Getting to the Bottom of the Top Line - Preparing to Adopt the New Revenue Recognition Standard – March 2016-04-11

Dixon Hughes Goodman

Description

views

March 2016

Getting to the Bottom of the Top Line

Action items for adopting the new revenue recognition standard

Risk Advisory Services

Introduction

On May 28, 2014, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2014-09,

Revenue from Contracts with Customers, a new accounting standard that will govern revenue recognition beginning Jan.

1, 2018 for public companies and Jan. 1, 2019 for private companies.1 The new standard will supersede substantially all

existing revenue guidance.

Many companies – both public and non-public – may have

to change the way they recognize revenue under the new

revenue standard. Based on the specifics of the company

and the industry, the changes could be quite dramatic. Such

changes may impact not only the way companies recognize

revenue but also a company’s processes – e.g., financial,

operational, IT, and business as a whole.

This paper highlights six practical actions companies need

to take to adopt the new revenue standard as well as areas

outside of accounting and finance that might be impacted.

Assurance | Tax | Advisory | dhgllp.com

Brief Overview of New Revenue Standard

The new revenue standard replaces existing revenue

guidance – including virtually all industry-specific guidance

– with an overarching revenue framework.

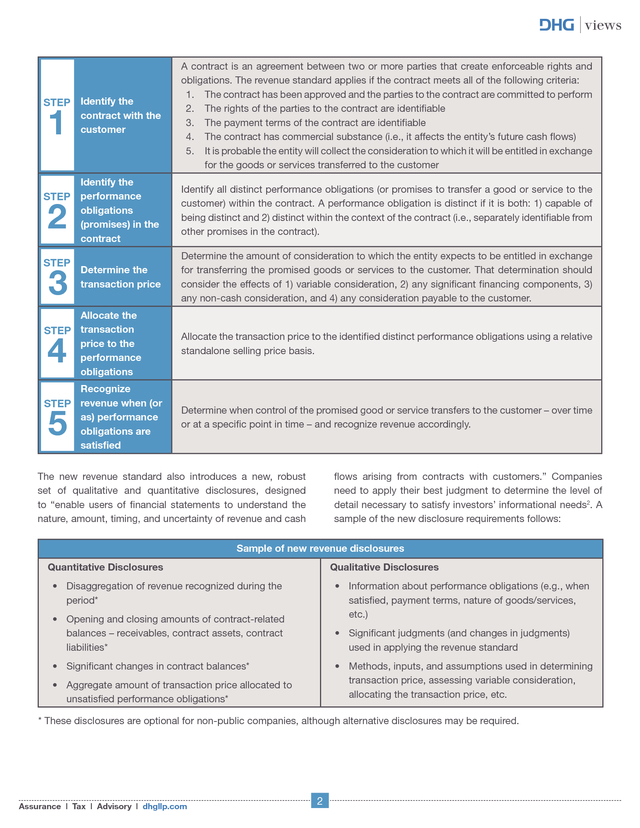

The core principle of this framework is that companies “should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.” To achieve that principle, a company needs to follow five steps: . views STEP Identify the 1 contract with the customer Identify the STEP performance 2 STEP 3 obligations (promises) in the contract Determine the transaction price A contract is an agreement between two or more parties that create enforceable rights and obligations. The revenue standard applies if the contract meets all of the following criteria: 1. The contract has been approved and the parties to the contract are committed to perform 2. The rights of the parties to the contract are identifiable 3. The payment terms of the contract are identifiable 4. The contract has commercial substance (i.e., it affects the entity’s future cash flows) 5. It is probable the entity will collect the consideration to which it will be entitled in exchange for the goods or services transferred to the customer Identify all distinct performance obligations (or promises to transfer a good or service to the customer) within the contract. A performance obligation is distinct if it is both: 1) capable of being distinct and 2) distinct within the context of the contract (i.e., separately identifiable from other promises in the contract). Determine the amount of consideration to which the entity expects to be entitled in exchange for transferring the promised goods or services to the customer. That determination should consider the effects of 1) variable consideration, 2) any significant financing components, 3) any non-cash consideration, and 4) any consideration payable to the customer. Allocate the STEP transaction 4 price to the performance obligations Recognize STEP revenue when (or as) performance obligations are satisfied 5 Allocate the transaction price to the identified distinct performance obligations using a relative standalone selling price basis. Determine when control of the promised good or service transfers to the customer – over time or at a specific point in time – and recognize revenue accordingly. The new revenue standard also introduces a new, robust set of qualitative and quantitative disclosures, designed to “enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.” Companies need to apply their best judgment to determine the level of detail necessary to satisfy investors’ informational needs2.

A sample of the new disclosure requirements follows: Sample of new revenue disclosures Quantitative Disclosures Qualitative Disclosures • Disaggregation of revenue recognized during the period* • Information about performance obligations (e.g., when satisfied, payment terms, nature of goods/services, etc.) • Opening and closing amounts of contract-related balances – receivables, contract assets, contract liabilities* • Significant judgments (and changes in judgments) used in applying the revenue standard • Significant changes in contract balances* • Methods, inputs, and assumptions used in determining transaction price, assessing variable consideration, allocating the transaction price, etc. • Aggregate amount of transaction price allocated to unsatisfied performance obligations* * These disclosures are optional for non-public companies, although alternative disclosures may be required. Assurance | Tax | Advisory | dhgllp.com 2 . views Practical Actions to Prepare Action Item 1 Educate and Inform Action Item 3 Determine the Transition Methodology The first action a company should take in preparing to adopt the new revenue standard is to educate itself about the new standard and how the standard differs from the company’s existing revenue recognition practices. This can take the form of education sessions for key stakeholders, in addition to the board of directors and audit committee, and deep-dive sessions for business lines. Such sessions should also be used to solicit initial feedback from key stakeholders about how the accounting change may impact existing reporting processes and controls, systems, and business practices. The new revenue standard allows companies to select one of two ways to adopt the standard’s provisions. The transition methodology a company selects will affect the population of contracts to which the new revenue standard applies. Therefore, companies should determine early in the process which of the following two adoption approaches they intend to use: Fully Retrospective Adoption – Under this approach, a company must restate all presented prior period financial statements to conform to the new revenue standard. However, to ease the operational burden of fully retrospective adoption, ASU 2014-09 offers certain practical expedients a company may elect.

These expedients include: The education process should include all of a company’s key stakeholders, including representation from the following areas: • • • • Accounting Policy Tax Technology Internal Audit • • • • Controllership Finance and Treasury Legal Business Operations 1. For completed contracts, an entity: a. Need not restate contracts that begin and end within the same annual reporting period, and b. May use the transaction price at the date the contract was completed rather than estimating variable consideration amounts (if any) in the comparative reporting periods. Action Item 2 Create an Inventory of Your Revenue Streams If one is not already in place, a company should create an inventory of all of its existing revenue streams. Companies will want to ensure this inventory includes any newly created revenue streams and all other types of non-revenue transactions that fall within the scope of the new revenue standard, including “other income” items such as sales of non-financial assets (e.g., PP&E). 2. For all reporting periods presented before the date of initial application, an entity need not disclose the amount of the transaction price allocated to the remaining performance obligations and an explanation of when the entity expects to recognize that amount as revenue. Modified Retrospective Adoption – Under this approach, a company records a cumulative effect adjustment to the opening balance sheet of the period in which the new revenue standard is first applied. Comparative prior year periods are not adjusted.

In determining the cumulative effect adjustment, a company would only apply the new revenue guidance to those contracts that are not completed at the time of initial adoption. However, companies electing this approach must disclose “the amount by which each financial statement line item is affected in the current reporting period by the application of the [new standard] as compared with the guidance that was in effect before the change,” and, “an explanation of the reasons for [the significant differences]” A good starting point for this exercise is to review the company’s general ledger and detailed chart of accounts. Also consider surveying appropriate stakeholders from each business line to ensure the inventory contains not only all revenue streams from the prior year but also any new or future revenue streams. The inventory should include, at a minimum, the following information about each revenue and “other income” streams: • A description of the revenue stream, including the nature of the goods and services provided, significant payment terms, and when the company’s obligation is generally satisfied (e.g., upon shipment, upon delivery, etc.). • General ledger account coding or how the stream maps into the general ledger. • The dollar amount of the revenue stream for the last fiscal year. Assurance | Tax | Advisory | dhgllp.com 3 Both adoption approaches have advantages and drawbacks. Fully retrospective adoption preserves helpful trend information for investors and other key stakeholders. Though, it could require a significant effort to restate prior period financials.

The modified retrospective adoption approach does not require restatement of prior period information, but would require a company to keep two sets of records in the first year of adoption to satisfy the accompanying disclosure requirements. . views Action Item 4 Perform Preliminary Scoping and Discovery Action Item 6 Analyze Contracts Under the New Revenue Standard To ease the burden of adopting the new revenue standard, companies should perform a preliminary scoping and discovery exercise. The purpose of this exercise is to: While the accounting treatment conclusions may not change for all revenue transactions, companies will need to have sufficient documentation supporting conclusions reached under the new revenue standard for all in-scope transactions. The documentation should clearly explain how the company walked through and applied each of the five steps of the new revenue framework to each transaction (or group of transactions). Key to this step is ensuring consistency across the conclusions reached, especially if a company has multiple business lines. a. Identify all open contracts for the revenue and “other income” streams included in the inventory listing (see “Create an Inventory of Your Revenue Streams” above). b. Group contracts with similar characteristics – e.g., type of performance obligation, timing of transfer of control, etc. – in order to eliminate the need for multiple accounting analyses. Companies should also prepare a summary document that identifies and describes all key accounting changes resulting from the adoption of the new revenue standard and the underlying cause for such changes. For example, this document should, at a minimum, capture all key changes related to: c. Identify immaterial revenue streams and determine whether the new revenue standard will be applied to such items. d. Gather documentation for all in-scope contracts and transactions. • The number of performance obligations arising from each transaction. e. Identify any information gaps and systems limitations and determine how to address such items. • The amount of revenue allocated to each performance obligation (e.g., due to application of the constraint on variable consideration). When performed correctly, this exercise could eliminate inefficiencies in the adoption process and assist companies in discovering (and potentially addressing) data and system shortfalls early in the implementation process, mitigating against potential delays down the road. • The timing of revenue recognition. • The accounting for costs arising from the revenue transaction (e.g., costs to fulfill performance obligations). Action Item 5 Create a Financial Disclosures Roadmap This document will serve as a roadmap to help key stakeholders – particularly the company’s board of directors, audit committee, and external auditors – understand how the new revenue standard has impacted a company’s reported results. Also early in the adoption process, companies should prepare a draft template of all the new disclosures required by the revenue standard.

Companies will need to apply their best judgment to determine the appropriate level of information to provide users and how such information should be presented. Consideration should first be given to the informational needs of investors; industry practice might also be considered. Don’t Forget…Beyond Accounting Because evaluations of accounting changes are typically sponsored and performed by the accounting and finance departments, companies may be tempted to primarily focus on how the new standard changes accounting processes. However, companies should look beyond the pure accounting elements and consider how the change could impact other parts of the business, such as non-financial processes, technology and personnel. The draft disclosures can then be used as a roadmap for identifying which data elements the company needs to capture from its revenue contracts and how to best capture that information. For example, with an understanding of which data elements are needed, a company might consider using the accounting analysis exercise (see “Analyze Contracts Under the New Revenue Standard” below) as a means for extracting the necessary information from the inscope contracts. Assurance | Tax | Advisory | dhgllp.com 4 . views Specific areas to consider include: technology. For example, consider whether any key billing system processes may be impacted by the new revenue recognition standard. • Marketing and Sales Operations – While this may not initially be a core accounting change, the new standard may impact processes for sales and/or service contracts to customers. • Geographic Impacts – Consider whether the standard will impact foreign and remote operations. • Key Legal Agreements – Legal agreements between companies might have sales terms embedded. • People – Consider which financial and non-financial employees will need to be involved in managing and implementing the change. How will non-financial employees be impacted? • Debt Covenants – Standard debt covenant calculations that are generated from revenue related data could be impacted. • External Auditors – Communicate with the external auditor, as appropriate, about the expected impact of transitioning to the new standard. • Tax – There are several instances in which the new revenue recognition standard for financial accounting purposes may impact a company’s tax reporting and the financial reporting for taxes. Conclusion The new revenue standard has the potential to significantly impact a company’s reported results, accounting processes and controls, and even general business operations. While the magnitude of the impact will vary across industries, companies should begin the implementation process now to ensure a smoother transition. • Key Financial and Operational Controls – How will changes to revenue processes impact key financial, operational and technology related controls? • Technology – There will likely be changes to information technology and impacts to key controls around How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies think through how the new revenue standard will impact their reported results and accompanying disclosures, accounting processes and controls, and other areas of their business. Understand the guidance For further details about how our Accounting Readiness team can assist your company, please contact us at riskadvisory@dhgllp.com. Assess the impact Get the accounting right • Provide CPE-eligible trainings for a company’s key stakeholders • Help inventory key revenue streams and related processes and controls • Perform accounting analyses on different revenue streams • Provide DHG thoughtware on forthcoming accounting changes • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) • Design and implement new accounting processes and controls • Draft new revenue disclosures and accounting policies 1. The formal effective date for public companies is annual reporting periods beginning after December 15, 2018, including interim periods within that reporting period.

For private companies, the effective date is annual reporting periods beginning after December 15, 2018, and interim periods within annual reporting periods beginning after December 15, 2019. 2. Refer to ASC 606-10-50-1. Assurance | Tax | Advisory | dhgllp.com 5 .

The core principle of this framework is that companies “should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.” To achieve that principle, a company needs to follow five steps: . views STEP Identify the 1 contract with the customer Identify the STEP performance 2 STEP 3 obligations (promises) in the contract Determine the transaction price A contract is an agreement between two or more parties that create enforceable rights and obligations. The revenue standard applies if the contract meets all of the following criteria: 1. The contract has been approved and the parties to the contract are committed to perform 2. The rights of the parties to the contract are identifiable 3. The payment terms of the contract are identifiable 4. The contract has commercial substance (i.e., it affects the entity’s future cash flows) 5. It is probable the entity will collect the consideration to which it will be entitled in exchange for the goods or services transferred to the customer Identify all distinct performance obligations (or promises to transfer a good or service to the customer) within the contract. A performance obligation is distinct if it is both: 1) capable of being distinct and 2) distinct within the context of the contract (i.e., separately identifiable from other promises in the contract). Determine the amount of consideration to which the entity expects to be entitled in exchange for transferring the promised goods or services to the customer. That determination should consider the effects of 1) variable consideration, 2) any significant financing components, 3) any non-cash consideration, and 4) any consideration payable to the customer. Allocate the STEP transaction 4 price to the performance obligations Recognize STEP revenue when (or as) performance obligations are satisfied 5 Allocate the transaction price to the identified distinct performance obligations using a relative standalone selling price basis. Determine when control of the promised good or service transfers to the customer – over time or at a specific point in time – and recognize revenue accordingly. The new revenue standard also introduces a new, robust set of qualitative and quantitative disclosures, designed to “enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.” Companies need to apply their best judgment to determine the level of detail necessary to satisfy investors’ informational needs2.

A sample of the new disclosure requirements follows: Sample of new revenue disclosures Quantitative Disclosures Qualitative Disclosures • Disaggregation of revenue recognized during the period* • Information about performance obligations (e.g., when satisfied, payment terms, nature of goods/services, etc.) • Opening and closing amounts of contract-related balances – receivables, contract assets, contract liabilities* • Significant judgments (and changes in judgments) used in applying the revenue standard • Significant changes in contract balances* • Methods, inputs, and assumptions used in determining transaction price, assessing variable consideration, allocating the transaction price, etc. • Aggregate amount of transaction price allocated to unsatisfied performance obligations* * These disclosures are optional for non-public companies, although alternative disclosures may be required. Assurance | Tax | Advisory | dhgllp.com 2 . views Practical Actions to Prepare Action Item 1 Educate and Inform Action Item 3 Determine the Transition Methodology The first action a company should take in preparing to adopt the new revenue standard is to educate itself about the new standard and how the standard differs from the company’s existing revenue recognition practices. This can take the form of education sessions for key stakeholders, in addition to the board of directors and audit committee, and deep-dive sessions for business lines. Such sessions should also be used to solicit initial feedback from key stakeholders about how the accounting change may impact existing reporting processes and controls, systems, and business practices. The new revenue standard allows companies to select one of two ways to adopt the standard’s provisions. The transition methodology a company selects will affect the population of contracts to which the new revenue standard applies. Therefore, companies should determine early in the process which of the following two adoption approaches they intend to use: Fully Retrospective Adoption – Under this approach, a company must restate all presented prior period financial statements to conform to the new revenue standard. However, to ease the operational burden of fully retrospective adoption, ASU 2014-09 offers certain practical expedients a company may elect.

These expedients include: The education process should include all of a company’s key stakeholders, including representation from the following areas: • • • • Accounting Policy Tax Technology Internal Audit • • • • Controllership Finance and Treasury Legal Business Operations 1. For completed contracts, an entity: a. Need not restate contracts that begin and end within the same annual reporting period, and b. May use the transaction price at the date the contract was completed rather than estimating variable consideration amounts (if any) in the comparative reporting periods. Action Item 2 Create an Inventory of Your Revenue Streams If one is not already in place, a company should create an inventory of all of its existing revenue streams. Companies will want to ensure this inventory includes any newly created revenue streams and all other types of non-revenue transactions that fall within the scope of the new revenue standard, including “other income” items such as sales of non-financial assets (e.g., PP&E). 2. For all reporting periods presented before the date of initial application, an entity need not disclose the amount of the transaction price allocated to the remaining performance obligations and an explanation of when the entity expects to recognize that amount as revenue. Modified Retrospective Adoption – Under this approach, a company records a cumulative effect adjustment to the opening balance sheet of the period in which the new revenue standard is first applied. Comparative prior year periods are not adjusted.

In determining the cumulative effect adjustment, a company would only apply the new revenue guidance to those contracts that are not completed at the time of initial adoption. However, companies electing this approach must disclose “the amount by which each financial statement line item is affected in the current reporting period by the application of the [new standard] as compared with the guidance that was in effect before the change,” and, “an explanation of the reasons for [the significant differences]” A good starting point for this exercise is to review the company’s general ledger and detailed chart of accounts. Also consider surveying appropriate stakeholders from each business line to ensure the inventory contains not only all revenue streams from the prior year but also any new or future revenue streams. The inventory should include, at a minimum, the following information about each revenue and “other income” streams: • A description of the revenue stream, including the nature of the goods and services provided, significant payment terms, and when the company’s obligation is generally satisfied (e.g., upon shipment, upon delivery, etc.). • General ledger account coding or how the stream maps into the general ledger. • The dollar amount of the revenue stream for the last fiscal year. Assurance | Tax | Advisory | dhgllp.com 3 Both adoption approaches have advantages and drawbacks. Fully retrospective adoption preserves helpful trend information for investors and other key stakeholders. Though, it could require a significant effort to restate prior period financials.

The modified retrospective adoption approach does not require restatement of prior period information, but would require a company to keep two sets of records in the first year of adoption to satisfy the accompanying disclosure requirements. . views Action Item 4 Perform Preliminary Scoping and Discovery Action Item 6 Analyze Contracts Under the New Revenue Standard To ease the burden of adopting the new revenue standard, companies should perform a preliminary scoping and discovery exercise. The purpose of this exercise is to: While the accounting treatment conclusions may not change for all revenue transactions, companies will need to have sufficient documentation supporting conclusions reached under the new revenue standard for all in-scope transactions. The documentation should clearly explain how the company walked through and applied each of the five steps of the new revenue framework to each transaction (or group of transactions). Key to this step is ensuring consistency across the conclusions reached, especially if a company has multiple business lines. a. Identify all open contracts for the revenue and “other income” streams included in the inventory listing (see “Create an Inventory of Your Revenue Streams” above). b. Group contracts with similar characteristics – e.g., type of performance obligation, timing of transfer of control, etc. – in order to eliminate the need for multiple accounting analyses. Companies should also prepare a summary document that identifies and describes all key accounting changes resulting from the adoption of the new revenue standard and the underlying cause for such changes. For example, this document should, at a minimum, capture all key changes related to: c. Identify immaterial revenue streams and determine whether the new revenue standard will be applied to such items. d. Gather documentation for all in-scope contracts and transactions. • The number of performance obligations arising from each transaction. e. Identify any information gaps and systems limitations and determine how to address such items. • The amount of revenue allocated to each performance obligation (e.g., due to application of the constraint on variable consideration). When performed correctly, this exercise could eliminate inefficiencies in the adoption process and assist companies in discovering (and potentially addressing) data and system shortfalls early in the implementation process, mitigating against potential delays down the road. • The timing of revenue recognition. • The accounting for costs arising from the revenue transaction (e.g., costs to fulfill performance obligations). Action Item 5 Create a Financial Disclosures Roadmap This document will serve as a roadmap to help key stakeholders – particularly the company’s board of directors, audit committee, and external auditors – understand how the new revenue standard has impacted a company’s reported results. Also early in the adoption process, companies should prepare a draft template of all the new disclosures required by the revenue standard.

Companies will need to apply their best judgment to determine the appropriate level of information to provide users and how such information should be presented. Consideration should first be given to the informational needs of investors; industry practice might also be considered. Don’t Forget…Beyond Accounting Because evaluations of accounting changes are typically sponsored and performed by the accounting and finance departments, companies may be tempted to primarily focus on how the new standard changes accounting processes. However, companies should look beyond the pure accounting elements and consider how the change could impact other parts of the business, such as non-financial processes, technology and personnel. The draft disclosures can then be used as a roadmap for identifying which data elements the company needs to capture from its revenue contracts and how to best capture that information. For example, with an understanding of which data elements are needed, a company might consider using the accounting analysis exercise (see “Analyze Contracts Under the New Revenue Standard” below) as a means for extracting the necessary information from the inscope contracts. Assurance | Tax | Advisory | dhgllp.com 4 . views Specific areas to consider include: technology. For example, consider whether any key billing system processes may be impacted by the new revenue recognition standard. • Marketing and Sales Operations – While this may not initially be a core accounting change, the new standard may impact processes for sales and/or service contracts to customers. • Geographic Impacts – Consider whether the standard will impact foreign and remote operations. • Key Legal Agreements – Legal agreements between companies might have sales terms embedded. • People – Consider which financial and non-financial employees will need to be involved in managing and implementing the change. How will non-financial employees be impacted? • Debt Covenants – Standard debt covenant calculations that are generated from revenue related data could be impacted. • External Auditors – Communicate with the external auditor, as appropriate, about the expected impact of transitioning to the new standard. • Tax – There are several instances in which the new revenue recognition standard for financial accounting purposes may impact a company’s tax reporting and the financial reporting for taxes. Conclusion The new revenue standard has the potential to significantly impact a company’s reported results, accounting processes and controls, and even general business operations. While the magnitude of the impact will vary across industries, companies should begin the implementation process now to ensure a smoother transition. • Key Financial and Operational Controls – How will changes to revenue processes impact key financial, operational and technology related controls? • Technology – There will likely be changes to information technology and impacts to key controls around How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies think through how the new revenue standard will impact their reported results and accompanying disclosures, accounting processes and controls, and other areas of their business. Understand the guidance For further details about how our Accounting Readiness team can assist your company, please contact us at riskadvisory@dhgllp.com. Assess the impact Get the accounting right • Provide CPE-eligible trainings for a company’s key stakeholders • Help inventory key revenue streams and related processes and controls • Perform accounting analyses on different revenue streams • Provide DHG thoughtware on forthcoming accounting changes • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) • Design and implement new accounting processes and controls • Draft new revenue disclosures and accounting policies 1. The formal effective date for public companies is annual reporting periods beginning after December 15, 2018, including interim periods within that reporting period.

For private companies, the effective date is annual reporting periods beginning after December 15, 2018, and interim periods within annual reporting periods beginning after December 15, 2019. 2. Refer to ASC 606-10-50-1. Assurance | Tax | Advisory | dhgllp.com 5 .