Private Equity Connections in the Middle Market - Special Edition by Buyouts Insider – Spring 2016

Duane Morris

Description

INNOVATIONS IN GLOBAL

CONNECTIONS

PRIVATE EQUITY

IN THE MIDDLE MARKET

SPRING 2016

SOVEREIGN WEALTH

FUNDS LIKE WHAT

THEY SEE IN U.S.

MIDDLE MARKET

BRITISH

COLUMBIA

INVESTMENT

MANAGEMENT

COMPANY

TEXAS

PERMANENT

SCHOOL

FUND STATE

BOARD OF

EDUCATION

CANADA

PENSION

PLAN

INVESTMENT

BOARD

LIBYAN

INVESTMENT

AUTHORITY

ABU DHABI

INVESTMENT

AUTHORITY

ALSO INSIDE!

CHINA

INVESTMENT

JAPAN'S

CORP

GOVERNMENT

PENSION

INVESTMENT

FUND

TEMASEK

HOLDINGS

Six tips when raising

money from SWFs

Medical outsourcing

draws fresh wave of sponsors

Valuations remain high

as the year begins

INNOVATIONS IN GLOBAL

PRIVATE EQUITY

www.duanemorris.com

Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Los Angeles | Chicago | Houston | Hanoi | Philadelphia

San Diego | San Francisco | Silicon Valley | Oman | Baltimore | Boston | Washington, D.C. | Las Vegas | Atlanta | Miami | Pittsburgh | Newark

Boca Raton | Wilmington | Cherry Hill | Lake Tahoe | Myanmar | Ho Chi Minh City | Duane Morris LLP – A Delaware limited liability partnership

Exclusive surveys on deal

pricing and leverage multiples

AUSTRALIAN

GOVERNMENT

FUTURE FUND

. INNOVATIONS IN GLOBAL

CONNECTIONS

PRIVATE EQUITY

IN THE MIDDLE MARKET

Contributor Profiles

David Toll,

executive editor,

MIDDLE

EAST

Paul Centopani,

research editor,

Buyouts Insider

ASIA

Tom Stein,

Contributor,

Buyouts Insider

Buyouts Insider

DAVID TOLL is the executive editor of

Buyouts Insider, where he oversees

the editorial direction of Buyouts

Magazine, Venture Capital Journal

and the peHUB.com community

website. David has been writing

about the private equity markets

since 1997, and publishes a biweekly column in Buyouts Magazine.

He is the co-author of several

survey-based studies on the private

equity and venture capital markets,

covering such topics as partnership

terms and employee compensation.

He is the chief cartoonist at

privateequitycartoon.com.

TOM STEIN provides a range of

editorial and marketing services

to corporate

clients, including

Yahoo!, Facebook, Sony, Oracle,

Saatchi & Saatchi, Marvell, Microsoft

and PayPal. His services include

contributed articles, newsletters,

white papers, website copy, social

media content, and speeches. He

has contributed to leading business

and general interest publications

including Buyouts Magazine, Wired

Magazine, Forbes, Tennis Magazine,

and

Venture

Capital

Journal.

Previously, Tom was a senior editor

at Red Herring, a magazine where

he covered start-ups and venture

capital.

He also worked as a staff writer at the San Francisco Chronicle, where he covered the tech industry. Additionally, Tom served as a senior editor at InformationWeek and Success Magazine. PAUL CENTOPANI is a writer and developer of media and editorial in print, online and presentation formats for Buyouts Insider. His work centers on plumbing the private equity industry for trends and ideas that can be turned into thoughtprovoking, high-quality content. His stories have been regularly featured in Buyouts Magazine, Venture Capital Journal and the peHUB. com community website.

Earlier in his career Paul was a pricing analyst and senior consultant for defense contractor Booz Allen Hamilton. There he managed more than 600 proposals representing nearly $900 million in value. . TABLE OF CONTENTS 2 A LETTER TO OUR READERS By David Toll, Richard Jaffe, Pierfrancesco Carbone 4 MEDICAL OUTSOURCING DRAWS FRESH WAVE OF SPONSORS By Tom Stein and David Toll 6,11 Market Intelligence: Notable fundraises, largest healthcare deals, and largest exits 8 13 16 Expert insights: How important are leverage, size and growth to navigating the healthcare market? At a glance: Notable sponsor-backed MSO and other outsourced service providers VALUATIONS REMAIN HIGH AS YEAR BEGINS By David Toll 16 16 18 Exclusive I-bank Survey: Year-end deal pricing and leverage multiples Exclusive Market Survey: Where are deal prices and credit markets heading? SOVEREIGN WEALTH FUNDS LIKE WHAT THEY SEE IN U.S. MIDDLE MARKET By David Toll 20 26 27 At a glance: Select SWFs and their private equity programs Actionable advice: Six tips when raising money from SWFs Market Intelligence: Alaska Permanent Fund Corp’s PE Performance 30 ABOUT DUANE MORRIS 32 ABOUT BUYOUTS INSIDER Executive Editor, David Toll (dtoll@buyoutsinsider.com/646-356-4507) Editorial Advisor, Richard P. Jaffe (RPJaffe@duanemorris.com/215-979-1935) Research Editor, Paul Centopani (pcentopani@buyoutsinsider.com/646-356-4506) Editor-in-Chief, Lawrence Aragon Contributor, Tom Stein Creative Director, Janet Yuen-Paldino Junior Graphic Designer, Allison Brown Sales Director: Robert Raidt (rraidt@buyoutsinsider.com/646-356-4502) Sales Associate: Kelley King (kking@buyoutsinsider.com/646-356-4504) Publisher: Jim Beecher (jbeecher@buyoutsinsider.com/646-356-4501) Connections in the Middle Market 1 . A LETTER TO OUR READERS I t’s easy to get caught up in the latest woe-is-me news headlines, whether about the slowing economy in China, flagging public equity valuations, or the chilled credit markets. But behind the scenes mid-market buyout firms are quietly going about their business of refilling their war chests, deploying capital, and borrowing money. Our latest edition of Connections in the Middle Market, the second off-spring of a partnership between publisher Buyouts Insider and global law firm Duane Morris, is dedicated to helping midmarket sponsors better navigate those basic tasks. You could be forgiven for thinking that landing a sovereign wealth fund as a limited partner was out of reach or not practical. Aren’t these behemoths too large to make a commitment to a fund of just a few hundred million dollars? One of two feature stories in this issue debunks the myth that SWFs don’t back small funds. They may be big, but they’re finding a way into the U.S.

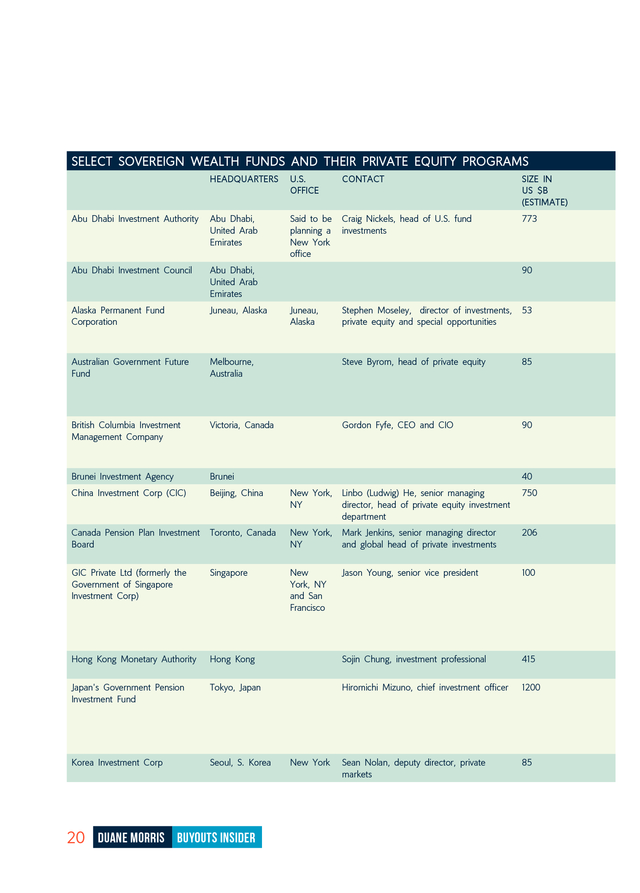

middle market, such as through custom managedaccount assignments. The list of mid-market firms that have secured backing from SWFs is large and growing. It includes the likes of Frazier Healthcare Partners, H.I.G. Capital, TA Associates and TorQuest Partners. No fewer than 25 SWFs have a known appetite for private equity— each briefly profiled on pp 20-23.

Together they manage more than $6 trillion. But raising money is only half the battle for mid-market sponsors, of course. And that fact inspired our second feature story, which describes one of the hottest trends in one of the hottest deal markets, healthcare. An estimated $3 trillion is spent in the United States on healthcare each year. When you consider that seven in 10 U.S.

healthcare companies outsource a portion of their work, you can appreciate the size of the opportunity in such fields as billing and temporary staffing. Our feature points to the latest and most fascinating opportunities emerging in healthcare outsourcing. You’ll learn about a company that provides patients with video-based interpretation services (InDemand Interpreting, backed by Health Enterprise Partners); one that supplies nurses from the Philippines to chronically understaffed hospitals in the United States (HCCA, backed by MTS Health Investors); and another that supplies hospitals with surgical equipment and personnel (Surgical Solutions, backed by Sterling Partners). A handy table shows you where some of the top healthcare-focused firms stand in their latest fundraises (p. 6). Meantime, this issue of Connections in the Middle Market marks the second time that we’re tracking pricing and leverage multiples via proprietary surveys of deal professionals. The bottom line? The frothy times are over in the credit markets, but relief may be in sight when it comes to deal pricing. A survey of some 60 deal professionals and investors conducted by Buyouts Insider in December and early January found more than four in 10 (44 percent) predicting the debt markets would be creditor-friendly over the next 12 months (see chart, p.

17). Just one in 2 DUANE MORRIS Buyouts Insider . four (24 percent) predicted that they would be borrower-friendly and one in three (32 percent) predicted they would be balanced. By comparison, three-quarters (76 percent) of respondents described the credit markets over the past 12 months as “borrower-friendly.” Just 5 percent described them as “creditorfriendly,” while the rest (19 percent) described them as “balanced.” The good news for sponsors: Given their expected turnabout in the credit markets, not many survey respondents believed that deal prices would be heading higher. Nearly a third of respondents (30 percent) predicted that prices would fall in the North American middle market over the next 18 months. Another 50 percent of respondents saw level prices ahead. Just one in five (20 percent) predicted prices would be heading higher. And just where are prices? A separate, informal survey of six investment banks conducted by Buyouts Insider at year-end found a median enterprise value-to-EBITDA multiple of 9.8x for North American companies generating more than $25 million in EBITDA, and 8.5x for companies generating less than that (see chart, p 16). Survey participants included Carl Marks Advisors, Duff & Phelps, Harris Williams, Lincoln International, Raymond James and Stifel Investment Banking. ACTION ITEM: Investment bank Make sure to send any comments or Robert W.

Baird & Co puts together suggestions on this edition of Connections in an excellent monthly report on M&A the Middle Market to dtoll@buyoutsinsider. pricing. www.rwbaird.com com or rpjaffe@duanemorris.com. David Toll Executive Editor Buyouts Insider Richard Jaffe Partner and Co-head of Private Equity – U.S. Duane Morris Pierfrancesco Carbone Partner and Co-head of Private Equity – UK / Europe Duane Morris Connections in the Middle Market 3 . ©iStock/xijian MEDICAL OUTSOURCING DRAWS FRESH WAVE OF SPONSORS BY TOM STEIN AND DAVID TOLL Companies that provide outsourced services to hospitals, clinics, and physician networks represent one of the hottest segments in healthcare—and a new crop of sponsors is trying to cash in. A ll told about seven in 10 U.S. healthcare companies outsource a portion of their work, according to recent estimates by IndustryArc, a market research firm. Just the U.S. healthcare business process outsourcing market, which encompasses claims processing, medical billing, and human resources, is projected to be worth $141.7 billion by 2018, according to market research firm MarketsandMarkets. A number of factors are driving the medical outsourcing trend, including the rapidly rising cost of healthcare, a shortage of well-trained staff in many areas, and an upwelling of new compliance requirements. Traditionally, hospitals and other healthcare providers limited the services they were willing to outsource to back-office functions like claims processing and medical billing. 4 DUANE MORRIS Buyouts Insider .

No longer. Under pressure to provide better shop for everything from surgery to custodial care at lower cost, hospitals are delving deeper services to food is no longer viable,” said Ezra into outsourced services in areas such as Mehlman, vice president at private equity surgical solutions, patient translation services, shop Health Enterprise Partners. Mehlman and even off-shore nursing services. Savvy recently led his firm’s investment in InDemand private equity firms have spotted this trend Interpreting, and are ramping up deal making in medical interpretation services.

“When you have an outsourcing companies, including healthcare industry that is in transformation, and you have MSOs (management services organizations), hospitals operating on single-digit operating which are typically jointly owned by the margins, MSOs will inevitably emerge to help physicians themselves. them survive in this environment.” “The old mode of doing business where a hospital functions as a complete one-stop shop for everything from surgery to custodial services to food is no longer viable.” HOSPITALS COMBINE FORCES —Ezra Mehlman, VP, Health Enterprise Partners trend. Hospitals in the United States are now a provider of video-based Further fuelling the outsourcing trend is the frenzy of M&A activity among acute care hospitals. As hospital systems combine, they often take the opportunity to evaluate what services need to stay in-house and which can be outsourced at a lower cost. InDemand Interpreting has benefited from the mandated to provide translation services for the growing number of patients who don’t speak English or at least not well.

Most hospitals do so Connections in the Middle Market has identified at least 11 growth equity and buyout through hiring their own in-person interpreters, or offering over-the-phone interpreting. transactions in the medical outsourcing market since late 2014, sponsored by such firms as InDemand provides this service via video, which Clearview Capital, MTS Health Investors and Mehlman says is more patient-friendly than Sterling Partners (see p. 11 table). over-the-phone interpreting. It is also promoted as lower cost and more convenient than hiring “The old mode of doing business where a an in-person interpreter.

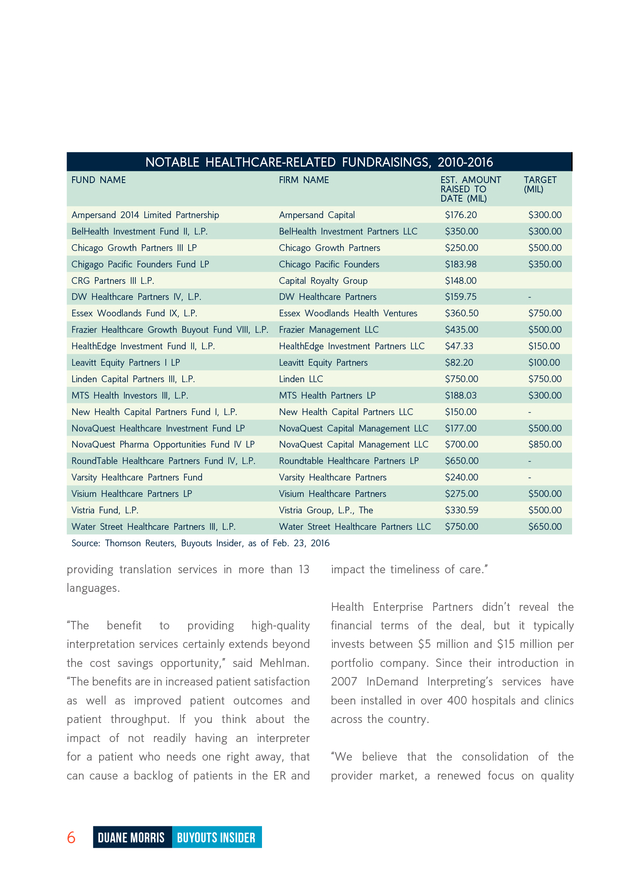

InDemand interpreters hospital functions as a complete one-stop are at the ready 24/7 in a matter of seconds, Connections in the Middle Market 5 . NOTABLE HEALTHCARE-RELATED FUNDRAISINGS, 2010-2016 FUND NAME FIRM NAME EST. AMOUNT RAISED TO DATE (MIL) Ampersand 2014 Limited Partnership Ampersand Capital $176.20 TARGET (MIL) $300.00 BelHealth Investment Fund II, L.P. BelHealth Investment Partners LLC $350.00 $300.00 Chicago Growth Partners III LP Chicago Growth Partners $250.00 $500.00 $350.00 Chigago Pacific Founders Fund LP Chicago Pacific Founders $183.98 CRG Partners III L.P. Capital Royalty Group $148.00 DW Healthcare Partners IV, L.P. DW Healthcare Partners $159.75 - Essex Woodlands Fund IX, L.P. Essex Woodlands Health Ventures $360.50 $750.00 Frazier Healthcare Growth Buyout Fund VIII, L.P. Frazier Management LLC $435.00 $500.00 HealthEdge Investment Fund II, L.P. HealthEdge Investment Partners LLC $47.33 $150.00 Leavitt Equity Partners I LP Leavitt Equity Partners $82.20 $100.00 Linden Capital Partners III, L.P. Linden LLC $750.00 $750.00 MTS Health Investors III, L.P. MTS Health Partners LP $188.03 $300.00 New Health Capital Partners Fund I, L.P. New Health Capital Partners LLC $150.00 - NovaQuest Healthcare Investment Fund LP NovaQuest Capital Management LLC $177.00 $500.00 NovaQuest Pharma Opportunities Fund IV LP NovaQuest Capital Management LLC $700.00 $850.00 RoundTable Healthcare Partners Fund IV, L.P. Roundtable Healthcare Partners LP $650.00 - Varsity Healthcare Partners Fund Varsity Healthcare Partners $240.00 - Visium Healthcare Partners LP Visium Healthcare Partners $275.00 $500.00 Vistria Fund, L.P. Vistria Group, L.P., The $330.59 $500.00 Water Street Healthcare Partners III, L.P. Water Street Healthcare Partners LLC $750.00 $650.00 Source: Thomson Reuters, Buyouts Insider, as of Feb. 23, 2016 providing translation services in more than 13 impact the timeliness of care.” languages. Health Enterprise Partners didn’t reveal the “The benefit to providing high-quality financial terms of the deal, but it typically interpretation services certainly extends beyond invests between $5 million and $15 million per the cost savings opportunity,” said Mehlman. portfolio company. Since their introduction in “The benefits are in increased patient satisfaction 2007 InDemand Interpreting’s services have as well as improved patient outcomes and been installed in over 400 hospitals and clinics patient throughput.

If you think about the across the country. impact of not readily having an interpreter for a patient who needs one right away, that “We believe that the consolidation of the can cause a backlog of patients in the ER and provider market, a renewed focus on quality 6 DUANE MORRIS Buyouts Insider . and patient-centric care, coupled with the “Efficiencies in the marketplace shifting demographics of the U.S., have created necessarily being a perfect storm for InDemand,” said Mehlman. healthcare organizations,” Moses said. “More “We look forward to continuing to expand our frequently, innovative models of service are customer base and solidifying our relationship being born in smaller companies that are then with trusted partners.” bringing those services on an outsourced basis born inside aren’t the large to the large payers and large provider groups. As for challenges, Mehlman said that providing At MTS, we look for those companies with high-quality outsourced services requires superb innovative models.” operational talent and a lot of attention to detail. He added that it is still tough for many hospital systems to wrap their heads around outsourced services, especially non-traditional services. “Selling the hospital on the value proposition of an outsourced service that it is evaluating for the first time can be difficult,” he said. “Whenever you are selling something that used to be in-sourced, there is an organizational change component that’s involved, which can be hard to overcome. What’s more, selling to a hospital is different from selling to, say, a large corporation because the sales cycles are much longer in the medical world.” Healthcare groups, he added, are increasingly willing to approaches lean that on can outsiders help with them novel improve “The larger provider systems and payers have over time developed cultures that are more embracing of the idea that everything doesn’t have to be built and managed in-house.” —Oliver Moses, senior managing director, MTS Health Investors GROWING RELEVANCE For Oliver Moses, a senior managing director their core competencies and become more at private equity shop MTS Health Investors, efficient—especially if they can do it at a lower the attraction of medical outsourcing is clear. cost.

“The large provider systems and payers Because of consolidation in the market and the have over time developed cultures that are need to reduce overhead, outsourcing will only more embracing of the idea that everything grow in relevance. doesn’t have to be built and managed in- Connections in the Middle Market 7 . How important are leverage, size and growth to navigating the health care market? Below are excerpts on this question from panelists speaking at an ACG New York-hosted healthcare conference at the Metropolitan Club in New York City on February 25, 2016. RUSTY HOLMAN, CHIEF MEDICAL OFFICER, JOSEPH BERARDO, CEO, MAGNACARE: We’re at We feel that consolidation is about 1,000 physicians, up from four about two years going to be an ongoing theme, and leverage, size ago as we bring on a lot of small practices. Our is a and growth are what independent systems and well-baked platform that generally allows physicians hospitals that we acquire or partner with are looking to stay independent and be part of something for. They may not be in financial distress as they bigger and still be compensated on a production were several years ago. But long-term they know basis versus having things dictated down from an that they’re not going to be successful without a owner, as they might have happen in a hospital. partner that can achieve scale.

Some of the hospitals What’s interesting about scale is that we’re trying to we acquire may have a higher degree of evolution in get to a place where we can manage populations terms of a given model or a given asset, whether it’s and change the reimbursement. So we have to get a business office, whether it’s a clinically-integrated to scale to be able to do that. But unfortunately network, whether it’s IT infrastructure and data we’ve got legislators that complain that in doing so analytics that can then be expanded and leveraged we’re narrowing the network and that’s not good for throughout several other regions.

So with growth the consumer. So we’re going to go through this comes unique assets that can then be leveraged into uncomfortable period where scale is important but LIFEPOINT HEALTH: a variety of different settings. JEFF LEBENGER, CEO, SUMMIT MEDICAL GROUP: Scale is very important to us. We’ve almost tripled in size in the last two or three years.

We grew from 200 to 600 physicians. When you scale and bring in new physician groups you’re introducing processes that you have to be certain are correct scale will be different in almost every micro-network and could literally be different county by county. GUY SANSONE, CHAIRMAN-HEALTH CARE GROUP, ALVAREZ & MARSAL: It’s clear that whether you’re a national player or in a regional physician practice or semi-regional health plan, healthcare is still local. The goal is to understand the local population. and accurate. It’s very costly to scale.

Under one of RUSTY HOLMAN: Across all of our communities only the shared savings contracts that we have, we need about one-third of our physicians are employed by to introduce new processes when we grow into a us. Two-thirds are independent physicians. We’re different region, whether that’s setting up urgent agnostic to the employment model. care or care management.

When the new doctors seeking the best partners in terms of willingness to aren’t used to your processes, you will lose at first. drive toward common quality goals and those that It’s a huge cost when they don’t understand your are embracing that as both a platform for improved processes. But eventually, if you can export your utilization and improved outcomes. When new way of practice to a region, you will reap the benefit. reimbursement models emerge, we’ll be prepared. 8 8 DUANE MORRIS Buyouts Insider DUANE MORRIS Buyouts Insider We’re really .

Jeff LeBenger, CEO, Summit Medical Group, a physician-owned medical group; Rusty Holman, chief medical officer, LifePoint Health, provider of healthcare services through 72 hospitals in 22 states, mainly in rural areas and small towns; Joseph Berardo, CEO, Magnacare, provider of healthcare plans in New York and New Jersey; Bill Abrams, president of distributed products division of Medline Industries, a family-owned supplier of hospital supplies and pharmaceutical products; Not pictured: Moderator Guy Sansone, chairman of healthcare group, consulting firm Alvarez & Marsal, and CEO of the Visiting Nurse Service of New York BILL ABRAMS, PRESIDENT-DISTRIBUTION PRODUCTS, RUSTY HOLMAN: I just came from a national MEDLINE INDUSTRIES: There’s no question that systems are getting larger. You can have a debate today about whether there’s going to be 1,000 systems that will ultimately control healthcare or 150. But as these systems aggregate we’re seeing two impacts. One is that healthcare providers are asking us for way more.

They’re asking for more services, for products that do more for them, that create better outcomes. They’re also doing way more data mining than they’ve ever done before. In many ways it doesn’t take away from the judgment of the individual physician, but it gives them way more information.

They can look at how many hips were replaced in a particular system, at what were the outcomes. They are then looking into the care protocols that produced those outcomes and trying to figure out what was changed and if there’s any correlation. That’s something you really need scale to do, in order to have the patient population to study, and you need scale to have the data analytics work. cardiovascular physician council that we convened from all of our communities nationally.

We came together to talk about pharmaceuticals, about devices, about core practices, about a variety of functions. There was a lot of focus on preference items and the huge variations that exist today in terms of pharmaceutical usage that has no basis in the evidence. Same with the use of devices, stents and a variety of other products.

We get groups of specialists in a room and put the issues on the table and encourage decisions based on efficacy, safety and then cost. If the first two are equal, then we look at the cost equation. The light bulbs go off like crazy because physicians have traditionally been insulated from the cost equation.

Engaging physicians in forums like that has been a game changer for us and for others in terms of managing those costs. Edited for clarity Connections in the Middle Market 9 . house,” said Moses. “And as they are forced HCCA’s recruiting top nurses and health care to become more efficient and reduce waste, professionals from around the world. they no longer feel they need to do everything themselves.” MTS Health Investors specializes in middlemarket buyouts, investing anywhere from $15 MTS Health Investors’s most recent investment million to $75 million per transaction, and involves HCCA, a company that provides U.S. HCCA fit that range, said Moses. The 43-year- hospitals with nurses from the Philippines old company employs over 1,500 people in and offers a range of clinical services on Nashville and the Philippines. an outsourced basis. The United States is “The large healthcare institutions have to become efficient to survive...” —Oliver Moses, senior managing director, MTS Health Investors Looking ahead, MTS Health Investors plans to support the company’s growth through new customer introductions and the evaluation of potential acquisitions.

The firm also intends to work with management to evaluate new service offerings and new geographies in which to expand. “The large healthcare institutions have to become efficient to survive, and they have to experiencing a chronic shortage of nurses, look to outsourcing as part of that efficiency,” while the Philippines enjoys a surplus. HCCA said Moses. “Outsourcers are proving that they helps these nurses get U.S.

accreditation and have more expertise in controlling medical costs them brings them over to work at hospitals and delivering administrative processes more here. cheaply. As a result, there is more opportunity It starts as a staffing relationship, but many hospitals end up hiring those nurses. for PE firms like us to find these assets and help them scale.” HCCA also has a team of nurses stationed in the Philippines who assist clients with clinical tasks, ‘CONCIERGE’ MEDICINE such as reviewing medical charts or identifying It is not just large hospital systems that are potential gaps in care. The benefit, said Moses, feeling the heat.

Doctor practices are also is that costs are significantly reduced due to under pressure. faster turnaround times and increased quality of service. Improved patient care results from 10 DUANE MORRIS Buyouts Insider That’s why private equity shop Shore Capital . LARGEST U.S.-SPONSOR-BACKED HEALTHCARE DEALS, 2010-2016 RANK DATE EFFECTIVE TARGET NAME DEAL VALUE ($MIL) INDUSTRY SPONSOR 1 06/30/2014 Ortho-Clinical Diagnostics Inc 4,000.00 Healthcare Equipment & Supplies The Carlyle Group LP 2 10/01/2010 NBTY Inc 3,779.43 Pharmaceuticals The Carlyle Group LP 3 12/05/2011 Pharmaceutical Product Development Inc 3,386.97 Biotechnology Pharm Product Dvlp Inc SPV 4 08/26/2010 MultiPlan Inc 3,100.00 Healthcare Providers & Services (HMOs) MultiPlan Inc SPV 5 05/25/2011 Emergency Medical Services Corp 2,923.20 Healthcare Providers & Services (HMOs) Clayton Dubilier & Rice LLC 6 08/01/2011 Capsugel 2,375.00 Pharmaceuticals KKR & Co LP 7 09/27/2010 Healthscope Ltd 2,348.08 Hospitals The Carlyle Group LP 8 09/28/2012 Par Pharmaceutical Cos Inc 1,961.54 Pharmaceuticals TPG Capital LP 9 03/31/2014 Panasonic Healthcare Co Ltd 1,679.54 Healthcare Equipment & Supplies KKR & Co LP Source: Thomson Reuters LARGEST U.S.-SPONSOR-BACKED HEALTHCARE EXITS, 2010-2016 RANK DATE EFFECTIVE SELLER COMPANY INDUSTRY VALUE ($MIL) ACQUIRER 1 08/06/2013 Warburg Pincus LLC Bausch & Lomb Inc Measuring, Medical, Photo Equipment; Clocks 11,647.50 Valeant Pharmaceuticals International Inc 2 04/08/2011 The Carlyle Group LP HCR ManorCare IncReal Estate Assets Health Services 6,079.65 HCP Inc 3 08/26/2010 The Carlyle Group LP MultiPlan Inc Insurance 3,100.00 MultiPlan Inc SPV 4 02/03/2014 TPG Capital LP Aptalis Pharma Inc Drugs 2,900.00 Forest Laboratories Inc 5 06/20/2011 Warburg Pincus LLC American Medical Systems Holdings Inc Measuring, Medical, Photo Equipment; Clocks 2,519.57 NIKA Merger Sub Inc 6 07/16/2014 Hellman & Friedman LLC Sheridan Healthcare Inc Health Services 2,343.96 AmSurg Corp 7 04/16/2015 Madison Dearborn Partners LLC Ikaria Inc Drugs 2,300.00 Mallinckrodt PLC 8 02/16/2016 Advent International Corp Priory Group Ltd Health Services 2,213.24 Acadia Healthcare Co Inc Source: Thomson Reuters Connections in the Middle Market 11 . recently invested in Specialdocs, a provider not 3,000. That means they can spend quality of time with each of their patients and ultimately consulting services to U.S. physicians transitioning from traditional medical practices provide better care.” to independent, personalized medicine models, also known as “concierge” medicine. But making that transition to a concierge practice can be nerve-wracking. So doctors are Doctors have to deal with an increasingly turning to specialists like Specialdocs. “Making complicated reimbursement environment, which that switch is a life-changing event for these leads to rising overhead costs.

They are also doctors,” said Cooper. “It is a seminal moment under strain from the prevalent fee-for-service in their careers. It’s like having a wedding and model that places more emphasis on seeing as worrying that no one is going to show up.

Most doctors don’t have the expertise, time or energy “Most doctors would tell you a lot can slip through the cracks because they are under such a huge time constraint when they are meeting with patients.” to go through that process on their own.” —Mike Cooper, partner, Shore Capital Once the new concierge practice is established, Specialdocs handles marketing, communicating with potential patients and explaining the benefits of concierge medicine. As part of that effort the company operates a patient information hotline and website staffed by marketing experts. Specialdocs stays on to perform services like billing and collection of annual retainer fees. It also continues to handle marketing, such as many patients as possible than on the quality of sending out holiday cards and flu shot reminders care. In fact, the average primary care visit in to patients, publishing quarterly newsletters, and the United States lasts just seven minutes. conducting patient satisfaction surveys.

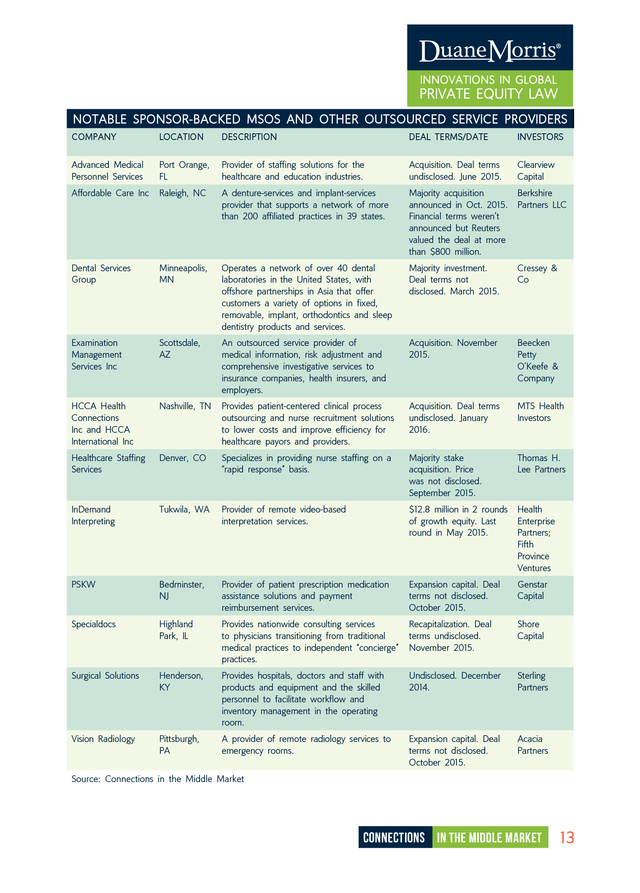

It holds networking events for concierge physicians to “Most doctors would tell you a lot can slip meet and discuss what’s working for them. through the cracks because they are under such a huge time constraint when they are meeting Shore Capital typically invests in companies with patients,” said Mike Cooper, a partner at with $5 million to $50 million in revenue, Shore Capital. “By contrast, in the concierge and the Specialdocs deal was in that range. model, a typical doctor has 300 total patients, Part of the money will go to help Specialdocs 12 DUANE MORRIS Buyouts Insider . NOTABLE SPONSOR-BACKED MSOS AND OTHER OUTSOURCED SERVICE PROVIDERS COMPANY LOCATION DESCRIPTION DEAL TERMS/DATE INVESTORS Advanced Medical Personnel Services Port Orange, FL Provider of staffing solutions for the healthcare and education industries. Acquisition. Deal terms undisclosed. June 2015. Clearview Capital Affordable Care Inc Raleigh, NC A denture-services and implant-services provider that supports a network of more than 200 affiliated practices in 39 states. Majority acquisition announced in Oct. 2015. Financial terms weren’t announced but Reuters valued the deal at more than $800 million. Berkshire Partners LLC Dental Services Group Minneapolis, MN Operates a network of over 40 dental laboratories in the United States, with offshore partnerships in Asia that offer customers a variety of options in fixed, removable, implant, orthodontics and sleep dentistry products and services. Majority investment. Deal terms not disclosed.

March 2015. Cressey & Co Examination Management Services Inc Scottsdale, AZ An outsourced service provider of medical information, risk adjustment and comprehensive investigative services to insurance companies, health insurers, and employers. Acquisition. November 2015. Beecken Petty O’Keefe & Company HCCA Health Connections Inc and HCCA International Inc Nashville, TN Provides patient-centered clinical process outsourcing and nurse recruitment solutions to lower costs and improve efficiency for healthcare payors and providers. Acquisition. Deal terms undisclosed.

January 2016. MTS Health Investors Healthcare Staffing Services Denver, CO Specializes in providing nurse staffing on a “rapid response” basis. Majority stake acquisition. Price was not disclosed. September 2015. Thomas H. Lee Partners InDemand Interpreting Tukwila, WA Provider of remote video-based interpretation services. $12.8 million in 2 rounds of growth equity. Last round in May 2015. Health Enterprise Partners; Fifth Province Ventures PSKW Bedminster, NJ Provider of patient prescription medication assistance solutions and payment reimbursement services. Expansion capital.

Deal terms not disclosed. October 2015. Genstar Capital Specialdocs Highland Park, IL Provides nationwide consulting services to physicians transitioning from traditional medical practices to independent “concierge” practices. Recapitalization. Deal terms undisclosed. November 2015. Shore Capital Surgical Solutions Henderson, KY Provides hospitals, doctors and staff with products and equipment and the skilled personnel to facilitate workflow and inventory management in the operating room. Undisclosed. December 2014. Sterling Partners Vision Radiology Pittsburgh, PA A provider of remote radiology services to emergency rooms. Expansion capital.

Deal terms not disclosed. October 2015. Acacia Partners Source: Connections in the Middle Market Connections in the Middle Market 13 . develop infrastructure to take a more aggressive surgical equipment so hospitals don’t have to approach toward reaching physicians who are make large up-front investments. And it also contemplating the concierge medicine model. provides 24/7 on-site clinical technicians. “Concierge medicine is a multi-billion dollar While Moffat wouldn’t disclose financial details industry. We feel like we are still scratching surrounding this deal, she said that Sterling the tip of the iceberg in terms of the number Partners of physicians that are converting,” said Cooper. investments ranging from $40 million to $200 “There is still a lot of white space for companies million. Surgical Solutions has a national footprint that want to serve this market.” with several hundred employees serving large typically targets majority equity and small, urban and rural hospitals and hospital SURGICAL SERVICES systems.

Sterling Partners plans to partner with Kim Vender Moffat, a principal at Sterling management and augment Surgical Solutions’s Partners, notes that, even though the medical infrastructure to support growth in number of outsourcing market has existed for decades, it services offered and regions served. has really gained steam over the last five or six years, with a lot of mutual success for both Investors like Moffat are encouraged by the fact healthcare providers and the outsourcers. that their medical outsourcing investments have a clear path to exit. She said these are businesses “Many large healthcare [providers] are ramping with many logical buyers, including other private up their outsourcing efforts as the number of equity firms, as well as strategic buyers that are companies offering new services proliferates,” building up a full suite of outsourcing services she said. “Overall, hospitals are seeing results and are looking for additional offerings. both in terms of improved quality and lower costs.

That success is helping to fuel even more “This is an opportunity that is far from exhausted,” activity in the space.” said Moffat. “There is an ever expanding and ever evolving universe of outsourced services Sterling Partners recently invested in Surgical for the healthcare market. We expect to see Solutions, an outsourced provider of equipment robust activity in this space for years to come.” and personnel.

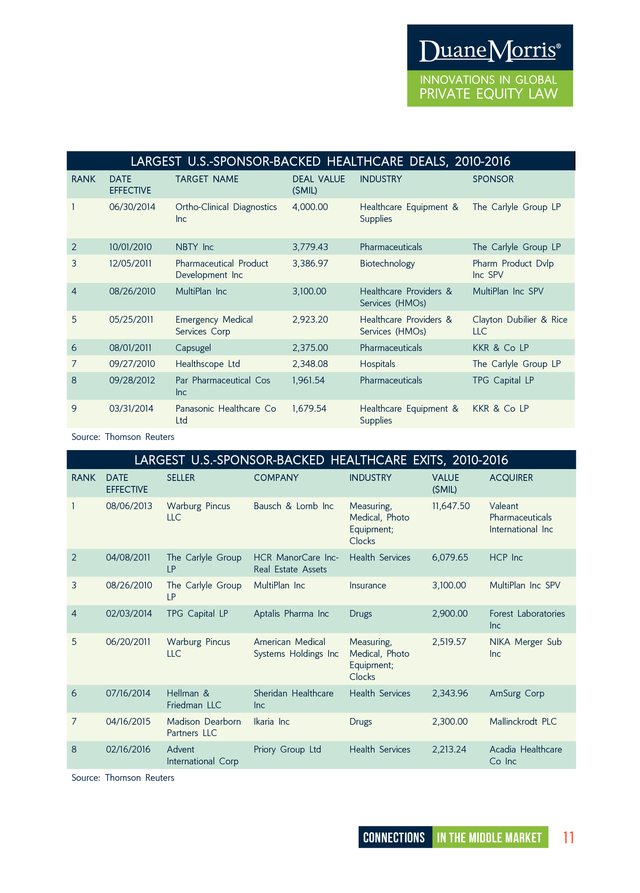

Founded in 2007, the company aims to make operating rooms run more efficiently and cost-effectively by taking on administrative tasks associated with laparoscopic and endoscopic surgery. It provides its own 14 DUANE MORRIS Buyouts Insider ACTION ITEM: Find a number of medical market intelligence reports available for sale at industryarc.com . 2016 REGISTER NOW PARTNERCONNECT MIDWEST JUNE 21-22, 2016 • THE WESTIN MICHIGAN AVENUE, CHICAGO, IL Expand Your Network, Supercharge Your Strategy, and Get Deals Done Whether you’re focused on fundraising or just looking to learn more about the trends shaping your business, the 9th Annual Buyouts Chicago conference is guaranteed to help you profit in 2016. You’ll meet more than 400 professionals at the region’s biggest PE event of the year for senior decision-makers. NEW THIS YEAR: We’re adding two new sessions for our attendees, based on their feedback: The Two-Part LP Symposium, which includes 5 panels on topics like Separate Accounts, Portfolio Management and more. We’re also adding The IR Bootcamp, an afternoon session which will drill in on the capital raising needs and best practices of fundraising GPs. Plus GPs can customize their networking opportunities with LPs by participating in our exclusive ExecConnect private meeting program: pre-arranged 1:1 meetings with LPs with mutual investment goals. Enrollment for ExecConnect is included with all GP tickets; and with more than 150 LPs attending, you’re sure to meet new investors eager to put money to work in the asset class. partnerconnectevents.com/partnerconnect-mw-2016 LEARN HOW TO PARTICIPATE AS A SPEAKER OR SPONSOR: Speaking Opportunities Mark Cecil PARTNERSHIP OPPORTUNITIES Bob Raidt 415.794.7045 | mcecil@buyoutsinsider.com 646.356.4502 | rraidt@buyoutsinsider.com .

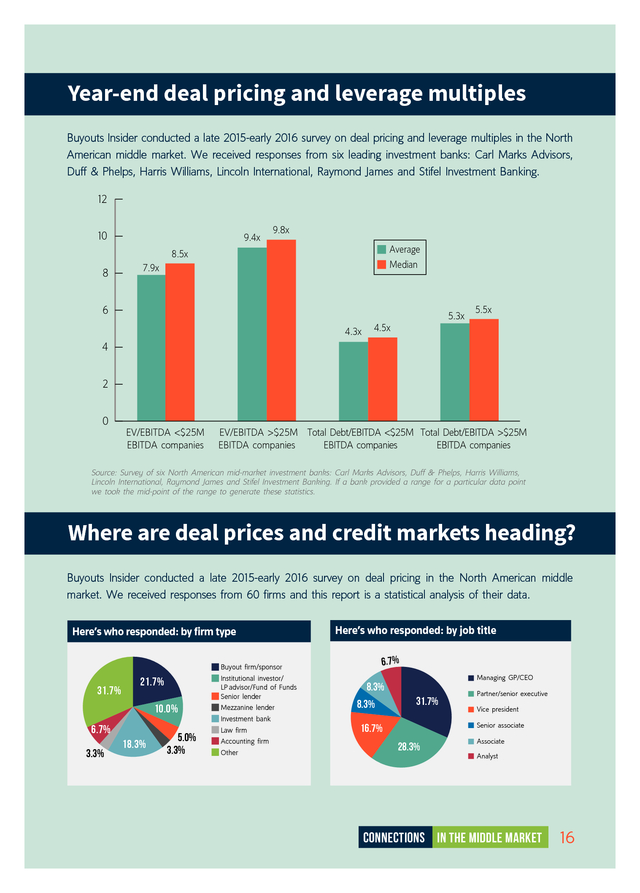

Year-end deal pricing and leverage multiples Buyouts Insider conducted a late 2015-early 2016 survey on deal pricing and leverage multiples in the North American middle market. We received responses from six leading investment banks: Carl Marks Advisors, Duff & Phelps, Harris Williams, Lincoln International, Raymond James and Stifel Investment Banking. 12 10 9.4x 9.8x Average 8.5x 8 Median 7.9x 6 5.3x 4.3x 5.5x 4.5x 4 2 0 EV/EBITDA <$25M EBITDA companies EV/EBITDA >$25M Total Debt/EBITDA <$25M Total Debt/EBITDA >$25M EBITDA companies EBITDA companies EBITDA companies Source: Survey of six North American mid-market investment banks: Carl Marks Advisors, Duff & Phelps, Harris Williams, Lincoln International, Raymond James and Stifel Investment Banking. If a bank provided a range for a particular data point we took the mid-point of the range to generate these statistics. Where are deal prices and credit markets heading? Buyouts Insider conducted a late 2015-early 2016 survey on deal pricing in the North American middle market. We received responses from 60 firms and this report is a statistical analysis of their data. Here’s who responded: by firm type Here’s who responded: by job title 6.7% Buyout firm/sponsor 31.7% Institutional investor/ LP advisor/Fund of Funds Senior lender 21.7% 10.0% Mezzanine lender Investment bank 6.7% 3.3% 18.3% 5.0% 3.3% Law firm Accounting firm Other 16 DUANE MORRIS Buyouts Insider Managing GP/CEO 8.3% 8.3% 31.7% Partner/senior executive Vice president Senior associate 16.7% 28.3% Associate Analyst Connections in the Middle Market 16 .

How would you describe deal pricing in the North American middle market right now? Where do you see prices heading in the North American middle market over the next 18 months? 1.7% 11.7% 10.0% 3.3% 0.0% Bubble territory 20.0% 26.7% High Much higher Higher About the same About average 76.7% What is the biggest factor sustaining prices right now? 50.0% Much lower How would you describe the strength of the credit markets over the past 12 months? 5.2% How do you anticipate the credit markets to be over the next 12 months? Creditor-friendly 76.3% Balanced Top ways sponsors are dealing with high prices (respondents could pick more than one answer) Moving into more regulated industries Creditor-friendly Balanced 44.1% Source: Survey of 60 mid-market investment professionals by Buyouts Insider Seeking investments in out-of-favor industries 27.3% 24.2% Looking for more complicated deals at lower prices 33.3% Stepping up efforts to find proprietary/limited auction deals 51.5% 48.5% Lowering return expectations 17 DUANE MORRIS Buyouts Insider 10% 0% 15.2% 20% Borrower-friendly 36.4% Finding ways to add value, such as through add-ons, to justify prices 23.7% Targeting underperforming companies Waiting for prices to settle down 32.2% 3.0% Connections in the Middle Market 60.% 10.3% Borrower-friendly 50% 25.9% Public equity valuations Supply of companies on the market Prevalence of auctions/lack of proprietary deals Strong performance by target companies 18.6% 5.1% 40% 36.2% 12.1% Sponsors with dry powder to deploy Competition from strategic buyers Borrower-friendly credit markets 30% 5.2% 5.2% Lower Low 17 . ©iStock/sarawuth702 SOVEREIGN WEALTH FUNDS LIKE WHAT THEY SEE IN U.S. MIDDLE MARKET BY DAVID TOLL Sovereign wealth funds manage staggering sums of money. But that doesn’t mean they’re so big they only invest with the likes of Blackstone Group, Carlyle Group and Kohlberg Kravis Roberts & Co. F rom the New Zealand Superannuation Fund to the Saudi Arabia General Organization for Social Insurance, from the Alaska Permanent Fund Corporation to the Abu Dhabi Investment Authority, sovereign wealth funds are channeling money into U.S. mid-market funds. They are also adding to the industry’s shadow-financing pool by making co-investments alongside fund managers.

The lengthy list of mid-market buyout and growth equity sponsors that have raised money from SWFs includes Columbia Capital, Frazier Healthcare Partners, H.I.G. Capital, JMI Equity, Sun Capital and TA Associates. 18 DUANE MORRIS Buyouts Insider . The biggest SWFs—inclined to make $100 After the financial crisis, many SWFs turned million to $200 million commitments or more— their backs on the United States, worried about may largely confine themselves to backing mid- having to endure a lengthy period of turmoil, market funds of at least $1 billion to avoid according to Kelly DePonte, managing director accounting for more than 10 percent of a fund, at placement agency Probitas Partners. Instead according to Justin Garrod, managing partner they moved on to growth opportunities in and co-founder of placement agency Stonington Asia and Latin America. Subsequent economic Capital Advisors. troubles in those markets, combined with a scarcity of experienced managers, convinced But many SWFs also are finding a way to back funds as small as just a few hundred million dollars, often through an intermediary, such as a managed account or funds of funds. Consider that RCP Advisors, the Chicago funds-of-funds manager trained on buyout funds of $200 million to $1 billion, has the $85 billion Australian Government Future Fund as a backer. Peter Petrillo, executive vice president of the “The U.S.

market has a number of experienced investment professionals who have been through investment cycles.” —Kelly DePonte, managing director, Probitas Partners direct equity division of Wafra Investment Advisory Group, which invests money in the U.S. middle market on behalf of several SWFs in Kuwait, called SWFs particularly “sophisticated” them to turn back to the United States. Today they consider investments in the U.S.

middle market “core holdings,” said DePonte. investors. “So they have an understanding that the middle market…is more of an inefficient frontier, One of the biggest attractions is the thirty- and [that by] working with good managers they plus-year history of the asset class. “The U.S. can take advantage of those inefficiencies versus market has a number of experienced investment other asset classes.” professionals who have been through investment cycles,” said DePonte.

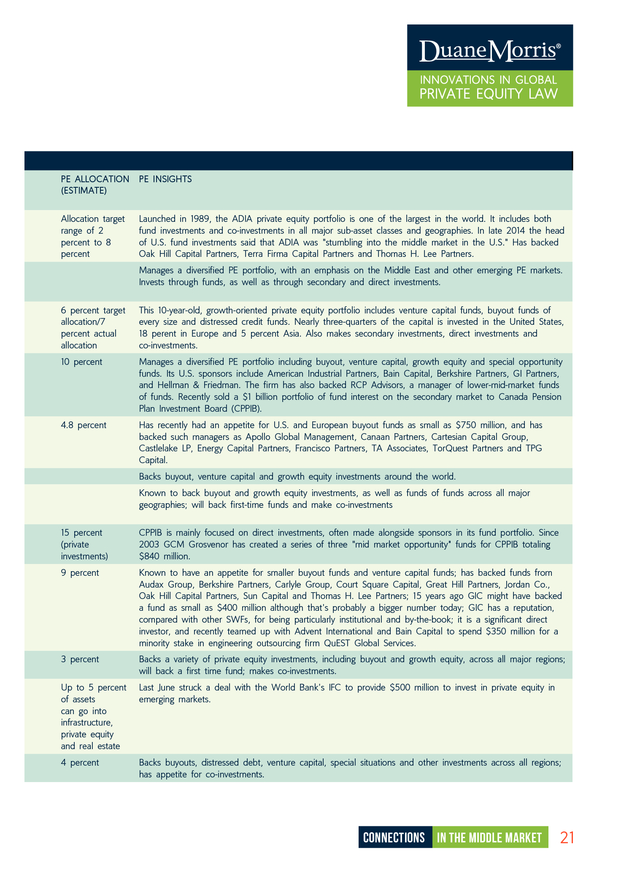

Another is the plethora To be sure, SWFs haven’t always placed their of small and mid-sized companies available to be bets on the U.S. middle market—not a big acquired, improved and sold for a higher price. surprise given that one of the defining features “It’s not a totally shopped market,” DePonte said. of many SWFs is that they try to time markets. “You’re able to buy things at a decent price.” Connections in the Middle Market 19 . SELECT SOVEREIGN WEALTH FUNDS AND THEIR PRIVATE EQUITY PROGRAMS HEADQUARTERS U.S. OFFICE CONTACT SIZE IN US $B (ESTIMATE) Abu Dhabi Investment Authority Abu Dhabi, United Arab Emirates Said to be planning a New York office Craig Nickels, head of U.S. fund investments 773 Abu Dhabi Investment Council Abu Dhabi, United Arab Emirates Alaska Permanent Fund Corporation Juneau, Alaska Australian Government Future Fund 90 Stephen Moseley, director of investments, private equity and special opportunities 53 Melbourne, Australia Steve Byrom, head of private equity 85 British Columbia Investment Management Company Victoria, Canada Gordon Fyfe, CEO and CIO 90 Brunei Investment Agency Brunei China Investment Corp (CIC) Beijing, China New York, NY Linbo (Ludwig) He, senior managing director, head of private equity investment department 750 Canada Pension Plan Investment Board Toronto, Canada New York, NY Mark Jenkins, senior managing director and global head of private investments 206 GIC Private Ltd (formerly the Government of Singapore Investment Corp) Singapore New York, NY and San Francisco Jason Young, senior vice president 100 Hong Kong Monetary Authority Hong Kong Sojin Chung, investment professional 415 Japan's Government Pension Investment Fund Tokyo, Japan Hiromichi Mizuno, chief investment officer 1200 Korea Investment Corp Seoul, S. Korea Sean Nolan, deputy director, private markets 85 20 DUANE MORRIS Buyouts Insider Juneau, Alaska 40 New York . PE ALLOCATION PE INSIGHTS (ESTIMATE) Allocation target range of 2 percent to 8 percent Launched in 1989, the ADIA private equity portfolio is one of the largest in the world. It includes both fund investments and co-investments in all major sub-asset classes and geographies. In late 2014 the head of U.S. fund investments said that ADIA was "stumbling into the middle market in the U.S." Has backed Oak Hill Capital Partners, Terra Firma Capital Partners and Thomas H.

Lee Partners. Manages a diversified PE portfolio, with an emphasis on the Middle East and other emerging PE markets. Invests through funds, as well as through secondary and direct investments. 6 percent target allocation/7 percent actual allocation This 10-year-old, growth-oriented private equity portfolio includes venture capital funds, buyout funds of every size and distressed credit funds. Nearly three-quarters of the capital is invested in the United States, 18 perent in Europe and 5 percent Asia. Also makes secondary investments, direct investments and co-investments. 10 percent Manages a diversified PE portfolio including buyout, venture capital, growth equity and special opportunity funds.

Its U.S. sponsors include American Industrial Partners, Bain Capital, Berkshire Partners, GI Partners, and Hellman & Friedman. The firm has also backed RCP Advisors, a manager of lower-mid-market funds of funds.

Recently sold a $1 billion portfolio of fund interest on the secondary market to Canada Pension Plan Investment Board (CPPIB). 4.8 percent Has recently had an appetite for U.S. and European buyout funds as small as $750 million, and has backed such managers as Apollo Global Management, Canaan Partners, Cartesian Capital Group, Castlelake LP, Energy Capital Partners, Francisco Partners, TA Associates, TorQuest Partners and TPG Capital. Backs buyout, venture capital and growth equity investments around the world. Known to back buyout and growth equity investments, as well as funds of funds across all major geographies; will back first-time funds and make co-investments 15 percent (private investments) CPPIB is mainly focused on direct investments, often made alongside sponsors in its fund portfolio. Since 2003 GCM Grosvenor has created a series of three "mid market opportunity" funds for CPPIB totaling $840 million. 9 percent Known to have an appetite for smaller buyout funds and venture capital funds; has backed funds from Audax Group, Berkshire Partners, Carlyle Group, Court Square Capital, Great Hill Partners, Jordan Co., Oak Hill Capital Partners, Sun Capital and Thomas H.

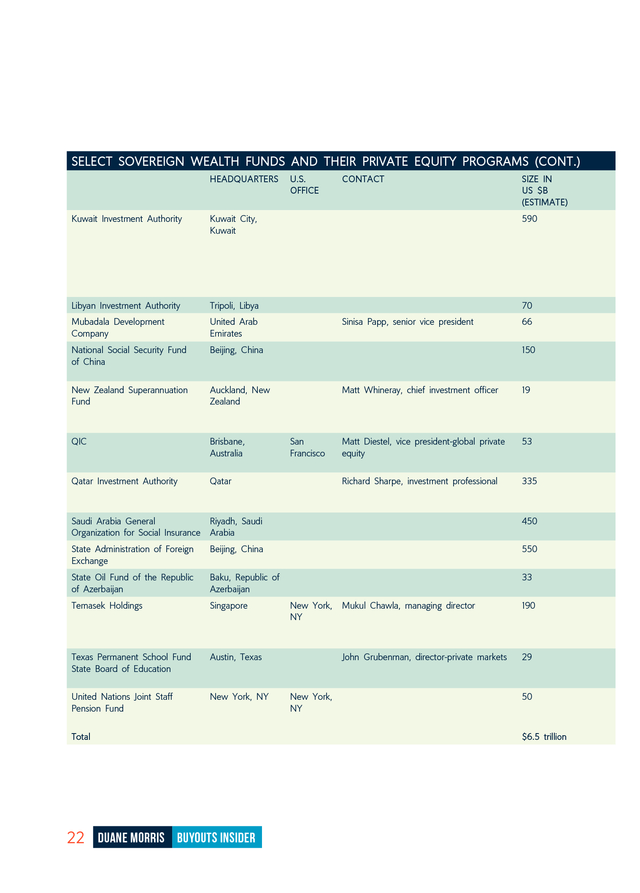

Lee Partners; 15 years ago GIC might have backed a fund as small as $400 million although that's probably a bigger number today; GIC has a reputation, compared with other SWFs, for being particularly institutional and by-the-book; it is a significant direct investor, and recently teamed up with Advent International and Bain Capital to spend $350 million for a minority stake in engineering outsourcing firm QuEST Global Services. 3 percent Backs a variety of private equity investments, including buyout and growth equity, across all major regions; will back a first time fund; makes co-investments. Up to 5 percent of assets can go into infrastructure, private equity and real estate Last June struck a deal with the World Bank's IFC to provide $500 million to invest in private equity in emerging markets. 4 percent Backs buyouts, distressed debt, venture capital, special situations and other investments across all regions; has appetite for co-investments. Connections in the Middle Market 21 . SELECT SOVEREIGN WEALTH FUNDS AND THEIR PRIVATE EQUITY PROGRAMS (CONT.) HEADQUARTERS U.S. OFFICE CONTACT SIZE IN US $B (ESTIMATE) Kuwait Investment Authority Kuwait City, Kuwait 590 Libyan Investment Authority Tripoli, Libya 70 Mubadala Development Company United Arab Emirates National Social Security Fund of China Beijing, China New Zealand Superannuation Fund Auckland, New Zealand QIC Brisbane, Australia Qatar Investment Authority Qatar Sinisa Papp, senior vice president 66 150 Matt Whineray, chief investment officer Matt Diestel, vice president-global private equity 53 Richard Sharpe, investment professional San Francisco 19 335 Saudi Arabia General Riyadh, Saudi Organization for Social Insurance Arabia 450 State Administration of Foreign Exchange Beijing, China 550 State Oil Fund of the Republic of Azerbaijan Baku, Republic of Azerbaijan 33 Temasek Holdings Singapore Texas Permanent School Fund State Board of Education Austin, Texas United Nations Joint Staff Pension Fund New York, NY Total 22 DUANE MORRIS Buyouts Insider New York, NY 190 John Grubenman, director-private markets New York, NY Mukul Chawla, managing director 29 50 $6.5 trillion . PE ALLOCATION PE INSIGHTS (ESTIMATE) 6 percent Launched in 1984, the private equity portfolio includes funds earmarked for all major strategies, including venture capital, in North America, Europe and emerging markets. KIA will make co-investments alongside sponsors. KIA, which counts StepStone as an advisor, says on its website it won't directly back a North American fund smaller than $1.5 billion, an emerging markets fund smaller than $1 billion and a European fund smaller than Euro 2 billion; however, through a separate program KIA is believed to be committing more than $100 million per year to buyout funds of all sizes. Wafra Investment Advisory Group, owned by the Public Institution for Social Security in Kuwait, also invests KIA money in the U.S.

middle market. Backs buyout, distressed debt and growth equity investments in the Middle East and developed markets. Backs buyouts around the world; acquired a minority stake in The Carlyle Group in 2007. Reportedly had plan to invest up to $7.8 billion in Chinese private equity market by end of last year; also backs buyout, growth equity and funds of funds in North America and Europe; has an appetite for firsttime funds. 3 percent Sponsors backed by the fund include Adam Street Partners, Apollo Global Management, HarbourVest Partners, Hellman & Friedman, H.I.G. Capital and JMI Equity. In early 2014 the fund made a big bet on energy, commiting to invest $250 million in North American oil and gas investments alongside Kohlberg Kravis Roberts & Co. 7 percent QIC, which has been investing in private equity since 2005, makes commitments around the world to lower-middle-market buyout funds of $200 million to $750 million.

It co-invests alongside a core group of some 15-20 firms, including Columbia Capital, Frazier Healthcare Partners and TSG Consumer Partners. Backs buyouts and venture capital investments across all major regions; has an appetite for co-investments; along with Colony Capital, QIA was part of an investment group that purchased Miramax from Disney in 2010. Is an active private equity investor with an appetite for buyout funds of all sizes. Counts StepStone as an advisor. Portfolio is diversified by strategy and region. Backs buyouts and co-investments in North America, South America, Europe and emerging markets 33 percent of portfolio is invested in unlisted assets Known to have an appetite for mid-market buyout funds and co-investments; has backed such firms as Affinity Equity Partners, Candover Investments PLC and Madison Dearborn Partners. 5 percent (10 percent target) Invests in buyout funds, distressed debt funds, venture funds, growth equity funds, mezzanine funds, special situation funds and secondaries across Europe and North America; will back first-time funds; has an appetite for co-investments; invests through separate accounts. 3.5 percent in alternatives/target is 5 percent Is an active private equity investor with an appetite for buyout funds of all sizes. Counts StepStone as an advisor. Source: Sovereign Wealth Institute, Preqin, Dow Jones, SWF web sites Connections in the Middle Market 23 .

Meantime, SWFs realize that the credit markets when it comes to taking risk, steadfast in hewing have been more consistently available to finance to a long-term strategic plan, and unmoved by mid-market deals, compared with mega-deals. the latest investment trend. The collective interest by SWFs in the U.S. SWFs that aren’t liability-driven tend to be middle market is having a profound impact on more opportunistic, more apt to time markets. fundraising. Connections in the Middle Market Korean SWFs, many of which are new to the has identified more than two dozen with a asset class, are a good example. known appetite for U.S. buyout funds or co- many big investors pick the best private-equity investments (see table, pp. 20-23).

Together managers they can, and back them so long as they control an estimated $6.5 trillion in assets. they continue to perform, Korean SWFs tend to Given their typical allocation target to private first pick an investment strategy that they feel equity of 5 percent to 10 percent, SWFs have will outperform over the next few years, said a staggering amount of money to add to the Probitas Partners’s DePonte. They then, in effect, collective war chests of U.S. sponsors.

In fact, a put out requests for proposals for managers. good estimate for the portion of all capital raised One upshot: they may miss backing a strong by U.S. sponsors from SWFs is a substantial 15 firm if it happens to be out of the market. Whereas percent, second only to public pensions. Like most institutional investors, these SO, HOW DOES A SWF BEHAVE? opportunistic SWFs may be sticklers for process Broad agreement is missing on how to define and paperwork and put sponsors through a SWFs but in this article we use the term to rigorous due diligence. include all government-controlled investment running a gauntlet of screens and tests. Success depends on pools. Excluded are U.S.

pension funds, since they constitute such a large source of capital in But other opportunistic SWFs, no matter how and of themselves. large, behave more like small family offices. What matters most are relationships built up Despite the difficulty of broad generalizations, over months or years. Said one advisor to LPs advisors, placement agents and the SWFs who wished to remain anonymous given the themselves point to some defining characteristics. sensitivity of the subject: “You get the feeling SWFs fall into two broad camps. Those that that the decision-making [at these SWFs] is manage pension money, so-called “liability- driven by a small group of individuals rather than driven” investors, behave by and large like an institutional decision-making process that GPs pension funds.

They tend to be conservative might be more familiar with...” 24 DUANE MORRIS Buyouts Insider . The biggest SWFs often employ large private • GCM Grosvenor has run a mid-market buyout equity investment teams that relish making program for CPPIB that has grown to more than decisions themselves. They eschew third-party $840 million in commitments since 2003; it is advisors or funds of funds. Several, including GIC also said to have done work for China Investment Private Ltd and Temasek Holdings, have boots on Corporation (CIC) and Korea National Pension the ground thanks to investment officers working Fund. in U.S. offices.

Seven international SWFs on our list of 25 have U.S. offices. • Wafra Investment Advisory Group, owned by the Public Institution for Social Security in That said, even the largest SWFs may not have the Kuwait, manages upwards of $20 billion, mainly expertise to navigate the hundreds of investment opportunities in the U.S. middle market.

Their high minimum commitment sizes can make it impractical to back smaller buyout funds. This has created an opportunity for advisors. Some create bespoke managed accounts; others invite the SWFs into their co-mingled funds of funds. Among some of the more prominent programs: • StepStone advises a number of SWFs, including Kuwait Investment Authority, Saudi Arabia General Organization for Social Insurance and United Nations Joint Staff Pension Fund. The three programs are believed to be active, “What I’ve found over time is that if you team up with the right managers, interesting co-investment deal flow falls out of that.” —Stephen Moseley, director of investments, private equity and special opportunities, Alaska Permanent Fund Corporation covering buyout funds of all sizes, together representing potential commitments of hundreds on behalf of its parent and other SWFs in Kuwait of millions of dollars per year. although it has launched an initiative to expand its investor base outside the Middle East.

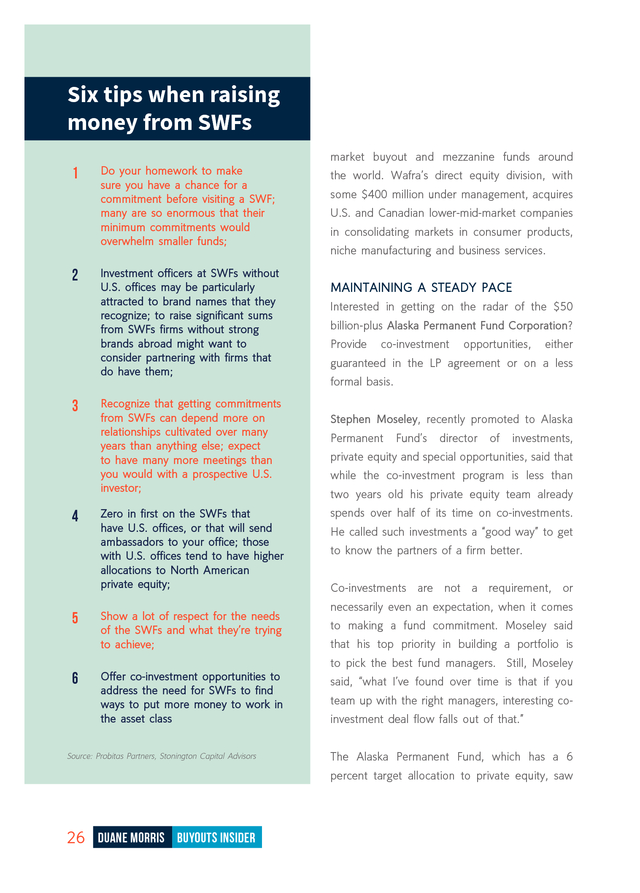

The • MLC Private Ltd, which last year opened an firm’s alternative investment group, with about office in New York City led by Andrew Kwee, is $4 billion under management, has taken minority known to handle a lot of private equity work on positions in Stone Point Capital and TowerBrook behalf of Australian pensions; it has a particular Capital Partners as part of its GP buyout program; appetite for buyout funds under $1 billion in its private asset management group, with about size. $3 billion under management, backs middle- Connections in the Middle Market 25 . Six tips when raising money from SWFs market buyout and mezzanine funds around 1 2 3 4 5 6 Do your homework to make sure you have a chance for a commitment before visiting a SWF; many are so enormous that their minimum commitments would overwhelm smaller funds; Investment officers at SWFs without U.S. offices may be particularly attracted to brand names that they recognize; to raise significant sums from SWFs firms without strong brands abroad might want to consider partnering with firms that do have them; Recognize that getting commitments from SWFs can depend more on relationships cultivated over many years than anything else; expect to have many more meetings than you would with a prospective U.S. investor; Zero in first on the SWFs that have U.S. offices, or that will send ambassadors to your office; those with U.S. offices tend to have higher allocations to North American private equity; Show a lot of respect for the needs of the SWFs and what they’re trying to achieve; the world.

Wafra’s direct equity division, with some $400 million under management, acquires U.S. and Canadian lower-mid-market companies in consolidating markets in consumer products, niche manufacturing and business services. MAINTAINING A STEADY PACE Interested in getting on the radar of the $50 billion-plus Alaska Permanent Fund Corporation? Provide co-investment opportunities, either guaranteed in the LP agreement or on a less formal basis. Stephen Moseley, recently promoted to Alaska Permanent Fund’s director of investments, private equity and special opportunities, said that while the co-investment program is less than two years old his private equity team already spends over half of its time on co-investments. He called such investments a “good way” to get to know the partners of a firm better. Co-investments are not a requirement, or necessarily even an expectation, when it comes to making a fund commitment. Moseley said that his top priority in building a portfolio is to pick the best fund managers.

Still, Moseley Offer co-investment opportunities to address the need for SWFs to find ways to put more money to work in the asset class Source: Probitas Partners, Stonington Capital Advisors said, “what I’ve found over time is that if you team up with the right managers, interesting coinvestment deal flow falls out of that.” The Alaska Permanent Fund, which has a 6 percent target allocation to private equity, saw 26 DUANE MORRIS Buyouts Insider . Alaska Permanent Fund Corp’s PE Performance its 10-year-old portfolio reach $3.2 billion in value and $5.8 billion in cumulative commitments by the end of last June. VINTAGE YEAR Compared with other institutional programs VINTAGE YEAR APFC IRR MEDIAN IRR BENCHMARK the portfolio leans heavily toward fast-growing 2005 11.3% 7.3% industries. The legacy portfolio consists of some 2006 8.4% 6.2% 270 separate commitments to 130 sponsors 2007 12.1% 8.3% specializing in venture capital funds (about 2008 12.2% 10.3% 2009 15.5% 13.0% 2010 17.8% 11.0% 2011 12.8% 11.7% buyout funds of $200 million to $1 billion (30 2012 23.4% 10.6% percent), large buyout funds of more than $1 2013 11.5% 6.6% billion (15 percent) and specialized distressed 2014 N/M N/M credit funds (5 percent). Total 11.8% 9.6% 27 percent of portfolio), small buyout funds of under $200 million (21 percent), mid-sized BY TIME HORIZON By region, about 72 percent of the capital is HORIZON Europe and 5 percent Asia. The Alaska Permanent APFC PE Industry 1-year earmarked for the United States, 18 percent 12.7% 7.9% 3-year 17.7% 13.4% Fund also has a 20 percent target allocation 5-year 15.9% 13.1% to special opportunities. The program includes Since Inception 11.8% 9.6% some private equity, including investments in Source: Alaska Permanent Fund Corporation healthcare start-ups and a commitment to the third fund of Dyal Capital Partners, earmarked In its 2015 fiscal year ending June 30 the fund for minority investments in private equity firms. committed $800 million to 19 funds.

In the last 12 months Alaska Permanent Fund has backed About two years ago, just as Moseley joined, the latest growth equity and mid-market buyout Alaska Permanent Fund decided to bring most funds of American Industrial Partners, Catterton of its private equity program in-house. It let a Partners, Centerbridge Partners, Genstar Capital, five-year contract for discretionary work with Harvest Partners, Nautic Partners, Ridgemont HarbourVest Partners expire and modified the Equity Partners and TA Associates, among discretionary assignment it had awarded to others. Pathway Capital. Since then it has ramped up the program every year. The SWF also made four co-investments totaling Connections in the Middle Market 27 .

$88 million in fiscal year 2015. These include also prefers to be a “significant investor” in each investments in wind turbine company Senvion SE fund, which is easier to accomplish in the middle alongside Centerbridge Partners and in software market. company Compuware Corp alongside Thoma Bravo. “All other things being equal I’d have a natural bias toward an existing relationship,” said This fiscal year, said Moseley, Alaska Permanent Moseley, adding that he spends a lot of time on Fund is up to $550 million in commitments on the road and that it’s not “required or expected” the way to a target of $900 million; it has also for sponsors to visit Juneau, Alaska. Still, the made two co-investments of about $41 million SWF is open to new relationships, including in total. While a typical fund commitment is on with first-time fund managers, such as Glendon the order of $75 million, the SWF might commit Capital Management, a firm founded by former Barclays executives. “We appreciate the risk-return profile of businesses in the lower middle market.” —Matt Diestel, VP-global private equity, QIC “It’s not easy but when we can find new groups with some demonstrable history and credibility that’s really exciting,” he said. CO-INVESTMENTS SOUGHT As with Alaska Permanent Fund, a good way to get on the radar of Brisbane, Australiabased QIC, created in 1991 by the Queensland less or more depending on the situation.

Alaska government to manage pension assets, is to Permanent Fund can account for up to 100 offer co-investment opportunities in the lower percent of the size of a fund—and has done so middle market. in many cases. Since 2007 QIC has completed some 24 coLooking ahead, said Moseley, Alaska Permanent investments alongside a group of 15-20 core Fund continues to be drawn to the U.S. middle sponsors, including Columbia Capital, Frazier market. It’s where the SWF has found an Healthcare Partners, TSG Consumer Partners abundance of “really talented managers applying and Webster Capital.

Among its best-performing specialized investment co-investments were a pair of 2012 deals— opportunities, undistracted by the demands of one done alongside TSG Consumer Partners managing a large, diversified shop. The SWF gymnasium chain Planet Fitness (now public) skills” to long-term 28 DUANE MORRIS Buyouts Insider . and another done alongside Columbia Capital the firm looks to put $15 million to $50 million in technology consulting firm Cloud Sherpas to work at a time. (recently sold to Accenture). The firm invests both through separate accounts and through a Lower-middle-market buyout funds of $200 dedicated co-investment pool of A$150 million million to $750 million in size make up QIC’s ($108 milllion). sweet spot. “We appreciate the risk-return profile of businesses in the lower middle market,” As of year-end the co-investment portfolio was Diestel said. “They are very much real businesses valued at A$800 million, while the entire private with good management teams,” he added, but equity portfolio, including fund investments, they can often benefit from an infusion of capital secondary to finance, say, a consolidation strategy. buys and co-investments, was valued at a little over A$5 billion. The firm has relationships with more than 50 sponsors In addition, the firm finds less competition for altogether.

About two-thirds of its capital goes co-investment opportunities, and more of an to the more developed private equity markets in opportunity to scrub through a deal on its own. the United States and Europe. The rest goes to That makes it more of a “true capital partner” to Australia and Asia. the sponsor, said Diestel. In the upper middle market, by contrast, co-investments resemble Matt Diestel, vice president-global private equity “more of a syndication process,” he said. based in San Francisco, said he spends a third to half of his time evaluating venture capital and Diestel said that the firm’s co-investment portfolio growth equity opportunities and the balance on has been “super-helpful” in boosting returns on buyouts. The firm is particularly interested in the private equity portfolio, having generated backing specialists with a track record of creating 33 percent per year net returns, well ahead of value in healthcare services, consumer goods, the 19 percent net IRR achieved by the entire specialty manufacturing and technology. program.

He added: “It’s been pretty incredible.” Part of a 13-investment-professional private equity team located in Brisbane, Europe and the United States, Diestel said that QIC wants “meaningful” ACTION ITEM: A good source of information on SWFs is the Sovereign Wealth Fund Institute at swfinstitute.org exposure to the buyout funds that it backs. In any given year expect the firm to commit $200 million to $300 million to funds and $150 million to $200 million in co-investments. In both cases Connections in the Middle Market 29 .

W About Duane Morris ith experienced private equity lawyers working in the middle market across our global platform, coupled with experience in key verticals and the deep capabilities of more than 700 lawyers from all major practice areas, Duane Morris creates competitive advantage for participants across the industry. For GPs, we deliver insights that optimize transactional value for both sellers and buyers in control and noncontrol investments and with exit strategies, and support portfolio company growth strategies. For LPs, we review LPA terms and advise on efficient, effective investment strategies, including co-investment and direct 30 DUANE MORRIS Buyouts Insider investment; alignment of interests; transparency; and governance issues. For business owners, we advise on growth strategies – not only on the mechanics of full or partial exits, but also on crafting wealth-planning approaches designed to positively impact economics for the owner. Given our strategic firmwide focus on private equity, broad experience in major industry sectors and an innovative culture deeply committed to client service, we are regularly called upon to work with company owners, as well as the most sophisticated and demanding players in the private equity marketplace. .

Duane Morris is proud to be an Official Sponsor of Growth® of the Association for Corporate Growth (ACG). UNITED STATES Atlanta Baltimore Boca Raton Boston Cherry Hill Chicago Houston Lake Tahoe Las Vegas Los Angeles Miami New York Newark Philadelphia INTERNATIONAL Pittsburgh San Diego San Francisco Silicon Valley Washington, D.C. Wilmington Hanoi Ho Chi Minh City London Mexico City (alliance) Myanmar Oman Singapore Connections in the Middle Market 31 . B About Buyouts Insider uyouts Insider delivers a portfolio of marketleading titles, online services, and senior executive conferences covering private equity and venture capital. The print and online publishing brands of Buyouts, Venture Capital Journal, and PE HUB offer the intelligence professionals need to raise money, find deal opportunities, secure loans to finance deals and benchmark their performance against rival firms. PartnerConnect, the suite of private BUYOUTS PE HUB NETWORK BUYOUTS VCJ PRATT’S ONLINE MembersDeals Jobs LPs & Exits Videos People PARTNERCONNECT EVENTS Data Room Videos Register BUYOUTS CHICAGO Search... SHOP Join the Buyouts editorial team and hundreds of LPs and GPs in Chicago for two days of deal flow, industry knowledge, networking and thought leadership. Buyouts Magazine Key Facts About Buyouts Chicago: • Produced by the editors of Buyouts and peHUB.com – knowledgeable leaders in these asset classes for as long as 50+ years J. Christopher Flowers J.C. Flowers & Co. PE HUB Community meetings will be pre• 250+ private 1:1 J.B.

Pritzker Pritzker Group May 18, 2015 • Issue 11 www.buyoutsnews.com Meet the Speakers • More than 300 fund managers, investors and intermediaries to attend over 2 days of programming • A blue-chip, senior executive conferences, ensuring you meet key decision-makers onsite Featured Content JUNE 23-24, 2015 THE PALMER HOUSE, CHICAGO buyoutsconferences.com/chicago15 EXPAND YOUR NETWORK AND YOUR BRAND WHILE GETTING DEALS DONE AT THE 8TH ANNUAL BUYOUTS CHICAGO! Wilbur L. Ross Jr. WL Ross & Co. Impact investing BUYOUTS Vol. 28, No.

11, May 18, 2015 Home News BriefsFundsOpinion & Firms Sign in equity and venture capital conferences, provides networking opportunities for fund managers to raise capital for their next fund and source deal flow by hearing from and meeting institutional investors and deal intermediaries. Senior executives involved in private capital have relied on Buyouts Insider products since 1961. For more information on our products, please call +1 646.356.4509. Deval Patrick wants to leave a mark at Bain Here are a sample of firms who have previously attended Buyouts Chicago from the past three years to give you a sense of the types of companies you’ll meet this year: 38 Join the 13430 members of PE HUB to • • • • • • • • 57 Stars 747 Capital Abbott Capital Management Adveq Management US American Securities Angelo Gordon Atlas Diligence Auximos Asset Management Group Babson Capital Management Barclays Bay Hills Capital BDO BlackRock Private Equity Partners Bow River Capital Partners Bowside Capital Brookfield Asset Management Castle Harlan Chicago Growth Partners CIC Partners Cimarron Capital Partners Coller Capital Comerica Bank • Commonfund • Crow Holdings Capital Partners • Crystal & Company • DB Private Equity & Private Markets • Diversified Trust Company • Evercore • Evolution Capital Partners • Fisher Lynch Capital • FLAG Capital Management • Franklin Park • GE Capital • Google inc • Greenberg Traurig • Green-Path Advisors • Grove Street Advisors • GTCR • Hamilton Lane • HarbourVest Partners • Harris Williams & Co. • Hauser Private Equity • Hewitt EnnisKnupp • Insight Equity • Lazard Middle Market • • • • • • • • • • • • • • • • • • Madison Capital Funding Manulife Capital McGladrey MCM Capital Partners McNally Capital Monroe Capital Muller & Monroe Asset NB Alternatives New Harbor Capital New MainStream Capital Northern Trust Alternatives Northwestern Mutual Capital Oak Hill Capital Management Oaktree Capital Ocean Avenue Capital Partners Odyssey Investment Partners Park Hill Group Performance Equity Management • Pine Brook • Private Advisors • Providence Equity • RCP Advisors • RDV Corporation make connections, share your opinion, and follow your favorite authors. • • • • • Join the Community BUYOUTS Ohio Police & Fire backs new Harvest agship (Subscription Required) BUYOUTS BUYOUTS ‘Godfather of PE’ Richard Rainwater inspired prominent careers Get your Q3 2015 Private Equity slide show • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • Rothstein Kass Shinrun Advisors Siguler Guff Silicon Valley Bank Sixpoint Partners SL Capital Partners Solar Capital Star Mountain Capital Sterling Partners Stonington Capital Advisors Summit Strategies Group Sun Capital Partners SURS Sutton Place The Hauser Group The Riverside Company TIAA-CREF Trive Capital TriVista Twin Bridge Capital UPS Group Trust Victory Park Capital Wind Point Partners WP Global Partners Impact investing: Deval Patrick wants to leave a mark at Bain Register TOday: buyoutsconferences.com/chicago15 arranged between LPs and GPs through the ExecConnect private meeting program Want to market in Europe? Get to know AIFMD Amid LP concerns, Saybrook resolves labor dispute LP Scorecard: Even the distributions are big in Texas Digital Edition 5 12 16 For effective leadership, improve your power score 1-800-455-5844 registrar@buyoutsinsider.com 37 The pendulum swings back in favor of GPs For more information contact our team at: 60 (Subscription Required) (Subscription Required) To read a digital copy of our latest magazine Most GPs think LPs are unrealistic: study By Luisa Beltran — 16 hours ago click here The capital of tomorrow May 4, 2015 • Issue 10 www.buyoutsnews.com BUYOUTS Vol.

28, No. 10, May 4, 2015 LPs unrealistically expect GPs to produce high returns. That’s according to a survey of investors [...] CONTINUE All eyes on GE Antares Goldman Sachs veteran Winkelried to join TPG as coCEO Lindsay Goldberg produces anything but small potatoes for Idaho Caisse de dépôt pivots further toward direct investing Advisory | Debt | Equities | Principal Investing Look Who’s Tweeting VC & PE Tweets co-chief [...] Tweets from a list by pehub www.buyoutsnews.com Carlyle eyes new infrastructure fund By Steve Gelsi — 18 hours ago Carlyle Group said it continues to see strong interest in its many funds in the [...] CONTINUE Apollo raises $3.3 bln in Q3 with boost to natural resources fund 32 DUANE MORRIS Buyouts Insider By Steve Gelsi — 18 hours ago Apollo Global Management said it drew in $3.3 billion of fresh capital in the third [...] CONTINUE macquarie.com/whiteboard These examples may not be representative of every client’s experience.

Past performance is not a guarantee of future performance or success. Macquarie Capital (USA) Inc. (Macquarie Capital) is a registered broker-dealer and member of FINRA and SIPC.

This document does not constitute an offer to sell or a solicitation of an offer to buy any securities. This document does not constitute and should not be interpreted as either an investment recommendation or advice, including legal, tax or accounting advice. Macquarie Capital is not an authorized deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia).