hours per week. Similar legislation has been introduced in the Senate (Forty Hours is Full Time Bill (Sen 30)). COMMENT.

The Senate is expected to soon take up the Hire More Heroes Bill (HR 22), which would permit an employer to exclude employees who have coverage under a health care program administered by the Department of Defense, from the employer shared responsibility requirements of the Affordable Care Act. The bill passed the House in January. Medical Device Excise Tax The Affordable Care Act imposes a 2.3 percent excise tax on taxable medical devices. Legislation to repeal the excise tax has been introduced in Congress. COMMENT. There appears to be significant bipartisan support in both the House and Senate to repeal the medical device excise tax.

No votes, however, have yet been scheduled. MORE TAX BILLS A host of tax-related proposals have been introduced in the 114th Congress and have been referred to the House and Senate tax-writing committees. They include: ï‚· Child Tax Credit Integrity Preservation Act of 2015 (Sen 53) ï‚· Death Tax Repeal Act (HR 173) ï‚· Taxpayer Protection and Preparer Proficiency Act of 2015 (Sen 137) ï‚· Dependent Care Savings Account Act of 2015 (Sen 74) ï‚· Investment Savings Access After Catastrophes Act of 2015 (Sen 76) ï‚· Stop Targeting of Political Beliefs by the IRS Bill of 2015 (HR 599) ï‚· Fifth Amendment Integrity Restoration (FAIR) Bill (Sen 255) 8 . ï‚· Education Tax Fraud Prevention Act (Sen 75) ï‚· Fair Tax Act of 2015 (HR 25) ï‚· Tax Code Termination Act (HR 27) ï‚· Incentives to Educate American Children (Sen 138) ï‚· No Tax Write-Offs for Corporate Wrongdoers Act (Sen 169) ï‚· Fairness in Taxation Act of 2015 (HR 389) ï‚· Offshoring Prevention Act (HR 305) ï‚· Gas Tax Replacement Act of 2015 (HR 309) ï‚· Obamacare Opt-Out Act of 2015 (HR 420) ï‚· Wild Game Donation Act of 2015 (HR 461) If you have any questions regarding this alert, please contact your Plante Moran client services representative or one of the contacts listed below. Mike Monaghan National Tax Office 877.622.2257 ext. 64943 mike.monaghan@plantemoran.com Mark Jolley National Tax Office 877.622.2257 ext. 26923 mark.jolley@plantemoran.com George Riddering Firmwide Director of Tax 877.622.2257 ext. 34065 george.riddering@plantemoran.com The information provided in this alert is only a general summary and is being distributed with the understanding that Plante Moran is not rendering legal, tax, accounting, or other professional advice, position, or opinions on specific facts or matters and, accordingly, assumes no liability whatsoever in connection with its use. ©2015 CCH Incorporated.

All Rights Reserved 9 .

179 expensing, and much more. The IRS, which has had its budget cut in recent years, would receive nearly $2 billion more in funding for FY 2016. IMPACT. President Obama’s FY 2016 Budget immediately made headlines as containing some room for deal making and compromise.

Both the White House and the Republican-controlled Congress have admitted over the last few months that the only way legislation will get approved and signed is through compromise. While the Administration’s Budget remains aimed at gaining populist support by calling for middle-class relief and higher-income taxpayers paying their fair share, it also looks to compromise with Republicans through using tax revenues for infrastructure and defense spending, as well as provisions that work toward corporate tax reform, a permanent research credit, and other business-friendly measures. Tax Reform. Both the President and Congressional Republicans have been fairly tight-lipped about specifics of tax reform but both sides have indicated a willingness to engage in serious discussions this year. President Obama and other administration officials alluded to behind the scenes talks with Congressional Republicans about tax reform.

In May, the Senate Finance Committee is expected to announce the results of a study of tax reform and the results could reflect a bipartisan path to tax reform. Many Capitol Hill observers predict that initial momentum for tax reform will come from the Senate. Senate Majority Leader Mitch McConnell, R-Ky., and Vice President Joe Biden have successfully brokered tax deals in the past. COMMENT.

Just like 2014, this year is again shaping up to be a battle over the tax extenders. The Tax Increase Prevention Act of 2014 only extended the extenders through 2014, leaving their fate to the 114th Congress. The extenders could be bargaining chips in negotiations over comprehensive tax reform. .

INDIVIDUAL REFORMS President Obama’s FY 2016 reforms for individuals are a mix of old and new proposals. Some provisions are grounds for compromise. Capital Gains Tax Rates The President proposed increasing the top long-term capital gains and qualified dividends tax rate from 20 percent to 24.2 percent for tax years beginning after December 31, 2015. IMPACT. Including the 3.8-percent tax on net investment income (NII), this proposal would increase the top effective long-term capital gains and qualified dividends tax rate to 28 percent. In perhaps a way out for some Republicans to support this increase, the White House stressed that 28 percent had been the capital gains rate under the Reagan Administration. Child and Dependent Care Credit The maximum child and dependent care credit for families with children under age five would increase to $3,000 per child.

The full, regular credit for the care of children under age 13 would be available to qualified taxpayers with incomes of up to $120,000. IMPACT. Child and dependent care credits that enable parents and other care-givers to work would effectively triple for many and also become available to a wider income band. The reduced portion of the credit would completely phase out only when income exceeded $178,000.

In return, however, the President proposed ending flexible spending accounts for dependent care. Second Earner Credit President Obama proposed a new “second earner” tax credit of up to $500 for qualified couples where both spouses work. IMPACT. Aimed principally at the middle income families, the full credit would start to be phased out at adjusted gross income (AGI) over $120,000, with complete phaseout reached at the $210,000 AGI level. Higher Income Taxpayers President Obama proposed to limit the value of itemized deductions and other tax preferences to 28 percent for certain higher income taxpayers. The President also renewed his “Buffett Rule” proposal of taxing higher-income taxpayers with large deductions and other tax preferences at a minimum 30-percent tax rate. IMPACT.

The President also used a “paying their fair share” theme to propose raising the top capital gain rate to 28 percent and recognizing taxable gain on the transfer of appreciated assets via gifts or inheritance (discussed below). EIC/Child Tax Credit Temporary enhancements to the earned income credit (EIC) and child tax credit, scheduled to expire after 2017, would be made permanent. Education Under the President’s plan, the American Opportunity Tax Credit (AOTC) would be made permanent and would be consolidated with other education incentives. IMPACT. The maximum refundable AOTC would be increased, and the AOTC would be available for five years as well as extended to part-time students. COMMENT. The President’s budget would repeal or let expire the Lifetime Learning Credit, the higher education tuition deduction, the student loan interest deduction (for new borrowers), and Coverdell Education Savings Accounts (for new contributions).

The President, however, backed down on his recent 2 . attempt to return to the pre-2001 taxation of 529 plans (i.e. no exclusion for withdrawals for educational purposes). Estate and Gift Planning The President’s budget would generally treat bequests and gifts of appreciated property above certain threshold amounts as realization events that would trigger tax liability for capital gains. Only then would an heir receive a “stepped-up basis.” Generally, a $100,000-exemption per person would exist, along with exceptions for surviving spouses, small businesses, charities, and residences, among others. IMPACT. The White House characterized this existing “stepped-up basis regime” as one of the largest existing loopholes left to be plugged. The President also renewed his proposal to reinstate the 2009 estate and gift tax rates and exclusions.

That benchmark calls for a top rate of 45 percent and an exclusion of $3.5 million for estates and $1 million for lifetime gifts. COMMENT. In contrast, some Republicans have called for complete elimination of the estate and gift tax. BUSINESS REFORMS Most business tax proposals are reiterated from past-year budget proposals. Many continue to have the support of Republican members of Congress and are seen as the area in which negotiations and compromise might be most easily jump-started. Corporate Tax Rate The President’s budget would reduce the corporate tax rate to 28 percent, with a 25 percent effective rate for domestic manufacturing.

The rate reduction would be offset, in part, by eliminating fossil fuel tax breaks and other unspecified business tax incentives to “broaden the tax base.” IMPACT. Previous statements by the White House and Congressional GOP leaders have indicated some common ground on reducing the corporate tax rate but show disagreement over how to pay for any reduction. Although President Obama’s proposal is not brand new, renewed interest in the corporate tax area as a starting point for “tax reform” is becoming more evident. Code Sec.

179 Expensing The President called for a $500,000 dollar limit and $2 million investment limit for 2015. For 2016, the dollar limit would be $1 million and the investment limit would be $2 million. These amounts would be indexed for inflation after 2016. COMMENT.

Congress extended the enhanced levels for 2014 only. Current levels without any “extenders legislation” are set at a $25,000 dollar limit, with a $200,000 investment level. With support for higher expensing on both sides of the aisle as a way for small businesses to avoid otherwise complex depreciation rules as well as cash-flow issues, consensus is that the existing 2015 levels will be increased as well. COMMENT.

President Obama did not propose to extend bonus depreciation, which expired after 2014 (after 2015 for certain longer-lived and transportation property). Small Business Stock The President renewed his proposal to permanently extend the 100-percent exclusion from tax by a non-corporate taxpayer for capital gains realized on the sale of qualified small business stock held for more than five-years. IMPACT. The proposal would apply to qualified stock issued after September 27, 2010 and held for more than five years. The amount of gain eligible for exclusion would be limited to the greater of $10 million or 10 times the taxpayer’s basis in the stock. 3 .

COMMENT. The proposal would create a new option that would extend the period for acquiring replacement stock to six months for stock held more than three years. Permanent Research Tax Credit The Tax Increase Prevention Act of 2014 extended the research tax credit through 2014. President Obama proposed to simplify the research credit and make it permanent. COMMENT. The research tax credit was identified as one key incentive to be made permanent in the failed House-Senate negotiations on the extenders legislations in November 2104.

As in past negotiations, the cost of a permanent credit emerged as one of the greatest stumbling blocks. Including a permanent provision in a tax package with a broader scope likely remains its best path to success. LIFO The President called for repeal of the last-in, first-out (LIFO) method of accounting. COMMENT. In 2014, the then chair of the House Ways and Means Committee, Dave Camp, R-Mich., included LIFO repeal in his comprehensive tax reform package. Expanded Code Sec.

45R Credit President Obama’s Budget calls for the expansion of the credit for small employers to provide health insurance to apply to up to 50 (rather than 25) full-time equivalent employees, with a phase out between 20-and-50 employees (rather than between 10 and 25). Financial Fees On Highly-Leveraged Banks President Obama’s FY 2016 Budget proposes the imposition of a tax on large banks and other financial institutions for highly leveraged activities. Large financial firms would pay a 7-basis point fee on their liabilities. IMPACT. This financial fee is designed to reduce the incentive for large financial institutions to leverage, therefore reducing the chances of default and any resulting costs to the federal government.

At a revenue gain of $111 billion, it is also expected to fund a portion of the middle-income tax relief within the President’s Budget. More Business Reforms Other business reforms include: ï‚· Permanent Work Opportunity Tax Credit ï‚· Permanent Production Tax Credit ï‚· Permanent Indian Employment Credit ï‚· New business credit for costs incurred with insourcing a U.S. business ï‚· Tax carried interest profits as ordinary income ï‚· Expanded use of the cash method of accounting for certain small businesses ï‚· Increased deduction for start-up expenses ï‚· Permanent New Markets Tax Credit ï‚· America Fast Forward Bonds and Qualified Public Infrastructure Bonds 4 . ï‚· Carbon Dioxide Investment and Sequestration Tax Credit ï‚· Reformed/Expanded Low-Income Housing Tax Credit (LIHTC) RETIREMENT REFORMS In the retirement area, President Obama called for increasing access to savings vehicles. Part-Time Employees The President’s budget would make employees who have worked for an employer at least 500 hours per year for at least three years eligible to participate in the employer’s existing retirement plan. COMMENT. Under the proposal, employers would not be required to offer matching contributions. Other retirement reforms include, among others: ï‚· Automatic enrollment in IRAs for workers without employer-sponsored retirement plans ï‚· Expanded tax breaks to assist employers setting up retirement savings plans. INTERNATIONAL REFORMS The President’s FY 2016 budget includes a number of international reforms. Among them is an attempt to build a hybrid territorial/worldwide system of international taxation. New for the FY 2016 budget is a mandatory two-part tax that would allow foreign profits to be repatriated into the U.S.: a one-time 14-percent tax and a 19-percent minimum tax going forward. One-Time Tax On Foreign Earnings President Obama called for a one-time 14-percent tax on earnings accumulated in controlled foreign corporations (CFCs) that have not previously been subject to U.S.

tax. Accumulated income could then be repatriated to the U.S. without further tax. IMPACT. Revenues from the one-time tax would be used for transportation and infrastructure spending, thus making these otherwise non-starter proposals possible trade offs for some members of Congress. COMMENT.

The one-time tax would apply to earnings accumulated for tax years beginning before January 1, 2016, and would be payable ratably over five years. Minimum Tax The President also proposed to impose a minimum tax on foreign income of U.S. multinationals at a rate of 19 percent reduced (but not below zero) by 85 percent of the effective foreign tax rate imposed on that income. More International Reforms Other international reforms would: ï‚· Remove tax deductions for outsourcing ï‚· Curb corporate inversions ï‚· Limit the shifting of income through intangible property transfers ï‚· Make revisions to Subpart F ï‚· Restrict the use of hybrid arrangements that create stateless income 5 . ï‚· Restrict deductions for excess interest of members of financial reporting groups IRS BUDGET President Obama proposed to undo several years of budget cuts to the IRS by increasing the agency’s FY 2016 budget. The President called for $12.9 billion in funding for the IRS for FY 2016. COMMENT. The IRS is currently absorbing a $346 million cut to its FY 2015 budget and has warned of longer wait times and other delays this filing season. Additional tax administration reforms would: ï‚· Revise due dates for partnerships and S corporation returns ï‚· Clarify that the IRS may regulate return preparers ï‚· Increase some preparer penalties ï‚· Authorize the IRS to absorb credit and debit card processing fees for certain payments ï‚· Expand IRS access to the National Directory of New Hires ï‚· Create a “Program Integrity Cap” for the IRS ï‚· Improve the whistleblower program. COMMENT. The President’s proposal would move the due date for filing for many information returns from late February to January 31. TAX REFORM Since the November 2014 elections, President Obama and Congressional Republicans have increasingly spoken about finding common ground on comprehensive tax reform.

One key question is whether a tax reform package must encompass both business and individual tax reform or if the two components can move separately. Tax reform also could move forward with a transportation/infrastructure spending bill. 6 . IMPACT. Both President Obama and Congressional Republicans have called for revenue neutral tax reform. Their definitions of revenue neutral often differ based on projections of economic growth and the impact of tax reform on the economy. House Republicans have approved the use of dynamic scoring for major bills and Senate Republicans may go along. The White House counters that dynamic scoring distorts the economic impact of tax cuts. COMMENT.

Comprehensive individual tax reform is likely not to be sorted out until after the 2016 Presidential Elections, although it likely will grow in visibility as candidates take sides and smaller tax bills are introduced this year. Business tax reform, on the other hand, remains more likely to take shape in 2015, especially on the corporate and international sides. President Obama’s Proposals President Obama has said that while he would prefer business tax reform be linked to individual tax reform, he is not adverse to starting with business tax reform first. The President has also not abandoned his 2012 Framework for Business Tax Reform.

That framework would reduce the corporate tax rate in exchange for the elimination of unspecified business tax breaks. The Framework also called for a minimum tax on foreign earnings. For individuals, President Obama wants to make permanent temporary enhancements to the earned income credit (EIC), consolidate and enhance education tax breaks, and boost the child and dependent care credit (discussed above). IMPACT.

President Obama has not, so far, discussed revisiting the individual income tax rates (although he has called for changes in the capital gains and dividends tax rates, discussed above). Many Congressional Republicans would like to see a roll back of the top 39.6 percent rate put in place in 2013. COMMENT. Some big-ticket proposals enjoy bipartisan support until lawmakers are reminded of the cost in lost revenues.

These include elimination of the alternative minimum tax (AMT), a permanent research tax credit, a permanent state and local sales tax deduction, and others. Congressional Republicans At this time, there is not a common Congressional GOP position on tax reform. The House Ways and Means Committee and the Senate Finance Committee (SFC) are expected to begin hearings on tax reform this spring. COMMENT. SFC Chair Orrin Hatch, R-Utah, has predicted that the committee can assemble a tax reform package by year-end 2015.

Hatch has not, however, predicted what would be in that package. Ways and Means Chair Paul Ryan, R-Wisc., has, so far, not made any predictions about the timing of a tax reform bill in his committee. COMMENT. Some Republicans in Congress have looked to the Tax Reform Bill of 2014, introduced by now retired Ways and Means Chair Dave Camp, R-Mich, as a blueprint for tax reform in 2015.

The 2014 bill would have eliminated a host of popular tax credits and deductions for both individuals and businesses in exchange for lower tax rates. Any attempt to eliminate popular tax breaks, such as the home mortgage interest deduction, bonus depreciation, and more, ultimately hit roadblocks from supporters. Congressional Democrats In January, a group of House Democrats unveiled a tax proposal. The proposal includes a Paycheck Bonus Tax Credit of $1,000 per worker per year, or $2,000 for a two-earner couple (subject to income thresholds), a Saver’s Bonus, and tax incentives for businesses that invest in apprenticeship or other training programs.

Costs would be offset by reducing tax incentives for higher-income earners and a new financial trading fee. AFFORDABLE CARE ACT With Republicans in control of both the House and Senate, opponents of the Affordable Care Act have been emboldened to move for repeal of the law. President Obama has said he will veto any legislation that rolls back the Affordable Care Act. Legislation, however, is not the only potential game-changer to the Affordable Care Act.

In June, the U.S. Supreme Court is expected to rule in a case dealing with the Code Sec. 36B premium assistance tax credit that could have major ramifications on the Affordable Care Act. 7 .

Employer Mandate The Affordable Care Act imposes new play or pay requirements on individuals who fail to carry minimum essential health coverage, unless exempt; and applicable large employers that do not offer health coverage or offer coverage that is deemed unaffordable. Several bills have been introduced in Congress to eliminate or scale back the employer mandate. Employer Mandate. In January, the House approved the Save American Workers Bill of 2015 (HR 30), which would generally revise the definition of full-time employment for the employer shared responsibility provisions from 30 hours per week to 40 hours per week. Similar legislation has been introduced in the Senate (Forty Hours is Full Time Bill (Sen 30)). COMMENT.

The Senate is expected to soon take up the Hire More Heroes Bill (HR 22), which would permit an employer to exclude employees who have coverage under a health care program administered by the Department of Defense, from the employer shared responsibility requirements of the Affordable Care Act. The bill passed the House in January. Medical Device Excise Tax The Affordable Care Act imposes a 2.3 percent excise tax on taxable medical devices. Legislation to repeal the excise tax has been introduced in Congress. COMMENT. There appears to be significant bipartisan support in both the House and Senate to repeal the medical device excise tax.

No votes, however, have yet been scheduled. MORE TAX BILLS A host of tax-related proposals have been introduced in the 114th Congress and have been referred to the House and Senate tax-writing committees. They include: ï‚· Child Tax Credit Integrity Preservation Act of 2015 (Sen 53) ï‚· Death Tax Repeal Act (HR 173) ï‚· Taxpayer Protection and Preparer Proficiency Act of 2015 (Sen 137) ï‚· Dependent Care Savings Account Act of 2015 (Sen 74) ï‚· Investment Savings Access After Catastrophes Act of 2015 (Sen 76) ï‚· Stop Targeting of Political Beliefs by the IRS Bill of 2015 (HR 599) ï‚· Fifth Amendment Integrity Restoration (FAIR) Bill (Sen 255) 8 . ï‚· Education Tax Fraud Prevention Act (Sen 75) ï‚· Fair Tax Act of 2015 (HR 25) ï‚· Tax Code Termination Act (HR 27) ï‚· Incentives to Educate American Children (Sen 138) ï‚· No Tax Write-Offs for Corporate Wrongdoers Act (Sen 169) ï‚· Fairness in Taxation Act of 2015 (HR 389) ï‚· Offshoring Prevention Act (HR 305) ï‚· Gas Tax Replacement Act of 2015 (HR 309) ï‚· Obamacare Opt-Out Act of 2015 (HR 420) ï‚· Wild Game Donation Act of 2015 (HR 461) If you have any questions regarding this alert, please contact your Plante Moran client services representative or one of the contacts listed below. Mike Monaghan National Tax Office 877.622.2257 ext. 64943 mike.monaghan@plantemoran.com Mark Jolley National Tax Office 877.622.2257 ext. 26923 mark.jolley@plantemoran.com George Riddering Firmwide Director of Tax 877.622.2257 ext. 34065 george.riddering@plantemoran.com The information provided in this alert is only a general summary and is being distributed with the understanding that Plante Moran is not rendering legal, tax, accounting, or other professional advice, position, or opinions on specific facts or matters and, accordingly, assumes no liability whatsoever in connection with its use. ©2015 CCH Incorporated.

All Rights Reserved 9 .