Description

M&A: Good

practices &

bad pitfalls

What to watch for

to assure success

The M&A process provides dealmakers with several opportunities

to enhance acquisition value — as well as pitfalls to destroy it.

What defines good targeting, negotiating, due diligence and integrating?

The process of conducting an M&A deal

has altered substantially over the years.

Yet the basic pillars of how deals are done

— targeting, negotiating, due diligence

and integrating — have remained constant

throughout these changes.

border M&A boom, for instance, has

brought issues surrounding cultural due

diligence and integration to the fore,

while the rise of M&A in the technology

sector has fueled a more flexible

approach to doing deals.

Despite this, the rapid pace of change

has seen these pillars take on new

significance over time. Technology, for

instance, has made gathering information

on potential targets exponentially easier

than in the past. Similarly, the advent of

online data rooms has significantly sped

up the due diligence process.

With all the changes to these processes,

however, dealmakers have had to react

accordingly in order to stay competitive in the

M&A market. And getting these processes

right is key to any successful deal.

On top of this, changing tastes and

macro trends have also changed the

focus of these processes.

The cross- With all these factors coming into prominence, Mergermarket and Vintage gathered five experts to discuss how the dealmaking process has changed. As well as this, they offer up the lessons they have learned, through decades of dealmaking experience, regarding what makes for successful M&A targeting, negotiation, due diligence and integration. We hope you enjoy this discussion and, as always, we welcome your feedback. Contents Target practice Digging deeper Putting it all together 2 6 10 . Target practice Sourcing potential acquisitions has become increasingly sophisticated over recent times. What does it entail, and how do you find the perfect target? MM (Mergermarket) BMM KM 2 I Vintage What factors, both internal and external, do you consider when determining a list of targets? It depends on the situation. From the point of view of a technology company doing standard deals, it would start with an analysis of your own gaps — in your product line, your technology, perhaps your geographic coverage. If you’ve decided to fill those gaps through inorganic means, then you need to identify what companies out there can fill the gaps. So, after compiling a list of potential targets, you narrow it down based on further criteria — size, affordability, reputation, product architecture and so on. The key items for us are strategic fit and the financial impact of the acquisition.

In terms of strategic fit, we have an internal team looking at the product categories and distribution channels we want “The pace of dealmaking has demanded that everyone improves their [targeting] skill levels because companies don’t have the time to make mistakes or lollygag through a transaction.” Matthew Gemello, Partner, Baker & McKenzie . The experts Brian Moriarty (BMM) former Vice President, Hewlett-Packard Karim Motani (KM) Corporate Development and Strategy Director, 1800flowers.com Jeff Drazan (JD) Managing Partner, Bertram Capital to get into. In terms of financial impact, the size of the business is a major factor for us. We’re usually after businesses with more than US$50m in sales, and ideally with better margins than ours. Even when a business doesn’t meet our financial criteria, our ability to drive cost and revenue synergies that will unlock value will put a target higher up on our list. MM What we do is help clients refine what they are looking for in the targeting phase, so that typically begins with a strategy discussion to determine the theme of the targeting.

A typical theme, for example, is looking at an acquisition strategy relative to a traditional strengths, weaknesses, opportunities and threats analysis. Some clients are looking to build on their strengths and leverage them in a synergistic way. Others are looking to shore up weaknesses and therefore plug holes in organizations or weaknesses in product offerings. Or then again, broadly speaking, responding to specific threats or opportunities available in the marketplace can drive an acquisition strategy.

After that baseline conversation with clients, then it becomes a question of financial and organizational capabilities. JD MM BMM We look for companies that fit our style of investing and value creation model. We are a buy and build shop with an additional emphasis on creating value through IT excellence. With that in mind, we look for companies that operate in fragmented industries with actionable acquisition targets and opportunities to apply our expertise in e-commerce and digital marketing to expand sales. Matthew Gemello (MG) Partner, Baker & McKenzie has to be the information available.

The sheer amount of information you can get a hold of, read up on and digest before even contacting people is astounding. MM Technology plays a big role today providing buyers the capability to screen lots of companies in many different ways and quickly. Access to information is huge as well, as Brian said, and intermediaries are important in that process from a relationship standpoint by connecting the data with the decision makers. KM For me, ten years ago you still had the ability to identify and acquire a proprietary target as far as private companies go. Now, every potential target can be found and there are a lot more intermediaries and the marketplace is much more transparent.

It is a lot more difficult to do a deal under the radar, which is a big change. MG Targeting has taken on a greater significance. Technology and innovation has a unique life cycle compared with other industries, which puts a premium on successful targeting in the tech space. Creative foresight and vision are often required to see the business at the idea stage. The pace of dealmaking has demanded that everyone improves their skill levels because companies don’t have time to make mistakes or lollygag through a transaction, or spend six months thinking about who their targets are. Successful firms are the ones who do that quickly and efficiently. And the ones that can’t do it are the ones that are missing out on these deals. JD From what you’ve seen, has targeting changed over the past five to ten years? In what way? Trends around target sizes ebb and flow, and can often hinge simply on how confident boards are. If they are optimistic, they will take bigger bets and flyers, and if they are more conservative they will do much fewer and much more solid M&A deals. Over the long term, the biggest change in targeting Marshall McKissack (MM) Managing Director, Head of M&A, Stephens Inc. MM BMM For us, we know better today what makes for a great Bertram deal.

Over time you develop experience with various value creation methodologies. We know what works for us. In your experience, what lessons did you learn for this stage of the deal? You have to keep a broad, open and creative mind when it comes to thinking about targets. Of course you have to be out there in the market physically — M&A: Good practices & bad pitfalls I 3 .

that means going to trade shows and, especially in tech, being close with the venture capital houses. It’s also vital to listen to your customers and sales people. Some of the best deals I’ve worked on have come from the sales force. In addition, your corporate development group should bring an outside perspective that might refine what you need. KM JD 4 I Vintage I’ve always worked for patient buyers or acquirers, and in many instances I have realized that patience does pay. For example, a deal we recently closed was with a target that we had been circling for close to ten years.

The firm had changed hands in that time, but we kept good relationships with the successive owners and eventually found ourselves in a place where the timing and rationale was right to do a deal. Our patience was rewarded. We know when to stretch and when not to stretch from a valuation perspective. It all comes down to the investment thesis on value creation.

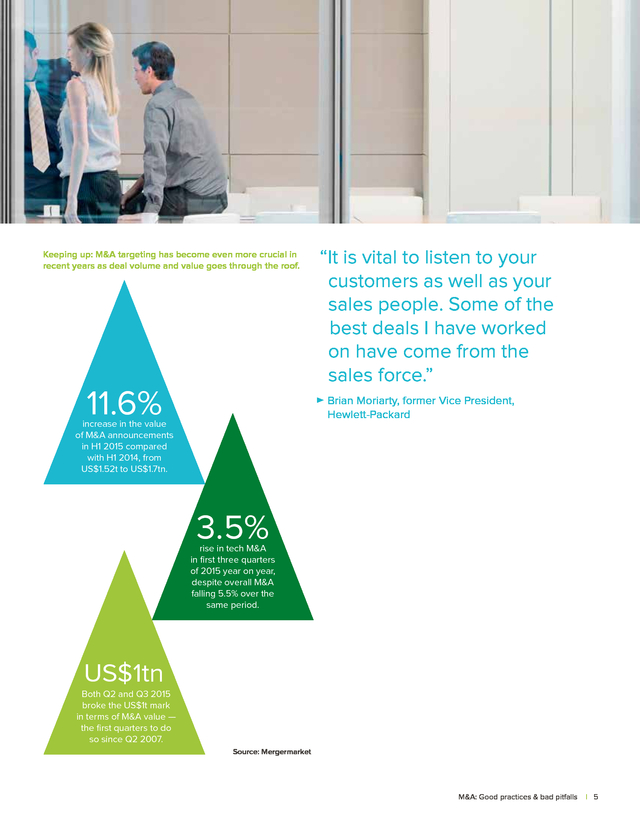

We know with high confidence what we can and cannot do. . Keeping up: M&A targeting has become even more crucial in recent years as deal volume and value goes through the roof. 11.6% “It is vital to listen to your customers as well as your sales people. Some of the best deals I have worked on have come from the sales force.” Brian Moriarty, former Vice President, Hewlett-Packard increase in the value of M&A announcements in H1 2015 compared with H1 2014, from US$1.52t to US$1.7tn. 3.5% rise in tech M&A in first three quarters of 2015 year on year, despite overall M&A falling 5.5% over the same period. US$1tn Both Q2 and Q3 2015 broke the US$1t mark in terms of M&A value — the first quarters to do so since Q2 2007. Source: Mergermarket M&A: Good practices & bad pitfalls I 5 . Digging deeper The negotiation and due diligence processes provide acquirers with one of the first times they can really get to know a company — both across the boardroom table and via its financials. How should they ensure they make the most of this opportunity? Meeting a potential target for the first time offers acquirers their first real glimpse into the heart of the company. On top of that, taking the first steps down the due diligence road provides the chance to see what a potential acquisition is really made of. Preparing for these steps is crucial. Marshall McKissack, head of M&A at investment bank Stephens Inc., points out that both negotiation and due diligence are intertwined. “I really think [a negotiation] starts with the due diligence process and determining where companies see risk”, he says.

“After you figure out where clients see issues, you can negotiate to protect their interests in the various transaction documents. Secondly, the market constantly evolves around terms and other conditions — having a sense of where the market is can be very beneficial in order to move a deal forward.” Prepping a deal Away from this, preparation for a deal can consist of several things, including forward planning, prioritizing, thinking from the other side and calmness. For Brian Moriarty, former vice president at HewlettPackard, thinking about what the businesses would be like combined is necessary even at this early stage, given that reaching a negotiation implies an interest on both sides. “You need to create a business integration plan, even at this stage, that is approved and supported,” he says. “There is no point negotiating unless you know you want to buy the target. This all comes before you even talk about price.” 6 I Vintage .

On top of this, buyers also need to center negotiation efforts around what interested them enough to get around the negotiating table in the first place. “You need to crystallize what the key drivers of the transaction are,” says Matthew Gemello, partner at Baker & McKenzie. “The majority of your negotiating efforts and resources should focus strategically on getting to an optimal result on those particular drivers.” One often overlooked point is putting yourself in the shoes of the target, and indeed the other stakeholders in the deal. “In our last deal we learned about the behavior of the bankers, as well as the seller’s behavior in prior deals,” says Jeff Drazan, managing partner at Bertram Capital. “You also need to make sure that you’re asking a lot of questions.” “You also need to bear in mind the target’s mind frame,” adds Moriarty.

“If they are private, for instance, why are they selling? What are their price expectations? This can help to structure an offer that you make.” Finally, adds Karim Motani, corporate development and strategy director for 1800flowers.com, it is important to be measured in your reactions. “Our last deal was an auction, and as a strategic, we’re not involved in as many auction processes as private equity firms, so we hired a banker to negotiate on our behalf,” he says. “Using an intermediary created space between ourselves and the target; it gave us time to be considered in our responses.

I believe this helped us to secure the deal at the right price.” Smooth things over Yet even with the best preparation in the world, acquiring negotiators need to accept that there will be some issues that both parties will wrangle over. “There are always sticking points,” says McKissack. “That’s why they call it a negotiation.” Indeed, just because an opposing party isn’t keen on some parts of an acquisition does not mean they don’t want to complete the transaction. It is more important to understand their concerns about the proposal. “If you’re open to more creative solutions, the best thing to ask is why they are taking that position,” says Moriarty.

“Often times, it’s not that they are dead against the deal, it is just that they have concerns about certain aspects. If there is a problem, you have to be able to identify a creative solution around it, and asking is the first step to that.” Creativity is something that is particularly acute the technology industry, and is much more noticeable since the sector’s rise in recent years. “The thorny negotiating points are not really surprising, given there’s such a narrow playing field of issues that come up.

What has changed, however – particularly evident in Silicon Valley and with technology-based plays — is a greater desire to be flexible to solve problems,” says Gemello. “With M&A players in the more traditional industries, there is a greater tendency to have two sides entrenched on their issues and wedded to their ‘standard’ way of dealing.” For Drazan, it’s also important that acquirers reiterate a solid business case for the deal. “You have to hit them straight with the facts,” he says. “Financial due diligence, accounting due diligence and quality of earnings are the basis of the foundation of value.” Marshall McKissack, Managing Director, Head of M&A, Stephens Inc. M&A: Good practices & bad pitfalls I 7 M&A: Good practices & bad pitfalls .

“Your behavior should be consistent as well. And your case must have a really solid rationale.” On top of this, acquiring negotiators shouldn’t forget that identifying potential trade-offs could help to bring the two sides closer together. “We first try to weigh up both sides’ sticking points and then look at the deal terms,” says Motani. “From that, we can look at possible trade-offs. In a recent deal, one of the sticking points we had surrounded break-up fees, escrow accounts and warranties.

And if you’re pushed, you have to be willing to make concessions.” Credit where it’s due Away from the boardroom, the due diligence process has become another avenue for companies, as well as thoroughly investigating their counterparts, to become more trusting of each other. “These days, sellers often have conventions in place in order to expedite the due diligence process. Bigger companies, for instance, will put forth a quality of earnings report,” says Motani. “It helps to get the parties more comfortable with each other while speeding up the process as well.” In terms of the process, due diligence has already been sped up exponentially over the last few decades. “It’s certainly moved — on a detail basis — almost exclusively online,” says McKissack.

“A lot of it is done in online data rooms in conjunction with lots of phone calls, compared with 10 to 15 years ago when a lot of it was done with paper on site, which was quite laborious.” It isn’t just the process that has changed, however. For Moriarty, due diligence has become a much more forward-thinking exercise. “When I started, due diligence was about identifying liabilities you did not know about. This, of course, still happens,” he says. Now, however, the process is much more focused on the future, on things such as integration plans, business plans and confirming assumptions.” Gemello agrees, adding that companies are becoming increasingly practical, especially in the midst of a cross- 8 I Vintage border M&A boom.

“One big shift has been having buyers who are increasingly comfortable enough with their risk management profile, and aren’t afraid to do business as the locals do – not across the board, but there is a big commercial willingness to do that,” he says. “It is that it’s a very interesting overlay of commercial and strategic practicality.” Diligent value While what consists of due diligence may have changed, what takes precedence in the process hasn’t. “It’s biased to whatever drives value,” says Moriarty.

“It’s also biased towards finding liabilities as well, of course, and both are critical. However, unless you do diligence and understand the former, there’s no need for the latter.” McKissack agrees. “Financial due diligence, accounting due diligence and quality of earnings — these are the basis of the foundation of value.

Legal, risk and contract reviews are also important. But they all drive value at the end of the day, whether it’s in dollars and cents or by protecting yourself from unnecessary risk.” From other perspectives, however, certain issues are more important than others at the moment. “The hottest button in the world right now is compliance,” Gemello says. “Unknowingly buying your way into a compliance problem can destroy the underlying value of the acquisition, putting aside the commercial and reputational impact on a buyer and its own business.

We are spending more time with clients at earlier stages of their deals, as they strive to better understand the local regulatory climate(s) in which their targets are operating. It’s been far and away the primary focus.” For Drazan, focusing on the product and the seller’s customers takes precedent. “Customer references are the single most important component of our diligence,” he says.

“What choices did the customer have before buying, did the product or service live up to the expectation, and how has the company behaved in the aftermath of the sale? Getting the . answers to those questions is crucial. Management references come next after that hurdle.” Motani adds that, as well as ensuring that the lawful side of things are taken care of, due diligence is also vital to understanding the competitive landscape. “The legal and contract side takes precedent. We don’t want to have any legal liabilities postpurchase,” he says. “We also want to adjust our competitive positioning. This means looking at the competitive nature of the market, as well as other macro-level issues we’re up against.” Lessons learned Our experts identified five key lessons that acquirers should bear in mind in order to make the most of their negotiations. Be prepared.

“I’m always surprised that people don’t do much real preparation work for negotiations as they should,” says Moriarty. “They do the valuation work and things around financial projections — but they rarely consider what is actually in their counterpart’s head.” 1. Gemello agrees, particularly when it comes to cross-border dealmaking. “Gone are the days of the imperialistic buyer that just jams something down the throat of the seller,” he says. “I spend a lot more time with my clients getting smart about the target, about how they do business, about how they will operate and behave in the negotiation, just so we can clear out as much unnecessary noise as possible.” Anchor away.

Moriarty believes that putting the question to the other side first can give a psychological advantage when discussing terms around the table. “It’s important to make the first offer,” he says. “This is a concept called anchoring.

If you make the first offer, the other side will often gravitate towards it. I’ve used it myself, and seen it used against us in negotiations. I’m surprised at how it effects people and it’s a very powerful tool.” 2. 3. Friend, not foe.

“M&A is inherently a social interaction,” says Gemello. “You’ve got to effectively build a bridge. As the world gets smaller, successful dealmakers have to bridge the social and cultural differences between parties, and take them into account when doing a deal.” This necessity means that meeting your counterparts in person takes on paramount importance.

“The heightened era of electronic connectivity puts a premium on face-to-face meetings. You can’t substitute for time together between principals to build relationships,” he says. “It’s the principalto-principal relationship that will carry the deal to success if it’s going to happen, and the business leaders negotiating the transaction at the highest level need to have trust between them so they can efficiently work through the deal.” Be upfront and honest.

Facing the big tasks head on first can save you time down the line. “The biggest thing for me is pinpointing where the issues are, to the extent you can sooner rather than later, and getting those items out on the table for conversation.” If you have an opportunity to do that, you can get over the big hurdles early.” 4. When doing this, however, it is vital that dealmakers are honest and open to compromise. “Integrity is everything,” says Drazan.

“Never say never unless you mean it.” Time is money. If you’re able to take your time through these processes, this can help valuegeneration greatly. “If you have time on your side, you will benefit greatly from a valuation perspective,” says Motani.

“I’ve been involved in auctions and direct sales, and while auctions can accelerate the time to closing, a direct deal usually results in a more buyer friendly purchase price.” 5. M&A: Good practices & bad pitfalls I 9 M&A: Good practices & bad pitfalls . Putting it all together After finding the perfect target and getting the deal over the line, companies can sometimes forget that fitting them togetheris crucial to a successful transaction. What are the key factors that make up a successful integration? MM (Mergermarket) BMM KM 10 I Vintage What are the key priorities in your integrations? There are several schools of thought on this and all have rationales. For me it’s key to integrate quickly because when you close, that is when a target will be at its most receptive to change. Missing this can be costly and destroy deal value. Achieving the financial targets is almost always the biggest priority. On top of this, it’s important to retain needed staff in such a turbulent time. We are a very seasonal business, and we tend to acquire other seasonal businesses.

When integrating, our key priority is to ensure minimal disruption around our major seasons — Christmas, Valentine’s Day, Mother’s Day and so on. “Our key priority when integrating is to ensure minimal disruption around our key seasons. When we acquired our most recent business, the integration stopped when we hit peak season, and picked up again afterwards.” Karim Motani, Corporate Development and Strategy Director, 1800flowers.com . The experts Brian Moriarty (BMM) former Vice President, Hewlett-Packard Karim Motani (KM) Corporate Development and Strategy Director, 1800flowers.com Jeff Drazan (JD) Managing Partner, Bertram Capital For instance, when we acquired our most recent business, the integration work slowed during our peak season, and it picked up again immediately afterwards. MG Speed and efficiency. We’ve got to go to market with the asset we just spent the money on, and whatever integration steps need to happen to allow us to do that efficiently and effectively, we have to do it. That recognition by clients is the single biggest change over the last 10 to 15 years. The integration is increasingly viewed as important as the acquisition itself. The value from the acquisition can erode quickly if the acquired business is not properly intergrated into the larger group.

Yet, speed and efficiency have always been the priorities when it comes to integration; what’s changed is the amount of attention and focus our clients are giving it. Matthew Gemello (MG) Partner, Baker & McKenzie MM BMM Marshall McKissack (MM) Managing Director, Head of M&A, Stephens Inc. What are the main obstacles you face when integrating, and how have you learned to overcome them? Before doing serious integration planning, a buyer must consider three fundamental questions: are you going to integrate?; if so, when?; and how long should integration take (i.e., are you willing to potentially adopt policies and procedures of the target in the merged company or do you want to align the target to the acquirer’s practices). Many buyers close deals without a fundamental view on these questions; this ultimately impacts the business plan. The biggest hurdle that we frequently see is internal resistance from the C-suite that manifests itself in two areas. The first is a more philosophical perspective as to the need to integrate and how critical integration is to acheiving longer-term objectives. Buyers simply have to get over that hump.

The second area is resource allocation and the internal importance placed by senior management on the integration effort itself. In more cases than not, companies have a dedicated M&A team that’s doing the buy-side of the transaction, and those folks disappear after the closing party and don’t have to deal with what’s afterwards. There are a host of employees who play a greater role on the operational side, who have to undertake these integration activities alongside their day to day activities. The priorities can vary. Some buyers need access to synergies as soon as possible, some buyers want to make sure when the deal closes that the business runs as smoothly and efficiently as possible, with no interruptions for employees and customers and the organization functions as smoothly as it did the day before you close.

It’s really about making sure those customers and employees are onboarded to your plan. From what I’ve seen, the companies that have a plan for integration that is well documented, well supervised, well thought out and benchmarked — those are the ones that are doing the best. It’s about recognizing the synergies you’ve identified and valued before buying, and making sure it comes to fruition. Buyers who have planned and prepared for those things and do it out of the gate are the most successful. JD Cultural aspects are also a challenge, and it is something you should expect to face when combining two different companies and company cultures. Motivating parties on both sides to help out with the integration can also be hard, especially as those people will still be doing their day-to-day jobs and have full calendars. It’s important to clearly communicate the value that the deal will generate, and that integrating properly is a key driver of that value.

Finally, you have to manage employee concerns. In the immediate aftermath of a deal there will be lots of questions and concerns from your employees, and addressing these questions and concerns early is very important. MG MM KM For us it’s all about the people. You can’t run a business without good people.

Then, we focus on IT, which is our value driver. M&A: Good practices & bad pitfalls I 11 . The companies that do it well are the ones that have dedicated integration teams, with a senior integration leader who has some gravitas within the company, who can really drive home the importance of the post-acquisition steps within the larger organization. Success here is dependent about driving full engagement and commitment. To overcome these challenges, we spend a lot of time talking about the integration up front including at the targeting stage. We really try to help clients think about synergies that can reduce the overall cost of the transaction, so we’re doing a lot of dualtrack due diligence for both the deal as well as the downstream integration, and thinking potentially where contracts or people might be moved or assets might be relocated. Getting the synergistic potential on the table early is often a critical step to buy-in from the C-suite. Interestingly, it takes one successful integration for clients to see the value.

We have found that this is not a continual fight, it’s more of an episodic battle and trying to help clients get over that hump. When they do, they’re cruising from there because the potential to save costs and accelerate “How you organize a project dictates its success. You can make a lot of smart decisions about what you’re going to do, but if you have a key function missing, you’re really in trouble.” Matthew Gemello, Partner, Baker & McKenzie 12 I Vintage the larger strategic goals are obvious.

We have three clients that have a VP to EVP level head of integration, and I can’t say that I knew those positions existed five to ten years ago. MM JD MM BMM Some problems are a result of those cultural differences, and not identifying those fairly with a corresponding plan to manage. A lot of organizations have fundamentally different cultures, that sometimes is difficult to understand and plan for. Understanding culture is a great perspective to have to properly assimilate organizations. As Marshall said, culture is everything.

You have to make sure you assimilate correctly, do so with integrity and communicate the changes effectively. What would you say are three key lessons of successful post-merger integration? Decision making must be quick. You need the firm to make decisions quickly as stalling can sometimes kill deals. It is often better to be quick — and sometimes, wrong — than to wait for incremental information. Secondly, as I mentioned, it is key to integrate quickly.

People are ready for a change right at closing, and it is hard to get that mindset again if you only start to integrate six to nine months later. Capitalize on the energy. Finally, it is key to consider cultural differences — something buyers sometimes overlook. You must assess the target’s culture and how it relates to your company and how it will affect it. Helping people to identify the differences and change them is essential, and often overlooked. KM As Brian hinted at, a lot of it centers on speed. For one, you should start integration planning before closing the deal.

This will help you get a clearer picture of what the integration will look like, and prepare people in advance. Secondly, the process should start on day one. And finally, ensure any personnel changes are done as soon as possible. .

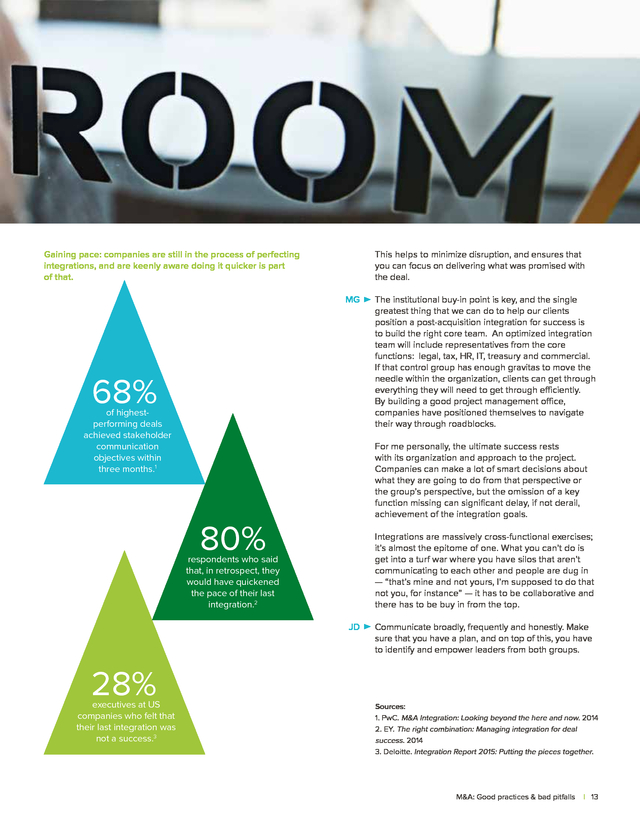

Gaining pace: companies are still in the process of perfecting integrations, and are keenly aware doing it quicker is part of that. This helps to minimize disruption, and ensures that you can focus on delivering what was promised with the deal. MG 68% of highestperforming deals achieved stakeholder communication objectives within three months.1 The institutional buy-in point is key, and the single greatest thing that we can do to help our clients position a post-acquisition integration for success is to build the right core team. An optimized integration team will include representatives from the core functions: legal, tax, HR, IT, treasury and commercial. If that control group has enough gravitas to move the needle within the organization, clients can get through everything they will need to get through efficiently. By building a good project management office, companies have positioned themselves to navigate their way through roadblocks. For me personally, the ultimate success rests with its organization and approach to the project. Companies can make a lot of smart decisions about what they are going to do from that perspective or the group’s perspective, but the omission of a key function missing can significant delay, if not derail, achievement of the integration goals. 80% Integrations are massively cross-functional exercises; it’s almost the epitome of one. What you can’t do is get into a turf war where you have silos that aren’t communicating to each other and people are dug in — “that’s mine and not yours, I’m supposed to do that not you, for instance” — it has to be collaborative and there has to be buy in from the top. respondents who said that, in retrospect, they would have quickened the pace of their last integration.2 JD Communicate broadly, frequently and honestly. Make sure that you have a plan, and on top of this, you have to identify and empower leaders from both groups. 28% executives at US companies who felt that their last integration was not a success.3 Sources: 1.

PwC. M&A Integration: Looking beyond the here and now. 2014 2.

EY. The right combination: Managing integration for deal success. 2014 3.

Deloitte. Integration Report 2015: Putting the pieces together. M&A: Good practices & bad pitfalls I 13 . 14 I Vintage . About Vintage Vintage, a PR Newswire division, is a top-three provider of full-service regulatory compliance and shareholder communications services, delivered across our three practice areas: Capital Markets, Corporate Services and Institutional & Fund Services. Founded in 2002 and acquired by PR Newswire in 2007, Vintage has evolved to become the industry’s intelligent value choice. We deliver a flexible balance of people, facilities and technology to ensure that regulatory compliance and shareholder communications processes are efficient, transparent and painless. Services include IPO registrations, transactions, virtual data rooms, EDGAR & XBRL filing, typesetting, financial printing and investor relations websites. theVintageGroup.com Trevor Loe Vice President Vintage, a Division of PR Newswire Direct: 201.360.6425 | Mobile: 440.787.9960 trevor.loe@thevintagegroup.com www.TheVintageGroup.com M&A: Good practices & bad pitfalls About Vintage I 15 . 16 I Vintage .

The cross- With all these factors coming into prominence, Mergermarket and Vintage gathered five experts to discuss how the dealmaking process has changed. As well as this, they offer up the lessons they have learned, through decades of dealmaking experience, regarding what makes for successful M&A targeting, negotiation, due diligence and integration. We hope you enjoy this discussion and, as always, we welcome your feedback. Contents Target practice Digging deeper Putting it all together 2 6 10 . Target practice Sourcing potential acquisitions has become increasingly sophisticated over recent times. What does it entail, and how do you find the perfect target? MM (Mergermarket) BMM KM 2 I Vintage What factors, both internal and external, do you consider when determining a list of targets? It depends on the situation. From the point of view of a technology company doing standard deals, it would start with an analysis of your own gaps — in your product line, your technology, perhaps your geographic coverage. If you’ve decided to fill those gaps through inorganic means, then you need to identify what companies out there can fill the gaps. So, after compiling a list of potential targets, you narrow it down based on further criteria — size, affordability, reputation, product architecture and so on. The key items for us are strategic fit and the financial impact of the acquisition.

In terms of strategic fit, we have an internal team looking at the product categories and distribution channels we want “The pace of dealmaking has demanded that everyone improves their [targeting] skill levels because companies don’t have the time to make mistakes or lollygag through a transaction.” Matthew Gemello, Partner, Baker & McKenzie . The experts Brian Moriarty (BMM) former Vice President, Hewlett-Packard Karim Motani (KM) Corporate Development and Strategy Director, 1800flowers.com Jeff Drazan (JD) Managing Partner, Bertram Capital to get into. In terms of financial impact, the size of the business is a major factor for us. We’re usually after businesses with more than US$50m in sales, and ideally with better margins than ours. Even when a business doesn’t meet our financial criteria, our ability to drive cost and revenue synergies that will unlock value will put a target higher up on our list. MM What we do is help clients refine what they are looking for in the targeting phase, so that typically begins with a strategy discussion to determine the theme of the targeting.

A typical theme, for example, is looking at an acquisition strategy relative to a traditional strengths, weaknesses, opportunities and threats analysis. Some clients are looking to build on their strengths and leverage them in a synergistic way. Others are looking to shore up weaknesses and therefore plug holes in organizations or weaknesses in product offerings. Or then again, broadly speaking, responding to specific threats or opportunities available in the marketplace can drive an acquisition strategy.

After that baseline conversation with clients, then it becomes a question of financial and organizational capabilities. JD MM BMM We look for companies that fit our style of investing and value creation model. We are a buy and build shop with an additional emphasis on creating value through IT excellence. With that in mind, we look for companies that operate in fragmented industries with actionable acquisition targets and opportunities to apply our expertise in e-commerce and digital marketing to expand sales. Matthew Gemello (MG) Partner, Baker & McKenzie has to be the information available.

The sheer amount of information you can get a hold of, read up on and digest before even contacting people is astounding. MM Technology plays a big role today providing buyers the capability to screen lots of companies in many different ways and quickly. Access to information is huge as well, as Brian said, and intermediaries are important in that process from a relationship standpoint by connecting the data with the decision makers. KM For me, ten years ago you still had the ability to identify and acquire a proprietary target as far as private companies go. Now, every potential target can be found and there are a lot more intermediaries and the marketplace is much more transparent.

It is a lot more difficult to do a deal under the radar, which is a big change. MG Targeting has taken on a greater significance. Technology and innovation has a unique life cycle compared with other industries, which puts a premium on successful targeting in the tech space. Creative foresight and vision are often required to see the business at the idea stage. The pace of dealmaking has demanded that everyone improves their skill levels because companies don’t have time to make mistakes or lollygag through a transaction, or spend six months thinking about who their targets are. Successful firms are the ones who do that quickly and efficiently. And the ones that can’t do it are the ones that are missing out on these deals. JD From what you’ve seen, has targeting changed over the past five to ten years? In what way? Trends around target sizes ebb and flow, and can often hinge simply on how confident boards are. If they are optimistic, they will take bigger bets and flyers, and if they are more conservative they will do much fewer and much more solid M&A deals. Over the long term, the biggest change in targeting Marshall McKissack (MM) Managing Director, Head of M&A, Stephens Inc. MM BMM For us, we know better today what makes for a great Bertram deal.

Over time you develop experience with various value creation methodologies. We know what works for us. In your experience, what lessons did you learn for this stage of the deal? You have to keep a broad, open and creative mind when it comes to thinking about targets. Of course you have to be out there in the market physically — M&A: Good practices & bad pitfalls I 3 .

that means going to trade shows and, especially in tech, being close with the venture capital houses. It’s also vital to listen to your customers and sales people. Some of the best deals I’ve worked on have come from the sales force. In addition, your corporate development group should bring an outside perspective that might refine what you need. KM JD 4 I Vintage I’ve always worked for patient buyers or acquirers, and in many instances I have realized that patience does pay. For example, a deal we recently closed was with a target that we had been circling for close to ten years.

The firm had changed hands in that time, but we kept good relationships with the successive owners and eventually found ourselves in a place where the timing and rationale was right to do a deal. Our patience was rewarded. We know when to stretch and when not to stretch from a valuation perspective. It all comes down to the investment thesis on value creation.

We know with high confidence what we can and cannot do. . Keeping up: M&A targeting has become even more crucial in recent years as deal volume and value goes through the roof. 11.6% “It is vital to listen to your customers as well as your sales people. Some of the best deals I have worked on have come from the sales force.” Brian Moriarty, former Vice President, Hewlett-Packard increase in the value of M&A announcements in H1 2015 compared with H1 2014, from US$1.52t to US$1.7tn. 3.5% rise in tech M&A in first three quarters of 2015 year on year, despite overall M&A falling 5.5% over the same period. US$1tn Both Q2 and Q3 2015 broke the US$1t mark in terms of M&A value — the first quarters to do so since Q2 2007. Source: Mergermarket M&A: Good practices & bad pitfalls I 5 . Digging deeper The negotiation and due diligence processes provide acquirers with one of the first times they can really get to know a company — both across the boardroom table and via its financials. How should they ensure they make the most of this opportunity? Meeting a potential target for the first time offers acquirers their first real glimpse into the heart of the company. On top of that, taking the first steps down the due diligence road provides the chance to see what a potential acquisition is really made of. Preparing for these steps is crucial. Marshall McKissack, head of M&A at investment bank Stephens Inc., points out that both negotiation and due diligence are intertwined. “I really think [a negotiation] starts with the due diligence process and determining where companies see risk”, he says.

“After you figure out where clients see issues, you can negotiate to protect their interests in the various transaction documents. Secondly, the market constantly evolves around terms and other conditions — having a sense of where the market is can be very beneficial in order to move a deal forward.” Prepping a deal Away from this, preparation for a deal can consist of several things, including forward planning, prioritizing, thinking from the other side and calmness. For Brian Moriarty, former vice president at HewlettPackard, thinking about what the businesses would be like combined is necessary even at this early stage, given that reaching a negotiation implies an interest on both sides. “You need to create a business integration plan, even at this stage, that is approved and supported,” he says. “There is no point negotiating unless you know you want to buy the target. This all comes before you even talk about price.” 6 I Vintage .

On top of this, buyers also need to center negotiation efforts around what interested them enough to get around the negotiating table in the first place. “You need to crystallize what the key drivers of the transaction are,” says Matthew Gemello, partner at Baker & McKenzie. “The majority of your negotiating efforts and resources should focus strategically on getting to an optimal result on those particular drivers.” One often overlooked point is putting yourself in the shoes of the target, and indeed the other stakeholders in the deal. “In our last deal we learned about the behavior of the bankers, as well as the seller’s behavior in prior deals,” says Jeff Drazan, managing partner at Bertram Capital. “You also need to make sure that you’re asking a lot of questions.” “You also need to bear in mind the target’s mind frame,” adds Moriarty.

“If they are private, for instance, why are they selling? What are their price expectations? This can help to structure an offer that you make.” Finally, adds Karim Motani, corporate development and strategy director for 1800flowers.com, it is important to be measured in your reactions. “Our last deal was an auction, and as a strategic, we’re not involved in as many auction processes as private equity firms, so we hired a banker to negotiate on our behalf,” he says. “Using an intermediary created space between ourselves and the target; it gave us time to be considered in our responses.

I believe this helped us to secure the deal at the right price.” Smooth things over Yet even with the best preparation in the world, acquiring negotiators need to accept that there will be some issues that both parties will wrangle over. “There are always sticking points,” says McKissack. “That’s why they call it a negotiation.” Indeed, just because an opposing party isn’t keen on some parts of an acquisition does not mean they don’t want to complete the transaction. It is more important to understand their concerns about the proposal. “If you’re open to more creative solutions, the best thing to ask is why they are taking that position,” says Moriarty.

“Often times, it’s not that they are dead against the deal, it is just that they have concerns about certain aspects. If there is a problem, you have to be able to identify a creative solution around it, and asking is the first step to that.” Creativity is something that is particularly acute the technology industry, and is much more noticeable since the sector’s rise in recent years. “The thorny negotiating points are not really surprising, given there’s such a narrow playing field of issues that come up.

What has changed, however – particularly evident in Silicon Valley and with technology-based plays — is a greater desire to be flexible to solve problems,” says Gemello. “With M&A players in the more traditional industries, there is a greater tendency to have two sides entrenched on their issues and wedded to their ‘standard’ way of dealing.” For Drazan, it’s also important that acquirers reiterate a solid business case for the deal. “You have to hit them straight with the facts,” he says. “Financial due diligence, accounting due diligence and quality of earnings are the basis of the foundation of value.” Marshall McKissack, Managing Director, Head of M&A, Stephens Inc. M&A: Good practices & bad pitfalls I 7 M&A: Good practices & bad pitfalls .

“Your behavior should be consistent as well. And your case must have a really solid rationale.” On top of this, acquiring negotiators shouldn’t forget that identifying potential trade-offs could help to bring the two sides closer together. “We first try to weigh up both sides’ sticking points and then look at the deal terms,” says Motani. “From that, we can look at possible trade-offs. In a recent deal, one of the sticking points we had surrounded break-up fees, escrow accounts and warranties.

And if you’re pushed, you have to be willing to make concessions.” Credit where it’s due Away from the boardroom, the due diligence process has become another avenue for companies, as well as thoroughly investigating their counterparts, to become more trusting of each other. “These days, sellers often have conventions in place in order to expedite the due diligence process. Bigger companies, for instance, will put forth a quality of earnings report,” says Motani. “It helps to get the parties more comfortable with each other while speeding up the process as well.” In terms of the process, due diligence has already been sped up exponentially over the last few decades. “It’s certainly moved — on a detail basis — almost exclusively online,” says McKissack.

“A lot of it is done in online data rooms in conjunction with lots of phone calls, compared with 10 to 15 years ago when a lot of it was done with paper on site, which was quite laborious.” It isn’t just the process that has changed, however. For Moriarty, due diligence has become a much more forward-thinking exercise. “When I started, due diligence was about identifying liabilities you did not know about. This, of course, still happens,” he says. Now, however, the process is much more focused on the future, on things such as integration plans, business plans and confirming assumptions.” Gemello agrees, adding that companies are becoming increasingly practical, especially in the midst of a cross- 8 I Vintage border M&A boom.

“One big shift has been having buyers who are increasingly comfortable enough with their risk management profile, and aren’t afraid to do business as the locals do – not across the board, but there is a big commercial willingness to do that,” he says. “It is that it’s a very interesting overlay of commercial and strategic practicality.” Diligent value While what consists of due diligence may have changed, what takes precedence in the process hasn’t. “It’s biased to whatever drives value,” says Moriarty.

“It’s also biased towards finding liabilities as well, of course, and both are critical. However, unless you do diligence and understand the former, there’s no need for the latter.” McKissack agrees. “Financial due diligence, accounting due diligence and quality of earnings — these are the basis of the foundation of value.

Legal, risk and contract reviews are also important. But they all drive value at the end of the day, whether it’s in dollars and cents or by protecting yourself from unnecessary risk.” From other perspectives, however, certain issues are more important than others at the moment. “The hottest button in the world right now is compliance,” Gemello says. “Unknowingly buying your way into a compliance problem can destroy the underlying value of the acquisition, putting aside the commercial and reputational impact on a buyer and its own business.

We are spending more time with clients at earlier stages of their deals, as they strive to better understand the local regulatory climate(s) in which their targets are operating. It’s been far and away the primary focus.” For Drazan, focusing on the product and the seller’s customers takes precedent. “Customer references are the single most important component of our diligence,” he says.

“What choices did the customer have before buying, did the product or service live up to the expectation, and how has the company behaved in the aftermath of the sale? Getting the . answers to those questions is crucial. Management references come next after that hurdle.” Motani adds that, as well as ensuring that the lawful side of things are taken care of, due diligence is also vital to understanding the competitive landscape. “The legal and contract side takes precedent. We don’t want to have any legal liabilities postpurchase,” he says. “We also want to adjust our competitive positioning. This means looking at the competitive nature of the market, as well as other macro-level issues we’re up against.” Lessons learned Our experts identified five key lessons that acquirers should bear in mind in order to make the most of their negotiations. Be prepared.

“I’m always surprised that people don’t do much real preparation work for negotiations as they should,” says Moriarty. “They do the valuation work and things around financial projections — but they rarely consider what is actually in their counterpart’s head.” 1. Gemello agrees, particularly when it comes to cross-border dealmaking. “Gone are the days of the imperialistic buyer that just jams something down the throat of the seller,” he says. “I spend a lot more time with my clients getting smart about the target, about how they do business, about how they will operate and behave in the negotiation, just so we can clear out as much unnecessary noise as possible.” Anchor away.

Moriarty believes that putting the question to the other side first can give a psychological advantage when discussing terms around the table. “It’s important to make the first offer,” he says. “This is a concept called anchoring.

If you make the first offer, the other side will often gravitate towards it. I’ve used it myself, and seen it used against us in negotiations. I’m surprised at how it effects people and it’s a very powerful tool.” 2. 3. Friend, not foe.

“M&A is inherently a social interaction,” says Gemello. “You’ve got to effectively build a bridge. As the world gets smaller, successful dealmakers have to bridge the social and cultural differences between parties, and take them into account when doing a deal.” This necessity means that meeting your counterparts in person takes on paramount importance.

“The heightened era of electronic connectivity puts a premium on face-to-face meetings. You can’t substitute for time together between principals to build relationships,” he says. “It’s the principalto-principal relationship that will carry the deal to success if it’s going to happen, and the business leaders negotiating the transaction at the highest level need to have trust between them so they can efficiently work through the deal.” Be upfront and honest.

Facing the big tasks head on first can save you time down the line. “The biggest thing for me is pinpointing where the issues are, to the extent you can sooner rather than later, and getting those items out on the table for conversation.” If you have an opportunity to do that, you can get over the big hurdles early.” 4. When doing this, however, it is vital that dealmakers are honest and open to compromise. “Integrity is everything,” says Drazan.

“Never say never unless you mean it.” Time is money. If you’re able to take your time through these processes, this can help valuegeneration greatly. “If you have time on your side, you will benefit greatly from a valuation perspective,” says Motani.

“I’ve been involved in auctions and direct sales, and while auctions can accelerate the time to closing, a direct deal usually results in a more buyer friendly purchase price.” 5. M&A: Good practices & bad pitfalls I 9 M&A: Good practices & bad pitfalls . Putting it all together After finding the perfect target and getting the deal over the line, companies can sometimes forget that fitting them togetheris crucial to a successful transaction. What are the key factors that make up a successful integration? MM (Mergermarket) BMM KM 10 I Vintage What are the key priorities in your integrations? There are several schools of thought on this and all have rationales. For me it’s key to integrate quickly because when you close, that is when a target will be at its most receptive to change. Missing this can be costly and destroy deal value. Achieving the financial targets is almost always the biggest priority. On top of this, it’s important to retain needed staff in such a turbulent time. We are a very seasonal business, and we tend to acquire other seasonal businesses.

When integrating, our key priority is to ensure minimal disruption around our major seasons — Christmas, Valentine’s Day, Mother’s Day and so on. “Our key priority when integrating is to ensure minimal disruption around our key seasons. When we acquired our most recent business, the integration stopped when we hit peak season, and picked up again afterwards.” Karim Motani, Corporate Development and Strategy Director, 1800flowers.com . The experts Brian Moriarty (BMM) former Vice President, Hewlett-Packard Karim Motani (KM) Corporate Development and Strategy Director, 1800flowers.com Jeff Drazan (JD) Managing Partner, Bertram Capital For instance, when we acquired our most recent business, the integration work slowed during our peak season, and it picked up again immediately afterwards. MG Speed and efficiency. We’ve got to go to market with the asset we just spent the money on, and whatever integration steps need to happen to allow us to do that efficiently and effectively, we have to do it. That recognition by clients is the single biggest change over the last 10 to 15 years. The integration is increasingly viewed as important as the acquisition itself. The value from the acquisition can erode quickly if the acquired business is not properly intergrated into the larger group.

Yet, speed and efficiency have always been the priorities when it comes to integration; what’s changed is the amount of attention and focus our clients are giving it. Matthew Gemello (MG) Partner, Baker & McKenzie MM BMM Marshall McKissack (MM) Managing Director, Head of M&A, Stephens Inc. What are the main obstacles you face when integrating, and how have you learned to overcome them? Before doing serious integration planning, a buyer must consider three fundamental questions: are you going to integrate?; if so, when?; and how long should integration take (i.e., are you willing to potentially adopt policies and procedures of the target in the merged company or do you want to align the target to the acquirer’s practices). Many buyers close deals without a fundamental view on these questions; this ultimately impacts the business plan. The biggest hurdle that we frequently see is internal resistance from the C-suite that manifests itself in two areas. The first is a more philosophical perspective as to the need to integrate and how critical integration is to acheiving longer-term objectives. Buyers simply have to get over that hump.

The second area is resource allocation and the internal importance placed by senior management on the integration effort itself. In more cases than not, companies have a dedicated M&A team that’s doing the buy-side of the transaction, and those folks disappear after the closing party and don’t have to deal with what’s afterwards. There are a host of employees who play a greater role on the operational side, who have to undertake these integration activities alongside their day to day activities. The priorities can vary. Some buyers need access to synergies as soon as possible, some buyers want to make sure when the deal closes that the business runs as smoothly and efficiently as possible, with no interruptions for employees and customers and the organization functions as smoothly as it did the day before you close.

It’s really about making sure those customers and employees are onboarded to your plan. From what I’ve seen, the companies that have a plan for integration that is well documented, well supervised, well thought out and benchmarked — those are the ones that are doing the best. It’s about recognizing the synergies you’ve identified and valued before buying, and making sure it comes to fruition. Buyers who have planned and prepared for those things and do it out of the gate are the most successful. JD Cultural aspects are also a challenge, and it is something you should expect to face when combining two different companies and company cultures. Motivating parties on both sides to help out with the integration can also be hard, especially as those people will still be doing their day-to-day jobs and have full calendars. It’s important to clearly communicate the value that the deal will generate, and that integrating properly is a key driver of that value.

Finally, you have to manage employee concerns. In the immediate aftermath of a deal there will be lots of questions and concerns from your employees, and addressing these questions and concerns early is very important. MG MM KM For us it’s all about the people. You can’t run a business without good people.

Then, we focus on IT, which is our value driver. M&A: Good practices & bad pitfalls I 11 . The companies that do it well are the ones that have dedicated integration teams, with a senior integration leader who has some gravitas within the company, who can really drive home the importance of the post-acquisition steps within the larger organization. Success here is dependent about driving full engagement and commitment. To overcome these challenges, we spend a lot of time talking about the integration up front including at the targeting stage. We really try to help clients think about synergies that can reduce the overall cost of the transaction, so we’re doing a lot of dualtrack due diligence for both the deal as well as the downstream integration, and thinking potentially where contracts or people might be moved or assets might be relocated. Getting the synergistic potential on the table early is often a critical step to buy-in from the C-suite. Interestingly, it takes one successful integration for clients to see the value.

We have found that this is not a continual fight, it’s more of an episodic battle and trying to help clients get over that hump. When they do, they’re cruising from there because the potential to save costs and accelerate “How you organize a project dictates its success. You can make a lot of smart decisions about what you’re going to do, but if you have a key function missing, you’re really in trouble.” Matthew Gemello, Partner, Baker & McKenzie 12 I Vintage the larger strategic goals are obvious.

We have three clients that have a VP to EVP level head of integration, and I can’t say that I knew those positions existed five to ten years ago. MM JD MM BMM Some problems are a result of those cultural differences, and not identifying those fairly with a corresponding plan to manage. A lot of organizations have fundamentally different cultures, that sometimes is difficult to understand and plan for. Understanding culture is a great perspective to have to properly assimilate organizations. As Marshall said, culture is everything.

You have to make sure you assimilate correctly, do so with integrity and communicate the changes effectively. What would you say are three key lessons of successful post-merger integration? Decision making must be quick. You need the firm to make decisions quickly as stalling can sometimes kill deals. It is often better to be quick — and sometimes, wrong — than to wait for incremental information. Secondly, as I mentioned, it is key to integrate quickly.

People are ready for a change right at closing, and it is hard to get that mindset again if you only start to integrate six to nine months later. Capitalize on the energy. Finally, it is key to consider cultural differences — something buyers sometimes overlook. You must assess the target’s culture and how it relates to your company and how it will affect it. Helping people to identify the differences and change them is essential, and often overlooked. KM As Brian hinted at, a lot of it centers on speed. For one, you should start integration planning before closing the deal.

This will help you get a clearer picture of what the integration will look like, and prepare people in advance. Secondly, the process should start on day one. And finally, ensure any personnel changes are done as soon as possible. .

Gaining pace: companies are still in the process of perfecting integrations, and are keenly aware doing it quicker is part of that. This helps to minimize disruption, and ensures that you can focus on delivering what was promised with the deal. MG 68% of highestperforming deals achieved stakeholder communication objectives within three months.1 The institutional buy-in point is key, and the single greatest thing that we can do to help our clients position a post-acquisition integration for success is to build the right core team. An optimized integration team will include representatives from the core functions: legal, tax, HR, IT, treasury and commercial. If that control group has enough gravitas to move the needle within the organization, clients can get through everything they will need to get through efficiently. By building a good project management office, companies have positioned themselves to navigate their way through roadblocks. For me personally, the ultimate success rests with its organization and approach to the project. Companies can make a lot of smart decisions about what they are going to do from that perspective or the group’s perspective, but the omission of a key function missing can significant delay, if not derail, achievement of the integration goals. 80% Integrations are massively cross-functional exercises; it’s almost the epitome of one. What you can’t do is get into a turf war where you have silos that aren’t communicating to each other and people are dug in — “that’s mine and not yours, I’m supposed to do that not you, for instance” — it has to be collaborative and there has to be buy in from the top. respondents who said that, in retrospect, they would have quickened the pace of their last integration.2 JD Communicate broadly, frequently and honestly. Make sure that you have a plan, and on top of this, you have to identify and empower leaders from both groups. 28% executives at US companies who felt that their last integration was not a success.3 Sources: 1.

PwC. M&A Integration: Looking beyond the here and now. 2014 2.

EY. The right combination: Managing integration for deal success. 2014 3.

Deloitte. Integration Report 2015: Putting the pieces together. M&A: Good practices & bad pitfalls I 13 . 14 I Vintage . About Vintage Vintage, a PR Newswire division, is a top-three provider of full-service regulatory compliance and shareholder communications services, delivered across our three practice areas: Capital Markets, Corporate Services and Institutional & Fund Services. Founded in 2002 and acquired by PR Newswire in 2007, Vintage has evolved to become the industry’s intelligent value choice. We deliver a flexible balance of people, facilities and technology to ensure that regulatory compliance and shareholder communications processes are efficient, transparent and painless. Services include IPO registrations, transactions, virtual data rooms, EDGAR & XBRL filing, typesetting, financial printing and investor relations websites. theVintageGroup.com Trevor Loe Vice President Vintage, a Division of PR Newswire Direct: 201.360.6425 | Mobile: 440.787.9960 trevor.loe@thevintagegroup.com www.TheVintageGroup.com M&A: Good practices & bad pitfalls About Vintage I 15 . 16 I Vintage .