Description

Under the Microscope

2015 Analysis of SEC Comment Letter Trends

Among Middle-Market and Pre-IPO Life Sciences Companies

. Moss Adams | Under the Microscope | Contents

2

Contents

Introduction

3

Methodology

4

Executive Summary

6

Overview of Trends

6

Results by Filing Type

10

Research and Development

11

Clinical Trials and Studies

11

FDA Filings and Communication

12

Entity-Related Information

13

Products and Services

Collaborative Arrangements

Related Parties

External Environment

15

Risk Disclosures

16

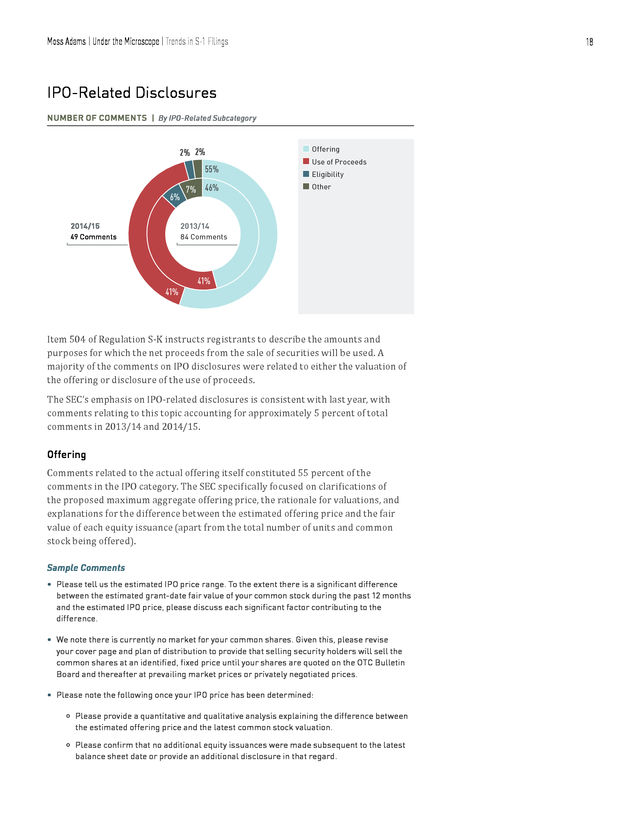

IPO-Related Disclosures

18

Offering

Use of Proceeds

19

Other Disclosure Topics

19

SEC Reporting

Patents

Material Contracts

Terms of License Agreements

Disclosures About Directors

26

Research and Development

Management’s Discussion and Analysis

Other Disclosure Topics

28

Patents

Results by Subindustry

Management’s Discussion and Analysis

Areas of Focus

24

SEC Reporting

Results by Market Capitalization Range

Trends in S-1 Filings

Trends in 10-K, 10-Q, and 20-F Filings

22

Market Capitalization Ranges

Subindustry Trends

31

Conclusion

33

About Moss Adams

35

. Moss Adams | Under the Microscope | Introduction

3

Introduction

According to Renaissance Capital’s US IPO market reports, the life sciences industry

saw a surge of initial public offering (IPO) activity in 2014, specifically during the

period from January 1 to December 31. In this time period, a total of 102 IPOs raised

approximately $9.2 billion. While the first quarter of 2015 saw only 16 companies

raising $1.2 billion, the second quarter of 2015 heated up again, with 30 companies

raising $2.7 billion.

Historically, IPO activity in the industry has followed a cyclical pattern. Following

2014, it’s likely that the market has entered a transitional period as the pipeline

builds before the next wave of activity.

It’s possible, therefore, that there are a number of companies currently in the process of preparing for their IPOs. For these companies, understanding the nature of SEC scrutiny toward financial filings is of great importance. The life sciences environment is also becoming increasingly competitive, partly due to the expiration of several patents and progressively shorter product life cycles. A recent study of 12 large, global life sciences companies found that their expected return on late-stage pipeline projects declined over the four-year period from early 2010 to late 2013, from 11 percent to 5 percent. Over the same period, the cost to develop and launch new medicines increased by 18 percent, to $1.3 billion.

Given this operationally strenuous environment, it’s become critical that companies avoid additional inefficiencies and operational delays when they can. Delays in SEC filings can create significant rollover effects throughout the product development pipeline, and to avoid this, companies need to be aware of accounting issues their peers have struggled with. Furthermore, evolving industry dynamics are resulting in greater SEC scrutiny in several areas. Due to the rising capital investment requirements to develop new products, companies are increasingly strategizing around mergers and acquisitions to acquire license agreements, share research and development (R&D) risks, restock depleted pipelines, and save costs by pooling their resources.

Stakeholders are also increasingly looking toward value-based care rather than volume-based care, and the quality of clinical trial results is becoming more important in leveraging competitive advantages. These trends were reflected in SEC comments during the period of our review, with frequent requests for greater transparency in terms of license agreements, results from clinical trials, and risks to consumers. What this means for life sciences companies is that as the SEC adjusts its scrutiny levels to meet this new reality, companies will do well to anticipate it while drafting their filings. This report is an analysis of the nature of SEC comments, comparing this year’s patterns with those identified last year. We hope middle-market life sciences companies, both pre- and post-IPO, will benefit from the actionable data provided here, and use these insights to reduce S-1, 10-K, 10-Q, and 20-F filing inefficiency. ERIC MILES, PARTNER National Practice Leader (408) 916-0571 eric.miles@mossadams.com RICHARD CROGHAN, PARTNER Northern California Practice Leader, Life Sciences (415) 677-8282 richard.croghan@mossadams.com FINDLEY GILLESPIE, PARTNER Pacific Northwest Practice Leader, Life Sciences (206) 302-6212 findley.gillespie@mossadams.com CARISA WISNIEWSKI, PARTNER Southern California Practice Leader, Life Sciences (858) 627-1402 carisa.wisniewski@mossadams.com .

Moss Adams | Under the Microscope | Methodology 4 Methodology To perform our analysis, we categorized all SEC comments directed toward companies in select life sciences subindustries during the period of our review. The following subindustries (as identified by their EDGAR SIC code) were covered in our analysis: EDGAR SIC Code Subindustry 2833 Medical Chemicals & Botanical Products 2834 Pharmaceutical Preparations 2835 In Vitro & In Vivo Diagnostics Substances 2836 Biological Products (No Diagnostic Substance) 3826 Laboratory Analytical Instruments 3841 Surgical & Medical Instruments & Apparatus 3842 Orthopedic, Prosthetic & Surgical Appliances & Supplies 3843 Dental Equipment & Supplies 3844 X-Ray Apparatuses & Tubes & Related Irradiation Apparatus 3845 Electromedical & Electrotherapeutic Apparatus 3851 Ophthalmic Goods 8731 Commercial Physical & Biological Research Comments for the following SEC filings were considered: S-1 (pages 10–23) 10-K 10-Q 20-F (pages 24–30) Because the focus of our study was middle-market companies, we excluded comments related to companies with market capitalizations greater than $2 billion (as of the date of analysis) from our research and assessment. Our analysis included comments filed on the SEC EDGAR database during the period from May 1, 2014, to April 30, 2015 (which we’ll refer to from here on as 2014/15). In order to achieve a fair and objective assessment of the data, we considered only the first instance of an SEC comment letter for an individual filing, given that in subsequent instances, letters from the SEC often contained comments of similar nature to those found in the first iteration. It should be noted that the period under analysis in last year’s report (2013/14) was approximately 14.5 months as compared to 12 months for this year’s report. Readers should bear this in mind before making direct comparisons in terms of the absolute number of comments from last year to this year.

To address this discrepancy, we used a ratio-based methodology to generate comparable data. We considered cases in which shifts in comment ratios in a given subset of comments (from last year to this year) exceeded the mean variance in that subset to be “significant” variances from last year. For example, out of 1,840 comments directed toward S-1 filings in 2013/14, 155 were related to R&D, amounting to a ratio of a little over 8 percent. The same ratio increased to a little under 13 percent .

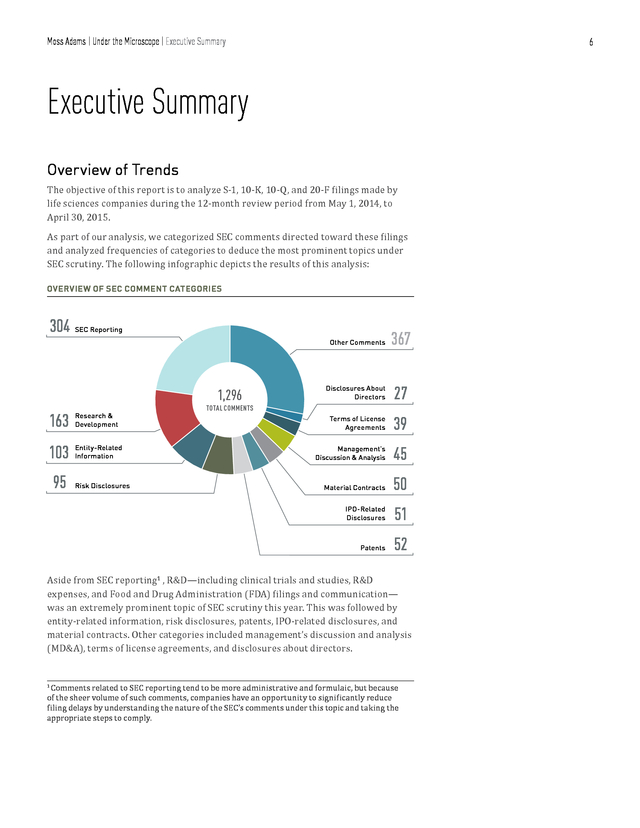

Moss Adams | Under the Microscope | Methodology in 2014/15, signifying an increase of approximately 4 percent. Because this was greater than the mean variance among other topics in S-1 filings, we considered the variance in R&D-related comments toward S-1 filings to be significant. Last, some of the comments in this report have been edited in the interests of clarity and brevity. Identifiable information, such as company name, dollar figures, product names, and place names, have therefore been omitted in the SEC sample comment sections. 5 . Moss Adams | Under the Microscope | Executive Summary 6 Executive Summary Overview of Trends The objective of this report is to analyze S-1, 10-K, 10-Q, and 20-F filings made by life sciences companies during the 12-month review period from May 1, 2014, to April 30, 2015. As part of our analysis, we categorized SEC comments directed toward these filings and analyzed frequencies of categories to deduce the most prominent topics under SEC scrutiny. The following infographic depicts the results of this analysis: OVERVIEW OF SEC COMMENT CATEGORIES 304 SEC Reporting Other Comments Research & Development 103 Entity-Related Information 95 Risk Disclosures 27 Terms of License Agreements 39 Management’s Discussion & Analysis 45 Material Contracts 50 51 Patents 163 Disclosures About Directors IPO-Related Disclosures 1,296 367 52 TOTAL COMMENTS Aside from SEC reporting1 , R&D—including clinical trials and studies, R&D expenses, and Food and Drug Administration (FDA) filings and communication— was an extremely prominent topic of SEC scrutiny this year. This was followed by entity-related information, risk disclosures, patents, IPO-related disclosures, and material contracts. Other categories included management’s discussion and analysis (MD&A), terms of license agreements, and disclosures about directors. Comments related to SEC reporting tend to be more administrative and formulaic, but because of the sheer volume of such comments, companies have an opportunity to significantly reduce filing delays by understanding the nature of the SEC’s comments under this topic and taking the appropriate steps to comply. 1 .

Moss Adams | Under the Microscope | Executive Summary 7 The following graph depicts topics we determined showed significant variance (either positive or negative) from 2013/14 to 2014/15. Variance was measured as ratios to the total number of comments. SIGNIFICANT SHIFTS IN SEC FOCUS FOR OVERALL FILINGS | By Ratio of Comments 30 24 (percentage) Total Comments 25 20 16 15 15 13 10 12 8 8 8 4 5 1 SEC Reporting R&D Entity-Related Information n 2013/14 Comment Percentage Risk Disclosures Share-Based Compensation n 2014/15 Comment Percentage The topics in which we’ve seen major shifts in trends compared with last year are share-based compensation, risk disclosures, entity-related information, R&D, and SEC reporting. Of these, SEC reporting and R&D by far saw the greatest relative increase in focus. Shares of comments relating to these topics increased by 8 percent and 4 percent, respectively.

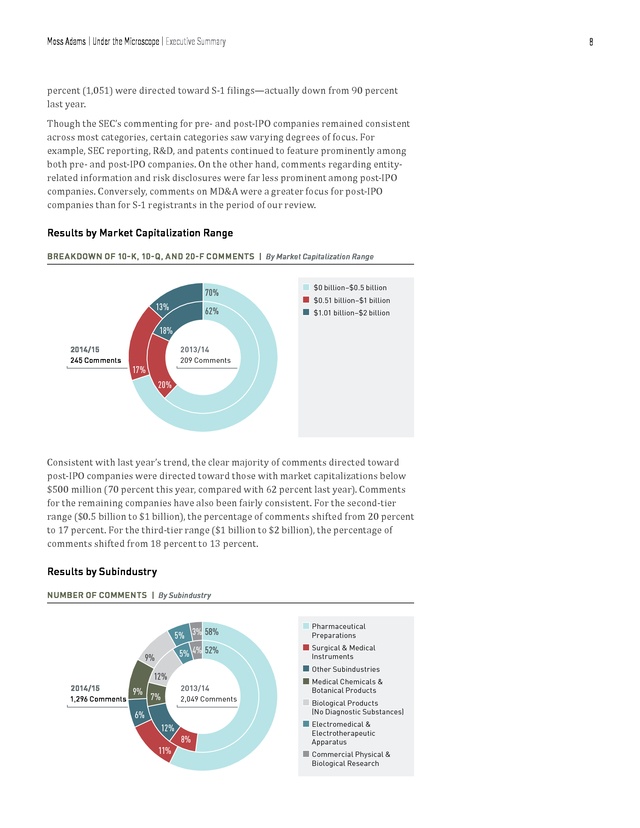

On the other hand, entity-related information and risk disclosures both saw significant decreases in their share of comments. Results by Filing Type NUMBER OF COMMENTS | By Filing Type 81% 19% 10% 90% 2014/15 S-1 Filings 10-K, 10-Q, 20-F Filings 2013/14 1,296 Comments n n 2,049 Comments Much like last year, the vast majority of comments analyzed were directed toward pre-IPO companies. Of the 1,296 comments analyzed in 2014/15, approximately 81 . Moss Adams | Under the Microscope | Executive Summary 8 percent (1,051) were directed toward S-1 filings—actually down from 90 percent last year. Though the SEC’s commenting for pre- and post-IPO companies remained consistent across most categories, certain categories saw varying degrees of focus. For example, SEC reporting, R&D, and patents continued to feature prominently among both pre- and post-IPO companies. On the other hand, comments regarding entityrelated information and risk disclosures were far less prominent among post-IPO companies. Conversely, comments on MD&A were a greater focus for post-IPO companies than for S-1 registrants in the period of our review. Results by Market Capitalization Range BREAKDOWN OF 10-K, 10-Q, AND 20-F COMMENTS | By Market Capitalization Range 70% 13% 62% n n n $0 billion–$0.5 billion $0.51 billion–$1 billion $1.01 billion–$2 billion 18% 2014/15 2013/14 245 Comments 209 Comments 17% 20% Consistent with last year’s trend, the clear majority of comments directed toward post-IPO companies were directed toward those with market capitalizations below $500 million (70 percent this year, compared with 62 percent last year).

Comments for the remaining companies have also been fairly consistent. For the second-tier range ($0.5 billion to $1 billion), the percentage of comments shifted from 20 percent to 17 percent. For the third-tier range ($1 billion to $2 billion), the percentage of comments shifted from 18 percent to 13 percent. Results by Subindustry NUMBER OF COMMENTS | By Subindustry 5% 3% 58% 5% 4% 52% 9% 12% 2014/15 1,296 Comments 9% 2013/14 7% 2,049 Comments n Pharmaceutical Preparations n Surgical & Medical Instruments n Other Subindustries n Medical Chemicals & Botanical Products n Biological Products (No Diagnostic Substances) 6% n Electromedical & 12% 8% 11% Electrotherapeutic Apparatus n Commercial Physical & Biological Research .

Moss Adams | Under the Microscope | Executive Summary Of the total number of comments analyzed this year (1,296), the majority (58 percent) were directed toward companies in the pharmaceutical preparations subindustry. Other notable subindustries included surgical and medical instruments and apparatus (11 percent), medical chemicals and botanical products (9 percent), and biological products (9 percent). The breakdown of comments among subindustries has remained mostly consistent with last year’s data. In both cases pharmaceutical preparations featured in over 50 percent of total comments. The results suggest that while some topics are consistent across subindustries, the SEC places varying degrees of focus on other topics depending on the subindustry along with pertinent micro- and macroeconomic factors.

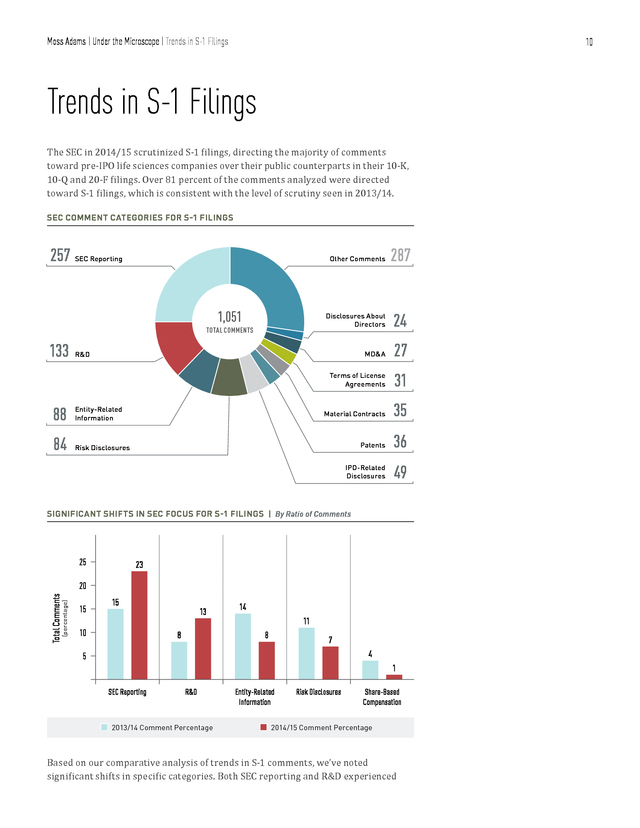

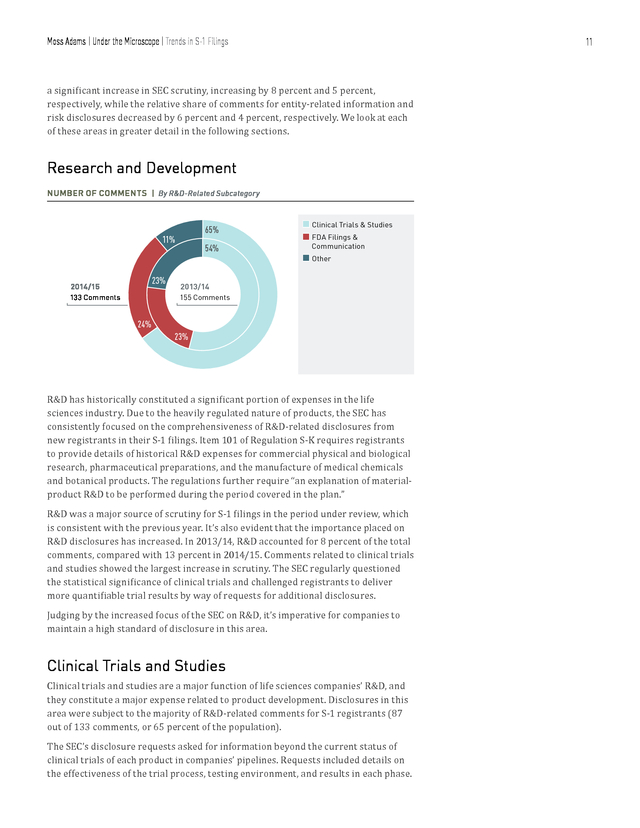

For example, R&D-related comments featured prominently for companies manufacturing biological products, electromedical and electrotherapeutic apparatus, and pharmaceutical preparations. 9 . Moss Adams | Under the Microscope | Trends in S-1 Filings 10 Trends in S-1 Filings The SEC in 2014/15 scrutinized S-1 filings, directing the majority of comments toward pre-IPO life sciences companies over their public counterparts in their 10-K, 10-Q and 20-F filings. Over 81 percent of the comments analyzed were directed toward S-1 filings, which is consistent with the level of scrutiny seen in 2013/14. SEC COMMENT CATEGORIES FOR S-1 FILINGS Other Comments Disclosures About Directors 31 35 Patents 36 IPO-Related Disclosures 133 27 Material Contracts 1,051 TOTAL COMMENTS 24 MD&A SEC Reporting 287 Terms of License Agreements 257 49 R&D 88 Entity-Related Information 84 Risk Disclosures SIGNIFICANT SHIFTS IN SEC FOCUS FOR S-1 FILINGS | By Ratio of Comments 25 23 (percentage) Total Comments 20 15 15 10 13 8 14 11 8 7 4 5 1 SEC Reporting n R&D 2013/14 Comment Percentage Entity-Related Information n Risk Disclosures Share-Based Compensation 2014/15 Comment Percentage Based on our comparative analysis of trends in S-1 comments, we’ve noted significant shifts in specific categories. Both SEC reporting and R&D experienced . Moss Adams | Under the Microscope | Trends in S-1 Filings 11 a significant increase in SEC scrutiny, increasing by 8 percent and 5 percent, respectively, while the relative share of comments for entity-related information and risk disclosures decreased by 6 percent and 4 percent, respectively. We look at each of these areas in greater detail in the following sections. Research and Development NUMBER OF COMMENTS | By R&D-Related Subcategory 65% 11% 23% 2014/15 133 Comments 54% n Clinical Trials & Studies n FDA Filings & Communication n Other 2013/14 155 Comments 24% 23% R&D has historically constituted a significant portion of expenses in the life sciences industry. Due to the heavily regulated nature of products, the SEC has consistently focused on the comprehensiveness of R&D-related disclosures from new registrants in their S-1 filings. Item 101 of Regulation S-K requires registrants to provide details of historical R&D expenses for commercial physical and biological research, pharmaceutical preparations, and the manufacture of medical chemicals and botanical products.

The regulations further require “an explanation of materialproduct R&D to be performed during the period covered in the plan.” R&D was a major source of scrutiny for S-1 filings in the period under review, which is consistent with the previous year. It’s also evident that the importance placed on R&D disclosures has increased. In 2013/14, R&D accounted for 8 percent of the total comments, compared with 13 percent in 2014/15.

Comments related to clinical trials and studies showed the largest increase in scrutiny. The SEC regularly questioned the statistical significance of clinical trials and challenged registrants to deliver more quantifiable trial results by way of requests for additional disclosures. Judging by the increased focus of the SEC on R&D, it’s imperative for companies to maintain a high standard of disclosure in this area. Clinical Trials and Studies Clinical trials and studies are a major function of life sciences companies’ R&D, and they constitute a major expense related to product development. Disclosures in this area were subject to the majority of R&D-related comments for S-1 registrants (87 out of 133 comments, or 65 percent of the population). The SEC’s disclosure requests asked for information beyond the current status of clinical trials of each product in companies’ pipelines.

Requests included details on the effectiveness of the trial process, testing environment, and results in each phase. . Moss Adams | Under the Microscope | Trends in S-1 Filings Any claims made by companies on the best-in-class nature of their product were followed by SEC requests to provide clear substantiation. The SEC has also remained consistent in its request for life sciences companies aspiring to go public to provide comprehensive documentation regarding clinical trials. The standard expectation is complete disclosure on the trial process, environment, duration, and results (both positive and negative, which need to be described either way). Sample Comments • Please quantify what you mean by “decreased slightly” and “remained slightly lower” when you state, “Of note, body fat decreased slightly in the 3.0 mg/kg group at the end of the treatment period and remained slightly lower than baseline four weeks after the cessation of treatment.” • In the table on page 85, you state that the results of the Phase 2a trial labeled [trial name] provide preliminary evidence of the ability of [product name] to alleviate symptoms associated with [condition]. We also note that on page 87, you disclose that this trial did not produce a statistically significant improvement in [medical condition]. We also note that there was no significant difference between [product name] and the placebo in the change of [medical condition] for trial [number].

Please amend your disclosure in the table and the related notes regarding each of these two studies to clarify that these two trials didn’t produce a statistically significant improvement in these selected endpoints. • Please briefly summarize any pertinent feedback received in your meetings with the FDA concerning your trial design and the adequacy of your proposed clinical package and how such feedback has impacted or is expected to impact your clinical development of [product name]. FDA Filings and Communication Comments related to FDA filings constituted the second largest portion of R&D comments, amounting to 32 comments out of 133, or 24 percent. The SEC recognizes adherence to FDA standards and regulations as an important control measure, and consequently it was of no surprise that pre-IPO companies received comments on inadequate disclosures in the context of filing of forms and applications, meetings with the FDA regarding their clinical trial process, and information on the products. Aspects related to the submission of investigational new drug (IND) applications and administrative communications also were a prominent feature in the SEC’s assessment. Sample Comments • It appears you have filed an IND application for [product name] but not [product name], [product name], or [product name]. Please disclose the identity of the filers and dates the application was filed for [product name], and explain to us why INDs have not been filed for your other product candidates. • Please indicate the number of IND applications you have filed with the FDA to date, the product candidates and indications to which they relate, and the approximate dates when filed. • We note on page 15 that you are initiating your planned confirmatory Phase 3 clinical trial without waiting for comments from the FDA.

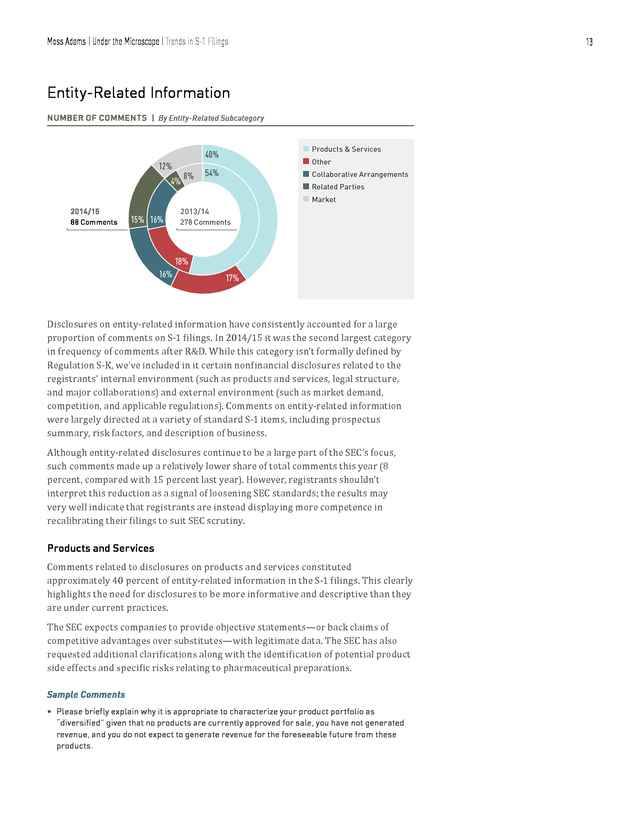

Please clarify whether you have now received comments or correspondence and, if applicable, expand your disclosure to include the substance of any such correspondence or discussions between you and the FDA regarding your first Phase 3 trial of [product name]. 12 . Moss Adams | Under the Microscope | Trends in S-1 Filings 13 Entity-Related Information NUMBER OF COMMENTS | By Entity-Related Subcategory n Products & Services n Other n Collaborative Arrangements n Related Parties n Market 40% 12% 4% 2014/15 88 Comments 15% 16% 8% 54% 2013/14 278 Comments 18% 16% 17% Disclosures on entity-related information have consistently accounted for a large proportion of comments on S-1 filings. In 2014/15 it was the second largest category in frequency of comments after R&D. While this category isn’t formally defined by Regulation S-K, we’ve included in it certain nonfinancial disclosures related to the registrants’ internal environment (such as products and services, legal structure, and major collaborations) and external environment (such as market demand, competition, and applicable regulations). Comments on entity-related information were largely directed at a variety of standard S-1 items, including prospectus summary, risk factors, and description of business. Although entity-related disclosures continue to be a large part of the SEC’s focus, such comments made up a relatively lower share of total comments this year (8 percent, compared with 15 percent last year).

However, registrants shouldn’t interpret this reduction as a signal of loosening SEC standards; the results may very well indicate that registrants are instead displaying more competence in recalibrating their filings to suit SEC scrutiny. Comments related to disclosures on products and services constituted approximately 40 percent of entity-related information in the S-1 filings. This clearly highlights the need for disclosures to be more informative and descriptive than they are under current practices. Products and Services The SEC expects companies to provide objective statements—or back claims of competitive advantages over substitutes—with legitimate data. The SEC has also requested additional clarifications along with the identification of potential product side effects and specific risks relating to pharmaceutical preparations. Sample Comments • Please briefly explain why it is appropriate to characterize your product portfolio as “diversified” given that no products are currently approved for sale, you have not generated revenue, and you do not expect to generate revenue for the foreseeable future from these products. .

Moss Adams | Under the Microscope | Trends in S-1 Filings • In general, you should clarify exactly what your product is and how you differentiate it from other products. For example, are [product name] and [product name] actual products, devices, or technologies? Is [product name] a type of closed-photo bioreactor? How is it different from other photo bioreactors? We note that you list a number of advantages your product offers but do not explain what differentiates how your products function from other similar products. Also, it is not clear whether the [product name] and [product name] are actually two different products or if they are two components of a single product or technology. Please review your entire description of business with this comment in mind, and revise wherever necessary to clarify the nature and function of your product or technology so readers who are not already familiar with it will have a better understanding. • Please disclose the stage of development of the competing product candidate being developed by [company name] in this discussion. Rising costs of research, product development, and production have led to collaborative arrangements with manufacturers, designers, and distributors as a strategy to enhance the bottom line.

These arrangements can have a direct impact on the operational health and financial position of a company, consequently necessitating detailed disclosures, as the SEC’s comments highlight. Collaborative Arrangements This was especially the case in subindustries such as laboratory analytical instruments, surgical and medical instruments, and prosthetic appliances (which is consistent in our observations last year). In these subindustries, the SEC requested filing companies to disclose not only the identity and location of key partners but also details regarding material and financial obligations and the terms and structure of such arrangements. The SEC and regulatory agencies require aspiring life sciences companies to file these detailed disclosures regarding arrangements as exhibits. Sample Comments • Your disclosures suggest that you continue to partner with [entity name] in some capacity. While we note your disclosure of advisors includes persons from [entity name], we further note in the collaboration agreement filed as Exhibit 10.5 that your agreement with [entity name] expired on March 31, 2013.

Please clarify for us and in your document the current status of your partnership with [entity name] and whether any formal agreements are currently in effect. • Please elaborate on the terms of your partnership and exclusive agreement with [entity name]. Please also ensure that you have filed any agreement currently in effect as an exhibit to the registration statement. We note that the agreement filed as Exhibit 10.5 would have terminated on March 31, 2013. • Please disclose the following information regarding your Joint Development and Supply agreement with [entity name]: The applicable royalty rate within a range of 10 percent (that is, twenties, single digits, etc.) If applicable, the total potential milestone payments either party may be required to make under the agreement All material provisions governing duration, including the “current term” referenced in this section The specific intellectual property licensed to [entity name] under the agreement The intellectual property that may be granted through a new license should one party terminate under the certain conditions specified in this section Any other material termination provisions 14 .

Moss Adams | Under the Microscope | Trends in S-1 Filings Item 404 of Regulation S-K requires registrants to disclose certain key information relating to transactions with related persons, promoters, and certain control persons. This includes disclosing pertinent information about such transactions, policies for the review and approval of the transactions (apart from details of promoters), and a history of their transactions and asset transfers. Related Parties The SEC is laying emphasis on comprehensive disclosures of relationships with promoters (both current and past) as well as on the clear identification of related parties. Aspiring registrants are encouraged to provide such disclosures to meet the SEC’s standards of transparency and accountability. Sample Comments • We note your response to prior comment 22. Please expand the disclosure concerning [person name], [person name], and [person name] to include that they joined [company name] in 2009 and 2010, and clearly indicate the positions they held with [company name] during the last five years. • In this subsection and the next subsection of your prospectus, please identify the parties to the disclosed agreement who are related persons as defined in Regulation S-K, Item 404.

Also, please tell us why you do not describe the other provisions of Exhibit 4.2 to this registration statement. External Environment One of the SEC’s roles is to act as a watchdog, preventing the flow of asymmetric information to stakeholders and increasingly informed consumers. The SEC has maintained the trend of constructively challenging claims relating to the external competitive environment and market positioning. This topic accounted for 12 percent of entity-related comments this year. In several comments the SEC requested historic data and statistics highlighting potential substitute products, in accordance with Item 101 of Regulation S-K.

In some cases, the registrants were required to disclose in their business description, if reasonably available, “competitive conditions in the business involved including, where material, the identity of the particular markets in which the registrant competes, an estimate of the number of competitors, and the registrant’s competitive position.” Aspiring life sciences registrants need to focus on the accuracy of their industry analysis and validating their competitive benchmarking. Claims related to unique selling propositions need to be substantiated with an examination of the scope of the market and reference points with evidence of the competition’s development stage. The SEC expects the disclosures to be comprehensive, going beyond basic declarations to provide rationales. Sample Comments • If you are aware of any particular competing product candidates, please disclose the name of the competitors and their respective stage of development. • Please tell us why you believe the reference to [dollar amount] among chronic sinusitis patients is appropriate given your estimate that the addressable market for your product in [country name] consists of approximately 630,000 patients. 15 .

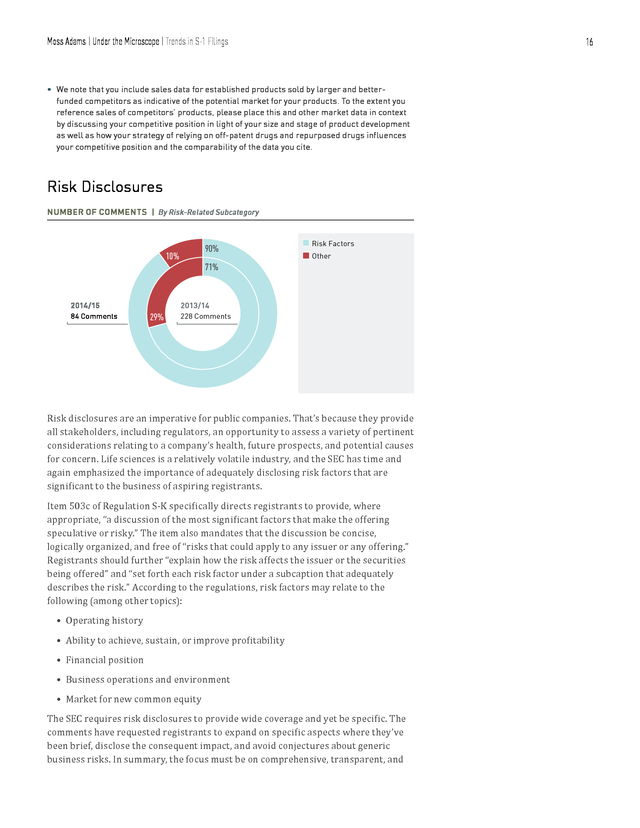

Moss Adams | Under the Microscope | Trends in S-1 Filings 16 • We note that you include sales data for established products sold by larger and betterfunded competitors as indicative of the potential market for your products. To the extent you reference sales of competitors’ products, please place this and other market data in context by discussing your competitive position in light of your size and stage of product development as well as how your strategy of relying on off-patent drugs and repurposed drugs influences your competitive position and the comparability of the data you cite. Risk Disclosures NUMBER OF COMMENTS | By Risk-Related Subcategory 90% 10% 2014/15 84 Comments 71% n Risk Factors n Other 2013/14 29% 228 Comments Risk disclosures are an imperative for public companies. That’s because they provide all stakeholders, including regulators, an opportunity to assess a variety of pertinent considerations relating to a company’s health, future prospects, and potential causes for concern. Life sciences is a relatively volatile industry, and the SEC has time and again emphasized the importance of adequately disclosing risk factors that are significant to the business of aspiring registrants. Item 503c of Regulation S-K specifically directs registrants to provide, where appropriate, “a discussion of the most significant factors that make the offering speculative or risky.” The item also mandates that the discussion be concise, logically organized, and free of “risks that could apply to any issuer or any offering.” Registrants should further “explain how the risk affects the issuer or the securities being offered” and “set forth each risk factor under a subcaption that adequately describes the risk.” According to the regulations, risk factors may relate to the following (among other topics): • Operating history • Ability to achieve, sustain, or improve profitability • Financial position • Business operations and environment • Market for new common equity The SEC requires risk disclosures to provide wide coverage and yet be specific.

The comments have requested registrants to expand on specific aspects where they’ve been brief, disclose the consequent impact, and avoid conjectures about generic business risks. In summary, the focus must be on comprehensive, transparent, and . Moss Adams | Under the Microscope | Trends in S-1 Filings specific risks associated with their particular circumstances, and these must be accompanied by the mitigation strategy the company has employed. For example, a business identifying its exposure to a variety of external risks needs to refocus its reporting by highlighting and expanding on the most important of these risks. Any material weakness in internal control over financial reporting also must be disclosed to maintain SEC standards. The SEC expects disclosures on internal risks to be as comprehensive as possible—a recurring example being the disclosure on senior executives managing the business. In several cases the SEC requested that certain management profiles with potential conflicts of interest and inadequate experience to be disclosed as operational risks in S-1 filings. The risk of insufficient liquidity was an additional area of focus for the SEC.

In cases where businesses identified the need for “additional capital in the future,” the SEC requested a disclosure for a specific contingent business plan if capital procurement was unsuccessful. It also requested specific numbers, with ratios such as working capital on hand, rate of negative cash flow per month, and disclosure on the requirement of capital for future short- and midterm operations. Other trends included requests for the addition of risks associated with classification as an emerging-growth company and the benefits and risks associated with loss of this status. In comparison with last year, risk disclosures constituted 8 percent of the SEC comments toward S-1 filings in the period of our review, compared to 12 percent last year. Though there was a reduction in the frequency of comments given by SEC, the nature and type of comments have remained consistent with those noted in the previous year.

It continues to be important for new registrants to disclose pertinent risks to their business in exhaustive and transparent detail. Specifically, risks related to patents, senior executives’ experience and commitments, and risks related to foreign countries in which a company may operate should be explored, quantified, and disclosed as precisely as possible. Sample Comments • Please expand this risk factor to disclose how long you expect your available cash and the net proceeds from this offering will be sufficient to fund your current operations. • Please expand your disclosure to add a bullet point regarding the risks associated with your ability to obtain and maintain protection for your intellectual property, including the fact that because your product candidates are reformulations of existing drugs, your ability to obtain patent protection for certain types of claims are limited. • Please expand your disclosure in the second paragraph of this risk factor to specify under which agreements you lack the right to control the preparation, filing, and prosecution of patent applications or to maintain the patents covering technology you license from third parties. 17 . Moss Adams | Under the Microscope | Trends in S-1 Filings 18 IPO-Related Disclosures NUMBER OF COMMENTS | By IPO-Related Subcategory 2% 2% 55% 6% 7% 46% 2014/15 2013/14 49 Comments n Offering n Use of Proceeds n Eligibility n Other 84 Comments 41% 41% Item 504 of Regulation S-K instructs registrants to describe the amounts and purposes for which the net proceeds from the sale of securities will be used. A majority of the comments on IPO disclosures were related to either the valuation of the offering or disclosure of the use of proceeds. The SEC’s emphasis on IPO-related disclosures is consistent with last year, with comments relating to this topic accounting for approximately 5 percent of total comments in 2013/14 and 2014/15. Comments related to the actual offering itself constituted 55 percent of the comments in the IPO category. The SEC specifically focused on clarifications of the proposed maximum aggregate offering price, the rationale for valuations, and explanations for the difference between the estimated offering price and the fair value of each equity issuance (apart from the total number of units and common stock being offered). Offering Sample Comments • Please tell us the estimated IPO price range. To the extent there is a significant difference between the estimated grant-date fair value of your common stock during the past 12 months and the estimated IPO price, please discuss each significant factor contributing to the difference. • We note there is currently no market for your common shares.

Given this, please revise your cover page and plan of distribution to provide that selling security holders will sell the common shares at an identified, fixed price until your shares are quoted on the OTC Bulletin Board and thereafter at prevailing market prices or privately negotiated prices. • Please note the following once your IPO price has been determined: Please provide a quantitative and qualitative analysis explaining the difference between the estimated offering price and the latest common stock valuation. Please confirm that no additional equity issuances were made subsequent to the latest balance sheet date or provide an additional disclosure in that regard. . Moss Adams | Under the Microscope | Trends in S-1 Filings 19 We may have additional comments on your accounting for stock compensation once you have disclosed an estimated offering price. Use of Proceeds The SEC asked for disclosures on the specific amount of capital raised and how it will be used, disclosing these purposes and functions separately. The importance of compliance with this standard is evident in the fact that 41 percent of IPO disclosure comments were related to the use of proceeds. Simply stating, for example, that proceeds will be used to “increase manufacturing capability” doesn’t meet the SEC’s disclosure standards. The key takeaway for registrants, therefore, is that comprehensive disclosures on the use of proceeds is important for maintaining the transparency and accountability expected by shareholders and the SEC. Sample Comments • Please expand this discussion to state with reasonable specificity the purposes toward which you will allocate your net proceeds.

That is, rather than saying “Internet,” please explain how these monies will be spent and the purpose you wish to accomplish with this allocation. • We note your statement that you intend to use a certain amount of the net proceeds from this offering to advance your ongoing clinical program. Please specify how you anticipate allocating the proceeds among your respective clinical studies, whether ongoing or planned, and estimate how far you expect the offering proceeds will enable you to advance your clinical program. Other Disclosure Topics NUMBER OF COMMENTS RELATED TO OTHER DISCLOSURE TOPICS 350 300 300 257 (percentage) Total Comments 250 200 150 100 49 50 SEC Reporting n 2013/14 88 67 36 Patents | 300 Comments 54 35 31 Material Contracts License Agreements n 2014/15 27 MD&A 21 24 Disclosures About Directors | 257 Comments Other disclosure topics in SEC comments to S-1 filings included SEC reporting, patents, material contracts, terms of license agreements, MD&A, and disclosures about directors. Of these, comments relating to SEC reporting made up more than 63 percent. .

Moss Adams | Under the Microscope | Trends in S-1 Filings As noted above, comments relating to SEC reporting accounted for 63 percent of other disclosure topics. They also accounted for 24 percent of total comments toward S-1 filings, so their importance can’t be dismissed. Companies shouldn’t undervalue or overlook the administrative requirements of the SEC, which range from proper usage of grammar to assurances that the information being submitted is accurate, complete, and complies with the instructions and format prescribed in Regulation S-K. Comments in this section were primarily related to the filing of exhibits and other material, submission of written communications to potential investors, requests for confidential treatments, demand for updated disclosures and clarifications, and the inclusion of relevant persons’ signatures. SEC Reporting Sample Comments • Please supplementally provide us with copies of all written communications, as defined in Rule 405 under the Securities Act of 1993, that you (or anyone authorized to do so on your behalf) present to potential investors in reliance on Section 5(d) of the Securities Act, regardless of whether they retain copies of the communications.

Similarly, please supplementally provide us with any research reports about you that are published or distributed in reliance upon Section 2(a)(3) of the Securities Act added by Section 105(a) of the Jumpstart Our Business Startups Act by any broker or dealer that is participating or will participate in your offering. • Please be advised that when you submit an application for confidential treatment relating to your exhibits, we will perform a separate review of this application. The review of your registration statement will not be complete until all comments concerning any related confidential treatment request have been cleared. • We note you disclose that “[company name] recognizes that many of its clients are global in nature.” As you do not currently have any clients, please revise to remove the impression that you do. Patents, along with clinical trials, form the backbone of the life sciences industry, particularly in the pharmaceutical preparations subindustry (which accounted for 73 percent of the patent-related comments in the period under review). Also, disclosures on patents are being increasingly scrutinized due to litigation regarding intellectual property violations.

Compared with last year, the share of the SEC’s comments in this category moved from 2.7 percent to 3.4 percent of total S-1 filing comments. The nature of comments on patent-related disclosures was consistent with last year, including disclosure on durations, geographic coverage and jurisdiction, pending applications, infringement risks, and owner entity information. Patents Sample Comments • Please revise your discussion to specify the types, jurisdictions, and expiration dates of those patents relating to each product candidate or product candidate group and the technologies to which such patents relate. For example, please identify whether, and how many of, your patents relate specifically to your [type of] product candidates and that relate to [product name]. • Please disclose exactly what patent rights you license under this agreement, including the type of protection offered by each patent and which of your product candidates are implicated under the patents. 20 .

Moss Adams | Under the Microscope | Trends in S-1 Filings • We note your disclosure in this section that you have 20 issued patents. You should disclose in this section the number of issued material patents, if any, covering [product name]. As to each material patent related to [product name], please provide the following information: The expiration date of the patent The jurisdiction covered by the patent The type of protection afforded by each such patent Whether the patent is owned by or licensed to the company As to any licensed material patent related to [product name], please indicate from whom the patent was licensed and describe all material terms of the license agreement, including its duration and any conditions that must be satisfied in order to maintain the license. For example, we note you have a license agreement with [company name] for a patent relating to [product name]; you should fully describe the material terms of this agreement.

Please ensure you address any intellectual property for [product name] relating to the acquisition of [company name] in 2006. Please file all material license agreements as exhibits to your registration statement. Material contract terms are significant because they directly affect a company’s operations and financial position. Disclosure of terms and agreements must be filed as an exhibit in accordance with Item 601 of Regulation S-K. Material Contracts Life sciences IPO aspirants should disclose the material terms of their contracts beyond basic SEC standards to prevent unforeseen delays in filing.

Disclosure requests from this year, in a continuation of last year’s trend, prioritized the rights and obligations of involved parties, aggregate amounts paid or received under the agreement, royalty rates, duration, and termination-related provisions. Sample Comments • Please describe the material terms of your proposed toll-processing agreement with [company name] and your marketing agreement with [company name]. Clarify, if true, that the memorandum of understanding for the toll-processing agreement is not an enforceable agreement and that there is no assurance you will actually enter into an enforceable agreement with [company name]. Also, please tell us what consideration you have given to filing as exhibits the memorandum of understanding, the [company name] agreement, or your agreement with [company name] as exhibits.

See Item 601(b)(10) of Regulation S-K. • Please file your shareholders’ agreement with the researchers at [company name] as an exhibit. Additionally, please disclose the material terms of this agreement in this section. • Please expand your disclosure to describe the material terms of your arrangement with [company name], including the following as may be applicable: Nature and scope of intellectual property rights granted Each party’s rights and obligations Duration of agreement Termination provisions Material payment provisions In addition, please file a copy of each agreement as an exhibit to your registration statement pursuant to Item 601(b)(10) of Regulation S-K. 21 . Moss Adams | Under the Microscope | Trends in S-1 Filings As the capital investments and opportunity costs of developing a new drug skyrocket, companies in the life sciences industry are increasingly engaging in complex license agreements to share product development risks. Terms of License Agreements Companies, particularly in the pharmaceutical preparations and biological products sectors, greatly benefit from licensing technology, products, patents, and branding to reduce costs and share risks. The terms of these agreements directly affect valuations and have a material impact on the company. According to Item 101 of Regulation S-K, registrants are required to disclose in their business description “the importance to the segment and the duration and effect of all patents, trademarks, licenses, franchises, and concessions held.” Item 601(b)(10) also requires all licenses to be filed as exhibits along with the IPO filing. It’s evident from our analysis that the terms of agreements themselves are of prime importance to SEC, and aspiring registrants need to match the expected standard regarding detailed disclosures of all financial, operational, terminating, and other contractual terms of agreements. Sample Comments • Please disclose the total amount of up-front payments you have received under this license agreement and the total amount of potential development, regulatory, and commercial milestone payments you may receive under the agreement. • We note that, in connection with the license agreement, you entered into a letter agreement with [entity name], pursuant to which you assumed [entity name]’s obligation to make a payment to [entity name] arising from the commercialization of products developed using the licensed data. Please expand your disclosure to quantify the amount of this payment. • We note that, as part of your risk-factor discussion, you provided a description of your obligations under your license agreement with [company name].

Please expand your disclosure to also discuss your obligation under your license agreement with [company name]. Management’s Discussion and Analysis The importance of MD&A cannot be understated, considering the in-depth scrutiny seen in the SEC comments in our analysis. Comments focused on topics including results from operations, liquidity and capital resources, and critical accounting policies, centering mainly on registrants’ financial and operational performance, which may be affected by internal and external fluctuations. Any material impact recognized through the management’s analysis needs to be disclosed to the SEC along with details on the accounting policy implemented. Last year, MD&A accounted for 2.9 percent of comments toward S-1 filings, decreasing to 2.6 percent in this year’s analysis. Sample Comments • Please disclose your “burn rate” and the amount of time your present capital will last at this rate, both here as well as in the business and MD&A sections.

In addition, please revise to state how much cash you have on hand as of the most recently practicable date. • With a view toward clarified disclosure, please explain why your products do not require the significant additional capital expenditures by otolaryngologic physicians associated with some competing products. 22 . Moss Adams | Under the Microscope | Trends in S-1 Filings • In light of your significant operating losses in recent periods, please revise to provide a more detailed discussion of the key challenges you face. See Section III.A of SEC Release No. 33-8350. In light of the risks, competition, and nature of the life sciences industry, directors not only need to be competent but also experienced. After all, the risks associated with strategic mismanagement are considerable.

Decisions should be in tandem with the expectations of the stakeholders. For companies looking to go public, the SEC’s role is to ensure adequate transparency on registrants’ directors. This level of importance is visible in our analysis, which shows a move from 1 percent to 2 percent of overall comments in this category from last year. Disclosures About Directors In accordance with Item 401(e) of Regulation S-K, the SEC this year requested aspiring registrants to add a brief on the “specific experience, qualifications, attributes or skills that led to the conclusion that each of the directors should serve as a director for [the company] in light of [its] business and structure.” The nature of comments was direct, and the regulation serves to prevent any unethical standards along with conflicts of interest that may have adverse effects on a publicly owned company. Sample Comments • Please revise to briefly describe the business experience during the past five years of all your executive officers and directors.

In addition, please discuss specific experience, qualifications, attributes or skills of your directors. Refer to Item 401(e) of Regulation S-K. • If you intend for this table to include the information about selling stockholders, as required by Item 507 of Regulation S-K, as well as certain beneficial owners, as required by Item 403 of Regulation S-K, please: Revise the introductory language under this caption to clarify that the table also includes beneficial ownership information for officers, directors, director nominees, and holders of more than 5 percent of your common stock. If any person whose share ownership should be reported under Item 403 is not also a selling stockholder, please ensure that you have also included them in the table. Add the beneficial share ownership of your two nominated directors, [person name] and [person name], to the selling shareholders table.

For example, we note that [person name] is the president of [company name], which owns [number] common shares prior to this offering. See Item 403(b) of Regulation S-K. Disclose the shares beneficially owned, both as a sum and a percentage of outstanding shares, by your named executive officers and nominated directors as a group. See Item 403(b) of Regulation S-K. 23 .

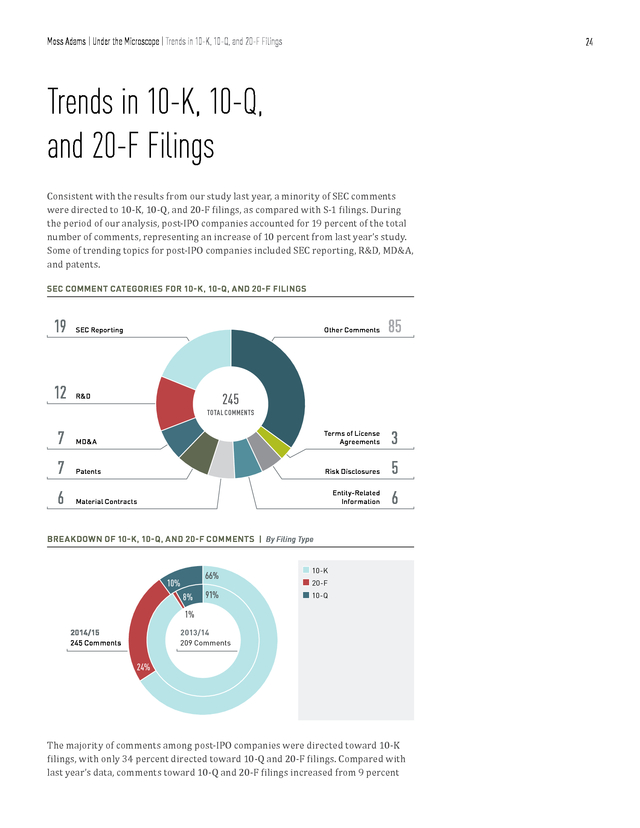

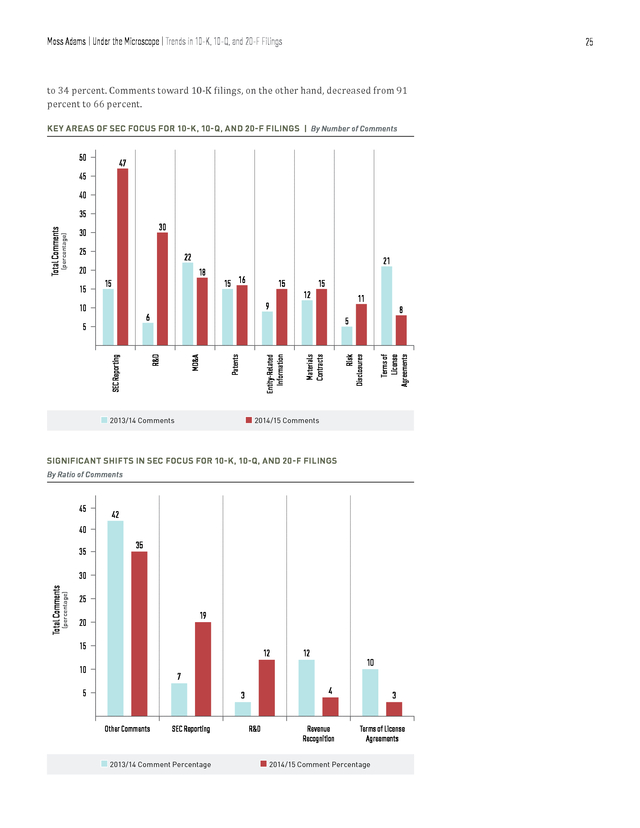

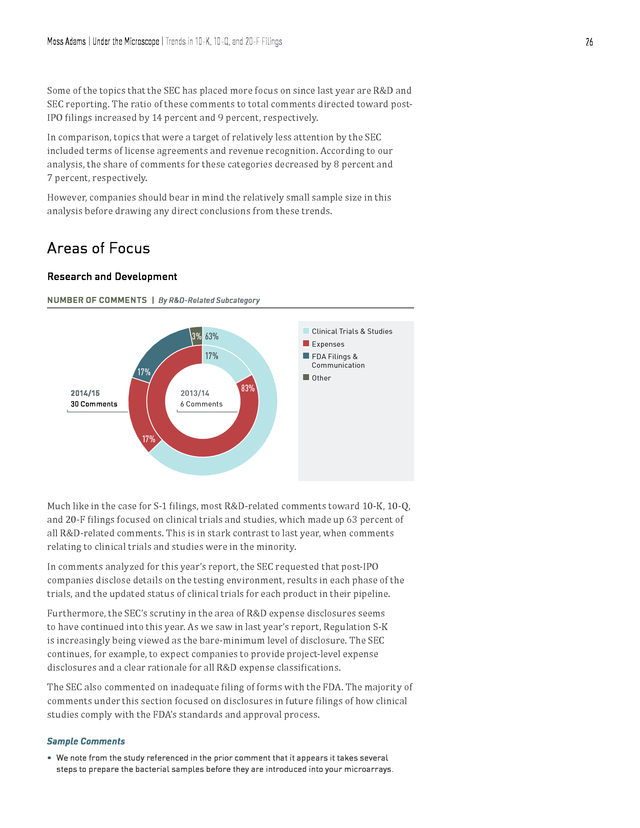

Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 24 Trends in 10-K, 10-Q, and 20-F Filings Consistent with the results from our study last year, a minority of SEC comments were directed to 10-K, 10-Q, and 20-F filings, as compared with S-1 filings. During the period of our analysis, post-IPO companies accounted for 19 percent of the total number of comments, representing an increase of 10 percent from last year’s study. Some of trending topics for post-IPO companies included SEC reporting, R&D, MD&A, and patents. SEC COMMENT CATEGORIES FOR 10-K, 10-Q, AND 20-F FILINGS 19 SEC Reporting 12 Other Comments R&D 85 245 TOTAL COMMENTS 7 MD&A Terms of License Agreements 3 7 Patents Risk Disclosures 5 6 Material Contracts Entity-Related Information 6 BREAKDOWN OF 10-K, 10-Q, AND 20-F COMMENTS | By Filing Type 66% 10% 8% 91% n 10-K n 20-F n 10-Q 1% 2014/15 2013/14 245 Comments 209 Comments 24% The majority of comments among post-IPO companies were directed toward 10-K filings, with only 34 percent directed toward 10-Q and 20-F filings. Compared with last year’s data, comments toward 10-Q and 20-F filings increased from 9 percent . Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 25 to 34 percent. Comments toward 10-K filings, on the other hand, decreased from 91 percent to 66 percent. KEY AREAS OF SEC FOCUS FOR 10-K, 10-Q, AND 20-F FILINGS | By Number of Comments 50 47 45 40 30 30 25 22 20 15 15 16 15 15 12 11 9 8 6 n 2013/14 Comments Risk Disclosures Materials Contracts Entity-Related Information R&D SEC Reporting 5 5 Terms of License Agreements 10 Patents 15 21 18 MD&A (percentage) Total Comments 35 n 2014/15 Comments SIGNIFICANT SHIFTS IN SEC FOCUS FOR 10-K, 10-Q, AND 20-F FILINGS By Ratio of Comments 45 42 40 35 35 (percentage) Total Comments 30 25 19 20 15 12 10 12 10 7 5 4 3 Other Comments SEC Reporting n 2013/14 Comment Percentage R&D Revenue Recognition 3 Terms of License Agreements n 2014/15 Comment Percentage . Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 26 Some of the topics that the SEC has placed more focus on since last year are R&D and SEC reporting. The ratio of these comments to total comments directed toward postIPO filings increased by 14 percent and 9 percent, respectively. In comparison, topics that were a target of relatively less attention by the SEC included terms of license agreements and revenue recognition. According to our analysis, the share of comments for these categories decreased by 8 percent and 7 percent, respectively. However, companies should bear in mind the relatively small sample size in this analysis before drawing any direct conclusions from these trends. Areas of Focus Research and Development NUMBER OF COMMENTS | By R&D-Related Subcategory n Clinical Trials & Studies n Expenses n FDA Filings & 3% 63% 17% Communication 17% 2014/15 2013/14 30 Comments 83% n Other 6 Comments 17% Much like in the case for S-1 filings, most R&D-related comments toward 10-K, 10-Q, and 20-F filings focused on clinical trials and studies, which made up 63 percent of all R&D-related comments. This is in stark contrast to last year, when comments relating to clinical trials and studies were in the minority. In comments analyzed for this year’s report, the SEC requested that post-IPO companies disclose details on the testing environment, results in each phase of the trials, and the updated status of clinical trials for each product in their pipeline. Furthermore, the SEC’s scrutiny in the area of R&D expense disclosures seems to have continued into this year.

As we saw in last year’s report, Regulation S-K is increasingly being viewed as the bare-minimum level of disclosure. The SEC continues, for example, to expect companies to provide project-level expense disclosures and a clear rationale for all R&D expense classifications. The SEC also commented on inadequate filing of forms with the FDA. The majority of comments under this section focused on disclosures in future filings of how clinical studies comply with the FDA’s standards and approval process. Sample Comments • We note from the study referenced in the prior comment that it appears it takes several steps to prepare the bacterial samples before they are introduced into your microarrays. .

Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 27 Please tell us and revise future filings to disclose the steps necessary prior to the automated microscopy, the amount of time necessary to perform those steps, and whether you intend to automate those steps. • Please revise your disclosure to address whether any of your Phase II studies included efficacy-related endpoints or control groups. If not, disclose why this is the case and whether the study designs were approved by the FDA. • You disclose that your R&D expenses include regulatory consulting and legal counsel. Please tell us the activities undertaken by your regulatory consultants and legal counsel and why their fees qualify as R&D under ASC 730-10-20. In your response, specifically explain how their activities are indicative of discovering new knowledge or applying new knowledge to new products and why these activities are not general or administrative in nature.

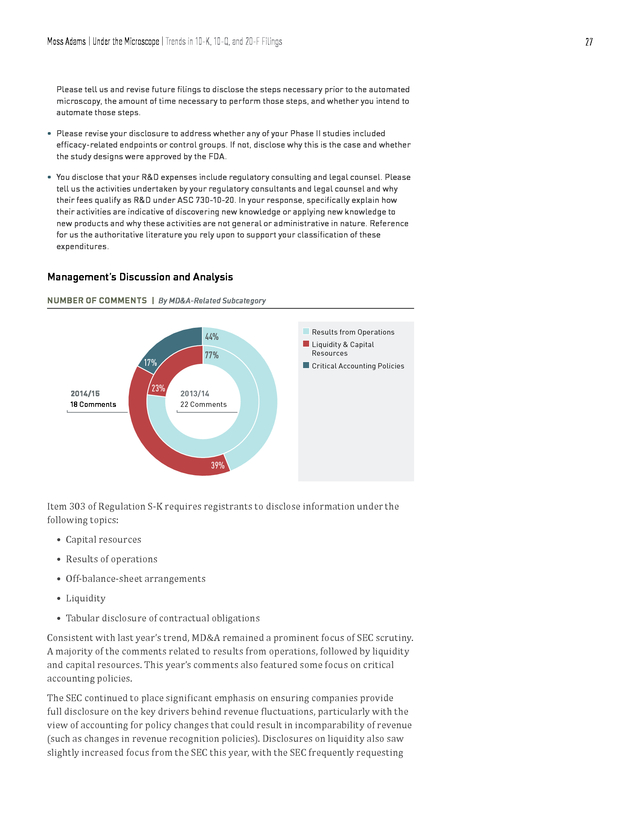

Reference for us the authoritative literature you rely upon to support your classification of these expenditures. Management’s Discussion and Analysis NUMBER OF COMMENTS | By MD&A-Related Subcategory 44% 17% 2014/15 23% 18 Comments 77% n Results from Operations n Liquidity & Capital Resources n Critical Accounting Policies 2013/14 22 Comments 39% Item 303 of Regulation S-K requires registrants to disclose information under the following topics: • Capital resources • Results of operations • Off-balance-sheet arrangements • Liquidity • Tabular disclosure of contractual obligations Consistent with last year’s trend, MD&A remained a prominent focus of SEC scrutiny. A majority of the comments related to results from operations, followed by liquidity and capital resources. This year’s comments also featured some focus on critical accounting policies. The SEC continued to place significant emphasis on ensuring companies provide full disclosure on the key drivers behind revenue fluctuations, particularly with the view of accounting for policy changes that could result in incomparability of revenue (such as changes in revenue recognition policies). Disclosures on liquidity also saw slightly increased focus from the SEC this year, with the SEC frequently requesting .

Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings that companies disclose the material effects planned capital expenses may have on future liquidity. Sample Comments • We see that you attribute the decline in product revenues to the “product mix,” “anticipated timing associated with larger system–related sales,” and the “new revenue recognition policy in 2014 for new customers.” In future filings please quantify the impact of each significant item that impacts the comparability of revenues. In addition, to the extent you reference product mix, please provide an indication of the composition of revenue for each period so that investors can understand how product mix shifted and contributed to the fluctuation in revenues. • Please provide a proposed revised disclosure of the changes in your product sales, period over period, that clearly delineates and quantifies the changes related to new product launches and price versus volume changes for existing products. Please see Item 303(a)(3)(iii) of Regulation S-K. • You disclose that the term loan is expected to provide sufficient liquidity, and you discuss the scale-up of manufacturing in Exhibit 99.1 of Form 8-K, which was filed [date]. Please discuss your material planned capital expenditures in this regard and any known trends, events, or uncertainties reasonably likely to have material future effects on your financial condition in future filings.

Refer to Item 303(a)(2)(i) of Regulation S-K. Other Disclosure Topics Comments in this section centered on the filing of exhibits and other material, requests for confidential treatment, demands for updated disclosures and clarifications, reasons for discrepancies, and acceptance of liability. The share of comments relating to SEC reporting for post-IPO companies increased by approximately 9 percent from last year. This further demonstrates that companies cannot disregard the need to devote sufficient attention to meeting the instructions and format prescribed in Regulation S-K. SEC Reporting Sample Comments • You disclose that [company name] has refused to reissue its audit report due to a disagreement related to outstanding service fees.

You indicated, however, in your Item 4.01 on Form 8-K, originally filed September 19, 2014, and subsequently amended October 1, 2014, and October 7, 2014, that the disagreement related to your refusal to grant access to online banking accounts. Please explain this apparent discrepancy to us. • We note there are additional exhibits that still need to be filed. Please provide these exhibits as promptly as possible and note we may have comments on these materials once they are provided. 28 .

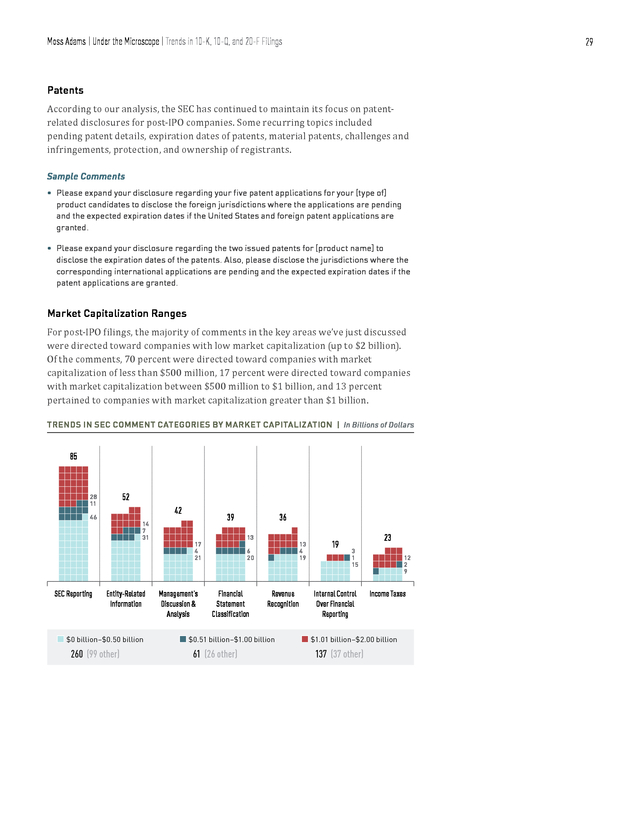

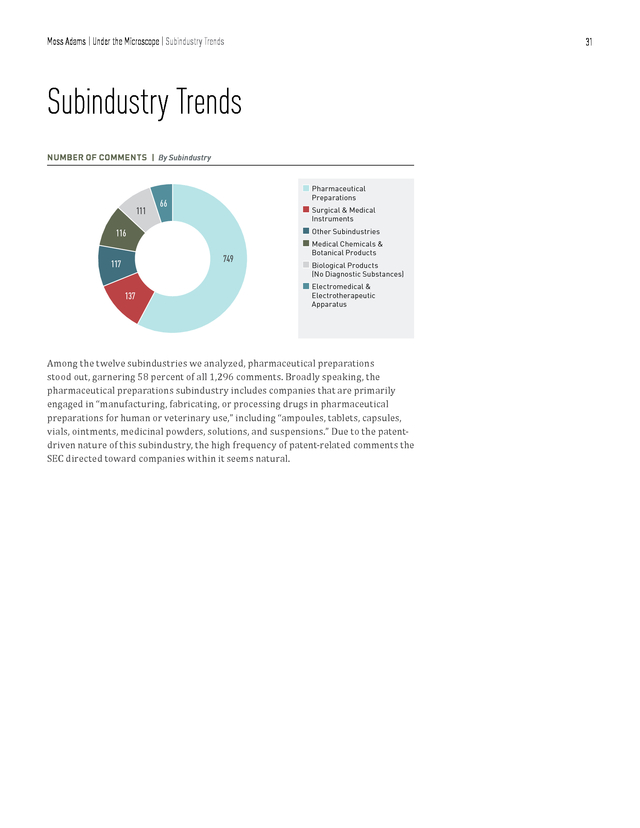

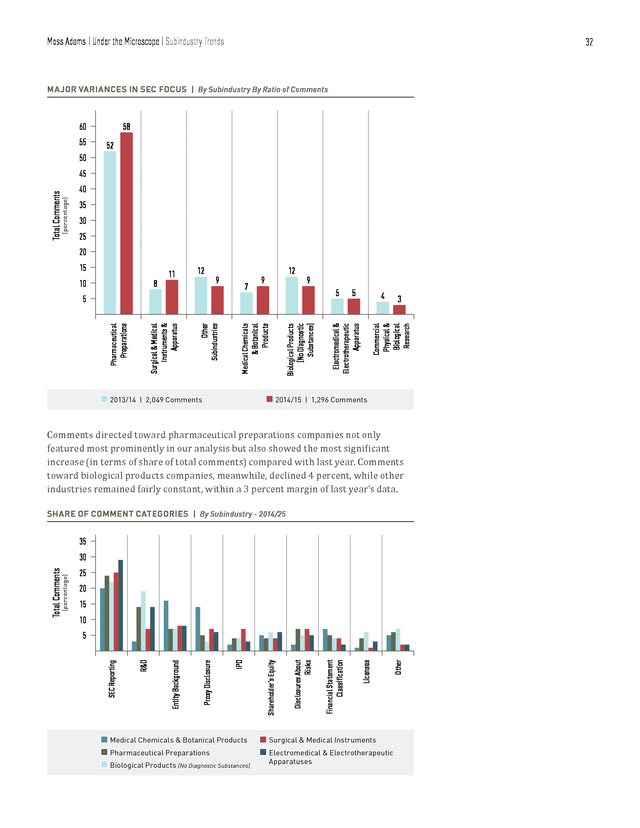

Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 29 According to our analysis, the SEC has continued to maintain its focus on patentrelated disclosures for post-IPO companies. Some recurring topics included pending patent details, expiration dates of patents, material patents, challenges and infringements, protection, and ownership of registrants. Patents Sample Comments • Please expand your disclosure regarding your five patent applications for your [type of] product candidates to disclose the foreign jurisdictions where the applications are pending and the expected expiration dates if the United States and foreign patent applications are granted. • Please expand your disclosure regarding the two issued patents for [product name] to disclose the expiration dates of the patents. Also, please disclose the jurisdictions where the corresponding international applications are pending and the expected expiration dates if the patent applications are granted. For post-IPO filings, the majority of comments in the key areas we’ve just discussed were directed toward companies with low market capitalization (up to $2 billion). Of the comments, 70 percent were directed toward companies with market capitalization of less than $500 million, 17 percent were directed toward companies with market capitalization between $500 million to $1 billion, and 13 percent pertained to companies with market capitalization greater than $1 billion. Market Capitalization Ranges TRENDS IN SEC COMMENT CATEGORIES BY MARKET CAPITALIZATION | In Billions of Dollars 85 28 11 46 SEC Reporting 52 42 14 7 31 Entity-Related Information n $0 billion–$0.50 billion 260 (99 other) 39 17 4 21 Management’s Discussion & Analysis 36 13 13 4 19 6 20 Financial Statement Classification Revenue Recognition n $0.51 billion–$1.00 billion 61 (26 other) 19 23 3 1 15 Internal Control Over Financial Reporting 12 2 9 Income Taxes n $1.01 billion–$2.00 billion 137 (37 other) . Moss Adams | Under the Microscope | Trends in 10-K, 10-Q, and 20-F Filings 30 BREAKDOWN OF 10-K, 10-Q, AND 20-F COMMENTS | By Market Capitalization Range 70% 13% 11% 66% 2014/15 $0 billion–$0.5 billion $0.51 billion–$1 billion $1.01 billion–$2 billion 2013/14 245 Comments n n n 122 Comments 17% 23% As was the case last year, the majority of SEC comments this year were targeted toward the bottom 50th percentile (in terms of market capitalization) of postIPO companies. One inference we can draw from this is less operationally mature companies have yet to establish the standard of governance and compliance frameworks to fully meet the SEC’s expectations in their first attempt at filings. However, the results might simply reflect the current, natural market-cap distribution among life sciences companies—that there are more small marketcap companies than medium market-cap companies. In any event, a thorough understanding of the SEC’s disclosure standards will smooth the filing process. . Moss Adams | Under the Microscope | Subindustry Trends 31 Subindustry Trends NUMBER OF COMMENTS | By Subindustry n Pharmaceutical 111 Preparations 66 n Surgical & Medical Instruments n Other Subindustries n Medical Chemicals & 116 749 117 Botanical Products n Biological Products (No Diagnostic Substances) 137 n Electromedical & Electrotherapeutic Apparatus Among the twelve subindustries we analyzed, pharmaceutical preparations stood out, garnering 58 percent of all 1,296 comments. Broadly speaking, the pharmaceutical preparations subindustry includes companies that are primarily engaged in “manufacturing, fabricating, or processing drugs in pharmaceutical preparations for human or veterinary use,” including “ampoules, tablets, capsules, vials, ointments, medicinal powders, solutions, and suspensions.” Due to the patentdriven nature of this subindustry, the high frequency of patent-related comments the SEC directed toward companies within it seems natural. . Moss Adams | Under the Microscope | Subindustry Trends 32 MAJOR VARIANCES IN SEC FOCUS | By Subindustry By Ratio of Comments 58 60 55 52 50 (percentage) Total Comments 45 40 35 30 25 20 11 12 9 7 12 9 9 5 n 2013/14 Biological Products (No Diagnostic Substances) Medical Chemicals & Botanical Products Other Subindustries Surgical & Medical Instruments & Apparatus Pharmaceutical Preparations 5 n 2014/15 | 2,049 Comments 5 4 3 Commercial Physical & Biological Research 8 10 Electromedical & Electrotherapeutic Apparatus 15 | 1,296 Comments Comments directed toward pharmaceutical preparations companies not only featured most prominently in our analysis but also showed the most significant increase (in terms of share of total comments) compared with last year. Comments toward biological products companies, meanwhile, declined 4 percent, while other industries remained fairly constant, within a 3 percent margin of last year’s data. SHARE OF COMMENT CATEGORIES | By Subindustry - 2014/25 35 20 15 10 Other Licenses Financial Statement Classification Disclosures About Risks Shareholder’s Equity IPO Proxy Disclosure Entity Background R&D 5 SEC Reporting (percentage) Total Comments 30 25 n Medical Chemicals & Botanical Products n Surgical & Medical Instruments n Pharmaceutical Preparations n Electromedical & Electrotherapeutic Apparatuses n Biological Products (No Diagnostic Substances) . Moss Adams | Under the Microscope | Subindustry Trends While still broadly categorized as a part of the life sciences industry, each subindustry is ultimately host to its own regulatory, market, and operating environment. It follows then that the nature of SEC scrutiny for each subindustry varies accordingly. The results of our analysis support this conclusion, with the SEC applying varying degrees of weight to particular topics in the context of each subindustry. R&D-related disclosures accounted for around 15 percent of the total comments for biological products and electromedical and electrotherapeutic apparatus, and they accounted for more than 18 percent for pharmaceutical preparations.

For medical chemicals and botanical products, a significantly larger number of comments—15 percent—were related to entity disclosures, but risk disclosures accounted for less than 5 percent of the comments. The takeaway is that SEC scrutiny and comments are influenced by the subindustry and nature of operations. A company engaging in R&D of biological products should expect heavier scrutiny around entity disclosures and clinical trials than a company producing surgical apparatus. 33 . Moss Adams | Under the Microscope | Conclusion 34 Conclusion As is evident from recent industry trends, life sciences companies are currently facing challenges on numerous fronts. Competition has increased, partly due to the expiration of patents and shorter product life cycles. There are signs that expected returns on late-stage pipeline projects are dropping just as development costs for new products are rising, placing additional pressure on bottom lines. Additionally, as the industry shifts from a volume-based paradigm to a value-based one, standards prescribed by the FDA, European Medicines Agency, and other regulators are evolving accordingly.

And as we’ve seen from the sample comments in this report, the SEC has heightened its scrutiny in line with these developments. What this means for life sciences companies is that even as they deal with latent competitive pressures, they also need to take care to avoid unneeded inefficiencies and operational delays in the filing process. The best way to do this is by anticipating the nature of the SEC’s scrutiny and taking steps to generate complete, welldocumented data and disclosures in advance of their filings. In our findings, the SEC required a wide range of specific clarifications from companies. Recognizing these trends will help you determine where your focus is best applied, leading to greater efficiency in the draft statement filing process. Topics that companies across subindustries should be especially mindful of include R&D (specifically results of clinical trials), information on products and services and collaborative arrangements, financial and operational risks, and patent-related disclosures.

Additionally, paying attention to simple administrative requirements— such as filing the appropriate exhibits or providing the right people’s signatures— can save companies significant amounts of time and effort in redrafting their filings. The mid-cap companies in the scope of our analysis and the aspirants currently in the process of filing with the SEC are sometimes unfamiliar with the comprehensiveness and complexity of the SEC’s requirements. The process is getting only more difficult and more resource intensive, and the costs of administrative inefficiency and delays can run high. For this reason, it’s imperative that companies do what they can to get it right the first time, finding suitable specialists to provide oversight and efficiency in the process. To gain more insight into the SEC’s comment process, or for help preparing your company for its IPO, contact a Moss Adams life sciences professional in your region: Pacific Northwest Southern California FINDLEY GILLESPIE, PARTNER CARISA WISNIEWSKI, PARTNER (206) 302-6212 (858) 627-1402 findley.gillespie@mossadams.com carisa.wisniewski@mossadams.com Northern California All Other Locations RICHARD CROGHAN, PARTNER ERIC MILES, NATIONAL PRACTICE LEADER (415) 677-8282 (408) 916-0571 richard.croghan@mossadams.com eric.miles@mossadams.com .

Moss Adams | Under the Microscope | About Moss Adams About Moss Adams Moss Adams LLP is a national leader in assurance, tax, consulting, risk management, transaction, and private client services. Our integrated service approach provides our clients with functional expertise, industry knowledge, and specialized services to help them overcome financial challenges and take advantage of valuable opportunities. Our Life Sciences Practice serves organizations of all sizes—from large multinational companies and publicly traded middle-market corporations to private firms and start-ups. Our clients specialize in many areas, including: • Biotechnology • Diagnostics • Medical devices • Pharmaceuticals • Digital health We bring deep resources and industry expertise to help our clients at every step of their business life cycle, whether they’re facing an audit, needing to reduce risk, or preparing for an IPO. Ours is also the only middle-market firm with five professionals who served two-year terms as fellows at the SEC. Put our knowledge to work for you.

Learn more at www.mossadams.com/lifesciences. 35 .

It’s possible, therefore, that there are a number of companies currently in the process of preparing for their IPOs. For these companies, understanding the nature of SEC scrutiny toward financial filings is of great importance. The life sciences environment is also becoming increasingly competitive, partly due to the expiration of several patents and progressively shorter product life cycles. A recent study of 12 large, global life sciences companies found that their expected return on late-stage pipeline projects declined over the four-year period from early 2010 to late 2013, from 11 percent to 5 percent. Over the same period, the cost to develop and launch new medicines increased by 18 percent, to $1.3 billion.

Given this operationally strenuous environment, it’s become critical that companies avoid additional inefficiencies and operational delays when they can. Delays in SEC filings can create significant rollover effects throughout the product development pipeline, and to avoid this, companies need to be aware of accounting issues their peers have struggled with. Furthermore, evolving industry dynamics are resulting in greater SEC scrutiny in several areas. Due to the rising capital investment requirements to develop new products, companies are increasingly strategizing around mergers and acquisitions to acquire license agreements, share research and development (R&D) risks, restock depleted pipelines, and save costs by pooling their resources.

Stakeholders are also increasingly looking toward value-based care rather than volume-based care, and the quality of clinical trial results is becoming more important in leveraging competitive advantages. These trends were reflected in SEC comments during the period of our review, with frequent requests for greater transparency in terms of license agreements, results from clinical trials, and risks to consumers. What this means for life sciences companies is that as the SEC adjusts its scrutiny levels to meet this new reality, companies will do well to anticipate it while drafting their filings. This report is an analysis of the nature of SEC comments, comparing this year’s patterns with those identified last year. We hope middle-market life sciences companies, both pre- and post-IPO, will benefit from the actionable data provided here, and use these insights to reduce S-1, 10-K, 10-Q, and 20-F filing inefficiency. ERIC MILES, PARTNER National Practice Leader (408) 916-0571 eric.miles@mossadams.com RICHARD CROGHAN, PARTNER Northern California Practice Leader, Life Sciences (415) 677-8282 richard.croghan@mossadams.com FINDLEY GILLESPIE, PARTNER Pacific Northwest Practice Leader, Life Sciences (206) 302-6212 findley.gillespie@mossadams.com CARISA WISNIEWSKI, PARTNER Southern California Practice Leader, Life Sciences (858) 627-1402 carisa.wisniewski@mossadams.com .

Moss Adams | Under the Microscope | Methodology 4 Methodology To perform our analysis, we categorized all SEC comments directed toward companies in select life sciences subindustries during the period of our review. The following subindustries (as identified by their EDGAR SIC code) were covered in our analysis: EDGAR SIC Code Subindustry 2833 Medical Chemicals & Botanical Products 2834 Pharmaceutical Preparations 2835 In Vitro & In Vivo Diagnostics Substances 2836 Biological Products (No Diagnostic Substance) 3826 Laboratory Analytical Instruments 3841 Surgical & Medical Instruments & Apparatus 3842 Orthopedic, Prosthetic & Surgical Appliances & Supplies 3843 Dental Equipment & Supplies 3844 X-Ray Apparatuses & Tubes & Related Irradiation Apparatus 3845 Electromedical & Electrotherapeutic Apparatus 3851 Ophthalmic Goods 8731 Commercial Physical & Biological Research Comments for the following SEC filings were considered: S-1 (pages 10–23) 10-K 10-Q 20-F (pages 24–30) Because the focus of our study was middle-market companies, we excluded comments related to companies with market capitalizations greater than $2 billion (as of the date of analysis) from our research and assessment. Our analysis included comments filed on the SEC EDGAR database during the period from May 1, 2014, to April 30, 2015 (which we’ll refer to from here on as 2014/15). In order to achieve a fair and objective assessment of the data, we considered only the first instance of an SEC comment letter for an individual filing, given that in subsequent instances, letters from the SEC often contained comments of similar nature to those found in the first iteration. It should be noted that the period under analysis in last year’s report (2013/14) was approximately 14.5 months as compared to 12 months for this year’s report. Readers should bear this in mind before making direct comparisons in terms of the absolute number of comments from last year to this year.

To address this discrepancy, we used a ratio-based methodology to generate comparable data. We considered cases in which shifts in comment ratios in a given subset of comments (from last year to this year) exceeded the mean variance in that subset to be “significant” variances from last year. For example, out of 1,840 comments directed toward S-1 filings in 2013/14, 155 were related to R&D, amounting to a ratio of a little over 8 percent. The same ratio increased to a little under 13 percent .

Moss Adams | Under the Microscope | Methodology in 2014/15, signifying an increase of approximately 4 percent. Because this was greater than the mean variance among other topics in S-1 filings, we considered the variance in R&D-related comments toward S-1 filings to be significant. Last, some of the comments in this report have been edited in the interests of clarity and brevity. Identifiable information, such as company name, dollar figures, product names, and place names, have therefore been omitted in the SEC sample comment sections. 5 . Moss Adams | Under the Microscope | Executive Summary 6 Executive Summary Overview of Trends The objective of this report is to analyze S-1, 10-K, 10-Q, and 20-F filings made by life sciences companies during the 12-month review period from May 1, 2014, to April 30, 2015. As part of our analysis, we categorized SEC comments directed toward these filings and analyzed frequencies of categories to deduce the most prominent topics under SEC scrutiny. The following infographic depicts the results of this analysis: OVERVIEW OF SEC COMMENT CATEGORIES 304 SEC Reporting Other Comments Research & Development 103 Entity-Related Information 95 Risk Disclosures 27 Terms of License Agreements 39 Management’s Discussion & Analysis 45 Material Contracts 50 51 Patents 163 Disclosures About Directors IPO-Related Disclosures 1,296 367 52 TOTAL COMMENTS Aside from SEC reporting1 , R&D—including clinical trials and studies, R&D expenses, and Food and Drug Administration (FDA) filings and communication— was an extremely prominent topic of SEC scrutiny this year. This was followed by entity-related information, risk disclosures, patents, IPO-related disclosures, and material contracts. Other categories included management’s discussion and analysis (MD&A), terms of license agreements, and disclosures about directors. Comments related to SEC reporting tend to be more administrative and formulaic, but because of the sheer volume of such comments, companies have an opportunity to significantly reduce filing delays by understanding the nature of the SEC’s comments under this topic and taking the appropriate steps to comply. 1 .