Financial Reporting Quick Hits: (P)Lease Help! Understanding and Preparing for the New Lease Standard – February 2016

Dixon Hughes Goodman

Description

views

February 2016

Financial Reporting Quick Hits: (P)Lease Help! Understanding and

Preparing for the New Lease Standard

Ryan Crowe, Partner | Risk Advisory

Sean Prince, Senior Manager | Risk Advisory

Jim Ewart, Director | Forensics & Valuation

In Under a Minute

• The FASB’s new lease standard is scheduled to take effect on January 1, 2019 for public companies. Early adoption is

permitted. At the adoption date, the standard must be applied to the earliest comparative reporting period presented.

• The most significant impact of the new standard is the requirement that lessees account for all leases – both operating

and finance – on the balance sheet, recognizing both an asset for the right to use the leased asset and an obligation to

make lease payments over the lease term.

• The new lease standard retains the notion of “lease classification” – i.e., operating versus finance – and the related income

statement profile for each lease type. The lease classification criteria are substantially the same as those in existing lease

guidance.

• Existing lessor accounting remains largely intact, with certain changes made to the lease classification criteria, leveraged

leases, initial direct costs and real estate leases.

On February 25, 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU)

2016-02, Leases, a new standard that will govern the accounting for lease contracts for public companies beginning

January 1, 2019.1 ASU 2016-02 represents the culmination of the FASB’s decade-long project to improve the accounting

for leases, especially the transparency of a company’s obligations arising from lease contracts.

Assurance | Tax | Advisory | dhgllp.com

.

views While the new lease standard isn’t scheduled to go into effect until 2019, given the pervasiveness of lease financing (e.g., for the use of corporate real estate, vehicles, copiers, etc.) and the substantial impact the accounting changes could have on a company’s financial position and reported results, companies should begin now to understand how the new standard differs from existing guidance and assess how such changes will likely impact their business. the balance sheet (with the exception of certain short-term leases addressed below). Specifically, the new standard requires lessees to recognize on the balance sheet at lease commencement both: This paper discusses some of the key changes to the accounting guidance and implementation issues companies will need to think through as they prepare to adopt the new lease standard.2 • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. • A right-of-use (ROU) asset, representing the lessee’s right to use the leased asset over the term of the lease; and, The lease liability is initially recorded at an amount equal to the present value of the remaining lease payments4 due over the lease term, discounted at the rate implicit in the lease.5 In essence, it is accounted for like any other financial liability (e.g., debt obligation) of the company. Definition of a Lease The new lease standard defines a lease as “a contract … that conveys the right to control the use of identified property, plant, or equipment … for a period of time in exchange for consideration.”3 While this definition is essentially the same as that in existing accounting guidance, the new lease standard provides new detailed guidance companies will use to determine when that definition is met. For a contract to meet the definition of a lease under the new standard, it must meet both of the following criteria: Lease Liability On the other side of the balance sheet, the ROU asset is initially recorded at an amount equal to: • The contract depends on the use of an identified asset. This analysis must consider whether the supplier of the asset holds any substantive substitution rights. • The initial lease liability; plus • Any lease payments commencement; plus • The contract conveys to the lessee the right to control the use of the identified asset, meaning that the lessee has the right to 1) direct how and for what purpose the asset is used and 2) obtain substantially all of the economic benefits from the use of the asset. made at or before lease • Any initial direct costs incurred by the lessee; less • Any lease incentives received from the lessor. Lease Liability Because the new lease standard requires all leases to be accounted for on the balance sheet (see below), the determination as to whether a contract contains a lease takes on much greater significance in the accounting analysis. Furthermore, due to the changes made to the implementation guidance, companies may need to reassess certain arrangements and use judgment in determining whether contracts that were previously accounted for as service arrangements will be treated as a lease under the new standard or vice versa. + ROU Asset = • Lease payments made at or before lease commencement • Initial direct costs - Changes to the Accounting by Lessees All Leases Going on Balance Sheet Lease incentives received from the lessor Perhaps the most significant change arising from the new lease standard is the requirement that lessees recognize all lease contracts – both operating and finance leases – on Assurance | Tax | Advisory | dhgllp.com = Present value of lease payments due over the lease term 2 .

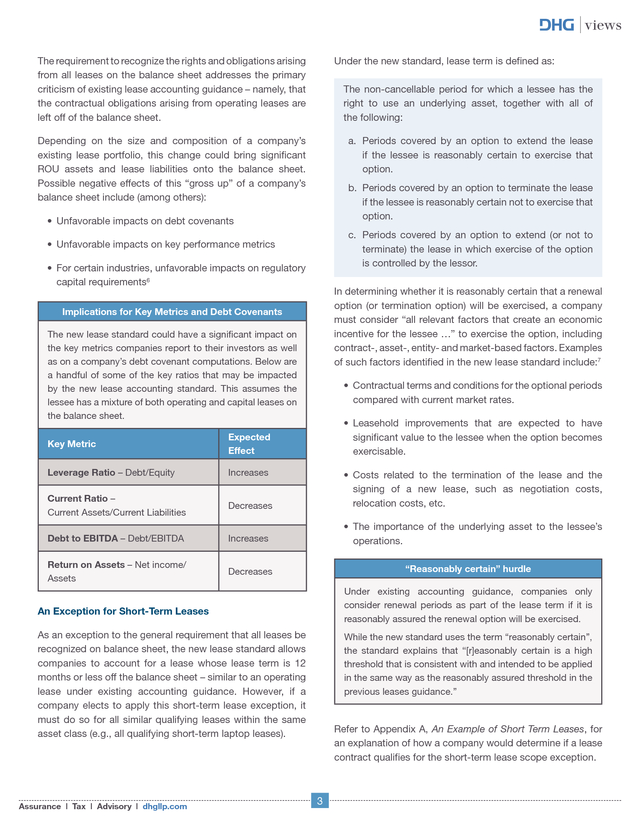

views Under the new standard, lease term is defined as: The requirement to recognize the rights and obligations arising from all leases on the balance sheet addresses the primary criticism of existing lease accounting guidance – namely, that the contractual obligations arising from operating leases are left off of the balance sheet. The non-cancellable period for which a lessee has the right to use an underlying asset, together with all of the following: a. Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option. Depending on the size and composition of a company’s existing lease portfolio, this change could bring significant ROU assets and lease liabilities onto the balance sheet. Possible negative effects of this “gross up” of a company’s balance sheet include (among others): b. Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option. • Unfavorable impacts on debt covenants c. Periods covered by an option to extend (or not to terminate) the lease in which exercise of the option is controlled by the lessor. • Unfavorable impacts on key performance metrics • For certain industries, unfavorable impacts on regulatory capital requirements6 In determining whether it is reasonably certain that a renewal option (or termination option) will be exercised, a company must consider “all relevant factors that create an economic incentive for the lessee …” to exercise the option, including contract-, asset-, entity- and market-based factors. Examples of such factors identified in the new lease standard include:7 Implications for Key Metrics and Debt Covenants The new lease standard could have a significant impact on the key metrics companies report to their investors as well as on a company’s debt covenant computations. Below are a handful of some of the key ratios that may be impacted by the new lease accounting standard. This assumes the lessee has a mixture of both operating and capital leases on the balance sheet. • Contractual terms and conditions for the optional periods compared with current market rates. • Leasehold improvements that are expected to have significant value to the lessee when the option becomes exercisable. Key Metric Expected Effect Leverage Ratio – Debt/Equity Increases Current Ratio – Current Assets/Current Liabilities Decreases • Costs related to the termination of the lease and the signing of a new lease, such as negotiation costs, relocation costs, etc. Debt to EBITDA – Debt/EBITDA Increases • The importance of the underlying asset to the lessee’s operations. Return on Assets – Net income/ Assets Decreases “Reasonably certain” hurdle Under existing accounting guidance, companies only consider renewal periods as part of the lease term if it is reasonably assured the renewal option will be exercised. An Exception for Short-Term Leases As an exception to the general requirement that all leases be recognized on balance sheet, the new lease standard allows companies to account for a lease whose lease term is 12 months or less off the balance sheet – similar to an operating lease under existing accounting guidance.

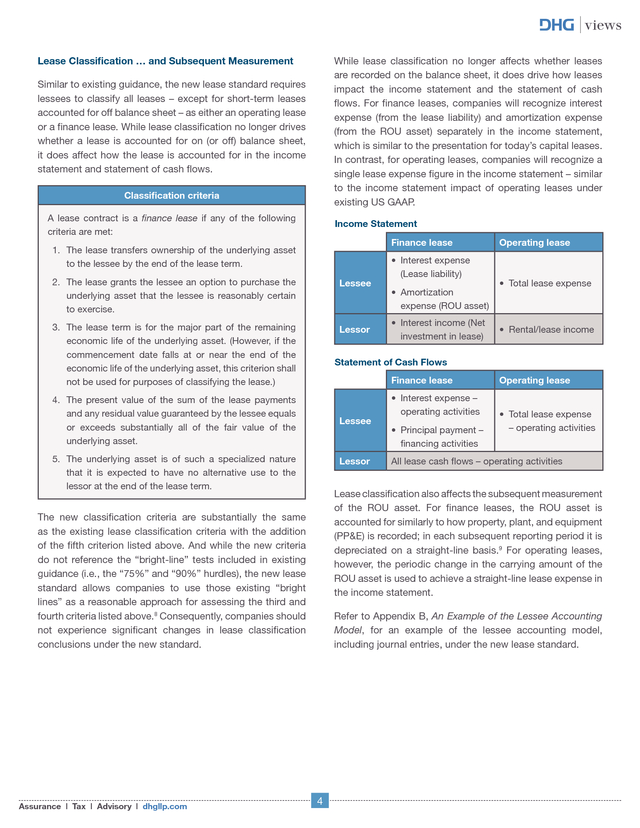

However, if a company elects to apply this short-term lease exception, it must do so for all similar qualifying leases within the same asset class (e.g., all qualifying short-term laptop leases). Assurance | Tax | Advisory | dhgllp.com While the new standard uses the term “reasonably certain”, the standard explains that “[r]easonably certain is a high threshold that is consistent with and intended to be applied in the same way as the reasonably assured threshold in the previous leases guidance.” Refer to Appendix A, An Example of Short Term Leases, for an explanation of how a company would determine if a lease contract qualifies for the short-term lease scope exception. 3 . views Lease Classification … and Subsequent Measurement While lease classification no longer affects whether leases are recorded on the balance sheet, it does drive how leases impact the income statement and the statement of cash flows. For finance leases, companies will recognize interest expense (from the lease liability) and amortization expense (from the ROU asset) separately in the income statement, which is similar to the presentation for today’s capital leases. In contrast, for operating leases, companies will recognize a single lease expense figure in the income statement – similar to the income statement impact of operating leases under existing US GAAP. Similar to existing guidance, the new lease standard requires lessees to classify all leases – except for short-term leases accounted for off balance sheet – as either an operating lease or a finance lease. While lease classification no longer drives whether a lease is accounted for on (or off) balance sheet, it does affect how the lease is accounted for in the income statement and statement of cash flows. Classification criteria A lease contract is a finance lease if any of the following criteria are met: Income Statement Finance lease 1. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. 2. The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. Lessee 3. The lease term is for the major part of the remaining economic life of the underlying asset. (However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease.) Lessor • Amortization expense (ROU asset) • Interest income (Net investment in lease) • Total lease expense • Rental/lease income Statement of Cash Flows Finance lease 4. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. Lessee 5. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. Lessor • Interest expense – operating activities • Principal payment – financing activities Operating lease • Total lease expense – operating activities All lease cash flows – operating activities Lease classification also affects the subsequent measurement of the ROU asset.

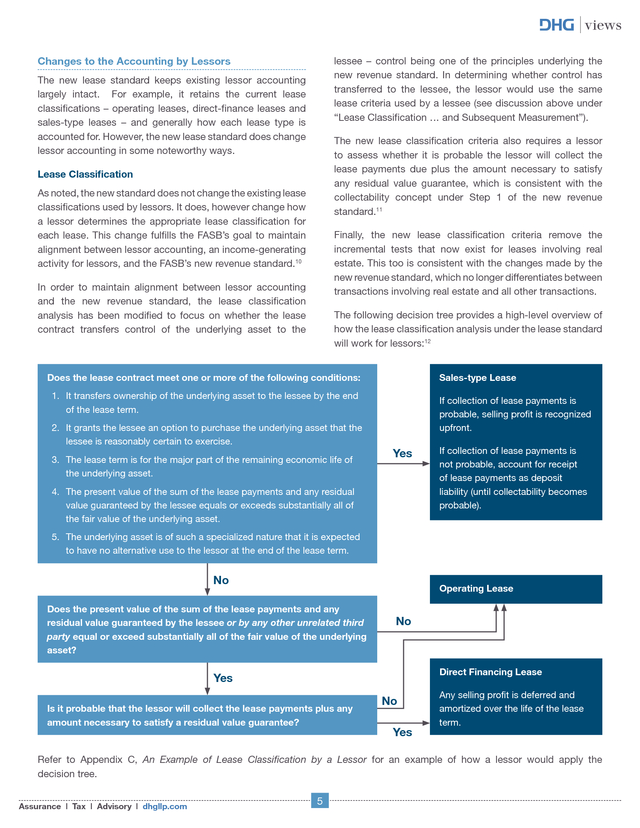

For finance leases, the ROU asset is accounted for similarly to how property, plant, and equipment (PP&E) is recorded; in each subsequent reporting period it is depreciated on a straight-line basis.9 For operating leases, however, the periodic change in the carrying amount of the ROU asset is used to achieve a straight-line lease expense in the income statement. The new classification criteria are substantially the same as the existing lease classification criteria with the addition of the fifth criterion listed above. And while the new criteria do not reference the “bright-line” tests included in existing guidance (i.e., the “75%” and “90%” hurdles), the new lease standard allows companies to use those existing “bright lines” as a reasonable approach for assessing the third and fourth criteria listed above.8 Consequently, companies should not experience significant changes in lease classification conclusions under the new standard. Assurance | Tax | Advisory | dhgllp.com • Interest expense (Lease liability) Operating lease Refer to Appendix B, An Example of the Lessee Accounting Model, for an example of the lessee accounting model, including journal entries, under the new lease standard. 4 . views Changes to the Accounting by Lessors lessee – control being one of the principles underlying the new revenue standard. In determining whether control has transferred to the lessee, the lessor would use the same lease criteria used by a lessee (see discussion above under “Lease Classification … and Subsequent Measurement”). The new lease standard keeps existing lessor accounting largely intact. For example, it retains the current lease classifications – operating leases, direct-finance leases and sales-type leases – and generally how each lease type is accounted for. However, the new lease standard does change lessor accounting in some noteworthy ways. The new lease classification criteria also requires a lessor to assess whether it is probable the lessor will collect the lease payments due plus the amount necessary to satisfy any residual value guarantee, which is consistent with the collectability concept under Step 1 of the new revenue standard.11 Lease Classification As noted, the new standard does not change the existing lease classifications used by lessors.

It does, however change how a lessor determines the appropriate lease classification for each lease. This change fulfills the FASB’s goal to maintain alignment between lessor accounting, an income-generating activity for lessors, and the FASB’s new revenue standard.10 Finally, the new lease classification criteria remove the incremental tests that now exist for leases involving real estate. This too is consistent with the changes made by the new revenue standard, which no longer differentiates between transactions involving real estate and all other transactions. In order to maintain alignment between lessor accounting and the new revenue standard, the lease classification analysis has been modified to focus on whether the lease contract transfers control of the underlying asset to the The following decision tree provides a high-level overview of how the lease classification analysis under the lease standard will work for lessors:12 Does the lease contract meet one or more of the following conditions: Sales-type Lease 1. It transfers ownership of the underlying asset to the lessee by the end of the lease term. 2. It grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. 3. The lease term is for the major part of the remaining economic life of the underlying asset. If collection of lease payments is probable, selling profit is recognized upfront. Yes 4. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. If collection of lease payments is not probable, account for receipt of lease payments as deposit liability (until collectability becomes probable). 5. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. No Operating Lease Does the present value of the sum of the lease payments and any residual value guaranteed by the lessee or by any other unrelated third party equal or exceed substantially all of the fair value of the underlying asset? No Direct Financing Lease Yes Is it probable that the lessor will collect the lease payments plus any amount necessary to satisfy a residual value guarantee? No Yes Any selling profit is deferred and amortized over the life of the lease term. Refer to Appendix C, An Example of Lease Classification by a Lessor for an example of how a lessor would apply the decision tree. Assurance | Tax | Advisory | dhgllp.com 5 .

views Leveraged Leases need to ensure they have an adequate process in place for appropriately identifying lease and non-lease components (e.g., common area maintenance, supply of utilities). However, as a practical expedient, the new lease standard allows lessees to elect – by class of underlying asset – to account for lease and non-lease components as a single lease component. Another change to existing lessor accounting is the FASB’s decision to eliminate the concept of a leveraged lease. Under existing accounting guidance, if certain criteria are met, a lessor can account for its lease investment on the face of the balance sheet net of the debt used to finance the leased asset. In the basis for conclusions of the new lease standard the FASB explains its reasoning for eliminating leveraged leases: Initial Direct Costs The new lease standard also redefines which types of expenditures qualify as initial direct costs. Under the new standard, only those costs that would not have been incurred if the lease had not been obtained (i.e., similar to the notion of incremental costs in the new revenue standard) qualify. As a result, costs incurred before a lease is executed (e.g., legal fees) as well as allocated costs (e.g., the portion of an employee’s salary) no longer qualify as initial direct costs. One reason is because leveraged lease accounting provides net presentation and some Board members do not agree with allowing a net presentation for only a subset of certain lease transactions.

Another reason is to limit some of the complexity in the lease accounting guidance by eliminating the unique accounting for leveraged leases. Sale-Leaseback Transactions The new lease standard does, however, grandfather in existing leveraged leases. Leveraged leases existing as of the date of adoption would continue to be accounted for under existing guidance for leveraged leases. This eliminates the complexities in unwinding the accounting for leveraged leases upon adoption. While the new lease standard retains the notion of a saleleaseback transaction, it modifies how the lessee and lessor determine the appropriate accounting for such a transaction. Under the new standard, the seller-lessee first assesses whether the transfer of the underlying asset to the buyerlessor qualifies as a sale under the new revenue standard. This analysis focuses on whether the buyer-lessor has obtained control over the asset.

The new lease standard clarifies that the leaseback arrangement does not preclude the buyer-lessor from obtaining control unless the lease is determined to be a finance lease. Additional Changes Impacting both Lessees and Lessors Separation of Lease and Non-Lease Components The requirement to identify and separately account for lease and non-lease components is not new. However, under the new lease standard, the requirement takes on greater importance because lease components are now accounted for on the balance sheet whereas non-lease components are generally accounted for off balance sheet. If the transfer does not qualify as a sale, the transaction is accounted for as a financing arrangement. The seller-lessee continues to record the underlying asset on its balance sheet and recognizes a liability for any proceeds received from the buyer-lessor. In contrast, if the transfer qualifies as a sale, then the sellerlessee derecognizes the underlying asset, recognizes a gain on sale and accounts for the leaseback in accordance with the new lease standard (i.e., based on an assessment of whether control of the asset has been transferred). In addition, because the new lease standard modifies the interpretive guidance surrounding the definition of a lease and provides incremental guidance on how to identify and separate lease and non-lease components, companies Assurance | Tax | Advisory | dhgllp.com 6 .

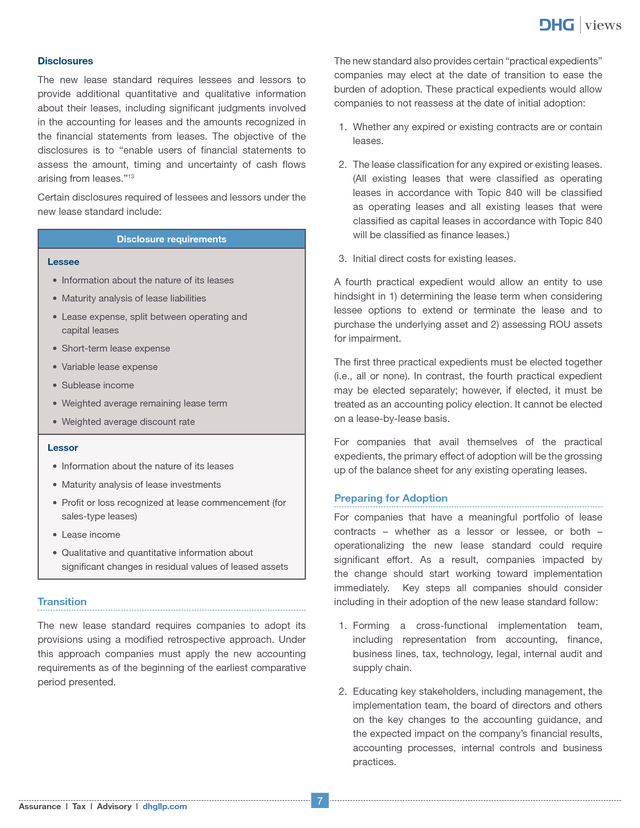

views Disclosures The new standard also provides certain “practical expedients” companies may elect at the date of transition to ease the burden of adoption. These practical expedients would allow companies to not reassess at the date of initial adoption: The new lease standard requires lessees and lessors to provide additional quantitative and qualitative information about their leases, including significant judgments involved in the accounting for leases and the amounts recognized in the financial statements from leases. The objective of the disclosures is to “enable users of financial statements to assess the amount, timing and uncertainty of cash flows arising from leases.”13 1. Whether any expired or existing contracts are or contain leases. 2. The lease classification for any expired or existing leases. (All existing leases that were classified as operating leases in accordance with Topic 840 will be classified as operating leases and all existing leases that were classified as capital leases in accordance with Topic 840 will be classified as finance leases.) Certain disclosures required of lessees and lessors under the new lease standard include: Disclosure requirements 3. Initial direct costs for existing leases. Lessee • Information about the nature of its leases A fourth practical expedient would allow an entity to use hindsight in 1) determining the lease term when considering lessee options to extend or terminate the lease and to purchase the underlying asset and 2) assessing ROU assets for impairment. • Maturity analysis of lease liabilities • Lease expense, split between operating and capital leases • Short-term lease expense The first three practical expedients must be elected together (i.e., all or none). In contrast, the fourth practical expedient may be elected separately; however, if elected, it must be treated as an accounting policy election.

It cannot be elected on a lease-by-lease basis. • Variable lease expense • Sublease income • Weighted average remaining lease term • Weighted average discount rate For companies that avail themselves of the practical expedients, the primary effect of adoption will be the grossing up of the balance sheet for any existing operating leases. Lessor • Information about the nature of its leases • Maturity analysis of lease investments Preparing for Adoption • Profit or loss recognized at lease commencement (for sales-type leases) For companies that have a meaningful portfolio of lease contracts – whether as a lessor or lessee, or both – operationalizing the new lease standard could require significant effort. As a result, companies impacted by the change should start working toward implementation immediately. Key steps all companies should consider including in their adoption of the new lease standard follow: • Lease income • Qualitative and quantitative information about significant changes in residual values of leased assets Transition The new lease standard requires companies to adopt its provisions using a modified retrospective approach.

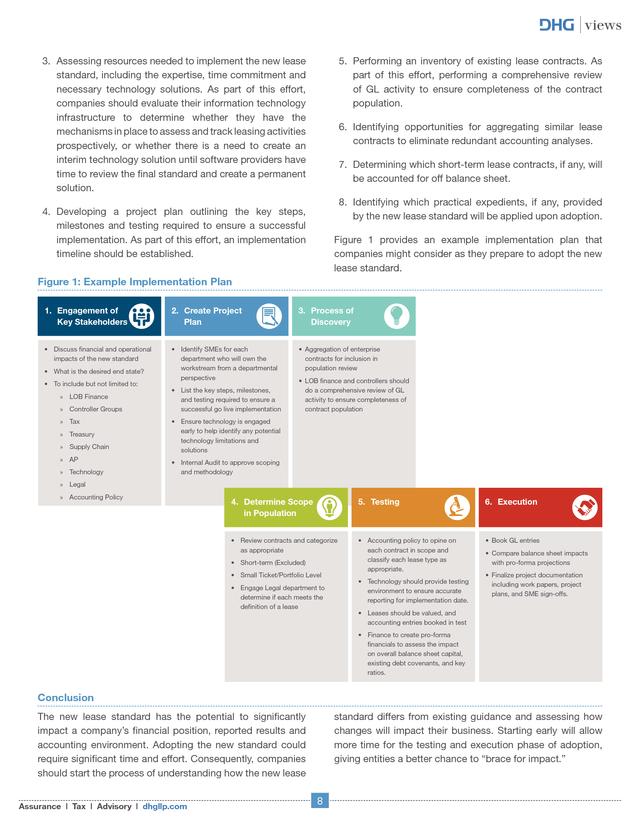

Under this approach companies must apply the new accounting requirements as of the beginning of the earliest comparative period presented. Assurance | Tax | Advisory | dhgllp.com 1. Forming a cross-functional implementation team, including representation from accounting, finance, business lines, tax, technology, legal, internal audit and supply chain. 2. Educating key stakeholders, including management, the implementation team, the board of directors and others on the key changes to the accounting guidance, and the expected impact on the company’s financial results, accounting processes, internal controls and business practices. 7 . views 5. Performing an inventory of existing lease contracts. As part of this effort, performing a comprehensive review of GL activity to ensure completeness of the contract population. 3. Assessing resources needed to implement the new lease standard, including the expertise, time commitment and necessary technology solutions. As part of this effort, companies should evaluate their information technology infrastructure to determine whether they have the mechanisms in place to assess and track leasing activities prospectively, or whether there is a need to create an interim technology solution until software providers have time to review the final standard and create a permanent solution. 6. Identifying opportunities for aggregating similar lease contracts to eliminate redundant accounting analyses. 7. Determining which short-term lease contracts, if any, will be accounted for off balance sheet. 8. Identifying which practical expedients, if any, provided by the new lease standard will be applied upon adoption. 4. Developing a project plan outlining the key steps, milestones and testing required to ensure a successful implementation. As part of this effort, an implementation timeline should be established. Figure 1 provides an example implementation plan that companies might consider as they prepare to adopt the new lease standard. Figure 1: Example Implementation Plan 1. Engagement of Key Stakeholders 2. Create Project Plan 3. Process of Discovery • Discuss financial and operational impacts of the new standard • Identify SMEs for each department who will own the workstream from a departmental perspective • Aggregation of enterprise contracts for inclusion in population review • What is the desired end state? • To include but not limited to: »» LOB Finance »» Controller Groups »» Tax »» Treasury »» Supply Chain »» AP »» Technology • List the key steps, milestones, and testing required to ensure a successful go live implementation • LOB finance and controllers should do a comprehensive review of GL activity to ensure completeness of contract population • Ensure technology is engaged early to help identify any potential technology limitations and solutions • Internal Audit to approve scoping and methodology »» Legal »» Accounting Policy 4. Determine Scope in Population 5. Testing 6. Execution • Review contracts and categorize as appropriate • Accounting policy to opine on each contract in scope and classify each lease type as appropriate. • Book GL entries • Short-term (Excluded) • Small Ticket/Portfolio Level • Engage Legal department to determine if each meets the definition of a lease • Technology should provide testing environment to ensure accurate reporting for implementation date. • Compare balance sheet impacts with pro-forma projections • Finalize project documentation including work papers, project plans, and SME sign-offs. • Leases should be valued, and accounting entries booked in test • Finance to create pro-forma financials to assess the impact on overall balance sheet capital, existing debt covenants, and key ratios. Conclusion The new lease standard has the potential to significantly impact a company’s financial position, reported results and accounting environment.

Adopting the new standard could require significant time and effort. Consequently, companies should start the process of understanding how the new lease Assurance | Tax | Advisory | dhgllp.com standard differs from existing guidance and assessing how changes will impact their business. Starting early will allow more time for the testing and execution phase of adoption, giving entities a better chance to “brace for impact.” 8 .

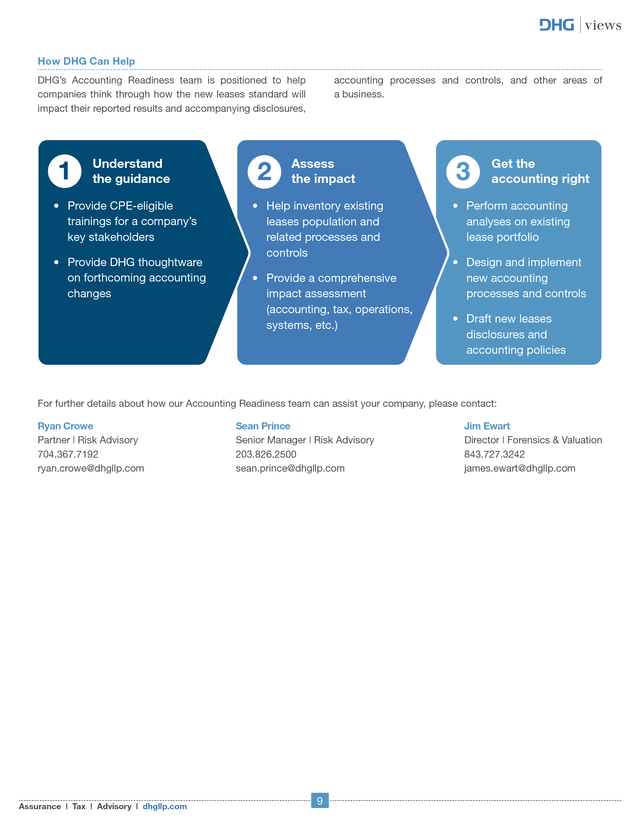

views How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies think through how the new leases standard will impact their reported results and accompanying disclosures, Understand the guidance • Provide CPE-eligible trainings for a company’s key stakeholders • Provide DHG thoughtware on forthcoming accounting changes accounting processes and controls, and other areas of a business. Assess the impact • Help inventory existing leases population and related processes and controls • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) Get the accounting right • Perform accounting analyses on existing lease portfolio • Design and implement new accounting processes and controls • Draft new leases disclosures and accounting policies For further details about how our Accounting Readiness team can assist your company, please contact: Ryan Crowe Partner | Risk Advisory 704.367.7192 ryan.crowe@dhgllp.com Assurance | Tax | Advisory | dhgllp.com Sean Prince Senior Manager | Risk Advisory 203.826.2500 sean.prince@dhgllp.com 9 Jim Ewart Director | Forensics & Valuation 843.727.3242 james.ewart@dhgllp.com . views APPENDIX A | An Example of Short-Term Leases This appendix provides an example of how a company would analyze a lease to determine if it qualifies for the new short-term lease scope exception. EXAMPLE Conclusion: Facts: • Based on a review of the relevant factors that create an economic incentive (e.g., the leasehold improvements involved, the material tax incentive being offered, and the importance of the building to Darling’s operations), Darling Widgets concludes it is reasonably certain that it will exercise the renewal option. As a result the lease does not qualify as a short-term lease because the lease term exceeds 12 months. • Darling Widgets enters into a lease agreement with RE Rental, Inc. to lease a building for an initial period of 12 months. • At the end of 12 months Darling Widgets has the option to renew the lease contract for an additional 36-month period. • Darling Widgets intends to use the building for the location of its new corporate headquarters, which will require the installation of significant leasehold improvements. • Had it not been for the factors noted above that make it reasonably certain Darling Widgets will exercise the renewal option, the company would have been able to elect the short-term lease scope exception because, in this case, the non-cancelable period of the lease is for only 12 months. • Additionally, Darling Widgets has been offered a material tax incentive from the local government for relocating its headquarters. However, to receive the tax incentive, the company must remain in the locality for at least two years.

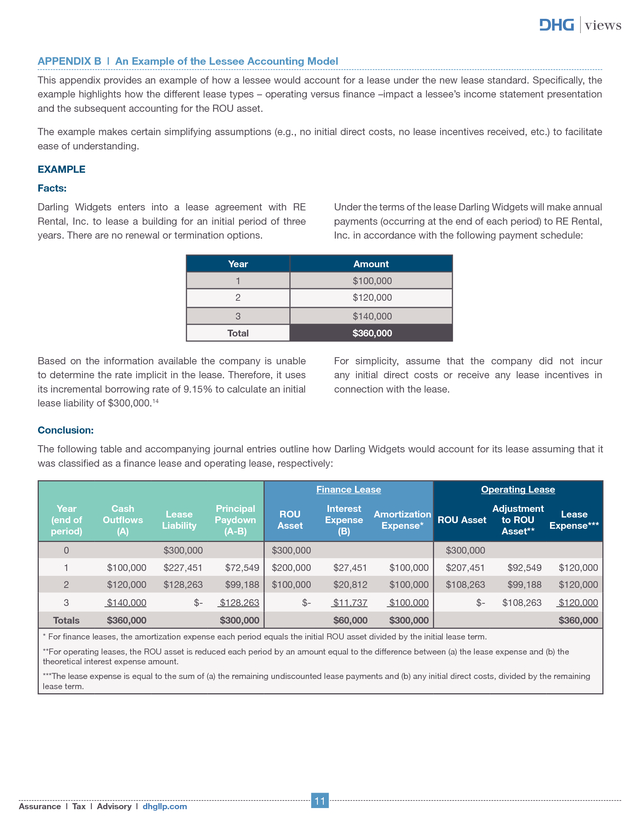

Darling Widgets intends to meet that requirement. Assurance | Tax | Advisory | dhgllp.com 10 . views APPENDIX B | An Example of the Lessee Accounting Model This appendix provides an example of how a lessee would account for a lease under the new lease standard. Specifically, the example highlights how the different lease types – operating versus finance –impact a lessee’s income statement presentation and the subsequent accounting for the ROU asset. The example makes certain simplifying assumptions (e.g., no initial direct costs, no lease incentives received, etc.) to facilitate ease of understanding. EXAMPLE Facts: Darling Widgets enters into a lease agreement with RE Rental, Inc. to lease a building for an initial period of three years. There are no renewal or termination options. Under the terms of the lease Darling Widgets will make annual payments (occurring at the end of each period) to RE Rental, Inc.

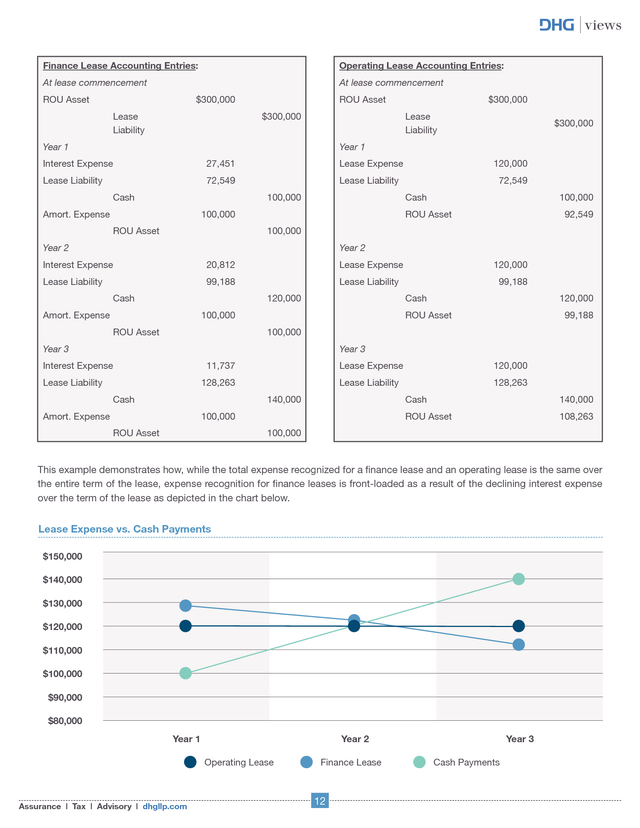

in accordance with the following payment schedule: Year Amount 1 $100,000 2 $120,000 3 $140,000 Total $360,000 Based on the information available the company is unable to determine the rate implicit in the lease. Therefore, it uses its incremental borrowing rate of 9.15% to calculate an initial lease liability of $300,000.14 For simplicity, assume that the company did not incur any initial direct costs or receive any lease incentives in connection with the lease. Conclusion: The following table and accompanying journal entries outline how Darling Widgets would account for its lease assuming that it was classified as a finance lease and operating lease, respectively: Finance Lease Year (end of period) Cash Outflows (A) 0 Lease Liability Principal Paydown (A-B) $300,000 ROU Asset Interest Expense (B) Operating Lease Amortization ROU Asset Expense* $300,000 Adjustment Lease to ROU Expense*** Asset** $300,000 1 $100,000 $227,451 $72,549 $200,000 $27,451 $100,000 $207,451 $92,549 $120,000 2 $120,000 $128,263 $99,188 $100,000 $20,812 $100,000 $108,263 $99,188 $120,000 3 $140,000 $- $128,263 $- $11,737 $100,000 $- $108,263 $120,000 Totals $360,000 $60,000 $300,000 $300,000 $360,000 * For finance leases, the amortization expense each period equals the initial ROU asset divided by the initial lease term. **For operating leases, the ROU asset is reduced each period by an amount equal to the difference between (a) the lease expense and (b) the theoretical interest expense amount. ***The lease expense is equal to the sum of (a) the remaining undiscounted lease payments and (b) any initial direct costs, divided by the remaining lease term. Assurance | Tax | Advisory | dhgllp.com 11 . views Finance Lease Accounting Entries: Operating Lease Accounting Entries: At lease commencement At lease commencement ROU Asset $300,000 Lease Liability ROU Asset $300,000 $300,000 Lease Liability Year 1 $300,000 Year 1 Interest Expense 27,451 Lease Expense 120,000 Lease Liability 72,549 Lease Liability 72,549 Cash Cash 100,000 Amort. Expense 100,000 ROU Asset 100,000 ROU Asset 92,549 100,000 Year 2 Year 2 Interest Expense 20,812 Lease Expense 120,000 Lease Liability 99,188 Lease Liability 99,188 Cash Cash 120,000 Amort. Expense ROU Asset 100,000 ROU Asset 120,000 99,188 100,000 Year 3 Year 3 Interest Expense 11,737 120,000 128,263 Lease Liability Lease Expense Lease Liability 128,263 Cash Cash Amort. Expense 100,000 ROU Asset 140,000 ROU Asset 140,000 108,263 100,000 This example demonstrates how, while the total expense recognized for a finance lease and an operating lease is the same over the entire term of the lease, expense recognition for finance leases is front-loaded as a result of the declining interest expense over the term of the lease as depicted in the chart below. Lease Expense vs.

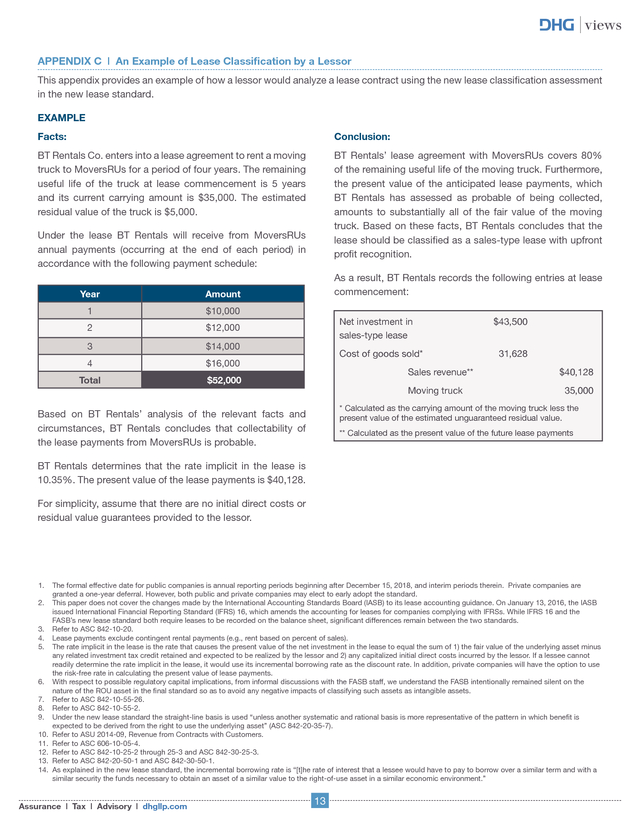

Cash Payments $150,000 $140,000 $130,000 $120,000 $110,000 $100,000 $90,000 $80,000 Year 1 Year 2 Operating Lease Assurance | Tax | Advisory | dhgllp.com Finance Lease 12 Year 3 Cash Payments . views APPENDIX C | An Example of Lease Classification by a Lessor This appendix provides an example of how a lessor would analyze a lease contract using the new lease classification assessment in the new lease standard. EXAMPLE Facts: Conclusion: BT Rentals Co. enters into a lease agreement to rent a moving truck to MoversRUs for a period of four years. The remaining useful life of the truck at lease commencement is 5 years and its current carrying amount is $35,000. The estimated residual value of the truck is $5,000. BT Rentals’ lease agreement with MoversRUs covers 80% of the remaining useful life of the moving truck.

Furthermore, the present value of the anticipated lease payments, which BT Rentals has assessed as probable of being collected, amounts to substantially all of the fair value of the moving truck. Based on these facts, BT Rentals concludes that the lease should be classified as a sales-type lease with upfront profit recognition. Under the lease BT Rentals will receive from MoversRUs annual payments (occurring at the end of each period) in accordance with the following payment schedule: Year Amount 1 $10,000 2 $12,000 3 $14,000 4 $16,000 Total As a result, BT Rentals records the following entries at lease commencement: $52,000 Net investment in sales-type lease Cost of goods sold* Sales revenue** Moving truck $43,500 31,628 $40,128 35,000 * Calculated as the carrying amount of the moving truck less the present value of the estimated unguaranteed residual value. Based on BT Rentals’ analysis of the relevant facts and circumstances, BT Rentals concludes that collectability of the lease payments from MoversRUs is probable. ** Calculated as the present value of the future lease payments BT Rentals determines that the rate implicit in the lease is 10.35%. The present value of the lease payments is $40,128. For simplicity, assume that there are no initial direct costs or residual value guarantees provided to the lessor. 1. The formal effective date for public companies is annual reporting periods beginning after December 15, 2018, and interim periods therein.

Private companies are granted a one-year deferral. However, both public and private companies may elect to early adopt the standard. 2. This paper does not cover the changes made by the International Accounting Standards Board (IASB) to its lease accounting guidance. On January 13, 2016, the IASB issued International Financial Reporting Standard (IFRS) 16, which amends the accounting for leases for companies complying with IFRSs.

While IFRS 16 and the FASB’s new lease standard both require leases to be recorded on the balance sheet, significant differences remain between the two standards. 3. Refer to ASC 842-10-20. 4. Lease payments exclude contingent rental payments (e.g., rent based on percent of sales). 5. The rate implicit in the lease is the rate that causes the present value of the net investment in the lease to equal the sum of 1) the fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and 2) any capitalized initial direct costs incurred by the lessor. If a lessee cannot readily determine the rate implicit in the lease, it would use its incremental borrowing rate as the discount rate. In addition, private companies will have the option to use the risk-free rate in calculating the present value of lease payments. 6. With respect to possible regulatory capital implications, from informal discussions with the FASB staff, we understand the FASB intentionally remained silent on the nature of the ROU asset in the final standard so as to avoid any negative impacts of classifying such assets as intangible assets. 7. Refer to ASC 842-10-55-26. 8. Refer to ASC 842-10-55-2. 9. Under the new lease standard the straight-line basis is used “unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived from the right to use the underlying asset” (ASC 842-20-35-7). 10. Refer to ASU 2014-09, Revenue from Contracts with Customers. 11. Refer to ASC 606-10-05-4. 12. Refer to ASC 842-10-25-2 through 25-3 and ASC 842-30-25-3. 13. Refer to ASC 842-20-50-1 and ASC 842-30-50-1. 14. As explained in the new lease standard, the incremental borrowing rate is “[t]he rate of interest that a lessee would have to pay to borrow over a similar term and with a similar security the funds necessary to obtain an asset of a similar value to the right-of-use asset in a similar economic environment.” Assurance | Tax | Advisory | dhgllp.com 13 .

views While the new lease standard isn’t scheduled to go into effect until 2019, given the pervasiveness of lease financing (e.g., for the use of corporate real estate, vehicles, copiers, etc.) and the substantial impact the accounting changes could have on a company’s financial position and reported results, companies should begin now to understand how the new standard differs from existing guidance and assess how such changes will likely impact their business. the balance sheet (with the exception of certain short-term leases addressed below). Specifically, the new standard requires lessees to recognize on the balance sheet at lease commencement both: This paper discusses some of the key changes to the accounting guidance and implementation issues companies will need to think through as they prepare to adopt the new lease standard.2 • A lease liability, representing the lessee’s contractual obligation to make lease payments over the term of the lease. • A right-of-use (ROU) asset, representing the lessee’s right to use the leased asset over the term of the lease; and, The lease liability is initially recorded at an amount equal to the present value of the remaining lease payments4 due over the lease term, discounted at the rate implicit in the lease.5 In essence, it is accounted for like any other financial liability (e.g., debt obligation) of the company. Definition of a Lease The new lease standard defines a lease as “a contract … that conveys the right to control the use of identified property, plant, or equipment … for a period of time in exchange for consideration.”3 While this definition is essentially the same as that in existing accounting guidance, the new lease standard provides new detailed guidance companies will use to determine when that definition is met. For a contract to meet the definition of a lease under the new standard, it must meet both of the following criteria: Lease Liability On the other side of the balance sheet, the ROU asset is initially recorded at an amount equal to: • The contract depends on the use of an identified asset. This analysis must consider whether the supplier of the asset holds any substantive substitution rights. • The initial lease liability; plus • Any lease payments commencement; plus • The contract conveys to the lessee the right to control the use of the identified asset, meaning that the lessee has the right to 1) direct how and for what purpose the asset is used and 2) obtain substantially all of the economic benefits from the use of the asset. made at or before lease • Any initial direct costs incurred by the lessee; less • Any lease incentives received from the lessor. Lease Liability Because the new lease standard requires all leases to be accounted for on the balance sheet (see below), the determination as to whether a contract contains a lease takes on much greater significance in the accounting analysis. Furthermore, due to the changes made to the implementation guidance, companies may need to reassess certain arrangements and use judgment in determining whether contracts that were previously accounted for as service arrangements will be treated as a lease under the new standard or vice versa. + ROU Asset = • Lease payments made at or before lease commencement • Initial direct costs - Changes to the Accounting by Lessees All Leases Going on Balance Sheet Lease incentives received from the lessor Perhaps the most significant change arising from the new lease standard is the requirement that lessees recognize all lease contracts – both operating and finance leases – on Assurance | Tax | Advisory | dhgllp.com = Present value of lease payments due over the lease term 2 .

views Under the new standard, lease term is defined as: The requirement to recognize the rights and obligations arising from all leases on the balance sheet addresses the primary criticism of existing lease accounting guidance – namely, that the contractual obligations arising from operating leases are left off of the balance sheet. The non-cancellable period for which a lessee has the right to use an underlying asset, together with all of the following: a. Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option. Depending on the size and composition of a company’s existing lease portfolio, this change could bring significant ROU assets and lease liabilities onto the balance sheet. Possible negative effects of this “gross up” of a company’s balance sheet include (among others): b. Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option. • Unfavorable impacts on debt covenants c. Periods covered by an option to extend (or not to terminate) the lease in which exercise of the option is controlled by the lessor. • Unfavorable impacts on key performance metrics • For certain industries, unfavorable impacts on regulatory capital requirements6 In determining whether it is reasonably certain that a renewal option (or termination option) will be exercised, a company must consider “all relevant factors that create an economic incentive for the lessee …” to exercise the option, including contract-, asset-, entity- and market-based factors. Examples of such factors identified in the new lease standard include:7 Implications for Key Metrics and Debt Covenants The new lease standard could have a significant impact on the key metrics companies report to their investors as well as on a company’s debt covenant computations. Below are a handful of some of the key ratios that may be impacted by the new lease accounting standard. This assumes the lessee has a mixture of both operating and capital leases on the balance sheet. • Contractual terms and conditions for the optional periods compared with current market rates. • Leasehold improvements that are expected to have significant value to the lessee when the option becomes exercisable. Key Metric Expected Effect Leverage Ratio – Debt/Equity Increases Current Ratio – Current Assets/Current Liabilities Decreases • Costs related to the termination of the lease and the signing of a new lease, such as negotiation costs, relocation costs, etc. Debt to EBITDA – Debt/EBITDA Increases • The importance of the underlying asset to the lessee’s operations. Return on Assets – Net income/ Assets Decreases “Reasonably certain” hurdle Under existing accounting guidance, companies only consider renewal periods as part of the lease term if it is reasonably assured the renewal option will be exercised. An Exception for Short-Term Leases As an exception to the general requirement that all leases be recognized on balance sheet, the new lease standard allows companies to account for a lease whose lease term is 12 months or less off the balance sheet – similar to an operating lease under existing accounting guidance.

However, if a company elects to apply this short-term lease exception, it must do so for all similar qualifying leases within the same asset class (e.g., all qualifying short-term laptop leases). Assurance | Tax | Advisory | dhgllp.com While the new standard uses the term “reasonably certain”, the standard explains that “[r]easonably certain is a high threshold that is consistent with and intended to be applied in the same way as the reasonably assured threshold in the previous leases guidance.” Refer to Appendix A, An Example of Short Term Leases, for an explanation of how a company would determine if a lease contract qualifies for the short-term lease scope exception. 3 . views Lease Classification … and Subsequent Measurement While lease classification no longer affects whether leases are recorded on the balance sheet, it does drive how leases impact the income statement and the statement of cash flows. For finance leases, companies will recognize interest expense (from the lease liability) and amortization expense (from the ROU asset) separately in the income statement, which is similar to the presentation for today’s capital leases. In contrast, for operating leases, companies will recognize a single lease expense figure in the income statement – similar to the income statement impact of operating leases under existing US GAAP. Similar to existing guidance, the new lease standard requires lessees to classify all leases – except for short-term leases accounted for off balance sheet – as either an operating lease or a finance lease. While lease classification no longer drives whether a lease is accounted for on (or off) balance sheet, it does affect how the lease is accounted for in the income statement and statement of cash flows. Classification criteria A lease contract is a finance lease if any of the following criteria are met: Income Statement Finance lease 1. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. 2. The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. Lessee 3. The lease term is for the major part of the remaining economic life of the underlying asset. (However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease.) Lessor • Amortization expense (ROU asset) • Interest income (Net investment in lease) • Total lease expense • Rental/lease income Statement of Cash Flows Finance lease 4. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. Lessee 5. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. Lessor • Interest expense – operating activities • Principal payment – financing activities Operating lease • Total lease expense – operating activities All lease cash flows – operating activities Lease classification also affects the subsequent measurement of the ROU asset.

For finance leases, the ROU asset is accounted for similarly to how property, plant, and equipment (PP&E) is recorded; in each subsequent reporting period it is depreciated on a straight-line basis.9 For operating leases, however, the periodic change in the carrying amount of the ROU asset is used to achieve a straight-line lease expense in the income statement. The new classification criteria are substantially the same as the existing lease classification criteria with the addition of the fifth criterion listed above. And while the new criteria do not reference the “bright-line” tests included in existing guidance (i.e., the “75%” and “90%” hurdles), the new lease standard allows companies to use those existing “bright lines” as a reasonable approach for assessing the third and fourth criteria listed above.8 Consequently, companies should not experience significant changes in lease classification conclusions under the new standard. Assurance | Tax | Advisory | dhgllp.com • Interest expense (Lease liability) Operating lease Refer to Appendix B, An Example of the Lessee Accounting Model, for an example of the lessee accounting model, including journal entries, under the new lease standard. 4 . views Changes to the Accounting by Lessors lessee – control being one of the principles underlying the new revenue standard. In determining whether control has transferred to the lessee, the lessor would use the same lease criteria used by a lessee (see discussion above under “Lease Classification … and Subsequent Measurement”). The new lease standard keeps existing lessor accounting largely intact. For example, it retains the current lease classifications – operating leases, direct-finance leases and sales-type leases – and generally how each lease type is accounted for. However, the new lease standard does change lessor accounting in some noteworthy ways. The new lease classification criteria also requires a lessor to assess whether it is probable the lessor will collect the lease payments due plus the amount necessary to satisfy any residual value guarantee, which is consistent with the collectability concept under Step 1 of the new revenue standard.11 Lease Classification As noted, the new standard does not change the existing lease classifications used by lessors.

It does, however change how a lessor determines the appropriate lease classification for each lease. This change fulfills the FASB’s goal to maintain alignment between lessor accounting, an income-generating activity for lessors, and the FASB’s new revenue standard.10 Finally, the new lease classification criteria remove the incremental tests that now exist for leases involving real estate. This too is consistent with the changes made by the new revenue standard, which no longer differentiates between transactions involving real estate and all other transactions. In order to maintain alignment between lessor accounting and the new revenue standard, the lease classification analysis has been modified to focus on whether the lease contract transfers control of the underlying asset to the The following decision tree provides a high-level overview of how the lease classification analysis under the lease standard will work for lessors:12 Does the lease contract meet one or more of the following conditions: Sales-type Lease 1. It transfers ownership of the underlying asset to the lessee by the end of the lease term. 2. It grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise. 3. The lease term is for the major part of the remaining economic life of the underlying asset. If collection of lease payments is probable, selling profit is recognized upfront. Yes 4. The present value of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the fair value of the underlying asset. If collection of lease payments is not probable, account for receipt of lease payments as deposit liability (until collectability becomes probable). 5. The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term. No Operating Lease Does the present value of the sum of the lease payments and any residual value guaranteed by the lessee or by any other unrelated third party equal or exceed substantially all of the fair value of the underlying asset? No Direct Financing Lease Yes Is it probable that the lessor will collect the lease payments plus any amount necessary to satisfy a residual value guarantee? No Yes Any selling profit is deferred and amortized over the life of the lease term. Refer to Appendix C, An Example of Lease Classification by a Lessor for an example of how a lessor would apply the decision tree. Assurance | Tax | Advisory | dhgllp.com 5 .

views Leveraged Leases need to ensure they have an adequate process in place for appropriately identifying lease and non-lease components (e.g., common area maintenance, supply of utilities). However, as a practical expedient, the new lease standard allows lessees to elect – by class of underlying asset – to account for lease and non-lease components as a single lease component. Another change to existing lessor accounting is the FASB’s decision to eliminate the concept of a leveraged lease. Under existing accounting guidance, if certain criteria are met, a lessor can account for its lease investment on the face of the balance sheet net of the debt used to finance the leased asset. In the basis for conclusions of the new lease standard the FASB explains its reasoning for eliminating leveraged leases: Initial Direct Costs The new lease standard also redefines which types of expenditures qualify as initial direct costs. Under the new standard, only those costs that would not have been incurred if the lease had not been obtained (i.e., similar to the notion of incremental costs in the new revenue standard) qualify. As a result, costs incurred before a lease is executed (e.g., legal fees) as well as allocated costs (e.g., the portion of an employee’s salary) no longer qualify as initial direct costs. One reason is because leveraged lease accounting provides net presentation and some Board members do not agree with allowing a net presentation for only a subset of certain lease transactions.

Another reason is to limit some of the complexity in the lease accounting guidance by eliminating the unique accounting for leveraged leases. Sale-Leaseback Transactions The new lease standard does, however, grandfather in existing leveraged leases. Leveraged leases existing as of the date of adoption would continue to be accounted for under existing guidance for leveraged leases. This eliminates the complexities in unwinding the accounting for leveraged leases upon adoption. While the new lease standard retains the notion of a saleleaseback transaction, it modifies how the lessee and lessor determine the appropriate accounting for such a transaction. Under the new standard, the seller-lessee first assesses whether the transfer of the underlying asset to the buyerlessor qualifies as a sale under the new revenue standard. This analysis focuses on whether the buyer-lessor has obtained control over the asset.

The new lease standard clarifies that the leaseback arrangement does not preclude the buyer-lessor from obtaining control unless the lease is determined to be a finance lease. Additional Changes Impacting both Lessees and Lessors Separation of Lease and Non-Lease Components The requirement to identify and separately account for lease and non-lease components is not new. However, under the new lease standard, the requirement takes on greater importance because lease components are now accounted for on the balance sheet whereas non-lease components are generally accounted for off balance sheet. If the transfer does not qualify as a sale, the transaction is accounted for as a financing arrangement. The seller-lessee continues to record the underlying asset on its balance sheet and recognizes a liability for any proceeds received from the buyer-lessor. In contrast, if the transfer qualifies as a sale, then the sellerlessee derecognizes the underlying asset, recognizes a gain on sale and accounts for the leaseback in accordance with the new lease standard (i.e., based on an assessment of whether control of the asset has been transferred). In addition, because the new lease standard modifies the interpretive guidance surrounding the definition of a lease and provides incremental guidance on how to identify and separate lease and non-lease components, companies Assurance | Tax | Advisory | dhgllp.com 6 .

views Disclosures The new standard also provides certain “practical expedients” companies may elect at the date of transition to ease the burden of adoption. These practical expedients would allow companies to not reassess at the date of initial adoption: The new lease standard requires lessees and lessors to provide additional quantitative and qualitative information about their leases, including significant judgments involved in the accounting for leases and the amounts recognized in the financial statements from leases. The objective of the disclosures is to “enable users of financial statements to assess the amount, timing and uncertainty of cash flows arising from leases.”13 1. Whether any expired or existing contracts are or contain leases. 2. The lease classification for any expired or existing leases. (All existing leases that were classified as operating leases in accordance with Topic 840 will be classified as operating leases and all existing leases that were classified as capital leases in accordance with Topic 840 will be classified as finance leases.) Certain disclosures required of lessees and lessors under the new lease standard include: Disclosure requirements 3. Initial direct costs for existing leases. Lessee • Information about the nature of its leases A fourth practical expedient would allow an entity to use hindsight in 1) determining the lease term when considering lessee options to extend or terminate the lease and to purchase the underlying asset and 2) assessing ROU assets for impairment. • Maturity analysis of lease liabilities • Lease expense, split between operating and capital leases • Short-term lease expense The first three practical expedients must be elected together (i.e., all or none). In contrast, the fourth practical expedient may be elected separately; however, if elected, it must be treated as an accounting policy election.

It cannot be elected on a lease-by-lease basis. • Variable lease expense • Sublease income • Weighted average remaining lease term • Weighted average discount rate For companies that avail themselves of the practical expedients, the primary effect of adoption will be the grossing up of the balance sheet for any existing operating leases. Lessor • Information about the nature of its leases • Maturity analysis of lease investments Preparing for Adoption • Profit or loss recognized at lease commencement (for sales-type leases) For companies that have a meaningful portfolio of lease contracts – whether as a lessor or lessee, or both – operationalizing the new lease standard could require significant effort. As a result, companies impacted by the change should start working toward implementation immediately. Key steps all companies should consider including in their adoption of the new lease standard follow: • Lease income • Qualitative and quantitative information about significant changes in residual values of leased assets Transition The new lease standard requires companies to adopt its provisions using a modified retrospective approach.

Under this approach companies must apply the new accounting requirements as of the beginning of the earliest comparative period presented. Assurance | Tax | Advisory | dhgllp.com 1. Forming a cross-functional implementation team, including representation from accounting, finance, business lines, tax, technology, legal, internal audit and supply chain. 2. Educating key stakeholders, including management, the implementation team, the board of directors and others on the key changes to the accounting guidance, and the expected impact on the company’s financial results, accounting processes, internal controls and business practices. 7 . views 5. Performing an inventory of existing lease contracts. As part of this effort, performing a comprehensive review of GL activity to ensure completeness of the contract population. 3. Assessing resources needed to implement the new lease standard, including the expertise, time commitment and necessary technology solutions. As part of this effort, companies should evaluate their information technology infrastructure to determine whether they have the mechanisms in place to assess and track leasing activities prospectively, or whether there is a need to create an interim technology solution until software providers have time to review the final standard and create a permanent solution. 6. Identifying opportunities for aggregating similar lease contracts to eliminate redundant accounting analyses. 7. Determining which short-term lease contracts, if any, will be accounted for off balance sheet. 8. Identifying which practical expedients, if any, provided by the new lease standard will be applied upon adoption. 4. Developing a project plan outlining the key steps, milestones and testing required to ensure a successful implementation. As part of this effort, an implementation timeline should be established. Figure 1 provides an example implementation plan that companies might consider as they prepare to adopt the new lease standard. Figure 1: Example Implementation Plan 1. Engagement of Key Stakeholders 2. Create Project Plan 3. Process of Discovery • Discuss financial and operational impacts of the new standard • Identify SMEs for each department who will own the workstream from a departmental perspective • Aggregation of enterprise contracts for inclusion in population review • What is the desired end state? • To include but not limited to: »» LOB Finance »» Controller Groups »» Tax »» Treasury »» Supply Chain »» AP »» Technology • List the key steps, milestones, and testing required to ensure a successful go live implementation • LOB finance and controllers should do a comprehensive review of GL activity to ensure completeness of contract population • Ensure technology is engaged early to help identify any potential technology limitations and solutions • Internal Audit to approve scoping and methodology »» Legal »» Accounting Policy 4. Determine Scope in Population 5. Testing 6. Execution • Review contracts and categorize as appropriate • Accounting policy to opine on each contract in scope and classify each lease type as appropriate. • Book GL entries • Short-term (Excluded) • Small Ticket/Portfolio Level • Engage Legal department to determine if each meets the definition of a lease • Technology should provide testing environment to ensure accurate reporting for implementation date. • Compare balance sheet impacts with pro-forma projections • Finalize project documentation including work papers, project plans, and SME sign-offs. • Leases should be valued, and accounting entries booked in test • Finance to create pro-forma financials to assess the impact on overall balance sheet capital, existing debt covenants, and key ratios. Conclusion The new lease standard has the potential to significantly impact a company’s financial position, reported results and accounting environment.

Adopting the new standard could require significant time and effort. Consequently, companies should start the process of understanding how the new lease Assurance | Tax | Advisory | dhgllp.com standard differs from existing guidance and assessing how changes will impact their business. Starting early will allow more time for the testing and execution phase of adoption, giving entities a better chance to “brace for impact.” 8 .

views How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies think through how the new leases standard will impact their reported results and accompanying disclosures, Understand the guidance • Provide CPE-eligible trainings for a company’s key stakeholders • Provide DHG thoughtware on forthcoming accounting changes accounting processes and controls, and other areas of a business. Assess the impact • Help inventory existing leases population and related processes and controls • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) Get the accounting right • Perform accounting analyses on existing lease portfolio • Design and implement new accounting processes and controls • Draft new leases disclosures and accounting policies For further details about how our Accounting Readiness team can assist your company, please contact: Ryan Crowe Partner | Risk Advisory 704.367.7192 ryan.crowe@dhgllp.com Assurance | Tax | Advisory | dhgllp.com Sean Prince Senior Manager | Risk Advisory 203.826.2500 sean.prince@dhgllp.com 9 Jim Ewart Director | Forensics & Valuation 843.727.3242 james.ewart@dhgllp.com . views APPENDIX A | An Example of Short-Term Leases This appendix provides an example of how a company would analyze a lease to determine if it qualifies for the new short-term lease scope exception. EXAMPLE Conclusion: Facts: • Based on a review of the relevant factors that create an economic incentive (e.g., the leasehold improvements involved, the material tax incentive being offered, and the importance of the building to Darling’s operations), Darling Widgets concludes it is reasonably certain that it will exercise the renewal option. As a result the lease does not qualify as a short-term lease because the lease term exceeds 12 months. • Darling Widgets enters into a lease agreement with RE Rental, Inc. to lease a building for an initial period of 12 months. • At the end of 12 months Darling Widgets has the option to renew the lease contract for an additional 36-month period. • Darling Widgets intends to use the building for the location of its new corporate headquarters, which will require the installation of significant leasehold improvements. • Had it not been for the factors noted above that make it reasonably certain Darling Widgets will exercise the renewal option, the company would have been able to elect the short-term lease scope exception because, in this case, the non-cancelable period of the lease is for only 12 months. • Additionally, Darling Widgets has been offered a material tax incentive from the local government for relocating its headquarters. However, to receive the tax incentive, the company must remain in the locality for at least two years.

Darling Widgets intends to meet that requirement. Assurance | Tax | Advisory | dhgllp.com 10 . views APPENDIX B | An Example of the Lessee Accounting Model This appendix provides an example of how a lessee would account for a lease under the new lease standard. Specifically, the example highlights how the different lease types – operating versus finance –impact a lessee’s income statement presentation and the subsequent accounting for the ROU asset. The example makes certain simplifying assumptions (e.g., no initial direct costs, no lease incentives received, etc.) to facilitate ease of understanding. EXAMPLE Facts: Darling Widgets enters into a lease agreement with RE Rental, Inc. to lease a building for an initial period of three years. There are no renewal or termination options. Under the terms of the lease Darling Widgets will make annual payments (occurring at the end of each period) to RE Rental, Inc.

in accordance with the following payment schedule: Year Amount 1 $100,000 2 $120,000 3 $140,000 Total $360,000 Based on the information available the company is unable to determine the rate implicit in the lease. Therefore, it uses its incremental borrowing rate of 9.15% to calculate an initial lease liability of $300,000.14 For simplicity, assume that the company did not incur any initial direct costs or receive any lease incentives in connection with the lease. Conclusion: The following table and accompanying journal entries outline how Darling Widgets would account for its lease assuming that it was classified as a finance lease and operating lease, respectively: Finance Lease Year (end of period) Cash Outflows (A) 0 Lease Liability Principal Paydown (A-B) $300,000 ROU Asset Interest Expense (B) Operating Lease Amortization ROU Asset Expense* $300,000 Adjustment Lease to ROU Expense*** Asset** $300,000 1 $100,000 $227,451 $72,549 $200,000 $27,451 $100,000 $207,451 $92,549 $120,000 2 $120,000 $128,263 $99,188 $100,000 $20,812 $100,000 $108,263 $99,188 $120,000 3 $140,000 $- $128,263 $- $11,737 $100,000 $- $108,263 $120,000 Totals $360,000 $60,000 $300,000 $300,000 $360,000 * For finance leases, the amortization expense each period equals the initial ROU asset divided by the initial lease term. **For operating leases, the ROU asset is reduced each period by an amount equal to the difference between (a) the lease expense and (b) the theoretical interest expense amount. ***The lease expense is equal to the sum of (a) the remaining undiscounted lease payments and (b) any initial direct costs, divided by the remaining lease term. Assurance | Tax | Advisory | dhgllp.com 11 . views Finance Lease Accounting Entries: Operating Lease Accounting Entries: At lease commencement At lease commencement ROU Asset $300,000 Lease Liability ROU Asset $300,000 $300,000 Lease Liability Year 1 $300,000 Year 1 Interest Expense 27,451 Lease Expense 120,000 Lease Liability 72,549 Lease Liability 72,549 Cash Cash 100,000 Amort. Expense 100,000 ROU Asset 100,000 ROU Asset 92,549 100,000 Year 2 Year 2 Interest Expense 20,812 Lease Expense 120,000 Lease Liability 99,188 Lease Liability 99,188 Cash Cash 120,000 Amort. Expense ROU Asset 100,000 ROU Asset 120,000 99,188 100,000 Year 3 Year 3 Interest Expense 11,737 120,000 128,263 Lease Liability Lease Expense Lease Liability 128,263 Cash Cash Amort. Expense 100,000 ROU Asset 140,000 ROU Asset 140,000 108,263 100,000 This example demonstrates how, while the total expense recognized for a finance lease and an operating lease is the same over the entire term of the lease, expense recognition for finance leases is front-loaded as a result of the declining interest expense over the term of the lease as depicted in the chart below. Lease Expense vs.

Cash Payments $150,000 $140,000 $130,000 $120,000 $110,000 $100,000 $90,000 $80,000 Year 1 Year 2 Operating Lease Assurance | Tax | Advisory | dhgllp.com Finance Lease 12 Year 3 Cash Payments . views APPENDIX C | An Example of Lease Classification by a Lessor This appendix provides an example of how a lessor would analyze a lease contract using the new lease classification assessment in the new lease standard. EXAMPLE Facts: Conclusion: BT Rentals Co. enters into a lease agreement to rent a moving truck to MoversRUs for a period of four years. The remaining useful life of the truck at lease commencement is 5 years and its current carrying amount is $35,000. The estimated residual value of the truck is $5,000. BT Rentals’ lease agreement with MoversRUs covers 80% of the remaining useful life of the moving truck.

Furthermore, the present value of the anticipated lease payments, which BT Rentals has assessed as probable of being collected, amounts to substantially all of the fair value of the moving truck. Based on these facts, BT Rentals concludes that the lease should be classified as a sales-type lease with upfront profit recognition. Under the lease BT Rentals will receive from MoversRUs annual payments (occurring at the end of each period) in accordance with the following payment schedule: Year Amount 1 $10,000 2 $12,000 3 $14,000 4 $16,000 Total As a result, BT Rentals records the following entries at lease commencement: $52,000 Net investment in sales-type lease Cost of goods sold* Sales revenue** Moving truck $43,500 31,628 $40,128 35,000 * Calculated as the carrying amount of the moving truck less the present value of the estimated unguaranteed residual value. Based on BT Rentals’ analysis of the relevant facts and circumstances, BT Rentals concludes that collectability of the lease payments from MoversRUs is probable. ** Calculated as the present value of the future lease payments BT Rentals determines that the rate implicit in the lease is 10.35%. The present value of the lease payments is $40,128. For simplicity, assume that there are no initial direct costs or residual value guarantees provided to the lessor. 1. The formal effective date for public companies is annual reporting periods beginning after December 15, 2018, and interim periods therein.

Private companies are granted a one-year deferral. However, both public and private companies may elect to early adopt the standard. 2. This paper does not cover the changes made by the International Accounting Standards Board (IASB) to its lease accounting guidance. On January 13, 2016, the IASB issued International Financial Reporting Standard (IFRS) 16, which amends the accounting for leases for companies complying with IFRSs.

While IFRS 16 and the FASB’s new lease standard both require leases to be recorded on the balance sheet, significant differences remain between the two standards. 3. Refer to ASC 842-10-20. 4. Lease payments exclude contingent rental payments (e.g., rent based on percent of sales). 5. The rate implicit in the lease is the rate that causes the present value of the net investment in the lease to equal the sum of 1) the fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and 2) any capitalized initial direct costs incurred by the lessor. If a lessee cannot readily determine the rate implicit in the lease, it would use its incremental borrowing rate as the discount rate. In addition, private companies will have the option to use the risk-free rate in calculating the present value of lease payments. 6. With respect to possible regulatory capital implications, from informal discussions with the FASB staff, we understand the FASB intentionally remained silent on the nature of the ROU asset in the final standard so as to avoid any negative impacts of classifying such assets as intangible assets. 7. Refer to ASC 842-10-55-26. 8. Refer to ASC 842-10-55-2. 9. Under the new lease standard the straight-line basis is used “unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived from the right to use the underlying asset” (ASC 842-20-35-7). 10. Refer to ASU 2014-09, Revenue from Contracts with Customers. 11. Refer to ASC 606-10-05-4. 12. Refer to ASC 842-10-25-2 through 25-3 and ASC 842-30-25-3. 13. Refer to ASC 842-20-50-1 and ASC 842-30-50-1. 14. As explained in the new lease standard, the incremental borrowing rate is “[t]he rate of interest that a lessee would have to pay to borrow over a similar term and with a similar security the funds necessary to obtain an asset of a similar value to the right-of-use asset in a similar economic environment.” Assurance | Tax | Advisory | dhgllp.com 13 .