First Quarter 2016 Accounting, Reporting and Auditing Developments – April 7, 2016

Dixon Hughes Goodman

Description

assurance

Q1

2016

Accounting, Reporting and Auditing Developments

April 7, 2016

Assurance | Tax | Advisory | dhgllp.com

. Accounting & Financial Reporting Matters...............................................................................................4

Financial Accounting Standards Board (FASB)........................................................................................4

Accounting Standards Updates (ASU)................................................................................................4

U.S. Securities & Exchange Commission (SEC).......................................................................................7

Assurance Matters......................................................................................................................................8

Public Company Accounting Oversight Board (PCAOB).........................................................................8

American Institute of CPAs (AICPA)..........................................................................................................8

Center for Audit Quality (CAQ).................................................................................................................8

External Publications..................................................................................................................................9

Appendix A – 2016 Effective Date Highlights for Public Business Entities..........................................10

Appendix B – 2017 & Beyond, Effective Date Highlights for Public Business Entities.......................14

Appendix C – Effective Date Highlights for Private Companies...........................................................18

Appendix D – SEC Final Rules Highlights...............................................................................................26

2

assurance

First Quarter 2016 Accounting, Reporting & Auditing Developments

. first quarter 2016 accounting & auditing update

The developments included in this Accounting and Auditing (A&A) Update are intended to be a reminder of recently

issued accounting and auditing standards and other guidance that may affect our clients in the current reporting period.

Throughout the document we have also referenced other DHG external publications, as applicable. This quarterly A&A

Update is intended as general information and should not be relied upon as being definitive or all-inclusive. Recent quarterly

A&A Updates, can be found under Assurance Alerts on the DHG Resource Center.

1.704.367.7020 | dhgllp.com

© 2016 by Dixon Hughes Goodman LLP. All rights reserved.

Permission is granted to view, store, print, reproduce and distribute any pages of this Newsletter provided that (a) no page is modified and (b) this page is included with any distribution. Disclaimer: This publication has been prepared by the Dixon Hughes Goodman LLP Professional Standards Group and contains information in summary form and is therefore intended for general guidance only; it is not intended to be a substitute for detailed research or the exercise of professional judgment. You should consult with Dixon Hughes Goodman LLP or other professional advisors familiar with your particular factual situation for advice concerning specific audit, tax or other matters before making any decision. assurance 3 First Quarter 2016 Accounting, Reporting & Auditing Developments . Accounting & Financial Reporting Matters Financial Accounting Standards Board (FASB) ACCOUNTING STANDARDS UPDATES (ASU) ASU 2016-08 – Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net) The following are ASUs recently issued by the FASB. For a summary of their effective dates, refer to Appendices A and B for public business entities and Appendix C for private companies. This ASU is intended to improve the operability and understandability of the implementation guidance on principal versus agent considerations by clarifying the following: 1. An entity determines whether it is a principal or an agent for each specified good or service promised to the customer. A specified good or service is a distinct good or service (or a distinct bundle of goods or services) to be provided to the customer. If a contract with a customer includes more than one specified good or service, an entity could be a principal for some specified goods or services and an agent for others. ASU 2016-09 – Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting views 2. An entity determines the nature of each specified good or service (for example, whether it is a good, a service, or a right to a good or service). A continuation of the FASB simplification initiative, this ASU is the result of FASB outreach and input from the Private Company Council regarding the complexity of implementing current guidance for accounting for stock compensation.

The FASB has also added to its agenda a project to improve the accounting for share-based payments to non-employees. 3. When another party is involved in providing goods or services to a customer, an entity that is a principal obtains control of (a) a good or another asset from the other party that it then transfers to the customer; (b) a right to a service that will be performed by another party, which gives the entity the ability to direct that party to provide the service to the customer on the entity’s behalf; or (c) a good or service from the other party that it combines with other goods or services to provide the specified good or service to the customer. The amendments in this ASU are intended to improve the accounting for employee share-based payments and affect all organizations that issue share-based payment awards to their employees. Several aspects of the accounting for share-based payment award transactions are simplified, including: (a) income tax consequences; (b) classification of awards as either equity or liabilities; and (c) classification on the statement of cash flows. Specifically related to private companies, changes include allowing private companies the option to (a) apply a practical expedient to estimate expected terms and (b) switch from measuring all liability classified awards at fair value to intrinsic value. 4. The purpose of the indicators in paragraph 606-10-5539 is to support or assist in the assessment of the control assessment and that one or more indicators may be more or less persuasive to the control assessment, depending on the facts and circumstances. To help clarify how to apply the implementation guidance on principal versus agent considerations, ASU 2016-08 amended existing illustrative examples (specifically, Examples 45 and 46 in paragraphs 606-10-55-317 through 55-324 and Examples 47 and 48 in paragraphs 606-10-55-325 through 55-334). To further assist preparers in applying the guidance, additional illustrative examples have been included under Example 46A in paragraphs 606-10-55-324A through 55-324G and Example 48A in paragraphs 606-10-55-334A through 55-334F. For public business entities, the amendments are effective for annual periods beginning after December 15, 2016, and interim periods within those annual periods.

For all other entities, the amendments are effective for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018. Early adoption is permitted for any organization in any interim or annual period. However, if early adopted in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period.

Also, if early adopted, all amendments must be adopted in the same period. assurance The amendments affect the guidance in ASU 2014-09, Revenue from Contracts with Customers (Topic 606), and have similar effective dates and transition requirements (i.e., effective for public business entities, certain not-for-profit entities, and certain employee benefit plans with annual reporting periods beginning after December 15, 2017, including interim periods therein; effective for all other entities with annual reporting periods beginning after December 15, 2018 and interim periods within annual reporting periods beginning after December 15, 2019). 4 First Quarter 2016 Accounting, Reporting & Auditing Developments . Accounting & Financial Reporting Matters ASU 2016-07 – Investments – Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting ASU 2016-05 – Derivatives and Hedging (Topic 815): Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships The amendments in this ASU eliminate the requirement that when an investment qualifies for use of the equity method as a result of an increase in the level of ownership interest or degree of influence, an investor must adjust the investment, results of operations, and retained earnings retroactively on a step-by step basis as if the equity method had been in effect during all previous periods that the investment had been held. The amendments require that the equity method investor add the cost of acquiring the additional interest in the investee to the current basis of the investor’s previously held interest and adopt the equity method of accounting as of the date the investment becomes qualified for equity method accounting. Therefore, upon qualifying for the equity method of accounting, no retroactive adjustment of the investment is required. This ASU applies to all reporting entities for which there is a change in the counterparty to a derivative instrument that has been designated as a hedging instrument under Topic 815. The amendments in this ASU clarify that a change in the counterparty to a derivative instrument that has been designated as the hedging instrument under Topic 815 does not, in and of itself, require dedesignation of that hedging relationship provided that all other hedge accounting criteria (including those in paragraphs 815-20-35-14 through 35-18) continue to be met. For public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years.

For all other entities, the amendments in this ASU are effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018. An entity has an option to apply the amendments on either a prospective basis or a modified retrospective basis. Early adoption is permitted, including adoption in an interim period. The ASU also requires that an entity that has an available-forsale equity security that becomes qualified for the equity method of accounting, to recognize through earnings the unrealized holding gain or loss in accumulated other comprehensive income at the date the investment becomes qualified for use of the equity method. ASU 2016-04 – Liabilities – Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage for Certain Prepaid Stored-Value Products The amendments are effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016.

The amendments should be applied prospectively upon their effective date to increases in the level of ownership interest or degree of influence that result in the adoption of the equity method. Earlier application is permitted. The amendments in this ASU apply to entities that offer certain prepaid stored-value products (for example, prepaid gift cards issued on a specific payment network and redeemable at networkaccepting merchant locations, prepaid telecommunication cards, and traveler’s checks). Liabilities related to the sale of prepaid stored-value products within the scope of this ASU are financial liabilities.

The amendments provide a narrow scope exception to the guidance in Subtopic 405-20 to require that breakage for those liabilities be accounted for consistent with the breakage guidance in Topic 606. ASU 2016-06 – Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments The amendments in this ASU clarify what steps are required when assessing whether the economic characteristics and risks of call (put) options are clearly and closely related to the economic characteristics and risks of their debt hosts, which is one of the criteria for bifurcating an embedded derivative. Consequently, when a call (put) option is contingently exercisable, an entity does not have to assess whether the event that triggers the ability to exercise a call (put) option is related to interest rates or credit risks. The amendments are effective for public business entities, certain not-for-profit entities, and certain employee benefit plans for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. For all other entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019. Earlier application is permitted, including adoption in an interim period.

The amendments should be applied either using a modified retrospective transition method by means of a cumulative-effect adjustment to retained earnings as of the beginning of the fiscal year in which the guidance is effective or retrospectively to each period presented. For public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. For entities other than public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018. Early adoption is permitted, including adoption in an interim period. If an entity early adopts in an interim period, any adjustments should be reflected as of the beginning of that fiscal year. assurance 5 First Quarter 2016 Accounting, Reporting & Auditing Developments .

Accounting & Financial Reporting Matters ASU 2016-03 – Intangibles – Goodwill and Other (Topic 350), Business Combinations (Topic 805), Consolidation (Topic 810), Derivatives and Hedging (Topic 815): Effective Date and Transition Guidance (a consensus of the Private Company Council) views Companies should start to assess the capabilities of their financial reporting systems and controls, as they relate to the adoption of this new standard. The new lease standard requires a modified retrospective implementation approach, which means when companies adopt, they will need to apply the new lease guidance to each comparable period presented. For instance, a public company who adopts for the 2019 calendar year-end and reports three years of comparable information will need to evaluate how the standard will impact the presentation of the 2017 and 2018 financial statements. views This ASU allows private companies to avoid having to assess the preferability of an accounting alternative when first electing a PCC alternative, regardless of when the first election is made. For private companies that have not yet made the decision of whether to adopt a PCC alternative, this ASU provides them with more time to evaluate the impact of such a decision. Lessor accounting is largely unchanged from current accounting principles generally accepted in the United States (U.S. GAAP), with the exception of some revisions made to ensure consistency with the revised lessee guidance of ASU 2016-02 and with Revenue from Contract with Customers (Topic 606), upon adoption. The amendments in this ASU make the guidance in ASUs 201402, 2014-03, 2014-07, and 2014-18 effective immediately by removing their effective dates.

The amendments also include transition provisions that provide that private companies are able to forgo a preferability assessment the first time they elect the accounting alternatives within the scope of this ASU. Any subsequent change to an accounting policy election requires justification that the change is preferable under Topic 250, Accounting Changes and Error Corrections. The amendments also extend the transition guidance in ASUs 2014-02, 201403, 2014-07, and 2014-18 indefinitely.

While this ASU extends transition guidance for ASU 2014-07 and 2014-18, there is no intention to change how transition is applied for those two ASUs. The amendments in this ASU are effective immediately. The amendments are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years, for a public business entity, a not-for-profit entity that has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market, and employee benefit plans that file financial statements with the SEC. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020. Early application is permitted. ASU 2015-02 – Leases (Topic 842) For further discussion, see DHG’s recent publications Leases: Not Just For the Footnotes Anymore and (P)Lease Help! Understanding and Preparing for the New Lease Standard. On February 25, 2016 the FASB issued ASU 2015-02, Leases (Topic 842) the long-awaited lease standard. The key difference between the existing standards and ASU 2016-02 is the requirement for lessees to recognize on their balance sheet all lease contracts with lease terms greater than 12 months, including operating leases.

Specifically, lessees are required to recognize on the balance sheet at lease commencement, both: ASU 2016-01 – Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities • A right-of-use asset, representing the lessee’s right to use the leased asset over the term of the lease; and, views • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. This ASU results in the elimination of the available-for-sale classification for investments in equity securities, which is expected to introduce greater earnings volatility into a company’s earnings measures. Fair value changes that were previously recorded through other comprehensive income will now be recorded directly through earnings. For lessees, ASU 2016-02 requires classification of leases as either operating or finance leases, which are similar to the current operating and capital lease classifications. However, the distinction between these two classifications under the ASU does not relate to balance sheet treatment, but relates to treatment and recognition in the statements of income and cash flows. assurance This ASU addresses certain aspects of recognition, measurement, presentation, and disclosure of financial instruments.

The FASB is also addressing measurement of credit losses on financial assets in a separate project. The amendments in this ASU make targeted improvements to GAAP as follows: 6 First Quarter 2016 Accounting, Reporting & Auditing Developments . Accounting & Financial Reporting Matters 1. Require equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income. However, an entity may choose to measure equity investments that do not have readily determinable fair values at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or a similar investment of the same issuer. Except for certain early application scenarios, early adoption of the amendments is not permitted. An entity should apply the amendments by means of a cumulative-effect adjustment to the balance sheet as of the beginning of the fiscal year of adoption. The amendments related to equity securities without readily determinable fair values (including disclosure requirements) should be applied prospectively to equity investments that exist as of the date of adoption. For further discussion, see DHG’s recent publication FASB Releases New Standard on Classification & Measurement of Financial Instruments. 2. Simplify the impairment assessment of equity investments without readily determinable fair values by requiring a qualitative assessment to identify impairment. When a qualitative assessment indicates that impairment exists, an entity is required to measure the investment at fair value. U.S.

Securities & Exchange Commission (SEC) 3. Eliminate the requirement to disclose the fair value of financial instruments measured at amortized cost for entities that are not public business entities. Financial Reporting Manual Updated The SEC staff in the Division of Corporation Finance (Corp Fin) has updated the Financial Reporting Manual (FRM) through March 17, 2016. The updates include revisions to: 4. Eliminate the requirement for public business entities to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet. • Section 2410.8 to provide guidance on significance testing for equity method investees after a retrospective change in accounting principle for purposed complying with S-X Rules 3-09 and 408(g), 5. Require public business entities to use the exit price notion when measuring the fair value of financial instruments for disclosure purposes. • Add guidance to Topic 11 relating to ASU 2014-09, Revenue from Contracts with Customers (Topic 606) and IFRS 15, Revenue from Contracts with Customers. 6. Require an entity to present separately in other comprehensive income the portion of the total change in the fair value of a liability resulting from a change in the instrument-specific credit risk when the entity has elected to measure the liability at fair value in accordance with the fair value option for financial instruments. • Conform to Fixing America’s Surface Transportation (FAST) Act. Fixing America’s Surface Transportation Act Provisions On January 13, 2016 the SEC approved interim final rules, Simplification of Disclosure Requirements for Emerging Growth Companies and Forward Incorporation by Reference on Form S-1 for Smaller Reporting Companies (Release 33-10003). The interim final rules implement two provisions of the FAST Act that revise financial reporting forms for emerging growth companies (EGCs) and smaller reporting companies.

The rules cover the following sections of the FAST Act: 7. Require separate presentation of financial assets and financial liabilities by measurement category and form of financial asset (that is, securities or loans and receivables) on the balance sheet or the accompanying notes to the financial statements. 8. Clarify that an entity should evaluate the need for a valuation allowance on a deferred tax asset related to available-for-sale debt securities in combination with the entity’s other deferred tax assets. • Sec. 71003 amends Section 102 of the Jumpstart Our Business Startups (JOBS) Act to allow an EGC that is filing a registration statement (or submitting a draft registration statement for confidential review) under Section 6 of the Securities Act on Form S-1 or Form F-1 to omit financial information for historical periods otherwise required by Regulation S-X if it reasonably believes the omitted information will not be required to be included in the filing at the time of the contemplated offering, so long as the issuer amends the registration statement prior to distributing a preliminary prospectus to include all financial information required by Regulation S-X at the time of the amendment. For public business entities, the amendments are effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. For all other entities including not-for-profit entities and employee benefit plans within the scope of Topics 960 through 965 on plan accounting, the amendments are effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

All entities that are not public business entities may adopt the amendments earlier as of the fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. assurance 7 First Quarter 2016 Accounting, Reporting & Auditing Developments . Accounting & Financial Reporting Matters American Institute of CPAs (AICPA) • Sec. 84001 requires the SEC to revise Form S-1 to permit a smaller reporting company to incorporate by reference into its registration statement any documents filed by the issuer subsequent to the effective date of the registration statement. The interim final rules add a new paragraph to Item 12 of Form S-1 to effect this provision. Statement on Auditing Standards No. 131, Amendment to Statement on Auditing Standards No.

122 Section 700, Forming an Opinion on Reporting on Financial Statements (SAS 131) SAS 131 clarifies the format of the auditor’s report that should be issued when the auditor conducts an audit in accordance the standards of the PCAOB, but the audit is not under the jurisdiction of the PCAOB. SAS 131 provides that in these circumstances, the auditor must; (a) also comply with generally accepted auditing standards (GAAS); and (b) use the form of reporting specified by the PCAOB auditing standards, amended to indicate that the audit was also conducted in accordance with GAAS. The interim final rules become effective upon publication in the Federal Register. The deadline for submitting comments on the rules was February 18, 2016. Compliance and Disclosure Interpretations (C&DIs) The SEC staff issued a C&DI that clarifies how a registrant should describe a Rule 14a-8 shareholder proposal on its proxy card. The guidance states that for both management and shareholder proposals, a proxy card should clearly identify and describe the specific action on which shareholders will be asked to vote. These C&DIs comprise the Staff’s interpretations of the rules adopted under the Securities Act. The amendments in SAS 131 are effective for audits of financial statements for periods ending on or after June 15, 2016.

Earlier application is permitted. Assurance Matters Center for Audit Quality (CAQ) Public Company Accounting Oversight Board (PCAOB) Cybersecurity Resource The CAQ released Understanding Cybersecurity and the External Audit, a resource that explains the role that public company auditors can play regarding cybersecurity in two important contexts: (1) the audits of financial statements and internal control over financial reporting (where applicable), and (2) disclosures. 2016 Schedule of PCAOB Forums Announced The PCAOB announced the dates for their 2016 Forums on Auditing in the Small Business Environment and Forums for Auditors of Broker-Dealers. • The Forum on Auditing in the Small Business Environment is a program for representatives of the small business community to learn more about the work of the PCAOB and discuss issues with Board members and staff. It also allows the PCAOB to receive feedback on issues and challenges facing smaller registered firms. SEC Regulations Committee Meeting Highlights The CAQ’s SEC Regulations Committee issued highlights from its October 21, 2015 meeting with the SEC staff. The CAQ’s SEC Regulations Committee meets periodically with the SEC staff to discuss emerging technical accounting and reporting issues relating to SEC rules and regulations.

The purpose of the highlights is to summarize the issues discussed at the meeting. These highlights are not authoritative and users are urged to refer directly to applicable authoritative pronouncements for the text of the technical literature. Meeting highlights included: • The Forum for Auditors of Broker-Dealers is designed specifically for those auditors who audit brokers or dealers. Forum discussion topics typically include inspection observations, enforcement matters, case studies and presentations from the staff of the Financial Industry Regulatory Authority (FINRA). • Implementation guidance related to the new accounting standard, ASU 2014-09, Revenue from Contracts with Customers (Topic 606), and retrospective adoption. For more information, including forum dates, or to register for any of the forums, visit the PCAOB’s website. • The guidance in FRM sections 2045.3 and 2050.3 related to shelf take downs and greater than 50% business acquisitions only applies to completed transactions, not probable. • Interaction between pushdown accounting and Rule 3-10(i) and SAB Topics 1-J and 6-K. assurance 8 First Quarter 2016 Accounting, Reporting & Auditing Developments . Assurance Matters External Publications International Practices Task Force (IPTF) Committee Meeting Highlights The following articles have recently been published and are available on the DHG website. The CAQ’s IPTF issued highlights from its November 17, 2015 meeting with the SEC staff. The CAQ’s IPTF also meet periodically with the staff of the SEC to discuss emerging financial reporting issues relating to SEC rules and regulations. These highlights are not authoritative positions or interpretations issued by the SEC or its staff. Meeting highlights included: • Leases: Not Just For the Footnotes Anymore, March 2016 • Getting to the Bottom of the Top Line - Preparing to Adopt the New Revenue Recognition Standard, March 2016 • FASB Releases New Standard on Classification & Measurement of Financial Instruments, January 2016 • Requirements in Regulation S-K 512(a)(4) related to “keeping current” in an F-4 exchange offer. • Preparing pro forma financial information in cross-border mergers that are accounted for as reverse acquisitions. • Monitoring inflation in certain countries and determining “highly inflationary” status on the basis of the International Monetary Fund’s World Economic Outlook database as of October 2015. Audit Quality Indicators (AQIs) The CAQ released Audit Quality Indicators: The Journey and Path Ahead, in January 2016, which provides insights from a global series of roundtable discussions with audit committee members and other stakeholders on a potential set of AQIs. assurance 9 First Quarter 2016 Accounting, Reporting & Auditing Developments .

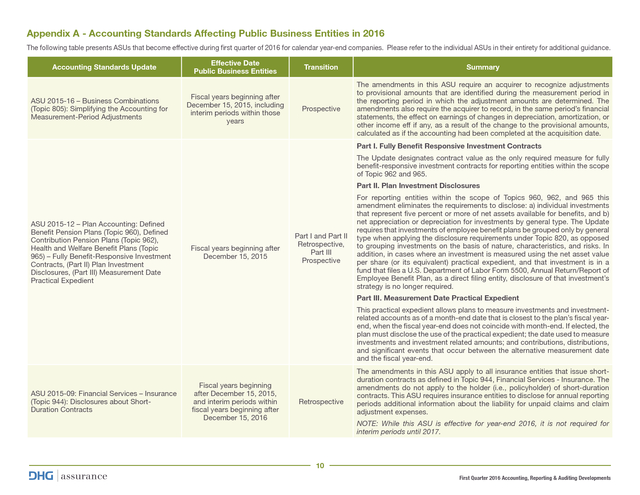

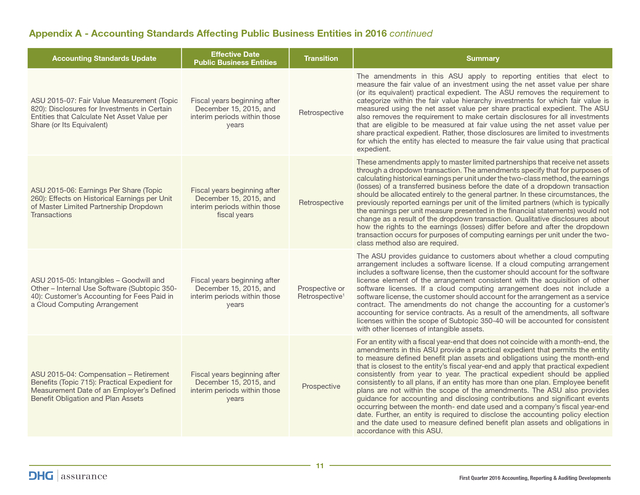

Appendix A - Accounting Standards Affecting Public Business Entities in 2016 The following table presents ASUs that become effective during first quarter of 2016 for calendar year-end companies. Please refer to the individual ASUs in their entirety for additional guidance. Accounting Standards Update ASU 2015-16 – Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments Effective Date Public Business Entities Fiscal years beginning after December 15, 2015, including interim periods within those years Transition Summary Prospective The amendments in this ASU require an acquirer to recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The amendments also require the acquirer to record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization, or other income eff if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. Part I. Fully Benefit Responsive Investment Contracts The Update designates contract value as the only required measure for fully benefit-responsive investment contracts for reporting entities within the scope of Topic 962 and 965. Part II.

Plan Investment Disclosures ASU 2015-12 – Plan Accounting: Defined Benefit Pension Plans (Topic 960), Defined Contribution Pension Plans (Topic 962), Health and Welfare Benefit Plans (Topic 965) – Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient Fiscal years beginning after December 15, 2015 Part I and Part II Retrospective, Part III Prospective For reporting entities within the scope of Topics 960, 962, and 965 this amendment eliminates the requirements to disclose: a) individual investments that represent five percent or more of net assets available for benefits, and b) net appreciation or depreciation for investments by general type. The Update requires that investments of employee benefit plans be grouped only by general type when applying the disclosure requirements under Topic 820, as opposed to grouping investments on the basis of nature, characteristics, and risks. In addition, in cases where an investment is measured using the net asset value per share (or its equivalent) practical expedient, and that investment is in a fund that files a U.S.

Department of Labor Form 5500, Annual Return/Report of Employee Benefit Plan, as a direct filing entity, disclosure of that investment’s strategy is no longer required. Part III. Measurement Date Practical Expedient This practical expedient allows plans to measure investments and investmentrelated accounts as of a month-end date that is closest to the plan’s fiscal yearend, when the fiscal year-end does not coincide with month-end. If elected, the plan must disclose the use of the practical expedient; the date used to measure investments and investment related amounts; and contributions, distributions, and significant events that occur between the alternative measurement date and the fiscal year-end. ASU 2015-09: Financial Services – Insurance (Topic 944): Disclosures about ShortDuration Contracts Fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016 Retrospective The amendments in this ASU apply to all insurance entities that issue shortduration contracts as defined in Topic 944, Financial Services - Insurance.

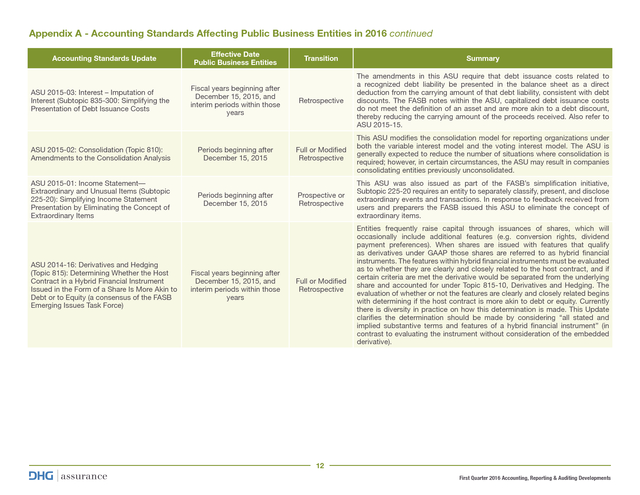

The amendments do not apply to the holder (i.e., policyholder) of short-duration contracts. This ASU requires insurance entities to disclose for annual reporting periods additional information about the liability for unpaid claims and claim adjustment expenses. NOTE: While this ASU is effective for year-end 2016, it is not required for interim periods until 2017. 10 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix A - Accounting Standards Affecting Public Business Entities in 2016 continued Accounting Standards Update ASU 2015-07: Fair Value Measurement (Topic 820): Disclosures for Investments in Certain Entities that Calculate Net Asset Value per Share (or Its Equivalent) ASU 2015-06: Earnings Per Share (Topic 260): Effects on Historical Earnings per Unit of Master Limited Partnership Dropdown Transactions ASU 2015-05: Intangibles – Goodwill and Other – Internal Use Software (Subtopic 35040): Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement ASU 2015-04: Compensation – Retirement Benefits (Topic 715): Practical Expedient for Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets Effective Date Public Business Entities Fiscal years beginning after December 15, 2015, and interim periods within those years Fiscal years beginning after December 15, 2015, and interim periods within those fiscal years Fiscal years beginning after December 15, 2015, and interim periods within those years Fiscal years beginning after December 15, 2015, and interim periods within those years Transition Summary Retrospective The amendments in this ASU apply to reporting entities that elect to measure the fair value of an investment using the net asset value per share (or its equivalent) practical expedient. The ASU removes the requirement to categorize within the fair value hierarchy investments for which fair value is measured using the net asset value per share practical expedient. The ASU also removes the requirement to make certain disclosures for all investments that are eligible to be measured at fair value using the net asset value per share practical expedient. Rather, those disclosures are limited to investments for which the entity has elected to measure the fair value using that practical expedient. Retrospective These amendments apply to master limited partnerships that receive net assets through a dropdown transaction.

The amendments specify that for purposes of calculating historical earnings per unit under the two-class method, the earnings (losses) of a transferred business before the date of a dropdown transaction should be allocated entirely to the general partner. In these circumstances, the previously reported earnings per unit of the limited partners (which is typically the earnings per unit measure presented in the financial statements) would not change as a result of the dropdown transaction. Qualitative disclosures about how the rights to the earnings (losses) differ before and after the dropdown transaction occurs for purposes of computing earnings per unit under the twoclass method also are required. Prospective or Retrospective1 The ASU provides guidance to customers about whether a cloud computing arrangement includes a software license.

If a cloud computing arrangement includes a software license, then the customer should account for the software license element of the arrangement consistent with the acquisition of other software licenses. If a cloud computing arrangement does not include a software license, the customer should account for the arrangement as a service contract. The amendments do not change the accounting for a customer’s accounting for service contracts.

As a result of the amendments, all software licenses within the scope of Subtopic 350-40 will be accounted for consistent with other licenses of intangible assets. Prospective For an entity with a fiscal year-end that does not coincide with a month-end, the amendments in this ASU provide a practical expedient that permits the entity to measure defined benefit plan assets and obligations using the month-end that is closest to the entity’s fiscal year-end and apply that practical expedient consistently from year to year. The practical expedient should be applied consistently to all plans, if an entity has more than one plan. Employee benefit plans are not within the scope of the amendments.

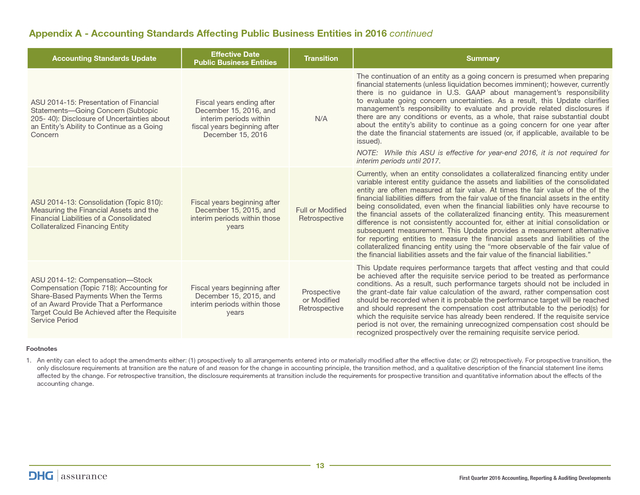

The ASU also provides guidance for accounting and disclosing contributions and significant events occurring between the month- end date used and a company’s fiscal year-end date. Further, an entity is required to disclose the accounting policy election and the date used to measure defined benefit plan assets and obligations in accordance with this ASU. 11 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix A - Accounting Standards Affecting Public Business Entities in 2016 continued Accounting Standards Update ASU 2015-03: Interest – Imputation of Interest (Subtopic 835-300: Simplifying the Presentation of Debt Issuance Costs ASU 2015-02: Consolidation (Topic 810): Amendments to the Consolidation Analysis ASU 2015-01: Income Statement— Extraordinary and Unusual Items (Subtopic 225-20): Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items ASU 2014-16: Derivatives and Hedging (Topic 815): Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity (a consensus of the FASB Emerging Issues Task Force) Effective Date Public Business Entities Fiscal years beginning after December 15, 2015, and interim periods within those years Periods beginning after December 15, 2015 Periods beginning after December 15, 2015 Fiscal years beginning after December 15, 2015, and interim periods within those years Transition Summary Retrospective The amendments in this ASU require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The FASB notes within the ASU, capitalized debt issuance costs do not meet the definition of an asset and are more akin to a debt discount, thereby reducing the carrying amount of the proceeds received. Also refer to ASU 2015-15. Full or Modified Retrospective This ASU modifies the consolidation model for reporting organizations under both the variable interest model and the voting interest model. The ASU is generally expected to reduce the number of situations where consolidation is required; however, in certain circumstances, the ASU may result in companies consolidating entities previously unconsolidated. Prospective or Retrospective This ASU was also issued as part of the FASB’s simplification initiative, Subtopic 225-20 requires an entity to separately classify, present, and disclose extraordinary events and transactions.

In response to feedback received from users and preparers the FASB issued this ASU to eliminate the concept of extraordinary items. Full or Modified Retrospective Entities frequently raise capital through issuances of shares, which will occasionally include additional features (e.g. conversion rights, dividend payment preferences). When shares are issued with features that qualify as derivatives under GAAP those shares are referred to as hybrid financial instruments.

The features within hybrid financial instruments must be evaluated as to whether they are clearly and closely related to the host contract, and if certain criteria are met the derivative would be separated from the underlying share and accounted for under Topic 815-10, Derivatives and Hedging. The evaluation of whether or not the features are clearly and closely related begins with determining if the host contract is more akin to debt or equity. Currently there is diversity in practice on how this determination is made.

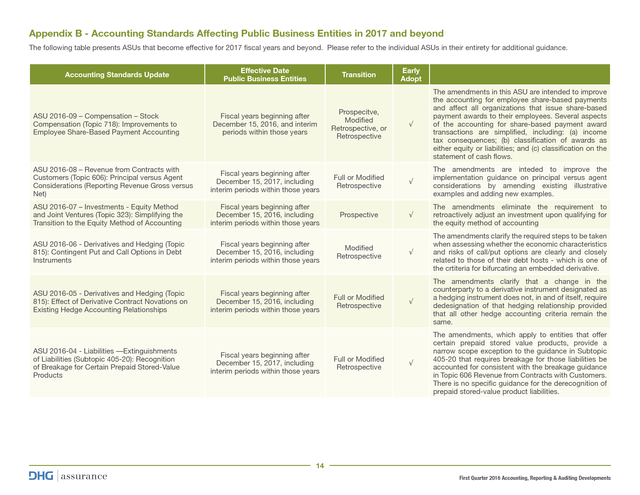

This Update clarifies the determination should be made by considering “all stated and implied substantive terms and features of a hybrid financial instrument” (in contrast to evaluating the instrument without consideration of the embedded derivative). 12 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix A - Accounting Standards Affecting Public Business Entities in 2016 continued Accounting Standards Update ASU 2014-15: Presentation of Financial Statements—Going Concern (Subtopic 205- 40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern Effective Date Public Business Entities Fiscal years ending after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2016 Transition N/A Summary The continuation of an entity as a going concern is presumed when preparing financial statements (unless liquidation becomes imminent); however, currently there is no guidance in U.S. GAAP about management’s responsibility to evaluate going concern uncertainties. As a result, this Update clarifies management’s responsibility to evaluate and provide related disclosures if there are any conditions or events, as a whole, that raise substantial doubt about the entity’s ability to continue as a going concern for one year after the date the financial statements are issued (or, if applicable, available to be issued). NOTE: While this ASU is effective for year-end 2016, it is not required for interim periods until 2017. ASU 2014-13: Consolidation (Topic 810): Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity ASU 2014-12: Compensation—Stock Compensation (Topic 718): Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period Fiscal years beginning after December 15, 2015, and interim periods within those years Fiscal years beginning after December 15, 2015, and interim periods within those years Full or Modified Retrospective Currently, when an entity consolidates a collateralized financing entity under variable interest entity guidance the assets and liabilities of the consolidated entity are often measured at fair value. At times the fair value of the of the financial liabilities differs from the fair value of the financial assets in the entity being consolidated, even when the financial liabilities only have recourse to the financial assets of the collateralized financing entity.

This measurement difference is not consistently accounted for, either at initial consolidation or subsequent measurement. This Update provides a measurement alternative for reporting entities to measure the financial assets and liabilities of the collateralized financing entity using the “more observable of the fair value of the financial liabilities assets and the fair value of the financial liabilities.” Prospective or Modified Retrospective This Update requires performance targets that affect vesting and that could be achieved after the requisite service period to be treated as performance conditions. As a result, such performance targets should not be included in the grant-date fair value calculation of the award, rather compensation cost should be recorded when it is probable the performance target will be reached and should represent the compensation cost attributable to the period(s) for which the requisite service has already been rendered.

If the requisite service period is not over, the remaining unrecognized compensation cost should be recognized prospectively over the remaining requisite service period. Footnotes 1. An entity can elect to adopt the amendments either: (1) prospectively to all arrangements entered into or materially modified after the effective date; or (2) retrospectively. For prospective transition, the only disclosure requirements at transition are the nature of and reason for the change in accounting principle, the transition method, and a qualitative description of the financial statement line items affected by the change. For retrospective transition, the disclosure requirements at transition include the requirements for prospective transition and quantitative information about the effects of the accounting change. 13 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments .

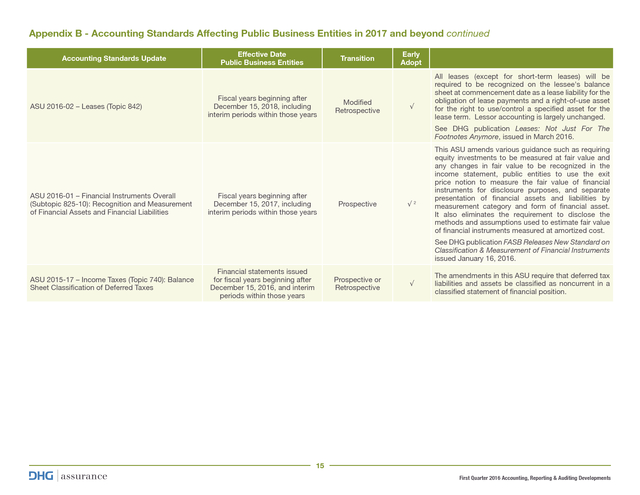

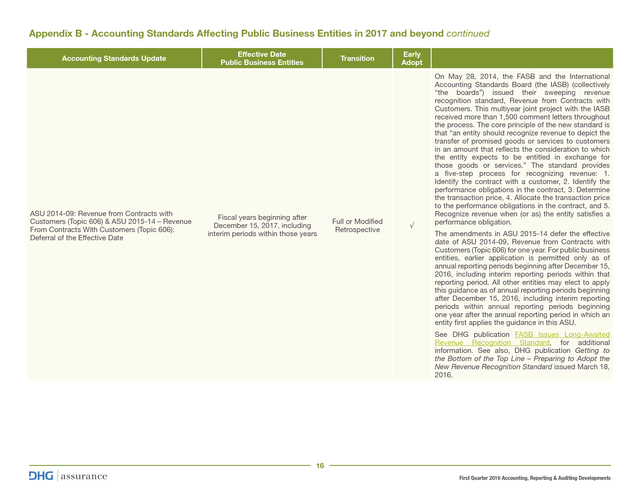

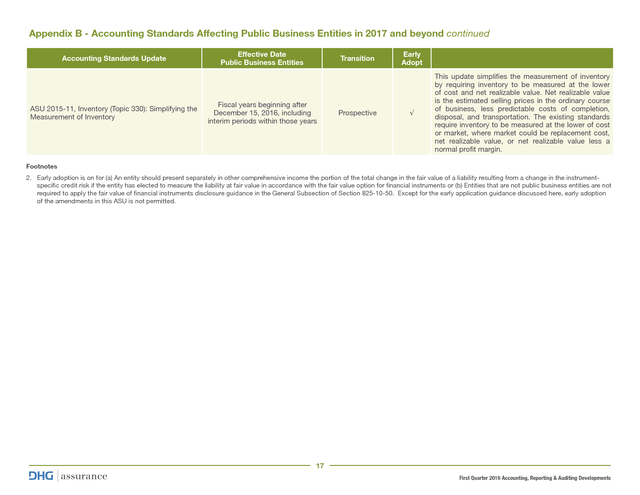

Appendix B - Accounting Standards Affecting Public Business Entities in 2017 and beyond The following table presents ASUs that become effective for 2017 fiscal years and beyond. Please refer to the individual ASUs in their entirety for additional guidance. Accounting Standards Update Effective Date Public Business Entities Transition Early Adopt Fiscal years beginning after December 15, 2016, and interim periods within those years Prospecitve, Modified Retrospective, or Retrospective √ The amendments in this ASU are intended to improve the accounting for employee share-based payments and affect all organizations that issue share-based payment awards to their employees. Several aspects of the accounting for share-based payment award transactions are simplified, including: (a) income tax consequences; (b) classification of awards as either equity or liabilities; and (c) classification on the statement of cash flows. ASU 2016-08 – Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net) Fiscal years beginning after December 15, 2017, including interim periods within those years Full or Modified Retrospective √ The amendments are inteded to improve the implementation guidance on principal versus agent considerations by amending existing illustrative examples and adding new examples. ASU 2016-07 – Investments - Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting Fiscal years beginning after December 15, 2016, including interim periods within those years Prospective √ The amendments eliminate the requirement to retroactively adjust an investment upon qualifying for the equity method of accounting ASU 2016-06 - Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments Fiscal years beginning after December 15, 2016, including interim periods within those years √ The amendments clarify the required steps to be taken when assessing whether the economic characteristics and risks of call/put options are clearly and closely related to those of their debt hosts - which is one of the crtiteria for bifurcating an embedded derivative. √ The amendments clarify that a change in the counterparty to a derivative instrument designated as a hedging instrument does not, in and of itself, require dedesignation of that hedging relationship provided that all other hedge accounting criteria remain the same. √ The amendments, which apply to entities that offer certain prepaid stored value products, provide a narrow scope exception to the guidance in Subtopic 405-20 that requires breakage for those liabilities be accounted for consistent with the breakage guidance in Topic 606 Revenue from Contracts with Customers. There is no specific guidance for the derecognition of prepaid stored-value product liabilities. ASU 2016-09 – Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting ASU 2016-05 - Derivatives and Hedging (Topic 815): Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships ASU 2016-04 - Liabilities —Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage for Certain Prepaid Stored-Value Products Fiscal years beginning after December 15, 2016, including interim periods within those years Fiscal years beginning after December 15, 2017, including interim periods within those years Modified Retrospective Full or Modified Retrospective Full or Modified Retrospective 14 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix B - Accounting Standards Affecting Public Business Entities in 2017 and beyond continued Accounting Standards Update ASU 2016-02 – Leases (Topic 842) Effective Date Public Business Entities Transition Fiscal years beginning after December 15, 2018, including interim periods within those years Modified Retrospective Early Adopt √ All leases (except for short-term leases) will be required to be recognized on the lessee's balance sheet at commencement date as a lease liability for the obligation of lease payments and a right-of-use asset for the right to use/control a specified asset for the lease term. Lessor accounting is largely unchanged. See DHG publication Leases: Not Just For The Footnotes Anymore, issued in March 2016. ASU 2016-01 – Financial Instruments Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities Fiscal years beginning after December 15, 2017, including interim periods within those years Prospective √2 This ASU amends various guidance such as requiring equity investments to be measured at fair value and any changes in fair value to be recognized in the income statement, public entities to use the exit price notion to measure the fair value of financial instruments for disclosure purposes, and separate presentation of financial assets and liabilities by measurement category and form of financial asset. It also eliminates the requirement to disclose the methods and assumptions used to estimate fair value of financial instruments measured at amortized cost. See DHG publication FASB Releases New Standard on Classification & Measurement of Financial Instruments issued January 16, 2016. ASU 2015-17 – Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes Financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those years Prospective or Retrospective √ The amendments in this ASU require that deferred tax liabilities and assets be classified as noncurrent in a classified statement of financial position. 15 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix B - Accounting Standards Affecting Public Business Entities in 2017 and beyond continued Accounting Standards Update ASU 2014-09: Revenue from Contracts with Customers (Topic 606) & ASU 2015-14 – Revenue From Contracts With Customers (Topic 606): Deferral of the Effective Date Effective Date Public Business Entities Transition Fiscal years beginning after December 15, 2017, including interim periods within those years Full or Modified Retrospective Early Adopt √ On May 28, 2014, the FASB and the International Accounting Standards Board (the IASB) (collectively “the boards”) issued their sweeping revenue recognition standard, Revenue from Contracts with Customers. This multiyear joint project with the IASB received more than 1,500 comment letters throughout the process. The core principle of the new standard is that “an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.” The standard provides a five-step process for recognizing revenue: 1. Identify the contract with a customer, 2. Identify the performance obligations in the contract, 3.

Determine the transaction price, 4. Allocate the transaction price to the performance obligations in the contract, and 5. Recognize revenue when (or as) the entity satisfies a performance obligation. The amendments in ASU 2015-14 defer the effective date of ASU 2014-09, Revenue from Contracts with Customers (Topic 606) for one year. For public business entities, earlier application is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period.

All other entities may elect to apply this guidance as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within annual reporting periods beginning one year after the annual reporting period in which an entity first applies the guidance in this ASU. See DHG publication FASB Issues Long-Awaited Revenue Recognition Standard, for additional information. See also, DHG publication Getting to the Bottom of the Top Line – Preparing to Adopt the New Revenue Recognition Standard issued March 18, 2016. 16 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix B - Accounting Standards Affecting Public Business Entities in 2017 and beyond continued Accounting Standards Update ASU 2015-11, Inventory (Topic 330): Simplifying the Measurement of Inventory Effective Date Public Business Entities Transition Fiscal years beginning after December 15, 2016, including interim periods within those years Prospective Early Adopt √ This update simplifies the measurement of inventory by requiring inventory to be measured at the lower of cost and net realizable value. Net realizable value is the estimated selling prices in the ordinary course of business, less predictable costs of completion, disposal, and transportation. The existing standards require inventory to be measured at the lower of cost or market, where market could be replacement cost, net realizable value, or net realizable value less a normal profit margin. Footnotes 2. Early adoption is on for (a) An entity should present separately in other comprehensive income the portion of the total change in the fair value of a liability resulting from a change in the instrumentspecific credit risk if the entity has elected to measure the liability at fair value in accordance with the fair value option for financial instruments or (b) Entities that are not public business entities are not required to apply the fair value of financial instruments disclosure guidance in the General Subsection of Section 825-10-50. Except for the early application guidance discussed here, early adoption of the amendments in this ASU is not permitted. 17 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments .

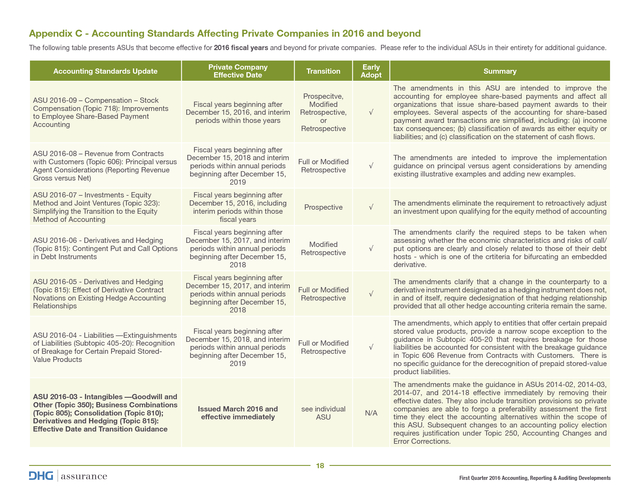

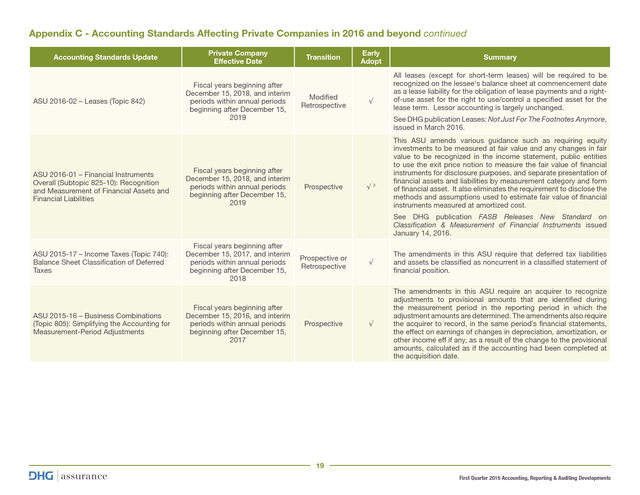

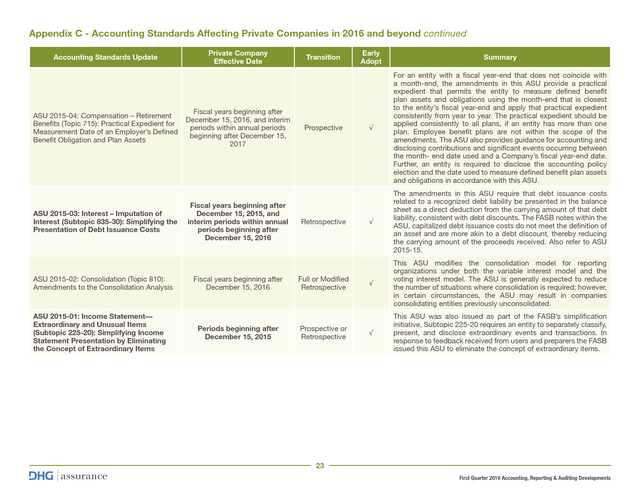

Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond The following table presents ASUs that become effective for 2016 fiscal years and beyond for private companies. Please refer to the individual ASUs in their entirety for additional guidance. Early Adopt Summary Fiscal years beginning after December 15, 2016, and interim periods within those years Prospecitve, Modified Retrospective, or Retrospective √ The amendments in this ASU are intended to improve the accounting for employee share-based payments and affect all organizations that issue share-based payment awards to their employees. Several aspects of the accounting for share-based payment award transactions are simplified, including: (a) income tax consequences; (b) classification of awards as either equity or liabilities; and (c) classification on the statement of cash flows. Fiscal years beginning after December 15, 2018 and interim periods within annual periods beginning after December 15, 2019 Full or Modified Retrospective √ The amendments are inteded to improve the implementation guidance on principal versus agent considerations by amending existing illustrative examples and adding new examples. Fiscal years beginning after December 15, 2016, including interim periods within those fiscal years Prospective √ The amendments eliminate the requirement to retroactively adjust an investment upon qualifying for the equity method of accounting √ The amendments clarify the required steps to be taken when assessing whether the economic characteristics and risks of call/ put options are clearly and closely related to those of their debt hosts - which is one of the crtiteria for bifurcating an embedded derivative. √ The amendments clarify that a change in the counterparty to a derivative instrument designated as a hedging instrument does not, in and of itself, require dedesignation of that hedging relationship provided that all other hedge accounting criteria remain the same. √ The amendments, which apply to entities that offer certain prepaid stored value products, provide a narrow scope exception to the guidance in Subtopic 405-20 that requires breakage for those liabilities be accounted for consistent with the breakage guidance in Topic 606 Revenue from Contracts with Customers. There is no specific guidance for the derecognition of prepaid stored-value product liabilities. N/A The amendments make the guidance in ASUs 2014-02, 2014-03, 2014-07, and 2014-18 effective immediately by removing their effective dates.

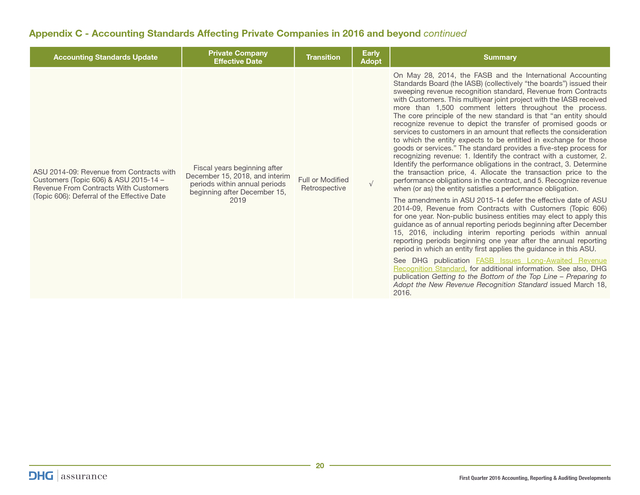

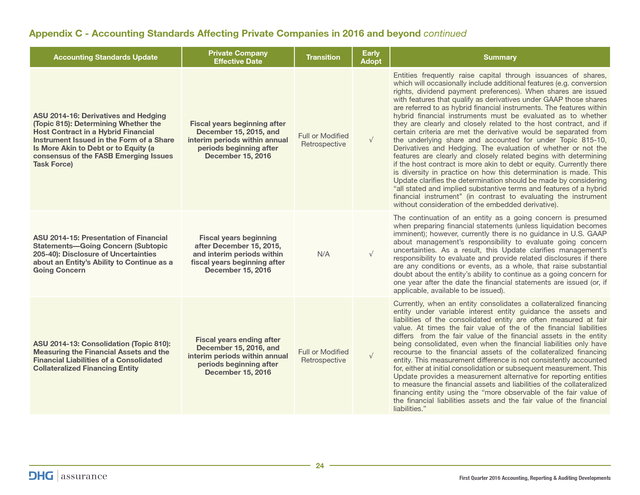

They also include transition provisions so private companies are able to forgo a preferability assessment the first time they elect the accounting alternatives within the scope of this ASU. Subsequent changes to an accounting policy election requires justification under Topic 250, Accounting Changes and Error Corrections. Private Company Effective Date Transition ASU 2016-09 – Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting ASU 2016-08 – Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net) Accounting Standards Update ASU 2016-07 – Investments - Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting ASU 2016-06 - Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments Fiscal years beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018 Modified Retrospective ASU 2016-05 - Derivatives and Hedging (Topic 815): Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships Fiscal years beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018 Full or Modified Retrospective ASU 2016-04 - Liabilities —Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage for Certain Prepaid StoredValue Products Fiscal years beginning after December 15, 2018, and interim periods within annual periods beginning after December 15, 2019 ASU 2016-03 - Intangibles —Goodwill and Other (Topic 350); Business Combinations (Topic 805); Consolidation (Topic 810); Derivatives and Hedging (Topic 815): Effective Date and Transition Guidance Issued March 2016 and effective immediately Full or Modified Retrospective see individual ASU 18 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update ASU 2016-02 – Leases (Topic 842) ASU 2016-01 – Financial Instruments Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities Private Company Effective Date Fiscal years beginning after December 15, 2018, and interim periods within annual periods beginning after December 15, 2019 Fiscal years beginning after December 15, 2018, and interim periods within annual periods beginning after December 15, 2019 Transition Modified Retrospective Early Adopt √ Summary All leases (except for short-term leases) will be required to be recognized on the lessee's balance sheet at commencement date as a lease liability for the obligation of lease payments and a rightof-use asset for the right to use/control a specified asset for the lease term. Lessor accounting is largely unchanged. See DHG publication Leases: Not Just For The Footnotes Anymore, issued in March 2016. Prospective √3 This ASU amends various guidance such as requiring equity investments to be measured at fair value and any changes in fair value to be recognized in the income statement, public entities to use the exit price notion to measure the fair value of financial instruments for disclosure purposes, and separate presentation of financial assets and liabilities by measurement category and form of financial asset. It also eliminates the requirement to disclose the methods and assumptions used to estimate fair value of financial instruments measured at amortized cost. See DHG publication FASB Releases New Standard on Classification & Measurement of Financial Instruments issued January 14, 2016. ASU 2015-17 – Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes ASU 2015-16 – Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments Fiscal years beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018 Fiscal years beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017 Prospective or Retrospective Prospective √ The amendments in this ASU require that deferred tax liabilities and assets be classified as noncurrent in a classified statement of financial position. √ The amendments in this ASU require an acquirer to recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The amendments also require the acquirer to record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization, or other income eff if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. 19 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments .

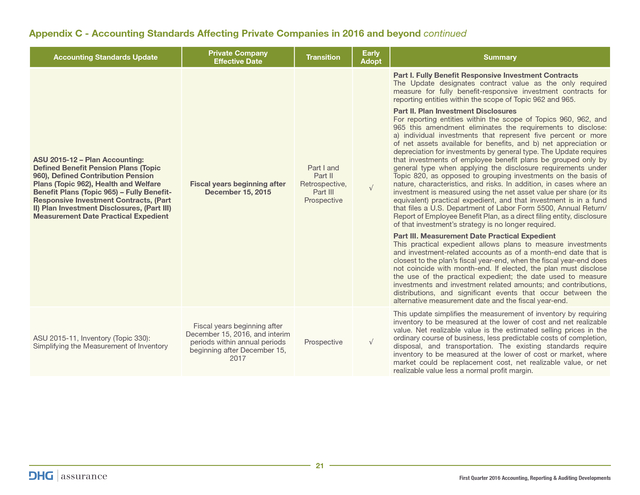

Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update ASU 2014-09: Revenue from Contracts with Customers (Topic 606) & ASU 2015-14 – Revenue From Contracts With Customers (Topic 606): Deferral of the Effective Date Private Company Effective Date Fiscal years beginning after December 15, 2018, and interim periods within annual periods beginning after December 15, 2019 Transition Full or Modified Retrospective Early Adopt √ Summary On May 28, 2014, the FASB and the International Accounting Standards Board (the IASB) (collectively “the boards”) issued their sweeping revenue recognition standard, Revenue from Contracts with Customers. This multiyear joint project with the IASB received more than 1,500 comment letters throughout the process. The core principle of the new standard is that “an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.” The standard provides a five-step process for recognizing revenue: 1. Identify the contract with a customer, 2. Identify the performance obligations in the contract, 3. Determine the transaction price, 4.

Allocate the transaction price to the performance obligations in the contract, and 5. Recognize revenue when (or as) the entity satisfies a performance obligation. The amendments in ASU 2015-14 defer the effective date of ASU 2014-09, Revenue from Contracts with Customers (Topic 606) for one year. Non-public business entities may elect to apply this guidance as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within annual reporting periods beginning one year after the annual reporting period in which an entity first applies the guidance in this ASU. See DHG publication FASB Issues Long-Awaited Revenue Recognition Standard, for additional information.

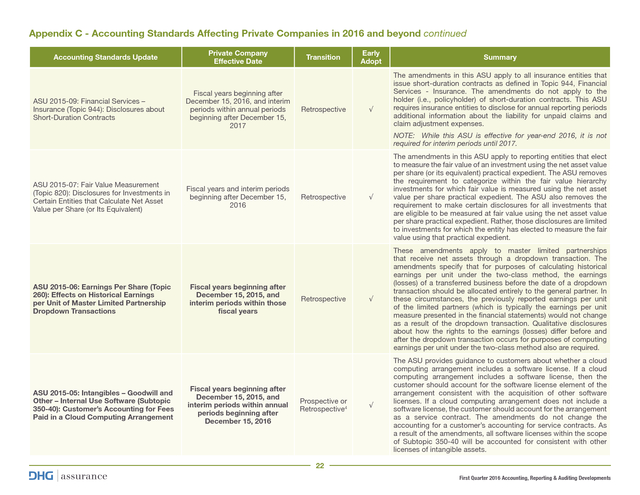

See also, DHG publication Getting to the Bottom of the Top Line – Preparing to Adopt the New Revenue Recognition Standard issued March 18, 2016. 20 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update Private Company Effective Date Transition Early Adopt Summary Part I. Fully Benefit Responsive Investment Contracts The Update designates contract value as the only required measure for fully benefit-responsive investment contracts for reporting entities within the scope of Topic 962 and 965. ASU 2015-12 – Plan Accounting: Defined Benefit Pension Plans (Topic 960), Defined Contribution Pension Plans (Topic 962), Health and Welfare Benefit Plans (Topic 965) – Fully BenefitResponsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient Fiscal years beginning after December 15, 2015 Part I and Part II Retrospective, Part III Prospective √ Part II. Plan Investment Disclosures For reporting entities within the scope of Topics 960, 962, and 965 this amendment eliminates the requirements to disclose: a) individual investments that represent five percent or more of net assets available for benefits, and b) net appreciation or depreciation for investments by general type. The Update requires that investments of employee benefit plans be grouped only by general type when applying the disclosure requirements under Topic 820, as opposed to grouping investments on the basis of nature, characteristics, and risks.

In addition, in cases where an investment is measured using the net asset value per share (or its equivalent) practical expedient, and that investment is in a fund that files a U.S. Department of Labor Form 5500, Annual Return/ Report of Employee Benefit Plan, as a direct filing entity, disclosure of that investment’s strategy is no longer required. Part III. Measurement Date Practical Expedient This practical expedient allows plans to measure investments and investment-related accounts as of a month-end date that is closest to the plan’s fiscal year-end, when the fiscal year-end does not coincide with month-end.

If elected, the plan must disclose the use of the practical expedient; the date used to measure investments and investment related amounts; and contributions, distributions, and significant events that occur between the alternative measurement date and the fiscal year-end. ASU 2015-11, Inventory (Topic 330): Simplifying the Measurement of Inventory Fiscal years beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017 Prospective √ This update simplifies the measurement of inventory by requiring inventory to be measured at the lower of cost and net realizable value. Net realizable value is the estimated selling prices in the ordinary course of business, less predictable costs of completion, disposal, and transportation. The existing standards require inventory to be measured at the lower of cost or market, where market could be replacement cost, net realizable value, or net realizable value less a normal profit margin. 21 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments .

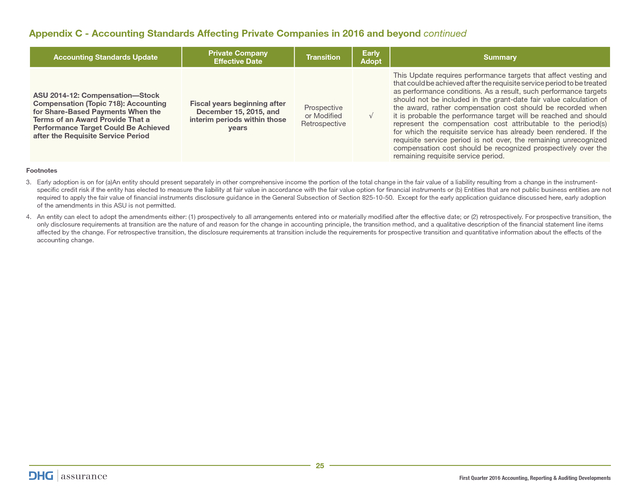

Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update ASU 2015-09: Financial Services – Insurance (Topic 944): Disclosures about Short-Duration Contracts Private Company Effective Date Fiscal years beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017 Transition Retrospective Early Adopt √ Summary The amendments in this ASU apply to all insurance entities that issue short-duration contracts as defined in Topic 944, Financial Services - Insurance. The amendments do not apply to the holder (i.e., policyholder) of short-duration contracts. This ASU requires insurance entities to disclose for annual reporting periods additional information about the liability for unpaid claims and claim adjustment expenses. NOTE: While this ASU is effective for year-end 2016, it is not required for interim periods until 2017. ASU 2015-07: Fair Value Measurement (Topic 820): Disclosures for Investments in Certain Entities that Calculate Net Asset Value per Share (or Its Equivalent) ASU 2015-06: Earnings Per Share (Topic 260): Effects on Historical Earnings per Unit of Master Limited Partnership Dropdown Transactions ASU 2015-05: Intangibles – Goodwill and Other – Internal Use Software (Subtopic 350-40): Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement Fiscal years and interim periods beginning after December 15, 2016 Fiscal years beginning after December 15, 2015, and interim periods within those fiscal years Fiscal years beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016 Retrospective Retrospective Prospective or Retrospective4 √ The amendments in this ASU apply to reporting entities that elect to measure the fair value of an investment using the net asset value per share (or its equivalent) practical expedient. The ASU removes the requirement to categorize within the fair value hierarchy investments for which fair value is measured using the net asset value per share practical expedient.

The ASU also removes the requirement to make certain disclosures for all investments that are eligible to be measured at fair value using the net asset value per share practical expedient. Rather, those disclosures are limited to investments for which the entity has elected to measure the fair value using that practical expedient. √ These amendments apply to master limited partnerships that receive net assets through a dropdown transaction. The amendments specify that for purposes of calculating historical earnings per unit under the two-class method, the earnings (losses) of a transferred business before the date of a dropdown transaction should be allocated entirely to the general partner.

In these circumstances, the previously reported earnings per unit of the limited partners (which is typically the earnings per unit measure presented in the financial statements) would not change as a result of the dropdown transaction. Qualitative disclosures about how the rights to the earnings (losses) differ before and after the dropdown transaction occurs for purposes of computing earnings per unit under the two-class method also are required. √ The ASU provides guidance to customers about whether a cloud computing arrangement includes a software license. If a cloud computing arrangement includes a software license, then the customer should account for the software license element of the arrangement consistent with the acquisition of other software licenses.

If a cloud computing arrangement does not include a software license, the customer should account for the arrangement as a service contract. The amendments do not change the accounting for a customer’s accounting for service contracts. As a result of the amendments, all software licenses within the scope of Subtopic 350-40 will be accounted for consistent with other licenses of intangible assets. 22 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments .

Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update ASU 2015-04: Compensation – Retirement Benefits (Topic 715): Practical Expedient for Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets ASU 2015-03: Interest – Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs ASU 2015-02: Consolidation (Topic 810): Amendments to the Consolidation Analysis ASU 2015-01: Income Statement— Extraordinary and Unusual Items (Subtopic 225-20): Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items Private Company Effective Date Fiscal years beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017 Fiscal years beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016 Fiscal years beginning after December 15, 2016 Periods beginning after December 15, 2015 Transition Prospective Retrospective Full or Modified Retrospective Prospective or Retrospective Early Adopt Summary √ For an entity with a fiscal year-end that does not coincide with a month-end, the amendments in this ASU provide a practical expedient that permits the entity to measure defined benefit plan assets and obligations using the month-end that is closest to the entity’s fiscal year-end and apply that practical expedient consistently from year to year. The practical expedient should be applied consistently to all plans, if an entity has more than one plan. Employee benefit plans are not within the scope of the amendments. The ASU also provides guidance for accounting and disclosing contributions and significant events occurring between the month- end date used and a Company’s fiscal year-end date. Further, an entity is required to disclose the accounting policy election and the date used to measure defined benefit plan assets and obligations in accordance with this ASU. √ The amendments in this ASU require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts.

The FASB notes within the ASU, capitalized debt issuance costs do not meet the definition of an asset and are more akin to a debt discount, thereby reducing the carrying amount of the proceeds received. Also refer to ASU 2015-15. √ This ASU modifies the consolidation model for reporting organizations under both the variable interest model and the voting interest model. The ASU is generally expected to reduce the number of situations where consolidation is required; however, in certain circumstances, the ASU may result in companies consolidating entities previously unconsolidated. √ This ASU was also issued as part of the FASB’s simplification initiative, Subtopic 225-20 requires an entity to separately classify, present, and disclose extraordinary events and transactions.

In response to feedback received from users and preparers the FASB issued this ASU to eliminate the concept of extraordinary items. 23 assurance First Quarter 2016 Accounting, Reporting & Auditing Developments . Appendix C - Accounting Standards Affecting Private Companies in 2016 and beyond continued Accounting Standards Update ASU 2014-16: Derivatives and Hedging (Topic 815): Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity (a consensus of the FASB Emerging Issues Task Force) ASU 2014-15: Presentation of Financial Statements—Going Concern (Subtopic 205-40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern ASU 2014-13: Consolidation (Topic 810): Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity Private Company Effective Date Fiscal years beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016 Fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016 Fiscal years ending after December 15, 2016, and interim periods within annual periods beginning after December 15, 2016 Transition Full or Modified Retrospective N/A Full or Modified Retrospective Early Adopt Summary √ Entities frequently raise capital through issuances of shares, which will occasionally include additional features (e.g. conversion rights, dividend payment preferences). When shares are issued with features that qualify as derivatives under GAAP those shares are referred to as hybrid financial instruments. The features within hybrid financial instruments must be evaluated as to whether they are clearly and closely related to the host contract, and if certain criteria are met the derivative would be separated from the underlying share and accounted for under Topic 815-10, Derivatives and Hedging.

The evaluation of whether or not the features are clearly and closely related begins with determining if the host contract is more akin to debt or equity. Currently there is diversity in practice on how this determination is made. This Update clarifies the determination should be made by considering “all stated and implied substantive terms and features of a hybrid financial instrument” (in contrast to evaluating the instrument without consideration of the embedded derivative). √ The continuation of an entity as a going concern is presumed when preparing financial statements (unless liquidation becomes imminent); however, currently there is no guidance in U.S.