Uncle Sam Follows Ex-U.S. Citizens and Green Card Holders – Even Past the Grave - April 2016

Hodgson Russ

Description

April 2016 - Vol. 3 No. 6

Message From The Chair, STEP Toronto

Welcome to Spring 2016 and the April issue of

CONNECTION. It has been a while since my last update

and some exciting things have and are happening at

STEP.

Our last program was Post Mortem Planning – Private Corporation Shares and while I was not able to attend, I have had wonderful feedback about the program and the information presented. Thanks again to our speakers and moderator. Our next educational session is on Wednesday April 13, 2016 and is an update on Insurance in Estates and Trusts, with Ted Polci and Chris Ireland speaking and Harris Jones moderating.

While webcast is available as always, I encourage all our members to try to attend in person to take advantage of the networking opportunities that doing so provides. Also, I remind you of our complimentary “Bring a Guest” initiative. You can bring a nonmember guest to our STEP Toronto educational sessions.

Details are in this newsletter, but please remember to pre-register your guest electronically. A complete list of our remaining 2015/2016 programming can be found at STEP.ca. March also brought our first ever “STEPping Out to Lunch Series”. We had approximately 40 STEP members attend this informal roundtable style session over the lunch period. The discussion was lively, interesting and most importantly driven by you, our members.

By the end of the session, people were asking for the next one. By the time this newsletter is distributed, we will have had our second session hosted again at Dentons. We hope to continue the “STEPping Out to Lunch Series” during the first week of each month and if there is interest, we can continue over the summer months too.

Please be sure to look to your email blasts for the announcement of future sessions and follow registration instructions. You must register for these sessions as space is limited and we want to be able to continue to encourage a lively discussion. Finally – enrolment for the 18th STEP National Conference is underway and is shaping up to be great event once again! Please be sure to review the conference material and register soon. As I have noted in all previous CONNECTION Newsletters – it is up to all of us to make STEP the best it can be. The simplest way to do this is simply to increase member involvement.

If you want to become more involved, please contact me or any of the Toronto executive. Of course, we continue to invite your contributions to “CONNECTION”. Only with your participation can we make STEP Toronto the best it can be. Brian Cohen, Chair STEP Toronto Executive In this Newsletter Message From the Chair STEP Toronto Presents... In Case You Missed It Other Upcoming Events STEP Toronto Announces : “BRING A GUEST” Article: Uncle Sam Follows Ex-U.S. Citizens and Green Card Holders – Even Past the Grave Article: Life insurance and Budget 2016 – What’s changed? Article: In Grocery Bags and Under Pads of Paper: The Validity of a Found Holograph Codicil About Connection STEP Toronto Executive Brian Cohen, Branch Chair Ted Polci, Branch Deputy Chair Elaine Blades, Secretary Marina Panourgias, Treasurer Kimberly Whaley, Branch Past Chair Craig Vander Zee, Program Officer Paul Keul, Member Services Officer Corina Weigl, Student Liaison Officer Daniel Dochylo, Governance Liaison Jeff Halpern, Sponsorship Officer Joan Jung, Newsletter Officer Chris Delaney, Ex-Officio (nonvoting) Members at Large: Harris Jones Ian Lebane Gillian Musk . STEP Toronto Presents... April 13, 2016 – Insurance in Estates and Trusts Looking at the practical use of life insurance in trusts and estate planning, including variation of a trust, pipeline planning, charitable donations - including redemption of private shares from a charity, leverage structures, and use of insurance in professional corporations. There will be a brief review of new budget proposals affecting life insurance planning. As well, a summary chart will be provided simplifying the changes and the impact on planning of the new exempt rules. Moderator: Harris Jones, CA, CFP, CLU, TEP: HarrisJones Advisory Inc Speakers Ted Polci, CLU, TEP: Partner, First York Chris Ireland, CA, TEP: Senior Vice-President, PPI Advisory Registration: :30 p.m. 2 Seminar: 3:00 p.m. – 5:00 p.m. Venue: Osgoode Hall, Donald Lamont Learning Centre, 130 Queen St West, Toronto Remote Sites: Wilson Vukelvich LLP Manulife Financial (Learn Room) Suite 710, 60 Columbia Way 600 Weber Street North Markham Kitchener-Waterloo Please note that at the remote sites (group webcast viewing), space is limited to room capacity. .

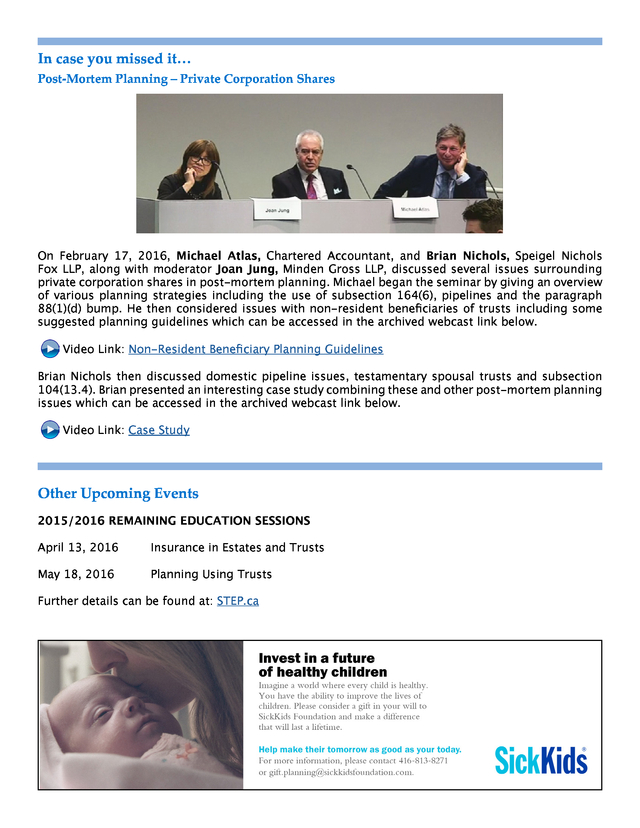

In case you missed it… Post-Mortem Planning – Private Corporation Shares On February 17, 2016, Michael Atlas, Chartered Accountant, and Brian Nichols, Speigel Nichols Fox LLP, along with moderator Joan Jung, Minden Gross LLP, discussed several issues surrounding private corporation shares in post-mortem planning. Michael began the seminar by giving an overview of various planning strategies including the use of subsection 164(6), pipelines and the paragraph 88(1)(d) bump. He then considered issues with non-resident beneficiaries of trusts including some suggested planning guidelines which can be accessed in the archived webcast link below. Video Link: Non-Resident Beneficiary Planning Guidelines Brian Nichols then discussed domestic pipeline issues, testamentary spousal trusts and subsection 104(13.4). Brian presented an interesting case study combining these and other post-mortem planning issues which can be accessed in the archived webcast link below. Video Link: Case Study Other Upcoming Events 2015/2016 REMAINING EDUCATION SESSIONS April 13, 2016 Insurance in Estates and Trusts May 18, 2016 Planning Using Trusts Further details can be found at: STEP.ca .

STEP Toronto Announces “BRING A GUEST” – COMPLIMENTARY to a STEP Toronto Educational Session. STEP Toronto is pleased to announce a special opportunity for members to share the benefits of STEP Toronto’s education program with colleagues who are potential members. STEP Toronto members registered for the program (or Passport holders) may bring a guest “compliments”. The following program sessions are eligible: April 13, 2016 - Insurance in Estates and Trusts May 18, 2016 - Planning Using Trusts Please register your guest (a non-member) by clicking on the link below. Let us know the name, firm and e-mail address of your guest and the program chosen so that he/she can be registered. Register My Guest - STEP Toronto Note: You may bring one different guest to each session . ARTICLE: Uncle Sam Follows Ex-U.S. Citizens and Green Card Holders – Even Past the Grave By: Carol A. Fitzsimmons, BA, JD, Partner, International Tax Practice Leader, Hodgson Russ LLP Many international practitioners are aware that U.S. citizens are taxed on their worldwide income and assets, under the U.S.

income, gift, estate and generation-skipping transfer tax regimes. Many are also aware that it is possible for a U.S. citizen to renounce U.S.

citizenship and remove himself or herself from the application of this worldwide income and asset taxation although for persons who are deemed to be “covered expatriates”, there is an “exit tax” (as well as potential acceleration of U.S. income tax on pension-related income, deferred compensation, stock options and the like). A covered expatriate is a person who has a net worth in excess of US$2M at the time of expatriation, or an average annual U.S.

federal tax liability for the prior five years of US$161,000 or has not complied with his or her U.S. tax obligations for the prior five years before expatriation. There are certain exceptions to covered expatriate status even if a U.S. citizen falls into one of the categories above, such as for persons renouncing before age 18 ½ and for persons born a dual citizen of the United States and the country in which they reside. Similar rules apply to “long term green card holders” who give up their green cards.

These persons can also be covered expatriates under the thresholds noted above. A long term green card holder is someone who has held a green card for more than 7 out of the prior 15 tax years. There is no “age 18 ½” or “dual citizen at birth” exception for long term green card holders, however. This expatriate regime for income tax purposes went into effect in 2008.

What many persons do not know, however, is that at the same time, Congress enacted an inheritance tax regime under Section 2801 of the Code that is applicable to the U.S. recipient of a gift or bequest from a covered expatriate. The Section 2801 tax applies at a 40% rate on the value of the gift or bequest. A gift or bequest from a covered expatriate on which inheritance tax is imposed also includes certain trusts (U.S.

trusts and “electing” foreign trusts). Recently, the IRS finally issued proposed regulations on this eight year old statute. The proposed regulations are quite detailed, and there are many provisions designed to address what might otherwise be techniques to avoid the inheritance tax rules – such as the covered expatriate leaving property to a foreign trust, which has U.S. beneficiaries.

Under the proposed regulations, the U.S. beneficiaries of such a trust are subject to the Section 2801 tax on distributions from the trust, unless the foreign trust elects to pay the Section 2801 tax “up front”. The inheritance tax has a particularly onerous feature to it, which is a very limited exclusion amount from the inheritance tax. Essentially, the U.S.

annual exclusion from gift tax (presently US$14,000 in . 2016) is the only exclusion that all recipients of gifts or bequests from covered expatriates are allowed to reduce the value subject to the inheritance tax. Thus, no use is allowed of the “lifetime” gift and estate tax unified credit, which provides an exemption of US$5.45M (in 2016), that would have applied to a non-expatriating U.S. citizen or U.S. domiciliary.

As a result, the inheritance tax is actually much worse than the U.S. gift and estate tax would have been had the covered expatriate remained a U.S. taxpayer. There are also a couple of fairly limited exclusions from the Section 2801 tax for certain transfers to a covered expatriate’s spouse if the spouse is a U.S.

citizen, and to charities. The proposed regulations set forth the reporting procedures for a U.S. person who receives a gift or bequest from a covered expatriate. There will be an IRS filing required on Form 708, once the proposed regulations are finalized.

The proposed regulations put the burden of ascertaining whether a gift or bequest was received from a covered expatriate on the U.S. recipient. While perhaps the IRS assumes that a beneficiary of a gift or bequest would know whether the person making the gift or bequest is a covered expatriate, that will not always be the case. It is important that practitioners who are counseling individuals who are U.S.

citizens or green card holders, and who may wish to change that status, take into account not only the more well-known U.S. income tax consequences of expatriation that may apply, but also the potential impact of the inheritance tax, particularly if there will be other persons in the individual’s family who will retain U.S. citizenship or green card status. Article: Life insurance and Budget 2016 – What’s changed? By: Hemal Balsara, CPA, CA, CFP, TEP, Assistant Vice President, Regional Tax, Retirement and Estate Planning Services, Manulife 1 The 2016 Federal Budget was presented on March 22, 2016. There were a variety of proposed changes to the existing tax rules.

Specifically, there were two measures proposed in the budget that relate to life insurance: 1. Capital dividend account (“CDA”) and life insurance proceeds 2. Transfers of life insurance policies to a corporation CDA and life insurance proceeds The Income Tax Act (“ITA”) provides that the death benefit from a life insurance policy is generally received tax free. In order to preserve this treatment when a private corporation is the recipient of a life insurance death benefit, the ITA provides that the corporation receives a credit to its CDA equal to the excess of the death benefit received over the adjusted cost basis (ACB) of the policy to that . corporation. Capital dividends can be paid by a private corporation to the extent of its CDA balance and are non-taxable in Canada to the shareholder. Prior to the budget some taxpayers were arranging their affairs in a manner that involved owning the life insurance policy in one corporation and having the beneficiary be another corporation. By structuring in this manner, the objective may have been to avoid the ACB reduction on the CDA credit and receive a full CDA credit for the death benefit of the life insurance policy. Some valid business reasons for this structure may have been for creditor protection and facilitating buy-sell planning as between operating companies and holding companies.

Due to the wording of the definition of CDA in subsection 89(1), the reduction in the CDA by the ACB only applied to the owner of the policy. The Canada Revenue Agency (“CRA”) has expressed concerns in the past with such arrangements. CRA indicated that where the primary objective of separating the ownership and beneficiary of the life insurance policy was to maximize CDA, the general anti-avoidance rule “GAAR” would apply to reduce the CDA credit by the ACB of the life insurance contract. The budget proposes to amend the ITA such that for deaths on or after March 22, 2016 the credit to the CDA will be reduced by the ACB of the policy regardless of who owns the policy.

This is being achieved by reducing the CDA credit by the ACB of “a policyholder’s interest in the policy” rather than the current language which reduces the CDA credit by the ACB of “the policy to the corporation”. A similar mechanism exists for partnerships to be able to distribute life insurance death benefits on a tax free basis, and a similar change is proposed to prevent this planning in the partnership context. As an enforcement mechanism, the budget also introduces an information reporting requirement applicable to a corporation or partnership that is not a policyholder or owner but is entitled to receive a policy benefit. The CRA has indicated in the past that it does not like splitting ownership and beneficiary in the corporate context and there may be income tax implications that result from such structures.

For example, in CRA’s view, where a subsidiary corporation is the owner and a parent corporation is the beneficiary, a shareholder benefit would apply to the parent corporation resulting in an income inclusion equal to the amount of premium. Similarly, where a parent corporation is the owner and premium payor of a policy and a subsidiary corporation is the beneficiary, there could be indirect benefits under 246(1) and income inclusions to the subsidiary corporation for the amount of the premiums. If the Parentco was reimbursed for the premiums by the subsidiary company, the impact of the indirect benefit to the subsidiary corporation would be reduced.

However, the reimbursement would create its own income inclusion to the parent corporation. This form will likely allow the CRA to better quantify and track these split ownership/beneficiary scenarios. Transfers of Life Insurance to a Corporation Transfers of a life insurance policy generally give rise to a taxable policy gain equal to the excess of the proceeds received over the policyholder’s ACB of the policy. There was a loophole in the pre2016 budget rules that allowed for tax arbitrage as it related to a sale of a life insurance policy by a shareholder to a non-arms length corporation.

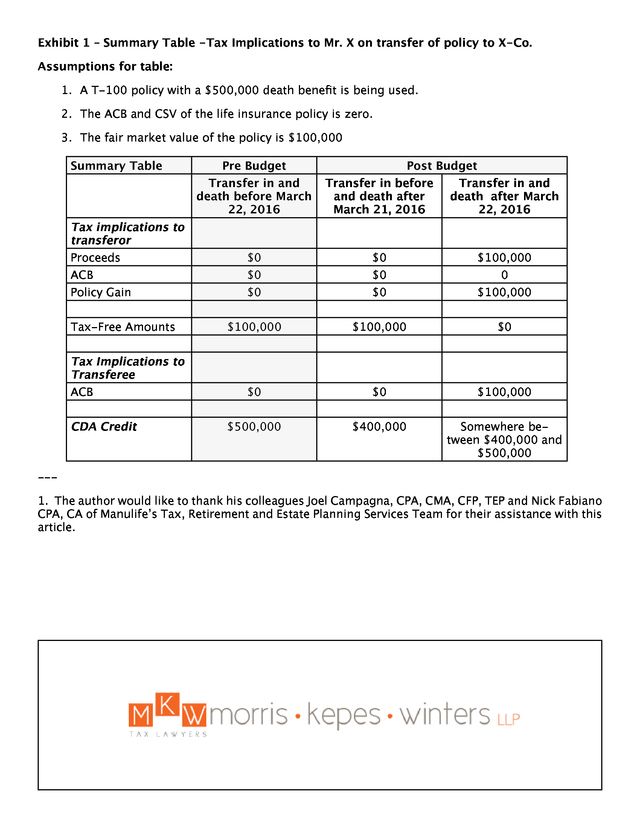

The individual transferring the policy would be . deemed under the ITA to have sold the policy to the corporation for proceeds equal to the cash surrender value (“CSV”) of their interest in the policy and the corporation acquiring the policy would be deemed to have acquired the policy at that CSV. The only tax implications to the shareholder would be to report a fully taxable policy gain to the extent that the CSV of their interest in the policy exceeded the ACB of their interest in the policy. However, since the shareholder was contributing an asset that could have a fair market value (“FMV”) in excess of the CSV, the shareholder could receive this excess tax-free. The FMV of a life insurance policy should be determined by an independent actuary through a valuation report. Valuation reports take into account a variety of different factors including the cash surrender value of the policy, the policy loan value, the face value of the policy, the state of health of the insured, conversion privileges and the replacement value of a policy to determine the estimated FMV of a life insurance policy. Assume Mr X owns a Term-100 life insurance policy with a $500,000 death benefit and an ACB and CSV of zero.

The policy has been determined to have a fair market value of $100,000. Mr. X also owns 100% of X-Co and he transferred his policy to X-Co prior to March 22, 2016.

. Upon transfer, he would have been deemed to dispose of the contract at CSV. Since CSV and ACB are nil, there would be no income inclusion to Mr.

X. Under the previous rules he could extract $100,000 from the corporation tax-free as this excess was not taxable. The budget includes proposals that will prevent this planning in respect of transfers on or after March 22, 2016 by ensuring the proceeds from the sale for the purposes of the ITA are not less than the amount of the consideration received from the corporation. Coming back to Mr.

X, if he transferred the policy to his corporation, on or after March 22, 2016 and wants to extract fair market value, he will have a full ordinary income inclusion of $100,000. Meanwhile, X-Co will have a policy with an ACB of $100,000. This higher ACB could serve to reduce the ultimate CDA credit on death if the ACB is not fully reduced to nil by the time of death. The most surprising part of the budget related to policies that were transferred into a corporation prior to March 22, 2016.

In these cases, the budget proposes that any excess consideration received on the transfer over the proceeds used to determine the policy gain (i.e. CSV) will permanently reduce the CDA credit to the private corporation. This will impact transfers that have already occurred.

Coming back to Mr. X, let’s assume he had transferred the policy to X-Co prior to the budget and was able to extract $100,000 tax-free from the corporation. When Mr.

X ultimately passes away, the death benefit of $500,000 would be paid into the corporation, X-Co would receive a CDA credit for $400,000 ($500,000 less $100,000). In other words, a past transfer would forever reduce the CDA credit by the amount of the excess extracted above the CSV. Similar changes are proposed to prevent this planning in the partnership context. Experienced, Independent, Professional Advice. Ted Polci, CLU, TEP tedp@fyork.com 416-966-9675 . Exhibit 1 – Summary Table -Tax Implications to Mr. X on transfer of policy to X-Co. Assumptions for table: 1. A T-100 policy with a $500,000 death benefit is being used. 2. The ACB and CSV of the life insurance policy is zero. 3. The fair market value of the policy is $100,000 Summary Table Tax implications to transferor Proceeds ACB Policy Gain Tax-Free Amounts Tax Implications to Transferee ACB CDA Credit Pre Budget Post Budget Transfer in and death before March 22, 2016 Transfer in before and death after March 21, 2016 Transfer in and death after March 22, 2016 $0 $0 $100,000 $0 $0 $100,000 $100,000 $100,000 $0 $0 $0 $100,000 $500,000 $400,000 Somewhere between $400,000 and $500,000 $0 $0 0 --1. The author would like to thank his colleagues Joel Campagna, CPA, CMA, CFP, TEP and Nick Fabiano CPA, CA of Manulife’s Tax, Retirement and Estate Planning Services Team for their assistance with this article. . ARTICLE: In Grocery Bags and Under Pads of Paper: The Validity of a Found Holograph Codicil By: Kimberly A. Whaley, CS, TEP, LLM, Principal, Whaley Estate Litigation “If the Testatrix considered a Sobey’s bag appropriate for storing her Will, then it stands to reason that the location of the Codicil on a ledge in the apartment does not detract from the analysis as to whether the Codicil was intended to be a testamentary document.” ~ Justice Marshall In King Estate v Hiscock, 2015 NLTD(G) 173, the Newfoundland Supreme Court Trial Division considered whether a handwritten codicil left folded under a pad of paper on a ledge in the apartment of the deceased was a valid testamentary document. The Court examined two issues: 1) was the Codicil testamentary in nature or only “deliberative or initiatory” and 2) was the Codicil validly signed? Background The deceased, Cynthia J. King, drafted a valid holograph Will in 2002.

She named an executrix under the Will and advised her of its existence. The executrix searched for the Will after the testatrix had died and found it in a card sized envelope with other unrelated papers in a plastic Sobey’s shopping bag, within a garbage bag. Later, when the executrix was cleaning out the deceased’s apartment she was making a note on a pad of paper located on a ledge where the deceased kept her telephone, when she discovered a second document, folded in half, under the pad of paper.

It was the alleged Codicil. The Codicil was entirely hand written by the deceased and was dated May 8, 2012 (just over a month before her death). The executrix submitted it for probate along with the holograph Will. The defendant in this matter, a sibling of the deceased, was not aware of the Codicil until after it had been probated. The defendant brought a motion to revoke the order of probate for the codicil, arguing that it was not valid under the Wills Act RSNL 1990, c.

W-10. The Codicil was a simple two page document that reflected a different distribution than the Will. One example: the Will provided that a property was to be sold and divided equally between two siblings while the Codicil indicated that the property was to be sold and the proceeds left to only one sibling. The Codicil was also unsigned but the deceased had written her name several times in the body of the Codicil (i.e. “For Cynthia J.

King’s Estate”, “I; Cynthia J. King. .

.says for my estate” and “Cynthia J. King says ‘Yes’ to what I have written here”. Furthermore, the testatrix had written at the bottom of the Codicil, “Witness: Jean Asernault [sic] – Cynthia King’s Best Friend”.

There was, however, no signature from Jean Arsenault. The Analysis: Justice Marshall first noted that even if the Codicil was properly executed its probate should be revoked if the Codicil “was only deliberative or initiatory”.1 In other words, if it does not show the testatrix’s final intention it should not be admitted to probate. If it merely expresses an intention to instruct a solicitor to prepare a will or her intention to draft a subsequent holograph will, it is not testamentary in nature. The defendant argued that the Codicil was merely a plan or notes about the contents of a subsequent will which was never made. It was not witnessed or signed by the deceased.

If it was supposed to be such an important document it would have been in a more secure spot than under a pad of paper on a ledge in her apartment. 1 2015 NLTD(G) 173 at para. 41. . But Justice Marshall noted that the deceased had kept her Will in a Sobey’s bag. The Sobey’s bag was also not a secure place: “The facts are that the Codicil existed; it was not discarded; and it was in a location where it could be, and was, found.”2 Considering also that a witness’s signature was not required on the holograph codicil, the fact that the witness’s signature was not obtained does not lead to the conclusion that the Codicil was “deliberative or initiatory” particularly where the contents of the entire Codicil are examined to determine if there is a disposing effect. Also, the deceased had used phrases such as “This is my wish & my Request” and “I; Cynthia J. King …says for my estate to do the following” which were indicative of the deceased’s intention as to the disposal of her property upon her death. Justice Marshall concluded that the Codicil was indeed a “deliberate or fixed and final expression” of the deceased’s intention and concluded that “the Codicil is not invalid due to Ms.

King not specifically referring to an executrix, the residue, the previous will, or the word “bequest”. The Codicil clearly described Ms. King’s intent as to the disposal of her property upon death and revoked only the inconsistent portions of the Will.3 But was it validly signed? It was clear that the deceased had not signed the document in a stand-alone fashion, either at the beginning or end of the document.

However, the deceased had signed her name multiple times within the body. Justice Marshall summarized: [i]t would be unjust to defeat the clear intentions of the Testatrix simply on the basis that none of her signatures, as contained in the Codicil, were ascribed on a stand-alone basis. Specifically, Ms.

King’s signature is contained in the first and last lines of the Codicil; and either of these lines was written last by the Testatrix. In my view, whichever of these lines was written last, such line constitutes an authentication of the Codicil. These lines should be considered in the context of the confirmatory middle sentence.

As stated, the signature in the middle sentence could also be deemed as the act of execution necessary to “breathe the life of intention” (Oliver Estate, (1993), 106 Nfld. & P.E.I.R. 32, (Nfld.

T.D.), aff’d (1994), 124 Nfld. & P.E.I.R. 294 (Nfld.

C.A.) at paragraph 42) into the document. Justice Marshall determined that the Codicil was validly executed. Concluding Comments While valid holograph wills are indeed proper testamentary documents, they are not without their complications, as this case evidences. It is surprising the number of people who rely on holograph wills - perhaps they wish to avoid lawyer’s fees or feel that their estate is simple enough to deal with themselves. However, the issues with holograph wills are numerous, including ambiguities and errors, failure to dispose of the entire estate, failure to name an executor, etc.

or they can easily go missing or not be found at all if the testator fails to tell anyone that the will exists or where it can be found. Spending a little money up front to get a properly drafted Will will likely save a lot of wasted court fees in the long run. 2 3 Ibid at para. 49. Ibid at para. 71. .

About Connection Please note that each advertiser is linked to their web page (as are our program sponsors on the last page). Please click through to their web pages to learn more about each of our sponsors and advertisers. STEP Toronto publishes ‘Connection’ for our membership 6-7 times per year between September and May. We welcome your feedback and contributions. Please send any comments or inquiries to Joan Jung jjung@mindengross.com. Letters, announcements, opinions, comments from members If you have an article or an idea that would be of interest to other members of STEP, please send them to paul.keul@scpllp.com for inclusion in our next edition of the STEP Toronto Connection. STEP continues to grow and we welcome membership inquires.

As a reminder, there are three routes to full membership; one based on experience (Experienced Practitioner) and two education routes (essay or exam). If you know anyone who would be a good candidate for STEP membership, please direct them to the STEP Canada website for information. Connection Newsletter Contacts Joan Jung – jjung@mindengross.com Paul Keul – paul.keul@scpllp.com Nicole Hastings – nhastings@millerthomson.com Teresa F. Lee - teresa@leewillsandestates.ca Program Sponsors PREMIER SPONSORS EVENT SPONSORS SUPPORTING SPONSORS de VRIES LITIGATION LLP, PPI Advisory, Thorsteinssons LLP Connection STEP Toronto Newsletter - April 2016, Vol.

3 No. 6 .

Our last program was Post Mortem Planning – Private Corporation Shares and while I was not able to attend, I have had wonderful feedback about the program and the information presented. Thanks again to our speakers and moderator. Our next educational session is on Wednesday April 13, 2016 and is an update on Insurance in Estates and Trusts, with Ted Polci and Chris Ireland speaking and Harris Jones moderating.

While webcast is available as always, I encourage all our members to try to attend in person to take advantage of the networking opportunities that doing so provides. Also, I remind you of our complimentary “Bring a Guest” initiative. You can bring a nonmember guest to our STEP Toronto educational sessions.

Details are in this newsletter, but please remember to pre-register your guest electronically. A complete list of our remaining 2015/2016 programming can be found at STEP.ca. March also brought our first ever “STEPping Out to Lunch Series”. We had approximately 40 STEP members attend this informal roundtable style session over the lunch period. The discussion was lively, interesting and most importantly driven by you, our members.

By the end of the session, people were asking for the next one. By the time this newsletter is distributed, we will have had our second session hosted again at Dentons. We hope to continue the “STEPping Out to Lunch Series” during the first week of each month and if there is interest, we can continue over the summer months too.

Please be sure to look to your email blasts for the announcement of future sessions and follow registration instructions. You must register for these sessions as space is limited and we want to be able to continue to encourage a lively discussion. Finally – enrolment for the 18th STEP National Conference is underway and is shaping up to be great event once again! Please be sure to review the conference material and register soon. As I have noted in all previous CONNECTION Newsletters – it is up to all of us to make STEP the best it can be. The simplest way to do this is simply to increase member involvement.

If you want to become more involved, please contact me or any of the Toronto executive. Of course, we continue to invite your contributions to “CONNECTION”. Only with your participation can we make STEP Toronto the best it can be. Brian Cohen, Chair STEP Toronto Executive In this Newsletter Message From the Chair STEP Toronto Presents... In Case You Missed It Other Upcoming Events STEP Toronto Announces : “BRING A GUEST” Article: Uncle Sam Follows Ex-U.S. Citizens and Green Card Holders – Even Past the Grave Article: Life insurance and Budget 2016 – What’s changed? Article: In Grocery Bags and Under Pads of Paper: The Validity of a Found Holograph Codicil About Connection STEP Toronto Executive Brian Cohen, Branch Chair Ted Polci, Branch Deputy Chair Elaine Blades, Secretary Marina Panourgias, Treasurer Kimberly Whaley, Branch Past Chair Craig Vander Zee, Program Officer Paul Keul, Member Services Officer Corina Weigl, Student Liaison Officer Daniel Dochylo, Governance Liaison Jeff Halpern, Sponsorship Officer Joan Jung, Newsletter Officer Chris Delaney, Ex-Officio (nonvoting) Members at Large: Harris Jones Ian Lebane Gillian Musk . STEP Toronto Presents... April 13, 2016 – Insurance in Estates and Trusts Looking at the practical use of life insurance in trusts and estate planning, including variation of a trust, pipeline planning, charitable donations - including redemption of private shares from a charity, leverage structures, and use of insurance in professional corporations. There will be a brief review of new budget proposals affecting life insurance planning. As well, a summary chart will be provided simplifying the changes and the impact on planning of the new exempt rules. Moderator: Harris Jones, CA, CFP, CLU, TEP: HarrisJones Advisory Inc Speakers Ted Polci, CLU, TEP: Partner, First York Chris Ireland, CA, TEP: Senior Vice-President, PPI Advisory Registration: :30 p.m. 2 Seminar: 3:00 p.m. – 5:00 p.m. Venue: Osgoode Hall, Donald Lamont Learning Centre, 130 Queen St West, Toronto Remote Sites: Wilson Vukelvich LLP Manulife Financial (Learn Room) Suite 710, 60 Columbia Way 600 Weber Street North Markham Kitchener-Waterloo Please note that at the remote sites (group webcast viewing), space is limited to room capacity. .

In case you missed it… Post-Mortem Planning – Private Corporation Shares On February 17, 2016, Michael Atlas, Chartered Accountant, and Brian Nichols, Speigel Nichols Fox LLP, along with moderator Joan Jung, Minden Gross LLP, discussed several issues surrounding private corporation shares in post-mortem planning. Michael began the seminar by giving an overview of various planning strategies including the use of subsection 164(6), pipelines and the paragraph 88(1)(d) bump. He then considered issues with non-resident beneficiaries of trusts including some suggested planning guidelines which can be accessed in the archived webcast link below. Video Link: Non-Resident Beneficiary Planning Guidelines Brian Nichols then discussed domestic pipeline issues, testamentary spousal trusts and subsection 104(13.4). Brian presented an interesting case study combining these and other post-mortem planning issues which can be accessed in the archived webcast link below. Video Link: Case Study Other Upcoming Events 2015/2016 REMAINING EDUCATION SESSIONS April 13, 2016 Insurance in Estates and Trusts May 18, 2016 Planning Using Trusts Further details can be found at: STEP.ca .

STEP Toronto Announces “BRING A GUEST” – COMPLIMENTARY to a STEP Toronto Educational Session. STEP Toronto is pleased to announce a special opportunity for members to share the benefits of STEP Toronto’s education program with colleagues who are potential members. STEP Toronto members registered for the program (or Passport holders) may bring a guest “compliments”. The following program sessions are eligible: April 13, 2016 - Insurance in Estates and Trusts May 18, 2016 - Planning Using Trusts Please register your guest (a non-member) by clicking on the link below. Let us know the name, firm and e-mail address of your guest and the program chosen so that he/she can be registered. Register My Guest - STEP Toronto Note: You may bring one different guest to each session . ARTICLE: Uncle Sam Follows Ex-U.S. Citizens and Green Card Holders – Even Past the Grave By: Carol A. Fitzsimmons, BA, JD, Partner, International Tax Practice Leader, Hodgson Russ LLP Many international practitioners are aware that U.S. citizens are taxed on their worldwide income and assets, under the U.S.

income, gift, estate and generation-skipping transfer tax regimes. Many are also aware that it is possible for a U.S. citizen to renounce U.S.

citizenship and remove himself or herself from the application of this worldwide income and asset taxation although for persons who are deemed to be “covered expatriates”, there is an “exit tax” (as well as potential acceleration of U.S. income tax on pension-related income, deferred compensation, stock options and the like). A covered expatriate is a person who has a net worth in excess of US$2M at the time of expatriation, or an average annual U.S.

federal tax liability for the prior five years of US$161,000 or has not complied with his or her U.S. tax obligations for the prior five years before expatriation. There are certain exceptions to covered expatriate status even if a U.S. citizen falls into one of the categories above, such as for persons renouncing before age 18 ½ and for persons born a dual citizen of the United States and the country in which they reside. Similar rules apply to “long term green card holders” who give up their green cards.

These persons can also be covered expatriates under the thresholds noted above. A long term green card holder is someone who has held a green card for more than 7 out of the prior 15 tax years. There is no “age 18 ½” or “dual citizen at birth” exception for long term green card holders, however. This expatriate regime for income tax purposes went into effect in 2008.

What many persons do not know, however, is that at the same time, Congress enacted an inheritance tax regime under Section 2801 of the Code that is applicable to the U.S. recipient of a gift or bequest from a covered expatriate. The Section 2801 tax applies at a 40% rate on the value of the gift or bequest. A gift or bequest from a covered expatriate on which inheritance tax is imposed also includes certain trusts (U.S.

trusts and “electing” foreign trusts). Recently, the IRS finally issued proposed regulations on this eight year old statute. The proposed regulations are quite detailed, and there are many provisions designed to address what might otherwise be techniques to avoid the inheritance tax rules – such as the covered expatriate leaving property to a foreign trust, which has U.S. beneficiaries.

Under the proposed regulations, the U.S. beneficiaries of such a trust are subject to the Section 2801 tax on distributions from the trust, unless the foreign trust elects to pay the Section 2801 tax “up front”. The inheritance tax has a particularly onerous feature to it, which is a very limited exclusion amount from the inheritance tax. Essentially, the U.S.

annual exclusion from gift tax (presently US$14,000 in . 2016) is the only exclusion that all recipients of gifts or bequests from covered expatriates are allowed to reduce the value subject to the inheritance tax. Thus, no use is allowed of the “lifetime” gift and estate tax unified credit, which provides an exemption of US$5.45M (in 2016), that would have applied to a non-expatriating U.S. citizen or U.S. domiciliary.

As a result, the inheritance tax is actually much worse than the U.S. gift and estate tax would have been had the covered expatriate remained a U.S. taxpayer. There are also a couple of fairly limited exclusions from the Section 2801 tax for certain transfers to a covered expatriate’s spouse if the spouse is a U.S.

citizen, and to charities. The proposed regulations set forth the reporting procedures for a U.S. person who receives a gift or bequest from a covered expatriate. There will be an IRS filing required on Form 708, once the proposed regulations are finalized.

The proposed regulations put the burden of ascertaining whether a gift or bequest was received from a covered expatriate on the U.S. recipient. While perhaps the IRS assumes that a beneficiary of a gift or bequest would know whether the person making the gift or bequest is a covered expatriate, that will not always be the case. It is important that practitioners who are counseling individuals who are U.S.

citizens or green card holders, and who may wish to change that status, take into account not only the more well-known U.S. income tax consequences of expatriation that may apply, but also the potential impact of the inheritance tax, particularly if there will be other persons in the individual’s family who will retain U.S. citizenship or green card status. Article: Life insurance and Budget 2016 – What’s changed? By: Hemal Balsara, CPA, CA, CFP, TEP, Assistant Vice President, Regional Tax, Retirement and Estate Planning Services, Manulife 1 The 2016 Federal Budget was presented on March 22, 2016. There were a variety of proposed changes to the existing tax rules.

Specifically, there were two measures proposed in the budget that relate to life insurance: 1. Capital dividend account (“CDA”) and life insurance proceeds 2. Transfers of life insurance policies to a corporation CDA and life insurance proceeds The Income Tax Act (“ITA”) provides that the death benefit from a life insurance policy is generally received tax free. In order to preserve this treatment when a private corporation is the recipient of a life insurance death benefit, the ITA provides that the corporation receives a credit to its CDA equal to the excess of the death benefit received over the adjusted cost basis (ACB) of the policy to that . corporation. Capital dividends can be paid by a private corporation to the extent of its CDA balance and are non-taxable in Canada to the shareholder. Prior to the budget some taxpayers were arranging their affairs in a manner that involved owning the life insurance policy in one corporation and having the beneficiary be another corporation. By structuring in this manner, the objective may have been to avoid the ACB reduction on the CDA credit and receive a full CDA credit for the death benefit of the life insurance policy. Some valid business reasons for this structure may have been for creditor protection and facilitating buy-sell planning as between operating companies and holding companies.

Due to the wording of the definition of CDA in subsection 89(1), the reduction in the CDA by the ACB only applied to the owner of the policy. The Canada Revenue Agency (“CRA”) has expressed concerns in the past with such arrangements. CRA indicated that where the primary objective of separating the ownership and beneficiary of the life insurance policy was to maximize CDA, the general anti-avoidance rule “GAAR” would apply to reduce the CDA credit by the ACB of the life insurance contract. The budget proposes to amend the ITA such that for deaths on or after March 22, 2016 the credit to the CDA will be reduced by the ACB of the policy regardless of who owns the policy.

This is being achieved by reducing the CDA credit by the ACB of “a policyholder’s interest in the policy” rather than the current language which reduces the CDA credit by the ACB of “the policy to the corporation”. A similar mechanism exists for partnerships to be able to distribute life insurance death benefits on a tax free basis, and a similar change is proposed to prevent this planning in the partnership context. As an enforcement mechanism, the budget also introduces an information reporting requirement applicable to a corporation or partnership that is not a policyholder or owner but is entitled to receive a policy benefit. The CRA has indicated in the past that it does not like splitting ownership and beneficiary in the corporate context and there may be income tax implications that result from such structures.

For example, in CRA’s view, where a subsidiary corporation is the owner and a parent corporation is the beneficiary, a shareholder benefit would apply to the parent corporation resulting in an income inclusion equal to the amount of premium. Similarly, where a parent corporation is the owner and premium payor of a policy and a subsidiary corporation is the beneficiary, there could be indirect benefits under 246(1) and income inclusions to the subsidiary corporation for the amount of the premiums. If the Parentco was reimbursed for the premiums by the subsidiary company, the impact of the indirect benefit to the subsidiary corporation would be reduced.

However, the reimbursement would create its own income inclusion to the parent corporation. This form will likely allow the CRA to better quantify and track these split ownership/beneficiary scenarios. Transfers of Life Insurance to a Corporation Transfers of a life insurance policy generally give rise to a taxable policy gain equal to the excess of the proceeds received over the policyholder’s ACB of the policy. There was a loophole in the pre2016 budget rules that allowed for tax arbitrage as it related to a sale of a life insurance policy by a shareholder to a non-arms length corporation.

The individual transferring the policy would be . deemed under the ITA to have sold the policy to the corporation for proceeds equal to the cash surrender value (“CSV”) of their interest in the policy and the corporation acquiring the policy would be deemed to have acquired the policy at that CSV. The only tax implications to the shareholder would be to report a fully taxable policy gain to the extent that the CSV of their interest in the policy exceeded the ACB of their interest in the policy. However, since the shareholder was contributing an asset that could have a fair market value (“FMV”) in excess of the CSV, the shareholder could receive this excess tax-free. The FMV of a life insurance policy should be determined by an independent actuary through a valuation report. Valuation reports take into account a variety of different factors including the cash surrender value of the policy, the policy loan value, the face value of the policy, the state of health of the insured, conversion privileges and the replacement value of a policy to determine the estimated FMV of a life insurance policy. Assume Mr X owns a Term-100 life insurance policy with a $500,000 death benefit and an ACB and CSV of zero.

The policy has been determined to have a fair market value of $100,000. Mr. X also owns 100% of X-Co and he transferred his policy to X-Co prior to March 22, 2016.

. Upon transfer, he would have been deemed to dispose of the contract at CSV. Since CSV and ACB are nil, there would be no income inclusion to Mr.

X. Under the previous rules he could extract $100,000 from the corporation tax-free as this excess was not taxable. The budget includes proposals that will prevent this planning in respect of transfers on or after March 22, 2016 by ensuring the proceeds from the sale for the purposes of the ITA are not less than the amount of the consideration received from the corporation. Coming back to Mr.

X, if he transferred the policy to his corporation, on or after March 22, 2016 and wants to extract fair market value, he will have a full ordinary income inclusion of $100,000. Meanwhile, X-Co will have a policy with an ACB of $100,000. This higher ACB could serve to reduce the ultimate CDA credit on death if the ACB is not fully reduced to nil by the time of death. The most surprising part of the budget related to policies that were transferred into a corporation prior to March 22, 2016.

In these cases, the budget proposes that any excess consideration received on the transfer over the proceeds used to determine the policy gain (i.e. CSV) will permanently reduce the CDA credit to the private corporation. This will impact transfers that have already occurred.

Coming back to Mr. X, let’s assume he had transferred the policy to X-Co prior to the budget and was able to extract $100,000 tax-free from the corporation. When Mr.

X ultimately passes away, the death benefit of $500,000 would be paid into the corporation, X-Co would receive a CDA credit for $400,000 ($500,000 less $100,000). In other words, a past transfer would forever reduce the CDA credit by the amount of the excess extracted above the CSV. Similar changes are proposed to prevent this planning in the partnership context. Experienced, Independent, Professional Advice. Ted Polci, CLU, TEP tedp@fyork.com 416-966-9675 . Exhibit 1 – Summary Table -Tax Implications to Mr. X on transfer of policy to X-Co. Assumptions for table: 1. A T-100 policy with a $500,000 death benefit is being used. 2. The ACB and CSV of the life insurance policy is zero. 3. The fair market value of the policy is $100,000 Summary Table Tax implications to transferor Proceeds ACB Policy Gain Tax-Free Amounts Tax Implications to Transferee ACB CDA Credit Pre Budget Post Budget Transfer in and death before March 22, 2016 Transfer in before and death after March 21, 2016 Transfer in and death after March 22, 2016 $0 $0 $100,000 $0 $0 $100,000 $100,000 $100,000 $0 $0 $0 $100,000 $500,000 $400,000 Somewhere between $400,000 and $500,000 $0 $0 0 --1. The author would like to thank his colleagues Joel Campagna, CPA, CMA, CFP, TEP and Nick Fabiano CPA, CA of Manulife’s Tax, Retirement and Estate Planning Services Team for their assistance with this article. . ARTICLE: In Grocery Bags and Under Pads of Paper: The Validity of a Found Holograph Codicil By: Kimberly A. Whaley, CS, TEP, LLM, Principal, Whaley Estate Litigation “If the Testatrix considered a Sobey’s bag appropriate for storing her Will, then it stands to reason that the location of the Codicil on a ledge in the apartment does not detract from the analysis as to whether the Codicil was intended to be a testamentary document.” ~ Justice Marshall In King Estate v Hiscock, 2015 NLTD(G) 173, the Newfoundland Supreme Court Trial Division considered whether a handwritten codicil left folded under a pad of paper on a ledge in the apartment of the deceased was a valid testamentary document. The Court examined two issues: 1) was the Codicil testamentary in nature or only “deliberative or initiatory” and 2) was the Codicil validly signed? Background The deceased, Cynthia J. King, drafted a valid holograph Will in 2002.

She named an executrix under the Will and advised her of its existence. The executrix searched for the Will after the testatrix had died and found it in a card sized envelope with other unrelated papers in a plastic Sobey’s shopping bag, within a garbage bag. Later, when the executrix was cleaning out the deceased’s apartment she was making a note on a pad of paper located on a ledge where the deceased kept her telephone, when she discovered a second document, folded in half, under the pad of paper.

It was the alleged Codicil. The Codicil was entirely hand written by the deceased and was dated May 8, 2012 (just over a month before her death). The executrix submitted it for probate along with the holograph Will. The defendant in this matter, a sibling of the deceased, was not aware of the Codicil until after it had been probated. The defendant brought a motion to revoke the order of probate for the codicil, arguing that it was not valid under the Wills Act RSNL 1990, c.

W-10. The Codicil was a simple two page document that reflected a different distribution than the Will. One example: the Will provided that a property was to be sold and divided equally between two siblings while the Codicil indicated that the property was to be sold and the proceeds left to only one sibling. The Codicil was also unsigned but the deceased had written her name several times in the body of the Codicil (i.e. “For Cynthia J.

King’s Estate”, “I; Cynthia J. King. .

.says for my estate” and “Cynthia J. King says ‘Yes’ to what I have written here”. Furthermore, the testatrix had written at the bottom of the Codicil, “Witness: Jean Asernault [sic] – Cynthia King’s Best Friend”.

There was, however, no signature from Jean Arsenault. The Analysis: Justice Marshall first noted that even if the Codicil was properly executed its probate should be revoked if the Codicil “was only deliberative or initiatory”.1 In other words, if it does not show the testatrix’s final intention it should not be admitted to probate. If it merely expresses an intention to instruct a solicitor to prepare a will or her intention to draft a subsequent holograph will, it is not testamentary in nature. The defendant argued that the Codicil was merely a plan or notes about the contents of a subsequent will which was never made. It was not witnessed or signed by the deceased.

If it was supposed to be such an important document it would have been in a more secure spot than under a pad of paper on a ledge in her apartment. 1 2015 NLTD(G) 173 at para. 41. . But Justice Marshall noted that the deceased had kept her Will in a Sobey’s bag. The Sobey’s bag was also not a secure place: “The facts are that the Codicil existed; it was not discarded; and it was in a location where it could be, and was, found.”2 Considering also that a witness’s signature was not required on the holograph codicil, the fact that the witness’s signature was not obtained does not lead to the conclusion that the Codicil was “deliberative or initiatory” particularly where the contents of the entire Codicil are examined to determine if there is a disposing effect. Also, the deceased had used phrases such as “This is my wish & my Request” and “I; Cynthia J. King …says for my estate to do the following” which were indicative of the deceased’s intention as to the disposal of her property upon her death. Justice Marshall concluded that the Codicil was indeed a “deliberate or fixed and final expression” of the deceased’s intention and concluded that “the Codicil is not invalid due to Ms.

King not specifically referring to an executrix, the residue, the previous will, or the word “bequest”. The Codicil clearly described Ms. King’s intent as to the disposal of her property upon death and revoked only the inconsistent portions of the Will.3 But was it validly signed? It was clear that the deceased had not signed the document in a stand-alone fashion, either at the beginning or end of the document.

However, the deceased had signed her name multiple times within the body. Justice Marshall summarized: [i]t would be unjust to defeat the clear intentions of the Testatrix simply on the basis that none of her signatures, as contained in the Codicil, were ascribed on a stand-alone basis. Specifically, Ms.

King’s signature is contained in the first and last lines of the Codicil; and either of these lines was written last by the Testatrix. In my view, whichever of these lines was written last, such line constitutes an authentication of the Codicil. These lines should be considered in the context of the confirmatory middle sentence.

As stated, the signature in the middle sentence could also be deemed as the act of execution necessary to “breathe the life of intention” (Oliver Estate, (1993), 106 Nfld. & P.E.I.R. 32, (Nfld.

T.D.), aff’d (1994), 124 Nfld. & P.E.I.R. 294 (Nfld.

C.A.) at paragraph 42) into the document. Justice Marshall determined that the Codicil was validly executed. Concluding Comments While valid holograph wills are indeed proper testamentary documents, they are not without their complications, as this case evidences. It is surprising the number of people who rely on holograph wills - perhaps they wish to avoid lawyer’s fees or feel that their estate is simple enough to deal with themselves. However, the issues with holograph wills are numerous, including ambiguities and errors, failure to dispose of the entire estate, failure to name an executor, etc.

or they can easily go missing or not be found at all if the testator fails to tell anyone that the will exists or where it can be found. Spending a little money up front to get a properly drafted Will will likely save a lot of wasted court fees in the long run. 2 3 Ibid at para. 49. Ibid at para. 71. .

About Connection Please note that each advertiser is linked to their web page (as are our program sponsors on the last page). Please click through to their web pages to learn more about each of our sponsors and advertisers. STEP Toronto publishes ‘Connection’ for our membership 6-7 times per year between September and May. We welcome your feedback and contributions. Please send any comments or inquiries to Joan Jung jjung@mindengross.com. Letters, announcements, opinions, comments from members If you have an article or an idea that would be of interest to other members of STEP, please send them to paul.keul@scpllp.com for inclusion in our next edition of the STEP Toronto Connection. STEP continues to grow and we welcome membership inquires.

As a reminder, there are three routes to full membership; one based on experience (Experienced Practitioner) and two education routes (essay or exam). If you know anyone who would be a good candidate for STEP membership, please direct them to the STEP Canada website for information. Connection Newsletter Contacts Joan Jung – jjung@mindengross.com Paul Keul – paul.keul@scpllp.com Nicole Hastings – nhastings@millerthomson.com Teresa F. Lee - teresa@leewillsandestates.ca Program Sponsors PREMIER SPONSORS EVENT SPONSORS SUPPORTING SPONSORS de VRIES LITIGATION LLP, PPI Advisory, Thorsteinssons LLP Connection STEP Toronto Newsletter - April 2016, Vol.

3 No. 6 .