Description

Enforcement: Connecting the Dots

Maria L. Caldwell, Esq. – Moderator

Panelists: Stacey L. Grooms, Esq., Randall A.

Ross, CPA, Lisa Snyder, CPA, CGMA . ENFORCEMENT “Connecting The Dots” M A R I A L . C A L DWE L L , E S Q . , C H I E F L EG A L O F F I C ER & D I R EC TOR O F C O MPL I A NC E S E RVI C ES S TAC E Y L . G R OOMS , E S Q .

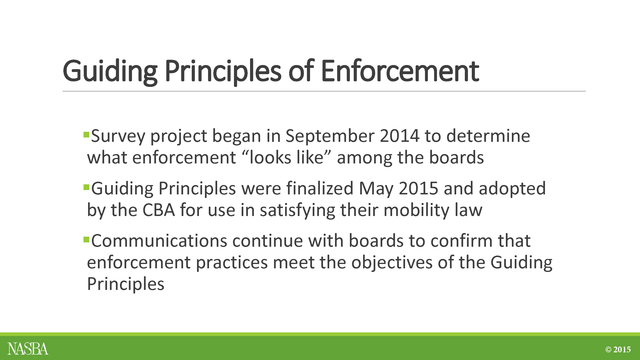

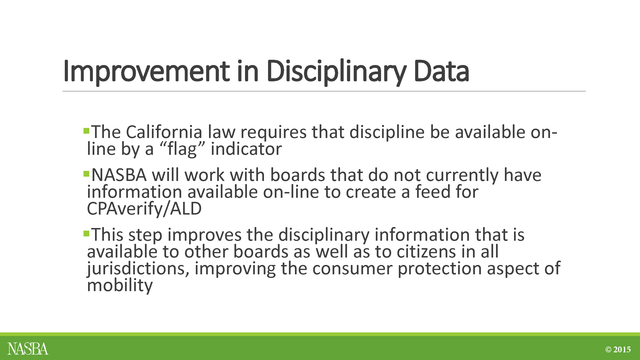

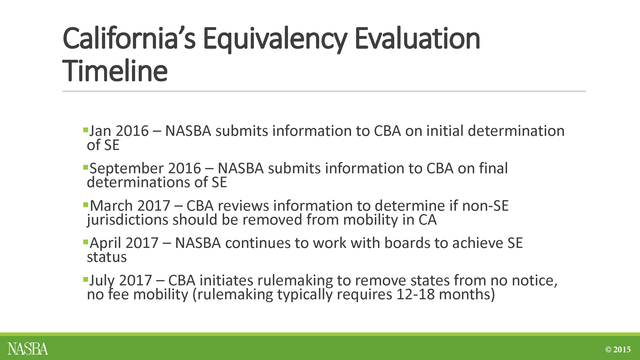

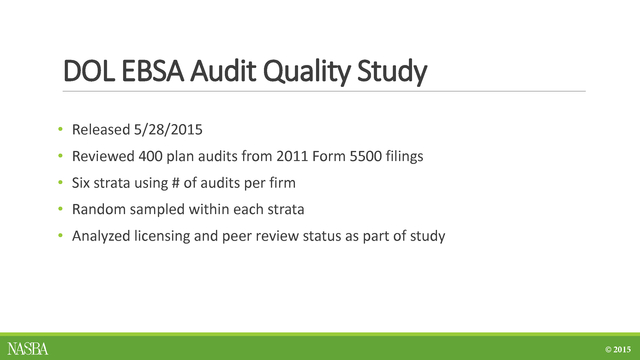

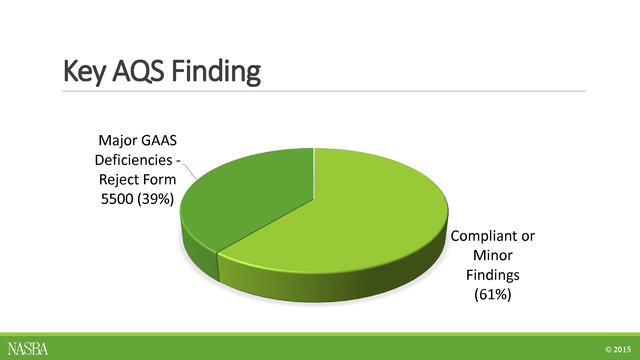

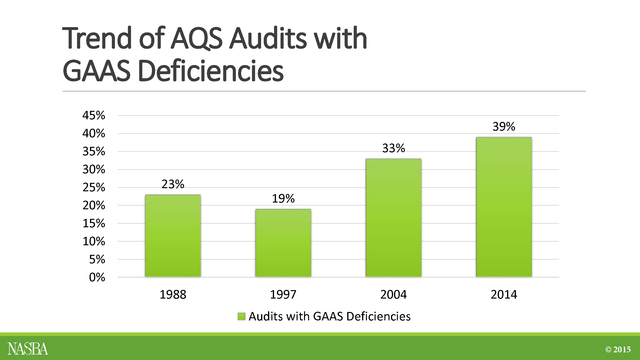

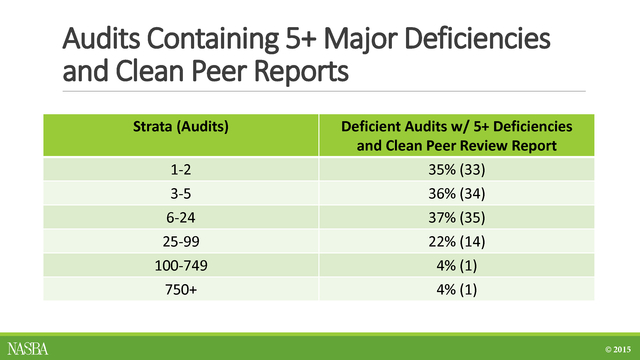

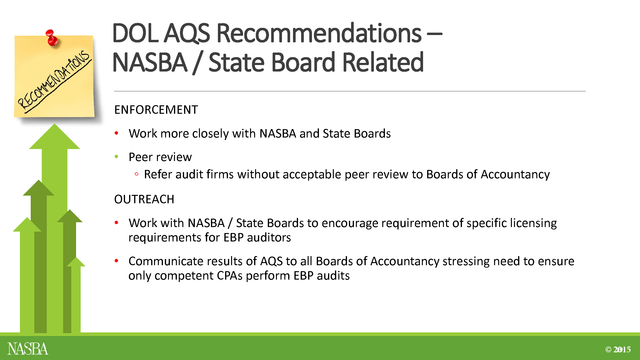

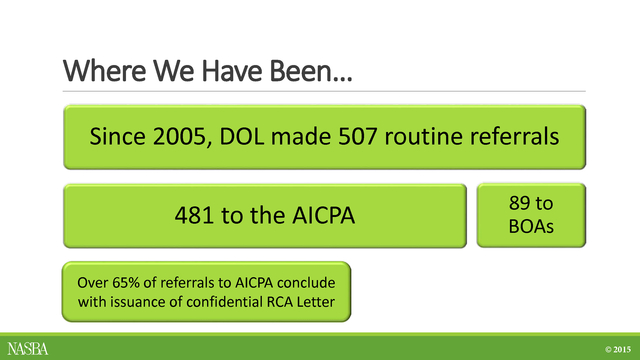

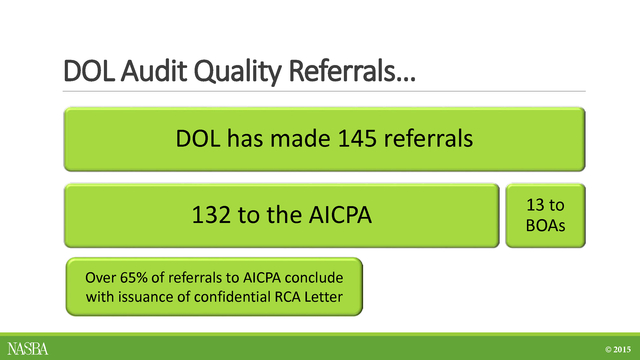

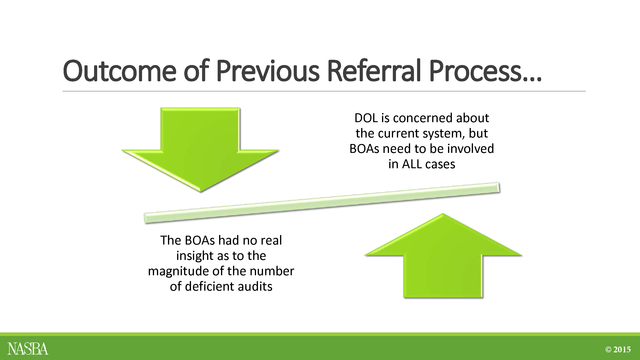

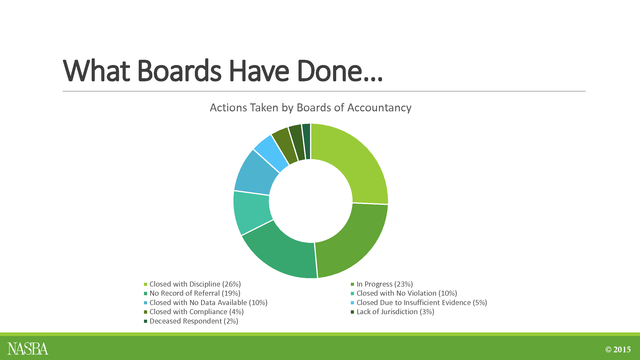

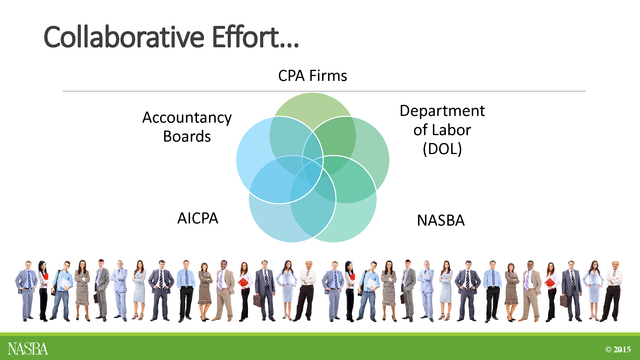

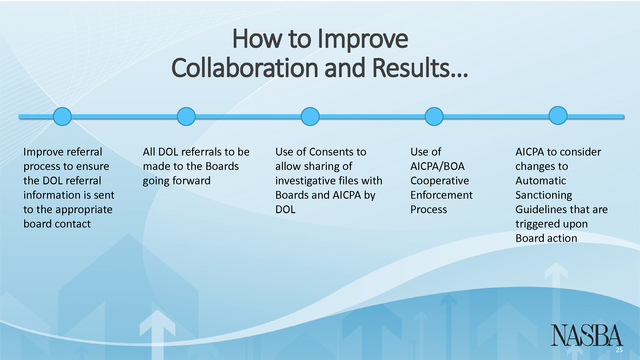

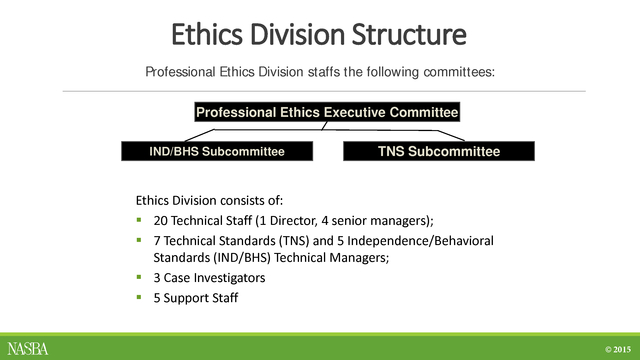

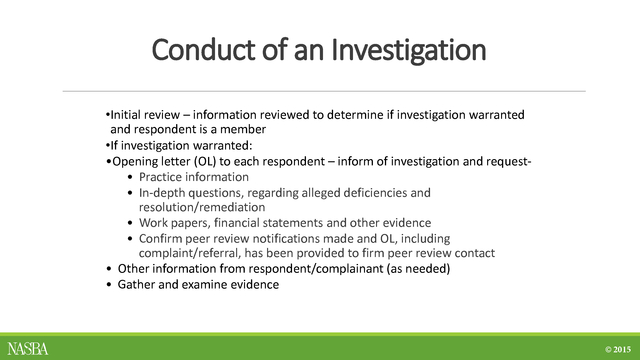

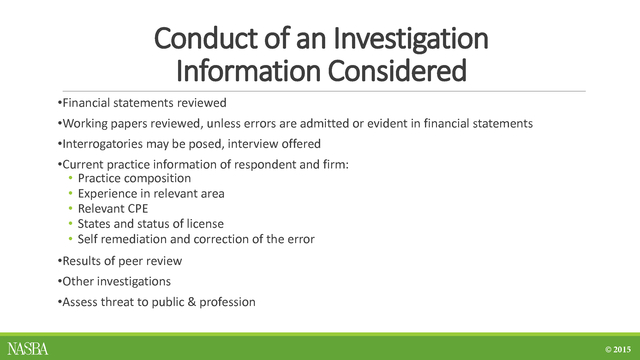

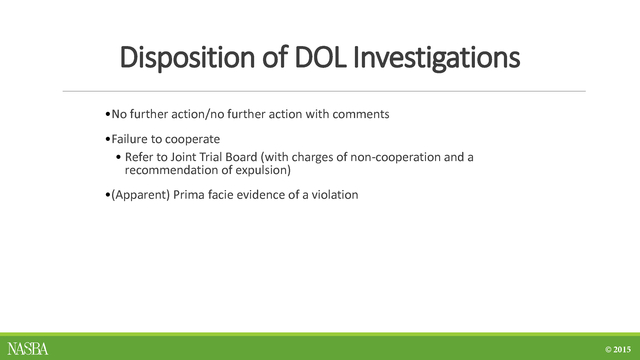

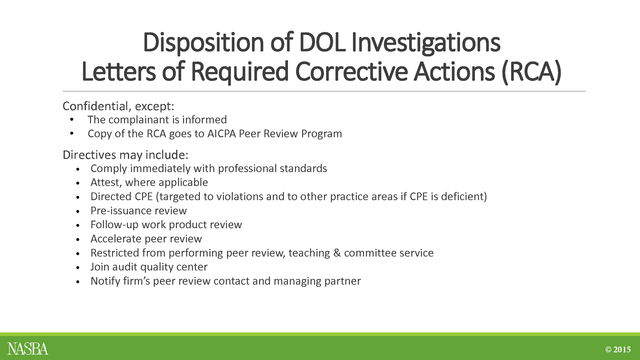

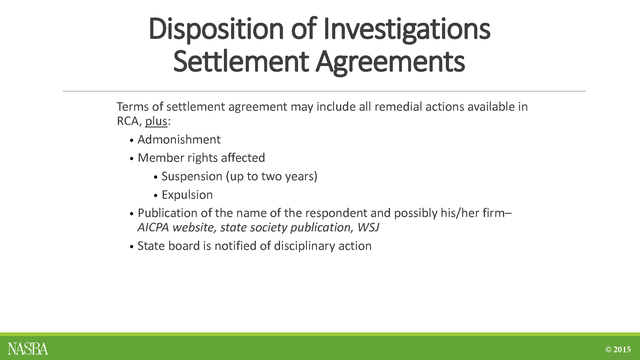

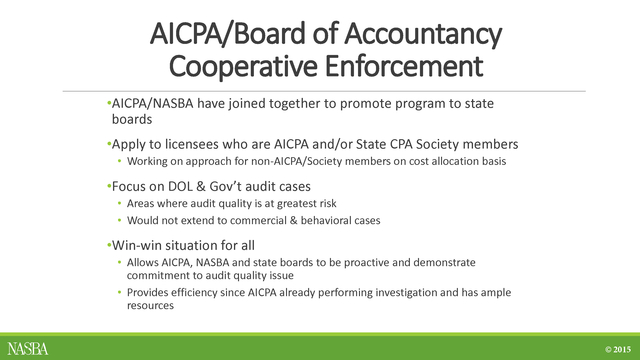

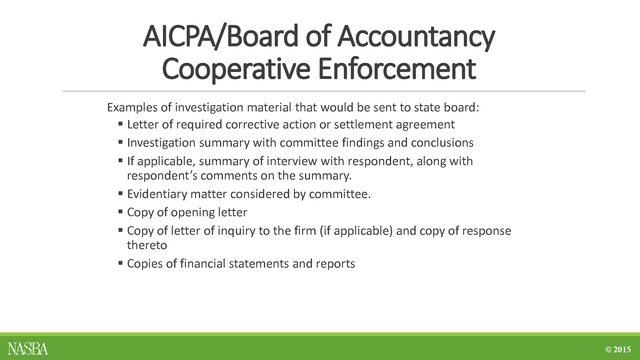

, R EGUL ATORY A F FA I RS M A N AG ER R A N DA L L R O S S , C PA , E X EC UT I VE D I R EC TOR, O K L AH OMA A C COU NTA NC Y B OA R D L I S A S N Y DE R , C PA , C G M A , D I R EC TOR , A I C PA P ROF ES S I ON A L E T H I C S D I V I S I ON © 2015 . Guiding Principles of Enforcement STACEY L. GROOMS, ESQ., REGULATORY AFFAIRS MANAGER . ’s Mission Enhance the effectiveness and advance the common interests of the Boards of Accountancy 4 © 2015 . Enforcement Resources Committee Mission Statement PROMOTE EFFECTIVE, EFFICIENT, AND WHERE APPROPRIATE UNIFORM ENFORCEMENT OF PROFESSIONAL STANDARDS BY BOARDS OF ACCOUNTANCY . Enforcement Tools Created Enforcement Resources Guide Federal Agencies Series Investigator Training Series Quarterly Enforcement Reports Enforcement Newsletters Investigator/Expert Witness Portals © 2015 . Guiding Principles of Enforcement A distillation of Enforcement Resources Guide and the data collected by NASBA regarding how boards put enforcement efforts into action © 2015 . Referrals & Leverage Boards are receiving more information on disciplinary matters through referrals from other boards, as well as referrals directly from state/federal agencies Recent coordination efforts with the DOL have increased the referrals that are being sent to boards Distribution of PTIN listings, EBP audit listing, Federal Clearinghouse listings, and Quarterly Enforcement Reports are notifying boards of actions by other agencies that may require enforcement action by their board “Guiding Principles” which are reflective of the enforcement process of most boards may provide boards with leverage to request more resources to improve their enforcement process © 2015 . Mobility Boards should have confidence in the enforcement process across the nation Boards of the home jurisdiction and the mobility jurisdiction need to be equipped to protect their citizens California’s mobility law specifically requires the CBA to verify that allowing practice privileges to a CPA from a particular jurisdiction does not violate the CBA’s duty to protect the public © 2015 . California (Code 5096.21) Verification of enforcement practices of other jurisdictions can be accomplished by: Determination of equivalency with a best practices guideline created by NASBA; or By individual evaluation by the CBA © 2015 . Guiding Principles of Enforcement Survey project began in September 2014 to determine what enforcement “looks like” among the boards Guiding Principles were finalized May 2015 and adopted by the CBA for use in satisfying their mobility law Communications continue with boards to confirm that enforcement practices meet the objectives of the Guiding Principles © 2015 . Improvement in Disciplinary Data The California law requires that discipline be available online by a “flag” indicator NASBA will work with boards that do not currently have information available on-line to create a feed for CPAverify/ALD This step improves the disciplinary information that is available to other boards as well as to citizens in all jurisdictions, improving the consumer protection aspect of mobility © 2015 . California’s Equivalency Evaluation Timeline Jan 2016 – NASBA submits information to CBA on initial determination of SE September 2016 – NASBA submits information to CBA on final determinations of SE March 2017 – CBA reviews information to determine if non-SE jurisdictions should be removed from mobility in CA April 2017 – NASBA continues to work with boards to achieve SE status July 2017 – CBA initiates rulemaking to remove states from no notice, no fee mobility (rulemaking typically requires 12-18 months) © 2015 . DOL Audit Quality Study Update STACEY L . GROOMS, ESQ., REGULATORY AFFAIRS MANAGER RANDALL ROSS, CPA, EXECUTIVE DIRECTOR, OKLAHOMA ACCOUNTANCY BOARD © 2015 . DOL EBSA Audit Quality Study • Released 5/28/2015 • Reviewed 400 plan audits from 2011 Form 5500 filings • Six strata using # of audits per firm • Random sampled within each strata • Analyzed licensing and peer review status as part of study © 2015 . Key AQS Finding Major GAAS Deficiencies Reject Form 5500 (39%) Compliant or Minor Findings (61%) © 2015 . Trend of AQS Audits with GAAS Deficiencies 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% 39% 33% 23% 1988 19% 1997 2004 2014 Audits with GAAS Deficiencies © 2015 . Audits Containing 5+ Major Deficiencies and Clean Peer Reports Strata (Audits) 1-2 3-5 6-24 25-99 100-749 750+ Deficient Audits w/ 5+ Deficiencies and Clean Peer Review Report 35% (33) 36% (34) 37% (35) 22% (14) 4% (1) 4% (1) © 2015 . DOL AQS Recommendations – NASBA / State Board Related ENFORCEMENT • Work more closely with NASBA and State Boards • Peer review â—¦ Refer audit firms without acceptable peer review to Boards of Accountancy OUTREACH • Work with NASBA / State Boards to encourage requirement of specific licensing requirements for EBP auditors • Communicate results of AQS to all Boards of Accountancy stressing need to ensure only competent CPAs perform EBP audits 19 © 2015 . Where We Have Been… Since 2005, DOL made 507 routine referrals 481 to the AICPA 89 to BOAs Over 65% of referrals to AICPA conclude with issuance of confidential RCA Letter © 2015 . DOL Audit Quality Referrals… DOL has made 145 referrals 132 to the AICPA 13 to BOAs Over 65% of referrals to AICPA conclude with issuance of confidential RCA Letter © 2015 . Outcome of Previous Referral Process… DOL is concerned about the current system, but BOAs need to be involved in ALL cases The BOAs had no real insight as to the magnitude of the number of deficient audits © 2015 . What Boards Have Done… Actions Taken by Boards of Accountancy Closed with Discipline (26%) No Record of Referral (19%) Closed with No Data Available (10%) Closed with Compliance (4%) Deceased Respondent (2%) In Progress (23%) Closed with No Violation (10%) Closed Due to Insufficient Evidence (5%) Lack of Jurisdiction (3%) © 2015 . Collaborative Effort… CPA Firms Accountancy Boards AICPA Department of Labor (DOL) NASBA 24 © 2015 . How to Improve Collaboration and Results… Improve referral process to ensure the DOL referral information is sent to the appropriate board contact All DOL referrals to be made to the Boards going forward Use of Consents to allow sharing of investigative files with Boards and AICPA by DOL Use of AICPA/BOA Cooperative Enforcement Process AICPA to consider changes to Automatic Sanctioning Guidelines that are triggered upon Board action 25 © 2015 . AICPA/Board Cooperative Enforcement Project LISA SNYDER, CPA, CGMA, DIRECTOR, AICPA PROFESSIONAL ETHICS DIVISION . Ethics Division Structure Professional Ethics Division staffs the following committees: Professional Ethics Executive Committee IND/BHS Subcommittee TNS Subcommittee Ethics Division consists of:  20 Technical Staff (1 Director, 4 senior managers);  7 Technical Standards (TNS) and 5 Independence/Behavioral Standards (IND/BHS) Technical Managers;  3 Case Investigators  5 Support Staff © 2015 . Conduct of an Investigation •Initial review – information reviewed to determine if investigation warranted and respondent is a member •If investigation warranted: •Opening letter (OL) to each respondent – inform of investigation and request• Practice information • In-depth questions, regarding alleged deficiencies and resolution/remediation • Work papers, financial statements and other evidence • Confirm peer review notifications made and OL, including complaint/referral, has been provided to firm peer review contact • Other information from respondent/complainant (as needed) • Gather and examine evidence © 2015 . Conduct of an Investigation Information Considered •Financial statements reviewed •Working papers reviewed, unless errors are admitted or evident in financial statements •Interrogatories may be posed, interview offered •Current practice information of respondent and firm: • Practice composition • Experience in relevant area • Relevant CPE • States and status of license • Self remediation and correction of the error •Results of peer review •Other investigations •Assess threat to public & profession © 2015 . Disposition of DOL Investigations •No further action/no further action with comments •Failure to cooperate • Refer to Joint Trial Board (with charges of non-cooperation and a recommendation of expulsion) •(Apparent) Prima facie evidence of a violation © 2015 . Disposition of DOL Investigations Letters of Required Corrective Actions (RCA) Confidential, except: The complainant is informed Copy of the RCA goes to AICPA Peer Review Program • • Directives may include: • • • • • • • • • Comply immediately with professional standards Attest, where applicable Directed CPE (targeted to violations and to other practice areas if CPE is deficient) Pre-issuance review Follow-up work product review Accelerate peer review Restricted from performing peer review, teaching & committee service Join audit quality center Notify firm’s peer review contact and managing partner © 2015 . Disposition of Investigations Settlement Agreements Terms of settlement agreement may include all remedial actions available in RCA, plus: • Admonishment • Member rights affected • Suspension (up to two years) • Expulsion • Publication of the name of the respondent and possibly his/her firm– AICPA website, state society publication, WSJ • State board is notified of disciplinary action © 2015 . AICPA/Board of Accountancy Cooperative Enforcement •AICPA/NASBA have joined together to promote program to state boards •Apply to licensees who are AICPA and/or State CPA Society members • Working on approach for non-AICPA/Society members on cost allocation basis •Focus on DOL & Gov’t audit cases • Areas where audit quality is at greatest risk • Would not extend to commercial & behavioral cases •Win-win situation for all • Allows AICPA, NASBA and state boards to be proactive and demonstrate commitment to audit quality issue • Provides efficiency since AICPA already performing investigation and has ample resources © 2015 . AICPA/Board of Accountancy Cooperative Enforcement •AICPA would not perform investigation “on behalf of” Board • AICPA would share investigative files and conclusions with Board •Board would defer its investigation until completion of AICPA investigation • If Board were to “open” investigation, licensee has right to defer AICPA investigation • Board would reach its own conclusions and determine sanctions •State board would request consent letter from licensee â—¦ Board will defer its investigation due to pending AICPA investigation â—¦ Upon completion of AICPA investigation, Board will request AICPA provide copies of its investigative files and conclusions â—¦ Board will commence its own investigation at that time and may take AICPA’s investigation, findings and conclusions into consideration â—¦ Board will reach its own findings/conclusions and may request licensee provide additional info â—¦ Request licensee provide consent for AICPA to share its investigative files and conclusions with Board © 2015 . AICPA/Board of Accountancy Cooperative Enforcement Examples of investigation material that would be sent to state board:  Letter of required corrective action or settlement agreement  Investigation summary with committee findings and conclusions  If applicable, summary of interview with respondent, along with respondent’s comments on the summary.  Evidentiary matter considered by committee.  Copy of opening letter  Copy of letter of inquiry to the firm (if applicable) and copy of response thereto  Copies of financial statements and reports © 2015 . QUESTIONS? © 2015 .

Ross, CPA, Lisa Snyder, CPA, CGMA . ENFORCEMENT “Connecting The Dots” M A R I A L . C A L DWE L L , E S Q . , C H I E F L EG A L O F F I C ER & D I R EC TOR O F C O MPL I A NC E S E RVI C ES S TAC E Y L . G R OOMS , E S Q .

, R EGUL ATORY A F FA I RS M A N AG ER R A N DA L L R O S S , C PA , E X EC UT I VE D I R EC TOR, O K L AH OMA A C COU NTA NC Y B OA R D L I S A S N Y DE R , C PA , C G M A , D I R EC TOR , A I C PA P ROF ES S I ON A L E T H I C S D I V I S I ON © 2015 . Guiding Principles of Enforcement STACEY L. GROOMS, ESQ., REGULATORY AFFAIRS MANAGER . ’s Mission Enhance the effectiveness and advance the common interests of the Boards of Accountancy 4 © 2015 . Enforcement Resources Committee Mission Statement PROMOTE EFFECTIVE, EFFICIENT, AND WHERE APPROPRIATE UNIFORM ENFORCEMENT OF PROFESSIONAL STANDARDS BY BOARDS OF ACCOUNTANCY . Enforcement Tools Created Enforcement Resources Guide Federal Agencies Series Investigator Training Series Quarterly Enforcement Reports Enforcement Newsletters Investigator/Expert Witness Portals © 2015 . Guiding Principles of Enforcement A distillation of Enforcement Resources Guide and the data collected by NASBA regarding how boards put enforcement efforts into action © 2015 . Referrals & Leverage Boards are receiving more information on disciplinary matters through referrals from other boards, as well as referrals directly from state/federal agencies Recent coordination efforts with the DOL have increased the referrals that are being sent to boards Distribution of PTIN listings, EBP audit listing, Federal Clearinghouse listings, and Quarterly Enforcement Reports are notifying boards of actions by other agencies that may require enforcement action by their board “Guiding Principles” which are reflective of the enforcement process of most boards may provide boards with leverage to request more resources to improve their enforcement process © 2015 . Mobility Boards should have confidence in the enforcement process across the nation Boards of the home jurisdiction and the mobility jurisdiction need to be equipped to protect their citizens California’s mobility law specifically requires the CBA to verify that allowing practice privileges to a CPA from a particular jurisdiction does not violate the CBA’s duty to protect the public © 2015 . California (Code 5096.21) Verification of enforcement practices of other jurisdictions can be accomplished by: Determination of equivalency with a best practices guideline created by NASBA; or By individual evaluation by the CBA © 2015 . Guiding Principles of Enforcement Survey project began in September 2014 to determine what enforcement “looks like” among the boards Guiding Principles were finalized May 2015 and adopted by the CBA for use in satisfying their mobility law Communications continue with boards to confirm that enforcement practices meet the objectives of the Guiding Principles © 2015 . Improvement in Disciplinary Data The California law requires that discipline be available online by a “flag” indicator NASBA will work with boards that do not currently have information available on-line to create a feed for CPAverify/ALD This step improves the disciplinary information that is available to other boards as well as to citizens in all jurisdictions, improving the consumer protection aspect of mobility © 2015 . California’s Equivalency Evaluation Timeline Jan 2016 – NASBA submits information to CBA on initial determination of SE September 2016 – NASBA submits information to CBA on final determinations of SE March 2017 – CBA reviews information to determine if non-SE jurisdictions should be removed from mobility in CA April 2017 – NASBA continues to work with boards to achieve SE status July 2017 – CBA initiates rulemaking to remove states from no notice, no fee mobility (rulemaking typically requires 12-18 months) © 2015 . DOL Audit Quality Study Update STACEY L . GROOMS, ESQ., REGULATORY AFFAIRS MANAGER RANDALL ROSS, CPA, EXECUTIVE DIRECTOR, OKLAHOMA ACCOUNTANCY BOARD © 2015 . DOL EBSA Audit Quality Study • Released 5/28/2015 • Reviewed 400 plan audits from 2011 Form 5500 filings • Six strata using # of audits per firm • Random sampled within each strata • Analyzed licensing and peer review status as part of study © 2015 . Key AQS Finding Major GAAS Deficiencies Reject Form 5500 (39%) Compliant or Minor Findings (61%) © 2015 . Trend of AQS Audits with GAAS Deficiencies 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% 39% 33% 23% 1988 19% 1997 2004 2014 Audits with GAAS Deficiencies © 2015 . Audits Containing 5+ Major Deficiencies and Clean Peer Reports Strata (Audits) 1-2 3-5 6-24 25-99 100-749 750+ Deficient Audits w/ 5+ Deficiencies and Clean Peer Review Report 35% (33) 36% (34) 37% (35) 22% (14) 4% (1) 4% (1) © 2015 . DOL AQS Recommendations – NASBA / State Board Related ENFORCEMENT • Work more closely with NASBA and State Boards • Peer review â—¦ Refer audit firms without acceptable peer review to Boards of Accountancy OUTREACH • Work with NASBA / State Boards to encourage requirement of specific licensing requirements for EBP auditors • Communicate results of AQS to all Boards of Accountancy stressing need to ensure only competent CPAs perform EBP audits 19 © 2015 . Where We Have Been… Since 2005, DOL made 507 routine referrals 481 to the AICPA 89 to BOAs Over 65% of referrals to AICPA conclude with issuance of confidential RCA Letter © 2015 . DOL Audit Quality Referrals… DOL has made 145 referrals 132 to the AICPA 13 to BOAs Over 65% of referrals to AICPA conclude with issuance of confidential RCA Letter © 2015 . Outcome of Previous Referral Process… DOL is concerned about the current system, but BOAs need to be involved in ALL cases The BOAs had no real insight as to the magnitude of the number of deficient audits © 2015 . What Boards Have Done… Actions Taken by Boards of Accountancy Closed with Discipline (26%) No Record of Referral (19%) Closed with No Data Available (10%) Closed with Compliance (4%) Deceased Respondent (2%) In Progress (23%) Closed with No Violation (10%) Closed Due to Insufficient Evidence (5%) Lack of Jurisdiction (3%) © 2015 . Collaborative Effort… CPA Firms Accountancy Boards AICPA Department of Labor (DOL) NASBA 24 © 2015 . How to Improve Collaboration and Results… Improve referral process to ensure the DOL referral information is sent to the appropriate board contact All DOL referrals to be made to the Boards going forward Use of Consents to allow sharing of investigative files with Boards and AICPA by DOL Use of AICPA/BOA Cooperative Enforcement Process AICPA to consider changes to Automatic Sanctioning Guidelines that are triggered upon Board action 25 © 2015 . AICPA/Board Cooperative Enforcement Project LISA SNYDER, CPA, CGMA, DIRECTOR, AICPA PROFESSIONAL ETHICS DIVISION . Ethics Division Structure Professional Ethics Division staffs the following committees: Professional Ethics Executive Committee IND/BHS Subcommittee TNS Subcommittee Ethics Division consists of:  20 Technical Staff (1 Director, 4 senior managers);  7 Technical Standards (TNS) and 5 Independence/Behavioral Standards (IND/BHS) Technical Managers;  3 Case Investigators  5 Support Staff © 2015 . Conduct of an Investigation •Initial review – information reviewed to determine if investigation warranted and respondent is a member •If investigation warranted: •Opening letter (OL) to each respondent – inform of investigation and request• Practice information • In-depth questions, regarding alleged deficiencies and resolution/remediation • Work papers, financial statements and other evidence • Confirm peer review notifications made and OL, including complaint/referral, has been provided to firm peer review contact • Other information from respondent/complainant (as needed) • Gather and examine evidence © 2015 . Conduct of an Investigation Information Considered •Financial statements reviewed •Working papers reviewed, unless errors are admitted or evident in financial statements •Interrogatories may be posed, interview offered •Current practice information of respondent and firm: • Practice composition • Experience in relevant area • Relevant CPE • States and status of license • Self remediation and correction of the error •Results of peer review •Other investigations •Assess threat to public & profession © 2015 . Disposition of DOL Investigations •No further action/no further action with comments •Failure to cooperate • Refer to Joint Trial Board (with charges of non-cooperation and a recommendation of expulsion) •(Apparent) Prima facie evidence of a violation © 2015 . Disposition of DOL Investigations Letters of Required Corrective Actions (RCA) Confidential, except: The complainant is informed Copy of the RCA goes to AICPA Peer Review Program • • Directives may include: • • • • • • • • • Comply immediately with professional standards Attest, where applicable Directed CPE (targeted to violations and to other practice areas if CPE is deficient) Pre-issuance review Follow-up work product review Accelerate peer review Restricted from performing peer review, teaching & committee service Join audit quality center Notify firm’s peer review contact and managing partner © 2015 . Disposition of Investigations Settlement Agreements Terms of settlement agreement may include all remedial actions available in RCA, plus: • Admonishment • Member rights affected • Suspension (up to two years) • Expulsion • Publication of the name of the respondent and possibly his/her firm– AICPA website, state society publication, WSJ • State board is notified of disciplinary action © 2015 . AICPA/Board of Accountancy Cooperative Enforcement •AICPA/NASBA have joined together to promote program to state boards •Apply to licensees who are AICPA and/or State CPA Society members • Working on approach for non-AICPA/Society members on cost allocation basis •Focus on DOL & Gov’t audit cases • Areas where audit quality is at greatest risk • Would not extend to commercial & behavioral cases •Win-win situation for all • Allows AICPA, NASBA and state boards to be proactive and demonstrate commitment to audit quality issue • Provides efficiency since AICPA already performing investigation and has ample resources © 2015 . AICPA/Board of Accountancy Cooperative Enforcement •AICPA would not perform investigation “on behalf of” Board • AICPA would share investigative files and conclusions with Board •Board would defer its investigation until completion of AICPA investigation • If Board were to “open” investigation, licensee has right to defer AICPA investigation • Board would reach its own conclusions and determine sanctions •State board would request consent letter from licensee â—¦ Board will defer its investigation due to pending AICPA investigation â—¦ Upon completion of AICPA investigation, Board will request AICPA provide copies of its investigative files and conclusions â—¦ Board will commence its own investigation at that time and may take AICPA’s investigation, findings and conclusions into consideration â—¦ Board will reach its own findings/conclusions and may request licensee provide additional info â—¦ Request licensee provide consent for AICPA to share its investigative files and conclusions with Board © 2015 . AICPA/Board of Accountancy Cooperative Enforcement Examples of investigation material that would be sent to state board:  Letter of required corrective action or settlement agreement  Investigation summary with committee findings and conclusions  If applicable, summary of interview with respondent, along with respondent’s comments on the summary.  Evidentiary matter considered by committee.  Copy of opening letter  Copy of letter of inquiry to the firm (if applicable) and copy of response thereto  Copies of financial statements and reports © 2015 . QUESTIONS? © 2015 .