Description

Change your Experience of Financial Printing

Making the right call?

The experts:

Telecoms M&A in 2015

1.

2.

MM

MM

IB

JB

The telecoms sector is undergoing substantial changes, as the industry players

get to grips with fast-evolving technology, tough regulators and changing consumer

tastes. But how are these factors changing M&A? Toppan Vite, in partnership with

Mergermarket, asked four industry-leading figures for their thoughts.

Mergermarket: From your perspective, what has

been happening in the telecoms dealmaking

arena so far in 2015 in terms of activity,

compared with the year before?

Our TMT practice as a whole has seen an increase

in activity this year. Within telecoms, however, we are

seeing fewer deals. I believe that this is a reflection

of the consolidation that has already occurred.

There are simply fewer mid-sized targets out there than there were several years ago. For me, dealmaking activity in telecoms has certainly rebounded from where it was last year. The deals we are working on at the moment are both announced and unannounced, and there are a couple of drivers 1 Making the right call? Telecoms M&A in 2015 behind them. One of these is bundling – indeed, we’ve seen recently the stock prices of content providers getting hammered.

At the moment there are a lot of unknowns in the market, and no one wants to be behind the curve. MC Looking at Europe, telecoms is still a very active sector. We’ve seen a lot of big mobile deals, and there is plenty of discussion about what is to come – perhaps Liberty and Vodafone. In the last three or four years, the types of deals being done have got a lot more interesting. The first few years were mobile consolidation. Now, the trend is towards investing in content delivery and advertising and in multi-play positions. We’re seeing this in Belgium, where Telenet is picking 3. 4. 1.

Ian Blasco (IB) Partner Riverside Partners 2. John Beahn (JB) Counsel Skadden, Arps, Slate, Meagher & Flom LLP 3. Miranda Cole (MC) Partner Covington & Burling 4.

Marc Leaf (ML) Partner Drinker Biddle . 2 What effect are antitrust concerns having on telecoms dealmaking? JB In the US, the Department of Justice takes a close look at any deal involving consolidation of distributors of content or holders of commercial spectrum licenses. We’ve seen that recently with announced cable deals and rumored wireless deals. Antitrust regulators can stop these deals in their tracks. Increased antitrust scrutiny in Europe is certainly an issue in the telecoms space, but (European Commissioner for Competition) Margrethe Vestager’s focus on a combined company’s power to raise prices is in fact a highly traditional approach to pre-merger review. A greater concern may be the EU’s recent inquiries into standard business practices such as volume pricing and rebates in the original equipment manufacturer’s supply-chain. In the current climate, potential regulatory exposure is a risk that may be particularly difficult to diligence. Meanwhile, in the US, regulators have shown a willingness to advance more creative theories of market power in pre-merger review, adding to execution risk even in cases in which there is little or no direct competition between merger parties. MC ML MM ML up Base in a deal.Essentially, there are two things happening.

One, multi-platform combinations — which are making the access routes higher — and two, vertical integration. It started with the Austrian mobile deal, which became a template for a series of deals where similar remedies were offered. The commission has since looked at whether these remedies Marc Leaf: We’re seeing a strong uptick in deal activity across the board, with buyers opportunistic and sellers anxious to catch the current wave of demand. Making the right call? Telecoms M&A in 2015 . were effective, and recent developments (namely TeliaSonera/Telenor) suggest that the bar has been raised. For those kind of horizontal deals, companies might need to think more broadly about regulatory concerns. Though OFCOM in the UK, for instance, approved to BT-EE deal despite worries. Regulators are pragmatic and are realistic when looking at alleged concerns. They are not killing deals, but they are performing their function. MM IB How are companies responding to consumers’ increasing preference for bundled telecoms and TV services, and how is this affecting dealmaking? Consumers are continuing to go for bundled packages. As this goes on, old business lines will start to crumble. For example, one of our portfolio companies has several university clients for bandwidth solutions.

In the past, they sought data only but are increasingly seeking a bundled data and video solution. To service this demand, we had to form partnerships with video providers in order to provide the full bundle of desired services. This shift is happening not just in enterprise, but also on the consumer side. And as consumers want more bundles, the more these kind of partnerships and takeovers will go on. 3 Making the right call? Telecoms M&A in 2015 “ We’re in a world where content providers can easily access the internet and broadcast.

Controlling more of the market with this in mind is critical. Ian Blasco, Riverside Partners ” . JB MC ML It’s hard to judge – it is somewhat of a known unknown. But it’s certainly an issue companies are aware of. With ‘cutting the cord’, so to speak, even with consumers wanting to get a bundle package, they will need a cord. However, with there being a resistance to bundled cable firms, they are wondering how to compete in a non-bundled world.They need to make sure they can compete. In terms of wireless, the big deals in a sense have already been done, so we’ll probably be seeing more and more ‘bolt-on’ deals – filling in the gaps, so to speak. We’ve already seen this with companies such as Verizon adding spectrum, and spectrum swaps taking place. They don’t care whether they get their bits by Wi-Fi, cellular, fiber, or whatever technology is just around the corner.

Consumers choose bundling when it results in lower pricing or greater value. Providers drive bundled service offerings because it helps cut-down churn. MM What is driving the spate of megadeals this year, such as the BT-EE, Alcatatel-Nokia and Charter Comms-Time Warner deals? I’m not sure that consumers do prefer to bundle their telecoms and TV services, to be honest. Consumers want the ability to access information, communications, and entertainment at anytime, anywhere, from any device. 4 Making the right call? Telecoms M&A in 2015 It’s about pursuing scale. We’re in a world where content providers can easily access the internet and broadcast.

Controlling more of the market with this in mind is critical. ML People are suggesting that the Telenet deal is a guinea pig – testing how the Commission will view multi-play (rather than mobile-to-mobile) deals. Service providers want to develop relationships with users so that whatever device they have on their ‘pipe’ – whether it be TV, PC, tablet, mobile – they get comparable content and services. This is something that will continue as consumers move in this direction. IB John Malone (famed telecoms executive) predicted the current wave of consolidation two years ago. He cited economies of scale and the ability of larger players to make the large investments in technology and infrastructure needed to meet consumer demand for faster broadband speeds. MC If you look at what BT are doing, they are following a similar pattern to Telenet with Base. BT is turning itself into a multi-play provider that is able to provide non-linear TV voice and with fixed and mobile broadband. JB The recent cable transactions were in part a reaction on the cable side.

If you think about it, the cable companies such as Charter . . Communications get their content from firms such as Time Warner and Fox, which have grown over the years by acquiring more content. For cable, they need to be able to display that they have the consumers to view the content being offered. Deals like this provide more leverage for them in order to attract that content. The BT and EE deal was really more of a scale issue, and the need to increase speed and coverage. With telecoms being such a competitive market, and to distinguish yourself you need to perform either in terms of price, performance, or both. Wireless companies are quickly realizing that they might not have the capacity to go direct to consumer. If you think of cell phones now, for example, many people now watch most of their content on these devices. MM Where will telecoms M&A become more apparent in 2015? IB We’ll see more deals in the broadband space. Providers are looking for growth, and smaller businesses can provide that with their broadband capabilities.

These kinds of companies will always be attractive to bigger firms. Whether it’s things such as managed services or OTT, it’ll be in demand. JB One aspect people are not focusing on is infrastructure – network equipment, IT infrastructure and the like. It becomes kind of like an arms race 6 Making the right call? Telecoms M&A in 2015 between content providers and carriers.

You will see as carriers are getting bigger, companies will be selling off infrastructure and wanting to keep the digital side. Also, more cross-border M&A is likely. We’ve already seen it with AT&T going into Mexico. Expect to see more transnational networks and services provided by US carriers. “ Wireless companies are quickly realizing that they might not have the capacity to go direct to consumer. If you think of cell phones now, for example, many people now watch most of their content on these devices. ” John Beahn, Skadden .

ML We’ll see a lot of deal activity in digital advertising technologies and other technology providers. MC Control over the access network will continue to be imporant. There is a challenge for regulators in this context that they don’t create a duopoly (in the absense of effective regulation). More vertical integration is also likely. We’ve seen Telecoms players looking at digital advertising and other parts of the “stack” (look at Verizon/AOL). MM MM IB Will we see increasing convergence of TMT companies as ‘quad plays’ become more apparent? IB want to reach customers on several platforms. If you look at AT&T, for example, they are now reaching customers basically on every screen they own – and soon, their appliances and cars. To be honest, I’m not a big believer in quad plays. Wireless is distant from land-line. There is a logic in combining the latter to residence and the wireless to the individual, but putting them together doesn’t make sense to me.

The triple play is a much more compelling case in my opinion. ML JB Convergence is here to stay. A bit is a bit, whether that bit carries a telephone call, text message, data file, web page, or audio-visual content, but whether US broadband providers will continue to acquire mobile telecom providers – or simply partner and re-sell mobile telephony on a co-branded or private label basis, remains to be seen. Like before, this is one of the known unknowns. I think it’s fair to say that in this environment, telecoms companies want diversification. And they 7 Making the right call? Telecoms M&A in 2015 JB How are telecoms companies coping with the need to provide better infrastructure? I’ve seen this pressure first hand.

Two of our telecoms portfolio companies, ITC and FirstLight, have enjoyed success in recent years, both landing big accounts. However, landing big accounts means you have to invest heavily in the infrastructure as well, both in terms of hardware and services. In terms of infrastructure, security is a growing concern. Considering the number of scandals these days involving companies losing customer data, clients want to make sure that the pipelines their information goes down is secure.

This is one area that will grow. But you also have to marry this with quality of service as well. Telcos use infrastructure, and will look at and try to obtain it. One of the issues the industry faces is generation changes.

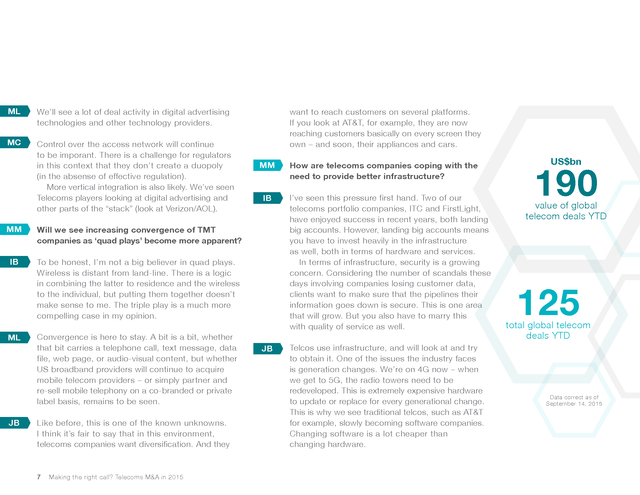

We’re on 4G now – when we get to 5G, the radio towers need to be redeveloped. This is extremely expensive hardware to update or replace for every generational change. This is why we see traditional telcos, such as AT&T for example, slowly becoming software companies. Changing software is a lot cheaper than changing hardware. US$bn 190 value of global telecom deals YTD 125 total global telecom deals YTD Data correct as of September 14, 2015 . ML Obviously, bigger companies can more easily bear the cost of investing in infrastructure. However, the same is true of more efficient companies, and both trends should continue to drive deal activity. MC This debate isn’t only playing out in a deal context – it’s also front and center in the regulatory context. Everyone has heard concerns about whether the network operators can invest to upgrade and keep up with technological advancements. The European Parliament is about to vote on the compromise position on net neutrality. It will be interesting in the coming years to see how that is implemented across the European member states. The language of the proposal leaves quite a lot of room for differing implementation. 8 Making the right call? Telecoms M&A in 2015 “[Radio towers are] extremely expensive hardware to update. This is why we’re seeing traditional telcos, such as AT&T for example, slowly becoming software companies.” John Beahn, Skadden . About Toppan Vite Mail Toppan Vite, a leader in financial printing, is part of the Toppan Printing Group, the world’s largest printing group, headquartered in Tokyo with approximately US$18 billion in annual sales. Our expanding U.S. operations deliver a hasslefree experience for mission-critical content for capital markets transactions, financial reporting and regulatory compliance filings, investment companies and insurance providers. Toppan Vite has been a pioneer and trusted partner in the financial markets for three decades, serving the financial, legal and corporate communities with meticulous, responsive service and unparalleled local market expertise and capabilities. For more information, please contact one of the following Toppan Vite representatives: Digital Asset Management Fulfillment Hive™ Marketing Solutions Print-OnDemand Pre-IPO Due Diligence M&A Due Diligence Corporate Repository Print Hive™ Virtual Data Rooms YOUR ONE STOP RESOURCE FOR CAPITAL MARKET TRANSACTIONS Publishing Typesetting XBRL EDGAR Jeff Riback President JeffRiback@toppanlf.com Ed Vaccaro VP of Operations EdVaccaro@toppanlf.com For more information, please go to www.toppanvite.com/us Stay connected with our linkedin and blog webpages. 9 About Toppan Vite Digital Print Offset Print . Toppan Vite Global Offices New Jersey 109 North 5th Street Saddle Brook, NJ 07663 U.S.A. Email: csnj@toppanlf.com Tel: (1) 800 866 637 New York 747 Third Avenue, 7th Floor New York, NY 10017 U.S.A. Email: cs@toppanlf.com Tel: (1) 212 596 7747 Massachusetts Fulfillment Facility 3 Paterson Road Shirley, MA 01464 Hong Kong Suite 4602, One Exchange Square 8 Connaught Place, Central, Hong Kong Suite 2001, International Commerce Centre 1 Austin Road West, Kowloon, Hong Kong Email: vite-enquiry@toppanleefung.com Tel: (852) 2877 8773 Singapore 3 Church Street #10-03, Samsung Hub, Singapore 049483 Email: vite-enquiry@toppanleefung.com Tel: (65) 6578 6522 10 Toppan Vite Global Offices www.toppanvite.com/us .

There are simply fewer mid-sized targets out there than there were several years ago. For me, dealmaking activity in telecoms has certainly rebounded from where it was last year. The deals we are working on at the moment are both announced and unannounced, and there are a couple of drivers 1 Making the right call? Telecoms M&A in 2015 behind them. One of these is bundling – indeed, we’ve seen recently the stock prices of content providers getting hammered.

At the moment there are a lot of unknowns in the market, and no one wants to be behind the curve. MC Looking at Europe, telecoms is still a very active sector. We’ve seen a lot of big mobile deals, and there is plenty of discussion about what is to come – perhaps Liberty and Vodafone. In the last three or four years, the types of deals being done have got a lot more interesting. The first few years were mobile consolidation. Now, the trend is towards investing in content delivery and advertising and in multi-play positions. We’re seeing this in Belgium, where Telenet is picking 3. 4. 1.

Ian Blasco (IB) Partner Riverside Partners 2. John Beahn (JB) Counsel Skadden, Arps, Slate, Meagher & Flom LLP 3. Miranda Cole (MC) Partner Covington & Burling 4.

Marc Leaf (ML) Partner Drinker Biddle . 2 What effect are antitrust concerns having on telecoms dealmaking? JB In the US, the Department of Justice takes a close look at any deal involving consolidation of distributors of content or holders of commercial spectrum licenses. We’ve seen that recently with announced cable deals and rumored wireless deals. Antitrust regulators can stop these deals in their tracks. Increased antitrust scrutiny in Europe is certainly an issue in the telecoms space, but (European Commissioner for Competition) Margrethe Vestager’s focus on a combined company’s power to raise prices is in fact a highly traditional approach to pre-merger review. A greater concern may be the EU’s recent inquiries into standard business practices such as volume pricing and rebates in the original equipment manufacturer’s supply-chain. In the current climate, potential regulatory exposure is a risk that may be particularly difficult to diligence. Meanwhile, in the US, regulators have shown a willingness to advance more creative theories of market power in pre-merger review, adding to execution risk even in cases in which there is little or no direct competition between merger parties. MC ML MM ML up Base in a deal.Essentially, there are two things happening.

One, multi-platform combinations — which are making the access routes higher — and two, vertical integration. It started with the Austrian mobile deal, which became a template for a series of deals where similar remedies were offered. The commission has since looked at whether these remedies Marc Leaf: We’re seeing a strong uptick in deal activity across the board, with buyers opportunistic and sellers anxious to catch the current wave of demand. Making the right call? Telecoms M&A in 2015 . were effective, and recent developments (namely TeliaSonera/Telenor) suggest that the bar has been raised. For those kind of horizontal deals, companies might need to think more broadly about regulatory concerns. Though OFCOM in the UK, for instance, approved to BT-EE deal despite worries. Regulators are pragmatic and are realistic when looking at alleged concerns. They are not killing deals, but they are performing their function. MM IB How are companies responding to consumers’ increasing preference for bundled telecoms and TV services, and how is this affecting dealmaking? Consumers are continuing to go for bundled packages. As this goes on, old business lines will start to crumble. For example, one of our portfolio companies has several university clients for bandwidth solutions.

In the past, they sought data only but are increasingly seeking a bundled data and video solution. To service this demand, we had to form partnerships with video providers in order to provide the full bundle of desired services. This shift is happening not just in enterprise, but also on the consumer side. And as consumers want more bundles, the more these kind of partnerships and takeovers will go on. 3 Making the right call? Telecoms M&A in 2015 “ We’re in a world where content providers can easily access the internet and broadcast.

Controlling more of the market with this in mind is critical. Ian Blasco, Riverside Partners ” . JB MC ML It’s hard to judge – it is somewhat of a known unknown. But it’s certainly an issue companies are aware of. With ‘cutting the cord’, so to speak, even with consumers wanting to get a bundle package, they will need a cord. However, with there being a resistance to bundled cable firms, they are wondering how to compete in a non-bundled world.They need to make sure they can compete. In terms of wireless, the big deals in a sense have already been done, so we’ll probably be seeing more and more ‘bolt-on’ deals – filling in the gaps, so to speak. We’ve already seen this with companies such as Verizon adding spectrum, and spectrum swaps taking place. They don’t care whether they get their bits by Wi-Fi, cellular, fiber, or whatever technology is just around the corner.

Consumers choose bundling when it results in lower pricing or greater value. Providers drive bundled service offerings because it helps cut-down churn. MM What is driving the spate of megadeals this year, such as the BT-EE, Alcatatel-Nokia and Charter Comms-Time Warner deals? I’m not sure that consumers do prefer to bundle their telecoms and TV services, to be honest. Consumers want the ability to access information, communications, and entertainment at anytime, anywhere, from any device. 4 Making the right call? Telecoms M&A in 2015 It’s about pursuing scale. We’re in a world where content providers can easily access the internet and broadcast.

Controlling more of the market with this in mind is critical. ML People are suggesting that the Telenet deal is a guinea pig – testing how the Commission will view multi-play (rather than mobile-to-mobile) deals. Service providers want to develop relationships with users so that whatever device they have on their ‘pipe’ – whether it be TV, PC, tablet, mobile – they get comparable content and services. This is something that will continue as consumers move in this direction. IB John Malone (famed telecoms executive) predicted the current wave of consolidation two years ago. He cited economies of scale and the ability of larger players to make the large investments in technology and infrastructure needed to meet consumer demand for faster broadband speeds. MC If you look at what BT are doing, they are following a similar pattern to Telenet with Base. BT is turning itself into a multi-play provider that is able to provide non-linear TV voice and with fixed and mobile broadband. JB The recent cable transactions were in part a reaction on the cable side.

If you think about it, the cable companies such as Charter . . Communications get their content from firms such as Time Warner and Fox, which have grown over the years by acquiring more content. For cable, they need to be able to display that they have the consumers to view the content being offered. Deals like this provide more leverage for them in order to attract that content. The BT and EE deal was really more of a scale issue, and the need to increase speed and coverage. With telecoms being such a competitive market, and to distinguish yourself you need to perform either in terms of price, performance, or both. Wireless companies are quickly realizing that they might not have the capacity to go direct to consumer. If you think of cell phones now, for example, many people now watch most of their content on these devices. MM Where will telecoms M&A become more apparent in 2015? IB We’ll see more deals in the broadband space. Providers are looking for growth, and smaller businesses can provide that with their broadband capabilities.

These kinds of companies will always be attractive to bigger firms. Whether it’s things such as managed services or OTT, it’ll be in demand. JB One aspect people are not focusing on is infrastructure – network equipment, IT infrastructure and the like. It becomes kind of like an arms race 6 Making the right call? Telecoms M&A in 2015 between content providers and carriers.

You will see as carriers are getting bigger, companies will be selling off infrastructure and wanting to keep the digital side. Also, more cross-border M&A is likely. We’ve already seen it with AT&T going into Mexico. Expect to see more transnational networks and services provided by US carriers. “ Wireless companies are quickly realizing that they might not have the capacity to go direct to consumer. If you think of cell phones now, for example, many people now watch most of their content on these devices. ” John Beahn, Skadden .

ML We’ll see a lot of deal activity in digital advertising technologies and other technology providers. MC Control over the access network will continue to be imporant. There is a challenge for regulators in this context that they don’t create a duopoly (in the absense of effective regulation). More vertical integration is also likely. We’ve seen Telecoms players looking at digital advertising and other parts of the “stack” (look at Verizon/AOL). MM MM IB Will we see increasing convergence of TMT companies as ‘quad plays’ become more apparent? IB want to reach customers on several platforms. If you look at AT&T, for example, they are now reaching customers basically on every screen they own – and soon, their appliances and cars. To be honest, I’m not a big believer in quad plays. Wireless is distant from land-line. There is a logic in combining the latter to residence and the wireless to the individual, but putting them together doesn’t make sense to me.

The triple play is a much more compelling case in my opinion. ML JB Convergence is here to stay. A bit is a bit, whether that bit carries a telephone call, text message, data file, web page, or audio-visual content, but whether US broadband providers will continue to acquire mobile telecom providers – or simply partner and re-sell mobile telephony on a co-branded or private label basis, remains to be seen. Like before, this is one of the known unknowns. I think it’s fair to say that in this environment, telecoms companies want diversification. And they 7 Making the right call? Telecoms M&A in 2015 JB How are telecoms companies coping with the need to provide better infrastructure? I’ve seen this pressure first hand.

Two of our telecoms portfolio companies, ITC and FirstLight, have enjoyed success in recent years, both landing big accounts. However, landing big accounts means you have to invest heavily in the infrastructure as well, both in terms of hardware and services. In terms of infrastructure, security is a growing concern. Considering the number of scandals these days involving companies losing customer data, clients want to make sure that the pipelines their information goes down is secure.

This is one area that will grow. But you also have to marry this with quality of service as well. Telcos use infrastructure, and will look at and try to obtain it. One of the issues the industry faces is generation changes.

We’re on 4G now – when we get to 5G, the radio towers need to be redeveloped. This is extremely expensive hardware to update or replace for every generational change. This is why we see traditional telcos, such as AT&T for example, slowly becoming software companies. Changing software is a lot cheaper than changing hardware. US$bn 190 value of global telecom deals YTD 125 total global telecom deals YTD Data correct as of September 14, 2015 . ML Obviously, bigger companies can more easily bear the cost of investing in infrastructure. However, the same is true of more efficient companies, and both trends should continue to drive deal activity. MC This debate isn’t only playing out in a deal context – it’s also front and center in the regulatory context. Everyone has heard concerns about whether the network operators can invest to upgrade and keep up with technological advancements. The European Parliament is about to vote on the compromise position on net neutrality. It will be interesting in the coming years to see how that is implemented across the European member states. The language of the proposal leaves quite a lot of room for differing implementation. 8 Making the right call? Telecoms M&A in 2015 “[Radio towers are] extremely expensive hardware to update. This is why we’re seeing traditional telcos, such as AT&T for example, slowly becoming software companies.” John Beahn, Skadden . About Toppan Vite Mail Toppan Vite, a leader in financial printing, is part of the Toppan Printing Group, the world’s largest printing group, headquartered in Tokyo with approximately US$18 billion in annual sales. Our expanding U.S. operations deliver a hasslefree experience for mission-critical content for capital markets transactions, financial reporting and regulatory compliance filings, investment companies and insurance providers. Toppan Vite has been a pioneer and trusted partner in the financial markets for three decades, serving the financial, legal and corporate communities with meticulous, responsive service and unparalleled local market expertise and capabilities. For more information, please contact one of the following Toppan Vite representatives: Digital Asset Management Fulfillment Hive™ Marketing Solutions Print-OnDemand Pre-IPO Due Diligence M&A Due Diligence Corporate Repository Print Hive™ Virtual Data Rooms YOUR ONE STOP RESOURCE FOR CAPITAL MARKET TRANSACTIONS Publishing Typesetting XBRL EDGAR Jeff Riback President JeffRiback@toppanlf.com Ed Vaccaro VP of Operations EdVaccaro@toppanlf.com For more information, please go to www.toppanvite.com/us Stay connected with our linkedin and blog webpages. 9 About Toppan Vite Digital Print Offset Print . Toppan Vite Global Offices New Jersey 109 North 5th Street Saddle Brook, NJ 07663 U.S.A. Email: csnj@toppanlf.com Tel: (1) 800 866 637 New York 747 Third Avenue, 7th Floor New York, NY 10017 U.S.A. Email: cs@toppanlf.com Tel: (1) 212 596 7747 Massachusetts Fulfillment Facility 3 Paterson Road Shirley, MA 01464 Hong Kong Suite 4602, One Exchange Square 8 Connaught Place, Central, Hong Kong Suite 2001, International Commerce Centre 1 Austin Road West, Kowloon, Hong Kong Email: vite-enquiry@toppanleefung.com Tel: (852) 2877 8773 Singapore 3 Church Street #10-03, Samsung Hub, Singapore 049483 Email: vite-enquiry@toppanleefung.com Tel: (65) 6578 6522 10 Toppan Vite Global Offices www.toppanvite.com/us .