FASB Releases New Standard on Classification & Measurement of Financial Instruments – January 2016

Dixon Hughes Goodman

Description

views

January 2016

Financial Reporting Quick Hits: FASB Releases New Standard on

Classification & Measurement of Financial Instruments

Ryan Crowe, Partner | Risk Advisory

Sean Prince, Senior Manager | Risk Advisory

On January 5, 2016, the Financial Accounting Standards Board (FASB) published Accounting Standards Update (ASU)

2016-01, Financial Instruments Overall: Recognition and Measurement of Financial Assets and Financial Liabilities that

amends the guidance on the classification and measurement of financial instruments. ASU 2016-01 becomes effective

for public business entities in fiscal years beginning after December 15, 2017, including interim periods therein. All other

entities are provided a one-year deferral.

Key Changes

While the new standard retains significant components

of existing guidance governing the classification and

measurement of financial instruments, it makes the following

key changes:

Accounting for Equity Securities

Currently, investments in equity securities with readily

determinable fair values (e.g., the common stock of a publicly

traded company) are governed by Accounting Standards

Codification (ASC) Topic 320, Investments—Debt and

Equity Securities.1 Under Topic 320, equity securities can be

classified as either trading or available-for-sale (AFS). While

Assurance | Tax | Advisory | dhgllp.com

all equity securities with readily determinable fair values are

measured at fair value on the statement of financial position,

changes in the fair value of equity securities classified as AFS

are initially recorded through other comprehensive income

(OCI) whereas changes in the fair value of equity securities

classified as trading are recorded through earnings.

ASU 2016-01 removes equity securities from the scope of

Topic 320 and creates ASC Topic 321, Investments—Equity

Securities.

Under the new Topic, all equity securities with readily determinable fair values are measured at fair value on the statement of financial position, with changes in fair value recorded through earnings. The update eliminates the option to record changes in the fair value of equity securities . views Under the practicability exception, a company would initially measure the equity investment at its initial cost. In subsequent periods, the equity security would be measured at cost, less any impairment recognized, “plus or minus changes resulting from observable price changes in orderly transactions for the identical investment or a similar investment of the same issuer.” through OCI. As a result, upon adoption of the new standard, equity securities currently classified as AFS will need to be reclassified and accounted for in a manner similar to equity securities currently classified as trading. Impact Analysis The elimination of the AFS classification for equity securities will introduce greater earnings volatility into a company’s earnings measures. Fair value changes that were previously recorded through OCI will now be recorded directly through earnings. To identify observable price changes, ASU 2016-01 explains that a company should consider known transactions as of the balance sheet date and make a reasonable effort (that is, without expending undue cost and effort) to identify price changes that can reasonably be known.

The company need not conduct an exhaustive search for all observable price changes. ASU 2016-01 further explains how companies will need to adjust the observable price of a similar security for the different rights and obligations (e.g. voting rights, distribution rights and preferences, and conversion features) to determine the amount that should be recorded as an upward or downward adjustment in the carrying value of the security. The elimination of the AFS classification may also affect a company’s existing hedge relationships.

For example, companies that previously hedged the FX risk of an AFS equity security denominated in another currency will need to cease applying hedge accounting to the hedge relationship. Regarding regulatory capital implications, we understand that certain banks are holding discussions with bank regulators to explore the possibility of excluding market value movements of equity securities from regulatory capital calculations. In addition, if the practicability exception is elected, a company would perform a qualitative assessment each reporting period to determine whether the investment is impaired. Impairment indicators that a company should consider in its analysis include, but are not limited to, the following:3 Accounting for Equity Securities without a Readily Determinable Fair Value Currently, an investment in an equity security without a readily determinable fair value2 (e.g., an investment in an unlisted limited partnership) is governed by ASC Topic 32520, Investments—Other—Cost Method Investments and recorded in the statement of financial position at its initial cost. In subsequent periods, unless such an investment is subject to an other-than-temporary impairment (OTTI), it continues to be carried at its initial cost. 1. A significant deterioration in the earnings performance, credit rating, asset quality, or business prospects of the investee. 2. A significant adverse change in the regulatory, economic, or technological environment of the investee. 3. A significant adverse change in the general market condition of either the geographical area or the industry in which the investee operates. As discussed above, ASU 2016-01 amends existing accounting guidance so that changes in the fair value of equity securities are recorded through earnings.

However, ASU 2016-01 provides a practicability exception for equity securities without a readily determinable fair value. 4. A bona fide offer to purchase, an offer by the investee to sell, or a completed auction process for the same or similar investment for an amount less than the carrying amount of that investment. Impact Analysis 5. Factors that raise significant concerns about the investee’s ability to continue as a going concern, such as negative cash flows from operations, working capital deficiencies, or noncompliance with statutory capital requirements or debt covenants. Companies would be able to elect the practicability exception on an investment-by-investment basis. However, the practicability exception would not be available for equity securities that qualify for the net asset value (NAV) practical expedient outlined in ASC 820-10-35-59. The practicability exception would also be unavailable for investment companies and brokers and dealers in securities. Assurance | Tax | Advisory | dhgllp.com 2 .

views New Disclosures If, based on an assessment of such factors, the company determines that its equity investment is impaired, it would record an impairment charge equal to the difference between the equity investment’s cost basis and its fair value. ASU 2016-01 retains the majority of existing U.S. GAAP disclosure requirements. However, the FASB determined that only public business entities would be required to continue disclosing the fair value of financial assets and financial liabilities measured at amortized cost, excluding receivables and payables due within one year and demand deposit liabilities. All other entities would now be exempt from this disclosure requirement. Impact Analysis The changes to the subsequent measurement guidance for equity securities without a readily determinable fair value may introduce greater earnings volatility due to the requirement to adjust the carrying value of those investments for observable price changes. Impact Analysis The new standard requires that fair value amounts disclosed for financial instruments measured at amortized cost should be determined in accordance with Topic 820.

This could present a change for certain companies that determine fair value amounts using an entry-price concept under an alternative interpretation of guidance currently in Topic 825. Accounting for Financial Liabilities Measured at Fair Value Currently, companies may elect the fair value option in ASC Topic 825 Financial Instruments for certain financial liabilities. When the fair value option is elected for a financial liability, changes in fair value, including changes in fair value attributable to changes in a company’s own creditworthiness, are recorded through earnings in the period those changes occur. Other noteworthy changes to the disclosure requirements include the following: • Public business entities would no longer be required to disclose the method(s) and significant assumptions used to estimate the fair of financial instruments measured at amortized cost. ASU 2016-01 amends Topic 825 to require changes in the fair value of a financial liability attributable to a change in instrumentspecific credit risk to be recorded separately in OCI.4 All other changes in fair value (e.g., those attributable to interest rate movements) should be recorded in earnings. • For equity securities without readily determinable fair values accounted for under the new practicability exception, a company would be required to disclose the carrying amount of such securities as well as any adjustments made to the carrying amount of those securities due to observable price changes, including any impairment charges recorded during the reporting period. The new standard allows companies to consider the portion of the total change in fair value of the financial liability that excludes the amount resulting from a change in a base market risk, such as a risk-free interest rate or a benchmark interest rate (e.g., LIBOR), to represent the change in instrument-specific credit risk. Alternatively, companies may use another method to identify fair value changes arising from changes in instrumentspecific credit risk if that method is deemed to faithfully represent changes in instrument-specific credit risk. Transition ASU 2016-01 permits limited early adoption opportunities for public business entities. However, all companies may early adopt the new presentation requirements for changes in the fair value of financial liabilities due to instrument-specific credit risk in OCI in financial statements not yet issued or not yet available for issuance.5 Impact Analysis The requirement to present fair value changes arising from “instrument-specific credit risk” separately from other fair value changes addresses an oft-criticized result of existing accounting guidance under which a deterioration in a company’s creditworthiness can result in an earnings increase. Assurance | Tax | Advisory | dhgllp.com In addition, companies that are not considered public business entities may elect to eliminate the disclosure of the fair value information currently required by Topic 825-10-50 for any reporting period for which financial statements have not yet been made available for issuance.

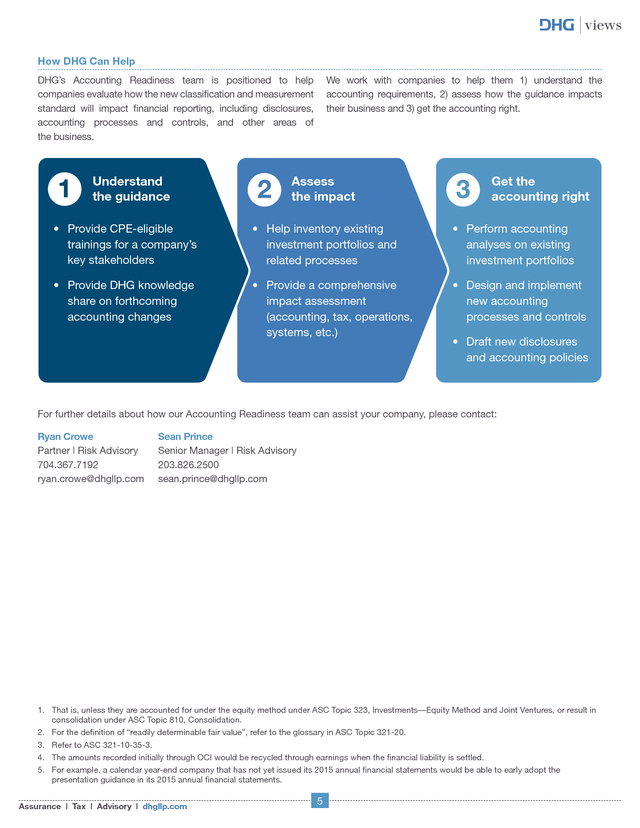

Companies that are not considered public business entities are also permitted to early adopt the entire standard at the same time the standard becomes effective for public business entities. 3 . views • The requirement to apply the exit-price notion in Topic 820 to a company’s disclosure of fair value for financial instruments measured at amortized cost in the balance sheet. ASU 2016-01 requires adoption of the standard by means of a cumulative-effect adjustment as of the beginning of the fiscal year in which the standard becomes effective. However, the following provisions of the standard would be applied prospectively: • If elected, the new practicability exception for investments in equity securities without readily determinable fair values. Key Tasks As a result of the key changes discussed above, companies will need to address the following items: Key Change Action Items Accounting for equity securities • Identify the existing population of equity securities classified as available for sale. • Determine whether such securities will be reclassified and accounted for at fair value through net income or otherwise disposed of. • For equity securities that are reclassified and accounted for at fair value through net income, calculate the cumulative-effect adjustment to be recorded upon adoption of the standard. Accounting for equity securities without readily determinable fair values • Identify the existing population of cost-method investments. • Determine whether to elect the new practicability exception or reclassify and account for such investments at fair value through net income. • If the practicability exception is elected: »» Develop a process and related controls for identifying observable price changes in orderly transactions for the identical investment or similar investments of the same issuer. »» Develop a process for implementing the new impairment test. »» Develop a process to re-assess at each reporting period whether the investment continues to qualify to be measured using the practicability exception. Accounting for financial liabilities measured under the fair value option • Identify the existing population of financial liabilities accounted for under the fair value option. Disclosures • Determine if any changes are required to fair value amounts disclosed for financial instruments measured at amortized cost. • Develop a process and related controls for measuring the change in fair value attributable to changes in instrument-specific credit risk. • Update the existing presentation of such liabilities in the financial statements. • Determine whether any new disclosures are needed for equity securities without readily determinable fair values. Assurance | Tax | Advisory | dhgllp.com 4 . views How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies evaluate how the new classification and measurement standard will impact financial reporting, including disclosures, accounting processes and controls, and other areas of the business. Understand the guidance We work with companies to help them 1) understand the accounting requirements, 2) assess how the guidance impacts their business and 3) get the accounting right. Assess the impact Get the accounting right • Provide CPE-eligible trainings for a company’s key stakeholders • Help inventory existing investment portfolios and related processes • Perform accounting analyses on existing investment portfolios • Provide DHG knowledge share on forthcoming accounting changes • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) • Design and implement new accounting processes and controls • Draft new disclosures and accounting policies For further details about how our Accounting Readiness team can assist your company, please contact: Ryan Crowe Partner | Risk Advisory 704.367.7192 ryan.crowe@dhgllp.com Sean Prince Senior Manager | Risk Advisory 203.826.2500 sean.prince@dhgllp.com 1. That is, unless they are accounted for under the equity method under ASC Topic 323, Investments—Equity Method and Joint Ventures, or result in consolidation under ASC Topic 810, Consolidation. 2. For the definition of “readily determinable fair value”, refer to the glossary in ASC Topic 321-20. 3. Refer to ASC 321-10-35-3. 4. The amounts recorded initially through OCI would be recycled through earnings when the financial liability is settled. 5. For example, a calendar year-end company that has not yet issued its 2015 annual financial statements would be able to early adopt the presentation guidance in its 2015 annual financial statements. Assurance | Tax | Advisory | dhgllp.com 5 .

Under the new Topic, all equity securities with readily determinable fair values are measured at fair value on the statement of financial position, with changes in fair value recorded through earnings. The update eliminates the option to record changes in the fair value of equity securities . views Under the practicability exception, a company would initially measure the equity investment at its initial cost. In subsequent periods, the equity security would be measured at cost, less any impairment recognized, “plus or minus changes resulting from observable price changes in orderly transactions for the identical investment or a similar investment of the same issuer.” through OCI. As a result, upon adoption of the new standard, equity securities currently classified as AFS will need to be reclassified and accounted for in a manner similar to equity securities currently classified as trading. Impact Analysis The elimination of the AFS classification for equity securities will introduce greater earnings volatility into a company’s earnings measures. Fair value changes that were previously recorded through OCI will now be recorded directly through earnings. To identify observable price changes, ASU 2016-01 explains that a company should consider known transactions as of the balance sheet date and make a reasonable effort (that is, without expending undue cost and effort) to identify price changes that can reasonably be known.

The company need not conduct an exhaustive search for all observable price changes. ASU 2016-01 further explains how companies will need to adjust the observable price of a similar security for the different rights and obligations (e.g. voting rights, distribution rights and preferences, and conversion features) to determine the amount that should be recorded as an upward or downward adjustment in the carrying value of the security. The elimination of the AFS classification may also affect a company’s existing hedge relationships.

For example, companies that previously hedged the FX risk of an AFS equity security denominated in another currency will need to cease applying hedge accounting to the hedge relationship. Regarding regulatory capital implications, we understand that certain banks are holding discussions with bank regulators to explore the possibility of excluding market value movements of equity securities from regulatory capital calculations. In addition, if the practicability exception is elected, a company would perform a qualitative assessment each reporting period to determine whether the investment is impaired. Impairment indicators that a company should consider in its analysis include, but are not limited to, the following:3 Accounting for Equity Securities without a Readily Determinable Fair Value Currently, an investment in an equity security without a readily determinable fair value2 (e.g., an investment in an unlisted limited partnership) is governed by ASC Topic 32520, Investments—Other—Cost Method Investments and recorded in the statement of financial position at its initial cost. In subsequent periods, unless such an investment is subject to an other-than-temporary impairment (OTTI), it continues to be carried at its initial cost. 1. A significant deterioration in the earnings performance, credit rating, asset quality, or business prospects of the investee. 2. A significant adverse change in the regulatory, economic, or technological environment of the investee. 3. A significant adverse change in the general market condition of either the geographical area or the industry in which the investee operates. As discussed above, ASU 2016-01 amends existing accounting guidance so that changes in the fair value of equity securities are recorded through earnings.

However, ASU 2016-01 provides a practicability exception for equity securities without a readily determinable fair value. 4. A bona fide offer to purchase, an offer by the investee to sell, or a completed auction process for the same or similar investment for an amount less than the carrying amount of that investment. Impact Analysis 5. Factors that raise significant concerns about the investee’s ability to continue as a going concern, such as negative cash flows from operations, working capital deficiencies, or noncompliance with statutory capital requirements or debt covenants. Companies would be able to elect the practicability exception on an investment-by-investment basis. However, the practicability exception would not be available for equity securities that qualify for the net asset value (NAV) practical expedient outlined in ASC 820-10-35-59. The practicability exception would also be unavailable for investment companies and brokers and dealers in securities. Assurance | Tax | Advisory | dhgllp.com 2 .

views New Disclosures If, based on an assessment of such factors, the company determines that its equity investment is impaired, it would record an impairment charge equal to the difference between the equity investment’s cost basis and its fair value. ASU 2016-01 retains the majority of existing U.S. GAAP disclosure requirements. However, the FASB determined that only public business entities would be required to continue disclosing the fair value of financial assets and financial liabilities measured at amortized cost, excluding receivables and payables due within one year and demand deposit liabilities. All other entities would now be exempt from this disclosure requirement. Impact Analysis The changes to the subsequent measurement guidance for equity securities without a readily determinable fair value may introduce greater earnings volatility due to the requirement to adjust the carrying value of those investments for observable price changes. Impact Analysis The new standard requires that fair value amounts disclosed for financial instruments measured at amortized cost should be determined in accordance with Topic 820.

This could present a change for certain companies that determine fair value amounts using an entry-price concept under an alternative interpretation of guidance currently in Topic 825. Accounting for Financial Liabilities Measured at Fair Value Currently, companies may elect the fair value option in ASC Topic 825 Financial Instruments for certain financial liabilities. When the fair value option is elected for a financial liability, changes in fair value, including changes in fair value attributable to changes in a company’s own creditworthiness, are recorded through earnings in the period those changes occur. Other noteworthy changes to the disclosure requirements include the following: • Public business entities would no longer be required to disclose the method(s) and significant assumptions used to estimate the fair of financial instruments measured at amortized cost. ASU 2016-01 amends Topic 825 to require changes in the fair value of a financial liability attributable to a change in instrumentspecific credit risk to be recorded separately in OCI.4 All other changes in fair value (e.g., those attributable to interest rate movements) should be recorded in earnings. • For equity securities without readily determinable fair values accounted for under the new practicability exception, a company would be required to disclose the carrying amount of such securities as well as any adjustments made to the carrying amount of those securities due to observable price changes, including any impairment charges recorded during the reporting period. The new standard allows companies to consider the portion of the total change in fair value of the financial liability that excludes the amount resulting from a change in a base market risk, such as a risk-free interest rate or a benchmark interest rate (e.g., LIBOR), to represent the change in instrument-specific credit risk. Alternatively, companies may use another method to identify fair value changes arising from changes in instrumentspecific credit risk if that method is deemed to faithfully represent changes in instrument-specific credit risk. Transition ASU 2016-01 permits limited early adoption opportunities for public business entities. However, all companies may early adopt the new presentation requirements for changes in the fair value of financial liabilities due to instrument-specific credit risk in OCI in financial statements not yet issued or not yet available for issuance.5 Impact Analysis The requirement to present fair value changes arising from “instrument-specific credit risk” separately from other fair value changes addresses an oft-criticized result of existing accounting guidance under which a deterioration in a company’s creditworthiness can result in an earnings increase. Assurance | Tax | Advisory | dhgllp.com In addition, companies that are not considered public business entities may elect to eliminate the disclosure of the fair value information currently required by Topic 825-10-50 for any reporting period for which financial statements have not yet been made available for issuance.

Companies that are not considered public business entities are also permitted to early adopt the entire standard at the same time the standard becomes effective for public business entities. 3 . views • The requirement to apply the exit-price notion in Topic 820 to a company’s disclosure of fair value for financial instruments measured at amortized cost in the balance sheet. ASU 2016-01 requires adoption of the standard by means of a cumulative-effect adjustment as of the beginning of the fiscal year in which the standard becomes effective. However, the following provisions of the standard would be applied prospectively: • If elected, the new practicability exception for investments in equity securities without readily determinable fair values. Key Tasks As a result of the key changes discussed above, companies will need to address the following items: Key Change Action Items Accounting for equity securities • Identify the existing population of equity securities classified as available for sale. • Determine whether such securities will be reclassified and accounted for at fair value through net income or otherwise disposed of. • For equity securities that are reclassified and accounted for at fair value through net income, calculate the cumulative-effect adjustment to be recorded upon adoption of the standard. Accounting for equity securities without readily determinable fair values • Identify the existing population of cost-method investments. • Determine whether to elect the new practicability exception or reclassify and account for such investments at fair value through net income. • If the practicability exception is elected: »» Develop a process and related controls for identifying observable price changes in orderly transactions for the identical investment or similar investments of the same issuer. »» Develop a process for implementing the new impairment test. »» Develop a process to re-assess at each reporting period whether the investment continues to qualify to be measured using the practicability exception. Accounting for financial liabilities measured under the fair value option • Identify the existing population of financial liabilities accounted for under the fair value option. Disclosures • Determine if any changes are required to fair value amounts disclosed for financial instruments measured at amortized cost. • Develop a process and related controls for measuring the change in fair value attributable to changes in instrument-specific credit risk. • Update the existing presentation of such liabilities in the financial statements. • Determine whether any new disclosures are needed for equity securities without readily determinable fair values. Assurance | Tax | Advisory | dhgllp.com 4 . views How DHG Can Help DHG’s Accounting Readiness team is positioned to help companies evaluate how the new classification and measurement standard will impact financial reporting, including disclosures, accounting processes and controls, and other areas of the business. Understand the guidance We work with companies to help them 1) understand the accounting requirements, 2) assess how the guidance impacts their business and 3) get the accounting right. Assess the impact Get the accounting right • Provide CPE-eligible trainings for a company’s key stakeholders • Help inventory existing investment portfolios and related processes • Perform accounting analyses on existing investment portfolios • Provide DHG knowledge share on forthcoming accounting changes • Provide a comprehensive impact assessment (accounting, tax, operations, systems, etc.) • Design and implement new accounting processes and controls • Draft new disclosures and accounting policies For further details about how our Accounting Readiness team can assist your company, please contact: Ryan Crowe Partner | Risk Advisory 704.367.7192 ryan.crowe@dhgllp.com Sean Prince Senior Manager | Risk Advisory 203.826.2500 sean.prince@dhgllp.com 1. That is, unless they are accounted for under the equity method under ASC Topic 323, Investments—Equity Method and Joint Ventures, or result in consolidation under ASC Topic 810, Consolidation. 2. For the definition of “readily determinable fair value”, refer to the glossary in ASC Topic 321-20. 3. Refer to ASC 321-10-35-3. 4. The amounts recorded initially through OCI would be recycled through earnings when the financial liability is settled. 5. For example, a calendar year-end company that has not yet issued its 2015 annual financial statements would be able to early adopt the presentation guidance in its 2015 annual financial statements. Assurance | Tax | Advisory | dhgllp.com 5 .