Making the break: Selling and disposing non-core and under-performing assets in Japan - September 2015

Mergermarket

Description

Making the break:

Selling and disposing

non-core and under-performing

assets in Japan

September 2015

Second line optional lorem ipsum

B Subhead lorem ipsum, date quatueriure

. Contents

3 Foreword

5

Executive summary

6

Profile of respondents and methodology

9

The business of break-ups: Divestitures in corporate Japan

12

Strategy drives divestitures

14

Internal challenges: Addressing concerns among managers

19

Maintaining the company’s image and other external challenges

20

Consistent portfolio reviews reveal value opportunities

21

A strategy for divesting is as important as one for the buy-side

22

Maximizing price: Considerations for auctions and exclusive negotiations

25

Divestitures remain domestic, but foreign capital shows promise

28

A roadmap to meeting deadlines

30

Making the best of your divestiture

33

Contact Deloitte

34

About Mergermarket

. Foreword

Sharp’s reported spinoff of its LCD panel business. Pioneer’s sale of its disc-jockey

equipment line. A comprehensive restructuring at Sony to separate its TV business

and sell its ailing PC division. These are just a few of the deals making headlines

as corporate Japan divests, availing companies of non-core assets and creating

opportunities for investors.

Now more so than ever, economic uncertainty and disruption from market competitors

demand that Japanese corporates be nimble and adaptable to increasing volatility.

Yet those with a diverse corporate portfolio, the result of years of acquisitions or

industry consolidation, may find it difficult to remain agile.

Even more may have loss-making or underperforming business units draining resources or returns to shareholders. As a result, many are using divestitures to scale back in certain sectors and bolster others as they reassess their long-term business objectives and prepare to defend and expand market share. To understand how corporations in Japan – including domestic corporations and their multinational counterparts – are approaching divestitures, Deloitte, in partnership with Mergermarket, surveyed a select group of 60 market participants that had divested at least one asset within the past 18 months. Their collected sentiment has helped in understanding the current market with regard to divestiture activity, rationale, and the inherent challenges of finding a buyer and selling assets. It has also been invaluable in painting a picture of expectations in the coming months and years, as well as highlighting best practices to make a clean break. Making the break: Selling and disposing non-core and under-performing assets in Japan 3 .

4 . Executive summary Corporates turn to divestitures Among Japanese corporates and foreign multinationals surveyed in this report, 90% said they had completed at least one divestiture in Japan in the past 12 months, and 15% said they had completed two or more such transactions. Almost half (49%) of respondents said they had completed the sale of a majority or wholly-owned subsidiary, while 45% said their divestiture involved the sale of an equity method investment. 17% said they contributed a business to a joint venture (JV). Strategy drives sell offs and splits Selling an asset that was not core to the company’s overall business strategy was the top driver of divestitures (44% of respondents). This was followed by 21% who said they sold non-core or underperforming assets to fulfill financing needs and 18% who said their divestiture was linked to the disposal of a distressed business unit. Internal and external challenges The greatest internal challenge in their recent divestitures involved gaining support from management toward executing the deal (55% of respondents), followed by 46% who said separating subsidiary operations from parent operations created one of the greatest challenges.

External matters that affected the divestiture included the impact the process would have on the company’s image (56% of respondents), followed by the valuation gap between buyer and seller (43% of respondents). Increasing the odds of closing When divestitures failed to close, 35% of respondents said it was due to a lack of preparation of management teams. To alleviate tension or misunderstanding during the process, respondents said internal marketing campaigns or direct communication with managers proved beneficial to maintaining operations and preventing a flight of managers once the deal was announced. Sale prices meet expectations Overwhelmingly, respondents agreed that the prices received from recent divestitures were as expected (79% of respondents), while 13% said the value was more than they anticipated. When negotiating and completing the sale of an asset, preference was heavily weighted towards an exclusive negotiation (73% of respondents) as opposed to an auction sale process (27% of respondents). Preference for Japanese buyers In terms of preferred buyers, respondents favored Japanese acquirers (corporates, trading houses, and private equity firms) over their foreign counterparts by a noticeable gap: 95% in favor of Japanese corporates compared to 25% for foreign multinationals and an even smaller 7% for foreign private equity firms. Respondents noted that while foreign buyers may offer competitive or even higher valuations, domestic buyers are perceived as more likely to close a transaction. Foreign investors will remain acquisitive While 91% of respondents had closed recent divestitures with Japanese buyers, survey participants expect that foreign investors will continue to actively pursue acquisitions in Japan.

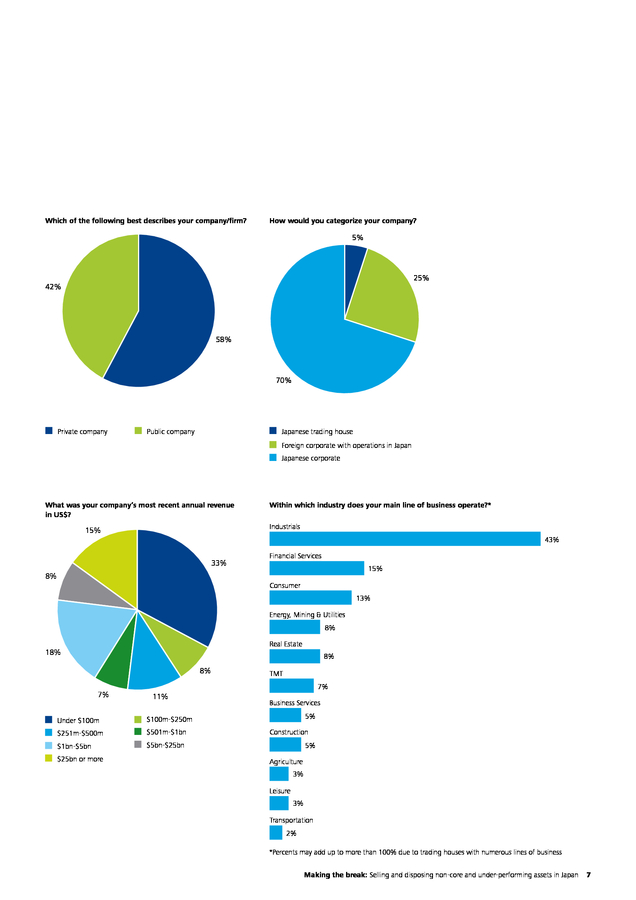

According to 41% of respondents, foreign multinationals are expected to show a high to moderate degree of interest in divested assets as they set their sights on the Japanese market. Foreign investors can increase their odds of being the selected bidder for a Japanese asset by being non-disruptive to the seller's core business (92% of respondents), a task that is often supported by utilizing Japanese financial advisors and consultants to facilitate bi-lingual negotiations and transactional guidance. Review early, review often Portfolio reviews were commonplace among respondents, with 40% saying these were carried out on an annual basis and 30% saying such reviews were completed every 6 months. These periodic evaluations helped managers prune their corporate portfolio by identifying businesses that no longer supported the long-term corporate goals and strategy. Making the break: Selling and disposing non-core and under-performing assets in Japan 5 . Profile of respondents and methodology From January to March 2015, Remark, the publishing division of Mergermarket, canvassed the opinions of 45 M&A practitioners from Japan and 15 that described themselves as foreign multinationals with operations in Japan. Fifty-eight percent described their company as a private company, while 42% said their organization was a public company. Forty-one percent of respondents said their company’s most recent annual revenue in US$ exceeded US$1bn. Within the graphed survey results, where figures add up to more than 100%, respondents were allowed to choose more than one answer. Where figures do not add up to 100%, this was due to rounding. Historical data includes all Mergermarket recorded transactions for the period 1 January 2012 to 30 June 2015. Transactions with a deal value greater than US$5m are included.

If the consideration is undisclosed, Mergermarket includes deals on the basis of a reported or estimated value of over US$5m. If the value is not disclosed, Mergermarket captures a transaction if the target’s turnover is greater than US$10m. Only completed and pending merger and acquisition deals are collated.

Transactions to be included usually involve a controlling stake in a company being transferred between two unrelated parties. In a case where the stake acquired is less than 30% (10% in Asia-Pacific), the deal will only be included if its value is greater than US$100m. All US$ symbols refer to US dollars unless otherwise stated. All ¥ symbols refer to Japanese yen unless otherwise stated. All data quoted is proprietary Mergermarket or Deloitte data unless otherwise stated. 6 . Which of the following best describes your company/firm? How would you categorize your company? 5% 25% 42% 58% 70% Private company Public company Japanese trading house Foreign corporate with operations in Japan Japanese corporate What was your company’s most recent annual revenue in US$? Within which industry does your main line of business operate?* Industrials 15% 43% 33% Financial Services 15% 8% Consumer 13% Energy, Mining & Utilities 8% Real Estate 18% 8% 8% 7% TMT 7% 11% Under $100m $251m-$500m $1bn-$5bn 5% $100m-$250m $501m-$1bn Business Services $5bn-$25bn $25bn or more Construction 5% Agriculture 3% Leisure 3% Transportation 2% *Percents may add up to more than 100% due to trading houses with numerous lines of business Making the break: Selling and disposing non-core and under-performing assets in Japan 7 . 8 . The business of break-ups: Divestitures in corporate Japan “In recent years some of our businesses have lost profitability. Where they once were catalysts for growth, some quickly became burdens to our bottom line. After careful consideration we decided that selling these businesses was the best option.” Director of corporate development, Japanese trading house Corporate divestitures can be an effective tool for unlocking value. The sale of an asset, a business unit or a subsidiary has the benefit of generating or freeing up capital and often increasing profitability margins and shareholder returns.

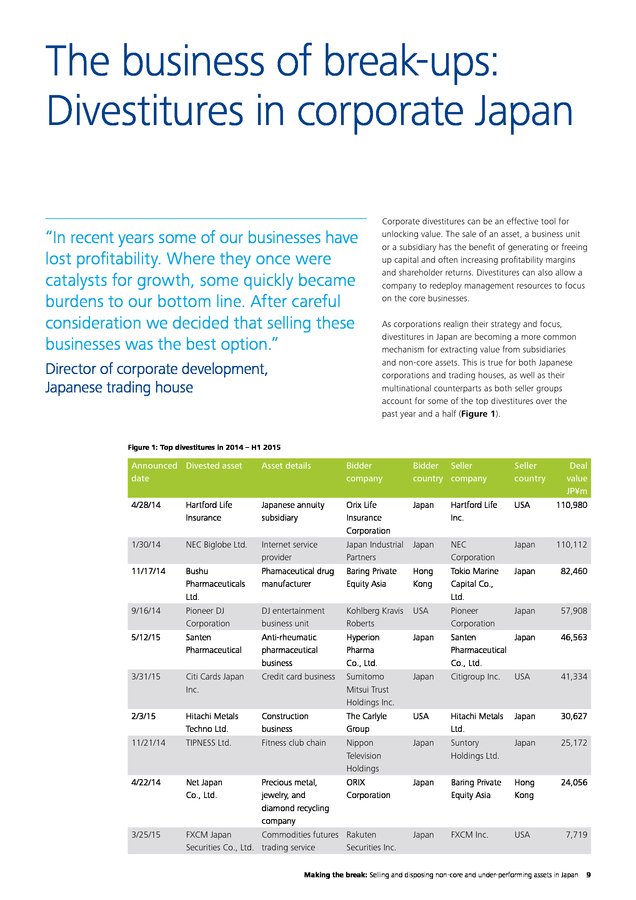

Divestitures can also allow a company to redeploy management resources to focus on the core businesses. As corporations realign their strategy and focus, divestitures in Japan are becoming a more common mechanism for extracting value from subsidiaries and non-core assets. This is true for both Japanese corporations and trading houses, as well as their multinational counterparts as both seller groups account for some of the top divestitures over the past year and a half (Figure 1). Figure 1: Top divestitures in 2014 – H1 2015 Announced Divested asset date Asset details Bidder company Bidder Seller country company Seller country Deal value JP¥m 4/28/14 Hartford Life Insurance Japanese annuity subsidiary Orix Life Insurance Corporation Japan Hartford Life Inc. USA 110,980 1/30/14 NEC Biglobe Ltd. Internet service provider Japan Industrial Partners Japan NEC Corporation Japan 110,112 11/17/14 Bushu Pharmaceuticals Ltd. Phamaceutical drug manufacturer Baring Private Equity Asia Hong Kong Tokio Marine Capital Co., Ltd. Japan 82,460 9/16/14 Pioneer DJ Corporation DJ entertainment business unit Kohlberg Kravis Roberts USA Pioneer Corporation Japan 57,908 5/12/15 Santen Pharmaceutical Anti-rheumatic pharmaceutical business Hyperion Pharma Co., Ltd. Japan Santen Japan Pharmaceutical Co., Ltd. 46,563 3/31/15 Citi Cards Japan Inc. Credit card business Sumitomo Mitsui Trust Holdings Inc. Japan Citigroup Inc. USA 41,334 2/3/15 Hitachi Metals Techno Ltd. Construction business The Carlyle Group USA Hitachi Metals Ltd. Japan 30,627 11/21/14 TIPNESS Ltd. Fitness club chain Nippon Television Holdings Japan Suntory Holdings Ltd. Japan 25,172 4/22/14 Net Japan Co., Ltd. Precious metal, jewelry, and diamond recycling company ORIX Corporation Japan Baring Private Equity Asia Hong Kong 24,056 3/25/15 FXCM Japan Commodities futures Rakuten Securities Co., Ltd. trading service Securities Inc. Japan FXCM Inc. USA 7,719 Making the break: Selling and disposing non-core and under-performing assets in Japan 9 .

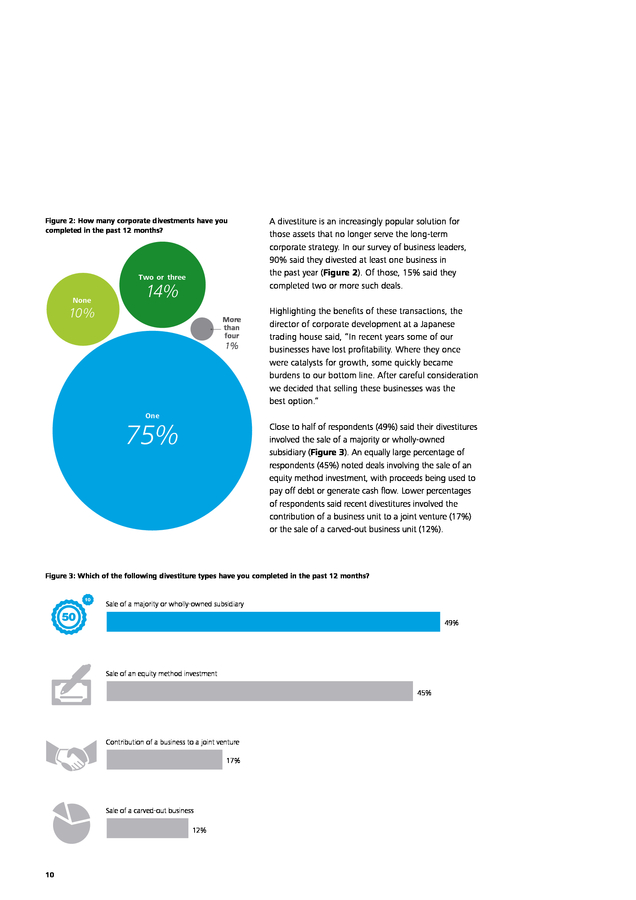

Figure 2: How many corporate divestments have you completed in the past 12 months? Two or three None 14% 10% More than four 1% A divestiture is an increasingly popular solution for those assets that no longer serve the long-term corporate strategy. In our survey of business leaders, 90% said they divested at least one business in the past year (Figure 2). Of those, 15% said they completed two or more such deals. Highlighting the benefits of these transactions, the director of corporate development at a Japanese trading house said, “In recent years some of our businesses have lost profitability. Where they once were catalysts for growth, some quickly became burdens to our bottom line.

After careful consideration we decided that selling these businesses was the best option.” One 75% Close to half of respondents (49%) said their divestitures involved the sale of a majority or wholly-owned subsidiary (Figure 3). An equally large percentage of respondents (45%) noted deals involving the sale of an equity method investment, with proceeds being used to pay off debt or generate cash flow. Lower percentages of respondents said recent divestitures involved the contribution of a business unit to a joint venture (17%) or the sale of a carved-out business unit (12%). Figure 3: Which of the following divestiture types have you completed in the past 12 months? Sale of a majority or wholly-owned subsidiary 49% Sale of an equity method investment 45% Contribution of a business to a joint venture 17% Sale of a carved-out business 12% 10 .

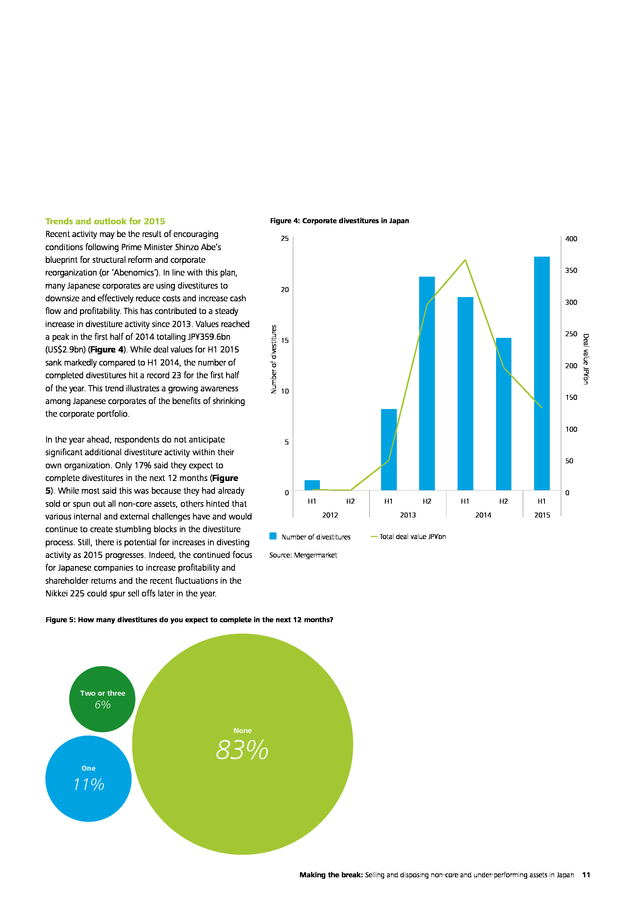

Figure 4: Corporate divestitures in Japan 25 400 350 20 Number of divestitures 300 250 15 200 10 Deal value JP¥bn Trends and outlook for 2015 Recent activity may be the result of encouraging conditions following Prime Minister Shinzo Abe’s blueprint for structural reform and corporate reorganization (or ’Abenomics’). In line with this plan, many Japanese corporates are using divestitures to downsize and effectively reduce costs and increase cash flow and profitability. This has contributed to a steady increase in divestiture activity since 2013. Values reached a peak in the first half of 2014 totalling JP¥359.6bn (US$2.9bn) (Figure 4).

While deal values for H1 2015 sank markedly compared to H1 2014, the number of completed divestitures hit a record 23 for the first half of the year. This trend illustrates a growing awareness among Japanese corporates of the benefits of shrinking the corporate portfolio. 150 100 In the year ahead, respondents do not anticipate significant additional divestiture activity within their own organization. Only 17% said they expect to complete divestitures in the next 12 months (Figure 5).

While most said this was because they had already sold or spun out all non-core assets, others hinted that various internal and external challenges have and would continue to create stumbling blocks in the divestiture process. Still, there is potential for increases in divesting activity as 2015 progresses. Indeed, the continued focus for Japanese companies to increase profitability and shareholder returns and the recent fluctuations in the Nikkei 225 could spur sell offs later in the year. 5 50 0 0 H1 H2 2012 Number of divestitures H1 H2 2013 H1 H2 2014 H1 2015 Total deal value JP¥bn Source: Mergermarket Figure 5: How many divestitures do you expect to complete in the next 12 months? Two or three 6% None One 83% 11% Making the break: Selling and disposing non-core and under-performing assets in Japan 11 .

Strategy drives divestitures "In the Japanese market we see companies in certain market segments – notably, manufacturing and technology – becoming more focused on defining the company’s core competencies and business strategy and proactively divesting non-core or unprofitable businesses as opposed to reacting to external pressures after the company has already experienced undesirable results.” Masaki Ide, Deloitte Partner, M&A Reorganization Services Companies overextending their reach can quickly find themselves in precarious positions when resources become scarce or when market changes threaten growth. Accordingly, 44% of respondents said divesting non-core assets was either the most or second-most important driver of divestiture activity in the past year (Figure 6). Selling non-core assets made their companies leaner and more agile, qualities essential to weathering market volatility and possible disruption from market competitors. Purely financial motives were also behind recent activity. According to 21% of respondents describing their recent divestitures, proceeds were used to pay down debt, strengthen the balance sheet, and raise capital to support products and services core to the business or explore new market segments with high growth potential. Disposal of distressed or unprofitable business units was mentioned by 18% and 8% of respondents, respectively.

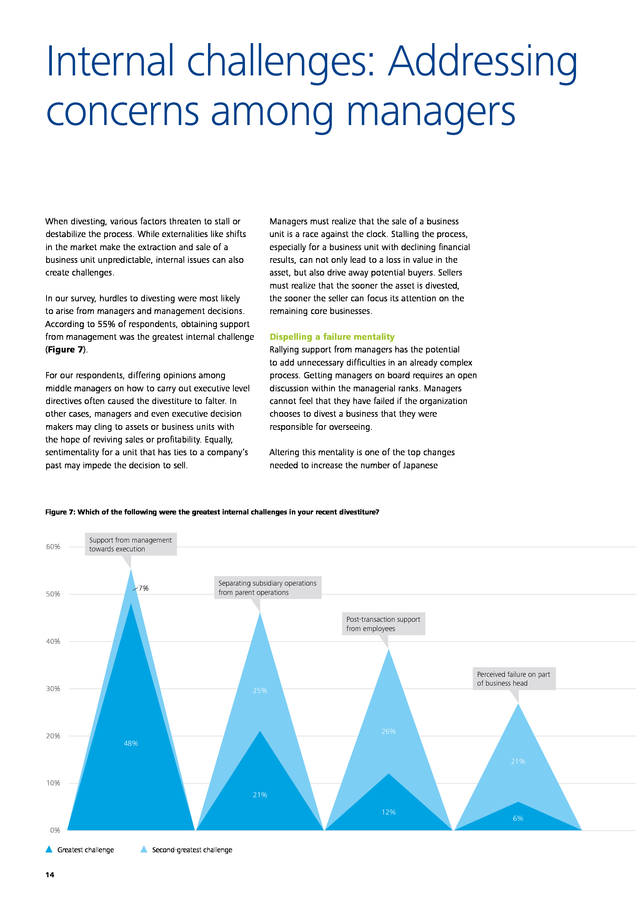

Especially in these cases, sellers often face the challenge of finding a new owner, be it another corporate or private equity firm, who can turn the unit around and return it to profitability. Timing of divestitures was another important consideration. According to 16% of respondents, company management waited until ideal market conditions manifested, making it an opportune moment to sell. 50% 12 . Figure 6: What was the rationale behind your recent divestiture? Non-core asset to business strategy 3% Financing needs (reduce debt/ raise capital) Market conditions made it a better time to divest Disposal of distressed business unit Business growth was constrained within the parent organization Unsolicited offer from interested party Too much risk in the business 41% 8% 6% 11% 13% Proï¬table but didn’t meet targets 11% 5% 40% 7% 30% 13% 7% 3% 3% 5% Not proï¬table 9% 3% 20% 5% 10% 0% Most important Second-most important Making the break: Selling and disposing non-core and under-performing assets in Japan 13 . Internal challenges: Addressing concerns among managers When divesting, various factors threaten to stall or destabilize the process. While externalities like shifts in the market make the extraction and sale of a business unit unpredictable, internal issues can also create challenges. In our survey, hurdles to divesting were most likely to arise from managers and management decisions. According to 55% of respondents, obtaining support from management was the greatest internal challenge (Figure 7). For our respondents, differing opinions among middle managers on how to carry out executive level directives often caused the divestiture to falter. In other cases, managers and even executive decision makers may cling to assets or business units with the hope of reviving sales or profitability. Equally, sentimentality for a unit that has ties to a company’s past may impede the decision to sell. Managers must realize that the sale of a business unit is a race against the clock.

Stalling the process, especially for a business unit with declining financial results, can not only lead to a loss in value in the asset, but also drive away potential buyers. Sellers must realize that the sooner the asset is divested, the sooner the seller can focus its attention on the remaining core businesses. Dispelling a failure mentality Rallying support from managers has the potential to add unnecessary difficulties in an already complex process. Getting managers on board requires an open discussion within the managerial ranks.

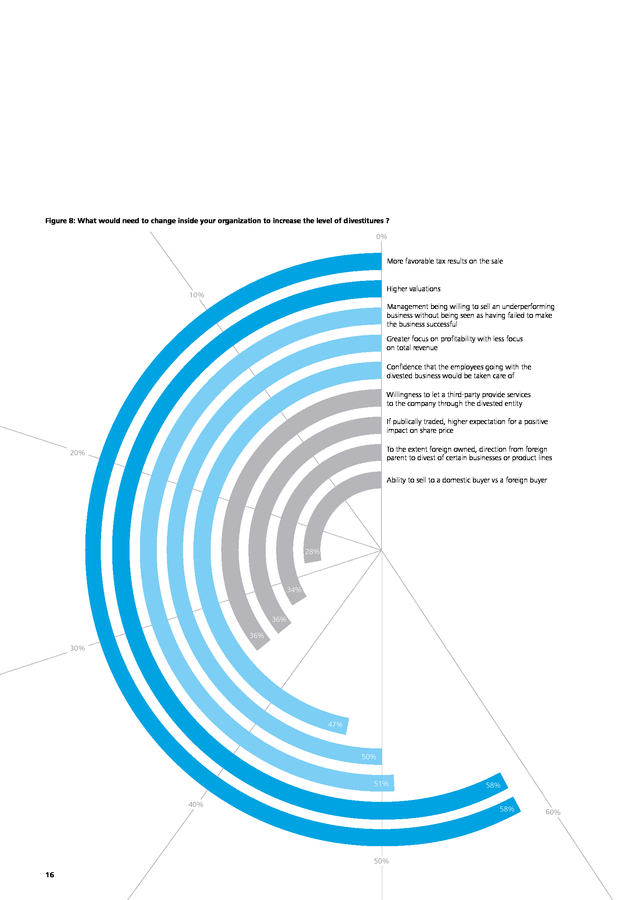

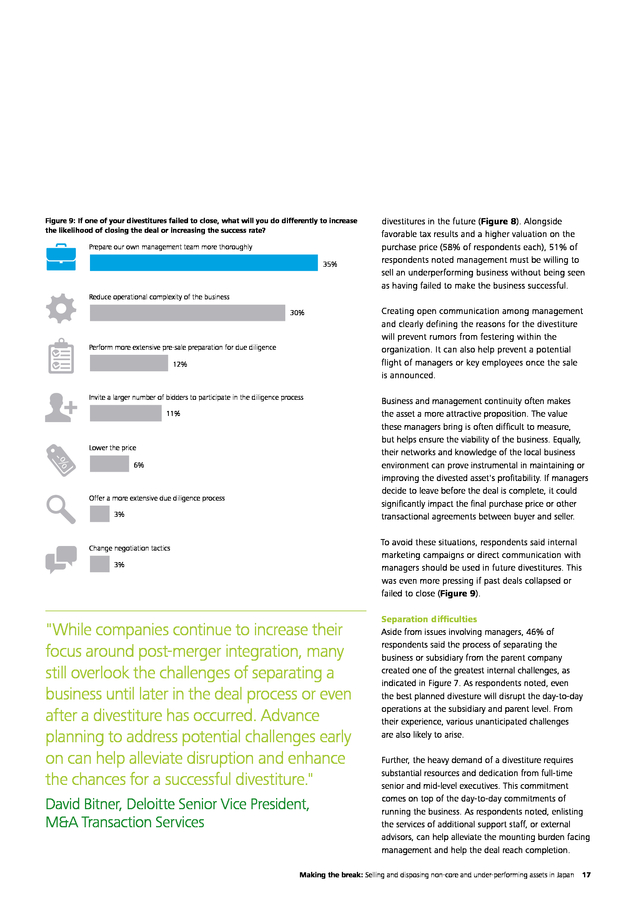

Managers cannot feel that they have failed if the organization chooses to divest a business that they were responsible for overseeing. Altering this mentality is one of the top changes needed to increase the number of Japanese Figure 7: Which of the following were the greatest internal challenges in your recent divestiture? 60% Support from management towards execution 7% 50% Separating subsidiary operations from parent operations Post-transaction support from employees 40% 30% 20% Perceived failure on part of business head 25% 26% 48% 21% 10% 21% 12% 0% Greatest challenge 14 Second-greatest challenge 6% . "When a business needs to be divested because it is non-core or underperforming, company management responsible for the business may be hesitant to support the decision over concerns that the divesture is a reflection of management’s inability to operate the business. This perception can be minimized by having a strategic plan in place that guides the decision-making process, and presents the divestiture as an opportunity to redeploy valuable capital and quality talent to other core businesses." Brian Lightle, Deloitte Executive Officer, M&A Transaction Services Impacts on the retained business Decoupling IT systems from subsidiary and parent company 11% 11% 9% 3% Making the break: Selling and disposing non-core and under-performing assets in Japan 15 . Figure 8: What would need to change inside your organization to increase the level of divestitures ? 0% More favorable tax results on the sale Higher valuations 10% Management being willing to sell an underperforming business without being seen as having failed to make the business successful Greater focus on proï¬tability with less focus on total revenue Conï¬dence that the employees going with the divested business would be taken care of Willingness to let a third-party provide services to the company through the divested entity If publically traded, higher expectation for a positive impact on share price To the extent foreign owned, direction from foreign parent to divest of certain businesses or product lines 20% Ability to sell to a domestic buyer vs a foreign buyer 28% 34% 36% 36% 30% 47% 50% 51% 40% 58% 50% 16 58% 60% . Figure 9: If one of your divestitures failed to close, what will you do differently to increase the likelihood of closing the deal or increasing the success rate? Prepare our own management team more thoroughly 35% divestitures in the future (Figure 8). Alongside favorable tax results and a higher valuation on the purchase price (58% of respondents each), 51% of respondents noted management must be willing to sell an underperforming business without being seen as having failed to make the business successful. Reduce operational complexity of the business 30% Perform more extensive pre-sale preparation for due diligence 12% Invite a larger number of bidders to participate in the diligence process 11% Lower the price 6% Offer a more extensive due diligence process 3% Creating open communication among management and clearly defining the reasons for the divestiture will prevent rumors from festering within the organization. It can also help prevent a potential flight of managers or key employees once the sale is announced. Business and management continuity often makes the asset a more attractive proposition. The value these managers bring is often difficult to measure, but helps ensure the viability of the business.

Equally, their networks and knowledge of the local business environment can prove instrumental in maintaining or improving the divested asset's profitability. If managers decide to leave before the deal is complete, it could significantly impact the final purchase price or other transactional agreements between buyer and seller. To avoid these situations, respondents said internal marketing campaigns or direct communication with managers should be used in future divestitures. This was even more pressing if past deals collapsed or failed to close (Figure 9). Change negotiation tactics 3% "While companies continue to increase their focus around post-merger integration, many still overlook the challenges of separating a business until later in the deal process or even after a divestiture has occurred.

Advance planning to address potential challenges early on can help alleviate disruption and enhance the chances for a successful divestiture." David Bitner, Deloitte Senior Vice President, M&A Transaction Services Separation difficulties Aside from issues involving managers, 46% of respondents said the process of separating the business or subsidiary from the parent company created one of the greatest internal challenges, as indicated in Figure 7. As respondents noted, even the best planned divesture will disrupt the day-to-day operations at the subsidiary and parent level. From their experience, various unanticipated challenges are also likely to arise. Further, the heavy demand of a divestiture requires substantial resources and dedication from full-time senior and mid-level executives.

This commitment comes on top of the day-to-day commitments of running the business. As respondents noted, enlisting the services of additional support staff, or external advisors, can help alleviate the mounting burden facing management and help the deal reach completion. Making the break: Selling and disposing non-core and under-performing assets in Japan 17 . Additionally, 38% of respondents said securing post-transaction support from employees posed significant challenges and setbacks. The director of corporate development at a Japanese trading house said, “Morale took a noticeable downturn during and after the divestiture and we saw a significant increase in employee turnover. Making employees understand the decision behind the sale was not easy, and their attachment and comfort with the business only added to the difficulties of separating from the parent company.” Bottom over top line performance Emphasizing profitability (the bottom line) over revenue (the top line) was another internal catalyst that could drive divestitures. According to 50% of respondents, as shown in Figure 8, adopting this approach could help corporate leaders identify more business units to divest, especially those generating relatively low returns compared to better performing portfolio assets. Historically, many Japanese corporates across industries have focused on growing revenue and market share. Profitability, especially today amid rising competition from Asian corporate rivals, has lacked such strength. Success and growth equates to more than sales totals, 18 a reality that has already led many Japanese businesses to improve profitability by adopting new technologies and innovative management practices, and also selling assets that no longer contribute to the company’s growth agenda and trajectory. Managing operational complexities Simplifying the divestiture process is a lofty goal that is often easier said than done.

However, it is a necessity that carries weight, particularly among survey respondents who experienced failed divestitures. The ability to reduce operational complexities at the business being sold was one of the top areas for improvement, an outcome supported by 30% of respondents, as shown in Figure 9, that saw their recent deals fail to close. This can mean different things for different companies and often entails industryspecific hurdles that will need to be overcome. Rolling out a plan to decouple operations, pinpointing where synergies will be lost, and separating IT systems can assist in streamlining the divestiture process.

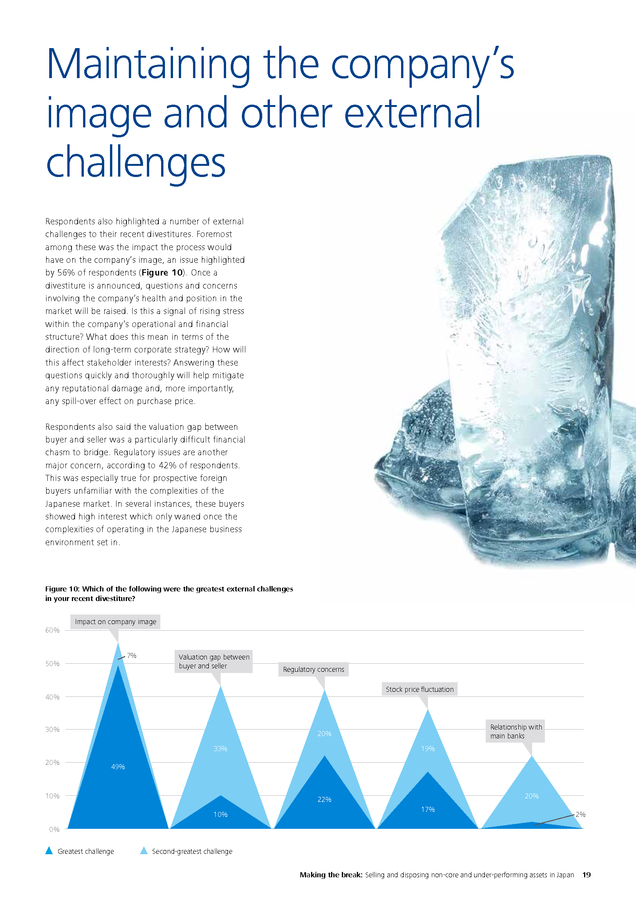

While a task best suited for internal managers knowledgeable on the inner workings of the business, consulting third-party advisors can often present new perspectives on how best to achieve these ends. . Maintaining the company’s image and other external challenges Respondents also highlighted a number of external challenges to their recent divestitures. Foremost among these was the impact the process would have on the company’s image, an issue highlighted by 56% of respondents (Figure 10). Once a divestiture is announced, questions and concerns involving the company’s health and position in the market will be raised. Is this a signal of rising stress within the company’s operational and financial structure? What does this mean in terms of the direction of long-term corporate strategy? How will this affect stakeholder interests? Answering these questions quickly and thoroughly will help mitigate any reputational damage and, more importantly, any spill-over effect on purchase price. Respondents also said the valuation gap between buyer and seller was a particularly difficult financial chasm to bridge.

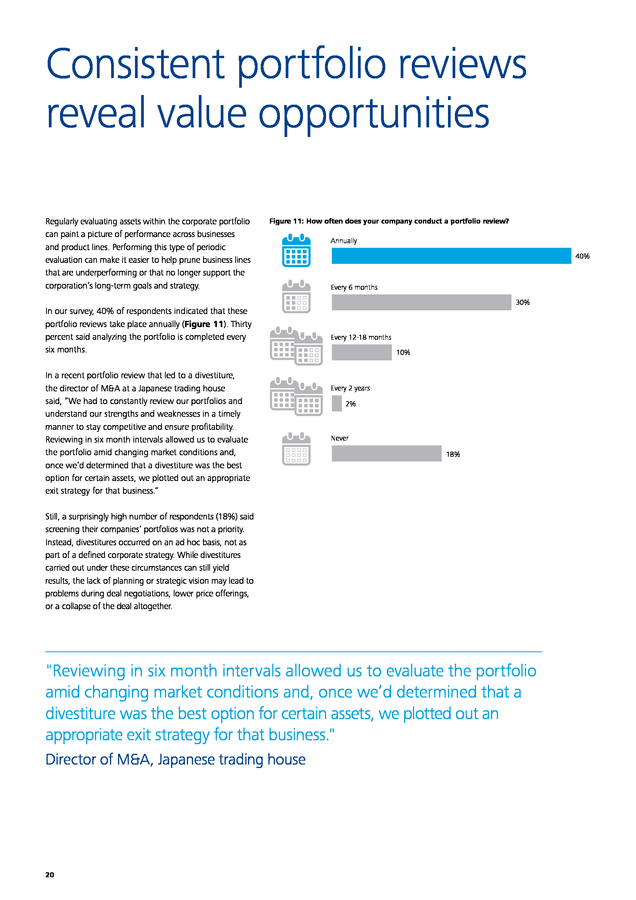

Regulatory issues are another major concern, according to 42% of respondents. This was especially true for prospective foreign buyers unfamiliar with the complexities of the Japanese market. In several instances, these buyers showed high interest which only waned once the complexities of operating in the Japanese business environment set in. Figure 10: Which of the following were the greatest external challenges in your recent divestiture? 60% Impact on company image 7% 50% Valuation gap between buyer and seller Regulatory concerns Stock price fluctuation 40% 30% 19% 33% 20% Relationship with main banks 20% 49% 10% 20% 22% 10% 17% 2% 0% Greatest challenge Second-greatest challenge Making the break: Selling and disposing non-core and under-performing assets in Japan 19 . Consistent portfolio reviews reveal value opportunities Regularly evaluating assets within the corporate portfolio can paint a picture of performance across businesses and product lines. Performing this type of periodic evaluation can make it easier to help prune business lines that are underperforming or that no longer support the corporation’s long-term goals and strategy. Figure 11: How often does your company conduct a portfolio review? In our survey, 40% of respondents indicated that these portfolio reviews take place annually (Figure 11). Thirty percent said analyzing the portfolio is completed every six months. In a recent portfolio review that led to a divestiture, the director of M&A at a Japanese trading house said, “We had to constantly review our portfolios and understand our strengths and weaknesses in a timely manner to stay competitive and ensure profitability. Reviewing in six month intervals allowed us to evaluate the portfolio amid changing market conditions and, once we’d determined that a divestiture was the best option for certain assets, we plotted out an appropriate exit strategy for that business.” Annually 40% Every 6 months 30% Every 12-18 months 10% Every 2 years 2% Never 18% Still, a surprisingly high number of respondents (18%) said screening their companies’ portfolios was not a priority. Instead, divestitures occurred on an ad hoc basis, not as part of a defined corporate strategy. While divestitures carried out under these circumstances can still yield results, the lack of planning or strategic vision may lead to problems during deal negotiations, lower price offerings, or a collapse of the deal altogether. "Reviewing in six month intervals allowed us to evaluate the portfolio amid changing market conditions and, once we’d determined that a divestiture was the best option for certain assets, we plotted out an appropriate exit strategy for that business." Director of M&A, Japanese trading house 20 .

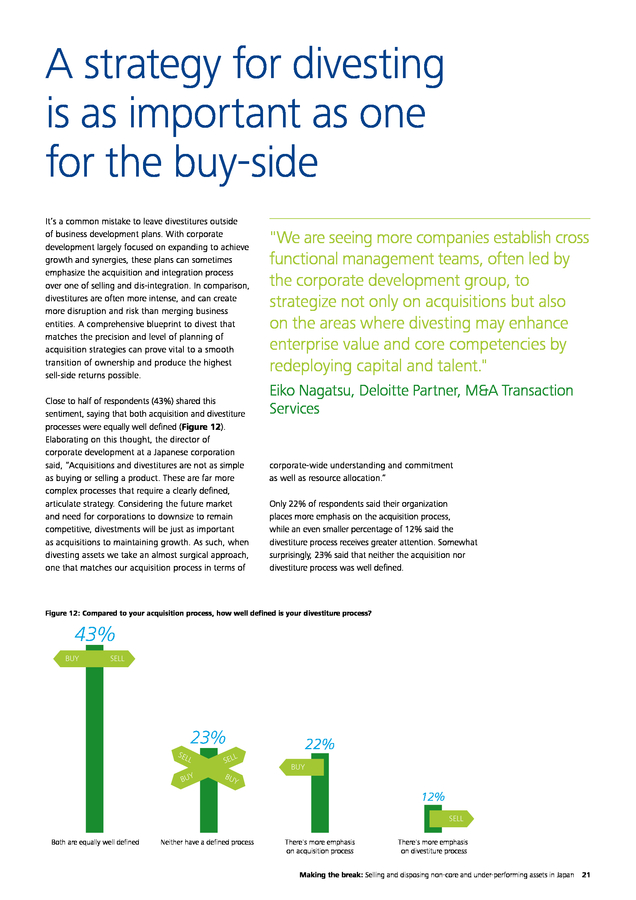

A strategy for divesting is as important as one for the buy-side It’s a common mistake to leave divestitures outside of business development plans. With corporate development largely focused on expanding to achieve growth and synergies, these plans can sometimes emphasize the acquisition and integration process over one of selling and dis-integration. In comparison, divestitures are often more intense, and can create more disruption and risk than merging business entities. A comprehensive blueprint to divest that matches the precision and level of planning of acquisition strategies can prove vital to a smooth transition of ownership and produce the highest sell-side returns possible. Close to half of respondents (43%) shared this sentiment, saying that both acquisition and divestiture processes were equally well defined (Figure 12). Elaborating on this thought, the director of corporate development at a Japanese corporation said, “Acquisitions and divestitures are not as simple as buying or selling a product.

These are far more complex processes that require a clearly defined, articulate strategy. Considering the future market and need for corporations to downsize to remain competitive, divestments will be just as important as acquisitions to maintaining growth. As such, when divesting assets we take an almost surgical approach, one that matches our acquisition process in terms of "We are seeing more companies establish cross functional management teams, often led by the corporate development group, to strategize not only on acquisitions but also on the areas where divesting may enhance enterprise value and core competencies by redeploying capital and talent." Eiko Nagatsu, Deloitte Partner, M&A Transaction Services corporate-wide understanding and commitment as well as resource allocation.” Only 22% of respondents said their organization places more emphasis on the acquisition process, while an even smaller percentage of 12% said the divestiture process receives greater attention.

Somewhat surprisingly, 23% said that neither the acquisition nor divestiture process was well defined. Figure 12: Compared to your acquisition process, how well defined is your divestiture process? 43% BUY SELL 23% SEL 22% L L SEL BUY BU BUY Y 12% SELL Both are equally well deï¬ned Neither have a deï¬ned process There's more emphasis on acquisition process There's more emphasis on divestiture process Making the break: Selling and disposing non-core and under-performing assets in Japan 21 . Maximizing price: Considerations for auctions and exclusive negotiations In terms of pricing, the survey shows that sellers are, in general, receiving their asking price for the assets being offered. Overwhelmingly, the agreed upon price met or exceeded seller expectations in their recent divestitures (Figure 13). Seventy-nine percent of respondents said they received the value they expected, while 13% noted the price was more than they had anticipated. When negotiating and completing the sale of an asset, respondent preferences leaned heavily toward exclusive negotiations (73% of respondents) over the more competitive auction process (27% of respondents) (Figure 14). While the auction brings more bidders to the table, its sometimes disruptive and unpredictable nature raises a number of obstacles. Respondents’ opinions reflect this uncertainty.

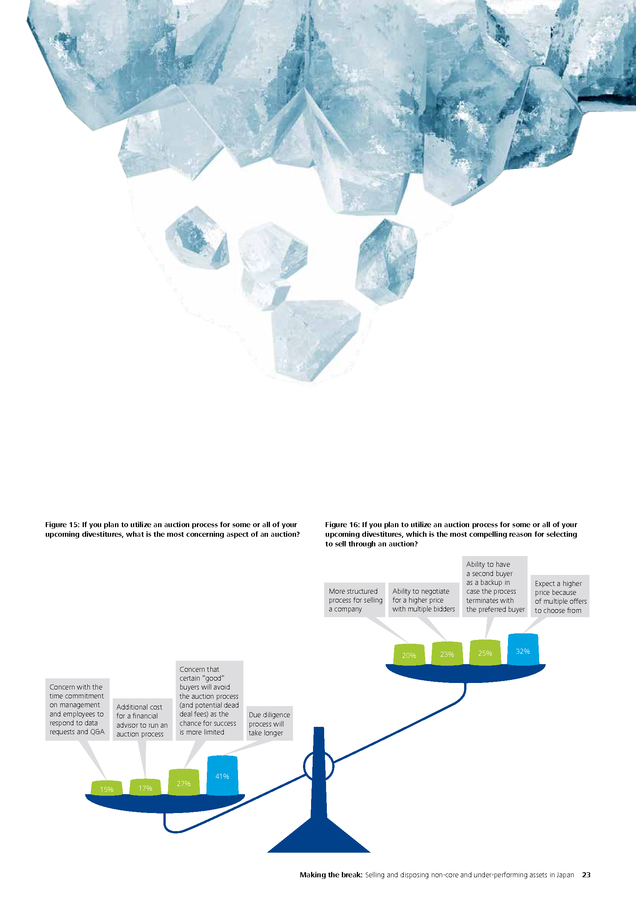

Primarily, issues revolving around the due diligence process and its potential impact on day-to-day operations at both the parent company and entity being sold were concerning aspects of the divestiture (Figure 15). Forty-one percent Figure 13: How did the agreed upon price for the asset compare to your expectations? of respondents cited the extended and sometimes intrusive nature of these investigations as reason to avoid the auction route. Another perceived limitation of the auction process is that certain preferred or qualified buyers might avoid the sale, a sentiment shared by 27% of respondents. This is due to the increased chance of being out-bid by competitors, leaving the losing bidders with nothing more than large dead deal fees owed to its M&A advisors. However, the auction process is not without its advantages. Thirty-two percent said they expect a higher price due to multiple offers and competition among bidders in their future divestitures (Figure 16). A further 25% said having a second buyer as a backup provided a small sense of security in selling the asset.

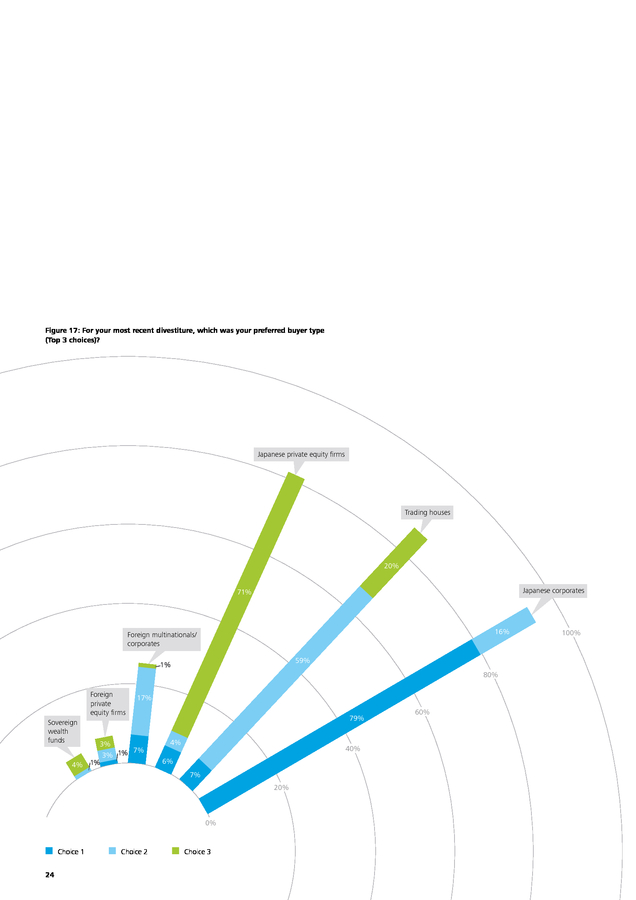

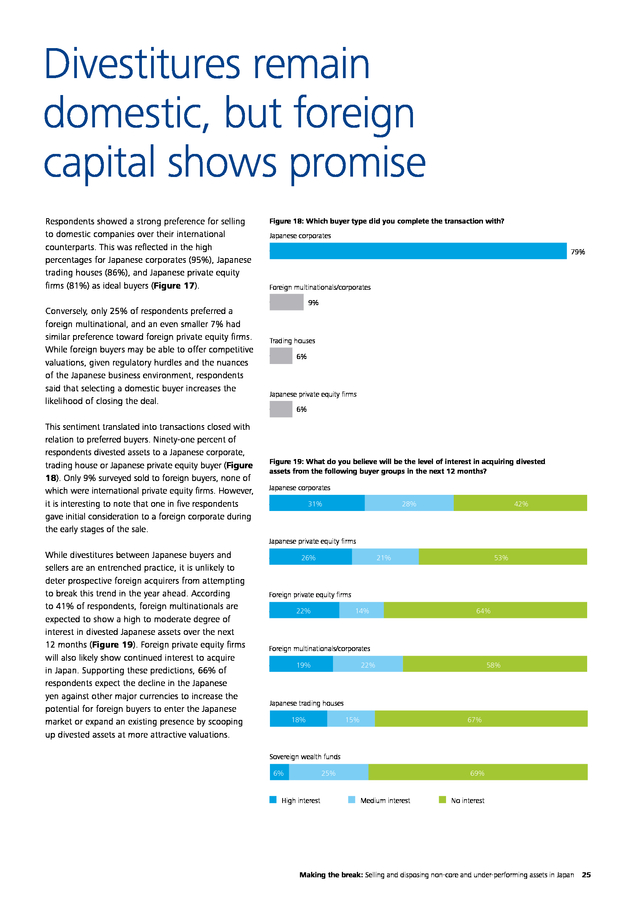

An equally large percentage of respondents (23%) said that a larger buyer pool provided opportunities to negotiate for a higher price if initial bids fell short of expectations. Figure 14: Preferred divestiture sale process Exclusive negotiation 3% Signiï¬cantly more than expected 73% Auction 10% 79% 8% 22 More than expected As expected Less than expected 27% . Figure 15: If you plan to utilize an auction process for some or all of your upcoming divestitures, what is the most concerning aspect of an auction? Figure 16: If you plan to utilize an auction process for some or all of your upcoming divestitures, which is the most compelling reason for selecting to sell through an auction? More structured process for selling a company Ability to negotiate for a higher price with multiple bidders 20% Concern with the time commitment on management and employees to respond to data requests and Q&A 15% Additional cost for a ï¬nancial advisor to run an auction process 17% Concern that certain “good” buyers will avoid the auction process (and potential dead deal fees) as the chance for success is more limited 27% 23% Ability to have a second buyer as a backup in case the process terminates with the preferred buyer 25% Expect a higher price because of multiple offers to choose from 32% Due diligence process will take longer 41% Making the break: Selling and disposing non-core and under-performing assets in Japan 23 . Figure 17: For your most recent divestiture, which was your preferred buyer type (Top 3 choices)? Japanese private equity ï¬rms Trading houses 20% Japanese corporates 71% 16% Foreign multinationals/ corporates 59% 1% 80% Foreign private equity ï¬rms 17% Sovereign wealth funds 3% 7% 3% 1% 4% 1% 79% 4% 40% 6% 7% 20% 0% Choice 1 24 Choice 2 Choice 3 60% 100% . Divestitures remain domestic, but foreign capital shows promise Respondents showed a strong preference for selling to domestic companies over their international counterparts. This was reflected in the high percentages for Japanese corporates (95%), Japanese trading houses (86%), and Japanese private equity firms (81%) as ideal buyers (Figure 17). Conversely, only 25% of respondents preferred a foreign multinational, and an even smaller 7% had similar preference toward foreign private equity firms. While foreign buyers may be able to offer competitive valuations, given regulatory hurdles and the nuances of the Japanese business environment, respondents said that selecting a domestic buyer increases the likelihood of closing the deal. This sentiment translated into transactions closed with relation to preferred buyers. Ninety-one percent of respondents divested assets to a Japanese corporate, trading house or Japanese private equity buyer (Figure 18). Only 9% surveyed sold to foreign buyers, none of which were international private equity firms.

However, it is interesting to note that one in five respondents gave initial consideration to a foreign corporate during the early stages of the sale. Figure 18: Which buyer type did you complete the transaction with? Japanese corporates 79% Foreign multinationals/corporates 9% Trading houses 6% Japanese private equity ï¬rms 6% Figure 19: What do you believe will be the level of interest in acquiring divested assets from the following buyer groups in the next 12 months? Japanese corporates 31% 28% 42% Japanese private equity ï¬rms While divestitures between Japanese buyers and sellers are an entrenched practice, it is unlikely to deter prospective foreign acquirers from attempting to break this trend in the year ahead. According to 41% of respondents, foreign multinationals are expected to show a high to moderate degree of interest in divested Japanese assets over the next 12 months (Figure 19). Foreign private equity firms will also likely show continued interest to acquire in Japan.

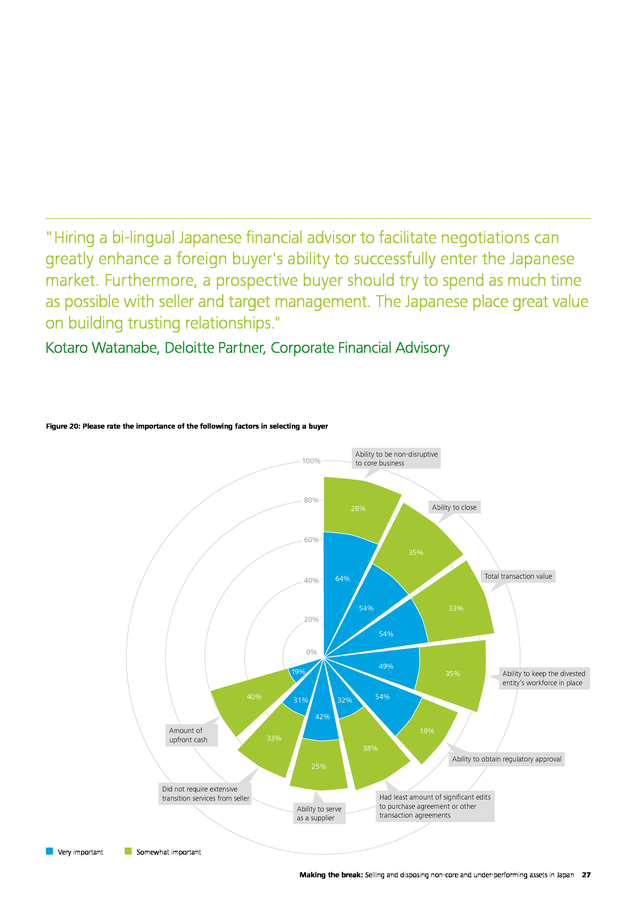

Supporting these predictions, 66% of respondents expect the decline in the Japanese yen against other major currencies to increase the potential for foreign buyers to enter the Japanese market or expand an existing presence by scooping up divested assets at more attractive valuations. 26% 21% 53% Foreign private equity ï¬rms 22% 14% 64% Foreign multinationals/corporates 19% 22% 58% Japanese trading houses 18% 15% 67% Sovereign wealth funds 6% 25% High interest 69% Medium interest No interest Making the break: Selling and disposing non-core and under-performing assets in Japan 25 . Finding the right fit Regardless of domicile country, ideal buyers must be able to do more than make an enticing cash offer when acquiring divested Japanese assets. Often times, certain qualities or factors are preferred above the financial considerations and total value of the deal. Top among these was the ability of buyers to be non-disruptive to the core operations, which 92% of respondents said is either very important or somewhat important (Figure 20). Once the sale process commences and prospective buyers begin investigating the target’s financials and operations, the sometimes invasive nature of due diligence and management involvement from both parties in the transaction can be both distracting and harmful to work flow at the target and parent company. For Japanese sellers, the perception is that this process may be easier to accomplish – and less invasive – with a Japanese buyer than a foreign buyer.

Aside from their familiarity with doing business in Japan, domestic companies need not worry about language or cultural barriers. Respondents did note that the use of bi-lingual Japanese financial sell-side advisors and consultants can help level the playing field between foreign and domestic bidders. 26 The ability to close transactions (89%) also ranked highly among qualities in an ideal buyer. Aside from securing financing, respondents also mentioned the ability for buyers to appreciate local conditions and cultures (both national and corporate) and consummate the transaction with ease.

As such, the geographic distance of foreign buyers was perceived to be an extreme disadvantage for them when competing against domestic bidding rivals. Employment considerations also received a large percentage of respondent sentiment in selecting a buyer. The buyer’s ability to keep the existing workforce in place (84%) after the business being divested has changed ownership is a particularly sensitive topic in Japan. Under the widely understood “social contract” between employer and employee, workers can expect to remain employed by the same company until retirement.

This concept is reinforced by Japanese labor laws which make it difficult to implement even minor reductions in workforce. While employee terminations are not impossible, the legal hurdles and burden of proof required to make such changes can prove much more challenging than executing similar rightsizing in other geographies. . "Hiring a bi-lingual Japanese financial advisor to facilitate negotiations can greatly enhance a foreign buyer's ability to successfully enter the Japanese market. Furthermore, a prospective buyer should try to spend as much time as possible with seller and target management. The Japanese place great value on building trusting relationships." Kotaro Watanabe, Deloitte Partner, Corporate Financial Advisory Figure 20: Please rate the importance of the following factors in selecting a buyer Ability to be non-disruptive to core business 100% 80% Ability to close 28% 60% 35% 40% Total transaction value 64% 33% 54% 20% 54% 0% 49% 19% 40% 31% 32% 35% Ability to keep the divested entity’s workforce in place 54% 42% Amount of upfront cash 19% 33% 38% 25% Did not require extensive transition services from seller Ability to serve as a supplier Very important Ability to obtain regulatory approval Had least amount of signiï¬cant edits to purchase agreement or other transaction agreements Somewhat important Making the break: Selling and disposing non-core and under-performing assets in Japan 27 . A roadmap to meeting deadlines When it comes to executing the deal on time, 89% of respondents said their recent divestitures were completed within a one-year window from the time the decision was made to divest to the actual execution of the purchase agreement. This included 44% who said deals typically required less than six months. For the most part, these timeframes line up with respondent expectations. Sixty-seven percent of survey respondents said the time it took to carry out the divestiture met their expectations, while 15% said the process was completed in a shorter amount of time than anticipated (Figure 21). Respondents said that prior experience divesting assets as well as a formal divestiture strategy helped them reach certain milestones in the sales process within a pre-defined timeframe. The use of financial sell-side advisors, used in more than 50% of respondents’ recent transactions, also helped expedite the process. 28 .

Figure 21: How did the time required to execute your most recent significant divestiture compare with original expectations? 15% 67% 18% Shorter than expected As expected Longer than expected However, several respondents said that one of the standout points in closing divestitures without unnecessary delays was anticipating potential roadblocks. Japanese corporates that look at the sale from a buyer's perspective may be better equipped to predict areas where the deal could stall. This type of proactive approach can help alleviate or minimize certain frictions, address issues that arise, and usher the divestiture across the finish line. Our survey reflects these issues: 18% of respondents said their divestitures took longer to execute than previously planned. In these instances, 42% of respondents identified negotiations around purchase agreements, transition service agreements (TSAs) and other contracts as the biggest culprit for delays (Figure 22). As one more hurdle to overcome before a divestiture is closed, addressing TSAs early and anticipating what buyers will require from these and other agreements can be beneficial to both parties involved. Economic volatility, regulatory delays, and extensive buyer due diligence were also blamed for slowing the deal process, according to 33% of respondents.

While external factors are often outside of a seller's control, proactively supporting the due diligence process by anticipating and providing pertinent information to buyers will not only give the deal momentum, but also build trust in the buyer-seller relationship. Figure 22: If you answered “longer than expected”, why was this the case? Negotiations around purchase agreement, TSAs or other contracts 42% General economic conditions 33% Regulatory delays 33% Extensive buyer due diligence 33% Had to extend the process in order to expand the bidder pool after initial bidders withdrew or were rejected 25% Continued ï¬nancial deterioration in the business being divested 8% Making the break: Selling and disposing non-core and under-performing assets in Japan 29 . Making the best of your divestiture Navigating the divestiture process, especially in a volatile market, need not be an overly complicated undertaking. Discussing strategies for success, Hiroki Okimoto, Kotaro Watanabe, Eiko Nagatsu, Masaki Ide, and Brian Lightle of Deloitte Tohmatsu Financial Advisory LLC and Deloitte Tohmatsu Anchor Management Co., Ltd. elaborate on the options and resources available to help sellers and buyers realize the value of these transactions. Hiroki Okimoto Managing Director Deloitte Tohmatsu Anchor Management 30 Kotaro Watanabe Partner Corporate Financial Advisory Eiko Nagatsu Partner M&A Transaction Services Masaki Ide Partner M&A Reorganization Services Brian Lightle Executive Officer M&A Transaction Services . While transition service agreements (TSAs) can take up time and resources, companies can benefit by using TSAs as part of their dealmaking strategy. How can TSAs best be used, and what services are most common? Hiroki Okimoto, Managing Director, Deloitte Tohmatsu Anchor Management Often times, acquired companies, especially entities that have been carved out from another entity, do not have all of the necessary processes in place on Day 1 to operate on a standalone basis. Therefore, it is common for the buyer to request the seller to provide transition services around operational processes and functions, such as accounting, human resources, and information systems. Often times the buyer and seller have different expectations around a TSA. Many sellers will desire a shorter, less extensive TSA.

Therefore, during due diligence, it is important to identify as early as possible the potential services that may be required in order to begin the discussions around potential TSA needs with the seller. Furthermore, a seller can make a divestiture more attractive by acknowledging up front that it is willing to provide certain services through a TSA for a set period of time and share drafts of TSA agreements early in the process. What options can sellers take if their divestiture fails to close? What considerations should be taken before putting the asset back on the market? Kotaro Watanabe, Partner, Corporate Financial Advisory If a divesture fails to close, the seller should examine and address where the process broke down before making future attempts to sell. For example, if the seller did not receive any bids or only received bids that substantially undervalued the business, the seller may need to re-evaluate the business plan and anticipate possible barriers for potential buyers.

Also, a seller should give consideration to both the adequacy of information disclosed during diligence as well as the material issues identified and voiced by the buyer during the fact finding process. If the deal failed to close after a buyer was chosen, the seller should ask themselves why this happened and what could they have done differently? Many factors can derail a transaction, but ideally a seller should be as prepared as possible. A seller may want to work with a financial advisor to develop a robust business plan, assist with valuation and negotiation strategies, and vet bidders to improve the prospects of closing the deal.

Also, an advisor can better position a seller to meet the challenges posed by potential buyers during the process, including the type of data a buyer is likely to expect. Some companies will also prepare a sell-side or vendor due diligence report to showcase the business being divested to increase the level of transparency and accelerate the diligence process. How can corporate leaders ensure that both the seller and the buyer remain competitive in their future markets post-transaction? Eiko Nagatsu, Partner, M&A Transaction Services One recommended strategy for remaining competitive is to ensure that customers do not see the divestiture as being overly disruptive to business. The buyer and the seller should proactively meet with key customers to explain what is being sold and to the extent products and services were commingled in the past, how these services and products will be decoupled in the future. Equally important is how both the buyer and seller will continue to seamlessly support customers that are purchasing these decoupled but complementary goods or services from both parties.

Further, to the extent there are TSA arrangements, supplier agreements between buyer and seller, or other continuing relationships, it will be important for negotiations to be conducted in good faith as both parties will be dependent on each other to successfully navigate the transition beyond Day 1. What considerations must companies make when choosing a divestiture route, such as IPO, contribution to a joint venture, asset/stock sale, or sale through a statutory demerger? Masaki Ide, Partner, M&A Reorganization Services Determining which route to choose is not always easy. While an IPO may sound attractive for raising potentially large sums of cash, the process often takes more time than initially considered and frequently encounters regulatory hurdles both during and after the IPO process. The most common divestiture path is to sell assets or stock of a legal entity, or transfer assets to another legal entity through a statutory demerger (bunkatsu) before selling, as a demerger can often offer legal and tax Making the break: Selling and disposing non-core and under-performing assets in Japan 31 . advantages over a direct asset sale. Companies may also choose to transfer a business to a joint venture, yet this process may require continuing involvement of the seller and may not generate significant additional capital. This, however, can be an effective divestiture path for a step-by-step exit by gradually selling one’s interest to another JV partner over time (often times referred to as a silent exit). What can foreign buyers do to level the playing field when entering the Japanese market and find common ground with potential sellers/targets? Brian Lightle, Executive Officer, M&A Transaction Services Japanese sellers often favor working with a local buyer that understands the Japanese language and culture and is perceived to be more likely to support the employees and the overall business being divested. A foreign buyer, however, with the right strategy can also be seen as an attractive option. To best position themselves, a foreign buyer should consider sharing future business plans and strategy early in the deal process and demonstrate, to the extent possible, how they will support and grow the divested business without disrupting the seller's remaining core businesses. A seller may also view a foreign buyer as a more likely prospect if the foreign buyer is able to demonstrate how it will utilize its own sales channels to expand the market opportunities for the divested entity’s products and services. Having the divested business be successful is an important factor to not be overlooked as many Japanese sellers want to avoid being perceived as having abandoned their employees, customers, suppliers and communities associated with the divested business. Which industries are likely to have increased divestitures in the year ahead? Kotaro Watanabe, Partner, Corporate Financial Advisory We have been seeing a number of divestitures in the technology, manufacturing, and consumer business industries and expect that trend to continue.

Recently, many Japanese companies have begun to focus more on profitability and realigning their core operations around a well-defined corporate strategy. 32 The result is an increase in the divestment of non-core or underperforming businesses, notably by large corporate conglomerates. It remains to be seen if and when the Japanese trading houses will increase their focus on divesture activity as market pressures intensify. What post-merger integration issues are most likely to arise during a divestiture, particularly one where the buyer is a foreign multinational? Brian Lightle, Executive Officer, M&A Transaction Services Post-merger integration is often a challenge due to the time required to transition the divested entity to the buyer’s systems and processes, which can be further complicated by cultural differences and language barriers in the case of a foreign buyer. The seller will often need to continue providing support for the financial and human resource systems and IT infrastructure unless the divested entity operates almost entirely on a standalone basis, which is rarely the case. Specific to foreign or multinational buyers, we often see issues arise when the buyer is a public company and thus requires IFRS, or US GAAP financial reporting, yet the divested entity or the seller providing the financial support through a TSA, is not equipped to provide information that complies with the foreign accounting standards used by the buyer. Buyers should be aware of this early on and develop detailed plans to address these potential issues in order to avoid delays in closing the buyer's books. Another issue that often arises is benefit plan alignment as Japan maintains strict labor laws, often preventing a buyer from reducing the level of benefits previously provided to employees of the divested business.

The nature of the transaction’s legal structure can also impact whether employee consent is required to modify employee benefits. As such, understanding employee issues is an area a buyer should pay careful attention to as the employment laws in Japan are often different (and in most cases support the employee) from what a buyer might be accustomed to in another country. . Contact Deloitte For more information, please contact: Masami Nitta Managing Partner Financial Advisory Services masami.nitta@tohmatsu.co.jp Koichi Uchiyama Partner Marketing koichi.uchiyama@tohmatsu.co.jp Kazuhiro Fukushima Partner Clients & Industries kazuhiro.fukushima@tohmatsu.co.jp Brian Lightle Executive Officer M&A Transaction Services brian.lightle@tohmatsu.co.jp Financial Advisory Services Industry / Service Line Leaders: Kazuchika Hagiya Partner Manufacturing/Consumer Business kazuchika.hagiya@tohmatsu.co.jp Hideyuki Tozawa Managing Director Technology, Media and Telecommunications hideyuki.tozawa@tohmatsu.co.jp Dai Arakawa Partner Financial Services Industry dai.arakawa@tohmatsu.co.jp Koichi Tamura Partner Trading House koichi.tamura@tohmatsu.co.jp Hotaka Kobayakawa Partner Energy & Resources hotaka.kobayakawa@tohmatsu.co.jp Kazunori Matsumoto Partner Life Sciences & Health Care kazunori.matsumoto@tohmatsu.co.jp Tsutomu Kishi Partner Reorganization Services tsutomu.kishi@tohmatsu.co.jp Yoshihiro Maeda Partner Corporate Strategy yoshihiro.maeda@tohmatsu.co.jp Hiroki Okimoto Managing Director Chief Restructuring/Transformation Officer Services Deloitte Tohmatsu Anchor Management hiroki.okimoto@tohmatsu.co.jp Hironori Ishizaka Managing Director Chief Restructuring/ Transformation Officer Services Deloitte Tohmatsu Anchor Management hironori.ishizaka@tohmatsu.co.jp Deloitte Tohmatsu Financial Advisory LLC Tel: +81-3-6213-1180 Deloitte Tohmatsu Anchor Management Co., Ltd. Tel: +81-3-6213-3500 Deloitte Tohmatsu Tax Co. Tel: +81-3-6213-3800 Deloitte Tohmatsu Consulting LLC Tel: +81-3-5220-8600 Shin Tokyo Building 3-3-1 Marunouchi Chiyoda-ku, Tokyo 100-0005 Japan www.deloitte.com/jp Making the break: Selling and disposing non-core and under-performing assets in Japan 33 . About Mergermarket Mergermarket is an unparalleled, independent mergers and acquisitions (M&A) proprietary intelligence tool. Unlike any other service of its kind, Mergermarket provides a complete overview of the M&A market by offering both a forward-looking intelligence database and a historical deals database, achieving real revenues for Mergermarket clients. Remark, the events and publications arm of the Mergermarket Group, offers a range of publishing, research and events services that enable clients to enhance their own profile, and to develop new business opportunities with their target audience. For more information please contact: Naveet McMahon Publisher, Remark Asia naveet.mcmahon@mergermarket.com Brandon Taylor Managing editor, Remark Asia brandon.taylor@mergermarket.com Joyce Wong Production, Remark Asia joyce.wong@mergermarket.com 34 . . Deloitte Tohmatsu Group (Deloitte Japan) is the name of the Japan member firm group of Deloitte Touche Tohmatsu Limited (DTTL), a UK private company limited by guarantee, which includes Deloitte Touche Tohmatsu LLC, Deloitte Tohmatsu Consulting LLC, Deloitte Tohmatsu Financial Advisory LLC, Deloitte Tohmatsu Tax Co., DT Legal Japan, and all of their respective subsidiaries and affiliates. Deloitte Tohmatsu Group (Deloitte Japan) is among the nation's leading professional services firms and each entity in Deloitte Tohmatsu Group (Deloitte Japan) provides services in accordance with applicable laws and regulations. The services include audit, tax, legal, consulting, and financial advisory services which are delivered to many clients including multinational enterprises and major Japanese business entities through over 8,500 professionals in nearly 40 cities throughout Japan. For more information, please visit the Deloitte Tohmatsu Group (Deloitte Japan)’s website at www.deloitte.com/jp/en. Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries.

With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings worldclass capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 220,000 professionals are committed to making an impact that matters. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients.

Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. © 2015. For information, contact Deloitte Tohmatsu Financial Advisory LLC. .

Even more may have loss-making or underperforming business units draining resources or returns to shareholders. As a result, many are using divestitures to scale back in certain sectors and bolster others as they reassess their long-term business objectives and prepare to defend and expand market share. To understand how corporations in Japan – including domestic corporations and their multinational counterparts – are approaching divestitures, Deloitte, in partnership with Mergermarket, surveyed a select group of 60 market participants that had divested at least one asset within the past 18 months. Their collected sentiment has helped in understanding the current market with regard to divestiture activity, rationale, and the inherent challenges of finding a buyer and selling assets. It has also been invaluable in painting a picture of expectations in the coming months and years, as well as highlighting best practices to make a clean break. Making the break: Selling and disposing non-core and under-performing assets in Japan 3 .

4 . Executive summary Corporates turn to divestitures Among Japanese corporates and foreign multinationals surveyed in this report, 90% said they had completed at least one divestiture in Japan in the past 12 months, and 15% said they had completed two or more such transactions. Almost half (49%) of respondents said they had completed the sale of a majority or wholly-owned subsidiary, while 45% said their divestiture involved the sale of an equity method investment. 17% said they contributed a business to a joint venture (JV). Strategy drives sell offs and splits Selling an asset that was not core to the company’s overall business strategy was the top driver of divestitures (44% of respondents). This was followed by 21% who said they sold non-core or underperforming assets to fulfill financing needs and 18% who said their divestiture was linked to the disposal of a distressed business unit. Internal and external challenges The greatest internal challenge in their recent divestitures involved gaining support from management toward executing the deal (55% of respondents), followed by 46% who said separating subsidiary operations from parent operations created one of the greatest challenges.

External matters that affected the divestiture included the impact the process would have on the company’s image (56% of respondents), followed by the valuation gap between buyer and seller (43% of respondents). Increasing the odds of closing When divestitures failed to close, 35% of respondents said it was due to a lack of preparation of management teams. To alleviate tension or misunderstanding during the process, respondents said internal marketing campaigns or direct communication with managers proved beneficial to maintaining operations and preventing a flight of managers once the deal was announced. Sale prices meet expectations Overwhelmingly, respondents agreed that the prices received from recent divestitures were as expected (79% of respondents), while 13% said the value was more than they anticipated. When negotiating and completing the sale of an asset, preference was heavily weighted towards an exclusive negotiation (73% of respondents) as opposed to an auction sale process (27% of respondents). Preference for Japanese buyers In terms of preferred buyers, respondents favored Japanese acquirers (corporates, trading houses, and private equity firms) over their foreign counterparts by a noticeable gap: 95% in favor of Japanese corporates compared to 25% for foreign multinationals and an even smaller 7% for foreign private equity firms. Respondents noted that while foreign buyers may offer competitive or even higher valuations, domestic buyers are perceived as more likely to close a transaction. Foreign investors will remain acquisitive While 91% of respondents had closed recent divestitures with Japanese buyers, survey participants expect that foreign investors will continue to actively pursue acquisitions in Japan.

According to 41% of respondents, foreign multinationals are expected to show a high to moderate degree of interest in divested assets as they set their sights on the Japanese market. Foreign investors can increase their odds of being the selected bidder for a Japanese asset by being non-disruptive to the seller's core business (92% of respondents), a task that is often supported by utilizing Japanese financial advisors and consultants to facilitate bi-lingual negotiations and transactional guidance. Review early, review often Portfolio reviews were commonplace among respondents, with 40% saying these were carried out on an annual basis and 30% saying such reviews were completed every 6 months. These periodic evaluations helped managers prune their corporate portfolio by identifying businesses that no longer supported the long-term corporate goals and strategy. Making the break: Selling and disposing non-core and under-performing assets in Japan 5 . Profile of respondents and methodology From January to March 2015, Remark, the publishing division of Mergermarket, canvassed the opinions of 45 M&A practitioners from Japan and 15 that described themselves as foreign multinationals with operations in Japan. Fifty-eight percent described their company as a private company, while 42% said their organization was a public company. Forty-one percent of respondents said their company’s most recent annual revenue in US$ exceeded US$1bn. Within the graphed survey results, where figures add up to more than 100%, respondents were allowed to choose more than one answer. Where figures do not add up to 100%, this was due to rounding. Historical data includes all Mergermarket recorded transactions for the period 1 January 2012 to 30 June 2015. Transactions with a deal value greater than US$5m are included.

If the consideration is undisclosed, Mergermarket includes deals on the basis of a reported or estimated value of over US$5m. If the value is not disclosed, Mergermarket captures a transaction if the target’s turnover is greater than US$10m. Only completed and pending merger and acquisition deals are collated.

Transactions to be included usually involve a controlling stake in a company being transferred between two unrelated parties. In a case where the stake acquired is less than 30% (10% in Asia-Pacific), the deal will only be included if its value is greater than US$100m. All US$ symbols refer to US dollars unless otherwise stated. All ¥ symbols refer to Japanese yen unless otherwise stated. All data quoted is proprietary Mergermarket or Deloitte data unless otherwise stated. 6 . Which of the following best describes your company/firm? How would you categorize your company? 5% 25% 42% 58% 70% Private company Public company Japanese trading house Foreign corporate with operations in Japan Japanese corporate What was your company’s most recent annual revenue in US$? Within which industry does your main line of business operate?* Industrials 15% 43% 33% Financial Services 15% 8% Consumer 13% Energy, Mining & Utilities 8% Real Estate 18% 8% 8% 7% TMT 7% 11% Under $100m $251m-$500m $1bn-$5bn 5% $100m-$250m $501m-$1bn Business Services $5bn-$25bn $25bn or more Construction 5% Agriculture 3% Leisure 3% Transportation 2% *Percents may add up to more than 100% due to trading houses with numerous lines of business Making the break: Selling and disposing non-core and under-performing assets in Japan 7 . 8 . The business of break-ups: Divestitures in corporate Japan “In recent years some of our businesses have lost profitability. Where they once were catalysts for growth, some quickly became burdens to our bottom line. After careful consideration we decided that selling these businesses was the best option.” Director of corporate development, Japanese trading house Corporate divestitures can be an effective tool for unlocking value. The sale of an asset, a business unit or a subsidiary has the benefit of generating or freeing up capital and often increasing profitability margins and shareholder returns.

Divestitures can also allow a company to redeploy management resources to focus on the core businesses. As corporations realign their strategy and focus, divestitures in Japan are becoming a more common mechanism for extracting value from subsidiaries and non-core assets. This is true for both Japanese corporations and trading houses, as well as their multinational counterparts as both seller groups account for some of the top divestitures over the past year and a half (Figure 1). Figure 1: Top divestitures in 2014 – H1 2015 Announced Divested asset date Asset details Bidder company Bidder Seller country company Seller country Deal value JP¥m 4/28/14 Hartford Life Insurance Japanese annuity subsidiary Orix Life Insurance Corporation Japan Hartford Life Inc. USA 110,980 1/30/14 NEC Biglobe Ltd. Internet service provider Japan Industrial Partners Japan NEC Corporation Japan 110,112 11/17/14 Bushu Pharmaceuticals Ltd. Phamaceutical drug manufacturer Baring Private Equity Asia Hong Kong Tokio Marine Capital Co., Ltd. Japan 82,460 9/16/14 Pioneer DJ Corporation DJ entertainment business unit Kohlberg Kravis Roberts USA Pioneer Corporation Japan 57,908 5/12/15 Santen Pharmaceutical Anti-rheumatic pharmaceutical business Hyperion Pharma Co., Ltd. Japan Santen Japan Pharmaceutical Co., Ltd. 46,563 3/31/15 Citi Cards Japan Inc. Credit card business Sumitomo Mitsui Trust Holdings Inc. Japan Citigroup Inc. USA 41,334 2/3/15 Hitachi Metals Techno Ltd. Construction business The Carlyle Group USA Hitachi Metals Ltd. Japan 30,627 11/21/14 TIPNESS Ltd. Fitness club chain Nippon Television Holdings Japan Suntory Holdings Ltd. Japan 25,172 4/22/14 Net Japan Co., Ltd. Precious metal, jewelry, and diamond recycling company ORIX Corporation Japan Baring Private Equity Asia Hong Kong 24,056 3/25/15 FXCM Japan Commodities futures Rakuten Securities Co., Ltd. trading service Securities Inc. Japan FXCM Inc. USA 7,719 Making the break: Selling and disposing non-core and under-performing assets in Japan 9 .

Figure 2: How many corporate divestments have you completed in the past 12 months? Two or three None 14% 10% More than four 1% A divestiture is an increasingly popular solution for those assets that no longer serve the long-term corporate strategy. In our survey of business leaders, 90% said they divested at least one business in the past year (Figure 2). Of those, 15% said they completed two or more such deals. Highlighting the benefits of these transactions, the director of corporate development at a Japanese trading house said, “In recent years some of our businesses have lost profitability. Where they once were catalysts for growth, some quickly became burdens to our bottom line.

After careful consideration we decided that selling these businesses was the best option.” One 75% Close to half of respondents (49%) said their divestitures involved the sale of a majority or wholly-owned subsidiary (Figure 3). An equally large percentage of respondents (45%) noted deals involving the sale of an equity method investment, with proceeds being used to pay off debt or generate cash flow. Lower percentages of respondents said recent divestitures involved the contribution of a business unit to a joint venture (17%) or the sale of a carved-out business unit (12%). Figure 3: Which of the following divestiture types have you completed in the past 12 months? Sale of a majority or wholly-owned subsidiary 49% Sale of an equity method investment 45% Contribution of a business to a joint venture 17% Sale of a carved-out business 12% 10 .

Figure 4: Corporate divestitures in Japan 25 400 350 20 Number of divestitures 300 250 15 200 10 Deal value JP¥bn Trends and outlook for 2015 Recent activity may be the result of encouraging conditions following Prime Minister Shinzo Abe’s blueprint for structural reform and corporate reorganization (or ’Abenomics’). In line with this plan, many Japanese corporates are using divestitures to downsize and effectively reduce costs and increase cash flow and profitability. This has contributed to a steady increase in divestiture activity since 2013. Values reached a peak in the first half of 2014 totalling JP¥359.6bn (US$2.9bn) (Figure 4).

While deal values for H1 2015 sank markedly compared to H1 2014, the number of completed divestitures hit a record 23 for the first half of the year. This trend illustrates a growing awareness among Japanese corporates of the benefits of shrinking the corporate portfolio. 150 100 In the year ahead, respondents do not anticipate significant additional divestiture activity within their own organization. Only 17% said they expect to complete divestitures in the next 12 months (Figure 5).

While most said this was because they had already sold or spun out all non-core assets, others hinted that various internal and external challenges have and would continue to create stumbling blocks in the divestiture process. Still, there is potential for increases in divesting activity as 2015 progresses. Indeed, the continued focus for Japanese companies to increase profitability and shareholder returns and the recent fluctuations in the Nikkei 225 could spur sell offs later in the year. 5 50 0 0 H1 H2 2012 Number of divestitures H1 H2 2013 H1 H2 2014 H1 2015 Total deal value JP¥bn Source: Mergermarket Figure 5: How many divestitures do you expect to complete in the next 12 months? Two or three 6% None One 83% 11% Making the break: Selling and disposing non-core and under-performing assets in Japan 11 .

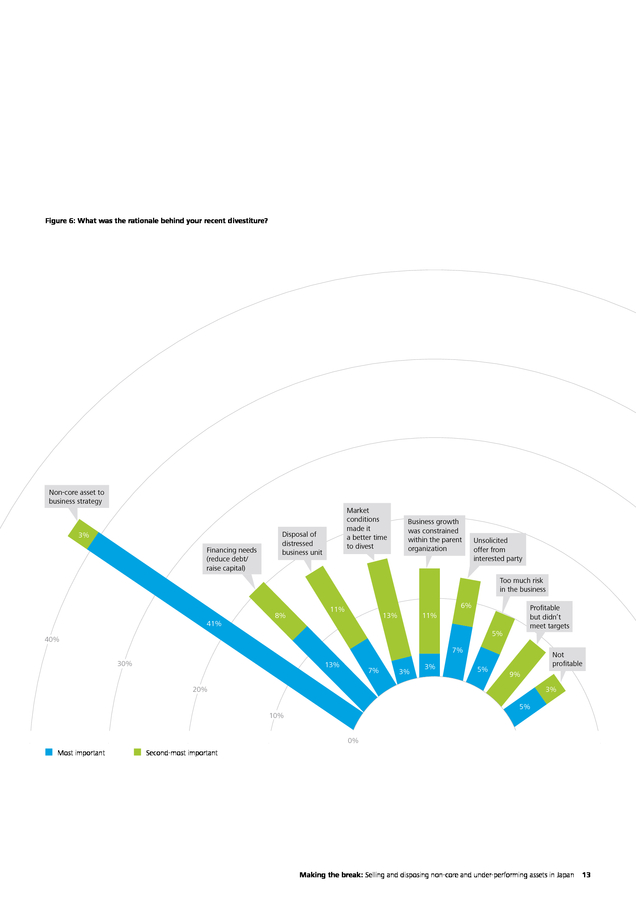

Strategy drives divestitures "In the Japanese market we see companies in certain market segments – notably, manufacturing and technology – becoming more focused on defining the company’s core competencies and business strategy and proactively divesting non-core or unprofitable businesses as opposed to reacting to external pressures after the company has already experienced undesirable results.” Masaki Ide, Deloitte Partner, M&A Reorganization Services Companies overextending their reach can quickly find themselves in precarious positions when resources become scarce or when market changes threaten growth. Accordingly, 44% of respondents said divesting non-core assets was either the most or second-most important driver of divestiture activity in the past year (Figure 6). Selling non-core assets made their companies leaner and more agile, qualities essential to weathering market volatility and possible disruption from market competitors. Purely financial motives were also behind recent activity. According to 21% of respondents describing their recent divestitures, proceeds were used to pay down debt, strengthen the balance sheet, and raise capital to support products and services core to the business or explore new market segments with high growth potential. Disposal of distressed or unprofitable business units was mentioned by 18% and 8% of respondents, respectively.

Especially in these cases, sellers often face the challenge of finding a new owner, be it another corporate or private equity firm, who can turn the unit around and return it to profitability. Timing of divestitures was another important consideration. According to 16% of respondents, company management waited until ideal market conditions manifested, making it an opportune moment to sell. 50% 12 . Figure 6: What was the rationale behind your recent divestiture? Non-core asset to business strategy 3% Financing needs (reduce debt/ raise capital) Market conditions made it a better time to divest Disposal of distressed business unit Business growth was constrained within the parent organization Unsolicited offer from interested party Too much risk in the business 41% 8% 6% 11% 13% Proï¬table but didn’t meet targets 11% 5% 40% 7% 30% 13% 7% 3% 3% 5% Not proï¬table 9% 3% 20% 5% 10% 0% Most important Second-most important Making the break: Selling and disposing non-core and under-performing assets in Japan 13 . Internal challenges: Addressing concerns among managers When divesting, various factors threaten to stall or destabilize the process. While externalities like shifts in the market make the extraction and sale of a business unit unpredictable, internal issues can also create challenges. In our survey, hurdles to divesting were most likely to arise from managers and management decisions. According to 55% of respondents, obtaining support from management was the greatest internal challenge (Figure 7). For our respondents, differing opinions among middle managers on how to carry out executive level directives often caused the divestiture to falter. In other cases, managers and even executive decision makers may cling to assets or business units with the hope of reviving sales or profitability. Equally, sentimentality for a unit that has ties to a company’s past may impede the decision to sell. Managers must realize that the sale of a business unit is a race against the clock.

Stalling the process, especially for a business unit with declining financial results, can not only lead to a loss in value in the asset, but also drive away potential buyers. Sellers must realize that the sooner the asset is divested, the sooner the seller can focus its attention on the remaining core businesses. Dispelling a failure mentality Rallying support from managers has the potential to add unnecessary difficulties in an already complex process. Getting managers on board requires an open discussion within the managerial ranks.