Description

CFO Insights

Activist shareholders:

How will you respond?

If it seems like activist investors have had a more visible

and powerful presence over the last few years, it’s because

they have.

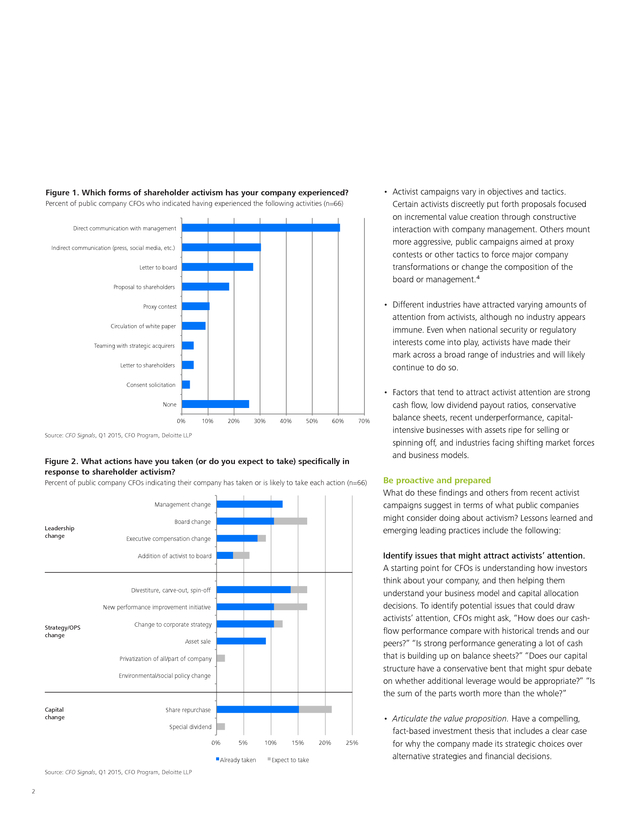

In fact, according to the results of the Q1 2015 CFO

Signals™ survey, just under three-quarters of public

company CFOs say they have experienced some form

of shareholder activism—most often in the form of

communication with management or the board, and

sometimes in the form of proposals that have gone

directly to shareholders. (See Figure 1, page 2.) Moreover,

about half say they have made at least one major business

change specifically because of shareholder activism (share

repurchases, leadership changes, and divestures being the

most common).¹ (See Figure 2, page 2.)

The trend also shows no signs of abating. In the wake

of the financial crisis, Dodd-Frank, and Say-on-Pay votes,

shareholders have become more assertive in expressing

what they want from the companies they invest in. And

for CFOs, this new dynamic between public companies

and shareholders presents an evolution in corporate

governance that may need to be addressed.

There are several steps that CFOs can take to prepare their

companies to manage increasingly vocal and influential

investors.

In this issue of CFO Insights, we will discuss how finance chiefs can identify and address company financial issues that could attract activist attention; why a more proactive engagement with the investment community is needed long before an activist campaign begins; and what some of the key components of a playbook are for responding to an activist campaign. Trends in shareholder activism One of the keys to being prepared for activists is to understand what they’re doing and why. To a large extent, activism is a debate about capital deployment, risk tolerance, and performance—topics that are typically part of management’s and the board’s agenda in the normal course of business. If your company has issues in these areas, however, you probably want to be in control of the situation and prepared to respond to activists. Being prepared also means understanding some of the trends shaping today’s shareholder-activist campaigns.

For example: • Some activists have a longer-term investment horizon than their reputation suggests. A study of 2,000 activist campaigns over the last 10 years by Columbia Business School Professor Wei Jiang found that activists’ average holding period is just over two years.2 • Activist campaigns are often “friendly.” The majority of such campaigns studied by Professor Jiang occurred without getting into the press. Typically, a shareholder approached a company with a point of view on either how capital should be deployed or opportunities to enhance value, and there was a conversation between company management and the investor.³ 1 .

• Activist campaigns vary in objectives and tactics. Certain activists discreetly put forth proposals focused on incremental value creation through constructive interaction with company management. Others mount more aggressive, public campaigns aimed at proxy contests or other tactics to force major company transformations or change the composition of the board or management.â´ Figure 1. Which forms of shareholder activism has your company experienced? Percent of public company CFOs who indicated having experienced the following activities (n=66) Direct communication with management Indirect communication (press, social media, etc.) Letter to board Proposal to shareholders • Different industries have attracted varying amounts of attention from activists, although no industry appears immune. Even when national security or regulatory interests come into play, activists have made their mark across a broad range of industries and will likely continue to do so. Proxy contest Circulation of white paper Teaming with strategic acquirers Letter to shareholders Consent solicitation None 0% 10% 20% 30% 40% 50% 60% 70% Source: CFO Signals, Q1 2015, CFO Program, Deloitte LLP Figure 2. What actions have you taken (or do you expect to take) specifically in response to shareholder activism? Percent of public company CFOs indicating their company has taken or is likely to take each action (n=66) Management change change Management Leadership change Board change change Board Executive compensation change change Executive compensation Divestiture, carve-out, spin-off Divestiture, carve-out, spin-off New performance improvement initiative New performance improvement initiative Change to corporate strategy Change to corporate strategy Asset sale sale Asset Privatization of all/partall/part of company Privatization of of company Environmental/social policy change change Environmental/social policy Capital change Share repurchase Share repurchase Special Special dividend dividend 0% 0% 5% 10% 10% 15% 15% 20% 20% 25% 25% 5% Already taken taken Expect Expect to take to take Already Source: CFO Signals, Q1 2015, CFO Program, Deloitte LLP 2 Be proactive and prepared What do these findings and others from recent activist campaigns suggest in terms of what public companies might consider doing about activism? Lessons learned and emerging leading practices include the following: Identify issues that might attract activists’ attention. A starting point for CFOs is understanding how investors think about your company, and then helping them understand your business model and capital allocation decisions.

To identify potential issues that could draw activists’ attention, CFOs might ask, “How does our cashflow performance compare with historical trends and our peers?” “Is strong performance generating a lot of cash that is building up on balance sheets?” “Does our capital structure have a conservative bent that might spur debate on whether additional leverage would be appropriate?” “Is the sum of the parts worth more than the whole?” Addition of activist activist to board Addition of to board Strategy/OPS change • Factors that tend to attract activist attention are strong cash flow, low dividend payout ratios, conservative balance sheets, recent underperformance, capitalintensive businesses with assets ripe for selling or spinning off, and industries facing shifting market forces and business models. • Articulate the value proposition. Have a compelling, fact-based investment thesis that includes a clear case for why the company made its strategic choices over alternative strategies and financial decisions. . • Regularly evaluate strategic and transaction alternatives. Companies need to regularly and objectively evaluate and prioritize various alternatives for delivering value to shareholders. If various alternatives haven’t been evaluated in a few years, or if they are not being reviewed objectively, you may be setting yourself up for trouble. • Review governance policies and board composition. In particular, determine if performance is aligned with compensation. Excessive compensation or a lack of alignment between performance and compensation in and of itself can generate activist interest. • Get out in front of significant events.

If management is contemplating a major strategic shift or a transformational M&A transaction, ask, “Are we out in front of that story, communicating what the investment or change in strategy or business model is, why that action makes sense, and how it is going to generate long-term value for shareholders?” • Monitor market activity. Be regularly apprised of what’s happening in your stock and with your shareholder base. Have there been recent changes in investor behavior or interactions? What is happening in the industry? Are peers being targeted by activists, and if so, which funds and what proposals are being put forth? Address shareholder demands for information, transparency, and access.

Proactively engaging with investors on a wide variety of topics can be a strong management tool. A high level of engagement and two-way communication help establish credibility with the investment community that management has the shareholders’ interests at heart, and provides crucial feedback on issues many investors are concerned about. This may be especially helpful when engaging with major shareholders, who can be cornerstones of an activist defense. Creating your response playbook Just as many companies have crisis management teams and playbooks, it can be critical to develop a clear plan on how to respond if an activist launches a campaign. Having a protocol and a dedicated team with clearly articulated responsibilities helps companies take control of the situation from Day 1 and avoid missteps in the heat of the moment. Consider including financial advisors, attorneys, accountants, IR, and public relations in the response team. And one of its first steps is not to ignore the activists. Stonewalling, after all, may only incite activists to become more aggressive. Moreover, it is critical that senior management keep the team informed and aligned with their response to the activist campaign. You don’t want the wrong message being communicated externally, so keep everyone informed of what management is thinking and planning. One question the team should ask almost on a daily basis is, “Should we inform the board?” Once directors are informed, however, consider engaging them in the dialogue.

For example, if the chair of the compensation committee can meet with an investor who questions the alignment between pay and performance and justify it and defend the compensation structure, it is far more effective than having the CEO defend it. And while you probably don’t want to make the chairman available on Day 1, you should have an idea of when you might take that step, if required. Attract and retain top talent in investor relations. A more dynamic IR strategy may require companies to significantly upgrade the talent and tools of their IR organization. The IR head should be working closely with the CEO and CFO on investor communications and be fluent in company strategy and finance so that he or she can have an interactive dialogue with stakeholders. 3 .

In our Q1 2015 CFO Signals survey, we asked CFOs how they are changing their IR approaches in response to activism. About half said they have changed very little—mostly citing preexisting programs that are already working well. The half who said they have made il, Global ResearchsubstantialProgram, Deloitte LLP; to cite heightened monitoring Director, CFO changes tended P of activist activity, more proactive planning around activists’ concerns, and more (and more preemptive) communication with current and potential investors.âµ Incorporating these steps and others outlined in this article may not lead to a comprehensive defense against shareholder activism, but they are crucial to effective management of an activist campaign. And given that shareholder activism is likely not going away anytime soon, the steps offer a road map to understanding and proactively dealing with this new environment. Primary contacts Bob Lamm Senior Advisor Center for Corporate Governance Deloitte LLP rlamm@deloitte.com Chris Ruggeri Principal; US M&A leader Deloitte Transaction and Business Analytics LLP cruggeri@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr.

Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. Endnotes About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary Corporate Development 2012: Leveraging Relationships in M&A, Deloitte Development LLC, pages. 38- 39. team of Deloitte leaders and subject matter 3 Ibid. specialists to help CFOs stay ahead in the face of 4 Ibid. 5 growing challenges and demands. The Program CFO Signals, Q1 2015, CFO Program, Deloitte LLP. harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of a CFO’s career – helping CFOs manage the eaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands.

The Program harnesses our roles, tackle their company’s complexities of their nsights for every stage of a CFO’s career – helping CFOs manage the complexities of their roles, tackle their company’s most compelling most compelling challenges, and adapt to strategic shifts in the market. t: 1 CFO Signals, Q1 2015, CFO Program, Deloitte LLP. 2 For more information by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This about Deloitte’s CFO Program, visit nor should it be used as a basis for any decision or action that may affect your business. Before making any our website at: www.deloitte.com/us/thecfoprogram. decision or taking any action that may .

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. Follow us @deloittecfo This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte As used in this document, “Deloitte” means Deloitte Consulting LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC.

All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 4 .

In this issue of CFO Insights, we will discuss how finance chiefs can identify and address company financial issues that could attract activist attention; why a more proactive engagement with the investment community is needed long before an activist campaign begins; and what some of the key components of a playbook are for responding to an activist campaign. Trends in shareholder activism One of the keys to being prepared for activists is to understand what they’re doing and why. To a large extent, activism is a debate about capital deployment, risk tolerance, and performance—topics that are typically part of management’s and the board’s agenda in the normal course of business. If your company has issues in these areas, however, you probably want to be in control of the situation and prepared to respond to activists. Being prepared also means understanding some of the trends shaping today’s shareholder-activist campaigns.

For example: • Some activists have a longer-term investment horizon than their reputation suggests. A study of 2,000 activist campaigns over the last 10 years by Columbia Business School Professor Wei Jiang found that activists’ average holding period is just over two years.2 • Activist campaigns are often “friendly.” The majority of such campaigns studied by Professor Jiang occurred without getting into the press. Typically, a shareholder approached a company with a point of view on either how capital should be deployed or opportunities to enhance value, and there was a conversation between company management and the investor.³ 1 .

• Activist campaigns vary in objectives and tactics. Certain activists discreetly put forth proposals focused on incremental value creation through constructive interaction with company management. Others mount more aggressive, public campaigns aimed at proxy contests or other tactics to force major company transformations or change the composition of the board or management.â´ Figure 1. Which forms of shareholder activism has your company experienced? Percent of public company CFOs who indicated having experienced the following activities (n=66) Direct communication with management Indirect communication (press, social media, etc.) Letter to board Proposal to shareholders • Different industries have attracted varying amounts of attention from activists, although no industry appears immune. Even when national security or regulatory interests come into play, activists have made their mark across a broad range of industries and will likely continue to do so. Proxy contest Circulation of white paper Teaming with strategic acquirers Letter to shareholders Consent solicitation None 0% 10% 20% 30% 40% 50% 60% 70% Source: CFO Signals, Q1 2015, CFO Program, Deloitte LLP Figure 2. What actions have you taken (or do you expect to take) specifically in response to shareholder activism? Percent of public company CFOs indicating their company has taken or is likely to take each action (n=66) Management change change Management Leadership change Board change change Board Executive compensation change change Executive compensation Divestiture, carve-out, spin-off Divestiture, carve-out, spin-off New performance improvement initiative New performance improvement initiative Change to corporate strategy Change to corporate strategy Asset sale sale Asset Privatization of all/partall/part of company Privatization of of company Environmental/social policy change change Environmental/social policy Capital change Share repurchase Share repurchase Special Special dividend dividend 0% 0% 5% 10% 10% 15% 15% 20% 20% 25% 25% 5% Already taken taken Expect Expect to take to take Already Source: CFO Signals, Q1 2015, CFO Program, Deloitte LLP 2 Be proactive and prepared What do these findings and others from recent activist campaigns suggest in terms of what public companies might consider doing about activism? Lessons learned and emerging leading practices include the following: Identify issues that might attract activists’ attention. A starting point for CFOs is understanding how investors think about your company, and then helping them understand your business model and capital allocation decisions.

To identify potential issues that could draw activists’ attention, CFOs might ask, “How does our cashflow performance compare with historical trends and our peers?” “Is strong performance generating a lot of cash that is building up on balance sheets?” “Does our capital structure have a conservative bent that might spur debate on whether additional leverage would be appropriate?” “Is the sum of the parts worth more than the whole?” Addition of activist activist to board Addition of to board Strategy/OPS change • Factors that tend to attract activist attention are strong cash flow, low dividend payout ratios, conservative balance sheets, recent underperformance, capitalintensive businesses with assets ripe for selling or spinning off, and industries facing shifting market forces and business models. • Articulate the value proposition. Have a compelling, fact-based investment thesis that includes a clear case for why the company made its strategic choices over alternative strategies and financial decisions. . • Regularly evaluate strategic and transaction alternatives. Companies need to regularly and objectively evaluate and prioritize various alternatives for delivering value to shareholders. If various alternatives haven’t been evaluated in a few years, or if they are not being reviewed objectively, you may be setting yourself up for trouble. • Review governance policies and board composition. In particular, determine if performance is aligned with compensation. Excessive compensation or a lack of alignment between performance and compensation in and of itself can generate activist interest. • Get out in front of significant events.

If management is contemplating a major strategic shift or a transformational M&A transaction, ask, “Are we out in front of that story, communicating what the investment or change in strategy or business model is, why that action makes sense, and how it is going to generate long-term value for shareholders?” • Monitor market activity. Be regularly apprised of what’s happening in your stock and with your shareholder base. Have there been recent changes in investor behavior or interactions? What is happening in the industry? Are peers being targeted by activists, and if so, which funds and what proposals are being put forth? Address shareholder demands for information, transparency, and access.

Proactively engaging with investors on a wide variety of topics can be a strong management tool. A high level of engagement and two-way communication help establish credibility with the investment community that management has the shareholders’ interests at heart, and provides crucial feedback on issues many investors are concerned about. This may be especially helpful when engaging with major shareholders, who can be cornerstones of an activist defense. Creating your response playbook Just as many companies have crisis management teams and playbooks, it can be critical to develop a clear plan on how to respond if an activist launches a campaign. Having a protocol and a dedicated team with clearly articulated responsibilities helps companies take control of the situation from Day 1 and avoid missteps in the heat of the moment. Consider including financial advisors, attorneys, accountants, IR, and public relations in the response team. And one of its first steps is not to ignore the activists. Stonewalling, after all, may only incite activists to become more aggressive. Moreover, it is critical that senior management keep the team informed and aligned with their response to the activist campaign. You don’t want the wrong message being communicated externally, so keep everyone informed of what management is thinking and planning. One question the team should ask almost on a daily basis is, “Should we inform the board?” Once directors are informed, however, consider engaging them in the dialogue.

For example, if the chair of the compensation committee can meet with an investor who questions the alignment between pay and performance and justify it and defend the compensation structure, it is far more effective than having the CEO defend it. And while you probably don’t want to make the chairman available on Day 1, you should have an idea of when you might take that step, if required. Attract and retain top talent in investor relations. A more dynamic IR strategy may require companies to significantly upgrade the talent and tools of their IR organization. The IR head should be working closely with the CEO and CFO on investor communications and be fluent in company strategy and finance so that he or she can have an interactive dialogue with stakeholders. 3 .

In our Q1 2015 CFO Signals survey, we asked CFOs how they are changing their IR approaches in response to activism. About half said they have changed very little—mostly citing preexisting programs that are already working well. The half who said they have made il, Global ResearchsubstantialProgram, Deloitte LLP; to cite heightened monitoring Director, CFO changes tended P of activist activity, more proactive planning around activists’ concerns, and more (and more preemptive) communication with current and potential investors.âµ Incorporating these steps and others outlined in this article may not lead to a comprehensive defense against shareholder activism, but they are crucial to effective management of an activist campaign. And given that shareholder activism is likely not going away anytime soon, the steps offer a road map to understanding and proactively dealing with this new environment. Primary contacts Bob Lamm Senior Advisor Center for Corporate Governance Deloitte LLP rlamm@deloitte.com Chris Ruggeri Principal; US M&A leader Deloitte Transaction and Business Analytics LLP cruggeri@deloitte.com Deloitte CFO Insights are developed with the guidance of Dr.

Ajit Kambil, Global Research Director, CFO Program, Deloitte LLP; and Lori Calabro, Senior Manager, CFO Education & Events, Deloitte LLP. Endnotes About Deloitte’s CFO Program The CFO Program brings together a multidisciplinary Corporate Development 2012: Leveraging Relationships in M&A, Deloitte Development LLC, pages. 38- 39. team of Deloitte leaders and subject matter 3 Ibid. specialists to help CFOs stay ahead in the face of 4 Ibid. 5 growing challenges and demands. The Program CFO Signals, Q1 2015, CFO Program, Deloitte LLP. harnesses our organization’s broad capabilities to deliver forward thinking and fresh insights for every stage of a CFO’s career – helping CFOs manage the eaders and subject matter specialists to help CFOs stay ahead in the face of growing challenges and demands.

The Program harnesses our roles, tackle their company’s complexities of their nsights for every stage of a CFO’s career – helping CFOs manage the complexities of their roles, tackle their company’s most compelling most compelling challenges, and adapt to strategic shifts in the market. t: 1 CFO Signals, Q1 2015, CFO Program, Deloitte LLP. 2 For more information by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This about Deloitte’s CFO Program, visit nor should it be used as a basis for any decision or action that may affect your business. Before making any our website at: www.deloitte.com/us/thecfoprogram. decision or taking any action that may .

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. Follow us @deloittecfo This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. About Deloitte As used in this document, “Deloitte” means Deloitte Consulting LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright© 2015 Deloitte Development LLC.

All rights reserved. Member of Deloitte Touche Tohmatsu Limited. 4 .