Description

RISK MANAGEMENT

ISE Risk Management

ISE Holdings leads the industry in offering a comprehensive portfolio of risk

management capabilities for orders that are routed to ISE and ISE GeminiTM.

In addition to our extensive elective risk management features, which enable firms to

customize their risk protections, ISE and ISE Gemini also offer “built-in” protections

that are automatically deployed for every order that is routed to our exchanges.

For more information on any of

these features or for assistance

in establishing or adjusting your

risk settings, please contact the

Business Development Team

at bizdev@ise.com.

ISE’s innovative trading architecture T7™ automatically provides additional risk management features specific to ISE and ISE Gemini.

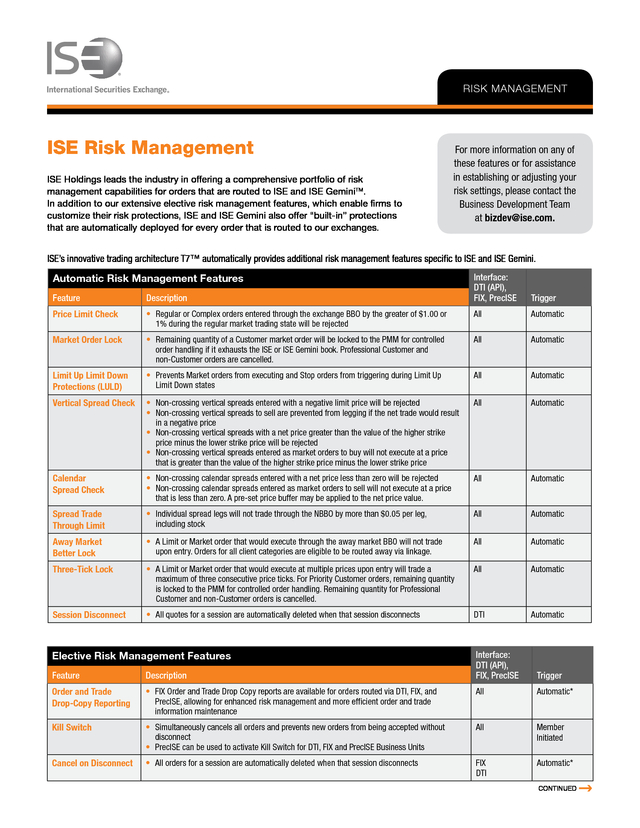

Automatic Risk Management Features

Interface:

DTI (API),

FIX, PrecISE

Trigger

Feature

Description

Price Limit Check

• Regular or Complex orders entered through the exchange BBO by the greater of $1.00 or

1% during the regular market trading state will be rejected

All

Automatic

Market Order Lock

• Remaining quantity of a Customer market order will be locked to the PMM for controlled

order handling if it exhausts the ISE or ISE Gemini book. Professional Customer and

non-Customer orders are cancelled.

All

Automatic

Limit Up Limit Down

Protections (LULD)

• Prevents Market orders from executing and Stop orders from triggering during Limit Up

Limit Down states

All

Automatic

Vertical Spread Check

• Non-crossing vertical spreads entered with a negative limit price will be rejected

• Non-crossing vertical spreads to sell are prevented from legging if the net trade would result

in a negative price

• Non-crossing vertical spreads with a net price greater than the value of the higher strike

price minus the lower strike price will be rejected

• Non-crossing vertical spreads entered as market orders to buy will not execute at a price

that is greater than the value of the higher strike price minus the lower strike price

All

Automatic

Calendar

Spread Check

• Non-crossing calendar spreads entered with a net price less than zero will be rejected

• Non-crossing calendar spreads entered as market orders to sell will not execute at a price

that is less than zero. A pre-set price buffer may be applied to the net price value.

All

Automatic

Spread Trade

Through Limit

• Individual spread legs will not trade through the NBBO by more than $0.05 per leg,

including stock

All

Automatic

Away Market

Better Lock

• A Limit or Market order that would execute through the away market BBO will not trade

upon entry. Orders for all client categories are eligible to be routed away via linkage.

All

Automatic

Three-Tick Lock

• A Limit or Market order that would execute at multiple prices upon entry will trade a

maximum of three consecutive price ticks.

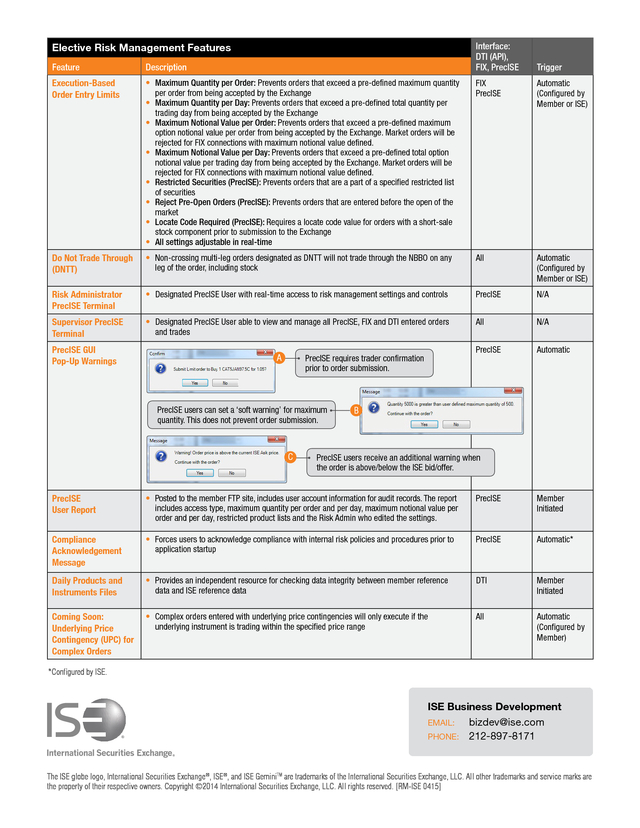

For Priority Customer orders, remaining quantity is locked to the PMM for controlled order handling. Remaining quantity for Professional Customer and non-Customer orders is cancelled. All Automatic Session Disconnect • All quotes for a session are automatically deleted when that session disconnects DTI Automatic Elective Risk Management Features Interface: DTI (API), FIX, PrecISE Trigger Feature Description Order and Trade Drop-Copy Reporting • FIX Order and Trade Drop Copy reports are available for orders routed via DTI, FIX, and PrecISE, allowing for enhanced risk management and more efficient order and trade information maintenance All Automatic* Kill Switch • Simultaneously cancels all orders and prevents new orders from being accepted without disconnect • PrecISE can be used to activate Kill Switch for DTI, FIX and PrecISE Business Units All Member Initiated Cancel on Disconnect • All orders for a session are automatically deleted when that session disconnects FIX DTI Automatic* CONTINUED . Interface: DTI (API), FIX, PrecISE Elective Risk Management Features Feature Description Execution-Based Order Entry Limits • Maximum Quantity per Order: Prevents orders that exceed a pre-defined maximum quantity per order from being accepted by the Exchange • Maximum Quantity per Day: Prevents orders that exceed a pre-defined total quantity per trading day from being accepted by the Exchange • Maximum Notional Value per Order: Prevents orders that exceed a pre-defined maximum option notional value per order from being accepted by the Exchange. Market orders will be rejected for FIX connections with maximum notional value defined. • Maximum Notional Value per Day: Prevents orders that exceed a pre-defined total option notional value per trading day from being accepted by the Exchange. Market orders will be rejected for FIX connections with maximum notional value defined. • Restricted Securities (PrecISE): Prevents orders that are a part of a specified restricted list of securities • Reject Pre-Open Orders (PrecISE): Prevents orders that are entered before the open of the market • Locate Code Required (PrecISE): Requires a locate code value for orders with a short-sale stock component prior to submission to the Exchange • All settings adjustable in real-time FIX PrecISE Automatic (Configured by Member or ISE) Do Not Trade Through (DNTT) • Non-crossing multi-leg orders designated as DNTT will not trade through the NBBO on any leg of the order, including stock All Automatic (Configured by Member or ISE) Risk Administrator PrecISE Terminal • Designated PrecISE User with real-time access to risk management settings and controls PrecISE N/A Supervisor PrecISE Terminal • Designated PrecISE User able to view and manage all PrecISE, FIX and DTI entered orders and trades All N/A PrecISE Automatic PrecISE GUI Pop-Up Warnings A PrecISE requires trader confirmation prior to order submission. PrecISE users can set a ‘soft warning’ for maximum quantity. This does not prevent order submission. C Trigger B PrecISE users receive an additional warning when the order is above/below the ISE bid/offer. PrecISE User Report • Posted to the member FTP site, includes user account information for audit records.

The report includes access type, maximum quantity per order and per day, maximum notional value per order and per day, restricted product lists and the Risk Admin who edited the settings. PrecISE Member Initiated Compliance Acknowledgement Message • Forces users to acknowledge compliance with internal risk policies and procedures prior to application startup PrecISE Automatic* Daily Products and Instruments Files • Provides an independent resource for checking data integrity between member reference data and ISE reference data DTI Member Initiated Coming Soon: Underlying Price Contingency (UPC) for Complex Orders • Complex orders entered with underlying price contingencies will only execute if the underlying instrument is trading within the specified price range All Automatic (Configured by Member) *Configured by ISE. ISE Business Development EMAIL: bizdev@ise.com PHONE: 212-897-8171 The ISE globe logo, International Securities Exchange®, ISE®, and ISE GeminiTM are trademarks of the International Securities Exchange, LLC. All other trademarks and service marks are the property of their respective owners. Copyright ©2014 International Securities Exchange, LLC.

All rights reserved. [RM-ISE 0415] .

For Priority Customer orders, remaining quantity is locked to the PMM for controlled order handling. Remaining quantity for Professional Customer and non-Customer orders is cancelled. All Automatic Session Disconnect • All quotes for a session are automatically deleted when that session disconnects DTI Automatic Elective Risk Management Features Interface: DTI (API), FIX, PrecISE Trigger Feature Description Order and Trade Drop-Copy Reporting • FIX Order and Trade Drop Copy reports are available for orders routed via DTI, FIX, and PrecISE, allowing for enhanced risk management and more efficient order and trade information maintenance All Automatic* Kill Switch • Simultaneously cancels all orders and prevents new orders from being accepted without disconnect • PrecISE can be used to activate Kill Switch for DTI, FIX and PrecISE Business Units All Member Initiated Cancel on Disconnect • All orders for a session are automatically deleted when that session disconnects FIX DTI Automatic* CONTINUED . Interface: DTI (API), FIX, PrecISE Elective Risk Management Features Feature Description Execution-Based Order Entry Limits • Maximum Quantity per Order: Prevents orders that exceed a pre-defined maximum quantity per order from being accepted by the Exchange • Maximum Quantity per Day: Prevents orders that exceed a pre-defined total quantity per trading day from being accepted by the Exchange • Maximum Notional Value per Order: Prevents orders that exceed a pre-defined maximum option notional value per order from being accepted by the Exchange. Market orders will be rejected for FIX connections with maximum notional value defined. • Maximum Notional Value per Day: Prevents orders that exceed a pre-defined total option notional value per trading day from being accepted by the Exchange. Market orders will be rejected for FIX connections with maximum notional value defined. • Restricted Securities (PrecISE): Prevents orders that are a part of a specified restricted list of securities • Reject Pre-Open Orders (PrecISE): Prevents orders that are entered before the open of the market • Locate Code Required (PrecISE): Requires a locate code value for orders with a short-sale stock component prior to submission to the Exchange • All settings adjustable in real-time FIX PrecISE Automatic (Configured by Member or ISE) Do Not Trade Through (DNTT) • Non-crossing multi-leg orders designated as DNTT will not trade through the NBBO on any leg of the order, including stock All Automatic (Configured by Member or ISE) Risk Administrator PrecISE Terminal • Designated PrecISE User with real-time access to risk management settings and controls PrecISE N/A Supervisor PrecISE Terminal • Designated PrecISE User able to view and manage all PrecISE, FIX and DTI entered orders and trades All N/A PrecISE Automatic PrecISE GUI Pop-Up Warnings A PrecISE requires trader confirmation prior to order submission. PrecISE users can set a ‘soft warning’ for maximum quantity. This does not prevent order submission. C Trigger B PrecISE users receive an additional warning when the order is above/below the ISE bid/offer. PrecISE User Report • Posted to the member FTP site, includes user account information for audit records.

The report includes access type, maximum quantity per order and per day, maximum notional value per order and per day, restricted product lists and the Risk Admin who edited the settings. PrecISE Member Initiated Compliance Acknowledgement Message • Forces users to acknowledge compliance with internal risk policies and procedures prior to application startup PrecISE Automatic* Daily Products and Instruments Files • Provides an independent resource for checking data integrity between member reference data and ISE reference data DTI Member Initiated Coming Soon: Underlying Price Contingency (UPC) for Complex Orders • Complex orders entered with underlying price contingencies will only execute if the underlying instrument is trading within the specified price range All Automatic (Configured by Member) *Configured by ISE. ISE Business Development EMAIL: bizdev@ise.com PHONE: 212-897-8171 The ISE globe logo, International Securities Exchange®, ISE®, and ISE GeminiTM are trademarks of the International Securities Exchange, LLC. All other trademarks and service marks are the property of their respective owners. Copyright ©2014 International Securities Exchange, LLC.

All rights reserved. [RM-ISE 0415] .