Description

CFO Insights

Should FX swings affect

incentive compensation?

The recent strengthening of the US dollar has had a

significant impact on corporate earnings at many USbased companies with significant foreign operations.

The magnitude of the change also caught a lot of

companies by surprise. Moreover, because these currency

fluctuations were not fully anticipated in the budgeting

or incentive-plan goal-setting process, the treatment of

foreign exchange (FX) in calculating incentives became a

boardroom topic.

Most companies decided not to make major changes

to their incentive calculations. In the most recent CFO

Signals™ survey, 70% of CFOs agreed that the issue was

relevant for their companies, but more than three-quarters

of those same CFOs did not plan to make adjustments.1

Instead, the prevailing sentiment was to keep the fates of

shareholders and executives closely aligned.

But the question remains: Should unanticipated FX

swings affect incentive compensation? Shareholders are

obviously interested in a resolution, since investors want

to see a stronger correlation between compensation

and company performance. Boards also want to ensure

alignment of incentives and shareholder returns and make

sure executives are properly motivated and rewarded

for decisions within their control.

In this issue of CFO Insights we will look at the different views on the issue of addressing the FX impact on incentive compensation and discuss how CFOs can contribute to the fairness debate. Three schools of thought FX swings are cyclical. When the dollar was weak against foreign currencies, its impact on incentive compensation was generally positive but relatively immaterial, as there was not a lot of year-over-year variation. But the recent surge in the US dollar made it the strongest it has been for many years against most world currencies, including the Canadian and Australian dollars, the British pound, and the euro.

The resulting change took a $31.7 billion toll on the earnings of American and European multinationals in the first quarter of 2015, according to a survey by FiREApps.2 In many cases, annual bonus and long-term incentive targets were built on the same financial assumptions as earnings. Because of FX’s recent adverse impact on earnings, there’s a more pressing need to raise the issue of whether or not incentive plans, which are partly impacted by FX fluctuations, should be revisited, and whether or not incentive compensation should be adjusted to reflect unanticipated FX fluctuations. There are three schools of thought in this regard: 1. Do nothing. This approach is based on the notion that changes in budget assumptions occur all the time, and it is up to management to adopt and adjust to the new conditions.

This view also considers the fact that if shareholders are experiencing lower-than-expected profits, management should earn less than expected incentive pay. Proponents also argue that because incentive compensation was not adjusted when profits received a boost from a weak US dollar against foreign currencies, then for consistency, no adjustment should be made when profits suffer from FX swings. 1 . 2. Hold-harmless approach. This approach neutralizes the impact of certain unplanned or unbudgeted items that affect profits used for incentive purposes, including FX. The rationale is that unplanned or unbudgeted items are largely out of management’s control, and excluding such items from incentive plan calculations allows the board to more properly recognize management’s performance. Advocates of the hold-harmless approach also exclude unplanned gains—such as lower commodity costs, gains on sale of assets, and positive FX—from reported earnings when calculating incentives. 3. Corridor approach.

In this scenario, the board holds management accountable for a portion of the variation in FX. Unlike the hold-harmless approach, management is not completely insulated from FX fluctuations, and will be more inclined to take prudent steps to manage the impact of FX on earnings, such as sourcing of raw materials in local currency, borrowing in local currency, and so on. To illustrate, suppose the euro is budgeted at US $1.14; as long as it remains within a given range, say, US $1.07 to US $1.21, the company allows the FX impact to flow through to the incentive plan calculation.

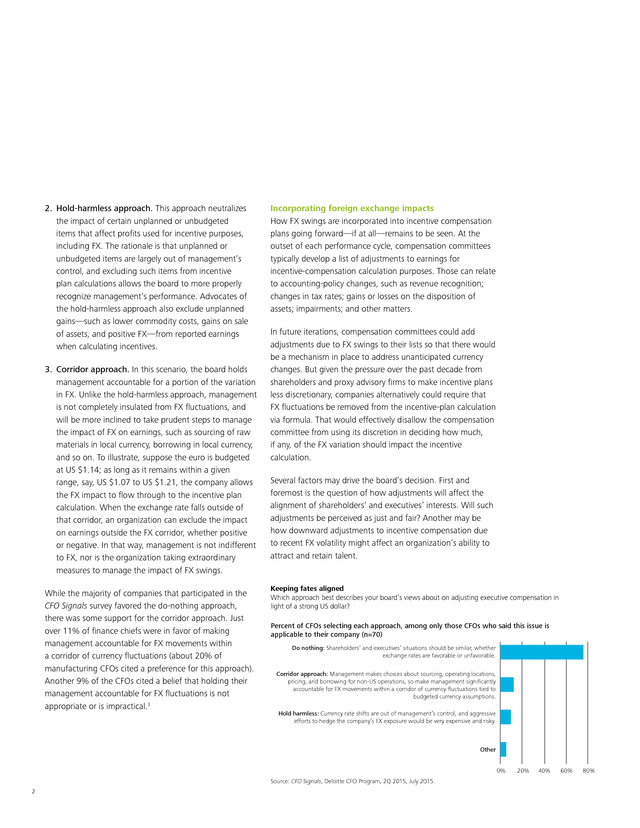

When the exchange rate falls outside of that corridor, an organization can exclude the impact on earnings outside the FX corridor, whether positive or negative. In that way, management is not indifferent to FX, nor is the organization taking extraordinary measures to manage the impact of FX swings. While the majority of companies that participated in the CFO Signals survey favored the do-nothing approach, there was some support for the corridor approach. Just over 11% of finance chiefs were in favor of making management accountable for FX movements within a corridor of currency fluctuations (about 20% of manufacturing CFOs cited a preference for this approach). Another 9% of the CFOs cited a belief that holding their management accountable for FX fluctuations is not appropriate or is impractical.3 Incorporating foreign exchange impacts How FX swings are incorporated into incentive compensation plans going forward—if at all—remains to be seen.

At the outset of each performance cycle, compensation committees typically develop a list of adjustments to earnings for incentive-compensation calculation purposes. Those can relate to accounting-policy changes, such as revenue recognition; changes in tax rates; gains or losses on the disposition of assets; impairments; and other matters. In future iterations, compensation committees could add adjustments due to FX swings to their lists so that there would be a mechanism in place to address unanticipated currency changes. But given the pressure over the past decade from shareholders and proxy advisory firms to make incentive plans less discretionary, companies alternatively could require that FX fluctuations be removed from the incentive-plan calculation via formula.

That would effectively disallow the compensation committee from using its discretion in deciding how much, if any, of the FX variation should impact the incentive calculation. Several factors may drive the board’s decision. First and foremost is the question of how adjustments will affect the alignment of shareholders’ and executives’ interests. Will such adjustments be perceived as just and fair? Another may be how downward adjustments to incentive compensation due to recent FX volatility might affect an organization’s ability to attract and retain talent. Keeping fates aligned Which approach best describes your board’s views about on adjusting executive compensation in light of a strong US dollar? Percent of CFOs selecting each approach, among only those CFOs who said this issue is applicable to their company (n=70) Do nothing: Shareholders’ and executives’ situations should be similar, whether exchange rates are favorable or unfavorable. Corridor approach: Management makes choices about sourcing, operating locations, pricing, and borrowing for non-US operations, so make management significantly accountable for FX movements within a corridor of currency fluctuations tied to budgeted currency assumptions. Hold harmless: Currency rate shifts are out of management’s control, and aggressive efforts to hedge the company’s FX exposure would be very expensive and risky. Other 0% Source: CFO Signals, Deloitte CFO Program, 2Q 2015, July 2015. 2 20% 40% 60% 80% .

New rule proposed on pay versus performance The Securities and Exchange Commission recently issued a proposed rule4 that would amend Regulation S-K, Item 402,5 to implement a mandate under the DoddFrank Act,6 requiring a registrant to disclose the relationship between executive compensation actually paid and the financial performance of the registrant. The proposal, which is intended to improve shareholders’ ability to objectively assess the link between executive compensation and company performance, raises a number of interesting questions. Employees, after all, want to be treated fairly and paid based on what they can influence and on how they perform. If incentive compensation is reduced as a result of FX fluctuations, which management and employees may not consider to be within their control, that could have an adverse effect on how workers feel about the fairness of the compensation program and whether their efforts are being properly valued. In the proposal, the SEC has requested comments on 64 questions. Thus, it is unclear what the final rule will look like and when it will be issued (although if finalized before year-end, it may be effective for the 2016 proxy season).

What is clear, however, is that shareholders, employees, and the media will heavily scrutinize the disclosures a registrant provides under the final rule. In addition, the impact of this issue could go deep into the organization, affecting anyone who is paid on an annual or long-term incentive plan. For example, an organization may have 1,000 or more employees participating in an annual incentive plan with only 10 to 15 of them senior officers. Thus, some companies may choose to provide relief to participants below the senior officer level to minimize the impact on morale and retention among the incentive-eligible population even if no adjustment is made for top officers. Because of the potential sensitivity associated with any disclosures about executive compensation, registrants affected by the proposal should review their past compensation practices and assess whether the proposed requirements would appropriately convey to investors the relationship between their executive compensation practices and company performance.

One way of doing so might be to model the proposed disclosures by using data for the past several years. Modeling might reveal possible unintended consequences of the proposal or the need to develop a strategy for communicating to investors the effects of specific aspects of the disclosures. Given that the proposal requested comment on virtually all aspects of its provisions, registrants had the opportunity to express their concerns and recommend improvements or disclosure alternatives. Comments were due on July 6, 2015. Bridging the information gap Still, some boards may worry that they will be criticized for making an adjustment to incentive compensation— upward or downward.

That’s particularly true in the event incentive compensation is adjusted upward when an organization is earning less. In such cases, it’s important for boards to have a strong rationale for the adjustment and to clearly communicate it to shareholders. In general, boards can help minimize the risk of being criticized by being consistent, having a strong rationale for their decision, being transparent about the factors that went into their decision, and making clear disclosures around the adjustment. 3 .

l, Global Research Director, CFO Program, Deloitte LLP; P For their part, CFOs can help shape the discussion and the decision by getting to know shareholders’ expectations through their interactions with analysts and major investors. In addition, it is important for finance chiefs to focus on what is affordable, albeit striking a balance with what is competitive. CFOs, even while struggling with the budget and trying to project out earnings for the next two to three years, should establish acceptable limits on compensation in terms of its dilutive effect on earnings. And finally, CFOs could spend considerable time with the audit and compensation committees to bridge the potential knowledge gap on compensation and financial performance. In the case of FX fluctuations, their input can help decide—in the case of either positive or negative swings—how these amounts should be reflected in incentive compensation targets and payouts. Primary Contact Michael S.

Kesner Principal; National Leader, Compensation Deloitte Consulting LLP mkesner@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr. Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary team of Deloitte leaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands. The Program harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of a CFO’s career – helping CFOs manage the aders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands.

The Program harnessestheir roles, tackle their company’s complexities of our nsights for every stage of a CFO’s career – helping CFOs manage the complexities of their roles, tackle their company’s most compelling most compelling challenges, and adapt to strategic shifts in the market. t: For more or services. This y means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional adviceinformation about Deloitte’s CFO Program, visit or should it be used as a basis for any decision or action that may affect your business. Before making any decision or takingat: www.deloitte.com/us/thecfoprogram. our website any action that may .

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. Follow us @deloittecfo Endnotes 1 CFO Signals, Deloitte CFO Program, see 2Q 2015, July 2015. 2 “FiREapps 2015 Q1 Corporate Earnings Currency Impact Report,” based on the analysis of the earnings calls of 1,200 publicly traded North American and European companies, June 2015. 3 CFO Signals, Deloitte CFO Program, see 2Q 2015, July 2015. 4 SEC Proposed Rule Release No. 34-74835, Pay Versus Performance. 5 SEC Regulation S-K, Item 402, “Executive Compensation.” 6 The proposed rule would implement Section 14(i) of the Securities Exchange Act of 1934, as added by Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act. This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business.

Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities.

DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 4 .

In this issue of CFO Insights we will look at the different views on the issue of addressing the FX impact on incentive compensation and discuss how CFOs can contribute to the fairness debate. Three schools of thought FX swings are cyclical. When the dollar was weak against foreign currencies, its impact on incentive compensation was generally positive but relatively immaterial, as there was not a lot of year-over-year variation. But the recent surge in the US dollar made it the strongest it has been for many years against most world currencies, including the Canadian and Australian dollars, the British pound, and the euro.

The resulting change took a $31.7 billion toll on the earnings of American and European multinationals in the first quarter of 2015, according to a survey by FiREApps.2 In many cases, annual bonus and long-term incentive targets were built on the same financial assumptions as earnings. Because of FX’s recent adverse impact on earnings, there’s a more pressing need to raise the issue of whether or not incentive plans, which are partly impacted by FX fluctuations, should be revisited, and whether or not incentive compensation should be adjusted to reflect unanticipated FX fluctuations. There are three schools of thought in this regard: 1. Do nothing. This approach is based on the notion that changes in budget assumptions occur all the time, and it is up to management to adopt and adjust to the new conditions.

This view also considers the fact that if shareholders are experiencing lower-than-expected profits, management should earn less than expected incentive pay. Proponents also argue that because incentive compensation was not adjusted when profits received a boost from a weak US dollar against foreign currencies, then for consistency, no adjustment should be made when profits suffer from FX swings. 1 . 2. Hold-harmless approach. This approach neutralizes the impact of certain unplanned or unbudgeted items that affect profits used for incentive purposes, including FX. The rationale is that unplanned or unbudgeted items are largely out of management’s control, and excluding such items from incentive plan calculations allows the board to more properly recognize management’s performance. Advocates of the hold-harmless approach also exclude unplanned gains—such as lower commodity costs, gains on sale of assets, and positive FX—from reported earnings when calculating incentives. 3. Corridor approach.

In this scenario, the board holds management accountable for a portion of the variation in FX. Unlike the hold-harmless approach, management is not completely insulated from FX fluctuations, and will be more inclined to take prudent steps to manage the impact of FX on earnings, such as sourcing of raw materials in local currency, borrowing in local currency, and so on. To illustrate, suppose the euro is budgeted at US $1.14; as long as it remains within a given range, say, US $1.07 to US $1.21, the company allows the FX impact to flow through to the incentive plan calculation.

When the exchange rate falls outside of that corridor, an organization can exclude the impact on earnings outside the FX corridor, whether positive or negative. In that way, management is not indifferent to FX, nor is the organization taking extraordinary measures to manage the impact of FX swings. While the majority of companies that participated in the CFO Signals survey favored the do-nothing approach, there was some support for the corridor approach. Just over 11% of finance chiefs were in favor of making management accountable for FX movements within a corridor of currency fluctuations (about 20% of manufacturing CFOs cited a preference for this approach). Another 9% of the CFOs cited a belief that holding their management accountable for FX fluctuations is not appropriate or is impractical.3 Incorporating foreign exchange impacts How FX swings are incorporated into incentive compensation plans going forward—if at all—remains to be seen.

At the outset of each performance cycle, compensation committees typically develop a list of adjustments to earnings for incentive-compensation calculation purposes. Those can relate to accounting-policy changes, such as revenue recognition; changes in tax rates; gains or losses on the disposition of assets; impairments; and other matters. In future iterations, compensation committees could add adjustments due to FX swings to their lists so that there would be a mechanism in place to address unanticipated currency changes. But given the pressure over the past decade from shareholders and proxy advisory firms to make incentive plans less discretionary, companies alternatively could require that FX fluctuations be removed from the incentive-plan calculation via formula.

That would effectively disallow the compensation committee from using its discretion in deciding how much, if any, of the FX variation should impact the incentive calculation. Several factors may drive the board’s decision. First and foremost is the question of how adjustments will affect the alignment of shareholders’ and executives’ interests. Will such adjustments be perceived as just and fair? Another may be how downward adjustments to incentive compensation due to recent FX volatility might affect an organization’s ability to attract and retain talent. Keeping fates aligned Which approach best describes your board’s views about on adjusting executive compensation in light of a strong US dollar? Percent of CFOs selecting each approach, among only those CFOs who said this issue is applicable to their company (n=70) Do nothing: Shareholders’ and executives’ situations should be similar, whether exchange rates are favorable or unfavorable. Corridor approach: Management makes choices about sourcing, operating locations, pricing, and borrowing for non-US operations, so make management significantly accountable for FX movements within a corridor of currency fluctuations tied to budgeted currency assumptions. Hold harmless: Currency rate shifts are out of management’s control, and aggressive efforts to hedge the company’s FX exposure would be very expensive and risky. Other 0% Source: CFO Signals, Deloitte CFO Program, 2Q 2015, July 2015. 2 20% 40% 60% 80% .

New rule proposed on pay versus performance The Securities and Exchange Commission recently issued a proposed rule4 that would amend Regulation S-K, Item 402,5 to implement a mandate under the DoddFrank Act,6 requiring a registrant to disclose the relationship between executive compensation actually paid and the financial performance of the registrant. The proposal, which is intended to improve shareholders’ ability to objectively assess the link between executive compensation and company performance, raises a number of interesting questions. Employees, after all, want to be treated fairly and paid based on what they can influence and on how they perform. If incentive compensation is reduced as a result of FX fluctuations, which management and employees may not consider to be within their control, that could have an adverse effect on how workers feel about the fairness of the compensation program and whether their efforts are being properly valued. In the proposal, the SEC has requested comments on 64 questions. Thus, it is unclear what the final rule will look like and when it will be issued (although if finalized before year-end, it may be effective for the 2016 proxy season).

What is clear, however, is that shareholders, employees, and the media will heavily scrutinize the disclosures a registrant provides under the final rule. In addition, the impact of this issue could go deep into the organization, affecting anyone who is paid on an annual or long-term incentive plan. For example, an organization may have 1,000 or more employees participating in an annual incentive plan with only 10 to 15 of them senior officers. Thus, some companies may choose to provide relief to participants below the senior officer level to minimize the impact on morale and retention among the incentive-eligible population even if no adjustment is made for top officers. Because of the potential sensitivity associated with any disclosures about executive compensation, registrants affected by the proposal should review their past compensation practices and assess whether the proposed requirements would appropriately convey to investors the relationship between their executive compensation practices and company performance.

One way of doing so might be to model the proposed disclosures by using data for the past several years. Modeling might reveal possible unintended consequences of the proposal or the need to develop a strategy for communicating to investors the effects of specific aspects of the disclosures. Given that the proposal requested comment on virtually all aspects of its provisions, registrants had the opportunity to express their concerns and recommend improvements or disclosure alternatives. Comments were due on July 6, 2015. Bridging the information gap Still, some boards may worry that they will be criticized for making an adjustment to incentive compensation— upward or downward.

That’s particularly true in the event incentive compensation is adjusted upward when an organization is earning less. In such cases, it’s important for boards to have a strong rationale for the adjustment and to clearly communicate it to shareholders. In general, boards can help minimize the risk of being criticized by being consistent, having a strong rationale for their decision, being transparent about the factors that went into their decision, and making clear disclosures around the adjustment. 3 .

l, Global Research Director, CFO Program, Deloitte LLP; P For their part, CFOs can help shape the discussion and the decision by getting to know shareholders’ expectations through their interactions with analysts and major investors. In addition, it is important for finance chiefs to focus on what is affordable, albeit striking a balance with what is competitive. CFOs, even while struggling with the budget and trying to project out earnings for the next two to three years, should establish acceptable limits on compensation in terms of its dilutive effect on earnings. And finally, CFOs could spend considerable time with the audit and compensation committees to bridge the potential knowledge gap on compensation and financial performance. In the case of FX fluctuations, their input can help decide—in the case of either positive or negative swings—how these amounts should be reflected in incentive compensation targets and payouts. Primary Contact Michael S.

Kesner Principal; National Leader, Compensation Deloitte Consulting LLP mkesner@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr. Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary team of Deloitte leaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands. The Program harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of a CFO’s career – helping CFOs manage the aders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands.

The Program harnessestheir roles, tackle their company’s complexities of our nsights for every stage of a CFO’s career – helping CFOs manage the complexities of their roles, tackle their company’s most compelling most compelling challenges, and adapt to strategic shifts in the market. t: For more or services. This y means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional adviceinformation about Deloitte’s CFO Program, visit or should it be used as a basis for any decision or action that may affect your business. Before making any decision or takingat: www.deloitte.com/us/thecfoprogram. our website any action that may .

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. Follow us @deloittecfo Endnotes 1 CFO Signals, Deloitte CFO Program, see 2Q 2015, July 2015. 2 “FiREapps 2015 Q1 Corporate Earnings Currency Impact Report,” based on the analysis of the earnings calls of 1,200 publicly traded North American and European companies, June 2015. 3 CFO Signals, Deloitte CFO Program, see 2Q 2015, July 2015. 4 SEC Proposed Rule Release No. 34-74835, Pay Versus Performance. 5 SEC Regulation S-K, Item 402, “Executive Compensation.” 6 The proposed rule would implement Section 14(i) of the Securities Exchange Act of 1934, as added by Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act. This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business.

Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities.

DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 4 .