Description

Winter 2014/2015

OPTIMIZE

VALUE FROM DISTRESSED ASSETS

THE NEED FOR SPEED

A race to sale, stalking horses galloping out

of the gate—in a slow bankruptcy market,

why are debtors and creditors in such a hurry?

Insights from Duane Morris’

32nd Annual Conference

Apollo Global Management

CBIZ MHM, LLC

Executive Sounding

Board Associates LLC

Imperial Capital

DUANE MORRIS - OPTIMIZE

1

. OPTIMIZE

VALUE FROM DISTRESSED ASSETS

THE NEED FOR SPEED

ANATOMY OF THE LOAN CYCLE

AN EXAMINATION OF THE LIFE CYCLE OF A CREDIT FACILITY,

FROM INCEPTION TO COMPLETION/TERMINATION

2

DUANE MORRIS - OPTIMIZE

. TABLE OF CONTENTS

02

LETTER FROM THE EDITORS

04

STATE OF PLAY: CREDIT IS

KING, RISK IS REASONABLE

09

FILINGS DOWN; WHEELS UP

14

SPRINT OR MARATHON?

18

SPEAKER PROFILES

20

ABOUT DUANE MORRIS

DUANE MORRIS - OPTIMIZE

1

. LETTER FROM THE EDITORS

In the aftermath of the financial crisis, the U.S. federal government provided banks with liquidity and

incentives to lend money to borrowers. Interest rates plummeted. Companies took on more debt to stay

afloat.

The results have been lasting: companies are still able to access cheap financing, thereby quelling the tide of bankruptcy filings, which continues to ebb. While there was speculation that 2014 might find retail, shipping and municipalities turning to the bankruptcy courts, for the most part, filings are at historical lows. However, bankruptcy professionals aren’t sitting on the sidelines. Pre-petition workouts, out-of-court restructurings and other alternatives remain popular.

When a chapter 11 case is filed, it’s increasingly common to consider a shorter, less expensive path: an asset sale, allowed under Section 363 of the Bankruptcy Code, for the benefit of the debtor, the buyer and, occasionally, creditors. Keeping pace with the speed of those deals—more sprint than marathon—requires a knowledge of the ins and outs of the Bankruptcy Code, the economy, and the politics of each deal. Gerard S. Catalanello James J. Vincequerra Partner, Duane Morris Partner, Duane Morris Business Reorganization and 2 Business Reorganization and Financial Restructuring Practice Group Financial Restructuring Practice Group DUANE MORRIS - OPTIMIZE .

And, of course, it is essential to choose the right bankruptcy team. In this publication, Duane Morris partners come together with financial industry and restructuring professionals to share commentary and insights into the markets and best practices for distressed companies, and the bankruptcy professionals who help debtors and creditors. It’s our goal with each event and subsequent issue of Optimize to provide clients with the very best in legal and business thought leadership in order to leverage the knowledge and experience of some of the most vital players in the industry. We hope you find this third edition of our Optimize series informative and interesting, and we welcome your questions and comments. William C. Heuer Partner, Duane Morris Business Reorganization and Financial Restructuring Practice Group Lawrence J. Kotler Walter J.

Greenhalgh Partner, Duane Morris Partner, Duane Morris Business Reorganization and Business Reorganization and Financial Restructuring Practice Group Financial Restructuring Practice Group DUANE MORRIS - OPTIMIZE 3 . STATE OF PLAY: CREDIT IS KING, RISK IS REASONABLE Bankruptcy has always been a last resort for troubled companies. But that is especially true now. In this economy, where’s the need? Duane Morris partner Lawrence J. Kotler moderated our two panel discussions during which our esteemed contributors provided insight and commentary.

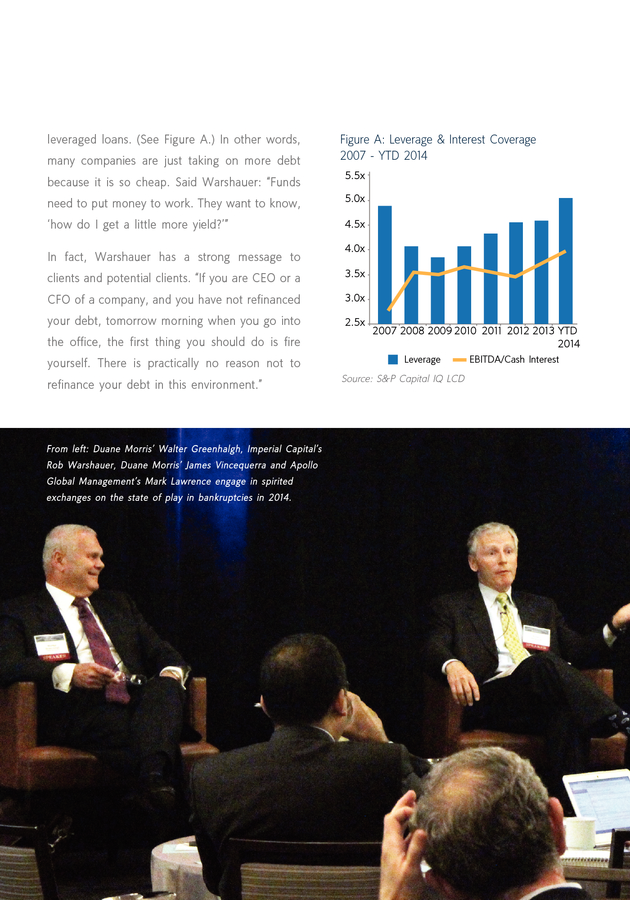

In our first panel, Duane Morris partners Walter J. Greenhalgh and James J. Vincequerra were joined by Mark Lawrence, Managing Director at Apollo Global Capital Management; and Rob Warshauer. They discussed the state of play in bankruptcies in 2014. “The capital markets are on fire” for companies seeking to raise new capital, said Rob Warshauer. Both leveraged loans and high-yield markets were very strong in 2013, and with the expectation of rising rates, companies have gravitated to high-yield deals with fixed interest rates, rather than the fluctuating rates of 4 DUANE MORRIS - OPTIMIZE . Funds need to put money to work. They want to know, ‘how do I get a little more yield?’ DUANE MORRIS - OPTIMIZE 5 . leveraged loans. (See Figure A.) In other words, many companies are just taking on more debt because it is so cheap. Said Warshauer: “Funds Figure A: Leverage & Interest Coverage 2007 - YTD 2014 5.5x need to put money to work. They want to know, 5.0x ‘how do I get a little more yield?’” 4.5x In fact, Warshauer has a strong message to 4.0x clients and potential clients.

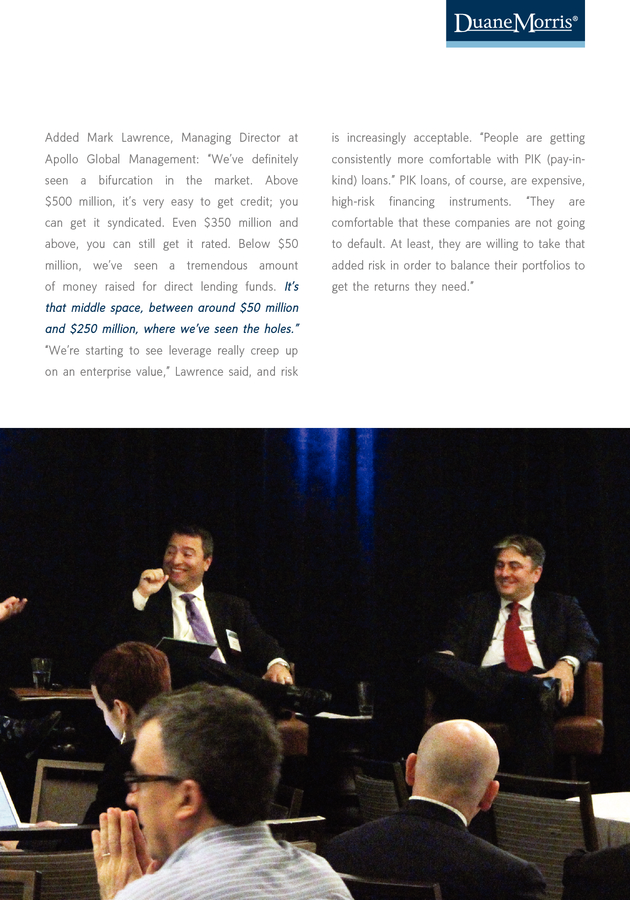

“If you are CEO or a 3.5x CFO of a company, and you have not refinanced 3.0x your debt, tomorrow morning when you go into 2.5x the office, the first thing you should do is fire yourself. There is practically no reason not to refinance your debt in this environment.” From left: Duane Morris’ Walter Greenhalgh, Imperial Capital’s Rob Warshauer, Duane Morris’ James Vincequerra and Apollo Global Management’s Mark Lawrence engage in spirited exchanges on the state of play in bankruptcies in 2014. 6 DUANE MORRIS - OPTIMIZE 2007 2008 2009 2010 2011 2012 2013 YTD 2014 Leverage Source: S&P Capital IQ LCD EBITDA/Cash Interest . Added Mark Lawrence, Managing Director at is increasingly acceptable. “People are getting Apollo Global Management: “We’ve definitely consistently more comfortable with PIK (pay-in- seen a bifurcation in the market. Above kind) loans.” PIK loans, of course, are expensive, $500 million, it’s very easy to get credit; you high-risk can get it syndicated. Even $350 million and comfortable that these companies are not going above, you can still get it rated.

Below $50 to default. At least, they are willing to take that million, we’ve seen a tremendous amount added risk in order to balance their portfolios to of money raised for direct lending funds. It’s get the returns they need.” financing instruments. “They are that middle space, between around $50 million and $250 million, where we’ve seen the holes.” “We’re starting to see leverage really creep up on an enterprise value,” Lawrence said, and risk DUANE MORRIS - OPTIMIZE 7 .

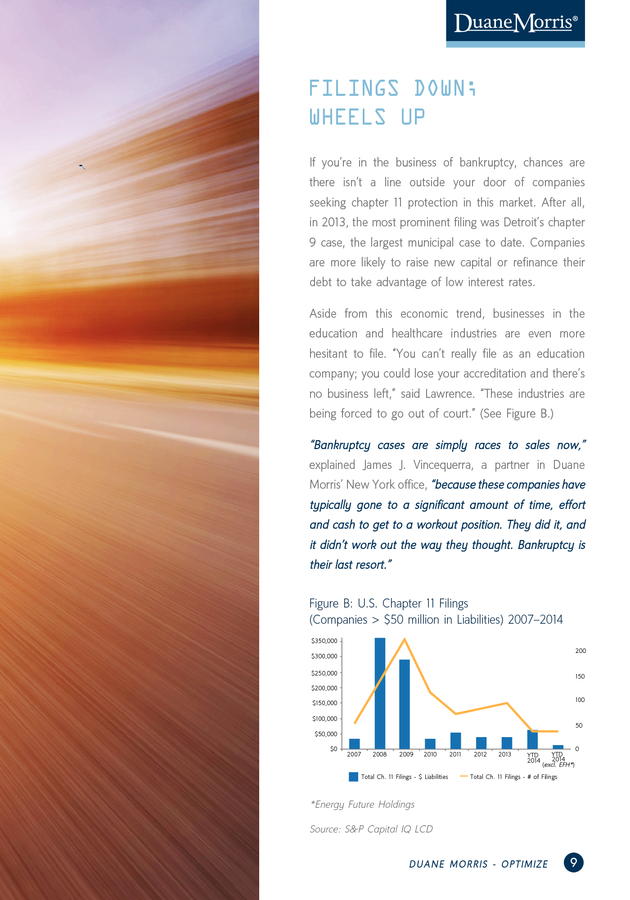

8 DUANE MORRIS - OPTIMIZE . FILINGS DOWN; WHEELS UP If you’re in the business of bankruptcy, chances are there isn’t a line outside your door of companies seeking chapter 11 protection in this market. After all, in 2013, the most prominent filing was Detroit’s chapter 9 case, the largest municipal case to date. Companies are more likely to raise new capital or refinance their debt to take advantage of low interest rates. Aside from this economic trend, businesses in the education and healthcare industries are even more hesitant to file. “You can’t really file as an education company; you could lose your accreditation and there’s no business left,” said Lawrence.

“These industries are being forced to go out of court.” (See Figure B.) “Bankruptcy cases are simply races to sales now,” explained James J. Vincequerra, a partner in Duane Morris’ New York office, “because these companies have typically gone to a significant amount of time, effort and cash to get to a workout position. They did it, and it didn’t work out the way they thought.

Bankruptcy is their last resort.” Figure B: U.S. Chapter 11 Filings (Companies > $50 million in Liabilities) 2007–2014 $400,000 250 $350,000 200 $300,000 $250,000 150 $200,000 100 $150,000 $100,000 50 $50,000 $0 2007 2008 2009 2010 Total Ch. 11 Filings - $ Liabilities 2011 2012 2013 YTD 2014 YTD 2014 (excl.

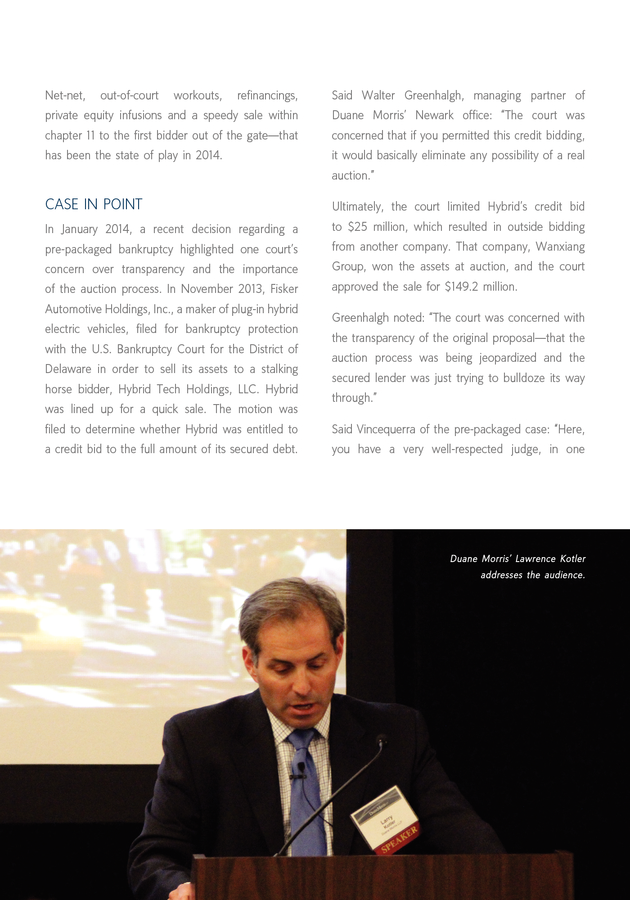

EFH*) 0 Total Ch. 11 Filings - # of Filings *Energy Future Holdings Source: S&P Capital IQ LCD DUANE MORRIS - OPTIMIZE 9 . Net-net, out-of-court workouts, refinancings, Said Walter Greenhalgh, managing partner of private equity infusions and a speedy sale within Duane Morris’ Newark office: “The court was chapter 11 to the first bidder out of the gate—that concerned that if you permitted this credit bidding, has been the state of play in 2014. it would basically eliminate any possibility of a real auction.” CASE IN POINT Ultimately, the court limited Hybrid’s credit bid In January 2014, a recent decision regarding a to $25 million, which resulted in outside bidding pre-packaged bankruptcy highlighted one court’s from another company. That company, Wanxiang concern over transparency and the importance Group, won the assets at auction, and the court of the auction process. In November 2013, Fisker approved the sale for $149.2 million. Automotive Holdings, Inc., a maker of plug-in hybrid electric vehicles, filed for bankruptcy protection with the U.S. Bankruptcy Court for the District of Delaware in order to sell its assets to a stalking horse bidder, Hybrid Tech Holdings, LLC.

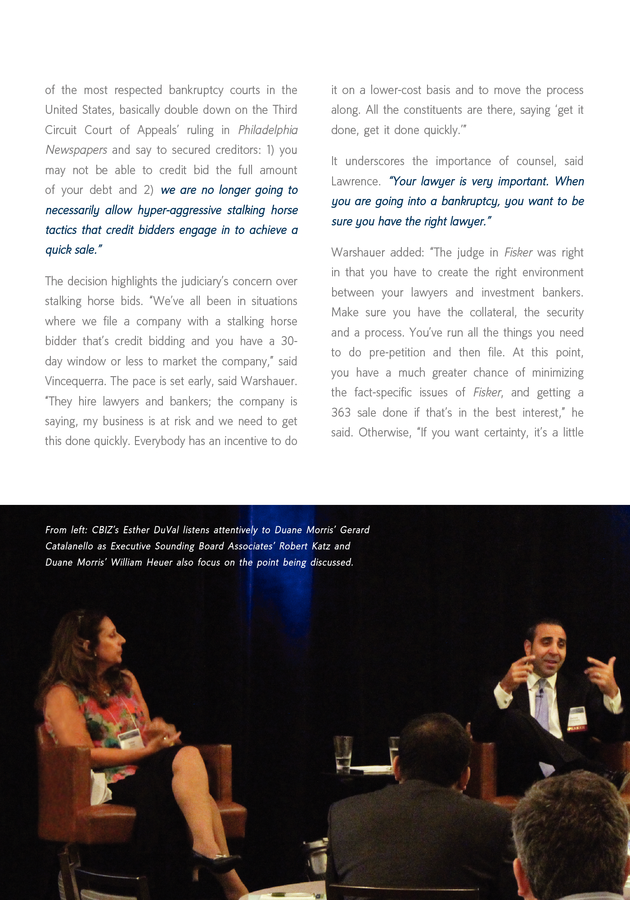

Hybrid was lined up for a quick sale. The motion was Greenhalgh noted: “The court was concerned with the transparency of the original proposal—that the auction process was being jeopardized and the secured lender was just trying to bulldoze its way through.” filed to determine whether Hybrid was entitled to Said Vincequerra of the pre-packaged case: “Here, a credit bid to the full amount of its secured debt. you have a very well-respected judge, in one Duane Morris’ Lawrence Kotler addresses the audience. 10 DUANE MORRIS - OPTIMIZE . We’ve all been in situations where we file a company with a stalking horse bidder that’s credit bidding and you have a 30-day window or less to market the company DUANE MORRIS - OPTIMIZE 11 . of the most respected bankruptcy courts in the it on a lower-cost basis and to move the process United States, basically double down on the Third along. All the constituents are there, saying ‘get it Circuit Court of Appeals’ ruling in Philadelphia done, get it done quickly.’” Newspapers and say to secured creditors: 1) you may not be able to credit bid the full amount of your debt and 2) we are no longer going to necessarily allow hyper-aggressive stalking horse tactics that credit bidders engage in to achieve a quick sale.” The decision highlights the judiciary’s concern over stalking horse bids. “We’ve all been in situations where we file a company with a stalking horse bidder that’s credit bidding and you have a 30day window or less to market the company,” said Vincequerra. The pace is set early, said Warshauer. “They hire lawyers and bankers; the company is saying, my business is at risk and we need to get this done quickly.

Everybody has an incentive to do It underscores the importance of counsel, said Lawrence. “Your lawyer is very important. When you are going into a bankruptcy, you want to be sure you have the right lawyer.” Warshauer added: “The judge in Fisker was right in that you have to create the right environment between your lawyers and investment bankers. Make sure you have the collateral, the security and a process.

You’ve run all the things you need to do pre-petition and then file. At this point, you have a much greater chance of minimizing the fact-specific issues of Fisker, and getting a 363 sale done if that’s in the best interest,” he said. Otherwise, “If you want certainty, it’s a little cap cap cap cap cap cap cap cap From left: CBIZ’s Esther DuVal listens attentively to Duane Morris’ Gerard Catalanello as Executive Sounding Board Associates’ Robert Katz and Duane Morris’ William Heuer also focus on the point being discussed. 12 DUANE MORRIS - OPTIMIZE .

bit longer of a process, but you go through the value exchanges since Chateaugay. “It is a very process of a plan of reorganization.” encouraging case for lenders and debtors who are Vincequerra referred to a second case “indicative involved in pre-petition workouts,” he said. of the trend favoring pre-petition workouts.” Basically, said Warshauer, “The judges want to Residential Capital, LLC (ResCap), once one of the expedite these cases. They are not interested in largest mortgage servicers and mortgage lenders in having investment bankers come in and spend the U.S., filed for bankruptcy protection in 2013. In many days in depositions and hearings discussing December 2013, Judge Martin Glenn of the U.S. and opining upon valuations.

Judges want to be Bankruptcy Court in New York’s Southern District fair and not subject to appeal. In ResCap, Judge confirmed ResCap’s plan to exit chapter 11 and Glenn effectively said, ‘Let’s make the process fair liquidate. and predictable for everyone.’” “It’s an important case in that it gives more The bottom line: Uncertainty for secured creditors certainty for fair value exchanges in pre-petition could lead to fewer bankruptcy cases, or at least workout scenarios,” said Lawrence. Judge Glenn be a disincentive.

When advising companies on determined that the original issue discount (OID) potential credit bidding or a Section 363 sale, it is allowable in bankruptcy after a fair value pre- pays to be cognizant of the facts and results in Fisker. petition debt exchange just as it has been in face DUANE MORRIS - OPTIMIZE 13 . While the company may have an appetite for a certain strategy on how to proceed, it’s the buyer or the end game that usually dictates where and how you do it. SPRINT OR MARATHON? In our second panel, Duane Morris partners Moderator Lawrence Kotler, a partner in the Gerard Catalanello and William Heuer teamed Philadelphia office of Duane Morris, asked the up with Esther DuVal, Managing Director of tough question: CBIZ MHM, LLC; and Robert Katz, Managing Director of Executive Sounding Board Associates LLC, to discuss how to prepare for bankruptcy. 14 DUANE MORRIS - OPTIMIZE “Our earlier panel talked about why the economy is flat and why bankruptcy is flat. Is there hope?” . issues to assess because the cost in and out of court becomes a big issue.” Professionals have, at times, pushed for alternatives to bankruptcy. “We’ve utilized a cheaper alternative, Article 9 of the UCC, known as a friendly foreclosure,” said Katz. Jurisdiction is important, too. “Assignments for the benefit of creditors (ABCs) have been done for years in the West and Midwest and are becoming more prevalent now in the East. If you have a favorable state court, it can also be a more flexible process, such as utilizing a receivership,” he said. “I see a rise in the use of the ABC,” said Esther DuVal, Managing Director at consulting firm CBIZ, referring to an assignment for the benefit of creditors, a private process to liquidate a business outside of bankruptcy.

“You need to have some synergy between what it is you’re assigning and to whom you are assigning it. If you are assigning a business to an individual and not another business, you could lose all the value of that business.” “The buyer often calls the plays,” said Catalanello, a partner in the New York office of Duane Morris. He noted: “The manner or process in which you try to restructure or liquidate is often dictated by the buyer who is waiting in the wings. A buyer looks at an asset that is troubled and decides whether an Article 9 sale gives it the type of title it needs. Sometimes, an out-of-court process just doesn’t give It’s all about strategy, said Robert Katz, President of a buyer the finality it believes is necessary to get consulting firm Executive Sounding Board Associates the benefit of its bargain.

While the company may LLC. “Here is where you really start to ask the have an appetite for a certain strategy on how to question and examine, is it a good thing to file for proceed, it’s the buyer or the end game that usually bankruptcy? What’s the purpose? Can you afford dictates where and how you do it.” the cost in both dollars and time? Those are two DUANE MORRIS - OPTIMIZE 15 . TRANSPARENCY FOR THE WIN it’s best to put in place the same professional team There are inherent power dynamics in the process, that you would have as if you were in a formal particularly if you have a renegade creditor. Said bankruptcy. That’s because it adds to the credibility Catalanello: “If you are transparent and open to of the process. To have the most likely chance of sharing information with even the most difficult succeeding in an out-of-court restructuring, choose creditor, if that creditor is looking for an economic the right team.” return rather than pure punishment, then you have “If your out-of-court doesn’t work,” said DuVal, “you a chance of convincing that creditor to come on don’t want to have to bring in a whole new team of board with the process.” professionals and bring them up to speed.

You’ve DuVal agreed. “It’s very difficult when you have got a learning curve that’s already met.” creditors who have interests that are not economic If the decision is made to file a chapter 11 petition, considerations,” she said. “I’ve had out-of-courts venue can be an issue, noted DuVal, due to fall apart because of political issues—maybe potential political issues. you’re dealing with an organization that doesn’t want to do anything precedent setting, or maybe “As is cash flow,” said Katz.

“Make sure you have people are angry and just would rather see enough. There’s always a hiccup, there’s always someone go to jail than get whatever pittance a reason, but it goes to the credibility” of the they would get in an out-of-court process.” team of professionals who are dealing with the creditors and other parties-in-interest, he said. “If BRING THE “A” TEAM Said Catalanello: “If you are going to travel down the road of a non-judicial workout or liquidation, CBIZ’s Esther DuVal conveys her views on out-of-courts and the use of the ABC. 16 DUANE MORRIS - OPTIMIZE you’re good the first month, you have flexibility.” .

THE SECTION 363 BATON The advantage of a Section 363 sale can be very attractive to both the debtor and the buyer. From the buyer’s perspective, said William Heuer, “When you go out and buy a company outside of a bankruptcy, you take all the fleas, ticks and warts that come with it, including any litigation pending against the company. When you buy a 363 asset, it sanitizes the assets,” he said. “You line up the sale, move on and get out of there.” SLOW AND STEADY WINS THE RACE A Section 363 sale is not always a clear cut Speed is necessary sometimes, but be warned: Its approach, and its results may vary over time as new impulsive younger brother, haste, can make waste. case law emerges.

“There is push at times,” said Heuer, a partner in Duane Morris’ New York office, “In the last few years, there’s been almost an “to do a Section 363 sale because of the quality of acceptance or normalcy for a 45- to 60-day sale title you get, but I question whether the full scope period from filing,” said Catalanello. “It’s incumbent of these protections is going to be available in the on the company side or creditors’ committee side to long term.” continue to push back on that. It’s really detrimental to the entire spirit of a fullsome sale process.

If “You have to be prepared to shift and move quickly there is a fire that needs to be put out, I get it, but in this environment,” said Catalanello. “On day one, I think we have to push back to see if it really is a the case could be over,” he continued. “If you take fire.

In this race to the finish line, people are getting the wrong turn early on, whether it’s cash collateral destroyed before the race begins. We’re pushing a or agreeing to some ridiculous restrictions on sale boulder up a hill. We shouldn’t just accept as status procedures, then the case is baked in stone.

If you quo that this asset has to be sold in 45 to 60 days.” feel that you have the better side, fight on day one. Set the tone and try to take control of the case. If In addition, those filing chapter 11 petitions need to you don’t, you’re letting someone else control the be prepared for contingencies. “The days of just filing case and possibly the outcome.” a chapter 11 case and then figuring out what you are going to do next are long over,” said Catalanello. DuVal pointed out that in addition to slowing down “You need to be prepared from the moment you the process, transparency is important.

“We had file with your plan A, which might be a complete a case where the CFO and all the officers had restructuring; plan B, which may be a partial a personal vested interest with a stalking horse restructuring with a sale of some non-core assets; bidder,” she recalled. “They did their best to chill the or plan C, which is ‘we’re going to sell everything.’” offers. With transparency, the value add is creating a fair process.” DUANE MORRIS - OPTIMIZE 17 .

SPEAKER PROFILES MODERATOR LAWRENCE J. KOTLER is a Partner at Duane Morris LLP. Mr. Kotler practices in the area of reorganization and finance, representing chapter 11 debtors-in-possession, chapter 11 trustees, chapter 7 trustees, liquidating trustees, creditors’ committees, secured creditors and large institutional unsecured creditors in all facets of bankruptcy.

Mr. Kotler is certified as a business bankruptcy specialist by the American Board of Certification. He is also a frequent speaker on bankruptcy and creditors’ rights issues. PANEL 1 MARK LAWRENCE is Managing Director, Opportunistic Credit, at Apollo Global Management.

Mr. Lawrence joined Apollo in 2012. He focuses on distressed investing and private capital solutions as part of Apollo’s Opportunistic Credit efforts.

Previously, Mr. Lawrence was a member of the investment group at Solus Alternative Asset Management, and prior to that, he was a member of the investment group at Stanfield Capital Partners. ROB WARSHAUER is Managing Director, Co-Head of Restructuring Group and Manager of Investment Banking Group at Imperial Capital. Mr.

Warshauer’s team has advised on hundreds of complex distressed situations, and it dedicates industry-specific, senior-level resources to each client matter. Prior to joining Imperial Capital, he was a Managing Director at Kroll Zolfo Cooper, where he primarily focused on the firm’s restructuring practice. Previously, he was a Managing Director and member of the Board of Directors of Giuliani Capital Advisors LLC, and its predecessor firm, Ernst & Young Corporate Finance LLC, where he specialized in corporate restructuring and mergers and acquisitions.

As part of his banking and restructuring experience, Mr. Warshauer has served as CEO and President of an international business services and manufacturing company responsible for over 2,500 employees in 16 countries, and he was President and a member of the Board of Directors of a publicly traded technology company that specialized in the development and manufacture of technologically advanced, energy-efficient, LED lighting products. WALTER J. GREENHALGH is a Partner at Duane Morris LLP.

Mr. Greenhalgh practices in the areas of commercial litigation and bankruptcy law, insolvency law and chapter 11 corporate and commercial reorganization. He is the managing partner of Duane Morris’ Newark office and a member of the firm’s national governing Partners Board. A past chair of the executive committee of the Bankruptcy Law Section of the New Jersey State Bar Association, he has been an officer of the Section for more than 10 years. JAMES J.

VINCEQUERRA is a Partner at Duane Morris LLP. Mr. Vincequerra focuses his practice on business reorganizations, creditors’ rights and general counseling.

He represents debtors, creditors’ committees, individual creditors, trustees and acquirers of assets of troubled companies in formal bankruptcy proceedings and in outof-court/workout scenarios. He is also actively involved in litigating disputes related to his client representations. 18 DUANE MORRIS - OPTIMIZE . PANEL 2 ESTHER DuVaL is the Managing Director at CBIZ MHM, LLC. Ms. DuVal serves as the Corporate Recovery Services group co-practice leader for the New York office. She specializes in creditors’ rights and has an extensive background working with matters ranging from mid-sized bankruptcies to high-profile cases.

Ms. DuVal has a thorough understanding of the complex issues involved in bankruptcy matters, and when applicable, she helps resolve disputes in an amicable manner through mediation. Ms.

DuVal joined the organization in 1996. Previously, she was a senior manager in the Corporate Recovery Group of BDO Seidman and developed industry experience with investment banking at Morgan Stanley. ROBERT D. KATZ is President of Executive Sounding Board Associates LLC.

Mr. Katz helps companies through crises and turnarounds with the vision and insight earned from more than 25 years on the front lines. Hundreds of companies have relied on him in high-pressure situations to create and execute the strategy needed to restructure or improve operating performance.

He works with public and private middle-market companies, both in and out of bankruptcy, who are facing operational or financial challenges. Mr. Katz acts as Interim President, Chief Financial Officer, Chief Operating Officer, Chief Restructuring Officer or Treasurer, helping companies improve operating performance and generate additional cash flow.

He acts as plan administrator, distribution trustee and receiver. Mr. Katz also serves as an advisor to U.S.

trustees, creditor committees, company management, lenders and private equity funds. GERARD S. CATALANELLO is a Partner at Duane Morris LLP. Mr.

Catalanello practices in the area of bankruptcy and creditors’ rights law, representing debtors, creditors, creditors’ committees, financial institutions, liquidation trusts, equity holders, trustees and acquirers of assets of troubled companies in formal bankruptcy proceedings, as well as in out-of-court workouts. Mr. Catalanello has also served as counsel to official committees of unsecured creditors in a range of chapter 11 cases and has represented major institutions in connection with the negotiation and sale of hundreds of millions of dollars of claims in major chapter 11 cases. WILLIAM C.

HEUER is a Partner at Duane Morris LLP. Mr. Heuer practices in the areas of business reorganization, bankruptcy law and creditors’ rights litigation.

He represents secured creditors in loan default workouts and bankruptcies, with experience in a wide range of industries, including commercial shipping, satellite and telecommunications, golf and entertainment, retail merchandise, air travel (domestic and international), healthcare and long-term health management facilities, and real estate. Mr. Heuer represents debtors in both domestic and international bankruptcy proceedings. DUANE MORRIS - OPTIMIZE 19 .

Chicago Lake Tahoe Pittsburgh San Francisco Silicon Valley Las Vegas Los Angeles San Diego Atlanta Houston Boston New York Newark Cherry Hill Philadelphia Wilmington Baltimore Washington, D.C. Boca Raton Miami Mexico City Duane Morris Office Representative / Liaison Office 20 DUANE MORRIS - OPTIMIZE . ABOUT DUANE MORRIS With experienced bankruptcy and restructuring lawyers across our domestic and global platform, coupled with the deep capabilities of more than 700 lawyers across all practice areas, Duane Morris offers the resources to optimize our clients’ interests. From creditor to debtor, and trustee to committee, our bankruptcy London, Uk practice is regularly recognized as one of the most active for both case volume and value of liabilities. We leverage our core experience in bankruptcy law, creditors’ rights and asset recovery actions and the full range of services for commercial mortgages and other asset classes, working with banks, non-bank lenders, special servicers, debt purchasers and asset buyers. On the distressed deal side, our lawyers have negotiated and brokered major transactions China industries Shanghai, in such as manufacturing, real estate, telecommunications and retail. Five of the practice group’s former attorneys are sitting United States Bankruptcy Court judges, and another is a judge on the United States Court of Appeals for the Third Circuit. Oman Hanoi, Vietnam Myanmar Ho Chi Minh City Singapore DUANE MORRIS - OPTIMIZE 21 .

Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Philadelphia | Chicago | Washington, D.C. | San Francisco Silicon Valley | San Diego | Shanghai | Boston | Houston | Los Angeles | Hanoi | Ho Chi Minh City | Atlanta | Baltimore | Wilmington | Miami Boca Raton | Pittsburgh | Newark | Las Vegas | Cherry Hill | Lake Tahoe | Myanmar | Oman | Duane Morris LLP – A Delaware limited liability partnership This publication is for general information and does not include full legal analysis of the matters presented. It should not be construed or relied upon as legal advice or legal opinion on any specific facts or circumstances. The invitation to contact the attorneys in our firm is not a solicitation to provide professional services and should not be construed as a statement as to any 22 DUANE MORRIS - OPTIMIZE availability to perform legal services in any jurisdiction in which such attorney is not permitted to practice.

© Duane Morris LLP 2014. .

The results have been lasting: companies are still able to access cheap financing, thereby quelling the tide of bankruptcy filings, which continues to ebb. While there was speculation that 2014 might find retail, shipping and municipalities turning to the bankruptcy courts, for the most part, filings are at historical lows. However, bankruptcy professionals aren’t sitting on the sidelines. Pre-petition workouts, out-of-court restructurings and other alternatives remain popular.

When a chapter 11 case is filed, it’s increasingly common to consider a shorter, less expensive path: an asset sale, allowed under Section 363 of the Bankruptcy Code, for the benefit of the debtor, the buyer and, occasionally, creditors. Keeping pace with the speed of those deals—more sprint than marathon—requires a knowledge of the ins and outs of the Bankruptcy Code, the economy, and the politics of each deal. Gerard S. Catalanello James J. Vincequerra Partner, Duane Morris Partner, Duane Morris Business Reorganization and 2 Business Reorganization and Financial Restructuring Practice Group Financial Restructuring Practice Group DUANE MORRIS - OPTIMIZE .

And, of course, it is essential to choose the right bankruptcy team. In this publication, Duane Morris partners come together with financial industry and restructuring professionals to share commentary and insights into the markets and best practices for distressed companies, and the bankruptcy professionals who help debtors and creditors. It’s our goal with each event and subsequent issue of Optimize to provide clients with the very best in legal and business thought leadership in order to leverage the knowledge and experience of some of the most vital players in the industry. We hope you find this third edition of our Optimize series informative and interesting, and we welcome your questions and comments. William C. Heuer Partner, Duane Morris Business Reorganization and Financial Restructuring Practice Group Lawrence J. Kotler Walter J.

Greenhalgh Partner, Duane Morris Partner, Duane Morris Business Reorganization and Business Reorganization and Financial Restructuring Practice Group Financial Restructuring Practice Group DUANE MORRIS - OPTIMIZE 3 . STATE OF PLAY: CREDIT IS KING, RISK IS REASONABLE Bankruptcy has always been a last resort for troubled companies. But that is especially true now. In this economy, where’s the need? Duane Morris partner Lawrence J. Kotler moderated our two panel discussions during which our esteemed contributors provided insight and commentary.

In our first panel, Duane Morris partners Walter J. Greenhalgh and James J. Vincequerra were joined by Mark Lawrence, Managing Director at Apollo Global Capital Management; and Rob Warshauer. They discussed the state of play in bankruptcies in 2014. “The capital markets are on fire” for companies seeking to raise new capital, said Rob Warshauer. Both leveraged loans and high-yield markets were very strong in 2013, and with the expectation of rising rates, companies have gravitated to high-yield deals with fixed interest rates, rather than the fluctuating rates of 4 DUANE MORRIS - OPTIMIZE . Funds need to put money to work. They want to know, ‘how do I get a little more yield?’ DUANE MORRIS - OPTIMIZE 5 . leveraged loans. (See Figure A.) In other words, many companies are just taking on more debt because it is so cheap. Said Warshauer: “Funds Figure A: Leverage & Interest Coverage 2007 - YTD 2014 5.5x need to put money to work. They want to know, 5.0x ‘how do I get a little more yield?’” 4.5x In fact, Warshauer has a strong message to 4.0x clients and potential clients.

“If you are CEO or a 3.5x CFO of a company, and you have not refinanced 3.0x your debt, tomorrow morning when you go into 2.5x the office, the first thing you should do is fire yourself. There is practically no reason not to refinance your debt in this environment.” From left: Duane Morris’ Walter Greenhalgh, Imperial Capital’s Rob Warshauer, Duane Morris’ James Vincequerra and Apollo Global Management’s Mark Lawrence engage in spirited exchanges on the state of play in bankruptcies in 2014. 6 DUANE MORRIS - OPTIMIZE 2007 2008 2009 2010 2011 2012 2013 YTD 2014 Leverage Source: S&P Capital IQ LCD EBITDA/Cash Interest . Added Mark Lawrence, Managing Director at is increasingly acceptable. “People are getting Apollo Global Management: “We’ve definitely consistently more comfortable with PIK (pay-in- seen a bifurcation in the market. Above kind) loans.” PIK loans, of course, are expensive, $500 million, it’s very easy to get credit; you high-risk can get it syndicated. Even $350 million and comfortable that these companies are not going above, you can still get it rated.

Below $50 to default. At least, they are willing to take that million, we’ve seen a tremendous amount added risk in order to balance their portfolios to of money raised for direct lending funds. It’s get the returns they need.” financing instruments. “They are that middle space, between around $50 million and $250 million, where we’ve seen the holes.” “We’re starting to see leverage really creep up on an enterprise value,” Lawrence said, and risk DUANE MORRIS - OPTIMIZE 7 .

8 DUANE MORRIS - OPTIMIZE . FILINGS DOWN; WHEELS UP If you’re in the business of bankruptcy, chances are there isn’t a line outside your door of companies seeking chapter 11 protection in this market. After all, in 2013, the most prominent filing was Detroit’s chapter 9 case, the largest municipal case to date. Companies are more likely to raise new capital or refinance their debt to take advantage of low interest rates. Aside from this economic trend, businesses in the education and healthcare industries are even more hesitant to file. “You can’t really file as an education company; you could lose your accreditation and there’s no business left,” said Lawrence.

“These industries are being forced to go out of court.” (See Figure B.) “Bankruptcy cases are simply races to sales now,” explained James J. Vincequerra, a partner in Duane Morris’ New York office, “because these companies have typically gone to a significant amount of time, effort and cash to get to a workout position. They did it, and it didn’t work out the way they thought.

Bankruptcy is their last resort.” Figure B: U.S. Chapter 11 Filings (Companies > $50 million in Liabilities) 2007–2014 $400,000 250 $350,000 200 $300,000 $250,000 150 $200,000 100 $150,000 $100,000 50 $50,000 $0 2007 2008 2009 2010 Total Ch. 11 Filings - $ Liabilities 2011 2012 2013 YTD 2014 YTD 2014 (excl.

EFH*) 0 Total Ch. 11 Filings - # of Filings *Energy Future Holdings Source: S&P Capital IQ LCD DUANE MORRIS - OPTIMIZE 9 . Net-net, out-of-court workouts, refinancings, Said Walter Greenhalgh, managing partner of private equity infusions and a speedy sale within Duane Morris’ Newark office: “The court was chapter 11 to the first bidder out of the gate—that concerned that if you permitted this credit bidding, has been the state of play in 2014. it would basically eliminate any possibility of a real auction.” CASE IN POINT Ultimately, the court limited Hybrid’s credit bid In January 2014, a recent decision regarding a to $25 million, which resulted in outside bidding pre-packaged bankruptcy highlighted one court’s from another company. That company, Wanxiang concern over transparency and the importance Group, won the assets at auction, and the court of the auction process. In November 2013, Fisker approved the sale for $149.2 million. Automotive Holdings, Inc., a maker of plug-in hybrid electric vehicles, filed for bankruptcy protection with the U.S. Bankruptcy Court for the District of Delaware in order to sell its assets to a stalking horse bidder, Hybrid Tech Holdings, LLC.

Hybrid was lined up for a quick sale. The motion was Greenhalgh noted: “The court was concerned with the transparency of the original proposal—that the auction process was being jeopardized and the secured lender was just trying to bulldoze its way through.” filed to determine whether Hybrid was entitled to Said Vincequerra of the pre-packaged case: “Here, a credit bid to the full amount of its secured debt. you have a very well-respected judge, in one Duane Morris’ Lawrence Kotler addresses the audience. 10 DUANE MORRIS - OPTIMIZE . We’ve all been in situations where we file a company with a stalking horse bidder that’s credit bidding and you have a 30-day window or less to market the company DUANE MORRIS - OPTIMIZE 11 . of the most respected bankruptcy courts in the it on a lower-cost basis and to move the process United States, basically double down on the Third along. All the constituents are there, saying ‘get it Circuit Court of Appeals’ ruling in Philadelphia done, get it done quickly.’” Newspapers and say to secured creditors: 1) you may not be able to credit bid the full amount of your debt and 2) we are no longer going to necessarily allow hyper-aggressive stalking horse tactics that credit bidders engage in to achieve a quick sale.” The decision highlights the judiciary’s concern over stalking horse bids. “We’ve all been in situations where we file a company with a stalking horse bidder that’s credit bidding and you have a 30day window or less to market the company,” said Vincequerra. The pace is set early, said Warshauer. “They hire lawyers and bankers; the company is saying, my business is at risk and we need to get this done quickly.

Everybody has an incentive to do It underscores the importance of counsel, said Lawrence. “Your lawyer is very important. When you are going into a bankruptcy, you want to be sure you have the right lawyer.” Warshauer added: “The judge in Fisker was right in that you have to create the right environment between your lawyers and investment bankers. Make sure you have the collateral, the security and a process.

You’ve run all the things you need to do pre-petition and then file. At this point, you have a much greater chance of minimizing the fact-specific issues of Fisker, and getting a 363 sale done if that’s in the best interest,” he said. Otherwise, “If you want certainty, it’s a little cap cap cap cap cap cap cap cap From left: CBIZ’s Esther DuVal listens attentively to Duane Morris’ Gerard Catalanello as Executive Sounding Board Associates’ Robert Katz and Duane Morris’ William Heuer also focus on the point being discussed. 12 DUANE MORRIS - OPTIMIZE .

bit longer of a process, but you go through the value exchanges since Chateaugay. “It is a very process of a plan of reorganization.” encouraging case for lenders and debtors who are Vincequerra referred to a second case “indicative involved in pre-petition workouts,” he said. of the trend favoring pre-petition workouts.” Basically, said Warshauer, “The judges want to Residential Capital, LLC (ResCap), once one of the expedite these cases. They are not interested in largest mortgage servicers and mortgage lenders in having investment bankers come in and spend the U.S., filed for bankruptcy protection in 2013. In many days in depositions and hearings discussing December 2013, Judge Martin Glenn of the U.S. and opining upon valuations.

Judges want to be Bankruptcy Court in New York’s Southern District fair and not subject to appeal. In ResCap, Judge confirmed ResCap’s plan to exit chapter 11 and Glenn effectively said, ‘Let’s make the process fair liquidate. and predictable for everyone.’” “It’s an important case in that it gives more The bottom line: Uncertainty for secured creditors certainty for fair value exchanges in pre-petition could lead to fewer bankruptcy cases, or at least workout scenarios,” said Lawrence. Judge Glenn be a disincentive.

When advising companies on determined that the original issue discount (OID) potential credit bidding or a Section 363 sale, it is allowable in bankruptcy after a fair value pre- pays to be cognizant of the facts and results in Fisker. petition debt exchange just as it has been in face DUANE MORRIS - OPTIMIZE 13 . While the company may have an appetite for a certain strategy on how to proceed, it’s the buyer or the end game that usually dictates where and how you do it. SPRINT OR MARATHON? In our second panel, Duane Morris partners Moderator Lawrence Kotler, a partner in the Gerard Catalanello and William Heuer teamed Philadelphia office of Duane Morris, asked the up with Esther DuVal, Managing Director of tough question: CBIZ MHM, LLC; and Robert Katz, Managing Director of Executive Sounding Board Associates LLC, to discuss how to prepare for bankruptcy. 14 DUANE MORRIS - OPTIMIZE “Our earlier panel talked about why the economy is flat and why bankruptcy is flat. Is there hope?” . issues to assess because the cost in and out of court becomes a big issue.” Professionals have, at times, pushed for alternatives to bankruptcy. “We’ve utilized a cheaper alternative, Article 9 of the UCC, known as a friendly foreclosure,” said Katz. Jurisdiction is important, too. “Assignments for the benefit of creditors (ABCs) have been done for years in the West and Midwest and are becoming more prevalent now in the East. If you have a favorable state court, it can also be a more flexible process, such as utilizing a receivership,” he said. “I see a rise in the use of the ABC,” said Esther DuVal, Managing Director at consulting firm CBIZ, referring to an assignment for the benefit of creditors, a private process to liquidate a business outside of bankruptcy.

“You need to have some synergy between what it is you’re assigning and to whom you are assigning it. If you are assigning a business to an individual and not another business, you could lose all the value of that business.” “The buyer often calls the plays,” said Catalanello, a partner in the New York office of Duane Morris. He noted: “The manner or process in which you try to restructure or liquidate is often dictated by the buyer who is waiting in the wings. A buyer looks at an asset that is troubled and decides whether an Article 9 sale gives it the type of title it needs. Sometimes, an out-of-court process just doesn’t give It’s all about strategy, said Robert Katz, President of a buyer the finality it believes is necessary to get consulting firm Executive Sounding Board Associates the benefit of its bargain.

While the company may LLC. “Here is where you really start to ask the have an appetite for a certain strategy on how to question and examine, is it a good thing to file for proceed, it’s the buyer or the end game that usually bankruptcy? What’s the purpose? Can you afford dictates where and how you do it.” the cost in both dollars and time? Those are two DUANE MORRIS - OPTIMIZE 15 . TRANSPARENCY FOR THE WIN it’s best to put in place the same professional team There are inherent power dynamics in the process, that you would have as if you were in a formal particularly if you have a renegade creditor. Said bankruptcy. That’s because it adds to the credibility Catalanello: “If you are transparent and open to of the process. To have the most likely chance of sharing information with even the most difficult succeeding in an out-of-court restructuring, choose creditor, if that creditor is looking for an economic the right team.” return rather than pure punishment, then you have “If your out-of-court doesn’t work,” said DuVal, “you a chance of convincing that creditor to come on don’t want to have to bring in a whole new team of board with the process.” professionals and bring them up to speed.

You’ve DuVal agreed. “It’s very difficult when you have got a learning curve that’s already met.” creditors who have interests that are not economic If the decision is made to file a chapter 11 petition, considerations,” she said. “I’ve had out-of-courts venue can be an issue, noted DuVal, due to fall apart because of political issues—maybe potential political issues. you’re dealing with an organization that doesn’t want to do anything precedent setting, or maybe “As is cash flow,” said Katz.

“Make sure you have people are angry and just would rather see enough. There’s always a hiccup, there’s always someone go to jail than get whatever pittance a reason, but it goes to the credibility” of the they would get in an out-of-court process.” team of professionals who are dealing with the creditors and other parties-in-interest, he said. “If BRING THE “A” TEAM Said Catalanello: “If you are going to travel down the road of a non-judicial workout or liquidation, CBIZ’s Esther DuVal conveys her views on out-of-courts and the use of the ABC. 16 DUANE MORRIS - OPTIMIZE you’re good the first month, you have flexibility.” .

THE SECTION 363 BATON The advantage of a Section 363 sale can be very attractive to both the debtor and the buyer. From the buyer’s perspective, said William Heuer, “When you go out and buy a company outside of a bankruptcy, you take all the fleas, ticks and warts that come with it, including any litigation pending against the company. When you buy a 363 asset, it sanitizes the assets,” he said. “You line up the sale, move on and get out of there.” SLOW AND STEADY WINS THE RACE A Section 363 sale is not always a clear cut Speed is necessary sometimes, but be warned: Its approach, and its results may vary over time as new impulsive younger brother, haste, can make waste. case law emerges.

“There is push at times,” said Heuer, a partner in Duane Morris’ New York office, “In the last few years, there’s been almost an “to do a Section 363 sale because of the quality of acceptance or normalcy for a 45- to 60-day sale title you get, but I question whether the full scope period from filing,” said Catalanello. “It’s incumbent of these protections is going to be available in the on the company side or creditors’ committee side to long term.” continue to push back on that. It’s really detrimental to the entire spirit of a fullsome sale process.

If “You have to be prepared to shift and move quickly there is a fire that needs to be put out, I get it, but in this environment,” said Catalanello. “On day one, I think we have to push back to see if it really is a the case could be over,” he continued. “If you take fire.

In this race to the finish line, people are getting the wrong turn early on, whether it’s cash collateral destroyed before the race begins. We’re pushing a or agreeing to some ridiculous restrictions on sale boulder up a hill. We shouldn’t just accept as status procedures, then the case is baked in stone.

If you quo that this asset has to be sold in 45 to 60 days.” feel that you have the better side, fight on day one. Set the tone and try to take control of the case. If In addition, those filing chapter 11 petitions need to you don’t, you’re letting someone else control the be prepared for contingencies. “The days of just filing case and possibly the outcome.” a chapter 11 case and then figuring out what you are going to do next are long over,” said Catalanello. DuVal pointed out that in addition to slowing down “You need to be prepared from the moment you the process, transparency is important.

“We had file with your plan A, which might be a complete a case where the CFO and all the officers had restructuring; plan B, which may be a partial a personal vested interest with a stalking horse restructuring with a sale of some non-core assets; bidder,” she recalled. “They did their best to chill the or plan C, which is ‘we’re going to sell everything.’” offers. With transparency, the value add is creating a fair process.” DUANE MORRIS - OPTIMIZE 17 .

SPEAKER PROFILES MODERATOR LAWRENCE J. KOTLER is a Partner at Duane Morris LLP. Mr. Kotler practices in the area of reorganization and finance, representing chapter 11 debtors-in-possession, chapter 11 trustees, chapter 7 trustees, liquidating trustees, creditors’ committees, secured creditors and large institutional unsecured creditors in all facets of bankruptcy.

Mr. Kotler is certified as a business bankruptcy specialist by the American Board of Certification. He is also a frequent speaker on bankruptcy and creditors’ rights issues. PANEL 1 MARK LAWRENCE is Managing Director, Opportunistic Credit, at Apollo Global Management.

Mr. Lawrence joined Apollo in 2012. He focuses on distressed investing and private capital solutions as part of Apollo’s Opportunistic Credit efforts.

Previously, Mr. Lawrence was a member of the investment group at Solus Alternative Asset Management, and prior to that, he was a member of the investment group at Stanfield Capital Partners. ROB WARSHAUER is Managing Director, Co-Head of Restructuring Group and Manager of Investment Banking Group at Imperial Capital. Mr.

Warshauer’s team has advised on hundreds of complex distressed situations, and it dedicates industry-specific, senior-level resources to each client matter. Prior to joining Imperial Capital, he was a Managing Director at Kroll Zolfo Cooper, where he primarily focused on the firm’s restructuring practice. Previously, he was a Managing Director and member of the Board of Directors of Giuliani Capital Advisors LLC, and its predecessor firm, Ernst & Young Corporate Finance LLC, where he specialized in corporate restructuring and mergers and acquisitions.

As part of his banking and restructuring experience, Mr. Warshauer has served as CEO and President of an international business services and manufacturing company responsible for over 2,500 employees in 16 countries, and he was President and a member of the Board of Directors of a publicly traded technology company that specialized in the development and manufacture of technologically advanced, energy-efficient, LED lighting products. WALTER J. GREENHALGH is a Partner at Duane Morris LLP.

Mr. Greenhalgh practices in the areas of commercial litigation and bankruptcy law, insolvency law and chapter 11 corporate and commercial reorganization. He is the managing partner of Duane Morris’ Newark office and a member of the firm’s national governing Partners Board. A past chair of the executive committee of the Bankruptcy Law Section of the New Jersey State Bar Association, he has been an officer of the Section for more than 10 years. JAMES J.

VINCEQUERRA is a Partner at Duane Morris LLP. Mr. Vincequerra focuses his practice on business reorganizations, creditors’ rights and general counseling.

He represents debtors, creditors’ committees, individual creditors, trustees and acquirers of assets of troubled companies in formal bankruptcy proceedings and in outof-court/workout scenarios. He is also actively involved in litigating disputes related to his client representations. 18 DUANE MORRIS - OPTIMIZE . PANEL 2 ESTHER DuVaL is the Managing Director at CBIZ MHM, LLC. Ms. DuVal serves as the Corporate Recovery Services group co-practice leader for the New York office. She specializes in creditors’ rights and has an extensive background working with matters ranging from mid-sized bankruptcies to high-profile cases.

Ms. DuVal has a thorough understanding of the complex issues involved in bankruptcy matters, and when applicable, she helps resolve disputes in an amicable manner through mediation. Ms.

DuVal joined the organization in 1996. Previously, she was a senior manager in the Corporate Recovery Group of BDO Seidman and developed industry experience with investment banking at Morgan Stanley. ROBERT D. KATZ is President of Executive Sounding Board Associates LLC.

Mr. Katz helps companies through crises and turnarounds with the vision and insight earned from more than 25 years on the front lines. Hundreds of companies have relied on him in high-pressure situations to create and execute the strategy needed to restructure or improve operating performance.

He works with public and private middle-market companies, both in and out of bankruptcy, who are facing operational or financial challenges. Mr. Katz acts as Interim President, Chief Financial Officer, Chief Operating Officer, Chief Restructuring Officer or Treasurer, helping companies improve operating performance and generate additional cash flow.

He acts as plan administrator, distribution trustee and receiver. Mr. Katz also serves as an advisor to U.S.

trustees, creditor committees, company management, lenders and private equity funds. GERARD S. CATALANELLO is a Partner at Duane Morris LLP. Mr.

Catalanello practices in the area of bankruptcy and creditors’ rights law, representing debtors, creditors, creditors’ committees, financial institutions, liquidation trusts, equity holders, trustees and acquirers of assets of troubled companies in formal bankruptcy proceedings, as well as in out-of-court workouts. Mr. Catalanello has also served as counsel to official committees of unsecured creditors in a range of chapter 11 cases and has represented major institutions in connection with the negotiation and sale of hundreds of millions of dollars of claims in major chapter 11 cases. WILLIAM C.

HEUER is a Partner at Duane Morris LLP. Mr. Heuer practices in the areas of business reorganization, bankruptcy law and creditors’ rights litigation.

He represents secured creditors in loan default workouts and bankruptcies, with experience in a wide range of industries, including commercial shipping, satellite and telecommunications, golf and entertainment, retail merchandise, air travel (domestic and international), healthcare and long-term health management facilities, and real estate. Mr. Heuer represents debtors in both domestic and international bankruptcy proceedings. DUANE MORRIS - OPTIMIZE 19 .

Chicago Lake Tahoe Pittsburgh San Francisco Silicon Valley Las Vegas Los Angeles San Diego Atlanta Houston Boston New York Newark Cherry Hill Philadelphia Wilmington Baltimore Washington, D.C. Boca Raton Miami Mexico City Duane Morris Office Representative / Liaison Office 20 DUANE MORRIS - OPTIMIZE . ABOUT DUANE MORRIS With experienced bankruptcy and restructuring lawyers across our domestic and global platform, coupled with the deep capabilities of more than 700 lawyers across all practice areas, Duane Morris offers the resources to optimize our clients’ interests. From creditor to debtor, and trustee to committee, our bankruptcy London, Uk practice is regularly recognized as one of the most active for both case volume and value of liabilities. We leverage our core experience in bankruptcy law, creditors’ rights and asset recovery actions and the full range of services for commercial mortgages and other asset classes, working with banks, non-bank lenders, special servicers, debt purchasers and asset buyers. On the distressed deal side, our lawyers have negotiated and brokered major transactions China industries Shanghai, in such as manufacturing, real estate, telecommunications and retail. Five of the practice group’s former attorneys are sitting United States Bankruptcy Court judges, and another is a judge on the United States Court of Appeals for the Third Circuit. Oman Hanoi, Vietnam Myanmar Ho Chi Minh City Singapore DUANE MORRIS - OPTIMIZE 21 .

Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Philadelphia | Chicago | Washington, D.C. | San Francisco Silicon Valley | San Diego | Shanghai | Boston | Houston | Los Angeles | Hanoi | Ho Chi Minh City | Atlanta | Baltimore | Wilmington | Miami Boca Raton | Pittsburgh | Newark | Las Vegas | Cherry Hill | Lake Tahoe | Myanmar | Oman | Duane Morris LLP – A Delaware limited liability partnership This publication is for general information and does not include full legal analysis of the matters presented. It should not be construed or relied upon as legal advice or legal opinion on any specific facts or circumstances. The invitation to contact the attorneys in our firm is not a solicitation to provide professional services and should not be construed as a statement as to any 22 DUANE MORRIS - OPTIMIZE availability to perform legal services in any jurisdiction in which such attorney is not permitted to practice.

© Duane Morris LLP 2014. .