Private Equity Connections in the Middle Market – Heading for the Exit – Spring 2015

Duane Morris

Description

Private Equity/Capital Markets

SPRING 2015

INNOVATIONS IN GLOBAL

CONNECTIONS

PRIVATE EQUITY

IN THE MIDDLE MARKET

HEADING for the

Owner, Investor and

Banker Perspectives

featuring

insights from

Grant Thornton LLP

NewSpring Capital

Raymond James & Associates

Relay Network

. INNOVATIONS IN GLOBAL

CONNECTIONS

PRIVATE EQUITY

IN THE MIDDLE MARKET

. Table of Contents

01

Letter to Our Readers

02

Market Environment:

The Macro Overview

06

The Exit Process: Key

Questions and Players

14

Industry Attractiveness:

Where to Find the Deals

20

Timing, Preparation and

Momentum

30

Valuation, Best Buyer and

Certainty Around Closure

37

Conclusion

38

SPEAKER profiles

40

ABOUT DUANE MORRIS

. a leTTer To our readers

s

Successfully selling a privately-held middle-market business—

whether outright, retaining a portion, or in an initial public

offering (IPO)—is one of the greatest personal, financial and

legal challenges an owner will face. Though the stakes are

indeed high for the owner, they are also considerable for

investors, employees and the legacy of the business.

“MORe IMPORtANt

tHAN tHe wIll

tO wIN IS tHe wIll

tO PRePARe.”

-Charlie Munger,

Berkshire Hathaway

Consequently, much can be gained from owners who have

“gotten it right” and especially those “serial owners” who have developed a true talent from

repeatedly selling their businesses. Similarly, the accumulated experience and know-how of

the key players in the exit process—investment bankers, investors, legal counsel and financial

advisors—are also worth careful review and study.

Duane Morris organized its “Heading for the Exit” event, held in Philadelphia last November,

specifically to bring together these key players to discuss the nuances around exiting a company

in today’s complex and crowded marketplace. We are honored to have the participation of the

following individuals who contributed to what was a lively and insightful discussion:

• DAVID ClARK, Managing Director, Head of Financial Sponsors Group, Raymond James & Associates

• MIKe DiPIANO, Managing General Partner and Founder of NewSpring Capital

• MAtt GIllIN, CEO and Co-Founder of Relay Network, formerly the Founder and CEO

of Ecount, which was sold in 2007

• DARRICK MIx, partner in the Duane Morris Capital Markets Practice

• JOHN StINe, Assistant Office Managing Partner and Tax Partner, Grant Thornton LLP

Ultimately, what an owner wants to achieve—in what can be a drawn-out, unpredictable

process—is a “good exit.” This may have many dimensions; however, we think it comes down

to owners’ receiving a fair price and feeling a sense of accomplishment, both for themselves,

as well as the broader business and its stakeholders.

.

A key takeaway from the event is the overriding importance of preparedness—getting out ahead of the process, e.g., clearly understanding what you as an owner-manager want to accomplish, deciding what approach to take to get there and choosing your team. Although preparedness may not guarantee a “good exit,” unpreparedness is most likely to lead to a “bad exit”—the sale does not close, a founder suffers seller’s remorse, employees feel let down and the legacy of the business is in question. We trust that you will find this publication, a collaborative effort of Duane Morris’ Private Equity and Capital Markets groups, to be both thought-provoking and a helpful guide to the exit process. Please let us know what you think. Pierfrancesco Carbone Co-Head of Private Equity – UK / Europe Duane Morris LLP Richard P. Jaffe Co-Head of Private Equity Duane Morris LLP Darrick Mix Partner Capital Markets Duane Morris LLP DUANE MORRIS — CONNECTIONS 1 .

From left: NewSpring Capital’s Mike DiPiano, Relay Network’s Matt Gillin and Raymond James’ David Clark contemplate the market environment. MarkeT environMenT: The MaCro overview D “Deal Boom Feeds on Surging Stocks” was the front-page story in The Wall Street Journal the day before Duane Morris’ “Heading for the Exit” event.1 The story noted that global M&A volume had already breached the $3 trillion mark for the year, up 32 percent over the similar period in 2013, as companies took advantage of rising stock prices and cheap credit, both a function of the Federal Reserve’s easy-money policies. The U.S. accounted for about half of this amount by value, up 37 percent relative to 2013 (See Chart 1). 2 DUANE MORRIS — CONNECTIONS . Chart 1: Big Year for North American M&A 6000 1,200.00 1,000.00 800.00 600.00 percent in 2014—indicating it was another good 3000 1,400.00 the majority of the value of IPOs—by nearly 62 4000 1,600.00 2000. Financial sponsors continue to account for 5000 1,800.00 $Billion non-financial sponsors) were the highest since year for investors of private equity funds.2 2000 400.00 1000 0.00 The corporate buying spree and strong IPO market 0 200.00 are occurring despite serious headwinds, such as 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Deal Value ($B) Deal Number Source: Capital IQ Includes transactions with disclosed value over $10mm recent market volatility, a weakening Chinese economy, Japan falling back into recession, continued lackluster economic performance in Europe and a faltering Russian economy. 2014 was also a big year for IPOs, which by value jumped by nearly 77 percent from the previous Panelists at the Duane Morris event were year to nearly $60 billion (See Chart 2). The generally upbeat, with Mike DiPiano, Managing 291 North American listings (by financial and General Partner and founder of NewSpring Chart 2: Value of Financial- and Non-Financial Sponsor-Backed IPOs 110 450 100 400 90 350 80 $ Billions 60 250 50 200 40 Number 300 70 150 30 100 20 50 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Non-PE IPO proceeds PE IPO proceeds 2012 2013 2014 0 PE IPO number Non-PE IPO number Source: EY DUANE MORRIS — CONNECTIONS 3 . Capital, observing that he did not see interest Office Managing Partner and Tax Partner at Grant rates rising much; hence, “there’s going to be Thornton LLP, notes that his firm is “unbelievably debt available.” In addition, he continues, “There busy on transactions right now,” which is not the is a fair amount of capital with buyout shops norm for this time of year. like ours that are paid to put money to work,” which would encourage the industry “to continue In Clark’s view, 2015 “is going to be another buying” and “the IPO market to perk up.” strong year” and “the IPO market is going to continue to be solid,”—barring any unexpected David Clark, Managing Director, Head of Financial events. Plenty of prospective buyers and an Sponsors Group at Raymond James & Associates, improving economy translate into a seller’s agrees with DiPiano—“Our economist’s view is market. A number of private equity firms, as well that interest rates may go up, but they are not as family-owned businesses, “have reached out going to go up by that much, so there’s still to us to talk about their business,” he says. The plenty of capital out there.” In addition to private question on their mind is: “Is this a good time equity money, “there is a lot of cash on the to exit, and if so, how is the best way to do balance sheets” of strategics, he noted.

Clark also it?” That said, from a buyer’s perspective, “The highlighted that limited partners increasingly want market is very frothy with a lot of capital chasing co-invest opportunities. deals,” Clark observes. Turning the spotlight on another leading indicator Indeed, the successful exit market last year, which saw private equity funds return an expected $479 of the market’s direction, John Stine, Assistant T he Duane Morris V i e w You can’t time a sale, but . . . A significant factor contributing to the liquidity the industry is experiencing is that the constellation of potential buyers and strategies has expanded well beyond the usual suspects. This phenomenon provides sellers—provided that they are well prepared—with more leverage so that they can better tailor an exit to address their particular goals and needs. 4 DUANE MORRIS — CONNECTIONS .

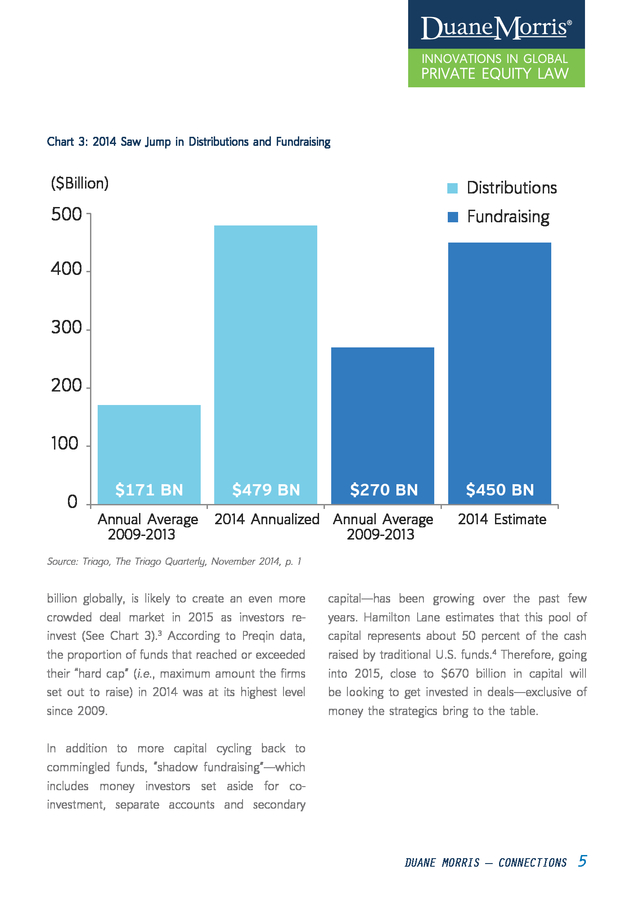

Chart 3: 2014 Saw Jump in Distributions and Fundraising ($Billion) Distributions 500 Fundraising 400 300 200 100 0 $171 BN Annual Average 2009-2013 $479 BN $270 BN 2014 Annualized Annual Average 2009-2013 $450 BN 2014 Estimate Source: Triago, The Triago Quarterly, November 2014, p. 1 billion globally, is likely to create an even more crowded deal market in 2015 as investors reinvest (See Chart 3).3 According to Preqin data, the proportion of funds that reached or exceeded their “hard cap” (i.e., maximum amount the firms set out to raise) in 2014 was at its highest level since 2009. capital—has been growing over the past few years. Hamilton Lane estimates that this pool of capital represents about 50 percent of the cash raised by traditional U.S. funds.4 Therefore, going into 2015, close to $670 billion in capital will be looking to get invested in deals—exclusive of money the strategics bring to the table. In addition to more capital cycling back to commingled funds, “shadow fundraising”—which includes money investors set aside for coinvestment, separate accounts and secondary DUANE MORRIS — CONNECTIONS 5 .

The exiT ProCess: key QuesTions and Players C Careful preparation and execution are two preconditions to a successful exit. “The key is getting prepared and getting everything done upfront, and running as efficient a process as possible,” observes Clark at Raymond James. “At the end, that’s where the value’s going to be,” he says. Thus, Clark spends considerable time with owners to provide guidance on whether “this is the right time for your business to come to market and exit,” and if so, “How do you want to do it? What is the best process?” .

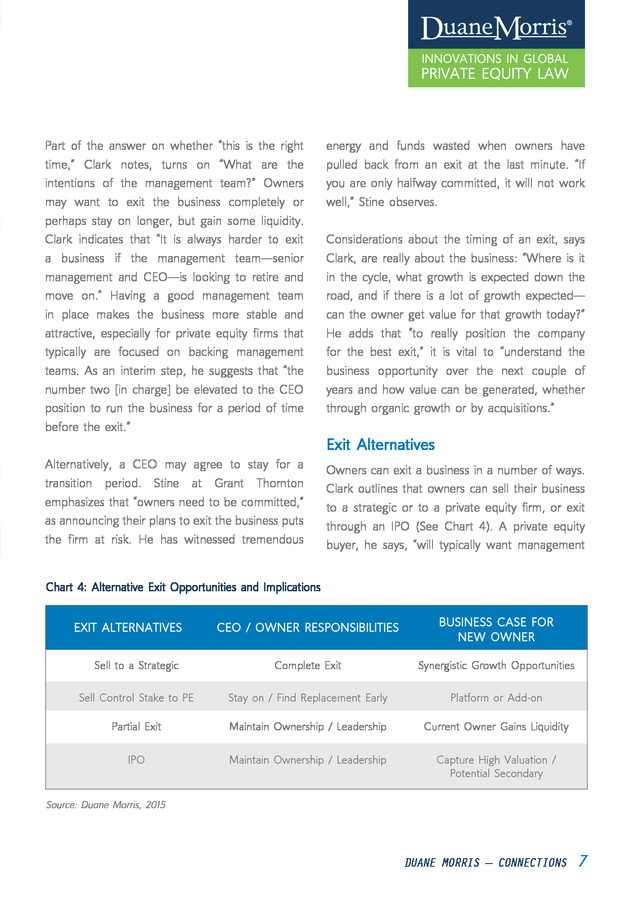

Part of the answer on whether “this is the right time,” Clark notes, turns on “What are the intentions of the management team?” Owners may want to exit the business completely or perhaps stay on longer, but gain some liquidity. Clark indicates that “It is always harder to exit a business if the management team—senior management and CEO—is looking to retire and move on.” Having a good management team in place makes the business more stable and attractive, especially for private equity firms that typically are focused on backing management teams. As an interim step, he suggests that “the number two [in charge] be elevated to the CEO position to run the business for a period of time before the exit.” energy and funds wasted when owners have pulled back from an exit at the last minute. “If you are only halfway committed, it will not work well,” Stine observes. Considerations about the timing of an exit, says Clark, are really about the business: “Where is it in the cycle, what growth is expected down the road, and if there is a lot of growth expected— can the owner get value for that growth today?” He adds that “to really position the company for the best exit,” it is vital to “understand the business opportunity over the next couple of years and how value can be generated, whether through organic growth or by acquisitions.” Exit Alternatives Alternatively, a CEO may agree to stay for a transition period. Stine at Grant Thornton emphasizes that “owners need to be committed,” as announcing their plans to exit the business puts the firm at risk.

He has witnessed tremendous Owners can exit a business in a number of ways. Clark outlines that owners can sell their business to a strategic or to a private equity firm, or exit through an IPO (See Chart 4). A private equity buyer, he says, “will typically want management Chart 4: Alternative Exit Opportunities and Implications CEO / Owner Responsibilities Business Case for New Owner Sell to a Strategic Complete Exit Synergistic Growth Opportunities Sell Control Stake to PE Stay on / Find Replacement Early Platform or Add-on Partial Exit Maintain Ownership / Leadership Current Owner Gains Liquidity IPO Maintain Ownership / Leadership Capture High Valuation / Potential Secondary Exit Alternatives Source: Duane Morris, 2015 DUANE MORRIS — CONNECTIONS 7 . or prior owners to keep some equity in the business,” and “will basically invest alongside them.” Finally, owners may choose a partial exit, “to take some money off the table and diversify their net worth,” Clark notes. There are key differences between a sale to a strategic versus a private equity firm. Clark indicates that “a strategic buyer typically can buy 100 percent of the stock,” which enables the owner to exit the business completely. “The owner may end up getting shares in the acquirer’s Through a minority recapitalization (recap), an owner can gain some liquidity by selling an interest in the business, but continue to maintain control. At NewSpring Capital, DiPiano has done a number of recaps and says, “Usually we do them when we think there is a lot of runway in the business for growth,” but he adds, they “retrigger timing.” He notes that “Once you take capital from somebody, and sell a portion of your business, you are setting a new clock for two, three or four years,” to enable the new investor to get the value they are looking for, which is a multiple of what they invested. stock,” but, he adds, “the owner is going to get value based on the business today.” Conversely, a private equity firm will generally look to management and owners to contribute some equity into the business and to continue to be involved.

By investing alongside the new owner, “Management will have equity that increases in value over time as the business grows,” said Clark. 8 DUANE MORRIS — CONNECTIONS In today’s market, the IPO market is a very attractive exit option, Clark maintains. It has advantages and disadvantages. The upside of an .

IPO, he says, is that “an owner will gain stock that reflects the firm’s growth prospects” and will have liquidity that enables the owner to monetize that value. The downside, Clark continues, is that when an owner exits the business through an IPO, he or she “is not truly exiting the business because the owner will continue to own a meaningful amount of the equity for a period of time and, thus, be subjected to the equity markets.” “I thought an IPO would be the most exciting thing in the world,” declares DiPiano, “and although it is exciting, it also turns out to be painful in some ways.” While “you hope to get a higher price than you would in an outright sale, you are subject to a lot of SEC scrutiny.” Moreover, he says, many CEOs do not like the limelight, as analysts covering the stock will shop the company. “I have found if you get a reasonable value, an all-out sale is one that we would prefer,” DiPiano concludes. That said, DiPiano agrees with Clark that it has been a good IPO market, thanks to plentiful debt and high stock market valuations. “We are seeing a number of successful IPOs and a very strong pipeline,” so it is clearly an option at this point in time, Clark observes.

“I think part of the reason why the M&A market is attractive right now,” he indicates, “is because of the positive IPO market.” The Quarterback and Key Players Making sure an exit goes smoothly and is successful requires a team effort. “It’s very important to have a strong team,” says Clark and “it’s going to be accountants, lawyers and bankers” (See Chart 5). Matt Gillin, CEO and Co-Founder of Relay Network, learned this as a CEO and Founder of Ecount, which he successfully exited in 2007.

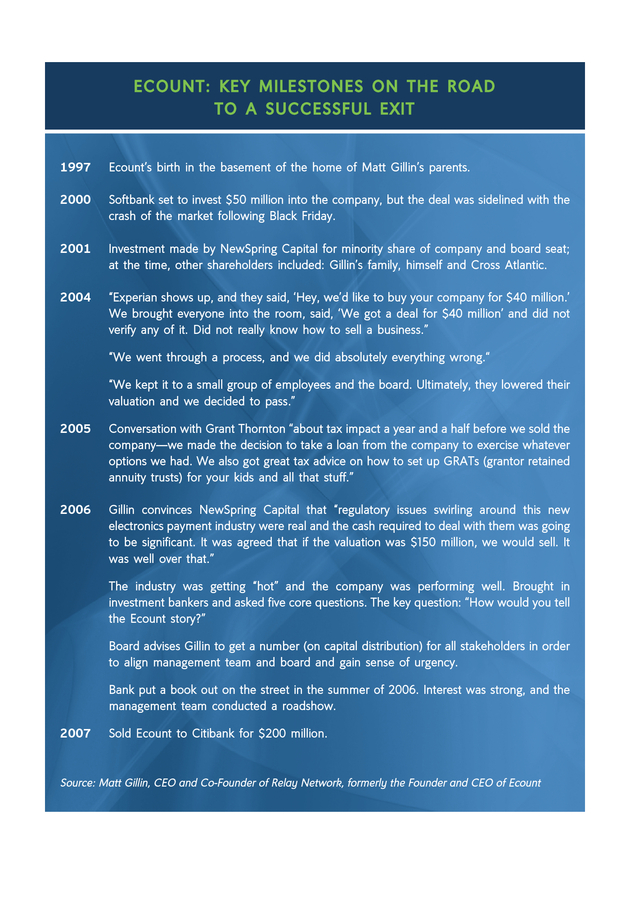

“You’ve got to choose your team wisely, both from a lawyer and a banker perspective,” he emphasizes. Fortunately for him, through the many twists and turns of selling Ecount, his team “was willing to do whatever it took.” As he relates his experience, Gillin says his training told him that “The best way to get the deal done was to get consensus across the board.” As the founder of Ecount since 1997, he knew the company’s intimate details, and having been burned a couple of times on prior exit attempts, Gillin wanted to ensure he was receiving as much advice as he could. “In our case, because we got everyone on board with a number up front [minimum transaction value], I was able to play the quarterback role,” he notes. (See Box: Ecount: Key Milestones on the Road to a Successful Exit, p.

12). Chart 5: Deal Team Investment Banker Financial Advisor OWNER Lead Board Member/ Investor Legal Counsel Source: Duane Morris, 2015 DUANE MORRIS — CONNECTIONS 9 . In Clark’s view, selling a company requires “a point person from within the company,” and it makes sense that this is the CEO “because ultimately, they have to sell the story to the buyer.” He adds that sometimes it actually makes sense for the owners and management to step back—for example, “when you are really trying to get down to the final deal valuation and terms.” Then, “The lawyers and the bankers can step in and basically be the bad guys, be in front of the buyer and push a particular point,” Clark says. DiPiano at NewSpring Capital tends to agree that the quarterback “is almost always your CEO.” Though he notes that “it’s sometimes your CEO tied together with a stakeholder that has experience,” or “sometimes there’s a trusted lawyer.” The CEO’s From left: Mike DiPiano of NewSpring Capital, Matt Gillin of Relay Network, David Clark of Raymond James and John Stine of Grant Thornton. 10 DUANE MORRIS — CONNECTIONS and lead board member’s vantage points can be instrumental to see a deal through and not get bogged down by minor details. Investment Bankers Another set of key players are investment bankers. DiPiano says NewSpring Capital has used a banker literally in every transaction where there was an exit because “they know the ropes, the market and the terms.” Whereas an owner and an investor may start to negotiate the transaction, the banker is “dealing with it every day” and is paid to deal with the “really contentious discussions,” he notes. As an investor, even if the owner has already picked a buyer, DiPiano retains a banker “to check out other options to make sure that . the buyer is being held accountable and there is a high certainty to close at the valuation we were hoping.” Stine at Grant Thornton recommends that “two, three, four years out from selling, owners of companies develop a relationship with one or more banks,” as they will “gain a tremendous amount of information.” He sees a massive upside, as bankers will “pick apart your numbers for free, give you a lot of insight into the market, help prepare you for the exit and give you a road map as to where you’re going.” The alternative, Stine says, is “waiting to the last minute and doing a ‘beauty contest,’ which means rushing the process,” and increasing the probability for failure. In Gillin’s experience, investment bankers are an “incredible resource.” While not engaging a banker in his first attempt to sell Ecount, the second time around, “we interviewed a bunch of them”—and asked each the same five questions. They included: “How would you tell the Ecount story? What valuation do you think we will get? Who exactly would you target at these companies?” Gillin says the process yielded an “incredible road map,” especially around how to “tell the Ecount story.” It helped his team “realize that to sell your company, you had to package it up like a product.” Another key role for bankers is to provide introductions. To help family-owned firms gain DUANE MORRIS — CONNECTIONS 11 . Ecount: Key Milestones on the Road to a Successful Exit 1997 Ecount’s birth in the basement of the home of Matt Gillin’s parents. 2000 Softbank set to invest $50 million into the company, but the deal was sidelined with the crash of the market following Black Friday. 2001 Investment made by NewSpring Capital for minority share of company and board seat; at the time, other shareholders included: Gillin’s family, himself and Cross Atlantic. 2004 “Experian shows up, and they said, ‘Hey, we’d like to buy your company for $40 million.’ We brought everyone into the room, said, ‘We got a deal for $40 million’ and did not verify any of it. Did not really know how to sell a business.” “We went through a process, and we did absolutely everything wrong.“ “We kept it to a small group of employees and the board. Ultimately, they lowered their valuation and we decided to pass.” 2005 Conversation with Grant Thornton “about tax impact a year and a half before we sold the company—we made the decision to take a loan from the company to exercise whatever options we had. We also got great tax advice on how to set up GRATs (grantor retained annuity trusts) for your kids and all that stuff.” 2006 Gillin convinces NewSpring Capital that “regulatory issues swirling around this new electronics payment industry were real and the cash required to deal with them was going to be significant.

It was agreed that if the valuation was $150 million, we would sell. It was well over that.” The industry was getting “hot” and the company was performing well. Brought in investment bankers and asked five core questions.

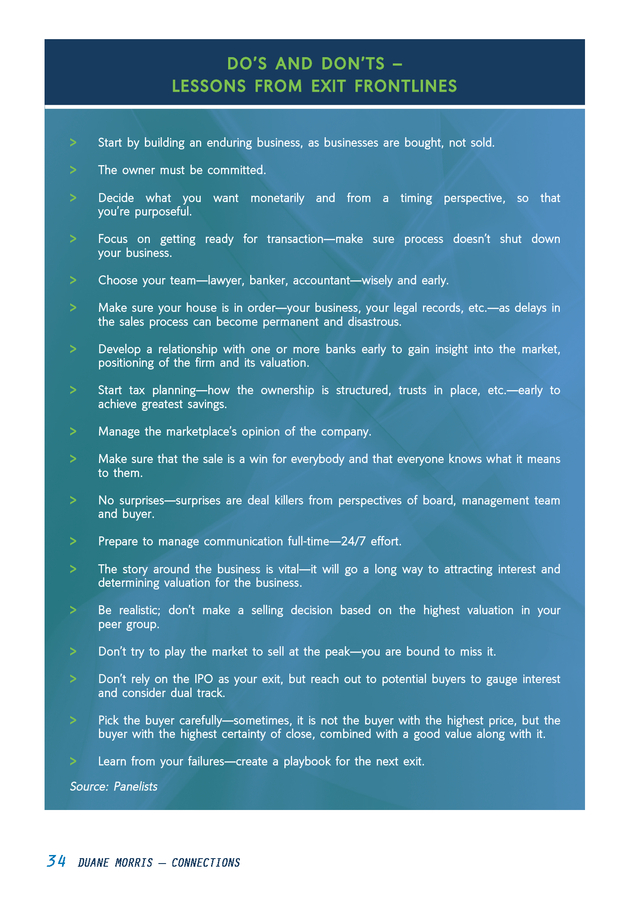

The key question: “How would you tell the Ecount story?” Board advises Gillin to get a number (on capital distribution) for all stakeholders in order to align management team and board and gain sense of urgency. Bank put a book out on the street in the summer of 2006. Interest was strong, and the management team conducted a roadshow. 2007 Sold Ecount to Citibank for $200 million. Source: Matt Gillin, CEO and Co-Founder of Relay Network, formerly the Founder and CEO of Ecount . better insights into how private equity firms look at their businesses, Clark says he “will introduce them to two or three firms who are willing to come in to learn about the business, and tell them how they think about partnering with management teams, how they look at investments, and just really helping the owner and the management team understand what it means to work with a private equity firm.” It often results in a great learning experience for owners, he continues, as the private equity firms will say, “Here’s how we see your business, and here’s where we see the opportunities going forward.” Lead Board Member What is the role of a lead board member, specifically one who is a non-controlling investor? According to DiPiano, as an investor, he is focused on “harvesting an investment return.” To achieve this requires balancing the dynamics of the different stakeholders, including management, the owner and other investors. “The advice we give is to get in a room and decide what it is you want, both monetarily and from a timing perspective,” he suggests. This makes sure that “you are purposeful about whether you really want to sell,” he emphasizes. If you are ready to sell, DiPiano continues, “You need to determine if the books and records are up to date, and if the data room that you are planning to put together will be robust and complete.” As an experienced quarterback, Gillin says he has “learned, through some good mentorship, to keep open the communication lines so there are no surprises.” In his view, “The kiss of death in any deal is a surprise.” He continues, “You don’t want the board to be surprised, you don’t want the management team to be surprised, and you certainly don’t want the buyer to be surprised.” Managing communication during an exit requires “a full-time, 24/7 effort” and “you need someone who has a lot of skin in the game and is committed.” Legal Counsel Lawyers can play various roles during the exit process and serve as a key party to drive the transaction to a close.

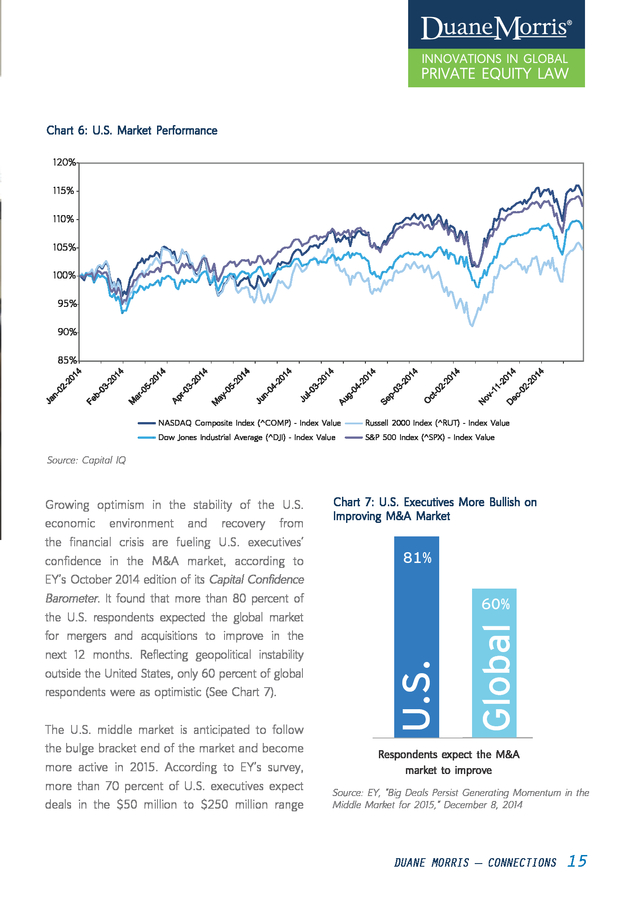

Depending on the situation and existing relationships, legal counsel can be the quarterback or the owner’s trusted advisor. They will be responsible for all legal matters, such as drafting a stock purchase agreement. Engaging a lawyer prior to initiating the process generally provides more opportunity to anticipate and address potentially problematic issues. Wealth Planning Finally, wealth planners are another set of key players, and they can be particularly important for owners to meet with earlier rather than later in the process. Stine stresses that “Thinking about your tax structure on the front end, in terms of how the ownership is structured, whether trusts are in place and picking the right form of entity, will reap huge rewards on the back end.” In his view, the big gains from proper tax planning, such as being able to “move an entire company down a generation,” require getting involved years—not weeks—before the exit. DUANE MORRIS — CONNECTIONS 13 . From left: Duane Morris’ Darrick Mix, NewSpring Capital’s Mike DiPiano, Relay Network’s Matt Gillin and Raymond James’ David Clark. indusTry aTTraCTiveness: where To find The deals the Middle Market Is Next up A As 2014 came to a close, the already good exit environment got better when the Dow Jones industrial average in late December posted a record high, just over 18,000 (See Chart 6). Strong economic growth in the U.S., readily available and inexpensive debt, soaring stock markets and plentiful IPOs are anticipated to encourage more owners to exit their businesses. 14 DUANE MORRIS — CONNECTIONS . Chart 6: U.S. Market Performance 120% 115% 110% 105% 100% 95% 90% 85% NASDAQ Composite Index (^COMP) - Index Value Russell 2000 Index (^RUT) - Index Value Dow Jones Industrial Average (^DJI) - Index Value S&P 500 Index (^SPX) - Index Value Source: Capital IQ 81% 60% Global The U.S. middle market is anticipated to follow the bulge bracket end of the market and become more active in 2015. According to EY’s survey, more than 70 percent of U.S.

executives expect deals in the $50 million to $250 million range Chart 7: U.S. Executives More Bullish on Improving M&A Market U.S. Growing optimism in the stability of the U.S. economic environment and recovery from the financial crisis are fueling U.S. executives’ confidence in the M&A market, according to EY’s October 2014 edition of its Capital Confidence Barometer.

It found that more than 80 percent of the U.S. respondents expected the global market for mergers and acquisitions to improve in the next 12 months. Reflecting geopolitical instability outside the United States, only 60 percent of global respondents were as optimistic (See Chart 7). Respondents expect the M&A market to improve Source: EY, “Big Deals Persist Generating Momentum in the Middle Market for 2015,” December 8, 2014 DUANE MORRIS — CONNECTIONS 15 .

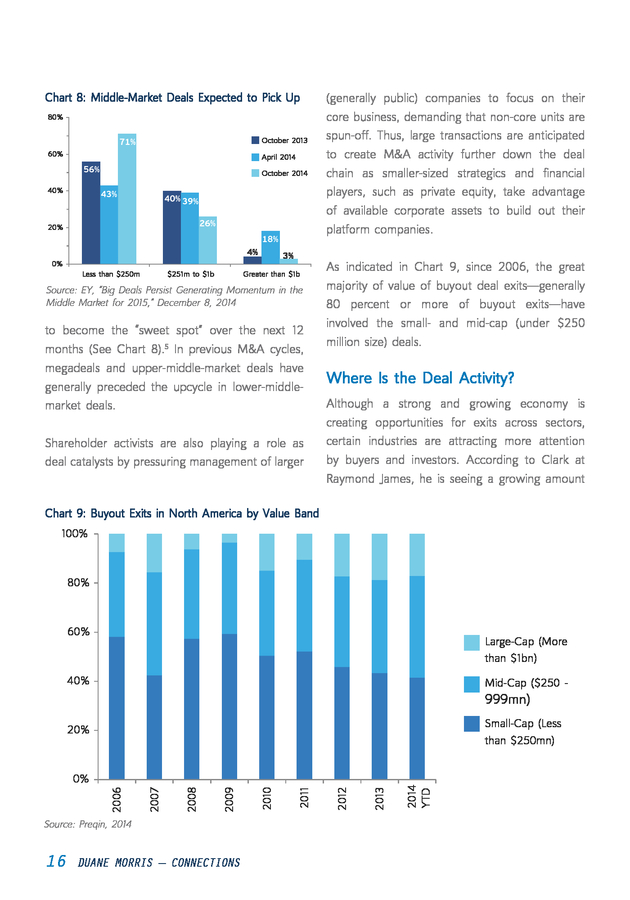

Chart 8: Middle-Market Deals Expected to Pick Up 80% 71% October 2013 60% April 2014 56% 40% October 2014 43% 40% 39% 26% 20% 18% 4% 3% 0% Less than $250m $251m to $1b Greater than $1b Source: EY, “Big Deals Persist Generating Momentum in the Middle Market for 2015,” December 8, 2014 to become the “sweet spot” over the next 12 months (See Chart 8).5 In previous M&A cycles, megadeals and upper-middle-market deals have generally preceded the upcycle in lower-middlemarket deals. Shareholder activists are also playing a role as deal catalysts by pressuring management of larger (generally public) companies to focus on their core business, demanding that non-core units are spun-off. Thus, large transactions are anticipated to create M&A activity further down the deal chain as smaller-sized strategics and financial players, such as private equity, take advantage of available corporate assets to build out their platform companies. As indicated in Chart 9, since 2006, the great majority of value of buyout deal exits—generally 80 percent or more of buyout exits—have involved the small- and mid-cap (under $250 million size) deals. Where Is the Deal Activity? Although a strong and growing economy is creating opportunities for exits across sectors, certain industries are attracting more attention by buyers and investors. According to Clark at Raymond James, he is seeing a growing amount Chart 9: Buyout Exits in North America by Value Band 100% 80% 60% Large-Cap (More than $1bn) 40% Mid-Cap ($250 - 999mn) Small-Cap (Less than $250mn) Source: Preqin, 2014 16 DUANE MORRIS — CONNECTIONS 2013 2012 2011 2010 2009 2008 2007 2006 0% 2014 YTD 20% . The Hot Sectors > Technology – A hot M&A sector, last year, the number of deals reached 2,400, up more than 13 percent over 2013 with deal value reaching $171.6 billion, a 26.7-percent increase. > Life Sciences – Although the number of deals reached only 603, down 18.7 percent from the prior year, deal value hit over $304 billion, up 49.5 percent compared to 2013. > Healthcare – Deal volumes were up slightly to 406, a 4.1-percent increase, but transaction values rose to $28.1 billion, up 25.1 percent from the prior year. > Consumer Products – 2014 transactions hit 963, up just 1.9 percent, while the rise in deal value jumped to $185.1 billion, or over 61 percent. > Financial Services – Deal volumes leveled off at 1,008, down 3.2 percent in 2014, with deal value also down 12.6 percent to $88.4 billion in 2014. Source: EY, “Big Deals Persist Generating Momentum in the Middle Market for 2015,” Press Release, December 8, 2014 of “interest in consumer-related sectors, whether it’s restaurants and other types of consumer businesses.” He says, “Institutional investors seem to believe that the consumer is going to come back and spend money.” Ecommerce businesses are also attractive, notes Clark, helped again by the “consumer angle.” He is seeing considerable activity in the technology sector, where people are betting on the future growth of these businesses. Finally, the master-limited partnership (MLP) structure, he points out, has been an attractive way for energy companies, especially midstream pipeline businesses, to exit. The collapse in oil prices has harmed MLPs recently, but some analysts note their performance is not directly correlated to oil-price trends as much as the E&P side of the business.6 According to EY, the U.S. sectors to watch for deal activity in 2015 include technology, life sciences, healthcare, consumer products and financial services.

In EY’s view, “Companies are either stripping down to their cores, or consolidating and pursuing acquisitions in order to fill gaps in innovation.”7 EY sees momentum built up in the five sectors over the last year being carried over to 2015. (See Box: The Hot Sectors). Over the past nine years, between 40 percent and 50 percent of private equity capital has been DUANE MORRIS — CONNECTIONS 17 . Chart 10: Private Equity Capital Invested by Industry 100% 90% B2B 80% 70% B2C 60% Energy 50% Financial Services Healthcare 40% 30% 20% IT 10% Materials & Resources 0% Source: PitchBook 4Q 2014 U.S. PE Breakdown, p. 12 directed at Business-to-Business (B2B) and the consumer (or B2C) sectors (See Chart 10). B2B showed the most impressive growth for the first three quarters of 2014.

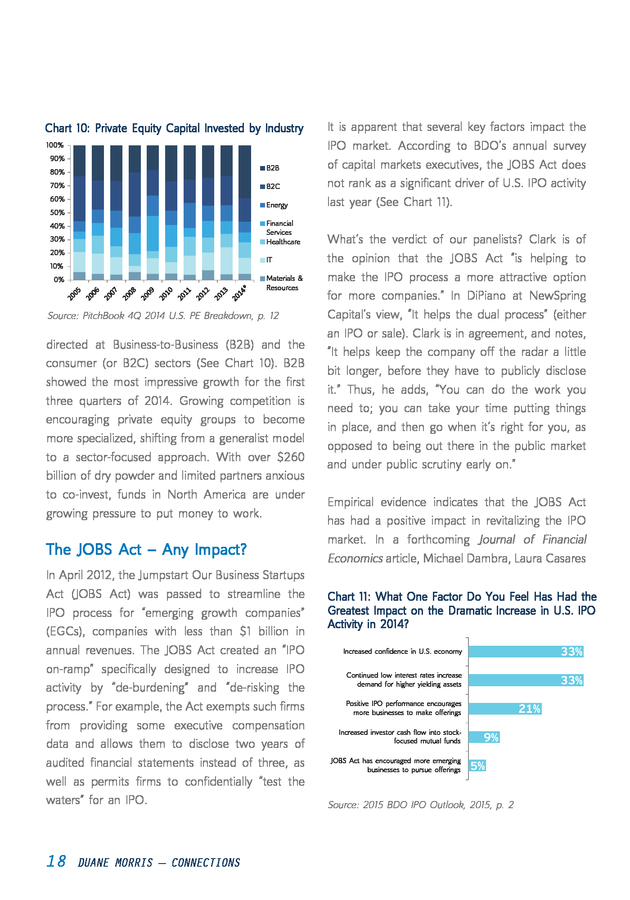

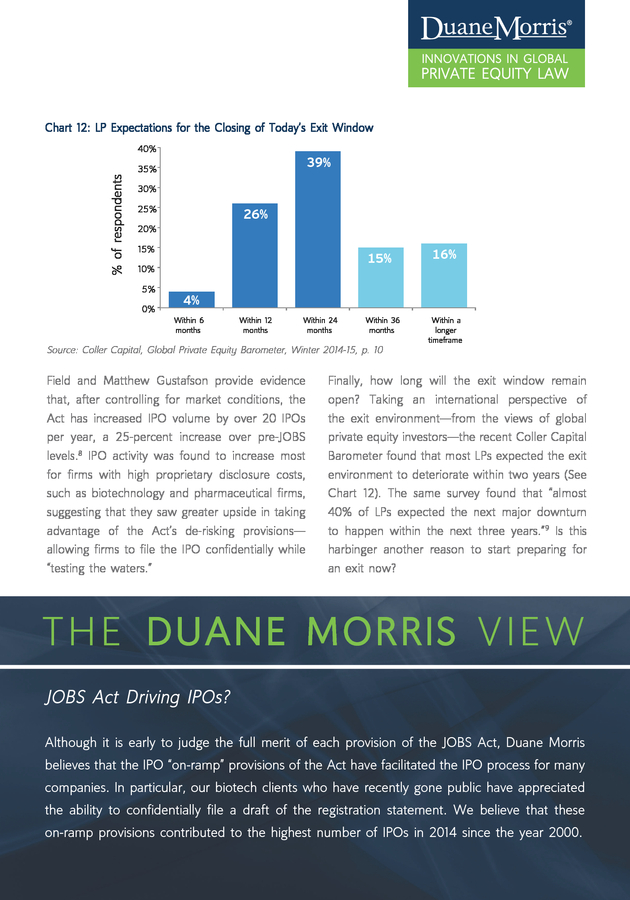

Growing competition is encouraging private equity groups to become more specialized, shifting from a generalist model to a sector-focused approach. With over $260 billion of dry powder and limited partners anxious to co-invest, funds in North America are under growing pressure to put money to work. The JOBS Act – Any Impact? In April 2012, the Jumpstart Our Business Startups Act (JOBS Act) was passed to streamline the IPO process for “emerging growth companies” (EGCs), companies with less than $1 billion in annual revenues. The JOBS Act created an “IPO on-ramp” specifically designed to increase IPO activity by “de-burdening” and “de-risking the process.” For example, the Act exempts such firms from providing some executive compensation data and allows them to disclose two years of audited financial statements instead of three, as well as permits firms to confidentially “test the waters” for an IPO. 18 DUANE MORRIS — CONNECTIONS It is apparent that several key factors impact the IPO market.

According to BDO’s annual survey of capital markets executives, the JOBS Act does not rank as a significant driver of U.S. IPO activity last year (See Chart 11). What’s the verdict of our panelists? Clark is of the opinion that the JOBS Act “is helping to make the IPO process a more attractive option for more companies.” In DiPiano at NewSpring Capital’s view, “It helps the dual process” (either an IPO or sale). Clark is in agreement, and notes, “It helps keep the company off the radar a little bit longer, before they have to publicly disclose it.” Thus, he adds, “You can do the work you need to; you can take your time putting things in place, and then go when it’s right for you, as opposed to being out there in the public market and under public scrutiny early on.” Empirical evidence indicates that the JOBS Act has had a positive impact in revitalizing the IPO market.

In a forthcoming Journal of Financial Economics article, Michael Dambra, Laura Casares Chart 11: What One Factor Do You Feel Has Had the Greatest Impact on the Dramatic Increase in U.S. IPO Activity in 2014? Increased confidence in U.S. economy 33% Continued low interest rates increase demand for higher yielding assets 33% Positive IPO performance encourages more businesses to make offerings Increased investor cash flow into stockfocused mutual funds JOBS Act has encouraged more emerging businesses to pursue offerings 21% 9% 5% Source: 2015 BDO IPO Outlook, 2015, p.

2 . Chart 12: LP Expectations for the Closing of Today’s Exit Window % of respondents 40% 39% 35% 30% 25% 26% 20% 15% 5% 0% 16% 15% 10% 4% Within 6 months Within 12 months Within 24 months Within 36 months Source: Coller Capital, Global Private Equity Barometer, Winter 2014-15, p. 10 Field and Matthew Gustafson provide evidence that, after controlling for market conditions, the Act has increased IPO volume by over 20 IPOs per year, a 25-percent increase over pre-JOBS levels.8 IPO activity was found to increase most for firms with high proprietary disclosure costs, such as biotechnology and pharmaceutical firms, suggesting that they saw greater upside in taking advantage of the Act’s de-risking provisions— allowing firms to file the IPO confidentially while “testing the waters.” Within a longer timeframe Finally, how long will the exit window remain open? Taking an international perspective of the exit environment—from the views of global private equity investors—the recent Coller Capital Barometer found that most LPs expected the exit environment to deteriorate within two years (See Chart 12). The same survey found that “almost 40% of LPs expected the next major downturn to happen within the next three years.”9 Is this harbinger another reason to start preparing for an exit now? T he Duane Morris V i e w JOBS Act Driving IPOs? Although it is early to judge the full merit of each provision of the JOBS Act, Duane Morris believes that the IPO “on-ramp” provisions of the Act have facilitated the IPO process for many companies. In particular, our biotech clients who have recently gone public have appreciated the ability to confidentially file a draft of the registration statement.

We believe that these on-ramp provisions contributed to the highest number of IPOs in 2014 since the year 2000. DUANE MORRIS — CONNECTIONS 19 . TiMing, PreParaTion and MoMenTuM N Market Conditions and experience “No tree grows to the sky forever,” is a saying often used to indicate the natural limitations to growth that all companies and markets face. It also highlights the significance for owners to consider how to time the exit from their companies. Generally, company founders may look to exit for a variety of reasons—to diversify their wealth, or on the negative side, because of one of the three Ds: death, divorce or a dispute.10 20 DUANE MORRIS — CONNECTIONS . To what does Gillin at Relay Network attribute “the failure led to a playbook for how to do it the success of getting the exit process and right the next time,” he emphasizes (See Box: timing right for Ecount, the business he sold in Gillin’s Exit Playbook). 2007? A failed earlier exit, in 2004, provided a highly valuable learning experience. As he tells Market conditions are a key factor in determining the story, “We did absolutely everything wrong.” the timing of an exit. When he was navigating With a $40 million offer from Experian on the Ecount’s exit the next time around, Gillin’s big table, Gillin remembers bringing everyone in the focus was on “things we cannot control.” As a room to announce the deal before we “verified new type of payments company offering a new any of it.” He did not think it was necessary for technology, this meant the regulatory environment Ecount to run a full exit process since a suitor would be a big deciding factor. Unlike PayPal, “came to us.” The deal did not get done—but he says, which was fighting these battles, “We Lessons Learned: Matt Gillin’s Exit Playbook > Be clear on the likely outcome (IPO, sale or other) > Prep early for the process > Get the board “on board” > Remember your fiduciary responsibility to all shareholders > Interview several bankers and hire the “right” one > Hire an experienced lawyer who’s been there, done that > Prepare targeted communications campaign to employees > Find a way to make all employees “feel good” about the outcome Source: Relay Network, LLC (2015) DUANE MORRIS — CONNECTIONS 21 .

did not have the war chest to really contest the decision.” Gillin had the choice of taking stock, regulatory stuff that was coming down the pike, which Stine says, “typically is going to be a tax- and we knew that a financial institution could.” free or tax-deferred deal until you sell the stock.” Alternatively, he continues, Gillin “could have Luck is also involved. At the time Gillin signed taken cash, which is all taxable.” While offering the deal to sell Ecount to Citibank in March 2007 tax benefits, the downside risk is that “now you and chose to take cash instead of stock, the have got somebody else’s paper and you do not market was frothy. “In hindsight, we looked like control the company anymore,” declares Stine. geniuses,” recalls Gillin as the market was about to collapse. The decision was made easier, as Identifying the Exit Tipping Point prior to the sale, he had discussions with five As an investor and board member of Ecount bankers that provided comfort and clarity over at the time, DiPiano at NewSpring Capital was “how the exit would shape up.” not convinced it was time to sell.

As he recalls, “We were executing superbly, Matt’s team and Stine at Grant Thornton underlines an important leadership were great, we had turned the corner lesson: “Do not let the tax answer force you on profitability, and cash was flowing significantly.” into a decision that is not the right economic Attendees listen to our panel discussion, their rapt attention evident. 22 DUANE MORRIS — CONNECTIONS . With “very high recurring revenue,” the business of investments, NewSpring Capital had the safety was attractive to hold, notes DiPiano, especially of a diversified portfolio whereas Gillin, focused because “we did not know that the world was on one business, did not. “Well, I can solve for going to enter into a recession.” the bank account by doing a recap if we really think there’s a lot of growth in the business,” is Having worked with many entrepreneurs, DiPiano how DiPiano approached the problem. says he was cognizant that as the chief owner of at least on paper, but “it was not necessarily in his Market and Regulatory Conditions Matter pocket.” As an investor and board member, a lot Ultimately, recalls DiPiano, Gillin convinced him of DiPiano’s discussions “were trying to verify that that “the regulatory issues were real, and that, the pressures of the regulatory environment were while we may be able to deal with them, the influencing Matt and not potentially what was cash required to do that was going to potentially going to be in his bank account.” With a number create difficulties.” From there, we “agreed that his company, Gillin had created significant value, DUANE MORRIS — CONNECTIONS 23 . if the valuation was $158 million we would sell— In answering the question, “Is this the right time?” and it was way over that,” he says. DiPiano gives he also recommends putting yourself in the Gillin substantial credit for “doing the right thing buyer’s shoes. “You want to leave some upside as a leader to work out the exit process with and some growth opportunities for the next his board members and shareholders and, in his owner, especially if it is a private equity firm,” case, some of his family members, who were Clark stresses. From the perspective of the next also shareholders.” owner, “They want to be able to say, ‘I’m going to buy the business and there is going to be Clark at Raymond James cautions against trying growth for me.’” Conversely, “If all the growth is to sell at a market peak.

He notes, “The problem out of the business, it is not really that exciting, is, you do not know the peak until you have and you are not going to get the valuation for it.” actually hit it, and at that point, you are now go right now.’” In his view, people also “make the Moving Forward with Purpose: Managing Communications, Positioning the Company and Achieving Momentum mistake in waiting too long,” saying, “Well, there The playbook Gillin created from the first failed is a little bit more opportunity here, the market is exit proved highly valuable in preparing him for his still strong, I’m going to wait.” next attempt. “We started interviewing bankers a going down the other side.” And given that the exit processes take a while, Clark believes, “You cannot just say, ‘I see the peak and I am going to Relay Network’s Matt Gillin (center) discusses his sale of Ecount, with NewSpring Capital’s Mike DiPiano (left) and Raymond James’ David Clark (right) listening closely. 24 DUANE MORRIS — CONNECTIONS . year before we wanted to sell,” he says, and “we to the banks was, “We want to get a sense as to kept the process to a small group of employees, what the market would be willing to bear.” and the board.” Gillin underscores that how you Clear communicate to the marketplace is vital, because management team is also necessary to move “you need to manage the marketplace’s opinion the deal forward. Speaking about the board’s of a company that is running through an exit perspective, Gillin says that “the best advice I got process.” At this early stage, he says, the message was to get a number” from the key constituencies. communication between board DUANE MORRIS — CONNECTIONS and 25 . 26 DUANE MORRIS — CONNECTIONS . He explains, “The moment you come in with what all prospective bidders “heard the same pitch.” the numbers are, the moment the number leaves In addition to taking questions from potential your mouth, it’s human nature that you want bidders, the firm addressed its own questions more.” By getting “a number” from everybody, with answers that “really positioned the company the management team and the board were as effectively as possible,” he mentions. As a aligned. Another key step Gillin learned through result of this novel approach, “we didn’t have to the failed transaction “was to go through the cap do a bunch of sit-downs” and “we cut down the table, understand what the distribution looks like number of bidders to a manageable number— and make sure that there were no surprises.” from 34 to 9.” As the process advances, “You have to start In getting ready for a transaction, “the most letting in more people at the company,” and Gillin important thing” is that the process “doesn’t shut emphasizes you have to manage this carefully, down your business,” Gillin notes. Making sure given that a message that the founder is cashing your business is in order before initiating an exit out may negatively impact employees who are is essential, says DiPiano.

Delays in closing a responsible for achieving the firm’s growth. “So transaction can become permanent, he mentions, the first and most important thing you can do and “not crossing the goal line can be disastrous.” is to make sure that it is a win for everybody,” In his experience, the exit decision sets in motion he says. We achieved this, he recounts, by a number of decisions, “everybody has counted making certain all the employees “knew what the the money, everybody is trying to figure out their transaction meant to them.” Gillin adds, “All of a new roles [and] some people are already starting sudden, everyone is on the same page moving to interview for new jobs.” Thus, “You really two steps at a time to ensure, for example, the want to evaluate your own business, your legal data room is set up properly.” records, everything you can think of to make sure your house is in order,” DiPiano emphasizes. Running an Efficient Auction Communication is especially vital in positioning Generating a sense of urgency is another key a company in an auction, which Gillin decided step, according to Gillin, which he learned the was the best way to maximize the value of the hard way.

He relates that back in 2000, “We had firm. The downside of an auction, he says, was a transaction with Softbank to put $50 million that it could involve many players, which could into our company.” In pushing a deal discussion be distracting and a lot of work. The firm took from Friday to Monday, which became Tuesday, an innovative step by creating an interactive “the day the market crashed—so we never got webinar to position the company and ensure that money.” Therefore, in preparing for the deal DUANE MORRIS — CONNECTIONS 27 .

The crowd is engaged and focused on the stimulating discussion. with Citi, “everyone was aligned with the urgency Clark points out that “When they buy a business, of getting it done quickly,” he notes. “As a matter most private equity firms are already starting to of fact, we moved our closing up a month.” think about the exit.” This is part of the process of visualizing a firm’s growth path and how it Starting Gun: When Should the Clock Start? is going to get there, and asking: “Where do How long should owners expect the exit process helps to “make sure you’ve got good numbers, to last? “To run a sale process from the time you you’ve got your accountants looking at the engage a banker to when you close is going to be numbers and being prepared, and you’ve got around six months,” says Clark. This is the time the lawyers looking at structure and everything,” it takes for the banker to do their work—“doing he says. Initiating discussions with bankers and their diligence, preparing the information that private equity firms will provide better answers needs to be prepared and getting the data room to questions like: “Where can I take the business ready.” But for owners to really ensure everything and what’s going to make my business attractive is prepared, they need to “start thinking about it to a strategic, or to a private equity firm?” a year before [they] start a process.” 28 DUANE MORRIS — CONNECTIONS I ultimately want to see the business?” This .

“If you’re central to your company, and don’t Gillin, who is onto his third business, says that want to be with the buying company, you might “If there’s a high probability that you’re going to want to think about it two years in advance,” sell the company, then there are things that you DiPiano suggests. “If you want to avoid being can do every day.” In his view, these are “simple swept into the purchase, then you have to start things like how you store your data and how you thinking even earlier about your succession to tell the story about how you operate.” Changes put a professional leader in the company,” he that “help in managing the business better, the notes. Stine at Grant Thornton agrees, saying type of people you hire, the systems you put in that “When we sold Smart, we started two-and- place,” he continues, are all things “you can do a-half years in front.” In the end, he continues, on day one.” “it worked out very well,” as it provided time “to restructure the firm, create the buzz and accomplish a whole ton of stuff.” T he Duane Morris V i e w Thinking About Your Exit? Remember the Boy Scout Motto. Yes, the Boy Scout Motto—“Always be prepared”—together with its corollary, “If you’re not prepared, start getting that way, now,” should be twin beacons for a business owner contemplating the sale of a business. In this regard, owners should pay special heed to the methods of private equity groups, masters of focus and preparedness, that start thinking on day one about what their exit will look like—possibly years down the road.

Depending on the company, “preparedness” could mean a top-to-bottom scrub down—cleaning up the books; ensuring protection of intellectual property, including trade secrets; and possibly even hiring a CFO if the company does not have one. If an IPO is a viable option—as opposed to selling to strategic player or a private equity group—the level of scrutiny will take on a whole new level of intensity; for example, composition of the board of directors. Owners who have been through the process before maintain a state of preparedness for sale as a basic operating principle. DUANE MORRIS — CONNECTIONS 29 .

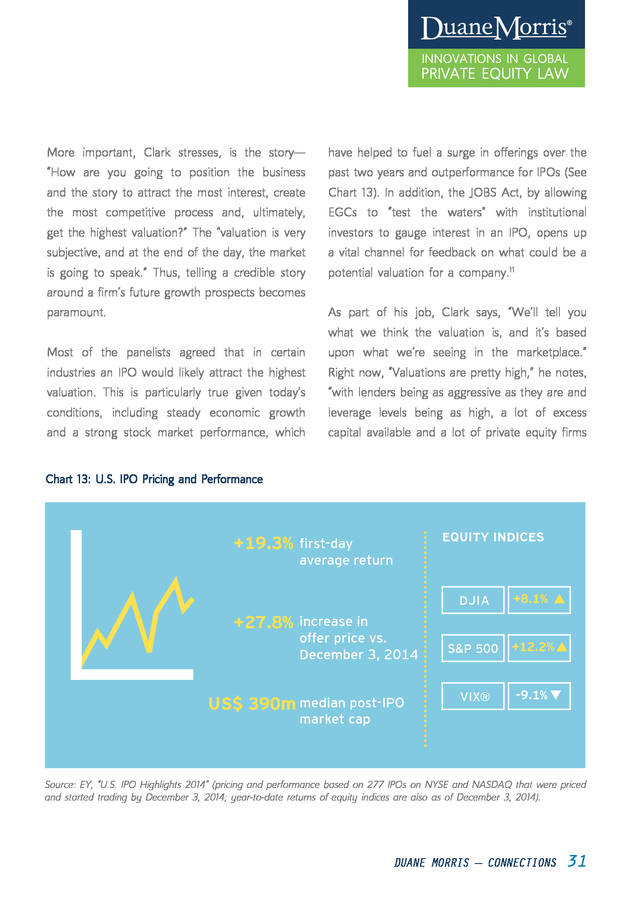

From left: Duane Morris’ Darrick Mix addresses the audience and our panelists. valuaTion, besT buyer and CerTainTy around Closure I In Clark’s view, coming up with a valuation for a company is a key step, but one that must be taken into context with other factors, such as “determining the right process to go down, and who is the right partner or buyer you want to be dealing with.” For example, if an owner of a family owned business wants to stay involved and continue to own a meaningful stake, “the highest valuation may not be the most important objective.” Instead, he continues, “finding the right partner, investor or private equity firm to help grow the business” takes precedence. 30 DUANE MORRIS — CONNECTIONS . More important, Clark stresses, is the story— have helped to fuel a surge in offerings over the “How are you going to position the business past two years and outperformance for IPOs (See and the story to attract the most interest, create Chart 13). In addition, the JOBS Act, by allowing the most competitive process and, ultimately, EGCs to “test the waters” with institutional get the highest valuation?” The “valuation is very investors to gauge interest in an IPO, opens up subjective, and at the end of the day, the market a vital channel for feedback on what could be a is going to speak.” Thus, telling a credible story potential valuation for a company.11 around a firm’s future growth prospects becomes As part of his job, Clark says, “We’ll tell you paramount. what we think the valuation is, and it’s based Most of the panelists agreed that in certain upon what we’re seeing in the marketplace.” industries an IPO would likely attract the highest Right now, “Valuations are pretty high,” he notes, valuation. This is particularly true given today’s “with lenders being as aggressive as they are and conditions, including steady economic growth leverage levels being as high, a lot of excess and a strong stock market performance, which capital available and a lot of private equity firms Chart 13: U.S. IPO Pricing and Performance +19.3% first-day average return Equity indices DJIA +27.8% increase in offer price vs. December 3, 2014 US$ 390m median post-IPO +8.1% S&P 500 +12.2% VIX® -9.1% market cap Source: EY, “U.S.

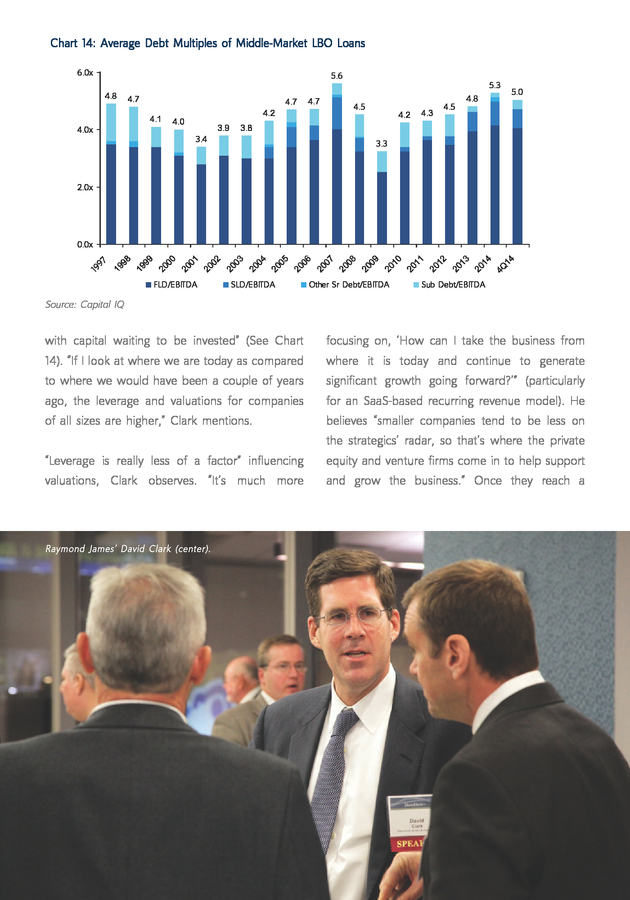

IPO Highlights 2014” (pricing and performance based on 277 IPOs on NYSE and NASDAQ that were priced and started trading by December 3, 2014; year-to-date returns of equity indices are also as of December 3, 2014). DUANE MORRIS — CONNECTIONS 31 . Chart 14: Average Debt Multiples of Middle-Market LBO Loans 6.0x 5.6 4.8 4.7 4.1 4.0x 4.2 4.0 3.9 4.7 4.7 5.3 4.5 4.2 4.3 4.5 4.8 5.0 3.8 3.4 3.3 2.0x FLD/EBITDA SLD/EBITDA 13 12 14 4Q 14 20 20 11 20 10 09 Other Sr Debt/EBITDA 20 20 20 07 08 20 20 05 06 20 20 03 04 20 20 01 02 20 20 99 98 00 20 19 19 19 97 0.0x Sub Debt/EBITDA Source: Capital IQ with capital waiting to be invested” (See Chart focusing on, ‘How can I take the business from 14). “If I look at where we are today as compared where it is today and continue to generate to where we would have been a couple of years significant growth going forward?’” (particularly ago, the leverage and valuations for companies for an SaaS-based recurring revenue model). He of all sizes are higher,” Clark mentions. believes “smaller companies tend to be less on the strategics’ radar, so that’s where the private “Leverage is really less of a factor” influencing equity and venture firms come in to help support valuations, Clark observes. “It’s much more and grow the business.” Once they reach a Raymond James’ David Clark (center). 32 DUANE MORRIS — CONNECTIONS .

Conversations continued flowing, even after our panel discussion wrapped up. certain size, “the strategics jump in,” and with a bigger customer base and opportunities to crosssell, they can justify paying a big multiple for the business. A key takeaway for DiPiano is that it is “a huge mistake to focus on one valuation that’s the highest in your peer group when you’re selling.” Clark agrees, noting that “It’s not in anybody’s interest to give an inflated view on value and set expectations too high.” His goal is “to set expectations at a reasonable level and then, ultimately, exceed that during the process.” DiPiano stresses, that in addition to being realistic, “also look at your cap table to ensure everybody moves forward with a purpose.” Exclusivity and Quality of Earnings Report To gain certainty to close and keep the bidding process honest, DiPiano suggests sellers have two bidders go through exclusivity. NewSpring Capital has been involved in this approach twice, and in both cases, “the seller offered to pay the losing bidder’s expenses.” He notes that “When one bidder has exclusivity, the seller loses some leverage,” and there is a fear of losing momentum. Both deals had a high degree of certainty to close and the close happened, relates DiPiano. Another practice to lessen uncertainty around closure is to “have the seller pay to do a quality-of- DUANE MORRIS — CONNECTIONS 33 . Do’s and Don’ts – Lessons from Exit Frontlines > Start by building an enduring business, as businesses are bought, not sold. > The owner must be committed. > Decide what you want monetarily and from a timing perspective, so that you’re purposeful. > Focus on getting ready for transaction—make sure process doesn’t shut down your business. > Choose your team—lawyer, banker, accountant—wisely and early. > Make sure your house is in order—your business, your legal records, etc.—as delays in the sales process can become permanent and disastrous. > Develop a relationship with one or more banks early to gain insight into the market, positioning of the firm and its valuation. > Start tax planning—how the ownership is structured, trusts in place, etc.—early to achieve greatest savings. > Manage the marketplace’s opinion of the company. > Make sure that the sale is a win for everybody and that everyone knows what it means to them. > No surprises—surprises are deal killers from perspectives of board, management team and buyer. > Prepare to manage communication full-time—24/7 effort. > The story around the business is vital—it will go a long way to attracting interest and determining valuation for the business. > Be realistic; don’t make a selling decision based on the highest valuation in your peer group. > Don’t try to play the market to sell at the peak—you are bound to miss it. > Don’t rely on the IPO as your exit, but reach out to potential buyers to gauge interest and consider dual track. > Pick the buyer carefully—sometimes, it is not the buyer with the highest price, but the buyer with the highest certainty of close, combined with a good value along with it. > Learn from your failures—create a playbook for the next exit. Source: Panelists 34 DUANE MORRIS — CONNECTIONS . earnings report prior to the process,” which Stine very fluid process and it is hard to predict who is says Grant Thornton is doing more and more. going to be the ultimate winner.” (See Box: “Do’s Some of the “biggest discussions between buyers and Don’ts.”) and sellers,” he notes, are around adjustments to earnings—e.g., “what is the true EBITDA or Clark reiterates that the best outcome will come revenue that we’re valuing the business off of”— from “getting everything done upfront and running which can be the “biggest trade on valuation.” as efficient a process as you can.” The highest Doing quality of earnings ahead of time, before price is not always the best guide to selecting a prospective buyers enter into a Letter of Intent buyer, says DiPiano: “Sometimes the buyer with (LOI), should speed up the process and create the highest certainty of close, combined with a more certainty around close. good value,” is better than the buyer offering the highest price. In summing up, Clark says, “The job of investment bankers is to package a story, run a process and ultimately get as much competitiveness in that process as they can and get the best outcome they can.” He emphasizes that “It is a T he Duane Morris V i e w How to See Around Corners The key to a successful process from the seller’s perspective is to engage advisers who can anticipate the potential obstacles in a transaction so that the seller is never surprised. One strategy to accomplish this is to ask the seller to look at his or her company as if it were a target of an unfriendly active investor in order to identify any particular issues that may be impacting the firm’s potential value so that they can be addressed in advance. DUANE MORRIS — CONNECTIONS 35 . 36 DUANE MORRIS — CONNECTIONS . ConClusion M Market conditions for U.S. middle-market owners considering exiting their businesses may never have been better. A stable U.S. economy, rising equity markets, easy access to favorable financing and a growing number of financial and strategic “I BelIeVe tHAt tHe buyers, taken together, make eNtRePReNeuR OwNeRfor a robust, seller-friendly exit MANAGeR OF A PRIVAte environment.

How long this window of opportunity will last is eNteRPRISe IS ONe OF anyone’s guess. tHe MOSt IMPORtANt PRO-eCONOMIC AND PROAs detailed in this report, the SOCIAl FORCeS ON tHe exit process is a well-worn path PlANet. tHAt IS BeCAuSe that has become increasingly eVeRYBODY SHAReS IN professionalized and sophisticated, tHe MASSIVe CAPItAl with a busy intersection of buyers GAINS CReAteD tHROuGH and sellers. Owners interested in tHe ReCAPItAlIZAtION achieving a “good exit” should OR SAle OF tHeSe consider taking advantage of this COMPANIeS.” evolving set of financial, legal and -Peter Worrell, Enterprise investor resources.

Careful and Value, 2014, p. 9. early preparation with the right team is essential to a successful wealth creation event—one whose benefits flow beyond the owner to investors, employees and broader stakeholders. In our view, a principal signpost of a “good exit” is how well the original owner and investors position the business to achieve future growth and how well its growth opportunities are clearly and convincingly articulated to the next owner. Exiting at a valuation that reflects future wealth creation opportunities and a strong business legacy provides perhaps the best and broadest measure of accomplishment and success. Duane Morris’ Heading for the Exit: Owner, Investor and Banker Perspectives was prepared with the assistance of the firm’s outside advisor David Haarmeyer. DUANE MORRIS — CONNECTIONS 37 .

SPEAKER profiles David Clark Managing Director, Head of Financial Sponsors Group, Raymond James & Associates David Clark joined Raymond James & Associates in 2009. Prior to joining Raymond James, he was a managing director at Lane, Berry & Co. International. Previously, David was a Director at UBS Warburg in the Global Industrial Group.

At UBS Warburg, He completed numerous debt, equity, M&A advisory and restructuring transactions. Prior to UBS Warburg, David worked for Dillon, Read & Co. and at Bank of Boston Corporation. David received his M.B.A.

from the Darden School of Business in 1997 and his B.A. in Economics from Harvard College in 1989. mike DiPiano Managing General Partner, NewSpring Capital Mike DiPiano serves as Managing General Partner, Partner and Managing Director at NewSpring Capital. Mike co-founded NewSpring Capital and is a part of the NewSpring Growth investment team.

Prior to joining NewSpring, Mike was a serial entrepreneur and investor; he led or co-led the investment into six companies in the business services, healthcare and information technology industries. He served as the Chief Executive Officer at Maxwell Systems from 1998 to 2002. He co-founded venture-backed startups; was affiliated with Safeguard Scientifics and its related funds; and served as Division Chief Executive Officer for six years at Chemical Leaman Corporation.

He started his career in 1980 with Baxter Healthcare Corporation. Mike holds an M.B.A. from the Stern School of Business at New York University and a B.S.

from Pennsylvania State University. Matt Gillin CEO and Co-Founder, Relay Network Matt Gillin is CEO and Co-Founder of Relay Network, a new technology company that connects trusted brands to their customers on a private, mobile communications network. At Relay, Matt is responsible for guiding the company’s strategy and overseeing the day-to-day operations. He has been an active entrepreneur and pioneer for nearly 20 years, and he has been widely recognized for turning innovative ideas into successful businesses.

Most recently, Matt served as the CEO of Ecount, a company he cofounded in his parent’s basement. Over a 10-year period, Matt built Ecount into a recognized leader in the prepaid card industry. In 2007, he sold the company to Citi and was successful in delivering considerable value to his investors and shareholders.

Following the sale to Citi, Matt remained as CEO of the renamed business and helped make Citi Prepaid Services the world’s first global prepaid solution provider. Prior to starting Ecount, Matt was also the co-founder of C/Base, a consultancy business that specialized in partnership marketing services for Internet-based companies. A recognized inventor and holder of three patents, Matt graduated with a B.A.

from Denison University. 38 DUANE MORRIS — CONNECTIONS . Darrick Mix Partner, Duane Morris LLP Darrick Mix practices corporate law with concentrations in the areas of securities law, mergers and acquisitions and corporate governance. He has experience representing public and private companies in connection with their capital-raising activities, including public offerings and private placements of equity and debt securities. Darrick also advises companies with respect to SEC regulations, compliance issues and other corporate and securities law matters, such as public reporting, Sarbanes-Oxley compliance and communications with analysts and investors. He has substantial experience representing public and private companies in selling and acquiring businesses, including private equity funds in control and minority investments. His clients span a variety of industries, including retail, financial services and REITs. Darrick is a 1997 graduate, with honors, of the Ohio State University, Michael E.

Moritz College of Law, and a graduate of Georgetown University’s School of Foreign Service. John Stine Assistant Office Managing Partner and Tax Partner, Grant Thornton LLP John Stine serves as the Assistant Office Managing Partner for the Philadelphia office, and as a senior tax partner in Grant Thornton’s Philadelphia tax practice. John has more than 38 years of experience with a wide variety of clients in varied industries, including manufacturing and distribution, financial services, technology, service companies and real estate. A teaming approach serves as the cornerstone of his business problem solving and transactions, and he uses his network of relationships with experts both inside and outside the firm to help his clients maximize value and reduce risks.

He has been involved in numerous business transactions both for buyers and sellers, as well as intra- and inter-family transactions. He is an alumnus of the Wharton School’s Accounting faculty, having served as a Lecturer for 20 years. DUANE MORRIS — CONNECTIONS 39 . About Duane Morris Private Equity Group With experienced private equity lawyers across our global platform, coupled with the deep capabilities of more than 700 lawyers across all practice areas, Duane Morris offers the resources to optimize transactional value for sellers and buyers; advise on formation of funds and other investment structures; introduce its extensive network of relationships; support portfolio company operations; and structure wealth planning strategies for sellers. Capital Markets Group With attorneys in all major financial centers across the U.S. and throughout the UK, Europe and Asia, Duane Morris routinely advises clients on securities issues specific to public companies and assists with preparing and filing registration and proxy statements, reports and other SEC filings, as well as private placement memoranda and related private offering materials. A number of our lawyers have served in SEC staff positions and hold leadership positions in professional and securities industry organizations, enhancing our ability to provide keen insights into novel policy and regulatory issues. We leverage our industry knowledge and contacts with underwriters, placement agents, investment banks and private investment funds to identify possible partners who can help our clients grow their businesses. Duane Morris is proud to be an Official Sponsor of Growth® of the Association for Corporate Growth (ACG). 40 DUANE MORRIS — CONNECTIONS .

Lo Chicago Lake Tahoe San Francisco Silicon Valley Las Vegas Los Angeles San Diego Pittsburgh Atlanta Houston Boston New York Newark Cherry Hill Philadelphia Wilmington Baltimore Washington, D.C. Boca Raton Miami Mexico City Duane Morris Office Representative / Liaison Office London, UK Chicago Pittsburgh Atlanta Houston Boston New York Newark Cherry Hill Philadelphia Wilmington Baltimore Washington, D.C. Shanghai, China Oman Singapore exico City United States Lake Tahoe Las Vegas Los Angeles Miami New York Newark Philadelphia Ho Chi Minh City Sri Lanka Boca Raton Miami Atlanta Baltimore Boca Raton Boston Cherry Hill Chicago Houston Hanoi, Vietnam Myanmar Pittsburgh San Diego San Francisco Silicon Valley Washington, D.C. Wilmington International Hanoi Ho Chi Minh City London Mexico City (alliance) Myanmar Oman Shanghai Singapore Sri Lanka (alliance) DUANE MORRIS — CONNECTIONS 41 . Notes 1 Dana Mattioli and Dana Cimilluca, “Deal Boom Feeds on Surging Stocks,” The Wall Street Journal, November 17, 2014. 2 All IPO data was provided by EY. 3 Dawn Lim, “Investors Struggle to Get Into Some Private Equity Funds,” The Wall Street Journal, December 29, 2014. Arleen Jacobius, “Assets Invested in Separate Accounts Starting to Add Up,” Pensions & Investments, December 22, 2014. 4 EY, “Big Deals Persist Generating Momentum in the Middle Market for 2015,” Press Release, December 8, 2014. 5 Michael Aneiro, “Do Natural-Gas MLPs Face More Downside Ahead?” Barron’s, December 30, 2014. 6 EY, “Big Deals Persist Generating Momentum in the Middle Market for 2015,” Press Release, December 8, 2014. 7 Michael Dambra, Laura Casares Field and Matthew Gustafson, “The JOBS Act and IPO Volume: Evidence That Disclosure Costs Affect the IPO Decision,” 8 forthcoming at Journal of Financial Economics; available at Social Science Research Network, August 26, 2014. Coller Capital, Global Private Equity Barometer, Winter 2014-15, p. 10. 9 10 Luke Johnson, “How Entrepreneurs Can Secure a ‘Good Exit’ from Their Company,” Financial Times, December 30, 2014. 11 Edward Teach, “On the IPO On-Ramp,” CFO Magazine, September 15, 2014. This publication is for general information and does not include full legal analysis of the matters presented. It should not be construed or relied upon as legal advice or legal opinion on any specific facts or circumstances. The invitation to contact the attorneys in our firm is not a solicitation to provide professional services and should not be construed as a statement as to any availability to perform legal services in any jurisdiction in which such attorney is not permitted to practice.

©2015 Duane Morris LLP. . . INNOVATIONS IN GLOBAL PRIVATE EQUITY www.duanemorris.com Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Philadelphia | Chicago | Washington, D.C. | San Francisco Silicon Valley | San Diego | Boston | Shanghai | Houston | Los Angeles | Hanoi | Ho Chi Minh City | Atlanta | Baltimore | Wilmington | Miami Boca Raton | Pittsburgh | Newark | Las Vegas | Cherry Hill | Lake Tahoe | Myanmar | Oman | Duane Morris LLP – A Delaware limited liability partnership .

A key takeaway from the event is the overriding importance of preparedness—getting out ahead of the process, e.g., clearly understanding what you as an owner-manager want to accomplish, deciding what approach to take to get there and choosing your team. Although preparedness may not guarantee a “good exit,” unpreparedness is most likely to lead to a “bad exit”—the sale does not close, a founder suffers seller’s remorse, employees feel let down and the legacy of the business is in question. We trust that you will find this publication, a collaborative effort of Duane Morris’ Private Equity and Capital Markets groups, to be both thought-provoking and a helpful guide to the exit process. Please let us know what you think. Pierfrancesco Carbone Co-Head of Private Equity – UK / Europe Duane Morris LLP Richard P. Jaffe Co-Head of Private Equity Duane Morris LLP Darrick Mix Partner Capital Markets Duane Morris LLP DUANE MORRIS — CONNECTIONS 1 .

From left: NewSpring Capital’s Mike DiPiano, Relay Network’s Matt Gillin and Raymond James’ David Clark contemplate the market environment. MarkeT environMenT: The MaCro overview D “Deal Boom Feeds on Surging Stocks” was the front-page story in The Wall Street Journal the day before Duane Morris’ “Heading for the Exit” event.1 The story noted that global M&A volume had already breached the $3 trillion mark for the year, up 32 percent over the similar period in 2013, as companies took advantage of rising stock prices and cheap credit, both a function of the Federal Reserve’s easy-money policies. The U.S. accounted for about half of this amount by value, up 37 percent relative to 2013 (See Chart 1). 2 DUANE MORRIS — CONNECTIONS . Chart 1: Big Year for North American M&A 6000 1,200.00 1,000.00 800.00 600.00 percent in 2014—indicating it was another good 3000 1,400.00 the majority of the value of IPOs—by nearly 62 4000 1,600.00 2000. Financial sponsors continue to account for 5000 1,800.00 $Billion non-financial sponsors) were the highest since year for investors of private equity funds.2 2000 400.00 1000 0.00 The corporate buying spree and strong IPO market 0 200.00 are occurring despite serious headwinds, such as 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Deal Value ($B) Deal Number Source: Capital IQ Includes transactions with disclosed value over $10mm recent market volatility, a weakening Chinese economy, Japan falling back into recession, continued lackluster economic performance in Europe and a faltering Russian economy. 2014 was also a big year for IPOs, which by value jumped by nearly 77 percent from the previous Panelists at the Duane Morris event were year to nearly $60 billion (See Chart 2). The generally upbeat, with Mike DiPiano, Managing 291 North American listings (by financial and General Partner and founder of NewSpring Chart 2: Value of Financial- and Non-Financial Sponsor-Backed IPOs 110 450 100 400 90 350 80 $ Billions 60 250 50 200 40 Number 300 70 150 30 100 20 50 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Non-PE IPO proceeds PE IPO proceeds 2012 2013 2014 0 PE IPO number Non-PE IPO number Source: EY DUANE MORRIS — CONNECTIONS 3 . Capital, observing that he did not see interest Office Managing Partner and Tax Partner at Grant rates rising much; hence, “there’s going to be Thornton LLP, notes that his firm is “unbelievably debt available.” In addition, he continues, “There busy on transactions right now,” which is not the is a fair amount of capital with buyout shops norm for this time of year. like ours that are paid to put money to work,” which would encourage the industry “to continue In Clark’s view, 2015 “is going to be another buying” and “the IPO market to perk up.” strong year” and “the IPO market is going to continue to be solid,”—barring any unexpected David Clark, Managing Director, Head of Financial events. Plenty of prospective buyers and an Sponsors Group at Raymond James & Associates, improving economy translate into a seller’s agrees with DiPiano—“Our economist’s view is market. A number of private equity firms, as well that interest rates may go up, but they are not as family-owned businesses, “have reached out going to go up by that much, so there’s still to us to talk about their business,” he says. The plenty of capital out there.” In addition to private question on their mind is: “Is this a good time equity money, “there is a lot of cash on the to exit, and if so, how is the best way to do balance sheets” of strategics, he noted.

Clark also it?” That said, from a buyer’s perspective, “The highlighted that limited partners increasingly want market is very frothy with a lot of capital chasing co-invest opportunities. deals,” Clark observes. Turning the spotlight on another leading indicator Indeed, the successful exit market last year, which saw private equity funds return an expected $479 of the market’s direction, John Stine, Assistant T he Duane Morris V i e w You can’t time a sale, but . . . A significant factor contributing to the liquidity the industry is experiencing is that the constellation of potential buyers and strategies has expanded well beyond the usual suspects. This phenomenon provides sellers—provided that they are well prepared—with more leverage so that they can better tailor an exit to address their particular goals and needs. 4 DUANE MORRIS — CONNECTIONS .

Chart 3: 2014 Saw Jump in Distributions and Fundraising ($Billion) Distributions 500 Fundraising 400 300 200 100 0 $171 BN Annual Average 2009-2013 $479 BN $270 BN 2014 Annualized Annual Average 2009-2013 $450 BN 2014 Estimate Source: Triago, The Triago Quarterly, November 2014, p. 1 billion globally, is likely to create an even more crowded deal market in 2015 as investors reinvest (See Chart 3).3 According to Preqin data, the proportion of funds that reached or exceeded their “hard cap” (i.e., maximum amount the firms set out to raise) in 2014 was at its highest level since 2009. capital—has been growing over the past few years. Hamilton Lane estimates that this pool of capital represents about 50 percent of the cash raised by traditional U.S. funds.4 Therefore, going into 2015, close to $670 billion in capital will be looking to get invested in deals—exclusive of money the strategics bring to the table. In addition to more capital cycling back to commingled funds, “shadow fundraising”—which includes money investors set aside for coinvestment, separate accounts and secondary DUANE MORRIS — CONNECTIONS 5 .

The exiT ProCess: key QuesTions and Players C Careful preparation and execution are two preconditions to a successful exit. “The key is getting prepared and getting everything done upfront, and running as efficient a process as possible,” observes Clark at Raymond James. “At the end, that’s where the value’s going to be,” he says. Thus, Clark spends considerable time with owners to provide guidance on whether “this is the right time for your business to come to market and exit,” and if so, “How do you want to do it? What is the best process?” .

Part of the answer on whether “this is the right time,” Clark notes, turns on “What are the intentions of the management team?” Owners may want to exit the business completely or perhaps stay on longer, but gain some liquidity. Clark indicates that “It is always harder to exit a business if the management team—senior management and CEO—is looking to retire and move on.” Having a good management team in place makes the business more stable and attractive, especially for private equity firms that typically are focused on backing management teams. As an interim step, he suggests that “the number two [in charge] be elevated to the CEO position to run the business for a period of time before the exit.” energy and funds wasted when owners have pulled back from an exit at the last minute. “If you are only halfway committed, it will not work well,” Stine observes. Considerations about the timing of an exit, says Clark, are really about the business: “Where is it in the cycle, what growth is expected down the road, and if there is a lot of growth expected— can the owner get value for that growth today?” He adds that “to really position the company for the best exit,” it is vital to “understand the business opportunity over the next couple of years and how value can be generated, whether through organic growth or by acquisitions.” Exit Alternatives Alternatively, a CEO may agree to stay for a transition period. Stine at Grant Thornton emphasizes that “owners need to be committed,” as announcing their plans to exit the business puts the firm at risk.