Description

DDRAFT

FHFA MORTGAGE

ANALYTICS

PLATFORM

Released by FHFA, July 10, 2014

Robert M. Dunsky

Xiaoming Zhou

Michael Kane

Ming Chow

Charles Hu

Andrew Varrieur

. FHFA Mortgage Analytics Platform

1.

BACKGROUND & INTRODUCTION........................................................................................................2

2.

FHFA MORTGAGE ANALYTICS PLATFORM OVERVIEW ................................................................3

3.

PERFORMING LOAN MODULE.................................................................................................................6

3.1

3.2

4.

COMMON INDEPENDENT VARIABLES IN THE PERFORMING LOAN MODULE ...............................................7

SPECIAL TREATMENT OF PERFORMING MODIFIED LOANS.......................................................................... 12

NON-PERFORMING LOAN MODULE ................................................................................................... 15

4.1

5.

INDEPENDENT VARIABLES IN THE NON-PERFORMING LOAN MODULE..................................................... 16

CREDIT LOSS MODULE ..............................................................................................................................

19 5.1 5.2 5.3 6. CHARGE-OFF TIMING ................................................................................................................................... 20 CHARGE-OFF AMOUNT ................................................................................................................................ 20 REO OPERATIONS EXPENSES .......................................................................................................................

25 INTEGRATION MODULE ............................................................................................................................ 27 6.1 6.2 6.3 SCHEDULED AND UNSCHEDULED RELATED PRINCIPAL ............................................................................. 27 CREDIT LOSS RELATED PRINCIPAL ..............................................................................................................

28 CREDIT LOSS MEASURES .............................................................................................................................. 28 7. STANDARDIZED REPORT ELEMENTS ................................................................................................. 30 8. REFERENCES .................................................................................................................................................

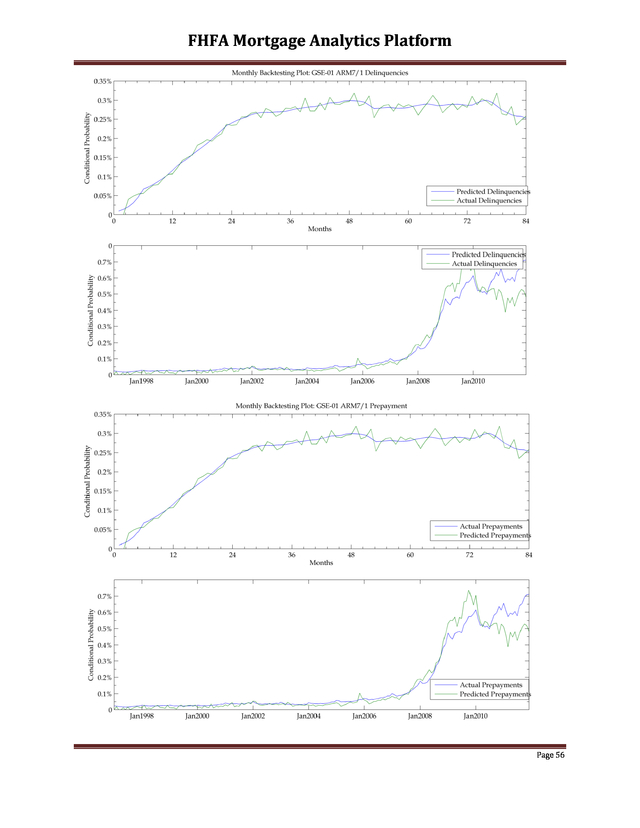

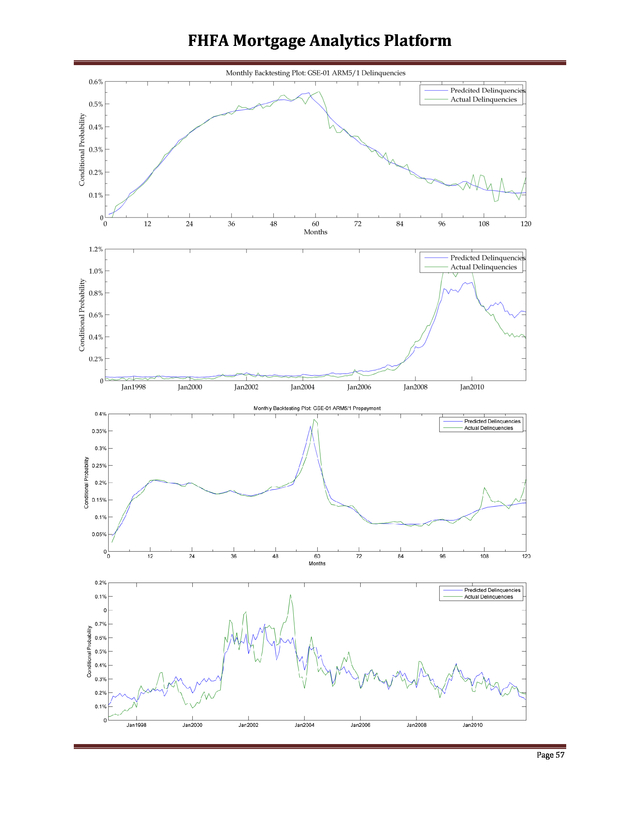

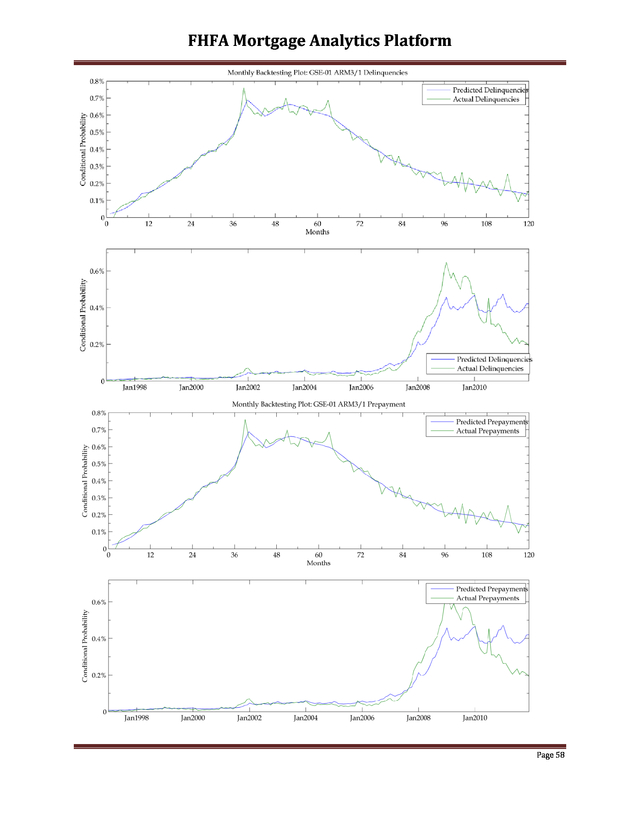

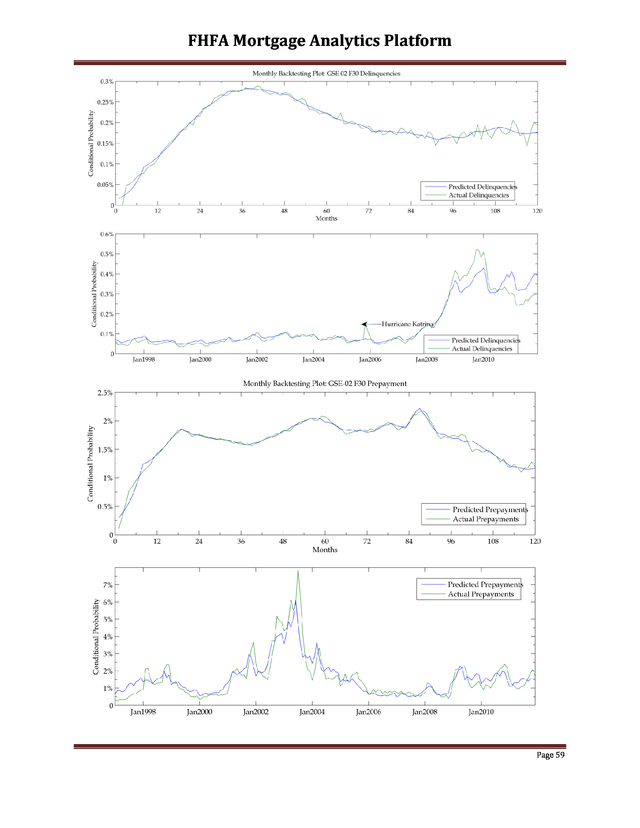

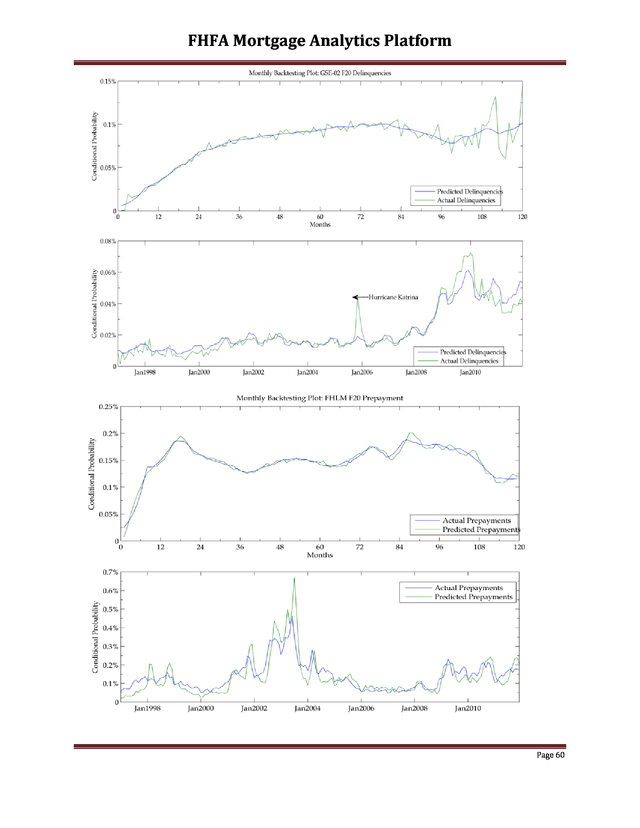

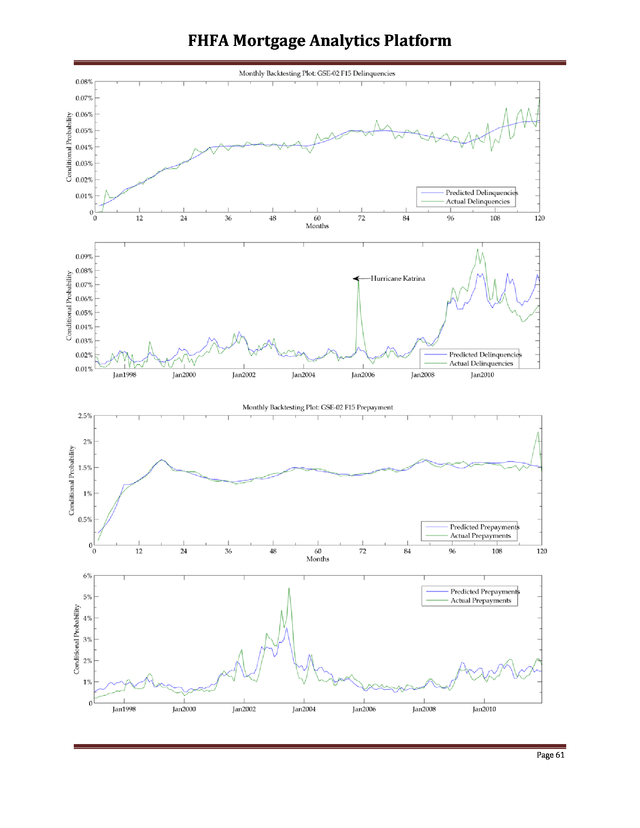

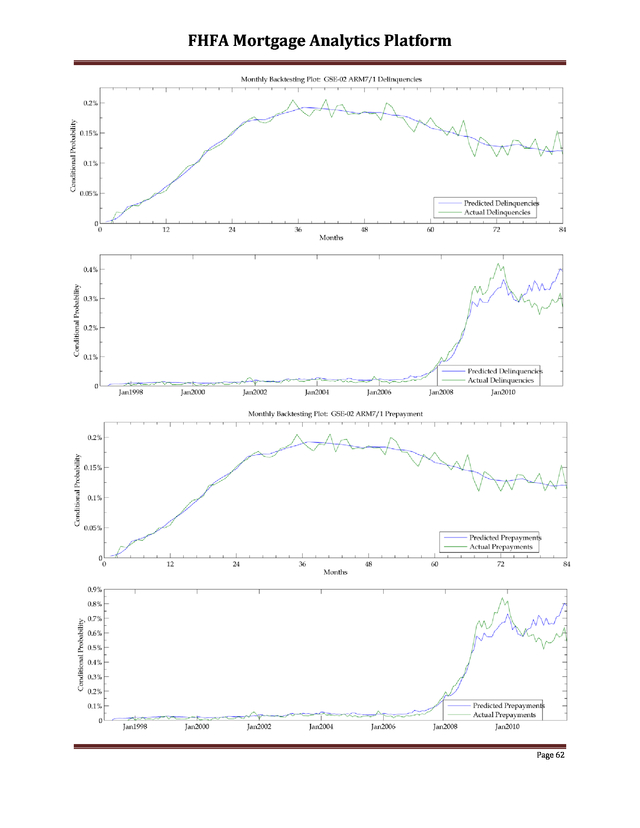

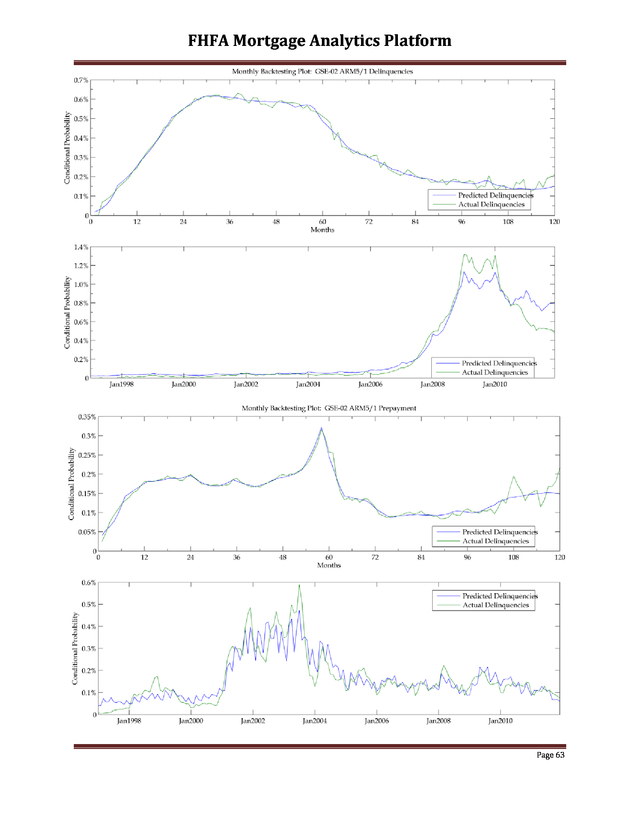

32 9. APPENDIX A: SPLINE CONSTRUCTION............................................................................................... 33 10. APPENDIX B: PERFORMING LOAN MODULE MODEL COEFFICIENTS.................................... 34 11. APPENDIX C: BACK-TESTING PLOTS ..................................................................................................

51 12. APPENDIX D: NON-PERFORMING LOAN EQUATION PARAMETERS...................................... 65 Page 1 . FHFA Mortgage Analytics Platform 1. Background & Introduction The Federal Housing Finance Agency (FHFA) maintains a proprietary Mortgage Analytics Platform to support the Agency’s strategic plan. The objective of this white paper is to provide interested stakeholders with a detailed description of the platform, as it is one of the tools the FHFA uses in policy analysis. The distribution of this white paper is part of a larger effort to increase transparency on mortgage performance and the analytical tools used for policy analysis and evaluation within the FHFA. The motivation to build the FHFA Mortgage Analytics Platform derived from the Agency’s need for an independent empirical view on multiple policy initiatives. Academic empirical studies may suffer from a lack of high quality data, while empirical work from inside the industry typically represents a specific view.

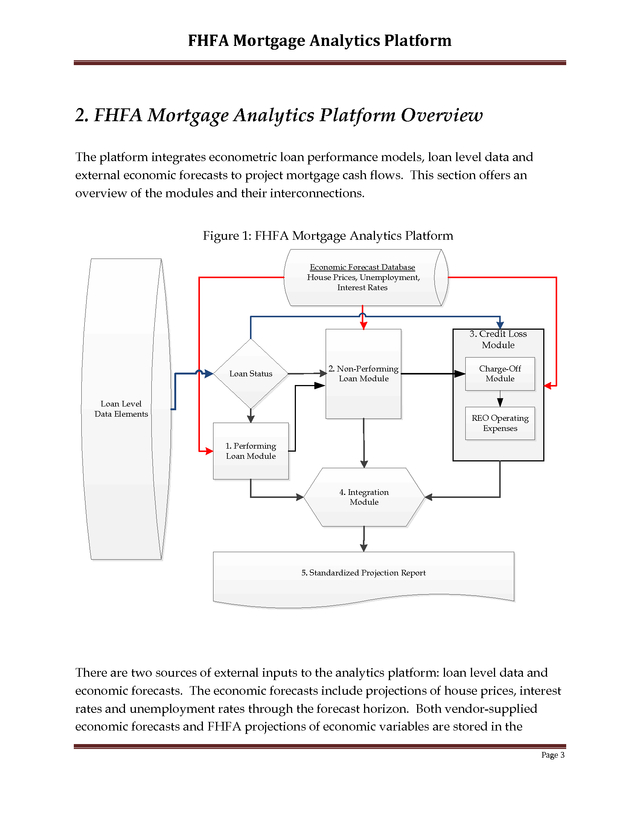

The FHFA maintains several vendor platforms from which an independent view is possible, yet these platforms tend to be inflexible and opaque. The unique role of the FHFA as regulator and conservator necessitated platform flexibility and transparency to carry out its responsibilities. The FHFA Mortgage Analytics Platform is maintained on a continuous basis; as such, the material herein represents the platform as of the publication date of this document. As resources permit, this document will be updated to reflect enhancements to the platform. Page 2 . FHFA Mortgage Analytics Platform 2. FHFA Mortgage Analytics Platform Overview The platform integrates econometric loan performance models, loan level data and external economic forecasts to project mortgage cash flows. This section offers an overview of the modules and their interconnections. Figure 1: FHFA Mortgage Analytics Platform Economic Forecast Database House Prices, Unemployment, Interest Rates 3. Credit Loss Module Loan Status 2.

Non-Performing Loan Module Loan Level Data Elements Charge-Off Module REO Operating Expenses 1. Performing Loan Module 4. Integration Module 5.

Standardized Projection Report There are two sources of external inputs to the analytics platform: loan level data and economic forecasts. The economic forecasts include projections of house prices, interest rates and unemployment rates through the forecast horizon. Both vendor-supplied economic forecasts and FHFA projections of economic variables are stored in the Page 3 .

FHFA Mortgage Analytics Platform economic forecast database. These economic forecasts cover a wide range of economic environments from baseline to highly optimistic to extremely stressful economic conditions. The economic forecast databases are quarterly. The loan level data elements are the second source of external inputs; these include approximately thirty variables per loan comprising loan attributes and borrower characteristics. The platform projects mortgage performance from the loan’s current age to termination, including foreclosure alternatives and the resolution of real estate owned (REO).

The platform applies projected probabilities of termination to performing loan balances such that a portion of the loan prepays, becomes delinquent and may resolve as a default each month. To simplify the discussion within this paper, when a loan is said to prepay (or default), only a portion of the loan is prepaying (or defaulting), not the whole loan. The components of the platform are summarized below and are described in greater detail in subsequent sections of this paper. 1. Performing Loan Module – the primary function of this module is to project monthly loan level prepayment and 90-day delinquency probabilities on performing and modified performing loans.

Loans enter into this module if they are current, less than 90 days delinquent, or forecasted to cure from a delinquency during the simulation. The prepayment and delinquency equations are functions of borrower characteristics, loan characteristics, home values and other economic variables. Multiple pairs of prepayment and delinquency equations collectively cover several loan products and modified loans guaranteed or owned by the Enterprises. 2. Non-Performing Loan Module – the primary function of this module is to project lifetime outcomes for delinquent loans. Loans enter into this module if they are 90 to 180 days delinquent at the beginning of the projection, or if they are predicted to become delinquent within the performing loan module.

The module outputs four mutually exclusive loan-specific probabilities each month: foreclosure completion (REO), voluntary prepayment, foreclosure alternative resolutions and re-performance (cure). The foreclosure alternative resolutions include deed-in-lieu of foreclosure, preforeclosure sale (short sale), and third party sale. A loan is defined as re-performing when all arrearages are paid and the cure is not due to a modification or restructuring. The models are a function of borrower characteristics, house prices and state legal structures.

Unlike the performing loan module where multiple product level models are constructed, only one set of equations is estimated for non-performing loans. Page 4 . FHFA Mortgage Analytics Platform 3. Credit Loss Module– the primary function of this module is to calculate loan level credit losses and determine the appropriate timing of loss recognition. Loans enter into this module if they are greater than 180 days delinquent at the start of the projection or are projected to generate a credit loss from the non-performing module. Credit losses are measured as charge-offs and REO operating expenses. Charge-offs and REO operating expenses are calculated at the loan level using an accounting approach. 4. The Integration Module - combines the forecasted performance elements, mortgage contractual terms, and interest rates to generate loan level cash flows. This module outputs are aggregated across loans into the Standardized Projection Report. 5. The Standardized Projection Report –summarizes projections of portfolio performance measures over the forecast horizon.

Key credit loss elements reported in the report are charge-offs and REO operation expenses. Other variables in the report include performing balances, dollars of new 90 day delinquencies, scheduled and unscheduled principal payments, guarantee fee income, and credit enhancement claims. The subsequent sections of the paper discuss each of the modules in detail. Sections 3 through 5 focus on the design of the econometric behavioral equations, Section 6 reviews the credit loss calculations, and Section 7 covers the calculation of the monthly projections.

The appendices include the parameter estimates and back testing results from the modules covered in Sections 3 through 5. Page 5 . FHFA Mortgage Analytics Platform 3. Performing Loan Module The Performing Loan Module contains a series of Multinomial Logit (MNL) equations that predict the loan’s monthly status: current, prepaid or delinquent. Many authors including Clapp et al (2005) and Jenkins (1995) demonstrate that the MNL provides a convenient method for structuring prepayment and delinquency risk as a discrete-time competing hazard. Using the estimated equation parameters, the platform calculates the conditional probability of prepayment and 90-day delinquency as, ( ) ( ˆ  exp xi ,t ' β pp  P( prepayi ,t ) = ˆ ˆ  1 + exp x ' β + exp v ' β i ,t pp i ,t f 90 ï£ ( ( ) ) ( )   , and   ˆ  exp vi ,t ' β f 90 P( f 90 i ,t ) =  ˆ ˆ  1 + exp x ' β + exp v ' β i ,t f 90 i ,t pp ï£ ( ) )  .   The probability of remaining current is calculated as, P(currenti ,t ) = 1 − P( f 90 i ,t ) − P( prepayi ,t ) . ˆ ˆ Where β pp and β f 90 represent the estimated prepayment and 90-day delinquency parameter vectors, while xi ,t and vi ,t represent the variables in the prepayment and delinquency equations for the ith loan at time period t.

The resulting prepayment probability represents the likelihood that loans will prepay in the current month, given that it has neither prepaid nor become 90 days delinquent in the prior month. The delinquency probability is similarly defined. Fifteen loan product specific models are estimated using historical loan-level data in addition to a single model for all modified loans. The treatment of performing modified loans is discussed in detail in Section 3.2.

The loan product models are based on the following eight products: Fixed Rate Products: 40yr. FRM, 30yr. FRM, 20yr.

FRM, 15yr. FRM Adjustable Rate Products: 10/1 ARM, 7/1 ARM, 5/1 ARM, 3/1 ARM, Page 6 . FHFA Mortgage Analytics Platform Separate loan product models are estimated for each Enterprise, with the exception of the fixed rate 40 year loan product and modified loans, which are estimated with data combined from both Enterprises due to the low volume of fixed rate 40 year loan product and modified loans. When possible, the entire historical population of loans is used for estimation. In the case of the fixed rate 30 year loans, a stratified proportional sample of three million loans is selected for each Enterprise. The stratification variables include: geography, credit scores, origination quarter, property type, loan size, original loan to value (LTV) and occupancy.

The marginal distributions of the population and the selected samples are compared to ensure representativeness to the loan population. These eight loan products for each GSE represent approximately 99 percent of the Enterprise mortgages originated since 1995. The remaining loans are comprised mostly of single family balloon mortgages and step rate mortgages. These loans are assigned to the product model based on their maturity term, for example, a 30 year step rate mortgage is assigned to the 30 year fixed rate model. 3.1 Common Independent Variables in the Performing Loan Module This section reviews the common independent variables across all of the estimated behavioral equations for performing loans.

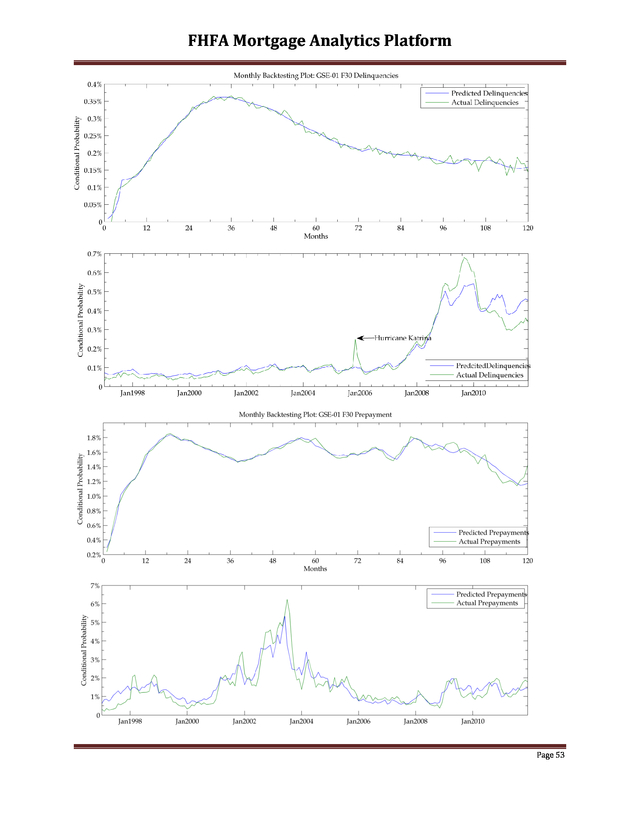

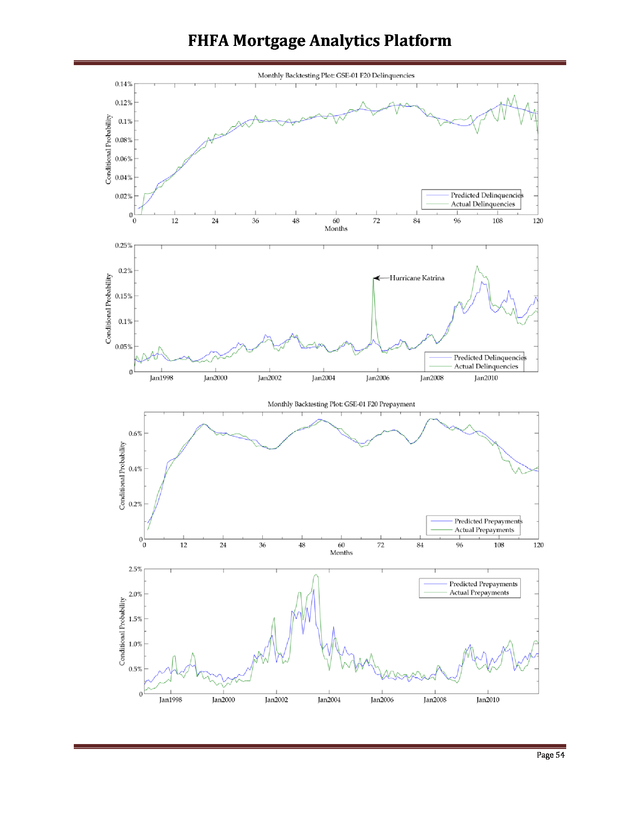

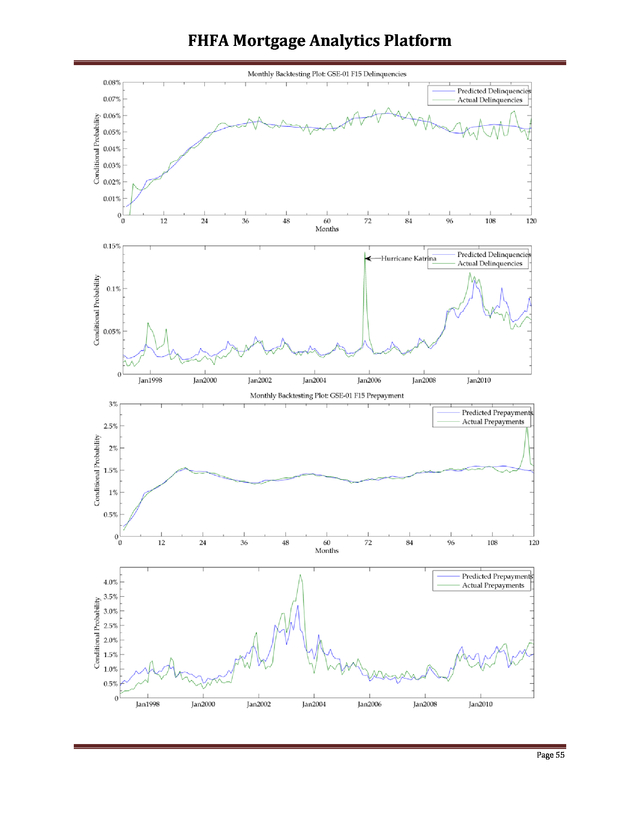

Most of the continuous explanatory variables are constructed as spline functions, with the locations of the spline knots varying across models 1. The parameter estimates, standardized errors, and the locations of spline knots are listed in Appendix B. Back-testing plots of each model is located in Appendix C. 3.1.1 Loan Seasoning The loan age, or seasoning, is included in the models to capture changes in the delinquency and prepayment tendencies over the life of the loan.

The seasoning functions in the models are constructed as a set of age spline variables; the spline knots The spline specification for continuous independent variables is a common practice in prepayment and default modeling (see Dunsky and Ho (2007), Bajari, Chu, and Park (2008), Tracey Seslen and William C. Wheaton (2010)). An important benefit of the spline specification is that it avoids sudden jumps within a continuous variable while allows for the non-linearity relationship between independent and dependent variable. 1 Page 7 .

FHFA Mortgage Analytics Platform are chosen from the product specific hazard curve(s) that best represents the product loan population 2. 3.1.2 Vintage-Fixed Effects In lieu of a constant term, each model is estimated with a series of vintage-specific fixed effects. The estimated fixed effects capture unobservable changes in underwriting standards and other non-observables that are not controlled for elsewhere in the model. 3.1.3 Seasonality All of the models include a set of eleven monthly indicators (dummy variables) to capture seasonality. Seasonality is a common phenomenon in mortgage performance: prepayments during the summer months are typically borrowers moving, while late payments frequently occur in April. The estimated seasonality parameters measure sensitivity of prepayment and delinquency relative to January, the omitted month. 3.1.4 Down Payment at Origination Down payment is measured in terms of the original loan-to-value (LTV) ratio; loan size is the balance of the loan at origination and value is the appraised value at origination. Underwriting requirements typically predetermine loan down payments.

Enterprise loans require a minimum original LTV of 80 on first lien mortgages, or, if the down payment is less than 20 percent, then a form of credit enhancement is required, (e.g. mortgage insurance) . The original LTV enters the model as a set of spline variables, where the spline knots are selected at approximately the 20th, 40th and 80th percentiles of original LTV in the estimation data. 3.1.5 Credit Score at Origination The Enterprises fully adopted credit scores in their underwriting criteria in the mid1990s. Nearly 100 percent of loans originated since 1995 in the estimation data contain credit scores.

Credit scores are typically reported from all three of the credit repositories. The model only uses one credit score per loan. When multiple scores are available per borrower, the model uses the lower of the two scores if two are reported, and the middle score if three scores are reported.

The lowest score across all borrowers is used when co-borrowers are reported in the loan data. Credit scores are specified as 2 The historical hazards are plotted from the loan populations even when sampling is required. Page 8 . FHFA Mortgage Analytics Platform five spline variables; the spline knots are selected based on the distribution of credit scores in the estimation data. 3.1.6 Spread at Origination (SATO) The SATO variable captures the difference between the borrower’s mortgage rate and the prevailing interest rate reported in the Primary Mortgage Market Survey (PMMS) on the date of the origination. Historically, this spread measures the borrower’s price of credit relative to the market average. To the extent that borrower credit is priced imperfectly, the SATO measure captures other unobservable in the transaction. There are two SATO spline variables (two spline segments, one spline knot) in each model. The spline knot is located at the median value of the difference between the initial rate on the mortgage and the market rate (PMMS rate) in the month of the first payment. 3.1.7 Loan Size at Origination Loan size (in thousands) is an important factor in the prepayment equation; the value of refinancing a loan is proportional to the size of the loan.

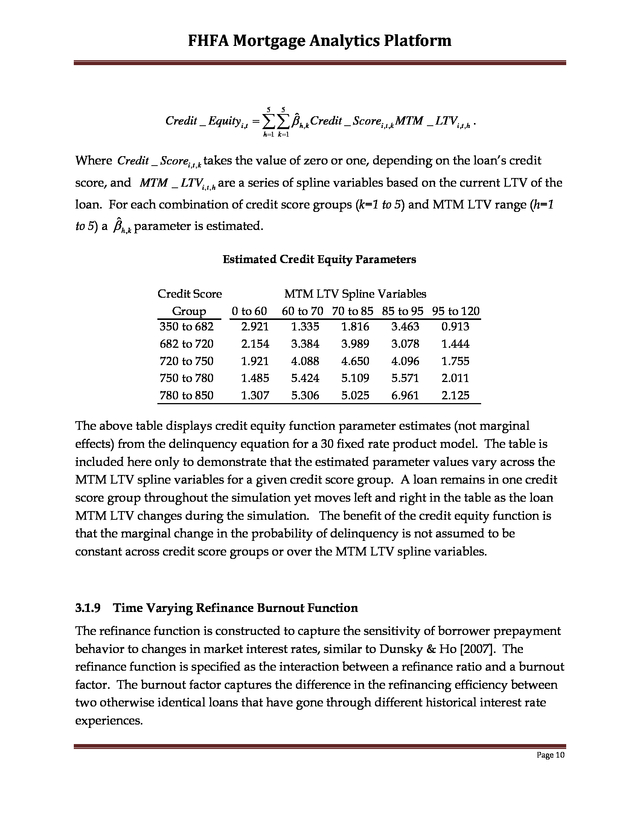

For some mortgage products, loan size is also inversely related to the incidence of delinquency. The loan size at origination enters the specification as a series of four spline variables; the spline knots are selected based on the distribution of loan size in the estimation data sets. 3.1.8 Time Varying Credit-Equity Function (Credit Score Current-LTV Interaction) The credit equity function is the interaction between the original credit score group indicator and spline variables of the current LTV (or mark-to-market LTV, MTM LTV) over the observed life of the loan, similar to Lam et al [2013] 3. The function enables measuring the borrower’s responsiveness to changes in current LTV while controlling for the borrower’s original credit score. There are (k) groups of credit score indicators; each borrower’s score falls uniquely into one of the five buckets (k=5).

The width of each bucket is based on the distribution observed in the estimation data. The time dependent MTM LTV ratio is expanded into (h) spline variables. The length and locations of the spline segments are defined from the estimation data.

The credit equity function in compact format for the ith loan in period t is defined as 3 LTVs are updated in the simulation model via house price indexes from the economic forecast database. The FHFA state-level purchase-only index is used for both model estimation and forecasting. Page 9 . FHFA Mortgage Analytics Platform 5 5 ˆ Credit _ Equityi ,t = ∑∑ β h ,k Credit _ Scorei ,t ,k MTM _ LTVi ,t ,h . h =1 k =1 Where Credit _ Scorei ,t , k takes the value of zero or one, depending on the loan’s credit score, and MTM _ LTVi ,t , h are a series of spline variables based on the current LTV of the loan. For each combination of credit score groups (k=1 to 5) and MTM LTV range (h=1 ˆ to 5) a β parameter is estimated. h, k Estimated Credit Equity Parameters Credit Score Group 0 to 60 350 to 682 2.921 682 to 720 2.154 720 to 750 1.921 750 to 780 1.485 780 to 850 1.307 MTM LTV Spline Variables 60 to 70 70 to 85 85 to 95 95 to 120 1.335 1.816 3.463 0.913 3.384 3.989 3.078 1.444 4.088 4.650 4.096 1.755 5.424 5.109 5.571 2.011 5.306 5.025 6.961 2.125 The above table displays credit equity function parameter estimates (not marginal effects) from the delinquency equation for a 30 fixed rate product model. The table is included here only to demonstrate that the estimated parameter values vary across the MTM LTV spline variables for a given credit score group. A loan remains in one credit score group throughout the simulation yet moves left and right in the table as the loan MTM LTV changes during the simulation.

The benefit of the credit equity function is that the marginal change in the probability of delinquency is not assumed to be constant across credit score groups or over the MTM LTV spline variables. 3.1.9 Time Varying Refinance Burnout Function The refinance function is constructed to capture the sensitivity of borrower prepayment behavior to changes in market interest rates, similar to Dunsky & Ho [2007]. The refinance function is specified as the interaction between a refinance ratio and a burnout factor. The burnout factor captures the difference in the refinancing efficiency between two otherwise identical loans that have gone through different historical interest rate experiences. Page 10 .

FHFA Mortgage Analytics Platform The refinance function is defined as refinance _ functioni ,t = refinance _ ratioi ,t * burnouti ,t , where  PMMSi ,t =0   refinance _ ratioi ,t =   PMMS  i ,t  ï£ The refinance ratio is constructed as the ratio of the Primary Mortgage Market Survey (PMMS) rate for the ith loan at origination (t=0) to the current period PMMS rate. The PMMS rate is the current mortgage rate at time t. The refinance ratio is a pure macroeconomic measure of the value of the refinance option and devoid of borrower specific credit information; this is in contrast to the spread at origination variable (SATO). The burnout factor is defined in terms of the significantly positive refinance spread cumulated over the age of the mortgage, reflecting missed refinance opportunities.

Explicitly the burnout function is defined as, T  PMMS i ,t =0 − PMMS i ,t  − 0.1,0  . burnout i ,t = ∑ MAX    PMMS i ,t t =0 ï£ ï£¸ We assume that a refinance opportunity occurs whenever the prevailing PMMS rate falls below the PMMS rate at origination by 10 percent. The refinance burnout function should have the qualitative behavior of an S curve, which typically represents the refinance incentive as a function of interest rates; when the refinance –ratio is low, there is a constant base refinancing rate. As the refinance ratio increases, the refinancing rate also increases. But when the refinance-ratio exceeds a certain level, the refinancing rate should remain stable, at a high level.

However, the behavior of this S function varies with the burnout level. The refinance function estimates multiple S functions as we categorize the loans into five buckets by the burnout function. The burnout refinance function is only included in the prepayment equations for the fixed rate products. Page 11 .

FHFA Mortgage Analytics Platform 3.1.10 State Unemployment Rate The unemployment rate serves as a proxy for job loss of the borrower as well as to capture local economic activity. Although prepayment is generally insensitive to the unemployment rate, the delinquency rate increases with the unemployment rate. There are four unemployment spline variables in each model. The selection of the spline knots is based on the distribution of the unemployment rate of the states represented in the input data. 3.1.11 Yield Curve Spread at Origination The yield curve spread, measured by the difference between the 2-year and the 10-year swap rate, captures the slope of the swap curve and serves as a proxy for the state of the macro-economy.

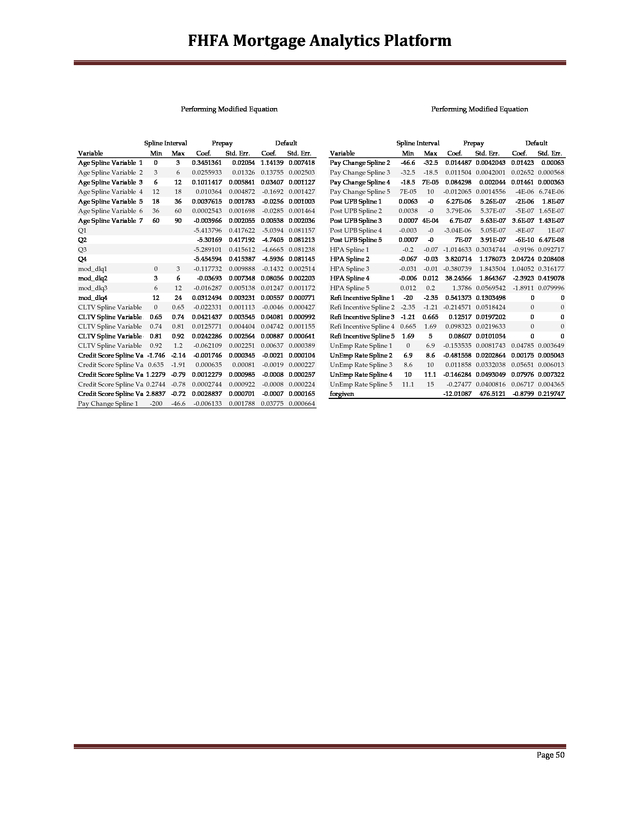

In the absence of large scale monetary intervention, empirical evidence suggests an upward sloping yield curve presents a healthy macro-economic environment. Existing borrowers would be expected to respond to a flattening of the yield curve when long term rates decline as a refinance opportunity. Alternatively, when the yield curve inverts, although refinance opportunities may persist, delinquencies typically increase reflecting a weaker macro-economic environment. Yield curve spread is only included in the prepayment equation. Parameter estimates, spline knots and back testing results of models discussed in the Performing Loan Module are located in Appendices B and C. 3.2 Special Treatment of Performing Modified Loans Performing modified loans include loans that have been modified through Home Affordable Modification Program (HAMP) or the Enterprises’ proprietary modification programs and have not re-defaulted (90+ days delinquent).

Performing modified loans are treated differently from unmodified performing loans. Modified loans, most of which were seriously delinquent before modification, have a higher likelihood of delinquency than unmodified performing loans. Modification of the mortgage terms (mortgage rate, amortization term and principal forbearance) and the delinquency status prior to modification are important variables in projecting the prepayment and re-default behaviors.

A single prepayment and re-default model is developed and deployed for all modified loans. The behavioral equations for modified loans are modeled in the same multinomial logit framework as unmodified performing loans described above. While most of the Page 12 . FHFA Mortgage Analytics Platform independent variables and all the economic variables used in the performing loan model are retained in the modified loan model, some independent variables are reconstructed. The reconstructed variables include loan age, seasonality, loan size and the refinance spread. Loan age for modified loans is measured from the modification date, and loan size is the post modification loan balance. Seasonality is captured by a quarterly dummy variable instead of a monthly dummy due to the short performance history of modified loans.

The refinance spread is defined as the modified interest rate of the mortgage minus the prevailing mortgage rate and is constructed as a spline variable. The independent variables for the performing loan behavioral equations that are not retained in the modified loans treatment are original vintage, original down payment, SATO and the credit equity function. Vintage is not considered for the modified loans treatment as most modified Enterprises loans were modified after 2009, and the underwriting environment has not changed significantly from 2009 to 2012. Down payment and SATO are also not retained as these two variables are not meaning given that loan has been modified.

Finally, the credit equity function is excluded to maintain a relatively simple structure for the modified loan equations. Additional independent variables are added to the behavioral equations for modified loans: Percentage Change in the Monthly Mortgage Payment: The monthly payment on most modified loans is reduced through interest rate reductions, term extensions or principal forbearance. The monthly payment reduction represents a financial relief to the distressed mortgage borrower and should reduce the borrower’s tendency to default on the loan. The percentage change in the monthly mortgage payment is constructed as a spline variable with the knots determined by the selected percentiles of the distribution of the monthly payment percentage change. Delinquency Status prior to Modification: Deeply delinquent borrowers face a greater financial challenge than less delinquent borrowers to bring the payment status of the loan back to current.

Deeply delinquent borrowers also have less flexibility to prepay the loan due to the large financial obligation of accrued or capitalized interest. The Delinquency Status prior to Modification is constructed as linear spline variables with knots at 3, 6 and 12 month delinquency. Page 13 . FHFA Mortgage Analytics Platform Home Price Appreciation since Modification: Home Price Appreciation since Modification is measured as a percentage change of the home price since modification at the state level. A positive home price appreciation indicates an improved borrower’s equity position in the property, and should reduce the borrower’s probability to redefault on the mortgage. Home Price Appreciation is measured at the state level and is constructed as linear spline variables with knots determined by selected percentiles of the distribution of the percentage of the home price change. The behavioral equations are estimated with performance history on Fannie Mae and Freddie Mac loans from June 2009 to December 2011. The estimated coefficients and back-testing results for the Modified Loan equations are included in Appendices B and C. Page 14 .

FHFA Mortgage Analytics Platform 4. Non-Performing Loan Module Loans enter into the non-performing module if they are 90 to 180 days delinquent at the beginning of the projection or if they are predicted to become 90-days or more delinquent (F90) during the forecast horizon. The module computes four mutually exclusive lifetime probabilities conditional on a loan being at least 90 days delinquent: re-performance (cure), voluntary prepayment, alternative foreclosure resolution, and foreclosure completion (REO). The lifetime probability of the loan resolving as real estate owned (REO) is calculated as the residual of one minus the other three computed probabilities.

The alternative foreclosure resolutions include deed-in-lieu of foreclosure, pre-foreclosure sale, and third party sale. Re-performance is defined as a loan returning to current status without having been modified or restructured. The loans that are projected to be re-performing are treated as performing loans and are sent back to the Performing Loan Module. The equations in the non-performing module are estimated simultaneously on a population of loans that became 90 days delinquent for the first time between 1997 and 2012.

The estimation data excludes loans that became 90 or more days delinquent and were subsequently modified. Conceptually, the resolution of delinquent loans is jointly determined by the borrower and the servicer. Information on servicers is unobservable; therefore the equations are a function of borrower, house characteristics and state legal structures.

The lifetime probability of each of the terminal states is represented below in a competing risks framework: ( ) ˆ  exp xi ,t ' β FCA P( LifetimeSalei ,t | f 90 i ,t ) =  ˆ ˆ ˆ  1 + exp x ' β i ,t FCA + exp vi ,t ' β RPerf + exp ω i ,t ' β PP ï£ ( ) ( ( ) ) ( ˆ  exp vi ,t ' β RPerf P ( RPerf i ,t | f 90 i ,t ) =  ˆ ˆ ˆ  1 + exp x ' β i ,t FCA + exp vi ,t ' β RPerf + exp ω i ,t ' β PP ï£ ( ) ( ) ( ) )         Page 15 . FHFA Mortgage Analytics Platform ( ) ˆ  exp ωi ,t ' β PP P (lifetimePrepayi ,t | f 90 i ,t ) =  ˆ ˆ ˆ  1 + exp x ' β i ,t FCA + exp vi ,t ' β RPerf + exp ω i ,t ' β PP ï£ ( ) ( ) ( )   , and   P( LifetimeREOi ,t | f 90i ,t ) = 1 − P( LifetimeSalei ,t | f 90i ,t ) − P( RPerfi ,t | f 90i ,t ) − P( LifetimePrepayi ,t | f 90i ,t ) . ˆ ˆ ˆ Where β FCA , β RPerf and β PP represent the equation specific parameters of exiting by a foreclosure alternative, re-performance and voluntary prepayment of the mortgage. The corresponding independent variable vectors are xi ,t , vi ,t and ωi, t for the ith loan at the time of the 90 day delinquency event, time t. The following subsection discusses the construction of the independent variables in the model. 4.1 Independent Variables in the Non-Performing Loan Module There are seven groups of independent variables in the non-performing loan model, and an intercept term. Similar to the performing modified loan model, only one model is deployed for all non-performing loans. Consideration of explanatory variables is restricted to variables that are observable in the month of the first 90 day delinquency and for which economic forecasts are available. 4.1.1 Current LTV at the Delinquency Date In order to capture the level of equity or negative equity in the property, the current LTV (MTM LTV) of the loan in the month of the first 90 day delinquency is included as five spline variables. The spline knots are located at 68%, 82%, 99% and 120% current LTV.

MTM LTV is calculated from the loan balance on the last paid installment, and house values are updated using the FHFA state-level purchase-only House Price Index. 4.1.2 Original Loan Size Similar to the performing loan module, original loan size (in thousands) is included in the model by five spline variables with knot locations based on the distribution of loan size in the delinquent loan data. The spline knots are located at $90k, $150k, $232k, and $360k. Page 16 . FHFA Mortgage Analytics Platform 4.1.3 Property Type The property type is represented by three indicator variables; condominium, planned urban development and manufactured housing. Single family detached residence serves as the comparator. 4.1.4 Stated Occupancy at Origination To differentiate between outcomes across owner occupants and non-owner occupants an indicator variable is included in all of the specifications. Relative to owner occupants, non-owner occupants are less likely to re-perform. 4.1.5 Mortgage Insurance Coverage For loans with mortgage insurance, two spline variables based on the level of insurance coverage are included in the specification. The spline knot is located at 25% coverage. The spline variables for loan without mortgage insurance are set at zero. 4.1.6 Credit Score at Origination Original credit scores enter into the model as five spline variables with spline knots located at 623, 661, 703, and 750.

Original credit scores may no longer accurately represent the borrower’s recent payment history, yet they remain statistically significant in the non-performing loan model. 4.1.7 State Unemployment at Delinquency Date Four unemployment spline variables are included in each model where the selection of the spline knots is based on the distribution of the unemployment rate of the states represented in the input data. The spline knots are located at 5.5, 7.8, and 10.3 percent. 4.1.8 Judicial State Indicator Lastly, a state legal structure indicator is included to control for variation in state foreclosure laws. The judicial state indicator is set to 1 when the loans is located in the following states: DE, FL, HI, IA, ID, IL, IN, KS, KY, LA, ND, NE, NJ, NM, NY, OH, OK, PA, SC, and SD.

In judicial foreclosure states, a lender is required to get a judgment against the borrower and a court order authorizing the sale of the property by an office of the court, (Hayre and Saraf, 2008). The foreclosure timelines in judicial states are longer than non-judicial states. As such, it is necessary to control for the local legal structures when modeling delinquent loan outcomes. Page 17 .

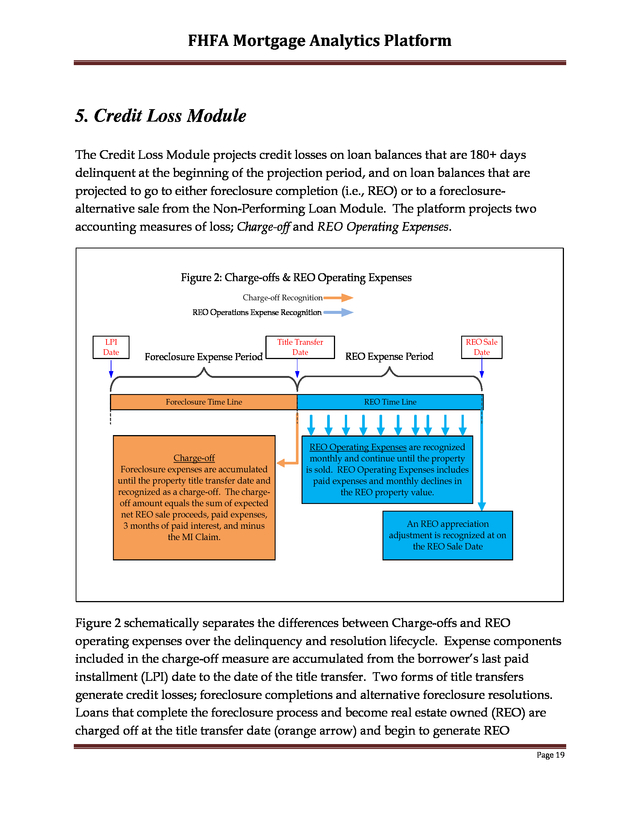

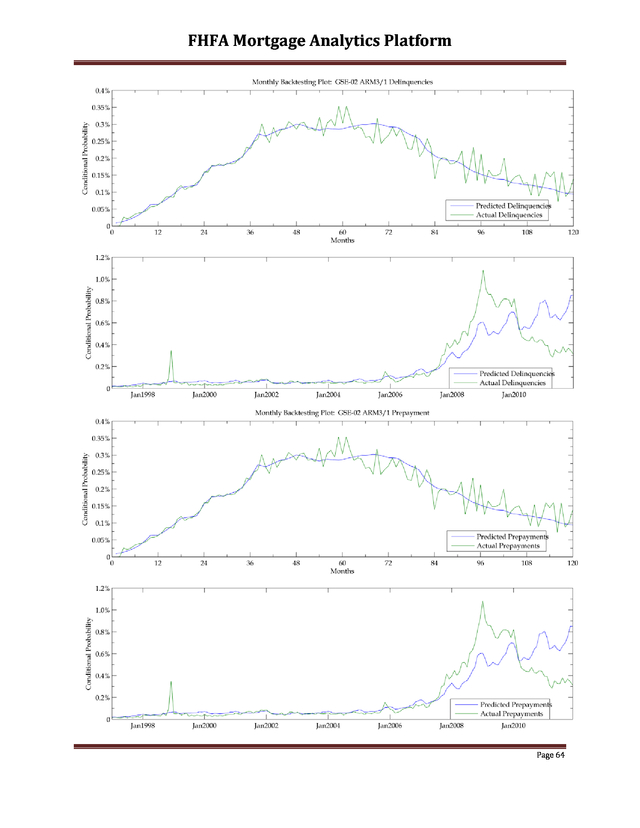

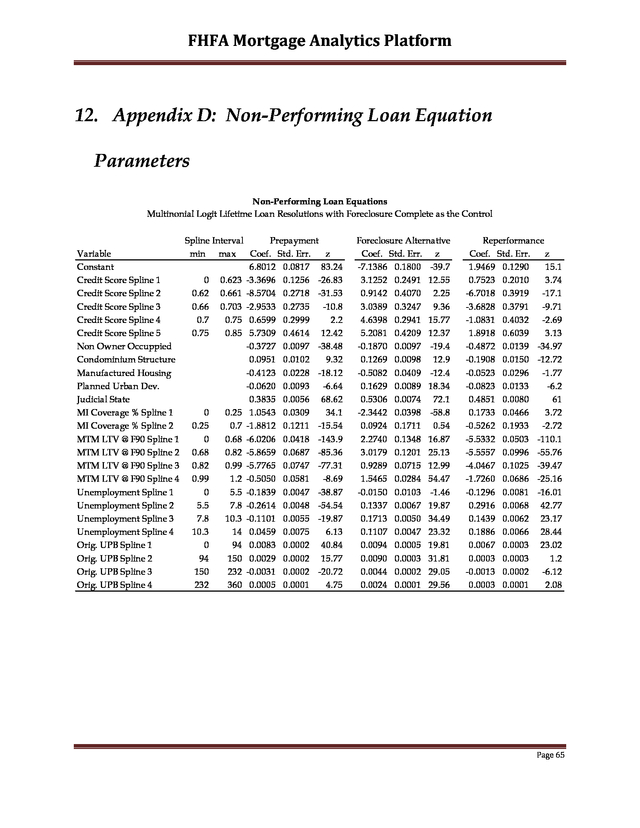

FHFA Mortgage Analytics Platform The estimated parameters for the equations of the non-performing loan module are provided in Appendix D. Page 18 . FHFA Mortgage Analytics Platform 5. Credit Loss Module The Credit Loss Module projects credit losses on loan balances that are 180+ days delinquent at the beginning of the projection period, and on loan balances that are projected to go to either foreclosure completion (i.e., REO) or to a foreclosurealternative sale from the Non-Performing Loan Module. The platform projects two accounting measures of loss; Charge-off and REO Operating Expenses. Figure 2: Charge-offs & REO Operating Expenses Charge-off Recognition REO Operations Expense Recognition LPI Date 6/1/2014 - 6/8/2014 Foreclosure Expense Period Foreclosure Time Line Charge-off Foreclosure expenses are accumulated until the property title transfer date and recognized as a charge-off. The chargeoff amount equals the sum of expected net REO sale proceeds, paid expenses, 3 months of paid interest, and minus the MI Claim. Title Transfer Date 6/1/2014 - 6/8/2014 REO Expense Period REO Sale Date REO Time Line REO Operating Expenses are recognized monthly and continue until the property is sold.

REO Operating Expenses includes paid expenses and monthly declines in the REO property value. An REO appreciation adjustment is recognized at on the REO Sale Date Figure 2 schematically separates the differences between Charge-offs and REO operating expenses over the delinquency and resolution lifecycle. Expense components included in the charge-off measure are accumulated from the borrower’s last paid installment (LPI) date to the date of the title transfer. Two forms of title transfers generate credit losses; foreclosure completions and alternative foreclosure resolutions. Loans that complete the foreclosure process and become real estate owned (REO) are charged off at the title transfer date (orange arrow) and begin to generate REO Page 19 .

FHFA Mortgage Analytics Platform operating expenses thereafter. Meanwhile, loans that terminate via an alternative foreclosure resolution are charged off at the title transfer date (orange arrow); these loans do not become REO and therefore do not generate REO operating expenses. The calculation of charge-offs for both forms of title transfer are identical, while only completed foreclosures generate losses captured in REO operating expense. In contrast to charge-offs, where expenses are accumulated over the foreclosure period and recognized on the title transfer date (orange arrow), REO Operating Expenses are calculated and recognized monthly (blue arrows). The sections below discuss the specifics of the recognition timing, charge-offs amounts, and REO Operations Expenses. 5.1 Charge-Off Timing Non-performing loans are charged off when the property title is transferred at the completion of the foreclosure process or at the culmination of an alternative foreclosure resolution 4.

The title-transfer timelines are calculated from historical data as the average number of months to complete the process in each state. The platform includes both a long run timeline and a stressed foreclosure timeline. The stressed timeline represents the average foreclosure timeline for loans that completed the foreclosure process (or alternative foreclosure resolution) during the December 2010 to December 2011 period.

The long-run average timelines are calculated from foreclosures (and alternatives) completed from January 1995 to December 2011. Non-performing loans with a level of delinquency greater than the historical state average foreclosure timelines require a special treatment. These loans are assumed to complete foreclosure (or an alternative foreclosure resolution) and be charged off during the first 12 months of the projection. To avoid concentrating all of the chargeoffs in a particular month, each of these loans were randomly assigned a charge-off date (based on a uniform distribution) during the first year of the projection. 5.2 Charge-Off Amount The charge-off amount represents the expected proceeds from the property sale net of all transaction costs, accrued expenses and credit enhancements. ð¶â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ = ð¸ð‘¥ð‘ð‘’ð‘ð‘¡ð‘’ð‘‘ ð‘ð‘’ð‘¡ ð‘…ð¸ð‘‚ ð‘†ð‘Žð‘™ð‘’ ð‘ƒð‘Ÿð‘œð‘ð‘’ð‘’ð‘‘ð‘ 4 Alternative foreclosure resolutions include deed-in-lieu of foreclosure, pre-foreclosure sale, and third party sales. Page 20 .

FHFA Mortgage Analytics Platform + ð‘ƒð‘Žð‘–ð‘‘ ð¸ð‘¥ð‘ð‘’ð‘›ð‘ ð‘’ð‘ + ð‘ƒð‘Žð‘–ð‘‘ ð¼ð‘›ð‘¡ð‘’ð‘Ÿð‘’ð‘ ð‘¡ − ð‘€ð¼ ð¶ð‘™ð‘Žð‘–ð‘š ð´ð‘šð‘œð‘¢ð‘›ð‘¡ More specifically, the charge-off amount is composed of four components: (1) Expected Net REO Sale Proceeds, (2) Paid Expenses during the Foreclosure Process, (3) Three Months of Lost Interest, and (4) the Mortgage Insurance Claim Amount. Each of these elements is discussed below. 5.2.1 Expected Net REO Sale Proceeds The expected net REO sale proceeds are calculated as, ð¸ð‘¥ð‘ð‘’ð‘ð‘¡ð‘’ð‘‘ ð‘ð‘’ð‘¡ ð‘…ð¸ð‘‚ ð‘†ð‘Žð‘™ð‘’ ð‘ƒð‘Ÿð‘œð‘ð‘’ð‘’ð‘‘ð‘ = �ð‘ˆð‘ƒðµ ∗ (1 + ð¹ð¶ ð¶ð‘œð‘ ð‘¡ð‘ )� − �ð‘…ð‘’ð‘œð‘†ð‘Žð‘™ð‘’ð‘ƒð‘Ÿð‘–ð‘ð‘’ ð‘¡+𑘠∗ (1 − ð‘†ð‘’ð‘¡ð‘¡ð‘™ð‘’ð‘šð‘’ð‘›ð‘¡ ð¶ð‘œð‘ ð‘¡ð‘ )� where �ð‘ˆð‘ƒðµ ∗ (1 + ð¹ð¶ ð‘ð‘œð‘ ð‘¡ð‘ )� represents the unpaid principal balance (UPB) scaled up by the foreclosure cost factor (1 + ð¹ð¶ ð‘ð‘œð‘ ð‘¡ð‘ ). The foreclosure cost factor is adapted from the Home Affordable Modification Program Net Present Value (HAMP NPV) model’s state-level averages of “Foreclosure and REO costs” as a percentage of UPB 5. The NPV model documentation indicates that these costs are comprised of the following. • • • • • • • • • • • • • • • Attorney and trustee fees Possessory and eviction fees and expenses Bankruptcy expenses Servicer liquidation expenses MI premium Flood insurance premium Title insurance Appraisal fees Property inspection Utilities Property maintenance/preservation Other foreclosure and holding costs Total repairs (capped at $3,000 to exclude discretionary repairs) Participation expenses Foreclosure costs paid out at property sale (from HUD-1) These items combine both foreclosure costs (which belong in charge-off) and REO costs (which do not belong in charge-off).

To balance out the inclusion of REO cost elements, The HAMP model documentation is available at, https://www.hmpadmin.com//portal/programs/docs/hamp_servicer/npvmodeldocumentationv502.pdf 5 Page 21 . FHFA Mortgage Analytics Platform the “Foreclosure and REO costs” are reduced by half when calculating the charge-off amount. The remaining half is allocated to REO operations expense in Section 5.3.2. The second part of expected net REO sale proceeds �ð‘…ð‘’ð‘œð‘†ð‘Žð‘™ð‘’ð‘ƒð‘Ÿð‘–ð‘ð‘’ ð‘¡+𑘠∗ (1 − ð‘†ð‘’ð‘¡ð‘¡ð‘™ð‘’ð‘šð‘’ð‘›ð‘¡ ð¶ð‘œð‘ ð‘¡ð‘ )� captures the expected revenue from the sale of the REO property net of brokerage fees and other settlement costs. REO sales price, denoted as ð‘…ð‘’ð‘œð‘†ð‘Žð‘™ð‘’ð‘ƒð‘Ÿð‘–ð‘ð‘’ ð‘¡+𑘠, represents the expected value at time period t given a foreclosure timeline of k months. REO property typically sells at a depressed price relative to a non-distressed transaction.

The REO sale price is calculated in two steps to account for the distressed nature of REO property. 1. The original value of the property is “marked forward” by the percentage change in the FHFA state-level purchase-only house price index between loan origination and charge-off date. 2. The “marked forward” value of the house is haircut by a state-level REO stigma correction. While many REO sales are cash transactions 6, the FHFA state-level purchase-only house price index includes a very small percentage of REO purchase transactions.

Therefore, it is necessary to adjust the REO property value in step 1 above by a state-level REO stigma. The REO stigma correction maps the relationship between FHFA state-level purchase-only house price index-based home values to distressed REO sales prices. REO stigma correction follows a modified version of the approach used in the HAMP Net Present Value (NPV) model 7. In contrast to the HAMP NPV model, where REO Sale prices are regressed on home values generated by an automated valuation model (AVM), the AVM prices are replaced by the property values in step 1 above (home values generated from the FHFA state-level purchase-only home price).

An REO stigma equation is estimated for each of the 50 states based on Enterprise data. For all alternative foreclosure resolutions, it is assumed that there is no REO stigma. See for example, http://www.corelogic.com/blog/authors/molly-boesel/2014/05/cash-sales-made-up-40-percent-of-totalhome-sales-in-february.aspx?WT.mc_id=crlg_140519_oBvIb&elq=a1f819d883a44c33952168e917f41adc#.U3osDfldV8E 6 Page 22 . FHFA Mortgage Analytics Platform The REO Sales price is reduced by settlement costs (1 − ð‘†ð‘’ð‘¡ð‘¡ð‘™ð‘’ð‘šð‘’ð‘›ð‘¡ ð¶ð‘œð‘ ð‘¡ð‘ ) as a percentage of the calculated REO disposition sale price, the percentage varies by state. The state-level settlement cost percentages are from the HAMP NPV model. Settlement Charges include: • • • • • • • • • • • • • 5.2.2 Discount Points Loan Origination Fees Broker’s Bonus Broker Commission Fees Buyer’s Closing Costs (paid by seller only—not total buyer’s closing costs) Title Fee Cost Seller’s Closing Costs Assessments FHA/VA Non-Allowable Costs Other Costs Wire Fees Subtract miscellaneous revenues received at property sale: o Per diem amount o Other rent/interest amount o Prepaid interest amount Paid Expenses during the Foreclosure Process There are three groups of expenses that are accumulated from the last paid installment to the foreclosure completion (or alternative foreclosure resolution) date: property taxes, property insurance, and maintenance costs. Lookup tables containing the three average expense rates are calculated from American Community Survey (ACS 2010) by location and property value. Apart from homeowners’ association fees or condominium fees, maintenance costs on single family homes are not reported in ACS. As a proxy for monthly maintenance cost on single family homes, it is assumed that the property maintenance costs are equal to one half homeowners’ association fees that would have been applied if the home belonged to a homeowners’ association. The expense rates are applied to the property value at loan origination and by geographic state to project these monthly expenses in dollars.

The monthly expenses Page 23 . FHFA Mortgage Analytics Platform are accumulated for every month between LPI date and foreclosure completion date and recognized on the charge-off date. 5.2.3 Paid Interest The module assumes that the loan servicer advances the borrower’s interest payment to investors for three months, and this amount is reimbursed to the loan servicer by the Enterprise when the loan is purchased out of the security. Three months of interest payments are included as an expense in the charge-off amount. 5.2.4 MI Claim Amount For loans with active MI coverage, the MI claim amount is limited to the insured UPB plus foreclosure expenses. Foreclosure expenses are equal to the expenses in charge-off plus lost interest for all months from the LPI date to foreclosure completion date. As noted in 5.2.3 above, only three months of lost interest is included in the charge-off measure. The model assumes that the MI Company will exercise their right to buy the foreclosed property (conveyance) in lieu of paying the MI Claim when the MI payment is greater than the sum of the charge-off and REO operating expenses.

In the case of conveyance, the value of the property is based on the FHFA state-level purchase-only house price index at the foreclosure completion date, not at the projected REO sale date. Both the charge-off and REO net expenses attributed to the Enterprise are zero when the MI Company purchases the foreclosed property. For loans with original LTV greater than 80% and with first pay date on or later than July 29, 1999, that coverage is projected to cancel at the earlier of: (a) the month after the loan’s amortization LTV reaches 78 percent, and (b) the month in which the loan’s age reaches one half its amortization term. 8 For loans originated before July 29, 1999 where the data indicate that MI coverage is in effect at the beginning of the projection, the coverage is never canceled. The calculated MI claim, whether or not the property conveys, is subject to the risk that the MI Company either fails to meet its obligations (e.g.

State regulator places the See 12 U.S. Code § 4902 - Termination of private mortgage insurance regarding the “automatic” and “final” termination provisions of section 3 of the Homeowners Protection Act of 1998. There is no projection of the borrower-initiated cancellation allowable under the Act. 8 Page 24 .

FHFA Mortgage Analytics Platform company into runoff), or the MI company denies the claims. To allow for these forms of counter party credit risk, the Module reduces the value of the calculated MI benefit by a “haircut” percentage. When the platform is run to measure counterparty exposures the haircut is assumed to be zero, yet when the platform is run to project GSE credit losses the haircut ranges between 20 and 25 percent. For alternative foreclosure resolutions, mortgage insurance is applied in the same way as it is with foreclosed loans. The conveyance calculation is identical to the one used for foreclosure, based on the idea that the MI would not make any payment beyond that which would reduce the Enterprise’s loss to zero. 5.3 REO Operations Expenses 5.3.1 REO Operation Expense Timing REO operation expenses are calculated and reported one month after foreclosure completion until the REO property is sold.

Similar to the foreclosure timings, the platform includes both a long run REO timeline and a stressful timeline. The stressed timeline represents the average state-level timelines for REO properties that were sold between December 2010 and December 2011. The long-run average timelines are calculated from REO sales completed from January 1995 to December 2011.

Both sets of REO sale time lines are computed from GSE historical data at the state level. 5.3.2 REO Operation Expense Amount REO operations expenses are posted monthly and calculated as the sum of (1) paid expenses and (2) mark-to-market REO property value changes. The REO expenses are the same as the expenses included in the charge-off amount; “Paid Expenses” described in Section 5.2.2 and the remaining 50% of the “Foreclosure and REO costs” allocated across the REO holding period. In contrast to the expenses in the charge-off amount, REO operating expenses are recognized each month while the property is held in inventory. Mark-to-market REO property values enter into the REO operations expense amount in two parts.

During the REO holding period, only declines in the value of the REO property are added to the monthly REO operations expenses. Increases in the REO property value are only included in the REO operating expenses when the property is Page 25 . FHFA Mortgage Analytics Platform sold. The mark-to-market property values are computed using projected FHFA statelevel purchase-only house price index. As noted above, if the calculated charge-off excluding the estimated MI payment is negative, both the charge-off and the REO operations expenses that would have been associated with the loan termination are set to zero. It is explicitly assumed that foreclosed or alternative foreclosures cannot generate gains. The best outcome for a non-performing loan is a zero credit loss. Page 26 .

FHFA Mortgage Analytics Platform 6. Integration Module This module integrates the prepayment and default probabilities from the Performing and Non-performing Modules with the outputs from the Credit Loss Module to project monthly loan-level cash flows. The primary outputs include scheduled and unscheduled principal payments, scheduled interest payments, and losses. Ancillary outputs include servicing fees, guaranty fee revenue, and MI payments. For each mortgage, the unpaid principal balance is projected forward one month by subtracting expected amounts of scheduled, prepaid (unscheduled), and defaulted principal from the performing balance (ð‘ˆð‘ƒðµ ð‘¡−1 ). ð‘ˆð‘ƒðµ ð‘¡+1 = ð‘ˆð‘ƒðµ ð‘¡−1 − ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘›ð‘ƒð‘Žð‘–ð‘‘ ð‘¡ − ð‘ð‘Ÿð‘’ð‘ð‘Žð‘¦ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡ − ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘ƒð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ − ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘…ð‘’𑜠𑡠− ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘†ð‘Žð‘™ð‘’ ð‘¡ . For expository purposes the above equation is separated into two parts, (1) scheduled and unscheduled principal, and (2) elements that are subtracted from performing balance that are directed to the credit losses (ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘…ð‘’𑜠𑡠, ð‘Žð‘›ð‘‘ ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘†ð‘Žð‘™ð‘’ ð‘¡ ). 6.1 Scheduled and Unscheduled Related Principal The scheduled and unscheduled principal payments include scheduled paid principal (schedPrinPaidt) net lifetime losses, unscheduled or prepaid principal (prepayDollarst) from performing balances, and unscheduled or prepaid principal from delinquent loans balances (dollarsF90toPrepayt).

More specifically, scheduled principal paid is defined as ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘›ð‘ƒð‘Žð‘–ð‘‘ ð‘¡ = ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘› ð‘¡ ∗ (1 − ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘…ð‘’𑜠𑡠|ð‘“90 ð‘¡ ) − ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘†ð‘Žð‘™ð‘’ ð‘¡ |ð‘“90 ð‘¡ )). And the remaining component (1 − ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘…ð‘’𑜠𑡠|ð‘“90 ð‘¡ ) − ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘†ð‘Žð‘™ð‘’ ð‘¡ |ð‘“90 ð‘¡ )) represents the portion of the balance related to foreclosure and foreclosure-alternative as described in the Non-Performing Module, Section 4. Prepaid dollars on performing loan balances (prepayDollarst) is defined as ð‘ð‘Ÿð‘’ð‘ð‘Žð‘¦ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡ = ð‘ƒ(ð‘ð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ ) ∗ (ð‘ˆð‘ƒðµ ð‘¡−1 − ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘› ð‘¡ ), Page 27 . FHFA Mortgage Analytics Platform Where ð‘ƒ(ð‘ð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ ) represents the probability of prepayment defined in Section 3, Performing Loan Module. The second term in the prepaid dollars equation (ð‘ˆð‘ƒðµ ð‘¡−1 − ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘› ð‘¡ ), represent the loan balances at risk of prepaying not of their scheduled principal payment. The final source of prepaid dollars is from repayments on non-performing loans. There are three components to ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘ƒð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ : (1) the probability of going 90 days delinquent from the performing loan module (Section 3), (2) the lifetime probability of prepaying given that the balance is delinquent from the Non-Performing Module (Section 4), and (3) the unpaid principal balance at risk. ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘ƒð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ = ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘ƒð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ |ð‘“90 ð‘¡ ) ∗ (ð‘ˆð‘ƒðµ ð‘¡−1 − ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘› ð‘¡ ) 6.2 Credit Loss Related Principal Non-performing loan balances resolving as REO or an alternative foreclosure resolution generate lost principal and contribute to the credit loss measures charge-off and REO operating expenses. These two components of principal are subtracted from the performing unpaid principal balance and represent the delinquent loan balances that are later used to calculate charge-offs. ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘…ð‘’𑜠𑡠= ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘…ð‘’𑜠𑡠|ð‘“90 ð‘¡ ) ∗ ð‘ˆð‘ƒðµ ð‘¡−1 ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘†ð‘Žð‘™ð‘’ ð‘¡ = ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘†ð‘Žð‘™ð‘’ ð‘¡ |ð‘“90 ð‘¡ ) ∗ ð‘ˆð‘ƒðµ ð‘¡−1 6.3 Credit Loss Measures Loan balance projected to go to REO or foreclosure-alternative sale lead to principal losses and are recognized as charge-offs.

The monthly expected values for foreclosurerelated charge-offs can be expressed in terms of the charge-off amount calculated in Section 5, ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡+𑘠= ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘…ð‘’𑜠𑡠|ð‘“90 ð‘¡ ) ∗ ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð‘¡+𑘠, or, equivalently for both foreclosure complete and alternative foreclosure resolutions, ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡+𑘠= (ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘…ð‘’𑜠𑡠/ð‘ˆð‘ƒðµ ð‘¡−1 ) ∗ ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð‘¡+𑘠Page 28 . FHFA Mortgage Analytics Platform ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡+𑘠= (ð‘‘ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð¹90ð‘‡ð‘œð‘†ð‘Žð‘™ð‘’ ð‘¡ /ð‘ˆð‘ƒðµ ð‘¡−1 ) ∗ ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð‘¡+𑘠where ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð‘¡+𑘠is the charge-off amount calculated in Section 6 (which would be the charge-off amount if the entire loan balance were going to foreclosure), and ð‘â„Žð‘Žð‘Ÿð‘”ð‘’ð‘‚ð‘“ð‘“ð·ð‘œð‘™ð‘™ð‘Žð‘Ÿð‘ ð‘¡+𑘠is the charge-off amount scaled to take account of the portion of the balance that is projected to go to foreclosure. The k subscript indicates that the charge-off will be realized following the appropriate foreclosure or alternative foreclosure time line. The logic for REO operating expenses is identical except that the charge-off amount is replaced with the REO Operating expense variable. Page 29 . FHFA Mortgage Analytics Platform 7. Standardized Report Elements The platform generates a summary report containing monthly projections of portfolio performance measures over the forecast horizon. The standard report includes key credit loss elements (charge-offs and REO operation expenses), and many ancillary variables: performing balances, dollars of new 90 day delinquencies, scheduled and unscheduled principal payments, guarantee fee income, and credit enhancement claims. Custom reports are frequently constructed to meet the needs of new projects, for example, aggregating credit losses by vintage year, credit score group, original LTV, and states. Most custom reports are aggregations of the variables in the standard report. The primary elements in the standardized report are aggregated across the portfolio and posted in the month of recognition: • • • • • • • • • Forecast Date – each row of the report corresponds to a future month during the forecast horizon for which the dollar amount is recognized. Performing UPB – is defined in Section 6 and represents aggregate unpaid principal balance in the forecast month that is at risk of defaults and prepayments (see Section 6). Scheduled Paid Principal Balance – is defined as aggregate scheduled principal paid on performing balances (see Section 6). Unscheduled Paid Principal –is defined as aggregate scheduled principal paid on performing balances.

Unscheduled principal includes prepayments from performing and non-performing loans. (see Section 6) Dollars of New 90 day Delinquencies (F90Dollars) - is defined as aggregate newly non-performing loan balances. Scheduled Interest Net of Fees – is defined as aggregate scheduled interest on loan balances before non-performing balances are removed. Paid Interest Net of Fees – is defined as aggregate paid interest on performing loan balances excluding servicing and guarantee fees. Paid Guarantee Fees – is defined as aggregate paid guarantee fees on performing loan balances. Non-Performing Lifetime Balances- three variables report the terminal outcome on non-performing balances in the future month in which they are recognized. Page 30 . FHFA Mortgage Analytics Platform • • • For example, loan balances projected to resolve as REO in month t will be recognized in a future date when foreclosure is completed. o 90 days delinquent balances completing the foreclosure process (REO) is calculated in Section 6 as ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘…ð‘’𑜠𑡠|ð‘“90 ð‘¡ ) ∗ ð‘ˆð‘ƒðµ ð‘¡−1 o 90 days delinquent balances completing the alternative foreclosure process is calculated in Section 6 as ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘†ð‘Žð‘™ð‘’ ð‘¡ |ð‘“90 ð‘¡ ) ∗ ð‘ˆð‘ƒðµ ð‘¡−1 o 90 days delinquent balances resolve as prepayments is calculated as ð‘ƒ(ð‘“90 ð‘¡ ) ∗ ð‘ƒ(ð‘™ð‘–ð‘“ð‘’ð‘¡ð‘–ð‘šð‘’ð‘ƒð‘Ÿð‘’ð‘ð‘Žð‘¦ ð‘¡ |ð‘“90 ð‘¡ ) ∗ (ð‘ˆð‘ƒðµ ð‘¡−1 − ð‘ ð‘â„Žð‘’ð‘‘ð‘ƒð‘Ÿð‘–ð‘› ð‘¡ ) Credit Loss Measures – Sections 5 and 6 discusses the construction and timing of both of the credit loss measures, Charge-Off Dollars and REO Operating Expenses. Charge-off Subcomponents (See Section 5) – the following components used to calculate charge-off are aggregated across the portfolio and contained in the standard report. These elements are posted in the month of the title transfer (recognition of losses). o Non-performing Balances o Property Value of Non-Performing Loans o Paid Expenses on non-performing loans during the foreclosure process o Three months of paid interest o 50% of “Foreclosure and REO costs” o Mortgage insurance claim amount REO Operations Expense Subcomponents (see Section 5) - the follow components used to calculate REO Operating Expenses are aggregated across the portfolio and contained in the standard report. These elements are recognized in the month they occur. o Monthly Paid Expenses & 50% of “Foreclosure and REO costs” on REO Properties o Mark-to-Market REO Property value declines o Mark-to-Market REO Property value increases at REO sale date Page 31 . FHFA Mortgage Analytics Platform 8. References Calhoun, C. A. and Y Deng, “ A Dynamic Analysis of Fixed- and Adjustable- Rate Mortgage Terminations, “ Journal of Real Estate Finance and Economics, 24 (1/2): 9-33, 2002. Clapp, John M., Deng, Yongheng and An, Xudong, "Unobserved Heterogeneity in Models of Competing Mortgage Termination" (August 22, 2005).

Available at SSRN: http://ssrn.com/abstract=512624 Dunsky, Robert M., and Thomas S.Y. Ho. (2007) "Valuing Fixed Rate Mortgage Loans with Default and Prepayment Options" The Journal of Fixed Income, Vol.

16, No. 4: 7-31. Hayre, Lahkbir and Robert Yong (2001), “Anatomy of Prepayments” The Salomon Smith Barney Prepayment Model in Salomon Smith Barney Guide to Mortgage-Backed and Asset Backed Securities. Ed Lakhir Hayre, John Wiley & Company; New York NY. Hayre, Lahkbir and Saraf Manish (2008), “A Loss Severity Model fro Residential Mortgages” CITI Research Paper. Jenkins, Stephen P.

(1995) "Easy Estimation Methods for Discrete-Time Duration Models." Oxford Bulletin of Economics and Statistics, Volume 57, Issue 1, pages 129–136. Pence, Karen M. (2006) “Foreclosing On Opportunity: State Laws and Mortgage Credit.” The Review of Economics and Statistics, February 2006, 88(1): 177–182. Lam, Ken, Robert M.Dunsky, and Austin Kelly (2013) "Impacts of Down Payment Underwriting Standards on Loan Performance" FHFA Working Paper 13-3. Patrick Bajari, Chenghuan Sean Chu, Minjung Park (2008) “An Empirical Model of Subprime Mortgage Default From 2000 to 2007”, NBER Working Paper No. 14625, December 2008. Page 32 .

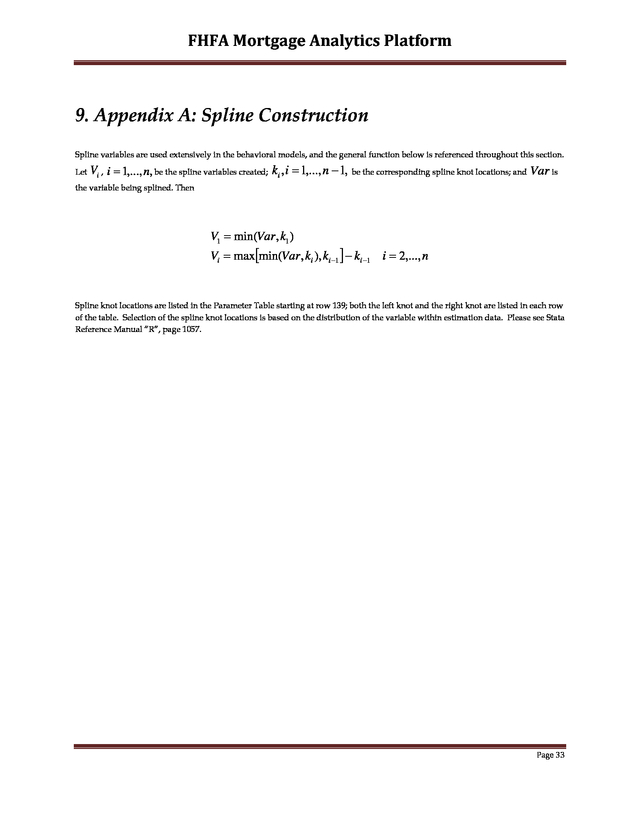

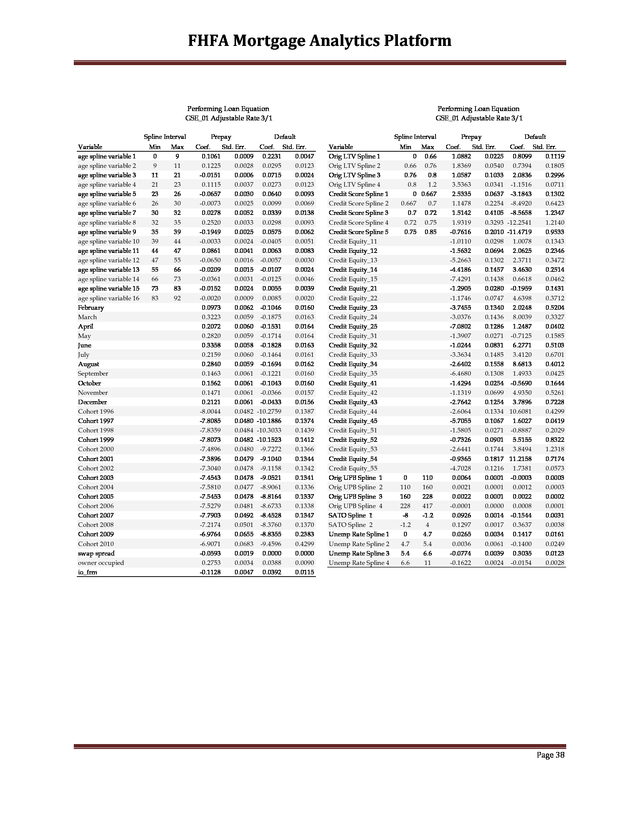

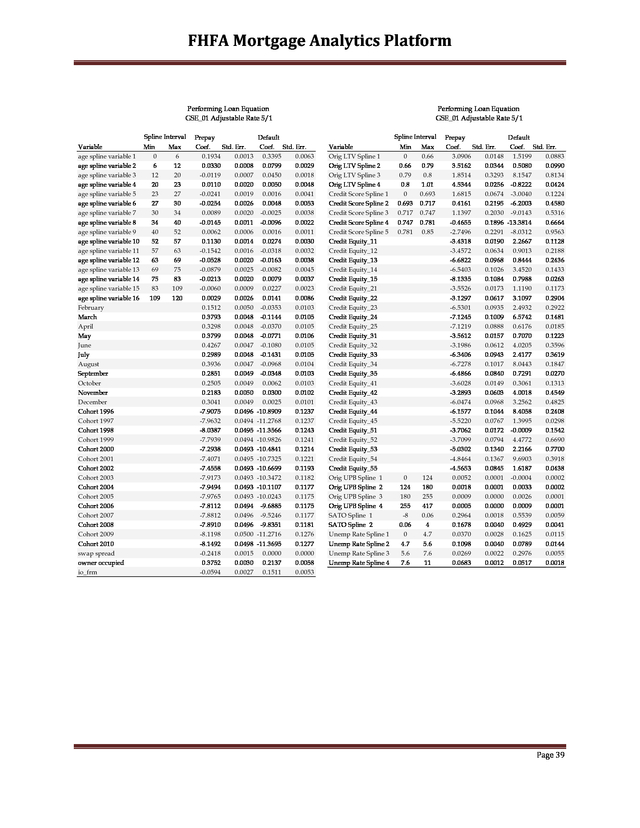

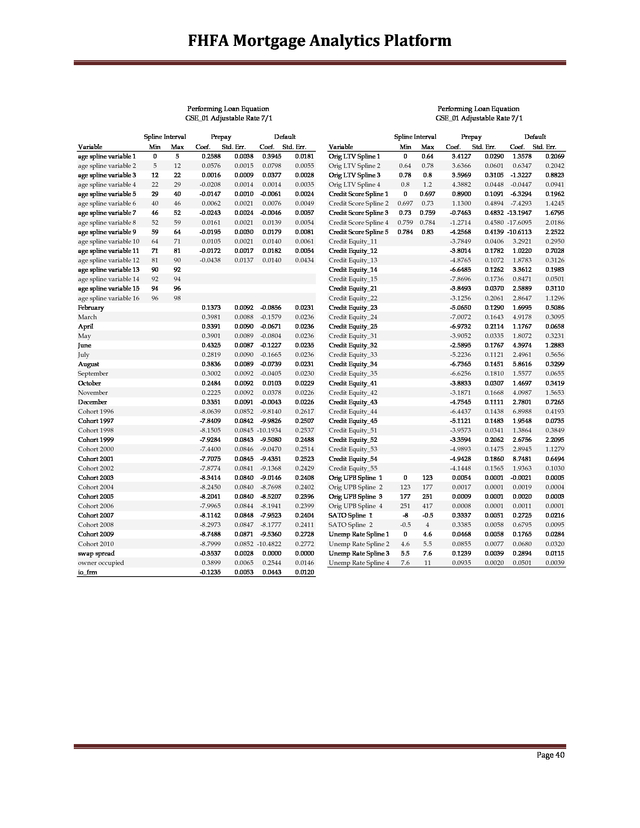

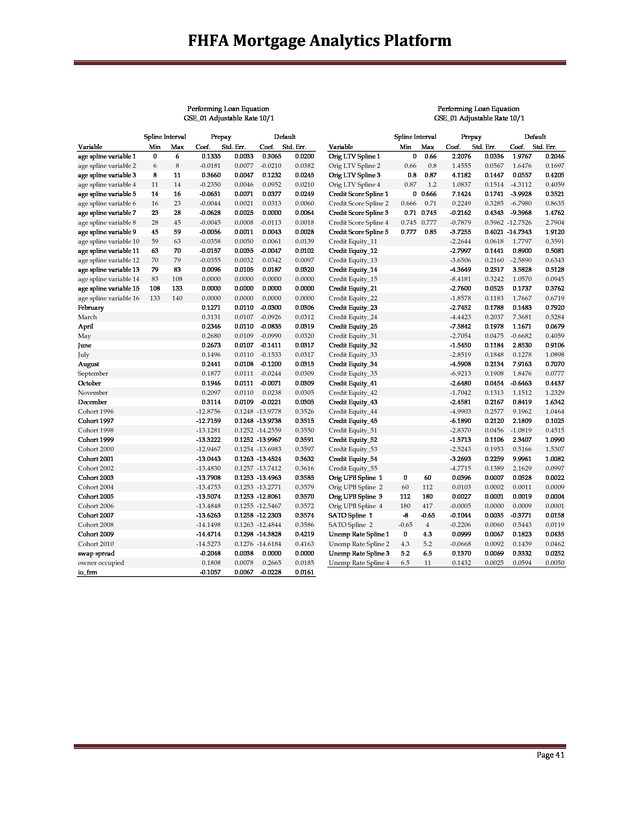

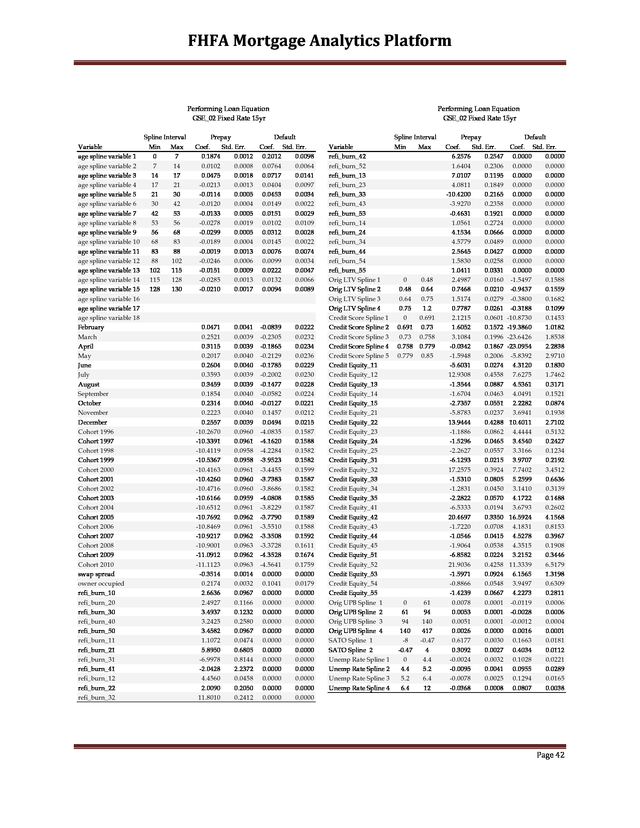

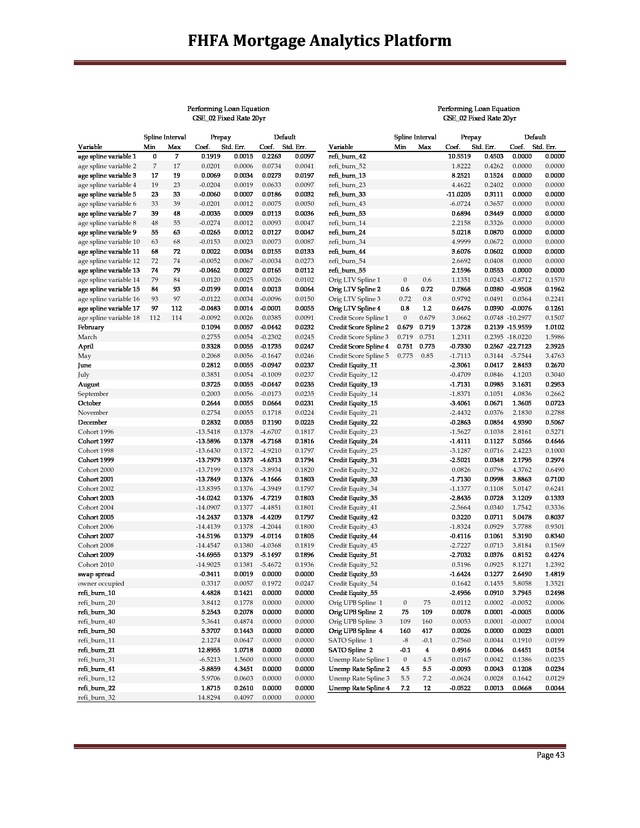

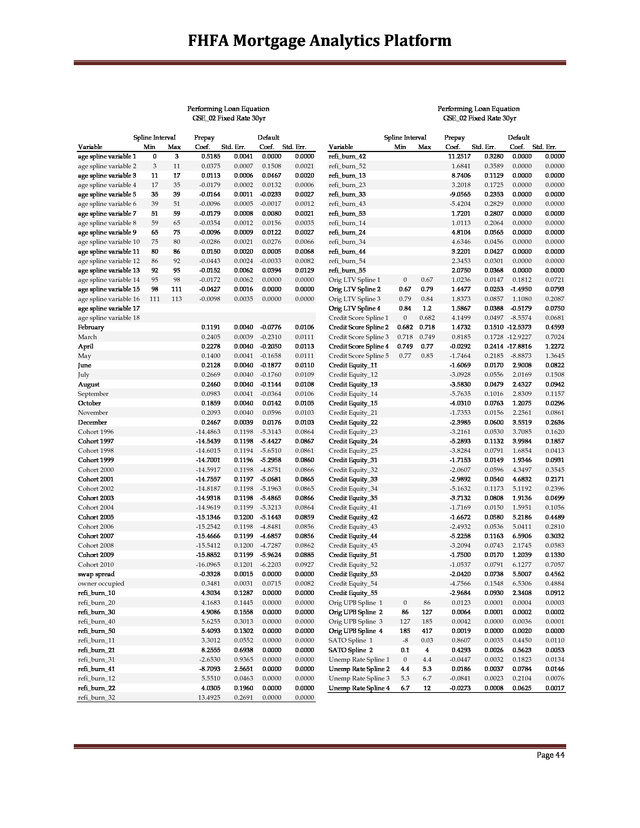

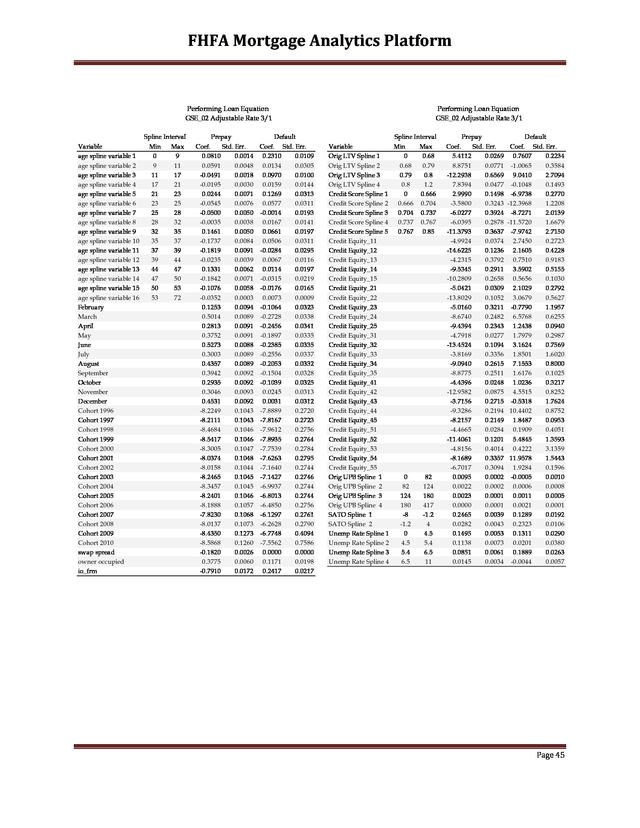

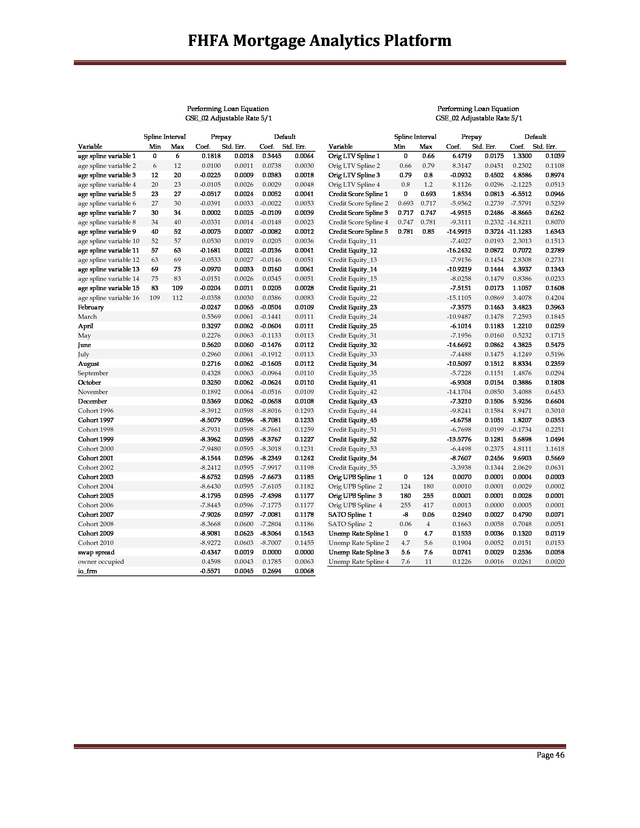

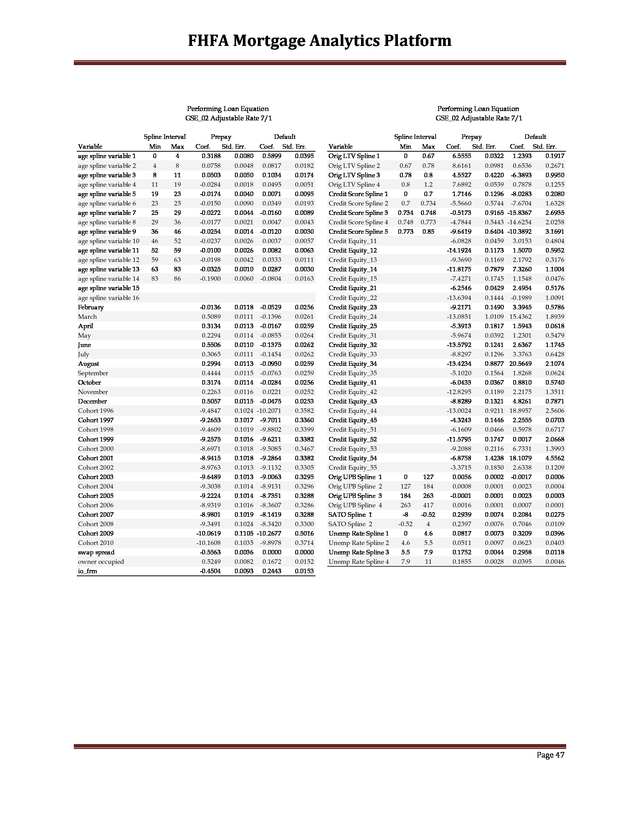

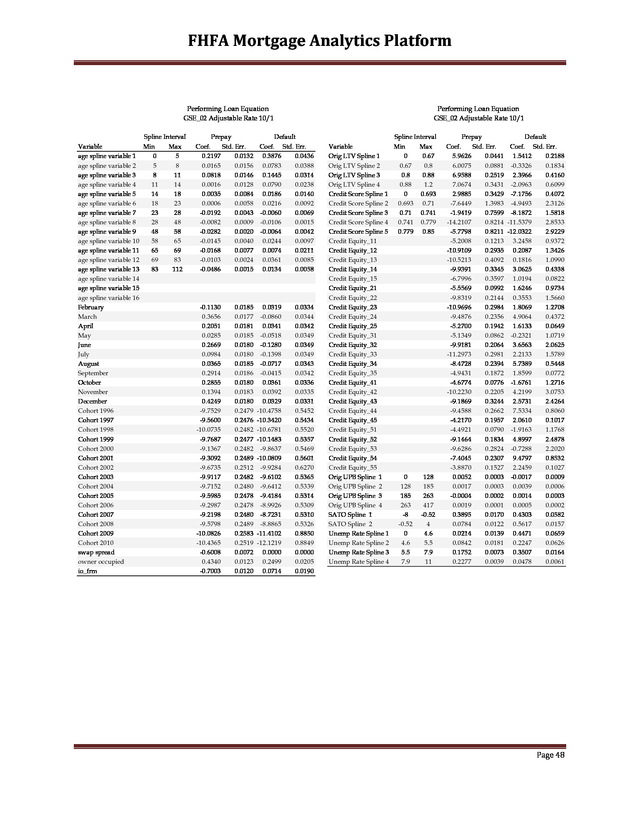

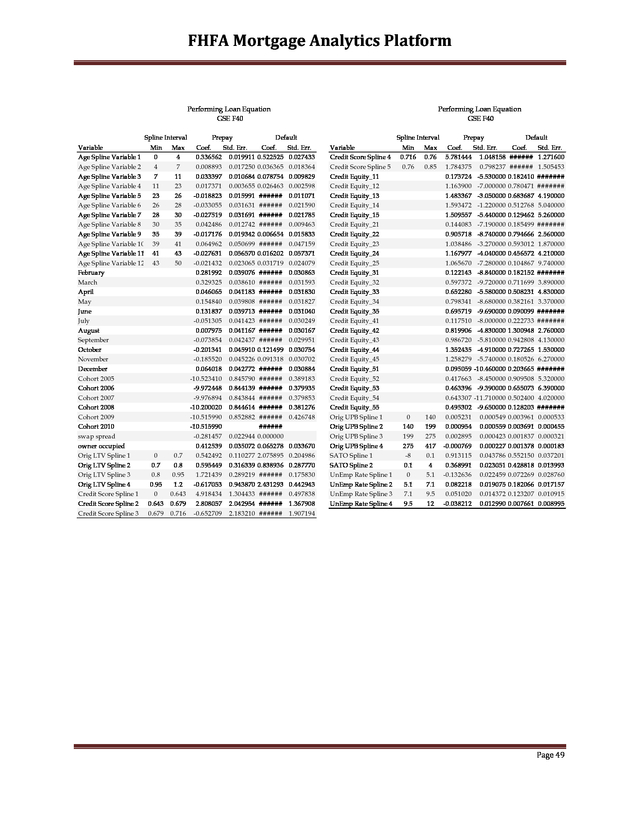

FHFA Mortgage Analytics Platform 9. Appendix A: Spline Construction Spline variables are used extensively in the behavioral models, and the general function below is referenced throughout this section. Let Vi , i = 1,..., n, be the spline variables created; ki , i = 1,..., n − 1, be the corresponding spline knot locations; and Var is the variable being splined. Then V1 = min(Var , k1 ) Vi = max[min(Var , ki ), ki −1 ] − ki −1 i = 2,..., n Spline knot locations are listed in the Parameter Table starting at row 139; both the left knot and the right knot are listed in each row of the table. Selection of the spline knot locations is based on the distribution of the variable within estimation data.

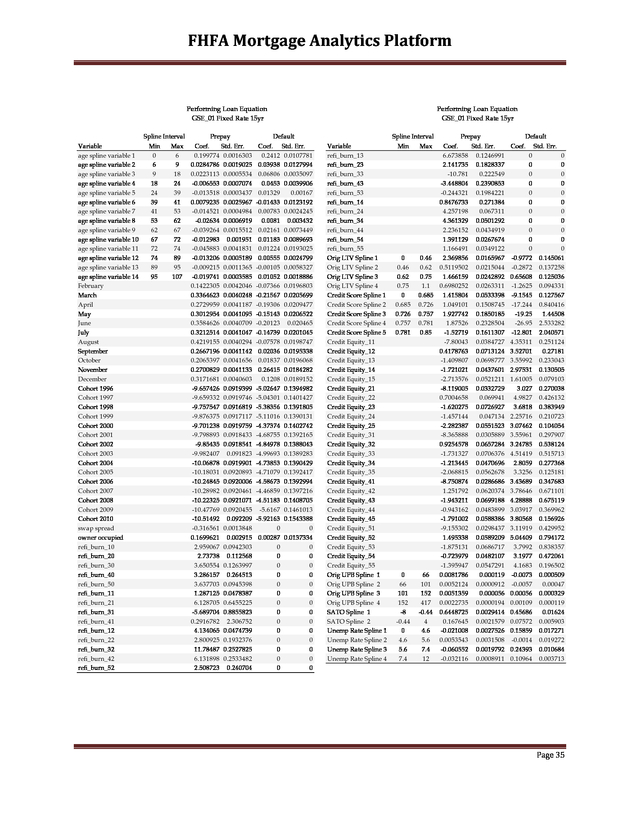

Please see Stata Reference Manual “R”, page 1057. Page 33 . FHFA Mortgage Analytics Platform 10. Appendix B: Performing Loan Module Model Coefficients Page 34 . FHFA Mortgage Analytics Platform Performing Loan Equation GSE_01 Fixed Rate 15yr Performing Loan Equation GSE_01 Fixed Rate 15yr Spline Interval Variable age spline variable 1 age spline variable 2 age spline variable 3 age spline variable 4 age spline variable 5 age spline variable 6 age spline variable 7 age spline variable 8 age spline variable 9 age spline variable 10 age spline variable 11 age spline variable 12 age spline variable 13 age spline variable 14 February March April May June July August September October November December Cohort 1996 Cohort 1997 Cohort 1998 Cohort 1999 Cohort 2000 Cohort 2001 Cohort 2002 Cohort 2003 Cohort 2004 Cohort 2005 Cohort 2006 Cohort 2007 Cohort 2008 Cohort 2009 Cohort 2010 swap spread owner occupied refi_burn_10 refi_burn_20 refi_burn_30 refi_burn_40 refi_burn_50 refi_burn_11 refi_burn_21 refi_burn_31 refi_burn_41 refi_burn_12 refi_burn_22 refi_burn_32 refi_burn_42 refi_burn_52 Min 0 6 9 18 24 39 41 53 62 67 72 74 89 95 Max 6 9 18 24 39 41 53 62 67 72 74 89 95 107 Prepay Default Coef. Std. Err. 0.199774 0.0016303 0.0284786 0.0019025 0.0223113 0.0005534 -0.006553 0.0007074 -0.013518 0.0003437 0.0079235 0.0025967 -0.014521 0.0004984 -0.02634 0.0006919 -0.039264 0.0015512 -0.012983 0.001951 -0.045883 0.0041831 -0.013206 0.0005189 -0.009215 0.0011365 -0.019741 0.0003585 0.1422305 0.0042046 0.3364623 0.0040248 0.2729959 0.0041187 0.3012954 0.0041095 0.3584626 0.0040709 0.3212514 0.0041047 0.4219155 0.0040294 0.2667196 0.0041142 0.2065397 0.0041656 0.2700829 0.0041133 0.3171681 0.0040603 -9.657426 0.0919399 -9.659332 0.0919746 -9.757547 0.0916819 -9.876375 0.0917117 -9.701238 0.0919759 -9.798893 0.0918433 -9.85435 0.0918541 -9.982407 0.091823 -10.06878 0.0919901 -10.18031 0.0920893 -10.24845 0.0920006 -10.28982 0.0920461 -10.22325 0.0921071 -10.47769 0.0920455 -10.51492 0.092209 -0.316561 0.0013848 0.1699621 0.002915 2.959067 0.0942303 2.73738 0.112568 3.650554 0.1263997 3.286157 0.264513 3.637703 0.0945398 1.287125 0.0478387 6.128705 0.6455225 -5.689704 0.8855823 0.2916782 2.306752 4.134065 0.0474739 2.800925 0.1932376 11.78487 0.2527825 6.131898 0.2533482 2.508723 0.240704 Coef. Std. Err. 0.2412 0.0107781 0.03938 0.0127994 0.06806 0.0035097 0.0453 0.0039906 0.01329 0.00167 -0.01433 0.0123192 0.00783 0.0024245 0.0081 0.003432 0.02161 0.0073449 0.01183 0.0089693 0.01224 0.0193025 0.00555 0.0024799 -0.00105 0.0058327 0.01052 0.0018886 -0.07366 0.0196803 -0.21567 0.0205699 -0.19306 0.0209477 -0.15143 0.0206522 -0.20123 0.020465 -0.14739 0.0201045 -0.07578 0.0198747 0.02036 0.0195338 0.01837 0.0196068 0.26415 0.0184282 0.1208 0.0189152 -5.02647 0.1394982 -5.04301 0.1401427 -5.38356 0.1391805 -5.11016 0.1390131 -4.37374 0.1402742 -4.68755 0.1392165 -4.84978 0.1388043 -4.99693 0.1389283 -4.73853 0.1390429 -4.71079 0.1392417 -4.58673 0.1392994 -4.46859 0.1397216 -4.51183 0.1408705 -5.6167 0.1461013 -5.92163 0.1543388 0 0 0.00287 0.0137334 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Spline Interval Variable refi_burn_13 refi_burn_23 refi_burn_33 refi_burn_43 refi_burn_53 refi_burn_14 refi_burn_24 refi_burn_34 refi_burn_44 refi_burn_54 refi_burn_55 Orig LTV Spline 1 Orig LTV Spline 2 Orig LTV Spline 3 Orig LTV Spline 4 Credit Score Spline 1 Credit Score Spline 2 Credit Score Spline 3 Credit Score Spline 4 Credit Score Spline 5 Credit Equity_11 Credit Equity_12 Credit Equity_13 Credit Equity_14 Credit Equity_15 Credit Equity_21 Credit Equity_22 Credit Equity_23 Credit Equity_24 Credit Equity_25 Credit Equity_31 Credit Equity_32 Credit Equity_33 Credit Equity_34 Credit Equity_35 Credit Equity_41 Credit Equity_42 Credit Equity_43 Credit Equity_44 Credit Equity_45 Credit Equity_51 Credit Equity_52 Credit Equity_53 Credit Equity_54 Credit Equity_55 Orig UPB Spline 1 Orig UPB Spline 2 Orig UPB Spline 3 Orig UPB Spline 4 SATO Spline 1 SATO Spline 2 Unemp Rate Spline 1 Unemp Rate Spline 2 Unemp Rate Spline 3 Unemp Rate Spline 4 Min Max 0 0.46 0.62 0.75 0 0.685 0.726 0.757 0.781 0.46 0.62 0.75 1.1 0.685 0.726 0.757 0.781 0.85 0 66 101 152 -8 -0.44 0 4.6 5.6 7.4 66 101 152 417 -0.44 4 4.6 5.6 7.4 12 Prepay Coef. Std.

Err. 6.673858 0.1246991 2.141735 0.1828337 -10.781 0.222549 -3.448804 0.2390853 -0.244321 0.1984221 0.8476733 0.271384 4.257198 0.067311 4.361329 0.0501292 2.236152 0.0434919 1.391129 0.0267674 1.166491 0.0349122 2.369856 0.0165967 0.5119502 0.0215044 1.466159 0.0242892 0.6980252 0.0263311 1.415804 0.0533398 1.049101 0.1508745 1.927742 0.1850185 1.87526 0.2328504 -1.52719 0.1611307 -7.80043 0.0384727 0.4178763 0.0713124 -1.409807 0.0698777 -1.721021 0.0437601 -2.713576 0.0521211 -8.119005 0.0332729 0.7004658 0.069941 -1.620275 0.0726927 -1.457144 0.047134 -2.282387 0.0551523 -8.365888 0.0305889 0.9254578 0.0657284 -1.731327 0.0706376 -1.213445 0.0470696 -2.068815 0.0562678 -8.750874 0.0286686 1.251792 0.0620374 -1.943211 0.0699188 -0.943162 0.0483899 -1.791002 0.0588386 -9.155302 0.0298437 1.495338 0.0589209 -1.875131 0.0686717 -0.723979 0.0482107 -1.395947 0.0547291 0.0081786 0.000119 0.0052124 0.0000912 0.0051359 0.000056 0.0022735 0.0000194 0.6448725 0.0029414 0.167645 0.0021579 -0.021008 0.0027526 0.0053543 0.0031508 -0.060552 0.0019792 -0.032116 0.0008911 Default Coef. 0 0 0 0 0 0 0 0 0 0 0 -0.9772 -0.2872 0.65608 -1.2625 -9.1545 -17.244 -19.25 -26.95 -12.801 4.35311 3.52701 3.55992 2.97531 1.61005 3.027 4.9827 3.6818 2.25716 3.07462 3.55961 3.24785 4.51419 2.8059 3.3256 3.43689 3.78646 4.28888 3.03917 3.80568 3.11919 5.04409 3.7992 3.1977 4.1683 -0.0073 -0.0057 0.00056 0.00109 0.45686 0.07572 0.15859 -0.0014 0.24393 0.10964 Std. Err. 0 0 0 0 0 0 0 0 0 0 0 0.145061 0.137258 0.125036 0.094331 0.127567 0.840416 1.44508 2.533282 2.040571 0.251124 0.27181 0.233043 0.130505 0.079103 0.270038 0.426132 0.383949 0.210723 0.104054 0.297907 0.538124 0.515713 0.277368 0.125181 0.347683 0.671101 0.675119 0.369962 0.156926 0.429952 0.794172 0.838357 0.472061 0.196502 0.000509 0.00047 0.000329 0.000119 0.01624 0.005903 0.017271 0.019272 0.010684 0.003713 Page 35 . FHFA Mortgage Analytics Platform Performing Loan Equation GSE_01 Fixed Rate 20yr Performing Loan Equation GSE_01 Fixed Rate 20yr Spline Interval Variable age spline variable 1 age spline variable 2 age spline variable 3 age spline variable 4 age spline variable 5 age spline variable 6 age spline variable 7 age spline variable 8 age spline variable 9 age spline variable 10 age spline variable 11 age spline variable 12 age spline variable 13 age spline variable 14 February March April May June July August September October November December Cohort 1996 Cohort 1997 Cohort 1998 Cohort 1999 Cohort 2000 Cohort 2001 Cohort 2002 Cohort 2003 Cohort 2004 Cohort 2005 Cohort 2006 Cohort 2007 Cohort 2008 Cohort 2009 Cohort 2010 swap spread owner occupied refi_burn_10 refi_burn_20 refi_burn_30 refi_burn_40 refi_burn_50 refi_burn_11 refi_burn_21 refi_burn_31 refi_burn_41 refi_burn_12 refi_burn_22 refi_burn_32 refi_burn_42 refi_burn_52 Min 0 6 17 20 33 35 39 45 53 66 72 75 80 83 Max 6 17 20 33 35 39 45 53 66 72 75 80 83 86 Prepay Default Coef. Std. Err. Coef. Std. Err. 0.2187 0.0016 0.2823 0.0090 0.0243 0.0005 0.0688 0.0026 -0.0139 0.0016 0.0519 0.0073 -0.0073 0.0005 0.0181 0.0018 -0.0333 0.0037 0.0043 0.0134 -0.0250 0.0022 -0.0047 0.0078 0.0099 0.0012 0.0014 0.0046 -0.0195 0.0008 0.0124 0.0031 -0.0307 0.0005 0.0062 0.0020 -0.0022 0.0015 0.0004 0.0054 -0.0254 0.0036 0.0122 0.0130 -0.0394 0.0026 0.0082 0.0090 0.0076 0.0046 0.0174 0.0159 0.0238 0.0041 -0.0279 0.0150 0.2036 0.0048 -0.1145 0.0176 0.3743 0.0046 -0.2584 0.0184 0.2563 0.0048 -0.1812 0.0185 0.3236 0.0048 -0.1709 0.0184 0.3821 0.0047 -0.1746 0.0180 0.3091 0.0048 -0.1462 0.0178 0.4558 0.0047 -0.0349 0.0174 0.2951 0.0047 0.0479 0.0172 0.2331 0.0048 0.0453 0.0172 0.3551 0.0047 0.1979 0.0165 0.3813 0.0047 0.1023 0.0168 -12.6431 0.1037 -7.0959 0.1222 -12.4992 0.1037 -6.7061 0.1217 0.1198 -12.5612 0.1033 -6.9252 -12.7289 0.1034 -6.5967 0.1197 -12.6719 0.1037 -6.0168 0.1213 -12.7201 0.1035 -6.1587 0.1202 -12.7865 0.1036 -6.3304 0.1200 0.1202 -12.9115 0.1036 -6.6682 -12.9903 0.1037 -6.4116 0.1201 0.1200 -13.1271 0.1038 -6.3716 -13.2767 0.1038 -6.0999 0.1202 -13.3498 0.1038 -5.9050 0.1205 -13.3019 0.1039 -5.8551 0.1213 -13.6550 0.1037 -7.0625 0.1254 -13.7726 0.1039 -6.9531 0.1274 -0.3167 0.0016 0.0000 0.0000 0.0486 0.0162 0.2582 0.0044 0.0000 0.0000 3.6871 0.1090 3.3282 0.1436 0.0000 0.0000 3.8858 0.1877 0.0000 0.0000 0.0000 4.1323 0.4131 0.0000 4.5235 0.1113 0.0000 0.0000 0.0000 2.5844 0.0531 0.0000 10.0437 0.9297 0.0000 0.0000 -1.0869 1.5361 0.0000 0.0000 0.0000 -1.4109 3.7027 0.0000 5.1317 0.0518 0.0000 0.0000 0.0000 2.8782 0.2241 0.0000 15.0422 0.3675 0.0000 0.0000 10.0460 0.3724 0.0000 0.0000 2.3733 0.3592 0.0000 0.0000 Spline Interval Variable refi_burn_13 refi_burn_23 refi_burn_33 refi_burn_43 refi_burn_53 refi_burn_14 refi_burn_24 refi_burn_34 refi_burn_44 refi_burn_54 refi_burn_55 Orig LTV Spline 1 Orig LTV Spline 2 Orig LTV Spline 3 Orig LTV Spline 4 Credit Score Spline 1 Credit Score Spline 2 Credit Score Spline 3 Credit Score Spline 4 Credit Score Spline 5 Credit Equity_11 Credit Equity_12 Credit Equity_13 Credit Equity_14 Credit Equity_15 Credit Equity_21 Credit Equity_22 Credit Equity_23 Credit Equity_24 Credit Equity_25 Credit Equity_31 Credit Equity_32 Credit Equity_33 Credit Equity_34 Credit Equity_35 Credit Equity_41 Credit Equity_42 Credit Equity_43 Credit Equity_44 Credit Equity_45 Credit Equity_51 Credit Equity_52 Credit Equity_53 Credit Equity_54 Credit Equity_55 Orig UPB Spline 1 Orig UPB Spline 2 Orig UPB Spline 3 Orig UPB Spline 4 SATO Spline 1 SATO Spline 2 Unemp Rate Spline 1 Unemp Rate Spline 2 Unemp Rate Spline 3 Unemp Rate Spline 4 Min Max 0 0.66 0.78 0.8 0 0.682 0.718 0.751 0.77 0.66 0.78 0.8 1.2 0.682 0.718 0.751 0.77 0.85 0 92 135 198 -8 0.1 0 4.5 5.4 6.8 92 135 198 417 0.1 4 4.5 5.4 6.8 12 Prepay Default Coef. Std.

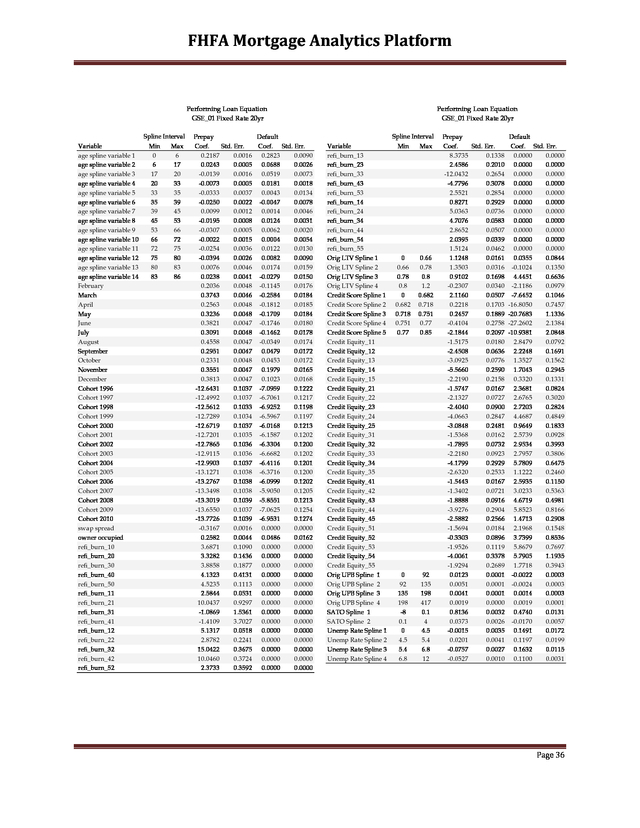

Err. Coef. Std. Err. 8.3735 0.1338 0.0000 0.0000 2.4586 0.2010 0.0000 0.0000 -12.0432 0.2654 0.0000 0.0000 -4.7796 0.3078 0.0000 0.0000 2.5521 0.2854 0.0000 0.0000 0.8271 0.2929 0.0000 0.0000 5.0363 0.0736 0.0000 0.0000 4.7076 0.0583 0.0000 0.0000 2.8652 0.0507 0.0000 0.0000 2.0395 0.0339 0.0000 0.0000 1.5124 0.0462 0.0000 0.0000 1.1248 0.0161 0.0355 0.0844 1.3503 0.0316 -0.1024 0.1350 0.9102 0.1698 4.4451 0.6636 -0.2307 0.0340 -2.1186 0.0979 2.1160 0.0507 -7.6452 0.1046 0.2218 0.1703 -16.8050 0.7457 0.2457 0.1889 -20.7683 1.1336 -0.4104 0.2758 -27.2602 2.1384 -2.1844 0.2097 -10.9381 2.0848 -1.5175 0.0180 2.8479 0.0792 -2.4508 0.0636 2.2248 0.1691 -3.0925 0.0776 1.3527 0.1562 -5.5660 0.2590 1.7043 0.2945 -2.2190 0.2158 0.3320 0.1331 -1.5747 0.0167 2.3681 0.0824 -2.1327 0.0727 2.6765 0.3020 -2.4040 0.0900 2.7203 0.2824 -4.0663 0.2847 4.4687 0.4849 -3.0848 0.2481 0.9649 0.1833 -1.5368 0.0162 2.5739 0.0928 -1.7895 0.0732 2.9534 0.3993 -2.2180 0.0923 2.7957 0.3806 -4.1799 0.2929 5.7809 0.6475 -2.6320 0.2533 1.1222 0.2460 -1.5443 0.0167 2.5935 0.1150 -1.3402 0.0721 3.0233 0.5363 -1.8888 0.0916 4.6719 0.4981 -3.9276 0.2904 5.8523 0.8166 -2.5882 0.2566 1.4713 0.2908 -1.5694 0.0184 2.1968 0.1548 -0.3303 0.0896 3.7399 0.8536 -1.9526 0.1119 5.8679 0.7697 -4.0061 0.3378 5.7905 1.1935 -1.9294 0.2689 1.7718 0.3943 0.0123 0.0001 -0.0022 0.0003 0.0051 0.0001 -0.0024 0.0003 0.0041 0.0001 0.0014 0.0003 0.0019 0.0000 0.0019 0.0001 0.8136 0.0032 0.4740 0.0131 0.0373 0.0026 -0.0170 0.0057 -0.0015 0.0035 0.1491 0.0172 0.0201 0.0041 0.1197 0.0199 -0.0757 0.0027 0.1632 0.0115 -0.0527 0.0010 0.1100 0.0031 Page 36 .

FHFA Mortgage Analytics Platform Performing Loan Equation GSE_01 Fixed Rate 30yr Performing Loan Equation GSE_01 Fixed Rate 30yr Spline Interval Variable age spline variable 1 age spline variable 2 age spline variable 3 age spline variable 4 age spline variable 5 age spline variable 6 age spline variable 7 age spline variable 8 age spline variable 9 age spline variable 10 age spline variable 11 age spline variable 12 age spline variable 13 age spline variable 14 February March April May June July August September October November December Cohort 1996 Cohort 1997 Cohort 1998 Cohort 1999 Cohort 2000 Cohort 2001 Cohort 2002 Cohort 2003 Cohort 2004 Cohort 2005 Cohort 2006 Cohort 2007 Cohort 2008 Cohort 2009 Cohort 2010 swap spread owner occupied refi_burn_10 refi_burn_20 refi_burn_30 refi_burn_40 refi_burn_50 refi_burn_11 refi_burn_21 refi_burn_31 refi_burn_41 refi_burn_12 refi_burn_22 refi_burn_32 refi_burn_42 refi_burn_52 Min 0 3 11 17 35 39 51 59 65 75 80 86 92 95 Max 3 11 17 35 39 51 59 65 75 80 86 92 95 98 Prepay Default Coef. Std. Err. Coef. Std. Err. 0.3578 0.0034 0.0000 0.0000 0.0427 0.0006 0.1415 0.0017 0.0027 0.0006 0.0400 0.0017 -0.0179 0.0002 0.0077 0.0005 -0.0184 0.0012 -0.0378 0.0024 -0.0091 0.0005 -0.0036 0.0011 -0.0193 0.0008 0.0058 0.0019 -0.0373 0.0013 0.0160 0.0032 -0.0128 0.0009 0.0179 0.0024 -0.0383 0.0021 0.0059 0.0059 0.0137 0.0021 0.0130 0.0059 -0.0191 0.0024 -0.0116 0.0070 -0.0117 0.0058 0.0149 0.0114 -0.0025 0.0057 0.0000 0.0000 0.1503 0.0040 -0.0908 0.0093 0.2807 0.0039 -0.2027 0.0096 0.2123 0.0040 -0.1718 0.0097 0.2073 0.0040 -0.1371 0.0096 0.2733 0.0040 -0.1402 0.0095 0.2409 0.0040 -0.1129 0.0094 0.2955 0.0040 -0.0505 0.0093 0.1371 0.0041 0.0265 0.0091 0.1538 0.0040 0.0327 0.0091 0.2042 0.0040 0.0742 0.0090 0.2541 0.0040 0.0358 0.0090 -12.8344 0.1047 -6.5830 0.0753 -12.8652 0.1047 -6.7309 0.0750 0.0741 -12.9073 0.1043 -6.9829 -12.9797 0.1045 -6.6019 0.0740 -12.9034 0.1047 -6.0899 0.0745 -13.0521 0.1046 -6.3233 0.0740 -13.1259 0.1046 -6.4035 0.0738 0.0737 -13.2120 0.1046 -6.5881 -13.2274 0.1048 -6.3806 0.0737 0.0733 -13.4098 0.1049 -6.2200 -13.5696 0.1047 -5.8924 0.0730 -13.7734 0.1048 -5.7478 0.0731 -13.7904 0.1049 -5.9153 0.0736 -14.1628 0.1048 -7.2585 0.0764 -14.3353 0.1051 -7.5306 0.0815 -0.2724 0.0014 0.0000 0.0000 0.0380 0.0066 0.3061 0.0029 0.0000 0.0000 4.4288 0.1120 4.0245 0.1328 0.0000 0.0000 5.0053 0.1520 0.0000 0.0000 0.0000 5.8969 0.2962 0.0000 5.3348 0.1143 0.0000 0.0000 0.0000 2.9548 0.0505 0.0000 10.5756 0.7305 0.0000 0.0000 -3.6227 1.0701 0.0000 0.0000 0.0000 -11.1106 2.5807 0.0000 5.0684 0.0452 0.0000 0.0000 0.0000 3.7501 0.1933 0.0000 14.2765 0.2958 0.0000 0.0000 11.4444 0.3297 0.0000 0.0000 2.0750 0.3587 0.0000 0.0000 Spline Interval Variable refi_burn_13 refi_burn_23 refi_burn_33 refi_burn_43 refi_burn_53 refi_burn_14 refi_burn_24 refi_burn_34 refi_burn_44 refi_burn_54 refi_burn_55 Orig LTV Spline 1 Orig LTV Spline 2 Orig LTV Spline 3 Orig LTV Spline 4 Credit Score Spline 1 Credit Score Spline 2 Credit Score Spline 3 Credit Score Spline 4 Credit Score Spline 5 Credit Equity_11 Credit Equity_12 Credit Equity_13 Credit Equity_14 Credit Equity_15 Credit Equity_21 Credit Equity_22 Credit Equity_23 Credit Equity_24 Credit Equity_25 Credit Equity_31 Credit Equity_32 Credit Equity_33 Credit Equity_34 Credit Equity_35 Credit Equity_41 Credit Equity_42 Credit Equity_43 Credit Equity_44 Credit Equity_45 Credit Equity_51 Credit Equity_52 Credit Equity_53 Credit Equity_54 Credit Equity_55 Orig UPB Spline 1 Orig UPB Spline 2 Orig UPB Spline 3 Orig UPB Spline 4 SATO Spline 1 SATO Spline 2 Unemp Rate Spline 1 Unemp Rate Spline 2 Unemp Rate Spline 3 Unemp Rate Spline 4 Min Max 0 0.66 0.79 0.83 0 0.678 0.716 0.75 0.78 0.66 0.79 0.83 1.2 0.678 0.716 0.75 0.78 0.85 0 96 141 206 -8 0.1 0 4.6 5.7 8 96 141 206 417 0.1 4 4.6 5.7 8 12 Prepay Default Coef. Std.

Err. Coef. Std. Err. 8.4176 0.1144 0.0000 0.0000 2.2872 0.1750 0.0000 0.0000 -9.4143 0.2405 0.0000 0.0000 -4.2828 0.2824 0.0000 0.0000 3.7319 0.2806 0.0000 0.0000 1.2167 0.2125 0.0000 0.0000 4.5996 0.0589 0.0000 0.0000 4.1885 0.0476 0.0000 0.0000 2.8383 0.0441 0.0000 0.0000 2.1544 0.0307 0.0000 0.0000 2.0800 0.0381 0.0000 0.0000 1.0940 0.0150 0.1756 0.0657 1.6214 0.0244 -0.4380 0.0676 1.0651 0.1085 -1.0846 0.2422 2.3861 0.0344 -0.0713 0.0594 2.3355 0.0458 -6.1786 0.0678 0.8921 0.1527 -10.6461 0.3921 0.7484 0.1710 -12.9296 0.5849 0.4587 0.1796 -16.6710 0.7910 -0.5375 0.2060 -10.7205 1.0852 -1.4952 0.0168 2.9214 0.0733 -3.5788 0.0536 1.3353 0.1349 -3.7905 0.0473 1.8157 0.0861 -5.7094 0.0964 3.4627 0.1021 -4.6356 0.0758 0.9129 0.0251 -1.5688 0.0156 2.1536 0.0767 -2.7274 0.0602 3.3840 0.2306 -3.4707 0.0541 3.9894 0.1397 -5.6149 0.1122 3.0778 0.1544 -4.3207 0.0808 1.4439 0.0336 -1.5535 0.0149 1.9205 0.0823 -2.4455 0.0612 4.0879 0.3048 -2.9277 0.0559 4.6502 0.1859 -5.5435 0.1173 4.0962 0.2017 -3.9967 0.0817 1.7546 0.0411 -1.5818 0.0151 1.4848 0.0931 -1.9546 0.0608 5.4235 0.4013 -2.4273 0.0563 5.1085 0.2467 -5.6257 0.1186 5.5709 0.2603 -3.4907 0.0767 2.0110 0.0491 -1.6361 0.0170 1.3074 0.1144 -1.2736 0.0766 5.3061 0.5974 -1.9186 0.0699 5.0251 0.3832 -5.0841 0.1400 6.9609 0.3964 -2.9671 0.0809 2.1250 0.0717 0.0110 0.0001 0.0003 0.0002 0.0052 0.0001 0.0010 0.0002 0.0039 0.0000 0.0036 0.0001 0.0015 0.0000 0.0018 0.0000 0.8478 0.0032 0.6349 0.0096 0.3419 0.0022 0.5067 0.0034 -0.0399 0.0027 0.1753 0.0098 0.0288 0.0028 0.0711 0.0091 -0.1182 0.0016 0.1546 0.0040 -0.0005 0.0010 0.0471 0.0018 Page 37 .