Description

CFO Insights

Diagnosing your team—

and curing its ills

As CFO, you are critically dependent on your leadership

team to successfully execute your vision. But just as

ineffective individuals can drain your time, an ineffective

leadership team can diminish your standing in your

company.

Still, executives often have a fuzzy definition of what a

team means to them. For some, it’s like a relay team—

with high-end runners who deliver the best possible

performance in their leg and cleanly hand off the baton

to the next participant. Others want a team that is more

like a basketball team—where people play their positions

but also mutually adjust to changing situations on the

court.

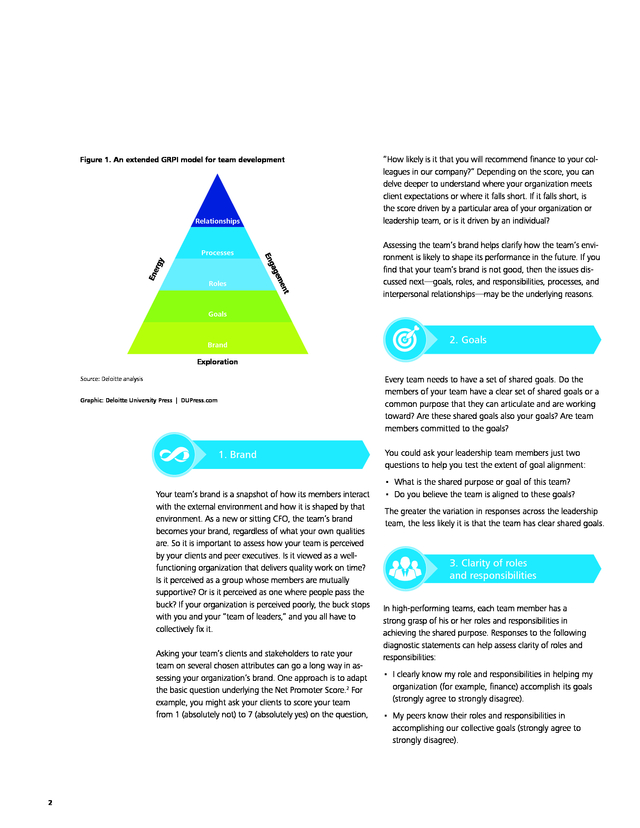

Sometimes the team must operate in both ways: a relay team for structured situations, a basketball team for unstructured ones. Building on the work of Richard Beckhard, a founder of the field of organization development, and the more recent work of Alex (Sandy) Pentland at the Massachusetts Institute of Technology (MIT), the framework lays out six key areas in which to assess a team: brand, shared goals, clear roles and responsibilities, clear processes, interpersonal relationships, and the communication dimensions of energy, engagement, and exploration (see Figure 1). For those familiar with the literature, we have added brand and communications to augment the Goals, Roles, Process, and Interpersonal Relations (GRPI) model credited to Richard Beckhard.1 In this issue of CFO Insights, we will offer a simple and practical framework to diagnose how your team works, framing a few questions that assess key team attributes. 1 . Figure 1. An extended GRPI model for team development Relationships nt gy Roles me ge En er ga En Processes “How likely is it that you will recommend finance to your colleagues in our company?” Depending on the score, you can delve deeper to understand where your organization meets client expectations or where it falls short. If it falls short, is the score driven by a particular area of your organization or leadership team, or is it driven by an individual? Assessing the team’s brand helps clarify how the team’s environment is likely to shape its performance in the future. If you find that your team’s brand is not good, then the issues discussed next—goals, roles, and responsibilities, processes, and interpersonal relationships—may be the underlying reasons. Goals Brand 2.

Goals Exploration Every team needs to have a set of shared goals. Do the members of your team have a clear set of shared goals or a common purpose that they can articulate and are working toward? Are these shared goals also your goals? Are team members committed to the goals? Source: Deloitte analysis Graphic: Deloitte University Press | DUPress.com 1. Brand Your team’s brand is a snapshot of how its members interact with the external environment and how it is shaped by that environment.

As a new or sitting CFO, the team’s brand becomes your brand, regardless of what your own qualities are. So it is important to assess how your team is perceived by your clients and peer executives. Is it viewed as a wellfunctioning organization that delivers quality work on time? Is it perceived as a group whose members are mutually supportive? Or is it perceived as one where people pass the buck? If your organization is perceived poorly, the buck stops with you and your “team of leaders,” and you all have to collectively fix it. Asking your team’s clients and stakeholders to rate your team on several chosen attributes can go a long way in assessing your organization’s brand.

One approach is to adapt the basic question underlying the Net Promoter Score.2 For example, you might ask your clients to score your team from 1 (absolutely not) to 7 (absolutely yes) on the question, 2 You could ask your leadership team members just two questions to help you test the extent of goal alignment: • What is the shared purpose or goal of this team? • Do you believe the team is aligned to these goals? The greater the variation in responses across the leadership team, the less likely it is that the team has clear shared goals. 3. Clarity of roles and responsibilities In high-performing teams, each team member has a strong grasp of his or her roles and responsibilities in achieving the shared purpose. Responses to the following diagnostic statements can help assess clarity of roles and responsibilities: • I clearly know my role and responsibilities in helping my organization (for example, finance) accomplish its goals (strongly agree to strongly disagree). • My peers know their roles and responsibilities in accomplishing our collective goals (strongly agree to strongly disagree). .

4. Team processes Processes can include rules for communication, problem solving, conflict resolution, and decision-making among team members. As CFO—and particularly as an incoming finance chief—you can assess processes by observing teams in action. Two useful questions you can ask team members are: • Our team has clear processes for solving routine problems and issues (strongly agree to strongly disagree). • Our team is effective in creating new processes to handle ambiguous problems (strongly agree to strongly disagree). 5.

Interpersonal relationships How do team members interact with one another? Are they tolerant of diverse viewpoints and mutually supportive? Can they handle conflict and resolve it among themselves? Do they have a foundation of mutual trust? Again, in addition to direct observations, responses to the statements below can help diagnose the state of interpersonal relationships: • There is a high level of trust across the leadership team (strongly agree to strongly disagree). • I perceive that team members generally have a strong foundation of mutual respect (strongly agree to strongly disagree). • I am not aware of interpersonal conflicts in my group (strongly agree to strongly disagree). 6. Communication—energy, engagement, and exploration Pentland of MIT undertook a series of studies on teams and their performance on different tasks. He found that communication within and outside the team was the single biggest predictor of team performance.3 The three critical dimensions of communication are energy, engagement, and exploration.

Energy is the number of communication exchanges among team members. Engagement is the distribution of communications across team members (for instance, engagement would be low if most team members are quiet and only a few team members interact, even if it is with high energy). Exploration is the extent to which team members communicate outside the team to gather information to solve problems or share solutions—in effect, it is the energy outside of the team. Three questions to explore your team’s communication patterns are: • I observe a high frequency of communications within the team across formal, informal, and back-channel meetings and exchanges (strongly agree to strongly disagree). • I observe a broad group of team members actively interacting and communicating with one another (strongly agree to strongly disagree). • I observe my team members actively communicating with non-team members to seek out solutions or inform others about team progress, challenges, and solutions (strongly agree to strongly disagree). Pentland’s work found high levels of communication to be a good predictor of team performance, consistent with prior literature on team communications and boundary spanning. There is extensive literature on teams,4 and many diagnostic tools for their assessment. For example, an online search for “GRPI” may reveal numerous assessments and tools. However, the addition of brand and communications and the few questions framed in each of the six areas mentioned should give you a practical way to quickly assess your team and focus your team-improvement efforts. As CFO, you oversee a leadership group that may or may not function as a team.

As a new or sitting finance leader, you will need to decide if you want a team committed to a shared purpose and a brand going forward. If so, the six areas of brand, goals, role clarity, processes, interpersonal relationships, and communications can provide a practical starting point for team assessment, and focus your attention on the issues that must be addressed to develop a higherperforming team. 3 . Your team is your brand Your team represents both your brand and the organization’s brand. To create cohesion around the brand you desire, have conversations with your leadership team that define the go-forward brand, set the context, and drive behaviors that make the brand a reality. Define the brand. A first step is to interview existing stakeholders and take an inventory of how they describe your existing organization. For instance, you may hear that finance is usually a naysayer, unable to support critical investments, or can’t provide critical information.

Negative as well as positive descriptions offer opportunities to reset the brand. In this instance, providing timely, insightful, and accurate information may become part of your desired brand. Another approach is to consider your goals for the organization. For example, CFOs often want to make finance an effective partner to the business.

This may be the overarching goal. But as the brand defines how you are perceived in delivering the goal, you might be more specific and say, “I want my finance folks to be trusted, confident, and insightful when partnering with the business.” A third approach is to brainstorm with your team on how to define critical brand attributes. This involves your team in the brand-definition process, enabling its members to take ownership of the result, which could lead to an expansion of the set of descriptors (for example, to be perceived as a fair and objective organization). Adding these descriptors, you could now frame the new desired brand: “The finance organization consistently delivers timely and accurate financial reports and insightful analyses to support business decision-making and value creation. Finance is a confident and trusted partner to the business that is fair, objective, and transparent in its processes.” Set the context. Resetting the context of the brand may require breaking prior patterns of interactions.

For example, if you find a business leader is making finance-related decisions without consulting your staff, it could prove challenging for your team to achieve its brand aspirations. The solution is to explore renegotiating your staff’s participation in this business unit’s finance-related decisions. If unsuccessful, you have to decide whether to escalate the issue or to temporarily dial down services to this business unit. Drive behaviors. The brand is defined not by what you say, but by what key stakeholders observe.

For example, once your team starts to own a new brand, you may need to tackle redefining the visuals, since visual perception often trumps auditory and other perceptions. Finance staff dressed in business casual in a formal environment could convey the wrong impression, whereas consistent visual identities and presentation formats can emphasize professionalism and attention to detail. For their part, leaders will also have to be role models for the desired behaviors.

If the goal is to be responsive to customers, leaders need to demonstrate this trait; if the team is to be perceived as insightful, leaders need to show that they value team members’ insights. Finally, incentives and rewards are essential to reinforcing the desired behaviors. Rewards can be varied— from recognition in newsletters to smaller monetary awards—but tying them to tangible measures of behaviors can enable you to track progress toward the consistent delivery of your organization’s brand promise. * For more information on team dynamics, visit the Executive Transitions collection on Deloitte University Press. Endnotes Richard Beckhard, “Optimizing team building efforts,” Journal of Contemporary Business (1972), Volume 1, Issue 3, pp 23-27. Frederick F.

Reicheld, “The one number you need to grow,” Harvard Business Review, December 2003. 3 Alex (Sandy) Pentland: “The new science of building teams,” Harvard Business Review, April 2012. 1 2 4 The Harvard Business Review Press’s HBR 10 Must Reads on Teams (2013) provides a readable snapshot of this literature, but misses Beckhard’s original model, which was published in a different journal. 4 . eloitte LLP; Contact: Ajit Kambil Global Research Director; CFO Program Deloitte LLP akambil@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr. Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary team of Deloitte leaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands. The Program harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of harnesses career—helping CFOs manage the CFOs stay ahead in the face of growing challenges and demands. The Programa CFO’s our lping CFOs manage the complexities of their roles, tackle their company’s most compelling complexities of their roles, tackle their company’s most compelling challenges, and adapt to strategic shifts in the market. unting, business, financial, investment, legal, tax, or other professional adviceinformation about Deloitte’s CFO Program, visit For more or services.

This on or action that may affect your business. Before making any decision or taking any action that may our website at: www.deloitte.com/us/thecfoprogram. ss sustained by any person who relies on this publication. Follow us @deloittecfo This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services.

This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 5 . .

Sometimes the team must operate in both ways: a relay team for structured situations, a basketball team for unstructured ones. Building on the work of Richard Beckhard, a founder of the field of organization development, and the more recent work of Alex (Sandy) Pentland at the Massachusetts Institute of Technology (MIT), the framework lays out six key areas in which to assess a team: brand, shared goals, clear roles and responsibilities, clear processes, interpersonal relationships, and the communication dimensions of energy, engagement, and exploration (see Figure 1). For those familiar with the literature, we have added brand and communications to augment the Goals, Roles, Process, and Interpersonal Relations (GRPI) model credited to Richard Beckhard.1 In this issue of CFO Insights, we will offer a simple and practical framework to diagnose how your team works, framing a few questions that assess key team attributes. 1 . Figure 1. An extended GRPI model for team development Relationships nt gy Roles me ge En er ga En Processes “How likely is it that you will recommend finance to your colleagues in our company?” Depending on the score, you can delve deeper to understand where your organization meets client expectations or where it falls short. If it falls short, is the score driven by a particular area of your organization or leadership team, or is it driven by an individual? Assessing the team’s brand helps clarify how the team’s environment is likely to shape its performance in the future. If you find that your team’s brand is not good, then the issues discussed next—goals, roles, and responsibilities, processes, and interpersonal relationships—may be the underlying reasons. Goals Brand 2.

Goals Exploration Every team needs to have a set of shared goals. Do the members of your team have a clear set of shared goals or a common purpose that they can articulate and are working toward? Are these shared goals also your goals? Are team members committed to the goals? Source: Deloitte analysis Graphic: Deloitte University Press | DUPress.com 1. Brand Your team’s brand is a snapshot of how its members interact with the external environment and how it is shaped by that environment.

As a new or sitting CFO, the team’s brand becomes your brand, regardless of what your own qualities are. So it is important to assess how your team is perceived by your clients and peer executives. Is it viewed as a wellfunctioning organization that delivers quality work on time? Is it perceived as a group whose members are mutually supportive? Or is it perceived as one where people pass the buck? If your organization is perceived poorly, the buck stops with you and your “team of leaders,” and you all have to collectively fix it. Asking your team’s clients and stakeholders to rate your team on several chosen attributes can go a long way in assessing your organization’s brand.

One approach is to adapt the basic question underlying the Net Promoter Score.2 For example, you might ask your clients to score your team from 1 (absolutely not) to 7 (absolutely yes) on the question, 2 You could ask your leadership team members just two questions to help you test the extent of goal alignment: • What is the shared purpose or goal of this team? • Do you believe the team is aligned to these goals? The greater the variation in responses across the leadership team, the less likely it is that the team has clear shared goals. 3. Clarity of roles and responsibilities In high-performing teams, each team member has a strong grasp of his or her roles and responsibilities in achieving the shared purpose. Responses to the following diagnostic statements can help assess clarity of roles and responsibilities: • I clearly know my role and responsibilities in helping my organization (for example, finance) accomplish its goals (strongly agree to strongly disagree). • My peers know their roles and responsibilities in accomplishing our collective goals (strongly agree to strongly disagree). .

4. Team processes Processes can include rules for communication, problem solving, conflict resolution, and decision-making among team members. As CFO—and particularly as an incoming finance chief—you can assess processes by observing teams in action. Two useful questions you can ask team members are: • Our team has clear processes for solving routine problems and issues (strongly agree to strongly disagree). • Our team is effective in creating new processes to handle ambiguous problems (strongly agree to strongly disagree). 5.

Interpersonal relationships How do team members interact with one another? Are they tolerant of diverse viewpoints and mutually supportive? Can they handle conflict and resolve it among themselves? Do they have a foundation of mutual trust? Again, in addition to direct observations, responses to the statements below can help diagnose the state of interpersonal relationships: • There is a high level of trust across the leadership team (strongly agree to strongly disagree). • I perceive that team members generally have a strong foundation of mutual respect (strongly agree to strongly disagree). • I am not aware of interpersonal conflicts in my group (strongly agree to strongly disagree). 6. Communication—energy, engagement, and exploration Pentland of MIT undertook a series of studies on teams and their performance on different tasks. He found that communication within and outside the team was the single biggest predictor of team performance.3 The three critical dimensions of communication are energy, engagement, and exploration.

Energy is the number of communication exchanges among team members. Engagement is the distribution of communications across team members (for instance, engagement would be low if most team members are quiet and only a few team members interact, even if it is with high energy). Exploration is the extent to which team members communicate outside the team to gather information to solve problems or share solutions—in effect, it is the energy outside of the team. Three questions to explore your team’s communication patterns are: • I observe a high frequency of communications within the team across formal, informal, and back-channel meetings and exchanges (strongly agree to strongly disagree). • I observe a broad group of team members actively interacting and communicating with one another (strongly agree to strongly disagree). • I observe my team members actively communicating with non-team members to seek out solutions or inform others about team progress, challenges, and solutions (strongly agree to strongly disagree). Pentland’s work found high levels of communication to be a good predictor of team performance, consistent with prior literature on team communications and boundary spanning. There is extensive literature on teams,4 and many diagnostic tools for their assessment. For example, an online search for “GRPI” may reveal numerous assessments and tools. However, the addition of brand and communications and the few questions framed in each of the six areas mentioned should give you a practical way to quickly assess your team and focus your team-improvement efforts. As CFO, you oversee a leadership group that may or may not function as a team.

As a new or sitting finance leader, you will need to decide if you want a team committed to a shared purpose and a brand going forward. If so, the six areas of brand, goals, role clarity, processes, interpersonal relationships, and communications can provide a practical starting point for team assessment, and focus your attention on the issues that must be addressed to develop a higherperforming team. 3 . Your team is your brand Your team represents both your brand and the organization’s brand. To create cohesion around the brand you desire, have conversations with your leadership team that define the go-forward brand, set the context, and drive behaviors that make the brand a reality. Define the brand. A first step is to interview existing stakeholders and take an inventory of how they describe your existing organization. For instance, you may hear that finance is usually a naysayer, unable to support critical investments, or can’t provide critical information.

Negative as well as positive descriptions offer opportunities to reset the brand. In this instance, providing timely, insightful, and accurate information may become part of your desired brand. Another approach is to consider your goals for the organization. For example, CFOs often want to make finance an effective partner to the business.

This may be the overarching goal. But as the brand defines how you are perceived in delivering the goal, you might be more specific and say, “I want my finance folks to be trusted, confident, and insightful when partnering with the business.” A third approach is to brainstorm with your team on how to define critical brand attributes. This involves your team in the brand-definition process, enabling its members to take ownership of the result, which could lead to an expansion of the set of descriptors (for example, to be perceived as a fair and objective organization). Adding these descriptors, you could now frame the new desired brand: “The finance organization consistently delivers timely and accurate financial reports and insightful analyses to support business decision-making and value creation. Finance is a confident and trusted partner to the business that is fair, objective, and transparent in its processes.” Set the context. Resetting the context of the brand may require breaking prior patterns of interactions.

For example, if you find a business leader is making finance-related decisions without consulting your staff, it could prove challenging for your team to achieve its brand aspirations. The solution is to explore renegotiating your staff’s participation in this business unit’s finance-related decisions. If unsuccessful, you have to decide whether to escalate the issue or to temporarily dial down services to this business unit. Drive behaviors. The brand is defined not by what you say, but by what key stakeholders observe.

For example, once your team starts to own a new brand, you may need to tackle redefining the visuals, since visual perception often trumps auditory and other perceptions. Finance staff dressed in business casual in a formal environment could convey the wrong impression, whereas consistent visual identities and presentation formats can emphasize professionalism and attention to detail. For their part, leaders will also have to be role models for the desired behaviors.

If the goal is to be responsive to customers, leaders need to demonstrate this trait; if the team is to be perceived as insightful, leaders need to show that they value team members’ insights. Finally, incentives and rewards are essential to reinforcing the desired behaviors. Rewards can be varied— from recognition in newsletters to smaller monetary awards—but tying them to tangible measures of behaviors can enable you to track progress toward the consistent delivery of your organization’s brand promise. * For more information on team dynamics, visit the Executive Transitions collection on Deloitte University Press. Endnotes Richard Beckhard, “Optimizing team building efforts,” Journal of Contemporary Business (1972), Volume 1, Issue 3, pp 23-27. Frederick F.

Reicheld, “The one number you need to grow,” Harvard Business Review, December 2003. 3 Alex (Sandy) Pentland: “The new science of building teams,” Harvard Business Review, April 2012. 1 2 4 The Harvard Business Review Press’s HBR 10 Must Reads on Teams (2013) provides a readable snapshot of this literature, but misses Beckhard’s original model, which was published in a different journal. 4 . eloitte LLP; Contact: Ajit Kambil Global Research Director; CFO Program Deloitte LLP akambil@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr. Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary team of Deloitte leaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands. The Program harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of harnesses career—helping CFOs manage the CFOs stay ahead in the face of growing challenges and demands. The Programa CFO’s our lping CFOs manage the complexities of their roles, tackle their company’s most compelling complexities of their roles, tackle their company’s most compelling challenges, and adapt to strategic shifts in the market. unting, business, financial, investment, legal, tax, or other professional adviceinformation about Deloitte’s CFO Program, visit For more or services.

This on or action that may affect your business. Before making any decision or taking any action that may our website at: www.deloitte.com/us/thecfoprogram. ss sustained by any person who relies on this publication. Follow us @deloittecfo This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services.

This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 5 . .