Form W2/1099 - 2015 YEAR-END - services may be classified under common-law rules

Eide Bailly

Description

2015 YEAR-END

W2/1099

. This W-2/1099 Year-End Book is distributed with the understanding that the information contained does not

constitute legal, accounting or other professional advice. It is not intended to be responsive to any individual

situation or concerns, as the contents of this book are intended for general informational purposes only.

Readers are urged not to act upon the information contained in this book without first consulting competent

legal, accounting or other professional advice regarding implications of a particular factual situation.

Questions and additional information can be submitted to your Eide Bailly representative.

© 2015 Eide Bailly LLP

. Table of Contents

Page

I.

Independent Contractor or Employee?

a.

b.

c.

d.

e.

f.

Common-Law Employees

Statutory Employees

Statutory Nonemployees

Factors Used by IRS in Determining Employee Status

IRS Reclassification: Employer Liability

Form SS-8 (Form Included)

8

8

9

10

12

15

II. 1099 Information Returns

a.

b.

c.

d.

e.

f.

g.

h.

i.

j.

k.

l.

m.

n.

o.

p.

q.

r.

s.

t.

General Requirements

Normal and Extended Due Dates

How to File Form 1099 with the IRS

Substitute Statement to Recipients

Backup Withholding

Taxpayer Identification Number (TIN) Matching

Truncating Payee Identification Number

Electronic Filing

Penalties for Noncompliance

Form 1096 Annual Summary and Transmittal

Form 1099-MISC

1. Rents

2. Royalties

3.

Other Income 4. Federal Income Tax 5. Fishing Boat Proceeds 6.

Medical and Health Care Payments 7. Nonemployee Compensation 8. Director’s Fees 9.

Substitute Payments in Lieu of Dividends or Interest 10. Payer Made Direct Sales 11. Crop Insurance Proceeds 12.

Foreign Tax 13. Foreign County or Possession 14. Excess Golden Parachute Payments 15.

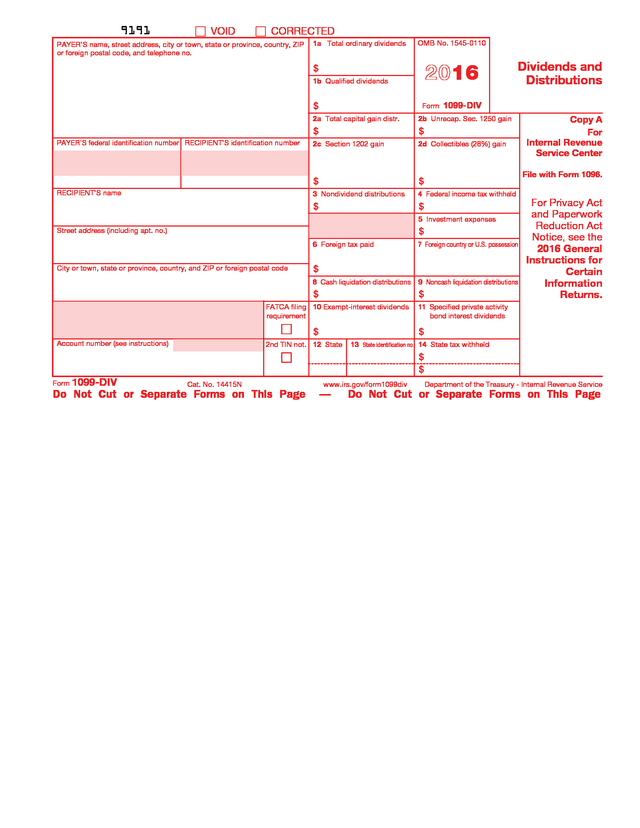

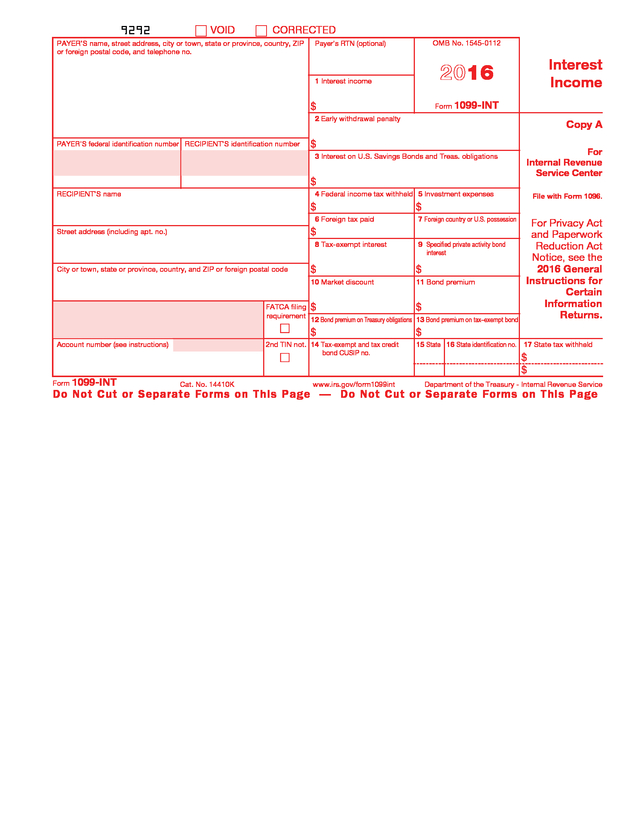

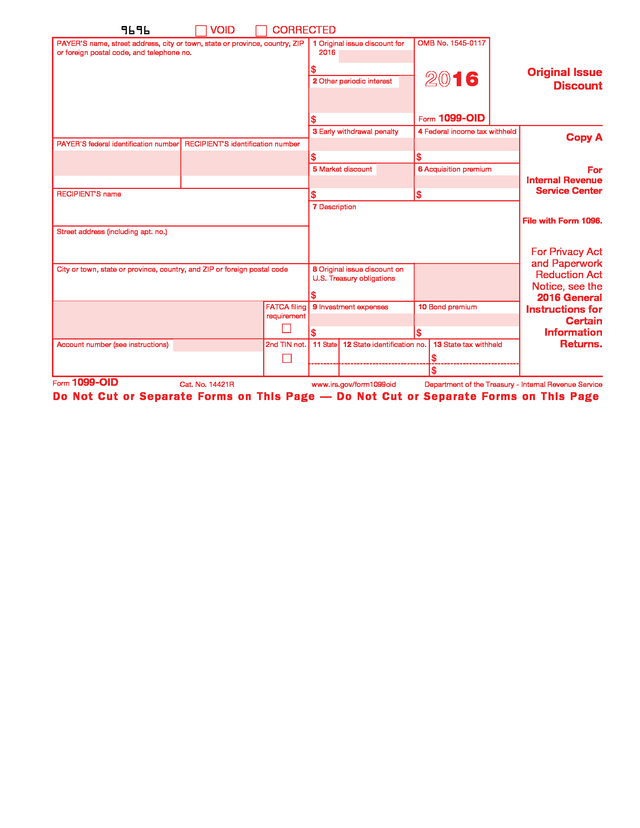

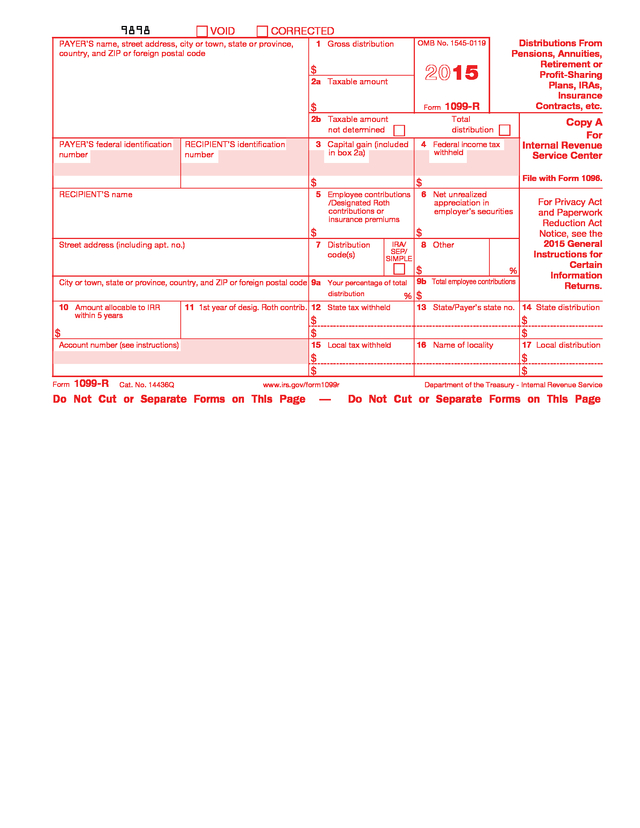

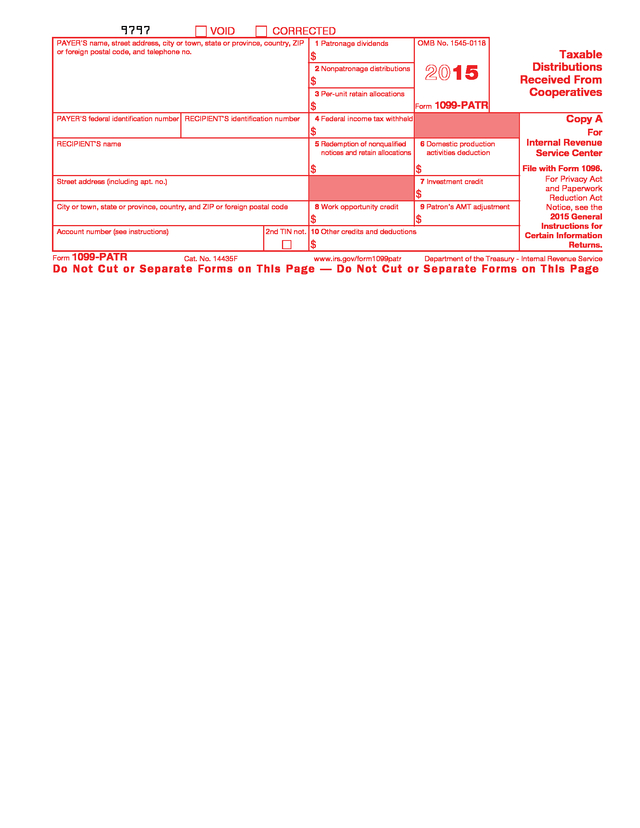

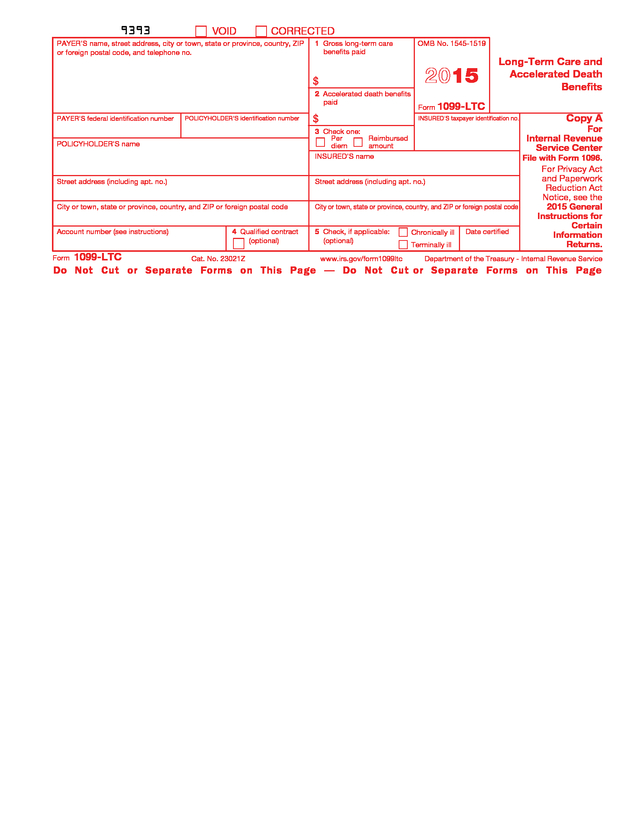

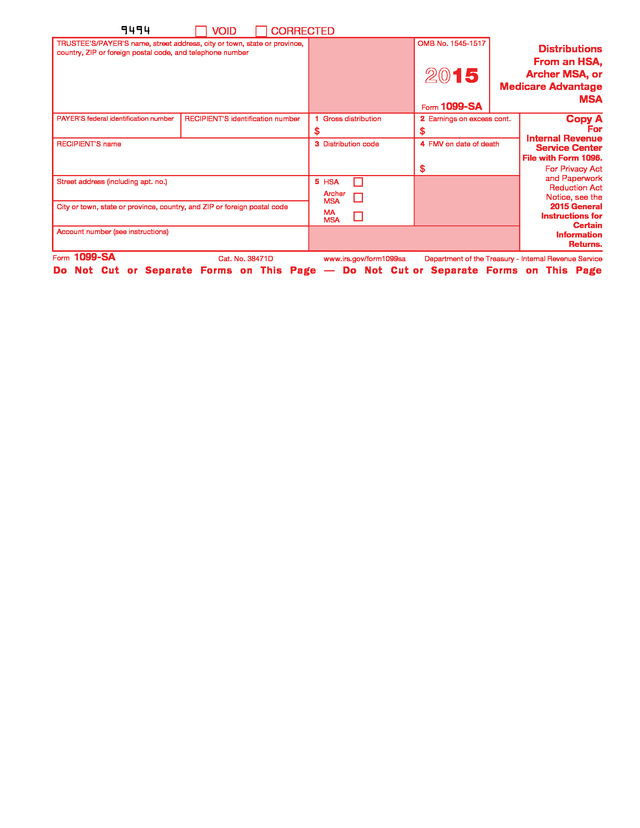

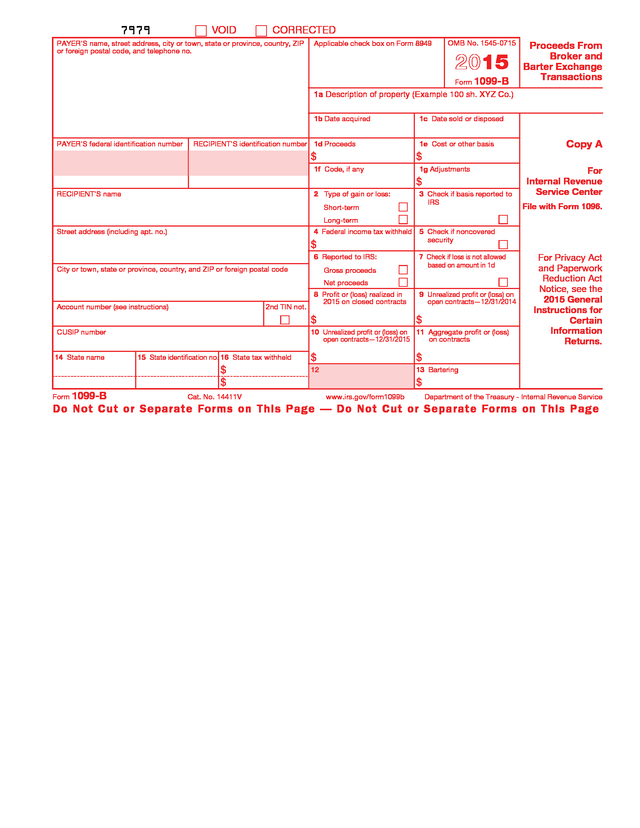

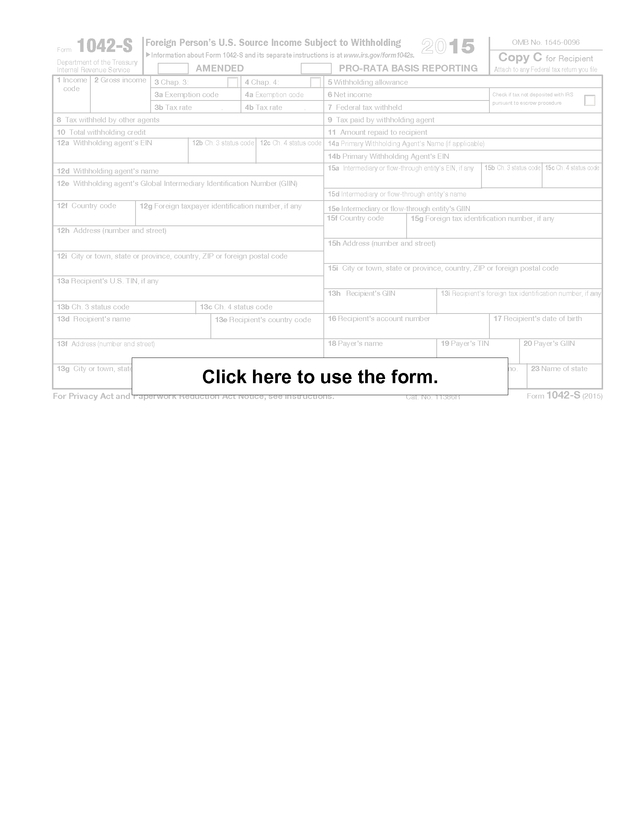

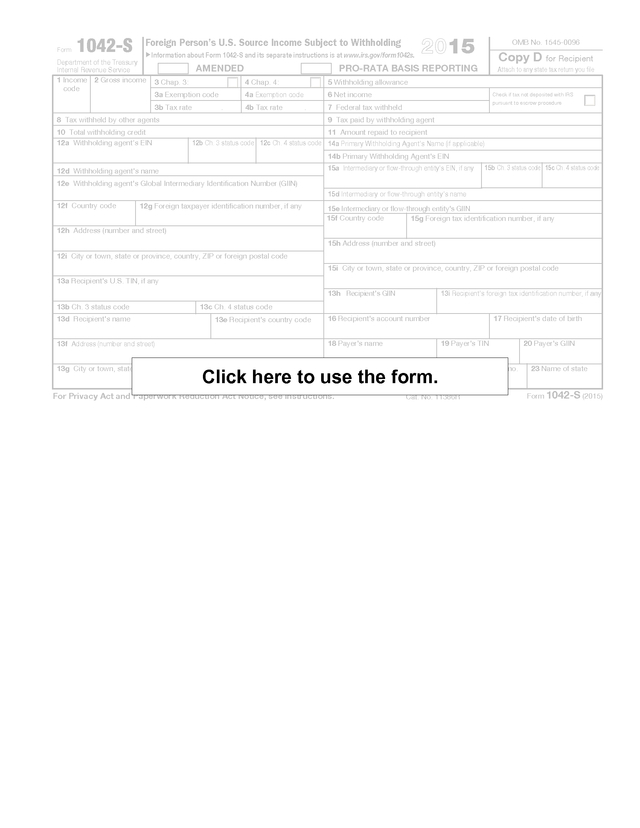

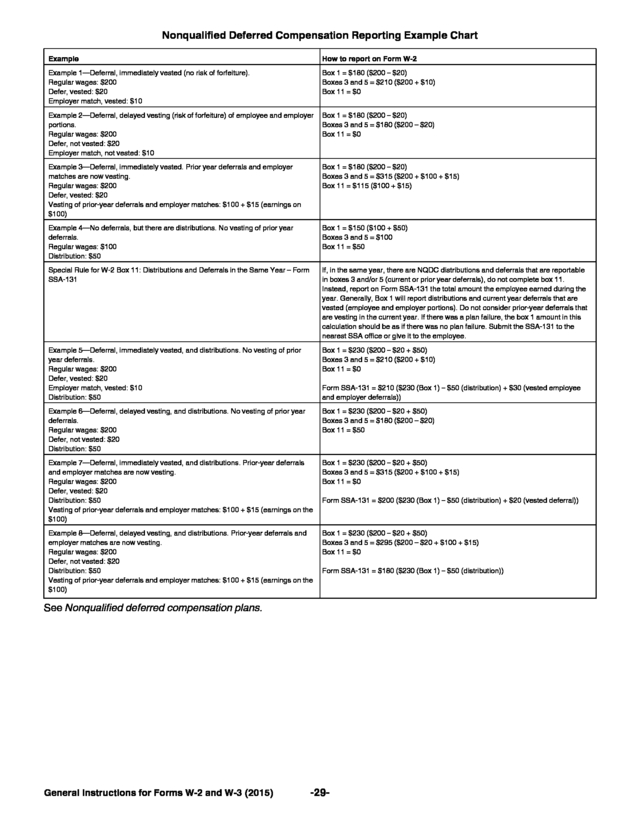

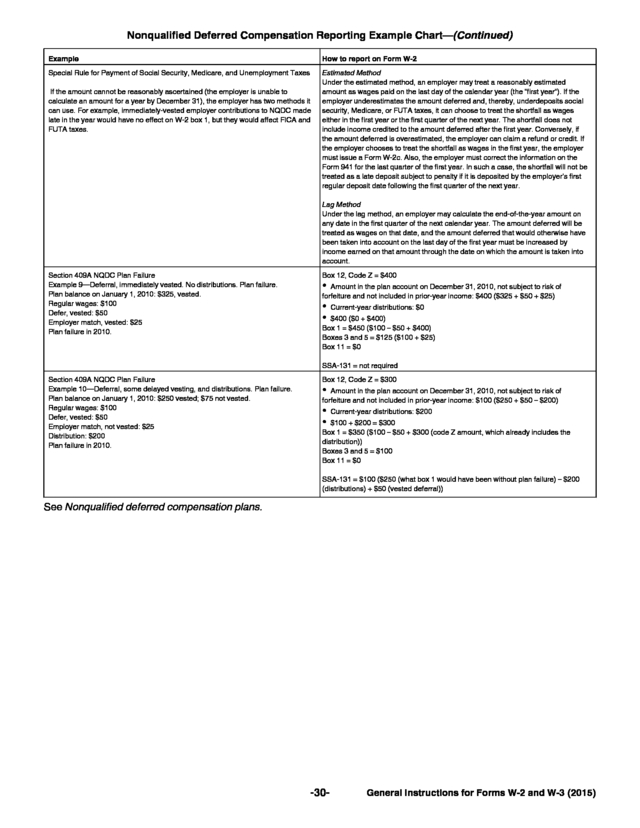

Gross Proceeds Paid to Attorneys 16. Section 409A Deferrals and Income Form 1099-DIV Form 1099-INT Form 1099-OID Form 1099-R 1. Distribution Codes Chart Form 1099-PATR Form 1099-LTC Form 1099-SA Form 1042-S Form 1099-A 20 20 20 21 21 22 22 23 23 25 26 27 27 28 29 29 29 29 31 31 31 32 32 32 32 32 33 34 34 35 35 37 39 39 39 40 40 .

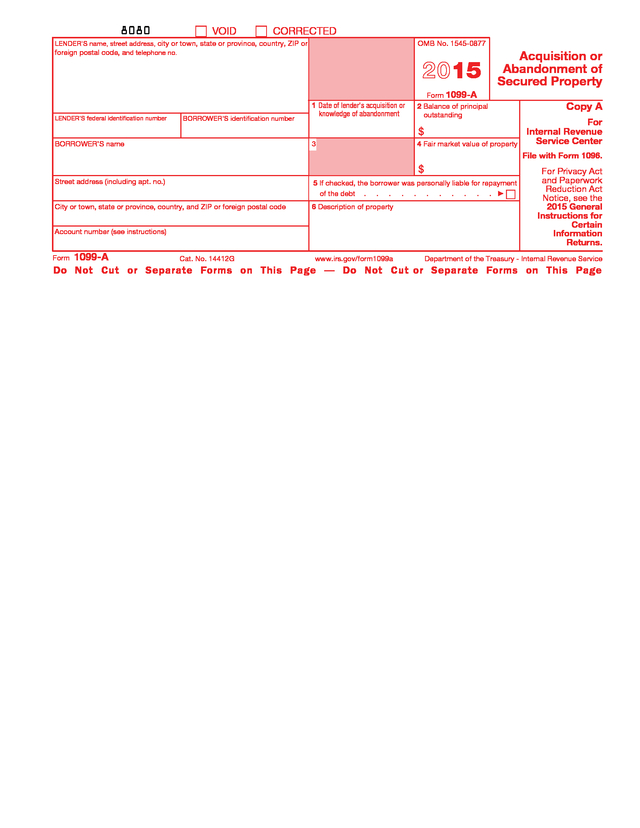

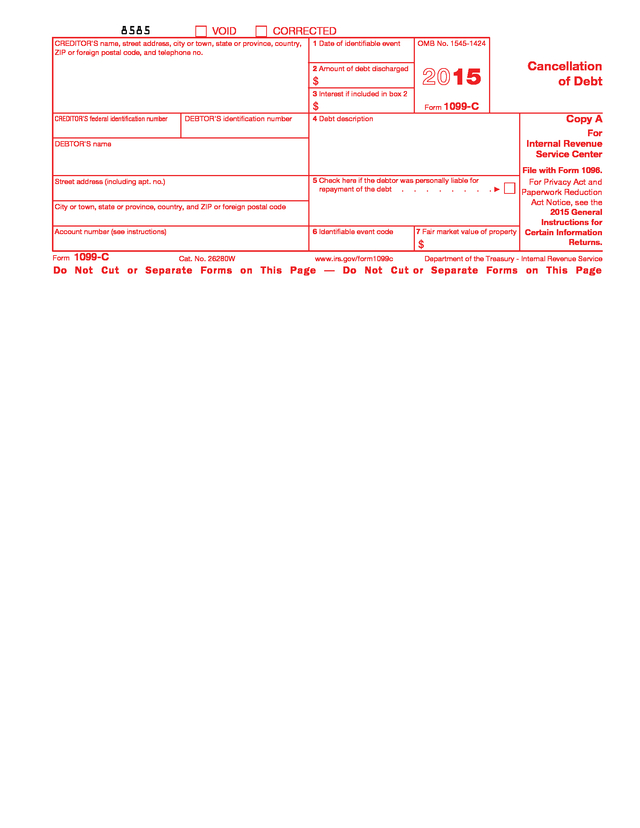

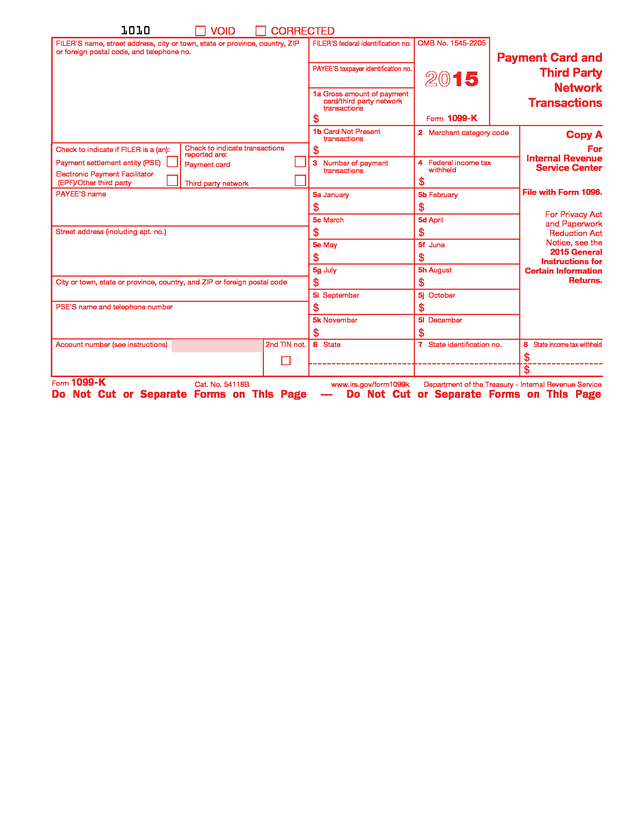

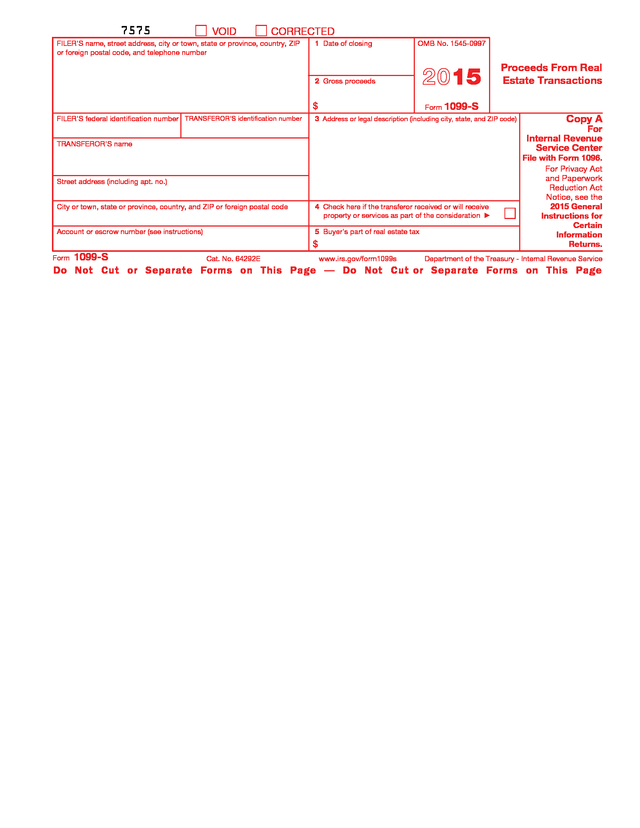

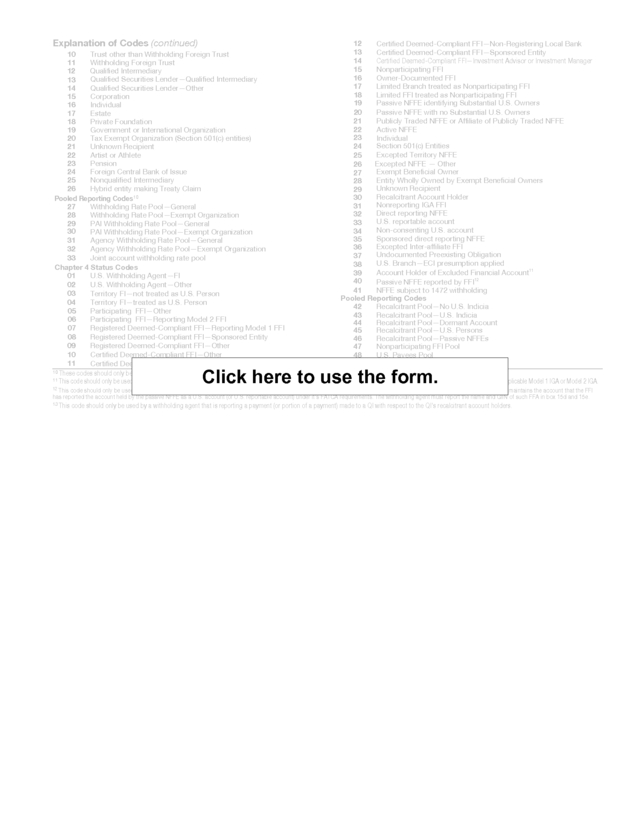

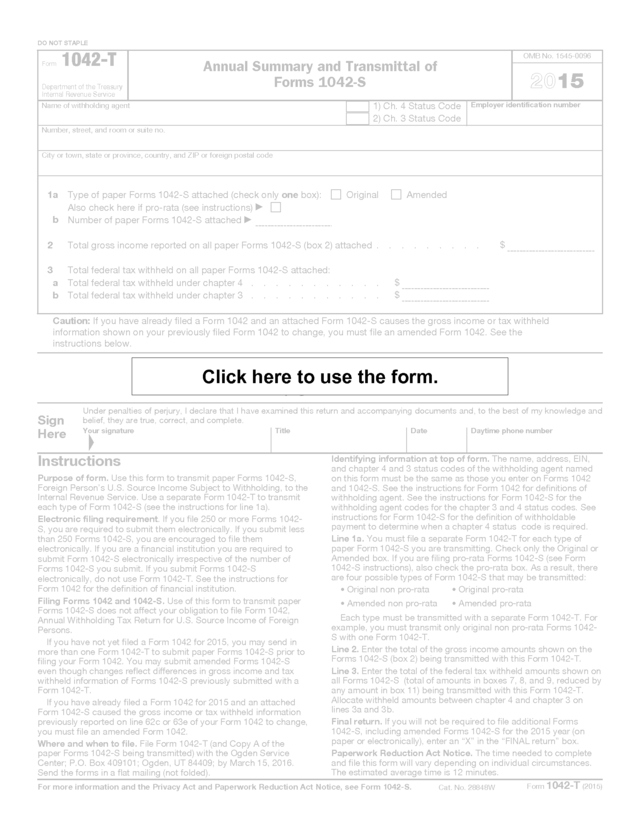

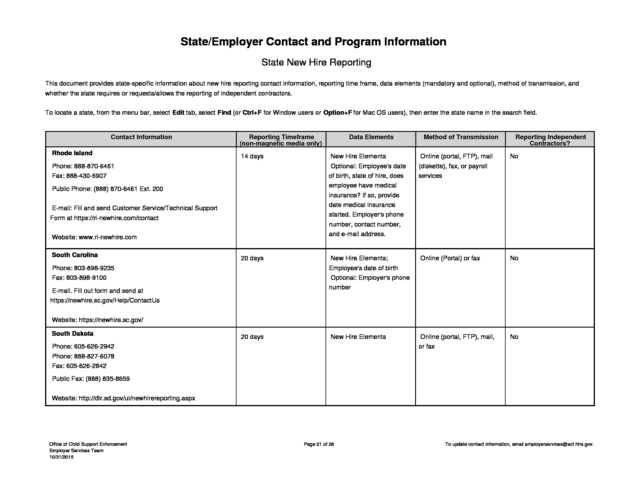

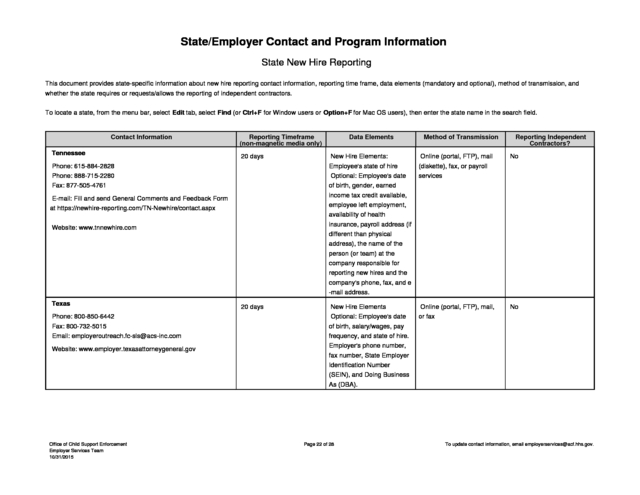

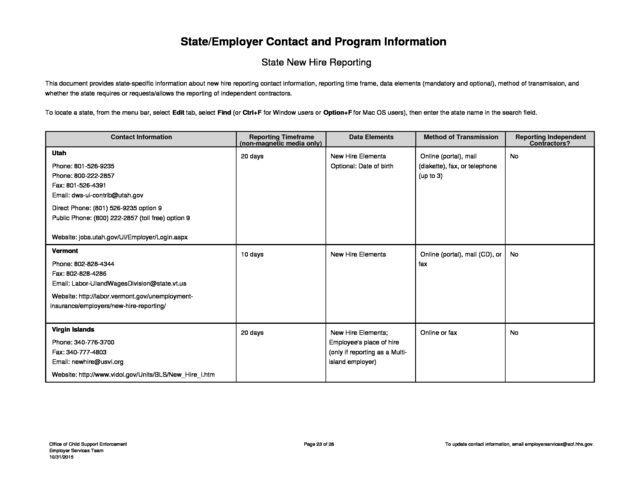

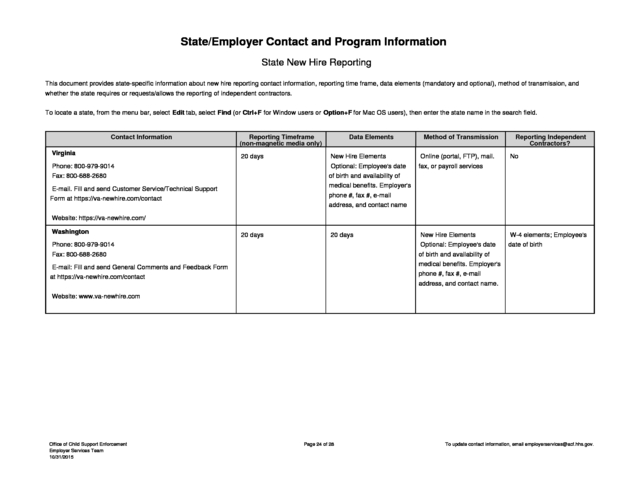

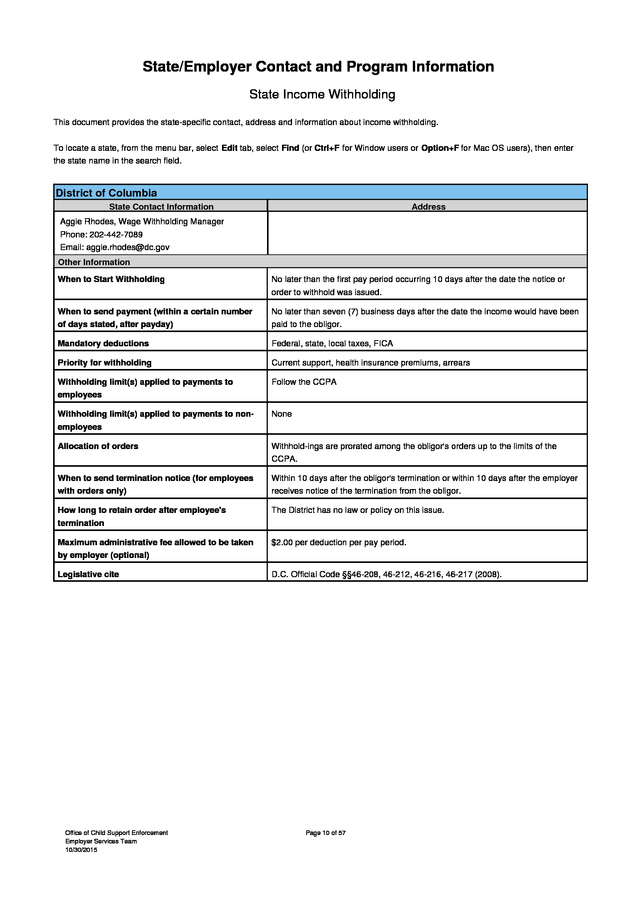

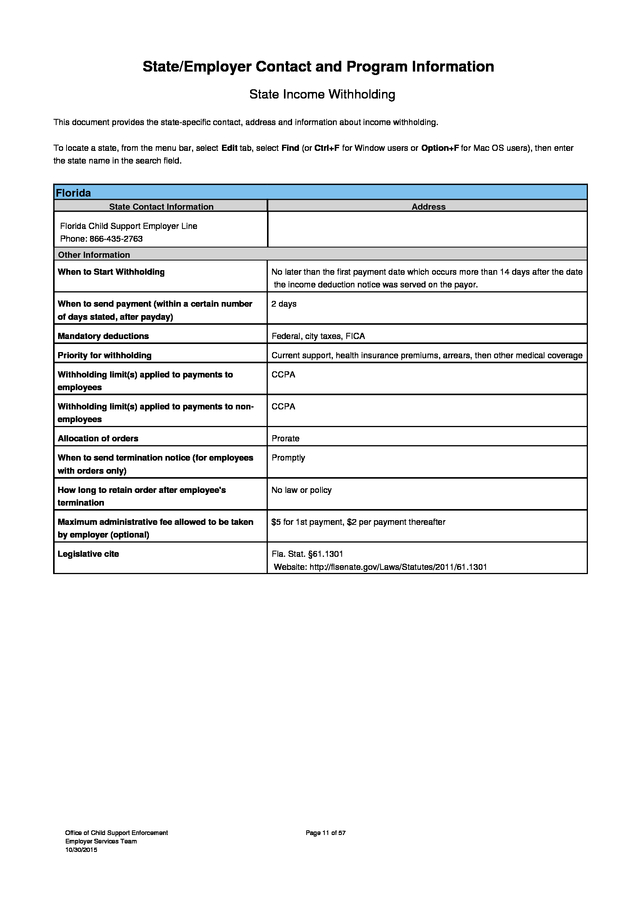

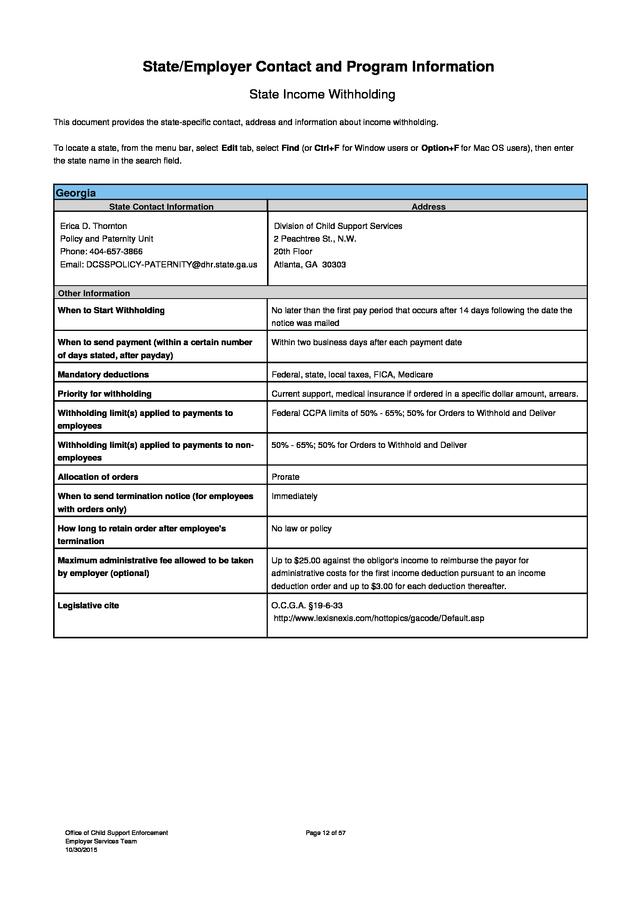

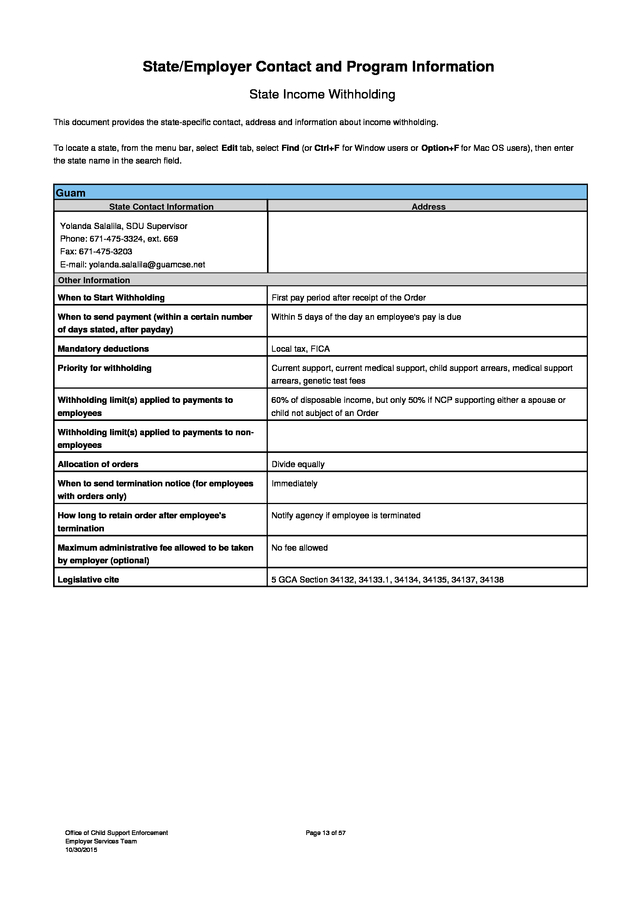

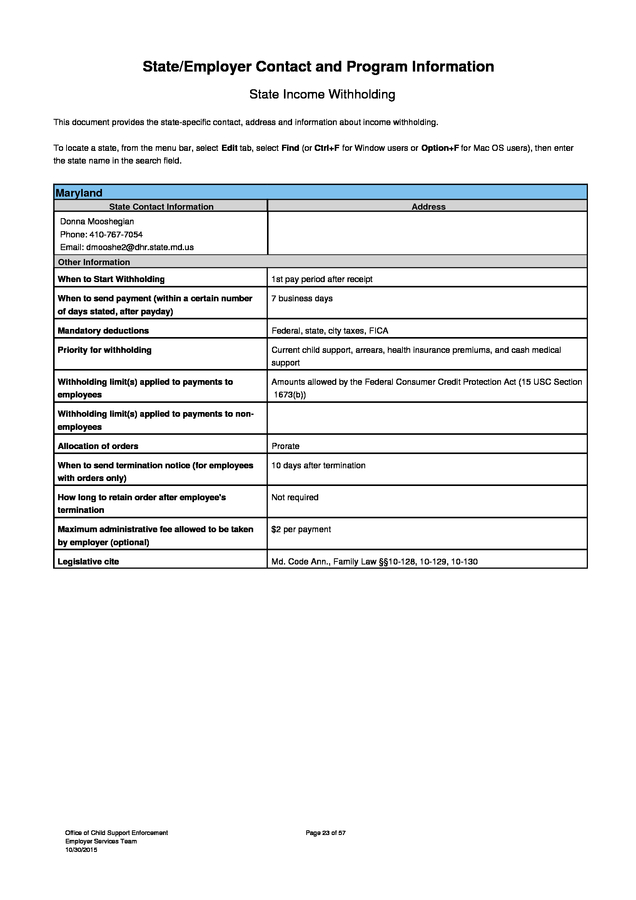

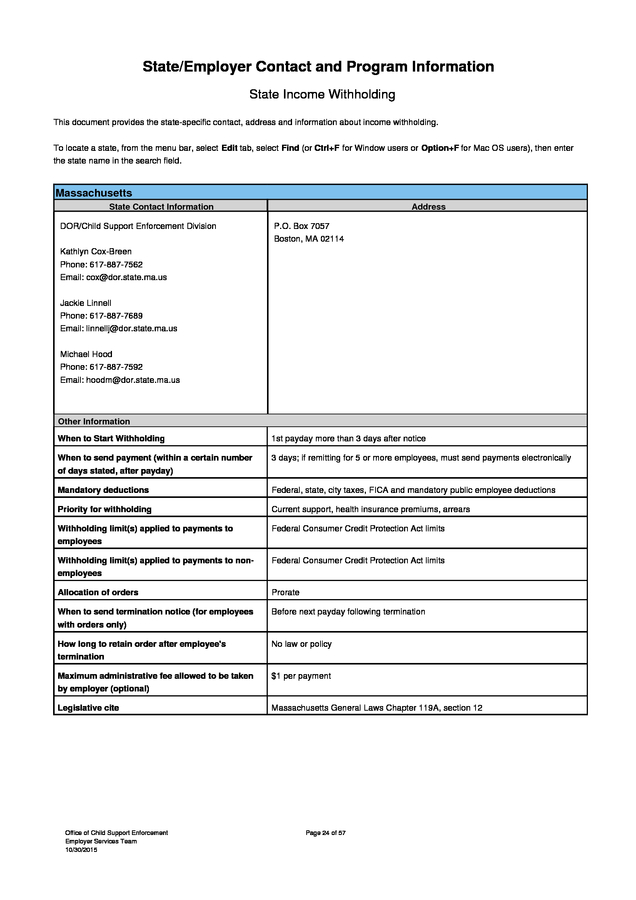

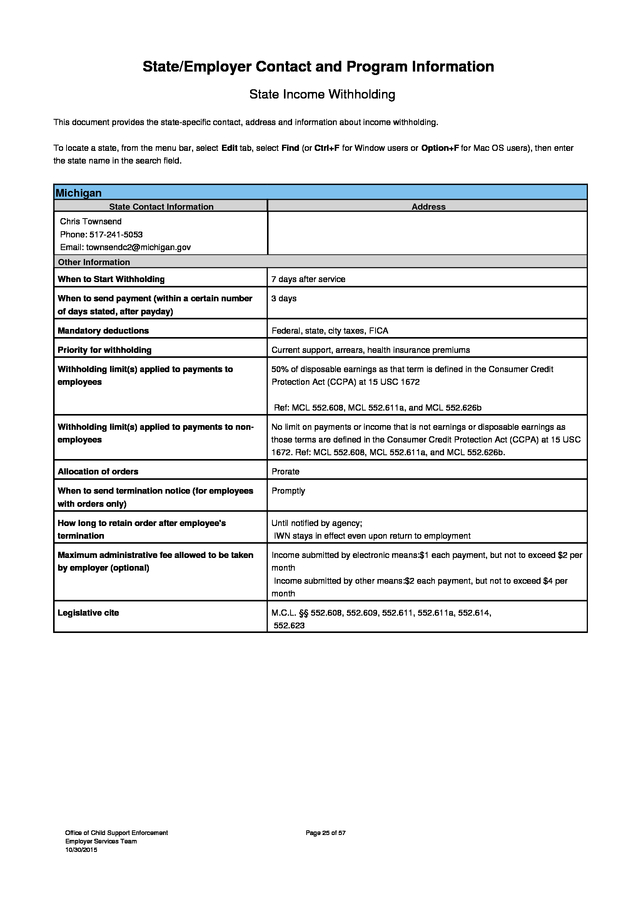

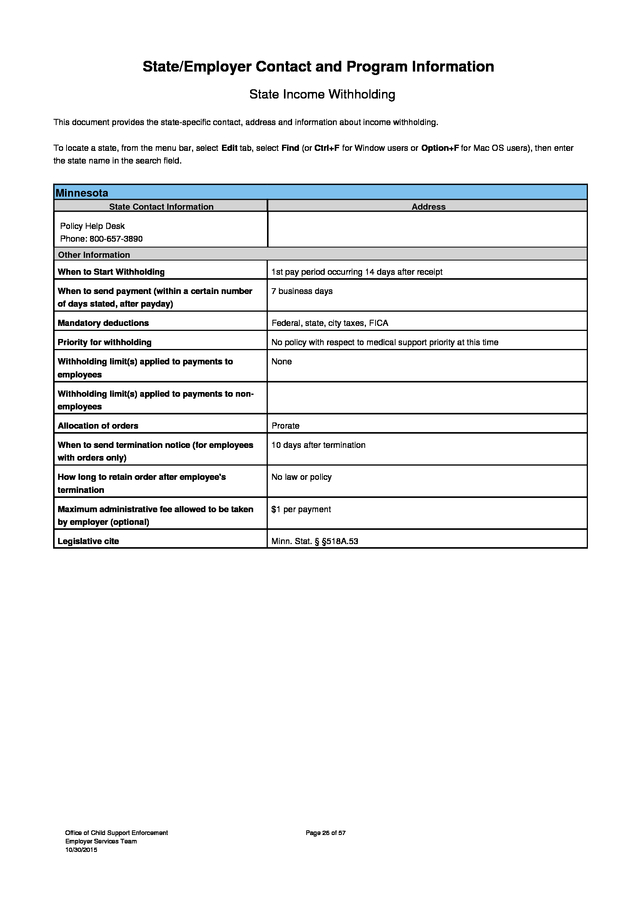

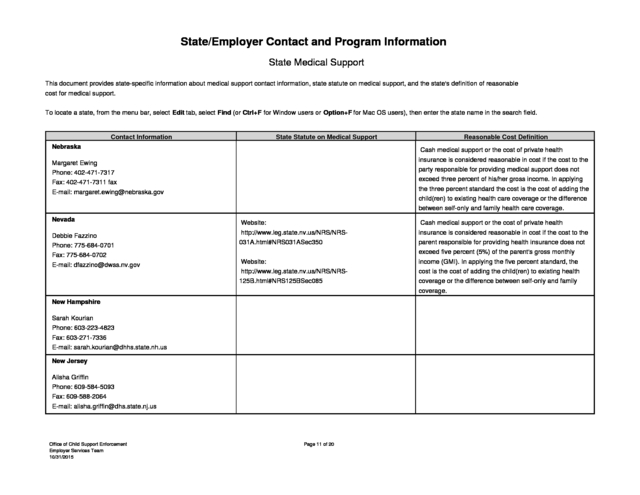

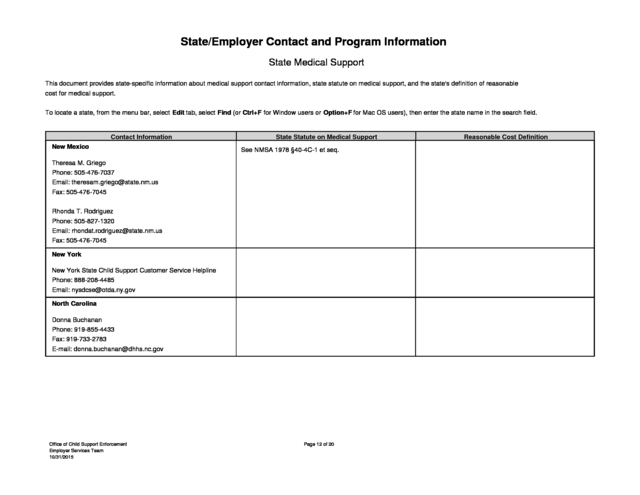

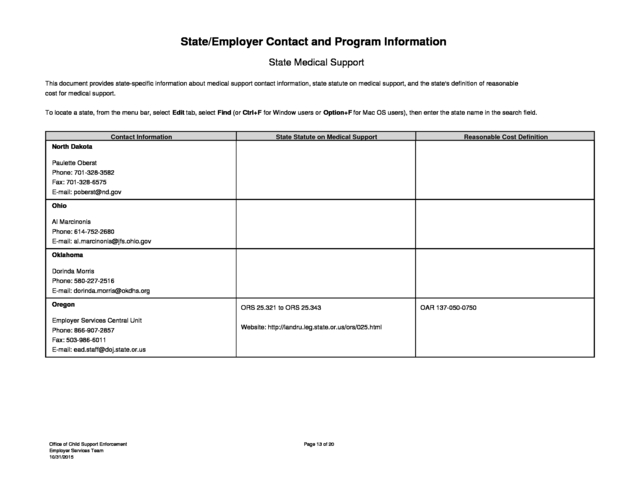

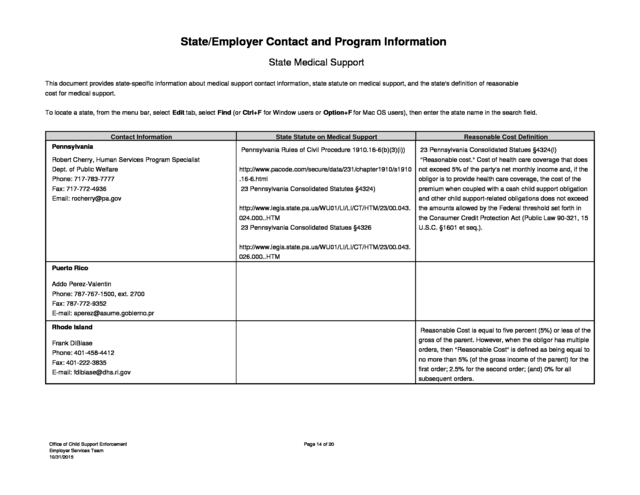

u. v. w. x. y. z. aa. bb. cc. dd. ee. ff. gg. hh. Form 1099-C Form 1099-B Form 1099-K Form 1042-S (Form Included) 1. Form 1042-S Codes Form 1042-T (Form Included) Form 8809 (Form Included) Form W-9 (Form Included) Points to Remember Guide to Information Returns Types of Payments Where to File Combined Federal/State Filing Program State Code Chart Correcting Information Returns Page 40 41 42 57 61 65 66 68 72 73 76 77 77 78 79 III. New Hire Reporting a. b. c. d. e. f. g. h. i. j. General Federal Requirements Employment Verification Rules SSA Social Security Number Verification Service State Verification Requirements Chart Penalties for Violation Deposit Requirements for Employment Taxes SSN “Randomization” State New Hire Reporting Information (from Child Support Enforcement Website) State/Employer Contact & Program Information (from Child Support Enforcement Website) State Medical Support Information (from Child Support Enforcement Website) 82 83 86 88 89 90 91 92 120 177 IV. Forms W-2 and W-3 a.

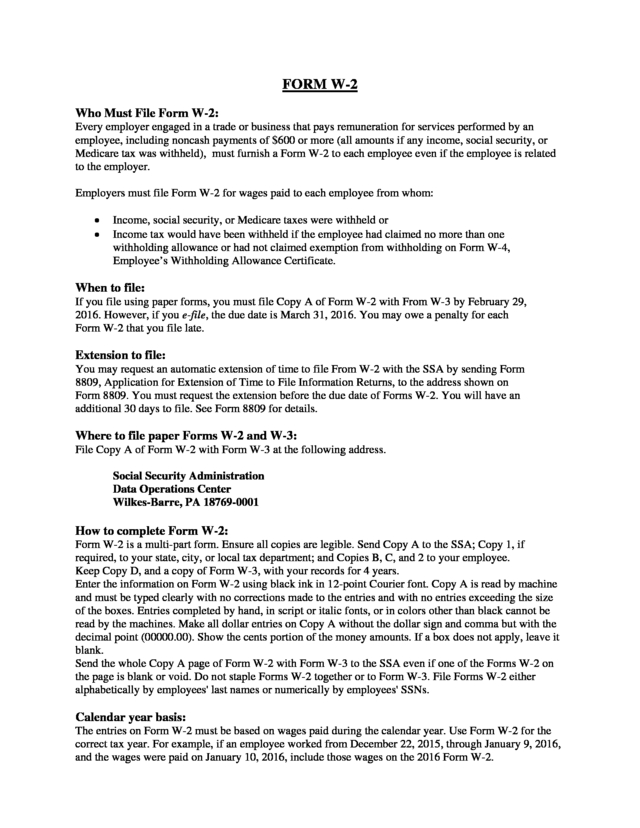

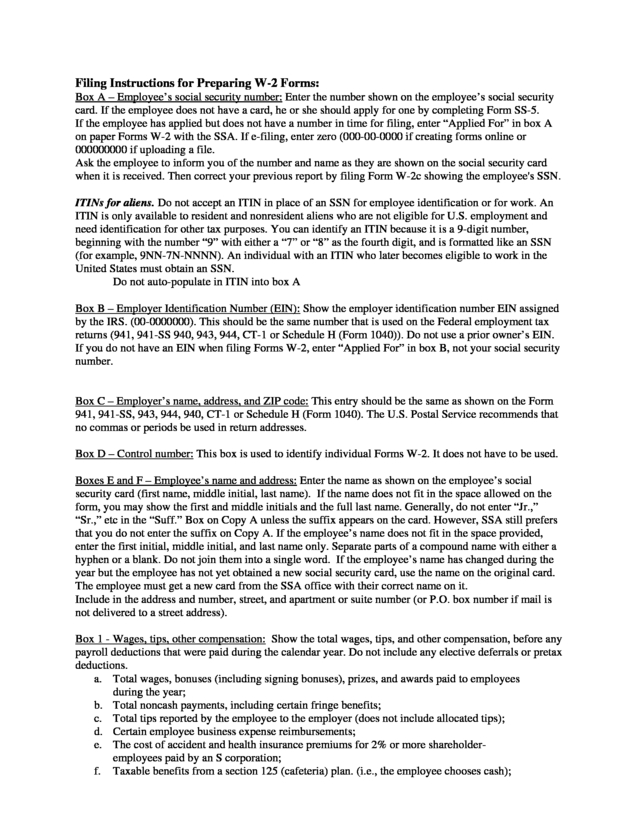

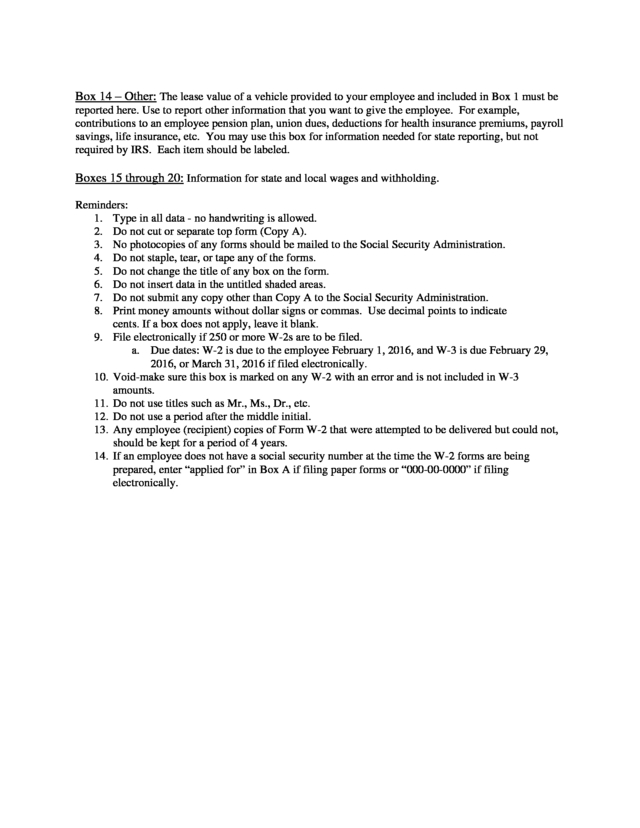

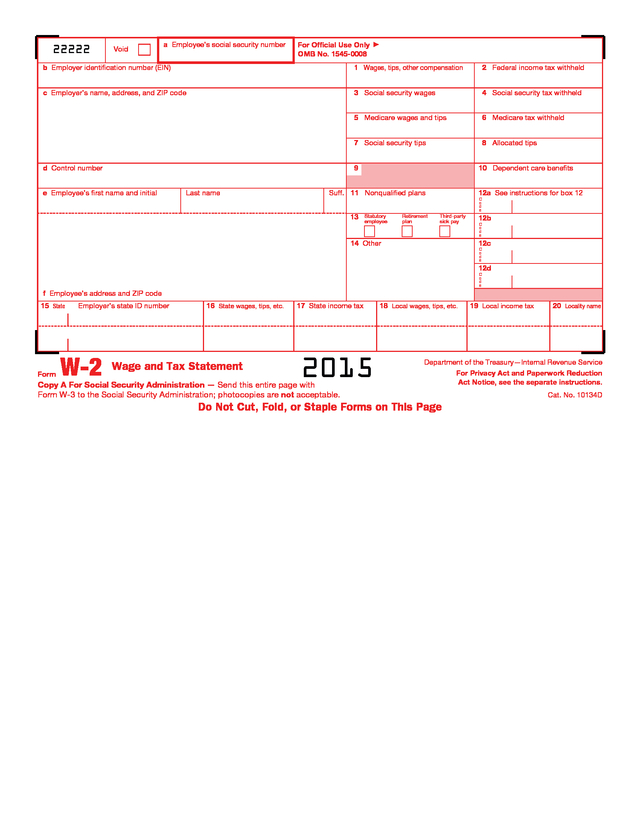

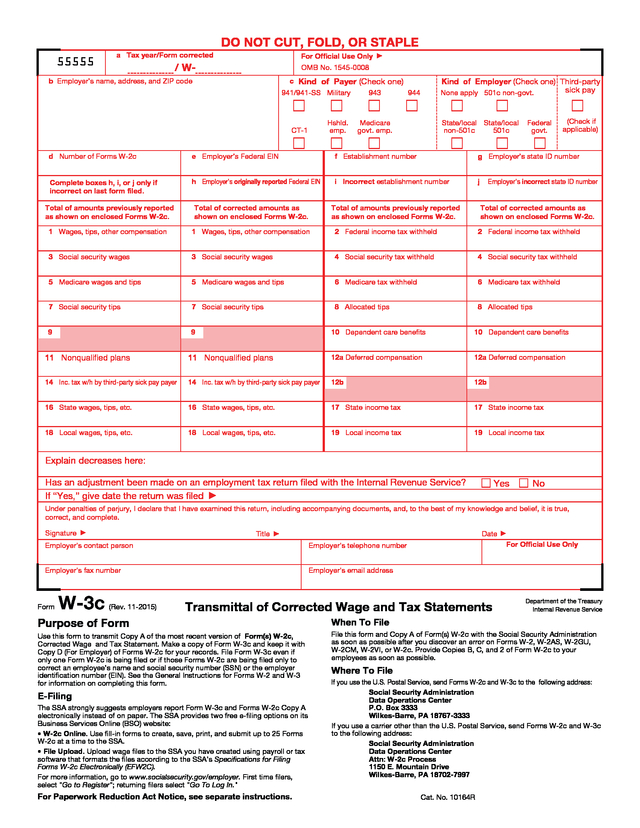

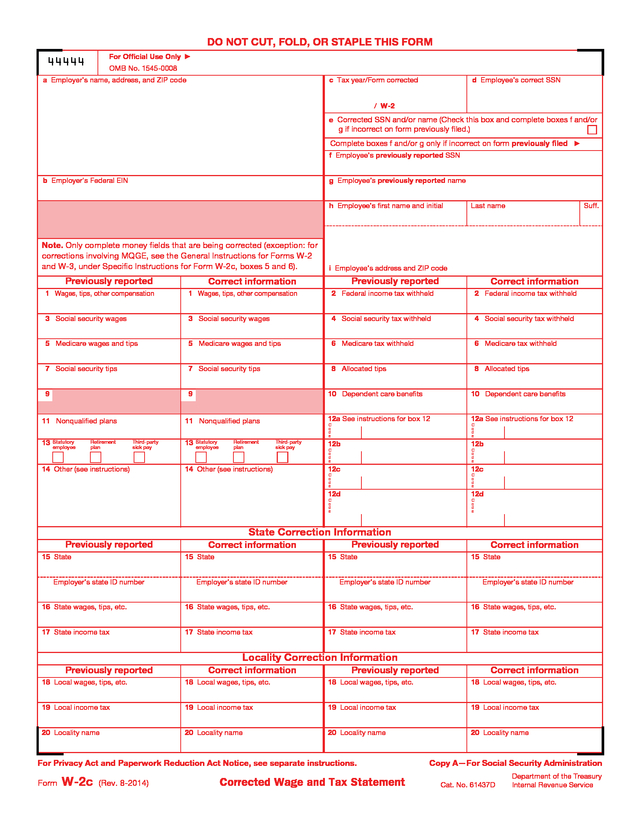

Who Must File Form W-2 b. Filing Instructions Per Box 1. Box 12 Codes c.

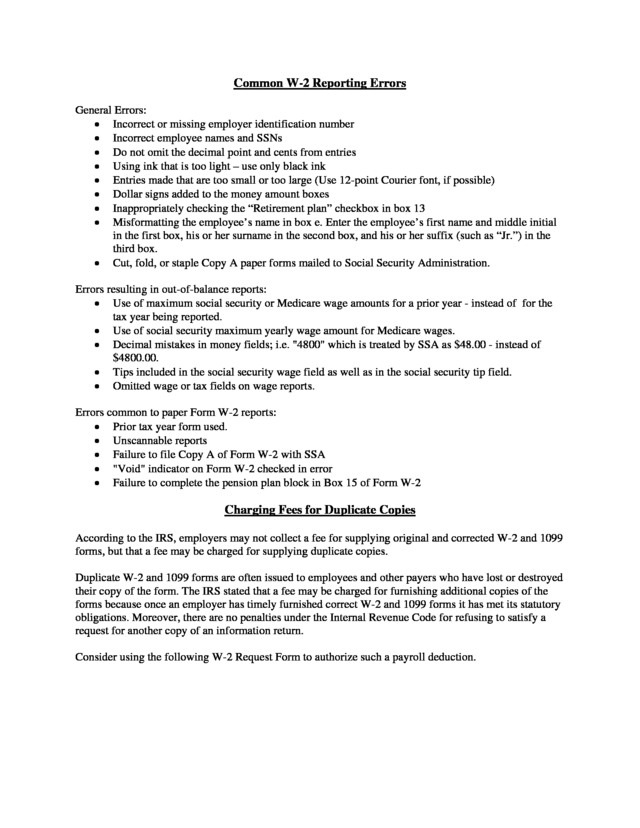

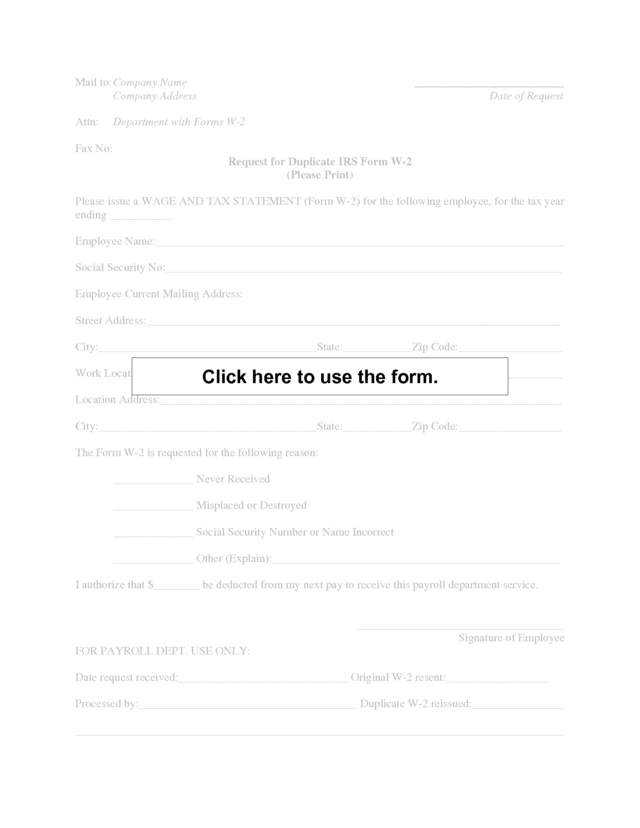

Common W-2 Reporting Errors d. Charging Fees for Duplicate Copies 1. Request for Duplicate Form W-2 (Form Included) e.

Form W-3 f. Electronic Filing g. Correcting Forms W-2/W-3 h.

Penalties i. Fringe Benefits and Special Reporting Issues 1. Taxable Fringe Benefits a.

When Fringe Benefits are Considered Paid b. Special Accounting Rule c. Depositing Taxes on Fringe Benefits d.

Withholding on Fringe Benefits e. Supplemental Wage Payments f. Employer-Paid Taxes 2.

Cafeteria Plans and Flexible Benefit Plans 198 199 202 206 206 207 208 209 211 212 215 215 215 216 216 216 219 220 . a. b. c. d. e. f. g. h. j. Effect of the Family and Medical Leave Act Flexible Spending Accounts Dependent Care Benefits Adoption Assistance Health Savings Accounts Employer-Provided Accident and Health Plan Health Insurance Premiums on 2% Shareholders New W-2 Reporting Requirement 1. IRS Reporting Chart 3. Group-Term Life Insurance Coverage a. Uniform Premium Table 4.

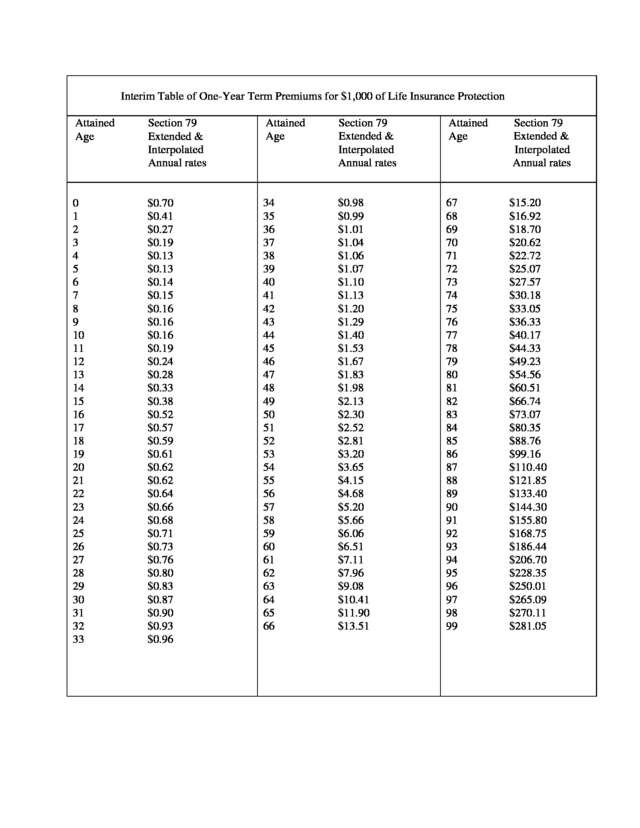

Whole-Life Insurance a. Premium Table 5. Deferred Compensation Plans a.

Qualified Plans b. Nonqualified Plans 1. Nonqualified Deferred Comp Examples 6.

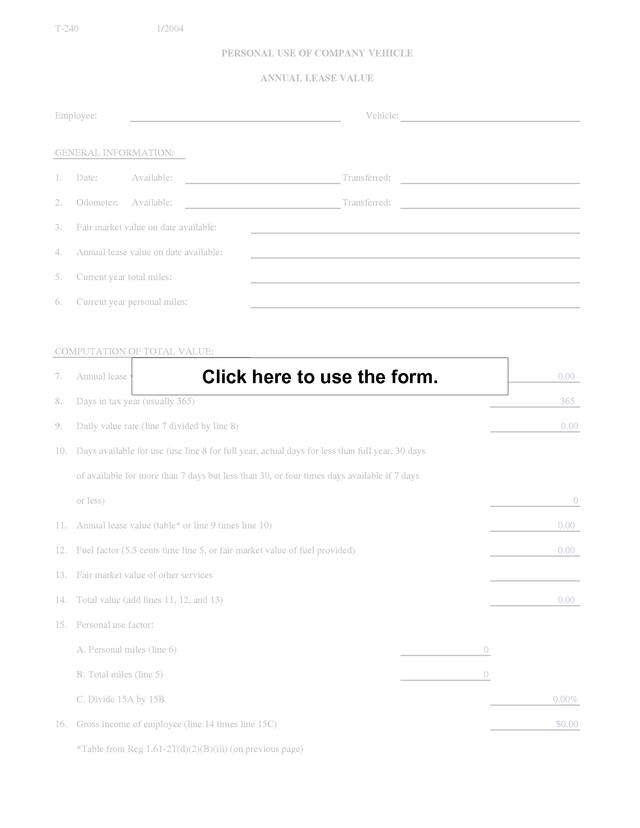

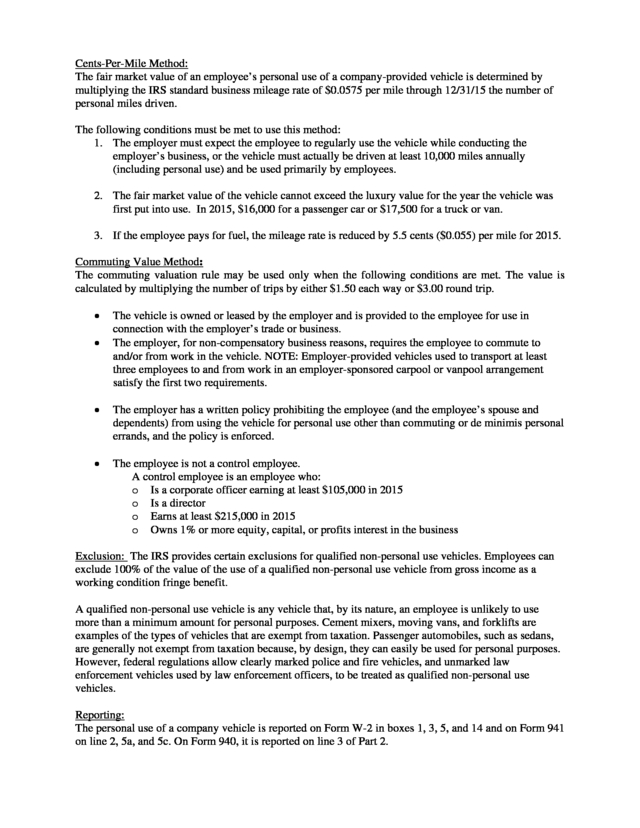

Personal Use of Company Vehicle a. Annual Lease Value Method 1. Annual Lease Value Table 2.

Annual Lease Value Worksheet (Form Included) b. Cents-Per-Mile Method c. Commuting Value Method 7.

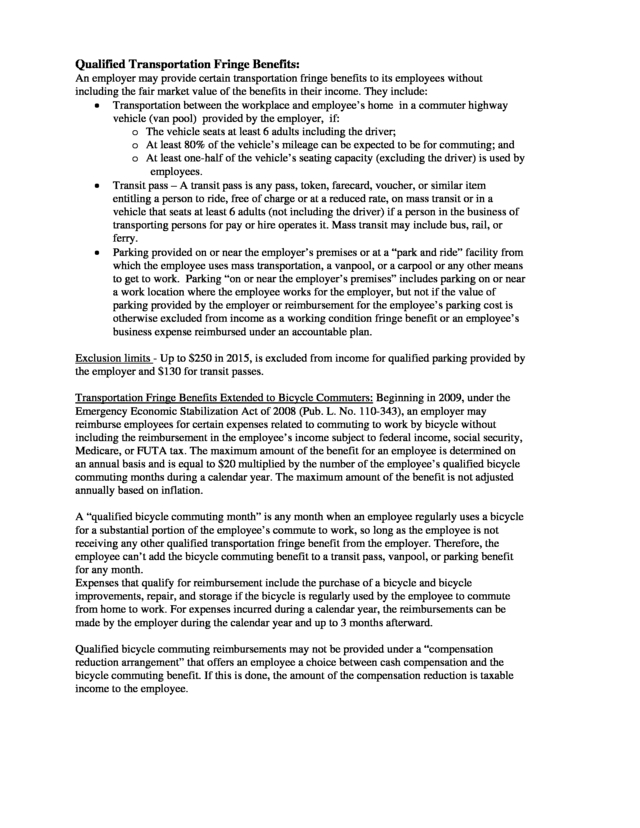

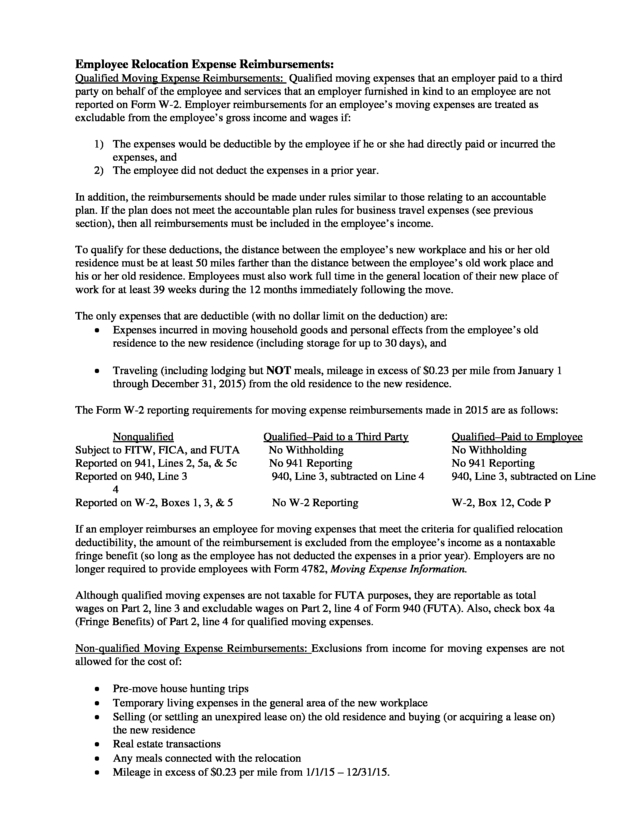

Qualified Transportation Fringe Benefits 8. Employee Relocation Expense Reimbursements 9. De Minimis Fringe Benefits 10.

Employer-Provided Cell Phone 11. Educational Assistance 12. Differential Military Pay 13.

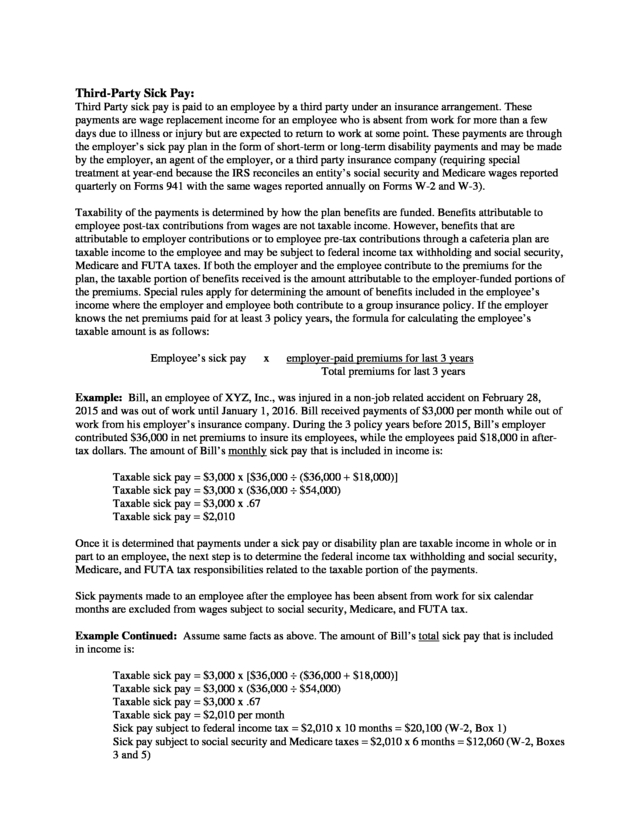

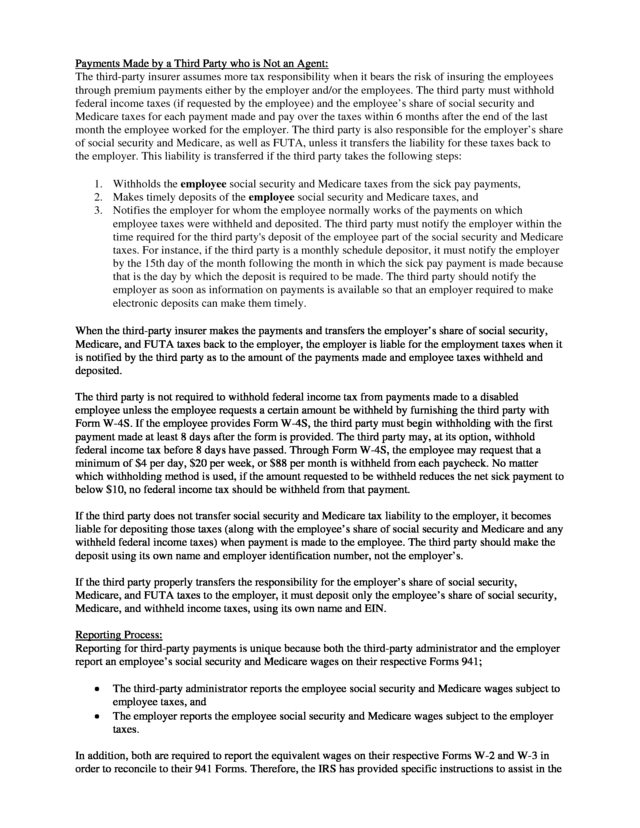

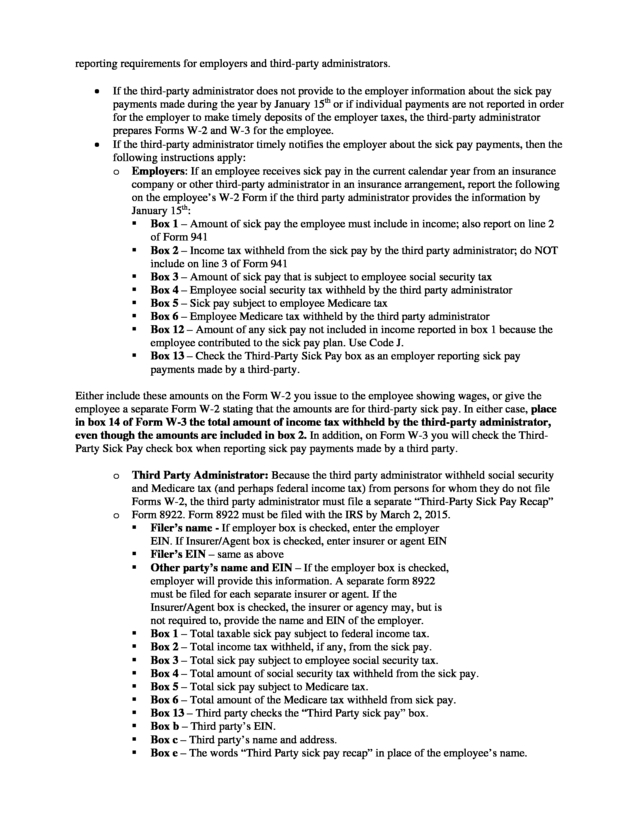

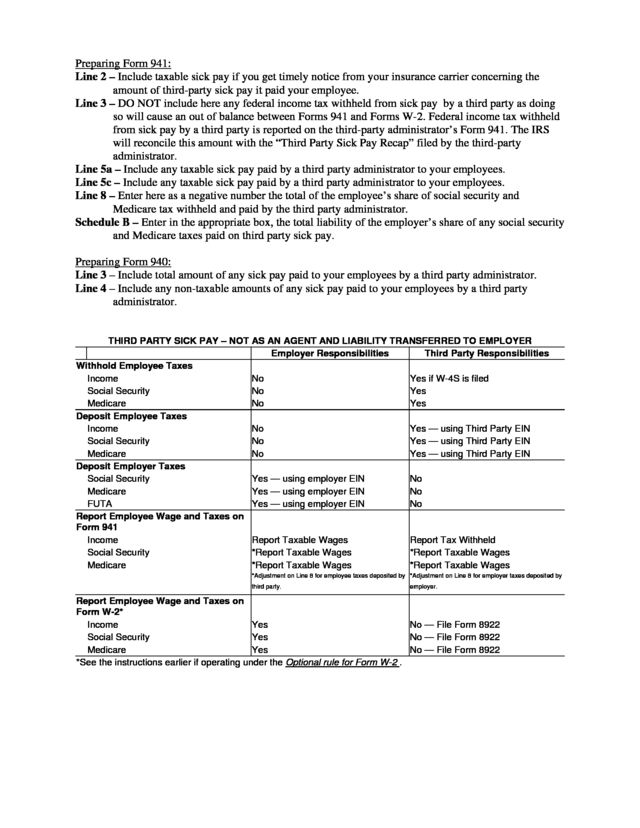

Loans to Employees 14. Employee Discounts 15. Third-Party Sick Pay 16.

Employee Business Expense Reimbursement 17. Wages Paid After Death 18. Special Rules for Various Fringe Benefits Chart 19.

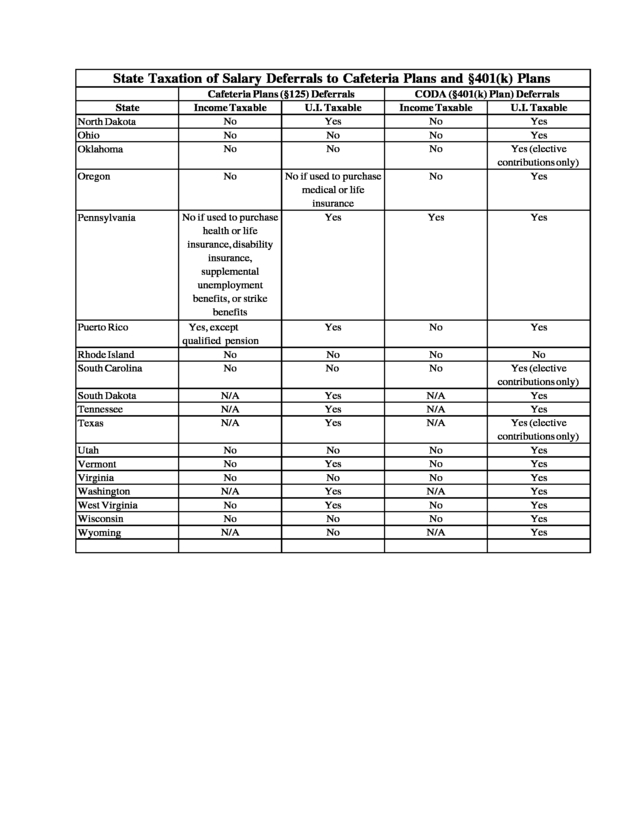

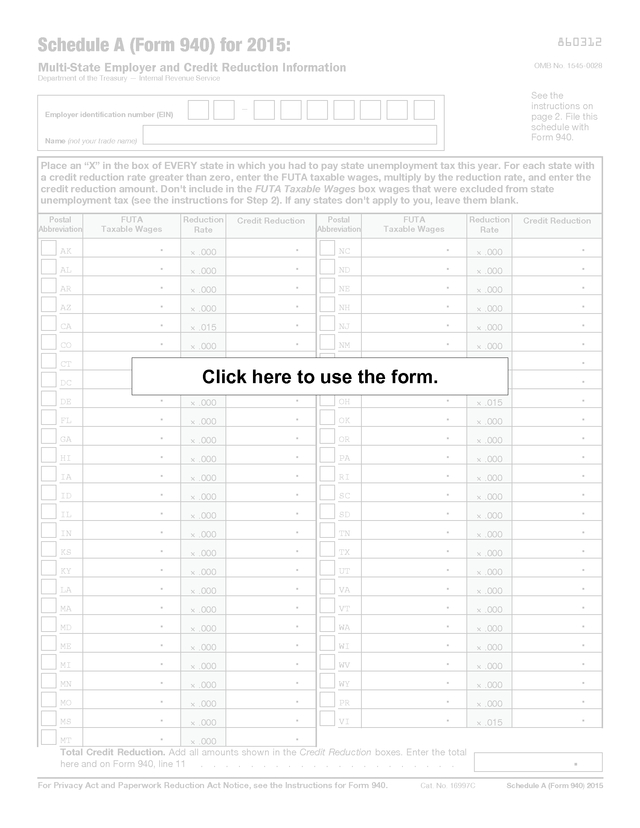

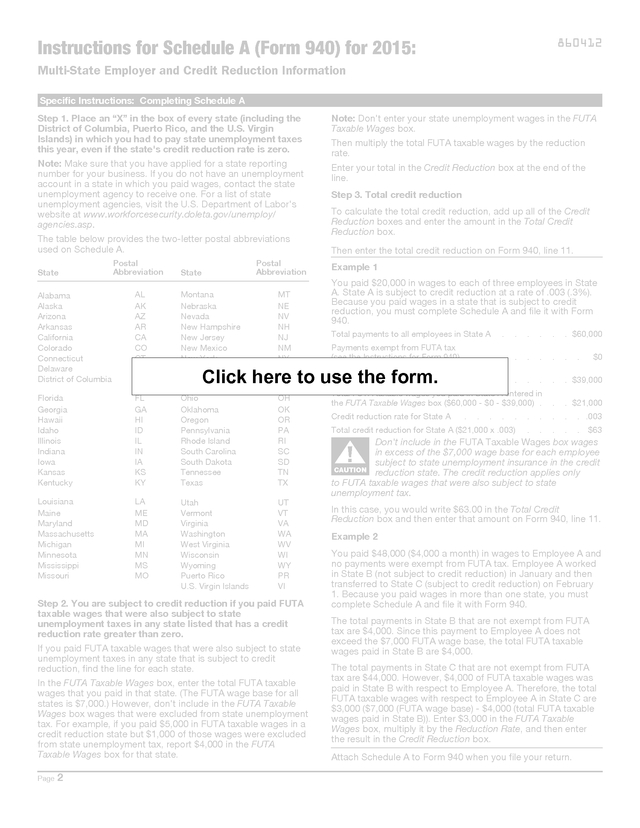

State Taxation of Salary Deferrals Chart 2015 - 2016 Changes 1. Returned Wage Reports 2. FUTA Credit Reductions Because of State Loans 3.

Credit Reductions States 4. FUTA Credit Reduction Rate Chart 5. Patient Protection & Affordable Care Act 6.

Publication 1542 – Per Diem Rate Tables – No Longer Updated Page 225 226 228 229 231 232 233 233 235 237 238 240 241 242 242 246 250 252 253 254 255 256 256 257 258 259 262 262 264 265 266 267 271 273 274 275 277 277 277 277 278 278 278 V. Appendix – Misc Contact Information, Forms, & Charts a. List of SSA Regional Employer Service Liaison Officers b.

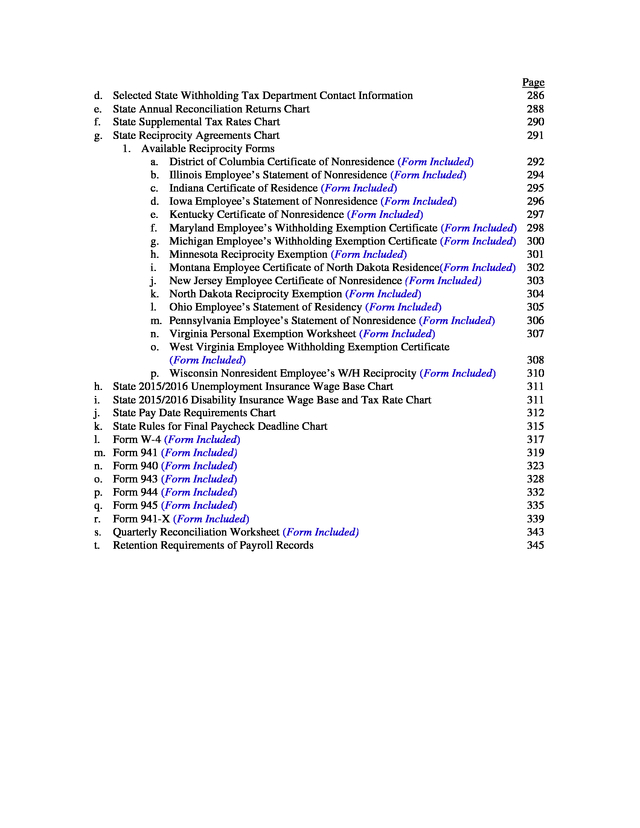

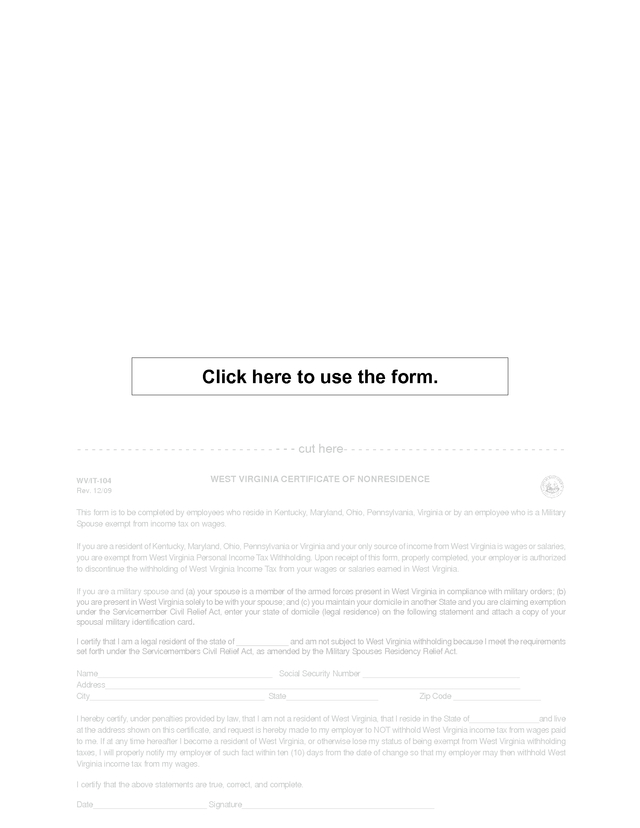

Other Websites and Information c. 2015/2016 Rate Chart 281 283 284 . d. e. f. g. h. i. j. k. l. m. n. o. p. q. r. s. t. Selected State Withholding Tax Department Contact Information State Annual Reconciliation Returns Chart State Supplemental Tax Rates Chart State Reciprocity Agreements Chart 1. Available Reciprocity Forms a. District of Columbia Certificate of Nonresidence (Form Included) b. Illinois Employee’s Statement of Nonresidence (Form Included) c.

Indiana Certificate of Residence (Form Included) d. Iowa Employee’s Statement of Nonresidence (Form Included) e. Kentucky Certificate of Nonresidence (Form Included) f.

Maryland Employee’s Withholding Exemption Certificate (Form Included) g. Michigan Employee’s Withholding Exemption Certificate (Form Included) h. Minnesota Reciprocity Exemption (Form Included) i.

Montana Employee Certificate of North Dakota Residence(Form Included) j. New Jersey Employee Certificate of Nonresidence (Form Included) k. North Dakota Reciprocity Exemption (Form Included) l.

Ohio Employee’s Statement of Residency (Form Included) m. Pennsylvania Employee’s Statement of Nonresidence (Form Included) n. Virginia Personal Exemption Worksheet (Form Included) o.

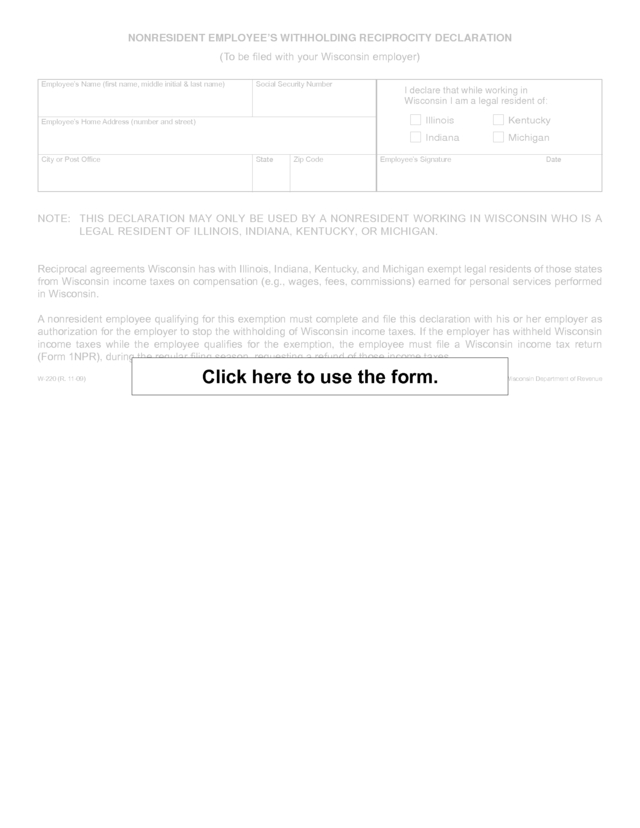

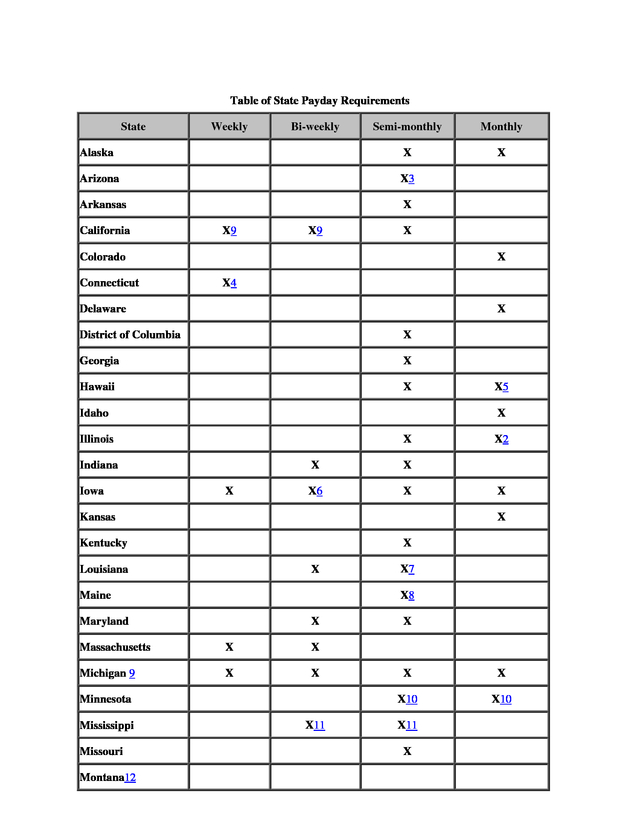

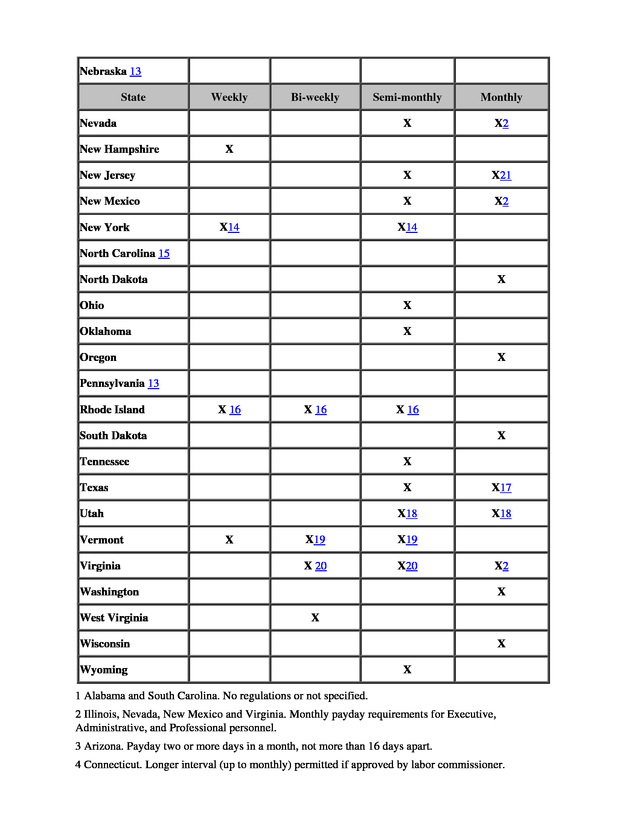

West Virginia Employee Withholding Exemption Certificate (Form Included) p. Wisconsin Nonresident Employee’s W/H Reciprocity (Form Included) State 2015/2016 Unemployment Insurance Wage Base Chart State 2015/2016 Disability Insurance Wage Base and Tax Rate Chart State Pay Date Requirements Chart State Rules for Final Paycheck Deadline Chart Form W-4 (Form Included) Form 941 (Form Included) Form 940 (Form Included) Form 943 (Form Included) Form 944 (Form Included) Form 945 (Form Included) Form 941-X (Form Included) Quarterly Reconciliation Worksheet (Form Included) Retention Requirements of Payroll Records Page 286 288 290 291 292 294 295 296 297 298 300 301 302 303 304 305 306 307 308 310 311 311 312 315 317 319 323 328 332 335 339 343 345 . I. INDEPENDENT CONTRACTOR OR EMPLOYEE? . Independent Contractor or Employee? The business relationship between the organization and the person performing the services must first be analyzed to determine how payments should be treated. The person performing the services may be classified as a common law employee, statutory employee, statutory non-employee, or an independent contractor. Common-Law Employees Under common-law rules, anyone performing services for an organization is the organization’s employee if the organization can control what will be done and how it will be done. This is so even when the organization gives the employee freedom of action. What matters is that the organization has the right to control the details of how the services are performed.

If there is an employer-employee relationship, it makes no difference how it is labeled. The substance of the relationship, not the label, governs the worker’s status. Nor does it matter whether the individual is employed full-time or part-time.

For employment tax purposes, no distinction is made between classes of employees. Superintendents, managers, and supervisory personnel are all employees. An officer of a corporation is generally an employee. An officer who performs no services or only minor services, and who neither receives nor is entitled to receive any pay, is not considered an employee.

A director of a corporation is not an employee with respect to services performed as a director. Partners are not employees. Statutory Employees: Workers may be treated as employees by statute (“statutory employees”) even if they are independent contractors under the common law rules. If the worker falls within any one of the following four categories and meets the three conditions below, they must be treated as an employee for certain employment tax purposes. 1) A driver who distributes beverages (other than milk) or meat, vegetable, fruit, or bakery products; or who picks up and delivers laundry or dry cleaning, if the driver is the organization’s agent or is paid on commission. 2) A full-time life insurance sales agent whose principal business activity is selling life insurance or annuity contracts, or both, primarily for one life insurance company. 3) An individual who works at home on materials or goods that the organization supplies and that must be returned to the organization or to a person named by the organization, if the organization also furnishes specifications for the work to be done. 4) A full-time traveling or city salesperson who works on the organizations behalf and turns in orders to the organization from wholesalers, retailers, contractors, or operators of hotels, restaurants, or other similar establishments. The goods sold must be merchandise for resale or supplies for use in the buyer’s business operation.

The work performed for the organization must be the salesperson’s principal business activity. Withhold social security and Medicare taxes from the wages of statutory employees if all three of the following conditions apply. 1) The service contract states or implies that substantially all the services are to be performed personally by them. . 2) They do not have a substantial investment in the equipment and property used to perform the services (other than an investment in transportation facilities, such as a car or truck). 3) The services are performed on a continuing basis for the same payer. For FUTA tax, the term “employee” means the same as it does for social security and Medicare taxes, except that it does not include statutory employees in categories 2 and 3 above. Thus any individual who is an employee under category 1 or 4 above is also an employee for FUTA tax purposes and subject to FUTA tax. Federal income tax is not withheld from the wages of statutory employees; however the wages are still reported in Box 1 of Form W-2. Be sure to check “Statutory Employee” in Box 13. Statutory Nonemployees: There are three categories of statutory nonemployees: direct sellers, licensed real estate agents, and certain companion sitters. Direct sellers and licensed real estate agents are treated as self-employed for all federal tax purposes, including income and employment taxes, if: ï‚· Substantially all payments for their services as direct sellers or real estate agents are directly related to sales or other output, rather than to the number of hours worked and ï‚· Their services are performed under a written contract providing that they will not be treated as employees for federal tax purposes. o Direct sellers include persons falling within any of the following three groups: 1) Persons engaged in selling (or soliciting the sale of) consumer products in the home or place of business other than in a permanent retail establishment. 2) Persons engaged in selling (or soliciting the sale of) consumer products to any buyer on a buy-sell basis, a deposit-commission basis, or any similar basis prescribed by regulations, for resale in the home or at a place of business other than in a permanent retail establishment. 3) Persons engaged in the trade or business of delivering or distributing newspapers or shopping news (including any services directly related to such delivery or distribution). Direct selling includes activities of individuals who attempt to increase direct sales activities of their direct sellers and who earn income based on the productivity of their direct sellers. Such activities include providing motivation and encouragement; imparting skills, knowledge, or experience; and recruiting. o Licensed Real Estate Agents include individuals engaged in appraisal activities for real estate sales if they earn income based on sales or other output. o Companion sitters include individuals who furnish personal attendance, companionship, or household care services to children, or individuals who are elderly or disabled.

A person engaged in the trade or business of putting the sitters in touch with individuals who wish to employ them (a companion sitting placement service) will not be treated as the employer of the sitters if that person does not receive or pay the salary or wages of the sitters and is compensated by the sitters or the persons who employ them on a fee basis. Companion sitters . who are not employees of a companion sitting placement service are generally treated as selfemployed for federal tax purposes. Determining who is an employee: The primary method used to determine whether an employee-employer relationship exists is the “common law” test. The central focus of the common law test is determining who has the right to control two basic elements: (1) what must be done – i.e., the results of the work, and (2) how it must be done – i.e., the method by which the work or services are performed. Under this test, a worker is considered an employee subject to payroll tax withholding if the employer has the right to control both the result to be accomplished and the method or means by which the result is achieved. If the employer has the right to control or direct only the result of the work – and not the method or means used to accomplish the result – the individual generally qualifies as an independent contractor. The common law test can be difficult to apply to specific cases or situations.

Proper application of the test requires an employer to consider a number of factors or characteristics of the work in question to determine whether an employer-employee relationship exists. The two primary characteristics that typically indicate that an individual is an employee are: (1) the employer has the right to discharge the worker, and (2) the employer supplies the worker with tools and a place to work. On the other hand, individuals such as lawyers, physicians, and contractors who offer their services to the general public in the pursuit of an independent trade, business, or profession normally are not considered employees. Keep in mind, however, that no one factor or set of factors is automatically controlling.

All the facts and circumstances of a particular situation must be taken into account in determining whether an individual worker should be treated as an employee or as an independent contractor. Factors Used by IRS in Determining Employee Status: The general rule for determining if a worker is an independent contractor is if the organization for which the services are performed, has the right to control or direct only the result of the work and not the means or methods of accomplishing the result. Facts that provide evidence of the degree of control and independence fall into three categories, behavioral control, financial control, and type of relationship. Behavioral Control: May be demonstrated by facts which illustrate that there is a right to direct or control how the worker performs the specific tasks for which he/she is engaged. Types and Degree of Instructions – An individual who must comply with another person’s instructions about when, where, or how to work is generally considered an employee. This applies even if the business simply has the right to require compliance, but does not exercise that right. Types of instructions that will tend to classify a worker as an employee include direction as to which tools or equipment to use, which workers to hire to assist with the work, where to purchase supplies or services, which work must be performed by a specified individual, which routines or patterns must be used, and which order or sequence of work must be followed, as well as a requirement to obtain approval before taking certain actions.

Instructions given in order to be in compliance with governmental agencies or industry governing bodies will be given little weight in determining worker status. More detailed instructions indicate the worker is an employee. Less detailed instruction affirms less control, indicating the workers is more likely to be and independent contractor. .

Evaluation – An evaluation system measuring the details of how work is performed would point to an employee. If the evaluation system measures only the end result, the individual could be either an independent contractor or employee. Training – Periodic or ongoing training provided by a business about procedures to be followed and methods to be used indicates that the business wants the services performed in a particular manner and is evidence of an employer-employee relationship. However, information about the business’ policies or products or about applicable governmental statutes or regulations are not considered training for worker status determination purposes, nor are training programs that are voluntary and for which no compensation is given. Independent contractors ordinarily use their own methods to perform services. Financial Control: May be demonstrated by facts which illustrate that there is a right to direct or control the economic aspects of the worker’s activities.

Whether or not the worker is personally economically dependent on the business has no bearing on this category of evidence, nor does the worker’s general economic status. Significant Investment – An independent contractor often has a significant investment in the facilities or tools used in performing the services for someone else. However; although a significant investment is not necessary for independent contractor status, the rental or purchase of items at fair market value will give a greater weight to the consideration of a worker as an independent contractor. Unreimbursed Expenses – The extent to which a worker chooses to incur expenses and bear their cost impact the worker’s opportunity for profit or loss and lends evidence towards the worker’s status as an independent contractor. Businesses may pay portions of the expenses of an independent contractor, so the focus should be on unreimbursed expenses, especially fixed, ongoing costs that are incurred regardless of whether work is performed.

Examples include rent and utilities, training, advertising, wages of assistants, licensing, insurance, and travel. Minor tool expenses generally do not lend evidence toward an independent contractor status. Services Available to the Relevant Market – Independent contractors often advertise and maintain a visible location in order to be available to work for the relevant market. However, the absence of these activities is a neutral fact, as an independent contractor may rely on word of mouth or may be under a long-term contract. Method of Payment – Employees generally are paid by the hour, day, week, or month, indicating a guaranteed return for labor.

Independent contractors typically are paid a flat fee or on a time and material basis for performance of a task. The frequency under which payments are made is not relevant. However, it is customary in certain types of businesses, such a law or accounting, to pay independent contractors by the hour. Opportunity for Profit or Loss – This is probably the most important type of evidence within the category of financial control, and the other four items (significant investment, unreimbursed expenses, services available, and method of payment) all have an impact on this one.

However, not all four are required in order for there to be an opportunity for profit or loss. Most important in this type of evidence is whether the worker is free to make business decisions affecting his/her own profit or loss. To the extent the worker makes such decisions, more weight will be given toward the status of independent contractor.

Examples include decisions regarding types and quantity of inventory, capital investment, and purchase or lease of premises and equipment. If the . individual has the possibility of incurring a loss, they are an independent contractor. The fact that a worker may receive more money by working longer hours does not enter into consideration. Relationship of the Parties: The relationship of how the worker and business perceive each other in terms of their intent concerning control will be considered by IRS auditors. Intent of Parties/Written Contracts – A written agreement describing the worker as an independent contractor is viewed as evidence of the parties’ intent, but is not, in itself, sufficient evidence for determining worker status. However, the contract may specify items that are relevant, such as methods of compensation, expenses to be reimbursed, or how work will be performed. If it is otherwise impossible for IRS to determine a worker’s status, the intent of the parties may be used to resolve the issue. Employee Benefits – Providing a worker with benefits traditionally associated with employee status will lend weight to the determination of the worker as an employee.

Examples of such benefits include paid vacation or sick pay, health insurance, life insurance, and a pension plan. The determination that a worker is an employee under certain state or federal laws, such as for unemployment benefits or for worker’s compensation coverage, shall have no impact on the IRS consideration. Permanency of the Relationship – Traditionally, the ability to immediately terminate the relationship on the part of either the business or the worker indicates an employee status, and the opposite was the case for an independent contractor. However, this is not universally the case anymore, and this type of evidence is used to a much lesser extent than it used to be, except in the case of a business’ ability to refuse payment for unsatisfactory work by an independent contractor. Employees usually are hired for an indefinite period, rather than for a specific project or period.

This is not to be confused with the potentially long-term (but definite) period of time for which independent contractors are often hired. Occasionally, employees are hired for definite periods of time (long- or short-term). For this reason, a relationship that is indefinite in length may be viewed as evidence of an employee status, but a relationship that is not indefinite is a neutral fact. Regular Business Activity – The fact that an individual’s services are a key aspect of the regular business of the organization may indicate that the individual is subject to a certain amount of control by the organization, which would lend evidence toward an employee status. However, this would need to be investigated.

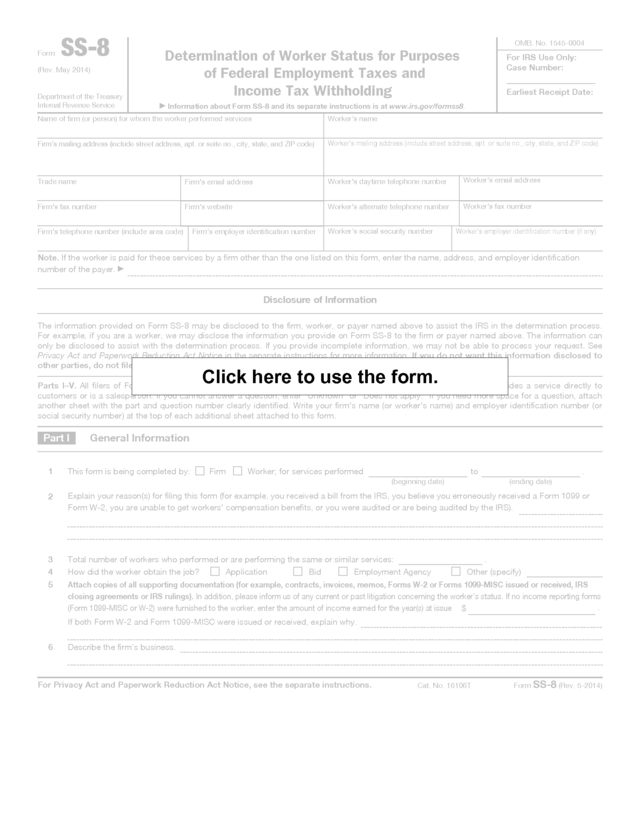

The fact that the services performed are part of the regular business does not itself lend weight toward determination as an employee. IRS assistance is available by filing a Form SS-8: Employers or workers who have doubts about an individual’s status under the federal employment tax and income tax withholding laws can fill out Form SS-8 and send it to IRS. The agency will use the information provided on the form, along with any information that it can obtain from all parties involved, to determine the status of a worker. Even if it is not mailed to the IRS, it may be beneficial to complete the SS-8 form on the worker in question to help analyze if they are an employee or an independent contractor. IRS Reclassification: Employer Liability: You will generally be liable for social security and Medicare taxes and withheld income tax if you do not deduct and withhold these taxes because you treated an employee as a nonemployee.

You may be able to calculate your liability using special rates in Internal Revenue Code Section 3509 for the employee’s share of social security, Medicare taxes and federal income tax withholding. The applicable rates depend on whether you filed required Forms 1099. You cannot recover the employee share of social security, Medicare tax, or .

income tax withholding from the employee. You are liable for the income tax withholding regardless of whether the employee paid income tax on the wages. You continue to owe the full employer share of social security and Medicare taxes. See Internal Revenue Code section 3509 for details.

Also see the instructions for Form 941-X. Section 3509 rates are not available if you intentionally disregard the requirement to withhold taxes from the employee or if you withheld income taxes but not social security or Medicare taxes. Section 3509 is not available for reclassifying statutory employees and for wages paid to employees in the current year. If the employer issued required information returns, the section 3509(a) rates are: ï‚· For social security taxes; employer rate of 6.2% plus 20% of the employee rate of 6.2%, for a total rate of 7.44% of wages. (see the Instructions for Form 941-X). ï‚· For Medicare taxes; employer rate of 1.45% plus 20% of the employee rate of 1.45%, for a total rate of 1.74% of wages. ï‚· For income tax withholding, the rate is 1.5% of wages. ï‚· The rate is .18% for additional Medicare tax on excess wages over $200,000. If the employer did not issue required information returns, the section 3509(b) rates are: ï‚· For social security taxes; employer rate of 6.2% plus 40% of the employee rate of 6.2%, for a total rate of 8.68% of wages.

(see the Instructions for Form 941-X). ï‚· For Medicare taxes; employer rate of 1.45% plus 40% of the employee rate of 1.45%, for a total rate of 2.03% of wages. ï‚· For income tax withholding, the rate is 3.0% of wages. ï‚· The rate is .36% for additional Medicare tax on excess wages over $200,000. Relief Provisions: Under Section 530, an organization may receive relief from owing employment taxes if they meet the relief requirements. If the organization does not meet the relief requirements, the IRS will need to determine whether the workers are independent contractors or employees and whether the organization owes employment taxes for those workers. To receive the relief, all three of the following requirements must be met: ï‚· Reasonable basis – there was a reasonable basis for not treating the workers as employees. To establish reasonable basis, the following must be shown: o You reasonably relied on a court case about Federal taxes or a ruling issued to you by the IRS; or o Your business was audited by the IRS at a time when you treated similar workers as independent contractors and the IRS did not reclassify those workers as employees.

You may not rely on an audit commenced after December 31, 1996, unless such audit included an examination for employment tax purposes of whether the individual involved (or any other individual holding a substantially similar position) should be treated as your employee; or o You treated the workers as independent contractors because you knew that was how a significant segment of your industry treated similar workers; or o You relied on some other reasonable basis. For example, you relied on the advice of a . business lawyer or accountant who knew the facts about your business. If you did not have a reasonable basis for treating the workers as independent contractors, you do not meet the relief requirements. ï‚· Substantive Consistency – In addition, you (and any predecessor business) must have treated the workers, and any similar workers, as independent contractors. If you treated similar workers as employees, this relief provision is not available. If you are paying an individual who is providing services as a test proctor or room supervisor assisting in the administration of college entrance or placements examinations, the substantive consistency requirement does not apply with respect to services performed after December 31, 2006, (and remuneration paid with respect to such services). The provision applies if the individual (1) is performing the services for a tax-exempt organization, and (2) is not otherwise treated as an employee of such organization for purposes of employment taxes. ï‚· Reporting Consistency – Finally, you must have filed all required federal tax returns (including information returns) consistent with your treatment of each worker as not being employees. This means, for example, that if you treated a worker as an independent contractor and paid him or her $600 or more, you must have filed Form 1099-MISC for the worker.

Relief is not available for any year and for any workers for whom you did not file the required information returns. Examples: 1. Kathy works for ABC, Inc. as a secretary from 8:00 to 5:00, Monday thru Friday. She learns that the company that was cleaning their offices has quit.

Kathy offers to clean the offices after working hours. The office manager agrees and shows Kathy where the vacuum and cleaning supplies are kept and instructs her to start cleaning at 7:00 pm and to be finished by 9:00 pm each evening. The manager also tells her that the nightly security guard will be checking on her periodically to make sure that she is there doing her work. Since Kathy has been given specific instructions on how to do the work, the hours in which to do it, will be supervised, and is provided with the necessary tools, she is an employee for payroll tax purposes.

Since she is also working 40 hours per week, she must also be paid overtime for her after hours work. 2. Bill also works for ABC, Inc as a shop foreman. Bill has his own cleaning service and cleans for several office buildings in the area. He discusses his services with the office manager and explains he has a cleaning crew.

He will bring his crew sometime between 7:00 pm and 6:00 am with their cleaning tools and supplies with them. The office manager agrees to the arrangement. Since Bill has an opportunity for profit or loss, a significant investment in supplies and labor, services are available to the market, and is not supervised or managed, he is an independent contractor. . Form SS-8 (Rev. May 2014) Department of the Treasury Internal Revenue Service OMB. No. 1545-0004 Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding For IRS Use Only: Case Number: Earliest Receipt Date: Information about Form SS-8 and its separate instructions is at www.irs.gov/formss8. Name of firm (or person) for whom the worker performed services Worker’s name Firm’s mailing address (include street address, apt.

or suite no., city, state, and ZIP code) Worker’s mailing address (include street address, apt. or suite no., city, state, and ZIP code) Trade name Firm's email address Worker's daytime telephone number Worker's email address Firm's fax number Firm's website Worker's alternate telephone number Worker's fax number Firm's telephone number (include area code) Firm’s employer identification number Worker’s social security number Worker’s employer identification number (if any) Note. If the worker is paid for these services by a firm other than the one listed on this form, enter the name, address, and employer identification number of the payer. Disclosure of Information The information provided on Form SS-8 may be disclosed to the firm, worker, or payer named above to assist the IRS in the determination process. For example, if you are a worker, we may disclose the information you provide on Form SS-8 to the firm or payer named above.

The information can only be disclosed to assist with the determination process. If you provide incomplete information, we may not be able to process your request. See Privacy Act and Paperwork Reduction Act Notice in the separate instructions for more information.

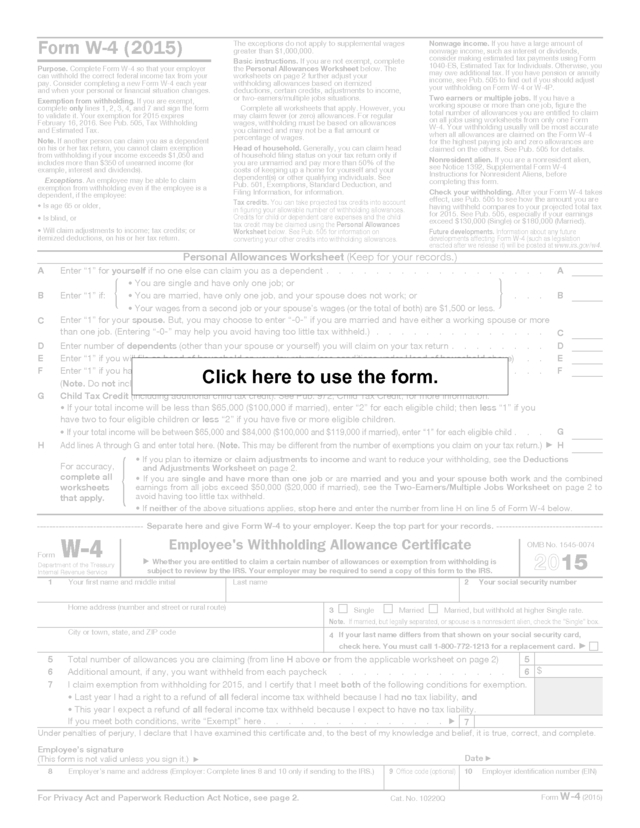

If you do not want this information disclosed to other parties, do not file Form SS-8. Click here to use the form. Parts I–V. All filers of Form SS-8 must complete all questions in Parts I–IV. Part V must be completed if the worker provides a service directly to customers or is a salesperson.

If you cannot answer a question, enter “Unknown” or “Does not apply.” If you need more space for a question, attach another sheet with the part and question number clearly identified. Write your firm's name (or worker's name) and employer identification number (or social security number) at the top of each additional sheet attached to this form. Part I 1 General Information This form is being completed by: Firm Worker; for services performed to (beginning date) . (ending date) 2 Explain your reason(s) for filing this form (for example, you received a bill from the IRS, you believe you erroneously received a Form 1099 or Form W-2, you are unable to get workers' compensation benefits, or you were audited or are being audited by the IRS). 3 4 Total number of workers who performed or are performing the same or similar services: Application Bid Employment Agency How did the worker obtain the job? 5 Attach copies of all supporting documentation (for example, contracts, invoices, memos, Forms W-2 or Forms 1099-MISC issued or received, IRS closing agreements or IRS rulings). In addition, please inform us of any current or past litigation concerning the worker’s status.

If no income reporting forms . (Form 1099-MISC or W-2) were furnished to the worker, enter the amount of income earned for the year(s) at issue $ . Other (specify) If both Form W-2 and Form 1099-MISC were issued or received, explain why. 6 Describe the firm’s business. For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 16106T Form SS-8 (Rev.

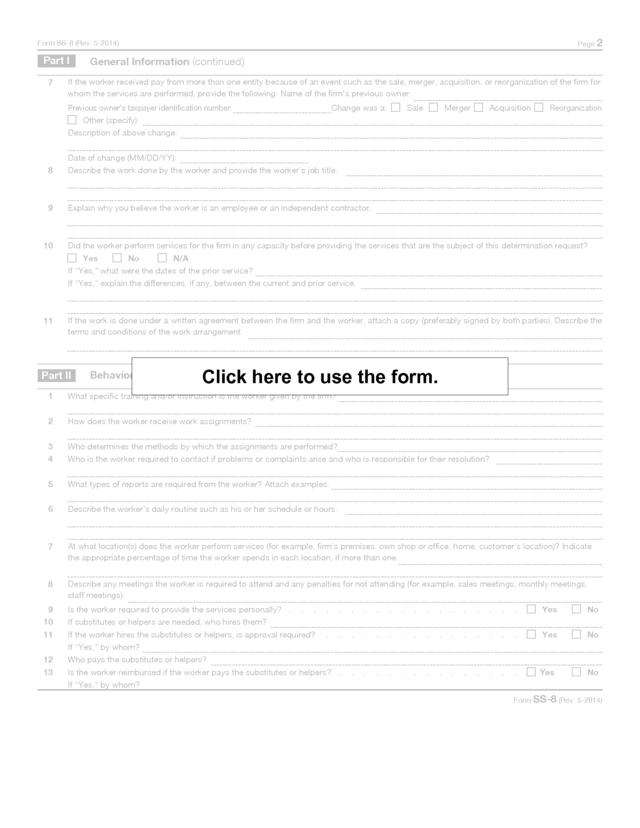

5-2014) . Page 2 Form SS-8 (Rev. 5-2014) Part I 7 General Information (continued) If the worker received pay from more than one entity because of an event such as the sale, merger, acquisition, or reorganization of the firm for whom the services are performed, provide the following: Name of the firm's previous owner: Previous owner's taxpayer identification number: Other (specify) Description of above change: Change was a: 8 Merger Acquisition Reorganization Date of change (MM/DD/YY): Describe the work done by the worker and provide the worker’s job title. 9 Sale Explain why you believe the worker is an employee or an independent contractor. 10 Did the worker perform services for the firm in any capacity before providing the services that are the subject of this determination request? Yes No N/A If “Yes,” what were the dates of the prior service? If “Yes,” explain the differences, if any, between the current and prior service. 11 If the work is done under a written agreement between the firm and the worker, attach a copy (preferably signed by both parties). Describe the terms and conditions of the work arrangement. Part II Click here to use the form. Behavioral Control (Provide names and titles of specific individuals, if applicable.) 1 What specific training and/or instruction is the worker given by the firm? 2 How does the worker receive work assignments? 3 Who determines the methods by which the assignments are performed? 4 Who is the worker required to contact if problems or complaints arise and who is responsible for their resolution? 5 What types of reports are required from the worker? Attach examples. 6 Describe the worker’s daily routine such as his or her schedule or hours. 7 At what location(s) does the worker perform services (for example, firm’s premises, own shop or office, home, customer’s location)? Indicate the appropriate percentage of time the worker spends in each location, if more than one. 8 Describe any meetings the worker is required to attend and any penalties for not attending (for example, sales meetings, monthly meetings, staff meetings). 9 10 11 Is the worker required to provide the services personally? . .

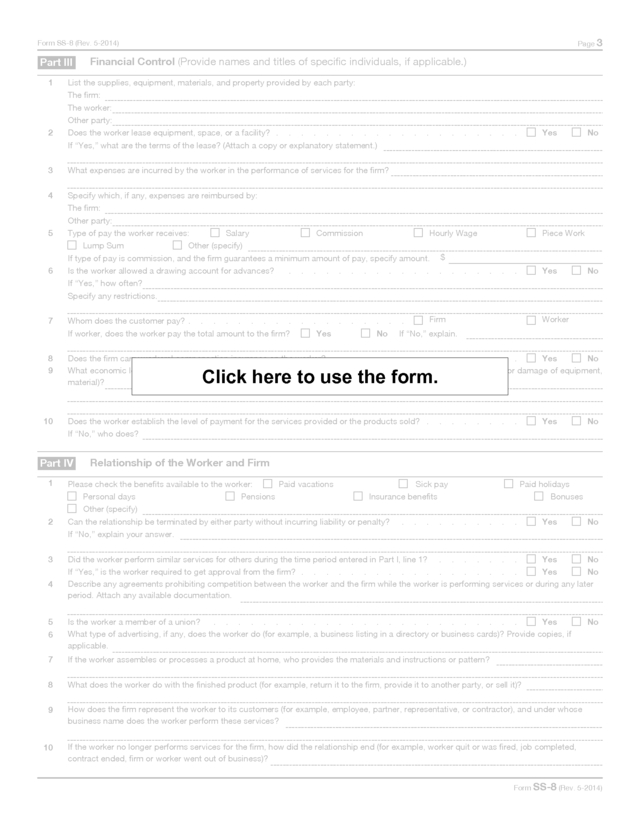

. If substitutes or helpers are needed, who hires them? If the worker hires the substitutes or helpers, is approval required? If “Yes,” by whom? . . . . . . . . . . . . . . . . Yes No . . . . . . . . . . . . . . . . Yes No 12 13 Who pays the substitutes or helpers? Is the worker reimbursed if the worker pays the substitutes or helpers? . If “Yes,” by whom? . . . . . . . . . . . . . . Yes No Form SS-8 (Rev. 5-2014) . Page 3 Form SS-8 (Rev. 5-2014) Part III 1 Financial Control (Provide names and titles of specific individuals, if applicable.) List the supplies, equipment, materials, and property provided by each party: The firm: The worker: 2 Other party: Does the worker lease equipment, space, or a facility? . . . . . . . . . . . . . . . . . . . . Yes No If “Yes,” what are the terms of the lease? (Attach a copy or explanatory statement.) 3 What expenses are incurred by the worker in the performance of services for the firm? 4 Specify which, if any, expenses are reimbursed by: The firm: Other party: 5 Type of pay the worker receives: Salary Commission Hourly Wage Lump Sum Other (specify) If type of pay is commission, and the firm guarantees a minimum amount of pay, specify amount. $ 6 Is the worker allowed a drawing account for advances? If “Yes,” how often? Specify any restrictions. . . . . . . . . 7 Whom does the customer pay? . .

. . .

. . .

. If worker, does the worker pay the total amount to the firm? . . . . Yes . . Firm . .

. No If “No,” explain. 8 9 Does the firm carry workers' compensation insurance on the worker? . . .

. . .

. . .

. . .

. . . Yes No What economic loss or financial risk, if any, can the worker incur beyond the normal loss of salary (for example, loss or damage of equipment, material)? 10 . . . . . . . . . Yes . No Worker Click here to use the form. Does the worker establish the level of payment for the services provided or the products sold? . If “No,” who does? Part IV 1 . Piece Work . . . . . . . Yes No Relationship of the Worker and Firm Please check the benefits available to the worker: Paid vacations Pensions Personal days Other (specify) Sick pay Paid holidays Bonuses Insurance benefits 2 Can the relationship be terminated by either party without incurring liability or penalty? If “No,” explain your answer. 3 Did the worker perform similar services for others during the time period entered in Part I, line 1? .

. . .

. . . Yes No Yes No If “Yes,” is the worker required to get approval from the firm? .

. . .

. . .

. . .

. . .

. . .

. . Describe any agreements prohibiting competition between the worker and the firm while the worker is performing services or during any later period. Attach any available documentation. 4 . . . . . . . . . . Yes 5 6 Is the worker a member of a union? .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . . Yes What type of advertising, if any, does the worker do (for example, a business listing in a directory or business cards)? Provide copies, if applicable. 7 If the worker assembles or processes a product at home, who provides the materials and instructions or pattern? 8 What does the worker do with the finished product (for example, return it to the firm, provide it to another party, or sell it)? 9 No How does the firm represent the worker to its customers (for example, employee, partner, representative, or contractor), and under whose business name does the worker perform these services? 10 No If the worker no longer performs services for the firm, how did the relationship end (for example, worker quit or was fired, job completed, contract ended, firm or worker went out of business)? Form SS-8 (Rev.

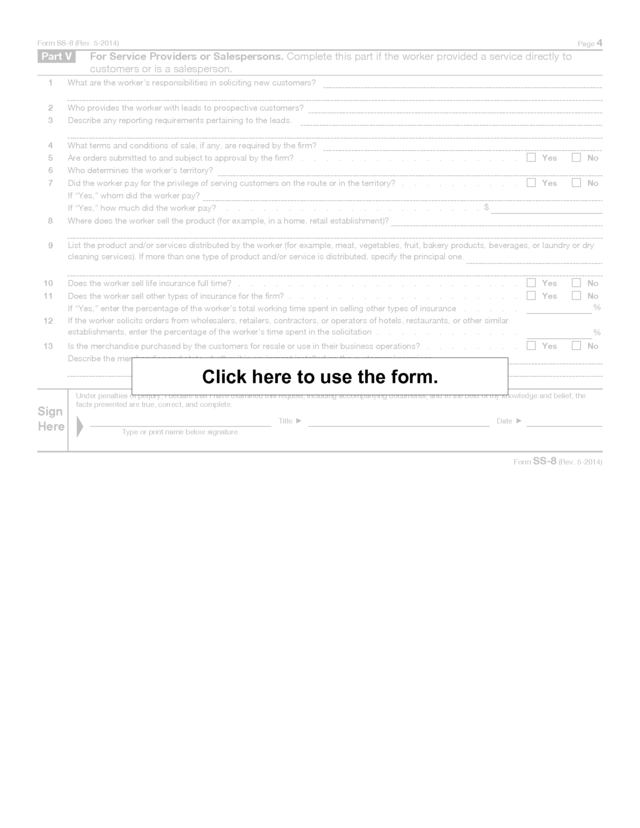

5-2014) . Page 4 Form SS-8 (Rev. 5-2014) Part V For Service Providers or Salespersons. Complete this part if the worker provided a service directly to customers or is a salesperson. 1 What are the worker’s responsibilities in soliciting new customers? 2 3 Who provides the worker with leads to prospective customers? Describe any reporting requirements pertaining to the leads. 4 5 What terms and conditions of sale, if any, are required by the firm? Are orders submitted to and subject to approval by the firm? . . . . . . . . . . . . Yes No 6 Who determines the worker’s territory? 7 Did the worker pay for the privilege of serving customers on the route or in the territory? . . . . . . . . . . Yes No If “Yes,” whom did the worker pay? If “Yes,” how much did the worker pay? . . . . . .

$ . . . . . . . . . . . . . . . . . . . . . 8 Where does the worker sell the product (for example, in a home, retail establishment)? 9 List the product and/or services distributed by the worker (for example, meat, vegetables, fruit, bakery products, beverages, or laundry or dry cleaning services). If more than one type of product and/or service is distributed, specify the principal one. 10 11 Does the worker sell life insurance full time? . .

. . . Does the worker sell other types of insurance for the firm? . 12 If “Yes,” enter the percentage of the worker’s total working time spent in selling other types of insurance .

. . .

. If the worker solicits orders from wholesalers, retailers, contractors, or operators of hotels, restaurants, or other similar establishments, enter the percentage of the worker’s time spent in the solicitation . . .

. . .

. . .

. . . 13 . . . . . . . . . . . . . . . . . . . . . . . . Is the merchandise purchased by the customers for resale or use in their business operations? .

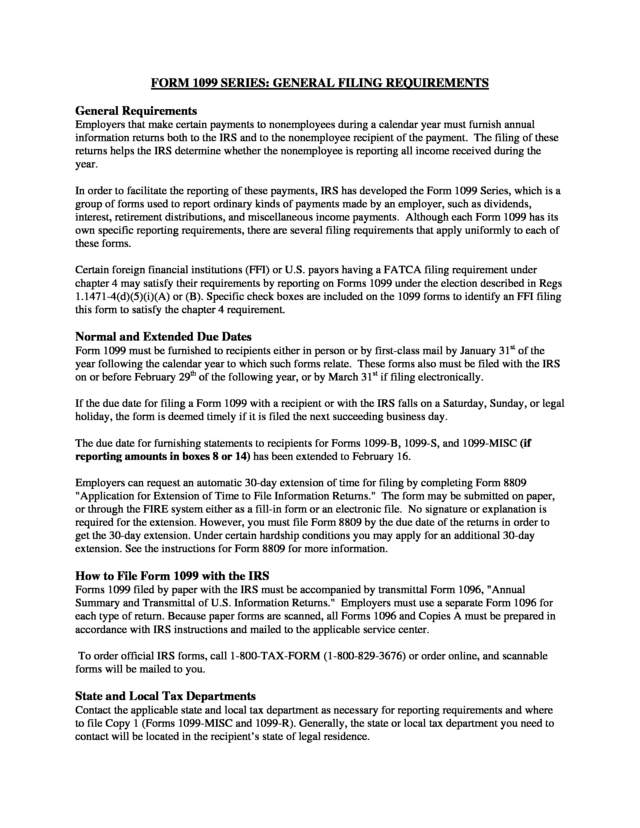

. Describe the merchandise and state whether it is equipment installed on the customers’ premises. . . . . . . . . . . . . . . . . . . Yes No Yes No % Yes No % Click here to use the form. Sign Here Under penalties of perjury, I declare that I have examined this request, including accompanying documents, and to the best of my knowledge and belief, the facts presented are true, correct, and complete. Title Date Type or print name below signature. Form SS-8 (Rev. 5-2014) . II. 1099 INFORMATION RETURNS . FORM 1099 SERIES: GENERAL FILING REQUIREMENTS General Requirements Employers that make certain payments to nonemployees during a calendar year must furnish annual information returns both to the IRS and to the nonemployee recipient of the payment. The filing of these returns helps the IRS determine whether the nonemployee is reporting all income received during the year. In order to facilitate the reporting of these payments, IRS has developed the Form 1099 Series, which is a group of forms used to report ordinary kinds of payments made by an employer, such as dividends, interest, retirement distributions, and miscellaneous income payments. Although each Form 1099 has its own specific reporting requirements, there are several filing requirements that apply uniformly to each of these forms. Certain foreign financial institutions (FFI) or U.S. payors having a FATCA filing requirement under chapter 4 may satisfy their requirements by reporting on Forms 1099 under the election described in Regs 1.1471-4(d)(5)(i)(A) or (B).

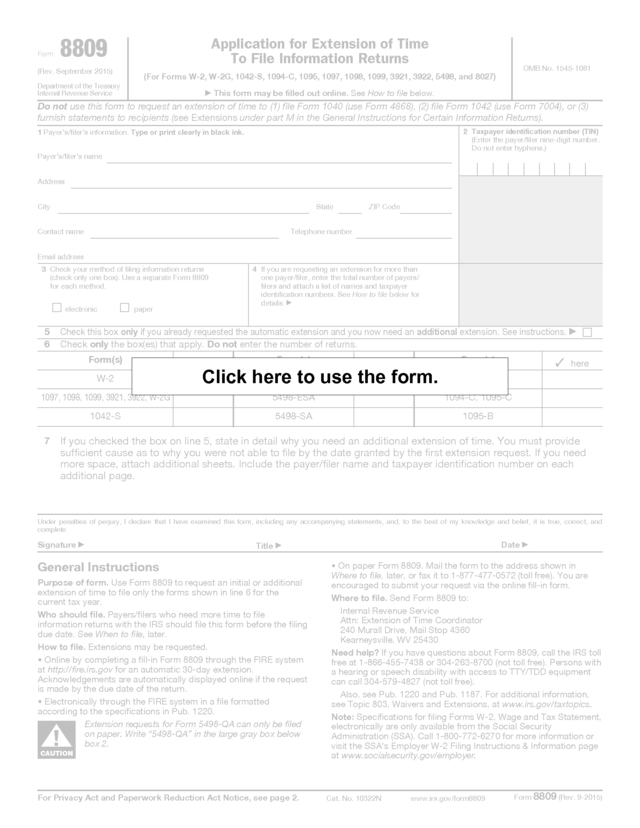

Specific check boxes are included on the 1099 forms to identify an FFI filing this form to satisfy the chapter 4 requirement. Normal and Extended Due Dates Form 1099 must be furnished to recipients either in person or by first-class mail by January 31st of the year following the calendar year to which such forms relate. These forms also must be filed with the IRS on or before February 29th of the following year, or by March 31st if filing electronically. If the due date for filing a Form 1099 with a recipient or with the IRS falls on a Saturday, Sunday, or legal holiday, the form is deemed timely if it is filed the next succeeding business day. The due date for furnishing statements to recipients for Forms 1099-B, 1099-S, and 1099-MISC (if reporting amounts in boxes 8 or 14) has been extended to February 16. Employers can request an automatic 30-day extension of time for filing by completing Form 8809 "Application for Extension of Time to File Information Returns." The form may be submitted on paper, or through the FIRE system either as a fill-in form or an electronic file. No signature or explanation is required for the extension.

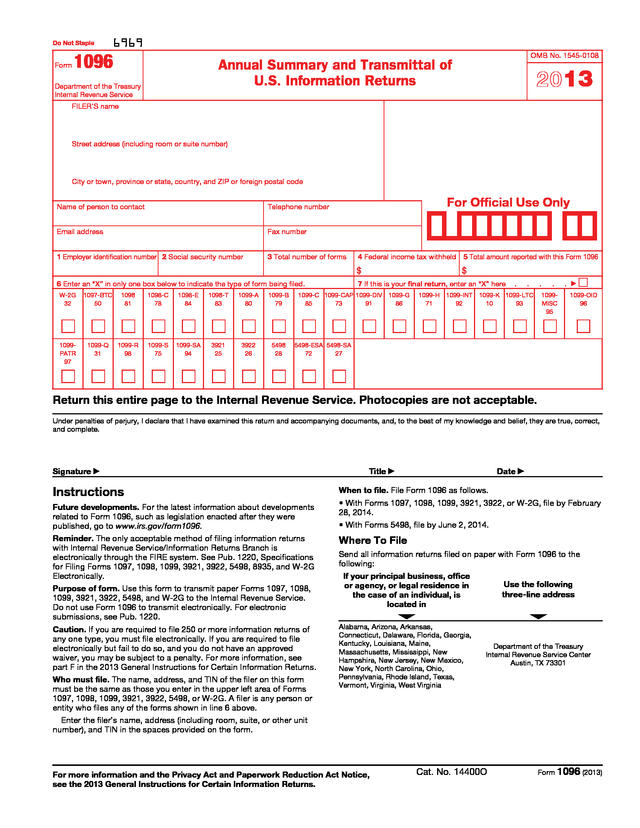

However, you must file Form 8809 by the due date of the returns in order to get the 30-day extension. Under certain hardship conditions you may apply for an additional 30-day extension. See the instructions for Form 8809 for more information. How to File Form 1099 with the IRS Forms 1099 filed by paper with the IRS must be accompanied by transmittal Form 1096, "Annual Summary and Transmittal of U.S.

Information Returns." Employers must use a separate Form 1096 for each type of return. Because paper forms are scanned, all Forms 1096 and Copies A must be prepared in accordance with IRS instructions and mailed to the applicable service center. To order official IRS forms, call 1-800-TAX-FORM (1-800-829-3676) or order online, and scannable forms will be mailed to you. State and Local Tax Departments Contact the applicable state and local tax department as necessary for reporting requirements and where to file Copy 1 (Forms 1099-MISC and 1099-R). Generally, the state or local tax department you need to contact will be located in the recipient’s state of legal residence. .

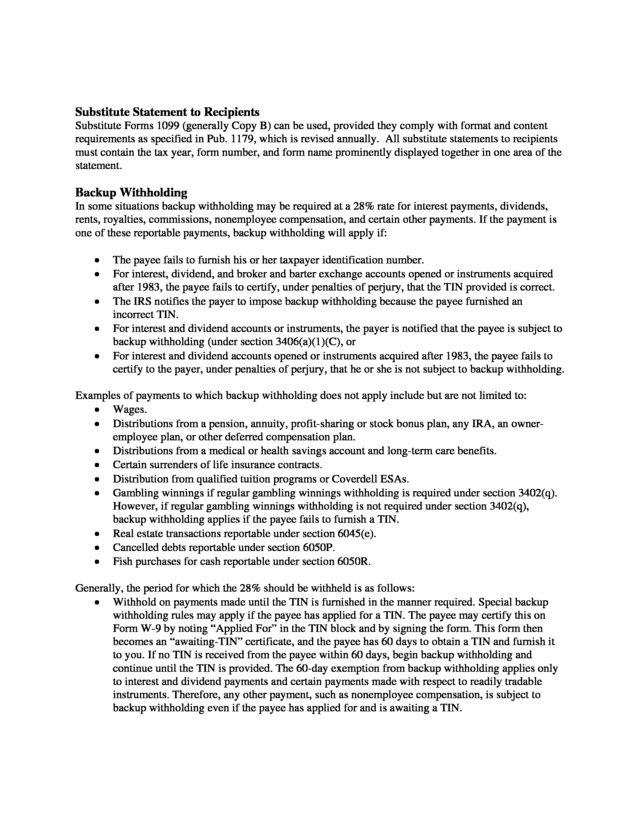

Substitute Statement to Recipients Substitute Forms 1099 (generally Copy B) can be used, provided they comply with format and content requirements as specified in Pub. 1179, which is revised annually. All substitute statements to recipients must contain the tax year, form number, and form name prominently displayed together in one area of the statement. Backup Withholding In some situations backup withholding may be required at a 28% rate for interest payments, dividends, rents, royalties, commissions, nonemployee compensation, and certain other payments. If the payment is one of these reportable payments, backup withholding will apply if: ï‚· ï‚· ï‚· ï‚· ï‚· The payee fails to furnish his or her taxpayer identification number. For interest, dividend, and broker and barter exchange accounts opened or instruments acquired after 1983, the payee fails to certify, under penalties of perjury, that the TIN provided is correct. The IRS notifies the payer to impose backup withholding because the payee furnished an incorrect TIN. For interest and dividend accounts or instruments, the payer is notified that the payee is subject to backup withholding (under section 3406(a)(1)(C), or For interest and dividend accounts opened or instruments acquired after 1983, the payee fails to certify to the payer, under penalties of perjury, that he or she is not subject to backup withholding. Examples of payments to which backup withholding does not apply include but are not limited to: ï‚· Wages. ï‚· Distributions from a pension, annuity, profit-sharing or stock bonus plan, any IRA, an owneremployee plan, or other deferred compensation plan. ï‚· Distributions from a medical or health savings account and long-term care benefits. ï‚· Certain surrenders of life insurance contracts. ï‚· Distribution from qualified tuition programs or Coverdell ESAs. ï‚· Gambling winnings if regular gambling winnings withholding is required under section 3402(q). However, if regular gambling winnings withholding is not required under section 3402(q), backup withholding applies if the payee fails to furnish a TIN. ï‚· Real estate transactions reportable under section 6045(e). ï‚· Cancelled debts reportable under section 6050P. ï‚· Fish purchases for cash reportable under section 6050R. Generally, the period for which the 28% should be withheld is as follows: ï‚· Withhold on payments made until the TIN is furnished in the manner required.

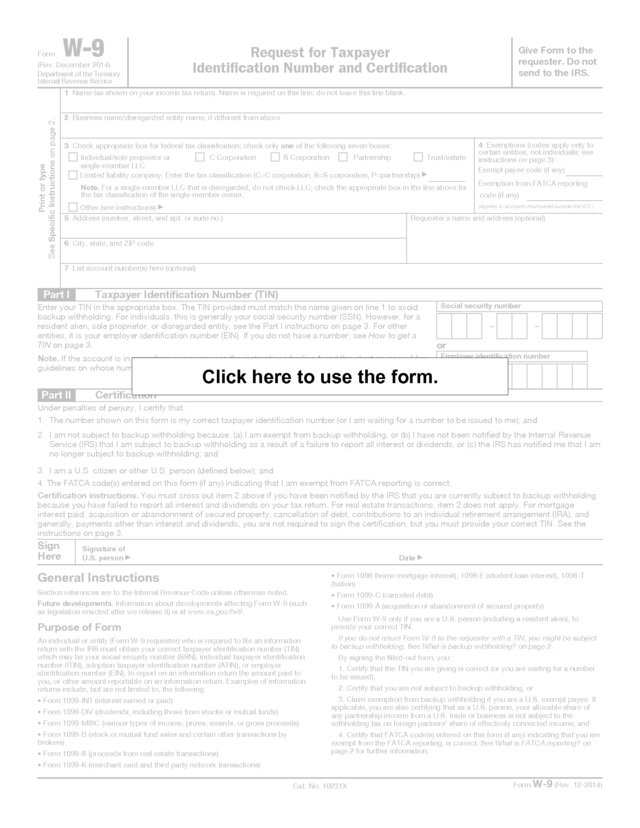

Special backup withholding rules may apply if the payee has applied for a TIN. The payee may certify this on Form W-9 by noting “Applied For” in the TIN block and by signing the form. This form then becomes an “awaiting-TIN” certificate, and the payee has 60 days to obtain a TIN and furnish it to you.

If no TIN is received from the payee within 60 days, begin backup withholding and continue until the TIN is provided. The 60-day exemption from backup withholding applies only to interest and dividend payments and certain payments made with respect to readily tradable instruments. Therefore, any other payment, such as nonemployee compensation, is subject to backup withholding even if the payee has applied for and is awaiting a TIN. .

ï‚· If a notice is received from the IRS that the payee’s TIN is incorrect, you may choose to withhold on any reportable payment made to the account(s) subject to backup withholding after receipt of the notice but you must begin backup withholding with any reportable payment made to the account more than 30 business days after the notice is received. Stop withholding within 30 days after you receive a certified Form W-9 (or other form that requires the payee to certify under penalty of perjury). The IRS will furnish a notice to the payer and the payer is required to promptly furnish a “B” notice or an acceptable substitute to the payee. ï‚· If an IRS notice is received that states that the payee is subject to backup withholding due to notified payee underreporting, you may choose to withhold on any reportable payment made to the account(s) subject to withholding after receipt of the notice, but you must withhold on any reportable payment made to the account more than 30 business days after you receive the notice. The payer must notify the payee when this procedure starts. The IRS will notify the payer in writing when the withholding can stop, or the payee may furnish a written certification from the IRS stating when the withholding will stop.

In most cases, the stop date will be January 1 of the year following the year of the notice. Report backup withholding on Form 945, Annual Return of Withheld Federal Income Tax. Also, report backup withholding and the amount of the payment on Forms W-2G, 1099-B, DIV, G, INT, MISC, OID, or PATR even if the amount of the payment is less than the amount for which an information return is normally required. Payments of withheld taxes must be deposited using EFTPS. Taxpayer Identification Number (TIN) Matching TIN Matching allows a payer to match TIN and name combinations with IRS records before submitting the forms to the IRS.

TIN Matching is one of the e-services products that is offered and is accessible through the IRS website. See Publication 2108-A, On-Line Taxpayer Identification (TIN) Matching Program, or go to the IRS.gov and enter keyword “TIN matching” in the upper right corner. Truncating Payee Identification Number Final regulations (REG-148873-09) permit filers of information returns in the Form 1098 series, Form 1099 series, and Form 5498 series to truncate an individual payee’s SSN, ITIN, or ATIN number on paper payee statements for the tax year 2015. Filers may truncate a payee’s identification number on the payee statement (including substitute and composite substitute statements) furnished to the payee in paper form or electronically.

Generally, the payee statement is that copy of an information return designated “Copy B” on the form. For some forms, the term “payee” will refer to beneficiary, borrower, debtor, insured, participant, payer, policyholder, recipient, shareholder, student, or transferor. If a filer truncates an identification number on Copy B, other copies of the form furnished to the payee may also include a truncated number. A filer may not truncate a payee’s identification number on any forms filed with the IRS or with state or local governments, on any payee statement furnished electronically, or on any payee statement not in the Form 1098, Form 1099, or Form 5498 series.

A filer’s identification number may not be truncated. A payee’s EIN may not be truncated. To truncate, replace the first 5 digits of the 9-digit number with asterisk (*) or Xs (for example, an SSN 123-45-6789 would appear on the paper payee statement as ***-**-6789 or XXX-XX-6789). . Electronic Filing If the payer files 250 or more returns of any individual Form 1099 type, it must file these returns electronically. The 250-or-more requirement applies separately to each type of form. For example, if you must file 500 Forms 1098 and 100 Forms 1099-A, you must file Forms 1098 electronically, but you are not required to file Forms 1099-A electronically. To receive a waiver from the required filing of information returns electronically, submit Form 8508, Request for Waiver From Filing Information Returns Electronically, at least 45 days before the due date of the returns.

You cannot apply for a waiver for more than 1 tax year at a time. If a waiver for original returns is approved, any corrections for the same types of returns will be covered under the waiver. 1099s may be filed electronically through the Filing Information Returns Electronically System (FIRE System); however you must have the software that can produce a file in the proper format according to Pub 1220.

The FIRE system does not provide a fill-in form option for information return reporting. You can access the FIRE system via the internet at http://FIRE.IRS.gov. Penalties for Noncompliance The penalties which can be imposed for failing to comply with the reporting and filing requirements associated with the Form 1099 Series, such as failing to file timely or electronically when required, failing to include all information required, or incorrect information included on the return has increased substantially. The amount of the penalty is based on when the correct information return is filed: ï‚· $30 per information return if correctly filed within 30 days; maximum penalty $250,000 per year ($75,000 for small businesses) ï‚· $60 per information return if correctly filed more than 30 days after the due date but by August 1st; maximum penalty $500,000 per year ($200,000 for small businesses) ï‚· $100 per information return if filed after August 1st or not filed at all; maximum penalty $1,500,000 per year ($500,000 for small businesses) A small business is defined as having average annual gross receipts for the three most recent tax years (or for the period of existence, if shorter) ending before the calendar year in which the information returns were due of $5 million or less. The following are exceptions to the failure to file penalty: ï‚· The penalty will not apply to any failure that was due to reasonable cause and not to willful neglect.

In general, one must be able to show that the failure was due to an event beyond control or due to significant mitigating factors. It must also be shown that the company acted in a responsible manner and steps were taken to avoid the failure. ï‚· An inconsequential error or omission is not considered a failure to include incorrect information. An inconsequential error or omission does not prevent or hinder the IRS from processing the return, from correlating the information required to be shown on the return with the information shown on the payee’s tax return, or from otherwise putting the return to its intended use. Errors and omissions that are never inconsequential are those related to (a) a TIN, (b) a payee’s surname, and (c) any money amount. .

ï‚· De minimus rule for corrections. If reasonable cause cannot be shown, the penalty for failure to file correct information returns will not apply to a certain number of returns if: a. The information returns were filed. b. Either all the information was not included or the incorrect information was included. c.

The corrections were filed by August 1st. If all of the conditions in a, b, and c above are met, the penalty for filing incorrect returns (but not for filing late) will not apply to the greater of 10 information returns or ½ of 1% of the total number of information returns that are required to file for the calendar year. Failure to provide correct payee/recipient statements by January 31 or February 16 (as required) without reasonable cause is subject to the same penalty provisions as those for late or failure to file noted earlier. Any failure to file or provide a correct information return that is due to intentional disregard of the filing or correct information requirements is penalized at a minimum of $250 per information return with no maximum penalty. Keeping Copies Generally, keep copies of information returns filed with the IRS or have the ability to reconstruct the data for at least 3 years, 4 years for Form 1099-C, from the due date of the returns. Keep copies of information returns 4 years if backup withholding was imposed. Special reporting requirements apply in many cases, the complete instructions for the proper completion and reporting of the following Forms 1099 can be found at www.irs.gov under the Forms and Publications tab. FORM 1096 - ANNUAL SUMMARY AND TRANSMITTAL Information return filers use Form 1096 to transmit paper Forms 1099, 1098, 3921, 3922, 5498, and W2G - to the IRS. Do not use the paper Form 1096 to transmit electronically.

For electronic submissions, see Pub. 1220, “Specifications for Filing Forms 1098, 1099, 3921, 3922, 5498, and W-2G Electronically”. When transmitting information returns to IRS, filers should use a separate Form 1096 for different groups of information returns - e.g., a separate 1096 for a group of Form 1099-MISC and another 1096 for a group of Form 1099-R. Form 1096 generally must be filed by the last day of February when used to transmit Forms 1098, 1099, 3921, 3922, and W-2G.

When used to transmit a Form 5498, 5498-ESA or 5498-SA the Form 1096 generally is due by May 31. . Do Not Staple Form 6969 1096 OMB No. 1545-0108 Annual Summary and Transmittal of U.S. Information Returns Department of the Treasury Internal Revenue Service 2013 FILER'S name Street address (including room or suite number) City or town, province or state, country, and ZIP or foreign postal code For Official Use Only Name of person to contact Telephone number Email address Fax number 1 Employer identification number 2 Social security number 3 Total number of forms 4 Federal income tax withheld 5 Total amount reported with this Form 1096 $ 6 Enter an “X” in only one box below to indicate the type of form being filed. W-2G 32 1097-BTC 50 1098 81 1098-C 78 1098-E 84 1098-T 83 1099-A 80 1099-B 79 1099PATR 97 1099-Q 31 1099-R 98 1099-S 75 1099-SA 94 3921 25 3922 26 5498 28 $ 7 If this is your final return, enter an “X” here 1099-C 1099-CAP 1099-DIV 85 73 91 1099-G 86 1099-H 71 1099-INT 92 . . 1099-K 1099-LTC 10 93 . . 1099MISC 95 . 1099-OID 96 5498-ESA 5498-SA 72 27 Return this entire page to the Internal Revenue Service. Photocopies are not acceptable. Under penalties of perjury, I declare that I have examined this return and accompanying documents, and, to the best of my knowledge and belief, they are true, correct, and complete. Signature Instructions Future developments.

For the latest information about developments related to Form 1096, such as legislation enacted after they were published, go to www.irs.gov/form1096. Reminder. The only acceptable method of filing information returns with Internal Revenue Service/Information Returns Branch is electronically through the FIRE system. See Pub.

1220, Specifications for Filing Forms 1097, 1098, 1099, 3921, 3922, 5498, 8935, and W-2G Electronically. Purpose of form. Use this form to transmit paper Forms 1097, 1098, 1099, 3921, 3922, 5498, and W-2G to the Internal Revenue Service. Do not use Form 1096 to transmit electronically. For electronic submissions, see Pub.

1220. Caution. If you are required to file 250 or more information returns of any one type, you must file electronically. If you are required to file electronically but fail to do so, and you do not have an approved waiver, you may be subject to a penalty.

For more information, see part F in the 2013 General Instructions for Certain Information Returns. Who must file. The name, address, and TIN of the filer on this form must be the same as those you enter in the upper left area of Forms 1097, 1098, 1099, 3921, 3922, 5498, or W-2G. A filer is any person or entity who files any of the forms shown in line 6 above. Enter the filer’s name, address (including room, suite, or other unit number), and TIN in the spaces provided on the form. Title Date When to file.

File Form 1096 as follows. • With Forms 1097, 1098, 1099, 3921, 3922, or W-2G, file by February 28, 2014. • With Forms 5498, file by June 2, 2014. Where To File Send all information returns filed on paper with Form 1096 to the following: If your principal business, office Use the following or agency, or legal residence in three-line address the case of an individual, is located in Alabama, Arizona, Arkansas, Connecticut, Delaware, Florida, Georgia, Kentucky, Louisiana, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, Texas, Vermont, Virginia, West Virginia For more information and the Privacy Act and Paperwork Reduction Act Notice, see the 2013 General Instructions for Certain Information Returns. Department of the Treasury Internal Revenue Service Center Austin, TX 73301 Cat. No. 14400O Form 1096 (2013) .

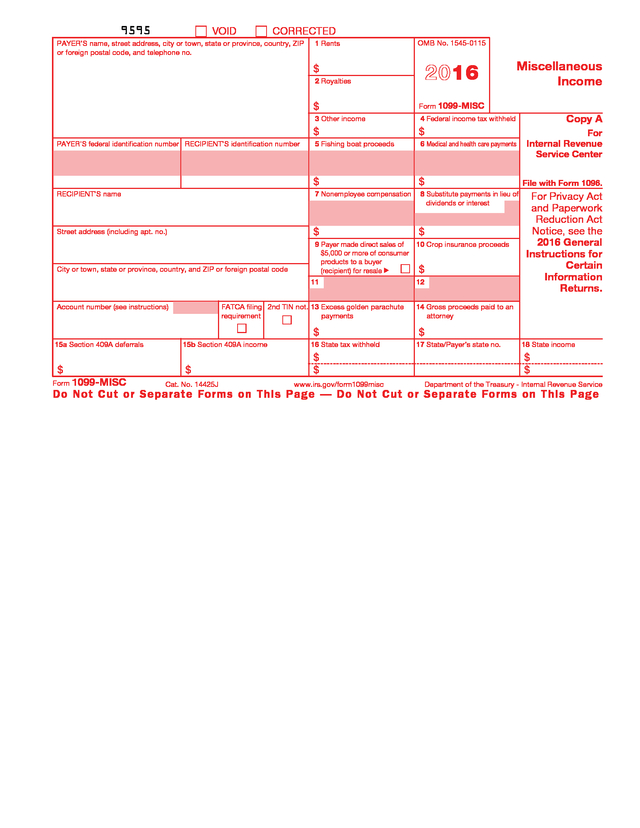

FORM 1099-MISC Form 1099-MISC, “Miscellaneous Income," must be filed by a business for certain payments made to nonemployees in the course of trade or business. Personal payments are not reportable. A trade or business is any entity that operates for gain or profit. However, non-profit organizations are also subject to these reporting requirements.

Organizations also subject to these reporting requirements include trusts of qualified pension or profit-sharing plans of employers, certain organizations exempt from tax under section 501(c) or (d), farmers’ cooperatives that are exempt from tax under section 521, and widely held fixed investment trusts. Payments made by federal, state, or local governments are also reportable. Form 1099-Misc is required for each person to whom payments have been made during the year: ï‚· $10 or more in royalties or broker payments in lieu of dividends or tax–exempt interest; ï‚· $600 or more in rents, services (including parts and materials), prizes and awards, other income payments, medical and health care payments, crop insurance proceeds, cash payments for fish you purchase from anyone engaged in the trade or business of catching fish, or generally, the cash paid from notional principal contract to an individual, partnership, or estate; ï‚· Any fish boat proceeds; ï‚· Gross proceeds to an attorney; ï‚· In addition, use Form 1099-Misc to report direct sales of at least $5000 of consumer products to a buyer for resale anywhere other than a permanent retail establishment; or ï‚· Any backup withholding regardless of the amount of payment. Examples of payments for which Forms 1099 are not required: ï‚· Generally payments to a corporation;* ï‚· Payments for merchandise, telegrams, telephone, freight, storage and similar items; ï‚· Payments of rent to real estate agents; ï‚· Wages paid to employees (report on Form W-2); ï‚· Military differential wage payments made to employees while they are on active duty in the Armed forces or other uniformed services (report on W-2); ï‚· Business travel allowances paid to employee (may be reportable on W-2); ï‚· Cost of current life insurance protection (report on Form W-2 or Form 1099-R, Distributions from Pensions, Annuities, Retirement, or Profit-Sharing plans, IRAs, Insurance Contracts, etc.); ï‚· Payments to a tax-exempt organization including tax-exempt trusts (IRAs, HSAs, Archer MSAs, and Coverdell ESAs), the United States, a state, the District of Columbia, a U.S. possession, or a foreign government; and ï‚· Payments made to or for homeowners from the HFA Hardest Hit Fund or the Emergency Homeowners’ Loan Program or similar state program. ï‚· Payments made with a credit card or payment card and certain other types of payments, including third party network transactions, must be reported on Form 1099-K by the payment settlement entity under section 6050W and are not subject to reporting on Form 1099-Misc. ï‚· A payment to an informer as an award, fee, or reward for information about criminal activity is not required to be reported if the payment is made by a federal, state, or local government agency, or by a nonprofit organization exempt from tax under section 501(c)(3) that makes the payment to further the charitable purpose of lessening the burdens of government. ï‚· Do not use Form 1099-MISC to report scholarship or fellowship grants.

Scholarship or fellowship grants that are taxable to the recipient because they are paid for teaching, research, or other services as a condition for receiving the grant are considered wages and must be reported on Form W-2. Other taxable scholarships or fellowship payments (to a degree or nondegree candidate) are not required to be reported to the IRS on any form. . ï‚· ï‚· Difficulty-of-care payments that are excludable from the recipient’s gross income are not required to be reported. Difficulty-of-care payments to foster care providers are not reportable if paid for not more than 11 children under age 19 and not more than six individuals age 19 or older. Amounts paid for more than 10 children or more than five other individuals are reportable on Form 1099-MISC. A canceled debt is not reportable on Form 1099-MISC. Canceled debts are required to be reported on Form 1099-C. *Reportable payments to corporations include medical and health payments reported in box 6, fish purchases for cash reported in box 7, attorneys’ fees reported in box 7, gross proceeds paid to an attorney reported in box 14, substitute payments in lieu of dividends or tax exempt interest reported in box 8, and payments by a federal executive agency for services reported in box 7. Rents-Box 1 Form 1099-MISC must be filed for each person to whom a taxpayer has paid at least $600 in rents. For these purposes, rents include real estate rentals paid for office space (unless paid to a real estate agent) and machine rentals (for example, renting a bulldozer to level your parking lot), and pasture rentals.

Note that if a rental fee for a machine is included in a contract that covers both the use of the machine and the operator, the contract fee rental should be prorated between the rent of the machine, reporting in box 1 and the operator's charge (reported as nonemployee compensation) in box 7. Public housing agencies must report in box 1 rental assistance payments made to owners of housing projects. See Rev. Rul.

88-53, 1988-1 C.B. 384. Coin-operated amusements: If an arrangement between an owner of coin-operated amusements and an owner of a business establishment where the amusements are placed is a lease of the amusements or the amusement space, the owner of the amusements or the owner of the space, whoever makes the payments, must report the lease payments in box 1 of Form 1099-MISC if the payments total at least $600. However, if the arrangement is a joint venture, the joint venture must file a Form 1065, U.S. Return or Partnership Income, and provide each partner with the information necessary to report the partner’s share of the taxable income.

Coin-operated amusements include video games, pinball machines, jukeboxes, pool tables, slot machines, and other machines and gaming devices operated by coins or tokens inserted into the machines by individual users. For more information, see Rev. Rul.

92-49, 1992-1 C.B. 433. Royalties-Box 2 If a taxpayer made royalty payments during the calendar year of at least $10 or more before reduction for severance and other taxes that may have been withheld and paid, it must file Form 1099-MISC. Royalty payments that must be reported include royalty payments for oil, gas, coal, timber, sand, gravel and other mineral interests.

Also include payments for intangible property such as patents, copyrights, trade names, trademarks, franchises, books and other literary compositions, musical compositions, artistic works, secret processes and formulas. Report gross royalties (before reduction for fees, commissions, or expenses) paid by a publisher directly to an author or literary agent in box 2 unless the agent is a corporation. The literary agent (whether or not a corporation) that received the royalty payment on behalf of the author must report the gross amount of royalty payments to the author on Form 1099-MISC whether or not the publisher reported the payment to the agent on its Form 1099-MISC. Payments for surface royalties should be reported in box 1. Oil or gas payments for a working interest should be reported in box 7.

Do not report timber royalties made under a pay-as-cut contract; report these timber royalties on Form 1099-S, Proceeds From Real Estate Transactions. . Other Income-Box 3 Enter other income of $600 or more to be reported on Form 1099-MISC that is not reportable in one of the other boxes on the form. Prizes and awards of $600 or more that are not for services rendered are reported on Form 1099-MISC box 3. Include the FMV (fair market value) of merchandise won on game shows. Also include amounts paid to a winner of a sweepstakes not involving a wager.

If a wager is made, report the winnings on Form W-2G, Certain Gambling Winnings. Prizes and awards granted in recognition of past accomplishments in religious, charitable, scientific, artistic, educational, literary, or civic fields are not reported on Form 1099-MISC if: (1) the winners are chosen without action on their part, and (2) the winners are not expected to perform future services, and (3) the payer transfers the prize or award to a charitable organization or governmental unit pursuant to a designation made by the recipient. Do not include prizes and awards paid to your employees. Report these on Form W-2.

Prizes and awards for services performed by nonemployees, such as an award for the top commission salesperson should be reported in box 7. Other items required to be reported in box 3 include the following: ï‚· Generally, all punitive damages, any damages for nonphysical injuries or sickness, and any other taxable damages. Report punitive damages even if they relate to physical injury or physical sickness. Generally, report all compensatory damages for nonphysical injuries or sickness, such as employment discrimination or defamation.

However, do not report damages (other than punitive damages): o Received on account of personal physical injuries or physical sickness; o That do not exceed the amount paid for medical care for emotional distress; o Received on account of nonphysical injuries (for example, emotional distress) under a written binding agreement, court decree, or mediation award in effect on or issued by September 13, 1995; or o That are for replacement of capital, such as damages paid to a buyer by a contractor who failed to complete construction of a building. Damages received on account of emotional distress, including physical symptoms such as insomnia, headaches, and stomach disorders, are not considered received for a physical injury or physical sickness and are reportable unless described above. However, damages received on account of emotional distress due to physical injuries or physical sickness are not reportable. ï‚· ï‚· Payments for deceased employee wages. (See W-2 section) Termination payments to former self-employed insurance salespeople.

These payments are not subject to self-employment tax and are reportable in box 3 (rather than box 7) if all the following apply: o The payments are received from an insurance company because of services performed as an insurance salesperson for the company. o The payments are received after termination of the salesperson’s agreement to perform services for the company. o The salesperson did not perform any services for the company after termination and before the end of the year. o The salesperson enters into a covenant not to compete against the company for at least 1 year after the date of termination. o The amount of the payments depends primarily on policies sold by the salesperson or credited to the salesperson’s account during the last year of the service agreement or to the extent those policies remain in force for some period after termination, or both. o The amount of the payments does not depend at all on length of service or overall earnings from the company (regardless of whether eligibility for payment depends on length of service). . ï‚· ï‚· If the termination payments do not meet all these requirements, report them in box 7. A payment or series of payments made to individuals for participating in a medical research study or studies. Payments for H-2A visa agricultural workers who did not give you a valid taxpayer identification number. You must also withhold federal income tax under the backup withholding rules Federal Income Tax-Box 4 Withholding for federal income taxes ordinarily is not required for payments to independent contractors. However, if at least $600 of "reportable payments" is made within a calendar year to an independent contractor or other nonemployee, and that individual fails to provide a correct taxpayer identification number before payment is made, the payer is required to withhold federal income taxes under the backup withholding rules. A flat 28 % of the payment must be withheld. Payers that withhold federal income taxes on miscellaneous income under the backup withholding rules must file Form 1099-MISC to report such amounts.

Backup withholding must be paid by EFTPS. Fishing Boat Proceeds- Box 5 Enter the individual’s share of all proceeds from the sale of catch or the FMV of a distribution in kind to each crew member of fishing boats with normally fewer than 10 crew members, or payments of up to $100 per trip that are contingent on a minimum catch and are paid solely for additional duties. Medical and Health Care Payments-Box 6 Enter payments of $600 or more made in the course of your trade or business to each physician or other supplier or provider of medical or health care services in box 6. Include payments made by medical or health care insurers under health, accident, and sickness insurance programs. If payment is made to a corporation, list the corporation as the recipient rather than the individual providing the services. Payments to persons providing health care services often include charges for injections, drugs, dentures, and similar items.

In these cases the entire payment is subject to information reporting. Payments to pharmacies for prescription drugs are not required to be reported. The exemption from issuing Form 1099-MISC to a corporation does not apply to payments for medical or health care services provided by corporations, including professional corporations. However, it is not required to report payments made to a tax-exempt hospital or extended care facility or to a United States (or its possessions), a state, the District of Columbia, or any of their political subdivisions, agencies, or instrumentalities. Generally, payments made under a flexible spending arrangement or a health reimbursement arrangement which is treated as employer-provided coverage under an accident or health plan for purposes of section 106 are exempt from the reporting requirements of section 6041. Nonemployee Compensation-Box 7 The types of nonemployee compensation that must be reported on Form 1099-MISC, box 7 include fees, commissions, prizes and awards for services performed by a nonemployee, other forms of compensation for services performed for a trade or business by an individual who is not an employee, and fish purchases for cash.

Include oil and gas payments for a working interest, whether or not services are performed. Also include expenses incurred for the use of an entertainment facility that you treat as compensation to a nonemployee. Federal executive agencies that make payments to vendors for services, including payments to corporations, must report the payments in this box. .