E&P Top 10 Bankruptcy Cases, which includes a list of the top 10 oil and gas bankruptcy cases since the beginning of 2015 - April 18, 2016

Haynes and Boone

Description

E&P TOP 10

CASES

Energy Bankruptcy Reports and Surveys

Summaries from Haynes and Boone, LLP

APRIL 2016 | ISSUE 01

CLICK HERE TO DOWNLOAD

THE LATEST

Oil Patch

Bankruptcy Monitor

CLICK HERE TO DOWNLOAD

THE LATEST

Oilfield Services

Bankruptcy Tracker

CLICK HERE TO DOWNLOAD

THE LATEST

Borrowing Base

Redeterminations Survey

HAYNESBOONE.COM

Austin Chicago Dallas Denver Fort Worth Houston Mexico City New York Orange County Palo Alto Richardson

San Antonio Shanghai Washington, D.C.

© 2016 Haynes and Boone, LLP

. E&P TOP 10

CASES

THE TOP TEN CASES

Samson

Resources

Corporation

Sabine Oil &

Gas Corp.

Magnum Hunter

Resources

Corporation

Swift Energy

Company

(Southern

District of

New York)

(Delaware)

Quicksilver

Resources

(Delaware)

(Delaware)

Energy &

Exploration

Partners, Inc.

Milagro

Oil & Gas

Venoco, Inc.

New Gulf

Resources, LLC

ERG Operating

Company, LLC

(Delaware)

(Northern

District of Texas)

(Delaware)

(Delaware)

(Delaware)

KEY STATISTICS

OF THE TOP TEN

(Northern

District of Texas)

TOTAL DEBT*

Approximately

$16.1billion

4

10

Four of the ten

pursued a sale pursuant

to section 363 of the

Bankruptcy Code

6

5

10

10

*”Total debt” information for each case is derived from the debtor’s summary of assets and

liabilities, if available. Specific amounts for various types of debt are generally obtained

from first day declarations filed in support of the bankruptcy petitions.

Six of the ten filed for chapter

11 with restructuring support

agreements in place

Five of the ten

sought post-petition

financing (“DIP Loans”)

Total DIP Loans: Approximately

$425 million

© 2016 Haynes and Boone, LLP

. E&P TOP 10

CASES

1

1

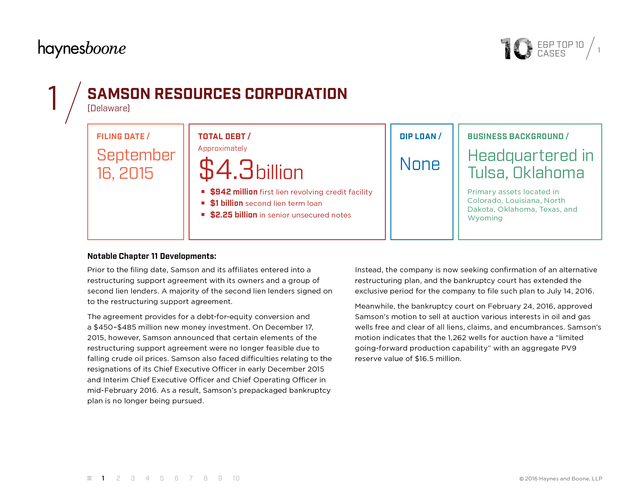

SAMSON RESOURCES CORPORATION

(Delaware)

FILING DATE

TOTAL DEBT

September

16, 2015

Approximately

$4.3  illion

b

DIP LOAN

None

$942 million first lien revolving credit facility

$1 billion second lien term loan

$2.25 billion in senior unsecured notes

BUSINESS BACKGROUND

Headquartered in

Tulsa, Oklahoma

Primary assets located in

Colorado, Louisiana, North

Dakota, Oklahoma, Texas, and

Wyoming

Notable Chapter 11 Developments:

Prior to the filing date, Samson and its affiliates entered into a

restructuring support agreement with its owners and a group of

second lien lenders. A majority of the second lien lenders signed on

to the restructuring support agreement.

The agreement provides for a debt-for-equity conversion and

a $450–$485 million new money investment. On December 17,

2015, however, Samson announced that certain elements of the

restructuring support agreement were no longer feasible due to

falling crude oil prices. Samson also faced difficulties relating to the

resignations of its Chief Executive Officer in early December 2015

and Interim Chief Executive Officer and Chief Operating Officer in

mid-February 2016.

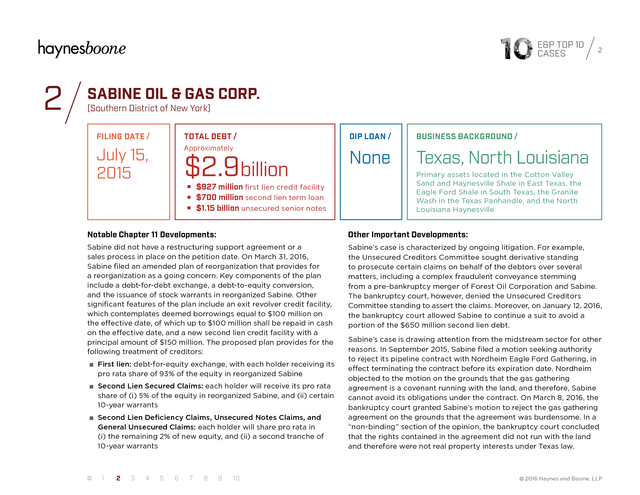

As a result, Samson’s prepackaged bankruptcy plan is no longer being pursued. 1 2 3 4 5 6 7 8 9 10 Instead, the company is now seeking confirmation of an alternative restructuring plan, and the bankruptcy court has extended the exclusive period for the company to file such plan to July 14, 2016. Meanwhile, the bankruptcy court on February 24, 2016, approved Samson's motion to sell at auction various interests in oil and gas wells free and clear of all liens, claims, and encumbrances. Samson’s motion indicates that the 1,262 wells for auction have a “limited going-forward production capability” with an aggregate PV9 reserve value of $16.5 million. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 2 2 SABINE OIL & GAS CORP. (Southern District of New York) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND July 15, 2015 Approximately None Texas, North Louisiana $2.9  illion b $927 million first lien credit facility $700 million second lien term loan $1.15 billion unsecured senior notes Primary assets located in the Cotton Valley Sand and Haynesville Shale in East Texas, the Eagle Ford Shale in South Texas, the Granite Wash in the Texas Panhandle, and the North Louisiana Haynesville Notable Chapter 11 Developments: Other Important Developments: Sabine did not have a restructuring support agreement or a sales process in place on the petition date. On March 31, 2016, Sabine filed an amended plan of reorganization that provides for a reorganization as a going concern. Key components of the plan include a debt-for-debt exchange, a debt-to-equity conversion, and the issuance of stock warrants in reorganized Sabine. Other significant features of the plan include an exit revolver credit facility, which contemplates deemed borrowings equal to $100 million on the effective date, of which up to $100 million shall be repaid in cash on the effective date, and a new second lien credit facility with a principal amount of $150 million.

The proposed plan provides for the following treatment of creditors: Sabine’s case is characterized by ongoing litigation. For example, the Unsecured Creditors Committee sought derivative standing to prosecute certain claims on behalf of the debtors over several matters, including a complex fraudulent conveyance stemming from a pre-bankruptcy merger of Forest Oil Corporation and Sabine. The bankruptcy court, however, denied the Unsecured Creditors Committee standing to assert the claims. Moreover, on January 12, 2016, the bankruptcy court allowed Sabine to continue a suit to avoid a portion of the $650 million second lien debt. First lien: debt-for-equity exchange, with each holder receiving its pro rata share of 93% of the equity in reorganized Sabine Second Lien Secured Claims: each holder will receive its pro rata share of (i) 5% of the equity in reorganized Sabine, and (ii) certain 10-year warrants Second Lien Deficiency Claims, Unsecured Notes Claims, and General Unsecured Claims: each holder will share pro rata in (i) the remaining 2% of new equity, and (ii) a second tranche of 10-year warrants 1 2 3 4 5 6 7 8 9 10 Sabine’s case is drawing attention from the midstream sector for other reasons.

In September 2015, Sabine filed a motion seeking authority to reject its pipeline contract with Nordheim Eagle Ford Gathering, in effect terminating the contract before its expiration date. Nordheim objected to the motion on the grounds that the gas gathering agreement is a covenant running with the land, and therefore, Sabine cannot avoid its obligations under the contract. On March 8, 2016, the bankruptcy court granted Sabine’s motion to reject the gas gathering agreement on the grounds that the agreement was burdensome.

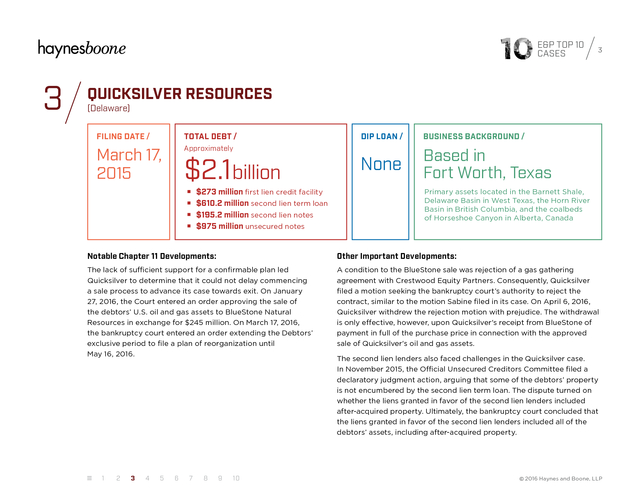

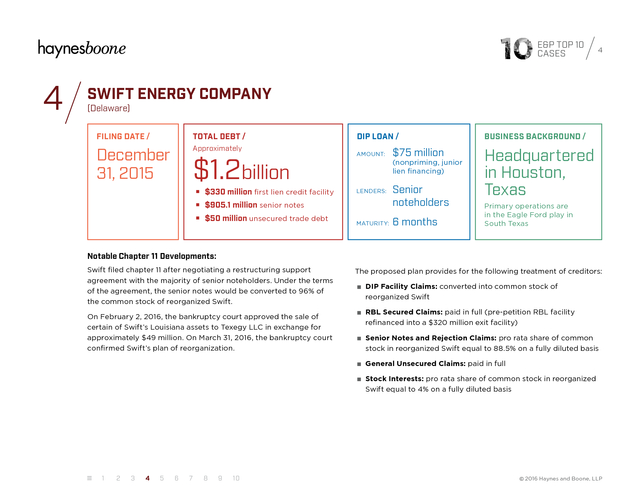

In a “non-binding” section of the opinion, the bankruptcy court concluded that the rights contained in the agreement did not run with the land and therefore were not real property interests under Texas law. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 3 3 QUICKSILVER RESOURCES (Delaware) FILING DATE TOTAL DEBT March 17, 2015 Approximately DIP LOAN $2.1  illion b $273 million first lien credit facility $610.2 million second lien term loan $195.2 million second lien notes $975 million unsecured notes BUSINESS BACKGROUND None Based in Fort Worth, Texas Primary assets located in the Barnett Shale, Delaware Basin in West Texas, the Horn River Basin in British Columbia, and the coalbeds of Horseshoe Canyon in Alberta, Canada Notable Chapter 11 Developments: Other Important Developments: The lack of sufficient support for a confirmable plan led Quicksilver to determine that it could not delay commencing a sale process to advance its case towards exit. On January 27, 2016, the Court entered an order approving the sale of the debtors’ U.S. oil and gas assets to BlueStone Natural Resources in exchange for $245 million. On March 17, 2016, the bankruptcy court entered an order extending the Debtors’ exclusive period to file a plan of reorganization until May 16, 2016. A condition to the BlueStone sale was rejection of a gas gathering agreement with Crestwood Equity Partners.

Consequently, Quicksilver filed a motion seeking the bankruptcy court’s authority to reject the contract, similar to the motion Sabine filed in its case. On April 6, 2016, Quicksilver withdrew the rejection motion with prejudice. The withdrawal is only effective, however, upon Quicksilver's receipt from BlueStone of payment in full of the purchase price in connection with the approved sale of Quicksilver's oil and gas assets. 1 2 3 4 5 6 7 8 9 10 The second lien lenders also faced challenges in the Quicksilver case. In November 2015, the Official Unsecured Creditors Committee filed a declaratory judgment action, arguing that some of the debtors’ property is not encumbered by the second lien term loan.

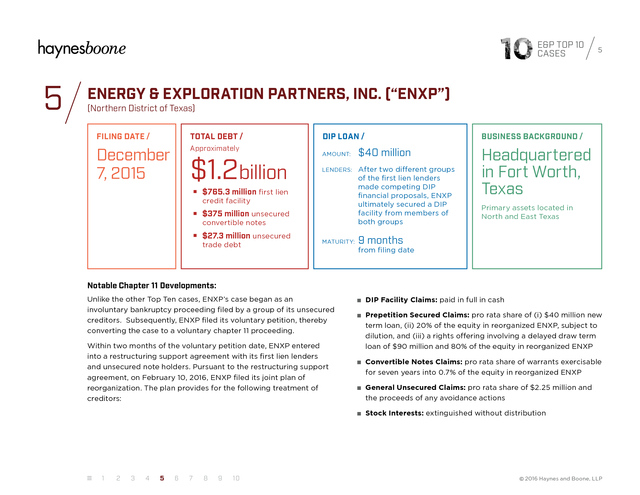

The dispute turned on whether the liens granted in favor of the second lien lenders included after-acquired property. Ultimately, the bankruptcy court concluded that the liens granted in favor of the second lien lenders included all of the debtors’ assets, including after-acquired property. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 4 4 SWIFT ENERGY COMPANY (Delaware) FILING DATE TOTAL DEBT December 31, 2015 Approximately $1.2 billion $330 million first lien credit facility DIP LOAN AMOUNT: (nonpriming, junior lien financing) LENDERS: $905.1 million senior notes $50 million unsecured trade debt $75 million MATURITY: Senior noteholders 6 months BUSINESS BACKGROUND Headquartered in Houston, Texas Primary operations are in the Eagle Ford play in South Texas Notable Chapter 11 Developments: Swift filed chapter 11 after negotiating a restructuring support agreement with the majority of senior noteholders. Under the terms of the agreement, the senior notes would be converted to 96% of the common stock of reorganized Swift. On February 2, 2016, the bankruptcy court approved the sale of certain of Swift’s Louisiana assets to Texegy LLC in exchange for approximately $49 million. On March 31, 2016, the bankruptcy court confirmed Swift’s plan of reorganization. The proposed plan provides for the following treatment of creditors: DIP Facility Claims: converted into common stock of reorganized Swift RBL Secured Claims: paid in full (pre-petition RBL facility refinanced into a $320 million exit facility) Senior Notes and Rejection Claims: pro rata share of common stock in reorganized Swift equal to 88.5% on a fully diluted basis General Unsecured Claims: paid in full Stock Interests: pro rata share of common stock in reorganized Swift equal to 4% on a fully diluted basis 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 5 5 ENERGY & EXPLORATION PARTNERS, INC. (“ENXP”) (Northern District of Texas) FILING DATE TOTAL DEBT December 7, 2015 Approximately $1.2  illion b DIP LOAN AMOUNT: LENDERS: $765.3 million first lien credit facility $375 million unsecured convertible notes $27.3 million unsecured trade debt MATURITY: BUSINESS BACKGROUND $40 million After two different groups of the first lien lenders made competing DIP financial proposals, ENXP ultimately secured a DIP facility from members of both groups Headquartered in Fort Worth, Texas Primary assets located in North and East Texas 9 months from filing date Notable Chapter 11 Developments: Unlike the other Top Ten cases, ENXP’s case began as an involuntary bankruptcy proceeding filed by a group of its unsecured creditors. Subsequently, ENXP filed its voluntary petition, thereby converting the case to a voluntary chapter 11 proceeding. Within two months of the voluntary petition date, ENXP entered into a restructuring support agreement with its first lien lenders and unsecured note holders. Pursuant to the restructuring support agreement, on February 10, 2016, ENXP filed its joint plan of reorganization.

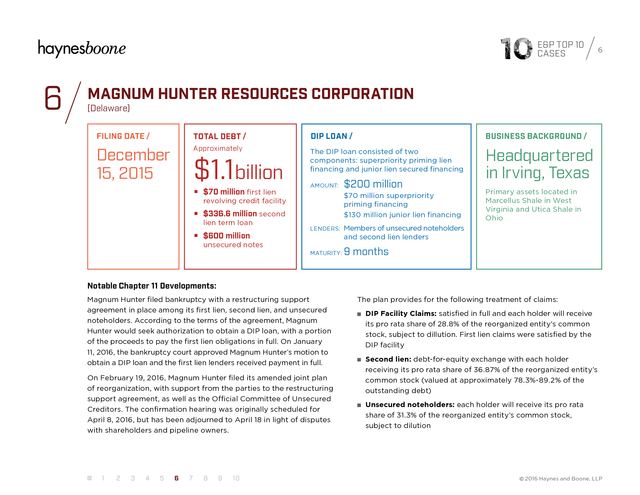

The plan provides for the following treatment of creditors: DIP Facility Claims: paid in full in cash Prepetition Secured Claims: pro rata share of (i) $40 million new term loan, (ii) 20% of the equity in reorganized ENXP, subject to dilution, and (iii) a rights offering involving a delayed draw term loan of $90 million and 80% of the equity in reorganized ENXP Convertible Notes Claims: pro rata share of warrants exercisable for seven years into 0.7% of the equity in reorganized ENXP General Unsecured Claims: pro rata share of $2.25 million and the proceeds of any avoidance actions Stock Interests: extinguished without distribution 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 6 6 MAGNUM HUNTER RESOURCES CORPORATION (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND December 15, 2015 Approximately The DIP loan consisted of two components: superpriority priming lien financing and junior lien secured financing Headquartered in Irving, Texas $1.1  illion b $70 million first lien revolving credit facility $336.6 million second lien term loan $600 million AMOUNT: $200 million $70 million superpriority priming financing $130 million junior lien financing Primary assets located in Marcellus Shale in West Virginia and Utica Shale in Ohio LENDERS: Members of unsecured noteholders and second lien lenders unsecured notes MATURITY: 9 months Notable Chapter 11 Developments: Magnum Hunter filed bankruptcy with a restructuring support agreement in place among its first lien, second lien, and unsecured noteholders. According to the terms of the agreement, Magnum Hunter would seek authorization to obtain a DIP loan, with a portion of the proceeds to pay the first lien obligations in full. On January 11, 2016, the bankruptcy court approved Magnum Hunter’s motion to obtain a DIP loan and the first lien lenders received payment in full. On February 19, 2016, Magnum Hunter filed its amended joint plan of reorganization, with support from the parties to the restructuring support agreement, as well as the Official Committee of Unsecured Creditors. The confirmation hearing was originally scheduled for April 8, 2016, but has been adjourned to April 18 in light of disputes with shareholders and pipeline owners. 1 2 3 4 5 6 7 8 9 10 The plan provides for the following treatment of claims: DIP Facility Claims: satisfied in full and each holder will receive its pro rata share of 28.8% of the reorganized entity's common stock, subject to dillution.

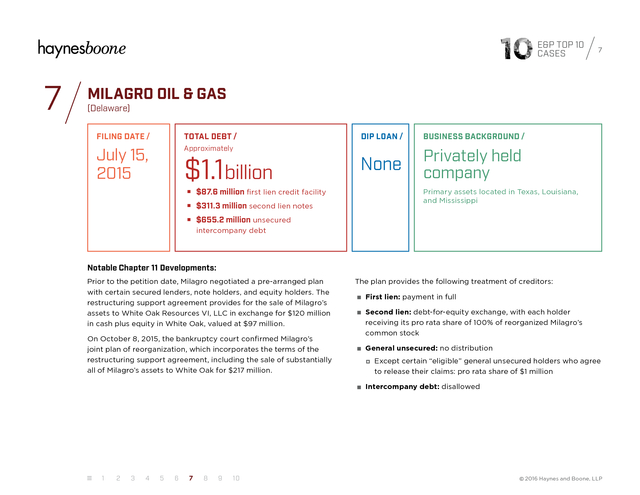

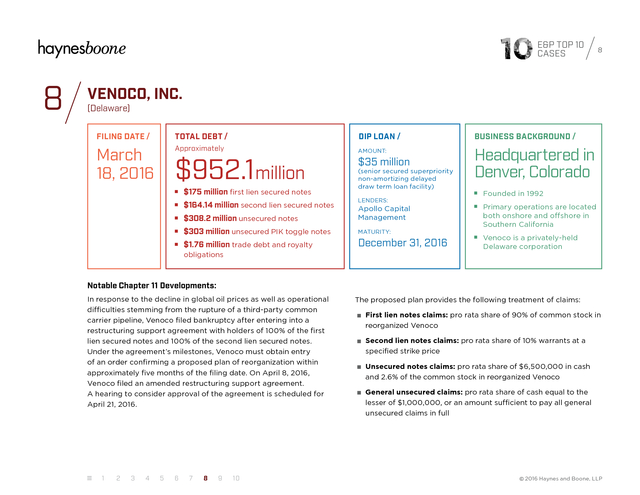

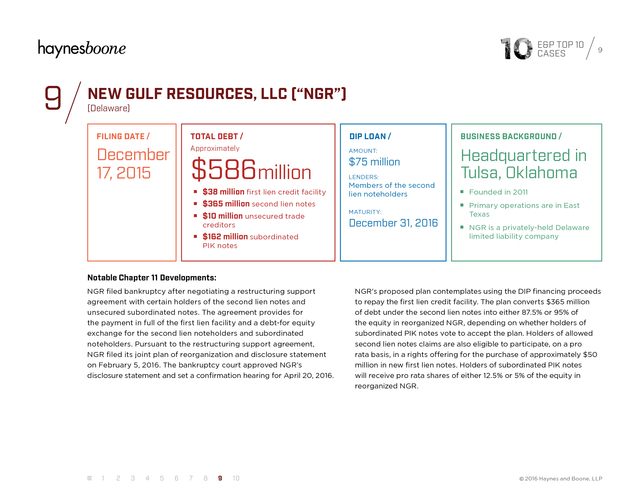

First lien claims were satisfied by the DIP facility Second lien: debt-for-equity exchange with each holder receiving its pro rata share of 36.87% of the reorganized entity’s common stock (valued at approximately 78.3%-89.2% of the outstanding debt) Unsecured noteholders: each holder will receive its pro rata share of 31.3% of the reorganized entity’s common stock, subject to dilution © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 7 7 MILAGRO OIL & GAS (Delaware) FILING DATE TOTAL DEBT July 15, 2015 Approximately DIP LOAN $1.1  illion b $87.6 million first lien credit facility $311.3 million second lien notes BUSINESS BACKGROUND None Privately held company Primary assets located in Texas, Louisiana, and Mississippi $655.2 million unsecured intercompany debt Notable Chapter 11 Developments: Prior to the petition date, Milagro negotiated a pre-arranged plan with certain secured lenders, note holders, and equity holders. The restructuring support agreement provides for the sale of Milagro’s assets to White Oak Resources VI, LLC in exchange for $120 million in cash plus equity in White Oak, valued at $97 million. On October 8, 2015, the bankruptcy court confirmed Milagro’s joint plan of reorganization, which incorporates the terms of the restructuring support agreement, including the sale of substantially all of Milagro’s assets to White Oak for $217 million. The plan provides the following treatment of creditors: First lien: payment in full Second lien: debt-for-equity exchange, with each holder receiving its pro rata share of 100% of reorganized Milagro’s common stock General unsecured: no distribution Except certain “eligible” general unsecured holders who agree to release their claims: pro rata share of $1 million Intercompany debt: disallowed 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 8 8 VENOCO, INC. (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND March 18, 2016 Approximately AMOUNT: Headquartered in Denver, Colorado $952.1  illion m $175 million first lien secured notes $164.14 million second lien secured notes $35 million (senior secured superpriority non-amortizing delayed draw term loan facility) LENDERS: $308.2 million unsecured notes Apollo Capital Management $303 million unsecured PIK toggle notes MATURITY: $1.76 million trade debt and royalty obligations December 31, 2016 Founded in 1992 Primary operations are located both onshore and offshore in Southern California Venoco is a privately-held Delaware corporation Notable Chapter 11 Developments: In response to the decline in global oil prices as well as operational difficulties stemming from the rupture of a third-party common carrier pipeline, Venoco filed bankruptcy after entering into a restructuring support agreement with holders of 100% of the first lien secured notes and 100% of the second lien secured notes. Under the agreement’s milestones, Venoco must obtain entry of an order confirming a proposed plan of reorganization within approximately five months of the filing date. On April 8, 2016, Venoco filed an amended restructuring support agreement. A hearing to consider approval of the agreement is scheduled for April 21, 2016. 1 2 3 4 5 6 7 8 9 10 The proposed plan provides the following treatment of claims: First lien notes claims: pro rata share of 90% of common stock in reorganized Venoco Second lien notes claims: pro rata share of 10% warrants at a specified strike price Unsecured notes claims: pro rata share of $6,500,000 in cash and 2.6% of the common stock in reorganized Venoco General unsecured claims: pro rata share of cash equal to the lesser of $1,000,000, or an amount sufficient to pay all general unsecured claims in full © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 9 9 NEW GULF RESOURCES, LLC (“NGR”) (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND December 17, 2015 Approximately AMOUNT: Headquartered in Tulsa, Oklahoma $586 million $38 million first lien credit facility $365 million second lien notes $10 million unsecured trade creditors $162 million subordinated $75 million LENDERS: Members of the second lien noteholders MATURITY: December 31, 2016 Founded in 2011 Primary operations are in East Texas NGR is a privately-held Delaware limited liability company PIK notes Notable Chapter 11 Developments: NGR filed bankruptcy after negotiating a restructuring support agreement with certain holders of the second lien notes and unsecured subordinated notes. The agreement provides for the payment in full of the first lien facility and a debt-for equity exchange for the second lien noteholders and subordinated noteholders. Pursuant to the restructuring support agreement, NGR filed its joint plan of reorganization and disclosure statement on February 5, 2016. The bankruptcy court approved NGR’s disclosure statement and set a confirmation hearing for April 20, 2016. 1 2 3 4 5 6 7 8 9 10 NGR's proposed plan contemplates using the DIP financing proceeds to repay the first lien credit facility.

The plan converts $365 million of debt under the second lien notes into either 87.5% or 95% of the equity in reorganized NGR, depending on whether holders of subordinated PIK notes vote to accept the plan. Holders of allowed second lien notes claims are also eligible to participate, on a pro rata basis, in a rights offering for the purchase of approximately $50 million in new first lien notes. Holders of subordinated PIK notes will receive pro rata shares of either 12.5% or 5% of the equity in reorganized NGR. © 2016 Haynes and Boone, LLP .

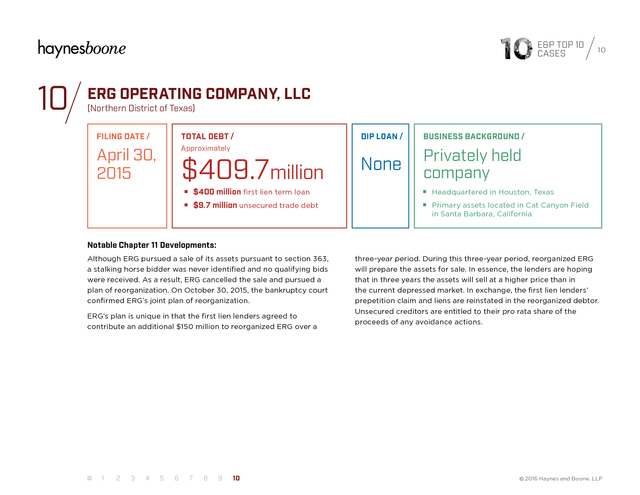

E&P TOP 10 CASES 10 10 ERG OPERATING COMPANY, LLC (Northern District of Texas) FILING DATE TOTAL DEBT April 30, 2015 Approximately DIP LOAN $409.7 million BUSINESS BACKGROUND None Privately held company $400 million first lien term loan Headquartered in Houston, Texas $9.7 million unsecured trade debt Primary assets located in Cat Canyon Field in Santa Barbara, California Notable Chapter 11 Developments: Although ERG pursued a sale of its assets pursuant to section 363, a stalking horse bidder was never identified and no qualifying bids were received. As a result, ERG cancelled the sale and pursued a plan of reorganization. On October 30, 2015, the bankruptcy court confirmed ERG’s joint plan of reorganization. ERG’s plan is unique in that the first lien lenders agreed to contribute an additional $150 million to reorganized ERG over a 1 2 3 4 5 6 7 8 9 10 three-year period. During this three-year period, reorganized ERG will prepare the assets for sale.

In essence, the lenders are hoping that in three years the assets will sell at a higher price than in the current depressed market. In exchange, the first lien lenders’ prepetition claim and liens are reinstated in the reorganized debtor. Unsecured creditors are entitled to their pro rata share of the proceeds of any avoidance actions. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES * Haynes and Boone has more than 575 lawyers, including more than 30 bankruptcy practitioners, serving clients across the country. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES LOCATIONS AUSTIN CHICAGO DALLAS DENVER FORT WORTH 600 Congress Avenue Suite 1300 Austin, TX 78701 United States of America T +1 512.867.8400 F +1 512.867.8470 180 N. LaSalle Street Suite 2215 Chicago, IL 60601 United States of America T +1 312.216.1620 F +1 312.216.1621 2323 Victory Avenue Suite 700 Dallas, TX 75219 United States of America T +1 214.651.5000 F +1 214.651.5940 1801 Broadway Street Suite 800 Denver, CO 80202 United States of America T +1 303.382.6200 F +1 303.382.6210 301 Commerce Street Suite 2600 Fort Worth, TX 76102 United States of America T +1 817.347.6600 F +1 817.347.6650 HOUSTON MEXICO CITY NEW YORK ORANGE COUNTY PALO ALTO 1221 McKinney Street Suite 2100 Houston, TX 77010 United States of America T +1 713.547.2000 F +1 713.547.2600 Torre Esmeralda I, Blvd. Manuel Ávila Camacho #40 Despacho 1601 Col. Lomas de Chapultepec, DF 11000 Mexico City, Mexico T +52.55.5249.1800 F +52.55.5249.1801 30 Rockefeller Plaza 26th Floor New York, NY 10112 United States of America T +1 212.659.7300 F +1 212.918.8989 600 Anton Boulevard Suite 700 Costa Mesa, CA 92626 United States of America T +1 949.202.3000 F +1 949.202.3001 525 University Avenue Suite 400 Palo Alto, CA 94301 United States of America T +1 650.687.8800 F +1 650.687.8801 RICHARDSON SAN ANTONIO SHANGHAI WASHINGTON, D.C. 2505 North Plano Road Suite 4000 Richardson, TX 75082 United States of America T +1 972.739.6900 F +1 972.680.7551 112 East Pecan Street Suite 1200 San Antonio, TX 78205 United States of America T +1 210.978.7000 F +1 210.978.7450 Shanghai International Finance Center, Tower 2 Unit 3620, Level 36 8 Century Avenue, Pudong Shanghai 200120, P.R. China T +86.21.6062.6179 F +86.21.6062.6347 800 17th Street, NW Suite 500 Washington, D.C.

20006 United States of America T +1 202.654.4500 F +1 202.654.4501 © 2016 Haynes and Boone, LLP . Haynes and Boone, LLP logo size: 2.5”(width) This publication is for informational purposes only and is not intended to be legal advice and does not establish an attorney-client relationship. Legal advice of any nature should be sought from legal counsel. © 2016 Haynes and Boone, LLP .

As a result, Samson’s prepackaged bankruptcy plan is no longer being pursued. 1 2 3 4 5 6 7 8 9 10 Instead, the company is now seeking confirmation of an alternative restructuring plan, and the bankruptcy court has extended the exclusive period for the company to file such plan to July 14, 2016. Meanwhile, the bankruptcy court on February 24, 2016, approved Samson's motion to sell at auction various interests in oil and gas wells free and clear of all liens, claims, and encumbrances. Samson’s motion indicates that the 1,262 wells for auction have a “limited going-forward production capability” with an aggregate PV9 reserve value of $16.5 million. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 2 2 SABINE OIL & GAS CORP. (Southern District of New York) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND July 15, 2015 Approximately None Texas, North Louisiana $2.9  illion b $927 million first lien credit facility $700 million second lien term loan $1.15 billion unsecured senior notes Primary assets located in the Cotton Valley Sand and Haynesville Shale in East Texas, the Eagle Ford Shale in South Texas, the Granite Wash in the Texas Panhandle, and the North Louisiana Haynesville Notable Chapter 11 Developments: Other Important Developments: Sabine did not have a restructuring support agreement or a sales process in place on the petition date. On March 31, 2016, Sabine filed an amended plan of reorganization that provides for a reorganization as a going concern. Key components of the plan include a debt-for-debt exchange, a debt-to-equity conversion, and the issuance of stock warrants in reorganized Sabine. Other significant features of the plan include an exit revolver credit facility, which contemplates deemed borrowings equal to $100 million on the effective date, of which up to $100 million shall be repaid in cash on the effective date, and a new second lien credit facility with a principal amount of $150 million.

The proposed plan provides for the following treatment of creditors: Sabine’s case is characterized by ongoing litigation. For example, the Unsecured Creditors Committee sought derivative standing to prosecute certain claims on behalf of the debtors over several matters, including a complex fraudulent conveyance stemming from a pre-bankruptcy merger of Forest Oil Corporation and Sabine. The bankruptcy court, however, denied the Unsecured Creditors Committee standing to assert the claims. Moreover, on January 12, 2016, the bankruptcy court allowed Sabine to continue a suit to avoid a portion of the $650 million second lien debt. First lien: debt-for-equity exchange, with each holder receiving its pro rata share of 93% of the equity in reorganized Sabine Second Lien Secured Claims: each holder will receive its pro rata share of (i) 5% of the equity in reorganized Sabine, and (ii) certain 10-year warrants Second Lien Deficiency Claims, Unsecured Notes Claims, and General Unsecured Claims: each holder will share pro rata in (i) the remaining 2% of new equity, and (ii) a second tranche of 10-year warrants 1 2 3 4 5 6 7 8 9 10 Sabine’s case is drawing attention from the midstream sector for other reasons.

In September 2015, Sabine filed a motion seeking authority to reject its pipeline contract with Nordheim Eagle Ford Gathering, in effect terminating the contract before its expiration date. Nordheim objected to the motion on the grounds that the gas gathering agreement is a covenant running with the land, and therefore, Sabine cannot avoid its obligations under the contract. On March 8, 2016, the bankruptcy court granted Sabine’s motion to reject the gas gathering agreement on the grounds that the agreement was burdensome.

In a “non-binding” section of the opinion, the bankruptcy court concluded that the rights contained in the agreement did not run with the land and therefore were not real property interests under Texas law. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 3 3 QUICKSILVER RESOURCES (Delaware) FILING DATE TOTAL DEBT March 17, 2015 Approximately DIP LOAN $2.1  illion b $273 million first lien credit facility $610.2 million second lien term loan $195.2 million second lien notes $975 million unsecured notes BUSINESS BACKGROUND None Based in Fort Worth, Texas Primary assets located in the Barnett Shale, Delaware Basin in West Texas, the Horn River Basin in British Columbia, and the coalbeds of Horseshoe Canyon in Alberta, Canada Notable Chapter 11 Developments: Other Important Developments: The lack of sufficient support for a confirmable plan led Quicksilver to determine that it could not delay commencing a sale process to advance its case towards exit. On January 27, 2016, the Court entered an order approving the sale of the debtors’ U.S. oil and gas assets to BlueStone Natural Resources in exchange for $245 million. On March 17, 2016, the bankruptcy court entered an order extending the Debtors’ exclusive period to file a plan of reorganization until May 16, 2016. A condition to the BlueStone sale was rejection of a gas gathering agreement with Crestwood Equity Partners.

Consequently, Quicksilver filed a motion seeking the bankruptcy court’s authority to reject the contract, similar to the motion Sabine filed in its case. On April 6, 2016, Quicksilver withdrew the rejection motion with prejudice. The withdrawal is only effective, however, upon Quicksilver's receipt from BlueStone of payment in full of the purchase price in connection with the approved sale of Quicksilver's oil and gas assets. 1 2 3 4 5 6 7 8 9 10 The second lien lenders also faced challenges in the Quicksilver case. In November 2015, the Official Unsecured Creditors Committee filed a declaratory judgment action, arguing that some of the debtors’ property is not encumbered by the second lien term loan.

The dispute turned on whether the liens granted in favor of the second lien lenders included after-acquired property. Ultimately, the bankruptcy court concluded that the liens granted in favor of the second lien lenders included all of the debtors’ assets, including after-acquired property. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 4 4 SWIFT ENERGY COMPANY (Delaware) FILING DATE TOTAL DEBT December 31, 2015 Approximately $1.2 billion $330 million first lien credit facility DIP LOAN AMOUNT: (nonpriming, junior lien financing) LENDERS: $905.1 million senior notes $50 million unsecured trade debt $75 million MATURITY: Senior noteholders 6 months BUSINESS BACKGROUND Headquartered in Houston, Texas Primary operations are in the Eagle Ford play in South Texas Notable Chapter 11 Developments: Swift filed chapter 11 after negotiating a restructuring support agreement with the majority of senior noteholders. Under the terms of the agreement, the senior notes would be converted to 96% of the common stock of reorganized Swift. On February 2, 2016, the bankruptcy court approved the sale of certain of Swift’s Louisiana assets to Texegy LLC in exchange for approximately $49 million. On March 31, 2016, the bankruptcy court confirmed Swift’s plan of reorganization. The proposed plan provides for the following treatment of creditors: DIP Facility Claims: converted into common stock of reorganized Swift RBL Secured Claims: paid in full (pre-petition RBL facility refinanced into a $320 million exit facility) Senior Notes and Rejection Claims: pro rata share of common stock in reorganized Swift equal to 88.5% on a fully diluted basis General Unsecured Claims: paid in full Stock Interests: pro rata share of common stock in reorganized Swift equal to 4% on a fully diluted basis 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 5 5 ENERGY & EXPLORATION PARTNERS, INC. (“ENXP”) (Northern District of Texas) FILING DATE TOTAL DEBT December 7, 2015 Approximately $1.2  illion b DIP LOAN AMOUNT: LENDERS: $765.3 million first lien credit facility $375 million unsecured convertible notes $27.3 million unsecured trade debt MATURITY: BUSINESS BACKGROUND $40 million After two different groups of the first lien lenders made competing DIP financial proposals, ENXP ultimately secured a DIP facility from members of both groups Headquartered in Fort Worth, Texas Primary assets located in North and East Texas 9 months from filing date Notable Chapter 11 Developments: Unlike the other Top Ten cases, ENXP’s case began as an involuntary bankruptcy proceeding filed by a group of its unsecured creditors. Subsequently, ENXP filed its voluntary petition, thereby converting the case to a voluntary chapter 11 proceeding. Within two months of the voluntary petition date, ENXP entered into a restructuring support agreement with its first lien lenders and unsecured note holders. Pursuant to the restructuring support agreement, on February 10, 2016, ENXP filed its joint plan of reorganization.

The plan provides for the following treatment of creditors: DIP Facility Claims: paid in full in cash Prepetition Secured Claims: pro rata share of (i) $40 million new term loan, (ii) 20% of the equity in reorganized ENXP, subject to dilution, and (iii) a rights offering involving a delayed draw term loan of $90 million and 80% of the equity in reorganized ENXP Convertible Notes Claims: pro rata share of warrants exercisable for seven years into 0.7% of the equity in reorganized ENXP General Unsecured Claims: pro rata share of $2.25 million and the proceeds of any avoidance actions Stock Interests: extinguished without distribution 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 6 6 MAGNUM HUNTER RESOURCES CORPORATION (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND December 15, 2015 Approximately The DIP loan consisted of two components: superpriority priming lien financing and junior lien secured financing Headquartered in Irving, Texas $1.1  illion b $70 million first lien revolving credit facility $336.6 million second lien term loan $600 million AMOUNT: $200 million $70 million superpriority priming financing $130 million junior lien financing Primary assets located in Marcellus Shale in West Virginia and Utica Shale in Ohio LENDERS: Members of unsecured noteholders and second lien lenders unsecured notes MATURITY: 9 months Notable Chapter 11 Developments: Magnum Hunter filed bankruptcy with a restructuring support agreement in place among its first lien, second lien, and unsecured noteholders. According to the terms of the agreement, Magnum Hunter would seek authorization to obtain a DIP loan, with a portion of the proceeds to pay the first lien obligations in full. On January 11, 2016, the bankruptcy court approved Magnum Hunter’s motion to obtain a DIP loan and the first lien lenders received payment in full. On February 19, 2016, Magnum Hunter filed its amended joint plan of reorganization, with support from the parties to the restructuring support agreement, as well as the Official Committee of Unsecured Creditors. The confirmation hearing was originally scheduled for April 8, 2016, but has been adjourned to April 18 in light of disputes with shareholders and pipeline owners. 1 2 3 4 5 6 7 8 9 10 The plan provides for the following treatment of claims: DIP Facility Claims: satisfied in full and each holder will receive its pro rata share of 28.8% of the reorganized entity's common stock, subject to dillution.

First lien claims were satisfied by the DIP facility Second lien: debt-for-equity exchange with each holder receiving its pro rata share of 36.87% of the reorganized entity’s common stock (valued at approximately 78.3%-89.2% of the outstanding debt) Unsecured noteholders: each holder will receive its pro rata share of 31.3% of the reorganized entity’s common stock, subject to dilution © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 7 7 MILAGRO OIL & GAS (Delaware) FILING DATE TOTAL DEBT July 15, 2015 Approximately DIP LOAN $1.1  illion b $87.6 million first lien credit facility $311.3 million second lien notes BUSINESS BACKGROUND None Privately held company Primary assets located in Texas, Louisiana, and Mississippi $655.2 million unsecured intercompany debt Notable Chapter 11 Developments: Prior to the petition date, Milagro negotiated a pre-arranged plan with certain secured lenders, note holders, and equity holders. The restructuring support agreement provides for the sale of Milagro’s assets to White Oak Resources VI, LLC in exchange for $120 million in cash plus equity in White Oak, valued at $97 million. On October 8, 2015, the bankruptcy court confirmed Milagro’s joint plan of reorganization, which incorporates the terms of the restructuring support agreement, including the sale of substantially all of Milagro’s assets to White Oak for $217 million. The plan provides the following treatment of creditors: First lien: payment in full Second lien: debt-for-equity exchange, with each holder receiving its pro rata share of 100% of reorganized Milagro’s common stock General unsecured: no distribution Except certain “eligible” general unsecured holders who agree to release their claims: pro rata share of $1 million Intercompany debt: disallowed 1 2 3 4 5 6 7 8 9 10 © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 8 8 VENOCO, INC. (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND March 18, 2016 Approximately AMOUNT: Headquartered in Denver, Colorado $952.1  illion m $175 million first lien secured notes $164.14 million second lien secured notes $35 million (senior secured superpriority non-amortizing delayed draw term loan facility) LENDERS: $308.2 million unsecured notes Apollo Capital Management $303 million unsecured PIK toggle notes MATURITY: $1.76 million trade debt and royalty obligations December 31, 2016 Founded in 1992 Primary operations are located both onshore and offshore in Southern California Venoco is a privately-held Delaware corporation Notable Chapter 11 Developments: In response to the decline in global oil prices as well as operational difficulties stemming from the rupture of a third-party common carrier pipeline, Venoco filed bankruptcy after entering into a restructuring support agreement with holders of 100% of the first lien secured notes and 100% of the second lien secured notes. Under the agreement’s milestones, Venoco must obtain entry of an order confirming a proposed plan of reorganization within approximately five months of the filing date. On April 8, 2016, Venoco filed an amended restructuring support agreement. A hearing to consider approval of the agreement is scheduled for April 21, 2016. 1 2 3 4 5 6 7 8 9 10 The proposed plan provides the following treatment of claims: First lien notes claims: pro rata share of 90% of common stock in reorganized Venoco Second lien notes claims: pro rata share of 10% warrants at a specified strike price Unsecured notes claims: pro rata share of $6,500,000 in cash and 2.6% of the common stock in reorganized Venoco General unsecured claims: pro rata share of cash equal to the lesser of $1,000,000, or an amount sufficient to pay all general unsecured claims in full © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES 9 9 NEW GULF RESOURCES, LLC (“NGR”) (Delaware) FILING DATE TOTAL DEBT DIP LOAN BUSINESS BACKGROUND December 17, 2015 Approximately AMOUNT: Headquartered in Tulsa, Oklahoma $586 million $38 million first lien credit facility $365 million second lien notes $10 million unsecured trade creditors $162 million subordinated $75 million LENDERS: Members of the second lien noteholders MATURITY: December 31, 2016 Founded in 2011 Primary operations are in East Texas NGR is a privately-held Delaware limited liability company PIK notes Notable Chapter 11 Developments: NGR filed bankruptcy after negotiating a restructuring support agreement with certain holders of the second lien notes and unsecured subordinated notes. The agreement provides for the payment in full of the first lien facility and a debt-for equity exchange for the second lien noteholders and subordinated noteholders. Pursuant to the restructuring support agreement, NGR filed its joint plan of reorganization and disclosure statement on February 5, 2016. The bankruptcy court approved NGR’s disclosure statement and set a confirmation hearing for April 20, 2016. 1 2 3 4 5 6 7 8 9 10 NGR's proposed plan contemplates using the DIP financing proceeds to repay the first lien credit facility.

The plan converts $365 million of debt under the second lien notes into either 87.5% or 95% of the equity in reorganized NGR, depending on whether holders of subordinated PIK notes vote to accept the plan. Holders of allowed second lien notes claims are also eligible to participate, on a pro rata basis, in a rights offering for the purchase of approximately $50 million in new first lien notes. Holders of subordinated PIK notes will receive pro rata shares of either 12.5% or 5% of the equity in reorganized NGR. © 2016 Haynes and Boone, LLP .

E&P TOP 10 CASES 10 10 ERG OPERATING COMPANY, LLC (Northern District of Texas) FILING DATE TOTAL DEBT April 30, 2015 Approximately DIP LOAN $409.7 million BUSINESS BACKGROUND None Privately held company $400 million first lien term loan Headquartered in Houston, Texas $9.7 million unsecured trade debt Primary assets located in Cat Canyon Field in Santa Barbara, California Notable Chapter 11 Developments: Although ERG pursued a sale of its assets pursuant to section 363, a stalking horse bidder was never identified and no qualifying bids were received. As a result, ERG cancelled the sale and pursued a plan of reorganization. On October 30, 2015, the bankruptcy court confirmed ERG’s joint plan of reorganization. ERG’s plan is unique in that the first lien lenders agreed to contribute an additional $150 million to reorganized ERG over a 1 2 3 4 5 6 7 8 9 10 three-year period. During this three-year period, reorganized ERG will prepare the assets for sale.

In essence, the lenders are hoping that in three years the assets will sell at a higher price than in the current depressed market. In exchange, the first lien lenders’ prepetition claim and liens are reinstated in the reorganized debtor. Unsecured creditors are entitled to their pro rata share of the proceeds of any avoidance actions. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES * Haynes and Boone has more than 575 lawyers, including more than 30 bankruptcy practitioners, serving clients across the country. © 2016 Haynes and Boone, LLP . E&P TOP 10 CASES LOCATIONS AUSTIN CHICAGO DALLAS DENVER FORT WORTH 600 Congress Avenue Suite 1300 Austin, TX 78701 United States of America T +1 512.867.8400 F +1 512.867.8470 180 N. LaSalle Street Suite 2215 Chicago, IL 60601 United States of America T +1 312.216.1620 F +1 312.216.1621 2323 Victory Avenue Suite 700 Dallas, TX 75219 United States of America T +1 214.651.5000 F +1 214.651.5940 1801 Broadway Street Suite 800 Denver, CO 80202 United States of America T +1 303.382.6200 F +1 303.382.6210 301 Commerce Street Suite 2600 Fort Worth, TX 76102 United States of America T +1 817.347.6600 F +1 817.347.6650 HOUSTON MEXICO CITY NEW YORK ORANGE COUNTY PALO ALTO 1221 McKinney Street Suite 2100 Houston, TX 77010 United States of America T +1 713.547.2000 F +1 713.547.2600 Torre Esmeralda I, Blvd. Manuel Ávila Camacho #40 Despacho 1601 Col. Lomas de Chapultepec, DF 11000 Mexico City, Mexico T +52.55.5249.1800 F +52.55.5249.1801 30 Rockefeller Plaza 26th Floor New York, NY 10112 United States of America T +1 212.659.7300 F +1 212.918.8989 600 Anton Boulevard Suite 700 Costa Mesa, CA 92626 United States of America T +1 949.202.3000 F +1 949.202.3001 525 University Avenue Suite 400 Palo Alto, CA 94301 United States of America T +1 650.687.8800 F +1 650.687.8801 RICHARDSON SAN ANTONIO SHANGHAI WASHINGTON, D.C. 2505 North Plano Road Suite 4000 Richardson, TX 75082 United States of America T +1 972.739.6900 F +1 972.680.7551 112 East Pecan Street Suite 1200 San Antonio, TX 78205 United States of America T +1 210.978.7000 F +1 210.978.7450 Shanghai International Finance Center, Tower 2 Unit 3620, Level 36 8 Century Avenue, Pudong Shanghai 200120, P.R. China T +86.21.6062.6179 F +86.21.6062.6347 800 17th Street, NW Suite 500 Washington, D.C.

20006 United States of America T +1 202.654.4500 F +1 202.654.4501 © 2016 Haynes and Boone, LLP . Haynes and Boone, LLP logo size: 2.5”(width) This publication is for informational purposes only and is not intended to be legal advice and does not establish an attorney-client relationship. Legal advice of any nature should be sought from legal counsel. © 2016 Haynes and Boone, LLP .