Clear Path Analysis Report: Collateral Management & Securities Lending, APAC - May 2015

Interactive Data

Description

COLLATERAL MANAGEMENT

& SECURITIES LENDING,

APAC

Published by

MAY 2015

Examining the meeting of regulatory requirements, generating returns on asset holdings and creating an optimal

collateral management programme.

Report Sponsor

To read the full version of this report and other informative, financial market reports please visit: www.clearpathanalysis.com

. WHITE PAPER

Assessing the true costs and benefits of OTC derivative market reform – a global

assessment and it’s impact on Asia-Pacific

Laura Kodres

Division Chief for

the Global Financial

Stability Division,

International Monetary

Fund

John Kiff

Senior Financial Sector

Expert, Global Financial

Stability Division,

International Monetary

Fund

At their 2009 Pittsburgh Summit, leaders of the Group of 20

advanced and emerging market economies (G-20) called for a

major overhaul of over-the-counter (OTC) derivatives markets

to be completed by end-2012. The reforms are supposed

to make derivatives markets safer and more transparent;

although concerns are being raised that some unintended

consequences may undermine these goals. This paper will

review some of these costs and benefits, and the impact on

Asian markets.

The reforms aim to clear all standardized OTC derivatives on

central counterparties (CCPs) and trade them on exchanges

or electronic trading platforms, where appropriate. For noncentrally cleared contracts, higher bank capital requirements

are to be imposed.

Also, all OTC derivative trades are to be reported to trade repositories. The Financial Stability Board (FSB), which G-20 leaders tasked with monitoring reform implementation, also called for improved risk management of non-centrally cleared derivatives, including consistent margin posting. of pre- and post-trade transparency than exchanges and electronic platform trading. Also, because OTC trading often was not subject to the same level of market surveillance as exchange or electronic platform trading, market abuse was less likely to be detected. Hence the G-20 reform package which, at their 2010 Toronto Summit, G-20 leaders committed to implement in an internationally consistent and non-discriminatory way attempted to address these problems. Reforms Implementation But more than two years after the end-2012 deadline, no jurisdiction has fully implemented all of the reforms and some countries have not started.

The reforms have been delayed in many cases because the legislative and regulatory reform processes –including cross-border coordination – have turned out to be more complex than anticipated. Some countries are hanging back until Europe and the United States make and mesh their reforms. Reforms Motivation Derivatives play a useful economic role. They are used by firms and governments to expand investment and borrowing opportunities, and make revenues and expenditures more predictable.

Derivatives sharpen the pricing of risk, and provide a useful window on market expectations of key economic variables. Credit derivatives can be used to disperse credit risks to a broader and more diverse group of investors than those originating credit instruments, which may mitigate and help absorb financial system shocks. Moreover, even where individual jurisdictions have made progress, regulatory inconsistencies and frictions between countries have created a rockier road than expected. G-20 leaders called for country authorities to find ways to defer to each other’s regulations, but, for example, EU regulators resisted the authorization of U.S.-based CCP use by EU counterparties and U.S.

regulators favor requiring transactions involving U.S. counterparties to be traded on U.S.-authorized trading platforms. Unintended Consequences But the crisis exposed weaknesses in OTC markets. There were large and opaque counterparty risks, some of which were not appropriately risk-managed, that created unseen interconnections and potential contagion.

The opacity of counterparty credit risk exposures also precipitated a loss of confidence and market liquidity in already stressed markets. Furthermore, there was a paucity of data available to authorities to monitor where risk was held and the nature of the interconnections. Opacity extended to the availability of transaction data such as prices and volumes, which made transactions valuation more difficult. OTC derivative trading provides lower levels Furthermore, concerns have been raised regarding some possibly unintended consequences of the reform process. For example, the central clearing mandate may create new concentrations of risks at too-big-to-fail CCPs.

The failure of a large CCP could result in liquidity dislocations and credit losses to its clearing members. More effort is underway to discern good resolution practices for CCP to avert such a situation. Also, the adoption of margin best practice outside a CCP can create tight couplings so that large missed margin payments can propagate unpredictably. 2 There is also an inherent procyclicality to initial margin (and 2 .

Assessing the true costs and benefits of OTC derivative market reform – a global assessment and it’s impact on Asia-Pacific default fund) requirements and collateral haircuts that could exacerbate cycles. These are usually based on value-at-risk methodologies fed by historical price data. Hence, collateral requirements and haircuts can increase dramatically when markets are under stress, thus increasing price volatility and/ or illiquidity of the contracts and underlying assets. The impact of procyclicality on centrally cleared trades may be muted (versus bilaterally cleared trades) by the netting efficiencies associated with CCPs. The mitigation may only be theoretical, however, due to jurisdictional and product line central clearing fragmentation.

Several national authorities have invoked a location requirement that derivatives in the local currency or derivatives traded by local banks be only cleared through a local CCP. Central clearing will also put further strains on already tight collateral markets, because CCPs generally do not allow assets posted as initial margin to be rehypothecated3. Not only is the stock of the “safe” assets typically posted against secured borrowings shrinking, but so has its “velocity”.4 On the other hand, central securities depositories and collateral transformation agents are offering creative solutions to manage collateral more efficiently. However, such schemes could cause new channels of interconnectedness and contagion. Central Clearing Cost-Benefit Analysis In order to address some of these concerns, global regulatory standard setters created the Macroeconomic Assessment Group on Derivatives (MAGD) in 2013.

The group was comprised of representatives from 18 FSB member countries, the International Monetary Fund, European Commission, and International Organization of Securities Commissions, working with the Bank of International Settlements. Also, the unintended consequences discussed above were not part of the analysis. Small Market Perspectives Small market jurisdictions face some special challenges. If they are too small to support domestic CCPs, their banks and dealers have to clear with a non-local CCPs that only accept major currencies as margin, so locals face currency risks. On the other hand, countries that can support domestic CCPs have to have equivalence status from other country supervisors to facilitate cross border transaction clearing in the domestic CCP. Compliance with other jurisdictions’ regulatory requirements is burdensome, but perhaps worth it for most CCPs. Equivalence status is important because, for example, if a European bank were to centrally clear a transaction with a CCP that was not “qualified” it could face punitively high capital charges on its margin and default fund contributions to the foreign CCP.

And so far, European regulators have issued equivalence designations to four OTC derivative CCPs, all of them Asian (Australia’s ASX Clear, Hong Kong’s HKFE Clearing and OTC Clearing, and the Japan Securities Clearing Corporation (JSCC)). The U.S. Commodity Futures Trading Commission (CFTC) has approved comparability determinations that would permit substituted compliance with U.S. regulations for CCPs in Australia, Canada, European Union, Japan, Hong Kong, and Switzerland.

Non-U.S. CCPs (CME Clearing Europe, Eurex Clearing, and JSCC) have applied to the CFTC to become “derivative clearing organizations” (DCOs) but none have yet been approved. However, the CFTC has exempted four nonU.S.

CCPs from DCO registration until end-2015, also all of them Asian (ASX Clear, Clearing Corporation of India, Korea Exchange and Hong Kong’s OTC Clearing). The MAGD focused on the economic effects of mandatory central clearing, margin requirements for non-centrally cleared transactions; and new bank capital requirements. It concluded that the benefits out-weighed the costs, where the main benefit is the reduced likelihood of financial crises and hence higher trend economic growth. The costs stem from the requirement to hold more high-quality, low-yielding assets as collateral, and the switch from lower-cost debt to higher-cost equity financing associated with the higher capital requirements. The global reform agenda also aims to all have all OTC derivative trades reported to trade repositories.

The availability of these stored records can help regulators detect the buildup of risk exposures and interconnections among financial entities. This requirement is proving to be burdensome for smaller operators that trade across borders, since they have to report to both their domestic trade repositories and those of their counterparties. The MAGD analysis did not consider other potential postreform market configurations, for example, without mandatory central clearing but with bank capital requirements on bilateral contracts that incentivizes multilateral compression. The MAGD analysis could have usefully compared marginal benefit of mandatory central clearing to such other configurations. The reforms also aim to push standardized OTC derivatives trading on to exchanges or electronic trading platforms, where appropriate (such as when there is sufficient trading volume). This requirement was driven by a view that when transactions are opaque, as they can be when trades are bilateral, markets Trading Platform Mandate 1. Notes 1. The views expressed herein are those of the authors and should not be attributed to the International Monetary Fund, its Executive Board, or its management. 2. Notes 3. Notes 3 . Assessing the true costs and benefits of OTC derivative market reform – a global assessment and it’s impact on Asia-Pacific are less reliable and prone to increased risks, particularly under stress. Only the United States currently has mandatory trading requirements in place, Japan will in September 2015, and perhaps India and Singapore in 2016. The EU will not even have the legislative authority to do so in place until 2016. According to the International Swaps and Derivatives Association (ISDA) the U.S. trading mandate is fragmenting some swap markets.

5 CFTC regulations require that all trades with U.S. entities involving swaps that fall under its trading mandate be traded on U.S.-designated trading platforms. Non-U.S. entities involved in such transactions would have to set up access to the trading platform, and be subject to all of its rules and regulations, and those of the CFTC, including what some view as onerous inspection and record keeping requirements.

Hence, many non-U.S. entities are said to be shying away from trading such swaps with U.S. counterparties. However, this is likely a transitional problem that will sort itself out when trading mandates have been fully implemented everywhere. The Road Ahead Completion of the OTC derivative market reform process is still a few years away, and the process has not been without a few bumps, many of which are part of the transition process. Also, a number of unintended consequences have arisen, but authorities are well aware and working to mitigate them. Asian OTC Derivative Central Counterparties (as of April 30, 2015) CCP Name Jurisdiction Products Cross-Border Equivalence ASX Clear Australia EQ, IR EU CCIL India FX, IR US HKFE Clearing Hong Kong IR EU OTC Clearing Hong Kong FX, IR EU, US JSCC Japan CR, EQ, FX, IR EU, US Korea Exchange Korea IR JP, US SGX Derivatives Clearing Singapore CO, FX, IR US Shanghai Clearing House China CO, FX, IR Key CO = Commodity, EQ = Equity, IR = Interest Rate, JP = Japan, CR = Credit, FX = Foreign Exchange, EU = European Union, US = United States 3. In a secured lending transaction, the borrower hypothecates collateral to the lender, so that the borrower retains ownership, but in the event of a default or missed margin call the lender can take immediate possession.

Reypothecation means the repledging of the collateral by the lender for its own borrowing transactions. 4. See Singh, Manmohan, 2011, “Velocity of Pledged Collateral: Analysis and Implications,” IMF Working Paper No. WP/11/256, November. 5. ISDA, 2014, “Cross-Border Fragmentation of Global Derivatives: End-Year 2014 Update,” April. 4 . WHITE PAPER Assessing the operational implications of generating intra-day collateral valuations Magnus Cattan Business Development Director (Asia), Interactive Data As a result of regulatory changes and clearing fragmentation, the demand for collateral has, and will continue to, increase. Finding collateral to meet regulatory requirements such as Dodd-Frank, EMIR and Basel III will also drive the need for greater transparency and greater risk controls around valuation of collateral and measuring liquidity. A recent DTCC paper estimates the future additional collateral requirements at anywhere between $800 billion and $10 trillion, and the paper also indicates that margin call activity may increase by 500-1000%. Margin call activity will be driven for example by the reduction or removal of thresholds for variation margin and Centralised Clearing Platforms (CCPs) potentially making intraday margin calls. Collateral Management is and always has been crucial for the financial services industry. In the broadest definition, Collateral Management is the process of analyzing, validating, granting and providing advice for collateral transactions in various markets.

Its usefulness spans risk management, capital adequacy, regulatory compliance and operational risk areas. Interactive Data’s end of day pricing, fixed income evaluations and reference data are used in traditional Collateral Management applications among lending institutions across the public and private sectors. For example, in the Asia Pacific region, Interactive Data recently announced that it is providing valuations of Austraclear securities to Clearstream in support of the recently launched ASX Collateral Service. Traditionally collateral management applications have relied upon end of day pricing data. For the reasons mentioned above, demand is shifting to a need for intra-day pricing data.

For asset classes like fixed income, the operational implications of generating intraday prices or evaluations can be very challenging indeed. Broadly speaking there are three operational hurdles that need to be overcome: (1) an experienced staff to value a broad range of asset types, (2) access to a significant amount of market data, and (3) technology that can process, organize and utilize vast amounts of unstructured data. All of this needs to be done on a global and resilient network. Interactive Data’s continuous evaluated pricing offering is one result of a multi-year effort and multi-million dollar investment in our infrastructure. Interactive Data’s continuous evaluations are updated as market information, including dealer runs and quotes and trades including information from ECNs and transaction reporting services, are received and processed.

Interactive Data receives on average over 5 million observations from the marketplace for the corporate bonds that we evaluate each day. Our continuous evaluation workflow is designed to rapidly process and apply incoming data while leveraging close evaluator oversight of market conditions. Unstructured data, such as emails from market participants, are parsed electronically and automatically linked to evaluated securities.

Incoming market data are enriched to derive spread, yield and/or price data as appropriate, enabling known data points to be extrapolated for application across a range of related securities. Enriched data is tested against the current evaluation and internal tolerances and parameters. From an application perspective, Interactive Data needed to build sophisticated valuation tools that are capable of linking disparate inputs to benchmarks and to specific securities. These applications have automation rules that drive the generation of evaluated prices as market data is received and processed. When exceptions are identified, based on an evaluator’s present tolerances, the system generates notifications for review by evaluators.

Evaluators review exceptions against additional data sources, comparable securities and input from market contacts. System parameters are not static and are adjusted based on lessons learned from the exception review process. "... demand is shifting to a need for intra-day pricing data" 1. Trends, Risks and Opportunities in Collateral Management.

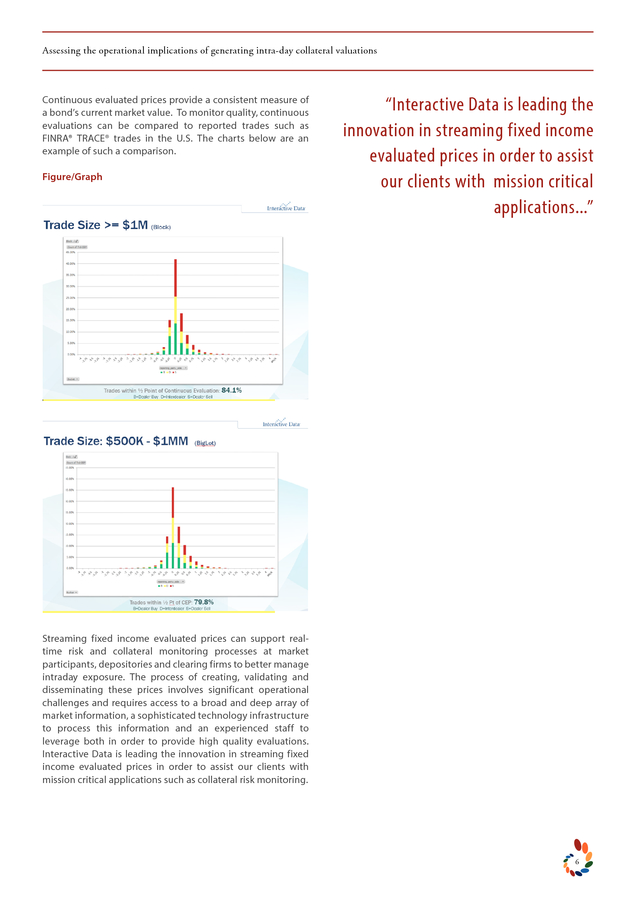

A Collateral Management White Paper, DTCC, January 2014 2. http://www.interactivedata.com/Assets/DevIDSite/PR-2014/Interactive-Data-Selected-as-Primary-Evaluations-Source-for-Australian-Security-Exchange-Collateral.pdf 5 . Assessing the operational implications of generating intra-day collateral valuations Continuous evaluated prices provide a consistent measure of a bond’s current market value. To monitor quality, continuous evaluations can be compared to reported trades such as FINRA® TRACE® trades in the U.S. The charts below are an example of such a comparison. Figure/Graph “Interactive Data is leading the innovation in streaming fixed income evaluated prices in order to assist our clients with mission critical applications...” Streaming fixed income evaluated prices can support realtime risk and collateral monitoring processes at market participants, depositories and clearing firms to better manage intraday exposure. The process of creating, validating and disseminating these prices involves significant operational challenges and requires access to a broad and deep array of market information, a sophisticated technology infrastructure to process this information and an experienced staff to leverage both in order to provide high quality evaluations. Interactive Data is leading the innovation in streaming fixed income evaluated prices in order to assist our clients with mission critical applications such as collateral risk monitoring. 6 .

ROUNDTABLE Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements Moderator Panellists Noel Hillmann Managing Director, Clear Path Analysis Noel Hillmann: Firstly, thank-you for joining me for this debate. I’ll begin by asking, as international fund managers, and in light of changes in European and US market collateral management rules, how have your investment operations changed and what has this meant for your APAC based securities lending activities? Adrian Song: For us in APAC, we do not have a securities lending programme currently. However changes in collateral requirements do affect us nonetheless. The introduction of margin requirements on non-centrally cleared derivatives will add costs to operationally support trading OTC derivatives. The activities of managing collateral increases as additional instruments are progressively inscope.

Investment management would need to look for more sources of eligible collateral in their portfolios and be more proficient in managing and reinvesting collateral. Without a scalable system, the benefits of mitigating counterparty risks would be eroded by a firm’s inability to cope, giving rise to increased operational risk. Despite regulators pushing back deadlines numerous times, in part to try to harmonise cross-border requirements and partly to allow firms sufficient time to be ready for it, we should not be hopeful that these requirements will go away. Frederic Rebry: To elaborate a bit on how securities lending activity is conducted by BNP Investment Partners, this is rather limited for the APAC region.

We have indeed global managed portfolios, managed out of Frederic Rebry Head of Financial Service Providers Front, Middle & Custody, BNP Paribas Investment Partners Asia, that are on the securities lending program. However, overall we can conclude that the local securities lending activity is limited. The majority of the business is European based at this stage. With regards to the collateral changes resulting from Europe and especially in the U.S., because they are front runners, we can all agree that current regulations are completely overseeing all businesses that do have any links with collateral.

We can list the big regulatory changes such as Dodd Frank, e.g. Over The Counter (OTC) clearing, European Market Infrastructure Regulation (EMIR) / European Securities & Markets Authority (ESMA), risk mitigation and “Efficient Portfolio Management”: everything that is related to concentration and diversification ratios, re-use of cash collateral and so forth. Next to these you have Basel III capital ratios, Liquidity Coverage Ratios (LCR), and ISOCO, mandatory bilateral collateralisation.

You need to look at these as part of the global picture. From a collateral management approach, it’s very important to understand that all of these need to be considered in the investment operations framework, not necessarily only those linked to securities lending. If I look at it from a BNP Investment Partners perspective, we have been closely following up these changes since day one, in close co-operation with our Securities Services team (as part of the group). As mentioned by Adrian, it’s important to indicate that in Adrian Song Head of Portfolio Operations, Schroder Investment Management (Singapore) some cases, we need to cope with an overall pushback of these regulations. The U.S. have been front runners on this subject.

They started in 2013 with the OTC clearing part. If you look at EMIR and OTC clearing, it will only commence mid-2016. It was foreseen at the end of 2012.

I also understand that International Organization of Securities Commissions (IOSCO) has been pushed back for 9 months and it doesn’t make it easy so anticipation is rather difficult, both for the sell and buy side. Over the last few years, a lot of discussions have been held around collateral overall, this from transformation to optimisation needs, so the cheapest to deliver and an eventual collateral squeeze, etc. There is definitely no doubt that indeed investment operations are heavily impacted by these changes, where decisions are to be taken on how to manage your collateral once you have it. I want to stress that the approach of this review cannot necessarily be linked to securities lending only.

There is a need for an overall consideration of all the collateral changes and impacts across assets, being part of one portfolio. Only by doing so, you will be able to adapt the current situation and cope with a most suitable approach. Noel Hillmann: How far along are you in designing a new or adapting an existing securities lending programme? What risk / reward considerations have you found yourselves needing to make as part of this process? 7 . Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements Frederic: As indicated, it is important to really understand all collateral changes and impacts, so within the current evolving collateral framework there is need to look at the global picture. OTC clearing will result in higher collateral requirements, coming with an opportunity cost. If you look at the current level of bilateral trades, we do not have that mandatory initial margin which is called an independent amount in the bilateral space. This is not being implemented on all sides at the moment for the bilateral trades. IOSCO will result in mandatory bilateral collateralisation.

Adding Basel III, you end up in a situation where all market participants are seeking high quality collateral. If I then focus on securities lending I would like at this stage to make a split between two approaches. First of all I would like to look at the lending activity, what is lent out to currently generate revenues for the portfolio, with a focus on portfolios that are active in any kind of assets that result into collateral requirements. The second approach, I would like to elaborate on is what is accepted as collateral in the securities lending framework; knowing that everybody is seeking high quality collateral due or resulting from all of these regulatory changes. If I start with the first point, it will be key to see what is basically lent out against the overall collateral requirements of each portfolio invested in any activity that needs collateralisation. So assets that are currently on loan might tomorrow be needed to cope with these collateral requirements, where basically the revenue of a typical asset that is on loan will need to be mirrored against any cost to obtain that asset in another way. This is in order to meet your collateral obligation resulting from any other trading activity.

If you have a portfolio which is active in, for example, both OTC and securities lending, it will be very important that there is very close monitoring in order to ensure that any collateral obligation will be met within a smooth front to back architecture. For example, if I have a security that is also eligible collateral and I lend it out in the securities lending framework and tomorrow I take a position in OTC clearing and my initial margin is requiring that eligible security that is on loan, what am I going to do? If I look at the cost to obtain the eligible security to cover my OTC deal – alternatively I will take another asset and transform it to meet that initial margin on OTC clearing – it might be higher than the revenue resulting from my securities lending activity. I will then recall that security. Basically there you are going to have to find a balance between your revenue and your cost. My second point leads to the collateral acceptance in the securities lending framework.

We all agree that high quality is of course preferred. However the potential growing lack of high quality assets is, as I explained, resulting from the several regulations. Everybody is seeking high quality collateral. There might be a need to look into other asset classes as being eligible collateral for securities lending. If not, there is a probability that you will need to be willing to cope with a decrease in the securities lending revenues.

We know that in the end, securities lending transactions can be stopped at any time with a 24h notice period. OTC contracts are longer term contracts and it is less common to use equities for OTC collateral. If I look at the securities lending and the collateral used, we do accept in some cases blue chip equities. If you look at OTC, accepting equities will have an impact on your pricing negotiations so everybody for the moment in the OTC space prefers cash. In addition, you will need to keep in mind some collateral principles such as: collateral needs to be liquid enough, it needs to have transparent pricing, it needs to be daily valuated, credit quality of the issuer is important, correlation counterparty/collateral, concentration diversification (sector, country) etc.

So again this is all very important. If you look at collateral you look at it within one portfolio, for example, for all asset classes that do require collateral. Basically we need to find a balance between the risk and rewards considerations. We follow a strict policy on collateral eligibility in the securities lending framework.

Accepting collateral other than high quality, e.g. blue chip equities/corporates, might indeed result in higher revenues. At the end, the risk/reward perspective is not a one off consideration but a continuous process to closely monitor every single day. Noel: What steps have you taken or do you propose to take too minimise operational risk in your securities lending programmes given the need for higher margin requirements? Frederic: If you look at the operational risk aspect, we all agree that’s it not necessarily something that links itself to securities lending only but it’s present in the overall investment activities. You can have, exchange problems, poor communication between stakeholders, failed settlement, settlement cycles overall, etc. If you understand these it might be easier to ensure that the operational risk part stays to a minimum. Keeping aside the upcoming collateral requirements, there is a need to have a robust recall process where for any sell order by the portfolio manager, an immediate trigger is set to recall the securities on loan.

We all know that if you look in Europe, Target 2 Sedcurities (T2S) has spread a lot of “fear” before implementation. However, whether it is purely linked to a sell order or linked to the recall of lent positions that will be requested to be returned to meet any collateral obligation, or linked to the collateral management exchanges overall, the model needs to prove that it is more than secure. 8 . Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements I do believe that it is key that first of all the recall process within the securities lending framework is working without any operational constraints. If you then extend this to the overall picture of meeting any collateral obligation, there will be a need for transparency and a “real time” view on the several activities within one portfolio, such as OTC bilateral, OTC clearing, Exchange Traded Derivatives (ETD), securities lending and repo activity, and the available collateral. By this I mean, it will give you the opportunity to anticipate, link up the overall activity and react in the most appropriate way. All of this is only possible if it is supported by a Front to Back (F2B) process that is robust enough and Straight Through Processing (STP) automated. With F2B, I do mean the complete chain, so if I look at securities lending and the borrowers, it’s also important that you screen your borrowers on a temporary basis and you follow them much closer and ensure that recall fails are an exception only. In addition, only lending out part of the portfolio and working with buffers are also important points to consider. This is where you keep aside part of your eligible collateral that might be used for all other coverage of transactions, so you only lend out X% of your portfolio for example. We ensure a continuous robustness of the F2B process with dedicated procedures, which are audited and controlled on a temporary basis in order to ensure that any lent out position is returned “at any time” and “in time”, for whatever need. As said in the beginning, with a 24 hours’ notice period you could stop your securities lending transaction so it’s very important that you can recall them at any time and that they come back in time.

All of this is only feasible if you have a robust front to back process. Noel: Adrian, in terms of moving forward and looking at introducing a securities lending/collateral management programme into Asia Pacific, you talked a little bit about those OTC derivative reforms that would certainly make the possibility greater. Do you foresee a market environment in the short-term where there is a need for you to initiate a securities lending and a collateral management programme in Asia Pacific or do you think it’s perfectly fine for it to be managed out of head office or elsewhere? Adrian: Currently in APAC, our volume on collaterals is not high and whilst we have a solution to manage our collaterals, we are working with our global counterparts to source a more robust and scalable solution across the group so as to enable our fund managers and back office to better manage the entire end-to-end collateral process in the future. enough to support the needs of all the funds. Noel: On that final note I’d like to finish. Thank-you very much to both of you for sharing your thoughts. “We are at a point where regulators’ timelines are fluid...” The OTC derivatives landscape is changing, where we previously do not need to collateralise certain OTC activities such as FX forwards. Including these activities would mean incremental volumes to collateral operations.

Systems need to be scalable and enhanced with tools to assist in the determination of collateral to deliver, e.g. cheapest to deliver. Collateral management activities would need to complement the core investment management activities. The portfolio would need to set aside a pool of assets as eligible collateral to sustain OTC activities or engage a third-party to facilitate collateral transformation at a fee; or eventually seek exchange-traded substitutes where the margin requirements are less onerous. We are at a point where regulators’ timelines are fluid and thus we need to actively look at the different options available. Repo, securities lending, collateral management through third-party providers, managing collateral inhouse: these are all potential avenues. The choice we make needs to be robust 9 . Powerful Solutions to Today’s Challenges Q Q Q Q A market leader in fixed-income evaluations, pricing and reference data A preeminent provider of fixed-income analytics An integrated solutions provider for the entire trading lifecycle A fast-growing presence in market data solutions for the wealth, commodities and energy sectors www.interactivedata.com .

Also, all OTC derivative trades are to be reported to trade repositories. The Financial Stability Board (FSB), which G-20 leaders tasked with monitoring reform implementation, also called for improved risk management of non-centrally cleared derivatives, including consistent margin posting. of pre- and post-trade transparency than exchanges and electronic platform trading. Also, because OTC trading often was not subject to the same level of market surveillance as exchange or electronic platform trading, market abuse was less likely to be detected. Hence the G-20 reform package which, at their 2010 Toronto Summit, G-20 leaders committed to implement in an internationally consistent and non-discriminatory way attempted to address these problems. Reforms Implementation But more than two years after the end-2012 deadline, no jurisdiction has fully implemented all of the reforms and some countries have not started.

The reforms have been delayed in many cases because the legislative and regulatory reform processes –including cross-border coordination – have turned out to be more complex than anticipated. Some countries are hanging back until Europe and the United States make and mesh their reforms. Reforms Motivation Derivatives play a useful economic role. They are used by firms and governments to expand investment and borrowing opportunities, and make revenues and expenditures more predictable.

Derivatives sharpen the pricing of risk, and provide a useful window on market expectations of key economic variables. Credit derivatives can be used to disperse credit risks to a broader and more diverse group of investors than those originating credit instruments, which may mitigate and help absorb financial system shocks. Moreover, even where individual jurisdictions have made progress, regulatory inconsistencies and frictions between countries have created a rockier road than expected. G-20 leaders called for country authorities to find ways to defer to each other’s regulations, but, for example, EU regulators resisted the authorization of U.S.-based CCP use by EU counterparties and U.S.

regulators favor requiring transactions involving U.S. counterparties to be traded on U.S.-authorized trading platforms. Unintended Consequences But the crisis exposed weaknesses in OTC markets. There were large and opaque counterparty risks, some of which were not appropriately risk-managed, that created unseen interconnections and potential contagion.

The opacity of counterparty credit risk exposures also precipitated a loss of confidence and market liquidity in already stressed markets. Furthermore, there was a paucity of data available to authorities to monitor where risk was held and the nature of the interconnections. Opacity extended to the availability of transaction data such as prices and volumes, which made transactions valuation more difficult. OTC derivative trading provides lower levels Furthermore, concerns have been raised regarding some possibly unintended consequences of the reform process. For example, the central clearing mandate may create new concentrations of risks at too-big-to-fail CCPs.

The failure of a large CCP could result in liquidity dislocations and credit losses to its clearing members. More effort is underway to discern good resolution practices for CCP to avert such a situation. Also, the adoption of margin best practice outside a CCP can create tight couplings so that large missed margin payments can propagate unpredictably. 2 There is also an inherent procyclicality to initial margin (and 2 .

Assessing the true costs and benefits of OTC derivative market reform – a global assessment and it’s impact on Asia-Pacific default fund) requirements and collateral haircuts that could exacerbate cycles. These are usually based on value-at-risk methodologies fed by historical price data. Hence, collateral requirements and haircuts can increase dramatically when markets are under stress, thus increasing price volatility and/ or illiquidity of the contracts and underlying assets. The impact of procyclicality on centrally cleared trades may be muted (versus bilaterally cleared trades) by the netting efficiencies associated with CCPs. The mitigation may only be theoretical, however, due to jurisdictional and product line central clearing fragmentation.

Several national authorities have invoked a location requirement that derivatives in the local currency or derivatives traded by local banks be only cleared through a local CCP. Central clearing will also put further strains on already tight collateral markets, because CCPs generally do not allow assets posted as initial margin to be rehypothecated3. Not only is the stock of the “safe” assets typically posted against secured borrowings shrinking, but so has its “velocity”.4 On the other hand, central securities depositories and collateral transformation agents are offering creative solutions to manage collateral more efficiently. However, such schemes could cause new channels of interconnectedness and contagion. Central Clearing Cost-Benefit Analysis In order to address some of these concerns, global regulatory standard setters created the Macroeconomic Assessment Group on Derivatives (MAGD) in 2013.

The group was comprised of representatives from 18 FSB member countries, the International Monetary Fund, European Commission, and International Organization of Securities Commissions, working with the Bank of International Settlements. Also, the unintended consequences discussed above were not part of the analysis. Small Market Perspectives Small market jurisdictions face some special challenges. If they are too small to support domestic CCPs, their banks and dealers have to clear with a non-local CCPs that only accept major currencies as margin, so locals face currency risks. On the other hand, countries that can support domestic CCPs have to have equivalence status from other country supervisors to facilitate cross border transaction clearing in the domestic CCP. Compliance with other jurisdictions’ regulatory requirements is burdensome, but perhaps worth it for most CCPs. Equivalence status is important because, for example, if a European bank were to centrally clear a transaction with a CCP that was not “qualified” it could face punitively high capital charges on its margin and default fund contributions to the foreign CCP.

And so far, European regulators have issued equivalence designations to four OTC derivative CCPs, all of them Asian (Australia’s ASX Clear, Hong Kong’s HKFE Clearing and OTC Clearing, and the Japan Securities Clearing Corporation (JSCC)). The U.S. Commodity Futures Trading Commission (CFTC) has approved comparability determinations that would permit substituted compliance with U.S. regulations for CCPs in Australia, Canada, European Union, Japan, Hong Kong, and Switzerland.

Non-U.S. CCPs (CME Clearing Europe, Eurex Clearing, and JSCC) have applied to the CFTC to become “derivative clearing organizations” (DCOs) but none have yet been approved. However, the CFTC has exempted four nonU.S.

CCPs from DCO registration until end-2015, also all of them Asian (ASX Clear, Clearing Corporation of India, Korea Exchange and Hong Kong’s OTC Clearing). The MAGD focused on the economic effects of mandatory central clearing, margin requirements for non-centrally cleared transactions; and new bank capital requirements. It concluded that the benefits out-weighed the costs, where the main benefit is the reduced likelihood of financial crises and hence higher trend economic growth. The costs stem from the requirement to hold more high-quality, low-yielding assets as collateral, and the switch from lower-cost debt to higher-cost equity financing associated with the higher capital requirements. The global reform agenda also aims to all have all OTC derivative trades reported to trade repositories.

The availability of these stored records can help regulators detect the buildup of risk exposures and interconnections among financial entities. This requirement is proving to be burdensome for smaller operators that trade across borders, since they have to report to both their domestic trade repositories and those of their counterparties. The MAGD analysis did not consider other potential postreform market configurations, for example, without mandatory central clearing but with bank capital requirements on bilateral contracts that incentivizes multilateral compression. The MAGD analysis could have usefully compared marginal benefit of mandatory central clearing to such other configurations. The reforms also aim to push standardized OTC derivatives trading on to exchanges or electronic trading platforms, where appropriate (such as when there is sufficient trading volume). This requirement was driven by a view that when transactions are opaque, as they can be when trades are bilateral, markets Trading Platform Mandate 1. Notes 1. The views expressed herein are those of the authors and should not be attributed to the International Monetary Fund, its Executive Board, or its management. 2. Notes 3. Notes 3 . Assessing the true costs and benefits of OTC derivative market reform – a global assessment and it’s impact on Asia-Pacific are less reliable and prone to increased risks, particularly under stress. Only the United States currently has mandatory trading requirements in place, Japan will in September 2015, and perhaps India and Singapore in 2016. The EU will not even have the legislative authority to do so in place until 2016. According to the International Swaps and Derivatives Association (ISDA) the U.S. trading mandate is fragmenting some swap markets.

5 CFTC regulations require that all trades with U.S. entities involving swaps that fall under its trading mandate be traded on U.S.-designated trading platforms. Non-U.S. entities involved in such transactions would have to set up access to the trading platform, and be subject to all of its rules and regulations, and those of the CFTC, including what some view as onerous inspection and record keeping requirements.

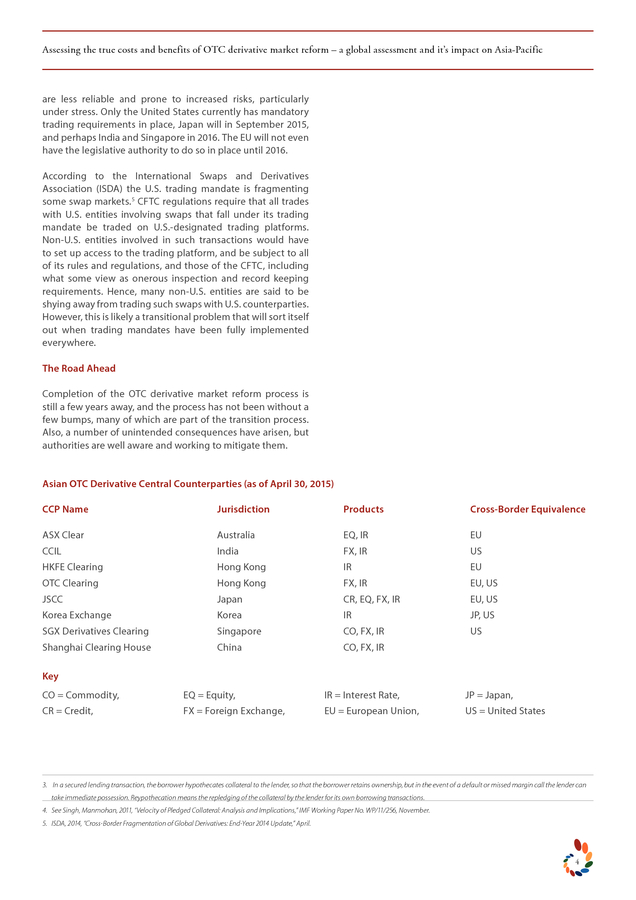

Hence, many non-U.S. entities are said to be shying away from trading such swaps with U.S. counterparties. However, this is likely a transitional problem that will sort itself out when trading mandates have been fully implemented everywhere. The Road Ahead Completion of the OTC derivative market reform process is still a few years away, and the process has not been without a few bumps, many of which are part of the transition process. Also, a number of unintended consequences have arisen, but authorities are well aware and working to mitigate them. Asian OTC Derivative Central Counterparties (as of April 30, 2015) CCP Name Jurisdiction Products Cross-Border Equivalence ASX Clear Australia EQ, IR EU CCIL India FX, IR US HKFE Clearing Hong Kong IR EU OTC Clearing Hong Kong FX, IR EU, US JSCC Japan CR, EQ, FX, IR EU, US Korea Exchange Korea IR JP, US SGX Derivatives Clearing Singapore CO, FX, IR US Shanghai Clearing House China CO, FX, IR Key CO = Commodity, EQ = Equity, IR = Interest Rate, JP = Japan, CR = Credit, FX = Foreign Exchange, EU = European Union, US = United States 3. In a secured lending transaction, the borrower hypothecates collateral to the lender, so that the borrower retains ownership, but in the event of a default or missed margin call the lender can take immediate possession.

Reypothecation means the repledging of the collateral by the lender for its own borrowing transactions. 4. See Singh, Manmohan, 2011, “Velocity of Pledged Collateral: Analysis and Implications,” IMF Working Paper No. WP/11/256, November. 5. ISDA, 2014, “Cross-Border Fragmentation of Global Derivatives: End-Year 2014 Update,” April. 4 . WHITE PAPER Assessing the operational implications of generating intra-day collateral valuations Magnus Cattan Business Development Director (Asia), Interactive Data As a result of regulatory changes and clearing fragmentation, the demand for collateral has, and will continue to, increase. Finding collateral to meet regulatory requirements such as Dodd-Frank, EMIR and Basel III will also drive the need for greater transparency and greater risk controls around valuation of collateral and measuring liquidity. A recent DTCC paper estimates the future additional collateral requirements at anywhere between $800 billion and $10 trillion, and the paper also indicates that margin call activity may increase by 500-1000%. Margin call activity will be driven for example by the reduction or removal of thresholds for variation margin and Centralised Clearing Platforms (CCPs) potentially making intraday margin calls. Collateral Management is and always has been crucial for the financial services industry. In the broadest definition, Collateral Management is the process of analyzing, validating, granting and providing advice for collateral transactions in various markets.

Its usefulness spans risk management, capital adequacy, regulatory compliance and operational risk areas. Interactive Data’s end of day pricing, fixed income evaluations and reference data are used in traditional Collateral Management applications among lending institutions across the public and private sectors. For example, in the Asia Pacific region, Interactive Data recently announced that it is providing valuations of Austraclear securities to Clearstream in support of the recently launched ASX Collateral Service. Traditionally collateral management applications have relied upon end of day pricing data. For the reasons mentioned above, demand is shifting to a need for intra-day pricing data.

For asset classes like fixed income, the operational implications of generating intraday prices or evaluations can be very challenging indeed. Broadly speaking there are three operational hurdles that need to be overcome: (1) an experienced staff to value a broad range of asset types, (2) access to a significant amount of market data, and (3) technology that can process, organize and utilize vast amounts of unstructured data. All of this needs to be done on a global and resilient network. Interactive Data’s continuous evaluated pricing offering is one result of a multi-year effort and multi-million dollar investment in our infrastructure. Interactive Data’s continuous evaluations are updated as market information, including dealer runs and quotes and trades including information from ECNs and transaction reporting services, are received and processed.

Interactive Data receives on average over 5 million observations from the marketplace for the corporate bonds that we evaluate each day. Our continuous evaluation workflow is designed to rapidly process and apply incoming data while leveraging close evaluator oversight of market conditions. Unstructured data, such as emails from market participants, are parsed electronically and automatically linked to evaluated securities.

Incoming market data are enriched to derive spread, yield and/or price data as appropriate, enabling known data points to be extrapolated for application across a range of related securities. Enriched data is tested against the current evaluation and internal tolerances and parameters. From an application perspective, Interactive Data needed to build sophisticated valuation tools that are capable of linking disparate inputs to benchmarks and to specific securities. These applications have automation rules that drive the generation of evaluated prices as market data is received and processed. When exceptions are identified, based on an evaluator’s present tolerances, the system generates notifications for review by evaluators.

Evaluators review exceptions against additional data sources, comparable securities and input from market contacts. System parameters are not static and are adjusted based on lessons learned from the exception review process. "... demand is shifting to a need for intra-day pricing data" 1. Trends, Risks and Opportunities in Collateral Management.

A Collateral Management White Paper, DTCC, January 2014 2. http://www.interactivedata.com/Assets/DevIDSite/PR-2014/Interactive-Data-Selected-as-Primary-Evaluations-Source-for-Australian-Security-Exchange-Collateral.pdf 5 . Assessing the operational implications of generating intra-day collateral valuations Continuous evaluated prices provide a consistent measure of a bond’s current market value. To monitor quality, continuous evaluations can be compared to reported trades such as FINRA® TRACE® trades in the U.S. The charts below are an example of such a comparison. Figure/Graph “Interactive Data is leading the innovation in streaming fixed income evaluated prices in order to assist our clients with mission critical applications...” Streaming fixed income evaluated prices can support realtime risk and collateral monitoring processes at market participants, depositories and clearing firms to better manage intraday exposure. The process of creating, validating and disseminating these prices involves significant operational challenges and requires access to a broad and deep array of market information, a sophisticated technology infrastructure to process this information and an experienced staff to leverage both in order to provide high quality evaluations. Interactive Data is leading the innovation in streaming fixed income evaluated prices in order to assist our clients with mission critical applications such as collateral risk monitoring. 6 .

ROUNDTABLE Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements Moderator Panellists Noel Hillmann Managing Director, Clear Path Analysis Noel Hillmann: Firstly, thank-you for joining me for this debate. I’ll begin by asking, as international fund managers, and in light of changes in European and US market collateral management rules, how have your investment operations changed and what has this meant for your APAC based securities lending activities? Adrian Song: For us in APAC, we do not have a securities lending programme currently. However changes in collateral requirements do affect us nonetheless. The introduction of margin requirements on non-centrally cleared derivatives will add costs to operationally support trading OTC derivatives. The activities of managing collateral increases as additional instruments are progressively inscope.

Investment management would need to look for more sources of eligible collateral in their portfolios and be more proficient in managing and reinvesting collateral. Without a scalable system, the benefits of mitigating counterparty risks would be eroded by a firm’s inability to cope, giving rise to increased operational risk. Despite regulators pushing back deadlines numerous times, in part to try to harmonise cross-border requirements and partly to allow firms sufficient time to be ready for it, we should not be hopeful that these requirements will go away. Frederic Rebry: To elaborate a bit on how securities lending activity is conducted by BNP Investment Partners, this is rather limited for the APAC region.

We have indeed global managed portfolios, managed out of Frederic Rebry Head of Financial Service Providers Front, Middle & Custody, BNP Paribas Investment Partners Asia, that are on the securities lending program. However, overall we can conclude that the local securities lending activity is limited. The majority of the business is European based at this stage. With regards to the collateral changes resulting from Europe and especially in the U.S., because they are front runners, we can all agree that current regulations are completely overseeing all businesses that do have any links with collateral.

We can list the big regulatory changes such as Dodd Frank, e.g. Over The Counter (OTC) clearing, European Market Infrastructure Regulation (EMIR) / European Securities & Markets Authority (ESMA), risk mitigation and “Efficient Portfolio Management”: everything that is related to concentration and diversification ratios, re-use of cash collateral and so forth. Next to these you have Basel III capital ratios, Liquidity Coverage Ratios (LCR), and ISOCO, mandatory bilateral collateralisation.

You need to look at these as part of the global picture. From a collateral management approach, it’s very important to understand that all of these need to be considered in the investment operations framework, not necessarily only those linked to securities lending. If I look at it from a BNP Investment Partners perspective, we have been closely following up these changes since day one, in close co-operation with our Securities Services team (as part of the group). As mentioned by Adrian, it’s important to indicate that in Adrian Song Head of Portfolio Operations, Schroder Investment Management (Singapore) some cases, we need to cope with an overall pushback of these regulations. The U.S. have been front runners on this subject.

They started in 2013 with the OTC clearing part. If you look at EMIR and OTC clearing, it will only commence mid-2016. It was foreseen at the end of 2012.

I also understand that International Organization of Securities Commissions (IOSCO) has been pushed back for 9 months and it doesn’t make it easy so anticipation is rather difficult, both for the sell and buy side. Over the last few years, a lot of discussions have been held around collateral overall, this from transformation to optimisation needs, so the cheapest to deliver and an eventual collateral squeeze, etc. There is definitely no doubt that indeed investment operations are heavily impacted by these changes, where decisions are to be taken on how to manage your collateral once you have it. I want to stress that the approach of this review cannot necessarily be linked to securities lending only.

There is a need for an overall consideration of all the collateral changes and impacts across assets, being part of one portfolio. Only by doing so, you will be able to adapt the current situation and cope with a most suitable approach. Noel Hillmann: How far along are you in designing a new or adapting an existing securities lending programme? What risk / reward considerations have you found yourselves needing to make as part of this process? 7 . Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements Frederic: As indicated, it is important to really understand all collateral changes and impacts, so within the current evolving collateral framework there is need to look at the global picture. OTC clearing will result in higher collateral requirements, coming with an opportunity cost. If you look at the current level of bilateral trades, we do not have that mandatory initial margin which is called an independent amount in the bilateral space. This is not being implemented on all sides at the moment for the bilateral trades. IOSCO will result in mandatory bilateral collateralisation.

Adding Basel III, you end up in a situation where all market participants are seeking high quality collateral. If I then focus on securities lending I would like at this stage to make a split between two approaches. First of all I would like to look at the lending activity, what is lent out to currently generate revenues for the portfolio, with a focus on portfolios that are active in any kind of assets that result into collateral requirements. The second approach, I would like to elaborate on is what is accepted as collateral in the securities lending framework; knowing that everybody is seeking high quality collateral due or resulting from all of these regulatory changes. If I start with the first point, it will be key to see what is basically lent out against the overall collateral requirements of each portfolio invested in any activity that needs collateralisation. So assets that are currently on loan might tomorrow be needed to cope with these collateral requirements, where basically the revenue of a typical asset that is on loan will need to be mirrored against any cost to obtain that asset in another way. This is in order to meet your collateral obligation resulting from any other trading activity.

If you have a portfolio which is active in, for example, both OTC and securities lending, it will be very important that there is very close monitoring in order to ensure that any collateral obligation will be met within a smooth front to back architecture. For example, if I have a security that is also eligible collateral and I lend it out in the securities lending framework and tomorrow I take a position in OTC clearing and my initial margin is requiring that eligible security that is on loan, what am I going to do? If I look at the cost to obtain the eligible security to cover my OTC deal – alternatively I will take another asset and transform it to meet that initial margin on OTC clearing – it might be higher than the revenue resulting from my securities lending activity. I will then recall that security. Basically there you are going to have to find a balance between your revenue and your cost. My second point leads to the collateral acceptance in the securities lending framework.

We all agree that high quality is of course preferred. However the potential growing lack of high quality assets is, as I explained, resulting from the several regulations. Everybody is seeking high quality collateral. There might be a need to look into other asset classes as being eligible collateral for securities lending. If not, there is a probability that you will need to be willing to cope with a decrease in the securities lending revenues.

We know that in the end, securities lending transactions can be stopped at any time with a 24h notice period. OTC contracts are longer term contracts and it is less common to use equities for OTC collateral. If I look at the securities lending and the collateral used, we do accept in some cases blue chip equities. If you look at OTC, accepting equities will have an impact on your pricing negotiations so everybody for the moment in the OTC space prefers cash. In addition, you will need to keep in mind some collateral principles such as: collateral needs to be liquid enough, it needs to have transparent pricing, it needs to be daily valuated, credit quality of the issuer is important, correlation counterparty/collateral, concentration diversification (sector, country) etc.

So again this is all very important. If you look at collateral you look at it within one portfolio, for example, for all asset classes that do require collateral. Basically we need to find a balance between the risk and rewards considerations. We follow a strict policy on collateral eligibility in the securities lending framework.

Accepting collateral other than high quality, e.g. blue chip equities/corporates, might indeed result in higher revenues. At the end, the risk/reward perspective is not a one off consideration but a continuous process to closely monitor every single day. Noel: What steps have you taken or do you propose to take too minimise operational risk in your securities lending programmes given the need for higher margin requirements? Frederic: If you look at the operational risk aspect, we all agree that’s it not necessarily something that links itself to securities lending only but it’s present in the overall investment activities. You can have, exchange problems, poor communication between stakeholders, failed settlement, settlement cycles overall, etc. If you understand these it might be easier to ensure that the operational risk part stays to a minimum. Keeping aside the upcoming collateral requirements, there is a need to have a robust recall process where for any sell order by the portfolio manager, an immediate trigger is set to recall the securities on loan.

We all know that if you look in Europe, Target 2 Sedcurities (T2S) has spread a lot of “fear” before implementation. However, whether it is purely linked to a sell order or linked to the recall of lent positions that will be requested to be returned to meet any collateral obligation, or linked to the collateral management exchanges overall, the model needs to prove that it is more than secure. 8 . Assessing the risk and reward of initiating a new securities lending programme against the needs for higher margin requirements I do believe that it is key that first of all the recall process within the securities lending framework is working without any operational constraints. If you then extend this to the overall picture of meeting any collateral obligation, there will be a need for transparency and a “real time” view on the several activities within one portfolio, such as OTC bilateral, OTC clearing, Exchange Traded Derivatives (ETD), securities lending and repo activity, and the available collateral. By this I mean, it will give you the opportunity to anticipate, link up the overall activity and react in the most appropriate way. All of this is only possible if it is supported by a Front to Back (F2B) process that is robust enough and Straight Through Processing (STP) automated. With F2B, I do mean the complete chain, so if I look at securities lending and the borrowers, it’s also important that you screen your borrowers on a temporary basis and you follow them much closer and ensure that recall fails are an exception only. In addition, only lending out part of the portfolio and working with buffers are also important points to consider. This is where you keep aside part of your eligible collateral that might be used for all other coverage of transactions, so you only lend out X% of your portfolio for example. We ensure a continuous robustness of the F2B process with dedicated procedures, which are audited and controlled on a temporary basis in order to ensure that any lent out position is returned “at any time” and “in time”, for whatever need. As said in the beginning, with a 24 hours’ notice period you could stop your securities lending transaction so it’s very important that you can recall them at any time and that they come back in time.

All of this is only feasible if you have a robust front to back process. Noel: Adrian, in terms of moving forward and looking at introducing a securities lending/collateral management programme into Asia Pacific, you talked a little bit about those OTC derivative reforms that would certainly make the possibility greater. Do you foresee a market environment in the short-term where there is a need for you to initiate a securities lending and a collateral management programme in Asia Pacific or do you think it’s perfectly fine for it to be managed out of head office or elsewhere? Adrian: Currently in APAC, our volume on collaterals is not high and whilst we have a solution to manage our collaterals, we are working with our global counterparts to source a more robust and scalable solution across the group so as to enable our fund managers and back office to better manage the entire end-to-end collateral process in the future. enough to support the needs of all the funds. Noel: On that final note I’d like to finish. Thank-you very much to both of you for sharing your thoughts. “We are at a point where regulators’ timelines are fluid...” The OTC derivatives landscape is changing, where we previously do not need to collateralise certain OTC activities such as FX forwards. Including these activities would mean incremental volumes to collateral operations.

Systems need to be scalable and enhanced with tools to assist in the determination of collateral to deliver, e.g. cheapest to deliver. Collateral management activities would need to complement the core investment management activities. The portfolio would need to set aside a pool of assets as eligible collateral to sustain OTC activities or engage a third-party to facilitate collateral transformation at a fee; or eventually seek exchange-traded substitutes where the margin requirements are less onerous. We are at a point where regulators’ timelines are fluid and thus we need to actively look at the different options available. Repo, securities lending, collateral management through third-party providers, managing collateral inhouse: these are all potential avenues. The choice we make needs to be robust 9 . Powerful Solutions to Today’s Challenges Q Q Q Q A market leader in fixed-income evaluations, pricing and reference data A preeminent provider of fixed-income analytics An integrated solutions provider for the entire trading lifecycle A fast-growing presence in market data solutions for the wealth, commodities and energy sectors www.interactivedata.com .