First Eagle Global Value Team - The Team opinions - December 31, 2015

First Eagle Asset Management

Description

First Eagle Global Value Team

Commentary

As of December 31, 2015

Market Overview

In the fourth quarter of 2015, the MSCI World Index rose 5.50% while in the United States the S&P 500 Index increased 7.04%.

In Europe, the German DAX was up 8.22% and the French CAC 40 index increased 1.29%. In Japan, the Nikkei 225 index gained

8.98% over the period. Crude oil fell 17.85% to $37.04 a barrel, and the price of gold fell 4.95% to $1,060 an ounce. The US dollar

strengthened 0.44% against the yen and strengthened 2.68% against the euro.

The biggest positive for the world, in our view, is lower oil prices, which not only may stimulate economic activity and potentially

help improve consumer disposable incomes and savings, but also may put the financial brakes on assertive regimes such as Russia,

Iran and ISIS.

We believe the biggest negative, other than significant geopolitical and policy concerns, is the deepening slowdown in China, and

the somewhat related crises that are unfolding in Brazil and Russia.

These countries, combined, were the largest source of marginal demand growth for most of the past decade but also the largest source of marginal growth in debt.1 Against a backdrop of high debt, high margins and high political risks, we believe assets remain pretty fully priced. In this setting, we’re seeing a bifurcation of prospects: Many manufacturing and commodity-linked businesses are already in recession, but service and Internet businesses have generally been growing healthily. The net result is that we are seeing some value emerge within our portfolio in areas such as industrials and commodities.

We believe valuations are high overall, but not wildly so, and beneath the surface of the market, we are finding what we think are underpriced securities. As long as there may be pockets of risk perception, there are pockets of lower-risk opportunity. Portfolio Review First Eagle Global Fund The Global Fund Class A shares (w/out sales charge) returned 4.51%2 for the quarter ending December 31, 2015 versus 5.50% for the MSCI World Index. While the Fund produced strong absolute returns in the fourth quarter, our performance lagged the MSCI World Index because of our holdings in cash and cash equivalents and gold bullion. Japanese companies and global IT companies were among the leading contributors in the quarter.

The top five contributors were Microsoft Corporation, KDDI Corporation, Hoya Corporation, Keyence Corporation and HeidelbergCement AG. Investors began to reward Microsoft for its transition to cloud computing and for the steady income that this business model has generated. KDDI, a Japanese mobile phone operator, gained ground as investors recognized that the regulatory environment for Japanese telecoms would be more benign than expected.

The sector had sold off after Prime Minister Abe stated that he wanted to see mobile phone costs lowered for consumers. Subsequently, investors learned that the Ministry of Internal Affairs and Communications does not have the power to regulate tariffs and that its goal is to introduce more competition, not to reduce the profits of the major telecom operators. Japan’s Hoya Corporation gained ground on the strength of its IT business.

The company’s semiconductor-related products met with strong demand, and weakness in the yen was favorable for the portion of Hoya’s business that provides glass disks for 1. Source: First Eagle Investment Management/BIS/Haver 2. If sales charge was included performance would have been lower. The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short-term performance. Current performance may be lower or higher than figures shown.

The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end is available at www.feim.com or by calling 800.334.2143. Page 1 . First Eagle Global Value Team Commentary As of December 31, 2015 hard disk drives. Keyence, a contributor this quarter but a detractor in the third quarter, is a leading player in the world of electronic sensors for factory automation. In addition to the high margins it enjoys in its home market of Japan, the company is rapidly growing its business in the United States. Investors also hope that Keyence will begin to distribute some of the excess it holds on its balance sheet. Detractors for the quarter included a number of companies in the energy and materials sectors.

The largest five detractors were gold bullion, National Oilwell Varco, Potash Corporation of Saskatchewan, Sanofi and American Express Company. National Oilwell Varco, which focuses on services for technically challenging oil wells, once again saw its shares fall along with the rest of the energy sector. Our long-term view of the company’s prospects is based on our belief that a $37 a barrel price for oil is not here to stay.

The price could certainly go lower for a time, but if the industry is to bring on new fields to replace those that are becoming depleted, we believe the price of oil will have to rise significantly. The oil fields being depleted are largely conventional ones, but they’re generally being replaced by unconventional oil—fracking onshore and ultra-deep wells offshore. These are areas where National Oilwell Varco plays a dominant role.

Canada’s Potash Corporation was weak both because of the general decline in commodities companies and because depreciation in the Russian ruble gave one of its key competitors a pricing advantage. Sanofi, a pharmaceutical company based in France lost ground, alongside others in its industry, when drug pricing became a prominent issue in US politics. American Express declined because of sharp competitive pressure from other credit card companies in the co-branded card business. For the year-ending December 31, 2015, the top five contributors were Microsoft Corporation, KDDI Corporation, Secom Company Ltd., Berkeley Group Holdings and Keyence Corporation. The five largest detractors for the year were National Oilwell Varco, gold bullion, Potash Corporation of Saskatchewan, Oracle Corporation and Teradata Corporation. First Eagle Overseas Fund The Overseas Fund Class A shares (w/out sales charge) returned 4.53%2 for the quarter ending December 31, 2015 versus 4.71% for the MSCI EAFE Index.

While the Fund produced strong absolute returns in the fourth quarter, our performance slightly lagged the MSCI EAFE Index because of our holdings in cash and cash equivalents and gold bullion. The top five contributors to performance for the quarter were KDDI Corporation, Hoya Corporation, Keyence Corporation, Heidelberg Cement and SMC Corporation. The five largest detractors to performance were gold bullion, Potash Corporation of Saskatchewan, Cenovus Energy, Sanofi and Hornbach Holding AG. For the year ending December 31, 2015, the top five contributors to performance for the quarter were KDDI Corporation, Sompo Japan Nipponkoa Holdings, Hoya Corporation, Berkeley Group Holdings and Keyence Corporation. The largest contributors for the year were Potash Corporation of Saskatchewan, Grupo Televisa, Cenovus Energy, gold bullion and Canadian Natural Resources Limited. U.S.

Value Fund The U.S. Value Fund Class A shares (w/out sales charge) returned 3.70%2 for the quarter ending December 31, 2015 versus 7.04% for the S&P 500 Index. The top five contributors to performance for the quarter were Microsoft Corporation, Omnicom Group, Intel Corporation, Plum Creek Timber Company and Alphabet Inc.

The five largest detractors to performance over the quarter were gold bullion, San Juan Basin Royalty Trust, National Oilwell Varco, American Express and Teradata Corporation. For the year-ending December 31, 2015, the top five contributors were Microsoft Corporation, Orbital ATK, Inc., Northrop Grumman Corporation, Alphabet Inc. and Cintas Corporation. The five largest detractors were National Oilwell Varco, Potash Corporation of Saskatchewan, Teradata Corporation, Oracle Corporation and gold bullion. We appreciate your confidence and thank you for your support. Sincerely, First Eagle Investment Management, LLC Page 2 .

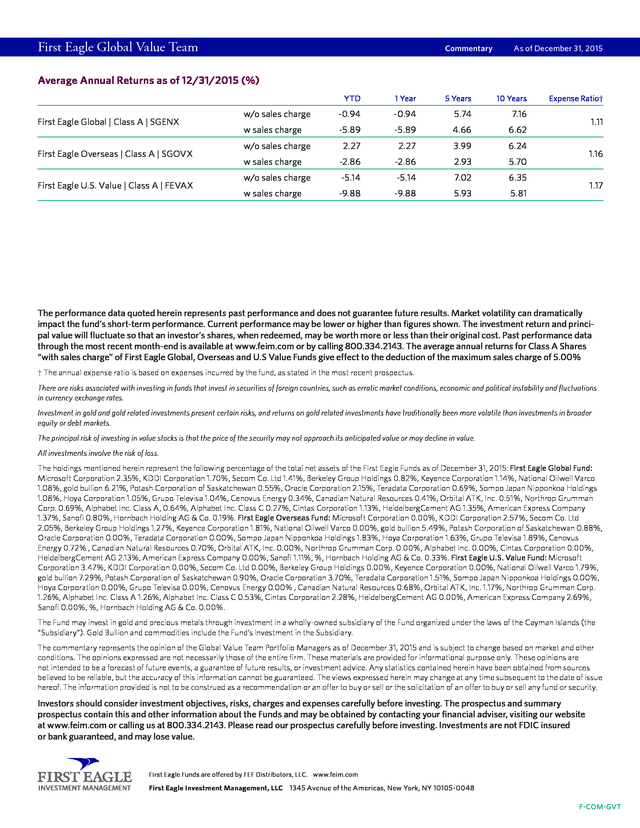

First Eagle Global Value Team Commentary As of December 31, 2015 Average Annual Returns as of 12/31/2015 (%) YTD First Eagle Global | Class A | SGENX First Eagle Overseas | Class A | SGOVX First Eagle U.S. Value | Class A | FEVAX 1 Year 5 Years 10 Years w/o sales charge -0.94 -0.94 5.74 7.16 w sales charge -5.89 -5.89 4.66 6.62 2.27 2.27 3.99 6.24 -2.86 -2.86 2.93 5.70 w/o sales charge w sales charge w/o sales charge -5.14 -5.14 7.02 -9.88 -9.88 5.93 1.11 1.16 6.35 w sales charge Expense Ratio† 5.81 1.17 The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short-term performance. Current performance may be lower or higher than figures shown.

The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end is available at www.feim.com or by calling 800.334.2143. The average annual returns for Class A Shares “with sales charge” of First Eagle Global, Overseas and U.S Value Funds give effect to the deduction of the maximum sales charge of 5.00% † The annual expense ratio is based on expenses incurred by the fund, as stated in the most recent prospectus. There are risks associated with investing in funds that invest in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates. Investment in gold and gold related investments present certain risks, and returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets. The principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value. All investments involve the risk of loss. The holdings mentioned herein represent the following percentage of the total net assets of the First Eagle Funds as of December 31, 2015: First Eagle Global Fund: Microsoft Corporation 2.35%, KDDI Corporation 1.70%, Secom Co.

Ltd 1.41%, Berkeley Group Holdings 0.82%, Keyence Corporation 1.14%, National Oilwell Varco 1.08%, gold bullion 6.21%, Potash Corporation of Saskatchewan 0.55%, Oracle Corporation 2.15%, Teradata Corporation 0.69%, Sompo Japan Nipponkoa Holdings 1.08%, Hoya Corporation 1.05%, Grupo Televisa 1.04%, Cenovus Energy 0.34%, Canadian Natural Resources 0.41%, Orbital ATK, Inc. 0.51%, Northrop Grumman Corp. 0.69%, Alphabet Inc.

Class A, 0.64%, Alphabet Inc. Class C 0.27%, Cintas Corporation 1.13%, HeidelbergCement AG 1.35%, American Express Company 1.37%, Sanofi 0.80%, Hornbach Holding AG & Co. 0.19%.

First Eagle Overseas Fund: Microsoft Corporation 0.00%, KDDI Corporation 2.57%, Secom Co. Ltd 2.05%, Berkeley Group Holdings 1.27%, Keyence Corporation 1.81%, National Oilwell Varco 0.00%, gold bullion 5.49%, Potash Corporation of Saskatchewan 0.88%, Oracle Corporation 0.00%, Teradata Corporation 0.00%, Sompo Japan Nipponkoa Holdings 1.83%, Hoya Corporation 1.63%, Grupo Televisa 1.89%, Cenovus Energy 0.72% , Canadian Natural Resources 0.70%, Orbital ATK, Inc. 0.00%, Northrop Grumman Corp.

0.00%, Alphabet Inc. 0.00%, Cintas Corporation 0.00%, HeidelbergCement AG 2.13%, American Express Company 0.00%, Sanofi 1.11%, %, Hornbach Holding AG & Co. 0.33%.

First Eagle U.S. Value Fund: Microsoft Corporation 3.47%, KDDI Corporation 0.00%, Secom Co. Ltd 0.00%, Berkeley Group Holdings 0.00%, Keyence Corporation 0.00%, National Oilwell Varco 1.79%, gold bullion 7.29%, Potash Corporation of Saskatchewan 0.90%, Oracle Corporation 3.70%, Teradata Corporation 1.51%, Sompo Japan Nipponkoa Holdings 0.00%, Hoya Corporation 0.00%, Grupo Televisa 0.00%, Cenovus Energy 0.00% , Canadian Natural Resources 0.68%, Orbital ATK, Inc.

1.17%, Northrop Grumman Corp. 1.26%, Alphabet Inc. Class A 1.26%, Alphabet Inc. Class C 0.53%, Cintas Corporation 2.28%, HeidelbergCement AG 0.00%, American Express Company 2.69%, Sanofi 0.00%, %, Hornbach Holding AG & Co.

0.00%. The Fund may invest in gold and precious metals through investment in a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). Gold Bullion and commodities include the Fund’s investment in the Subsidiary. The commentary represents the opinion of the Global Value Team Portfolio Managers as of December 31, 2015 and is subject to change based on market and other conditions. The opinions expressed are not necessarily those of the entire firm.

These materials are provided for informational purpose only. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed.

The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation or an offer to buy or sell or the solicitation of an offer to buy or sell any fund or security. Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds and may be obtained by contacting your financial adviser, visiting our website at www.feim.com or calling us at 800.334.2143.

Please read our prospectus carefully before investing. Investments are not FDIC insured or bank guaranteed, and may lose value. First Eagle Funds are offered by FEF Distributors, LLC. www.feim.com First Eagle Investment Management, LLC 1345 Avenue of the Americas, New York, NY 10105-0048 F-COM-GVT .

These countries, combined, were the largest source of marginal demand growth for most of the past decade but also the largest source of marginal growth in debt.1 Against a backdrop of high debt, high margins and high political risks, we believe assets remain pretty fully priced. In this setting, we’re seeing a bifurcation of prospects: Many manufacturing and commodity-linked businesses are already in recession, but service and Internet businesses have generally been growing healthily. The net result is that we are seeing some value emerge within our portfolio in areas such as industrials and commodities.

We believe valuations are high overall, but not wildly so, and beneath the surface of the market, we are finding what we think are underpriced securities. As long as there may be pockets of risk perception, there are pockets of lower-risk opportunity. Portfolio Review First Eagle Global Fund The Global Fund Class A shares (w/out sales charge) returned 4.51%2 for the quarter ending December 31, 2015 versus 5.50% for the MSCI World Index. While the Fund produced strong absolute returns in the fourth quarter, our performance lagged the MSCI World Index because of our holdings in cash and cash equivalents and gold bullion. Japanese companies and global IT companies were among the leading contributors in the quarter.

The top five contributors were Microsoft Corporation, KDDI Corporation, Hoya Corporation, Keyence Corporation and HeidelbergCement AG. Investors began to reward Microsoft for its transition to cloud computing and for the steady income that this business model has generated. KDDI, a Japanese mobile phone operator, gained ground as investors recognized that the regulatory environment for Japanese telecoms would be more benign than expected.

The sector had sold off after Prime Minister Abe stated that he wanted to see mobile phone costs lowered for consumers. Subsequently, investors learned that the Ministry of Internal Affairs and Communications does not have the power to regulate tariffs and that its goal is to introduce more competition, not to reduce the profits of the major telecom operators. Japan’s Hoya Corporation gained ground on the strength of its IT business.

The company’s semiconductor-related products met with strong demand, and weakness in the yen was favorable for the portion of Hoya’s business that provides glass disks for 1. Source: First Eagle Investment Management/BIS/Haver 2. If sales charge was included performance would have been lower. The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short-term performance. Current performance may be lower or higher than figures shown.

The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end is available at www.feim.com or by calling 800.334.2143. Page 1 . First Eagle Global Value Team Commentary As of December 31, 2015 hard disk drives. Keyence, a contributor this quarter but a detractor in the third quarter, is a leading player in the world of electronic sensors for factory automation. In addition to the high margins it enjoys in its home market of Japan, the company is rapidly growing its business in the United States. Investors also hope that Keyence will begin to distribute some of the excess it holds on its balance sheet. Detractors for the quarter included a number of companies in the energy and materials sectors.

The largest five detractors were gold bullion, National Oilwell Varco, Potash Corporation of Saskatchewan, Sanofi and American Express Company. National Oilwell Varco, which focuses on services for technically challenging oil wells, once again saw its shares fall along with the rest of the energy sector. Our long-term view of the company’s prospects is based on our belief that a $37 a barrel price for oil is not here to stay.

The price could certainly go lower for a time, but if the industry is to bring on new fields to replace those that are becoming depleted, we believe the price of oil will have to rise significantly. The oil fields being depleted are largely conventional ones, but they’re generally being replaced by unconventional oil—fracking onshore and ultra-deep wells offshore. These are areas where National Oilwell Varco plays a dominant role.

Canada’s Potash Corporation was weak both because of the general decline in commodities companies and because depreciation in the Russian ruble gave one of its key competitors a pricing advantage. Sanofi, a pharmaceutical company based in France lost ground, alongside others in its industry, when drug pricing became a prominent issue in US politics. American Express declined because of sharp competitive pressure from other credit card companies in the co-branded card business. For the year-ending December 31, 2015, the top five contributors were Microsoft Corporation, KDDI Corporation, Secom Company Ltd., Berkeley Group Holdings and Keyence Corporation. The five largest detractors for the year were National Oilwell Varco, gold bullion, Potash Corporation of Saskatchewan, Oracle Corporation and Teradata Corporation. First Eagle Overseas Fund The Overseas Fund Class A shares (w/out sales charge) returned 4.53%2 for the quarter ending December 31, 2015 versus 4.71% for the MSCI EAFE Index.

While the Fund produced strong absolute returns in the fourth quarter, our performance slightly lagged the MSCI EAFE Index because of our holdings in cash and cash equivalents and gold bullion. The top five contributors to performance for the quarter were KDDI Corporation, Hoya Corporation, Keyence Corporation, Heidelberg Cement and SMC Corporation. The five largest detractors to performance were gold bullion, Potash Corporation of Saskatchewan, Cenovus Energy, Sanofi and Hornbach Holding AG. For the year ending December 31, 2015, the top five contributors to performance for the quarter were KDDI Corporation, Sompo Japan Nipponkoa Holdings, Hoya Corporation, Berkeley Group Holdings and Keyence Corporation. The largest contributors for the year were Potash Corporation of Saskatchewan, Grupo Televisa, Cenovus Energy, gold bullion and Canadian Natural Resources Limited. U.S.

Value Fund The U.S. Value Fund Class A shares (w/out sales charge) returned 3.70%2 for the quarter ending December 31, 2015 versus 7.04% for the S&P 500 Index. The top five contributors to performance for the quarter were Microsoft Corporation, Omnicom Group, Intel Corporation, Plum Creek Timber Company and Alphabet Inc.

The five largest detractors to performance over the quarter were gold bullion, San Juan Basin Royalty Trust, National Oilwell Varco, American Express and Teradata Corporation. For the year-ending December 31, 2015, the top five contributors were Microsoft Corporation, Orbital ATK, Inc., Northrop Grumman Corporation, Alphabet Inc. and Cintas Corporation. The five largest detractors were National Oilwell Varco, Potash Corporation of Saskatchewan, Teradata Corporation, Oracle Corporation and gold bullion. We appreciate your confidence and thank you for your support. Sincerely, First Eagle Investment Management, LLC Page 2 .

First Eagle Global Value Team Commentary As of December 31, 2015 Average Annual Returns as of 12/31/2015 (%) YTD First Eagle Global | Class A | SGENX First Eagle Overseas | Class A | SGOVX First Eagle U.S. Value | Class A | FEVAX 1 Year 5 Years 10 Years w/o sales charge -0.94 -0.94 5.74 7.16 w sales charge -5.89 -5.89 4.66 6.62 2.27 2.27 3.99 6.24 -2.86 -2.86 2.93 5.70 w/o sales charge w sales charge w/o sales charge -5.14 -5.14 7.02 -9.88 -9.88 5.93 1.11 1.16 6.35 w sales charge Expense Ratio† 5.81 1.17 The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short-term performance. Current performance may be lower or higher than figures shown.

The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end is available at www.feim.com or by calling 800.334.2143. The average annual returns for Class A Shares “with sales charge” of First Eagle Global, Overseas and U.S Value Funds give effect to the deduction of the maximum sales charge of 5.00% † The annual expense ratio is based on expenses incurred by the fund, as stated in the most recent prospectus. There are risks associated with investing in funds that invest in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates. Investment in gold and gold related investments present certain risks, and returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets. The principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value. All investments involve the risk of loss. The holdings mentioned herein represent the following percentage of the total net assets of the First Eagle Funds as of December 31, 2015: First Eagle Global Fund: Microsoft Corporation 2.35%, KDDI Corporation 1.70%, Secom Co.

Ltd 1.41%, Berkeley Group Holdings 0.82%, Keyence Corporation 1.14%, National Oilwell Varco 1.08%, gold bullion 6.21%, Potash Corporation of Saskatchewan 0.55%, Oracle Corporation 2.15%, Teradata Corporation 0.69%, Sompo Japan Nipponkoa Holdings 1.08%, Hoya Corporation 1.05%, Grupo Televisa 1.04%, Cenovus Energy 0.34%, Canadian Natural Resources 0.41%, Orbital ATK, Inc. 0.51%, Northrop Grumman Corp. 0.69%, Alphabet Inc.

Class A, 0.64%, Alphabet Inc. Class C 0.27%, Cintas Corporation 1.13%, HeidelbergCement AG 1.35%, American Express Company 1.37%, Sanofi 0.80%, Hornbach Holding AG & Co. 0.19%.

First Eagle Overseas Fund: Microsoft Corporation 0.00%, KDDI Corporation 2.57%, Secom Co. Ltd 2.05%, Berkeley Group Holdings 1.27%, Keyence Corporation 1.81%, National Oilwell Varco 0.00%, gold bullion 5.49%, Potash Corporation of Saskatchewan 0.88%, Oracle Corporation 0.00%, Teradata Corporation 0.00%, Sompo Japan Nipponkoa Holdings 1.83%, Hoya Corporation 1.63%, Grupo Televisa 1.89%, Cenovus Energy 0.72% , Canadian Natural Resources 0.70%, Orbital ATK, Inc. 0.00%, Northrop Grumman Corp.

0.00%, Alphabet Inc. 0.00%, Cintas Corporation 0.00%, HeidelbergCement AG 2.13%, American Express Company 0.00%, Sanofi 1.11%, %, Hornbach Holding AG & Co. 0.33%.

First Eagle U.S. Value Fund: Microsoft Corporation 3.47%, KDDI Corporation 0.00%, Secom Co. Ltd 0.00%, Berkeley Group Holdings 0.00%, Keyence Corporation 0.00%, National Oilwell Varco 1.79%, gold bullion 7.29%, Potash Corporation of Saskatchewan 0.90%, Oracle Corporation 3.70%, Teradata Corporation 1.51%, Sompo Japan Nipponkoa Holdings 0.00%, Hoya Corporation 0.00%, Grupo Televisa 0.00%, Cenovus Energy 0.00% , Canadian Natural Resources 0.68%, Orbital ATK, Inc.

1.17%, Northrop Grumman Corp. 1.26%, Alphabet Inc. Class A 1.26%, Alphabet Inc. Class C 0.53%, Cintas Corporation 2.28%, HeidelbergCement AG 0.00%, American Express Company 2.69%, Sanofi 0.00%, %, Hornbach Holding AG & Co.

0.00%. The Fund may invest in gold and precious metals through investment in a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). Gold Bullion and commodities include the Fund’s investment in the Subsidiary. The commentary represents the opinion of the Global Value Team Portfolio Managers as of December 31, 2015 and is subject to change based on market and other conditions. The opinions expressed are not necessarily those of the entire firm.

These materials are provided for informational purpose only. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed.

The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation or an offer to buy or sell or the solicitation of an offer to buy or sell any fund or security. Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds and may be obtained by contacting your financial adviser, visiting our website at www.feim.com or calling us at 800.334.2143.

Please read our prospectus carefully before investing. Investments are not FDIC insured or bank guaranteed, and may lose value. First Eagle Funds are offered by FEF Distributors, LLC. www.feim.com First Eagle Investment Management, LLC 1345 Avenue of the Americas, New York, NY 10105-0048 F-COM-GVT .