Description

January 2016

Enclosed for your convenience are the following items:

Exhibit 1 Guide to Information Returns

Exhibit 1(a) Supplemental Information

Exhibit 2 Payments to Outside Providers or Contractors for Business Purposes

Exhibit 3 Nontaxable Benefits Provided to Employees

Exhibit 4 Payments to Directors

Exhibit 5 Employee Business Expenses and Expense Accounts

Exhibit 6 Record-Keeping for Travel, Entertainment and Meals Expense

Exhibit 7 Record-Keeping and Deductions for Business Vehicles

Exhibit 8 Travel Per Diem Rates for Certain States

Exhibit 9 Reporting Cash Payments Over $10,000

Exhibit 10 Electronic Filing Requirements for Payroll and Information Returns When Over 250 Documents

Exhibit 11 Instructions for Filing Payroll and Information Returns (Paper Filings)

Exhibit 12 Dues Paid to Social Associations and Clubs or for Lobbying Activities

Exhibit 13 Energy Subsidy Payments

Exhibit 14 Taxation and Reporting of Capital Credits From Electric and Telephone Cooperatives

Exhibit 15 Form 1099-A Foreclosures and Abandonment of Security

Exhibit 16 Form 1099-C Cancellation of Debt

Exhibit 17 Form 1098-E Student Loan Interest Reporting & Form 1098-T Regarding Tuition Reporting

Exhibit 18 Public Inspection of Tax Exempt Organizations Filings, Forms 990, 990-T, 1023, etc. and IRS Sanctions

Regarding Transactions with Certain Persons (Insiders)

Exhibit 19 Credit Card Sales

Exhibit 20 Proceeds From Broker and Barter Exchange Transactions

Exhibit 21 Health Care Value Reporting

Exhibit 22 Health Care Coverage Reporting

We recommend you review the specific areas related to your business each year as rules change from year to year.

The 2016 vehicle standard business mileage rate was decreased to 54 cents per mile. The 2015 vehicle standard

business mileage rate was 57.5 cents per mile.

For most Forms 1099, detailed on the following pages, a telephone number for recipient inquiries must be provided.

If you have any questions concerning the enclosures, please feel free to contact us.

Sincerely,

EIDE BAILLY LLP

1

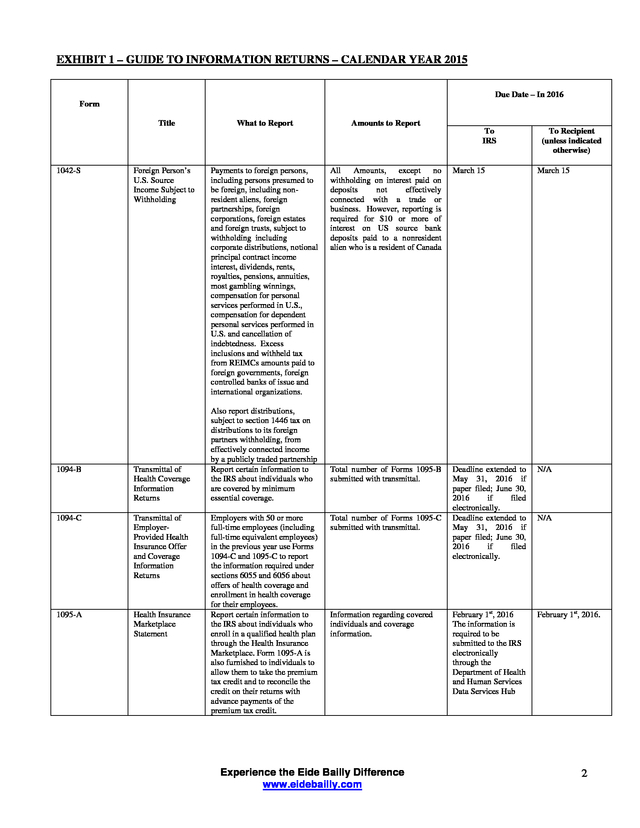

. EXHIBIT 1 – GUIDE TO INFORMATION RETURNS – CALENDAR YEAR 2015

Due Date – In 2016

Form

Title

What to Report

Amounts to Report

To

IRS

1042-S

Foreign Person’s

U.S. Source

Income Subject to

Withholding

1094-B

Transmittal of

Health Coverage

Information

Returns

1094-C

Transmittal of

EmployerProvided Health

Insurance Offer

and Coverage

Information

Returns

1095-A

Health Insurance

Marketplace

Statement

Payments to foreign persons,

including persons presumed to

be foreign, including nonresident aliens, foreign

partnerships, foreign

corporations, foreign estates

and foreign trusts, subject to

withholding including

corporate distributions, notional

principal contract income

interest, dividends, rents,

royalties, pensions, annuities,

most gambling winnings,

compensation for personal

services performed in U.S.,

compensation for dependent

personal services performed in

U.S. and cancellation of

indebtedness. Excess

inclusions and withheld tax

from REIMCs amounts paid to

foreign governments, foreign

controlled banks of issue and

international organizations.

Also report distributions,

subject to section 1446 tax on

distributions to its foreign

partners withholding, from

effectively connected income

by a publicly traded partnership

Report certain information to

the IRS about individuals who

are covered by minimum

essential coverage.

Employers with 50 or more

full-time employees (including

full-time equivalent employees)

in the previous year use Forms

1094-C and 1095-C to report

the information required under

sections 6055 and 6056 about

offers of health coverage and

enrollment in health coverage

for their employees.

Report certain information to

the IRS about individuals who

enroll in a qualified health plan

through the Health Insurance

Marketplace.

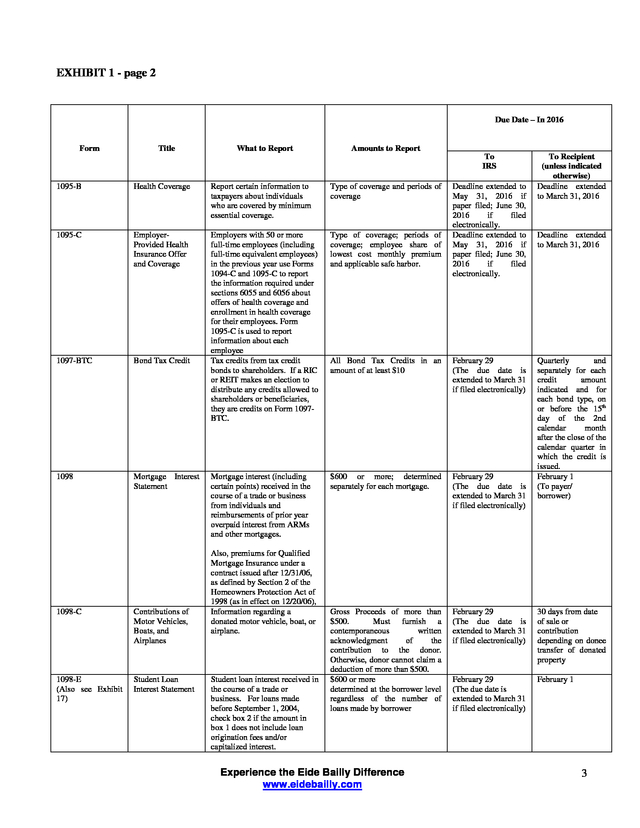

Form 1095-A is also furnished to individuals to allow them to take the premium tax credit and to reconcile the credit on their returns with advance payments of the premium tax credit. To Recipient (unless indicated otherwise) All Amounts, except no withholding on interest paid on deposits not effectively connected with a trade or business. However, reporting is required for $10 or more of interest on US source bank deposits paid to a nonresident alien who is a resident of Canada March 15 March 15 Total number of Forms 1095-B submitted with transmittal. Deadline extended to May 31, 2016 if paper filed; June 30, 2016 if filed electronically. Deadline extended to May 31, 2016 if paper filed; June 30, 2016 if filed electronically. N/A February 1st, 2016 The information is required to be submitted to the IRS electronically through the Department of Health and Human Services Data Services Hub February 1st, 2016. Total number of Forms 1095-C submitted with transmittal. Information regarding covered individuals and coverage information. Experience the Eide Bailly Difference www.eidebailly.com N/A 2 . EXHIBIT 1 - page 2 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 1095-B Health Coverage Report certain information to taxpayers about individuals who are covered by minimum essential coverage. Type of coverage and periods of coverage 1095-C EmployerProvided Health Insurance Offer and Coverage Type of coverage; periods of coverage; employee share of lowest cost monthly premium and applicable safe harbor. 1097-BTC Bond Tax Credit Employers with 50 or more full-time employees (including full-time equivalent employees) in the previous year use Forms 1094-C and 1095-C to report the information required under sections 6055 and 6056 about offers of health coverage and enrollment in health coverage for their employees. Form 1095-C is used to report information about each employee Tax credits from tax credit bonds to shareholders. If a RIC or REIT makes an election to distribute any credits allowed to shareholders or beneficiaries, they are credits on Form 1097BTC. All Bond Tax Credits in an amount of at least $10 February 29 (The due date is extended to March 31 if filed electronically) 1098 Mortgage Interest Statement Mortgage interest (including certain points) received in the course of a trade or business from individuals and reimbursements of prior year overpaid interest from ARMs and other mortgages. $600 or more; determined separately for each mortgage. February 29 (The due date is extended to March 31 if filed electronically) Gross Proceeds of more than $500. Must furnish a contemporaneous written acknowledgment of the contribution to the donor. Otherwise, donor cannot claim a deduction of more than $500. $600 or more determined at the borrower level regardless of the number of loans made by borrower February 29 (The due date is extended to March 31 if filed electronically) 30 days from date of sale or contribution depending on donee transfer of donated property February 29 (The due date is extended to March 31 if filed electronically) February 1 1098-C Contributions of Motor Vehicles, Boats, and Airplanes 1098-E (Also see Exhibit 17) Student Loan Interest Statement Also, premiums for Qualified Mortgage Insurance under a contract issued after 12/31/06, as defined by Section 2 of the Homeowners Protection Act of 1998 (as in effect on 12/20/06), Information regarding a donated motor vehicle, boat, or airplane. Student loan interest received in the course of a trade or business. For loans made before September 1, 2004, check box 2 if the amount in box 1 does not include loan origination fees and/or capitalized interest. Experience the Eide Bailly Difference www.eidebailly.com Deadline extended to May 31, 2016 if paper filed; June 30, 2016 if filed electronically. Deadline extended to May 31, 2016 if paper filed; June 30, 2016 if filed electronically. To Recipient (unless indicated otherwise) Deadline extended to March 31, 2016 Deadline extended to March 31, 2016 Quarterly and separately for each credit amount indicated and for each bond type, on or before the 15th day of the 2nd calendar month after the close of the calendar quarter in which the credit is issued. February 1 (To payer/ borrower) 3 .

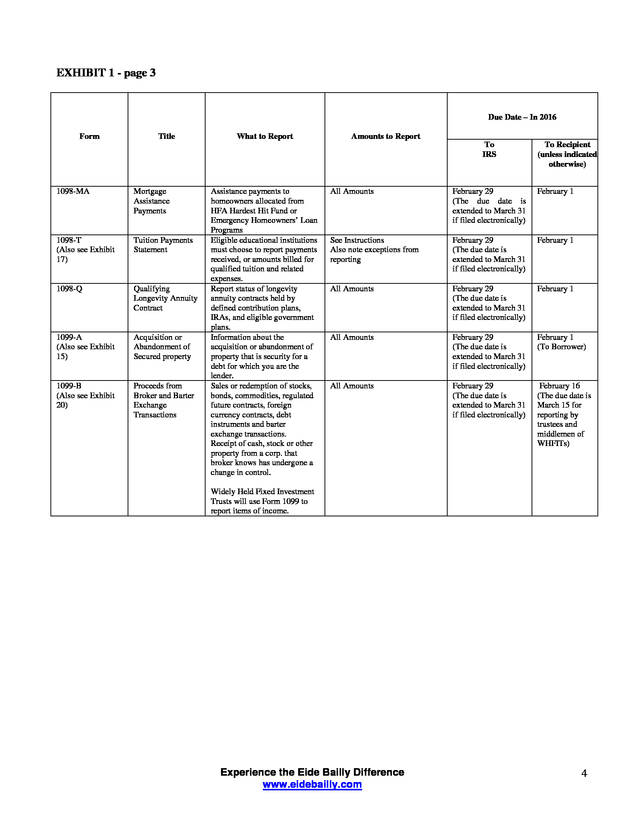

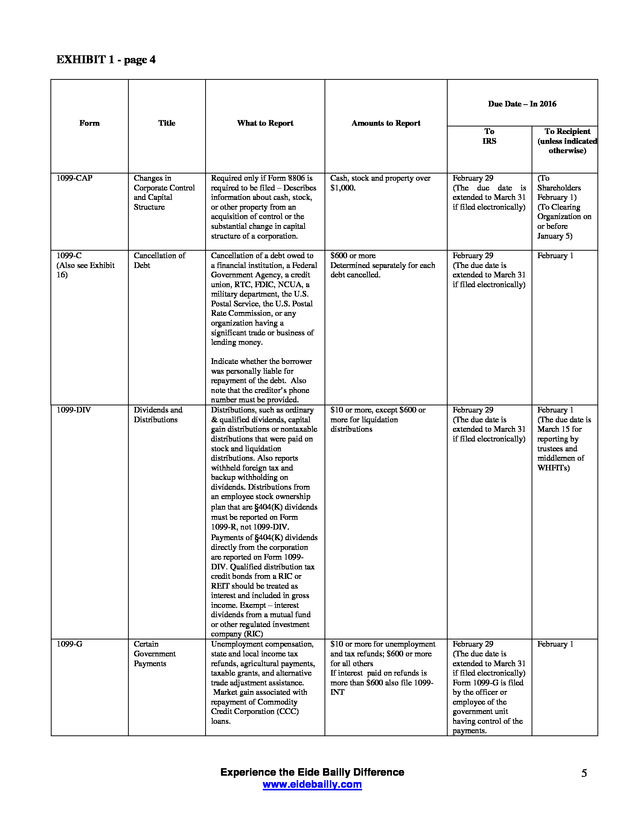

EXHIBIT 1 - page 3 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 1098-MA Mortgage Assistance Payments 1098-T (Also see Exhibit 17) Tuition Payments Statement 1098-Q Qualifying Longevity Annuity Contract 1099-A (Also see Exhibit 15) Acquisition or Abandonment of Secured property 1099-B (Also see Exhibit 20) Proceeds from Broker and Barter Exchange Transactions Assistance payments to homeowners allocated from HFA Hardest Hit Fund or Emergency Homeowners’ Loan Programs Eligible educational institutions must choose to report payments received, or amounts billed for qualified tuition and related expenses. Report status of longevity annuity contracts held by defined contribution plans, IRAs, and eligible government plans. Information about the acquisition or abandonment of property that is security for a debt for which you are the lender. Sales or redemption of stocks, bonds, commodities, regulated future contracts, foreign currency contracts, debt instruments and barter exchange transactions. Receipt of cash, stock or other property from a corp. that broker knows has undergone a change in control. To Recipient (unless indicated otherwise) All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 1 See Instructions Also note exceptions from reporting February 29 (The due date is extended to March 31 if filed electronically) February 1 All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 1 All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 1 (To Borrower) All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 16 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) Widely Held Fixed Investment Trusts will use Form 1099 to report items of income. Experience the Eide Bailly Difference www.eidebailly.com 4 . EXHIBIT 1 - page 4 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS To Recipient (unless indicated otherwise) 1099-CAP Changes in Corporate Control and Capital Structure Required only if Form 8806 is required to be filed – Describes information about cash, stock, or other property from an acquisition of control or the substantial change in capital structure of a corporation. Cash, stock and property over $1,000. February 29 (The due date is extended to March 31 if filed electronically) (To Shareholders February 1) (To Clearing Organization on or before January 5) 1099-C (Also see Exhibit 16) Cancellation of Debt Cancellation of a debt owed to a financial institution, a Federal Government Agency, a credit union, RTC, FDIC, NCUA, a military department, the U.S. Postal Service, the U.S. Postal Rate Commission, or any organization having a significant trade or business of lending money. $600 or more Determined separately for each debt cancelled. February 29 (The due date is extended to March 31 if filed electronically) February 1 $10 or more, except $600 or more for liquidation distributions February 29 (The due date is extended to March 31 if filed electronically) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) $10 or more for unemployment and tax refunds; $600 or more for all others If interest paid on refunds is more than $600 also file 1099INT February 29 (The due date is extended to March 31 if filed electronically) Form 1099-G is filed by the officer or employee of the government unit having control of the payments. February 1 1099-DIV Dividends and Distributions 1099-G Certain Government Payments Indicate whether the borrower was personally liable for repayment of the debt. Also note that the creditor’s phone number must be provided. Distributions, such as ordinary & qualified dividends, capital gain distributions or nontaxable distributions that were paid on stock and liquidation distributions. Also reports withheld foreign tax and backup withholding on dividends.

Distributions from an employee stock ownership plan that are §404(K) dividends must be reported on Form 1099-R, not 1099-DIV. Payments of §404(K) dividends directly from the corporation are reported on Form 1099DIV. Qualified distribution tax credit bonds from a RIC or REIT should be treated as interest and included in gross income. Exempt – interest dividends from a mutual fund or other regulated investment company (RIC) Unemployment compensation, state and local income tax refunds, agricultural payments, taxable grants, and alternative trade adjustment assistance. Market gain associated with repayment of Commodity Credit Corporation (CCC) loans. Experience the Eide Bailly Difference www.eidebailly.com 5 .

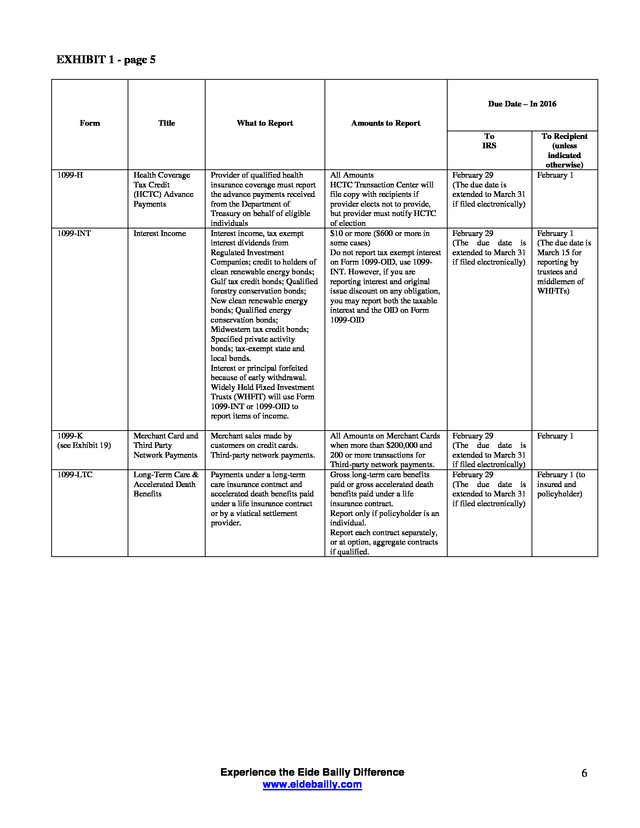

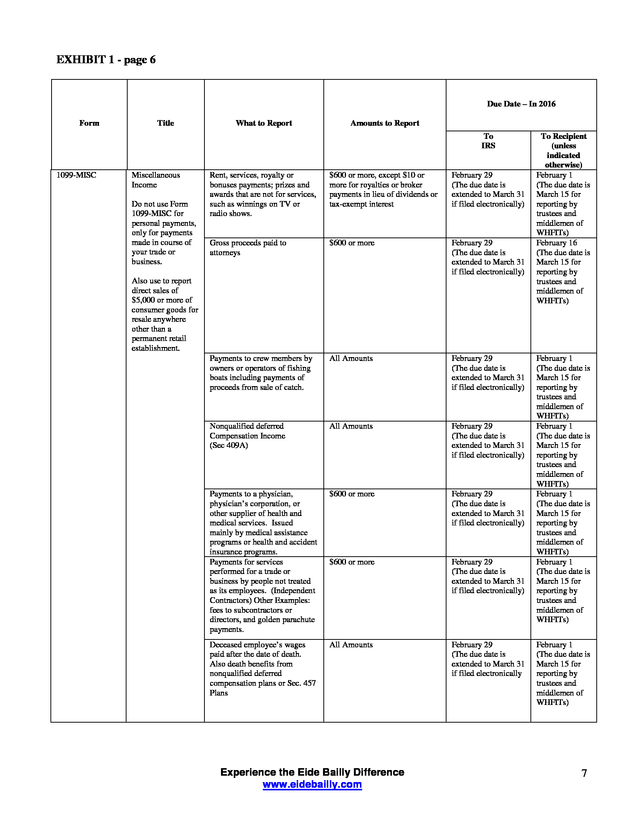

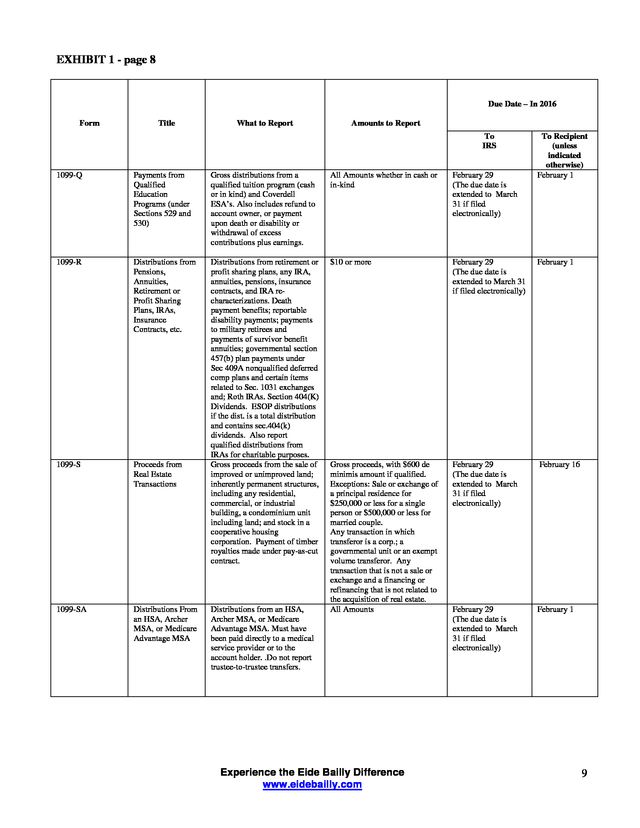

EXHIBIT 1 - page 5 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 1099-H Health Coverage Tax Credit (HCTC) Advance Payments 1099-INT Interest Income 1099-K (see Exhibit 19) 1099-LTC To Recipient (unless indicated otherwise) February 1 Provider of qualified health insurance coverage must report the advance payments received from the Department of Treasury on behalf of eligible individuals Interest income, tax exempt interest dividends from Regulated Investment Companies; credit to holders of clean renewable energy bonds; Gulf tax credit bonds; Qualified forestry conservation bonds; New clean renewable energy bonds; Qualified energy conservation bonds; Midwestern tax credit bonds; Specified private activity bonds; tax-exempt state and local bonds. Interest or principal forfeited because of early withdrawal. Widely Held Fixed Investment Trusts (WHFIT) will use Form 1099-INT or 1099-OID to report items of income. All Amounts HCTC Transaction Center will file copy with recipients if provider elects not to provide, but provider must notify HCTC of election $10 or more ($600 or more in some cases) Do not report tax exempt interest on Form 1099-OID, use 1099INT. However, if you are reporting interest and original issue discount on any obligation, you may report both the taxable interest and the OID on Form 1099-OID February 29 (The due date is extended to March 31 if filed electronically) February 29 (The due date is extended to March 31 if filed electronically) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) Merchant Card and Third Party Network Payments Merchant sales made by customers on credit cards. Third-party network payments. Payments under a long-term care insurance contract and accelerated death benefits paid under a life insurance contract or by a viatical settlement provider. February 29 (The due date is extended to March 31 if filed electronically) February 29 (The due date is extended to March 31 if filed electronically) February 1 Long-Term Care & Accelerated Death Benefits All Amounts on Merchant Cards when more than $200,000 and 200 or more transactions for Third-party network payments. Gross long-term care benefits paid or gross accelerated death benefits paid under a life insurance contract. Report only if policyholder is an individual. Report each contract separately, or at option, aggregate contracts if qualified. Experience the Eide Bailly Difference www.eidebailly.com February 1 (to insured and policyholder) 6 . EXHIBIT 1 - page 6 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 1099-MISC Miscellaneous Income Do not use Form 1099-MISC for personal payments, only for payments made in course of your trade or business. Rent, services, royalty or bonuses payments; prizes and awards that are not for services, such as winnings on TV or radio shows. $600 or more, except $10 or more for royalties or broker payments in lieu of dividends or tax-exempt interest February 29 (The due date is extended to March 31 if filed electronically) Gross proceeds paid to attorneys $600 or more February 29 (The due date is extended to March 31 if filed electronically) Payments to crew members by owners or operators of fishing boats including payments of proceeds from sale of catch. All Amounts February 29 (The due date is extended to March 31 if filed electronically) Nonqualified deferred Compensation Income (Sec 409A) All Amounts February 29 (The due date is extended to March 31 if filed electronically) Payments to a physician, physician’s corporation, or other supplier of health and medical services. Issued mainly by medical assistance programs or health and accident insurance programs. Payments for services performed for a trade or business by people not treated as its employees. (Independent Contractors) Other Examples: fees to subcontractors or directors, and golden parachute payments. $600 or more February 29 (The due date is extended to March 31 if filed electronically) $600 or more February 29 (The due date is extended to March 31 if filed electronically) Deceased employee’s wages paid after the date of death. Also death benefits from nonqualified deferred compensation plans or Sec. 457 Plans All Amounts February 29 (The due date is extended to March 31 if filed electronically Also use to report direct sales of $5,000 or more of consumer goods for resale anywhere other than a permanent retail establishment. Experience the Eide Bailly Difference www.eidebailly.com To Recipient (unless indicated otherwise) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 16 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) 7 .

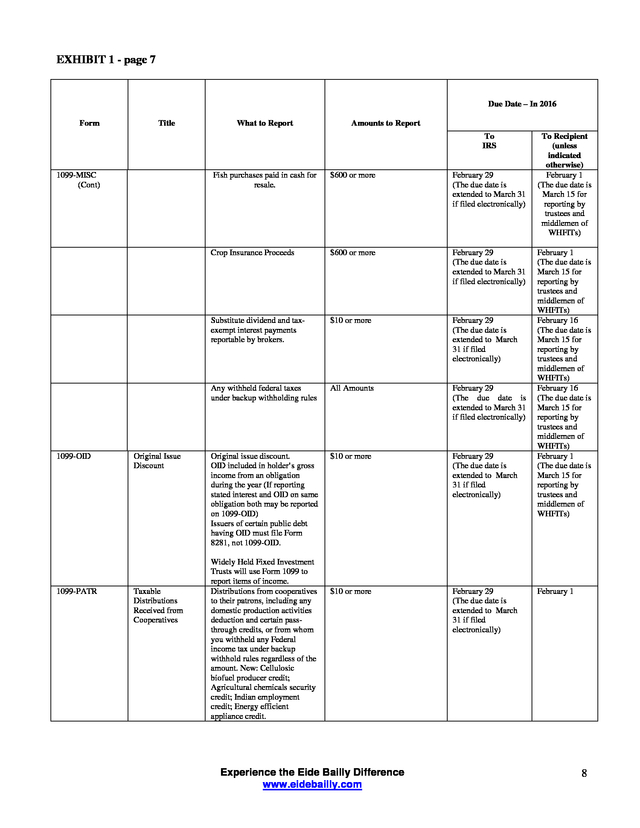

EXHIBIT 1 - page 7 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 1099-MISC (Cont) Taxable Distributions Received from Cooperatives $600 or more February 29 (The due date is extended to March 31 if filed electronically) $10 or more February 29 (The due date is extended to March 31 if filed electronically) Any withheld federal taxes under backup withholding rules 1099-PATR February 29 (The due date is extended to March 31 if filed electronically) Substitute dividend and taxexempt interest payments reportable by brokers. Original Issue Discount $600 or more Crop Insurance Proceeds 1099-OID Fish purchases paid in cash for resale. All Amounts February 29 (The due date is extended to March 31 if filed electronically) Original issue discount. OID included in holder’s gross income from an obligation during the year (If reporting stated interest and OID on same obligation both may be reported on 1099-OID) Issuers of certain public debt having OID must file Form 8281, not 1099-OID. $10 or more February 29 (The due date is extended to March 31 if filed electronically) $10 or more February 29 (The due date is extended to March 31 if filed electronically) Widely Held Fixed Investment Trusts will use Form 1099 to report items of income. Distributions from cooperatives to their patrons, including any domestic production activities deduction and certain passthrough credits, or from whom you withheld any Federal income tax under backup withhold rules regardless of the amount. New: Cellulosic biofuel producer credit; Agricultural chemicals security credit; Indian employment credit; Energy efficient appliance credit. Experience the Eide Bailly Difference www.eidebailly.com To Recipient (unless indicated otherwise) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 16 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 16 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 (The due date is March 15 for reporting by trustees and middlemen of WHFITs) February 1 8 . EXHIBIT 1 - page 8 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS To Recipient (unless indicated otherwise) February 1 1099-Q Payments from Qualified Education Programs (under Sections 529 and 530) Gross distributions from a qualified tuition program (cash or in kind) and Coverdell ESA’s. Also includes refund to account owner, or payment upon death or disability or withdrawal of excess contributions plus earnings. All Amounts whether in cash or in-kind February 29 (The due date is extended to March 31 if filed electronically) 1099-R Distributions from Pensions, Annuities, Retirement or Profit Sharing Plans, IRAs, Insurance Contracts, etc. $10 or more February 29 (The due date is extended to March 31 if filed electronically) February 1 1099-S Proceeds from Real Estate Transactions Distributions from retirement or profit sharing plans, any IRA, annuities, pensions, insurance contracts, and IRA recharacterizations. Death payment benefits; reportable disability payments; payments to military retirees and payments of survivor benefit annuities; governmental section 457(b) plan payments under Sec 409A nonqualified deferred comp plans and certain items related to Sec. 1031 exchanges and; Roth IRAs.

Section 404(K) Dividends. ESOP distributions if the dist. is a total distribution and contains sec.404(k) dividends.

Also report qualified distributions from IRAs for charitable purposes. Gross proceeds from the sale of improved or unimproved land; inherently permanent structures, including any residential, commercial, or industrial building, a condominium unit including land; and stock in a cooperative housing corporation. Payment of timber royalties made under pay-as-cut contract. February 29 (The due date is extended to March 31 if filed electronically) February 16 1099-SA Distributions From an HSA, Archer MSA, or Medicare Advantage MSA Gross proceeds, with $600 de minimis amount if qualified. Exceptions: Sale or exchange of a principal residence for $250,000 or less for a single person or $500,000 or less for married couple. Any transaction in which transferor is a corp.; a governmental unit or an exempt volume transferor. Any transaction that is not a sale or exchange and a financing or refinancing that is not related to the acquisition of real estate. All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 1 Distributions from an HSA, Archer MSA, or Medicare Advantage MSA.

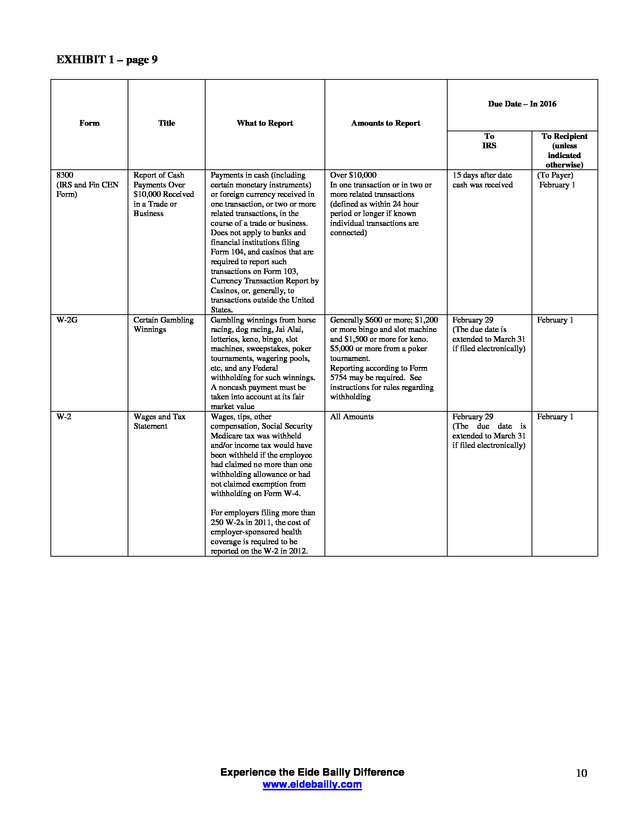

Must have been paid directly to a medical service provider or to the account holder. .Do not report trustee-to-trustee transfers. Experience the Eide Bailly Difference www.eidebailly.com 9 . EXHIBIT 1 – page 9 Due Date – In 2016 Form Title What to Report Amounts to Report To IRS 8300 (IRS and Fin CEN Form) Report of Cash Payments Over $10,000 Received in a Trade or Business W-2G Certain Gambling Winnings W-2 Wages and Tax Statement Payments in cash (including certain monetary instruments) or foreign currency received in one transaction, or two or more related transactions, in the course of a trade or business. Does not apply to banks and financial institutions filing Form 104, and casinos that are required to report such transactions on Form 103, Currency Transaction Report by Casinos, or, generally, to transactions outside the United States. Gambling winnings from horse racing, dog racing, Jai Alai, lotteries, keno, bingo, slot machines, sweepstakes, poker tournaments, wagering pools, etc, and any Federal withholding for such winnings. A noncash payment must be taken into account at its fair market value Wages, tips, other compensation, Social Security Medicare tax was withheld and/or income tax would have been withheld if the employee had claimed no more than one withholding allowance or had not claimed exemption from withholding on Form W-4. To Recipient (unless indicated otherwise) (To Payer) February 1 Over $10,000 In one transaction or in two or more related transactions (defined as within 24 hour period or longer if known individual transactions are connected) 15 days after date cash was received Generally $600 or more; $1,200 or more bingo and slot machine and $1,500 or more for keno. $5,000 or more from a poker tournament. Reporting according to Form 5754 may be required. See instructions for rules regarding withholding February 29 (The due date is extended to March 31 if filed electronically) February 1 All Amounts February 29 (The due date is extended to March 31 if filed electronically) February 1 For employers filing more than 250 W-2s in 2011, the cost of employer-sponsored health coverage is required to be reported on the W-2 in 2012. Experience the Eide Bailly Difference www.eidebailly.com 10 . EXHIBIT 1(a)—SUPPLEMENTAL INFORMATION Truncating taxpayer identifying numbers: Final regulations have been issued that allow issuers to truncate payee identifying numbers (SSN, ITIN, ATIN or EIN) on information Forms 1097, 1098, 1099, 3921, 3922 and 5498 for 2015. The filer’s identification number cannot be truncated on any form. To truncate where allowed, replace the first 5 digits of the 9 digit payee identification number with asterisks (*) or Xs (for example, an SSN would show as ***-**-NNNN or XXX_XX_NNNN). See Treasury Decision 9675, 2014-31 I.R.B. 242 https://www.irs.gov/irb/2014-31_IRB/ar07.html. FACTA reporting: A foreign financial institution (FFI) with a chapter 4 requirement to report a U.S.

account maintained by the FFI that is held by a specific U.S. person may satisfy the reporting requirement by reporting on Form(s) 1099 under the election described in Regulations section 1.1471-4(d)(5)(i)(A) or (B). Additionally, a U.S.

payor may satisfy a chapter 4 reporting requirement to report a U.S. account by reporting on Form(s) 1099. See Regulations section 1.1471-4(d)(2)(iii)(A). Latest developments for information returns: For the latest information about developments to information returns after they are published, go to https://www.irs.gov/uac/About-Form-1099. Where to paper file: There are only two Internal Revenue Service Centers that will accept paper filed information returns: Austin, TX and Kansas City, MO. Extension to file is possible: Returns filed with the IRS: An automatic 30-day extension of time to file a payor required information return with the IRS is made by completing and filing Form 8809, Application for Extension of Time To File Information Returns, by the due date of the return to be extended.

And, a second 30-day extension is possible under certain hardship conditions. The Form 8809 may be submitted on paper, or through the FIRE System. No signature or explanation of the reason for the extension request is required. Simply follow the instruction on Form 8809 for necessary information to be provided and how to submit the Form 8809 to the IRS. Returns filed with recipients: An extension of time to furnish information statements to recipients can be requested by sending a letter to the Internal Revenue Service, Information Returns Branch, Attn: Extension of Time Coordinator, 240 Murall Drive, Mail Stop 4360, Kearneysville, WV 25430.

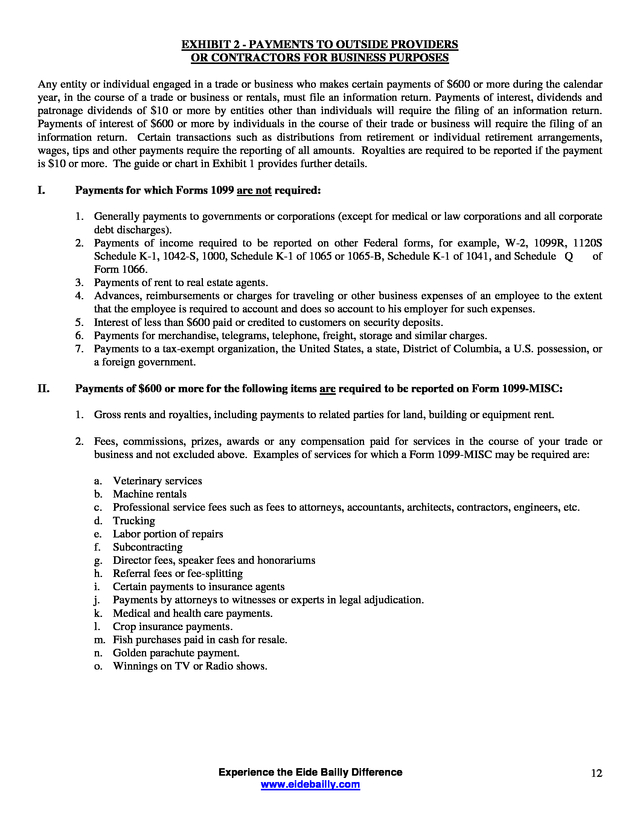

The letter requesting extension must contain information about the recipients, the reason for requesting the extension and be postmarked no later than the date the information statements would be due to the recipients. If the extension is approved by the IRS, the extension will generally be allowed for a maximum of 30 days. And, if there are more than 10 recipients whose information statements will be delayed by the extension being granted, the extension request must be submitted electronically. See IRS Pub 1220, Part D, Sec 4. Experience the Eide Bailly Difference www.eidebailly.com 11 . EXHIBIT 2 - PAYMENTS TO OUTSIDE PROVIDERS OR CONTRACTORS FOR BUSINESS PURPOSES Any entity or individual engaged in a trade or business who makes certain payments of $600 or more during the calendar year, in the course of a trade or business or rentals, must file an information return. Payments of interest, dividends and patronage dividends of $10 or more by entities other than individuals will require the filing of an information return. Payments of interest of $600 or more by individuals in the course of their trade or business will require the filing of an information return. Certain transactions such as distributions from retirement or individual retirement arrangements, wages, tips and other payments require the reporting of all amounts. Royalties are required to be reported if the payment is $10 or more.

The guide or chart in Exhibit 1 provides further details. I. Payments for which Forms 1099 are not required: 1. Generally payments to governments or corporations (except for medical or law corporations and all corporate debt discharges). 2. Payments of income required to be reported on other Federal forms, for example, W-2, 1099R, 1120S Schedule K-1, 1042-S, 1000, Schedule K-1 of 1065 or 1065-B, Schedule K-1 of 1041, and Schedule Q of Form 1066. 3.

Payments of rent to real estate agents. 4. Advances, reimbursements or charges for traveling or other business expenses of an employee to the extent that the employee is required to account and does so account to his employer for such expenses. 5. Interest of less than $600 paid or credited to customers on security deposits. 6.

Payments for merchandise, telegrams, telephone, freight, storage and similar charges. 7. Payments to a tax-exempt organization, the United States, a state, District of Columbia, a U.S. possession, or a foreign government. II. Payments of $600 or more for the following items are required to be reported on Form 1099-MISC: 1.

Gross rents and royalties, including payments to related parties for land, building or equipment rent. 2. Fees, commissions, prizes, awards or any compensation paid for services in the course of your trade or business and not excluded above. Examples of services for which a Form 1099-MISC may be required are: a. b. c. d. e. f. g. h. i. j. k. l. m. n. o. Veterinary services Machine rentals Professional service fees such as fees to attorneys, accountants, architects, contractors, engineers, etc. Trucking Labor portion of repairs Subcontracting Director fees, speaker fees and honorariums Referral fees or fee-splitting Certain payments to insurance agents Payments by attorneys to witnesses or experts in legal adjudication. Medical and health care payments. Crop insurance payments. Fish purchases paid in cash for resale. Golden parachute payment. Winnings on TV or Radio shows. Experience the Eide Bailly Difference www.eidebailly.com 12 .

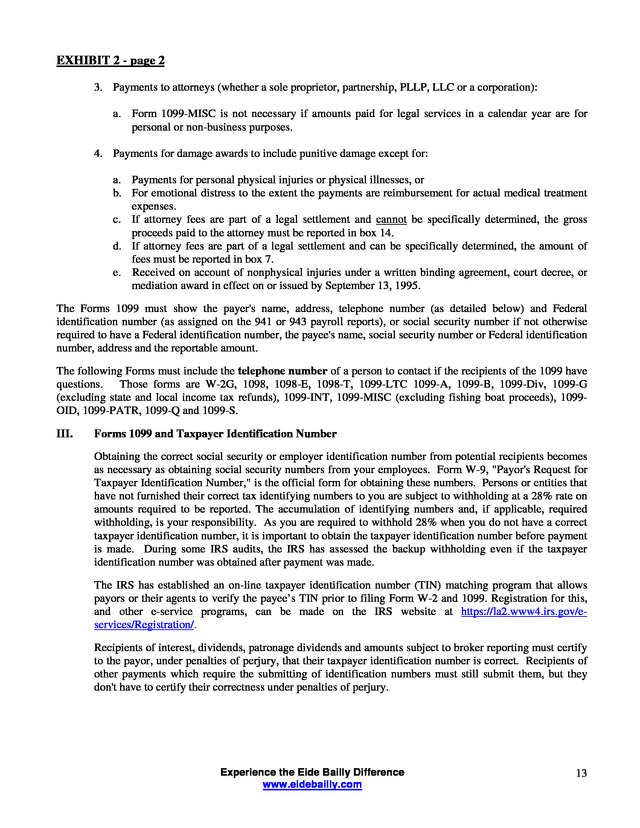

EXHIBIT 2 - page 2 3. Payments to attorneys (whether a sole proprietor, partnership, PLLP, LLC or a corporation): a. Form 1099-MISC is not necessary if amounts paid for legal services in a calendar year are for personal or non-business purposes. 4. Payments for damage awards to include punitive damage except for: a.

Payments for personal physical injuries or physical illnesses, or b. For emotional distress to the extent the payments are reimbursement for actual medical treatment expenses. c. If attorney fees are part of a legal settlement and cannot be specifically determined, the gross proceeds paid to the attorney must be reported in box 14. d.

If attorney fees are part of a legal settlement and can be specifically determined, the amount of fees must be reported in box 7. e. Received on account of nonphysical injuries under a written binding agreement, court decree, or mediation award in effect on or issued by September 13, 1995. The Forms 1099 must show the payer's name, address, telephone number (as detailed below) and Federal identification number (as assigned on the 941 or 943 payroll reports), or social security number if not otherwise required to have a Federal identification number, the payee's name, social security number or Federal identification number, address and the reportable amount. The following Forms must include the telephone number of a person to contact if the recipients of the 1099 have questions. Those forms are W-2G, 1098, 1098-E, 1098-T, 1099-LTC 1099-A, 1099-B, 1099-Div, 1099-G (excluding state and local income tax refunds), 1099-INT, 1099-MISC (excluding fishing boat proceeds), 1099OID, 1099-PATR, 1099-Q and 1099-S. III. Forms 1099 and Taxpayer Identification Number Obtaining the correct social security or employer identification number from potential recipients becomes as necessary as obtaining social security numbers from your employees.

Form W-9, "Payor's Request for Taxpayer Identification Number," is the official form for obtaining these numbers. Persons or entities that have not furnished their correct tax identifying numbers to you are subject to withholding at a 28% rate on amounts required to be reported. The accumulation of identifying numbers and, if applicable, required withholding, is your responsibility.

As you are required to withhold 28% when you do not have a correct taxpayer identification number, it is important to obtain the taxpayer identification number before payment is made. During some IRS audits, the IRS has assessed the backup withholding even if the taxpayer identification number was obtained after payment was made. The IRS has established an on-line taxpayer identification number (TIN) matching program that allows payors or their agents to verify the payee’s TIN prior to filing Form W-2 and 1099. Registration for this, and other e-service programs, can be made on the IRS website at https://la2.www4.irs.gov/eservices/Registration/. Recipients of interest, dividends, patronage dividends and amounts subject to broker reporting must certify to the payor, under penalties of perjury, that their taxpayer identification number is correct.

Recipients of other payments which require the submitting of identification numbers must still submit them, but they don't have to certify their correctness under penalties of perjury. Experience the Eide Bailly Difference www.eidebailly.com 13 . EXHIBIT 2 - page 3 For calendar year 2015, the original Form 1099 along with the recap Form 1096 must be filed by February 29, 2016 with your Internal Revenue Service Center. The due date is extended to March 31, 2016 if Forms 1099 are filed electronically. You must provide each payee a copy of their 1099 by February 1, 2016, except Forms 1099-MISC for gross proceeds paid to attorneys (box 14) or substitute dividend and tax-exempt interest payments reportable by brokers (box 8) which must be provided no later than February 16, 2016. Forms 1099-B and 1099-S must also be provided to the recipient by February 16, 2016, other extended dates may be applicable, see Exhibit 1 for additional information. Taxpayers who fail to prepare and file information returns are subject to a penalty of up to $100 per form subject to maximum amounts, plus the backup withholding if the tax identification number had not been obtained prior to payment. If one or more of the failures to file correct information returns are due to intentional disregard of the filing requirements or the correct information reporting requirements, the penalty is at least $250 per information return with no maximum penalty. Additionally, backup withholding will apply if the tax identification number had not been obtained prior to payment. If the failure to file an information return or to provide a copy to the taxpayer or to include correct information is due to reasonable cause and not to willful neglect, the penalty may be waived. Payments to Corporations and Partnerships 1.

Generally, payments to corporations are not reportable. However, you must report payments to corporations for the following: a. b. c. d. e. f. g. h. i. j. k. Medical and health care payments (Form 1099-MISC), Withheld federal income tax or foreign tax, Barter exchange transactions (Form 1099-B), Substitute payments in lieu of dividends and tax-exempt interest (Form 1099-MISC), Acquisitions or abandonments of secured property (Form 1099-A), Cancellation of debt (Form 1099-C), Payments of attorneys' fees and gross proceeds paid to attorneys (Form 1099-MISC), Fish purchases for cash (Form 1099-MISC), The credits for qualified tax credit bonds treated as interest and reported on Form 1099-INT, Merchant card and third-party network payments (Form 1099-K), and Federal executive agency payments for services (Form 1099-MISC). For additional reporting requirements, see Internal Revenue Bulletin 2003-26 at www.irs.gov/pub/irsirbs/irb03-26.pdf. 2. Reporting generally is required for all payments to partnerships.

For example, payments of $600 or more made in the course of your trade or business to an architectural firm that is a partnership are reportable on Form 1099-MISC. Eide Bailly LLP is a limited liability partnership, therefore, payments made to Eide Bailly LLP in the course of your business of $600 or more must be reported on Form 1099-MISC. For your convenience, the Eide Bailly LLP Federal identification number for Form 1099 reporting is 45-0250958. Experience the Eide Bailly Difference www.eidebailly.com 14 . EXHIBIT 3 – NONTAXABLE BENEFITS PROVIDED TO EMPLOYEES Generally speaking, the Internal Revenue Code (IRC) requires that income includes all compensation for services rendered, unless excluded by law. For this purpose, compensation means wages, salaries, fees, tips, commissions, bonuses, termination or severance pay and fringe benefits not excluded by Statute. The IRC allows exclusions from compensation for certain items provided for employees; for example: 1. Employer contributions to qualified employee benefit plans (profit-sharing plans, pension plans, 401(k), SEP’s, SIMPLE IRA’s, SIMPLE 401(k)). 2. Employee benefits, up to $5,250 per year for tuition, fees, books, supplies, etc., under an employer's nondiscriminatory educational assistance plan if the plan is in writing and is limited to providing employees with educational assistance. 3.

Group term life insurance premiums for up to $50,000 of life insurance. The following table is provided for your convenience for computing the taxable amount when the group term life insurance for an employee is over $50,000. UNIFORM PREMIUM TABLE – IRS TABLE I (Cost per $1,000 of coverage for a 1-month period) Applicable To 2015 Age of Individual* Cost Per $1,000 Under Age 25 Age 25-29 Age 30-34 Age 35-39 Age 40-44 Age 45-49 Age 50-54 Age 55-59 Age 60-64 Age 65-69 Age 70 and Over * Age as of last day of individual’s tax year $0.05 0.06 0.08 0.09 0.10 0.15 0.23 0.43 0.66 1.27 2.06 4. Accident and health insurance premiums for insurance to provide benefits for employees in the event of personal injury or sickness.

In addition, amounts received as damages (other than punitive damages) on account of personal physical injuries or physical sickness. However, interest included in an award of damages for personal physical injury action is includible in gross income. Damages received for emotional distress may not be treated as damages on account of a personal physical injury or sickness, except to the amount paid for medical care attributable to emotional distress. 5.

Amounts paid specifically - either as advances or reimbursements - for traveling and other bona fide ordinary and necessary expenses incurred in or reasonably expected to be incurred in the business of the employer. See Exhibit 5 for more details. 6. Incentive stock options and employee stock purchase plan options are generally excludible.

However, the spread between exercise price and fair market value of exercised nonstatutory stock option is reportable compensation. Use box 12 of Form W-2 and Code V. Generally, all withholding rules apply. Experience the Eide Bailly Difference www.eidebailly.com 15 .

EXHIBIT 3 – page 2 7. Up to $5,000 of child or dependent care assistance services that are paid by an employer and furnished pursuant to a written plan generally are not includable in the employee’s gross income if the qualifying person is either (1) under 13 years of age when the care was provided, (2) a dependent who is physically or mentally dependent and resides with recipient employee for more than six months of the year, or (3) a spouse who is physically or mentally incapable of caring for themselves, who resides with recipient employee for more than six months of the year. In addition to the benefits listed above, various noncash “Fringe Benefits” qualify for exclusion from employee compensation. Such noncash “Fringe Benefits” include the following: 8. No additional cost services, which are services provided to an employee that does not cause the employer any substantial additional cost because these services are already offered to the customers in the ordinary course of business. 9.

Adoption assistance programs. Qualified adoption expenses under a written adoption assistance program are excludable from an employee’s gross income. The qualified expenses may be paid to a third party or reimbursed to an employee by an employer.

The dollar amounts of the exclusion and the phase out for higher income taxpayers are the same as the adoption credit; for 2016 the amount that may be excluded is $13,460. The phase-out range for 2016 income is $201,920 to $241,920. The amount that may be excluded for 2015 is $13,400 and the 2015 phase-out range is $201,010 to $241,010. 10. “Qualified” Achievement awards of tangible personal property for either length of service or safety achievement valued up to $1,600.

However $400 is the ceiling, if the awards are not “qualified” plan awards. Further, the “qualified award plans” must not average over $400 per year for all awards given that year. Refer to IRC Section 274(j)(3)(B) 11. Various “de minimis” benefits.

Examples include occasional meals, supper money, or local transportation provided because of overtime work, meals to employee-operated eating facilities; taxi fare; occasional cocktail parties or picnics; traditional holiday gifts. 12. Qualified moving expense reimbursements that the employee could deduct if paid without reimbursement. 13. Qualified employee discounts.

An employee discount is the excess of (1) the price at which property or services are offered by an employer to nonemployee customers, over (2) the price at which the employer offers the same property or services to employees. 14. Working condition fringes. A working condition fringe is any property or service provided to an employee by the employer to the extent that the cost of the property or services would have been deductible by the employee as a trade or business expense under Code Sec.

162 or as a depreciation deduction under Code Sec. 167, if the employee had paid for the property himself. Examples are employee-paid business travel and the use of employer provided vehicles for business purposes. 15. Qualified transportation fringe benefits.

The benefits include: a. Transportation in a commuter highway vehicle (van pool), if in connection with travel between the employee’s residence and place of employment. b. Transit passes for use on a mass transit facility (e.g., rail, bus or ferry) or a commuter highway vehicle Experience the Eide Bailly Difference www.eidebailly.com 16 .

EXHIBIT 3 – page 3 c. Qualified parking at or near the employer’s business premises or a location from which the employee commutes to work by mass transit, employer provided commuter highway vehicle or car pool. d. For transit passes or employer provided commuter highway vehicle “van pooling” a maximum of $250 and $255 per month can be excluded by employees in 2015 and 2016, respectively (2015 PATH Act). i. The rule that an employer reimbursement is excludible only if vouchers are not available to provide the benefit continues to apply, except in the case of reimbursements for vanpool or transit benefits of between $130 and $250, provided for months beginning after December 31, 2014, and before enactment of the 2015 PATH Act. e.

For 2015 and 2016, up to $250 and $255 a month, respectively, of qualified parking may be excluded. f. Employers may offer excludable bicycle commuting benefits up to $20 per month, for qualified bicycle commuting months during calendar year 2015 and 2016. 16. Qualified employer provided retirement advice.

This includes any retirement planning services provided to an employee and spouse by an employer maintaining a qualified employer plan. A word of caution, employee/owners (owning more than 2%) of a Subchapter S Corporation are not treated as an employee for fringe benefit purposes and may be subject to tax on such benefits. Also, unless specifically excluded, the value of fringe benefits provided to a partner for services rendered as a partner is generally treated as a guaranteed payment included in the partner’s income. All taxable compensation to employees should be reported on the employee's Form W-2. The W-2 should include taxable employee fringe benefits, even if they are not subject to income tax withholding. Effective on March 30, 2010, children under the age of 27 are considered dependents of a taxpayer for purposes of the general exclusion of reimbursements for medical care expenses of an employee, spouse, and dependents under an employer-provided accident or health plan. See IRS Publication 15-B for more detailed information. Experience the Eide Bailly Difference www.eidebailly.com 17 .

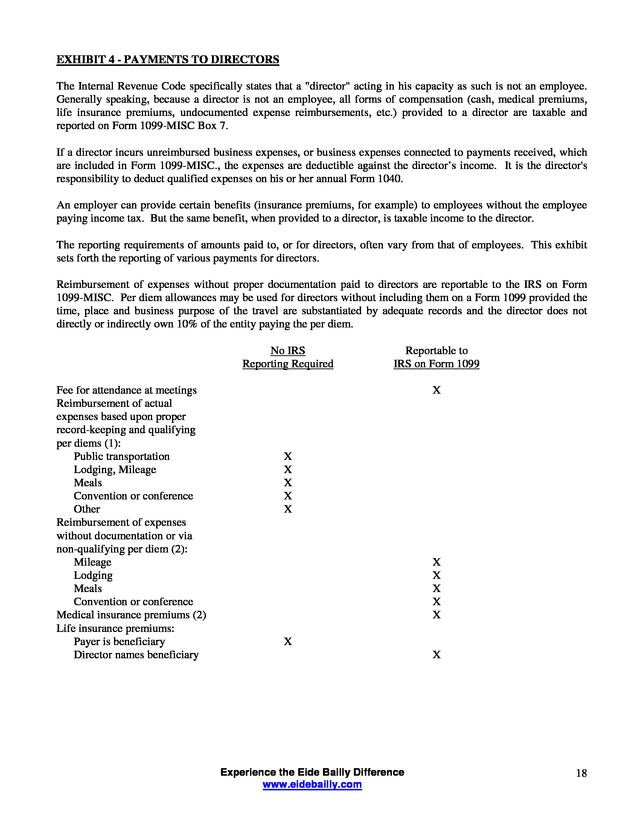

EXHIBIT 4 - PAYMENTS TO DIRECTORS The Internal Revenue Code specifically states that a "director" acting in his capacity as such is not an employee. Generally speaking, because a director is not an employee, all forms of compensation (cash, medical premiums, life insurance premiums, undocumented expense reimbursements, etc.) provided to a director are taxable and reported on Form 1099-MISC Box 7. If a director incurs unreimbursed business expenses, or business expenses connected to payments received, which are included in Form 1099-MISC., the expenses are deductible against the director’s income. It is the director's responsibility to deduct qualified expenses on his or her annual Form 1040. An employer can provide certain benefits (insurance premiums, for example) to employees without the employee paying income tax. But the same benefit, when provided to a director, is taxable income to the director. The reporting requirements of amounts paid to, or for directors, often vary from that of employees. This exhibit sets forth the reporting of various payments for directors. Reimbursement of expenses without proper documentation paid to directors are reportable to the IRS on Form 1099-MISC.

Per diem allowances may be used for directors without including them on a Form 1099 provided the time, place and business purpose of the travel are substantiated by adequate records and the director does not directly or indirectly own 10% of the entity paying the per diem. No IRS Reporting Required Fee for attendance at meetings Reimbursement of actual expenses based upon proper record-keeping and qualifying per diems (1): Public transportation Lodging, Mileage Meals Convention or conference Other Reimbursement of expenses without documentation or via non-qualifying per diem (2): Mileage Lodging Meals Convention or conference Medical insurance premiums (2) Life insurance premiums: Payer is beneficiary Director names beneficiary Reportable to IRS on Form 1099 X X X X X X X X X X X X X Experience the Eide Bailly Difference www.eidebailly.com 18 . EXHIBIT 4 – page 2 (1) Proper documentation includes the substantiation of amount, time, place, business purpose, etc. Normally this will include completion of an expense report with receipts attached. (2) These items are reportable to the Director as taxable income; however, the Director then has the opportunity to deduct expenses on his or her individual income tax return. When these payments are included in a Form 1099, it is helpful to the recipient if a schedule showing a breakdown by category is enclosed with the Form 1099. Experience the Eide Bailly Difference www.eidebailly.com 19 . EXHIBIT 5 – EMPLOYEE BUSINESS EXPENSES AND EXPENSE ACCOUNTS The IRS has issued guidance on the reporting and substantiation requirements for employee business expenses. The rules affect the way employers and employees report expenses and reimbursements. Employers are required to withhold Federal income and Social Security taxes from expense account allowances paid to employees where the employee is not required to substantiate the amount of business mileage or business expenses to the employer. The rules begin by separating expense reimbursement policies into "accountable" and "non-accountable" plans. An accountable plan REQUIRES an employee to substantiate expenses incurred to the employer. This type of plan limits reimbursements to deductible business expenses paid or incurred in connection with the performance of services as an employee. This type of plan also requires that excess amounts be returned to the employer.

Any unsubstantiated amounts which are not returned to the employer within a reasonable period of time will be subject to payroll taxes. IRS has provided safe harbor rules defining a reasonable period of time. An example would be advances made not more than 30 days prior to the reimbursable expense where the employee accounts to the employer within 60 days after the reimbursable expense. Another example is where employers provide at least quarterly statements to employees reflecting unsubstantiated expenses.

Under this safe harbor rule, any additional amounts substantiated and any reimbursements made by the employee within 120 days of the statement qualify thereby exempting those amounts from payroll taxes. A practical distinction between an accountable and non-accountable plan focuses on the party who is responsible for substantiating the business purpose and amount of expenses incurred. A non-accountable plan leaves this burden upon the employee on his or her personal tax return. An accountable plan requires the employee to transfer this required detail of business expenses to the employer for tax reporting. There are two major disadvantages to maintaining a non-accountable plan.

The first affects employers. Employers must pay payroll taxes on the expense allowances. This payroll tax cost may be offset, in part, by the cost savings associated with reduced record keeping by the employer.

The second major disadvantage affects the employee. Employee business expenses are deductible only as a miscellaneous itemized deduction which is subject to a limitation of 2% of adjusted gross income. The deductions are not available if the employee does not itemize deductions on their personal return. In addition, the nondeductible portion of meals and entertainment will be absorbed by the employee rather than the employer. A method used to reduce the record keeping burden for both employers and employees is the use of per diems and mileage allowances.

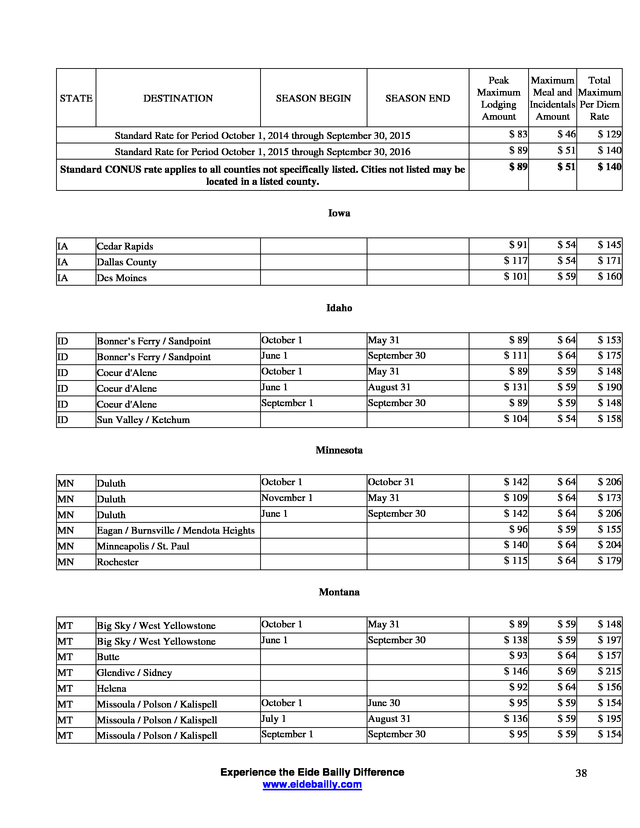

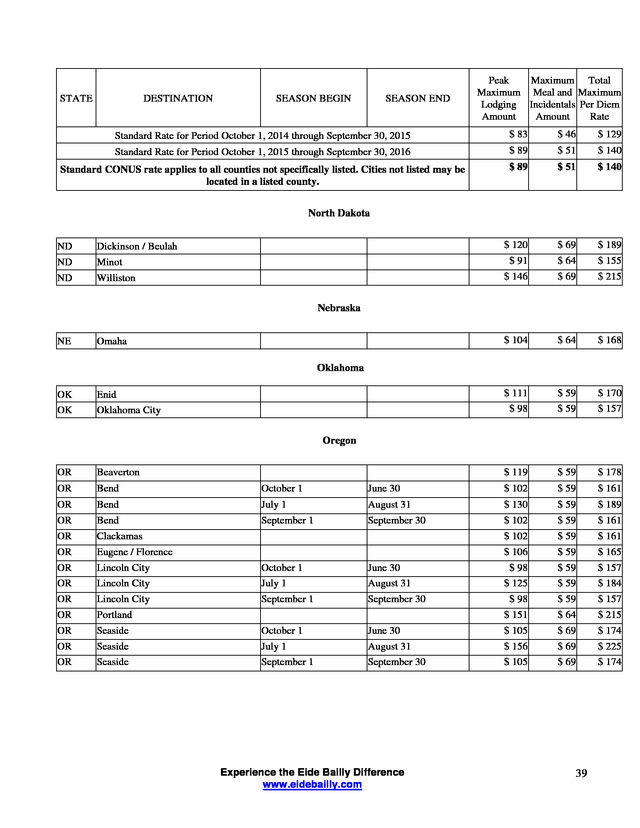

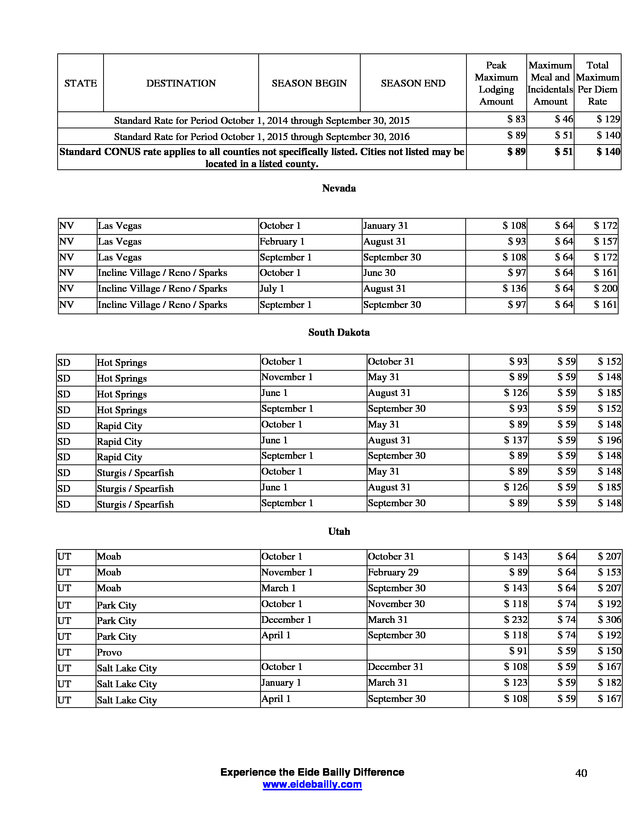

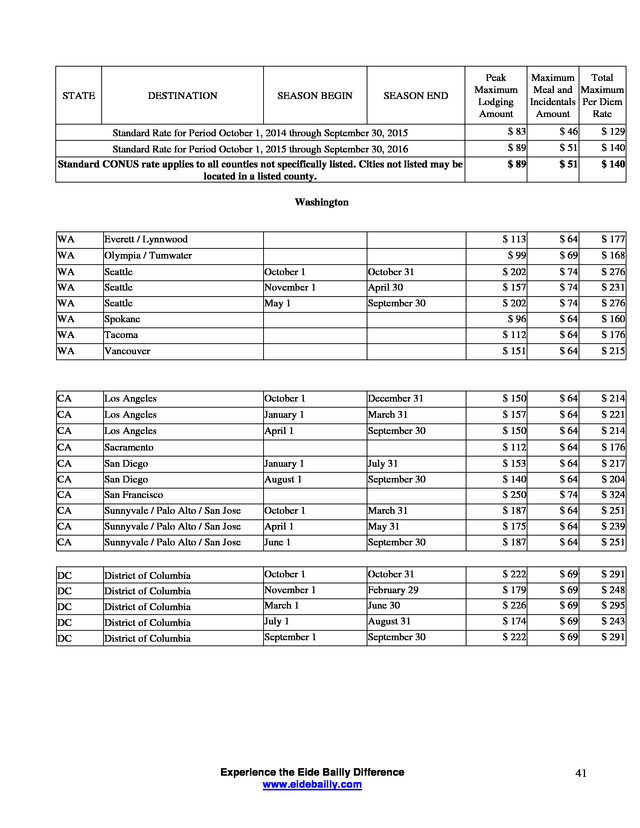

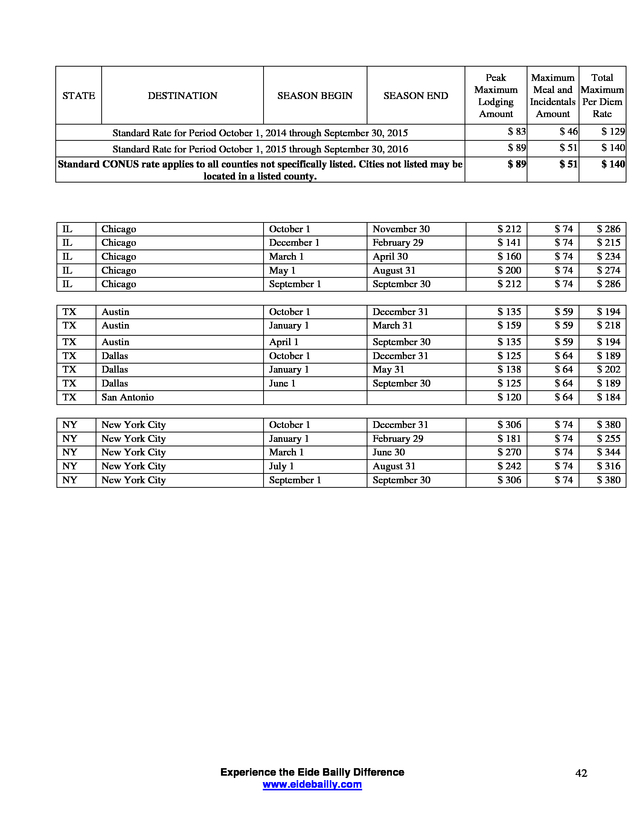

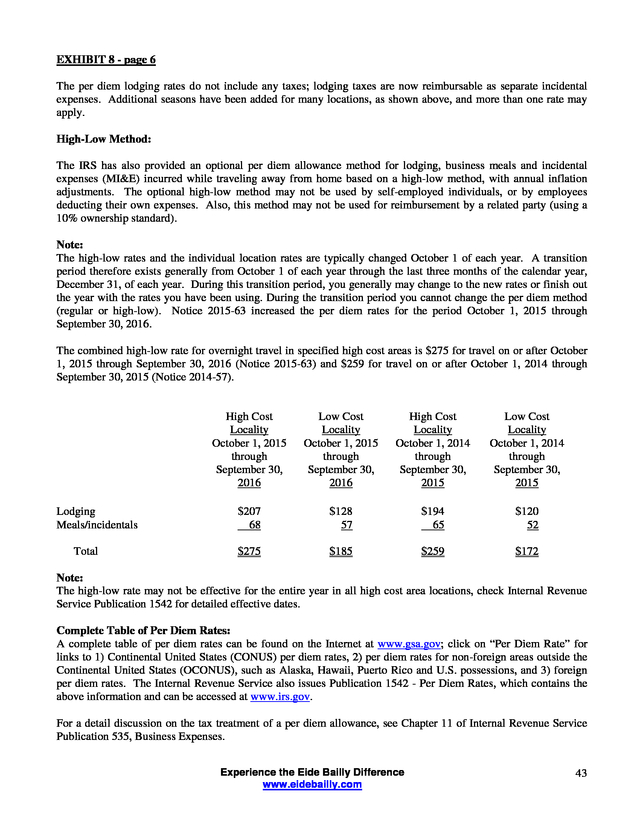

If the per diem amount does not exceed the Federal guideline for the area in which the travel and meal costs are incurred, substantiation is not required for the actual amount of the expenses incurred. However, the other substantiation requirements must still be met, (i.e., place and business purpose of the expense). The per diems vary by locality and are published by the IRS. The IRS has set specific per diem rates for various locations. See Exhibit 8 for a listing. A person who owns at least 10% of a corporation or is a family member of a business owner cannot use the regular per diem method or the alternate high-low per diem method to substantiate expenses.

Any amounts paid in excess of the Federal per diem will be subject to payroll taxes. The mileage allowance for business miles was 57.5 cents per mile for 2015. The IRS has announced the mileage rate beginning January 1, 2016 will be 54 cents per mile. Experience the Eide Bailly Difference www.eidebailly.com 20 .

EXHIBIT 5 - page 2 Following are some sample situations and respective answers: 1. Situation: Employer reimburses employee actual expenses incurred, employee turned in receipts or documented expense vouchers. Answer: Employer has the policing responsibility of making sure that the expenses are properly documented and are otherwise a legitimate business expense. An employee policy should be set that expenses will not be reimbursed unless they are properly documented. If they are not properly documented, they should either not be reimbursed by the employer or else they should be added to the employee's W-2. 2.

Situation: Employee is reimbursed expenses by employer, employer requires no documentation to verify amount. Answer: The reimbursed amount is to be reported on a W-2 as additional compensation to the employee. Then the employee has the responsibility of deducting appropriate expenses on his or her return. 3. Situation: Employee receives per diem of X-dollars per day when out of town. Answer: If the per diem (a) is paid only when the employee is out overnight, (b) the per diem amount is reasonable, and (c) the per diem amount does not exceed the IRS guidelines (see Exhibit 8), then the amount does not have to be reported on the employee's W-2. 4. Situation: Employee receives mileage paid at a rate of 57.5 cents per mile for 2015. Answer: As long as the mileage is for business and not commuting expense, reimbursement up to the amounts indicated during the specified time period for 2015 does not have to be reported on the employee's W-2.

For reimbursements exceeding this, the employer is required to report the excess reimbursement on Form W-2. The amounts may be reported on the same Form W-2 showing wages paid to the employee, or may be reported on a separate W-2. 5. Situation: Employee or director receives company paid meals and amount is billed directly to company by restaurant. Answer: If the bill or supporting data with the bill contains adequate documentation that it was for a legitimate business purpose and not for a convenience meal, the amount does not have to be reported on the employee's W-2 (or on Form 1099-MISC for directors). If the amount does not contain proper documentation, it should either be charged back and deducted from the employee's paycheck or else included in his W-2 (or on Form 1099-MISC for directors).

It should be noted that the recommended treatment of deducting the amount from the employee's paycheck is to foster proper documentation on the charge slip. 6. Situation: Employee or director is given credit card for expenses incurred for employer, company pays all bills, employee generally does not complete expense vouchers unless out of town overnight. Answer: The amounts do not have to be included in an employee's W-2, (or on Form 1099-MISC for directors), provided the expenses are legitimate business expenses and they are properly documented. If the employee is not out of town overnight and incurs meals, he or she should substantiate that this was a business meal and not a personal meal.

If he or she cannot document that it was a business meal or was not out of town overnight, the amount should either be charged back to the employee, or included on Form W-2 (or on Form 1099-MISC for directors). Experience the Eide Bailly Difference www.eidebailly.com 21 . EXHIBIT 5 - page 3 7. Situation: What is the tax treatment of expenses incurred by officers and employees in connection with travel to national or district conventions? In some cases, the travel expenses include expenses for employees and their spouses. Answer: If an employee is reimbursed on an actual expenses basis for ordinary and necessary expenses incurred as a delegate or participant in national or district conventions or conferences, the amounts reimbursed to them are not taxable to them, nor are they reportable on their income tax returns. No deduction is allowed for spouses of directors or employees, unless it can be proven the spouse is a bona fide employee and is partaking in the trip because of a bona fide business purpose. NOTE: If an employee was reimbursed at a rate which exceeds the legal per diem rate for use of the employee's automobile, it will be necessary for the employer to include the excess amounts paid as additional compensation to the employee or officer in a Form W-2. As stated above, if an employee is reimbursed on an actual expense basis or per diem which does not exceed the limits provided by law, the reporting of additional compensation on Form W-2 will not be required. When employee business expenses are reported on a W-2, the unsubstantiated amounts and the amounts in excess of per diem rates are reported in box 1, 3 and 5 of the Form W-2.

The substantiated amounts and amounts up to the per diem rates are reported in box 12 of the Form W-2 using code L. Employees who are related to their employers (members of the same family as the employer or who are stockholders owning more than 10% of the outstanding stock of an employer corporation) in addition to establishing time, place and business purpose of travel, must keep records of the amount spent daily for travel, broken down into reasonable categories such as meals, gasoline, oil and taxi fares. They must also obtain receipts for lodging regardless of amount. EXCEPTIONS TO PAYROLL REPORTING REQUIREMENTS The Internal Revenue Code specifically excludes certain expenses from the rigid requirements it sets forth: Food and Beverages for Employees - Costs of operating an employee cafeteria are excluded, provided the eating facility is located on or near the employer's business premises and the revenue derived from the facility normally equals or exceeds the direct operating cost of the facility. Business Meetings for Employees - Entertainment expenses directly related to bona fide business meetings for a taxpayer's employees involving the discussion of business matters, training, etc. are only subject to the record-keeping requirements as detailed in the next exhibit on record keeping. Recreational and Social Expenses for Employees - Expenditures for social or recreational activities primarily for the benefit of a taxpayer's employees are only subject to the record-keeping requirement as detailed in the exhibit on record-keeping.

For these items, the employer must not discriminate in favor of corporate officers, shareholders or highly compensated individuals. This exclusion applies to employee benefit programs such as: 1. Christmas parties, annual picnics, summer outings, etc., or 2.

Maintaining a swimming pool, baseball diamond, bowling alley or golf course. Experience the Eide Bailly Difference www.eidebailly.com 22 . EXHIBIT 6 - RECORD-KEEPING FOR TRAVEL, ENTERTAINMENT AND MEALS EXPENSE The requirements pertaining to travel and entertainment expenses affect all businesses and individuals. The following summary should clarify the requirements pertaining to the deduction of travel, entertainment and gift expenses. Entertainment and Meal Expenses As a general rule, business entertainment and meal expenses will be deductible only if it can be established that they are ordinary and necessary expenses of carrying on a trade or business. The business entertainment and meal expenses must also be properly substantiated. If you are not in a particular trade or business, entertainment and meal expenses may be deductible if they are to be used for the production or collection of income, provided the individual itemizes deductions. To establish that expenditures are ordinary and necessary expenses, you must be able to show that the expenses are: 1.

Directly related to the active conduct of your trade or business, or 2. Associated with the active conduct of your trade or business. For an entertainment or meal expenditure to meet the "directly related" test, you must be able to show that: 1. You had more than a general expectation of deriving income or some other specific benefit at some time in the future.

This specifically excludes items of expenditure made in the sense of a goodwill gesture. 2. That you did engage in business during the entertainment or meal period with the person being entertained. 3. The primary reason for or aspect of the combined business and entertainment or meal was the transaction of business. The key point in establishing whether an activity meets the "directly related" test would be the proximity of the meeting place to a clear business setting.

Expenses for entertainment or meals in a clear business setting directly in furtherance of your trade or business are considered directly related to the active conduct of your trade or business. Expenses are considered not to meet the "directly related" test when there are circumstances present which indicate there will be little or no possibility of engaging in active conduct of business. Examples of expenses which would have difficulty meeting the "directly related" test are those incurred at meetings which are conducted at lounges or night clubs, theaters, sporting events, or at social gatherings in which you meet with groups of people. This assumption can be overcome by proving you did engage in a substantial business discussion during the entertainment. It should be noted, however, that the burden of proof and substantiation is on you. Entertainment and meal expenses that do not meet the "directly related" test, but which are "associated with" the active conduct of your trade or business are allowable if it directly precedes or follows a substantial and bona fide business discussion.

If you were to have a business discussion with a client or a potential client which was followed by some form of entertainment or meal expenditure, the "associated with" test would have been met. Goodwill entertaining is generally deductible as "associated with" entertainment if its purpose is to get new business or encourage the continuation of a business relationship or it can be shown that the entertainment is associated with the active conduct of your business. For entertainment related meals to be deductible two other restrictions apply, you (or an employee of yours) must be present at the meal and food and beverages cost that are considered lavish or extravagant under the circumstances will not be deductible. Experience the Eide Bailly Difference www.eidebailly.com 23 . EXHIBIT 6 - page 2 In addition to substantiating the business purpose, you must maintain adequate records of the transaction. The following are types of documentation that are to be maintained for travel, meals and entertainment. Travel - you are required to maintain the following records: 1. The mileage reading of your business automobile should be recorded on the first and last day of each year. 2. The business mileage driven is not required to be written in a dairy.

However, adequate records need to be maintained to substantiate the business use of vehicles. 3. If you travel by a method other than your business automobile, you should retain the receipts. 4. In addition to the business mileage or the cost of alternate travel methods, you should note where you went, whom you went to see and why you went to see them. 5.

The cost of lodging must be supported by a receipt. 6. The cost of meals incurred in your travel while out of town overnight should be written in a diary and if less than $75, no receipt is required. 7. The cost of incidental expenses, such as gratuities, cab fares, laundry, tolls, parking and telephone calls, incurred in your travel should be written in a diary and no receipt is generally required if less than $75 per day. These incidental expenses can be grouped by category. 8.

If you claim actual automobile expenses in lieu of the standard mileage allowance, the costs of business automobile operations, such as gasoline and oil, repairs, tires and supplies, insurance, taxes, licenses, interest and miscellaneous, must be supported by receipts. 9. Whether actual expenses plus depreciation or lease payments, or the mileage allowance method is used, the cost of business – connected tolls and parking can also be deducted as long as there’s a record of the expense. Meals and Entertainment - you must maintain the following records: 1. The receipted amount of each separate expenditure for meals and entertainment.

This receipt should indicate the name, date, location and type of entertainment. 2. Either on the receipt or in a diary you should indicate who was entertained and the business purpose of meals or entertainment. A summary of the business relationship and discussion should also be made either on the receipt or in a diary. You should record the elements of an expenditure in your records at or near the time of the expenditure. Recording these entries substantially after the fact will not comply with the record-keeping rules. A canceled check, together with a receipt, paid bill, or similar evidence sufficient to support an expenditure, ordinarily will establish the nature of an expense. Experience the Eide Bailly Difference www.eidebailly.com 24 .

EXHIBIT 6 - page 3 Dues for country clubs and other facilities which you use for entertaining such as yachts, lodges and boats are not deductible. For entertainment facilities, the no-deduction rules applies to rent, depreciation, maintenance, operating expenses, but not to expenses that would otherwise be deductible such as taxes. In addition the following requirements must be met: 1) meals must not be lavish or extravagant, 2) a bona fide business discussion must precede, directly follow or be discussed during the meal, and 3) an employee must be present at the meal. The amount allowable as a deduction will be limited to 50% of such expenses. This 50% provision will affect the employers if employees are reimbursed for their meal and entertainment expenses. The 50% deduction limit for meals and entertainment also applies to tax-exempt organizations filing Form 990-T. For 2015, the out-of-town business meals deduction is 80% for individuals subject to the Department of Transportation's hours-of-service limitations. Business Gifts You are permitted to deduct business gifts if you can prove that the gift was an ordinary and necessary business expense or an investment related expense.

The amount which you may deduct is limited to $25 per year for each recipient. However, there is no dollar limit on the deductions of a gift made to a corporation, partnership and other business entity. But, if the gift is intended for the eventual use of an employee, they are subject to the $25 limitation. You may exclude from the $25 limitation items which cost less than $4 each which contain your business name (i.e., pens, etc.).

You may also exclude promotional items such as signs, display racks or other promotional material which are intended for use on the business premises of the recipient. Finally, you may exclude gifts of tangible personal property having a cost of $400 or less which are awarded to an employee for length of service or safety achievement. As an employer, you can distribute turkeys, hams or other merchandise of nominal value to employees as holiday gifts. Employees do not have to include the value of these gifts in their income. Travel Expenses - Domestic Any expenses which you may incur in business travel away from home overnight are generally deductible as trade or business expenses.

You may also deduct travel expenses which are utilized for the production of income. If you own rental property, you may be allowed to deduct the travel expenses incurred to inspect your rental property. Travel expenses include mileage fares, meals and lodging.

To be deductible, domestic travel must be primarily related to business; also, it is subject to the record-keeping requirements and deductible limits discussed in the entertainment section. See Caution under Foreign Conventions below for discussion of cruise ship expenses. Experience the Eide Bailly Difference www.eidebailly.com 25 . EXHIBIT 6 - page 4 Travel - Foreign (other than conventions) If you travel outside the United States and spend the entire time on business activities, all related costs are deductible. Even if you did not spend all the time on business activities, there are four situations that allow all expenses to be deducted anyway. These exceptions are: 1. The length of the trip is seven consecutive days or less (not counting the day you leave the United States and the day you return); all of the related expenses are deductible. 2.

The length of the trip is more than 7 days but less than 25% of the total time was spent on non-business activities. 3. The traveler has no substantial control over arranging the trip outside the United States. An employee is considered not having substantial control if he isn’t a managing executive or doesn’t own 10% or more of the employer. 4.

The individual can establish that a personal vacation was not a major consideration in making the trip. Travel expenses that are primarily for business must be allocated based on a fraction of business days to total days. Travel days (not including extra travel time for non-business activities), “presence required” days (even if most of the time was not spent on business) and weekends/holidays that fall between business days are all counted as business days. Travel expenses for primarily personal reasons are non-deductible except for conference fees or registration costs. Foreign Conventions A foreign convention is defined as a convention, seminar or similar meeting held outside the “North American area”. The North American area is defined as the United States, its possessions, the former Trust Territory of the Pacific Islands, (the Republic of Marshall Islands, the Federated States of Micronesia and the Republic of Palau), Canada and Mexico. The United States consists of the fifty states and the District of Columbia.

The IRS treats as possessions of the United States for this purpose: American Samoa, Baker Island, Puerto Rico, the Northern Mariana Islands, Guam, Howland Island, Jarvis Island, Johnston Island, Kingman Reef, Midway Island, Palmyra Atoll, the U.S. Virgin Islands, Wake Island and other U.S. Islands.

The North American area also includes what is termed a “beneficiary country”. Beneficiary countries include: Antigua and Barbuda, Barbados, Bermuda, Costa Rica, Dominica, Dominican Republic, Grenada, Guyana, Honduras, Jamaica, Trinidad and Tobago. In addition, certain agreements provide that Aruba, Bahamas and Netherland Antilles are North American areas. Travel expenses to and from foreign conventions are fully deductible only if at least one-half of the total days (not including travel days) are devoted to business related activities.

If less than one-half of the days are devoted to business related activities, only the percentage of business days to total days will be allowed. A deduction for a full day is allowed only if there are at least 6 hours of scheduled business activities. If there are 3 hours of scheduled business activities on a certain day, a deduction for one-half day is allowed. Experience the Eide Bailly Difference www.eidebailly.com 26 .

EXHIBIT 6 - page 5 Deductible transportation costs are limited to the lowest coach or economy rate charged by a commercial airline during the calendar month in which the convention begins. The deduction for meals, lodging and local transportation is limited to the per diem rate allowable to U.S. civil servants in that country during the month of the convention. In addition, you must attend two-thirds of the total scheduled business activities to obtain the deduction for the meals, lodging and local transportation. The substantiation requirements for foreign convention deductions impose responsibilities upon both the individual who attends the convention and the organization which sponsors the convention.

The following documents must be attached to the tax return on which the deduction is claimed: 1. A written statement signed by the individual attending the convention which includes: A. Information disclosing the total number of days on the trip excluding travel days to and from the convention. B.

The number of hours which the individual devoted to scheduled business activity on a day by day basis. C. A program of the scheduled business activities of the convention. 2. A written statement signed by an officer of the organization or group sponsoring the convention which includes: A.

A schedule of the business activities of each day of the convention. . B. The number of hours which the individual attending the convention attended scheduled business activities. Caution – Meetings aboard cruise ships have additional limitations and requirements to be considered. The deduction for attending a convention, seminar or meeting on a cruise ship is limited to $2,000, per reporting person, and may only be deductible if the following requirements are met: 1. Reporting requirements – 2 statements – First, a statement, signed by the person attending the convention, seminar or meeting, that includes information as to the total days of the trip, not including travel days to and from the place of department, and the number of hours each day spent on scheduled business activity, a program of the scheduled events and other information the IRS may require.

The second statement, signed by an officer of the event convention, seminar or meeting sponsoring group, must include a schedule of business activity attended scheduled events and other information the IRS may require. 2. A direct connection between the convention, seminar or meeting and the active conduct of the taxpayer’s trade or business is established. 3. The cruise ship is registered in the U.S. 4.

All ports of call on the cruise are located in the U.S. or U.S. possessions. Because the cruise ship must be registered in the U.S., no deductions can be taken for conventions, seminars or meetings held on a cruise ship with a foreign flag registry and no deduction is allowed if any port of call is a foreign port. Experience the Eide Bailly Difference www.eidebailly.com 27 .

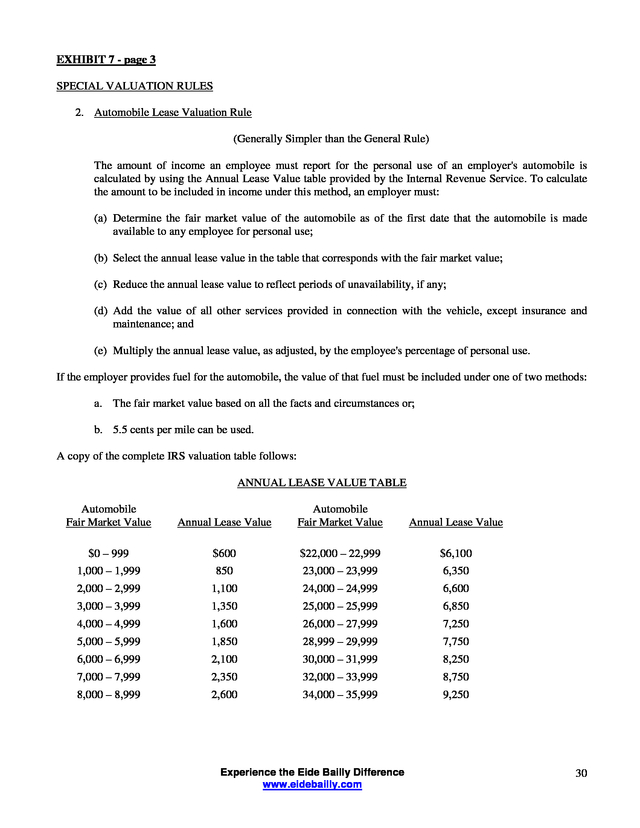

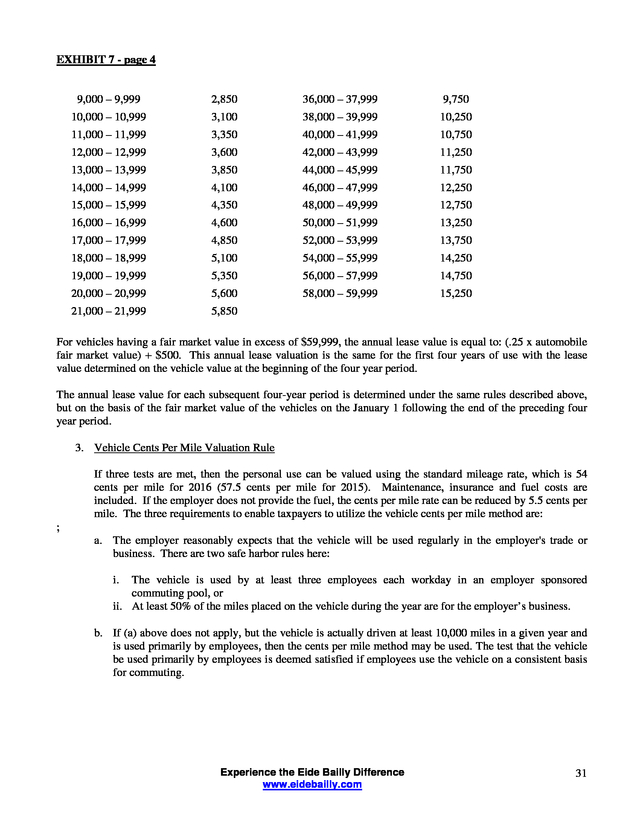

EXHIBIT 7 - RECORD-KEEPING AND DEDUCTIONS FOR BUSINESS VEHICLES You are required to substantiate the amount of vehicle expenses, the time and place of the expenses and the business purpose of the expenses. Contemporaneous records (daily logs) are recommended but not required. However, some form of written substantiation will be necessary. Employers will not be required to keep duplicate copies of the records kept by employees. Employers can have the employee prepare a summary statement of the total mileage, the business mileage, the percentage of business use and indicate whether or not the employee has written records. Employers can rely on the statement by employees for purposes of payroll tax withholding (if the vehicle is used for the employee's personal use) unless the employer knows or has reason to know the information is false.

Similarly, questions regarding total mileage, percentage of business use and whether written records exist will be required on the employer's income tax returns. VEHICLES FOR INDIVIDUALS FOR WHICH NO RECORDS ARE REQUIRED No records are needed for vehicles operated under an observed written policy of the employer limiting personal use and those that, by their nature, are unlikely to be used for personal purposes. The first category (employer's written policy limiting personal use) covers two situations: (1) vehicles that are kept on the employer's premises during non-business hours, and (2) vehicles for which the only personal use is commuting between the employee's residence and their place of employment. Thus, no records are required for a vehicle owned or leased by an employer that is kept on the employer's premises when it is not being used for business purposes, provided there is a generally observed written policy that no employee can use the vehicle for personal purposes. Also, no records are required for a vehicle owned or leased by the employer if (1) an employee (other than an officer, director or 1% or more owner) is required to commute in the vehicle for valid business reasons, (2) there is a generally observed written policy that the vehicle is not used for personal purposes other than commuting, and (3) an appropriate amount is included in the employee's wages for the commuting use. The optional $3 per day valuation for commuting use under previous IRS regulations can still be used. The second category (vehicles unlikely to be used for personal purposes) consists of the following list of vehicles exempt from the record keeping and rules: 1.

Clearly marked police and fire vehicles (and in certain cases unmarked police vehicles) 2. Delivery trucks with seating only for the driver and a folding jump seat 3. Cargo vehicles with a gross vehicle weight over 14,000 pounds 4.

Passenger buses with a capacity of at least 20 passengers 5. Ambulances or hearses 6. Tractors and specialized farm vehicles 7.

School buses 8. Flatbed trucks 9. Bucket trucks (“cherry pickers”) 10.

Cranes & derricks 11. Forklifts 12. Cement mixers 13.

Dump trucks including garbage trucks 14. Refrigerated trucks 15. Qualified moving vans 16.

Combines 17. Qualified specialized utility repair trucks 18. Unmarked law enforcement vehicles Experience the Eide Bailly Difference www.eidebailly.com 28 .

EXHIBIT 7 - page 2 WITHHOLDING RULES Employers are required to include amounts in an employee's wages based on personal use of an automobile. However, income tax withholding is not mandatory. An employer will be able to elect not to withhold income taxes on wages due to personal use of vehicles if the affected employees are so notified by the employer. The annual income tax withholding election is made by the employer on an employee-by-employee basis. The election not to withhold must be made by February 1of the year the employer elects not to withhold income taxes, or 30 days after the employer first makes a vehicle available for an employee’s personal use.

Employers will still have to withhold and match the employee's share of FICA taxes and pay unemployment taxes on the personal use. An employer can elect to withhold and pay the applicable payroll taxes by pay period, quarterly, semiannually, or annually, as long as all taxable benefits received are treated as paid in the calendar year in which they are provided. The period of reporting income can vary from employee to employee. Employers may also elect to include the full value of the use of a company vehicle in an employee's wages without regard to the actual business or personal use of the employee.