Description

views

March 2016

Leases: Not Just for the Footnotes Anymore

Adam Roark, Senior Manager | DHG Assurance Services

Overview

On February 25, 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 201602 Leases (Topic 842), a new standard that will govern the accounting for lease contracts beginning with the 2019 calendar

year-end for public companies and the 2020 calendar year-end for all other entities1. To affect these changes, this ASU

amends the existing FASB Accounting Standards Codification (ASC) and creates a new Topic 842, Leases.

Contents

Overview................................................................. 1

Key concepts......................................................... 2

Lessee accounting.................................................

4 Lessor accounting.................................................. 7 Sale-Leaseback transactions................................. 7 Presentation and disclosure...................................

8 Scope, effective dates, and transition.................... 8 Appendix A – Identifying a lease.......................... 10 Appendix B – Examples.......................................

11 Assurance | Tax | Advisory | dhgllp.com Lease assets and liabilities will be recorded on the balance sheet The key difference between existing standards and ASU 2016-02 is the requirement for lessees to recognize on their balance sheet all lease contracts with lease terms greater than 12 months, including operating leases. Specifically, lessees are required to recognize on the balance sheet at lease commencement, both: • A right-of-use (ROU) asset, representing the lessee’s right to use the leased asset over the term of the lease; and, • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. Reporting considerations relating specifically to private company matters are denoted with this symbol . views The new lease standard requires lessees to classify leases as either operating or finance leases, which are similar to the current operating and capital lease classifications. However, the distinction between these two classifications under the new standard does not relate to balance sheet treatment, but relates to treatment and recognition in the statements of income and cash flows. As discussed later in this document, the standard requires a modified retrospective application, which requires companies to apply the new guidance as of the beginning of the earliest comparative period presented in the period in which the standard is adopted. As a result, companies should begin now to familiarize themselves with the new standard, particularly how it differs from existing guidance, and assess how these changes could impact their compensation plans, loan covenants and other business dynamics. Lessor accounting is largely unchanged from current accounting principles generally accepted in the United States (U.S. GAAP), with the exception of some revisions made to ensure consistency with the revised lessee guidance of ASU 2016-02 and with FASB ASC 606, Revenue from Contract with Customers. Key concepts Identifying a lease A company is required to determine whether a contract is, or contains, a lease at the inception of the contract.

Once the initial determination has been made, the company cannot reassess, unless the terms and conditions of the contract are modified. Big changes, bigger impact expected It has been speculated that the release of this standard could result in as much as $2 trillion in assets and liabilities being added to the balance sheets of U.S companies.2 Certain industries where it is common practice to hold numerous equipment and real estate leases, such as retail stores, telecommunications, restaurant chains, airlines, and banks, are expected to be most impacted. All companies with leases will be impacted to some degree, however, the final impact of the new leasing standard will vary, depending on the size and scope of a company’s leasing activities. Appendix A of this document includes a flowchart to assist with the determination of identifying a lease. A contract is defined as being, or containing, a lease if it conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration. Assets can be either explicitly or implicitly specified by a contract. Although the final economic impact is undetermined, the changes within the new standard will effect multiple aspects of a business’s operations.

For instance, the addition of leases to the balance sheet is likely to impact commonly used financial indicators, such as debt covenants ratios, regulatory capital requirements, and other contracts (e.g. some management compensation plans may have performance based metrics, which may be impacted). Control over the use of the asset means that for a period of time the customer has both: • The right to obtain substantially all of the economic benefits from the use of the asset, and • The right to direct the use of the asset. The assessment of whether a company has the right to direct the use of the asset requires judgement. However, a company would have the right to direct the use of the asset in either of the following situations: Implications for Key Metrics and Debt Covenants The new lease standard could have a significant impact on the key metrics companies report to their investors as well as on a company’s debt covenant computations.

Below are a some of the key ratios that may be impacted by the new lease accounting standard. Key Metric Expected Effect Leverage Ratio: Debt/Equity Increases Current Ratio: Current Assets/Current Liabilities Decreases Debt to EBITDA: Debt/EBITDA Increases Return on Assets: Net Income/Assets • The customer has the right to operate the asset throughout the period of use, without the supplier having the right to change the operating instructions. Decreases Assurance | Tax | Advisory | dhgllp.com • The customer designed the asset in a way that predetermines how, and for what purpose, the asset will be used throughout the period of use. If a supplier has substantive substitution rights (i.e., the right to substitute the identified asset for another asset) then the customer does not have the right to use an identified asset. For substitution rights to be considered substantive, both of the following must be true: • The supplier has the practical ability to substitute alternative assets throughout the period of use, 2 . views The identification of a lease in a contract, in most cases, will decide whether or not leases are recognized on the balance sheet. This decision caries similar weight to the determination of whether a lease was a capital lease or an operating lease under the existing standard. In determining whether it is ‘reasonably certain’ that a renewal option (or termination option) will be exercised, a company must consider all relevant factors that create an economic incentive for the lessee to exercise the option, including contract, asset, entity, and market based factors. Examples of these factors include: • The economic benefits for the supplier to substitute the asset are expected to exceed the costs of substitution. The consideration of whether or not substitution rights are substantive should occur at inception of the contract. Further, future events, not deemed likely to occur, are to be excluded from the evaluation of whether or not substitution rights are substantive.

ASC 842-10-15-11 includes specific examples of future events that would be excluded. • Contractual terms and conditions for optional periods compared with current market rates. • Leasehold improvements that are expected to have significant value to the lessee when the option becomes exercisable. Short-term leases and lease term As an exception to the general requirement that all leases be recognized on balance sheet, the new lease standard allows companies to account for leases whose lease term is 12 months or less off the balance sheet – similar to operating leases under existing accounting guidance. However, if a company elects an accounting policy to apply this short-term lease exception, it must do so for all similar qualifying leases within the same asset class (e.g., all qualifying short-term laptop leases). • Costs related to the termination of the lease and the signing of a new lease, such as negotiation costs and relocation costs. • The importance of the underlying asset to the lessee’s operations. Under existing accounting guidance, companies only consider renewal periods as part of the lease term if it is reasonably assured the renewal option will be exercised. While the new standard uses the term “reasonably certain”, the standard explains that “the [FASB] views reasonably certain and reasonably assured as synonyms that should be applied in the same way.” Under the new standard, lease term is defined as: The non-cancellable period for which a lessee has the right to use an underlying asset, together with all of the following: a. Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option; b. Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option; and c. Periods representing renewals or extensions of the lease at the option of the lessor. Refer to Appendix B-1, Example – Lease term, for an explanation of how a company could determine if a lease contract qualifies for the short-term lease scope exception. Assurance | Tax | Advisory | dhgllp.com 3 .

views Lease components • The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. It is common for many lease contracts to contain both lease and non-lease components. For example, a contract containing the lease of specialized equipment, may also include provisions for maintenance services to be provided by the lessor. These maintenance services would be considered non-lease components and would be separated from the lease components under the existing standards. Similarly, the new standard requires separation of the lease and nonlease components.

The new standard also contains additional guidance on the identification of non-lease components, as this determination is more significant given that lease components of a contract will now be accounted for on the balance sheet. • The lease term is for the major part of the remaining economic life of the underlying asset. However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for the purposes of classifying the lease. • The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. • The underlying asset is of such specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. In general, contract consideration and any initial direct costs should be allocated to lease and non-lease components based on the relative standalone price of the separate components. However, the new standard allows lessees, as a practical expedient, to make an accounting policy election to account for lease and non-lease components as a single lease component.

This accounting policy election should be made by class of underlying assets – similar to the short term lease exception. Although the finance lease classification criteria is substantially the same as the pre-existing capital lease criteria, the new standard adds the criterion that a lease of specialized assets for which there is no alternative use at the end of the lease term would qualify as a finance lease. This criterion was added to reflect the economic reality that if an asset has no alternative use at the end of a lease, then the lessee has substantially used all of the benefits of that asset. Related party leases Related party leases are to be accounted for and classified under the new standard on the basis of the legally enforceable terms and conditions of the lease. Further, in the separate financial statements of related parties, the accounting and classification of leases should be the same as for leases between unrelated parties.

This differs from current guidance, which requires related party leases to be accounted for and classified on the basis of the economic substance of the arrangement. The guidance in the new standard may remove some of the current challenges encountered when there are no legally enforceable terms and conditions (e.g. month to month related party leases, or related party leases with undefined payment terms). Any leases not meeting the criteria for a finance lease shall be classified as an operating lease. The new classification criteria are substantially the same as the existing operating vs.

capital lease classification criteria with the addition of the specialized assets criterion listed above. And while the new criteria do not reference the “brightline” tests included in existing guidance (i.e., the “75%” and “90%” hurdles), the new lease standard allows companies to use those existing “bright lines” as one reasonable approach for assessing the criteria listed above. Consequently, companies should not experience significant changes in lease classification conclusions under the new standard. Lessee accounting Classification Leases are required to be classified by lessees as either operating leases or finance leases.

A lease contract is a finance lease for a lessee if any of the following are met: • The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. Assurance | Tax | Advisory | dhgllp.com 4 . views Private Company Matters Private companies, those companies that do not meet the FASB definition of a Public Business Entity, are permitted to make an accounting policy election for all leases to use a risk-free discount rate when calculating the lease liability. The risk-free rate used for any particular lease should be determined using a period that is comparable with the lease term. This option may make the additional calculations under the standard easier to implement for some private companies. However, since the risk free rate is most often lower than applicable borrowing rates, this option is likely to result in a larger liability. Initial measurement The new standard requires lessees to recognize on the balance sheet at commencement for all leases both: If a lessee cannot readily determine the rate implicit in the lease, it should use its incremental borrowing rate to discount the lease.

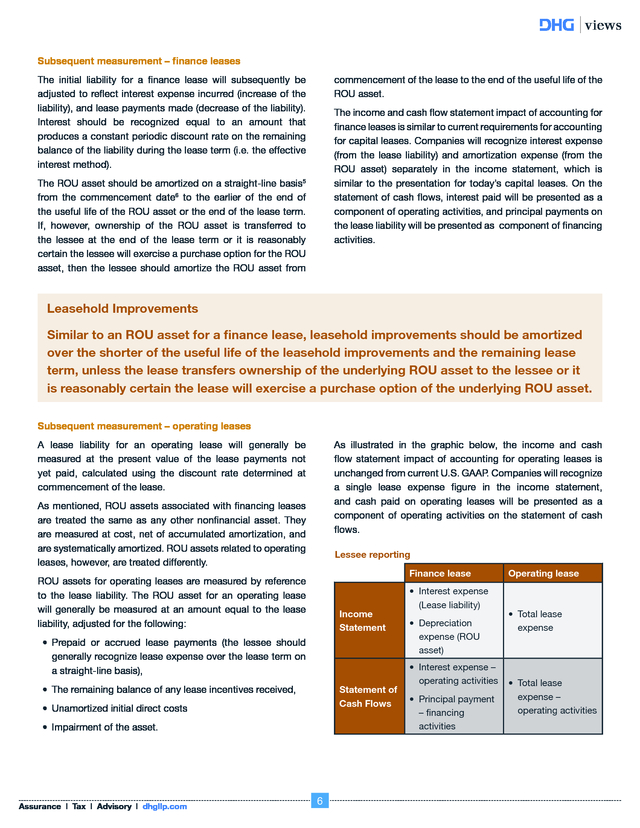

In addition, private companies4 will have the option to use the risk-free rate in calculating the present value of lease payments. • A ROU asset, representing the lessee’s right to use the leased asset over the term of the lease; and, • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. As illustrated below, the ROU asset is initially recorded at an amount equal to: The lease liability is initially recorded at an amount equal to the present value of the remaining lease payments3 due over the lease term, discounted at the rate implicit in the lease. • The initial lease liability; plus The rate implicit in the lease is the rate that causes the present value of the net investment in the lease to equal the sum of: • Any initial direct costs incurred by the lessee; less • Any lease payments made at or before lease commencement; plus • Any lease incentives received from the lessor. • The fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor, and • Any capitalized initial direct costs incurred by the lessor. The following illustrates the initial balance sheet measurement concepts under the new lease accounting standard. = Initial Lease Liability Initial ROU Asset = Assurance | Tax | Advisory | dhgllp.com Initial Lease Liability + Present value of lease payments due over the lease term • Lease payments made at or before lease commencement • Initial direct costs 5 - Lease incentives received from the lessor . views Subsequent measurement – finance leases The initial liability for a finance lease will subsequently be adjusted to reflect interest expense incurred (increase of the liability), and lease payments made (decrease of the liability). Interest should be recognized equal to an amount that produces a constant periodic discount rate on the remaining balance of the liability during the lease term (i.e. the effective interest method). commencement of the lease to the end of the useful life of the ROU asset. The income and cash flow statement impact of accounting for finance leases is similar to current requirements for accounting for capital leases. Companies will recognize interest expense (from the lease liability) and amortization expense (from the ROU asset) separately in the income statement, which is similar to the presentation for today’s capital leases. On the statement of cash flows, interest paid will be presented as a component of operating activities, and principal payments on the lease liability will be presented as component of financing activities. The ROU asset should be amortized on a straight-line basis5 from the commencement date6 to the earlier of the end of the useful life of the ROU asset or the end of the lease term. If, however, ownership of the ROU asset is transferred to the lessee at the end of the lease term or it is reasonably certain the lessee will exercise a purchase option for the ROU asset, then the lessee should amortize the ROU asset from Leasehold Improvements Similar to an ROU asset for a finance lease, leasehold improvements should be amortized over the shorter of the useful life of the leasehold improvements and the remaining lease term, unless the lease transfers ownership of the underlying ROU asset to the lessee or it is reasonably certain the lease will exercise a purchase option of the underlying ROU asset. Subsequent measurement – operating leases A lease liability for an operating lease will generally be measured at the present value of the lease payments not yet paid, calculated using the discount rate determined at commencement of the lease. As illustrated in the graphic below, the income and cash flow statement impact of accounting for operating leases is unchanged from current U.S.

GAAP. Companies will recognize a single lease expense figure in the income statement, and cash paid on operating leases will be presented as a component of operating activities on the statement of cash flows. As mentioned, ROU assets associated with financing leases are treated the same as any other nonfinancial asset. They are measured at cost, net of accumulated amortization, and are systematically amortized.

ROU assets related to operating leases, however, are treated differently. Lessee reporting Finance lease ROU assets for operating leases are measured by reference to the lease liability. The ROU asset for an operating lease will generally be measured at an amount equal to the lease liability, adjusted for the following: Income Statement • Prepaid or accrued lease payments (the lessee should generally recognize lease expense over the lease term on a straight-line basis), • The remaining balance of any lease incentives received, Statement of Cash Flows • Unamortized initial direct costs • Impairment of the asset. Assurance | Tax | Advisory | dhgllp.com 6 • Interest expense (Lease liability) • Depreciation expense (ROU asset) • Interest expense – operating activities • Principal payment – financing activities Operating lease • Total lease expense • Total lease expense – operating activities . views There will be a number of different approaches to implement and account for leases under the new standard. The selection of policies and procedures to account for adopting the standard will require consideration of internal controls and other financial reporting requirements Appendix B-2, Example lessee accounting, demonstrates multiple ways in which a company would record a lease for both a finance and operating lease. These lease accounting examples include both a comprehensive methodology and a high-level “display approach”, which would likely be more appropriate for private companies with relatively few leases. Impairment • If a lease does not meet the criteria of a sales-type lease, a lessor would classify the lease as a direct financing lease if both 1) the present value of the sum of the lease payments and any residual value guaranteed by the lessee exceeds the fair value of the underlying asset, and 2) it is probable the lessor will collect the lease payment plus any amount necessary to satisfy a residual value guarantee. The ROU asset for both finance and operating leases is subject to the same impairment considerations as is required of other long-lived assets.7 If a ROU asset is impaired, the asset will be measured at its carrying amount immediately after the impairment less any accumulated amortization. ROU assets relating to finance leases should continue to be amortized on a straight-line basis, as described above, from the date of impairment to the earlier of the end of the useful life of the ROU asset or the end of the lease term. If impairment of an ROU asset associated with an operating lease is recorded, then subsequent to impairment the single lease cost will be calculated as the sum of the following: • Leases that do not meet the definition of either a salestype lease or a direct financing lease are operating leases. • The new lease classification criteria remove the incremental tests that now exist for leases involving real estate to achieve better alignment with the new revenue recognition standard. • Amortization of the remaining right-of-use asset after the impairment on a straight-line basis, and • The accounting model for leveraged leases in current U.S. GAAP was not retained for leases that commence after the effective date of the new standard. • Accretion of the lease liability, determined for each remaining period during the lease term as the amount that produces a constant periodic discount rate on the remaining balance of the liability. Sale-leaseback transactions While the new lease standard retains the notion of a saleleaseback transaction, it modifies how the lessee and lessor determine the appropriate accounting for such a transaction. Lessor accounting Lessor accounting is largely unchanged from current U.S. GAAP. A majority of operating leases should remain classified as operating leases, and lessors should continue to recognize income, generally, on a straight-line basis over the lease term. The changes made to the lessor accounting model within the new lease standard were primarily related to aligning the lessor guidance with the revised lessee guidance and with the new revenue standard, FASB ASC 606, Revenue from Contracts with Customers.

Key aspects of the lessor guidance include the following: Under the new standard, the seller-lessee first assesses whether the transfer of the underlying asset to the buyerlessor qualifies as a sale under the new revenue standard. This analysis focuses on whether the buyer-lessor has obtained control over the asset. The new lease standard clarifies that the leaseback arrangement does not preclude the buyer-lessor from obtaining control (thus accounting as a sale) unless the lease is determined to be a finance lease. If the transfer does not qualify as a sale, the transaction is accounted for as a financing arrangement. The seller-lessee continues to record the underlying asset on its balance sheet and recognizes a liability for any proceeds received from the buyer-lessor. • Retains the current lease classifications – operating leases, direct-finance leases and sales-type leases – and generally how each lease type is accounted for. • The standard does change how a lessor determines the appropriate lease classification for each lease to better align the lessor guidance with the revised lessee classification guidance noted above. In contrast, if the transfer qualifies as a sale, then the sellerlessee derecognizes the underlying asset and recognizes a gain or loss on sale.

The leaseback would be accounted in accordance with the new lease standard as an operating lease. (i.e. accounted for as an operating lease by the lessee). • A sales-type lease is subject to the same classification criteria as a finance lease in the lessee model. Assurance | Tax | Advisory | dhgllp.com 7 .

views Presentation and disclosure The new lease standard includes expanded presentation and disclosure requirements to provide additional quantitative and qualitative information, including significant judgments involved in the accounting for leases and the amounts recognized in the financial statements from leases. The objective of the disclosures is to enable users of the financial statements to assess the amount, timing and uncertainty of cash flows arising from leases. Among these requirements, companies will present separately financing ROU assets and liabilities from operating ROU assets and liabilities. Certain other disclosures required under the new lease standard include: Disclosure requirements Lessor Lessee • Information about the nature of its leases • Information about the nature of its leases • Maturity analysis of lease liabilities • Maturity analysis of lease investments • Lease expense, split between operating and capital leases • Profit or loss recognized at lease commencement (for sales-type leases) • Short-term lease expense • Lease income • Variable lease expense • Qualitative and quantitative information about significant changes in residual values of leased assets • Sublease income • Weighted average remaining lease term • Weighted average discount rate Scope, effective dates, and transition Scope Effective dates ASU 2016-02 applies to all leases, including subleases, with the following exceptions: The effective date for public companies8 is fiscal years beginning after December 15, 2018, and interim periods therein.

For all other companies the standard is effective for fiscal years beginning after December 15, 2019 and interim periods within those fiscal years beginning after December 15, 2020. Early adoption is permitted for all companies and organizations. • Leases of intangible assets, • Leases to explore or use minerals, oil, natural gas, and similar nonregenerative resources, • Leases of biological assets, including timber, • Leases of inventory, and • Leases of assets under construction. Companies need to start now to assess the capabilities of their financial reporting systems and controls, as they relate to the adoption of this new standard. The new lease standard requires a modified retrospective implementation approach, which means when companies adopt they will need to apply the new lease guidance to each comparable period presented.

For instance, a public company who adopts for the 2019 calendar year-end and reports three years of comparable information will need to evaluate how the standard will impact the presentation of the 2017 and 2018 calendar year-end financial statements. Assurance | Tax | Advisory | dhgllp.com 8 . views Transition The first three practical expedients must be elected together (i.e., all or none). In contrast, the fourth practical expedient may be elected separately; however, if elected, it must be treated as an accounting policy election (i.e., it cannot be elected on a lease-by-lease basis). Further, the policy election for the short-term lease exemption would also apply to comparable periods presented upon adoption. For companies that avail themselves of the practical expedients, the primary effect of adoption will be the grossing up of the balance sheet for any existing operating leases. ASU 2016-02 requires companies to adopt its provisions using a modified retrospective approach, which requires the application of the new standard as of the beginning of the earliest comparative period presented.

This requirement is irrespective of whether or not a company elects to early adopt the standard. Therefore, whenever a company adopts the new standard, it will be required to consider the impact of the new standard for all comparable periods presented in the financial statements issued during the year of adoption. Upon adoption, a lessee will be required to recognize a ROU asset and a lease liability for operating leases at the later of the beginning of the earliest period presented on the balance sheet and the commencement date of the lease. Further, the lessee will measure the lease liability at present value using a discount rate established at the later of the beginning of the earliest period presented and the lease commencement date.

For instance, consider the case of a calendar year-end reporting company who presents three comparable periods and adopts the standard in 2019. This company would need to present an ROU asset and a lease liability as of the later of beginning of 2017, or the lease commencement date for leases that had not commenced as of the beginning of 2017. The lease liability for each lease will be calculated using the discount rate in effect as of the beginning of 2017, or the lease commencement date for leases that had not commenced as of the beginning of 2017. The new standard also provides certain “practical expedients” that companies may elect at the date of transition to ease the burden of adoption. The practical expedients are as follows: 1. A company need not reassess whether any expired or existing contracts are or contain leases. 2. A company need not reassess the lease classification for any expired or existing leases (i.e., all existing leases that were classified as operating leases in accordance with Topic 840 will be classified as operating leases and all existing leases that were classified as capital leases in accordance with Topic 840 will be classified as finance leases). 3. A company need not reassess initial direct costs for any existing leases. 4. A company also may elect a practical expedient to use hindsight in determining the lease term when considering lessee options to extend or terminate the lease and to purchase the underlying asset. 1. ASU 2016-02 applies to all entities that enter into a lease, with some specified scope exceptions.

Throughout this document the term “company” is used to refer to the entity entering into a lease. This term “company” is used as a general term to aid in the readability of the document. As such, the guidance is equally as applicable to not-for-profit organizations and other entities that enter into a lease. For the purpose of this transition guidance the following are included in the definition of a public company: a public business entity, a not-for-profit entity that has issued or is a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market, and an employee benefit plan that files or furnishes financial statements with or to the U.S.

Securities and Exchange Commission. 2. Rapoport, Michael (2015, November 10) Coming to Balance Sheet Near You: $2 Trillion in Leases. The Wall Street Journal. Retrieved from http://www.wsj.com. 3. Lease payments exclude contingent rental payments (e.g., rent based on percent of sales). 4. Entities that are not public business entities. 5. Under the new lease standard the straight-line basis is used “unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived from the right to use the underlying asset” (ASC 842-20-35-7). 6. The date on which a lessor makes an underlying asset available for use by an lessee. 7. Refer to ASC 360-10-35 for additional information on the impairment guidance for long-lived assets. 8. For the purpose of this transition guidance the following are included in the definition of a public company: a public business entity, a not-for-profit entity that has issued or is a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market, and an employee benefit plan that files or furnishes financial statements with or to the U.S.

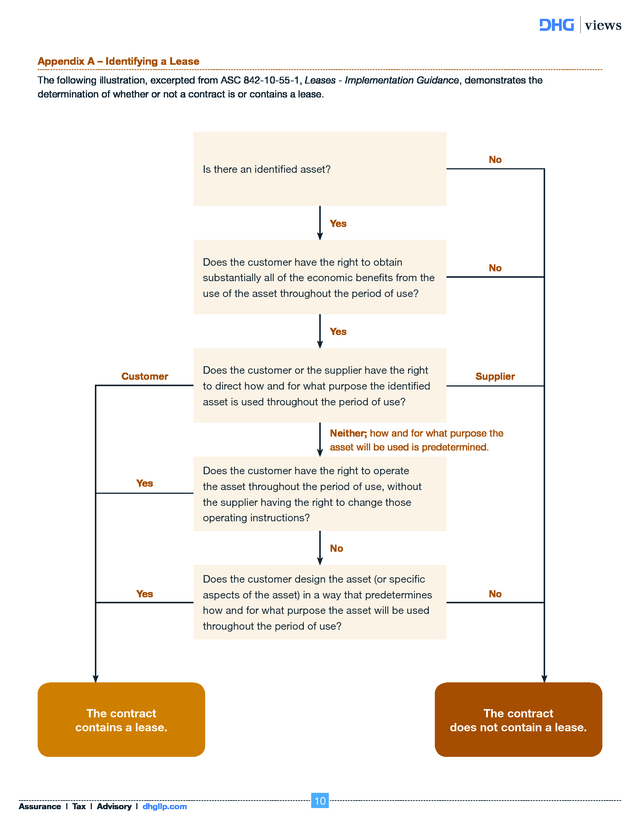

Securities and Exchange Commission. Assurance | Tax | Advisory | dhgllp.com 9 . views Appendix A – Identifying a Lease The following illustration, excerpted from ASC 842-10-55-1, Leases - Implementation Guidance, demonstrates the determination of whether or not a contract is or contains a lease. Is there an identified asset? No Yes Does the customer have the right to obtain substantially all of the economic benefits from the use of the asset throughout the period of use? No Yes Customer Does the customer or the supplier have the right to direct how and for what purpose the identified asset is used throughout the period of use? Supplier Neither; how and for what purpose the asset will be used is predetermined. Yes Does the customer have the right to operate the asset throughout the period of use, without the supplier having the right to change those operating instructions? No Yes Does the customer design the asset (or specific aspects of the asset) in a way that predetermines how and for what purpose the asset will be used throughout the period of use? The contract contains a lease. Assurance | Tax | Advisory | dhgllp.com No The contract does not contain a lease. 10 . views Appendix B – Examples B-1 – Lease terms – short-term determination Conclusion: Facts: Based on a review of the relevant factors that create an economic incentive (e.g., the significant leasehold improvements involved, the material tax incentive being offered), Darling Widgets concludes it is reasonably certain that it will exercise the renewal option. As a result, the lease does not qualify as a short-term lease (because the lease term exceeds 12 months). • Darling Widgets enters into a lease agreement with RE Rental Inc. to lease a building for an initial period of 10 months. • At the end of 10 months, Darling Widgets has the option to renew the lease contract for an additional 36-month period. • Darling Widgets intends to use the building for the location of its new corporate headquarters, which requires the installation of significant leasehold improvements. • Additionally, Darling Widgets has been offered a material tax incentive from the local government for relocating its headquarters. However, to receive the tax incentive, Darling must remain in the locality for at least two years. Darling intends to meet that requirement. B-2 – Lessee accounting The following example walks through the initial and subsequent accounting treatment of the same lease for both the operating and finance lease classifications.

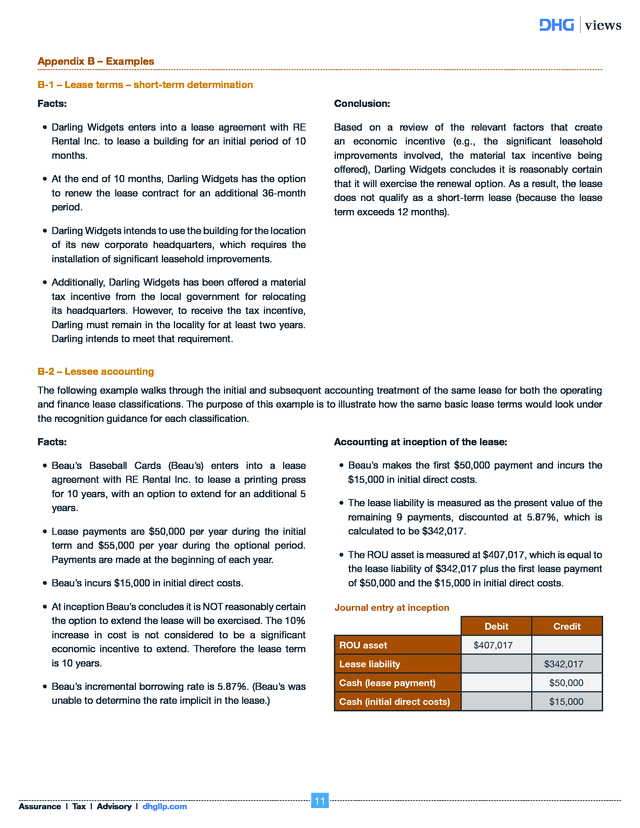

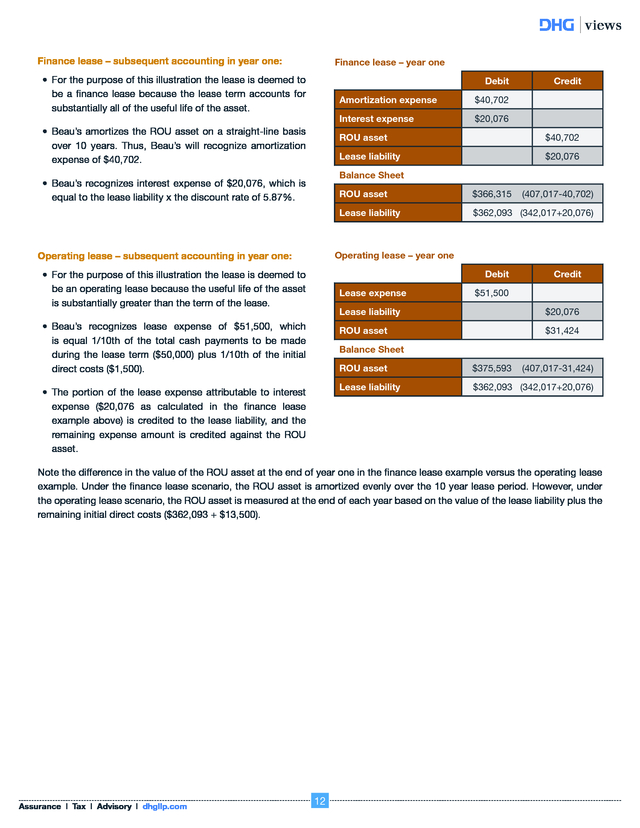

The purpose of this example is to illustrate how the same basic lease terms would look under the recognition guidance for each classification. Accounting at inception of the lease: Facts: • Beau’s makes the first $50,000 payment and incurs the $15,000 in initial direct costs. • Beau’s Baseball Cards (Beau’s) enters into a lease agreement with RE Rental Inc. to lease a printing press for 10 years, with an option to extend for an additional 5 years. • The lease liability is measured as the present value of the remaining 9 payments, discounted at 5.87%, which is calculated to be $342,017. • Lease payments are $50,000 per year during the initial term and $55,000 per year during the optional period. Payments are made at the beginning of each year. • The ROU asset is measured at $407,017, which is equal to the lease liability of $342,017 plus the first lease payment of $50,000 and the $15,000 in initial direct costs. • Beau’s incurs $15,000 in initial direct costs. • At inception Beau’s concludes it is NOT reasonably certain the option to extend the lease will be exercised. The 10% increase in cost is not considered to be a significant economic incentive to extend.

Therefore the lease term is 10 years. Journal entry at inception Debit ROU asset Lease liability $407,017 $342,017 Cash (lease payment) 11 $50,000 Cash (initial direct costs) • Beau’s incremental borrowing rate is 5.87%. (Beau’s was unable to determine the rate implicit in the lease.) Assurance | Tax | Advisory | dhgllp.com Credit $15,000 . views Finance lease – subsequent accounting in year one: Finance lease – year one • For the purpose of this illustration the lease is deemed to be a finance lease because the lease term accounts for substantially all of the useful life of the asset. Debit Amortization expense $40,702 Interest expense • Beau’s amortizes the ROU asset on a straight-line basis over 10 years. Thus, Beau’s will recognize amortization expense of $40,702. Credit $20,076 ROU asset $40,702 Lease liability $20,076 Balance Sheet • Beau’s recognizes interest expense of $20,076, which is equal to the lease liability x the discount rate of 5.87%. ROU asset $366,315 Lease liability $362,093 (342,017+20,076) (407,017-40,702) Operating lease – year one Operating lease – subsequent accounting in year one: Debit • For the purpose of this illustration the lease is deemed to be an operating lease because the useful life of the asset is substantially greater than the term of the lease. Lease expense Credit $51,500 Lease liability $20,076 ROU asset • Beau’s recognizes lease expense of $51,500, which is equal 1/10th of the total cash payments to be made during the lease term ($50,000) plus 1/10th of the initial direct costs ($1,500). $31,424 Balance Sheet ROU asset Lease liability • The portion of the lease expense attributable to interest expense ($20,076 as calculated in the finance lease example above) is credited to the lease liability, and the remaining expense amount is credited against the ROU asset. $375,593 $362,093 (342,017+20,076) (407,017-31,424) Note the difference in the value of the ROU asset at the end of year one in the finance lease example versus the operating lease example. Under the finance lease scenario, the ROU asset is amortized evenly over the 10 year lease period. However, under the operating lease scenario, the ROU asset is measured at the end of each year based on the value of the lease liability plus the remaining initial direct costs ($362,093 + $13,500). Assurance | Tax | Advisory | dhgllp.com 12 .

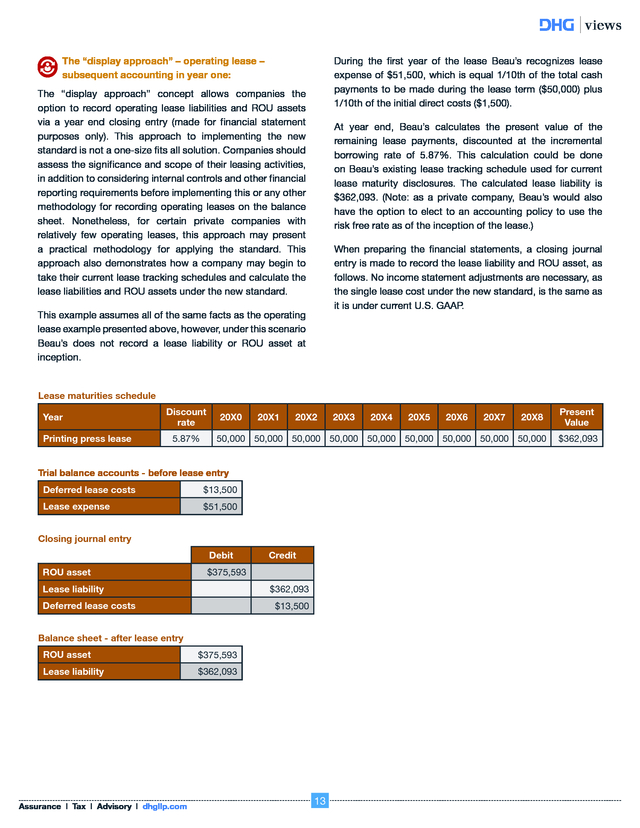

views The “display approach” – operating lease – subsequent accounting in year one: During the first year of the lease Beau’s recognizes lease expense of $51,500, which is equal 1/10th of the total cash payments to be made during the lease term ($50,000) plus 1/10th of the initial direct costs ($1,500). The “display approach” concept allows companies the option to record operating lease liabilities and ROU assets via a year end closing entry (made for financial statement purposes only). This approach to implementing the new standard is not a one-size fits all solution. Companies should assess the significance and scope of their leasing activities, in addition to considering internal controls and other financial reporting requirements before implementing this or any other methodology for recording operating leases on the balance sheet. Nonetheless, for certain private companies with relatively few operating leases, this approach may present a practical methodology for applying the standard.

This approach also demonstrates how a company may begin to take their current lease tracking schedules and calculate the lease liabilities and ROU assets under the new standard. At year end, Beau’s calculates the present value of the remaining lease payments, discounted at the incremental borrowing rate of 5.87%. This calculation could be done on Beau’s existing lease tracking schedule used for current lease maturity disclosures. The calculated lease liability is $362,093.

(Note: as a private company, Beau’s would also have the option to elect to an accounting policy to use the risk free rate as of the inception of the lease.) When preparing the financial statements, a closing journal entry is made to record the lease liability and ROU asset, as follows. No income statement adjustments are necessary, as the single lease cost under the new standard, is the same as it is under current U.S. GAAP. This example assumes all of the same facts as the operating lease example presented above, however, under this scenario Beau’s does not record a lease liability or ROU asset at inception. Lease maturities schedule Year Printing press lease Discount rate 5.87% 20X0 20X1 20X2 Deferred lease costs $13,500 Lease expense $51,500 Closing journal entry Debit Credit $375,593 Lease liability $362,093 Deferred lease costs $13,500 Balance sheet - after lease entry ROU asset $375,593 Lease liability $362,093 Assurance | Tax | Advisory | dhgllp.com 20X4 20X5 20X6 20X7 20X8 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 Trial balance accounts - before lease entry ROU asset 20X3 13 Present Value $362,093 .

4 Lessor accounting.................................................. 7 Sale-Leaseback transactions................................. 7 Presentation and disclosure...................................

8 Scope, effective dates, and transition.................... 8 Appendix A – Identifying a lease.......................... 10 Appendix B – Examples.......................................

11 Assurance | Tax | Advisory | dhgllp.com Lease assets and liabilities will be recorded on the balance sheet The key difference between existing standards and ASU 2016-02 is the requirement for lessees to recognize on their balance sheet all lease contracts with lease terms greater than 12 months, including operating leases. Specifically, lessees are required to recognize on the balance sheet at lease commencement, both: • A right-of-use (ROU) asset, representing the lessee’s right to use the leased asset over the term of the lease; and, • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. Reporting considerations relating specifically to private company matters are denoted with this symbol . views The new lease standard requires lessees to classify leases as either operating or finance leases, which are similar to the current operating and capital lease classifications. However, the distinction between these two classifications under the new standard does not relate to balance sheet treatment, but relates to treatment and recognition in the statements of income and cash flows. As discussed later in this document, the standard requires a modified retrospective application, which requires companies to apply the new guidance as of the beginning of the earliest comparative period presented in the period in which the standard is adopted. As a result, companies should begin now to familiarize themselves with the new standard, particularly how it differs from existing guidance, and assess how these changes could impact their compensation plans, loan covenants and other business dynamics. Lessor accounting is largely unchanged from current accounting principles generally accepted in the United States (U.S. GAAP), with the exception of some revisions made to ensure consistency with the revised lessee guidance of ASU 2016-02 and with FASB ASC 606, Revenue from Contract with Customers. Key concepts Identifying a lease A company is required to determine whether a contract is, or contains, a lease at the inception of the contract.

Once the initial determination has been made, the company cannot reassess, unless the terms and conditions of the contract are modified. Big changes, bigger impact expected It has been speculated that the release of this standard could result in as much as $2 trillion in assets and liabilities being added to the balance sheets of U.S companies.2 Certain industries where it is common practice to hold numerous equipment and real estate leases, such as retail stores, telecommunications, restaurant chains, airlines, and banks, are expected to be most impacted. All companies with leases will be impacted to some degree, however, the final impact of the new leasing standard will vary, depending on the size and scope of a company’s leasing activities. Appendix A of this document includes a flowchart to assist with the determination of identifying a lease. A contract is defined as being, or containing, a lease if it conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration. Assets can be either explicitly or implicitly specified by a contract. Although the final economic impact is undetermined, the changes within the new standard will effect multiple aspects of a business’s operations.

For instance, the addition of leases to the balance sheet is likely to impact commonly used financial indicators, such as debt covenants ratios, regulatory capital requirements, and other contracts (e.g. some management compensation plans may have performance based metrics, which may be impacted). Control over the use of the asset means that for a period of time the customer has both: • The right to obtain substantially all of the economic benefits from the use of the asset, and • The right to direct the use of the asset. The assessment of whether a company has the right to direct the use of the asset requires judgement. However, a company would have the right to direct the use of the asset in either of the following situations: Implications for Key Metrics and Debt Covenants The new lease standard could have a significant impact on the key metrics companies report to their investors as well as on a company’s debt covenant computations.

Below are a some of the key ratios that may be impacted by the new lease accounting standard. Key Metric Expected Effect Leverage Ratio: Debt/Equity Increases Current Ratio: Current Assets/Current Liabilities Decreases Debt to EBITDA: Debt/EBITDA Increases Return on Assets: Net Income/Assets • The customer has the right to operate the asset throughout the period of use, without the supplier having the right to change the operating instructions. Decreases Assurance | Tax | Advisory | dhgllp.com • The customer designed the asset in a way that predetermines how, and for what purpose, the asset will be used throughout the period of use. If a supplier has substantive substitution rights (i.e., the right to substitute the identified asset for another asset) then the customer does not have the right to use an identified asset. For substitution rights to be considered substantive, both of the following must be true: • The supplier has the practical ability to substitute alternative assets throughout the period of use, 2 . views The identification of a lease in a contract, in most cases, will decide whether or not leases are recognized on the balance sheet. This decision caries similar weight to the determination of whether a lease was a capital lease or an operating lease under the existing standard. In determining whether it is ‘reasonably certain’ that a renewal option (or termination option) will be exercised, a company must consider all relevant factors that create an economic incentive for the lessee to exercise the option, including contract, asset, entity, and market based factors. Examples of these factors include: • The economic benefits for the supplier to substitute the asset are expected to exceed the costs of substitution. The consideration of whether or not substitution rights are substantive should occur at inception of the contract. Further, future events, not deemed likely to occur, are to be excluded from the evaluation of whether or not substitution rights are substantive.

ASC 842-10-15-11 includes specific examples of future events that would be excluded. • Contractual terms and conditions for optional periods compared with current market rates. • Leasehold improvements that are expected to have significant value to the lessee when the option becomes exercisable. Short-term leases and lease term As an exception to the general requirement that all leases be recognized on balance sheet, the new lease standard allows companies to account for leases whose lease term is 12 months or less off the balance sheet – similar to operating leases under existing accounting guidance. However, if a company elects an accounting policy to apply this short-term lease exception, it must do so for all similar qualifying leases within the same asset class (e.g., all qualifying short-term laptop leases). • Costs related to the termination of the lease and the signing of a new lease, such as negotiation costs and relocation costs. • The importance of the underlying asset to the lessee’s operations. Under existing accounting guidance, companies only consider renewal periods as part of the lease term if it is reasonably assured the renewal option will be exercised. While the new standard uses the term “reasonably certain”, the standard explains that “the [FASB] views reasonably certain and reasonably assured as synonyms that should be applied in the same way.” Under the new standard, lease term is defined as: The non-cancellable period for which a lessee has the right to use an underlying asset, together with all of the following: a. Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option; b. Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option; and c. Periods representing renewals or extensions of the lease at the option of the lessor. Refer to Appendix B-1, Example – Lease term, for an explanation of how a company could determine if a lease contract qualifies for the short-term lease scope exception. Assurance | Tax | Advisory | dhgllp.com 3 .

views Lease components • The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. It is common for many lease contracts to contain both lease and non-lease components. For example, a contract containing the lease of specialized equipment, may also include provisions for maintenance services to be provided by the lessor. These maintenance services would be considered non-lease components and would be separated from the lease components under the existing standards. Similarly, the new standard requires separation of the lease and nonlease components.

The new standard also contains additional guidance on the identification of non-lease components, as this determination is more significant given that lease components of a contract will now be accounted for on the balance sheet. • The lease term is for the major part of the remaining economic life of the underlying asset. However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for the purposes of classifying the lease. • The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. • The underlying asset is of such specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. In general, contract consideration and any initial direct costs should be allocated to lease and non-lease components based on the relative standalone price of the separate components. However, the new standard allows lessees, as a practical expedient, to make an accounting policy election to account for lease and non-lease components as a single lease component.

This accounting policy election should be made by class of underlying assets – similar to the short term lease exception. Although the finance lease classification criteria is substantially the same as the pre-existing capital lease criteria, the new standard adds the criterion that a lease of specialized assets for which there is no alternative use at the end of the lease term would qualify as a finance lease. This criterion was added to reflect the economic reality that if an asset has no alternative use at the end of a lease, then the lessee has substantially used all of the benefits of that asset. Related party leases Related party leases are to be accounted for and classified under the new standard on the basis of the legally enforceable terms and conditions of the lease. Further, in the separate financial statements of related parties, the accounting and classification of leases should be the same as for leases between unrelated parties.

This differs from current guidance, which requires related party leases to be accounted for and classified on the basis of the economic substance of the arrangement. The guidance in the new standard may remove some of the current challenges encountered when there are no legally enforceable terms and conditions (e.g. month to month related party leases, or related party leases with undefined payment terms). Any leases not meeting the criteria for a finance lease shall be classified as an operating lease. The new classification criteria are substantially the same as the existing operating vs.

capital lease classification criteria with the addition of the specialized assets criterion listed above. And while the new criteria do not reference the “brightline” tests included in existing guidance (i.e., the “75%” and “90%” hurdles), the new lease standard allows companies to use those existing “bright lines” as one reasonable approach for assessing the criteria listed above. Consequently, companies should not experience significant changes in lease classification conclusions under the new standard. Lessee accounting Classification Leases are required to be classified by lessees as either operating leases or finance leases.

A lease contract is a finance lease for a lessee if any of the following are met: • The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. Assurance | Tax | Advisory | dhgllp.com 4 . views Private Company Matters Private companies, those companies that do not meet the FASB definition of a Public Business Entity, are permitted to make an accounting policy election for all leases to use a risk-free discount rate when calculating the lease liability. The risk-free rate used for any particular lease should be determined using a period that is comparable with the lease term. This option may make the additional calculations under the standard easier to implement for some private companies. However, since the risk free rate is most often lower than applicable borrowing rates, this option is likely to result in a larger liability. Initial measurement The new standard requires lessees to recognize on the balance sheet at commencement for all leases both: If a lessee cannot readily determine the rate implicit in the lease, it should use its incremental borrowing rate to discount the lease.

In addition, private companies4 will have the option to use the risk-free rate in calculating the present value of lease payments. • A ROU asset, representing the lessee’s right to use the leased asset over the term of the lease; and, • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. As illustrated below, the ROU asset is initially recorded at an amount equal to: The lease liability is initially recorded at an amount equal to the present value of the remaining lease payments3 due over the lease term, discounted at the rate implicit in the lease. • The initial lease liability; plus The rate implicit in the lease is the rate that causes the present value of the net investment in the lease to equal the sum of: • Any initial direct costs incurred by the lessee; less • Any lease payments made at or before lease commencement; plus • Any lease incentives received from the lessor. • The fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor, and • Any capitalized initial direct costs incurred by the lessor. The following illustrates the initial balance sheet measurement concepts under the new lease accounting standard. = Initial Lease Liability Initial ROU Asset = Assurance | Tax | Advisory | dhgllp.com Initial Lease Liability + Present value of lease payments due over the lease term • Lease payments made at or before lease commencement • Initial direct costs 5 - Lease incentives received from the lessor . views Subsequent measurement – finance leases The initial liability for a finance lease will subsequently be adjusted to reflect interest expense incurred (increase of the liability), and lease payments made (decrease of the liability). Interest should be recognized equal to an amount that produces a constant periodic discount rate on the remaining balance of the liability during the lease term (i.e. the effective interest method). commencement of the lease to the end of the useful life of the ROU asset. The income and cash flow statement impact of accounting for finance leases is similar to current requirements for accounting for capital leases. Companies will recognize interest expense (from the lease liability) and amortization expense (from the ROU asset) separately in the income statement, which is similar to the presentation for today’s capital leases. On the statement of cash flows, interest paid will be presented as a component of operating activities, and principal payments on the lease liability will be presented as component of financing activities. The ROU asset should be amortized on a straight-line basis5 from the commencement date6 to the earlier of the end of the useful life of the ROU asset or the end of the lease term. If, however, ownership of the ROU asset is transferred to the lessee at the end of the lease term or it is reasonably certain the lessee will exercise a purchase option for the ROU asset, then the lessee should amortize the ROU asset from Leasehold Improvements Similar to an ROU asset for a finance lease, leasehold improvements should be amortized over the shorter of the useful life of the leasehold improvements and the remaining lease term, unless the lease transfers ownership of the underlying ROU asset to the lessee or it is reasonably certain the lease will exercise a purchase option of the underlying ROU asset. Subsequent measurement – operating leases A lease liability for an operating lease will generally be measured at the present value of the lease payments not yet paid, calculated using the discount rate determined at commencement of the lease. As illustrated in the graphic below, the income and cash flow statement impact of accounting for operating leases is unchanged from current U.S.

GAAP. Companies will recognize a single lease expense figure in the income statement, and cash paid on operating leases will be presented as a component of operating activities on the statement of cash flows. As mentioned, ROU assets associated with financing leases are treated the same as any other nonfinancial asset. They are measured at cost, net of accumulated amortization, and are systematically amortized.

ROU assets related to operating leases, however, are treated differently. Lessee reporting Finance lease ROU assets for operating leases are measured by reference to the lease liability. The ROU asset for an operating lease will generally be measured at an amount equal to the lease liability, adjusted for the following: Income Statement • Prepaid or accrued lease payments (the lessee should generally recognize lease expense over the lease term on a straight-line basis), • The remaining balance of any lease incentives received, Statement of Cash Flows • Unamortized initial direct costs • Impairment of the asset. Assurance | Tax | Advisory | dhgllp.com 6 • Interest expense (Lease liability) • Depreciation expense (ROU asset) • Interest expense – operating activities • Principal payment – financing activities Operating lease • Total lease expense • Total lease expense – operating activities . views There will be a number of different approaches to implement and account for leases under the new standard. The selection of policies and procedures to account for adopting the standard will require consideration of internal controls and other financial reporting requirements Appendix B-2, Example lessee accounting, demonstrates multiple ways in which a company would record a lease for both a finance and operating lease. These lease accounting examples include both a comprehensive methodology and a high-level “display approach”, which would likely be more appropriate for private companies with relatively few leases. Impairment • If a lease does not meet the criteria of a sales-type lease, a lessor would classify the lease as a direct financing lease if both 1) the present value of the sum of the lease payments and any residual value guaranteed by the lessee exceeds the fair value of the underlying asset, and 2) it is probable the lessor will collect the lease payment plus any amount necessary to satisfy a residual value guarantee. The ROU asset for both finance and operating leases is subject to the same impairment considerations as is required of other long-lived assets.7 If a ROU asset is impaired, the asset will be measured at its carrying amount immediately after the impairment less any accumulated amortization. ROU assets relating to finance leases should continue to be amortized on a straight-line basis, as described above, from the date of impairment to the earlier of the end of the useful life of the ROU asset or the end of the lease term. If impairment of an ROU asset associated with an operating lease is recorded, then subsequent to impairment the single lease cost will be calculated as the sum of the following: • Leases that do not meet the definition of either a salestype lease or a direct financing lease are operating leases. • The new lease classification criteria remove the incremental tests that now exist for leases involving real estate to achieve better alignment with the new revenue recognition standard. • Amortization of the remaining right-of-use asset after the impairment on a straight-line basis, and • The accounting model for leveraged leases in current U.S. GAAP was not retained for leases that commence after the effective date of the new standard. • Accretion of the lease liability, determined for each remaining period during the lease term as the amount that produces a constant periodic discount rate on the remaining balance of the liability. Sale-leaseback transactions While the new lease standard retains the notion of a saleleaseback transaction, it modifies how the lessee and lessor determine the appropriate accounting for such a transaction. Lessor accounting Lessor accounting is largely unchanged from current U.S. GAAP. A majority of operating leases should remain classified as operating leases, and lessors should continue to recognize income, generally, on a straight-line basis over the lease term. The changes made to the lessor accounting model within the new lease standard were primarily related to aligning the lessor guidance with the revised lessee guidance and with the new revenue standard, FASB ASC 606, Revenue from Contracts with Customers.

Key aspects of the lessor guidance include the following: Under the new standard, the seller-lessee first assesses whether the transfer of the underlying asset to the buyerlessor qualifies as a sale under the new revenue standard. This analysis focuses on whether the buyer-lessor has obtained control over the asset. The new lease standard clarifies that the leaseback arrangement does not preclude the buyer-lessor from obtaining control (thus accounting as a sale) unless the lease is determined to be a finance lease. If the transfer does not qualify as a sale, the transaction is accounted for as a financing arrangement. The seller-lessee continues to record the underlying asset on its balance sheet and recognizes a liability for any proceeds received from the buyer-lessor. • Retains the current lease classifications – operating leases, direct-finance leases and sales-type leases – and generally how each lease type is accounted for. • The standard does change how a lessor determines the appropriate lease classification for each lease to better align the lessor guidance with the revised lessee classification guidance noted above. In contrast, if the transfer qualifies as a sale, then the sellerlessee derecognizes the underlying asset and recognizes a gain or loss on sale.

The leaseback would be accounted in accordance with the new lease standard as an operating lease. (i.e. accounted for as an operating lease by the lessee). • A sales-type lease is subject to the same classification criteria as a finance lease in the lessee model. Assurance | Tax | Advisory | dhgllp.com 7 .

views Presentation and disclosure The new lease standard includes expanded presentation and disclosure requirements to provide additional quantitative and qualitative information, including significant judgments involved in the accounting for leases and the amounts recognized in the financial statements from leases. The objective of the disclosures is to enable users of the financial statements to assess the amount, timing and uncertainty of cash flows arising from leases. Among these requirements, companies will present separately financing ROU assets and liabilities from operating ROU assets and liabilities. Certain other disclosures required under the new lease standard include: Disclosure requirements Lessor Lessee • Information about the nature of its leases • Information about the nature of its leases • Maturity analysis of lease liabilities • Maturity analysis of lease investments • Lease expense, split between operating and capital leases • Profit or loss recognized at lease commencement (for sales-type leases) • Short-term lease expense • Lease income • Variable lease expense • Qualitative and quantitative information about significant changes in residual values of leased assets • Sublease income • Weighted average remaining lease term • Weighted average discount rate Scope, effective dates, and transition Scope Effective dates ASU 2016-02 applies to all leases, including subleases, with the following exceptions: The effective date for public companies8 is fiscal years beginning after December 15, 2018, and interim periods therein.

For all other companies the standard is effective for fiscal years beginning after December 15, 2019 and interim periods within those fiscal years beginning after December 15, 2020. Early adoption is permitted for all companies and organizations. • Leases of intangible assets, • Leases to explore or use minerals, oil, natural gas, and similar nonregenerative resources, • Leases of biological assets, including timber, • Leases of inventory, and • Leases of assets under construction. Companies need to start now to assess the capabilities of their financial reporting systems and controls, as they relate to the adoption of this new standard. The new lease standard requires a modified retrospective implementation approach, which means when companies adopt they will need to apply the new lease guidance to each comparable period presented.

For instance, a public company who adopts for the 2019 calendar year-end and reports three years of comparable information will need to evaluate how the standard will impact the presentation of the 2017 and 2018 calendar year-end financial statements. Assurance | Tax | Advisory | dhgllp.com 8 . views Transition The first three practical expedients must be elected together (i.e., all or none). In contrast, the fourth practical expedient may be elected separately; however, if elected, it must be treated as an accounting policy election (i.e., it cannot be elected on a lease-by-lease basis). Further, the policy election for the short-term lease exemption would also apply to comparable periods presented upon adoption. For companies that avail themselves of the practical expedients, the primary effect of adoption will be the grossing up of the balance sheet for any existing operating leases. ASU 2016-02 requires companies to adopt its provisions using a modified retrospective approach, which requires the application of the new standard as of the beginning of the earliest comparative period presented.

This requirement is irrespective of whether or not a company elects to early adopt the standard. Therefore, whenever a company adopts the new standard, it will be required to consider the impact of the new standard for all comparable periods presented in the financial statements issued during the year of adoption. Upon adoption, a lessee will be required to recognize a ROU asset and a lease liability for operating leases at the later of the beginning of the earliest period presented on the balance sheet and the commencement date of the lease. Further, the lessee will measure the lease liability at present value using a discount rate established at the later of the beginning of the earliest period presented and the lease commencement date.

For instance, consider the case of a calendar year-end reporting company who presents three comparable periods and adopts the standard in 2019. This company would need to present an ROU asset and a lease liability as of the later of beginning of 2017, or the lease commencement date for leases that had not commenced as of the beginning of 2017. The lease liability for each lease will be calculated using the discount rate in effect as of the beginning of 2017, or the lease commencement date for leases that had not commenced as of the beginning of 2017. The new standard also provides certain “practical expedients” that companies may elect at the date of transition to ease the burden of adoption. The practical expedients are as follows: 1. A company need not reassess whether any expired or existing contracts are or contain leases. 2. A company need not reassess the lease classification for any expired or existing leases (i.e., all existing leases that were classified as operating leases in accordance with Topic 840 will be classified as operating leases and all existing leases that were classified as capital leases in accordance with Topic 840 will be classified as finance leases). 3. A company need not reassess initial direct costs for any existing leases. 4. A company also may elect a practical expedient to use hindsight in determining the lease term when considering lessee options to extend or terminate the lease and to purchase the underlying asset. 1. ASU 2016-02 applies to all entities that enter into a lease, with some specified scope exceptions.

Throughout this document the term “company” is used to refer to the entity entering into a lease. This term “company” is used as a general term to aid in the readability of the document. As such, the guidance is equally as applicable to not-for-profit organizations and other entities that enter into a lease. For the purpose of this transition guidance the following are included in the definition of a public company: a public business entity, a not-for-profit entity that has issued or is a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market, and an employee benefit plan that files or furnishes financial statements with or to the U.S.

Securities and Exchange Commission. 2. Rapoport, Michael (2015, November 10) Coming to Balance Sheet Near You: $2 Trillion in Leases. The Wall Street Journal. Retrieved from http://www.wsj.com. 3. Lease payments exclude contingent rental payments (e.g., rent based on percent of sales). 4. Entities that are not public business entities. 5. Under the new lease standard the straight-line basis is used “unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived from the right to use the underlying asset” (ASC 842-20-35-7). 6. The date on which a lessor makes an underlying asset available for use by an lessee. 7. Refer to ASC 360-10-35 for additional information on the impairment guidance for long-lived assets. 8. For the purpose of this transition guidance the following are included in the definition of a public company: a public business entity, a not-for-profit entity that has issued or is a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market, and an employee benefit plan that files or furnishes financial statements with or to the U.S.

Securities and Exchange Commission. Assurance | Tax | Advisory | dhgllp.com 9 . views Appendix A – Identifying a Lease The following illustration, excerpted from ASC 842-10-55-1, Leases - Implementation Guidance, demonstrates the determination of whether or not a contract is or contains a lease. Is there an identified asset? No Yes Does the customer have the right to obtain substantially all of the economic benefits from the use of the asset throughout the period of use? No Yes Customer Does the customer or the supplier have the right to direct how and for what purpose the identified asset is used throughout the period of use? Supplier Neither; how and for what purpose the asset will be used is predetermined. Yes Does the customer have the right to operate the asset throughout the period of use, without the supplier having the right to change those operating instructions? No Yes Does the customer design the asset (or specific aspects of the asset) in a way that predetermines how and for what purpose the asset will be used throughout the period of use? The contract contains a lease. Assurance | Tax | Advisory | dhgllp.com No The contract does not contain a lease. 10 . views Appendix B – Examples B-1 – Lease terms – short-term determination Conclusion: Facts: Based on a review of the relevant factors that create an economic incentive (e.g., the significant leasehold improvements involved, the material tax incentive being offered), Darling Widgets concludes it is reasonably certain that it will exercise the renewal option. As a result, the lease does not qualify as a short-term lease (because the lease term exceeds 12 months). • Darling Widgets enters into a lease agreement with RE Rental Inc. to lease a building for an initial period of 10 months. • At the end of 10 months, Darling Widgets has the option to renew the lease contract for an additional 36-month period. • Darling Widgets intends to use the building for the location of its new corporate headquarters, which requires the installation of significant leasehold improvements. • Additionally, Darling Widgets has been offered a material tax incentive from the local government for relocating its headquarters. However, to receive the tax incentive, Darling must remain in the locality for at least two years. Darling intends to meet that requirement. B-2 – Lessee accounting The following example walks through the initial and subsequent accounting treatment of the same lease for both the operating and finance lease classifications.

The purpose of this example is to illustrate how the same basic lease terms would look under the recognition guidance for each classification. Accounting at inception of the lease: Facts: • Beau’s makes the first $50,000 payment and incurs the $15,000 in initial direct costs. • Beau’s Baseball Cards (Beau’s) enters into a lease agreement with RE Rental Inc. to lease a printing press for 10 years, with an option to extend for an additional 5 years. • The lease liability is measured as the present value of the remaining 9 payments, discounted at 5.87%, which is calculated to be $342,017. • Lease payments are $50,000 per year during the initial term and $55,000 per year during the optional period. Payments are made at the beginning of each year. • The ROU asset is measured at $407,017, which is equal to the lease liability of $342,017 plus the first lease payment of $50,000 and the $15,000 in initial direct costs. • Beau’s incurs $15,000 in initial direct costs. • At inception Beau’s concludes it is NOT reasonably certain the option to extend the lease will be exercised. The 10% increase in cost is not considered to be a significant economic incentive to extend.

Therefore the lease term is 10 years. Journal entry at inception Debit ROU asset Lease liability $407,017 $342,017 Cash (lease payment) 11 $50,000 Cash (initial direct costs) • Beau’s incremental borrowing rate is 5.87%. (Beau’s was unable to determine the rate implicit in the lease.) Assurance | Tax | Advisory | dhgllp.com Credit $15,000 . views Finance lease – subsequent accounting in year one: Finance lease – year one • For the purpose of this illustration the lease is deemed to be a finance lease because the lease term accounts for substantially all of the useful life of the asset. Debit Amortization expense $40,702 Interest expense • Beau’s amortizes the ROU asset on a straight-line basis over 10 years. Thus, Beau’s will recognize amortization expense of $40,702. Credit $20,076 ROU asset $40,702 Lease liability $20,076 Balance Sheet • Beau’s recognizes interest expense of $20,076, which is equal to the lease liability x the discount rate of 5.87%. ROU asset $366,315 Lease liability $362,093 (342,017+20,076) (407,017-40,702) Operating lease – year one Operating lease – subsequent accounting in year one: Debit • For the purpose of this illustration the lease is deemed to be an operating lease because the useful life of the asset is substantially greater than the term of the lease. Lease expense Credit $51,500 Lease liability $20,076 ROU asset • Beau’s recognizes lease expense of $51,500, which is equal 1/10th of the total cash payments to be made during the lease term ($50,000) plus 1/10th of the initial direct costs ($1,500). $31,424 Balance Sheet ROU asset Lease liability • The portion of the lease expense attributable to interest expense ($20,076 as calculated in the finance lease example above) is credited to the lease liability, and the remaining expense amount is credited against the ROU asset. $375,593 $362,093 (342,017+20,076) (407,017-31,424) Note the difference in the value of the ROU asset at the end of year one in the finance lease example versus the operating lease example. Under the finance lease scenario, the ROU asset is amortized evenly over the 10 year lease period. However, under the operating lease scenario, the ROU asset is measured at the end of each year based on the value of the lease liability plus the remaining initial direct costs ($362,093 + $13,500). Assurance | Tax | Advisory | dhgllp.com 12 .